Exempt or Non-Exempt? Employee Misclassification...

73

Exempt or Non-Exempt? Employee Misclassification Challenges Identifying Vulnerabilities and Minimizing Liability Under FLSA and State Law Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. TUESDAY, MAY 8, 2012 Presenting a live 90-minute webinar with interactive Q&A Mark E. Tabakman, Partner, Fox Rothschild, Roseland, N.J. Brent E. Pelton, Esq., Pelton & Associates, New York Daniel J. McCoy, Partner, Fenwick & West, Moutainview, Calif. Christine W. Johnston, Partner, K&L Gates, Boston

Transcript of Exempt or Non-Exempt? Employee Misclassification...

Exempt or Non-Exempt?

Employee Misclassification Challenges Identifying Vulnerabilities and Minimizing Liability Under FLSA and State Law

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

TUESDAY, MAY 8, 2012

Presenting a live 90-minute webinar with interactive Q&A

Mark E. Tabakman, Partner, Fox Rothschild, Roseland, N.J.

Brent E. Pelton, Esq., Pelton & Associates, New York

Daniel J. McCoy, Partner, Fenwick & West, Moutainview, Calif.

Christine W. Johnston, Partner, K&L Gates, Boston

Conference Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

2

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

FOR LIVE EVENT ONLY

3

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality of

your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory and you are listening via your computer

speakers, you may listen via the phone: dial 1-866-258-2056 and enter your

PIN -when prompted. Otherwise, please send us a chat or e-mail

[email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

4

FLSA Exemptions

© 2009 Fox Rothschild

EXEMPT OR NON-EXEMPT? EMPLOYEE

MISCLASSIFICATION CHALLENGES

Positions Most Vulnerable to FLSA and State Claims

Mark Tabakman, Esq.

Fox Rothschild LLP

http://wagehourlaw.foxrothschild.com

May 8, 2012

FLSA Exemptions

© 2009 Fox Rothschild

6

FLSA EXEMPTIONS:

EMERGING CLASS ACTION THREAT

AT-RISK POSITIONS

Financial Services Industry

I.T. Workers/Computer Programmers

Assistant Managers

Clerical/Administrative Employees

Sales Staff

FLSA Exemptions

© 2009 Fox Rothschild

7

FLSA SECTION 13(a)(1), GENERALLY

Section 13(a)(1) of the FLSA provides an exemption from both minimum wage and overtime pay for individuals employed as bona fide executive, administrative, professional, and outside sales employees. Sections 13(a)(1) and 13(a)(17) also exempt certain computer employees.

- To qualify for exemption, employees generally must meet certain tests regarding their job duties and be paid on a salary basis at not less than $455 per week.

- Job titles do not determine exempt status. - In order for an exemption to apply, an employee’s specific job

duties and salary must meet all the requirements of the DOL’s regulations.

FLSA Exemptions

© 2009 Fox Rothschild

ASSISTANT MANAGERS

To qualify for the executive employee exemption, all of the following tests must be met:

- The employee must be compensated on a salary basis (as defined in the regulations) at a rate not less than $455 per week;

- The employee’s primary duty must be managing the enterprise, or managing a customarily recognized department or subdivision of the enterprise;

- The employee must customarily and regularly direct the work of at least two or more other full-time employees or their equivalent; and

- The employee must have the authority to hire or fire other employees, or the employee’s suggestions and recommendations as to the hiring, firing, advancement, promotion or any other change of status of other employees must be given particular weight.

8

FLSA Exemptions

© 2009 Fox Rothschild

9

ASSISTANT MANAGERS (cnt’d)

The duties and responsibilities of assistant managers vary and may be determined by the industry in which the assistant manager works, the size of the business and/or the structure of the business (e.g., single establishment versus multi-establishment). An assistant manager whose primary duties or functions are ordinary production work or routine, recurrent or repetitive tasks is not exempt under the Regulations, Part 541.

However, to determine whether a worker employed as an assistant manager who regularly supervises the work of others meets the duties tests for exemption from the FLSA's minimum wage and overtime pay requirements, begin with the Executive Employee analysis.

FLSA Exemptions

© 2009 Fox Rothschild

10

ASSISTANT MANAGERS (cnt’d)

The Assistant Manager classification has always been problematic from an FLSA exemption perspective. These employees must be endowed with some actual/real authority relating to hiring and firing as well as other employee terms and condition or the employer will be an easy target for a class action suit. Moreover, they must supervise and manage the majority of the time.

- This becomes a fine line that often gets crossed in the hectic world of store operations, where the job has to get done.

Plaintiffs claiming to be misclassified as exempt Assistant Managers often assert that they were compelled to perform non-exempt duties a disproportionate amount of their work day and this amount of rank-and-file work destroyed the exemption.

On the Assistant Manager issue, the best defense is that these workers are truly exempt. The second best defense is that the class certification motion must fail because individualized assessment of each Assistant Manager is needed because some might have exercised more managerial duties than others. The need for individual scrutiny is the antithesis of a class action .

FLSA Exemptions

© 2009 Fox Rothschild

11

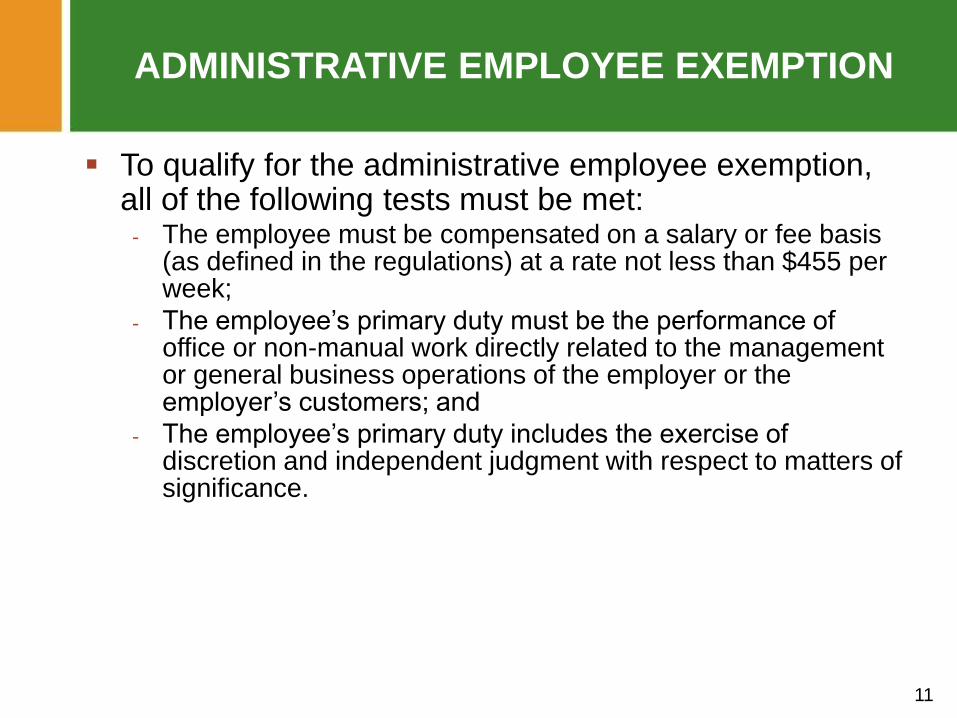

ADMINISTRATIVE EMPLOYEE EXEMPTION

To qualify for the administrative employee exemption, all of the following tests must be met:

- The employee must be compensated on a salary or fee basis (as defined in the regulations) at a rate not less than $455 per week;

- The employee’s primary duty must be the performance of office or non-manual work directly related to the management or general business operations of the employer or the employer’s customers; and

- The employee’s primary duty includes the exercise of discretion and independent judgment with respect to matters of significance.

FLSA Exemptions

© 2009 Fox Rothschild

12

PROFESSIONAL EMPLOYEE EXEMPTION

To qualify for the professional employee

exemption, following must be met: - The employee must be compensated on a salary or

fee basis at a rate of not less than $455 per week, exclusive of board, lodging, or other facilities; and

- Whose primary duty is the performance of work: Requiring knowledge of an advanced type in a field of

science or learning customarily acquired by a prolonged course of specialized intellectual instruction; or

Requiring invention, imagination, originality or talent in a recognized field of artistic or creative endeavor.

FLSA Exemptions

© 2009 Fox Rothschild

13

FINANCIAL SERVICES

Over the last several years there has

been a torrent of litigation concerning the

exempt status of positions in the financial

services industry (mortgage brokers,

originators, etc.).

FLSA Exemptions

© 2009 Fox Rothschild

14

FINANCIAL SERVICES (cont’d)

Prior to the DOL’s issuance of its 2010 White Paper (guidance statement) on the matter, employees were deemed exempt as administrative if their duties included work such as collecting and analyzing information regarding a customer’s income, assets, investments, or debts; determining which financial products best meet the customer’s needs and financial circumstances; advising the customer regarding the advantages and disadvantages of financial products; and servicing, promoting, and marketing the employer’s financial products.

FLSA Exemptions

© 2009 Fox Rothschild

15

FINANCIAL SERVICES (cont’d)

Per DOL’s 2010 White Paper, except in certain circumstances, mortgage loan officers will not qualify for the administrative exemption under the Fair Labor Standards Act.

If mortgage loan officers perform supervisory duties, they may still fall under the executive exemption, but the most commonly urged exemption for them, i.e. administrative, is now foreclosed.

The DOL concluded that “mortgage loan officers typically have the primary duty of making sales on behalf of their employer; as such, their primary duty is not directly related to the management or general business operations of their employer or their employer’s customers.”

- Mortgage loan officers will not qualify for the administrative exemption because their primary duty is production work, i.e. sales.

FLSA Exemptions

© 2009 Fox Rothschild

16

I.T. WORKERS/COMPUTER PROGRAMMERS

Computer systems analysts, computer

programmers, software engineers, and other

similarly skilled workers in the computer field

who meet certain tests regarding their job

duties may be exempt from minimum wage and

overtime requirements of the FLSA. - To be exempt, these employees must be paid at

least $455 per week on a salary basis or paid on an hourly basis, at a rate not less than $27.63 per hour.

FLSA Exemptions

© 2009 Fox Rothschild

17

I.T. WORKERS/COMPUTER PROGRAMMERS

(cont’d)

To qualify for the computer employee exemption, the following tests must be met:

- Employee must be paid at least $455 per week on a salary basis or paid on an hourly basis, at a rate not less than $27.63 per hour;

- Employee must be employed as a computer systems analyst, computer programmer, software engineer or other similarly skilled worker in the computer field performing the duties described below;

- The employee’s primary duty must consist of: The application of systems analysis techniques and procedures, including

consulting with users, to determine hardware, software or system function specifications;

The design, development, documentation, analysis, creation, testing or modification of computer systems or programs, or of programs related to user or system design specifications; or

The design, documentation, testing, creation or modification of computer programs related to machine operating systems; or

A combination of the aforementioned duties, the performance of which requires the same level of skills.

FLSA Exemptions

© 2009 Fox Rothschild

18

I.T. WORKERS/COMPUTER PROGRAMMERS

(cont’d)

The computer employee exemption does not include employees engaged in the manufacture or repair of computer hardware and related equipment.

Exemption also does not apply to employees whose work is highly dependent upon computers, but who are not primarily engaged in computer systems analysis and programming or other similarly skilled computer-related occupations.

FLSA Exemptions

© 2009 Fox Rothschild

19

I.T. WORKERS/COMPUTER PROGRAMMERS

(cont’d)

Martin v. Indiana Michigan Power Co., 9 WH Cases2d 1505 (6th Cir.2004):

- Computer help desk employees who provide computer maintenance and support do not qualify for administrative exemption, as they are not designing or creating computer systems and their primary function is to assist in keeping the computers and the network running to the specifications and designs of others.

Jackson v. McKeeson Health Solutions, 19 WH Cases2d 374 (D. Mass.2004):

- Computer support employees who spend the predominant amount of their time troubleshooting computer problems encountered by various company departments and entities was not exercising discretion and independent judgment required under the regulations, but rather highly technical skill.

FLSA Exemptions

© 2009 Fox Rothschild

20

I.T. WORKERS/COMPUTER PROGRAMMERS

(cont’d)

Pellerin v. Xspedius Mgm’t Co., 432 F.Supp. 2d 627 (W.D. La. 2006):

- Exemption applies to employee responsible for maintaining and supporting software applications by adding input fields, correcting bugs, and changing codes.

Bergquist v. Fidelity Info. Servs., Inc., 399 F.Supp. 2d 1320 (11th Cir. 2006):

- Exemption applies to computer programmer responsible for designing programs, assisting the business analyst with technical details of computer programs, and working on a project team to design pieces of programs that would be integrated into the work of other team members.

FLSA Exemptions

© 2009 Fox Rothschild

21

SALES STAFF

To qualify for the outside sales exemption, all of

the following tests must be met: - Employee’s primary duty must be making sales (as

defined in FLSA), or obtaining orders or contracts for services or for the use of facilities for which a consideration will be paid by the client or customer; and

- The employee must be customarily and regularly engaged away from the employer’s place or places of business.

FLSA Exemptions

© 2009 Fox Rothschild

22

SALES STAFF (cont’d)

The salary requirements of the regulation

do not apply to the outside sales

exemption. An employee who does not

satisfy the requirements of the outside

sales exemption may still qualify as an

exempt employee under one of the other

exemptions allowed by the FLSA.

FLSA Exemptions

© 2009 Fox Rothschild

23

SALES STAFF (cont’d)

Primary duty: - Principal, main, major or most important duty that the

employee performs.

Making sales: - “Sales” includes any sale, exchange, contract to sell,

consignment for sales, shipment for sale, or other disposition. It includes the transfer of title to tangible property, and in certain cases, of tangible and valuable evidences of intangible property.

Away from employer’s place of business: - An outside sales employee makes sales at the customer’s

place of business, or, if selling door-to-door, at the customer’s home. Outside sales does not include sales made by mail, telephone or the Internet unless such contact is used merely as an adjunct to personal calls.

FLSA Exemptions

© 2009 Fox Rothschild

24

SALES STAFF (cont’d)

Some states recognize a formal inside sales

exemption. For instance, New Jersey’s inside

sales exemption covers any employee whose

primary duty consists of sales activity and who

receives at least 50% of his or her total

compensation from commissions and a total

compensation of not less than $400 per week.

FLSA Exemptions

© 2009 Fox Rothschild

25

SALES STAFF (cont’d)

Martin v. Cooper Elec. Supply Co., 940

F2d 896 (3rd Cir.1991):

- Court holds that employer violated FLSA, as inside salespersons were not bona fide “administrative” employees and thus were not eligible for statutory exemption from Act’s overtime and record keeping requirements.

FLSA Exemptions

© 2009 Fox Rothschild

26

CLERICAL EMPLOYEE EXEMPTION

An executive assistant or administrative

assistant to a business owner or senior

executive of a large business generally meets

the duties requirements for the administrative

exemption if such employee, without specific

instructions or prescribed procedures, has

been delegated authority regarding matters of

significance.

FLSA Exemptions

© 2009 Fox Rothschild

27

Contact Information

Mark Tabakman, Esq.

973.994.7554

[email protected] http://wagehourlaw.foxrothschild.com

Exempt or Non-Exempt? Employee Misclassification Challenges

Current Trends & Vulnerable Positions

Brent E. Pelton, Esq. Pelton & Associates, PC 111 Broadway, Suite 901

New York, New York 10006 www.peltonlaw.com

5/8/2012

28

Assistant Managers

What percentage of the workforce is “managerial”?

Different color shirt is not enough – job duties must truly include managerial responsibilities

Looks bad if paid less than what non-managerial crew members would have earned with overtime (unofficial smell test cross-check)

Not allowed to pro-rate salaries!

29

“Analysts” or “Associates”

Recent college graduates

Positions that require employees to “pay their dues”

May work with significant amounts of $ but position does not exercise significant independent judgment or control

Finance – reconciliations & trade confirmations

Accounting – new unlicensed “accountants”

Interns

30

Financial Services

Employees who have risen through the ranks but still perform ministerial duties

Assistants and highly-compensated employees who have not been delegated significant authority regarding matters of significance

Mortgage loan officers – most companies have resolved this change

IT employees

31

Computer Workers

Help desk & other “break fix” employees

Hedge fund computer employees work on systems used to control billions of dollars, but simply because the work they perform is important does not mean that it is exempt!

Setting up computers & phone systems

Watch out for “on call” work and working from home

32

Other Misclassification Issues Day-rate industries (E.g., construction)

Piece-rate workers get overtime too

Clerical workers – being paid a salary is not enough

Household help – drivers, chefs, housekeepers & nannies

E.g., Hedge fund founder requires his Hamptons staff to work 15+ hour days and to sleep in the basement!

Hourly managers

Partial-day salary deductions are always impermissible!

33

Exempt or Non-Exempt?

Employee Misclassification

Challenges

Identifying Vulnerabilities and Minimizing

Liability Under FLSA and State Law

Daniel J. McCoy, Esq.

Partner and Co-Chair, Employment Practices Group

650-335-7897

Fenwick & West LLP

May 8, 2012

SELF-AUDIT STRATEGIES

Selecting the Auditor

Pay Practices and Policies

Job Descriptions

Post-Merger Integration

Documentation

35

SELF-AUDIT STRATEGIES Selecting the Auditor

Factors in Selecting:

• Skill

• Preserving Atty-Client Privilege

• Optics Of Internal vs. External Resource

– Evaluate Pros And Cons Of Having “Outsiders” Conduct Audit

Engage an auditor with solid knowledge of federal

and state law, and the skill to critically look beyond

job descriptions and questionnaires to ask hard

questions.

36

SELF-AUDIT STRATEGIES Pay Practices and Policies

The duties test is merely half the battle.

Employers must meet the salary test as well to

establish the exemption.

In general, “supplemental” wages beyond base

salary will not defeat the exemption, while

deductions from base pay generally will.

37

SELF-AUDIT STRATEGIES Pay Practices and Policies

Hours-based bonuses are risky and should be

avoided.

MBOs and other performance/merit-based

bonuses are generally permissible, i.e.

consistent with the salary test.

Time-tracking: if you are tracking exempt

worker’s time, is there a good reason for doing

so (e.g. customer billings)?

38

SELF-AUDIT STRATEGIES Job Descriptions

They are Exhibit A in the employer’s exemption

defense, but they are of little value if they do not

reflect a reality and/or are embellished.

Every employer should have a gatekeeper who is

responsible to keep JDs current.

Are internal and external descriptions of exempt

positions consistent? Review job postings and

compare against internal (e.g. JDs, performance

reviews, offer letters, etc.) for consistency.

39

SELF-AUDIT STRATEGIES Post-Merger Integration

It is vitally important for the Acquiror to assess exempt

classifications within the Target’s organization.

Ideally, this is vetted and assessed during the diligence process

and prior to the close, but time and other practical limitations

may prevent this from happening until post-close.

Employers must implement a strategy to explain, in a non-

provocative manner, why employees may be converted from

exempt to non-exempt status.

The Acquiror should use a purchase price escrow and/or strong

indemnification provisions to deal with potential post-close

overtime claims based on alleged misclassification.

40

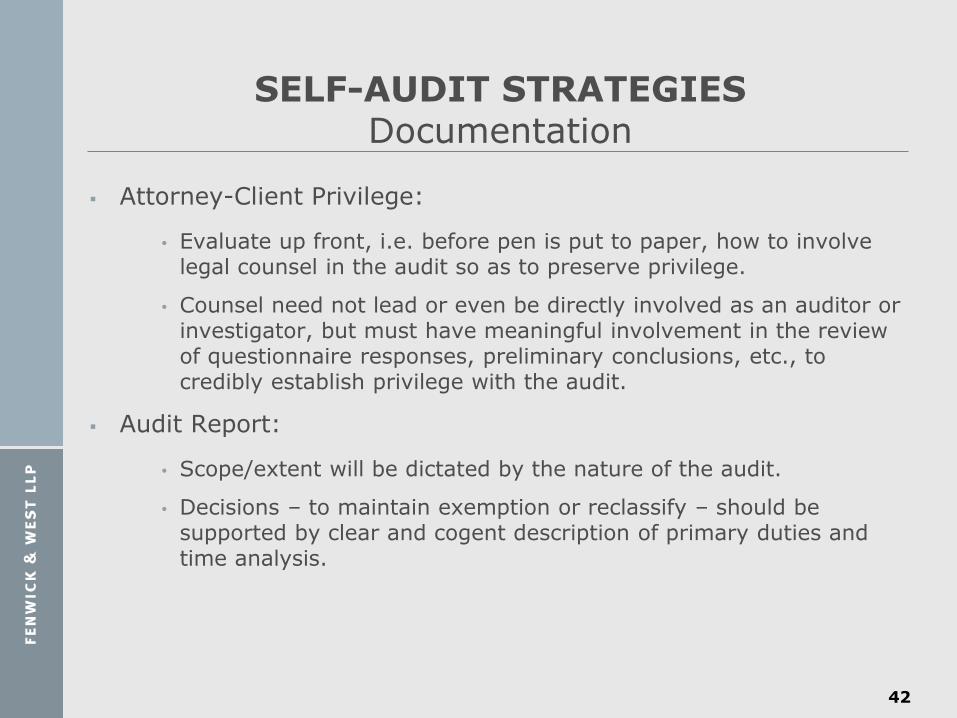

SELF-AUDIT STRATEGIES Documentation

At the outset, the employer should prepare a clear and

comprehensive scope document, setting forth the

groups/positions that will be analyzed and the general plan of

action for the analysis.

Auditor’s primary sources of information:

• Job Descriptions

• Performance Reviews

• Supervisor Input (through interviews and questionnaire responses)

41

SELF-AUDIT STRATEGIES Documentation

Attorney-Client Privilege:

• Evaluate up front, i.e. before pen is put to paper, how to involve legal counsel in the audit so as to preserve privilege.

• Counsel need not lead or even be directly involved as an auditor or investigator, but must have meaningful involvement in the review of questionnaire responses, preliminary conclusions, etc., to credibly establish privilege with the audit.

Audit Report:

• Scope/extent will be dictated by the nature of the audit.

• Decisions – to maintain exemption or reclassify – should be supported by clear and cogent description of primary duties and time analysis.

42

Exempt or Non-Exempt? Employee Misclassification Challenges

Self-Audit Strategies

Brent E. Pelton, Esq. Pelton & Associates, PC 111 Broadway, Suite 901

New York, New York 10006 www.peltonlaw.com

5/8/2012

43

Self-Audit

Most wage & hour complaints arise from unhappy workers

Electronic discovery may provide significant evidence of willful violation

Does the company hire independent contractors?

Is the company trying to do the right thing? Courts are impressed where companies are able to explain the

work that was put into arriving at a classification.

Has the company responded to recent lawsuits and trends?

44

Self-Audit Watch out for: Variations as to classification within departments & across the

industry; Unlawful payroll deductions, meal & rest breaks & accurate

timekeeping systems; Comp-time policies & hourly employees who are automatically paid

based on an 8-hour day; On call & time spent performing work that is not within the regular

workday; and Unpaid prevailing wages within construction and building services

industries.

45

Copyright © 2012 by K&L Gates LLP. All rights reserved.

EXEMPT OR NON-EXEMPT: Employee

Misclassification Challenges

Correcting Errors and Limiting Liability Exposure

May 8, 2012

Christine Watts Johnston

K&L Gates LLP

47

What possible exposure might a company face as a result of misclassification errors?

48

Possible Damages

Damages include:

Minimum wage and overtime

Liquidated (DOUBLE) damages

Prejudgment interest

Reasonable attorneys’ fees

Injunctive relief

Civil Money Penalties per violation

49

Government Enforcement

Civil enforcement by Secretary of Labor

Criminal prosecution by Department of Justice

50

DOL Enforcement Agenda

Goal = Good Jobs for Everyone

Compliance strategy = Plan/Prevent/Protect

Strict construction for application of exemptions

51

How can my company limit

liability for FLSA violations in

litigation?

52

Avoid Finding of Willfulness

Statute of Limitations—extends from 2 to 3 years

for “willful” violations

Willfulness = employer knew or showed reckless

disregard for whether conduct was prohibited

53

Establish Good Faith Reliance Defense

29 U.S.C. §259: employers actions were taken in good

faith conformance with and in reliance on an

administrative regulation, ruling approval or

interpretation of WHD or enforcement policy of WHD

Must be a written ruling, policy, regulation or order

Employer’s actions must be based on reasonableness

under same or similar circumstances

Good faith = bar to action

54

Establish Good Faith Defense

29 U.S.C. §260 Good faith requires:

Subjective good faith belief proceeding lawfully; and

Objective reasonableness

Strong presumption of doubling damages UNLESS

employer establishes good faith

Employer must have taken affirmative or active steps to

ascertain statutory requirements

55

Establish a Compliance

Program

56

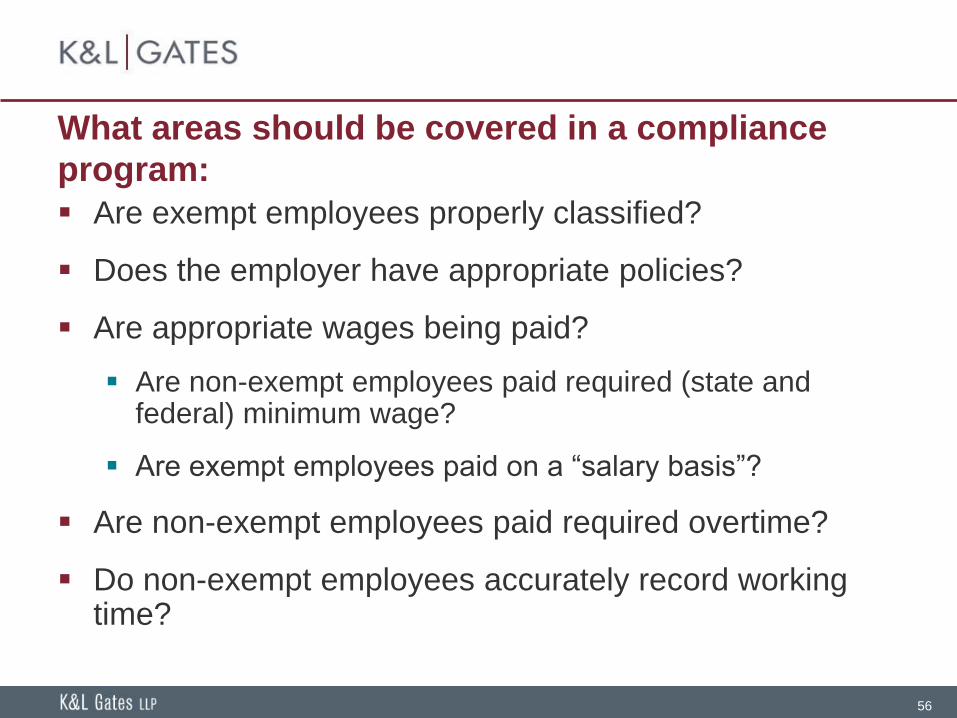

What areas should be covered in a compliance

program:

Are exempt employees properly classified?

Does the employer have appropriate policies?

Are appropriate wages being paid?

Are non-exempt employees paid required (state and federal) minimum wage?

Are exempt employees paid on a “salary basis”?

Are non-exempt employees paid required overtime?

Do non-exempt employees accurately record working time?

57

What areas should be covered in a compliance

program (continued):

Does the company have required postings properly

displayed?

Is the company compliant with record-keeping

requirements?

Is the company following applicable child labor law

restrictions?

58

What should a compliance program include:

Appointment of a compliance manager charged with

oversight of ongoing compliance efforts

Updated policies concerning overtime and pay practices

including safe harbor

Regular and systematic review of classifications and

auditing practices

Education and training of managers responsible for

overseeing pay practices

59

What should a compliance program include:

A toll-free number for employee questions and

complaints

A process for investigating complaints

Payroll integrity policies that guard against practices

such as falsifying time records and working off the clock

Consequences for managers who do not follow company

policies

Regular communication with employees

60

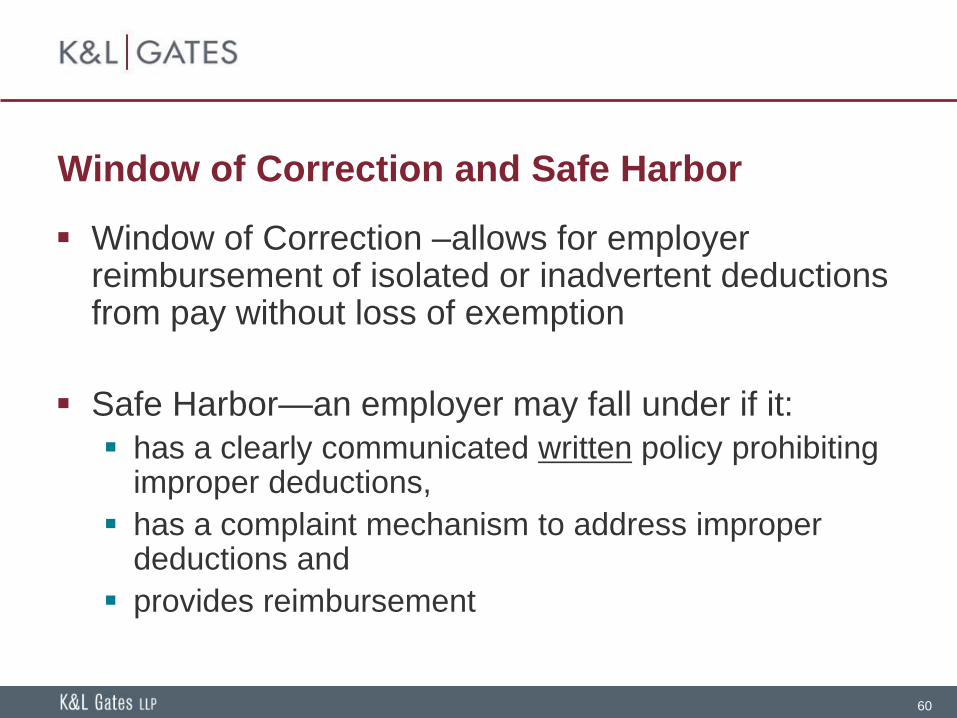

Window of Correction and Safe Harbor

Window of Correction –allows for employer reimbursement of isolated or inadvertent deductions from pay without loss of exemption

Safe Harbor—an employer may fall under if it:

has a clearly communicated written policy prohibiting improper deductions,

has a complaint mechanism to address improper deductions and

provides reimbursement

61

Prompt Investigation and Remedial Action

Complaint response important part of compliance program

In Kasten v. Saint-Gobain Performance the Supreme Court

held that oral complaints of an FLSA violation are protected

conduct under the anti-retaliation provisions

Complaint must be “sufficiently clear and detailed for a

reasonable employer to understand” it as a request for

protection under the FLSA

Rejected notion that only complaints to governmental

agencies were protected

62

Should you notify the DOL of

errors and voluntarily pay back

wages?

63

Fixing a Problem—Changing Classification from

Exempt to Non-Exempt

Once a misclassification is identified, move toward

stemming damages

Consider appropriate timing for communicating and

implementing appropriate changes

Convey message to affected employees with a

clear understanding of how pay/job will be affected

Consider involvement of DOL

64

Confidentiality Protocol for Compliance Assistance

Applies only to telephone inquiries not related to

any DOL investigation, inspection or other matter

where contact initiated by DOL

Information kept confidential “within the bounds of

the law”

No protection from inspection, audit or investigation

as a result of “ordinary” operations

65

Voluntary Resolution of Claims

No prospective waiver of FLSA claims BUT

settlements of bona fide disputes are permitted

Out of court payments for unpaid wages IF

supervised by Secretary of Labor

Litigation settlement subject to scrutiny of courts for

fairness before stipulated judgment

No court approval required where back wages paid

in full (includes liquidated damages)

66

Example—Walmart Settles for $5.29M

DOL announced settlement of claims on 5/1/12 for the time period from June 2004 to March 2007

Affected employees were vision center managers and asset protection coordinators (approx. 4500 employees)

Classifications changed in 2007 – 5 years to reach settlement on amount of payments

Settlement components

$4.6M in back overtime

$155K in damages

$465K in CMPs

Walmart = repeat offender

67

Benefits and Risks of Involving DOL

An employee may NOT bring suit under the FLSA if

s/he has been paid back wages under supervision

of WHD or if Secretary of Labor has filed suit to

recover wages

Federal and state agency partnerships and

information sharing may mean that opening the

door a crack results in a flood of scrutiny

Union organizing campaigns may use knowledge of

compliance shortcomings to further own agenda

68

DOL’s Mobile Tracking Application

Allows workers to track hours work

Summarizes total working time

Calculates wages including overtime

Provides information on wage laws and issues

screen alerts when violations may have

occurred

Does not handle items such as tips,

commissions, bonuses, deductions, holiday

pay, pay for weekends, shift differentials, or pay

for regular days of rest

Copyright © 2012 by K&L Gates LLP. All rights reserved.

EXEMPT OR NON-EXEMPT: Employee

Misclassification Challenges

Correcting Errors and Limiting Liability Exposure

May 8, 2012

Christine Watts Johnston

K&L Gates LLP

Exempt or Non-Exempt? Employee Misclassification Challenges

Correcting Errors & Limiting Liability

Brent E. Pelton, Esq. Pelton & Associates, PC

111 Broadway, Suite 901 New York, New York 10006

www.peltonlaw.com 5/8/2012

70

Correcting Errors & Limiting Liability Exposure

Use care in reclassifying employees or you will hear “the company admitted they were paying us improperly!”

Coordinate DOL investigation & private lawsuit – often DOL will forego its investigation if a federal lawsuit is pending

DO NOT RETALIATE – retaliation may result in additional claims and punitive damages!

Are there records? If not, back wage payments may be based upon employees’ best testimony.

71

Correcting Errors and Limiting Liability Exposure

Is it company-wide or just a rouge manager or one division?

Informal discovery and mediation?

Agree to conditional certification with respect to a narrower class of employees? (job title or geographic location)

Avoid attorneys’ fees and negotiate liquidated damages

Admit mistakes – Judge Cogan recently praised defendant company for admitting misclassification error and negotiating a fair resolution that paid employees 100% of unpaid wages plus some liquidated damages.

Expect judicial scrutiny

72

Correcting Errors and Limiting Liability Exposure

Unions may demand a seat at the table or threaten to object to a settlement

Release of claim must be supervised by the DOL or the court

Use available records to estimate claims

NY DOL will issue back payments but rarely releases – class settlement may be the only way to truly resolve the claim.

If not resolved quickly, FLSA claims tend to grow.

73