ExEcutivE SummariES of SElEctEd SESSionS - … · ExEcutivE SummariES of SElEctEd SESSionS ......

16

EXECUTIVE SUMMARIES OF SELECTED SESSIONS Sponsored by

-

Upload

dangnguyet -

Category

Documents

-

view

240 -

download

0

Transcript of ExEcutivE SummariES of SElEctEd SESSionS - … · ExEcutivE SummariES of SElEctEd SESSionS ......

ExEcutivE SummariES of SElEctEd SESSionS

Sponsored by

Page 2

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

tablE of contEntS

Keynote: business model of the future 3Chris Roark, Managing Director, AccentureKim Anne Starke, Vice President, 2x Consumer Products Growth Partners

food in america – a redefinition of our industry 6Jack Li, Builder, Datassential

the fight for the consumer 9David Portalatin, Vice President, Food Industry Analyst, The NPD GroupScott Gittrich, President, Toppers PizzaGary Kliegman, Vice President, Operations, Blue ApronKeith Boston, Vice President, Foodservice, Cumberland Farms

digital battleground – triggers of change 11Kelly Ungerman, Partner, McKinsey & CompanyCullen Andrews, Vice President of National Accounts, Dot Foods, Inc.Alison Gladwin, Senior Director of Digital and IT, Pizza Hut John Dillon, Chief Marketing Officer, Denny’sDan Ward, Co-Founder and Chief Creative Officer, Detroit Labs

closing Keynote address 15Nigel Travis, Chairman and CEO, Dunkin’ Brands

Presidents ConferenCe

The IFMA Presidents Conference is the place “Where Leaders Meet.” This annual premier top-to-top forum, co-hosted by the NRA and IFDA, brings together influential leaders of foodservice from the operator, manufacturer, and distributor communities. Attendees of this strategic by-invitation-only event meet, connect, and discover insights into the channel’s most timely, critical issues and opportunities.

Page 3

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

develop new business models. Under Armour sees itself as a data company, rather than an apparel company. It has acquired major fitness apps and has more consumer fitness data than any other company. At some point, Under Armour will monetize this data and restructure the industry.

“I would challenge you all to think about disruption and what you could do differently. What could the future look like? How could you fight against the large elephants that dominate industries today?”

— Chris Roark

Financial performance, market dynamics, and strategic investments signal disruptive risk. Accenture has developed a framework that predicts the risk of disruption. Warning signs for disruption fall into three categories:

1. financial performance. Key factors include a change in enterprise value, market share, or pricing power. Enterprise value includes the value of a company based on its assets and free cash flows, and future expectations. If industry economics haven’t changed, the current value of a compa-ny stays constant. If the enterprise value changes, howev-er, the market is predicting an industry change. Decreasing regional- or city-specific market share, as well as eroding pricing power, are tremendous indicators of disruptive risk.

2. Market dynamics. Key factors include non-traditional com-petitors or entrants, acquisitions and joint ventures, and market innovation. For example, Under Armour’s acquisi-tion of MyFitnessPal suggests something is different in the market.

3. strategic investments. Key factors include large invest-ments in adjacencies, solutions, and experiences. These are the best indicators of where larger companies are going.

overviewIndustry disruptors are everywhere, including foodservice. Companies must change their business models to adapt and develop capabilities to stay competitive. It can be helpful to analyze factors like financial performance, market dynam-ics, and strategic investments to assess the risk of industry disruption. Although large, established companies must focus their core business, it is still possible to innovate. The key is to create an ecosystem of partners and leverage data and technology.

contextChris Roark discussed disruption in the food and beverage industry. Kim Anne Starke described how foodservice compa-nies can succeed in today’s dynamic environment.

Key takeawaysDisruption is a radical change like aggregation, disintermediation, or restructuring. In an industry, disruption is a radical change that materially affects the economics and/or creates a new market. Compa-nies face three forms of disruption:

1. Aggregation in the value chain. This is characterized by consolidation of market power while preserving value chain structure and consumer expectations. An example is Marriott’s acquisition of Starwood. The key to countering aggregation is having clarity about what the organization stands for.

2. disintermediation of the value chain. This eliminates intermediary value chain steps, resulting in reduced market influence or competitiveness. IKEA, for example, redefined how people think about furniture and household goods.

3. restructuring the industry. In this case, the industry shifts the supplier, customer, and partner ecosystem in pursuit of a differentiated value proposition or market position. Restructuring is difficult since an entire ecosystem must be created. Starbucks uses partners and prototyping to

KEynotE: buSinESS modEl of thE futurE Chris Roark, managing director, accentureKim Anne Starke, vice President, 2x consumer Products Growth

Page 4

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

In a disruptive market environment, food and beverage companies must reevaluate their strategy. For 40 years, company strategy development focused on where to play and how to win. Traditional sources of competi-tive and market positioning, however, are being disrupted by new business and operating models. When developing strategy, companies must ask what to disrupt.

� identify your real competition. Direct competitors are firms with which you fight on price or service. Experien-tial competitors offer services that replace the need for yours. Examples include Blue Apron or Peapod. Perceptual influencers provide services that fundamentally change customer expectations, such as Amazon or Uber.

� Consider how to disrupt. A good starting point is the services, experiences, and solutions that a company already provides. It is also important to look at the future of the industry and build capabilities now to support those scenarios.

� Assume a start-up mentality. Take a fresh approach to thinking, acting, and operating.

� Think. Prototyping innovation doesn’t have to be expen-sive. Companies must think in different, collaborative ways. The element of local can play an important role. When creating rapid prototypes, play the local game. Disruptive firms also focus on providing solutions and experiences.

� Act. Servicification is coming to the food and beverage industry in the next five to ten years. Most existing com-panies today, however, are defined by customers and product categories.

� Operate. Disrupting a business model often means revamping the cost structure. Many cost structures are heavy on SG&A and light on activities that activate the market. They aren’t designed around capabilities needed to win in 2020. To support investment in digital and ana-lytics, companies can generate additional revenue with new business cases or reduce costs by addressing inef-ficiencies in operating processes. Sustainability and con-sumer trust will become differentiators for distributors and operators. Product traceability is changing the game and leading companies to different ways of working.

To evaluate the disruptive risk in an industry, assess each of the nine factors below.

Over the next five years, the food and beverage industry will experience moderate disruptive risk. Looking ahead, Roark estimates the food and beverage in-dustry has moderate disruptive risk. With regard to packaged foods manufacturers, small is better than big. The largest manufacturers own 45% of the market, but have driven just 3% of the market growth over the past several years. Small brands and companies are winning. The days of one or two billion dollar, blockbuster consumer brands are over. Today’s world will be characterized by ten $100 million dollar brands.

Additional signs of disruption in the industry include:

� Over half of guests (56%) prefer spending money on experience over purchasing in a store.

� Weekly usage of meal delivery increased from 16% in 2010 to 28% in 2015.

� Close to one third of consumers (30%) regularly shop for groceries at four or more stores.

� Over half of guests order from restaurants’ digital plat-forms.

� In the last five years, the number of food trucks has in-creased 12%.

� Close to half of chefs (44%) say local sourcing is the big-gest trend over the last 10 years.

� In the last five years, the number of craft breweries increased 140%.

Over the past three years, many foodservice companies have received venture funding. While none is directly attacking ex-isting companies’ core business models, they are attacking on the fringe. Since big companies are focused on running their core business, they can’t respond. The best alternative is to develop an ecosystem of partners to continuously prototype and innovate.

Page 5

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

For more insights from IFMA programs and events, visit ifmaworld.com.

“The ability to order from anywhere and have it delivered is where technology is going to drive the biggest change in the foodservice industry.”

— Kim Anne Starke

� technology can help large manufacturers leverage their supply chains. Traceability is increasingly important and dif-ficult. Technology will support traceability and food safety.

� data is essential to guide business decisions. 2x Con-sumer Products Growth Partners has its partner companies gather regional data weekly. Even with 12, 24, or 26 weeks of data, it is possible to see the impact of consumer ac-ceptance and trade spending. Data should be shared, as sharing is powerful. Cooperation strengthens what compa-nies can accomplish together.

� Looking ahead, both distributor and manufacturer brands will be important. Consumers don’t know the dif-ference and aren’t loyal to the source of products.

� technologies that support self-service will disrupt foodservice. The ability to order from anywhere and have it delivered is where technology will drive the biggest change.

� Companies with both retail and foodservice business units have an opportunity to create synergies. The food-service business is an avenue for giving exposure to retail brands. Branding in foodservice is critical to success.

� examine what-if questions at least twice a year. For example, what if consumers moved aggressively towards fresh, local, and sustainable? On the operator side, what if operators could share consumer preferences with manu-facturers in real time via POS? What if distributors formed partnerships and ecosystems that created differentiation with manufacturers and operators?

The most successful foodservice companies innovate, leverage technology, and use data. 2x Consumer Products Growth Partners helps build brands through deep operating experience and capital. The firm assists growing companies with investments of $2 to $10 million. It has six full-time employees who work with compa-nies formally and informally. The firm has a broad network of industry venture partners that can help grow businesses.

When looking for investments, 2x Consumer Products Growth Partners seeks differentiated products with a strong consumer position, a strong growth history, and an opportu-nity for exponential growth. Based on her experience with nu-merous foodservice companies, Kim Anne Starke observed:

� innovation in large companies is often stifled due to roi requirements. Good ideas can be born in large and small companies. However, new business ideas need capital and an incubation period. 2x Consumer Products Growth Partners has found that early-stage private companies may need a five- to seven-year time horizon, while more mature companies need three to five years. Publicly traded compa-nies seek quicker returns.

� Looking ahead, consumers will demand natural foods and positive environments from foodservice. Consum-ers care about what they put in their bodies, so it is not surprising that the natural and organic space has been blos-soming and impacting foodservice.

Page 6

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

� Close to three quarters (74%) of all food is eaten at home.

� One in six away-from-home instances also include food from home.

The home represents a major opportunity for foodservice, since it plays a pivotal role in consumer habits. Looking ahead, home meals are expected to become much more important. When people entertain at home, for example, they often acquire food from many different places, which include both retail and foodservice sources.

“From the consumer’s point of view, it’s more of foodservice and retail working together in some way to collectively fulfill all of their needs. I think that’s where we want to find some more collaboration and think about the consumer’s journey for food in terms of all the places they could source things.”

— Jack Li

Foodservice companies could play a larger role in “super occasions” when consumers are multitasking. Occasions are the scenarios in which people eat and drink. Foodservice occasions tend to be for a quick bite, casual lunch, or while running errands. Retail occasions, in contrast, are more likely to be for simple and fast meals or food for fuel.

ovErviEWFor decades, foodservice has been defined as food prepared away from home. Today, however, the lines are blurring be-tween foodservice and in-home meals. When people enter-tain at home, for example, they often acquire food from both retail and foodservice sources. Research shows that people enjoy eating at home when they are multitasking or when they want a comfortable atmosphere. On the other hand, consumers are excited and passionate about away-from-home meals. Rather than trying to get people into restau-rants, foodservice companies can succeed by bringing food to consumers at home. Keys to success are improved access, delivery, and automation.

contExtExclusive to the Presidents Conference, Jack Li shared propri-etary research which shows how consumers use food at and away from home, as well as implications for the foodservice industry.

KEy taKEaWaySHome is becoming a much bigger opportunity for the foodservice industry. Datassential’s research has found that people eat all day long, and eating occasions aren’t easily classified as either foodser-vice or retail. Over the course of a day, it is not uncommon for consumers to have eight distinct eating events. People simply reach out for what is available at the time, rather than making conscious decisions about buying meals from foodservice or retail.

To better understand consumers’ decision-making process, it is important to understand how food is consumed:

� One third of food that is sourced away from home is eaten at that venue.

� Over half the food sourced away from home is eaten at home, at work, or at school.

food in amErica – a rEdEfinition of our induStryJack Li, builder, datassential

Page 7

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

It is important to remember, however, that behavior at home impacts consumers’ opportunities away from home. Jack Li reviewed several statistics about eating at home:

� Habit drives how people eat at home. Three quarters of home decisions are habitual.

� Just half of at-home meals are eaten at the dinner table. One quarter are eaten on the couch and 11% in the bedroom.

� Around half (54%) of at-home meals involve real cook-ing. Approximately one third (30%) are true scratch meals and around one third (32%) are mostly prepared foods.

� Although saving money is a top reason for eating at home, many consumers prefer to eat in the comfort of their home. In addition, there may be a reason like the TV or computer that requires people to be at home.

Rather than trying to get people off their couches and into restaurants, foodservice companies may want to consider bringing food to consumers. This would give people the com-fort and multitasking they desire, while providing the passion associated with away-from-home food. Research shows that people find away-from-home leftovers more exciting than mostly scratch meals, mostly prepared food meals, or home leftovers.

“We have a huge advantage in passion and excitement. We just need to close the gap on convenience, the ability to multitask, and some of the health pieces. Foodservice at home is going to be the biggest growth opportunity for this industry.”

— Jack Li

Research has found, however, that crossover exists between food sourced away from home, food that is sourced from home, and food sourced through a combination of the two. Datassential refers to instances that combine both foodser-vice and retail sources as “super occasions.”

Although consumers are more likely to source food from away from home for most super occasions, the one super oc-casion that is most likely to be associated with food sourced at home is “while doing other things.” Multitasking at home represents a significant opportunity for foodservice to serve consumers.

The foodservice industry has the unique opportunity to marry the passion that consumers have for away-from-home food with the convenience of eating at home. When people want something quick, easy to eat, and healthy, home-sourced food wins. On the other hand, away-from-home food wins in terms of meals that are fun to eat, indulgent, and have bold flavor. Foodservice clearly generates passion and excitement among consumers.

Page 8

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

For more insights from IFMA programs and events, visit ifmaworld.com.

Foodservice companies may want to reevaluate their packaging and food preparation requirements. To help get their food into homes, foodservice companies may need to reexamine their packaging and preparation requirements. If a company’s product categories don’t travel well to consumers, it may be worthwhile to consider packag-ing partnerships. Another key factor is how to prepare foods in ways that will help them travel well.

:

Access, delivery and automation can drive foodservice at home forward. Three factors can promote foodservice at home:

1. Access. Consumers can order food in many different ways today, such as online ordering apps, Amazon, Facebook, Google, and more. Pizza companies have traditionally been very good at access. Domino’s, Pizza Hut, and Papa John’s account for about 40% of online food orders. Datassential believes the access piece is close to being figured out in a big way for consumers.

2. delivery. There are many interesting initiatives under-way to get food to consumers. Autonomous vehicles will play an important role in the future and could significantly reduce delivery costs. Drones may also be used for food delivery. These innovations will make it easier for people to enjoy away-from-home food in the comfort of their homes. Datassential believes the industry is in the early stages of delivery innovation based on emerging technologies.

3. Automation. Robots will become a big thing in everyday life. Consumers are becoming more accepting of automa-tion related to their food. Xavier University, for example, has a pizza ATM. Zume Pizza uses robots to create pizzas in food trucks with onboard ovens.

Page 9

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

Three main drivers create today’s “1% world”:

1. the economy and food inflation. In the 1970s, 1980s, and 1990s, dual-income families drove high traffic growth at restaurants. They demanded convenience and were af-fluent enough to outsource everything in their lives. Today, those fundamentals have changed. Household income may be improving, but the fastest growing household type is one where no one works due to the aging population and retirement.

It is becoming cheaper to eat at home and more expen-sive to eat away from home. The consumer price index for meals sourced away from home is about +2.7%, while it is in negative territory for eating at home.

Total food spending represents a relatively fixed share of household disposable income, hovering around 10%. As the cost of food away from home increases, it collects a greater share of that 10%. Although the FDA estimates that the dollars spent at foodservice is slightly over 50%, the occasions underlying that reveal a different story. Most meals (82%) are sourced from at home, while 18% are sourced from a restaurant. The number of meals per capita eaten on premise in a restaurant remains at or near an all-time low for the fourth consecutive year.

2. Where we work and eat. Many people work at least one day a week at home, which reduces the number of meals eaten in restaurants. Research shows, however, that more in-home meals are sourced from foodservice, especially at dinner.

overviewTraffic growth of 1% or below has become the new normal in the restaurant industry. This can be attributed to the slow economy, food inflation, and consumer preferences for in-home meals. The fight for the consumer dollar has intensified and includes newer food solutions such as meal kits and retail foodservice and an increased focus on foodservice at home. Industry leaders across channels such as Toppers Pizza, Blue Apron, and Cumberland Farms are responding to these trends through experiential offerings and cutting-edge technology.

contextDavid Portalatin described the phenomenon of “blurring lines,” and a panel of industry executives discussed how to win share in today’s ever-changing environment.

Key takeawaysThe economy, work and eating trends, and generational values are driving slow foodservice traffic growth. Traffic growth at 1% or below has become the new normal in the restaurant industry. The NPD Group measures ap-proximately $1.9 trillion of consumer spending. For decades, customer traffic at commercial restaurants has been rising in the 1% range. But for 2016, The NPD Group expects negative traffic numbers.

thE fiGht for thE conSumErDavid Portalatin, vice President, food industry analyst, the nPd GroupScott Gittrich, President, toppers PizzaGary Kliegman, vice President, operations, blue apronKeith Boston, vice President, foodservice, cumberland farms

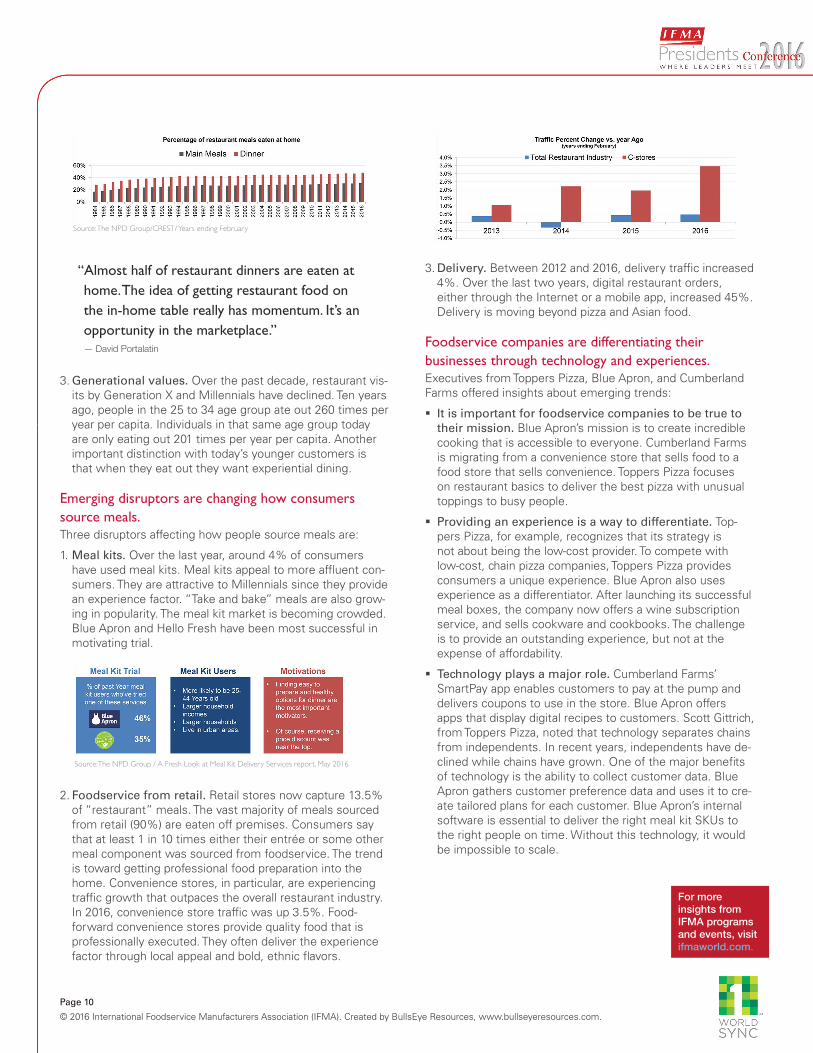

Source: the nPd group/crESt, yE february

Source: bureau of labor Statistics; data through Q1 2016; Graph shows quarterly % change versus year ago

Page 10

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

For more insights from IFMA programs and events, visit ifmaworld.com.

3. delivery. Between 2012 and 2016, delivery traffic increased 4%. Over the last two years, digital restaurant orders, either through the Internet or a mobile app, increased 45%. Delivery is moving beyond pizza and Asian food.

Foodservice companies are differentiating their businesses through technology and experiences. Executives from Toppers Pizza, Blue Apron, and Cumberland Farms offered insights about emerging trends:

� it is important for foodservice companies to be true to their mission. Blue Apron’s mission is to create incredible cooking that is accessible to everyone. Cumberland Farms is migrating from a convenience store that sells food to a food store that sells convenience. Toppers Pizza focuses on restaurant basics to deliver the best pizza with unusual toppings to busy people.

� Providing an experience is a way to differentiate. Top-pers Pizza, for example, recognizes that its strategy is not about being the low-cost provider. To compete with low-cost, chain pizza companies, Toppers Pizza provides consumers a unique experience. Blue Apron also uses experience as a differentiator. After launching its successful meal boxes, the company now offers a wine subscription service, and sells cookware and cookbooks. The challenge is to provide an outstanding experience, but not at the expense of affordability.

� technology plays a major role. Cumberland Farms’ SmartPay app enables customers to pay at the pump and delivers coupons to use in the store. Blue Apron offers apps that display digital recipes to customers. Scott Gittrich, from Toppers Pizza, noted that technology separates chains from independents. In recent years, independents have de-clined while chains have grown. One of the major benefits of technology is the ability to collect customer data. Blue Apron gathers customer preference data and uses it to cre-ate tailored plans for each customer. Blue Apron’s internal software is essential to deliver the right meal kit SKUs to the right people on time. Without this technology, it would be impossible to scale.

“Almost half of restaurant dinners are eaten at home. The idea of getting restaurant food on the in-home table really has momentum. It’s an opportunity in the marketplace.”

— David Portalatin

3. Generational values. Over the past decade, restaurant vis-its by Generation X and Millennials have declined. Ten years ago, people in the 25 to 34 age group ate out 260 times per year per capita. Individuals in that same age group today are only eating out 201 times per year per capita. Another important distinction with today’s younger customers is that when they eat out they want experiential dining.

Emerging disruptors are changing how consumers source meals. Three disruptors affecting how people source meals are:

1. Meal kits. Over the last year, around 4% of consumers have used meal kits. Meal kits appeal to more affluent con-sumers. They are attractive to Millennials since they provide an experience factor. “Take and bake” meals are also grow-ing in popularity. The meal kit market is becoming crowded. Blue Apron and Hello Fresh have been most successful in motivating trial.

2. foodservice from retail. Retail stores now capture 13.5% of “restaurant” meals. The vast majority of meals sourced from retail (90%) are eaten off premises. Consumers say that at least 1 in 10 times either their entrée or some other meal component was sourced from foodservice. The trend is toward getting professional food preparation into the home. Convenience stores, in particular, are experiencing traffic growth that outpaces the overall restaurant industry. In 2016, convenience store traffic was up 3.5%. Food-forward convenience stores provide quality food that is professionally executed. They often deliver the experience factor through local appeal and bold, ethnic flavors.

Source: the nPd Group/crESt/ years ending february

Source:the nPd Group / a fresh look at meal Kit delivery Services report, may 2016

Page 11

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

4. the store still matters. Around 50% of consumers have used or are keen to try “click and collect,” and 42% consid-er it important. Over two thirds of holiday shoppers (69%) who used click and collect purchased additional items while picking up in store. Restaurants are not going away anytime soon, but an open question is how much business will be dine in and how much will be delivery and fulfillment.

5. the notion of customer loyalty has changed. As con-sumers migrate online, many reconsider their retail prefer-ences. When consumers establish new behavior, retailers often see a new level of stickiness. Over half of “add to baskets” are from customers’ favorites lists. Over half of consumers (55%) who leave feedback in an app will churn if their feedback is ignored, while 97% will become more loyal if feedback is implemented.

The move to digital is changing the competitive landscape. Consumers’ move to digital has significant implications for retailers, restaurants, and food manufacturers:

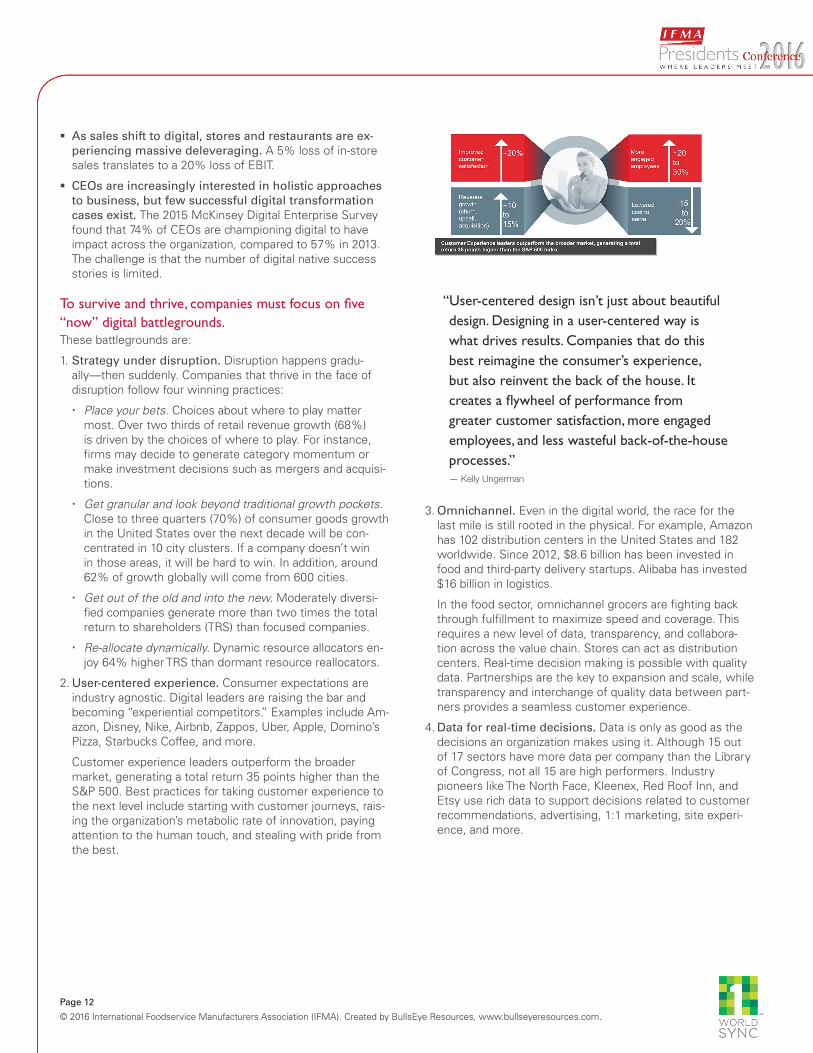

� offline leadership doesn’t guarantee online leader-ship, and catching up is hard. In some retail segments, especially consumer packaged goods, there is a first mover advantage. Once companies lose incumbency, it is hard to catch up. Online leaders in categories like pet food, home care, coffee, and razor blades, for example, are different from the offline leaders.

overviewWith digitalization and the continued evolution of technology, consumers have embraced mobile, and Amazon has rede-fined the online user experience. The foodservice industry is coming to terms with these changes and is gaining momen-tum in the realm of digital.

To succeed, firms must place strategic bets, differentiate on design, use assets to support the omnichannel experience, use data for real-time decision making, and cultivate a culture with a high digital quotient.

contextKelly Ungerman described five digital battlegrounds facing foodservice companies today. A panel of industry executives discussed digital best practices and lessons learned.

Key takeawaysDigital has transformed the consumer decision journey. Across nearly every stage of the consumer decision journey, digital now plays a major role. Observations about today’s digital disruption include:

1. Mobile is the new “front door.” Close to two thirds of the time (65%) that consumers spend on digital media is done through mobile and mainly on apps. Over half of ecom-merce traffic is now from mobile, overtaking desktops.

2. Amazon is the Google of product search. Almost half (45%) of consumers start their mobile journey on Amazon. Data shows that across nearly every category, Amazon has surpassed Google as the first page for product search. Amazon’s online reach is between 500 and 2,500 times greater than other global brands.

3. Amazon is no ordinary disruptor. Amazon is fighting on multiple battlegrounds. The company is focused on logistics and last mile “now” supremacy in many areas, including restaurant delivery. In addition, it is going physical, becom-ing a new media platform, connecting to consumers’ lives through devices like Echo and Dash, and evolving from a retailer to a manufacturer.

diGital battlEGround – triGGErS of chanGE Kelly Ungerman, Partner, mcKinsey & companyCullen Andrews, vice President of national accounts, dot foods, inc.Alison Gladwin, Senior director of digital and it, Pizza hut John Dillon, chief marketing officer, denny’sDan Ward, co-founder and chief creative officer, detroit labs

Source: Slice, Euromonitor

Page 12

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

“User-centered design isn’t just about beautiful design. Designing in a user-centered way is what drives results. Companies that do this best reimagine the consumer’s experience, but also reinvent the back of the house. It creates a flywheel of performance from greater customer satisfaction, more engaged employees, and less wasteful back-of-the-house processes.”

— Kelly Ungerman

3. omnichannel. Even in the digital world, the race for the last mile is still rooted in the physical. For example, Amazon has 102 distribution centers in the United States and 182 worldwide. Since 2012, $8.6 billion has been invested in food and third-party delivery startups. Alibaba has invested $16 billion in logistics.

In the food sector, omnichannel grocers are fighting back through fulfillment to maximize speed and coverage. This requires a new level of data, transparency, and collabora-tion across the value chain. Stores can act as distribution centers. Real-time decision making is possible with quality data. Partnerships are the key to expansion and scale, while transparency and interchange of quality data between part-ners provides a seamless customer experience.

4. data for real-time decisions. Data is only as good as the decisions an organization makes using it. Although 15 out of 17 sectors have more data per company than the Library of Congress, not all 15 are high performers. Industry pioneers like The North Face, Kleenex, Red Roof Inn, and Etsy use rich data to support decisions related to customer recommendations, advertising, 1:1 marketing, site experi-ence, and more.

� As sales shift to digital, stores and restaurants are ex-periencing massive deleveraging. A 5% loss of in-store sales translates to a 20% loss of EBIT.

� Ceos are increasingly interested in holistic approaches to business, but few successful digital transformation cases exist. The 2015 McKinsey Digital Enterprise Survey found that 74% of CEOs are championing digital to have impact across the organization, compared to 57% in 2013. The challenge is that the number of digital native success stories is limited.

To survive and thrive, companies must focus on five “now” digital battlegrounds. These battlegrounds are:

1. strategy under disruption. Disruption happens gradu-ally—then suddenly. Companies that thrive in the face of disruption follow four winning practices:

� Place your bets. Choices about where to play matter most. Over two thirds of retail revenue growth (68%) is driven by the choices of where to play. For instance, firms may decide to generate category momentum or make investment decisions such as mergers and acquisi-tions.

� Get granular and look beyond traditional growth pockets. Close to three quarters (70%) of consumer goods growth in the United States over the next decade will be con-centrated in 10 city clusters. If a company doesn’t win in those areas, it will be hard to win. In addition, around 62% of growth globally will come from 600 cities.

� Get out of the old and into the new. Moderately diversi-fied companies generate more than two times the total return to shareholders (TRS) than focused companies.

� Re-allocate dynamically. Dynamic resource allocators en-joy 64% higher TRS than dormant resource reallocators.

2. User-centered experience. Consumer expectations are industry agnostic. Digital leaders are raising the bar and becoming “experiential competitors.” Examples include Am-azon, Disney, Nike, Airbnb, Zappos, Uber, Apple, Domino’s Pizza, Starbucks Coffee, and more.

Customer experience leaders outperform the broader market, generating a total return 35 points higher than the S&P 500. Best practices for taking customer experience to the next level include starting with customer journeys, rais-ing the organization’s metabolic rate of innovation, paying attention to the human touch, and stealing with pride from the best.

Page 13

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

Battleground 2: Personalization and consistency are impor-tant elements of a user-centered experience. � Personalization is important, but requires a significant investment. Dot Foods has implemented a one-to-one mar-keting platform to communicate with distribution custom-ers and the customers distributors serve. This required a major investment to ensure that marketing messages are relevant and on point. Dot Foods is using analytics to understand customer behavior and deliver applicable user experiences.

� the user experience online and in the restaurant must be consistent. Denny’s has established a strong brand voice, but more work is needed once customers get inside the restaurant. The company established the Guest Experience 2020 Committee to help Denny’s work in conjunction with franchisees. This initiative has rallied the entire system behind incremental, quick adjustments to the guest experience.

Battleground 3: Data and user experience design are the foundation of successful omnichannel initiatives. � reinventing the takeout experience is critical for every brand. Denny’s has been testing delivery and is aggres-sively pursuing partnership opportunities.

� internal data is helpful for marketing to different con-sumer groups. Pizza Hut is embracing the food aggregator space. It recognizes that people that buy from companies like GrubHub are different consumers from those who want a $5.99 carryout pizza. The company is using its internal data to identify how to market to different consumer seg-ments.

� the new generation of customers expects an easy, ac-cessible user experience. Detroit Labs has found that the newer generation of customers is less forgiving. Compa-nies must focus on providing user experiences that are fast and easy.

Battleground 4: With data, it is possible to deliver better customer experiences and reduce costs. � Gs1 standards improve online product searches. Dot Foods relies on GS1 online search capabilities that support product attributes.

� Analytics can identify friction points in the customer journey. Dot Foods uses KPIs to understand online user behavior and to identify friction. This helps the company allocate resources in ways that deliver greater value to customers.

� data supports personalization. Pizza Hut is reconciling internally how much information to push to online cus-tomers and how much to personalize based on customer preferences. Personalization cannot happen without data at the core.

� With digital, manufacturers may improve margins. Digital initiatives can disrupt back-of-house operations and reduce operating costs.

Experience shows that incumbents can adapt to this new environment. Best practices include:

� Don’t let perfect be the enemy of good. Don’t wait for “perfect” data to get started, because it doesn’t exist.

� Create buy-in at the top. Position digital as a new way of doing business, rather than an initiative. Provide digital immersion for the senior team.

� Collaborate and break down silos. Successful analytics applications are a team sport.

� Adopt a fail fast mentality. Experiment often as a means to innovate at speed. Consider conducting over 250 tests per year.

� Formalize new behaviors and processes. Business as usual isn’t an option.

5. digital Quotient (dQ). Most transformations fail because of people. It is essential to raise the digital fluency of all employees, from the C-suite to the front line. Digital lead-ers share several common characteristics:

� They are 5X more likely to define their strategy based on a granular understanding of customer needs along the consumer decision journey.

� They are 4X more likely to take bold risks to transform the customer experience.

� 4 of 5 leading companies have senior leadership commit-ted to digital.

� They are 7X more likely to have made digital a top priority for IT investment.

� Over two thirds (70%) of digital leaders have executive leadership teams that are keenly aware of digital trends and have a track record of impactful digital investment.

There are best practices and lessons learned related to the digital battlegrounds.

Battleground 1: Take a customer-centric view and don’t underestimate the importance of data. � Customer journey mapping is an effective way to guide digital initiatives. Pizza Hut spends considerable time on customer journey mapping. They have analyzed the purchase path to discover friction points, especially in the payment process. Digital can disrupt every part of the value chain, once friction points are identified.

� When it comes to digital, companies must make build vs. buy decisions. Pizza Hut is examining each compo-nent of its technology stack and deciding whether to own, outsource, build, or buy.

� Clean, accurate data is the key to successful digital initiatives. Firms that own their data and know everything about their customers have a stronger marketing position.

Page 14

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

For more insights from IFMA programs and events, visit ifmaworld.com.

� transparent franchise systems reduce friction. Denny’s has developed a transparent franchise system that rein-forces the company’s collaborative culture. This has made it easier to launch digital projects.

Battleground 5: Cultures that value transparency and col-laboration are well suited to digital. � Moving quickly with digital requires cross-functional teams. To deploy digital initiatives more rapidly, Denny’s creates cross-functional projects.

Page 15

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

Dunkin’ Donuts strategy includes two particular areas of em-phasis: digital and coffee.

� digital. By 2020, there will be more mobile subscriptions than people in the world. Dunkin’ Donuts has recognized that digital is a major way to serve guests. In 2012, the company launched the DD mobile app. This was followed by the national launch of on-the-go ordering which was the biggest operational change since the drive-through. The DD Perks program has been a big success. DD Perks members spend more and the data from their visits helps with new product development. The company is also expanding deliv-ery testing. Delivery is the future.

� Coffee. Cold brew coffee was the best product launch Dunkin’ Donuts has had this century. The product is easy for operators to make. In the world of minimum wage, manufacturers should recognize the importance of product simplicity.

The foodservice industry must learn how to operate during turbulent times. Change is happening rapidly in many different areas:

� Politics, economies, and regulations. The world is dealing with issues like Brexit, the U.S. presidential election, and changing Middle East economies.

� fast changing consumers. All consumers, not just Millen-nials, will become more demanding.

� Advertising and digital trends. Fewer people are watching television commercials, which means that companies must reach consumers in different ways.

� Personal safety and security. Every Dunkin’ Brands restaurant must have a safety plan. Other safety concerns include cyber security and food safety.

Blockbuster and other companies demonstrate that firms must disrupt or be disrupted. Many prominent companies have fallen victim to new, more innovative firms. Examples include Kodak, RCA, K-Mart, and Circuit City. One of the biggest disruptors today is Amazon.com. (Travis previously was the CEO at Blockbuster Video. Although the company transformed the video industry, it later fell to Netflix.)

overviewThe world today is characterized by constant change. The foodservice industry must accept turbulence as the new normal and recognize that companies that don’t disrupt are at risk of becoming disrupted. Listening to the customer is more important than ever, as is keeping up with technology, conducting rigorous tests, and paying attention to investors and other stakeholders. Restaurants, suppliers, and distribu-tors who succeed in this environment will meet customer needs, compete with “at home” through competitive pricing, and innovate constantly.

contextNigel Travis discussed Dunkin’ Brands’ approach to business and described ways that suppliers, distributors, and restau-rants can work together more productively.

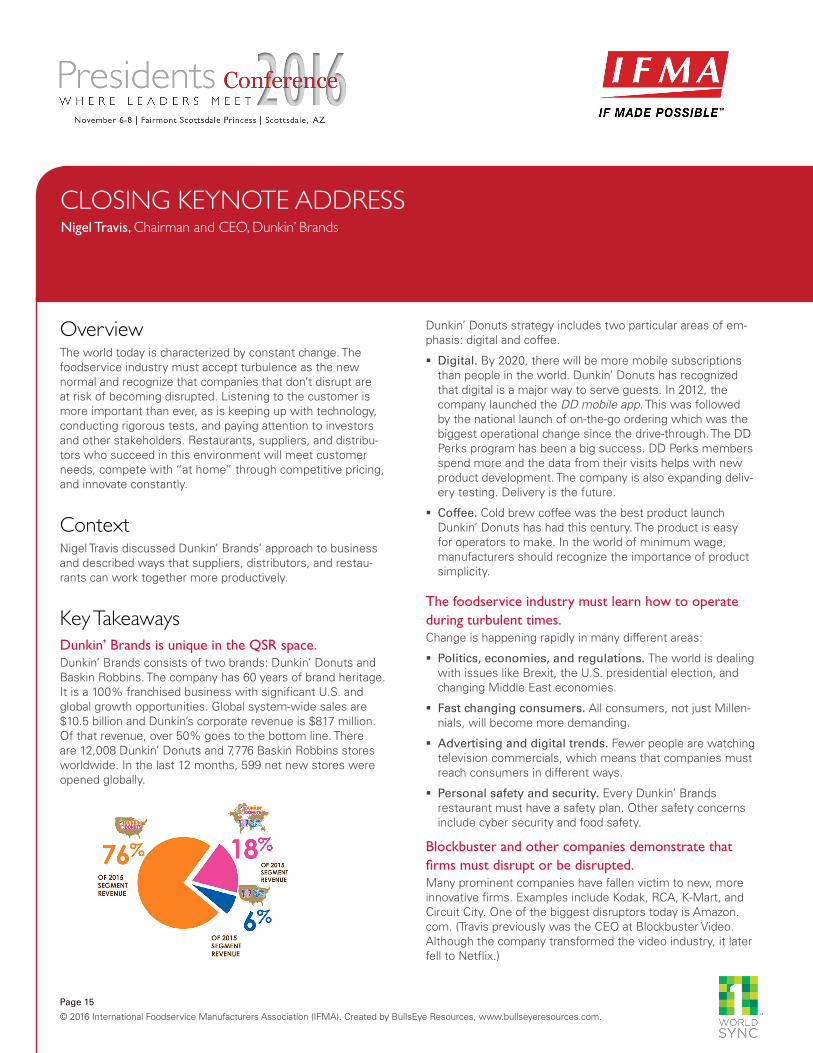

Key takeawaysDunkin’ Brands is unique in the QSR space. Dunkin’ Brands consists of two brands: Dunkin’ Donuts and Baskin Robbins. The company has 60 years of brand heritage. It is a 100% franchised business with significant U.S. and global growth opportunities. Global system-wide sales are $10.5 billion and Dunkin’s corporate revenue is $817 million. Of that revenue, over 50% goes to the bottom line. There are 12,008 Dunkin’ Donuts and 7,776 Baskin Robbins stores worldwide. In the last 12 months, 599 net new stores were opened globally.

cloSinG KEynotE addrESSNigel Travis, chairman and cEo, dunkin’ brands

Page 16

© 2016 International Foodservice Manufacturers Association (IFMA). Created by BullsEye Resources, www.bullseyeresources.com.

For more insights from IFMA programs and events, visit ifmaworld.com.

4. Are we competing with “at home” well enough? Over the last eight months, the price of food at home has been going down. Yet, restaurant prices are going up, due to the minimum wage. Foodservice companies must find ways to compete. Suppliers and distributors can play a large role.

5. Are we delivering the product how customers want it? There are many new ways of delivering product, such as on-the-go and drive through. Delivery will be the real game changer. In the near future, there could be Dunkin’ Donuts Drones.

“There’s going to be a double whammy for our industry of increasing labor costs and increasing commodity costs. Foodservice companies, suppliers, and distributors must find a way together to tackle these issues.”

— Nigel Travis

Suppliers and distributors can work more productively with restaurants.There are several ways suppliers and distributors can work more productively with restaurants:

� Use speed in keeping up to date. Restaurants expect sup-pliers and distributors to share important information in a timely way.

� Constantly listen to the customer. The customer is the consumer who buys products from franchisees. It is essen-tial to think about the unit economics of the franchisees.

� influence regulators and legislators. Suppliers and distributors need to be part of the solution with issues like ingredients and labeling.

� Global trade deals help global unit economics. When Dunkin’ Donuts or Baskin Robbins uses American com-panies, they are more likely to work with these known partners to support overseas operations.

� imagine total disruption. Companies must create contin-gency plans to ensure continuous supply in case disrup-tions occur.

� innovate non-stop. This is essential to meet customer needs.

� optimize costs. Labor costs will keep rising, so restaurants need cost-effective products. As consumers become more demanding, restaurants need cost savings from suppliers and distributors.

The Blockbuster experience illustrates several lessons about industry disruption:

� Listen to the customer and be strategic. Blockbuster didn’t see that customers wanted to migrate away from the struggles associated with video and DVD rentals, like late fees.

� remember that technology change happens at warp speed. For a time, Blockbuster battled changes in DVDs, video-on-demand, and satellite TV. Then the company be-came complacent and technology changes started coming very rapidly.

� don’t underestimate the importance of testing. Block-buster failed to test vending properly. As a result, Redbox gained a foothold. Travis advised foodservice manufacturers to challenge companies like Dunkin’ Brands about how they are conducting testing.

� recognize that stakeholders like activist investors can affect the business. Blockbuster launched Blockbuster Online. This program was integrated with the stores and dif-ferentiated the company from Netflix. Blockbuster grew its share quickly after Blockbuster Online launched and Netflix no longer looked like a major threat. Unfortunately, activist shareholders didn’t like digital since the company had many stores. The end result was that the company took their eye off the digital ball and pursued other tactics, like acquisi-tions. The end result was that Netflix killed Blockbuster.

The foodservice industry must consider whether it is paying attention to customer needs and evolving rapidly enough.Five questions for the foodservice industry to answer are:

1. do we listen to our customers enough? Don’t cut back on customer research. It is more important than ever. Dunkin’ Brands conducts a great deal of consumer re-search. As a result, it discovered that consumers want Dunkin’ products in grocery stores. In response, Dunkin’ launched Dunkin’ K-cups, bean coffee, and creamers into grocery stores. Dunkin’ K-cups was one of the biggest launches ever; in the first year, the company had $220 mil-lion in retail sales and sold 300 million K-cups. By the end of the year, Dunkin’ Donuts ready-to-drink iced coffee will be available in grocery stores, online, and elsewhere.

2. How do we see the future for food and beverage? Com-panies have to go where the consumer is going. Consum-ers want clean ingredients and less sodium.

3. Are we changing fast enough? Suppliers and distributors must challenge foodservice companies and ask if they are changing enough. For example, Travis believes that in a few years Styrofoam cups will go away. Companies must constantly think about what is happening in the market and what consumers want.