Exchange Bulletin - Cboe · with Compagnie JanuaryGenerale de Geophysique (“GGY”) Research...

28

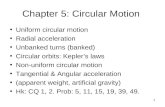

Exchange Bulletin January 19, 2007 Volume 35, Number 3 The Constitution and Rules of the Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, require the Exchange to provide notice to the Exchange membership. To satisfy this requirement, a copy of the Exchange Bul- letin, including the Regulatory Bulletin, is delivered by e-mail free of charge or by hard copy for a fee to all effective members on a weekly basis. Members are encouraged to receive the Exchange and Regulatory Bulletin and Information Circulars via e-mail. E-mail subscrip- tions may be obtained by submitting your name, firm if applicable, e-mail address, and phone number, to [email protected]. There is no charge for e-mail delivery of the Exchange and Regulatory Bulletin or for Information Circulars. If you do sign up for e-mail delivery, please remember to inform the Membership Department of e-mail address changes. Subscriptions for hard copy delivery may be obtained by submitting your name, firm if any, mailing address and telephone num- ber to: Chicago Board Options Exchange, Accounting Department, 400 South LaSalle, Chicago, Illinois 60605, Attention: Bulletin Subscriptions. The cost of an annual subscription (January 1 through December 31) is $200.00 ($100.00 after July 1), payable in advance. For up-to-date Seat Market Quotes, call 1-877-THE-CBOE and select choice 3 from the main menu, or, visit www.CBOE.org, click “CBOE Member Site” and then “Seat Market Information” on the following page. For access to the CBOE Member Web Site, please also notify the Membership Department by sending an e-mail to [email protected] or by phone at 312-786-7449. Copyright © 2007 Chicago Board Options Exchange, Incorporated SEAT MARKET QUOTES AS OF FRIDAY, January 19, 2007 CLASS BID OFFER LAST SALE AMOUNT LAST SALE DATE CBOE $1,825,000.00 $1,995,000.00 $1,900,000.00 January 16, 2007 CBOT FULL MEMBERSHIP CLASS BID OFFER LAST SALE AMOUNT LAST SALE DATE With CBOE Exercise Right $1,801,000.00 $3,000,000.00 $1,950,000.00 November 17, 2006 Without CBOE Exercise Right $1,600,000.00 $6,000,000.00 $1,850,000.00 May 31, 2006 CBOE Exercise Right $148,000.00 $165,000.00 $160,000.00 January 8, 2007 CBOE MEMBERSHIP SALES AND TRANSFERS From To Price/ Transfer Date Harbar Trading Co. Inc. Doron Gahtan $1,900,000.00 1/16/07 Attention CBOE Members and Member Organizations The launch date of the CBOE Stock Exchange (CBSX) is fast approaching. Don’t be left out. Fill out your application today. See Application forms inside. To visit the CBSX website click here.

Transcript of Exchange Bulletin - Cboe · with Compagnie JanuaryGenerale de Geophysique (“GGY”) Research...

ExchangeBulletinJanuary 19, 2007 Volume 35, Number 3

The Constitution and Rules of the Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, require the Exchange to provide notice to the Exchange membership. To satisfy this requirement, a copy of the Exchange Bul-letin, including the Regulatory Bulletin, is delivered by e-mail free of charge or by hard copy for a fee to all effective members on a weekly basis.

Members are encouraged to receive the Exchange and Regulatory Bulletin and Information Circulars via e-mail. E-mail subscrip-tions may be obtained by submitting your name, firm if applicable, e-mail address, and phone number, to [email protected]. There is no charge for e-mail delivery of the Exchange and Regulatory Bulletin or for Information Circulars. If you do sign up for e-mail delivery, please remember to inform the Membership Department of e-mail address changes.

Subscriptions for hard copy delivery may be obtained by submitting your name, firm if any, mailing address and telephone num-ber to: Chicago Board Options Exchange, Accounting Department, 400 South LaSalle, Chicago, Illinois 60605, Attention: Bulletin Subscriptions. The cost of an annual subscription (January 1 through December 31) is $200.00 ($100.00 after July 1), payable in advance.

For up-to-date Seat Market Quotes, call 1-877-THE-CBOE and select choice 3 from the main menu, or, visit www.CBOE.org, click “CBOE Member Site” and then “Seat Market Information” on the following page. For access to the CBOE Member Web Site, please also notify the Membership Department by sending an e-mail to [email protected] or by phone at 312-786-7449.

Copyright © 2007 Chicago Board Options Exchange, Incorporated

SEAT MARKET QUOTES AS OF FRIDAY, January 19, 2007

CLASS BID OFFER LAST SALE AMOUNT LAST SALE DATE

CBOE $1,825,000.00 $1,995,000.00 $1,900,000.00 January 16, 2007

CBOT FULL MEMBERSHIP

CLASS BID OFFER LAST SALE AMOUNT LAST SALE DATE

With CBOE Exercise Right $1,801,000.00 $3,000,000.00 $1,950,000.00 November 17, 2006

Without CBOE Exercise Right $1,600,000.00 $6,000,000.00 $1,850,000.00 May 31, 2006

CBOE Exercise Right $148,000.00 $165,000.00 $160,000.00 January 8, 2007

CBOE MEMBERSHIP SALES AND TRANSFERS

From To Price/Transfer Date

CBOE MEMBERSHIP SALES AND TRANSFERS From To Price/Transfer Date Harbar Trading Co. Inc. Doron Gahtan $1,900,000.00 1/16/07

Attention CBOE Members and Member Organizations

ThelaunchdateoftheCBOEStockExchange(CBSX)isfastapproaching.Don’tbeleftout.

Filloutyourapplicationtoday.SeeApplicationformsinside.

TovisittheCBSXwebsiteclickhere.

Page � January 19, �007 Volume 35, Number 3 Chicago Board Options Exchange

MEMBERSHIP INFORMATION FOR 1/11/07 THROUGH 1/17/07 TerminationDate

Lessor: William F. Egbert 1/16/07Lessee: Drysdale Holdings, LLC

Lessor: Joseph Ianiro 1/17/07Lessee: McGowan Investors, LP

MEMBERSHIP TERMINATIONS

Individual MembersLessor(s): TerminationDate

John H. Hicks 1/11/07

Michael A. Green 1/16/07

Nominee(s) / Inactive Nominee(s): TerminationDate

Bradley D. McCarty (UCB) 1/11/07Susquehanna Investment Group

Daniel H. Frailey (DAN) 1/11/07Susquehanna Investment Group

Trent S. Cutler (TSC) 1/12/07Cutler Group, LP

Thomas W. Pruter 1/12/07Drysdale Holdings, LLC

Courtney T. Andrews (CTY) 1/12/07Timber Hill, LLC

Adnan Zenullahi (AZE) 1/12/07Timber Hill, LLC

Michael P. Marchese (KZE) 1/16/07Cutler Group, LP

Anthony Bond (PRY) 1/16/07Timber Hill, LLC

Gabriel M. Zelwin (GMZ) 1/16/07Grace Trading, LLC

Matthew R. Shaffer (SHA) 1/16/07McGowan Investors, LP

Svebor Smolic (LIC) 1/16/07McGowan Investors, LP

Christopher T. Joseph (CUJ) 1/16/07Diamond Capital Partners, LLC

Daniel C. Zandi (DAZ) 1/17/07MEB Options, Inc.EFFECTIVE MEMBERSHIPS

Individual MembersNominee(s) / Inactive Nominee(s): EffectiveDate

Trent S. Cutler (TSC) 1/11/07Cutler Group, LPTypeofBusinesstobeConducted:MarketMaker

Michael P. Marchese (KZE) 1/12/07Cutler Group, LPTypeofBusinesstobeConducted:MarketMaker

MEMBERSHIP LEASES

New Leases EffectiveDate

Lessor: TRO Trading Group, LLC 1/11/07Lessee: Holland Trading House, LLCRate: $3,800Term:Monthly

Lessor: Fugue 1/11/07Lessee: Cutler Group, LP TrentS.Cutler,NOMINEERate: 0.25%Term:Monthly

Lessor: Robert H. Bloch 1/12/07Lessee: Sallerson-Troob, LLC Matthew E. Minnerick, NOMINEERate: 0.25%Term:Monthly

Lessor: Burt R. Bondy 1/16/07Lessee: SLK-Hull Derivatives, LLCRate: 0.2359%Term:Monthly

Lessor: Scott H. Arenstein 1/16/07Lessee: Lance S. O’DonnellRate: 0.25%Term:Monthly

Lessor: Jennet B. Lingle 1/16/07Lessee: Wolverine Execution Services, LLC Myles Thompson, NOMINEERate: $3,600Term:Monthly

Lessor: Mary Jane O’Connor 1/16/07Lessee: Optiver US, LLCRate: 0.25%Term:Monthly

Lessor: Sam L. Eadie 1/16/07Lessee: Wolverine Execution Services, LLC James E. Bennett, NOMINEERate: $3,800Term:Monthly

Lessor: Daniel A. Gooze 1/16/07Lessee: Wolverine Trading, LLC Andrew J. Skolnick, NOMINEERate: $3,800Term:Monthly

Lessor: Fairfield Investments, Inc. 1/17/07Lessee: Fat Squirrel Trading Group, LLCRate: 0.25%Term:Monthly

Lessor: Neil K. Braverman 1/17/07Lessee: Citadel Derivatives Group, LLCRate: 0.375%Term:Monthly

Lessor: Joseph Ianiro 1/17/07Lessee: Market Street Securities, Inc.Rate: 0.25%Term:Monthly

Terminated Leases TerminationDate

Lessor: John H. Hicks 1/11/07Lessee: Holland Trading House, LLC

Lessor: Fugue 1/11/07Lessee: Jane Street Options, LLC

Lessor: Michael A. Green 1/16/07Lessee: SLK-Hull Derivatives, LLC

Lessor: Sam L. Eadie 1/16/07Lessee: Wolverine Trading, LLC Andrew J. Skolnick (SKO), NOMINEE

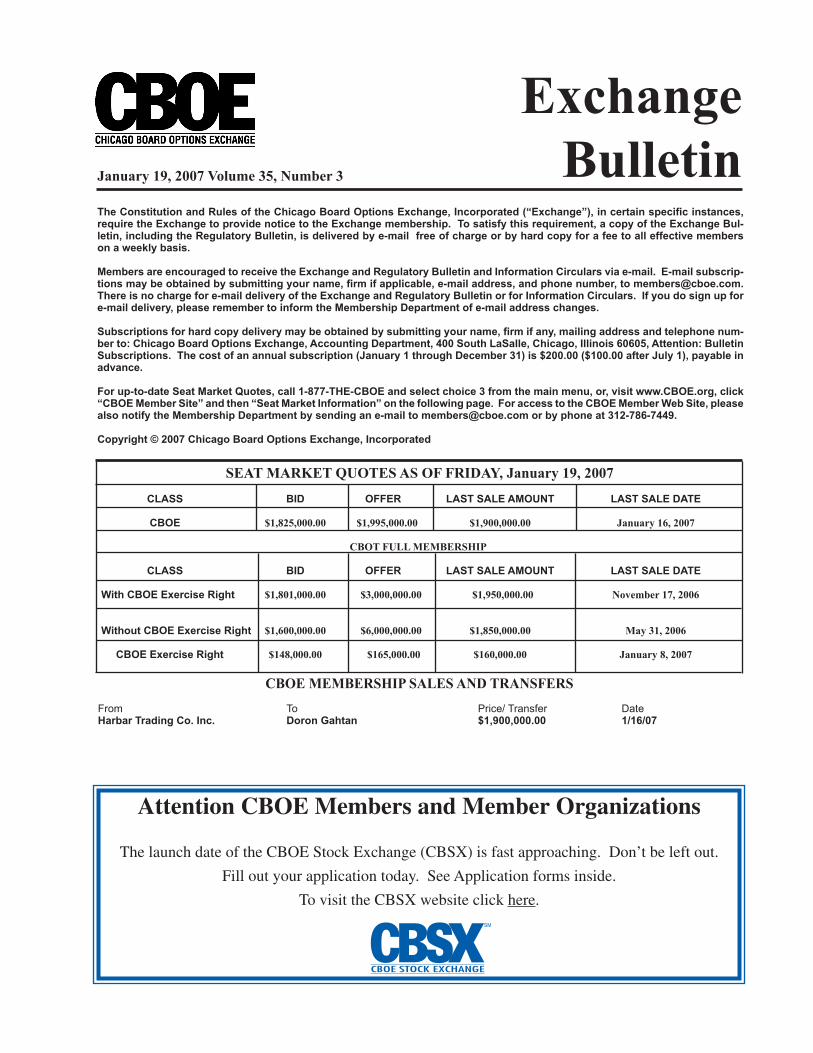

Page 3 January 19, �007 Volume 35, Number 3 Chicago Board Options Exchange

EffectiveDate

Matthew E. Minnerick (MEM) 1/12/07Sallerson-Troob, LLCTypeofBusinesstobeConducted:MarketMaker

Myles Thompson (MLZ) 1/16/07Wolverine Execution Services, LLCTypeofBusinesstobeConducted:FloorBroker

Keith F. Ellett (ELT) 1/16/07Grace Trading, LLCTypeofBusinesstobeConducted:MarketMaker

Steven E. Peter 1/17/07Fat Squirrel Trading Group, LLCTypeofBusinesstobeConducted:RemoteMarketMaker

Member OrganizationsLessor(s): EffectiveDate

Cluny Road Rental, LP 1/11/07

Lessee(s): EffectiveDate

Fat Squirrel Trading Group, LLC 1/17/07TypeofBusinesstobeConducted:RemoteMarketMaker

CHANGES IN MEMBERSHIP STATUS

Individual Members EffectiveDate

Lance S. O’Donnell 1/16/07From: Owner; Market Maker/ Floor BrokerTo: Lessee; Market Maker

Member Organizations EffectiveDate

McGowan Investors, LP 1/16/07From: Lessee; Associated with a Market Maker/ Remote Market MakerTo: Lessee; Associated with a Market Maker

Drysdale Holdings, LLC 1/12/07From: Lessee; Associated with a Market Maker/ Floor Broker/ Remote Market MakerTo: Lessee; Associated with a Market Maker/ Floor Broker

POSITION LIMIT CIRCULARSPursuanttoExchangeRule4.11,theExchangeissuedthebelowlistedPositionLimitCircularsonJanuary12,2007.ThecompletecircularsareavailablefromtheDepartmentofMarketRegulation,inthedatainformationbinsonthe2ndFlooroftheExchange,andontheCBOEwebsiteatcboe.comunderthe“MarketData”tab.

Toreceiveregularupdatesofthepositionlimitlistviafax,contactCandiceNickrandat(312)786-7730.QuestionsconcerningpositionandexerciselimitsmaybedirectedtotheDepartmentofMarketRegulationtoJoeAcevedoat(312)786-7602orTimMacDonaldat(312)786-7706.

RESEARCH CIRCULARS ThefollowingResearchCircularsweredistributedbetweenJanuary12andJanuary19,2007.Ifyouwishtoreadtheentiredocument,pleaserefertotheCBOEwebsiteatwww.cboe.comandclickonthe“TradingTools”Tab.Newlistingsandseriesinformationisalsoavail-ableintheTradingToolssectionofthewebsite.ForquestionsregardinginformationdiscussedinaResearchCircular,pleasecallTheOptionsClearingCorporationat1-888-OPTIONS.

ResearchCircular#RS07-034January12,2007GlobalSignalInc.(“GSL”)ElectionMergerCOMPLETEDwithCrownCastleInternationalCorp.(“CCI/WFB/VVA”)

ResearchCircular#RS07-038January12,2007VeritasDGCInc.(“VTS/YSF/OQS”)ElectionMergerCOMPLETEDwithCompagnieGeneraledeGeophysique(“GGY”)

ResearchCircular#RS07-040January17,2007SeronoS.A.(“SRA”)NameChangeto:MerckSeronoS.A.EffectiveDate:January19,2007

ResearchCircular#RS07-041January17,2007*****UPDATE-REVISIONTOTERMS*****ICOSCorporation(“ICOS/IIQ/WJI/VJI”)ProposedMergerwithEliLillyandCompany

ResearchCircular#RS07-043January17,2007JacuzziBrands,Inc.(“JJZ”)ProposedMergerwithJupiterAcquisition,LLC

ResearchCircular#RS07-046January17,2007McDATACorporationClassA(“MCDTA/MQG/YGV/OVK:)andMcDATACorporationClassB(“MCDT/DXZ/YTO/VGF”)ProposedMergerwithBrocadeCommunicationsSystems,Inc.(“BRCD/BQB”)

ResearchCircular#RS07-047January18,2007VeritasDGCInc.(“VTS/adj.VTU/YSE/OQP”)DeterminationofContractDeliverable

ResearchCircular#RS07-049January18,2007Solexa,Inc.(“SLXA/QMB”)ProposedMergerwithIllumina,Inc.(“ILMN/IQA”)

ResearchCircular#RS07-050January19,2007TheReader’sDigestAssociation,Inc.(“RDA”)ProposedMergerwithRipplewoodHoldings,LLC

PositionLimitCircularPL07-05January12,2007GlobalSignalInc.(“GSL”)mergercompletedwithCrownCastleInternationalCorp.(“CCI/WFB/VVA”)EffectiveDateJanuary16,2007

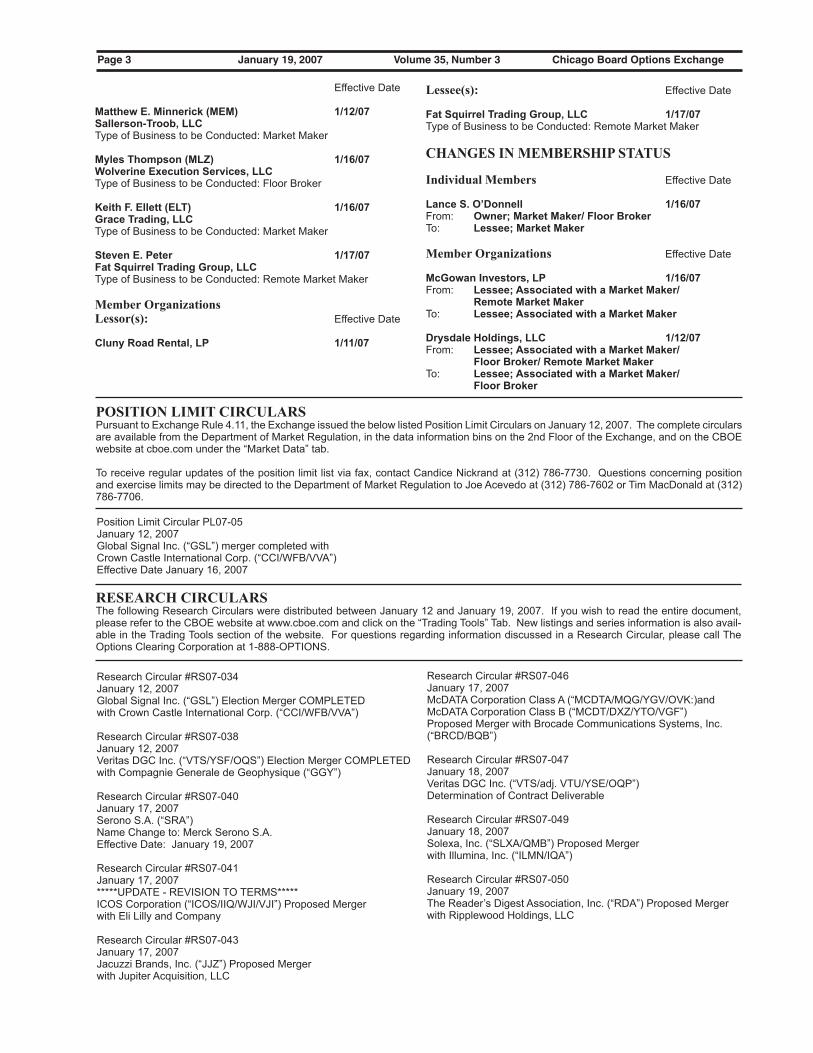

January 24, 2007 Volume RB17, Number 4 1

January 24, 2007 Volume RB18, Number 4

___________________________________________________________________________________ The Constitution and Rules of the Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, require the Exchange to provide notice to the membership. The weekly Regulatory Bulletin is delivered to all effective members to satisfy this requirement. Copyright © 2006 Chicago Board Options Exchange, Incorporated.

REGULATORY CIRCULARS Regulatory Circular RG07-01 To: Members and Member Organizations From: Regulatory Services Division Re: Anti-Money Laundering (“AML”) Compliance Program (CBOE Rule 4.20): Annual Requirements for Previous Filers Meeting Certain Conditions Date: January 16, 2007 All registered broker-dealers, including sole proprietors, are required to demonstrate compliance with the requirements of the USA PATRIOT Act. This Regulatory Circular applies only to those members for which ALL of the following conditions are true 1: • Primary regulator is the CBOE • Not required to file monthly FOCUS reports 2 • Have previously filed AML documents with the CBOE • Your previous filing was complete • Your AML program has not changed • Your Designated AML Compliance Officer has not changed All filers to whom this circular applies are required to submit the following:

• Evidence of annual (or more frequent) AML training for all appropriate persons • A copy of the annual independent review letter identifying the results of the independent review

conducted by an individual not involved with the broker-dealer’s AML function

1 If you have not previously filed AML documents with the Exchange, or you have made changes to your AML procedures, or your designated AML compliance individual has changed or your previous filing was incomplete, please see Regulatory Circular RG07-03 for a description of your CBOE filing requirements. 2 Monthly filers are required to maintain AML documentation as part of the annual routine examination program.

January 24, 2007 Volume RB17, Number 4 2

This information must be submitted to the Department of Member Firm Regulation no later than March 1, 2007. Please do not submit your original documents. Broker-dealers have a books and records requirement to maintain copies of this information. Additionally, please be advised that all AML documentation and ongoing procedures are subject to regulatory review at any time. The following information may be helpful in fulfilling the above requirements. Annual Training Training should be conducted at least annually and developed under the leadership of the AML Compliance Officer or senior management. Broker-dealers should document the content of the training and maintain a list of the participants. The broker-dealer may wish to have participants sign an attestation acknowledging that they have participated in the training and understand the firm’s AML program. The attestation could contain language directing any questions to the firm’s AML Compliance Officer. In addition, training should be updated as necessary to reflect new developments in the PATRIOT Act.

The NASD (http://www.nasd.com) and SIA (http://www.sia.com) websites have on-line training and guidance available which would be considered appropriate training for CBOE Market-Makers that are non-clearing and do not conduct a non-member customer business. Annual Independent Review Letter Broker-dealers must have an independent testing function to review and assess at least annually the adequacy of compliance with the firm’s AML compliance program. In an effort to accommodate CBOE members, the Division has included an example of an independent review letter for members to use as a guideline. This letter should be tailored to accommodate the individual broker-dealer’s business situation. Please direct any questions to the Department of Member Firm Regulation, Mike LaGioia at (312) 786-7728 or Tyson Wilson at (312) 786-7011. Please note: CBOE Rule 4.6 states in part, “no member, person associated with a member or applicant for membership shall make any willful or material misrepresentation, including a misstatement or false statement, or omission in any application, report or other communication to the Exchange, or to the Clearing Corporation….” If you make a false statement you may be subject to disciplinary action by the Exchange.

January 24, 2007 Volume RB17, Number 4 3

Broker-Dealer Annual Training: Attendees: _________________________ ________________________________ __________________________________ ________________________________ __________________________________ ________________________________ The broker-dealer training was conducted on _______________, 200___ and date was done _______________________________________. Some of the topics covered were _______ (internally/externally/via an internet website) ___________________________________________________________________________________ ___________________________________________________________________________________. * Broker-Dealers are required to maintain evidence of the training conducted and a list of

participants. Independent Review: The independent review of the broker-dealer AML program was conducted on __________________, 200___, by __________________________________, date name of ________________________________________________________. company name (internal or external) * Broker-Dealers are required to maintain written documentation of the Independent Review

conducted. I __________________________________, as _________________________________, of name title _______________________________________________, certify that the information listed broker-dealer name above is accurate. Member Signature: __________________________________ Date ___________________

January 24, 2007 Volume RB17, Number 4 4

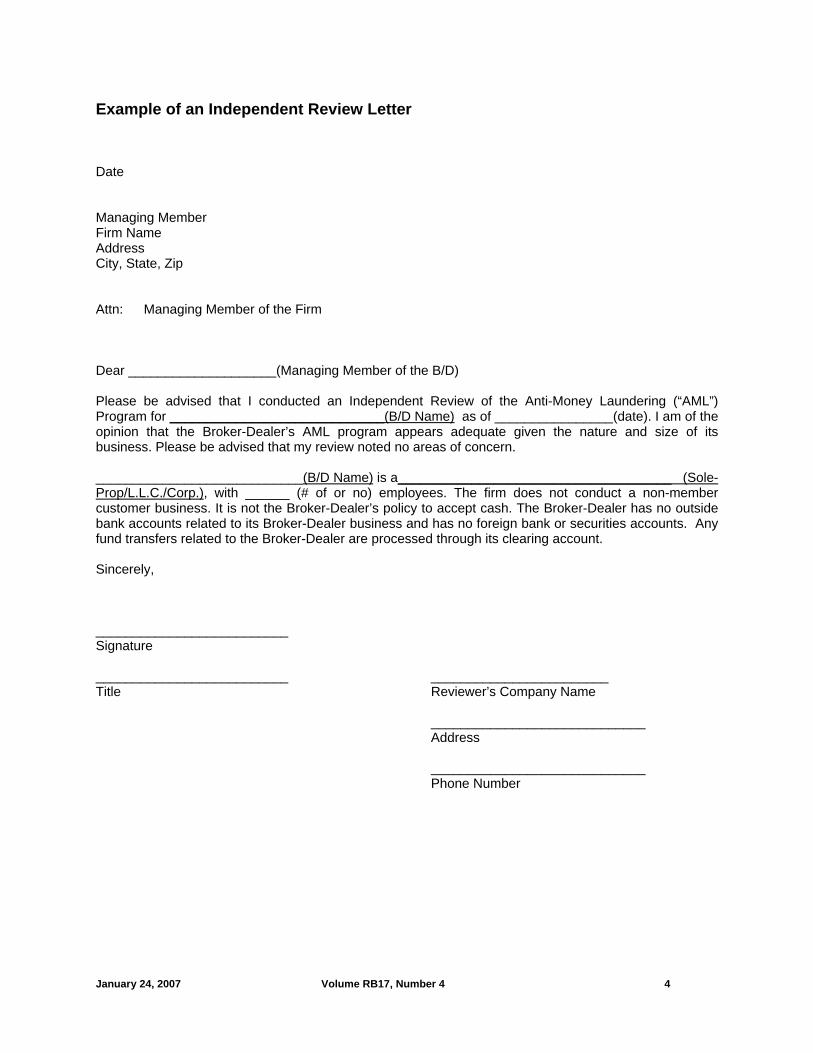

Example of an Independent Review Letter

Date Managing Member Firm Name Address City, State, Zip Attn: Managing Member of the Firm Dear ____________________(Managing Member of the B/D) Please be advised that I conducted an Independent Review of the Anti-Money Laundering (“AML”) Program for _____________________________(B/D Name) as of ________________(date). I am of the opinion that the Broker-Dealer’s AML program appears adequate given the nature and size of its business. Please be advised that my review noted no areas of concern. ____________________________(B/D Name) is a_____________________________________ (Sole-Prop/L.L.C./Corp.), with ______ (# of or no) employees. The firm does not conduct a non-member customer business. It is not the Broker-Dealer’s policy to accept cash. The Broker-Dealer has no outside bank accounts related to its Broker-Dealer business and has no foreign bank or securities accounts. Any fund transfers related to the Broker-Dealer are processed through its clearing account. Sincerely, __________________________ Signature __________________________ ________________________ Title Reviewer’s Company Name

_____________________________ Address _____________________________ Phone Number

January 24, 2007 Volume RB17, Number 4 5

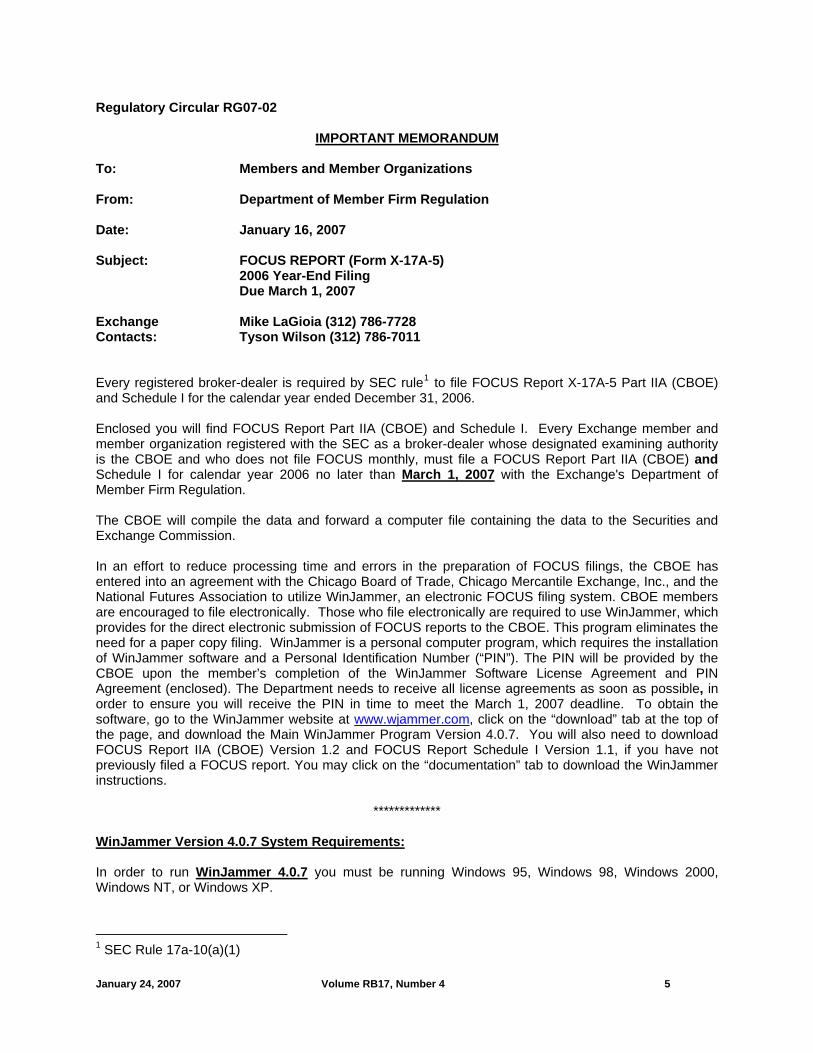

Regulatory Circular RG07-02 IMPORTANT MEMORANDUM To: Members and Member Organizations

From: Department of Member Firm Regulation Date: January 16, 2007

Subject: FOCUS REPORT (Form X-17A-5)

2006 Year-End Filing Due March 1, 2007

Exchange Mike LaGioia (312) 786-7728 Contacts: Tyson Wilson (312) 786-7011

Every registered broker-dealer is required by SEC rule1 to file FOCUS Report X-17A-5 Part IIA (CBOE) and Schedule I for the calendar year ended December 31, 2006. Enclosed you will find FOCUS Report Part IIA (CBOE) and Schedule I. Every Exchange member and member organization registered with the SEC as a broker-dealer whose designated examining authority is the CBOE and who does not file FOCUS monthly, must file a FOCUS Report Part IIA (CBOE) and Schedule I for calendar year 2006 no later than March 1, 2007 with the Exchange's Department of Member Firm Regulation. The CBOE will compile the data and forward a computer file containing the data to the Securities and Exchange Commission. In an effort to reduce processing time and errors in the preparation of FOCUS filings, the CBOE has entered into an agreement with the Chicago Board of Trade, Chicago Mercantile Exchange, Inc., and the National Futures Association to utilize WinJammer, an electronic FOCUS filing system. CBOE members are encouraged to file electronically. Those who file electronically are required to use WinJammer, which provides for the direct electronic submission of FOCUS reports to the CBOE. This program eliminates the need for a paper copy filing. WinJammer is a personal computer program, which requires the installation of WinJammer software and a Personal Identification Number (“PIN”). The PIN will be provided by the CBOE upon the member’s completion of the WinJammer Software License Agreement and PIN Agreement (enclosed). The Department needs to receive all license agreements as soon as possible, in order to ensure you will receive the PIN in time to meet the March 1, 2007 deadline. To obtain the software, go to the WinJammer website at www.wjammer.com, click on the “download” tab at the top of the page, and download the Main WinJammer Program Version 4.0.7. You will also need to download FOCUS Report IIA (CBOE) Version 1.2 and FOCUS Report Schedule I Version 1.1, if you have not previously filed a FOCUS report. You may click on the “documentation” tab to download the WinJammer instructions.

************* WinJammer Version 4.0.7 System Requirements: In order to run WinJammer 4.0.7 you must be running Windows 95, Windows 98, Windows 2000, Windows NT, or Windows XP.

1 SEC Rule 17a-10(a)(1)

January 24, 2007 Volume RB17, Number 4 6

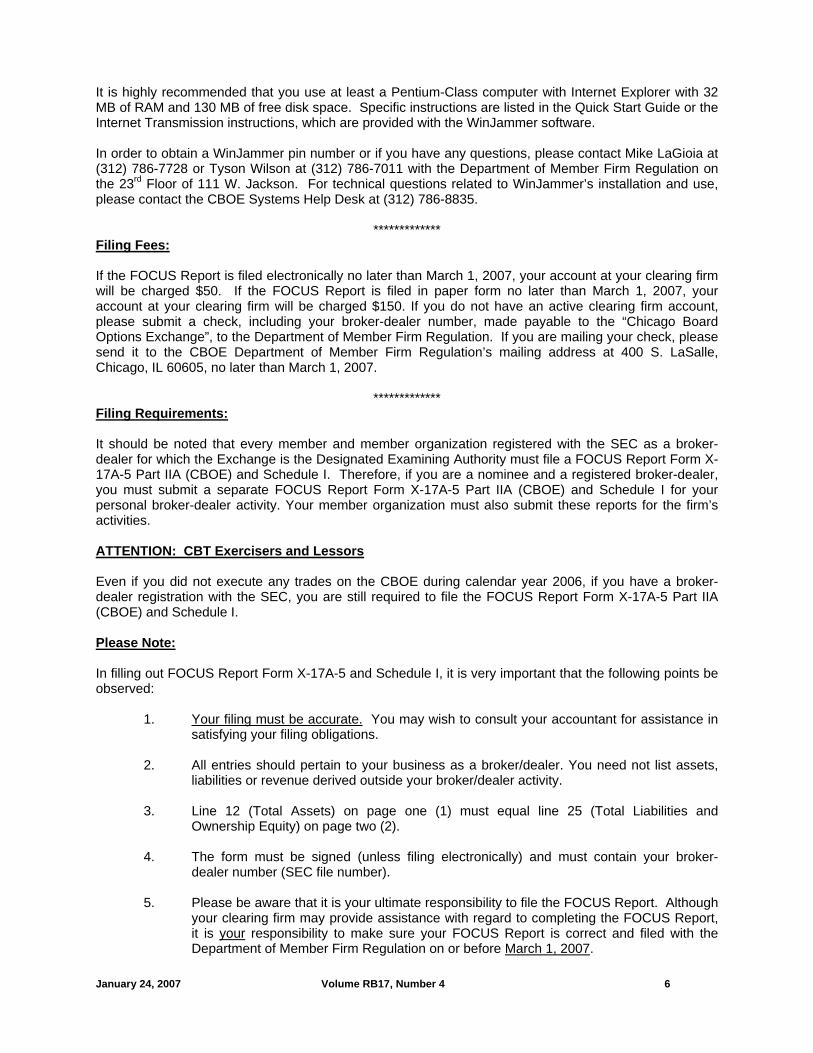

It is highly recommended that you use at least a Pentium-Class computer with Internet Explorer with 32 MB of RAM and 130 MB of free disk space. Specific instructions are listed in the Quick Start Guide or the Internet Transmission instructions, which are provided with the WinJammer software. In order to obtain a WinJammer pin number or if you have any questions, please contact Mike LaGioia at (312) 786-7728 or Tyson Wilson at (312) 786-7011 with the Department of Member Firm Regulation on the 23rd Floor of 111 W. Jackson. For technical questions related to WinJammer’s installation and use, please contact the CBOE Systems Help Desk at (312) 786-8835.

************* Filing Fees: If the FOCUS Report is filed electronically no later than March 1, 2007, your account at your clearing firm will be charged $50. If the FOCUS Report is filed in paper form no later than March 1, 2007, your account at your clearing firm will be charged $150. If you do not have an active clearing firm account, please submit a check, including your broker-dealer number, made payable to the “Chicago Board Options Exchange”, to the Department of Member Firm Regulation. If you are mailing your check, please send it to the CBOE Department of Member Firm Regulation’s mailing address at 400 S. LaSalle, Chicago, IL 60605, no later than March 1, 2007.

************* Filing Requirements: It should be noted that every member and member organization registered with the SEC as a broker-dealer for which the Exchange is the Designated Examining Authority must file a FOCUS Report Form X-17A-5 Part IIA (CBOE) and Schedule I. Therefore, if you are a nominee and a registered broker-dealer, you must submit a separate FOCUS Report Form X-17A-5 Part IIA (CBOE) and Schedule I for your personal broker-dealer activity. Your member organization must also submit these reports for the firm’s activities. ATTENTION: CBT Exercisers and Lessors Even if you did not execute any trades on the CBOE during calendar year 2006, if you have a broker-dealer registration with the SEC, you are still required to file the FOCUS Report Form X-17A-5 Part IIA (CBOE) and Schedule I. Please Note: In filling out FOCUS Report Form X-17A-5 and Schedule I, it is very important that the following points be observed:

1. Your filing must be accurate. You may wish to consult your accountant for assistance in satisfying your filing obligations.

2. All entries should pertain to your business as a broker/dealer. You need not list assets,

liabilities or revenue derived outside your broker/dealer activity.

3. Line 12 (Total Assets) on page one (1) must equal line 25 (Total Liabilities and Ownership Equity) on page two (2).

4. The form must be signed (unless filing electronically) and must contain your broker-

dealer number (SEC file number).

5. Please be aware that it is your ultimate responsibility to file the FOCUS Report. Although your clearing firm may provide assistance with regard to completing the FOCUS Report, it is your responsibility to make sure your FOCUS Report is correct and filed with the Department of Member Firm Regulation on or before March 1, 2007.

January 24, 2007 Volume RB17, Number 4 7

*************

Late Filing Fines: In accordance with CBOE Rule 17.50(g)(2), any member who fails to file Form X-17A-5 and Schedule I for calendar year 2006 by March 1, 2007 will be subject to the following fines:

DAYS LATE AMOUNT

1-30 $200 31-60 $400 61-90 $800

A failure to file by June 1, 2007 will be referred to the Exchange's Business Conduct Committee. The Business Conduct Committee may take whatever action it deems appropriate under the circumstances in addition to the fines noted above. If you are unsure as to whether you are required to file or have any questions, please contact Mike LaGioia at (312) 786-7728 or Tyson Wilson at (312) 786-7011 with the Department of Member Firm Regulation on the 23rd floor of 111 W. Jackson. ____________________________________________________________________________________ Regulatory Circular RG07-03 To: Members and Member Organizations From: Regulatory Services Division Re: Anti-Money Laundering (“AML”) Compliance Program (CBOE Rule 4.20): Annual Requirements for

• First time filers, or • Previous filers whose AML procedures or designated AML compliance

individual have changed since their last filing Date: January 16, 2007 All registered broker-dealers, including sole proprietors, are required to demonstrate compliance with the requirements of the USA PATRIOT Act. This Regulatory Circular applies to members for which ALL of the following conditions are true1: • Primary regulator is the CBOE • You have not filed AML documents with the CBOE OR any part of the AML program has changed • You are not required to file monthly FOCUS reports2 Please note that this circular also applies to sole proprietors, lessors and other individuals who may not necessarily be actively trading. All filers to whom this circular applies are required to submit the following:

1 If you previously filed AML documents with the Exchange, have made no changes to your AML procedures, and your designated AML compliance individual remains the same, please see Regulatory Circular RG07-01 for a description of your CBOE filing requirements. 2 Monthly filers are required to maintain complete AML documentation, which will be reviewed as part of the annual routine examination program.

January 24, 2007 Volume RB17, Number 4 8

A copy of the broker-dealer’s written supervisory procedures for its AML compliance program AML attestation identifying the broker-dealer’s AML Compliance Officer (or other AML compliance

designated person), signed by a member of senior management Evidence of annual (or more frequent) AML training for all appropriate persons of the broker-dealer A copy of an independent review letter identifying the results of the independent review conducted by

an individual not involved with the broker-dealer’s AML function

This information must be submitted to the Department of Member Firm Regulation no later than March 1, 2007. Please do not submit your original documents. Broker-dealers have a books and records requirement to maintain copies of this information. Additionally, please be advised that all AML documentation and ongoing procedures are subject to regulatory review at any time. The following page contains additional information that may be helpful in fulfilling the above requirements.

Procedures To accommodate CBOE members that are non-clearing, do not conduct a non-member customer business, and do not receive customer funds or securities, the Regulatory Services Division created a small-firm AML compliance program template, which is attached to this Circular. This template may suffice in complying with the written procedures requirement. However, every broker-dealer must decide, based on the type of business it is conducting, whether it must adopt highly extensive procedures or whether something less detailed such as the template, will suffice. Training Training should be conducted at least annually and developed under the leadership of the AML Compliance Officer or senior management. Broker-dealers should document the content of the training and maintain a list of the participants. The broker-dealer may wish to have participants sign an attestation acknowledging that they have participated in the training and understand the firm’s AML program. The attestation could contain language directing any questions to the firm’s AML Compliance Officer. In addition, training should be updated as necessary to reflect new developments in the PATRIOT Act. The NASD (http://www.nasd.com) and SIA (http://www.sia.com) websites have on-line training and guidance available to all broker-dealers which would be considered appropriate training for CBOE Market-Makers that are non-clearing and do not conduct a non-member customer business.

Independent Review Letter Broker-dealers must have an independent testing function to review and assess at least annually the adequacy of compliance with the firm’s AML compliance program. In an effort to accommodate CBOE members, the Division has included an example of an independent review letter for members to use as a guideline. This letter should be tailored to accommodate the individual broker-dealer’s business situation.

Please direct any questions to the Department of Member Firm Regulation, Mike LaGioia at (312) 786-7728 or Tyson Wilson at (312) 786-7011.

January 24, 2007 Volume RB17, Number 4 9

Please note: CBOE Rule 4.6 states in part, “no member, person associated with a member or applicant for membership shall make any willful or material misrepresentation, including a misstatement or false statement, or omission in any application, report or other communication to the Exchange, or to the Clearing Corporation…” If you make a false statement you may be subject to disciplinary action by the Exchange.

January 24, 2007 Volume RB17, Number 4 10

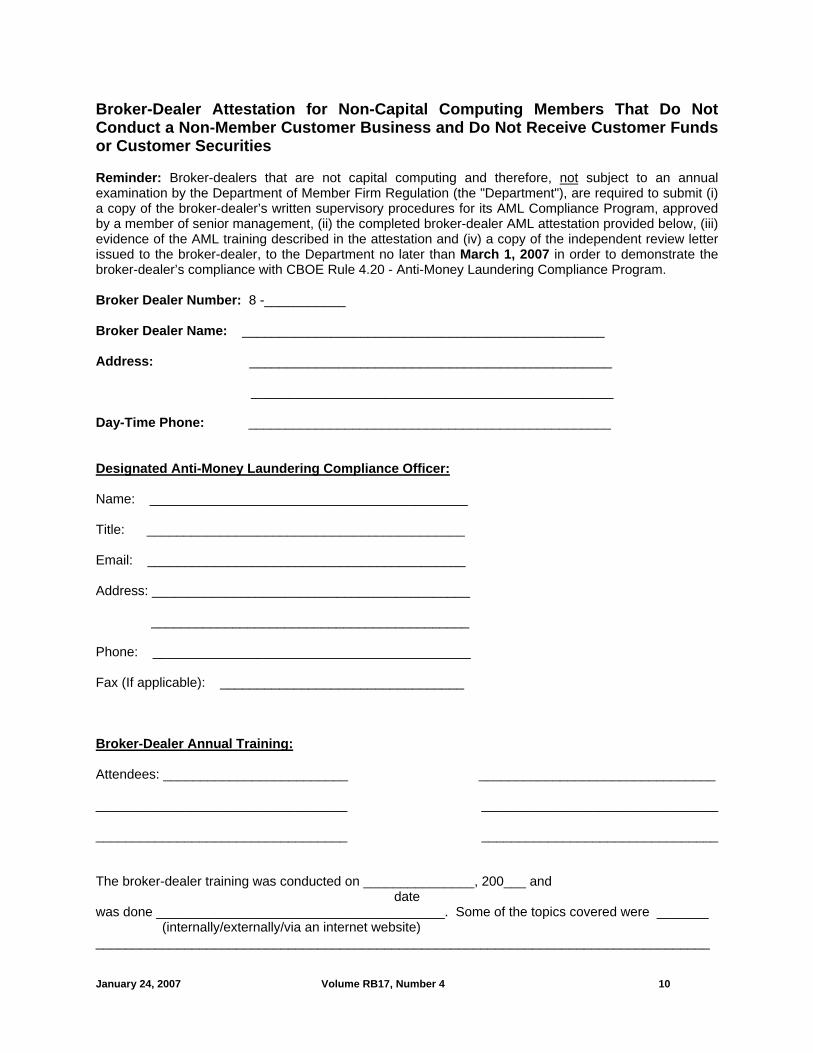

Broker-Dealer Attestation for Non-Capital Computing Members That Do Not Conduct a Non-Member Customer Business and Do Not Receive Customer Funds or Customer Securities Reminder: Broker-dealers that are not capital computing and therefore, not subject to an annual examination by the Department of Member Firm Regulation (the "Department"), are required to submit (i) a copy of the broker-dealer’s written supervisory procedures for its AML Compliance Program, approved by a member of senior management, (ii) the completed broker-dealer AML attestation provided below, (iii) evidence of the AML training described in the attestation and (iv) a copy of the independent review letter issued to the broker-dealer, to the Department no later than March 1, 2007 in order to demonstrate the broker-dealer’s compliance with CBOE Rule 4.20 - Anti-Money Laundering Compliance Program. Broker Dealer Number: 8 -___________ Broker Dealer Name: _________________________________________________ Address: _________________________________________________ _________________________________________________ Day-Time Phone: _________________________________________________ Designated Anti-Money Laundering Compliance Officer: Name: ___________________________________________ Title: ___________________________________________ Email: ___________________________________________ Address: ___________________________________________ ___________________________________________ Phone: ___________________________________________ Fax (If applicable): _________________________________ Broker-Dealer Annual Training: Attendees: _________________________ ________________________________ __________________________________ ________________________________ __________________________________ ________________________________ The broker-dealer training was conducted on _______________, 200___ and date was done _______________________________________. Some of the topics covered were _______ (internally/externally/via an internet website) ___________________________________________________________________________________

January 24, 2007 Volume RB17, Number 4 11

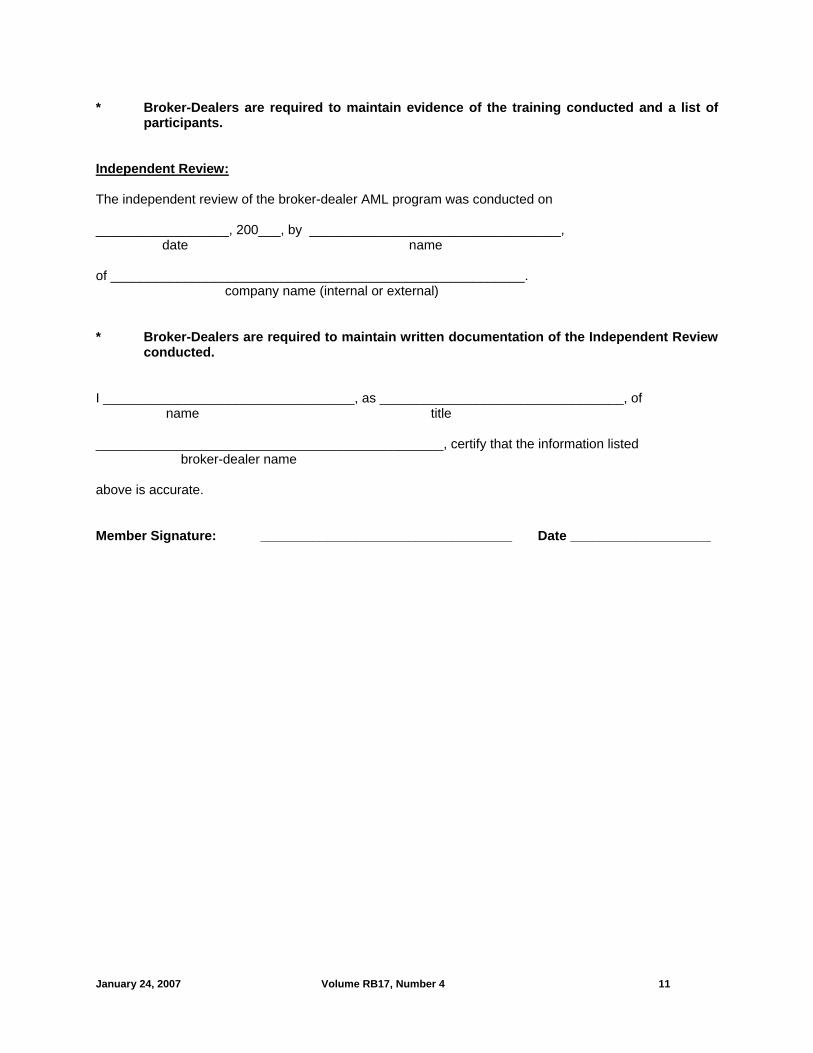

* Broker-Dealers are required to maintain evidence of the training conducted and a list of

participants. Independent Review: The independent review of the broker-dealer AML program was conducted on __________________, 200___, by __________________________________, date name of ________________________________________________________. company name (internal or external) * Broker-Dealers are required to maintain written documentation of the Independent Review

conducted. I __________________________________, as _________________________________, of name title _______________________________________________, certify that the information listed broker-dealer name above is accurate. Member Signature: __________________________________ Date ___________________

January 24, 2007 Volume RB17, Number 4 12

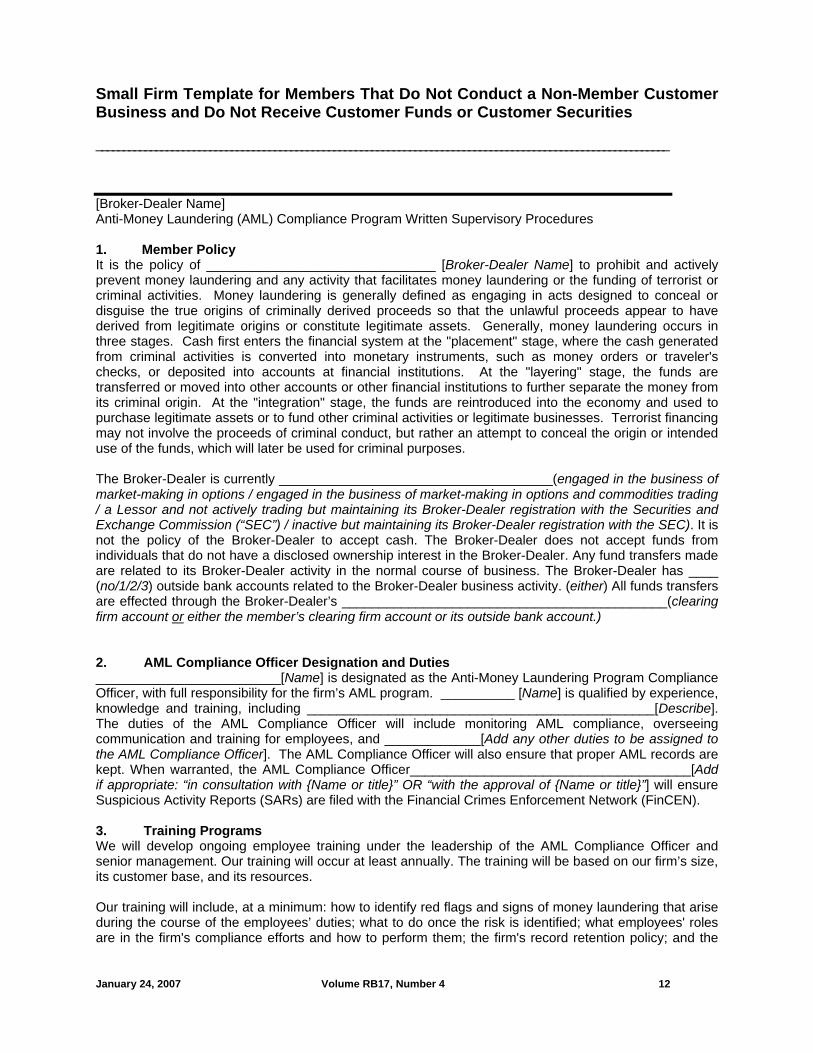

Small Firm Template for Members That Do Not Conduct a Non-Member Customer Business and Do Not Receive Customer Funds or Customer Securities __________________________________________________________________________________________________________

[Broker-Dealer Name] Anti-Money Laundering (AML) Compliance Program Written Supervisory Procedures 1. Member Policy It is the policy of _______________________________ [Broker-Dealer Name] to prohibit and actively prevent money laundering and any activity that facilitates money laundering or the funding of terrorist or criminal activities. Money laundering is generally defined as engaging in acts designed to conceal or disguise the true origins of criminally derived proceeds so that the unlawful proceeds appear to have derived from legitimate origins or constitute legitimate assets. Generally, money laundering occurs in three stages. Cash first enters the financial system at the "placement" stage, where the cash generated from criminal activities is converted into monetary instruments, such as money orders or traveler's checks, or deposited into accounts at financial institutions. At the "layering" stage, the funds are transferred or moved into other accounts or other financial institutions to further separate the money from its criminal origin. At the "integration" stage, the funds are reintroduced into the economy and used to purchase legitimate assets or to fund other criminal activities or legitimate businesses. Terrorist financing may not involve the proceeds of criminal conduct, but rather an attempt to conceal the origin or intended use of the funds, which will later be used for criminal purposes. The Broker-Dealer is currently _____________________________________(engaged in the business of market-making in options / engaged in the business of market-making in options and commodities trading / a Lessor and not actively trading but maintaining its Broker-Dealer registration with the Securities and Exchange Commission (“SEC”) / inactive but maintaining its Broker-Dealer registration with the SEC). It is not the policy of the Broker-Dealer to accept cash. The Broker-Dealer does not accept funds from individuals that do not have a disclosed ownership interest in the Broker-Dealer. Any fund transfers made are related to its Broker-Dealer activity in the normal course of business. The Broker-Dealer has ____ (no/1/2/3) outside bank accounts related to the Broker-Dealer business activity. (either) All funds transfers are effected through the Broker-Dealer’s ____________________________________________(clearing firm account or either the member’s clearing firm account or its outside bank account.) 2. AML Compliance Officer Designation and Duties _________________________[Name] is designated as the Anti-Money Laundering Program Compliance Officer, with full responsibility for the firm’s AML program. __________ [Name] is qualified by experience, knowledge and training, including _______________________________________________[Describe]. The duties of the AML Compliance Officer will include monitoring AML compliance, overseeing communication and training for employees, and _____________[Add any other duties to be assigned to the AML Compliance Officer]. The AML Compliance Officer will also ensure that proper AML records are kept. When warranted, the AML Compliance Officer______________________________________[Add if appropriate: “in consultation with {Name or title}” OR “with the approval of {Name or title}”] will ensure Suspicious Activity Reports (SARs) are filed with the Financial Crimes Enforcement Network (FinCEN). 3. Training Programs We will develop ongoing employee training under the leadership of the AML Compliance Officer and senior management. Our training will occur at least annually. The training will be based on our firm’s size, its customer base, and its resources. Our training will include, at a minimum: how to identify red flags and signs of money laundering that arise during the course of the employees’ duties; what to do once the risk is identified; what employees' roles are in the firm's compliance efforts and how to perform them; the firm's record retention policy; and the

January 24, 2007 Volume RB17, Number 4 13

disciplinary consequences (including civil and criminal penalties) for non-compliance with the PATRIOT Act. We will develop training, or contract for it. Delivery of the training may include educational pamphlets, videos, intranet systems, in-person lectures, and explanatory memos. Currently our training program is:_______________________________________________________________________________________________________________________________________________[Insert specifics, such as “all must view the video entitled “Spotting Money Laundering” by X date or within two weeks of being hired, etc.] We will maintain records to show the persons trained, the dates, and the subject matter of their training. We will review our operations to see if certain employees require specialized additional training. Our written procedures will be updated to reflect any such changes. 4. Independent Testing of the AML Program If conducted by an outside party: The testing of our AML program will be performed by _______________________________ _______________________[Name and Title], an independent third party. Their qualifications include _____________________________________________________________[Describe]. OR If conducted by an employee internally: The testing of our AML program will be performed by _________________________________[Names]. Their qualifications include____________________________________________[Describe.] To ensure that they remain independent, we will separate their functions from other AML activities by____________________________________________________________________________________________________________________[Describe]. Evaluation and Reporting: AML testing will be completed at least annually. The testing will include at a minimum, a review of the Firm’s procedures in correlation with its business activity, a review of any bank account deposit activity for a specific period of time, a review of the Broker-Dealer’s fund transfer activity, both incoming and outgoing made through any clearing firm account or bank account for a specific period of time, a review of any Bank Secrecy Act (“BSA”) forms required to be filed and a review of any Suspicious Activity Reports filed. After the testing is completed, the reviewer will report its findings to ________________________ [Senior Management]. We will address each of the resulting recommendations. 5. Approval I hereby attest that I do not conduct a non-member customer business and do not receive customer funds or customer securities. I have approved this AML program as reasonably designed to achieve and monitor ongoing compliance with the requirements of the USA PATRIOT Act and the implementing regulations under the BSA. AML Program Approval (Approved by Senior Management): Signed:_____________________________________ Print Name: _________________________________ Title:_______________________________________ Broker-Dealer Number: ________________________ Date:_______________________________________

January 24, 2007 Volume RB17, Number 4 14

Example of an Independent Review Letter

Date Managing Member Firm Name Address City, State, Zip Attn: Managing Member of the Firm Dear ____________________(Managing Member of the B/D) Please be advised that I conducted an Independent Review of the Anti-Money Laundering (“AML”) Program for _______________________________(B/D Name) as of ________________(date). I am of the opinion that the Broker-Dealer’s AML program appears adequate given the nature and size of its business. Please be advised that my review noted no areas of concern. ______________________________(B/D Name) is a_____________________(Sole-Prop/L.L.C./Corp.), with ______ (# of or no) employees. The firm does not conduct a non-member customer business. It is not the Broker-Dealer’s policy to accept cash. The Broker-Dealer has no outside bank accounts related to its Broker-Dealer business and has no foreign bank or securities accounts. Any fund transfers related to the Broker-Dealer are processed through its clearing account. Sincerely, __________________________ Signature __________________________ ________________________ Title Reviewer’s Company Name

_____________________________ Address _____________________________ Phone Number

January 24, 2007 Volume RB17, Number 4 15

Regulatory Circular RG07-06 To: Members and Member Organizations From: Legal & Regulatory Services Divisions Date: January 17, 2007 RE: SPX Combination Orders

The purpose of this Regulatory Circular is to remind SPX traders of the requirements for executing SPX Combo Orders pursuant to CBOE Rule 24.20.

Key Issues

The purpose of Rule 24.20 is to facilitate the transaction of an "SPX Combo Order," which is defined in the Rule as an order to purchase or sell SPX options and the offsetting number of SPX combinations defined by the delta. An “SPX combination” is defined as a long (short) SPX call and a short (long) SPX put having the same expiration date and strike price. The “delta” is defined as the positive (negative) number of SPX combinations that must be sold (bought) to establish a market neutral hedge with an SPX option position.

Rule 24.20 will allow a member holding an SPX Combo Order to execute and print the SPX Combo Order at the prices originally quoted within 2 hours after the time of the original quotes, provided that the prices originally quoted satisfy the requirements of Rule 24.20 (b)(1).

When an SPX Combo Order is transacted, the prices of the component series of the order will be reported to the trading floor and to OPRA using the prefix “CMBO.” All handwritten tickets and electronic execution systems, such as the Market-Maker Hand-Held Terminal, should designate the trade as “CMBO” when submitted to the Exchange for price reporting. The “CMBO” prefix acts as notice to the public that the reported prices are part of an SPX Combo Order.

Although other strategies may accomplish a market neutral hedge for SPX options, the relief applicable to SPX Combo Orders only applies if the requirements of Rule 24.20 are satisfied.

Discussion

The purpose of Rule 24.20 is to facilitate hedging SPX options with SPX combinations during times of market volatility. Prior to approval of Rule 24.20 in 2002, SPX market participants holding orders for options tied to combinations frequently experienced difficulty completing such transactions in a volatile market. If the order did not trade immediately, subsequent market volatility would often times prevent the trade from being completed as originally designed because the prices originally quoted for the component legs of the order could no longer be traded within the displayed market quotes, as required under Exchange rules.

Rule 24.20 provides limited relief to SPX market participants in this regard by allowing the component legs of an “SPX Combo Order,” defined as an order to purchase or sell SPX options and the offsetting number of SPX combinations defined by the delta,1 to be traded outside the market quotes (“out-of-range”) under certain circumstances. Specifically, Rule 24.20 allows a member holding an SPX Combo Order to execute and print the SPX Combo Order at the prices originally quoted within 2 hours after the time of the original quotes, provided that the prices originally quoted satisfy the requirements of paragraph (b)(1) of Rule 24.20.

Paragraph (b)(1) of the Rule states the priority requirement for SPX Combo Orders in the same manner as CBOE Rules 6.45(e).2 Specifically, when a member holding an SPX Combo Order and bidding or offering in a multiple of the minimum increment on the basis of a total debit or credit for the order has determined that the order may not be executed by a combination of transactions with the bids 1 See the “key issues” summary above for the definitions of an “SPX combination” and the “delta.” 2 Rule 6.45(e) provides a limited exception from the normal time and price priority rules for certain complex orders.

January 24, 2007 Volume RB17, Number 4 16

and offers displayed in the SPX limit order book or by the displayed quotes of the crowd, then the order may be executed at the best net debit or credit so long as: (A) no leg of the order would trade at a price outside the currently displayed bids or offers in the trading crowd or bids or offers in the SPX limit order book and (B) at least one leg of the SPX combination would trade at a price that is better than the corresponding bid or offer in the SPX limit order book. Thus, SPX traders continue to be required to check the limit order book when an SPX Combo Order is first entered and before trading the order.

When an SPX Combo Order is transacted, the prices of the component series of the order will be reported to the trading floor and to OPRA using the new prefix “CMBO.” The “CMBO” will act as notice to the public that the reported prices are part of an SPX Combo Order. All handwritten tickets and electronic execution systems, such as the Market-Maker Hand-Held Terminal, should designate the trade as “CMBO” when submitted to the Exchange for price reporting.

Please be reminded that, although other strategies may accomplish a market neutral hedge for SPX options, the relief applicable to SPX Combo Orders only applies if the requirements of Rule 24.20 are satisfied.

The Regulatory Services Division monitors member trading activity for compliance with Rule 24.20. Rule 24.20 does not diminish the obligation of CBOE members to obtain best execution for their customers. The appearance of a pattern or practice of failing to execute and report these trades pursuant to the Rule without exceptional circumstances may be subject to referral to the Exchange’s Business Conduct Committee for formal disciplinary action.

If you have any questions concerning this circular, please contact Joanne Heenan-Hustad, Regulatory Services Division, at 312-786-7786, or Jennifer Lamie, Legal Division, at 312-786-7576. The complete text of Rule 24.20 is included below for reference.

* * * * *

SPX Combination Orders

RULE 24.20 (a) For purposes of this rule, the following terms shall have the following meanings:

(1) An “SPX combination” is a long SPX call and a short SPX put having the same expiration date and strike price.

(2) A “delta” is the positive (negative) number of SPX combinations that must be sold (bought) to establish a market neutral hedge with an SPX option position.

(3) An "SPX Combo Order" is an order to purchase or sell SPX options and the offsetting number of SPX combinations defined by the delta.

(b) An SPX Combo Order may be transacted in the following manner:

(1) When a member holding an SPX Combo Order and bidding or offering in a multiple of the minimum increment on the basis of a total debit or credit for the order has determined that the order may not be executed by a combination of transactions with the bids and offers displayed in the SPX limit order book or by the displayed quotes of the crowd, then the order may be executed at the best net debit or credit so long as (A) no leg of the order would trade at a price outside the currently displayed bids or offers in the trading crowd or bids or offers in the SPX limit order book and (B) at least one leg of the SPX combination would trade at a price that is better than the corresponding bid or offer in the SPX limit order book.

(2) Notwithstanding any other rules of the Exchange, if an SPX Combo Order is not executed immediately, the SPX Combo Order may be executed and printed at the prices originally quoted for each of the component option series within 2 hours after the time of the original quotes.

* * * * *

(This circular replaces Regulatory Circulars RG02-013 and RG02-016.)

___________________________________________________________________________________

January 24, 2007 Volume RB17, Number 4 17

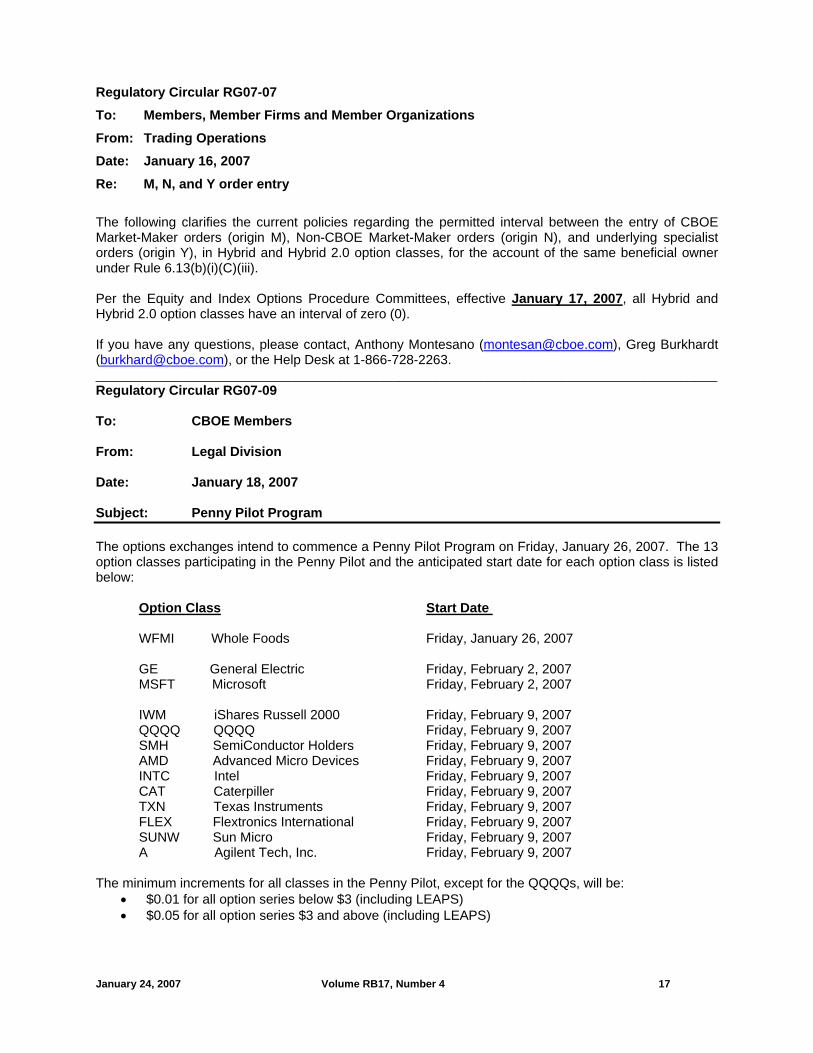

Regulatory Circular RG07-07 To: Members, Member Firms and Member Organizations From: Trading Operations Date: January 16, 2007 Re: M, N, and Y order entry The following clarifies the current policies regarding the permitted interval between the entry of CBOE Market-Maker orders (origin M), Non-CBOE Market-Maker orders (origin N), and underlying specialist orders (origin Y), in Hybrid and Hybrid 2.0 option classes, for the account of the same beneficial owner under Rule 6.13(b)(i)(C)(iii). Per the Equity and Index Options Procedure Committees, effective January 17, 2007, all Hybrid and Hybrid 2.0 option classes have an interval of zero (0). If you have any questions, please contact, Anthony Montesano ([email protected]), Greg Burkhardt ([email protected]), or the Help Desk at 1-866-728-2263. ____________________________________________________________________________________ Regulatory Circular RG07-09 To: CBOE Members From: Legal Division Date: January 18, 2007 Subject: Penny Pilot Program The options exchanges intend to commence a Penny Pilot Program on Friday, January 26, 2007. The 13 option classes participating in the Penny Pilot and the anticipated start date for each option class is listed below:

Option Class

Start Date

WFMI Whole Foods Friday, January 26, 2007 GE General Electric Friday, February 2, 2007 MSFT Microsoft Friday, February 2, 2007 IWM iShares Russell 2000 Friday, February 9, 2007 QQQQ QQQQ Friday, February 9, 2007 SMH SemiConductor Holders Friday, February 9, 2007 AMD Advanced Micro Devices Friday, February 9, 2007 INTC Intel Friday, February 9, 2007 CAT Caterpiller Friday, February 9, 2007 TXN Texas Instruments Friday, February 9, 2007 FLEX Flextronics International Friday, February 9, 2007 SUNW Sun Micro Friday, February 9, 2007 A Agilent Tech, Inc. Friday, February 9, 2007

The minimum increments for all classes in the Penny Pilot, except for the QQQQs, will be:

• $0.01 for all option series below $3 (including LEAPS) • $0.05 for all option series $3 and above (including LEAPS)

January 24, 2007 Volume RB17, Number 4 18

For QQQQs, the minimum increment will be $0.01 for all option series. For all other option classes not participating in the Penny Pilot, the current quoting and trading minimum increments will remain the same. If you have any questions, please contact Tom Knorring at (312) 786-7363 or [email protected], or Patrick Sexton at (312) 786-7467 or [email protected]

RULE CHANGES APPROVED RULE CHANGE(S) The Securities and Exchange Commission ("SEC") has approved the following change(s) to Exchange Rules pursuant to Section 19(b) of the Securities Exchange Act of 1934, as amended ("the Act"). Copies are available on the CBOE public website at www.cboe.com/legal/effectivefiling.aspx. The effective date of the rule change is the date of approval unless otherwise noted. ____________________________________________________________________________________ SR-CBOE-2006-88 Market Data Fees On January 8, 2007, the SEC approved Rule Change File No. SR-CBOE-2006-88, which filing codifies a fee schedule for the sale of open and close volume data on CBOE-listed options by Market Data EXpress, LLC, a wholly-owned subsidiary of CBOE. Any questions regarding the rule change may be directed to Jaime Galvan, Legal Division, at 312-786-7058. The rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2006-088.pdf. ____________________________________________________________________________________ EFFECTIVE-ON-FILING RULE CHANGE(S) The following rule filing(s) were submitted to the SEC “effective-on-filing,” and may have taken effect pursuant to Section 19(b)(3) of the Securities Exchange Act. They will remain in effect barring further action by the SEC within 60 days after their publication in the Federal Register. Copies are available on the CBOE public website at www.cboe.com/legal/effectivefiling.aspx. ____________________________________________________________________________________ SR-CBOE-2007-07 SizeQuote Mechanism On January 16, 2007, the Exchange filed Rule Change File No. SR-CBOE-2007-07, which filing proposes to extend through February 15, 2008 the pilot in CBOE Rule 6.74(f) pertaining to the SizeQuote Mechanism, which is a process by which a Floor Broker may execute and facilitate large-sized orders in open outcry. Any questions regarding the rule change may be directed to Jennifer Lamie, Legal Division, at 312-786-7576. The rule text is shown below and the rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2006-088.pdf. Additions are underlined. Deletions are [bracketed].

Rule 6.74 Crossing Orders RULE 6.74. (a) – (e) No change. (f) Open Outcry "SizeQuote" Mechanism

(i) SizeQuotes Generally: The SizeQuote Mechanism is a process by which a floor broker ("FB") may execute and facilitate large-sized orders in open outcry. Floor brokers must be willing to facilitate the entire size of the order for which they request SizeQuotes (the "SizeQuote Order") or to execute it against one or more solicited orders, or against a combination of solicited and facilitation orders. The appropriate

January 24, 2007 Volume RB17, Number 4 19

Market Performance Committee shall determine the classes in which the SizeQuote Mechanism shall apply. The SizeQuote Mechanism will operate as a pilot program which expires February 15, [2007]2008.

(A) – (D) No change.

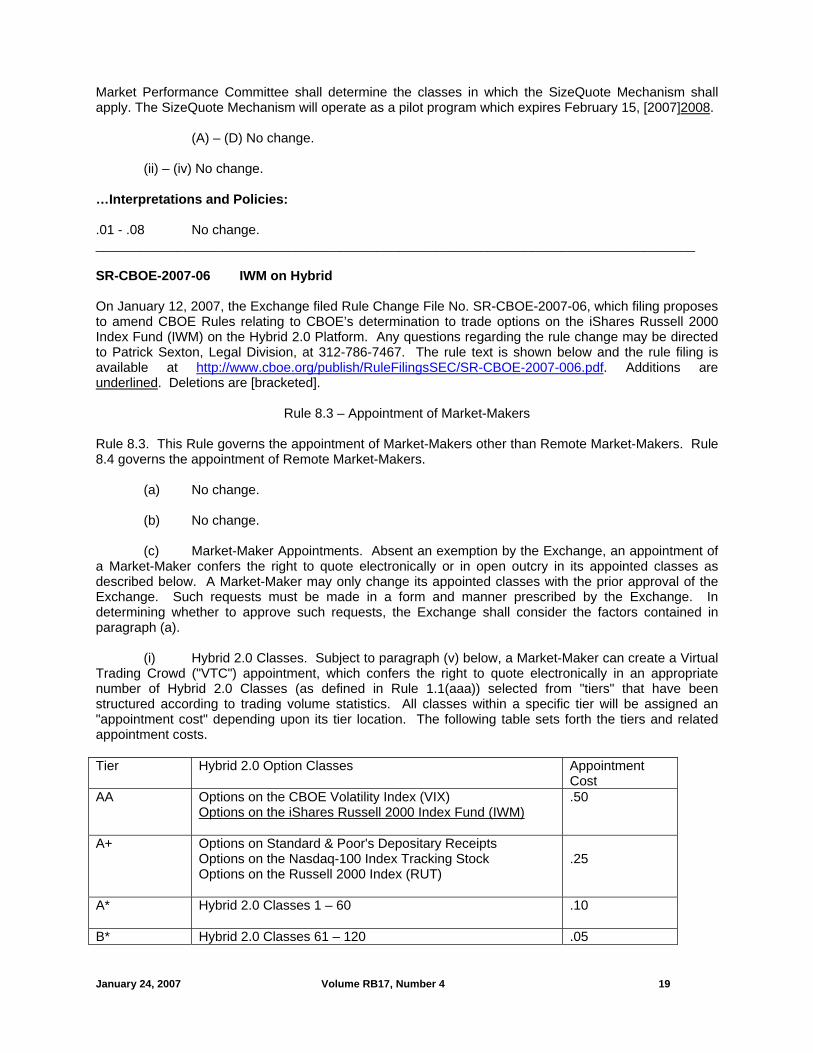

(ii) – (iv) No change. …Interpretations and Policies: .01 - .08 No change. _________________________________________________________________________________ SR-CBOE-2007-06 IWM on Hybrid On January 12, 2007, the Exchange filed Rule Change File No. SR-CBOE-2007-06, which filing proposes to amend CBOE Rules relating to CBOE’s determination to trade options on the iShares Russell 2000 Index Fund (IWM) on the Hybrid 2.0 Platform. Any questions regarding the rule change may be directed to Patrick Sexton, Legal Division, at 312-786-7467. The rule text is shown below and the rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2007-006.pdf. Additions are underlined. Deletions are [bracketed].

Rule 8.3 – Appointment of Market-Makers Rule 8.3. This Rule governs the appointment of Market-Makers other than Remote Market-Makers. Rule 8.4 governs the appointment of Remote Market-Makers.

(a) No change. (b) No change. (c) Market-Maker Appointments. Absent an exemption by the Exchange, an appointment of a Market-Maker confers the right to quote electronically or in open outcry in its appointed classes as described below. A Market-Maker may only change its appointed classes with the prior approval of the Exchange. Such requests must be made in a form and manner prescribed by the Exchange. In determining whether to approve such requests, the Exchange shall consider the factors contained in paragraph (a). (i) Hybrid 2.0 Classes. Subject to paragraph (v) below, a Market-Maker can create a Virtual Trading Crowd ("VTC") appointment, which confers the right to quote electronically in an appropriate number of Hybrid 2.0 Classes (as defined in Rule 1.1(aaa)) selected from "tiers" that have been structured according to trading volume statistics. All classes within a specific tier will be assigned an "appointment cost" depending upon its tier location. The following table sets forth the tiers and related appointment costs. Tier

Hybrid 2.0 Option Classes Appointment Cost

AA

Options on the CBOE Volatility Index (VIX) Options on the iShares Russell 2000 Index Fund (IWM)

.50

A+

Options on Standard & Poor's Depositary Receipts Options on the Nasdaq-100 Index Tracking Stock Options on the Russell 2000 Index (RUT)

.25

A*

Hybrid 2.0 Classes 1 – 60

.10

B* Hybrid 2.0 Classes 61 – 120 .05

January 24, 2007 Volume RB17, Number 4 20

Tier

Hybrid 2.0 Option Classes Appointment Cost

C*

Hybrid 2.0 Classes 121 – 345

.04

D*

Hybrid 2.0 Classes 346 – 570

.02

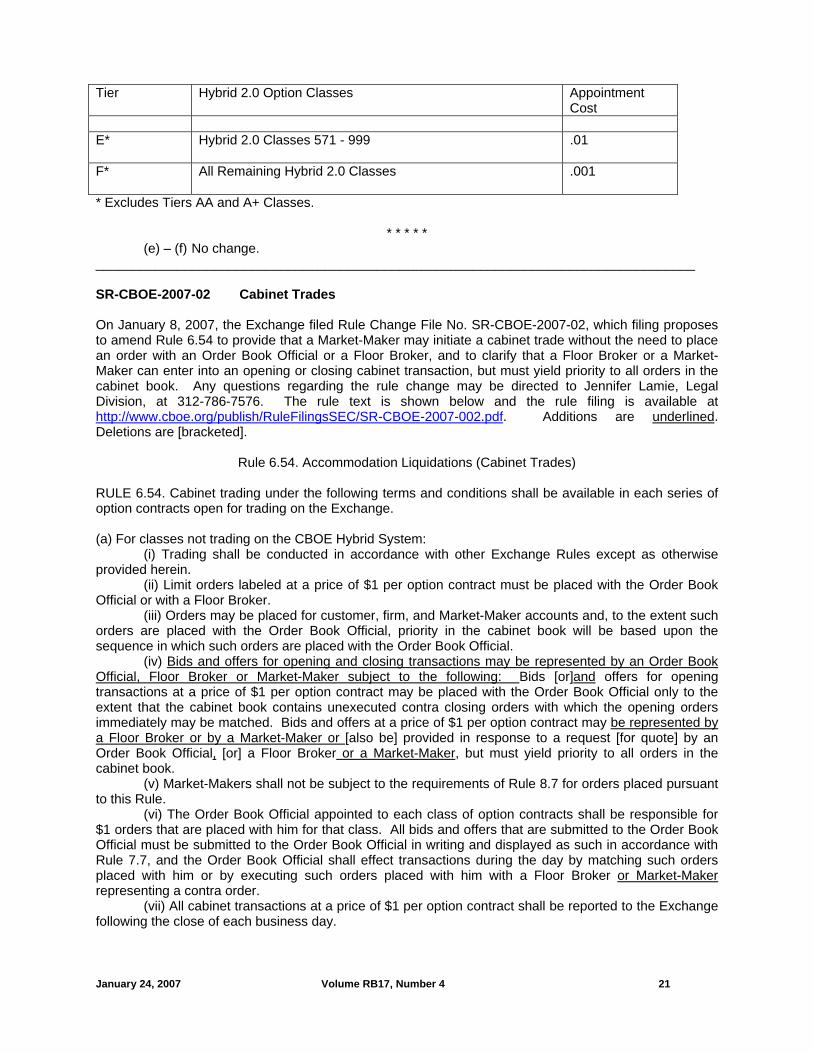

E*

Hybrid 2.0 Classes 571 - 999

.01

F*

All Remaining Hybrid 2.0 Classes .001

* Excludes Tier AA and A+ Classes. (ii) Hybrid Classes. Subject to paragraph (v) below, a Market-Maker can quote electronically in an appropriate number of Hybrid Classes that are located at one trading station. The appointment cost of each Hybrid Class is .01, except for [options on the iShares Russell 2000 Index Fund (IWM), which has an appointment cost of .50, and] options on the NASDAQ 100 Index (NDX), which has an appointment cost of 1.0.

(iii) - (viii) No change.

(d) No change. . . . Interpretations and Policies: .01 No change.

* * * * * Rule 8.4 – Remote Market-Makers

Rule 8.4. (a) No change.

(b) – (c) No change. (d) Appointment of RMMs: An RMM will have a Virtual Trading Crowd ("VTC") Appointment, which confers the right to quote electronically (and not in open outcry) an appropriate number of Hybrid 2.0 Classes selected from "tiers" that have been structured according to trading volume statistics. All Hybrid 2.0 Classes within a specific tier will be assigned an "appointment cost" depending upon its tier location. The following table sets forth the tiers and related appointment costs. Tier

Hybrid 2.0 Option Classes Appointment Cost

AA

Options on the CBOE Volatility Index (VIX) Options on the iShares Russell 2000 Index Fund (IWM)

.50

A+

Options on Standard & Poor's Depositary Receipts Options on the Nasdaq-100 Index Tracking Stock Options on the Russell 2000 Index (RUT)

.25

A*

Hybrid 2.0 Classes 1 – 60

.10

B*

Hybrid 2.0 Classes 61 – 120

.05

C*

Hybrid 2.0 Classes 121 – 345

.04

D* Hybrid 2.0 Classes 346 – 570 .02

January 24, 2007 Volume RB17, Number 4 21

Tier

Hybrid 2.0 Option Classes Appointment Cost

E*

Hybrid 2.0 Classes 571 - 999

.01

F*

All Remaining Hybrid 2.0 Classes .001

* Excludes Tiers AA and A+ Classes.

* * * * * (e) – (f) No change. _________________________________________________________________________________ SR-CBOE-2007-02 Cabinet Trades On January 8, 2007, the Exchange filed Rule Change File No. SR-CBOE-2007-02, which filing proposes to amend Rule 6.54 to provide that a Market-Maker may initiate a cabinet trade without the need to place an order with an Order Book Official or a Floor Broker, and to clarify that a Floor Broker or a Market-Maker can enter into an opening or closing cabinet transaction, but must yield priority to all orders in the cabinet book. Any questions regarding the rule change may be directed to Jennifer Lamie, Legal Division, at 312-786-7576. The rule text is shown below and the rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2007-002.pdf. Additions are underlined. Deletions are [bracketed].

Rule 6.54. Accommodation Liquidations (Cabinet Trades) RULE 6.54. Cabinet trading under the following terms and conditions shall be available in each series of option contracts open for trading on the Exchange. (a) For classes not trading on the CBOE Hybrid System:

(i) Trading shall be conducted in accordance with other Exchange Rules except as otherwise provided herein.

(ii) Limit orders labeled at a price of $1 per option contract must be placed with the Order Book Official or with a Floor Broker.

(iii) Orders may be placed for customer, firm, and Market-Maker accounts and, to the extent such orders are placed with the Order Book Official, priority in the cabinet book will be based upon the sequence in which such orders are placed with the Order Book Official.

(iv) Bids and offers for opening and closing transactions may be represented by an Order Book Official, Floor Broker or Market-Maker subject to the following: Bids [or]and offers for opening transactions at a price of $1 per option contract may be placed with the Order Book Official only to the extent that the cabinet book contains unexecuted contra closing orders with which the opening orders immediately may be matched. Bids and offers at a price of $1 per option contract may be represented by a Floor Broker or by a Market-Maker or [also be] provided in response to a request [for quote] by an Order Book Official, [or] a Floor Broker or a Market-Maker, but must yield priority to all orders in the cabinet book.

(v) Market-Makers shall not be subject to the requirements of Rule 8.7 for orders placed pursuant to this Rule.

(vi) The Order Book Official appointed to each class of option contracts shall be responsible for $1 orders that are placed with him for that class. All bids and offers that are submitted to the Order Book Official must be submitted to the Order Book Official in writing and displayed as such in accordance with Rule 7.7, and the Order Book Official shall effect transactions during the day by matching such orders placed with him or by executing such orders placed with him with a Floor Broker or Market-Maker representing a contra order.

(vii) All cabinet transactions at a price of $1 per option contract shall be reported to the Exchange following the close of each business day.

January 24, 2007 Volume RB17, Number 4 22

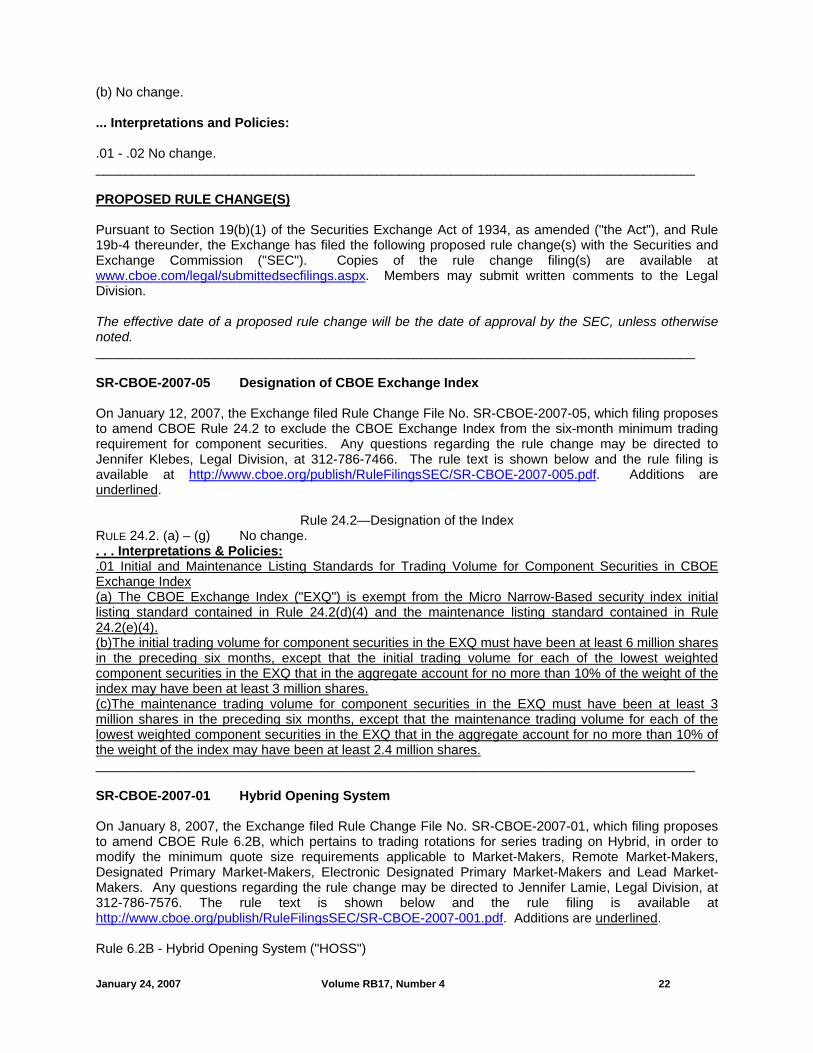

(b) No change. ... Interpretations and Policies: .01 - .02 No change. _________________________________________________________________________________ PROPOSED RULE CHANGE(S) Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934, as amended ("the Act"), and Rule 19b-4 thereunder, the Exchange has filed the following proposed rule change(s) with the Securities and Exchange Commission ("SEC"). Copies of the rule change filing(s) are available at www.cboe.com/legal/submittedsecfilings.aspx. Members may submit written comments to the Legal Division. The effective date of a proposed rule change will be the date of approval by the SEC, unless otherwise noted. _________________________________________________________________________________ SR-CBOE-2007-05 Designation of CBOE Exchange Index On January 12, 2007, the Exchange filed Rule Change File No. SR-CBOE-2007-05, which filing proposes to amend CBOE Rule 24.2 to exclude the CBOE Exchange Index from the six-month minimum trading requirement for component securities. Any questions regarding the rule change may be directed to Jennifer Klebes, Legal Division, at 312-786-7466. The rule text is shown below and the rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2007-005.pdf. Additions are underlined.

Rule 24.2—Designation of the Index RULE 24.2. (a) – (g) No change. . . . Interpretations & Policies: .01 Initial and Maintenance Listing Standards for Trading Volume for Component Securities in CBOE Exchange Index (a) The CBOE Exchange Index ("EXQ") is exempt from the Micro Narrow-Based security index initial listing standard contained in Rule 24.2(d)(4) and the maintenance listing standard contained in Rule 24.2(e)(4). (b)The initial trading volume for component securities in the EXQ must have been at least 6 million shares in the preceding six months, except that the initial trading volume for each of the lowest weighted component securities in the EXQ that in the aggregate account for no more than 10% of the weight of the index may have been at least 3 million shares. (c)The maintenance trading volume for component securities in the EXQ must have been at least 3 million shares in the preceding six months, except that the maintenance trading volume for each of the lowest weighted component securities in the EXQ that in the aggregate account for no more than 10% of the weight of the index may have been at least 2.4 million shares._________________________________________________________________________________ SR-CBOE-2007-01 Hybrid Opening System On January 8, 2007, the Exchange filed Rule Change File No. SR-CBOE-2007-01, which filing proposes to amend CBOE Rule 6.2B, which pertains to trading rotations for series trading on Hybrid, in order to modify the minimum quote size requirements applicable to Market-Makers, Remote Market-Makers, Designated Primary Market-Makers, Electronic Designated Primary Market-Makers and Lead Market-Makers. Any questions regarding the rule change may be directed to Jennifer Lamie, Legal Division, at 312-786-7576. The rule text is shown below and the rule filing is available at http://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2007-001.pdf. Additions are underlined. Rule 6.2B - Hybrid Opening System ("HOSS")

January 24, 2007 Volume RB17, Number 4 23

RULE 6.2B. (a) – (b) No change. (c) After the Rotation Notice is sent, the System will enter into a Rotation Period, during which the opening price will be established for each series.

(i) – (ii) No change.

(iii) Prior to the expiration of this period, the DPM or any appointed LMM and each e-DPM for the class must enter opening quotes that comply with the legal width quote requirements of Rule 8.7(b)(iv). The initial size of a DPM’s, LMM’s, e-DPM’s, Market-Maker or RMM’s opening quote must be for at least ten contracts in accordance with Rule 8.7; however, if the underlying primary market disseminates less than a 1000-share quote or trade on the opening, an opening quote for as low as one contract may be submitted.

(iv) No change. (d) – (i) No change. ______________________________________________________________________

Membership Department400 S. LaSalle StreetChicago, Illinois 60605(312) 786-7449 - Phone(312) 786-8140 - Faxwww.cboe.org

CBOE INDIVIDUAL MEMBER APPLICATION

1. Name: Social Security #:

2. E-mail Address: BD #: 8 -

3. Mailing Address:

City: State: Zip Code: Phone:

5. Capacity in which I seek to act on CBSX: q RMM q Proprietary Trader q Broker

6. The clearing firm issuing the guarantee for my activity on CBSX is: Name: NSCC #:

I hereby agree to abide by the Constitution and Rules of CBOE and of CBOE Stock Exchange, LLC, as they shall be in effect from time to time.

I agree that CBSX, in compliance with Regulation NMS, may route linkage orders to other markets on behalf of non-IOC orders sent to CBSX from me.

Signature of Applicant: Date:

January 2007

Membership Department400 S. LaSalle StreetChicago, Illinois 60605(312) 786-7449 - Phone(312) 786-8140 - Faxwww.cboe.org

CBOE MEMBER ORGANIZATION APPLICATION

1. Name: Tax ID #: -

2. E-mail Address: BD #: 8 - 3. Mailing Address:

City: State: Zip Code: Phone:

4. Designate at least one employee or agent (Responsible Person) as your administrator for the organization’s use of the CBOEdirect system (including its affiliated Individual members).

Name Phone E-mail Address

Name Phone E-mail Address

5. Capacity (ies) in which the organization seeks to act on CBSX: q RMM q Proprietary Trader q DPM q Clearing Firm q Broker q NMCB (CBOE application must be attached)

6. Identify the Clearing Firm issuing the guarantee for the organization’s activity on CBSX:

Name: NSCC #:

The organization hereby agrees on behalf of itself and its associated persons to abide by the Constitution and Rules of CBOE and of CBOE Stock Exchange, LLC, as they shall be in effect from time to time.

The organization agrees that CBSX, in compliance with Regulation NMS, may route linkage orders to other markets on behalf of non-IOC orders sent to CBSX from the organization.

Authorized Signatory’s Name Title

Signature of Authorized Signatory Date

January 2007