Excel as a potent forensic accounting tool

22

-

Upload

dhruv-seth -

Category

Data & Analytics

-

view

246 -

download

2

Transcript of Excel as a potent forensic accounting tool

Coverage of today’s presentation

•What is Forensic audit ?

•The need of forensic auditors

•How is it different from normal audit

•Traits of a good forensic auditor

•Why auditors need forensic angle in all cases

•Tools available in Excel

•Excel Limitations

Name Number of Cases Amount

PNB 123 2036,00,00,000.00

CBI 174 1736,00,00,000.00

SBI 474 1327,00,00,000.00

Syndicate 114 749,00,00,000.00

OBC 86 719,00,00,000.00

BOB --- 597,00,00,000.00

IDBI --- 507,00,00,000.00

UCO --- 424,00,00,000.00

United Bank --- 376,00,00,000.00

TOTAL 7542,00,00,000.00

Bank frauds – 9 months FY 2014-15

Need for forensic auditors

•As per Association of certified fraud examiner

•Each organization loses 5% of their REVENUE to fraud

•Asset Misappropriation is the biggest factor

•Fraud are generally NOT discovered for 18 months

•Higher the fraud perpetrator BIGGER the fraud

•53% frauds were by people working greater than 5 yrs

•58% organizations NEVER recovered anything

Need for learning the traits

Why frauds go unnoticed during stat audit -

•extremely intelligent

•Conversant with internal systems

•Technology savvy

•Aware of stale audit procedures

What is forensic audit

•The use of accounting skills;

•To investigate frauds / embezzlement and

•To analyze financial information

•For use in legal proceedings

Forensic vis-à-vis Statutory

Forensic StatutoryVery focused and micro approach Macro approach with wide coverage

Examines Reliability of documentation Relies on Documentary evidences

Not compulsory Regulatory compliance

Establishing existence of fraud Ensuring True and fair view

Determining the quantum of loss Verifying correct representations

Gathering evidences Evaluating Internal Controls

Traits of a forensic auditor

•Think out of the box

•Distrust the obvious

•Develop cognitive dissonance

•Test of absurdity

Test of absurdity

Think of events which may be possible but

not probable.

Microsoft Excel as a potent

forensic auditing tool

Why Excel

•Availability

•Compatibility

•Powerful features

•Considerable volumes of data

Tools available in excel

•Analyze round number transactions

•Duplicate detection

•Same, Same and different tests

•Above average payments to vendors

Tools available in excel

•Gap detection

•Automated sampling

•MATCH function

•Employee – Vendor match

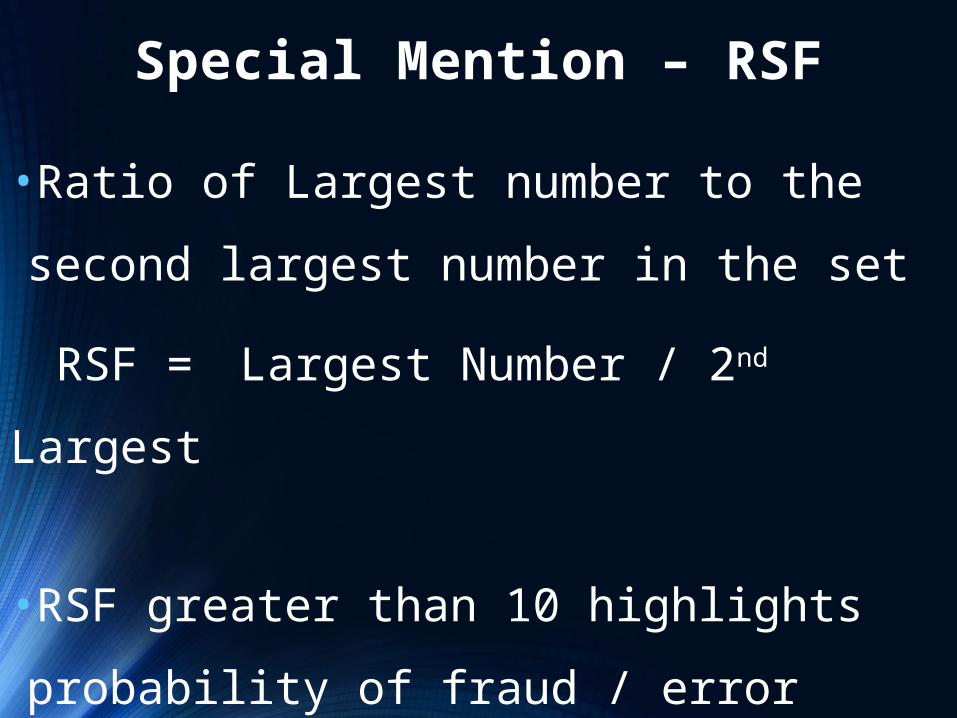

Special Mention – RSF

•Ratio of Largest number to the second

largest number in the set

RSF = Largest Number / 2nd Largest

•RSF greater than 10 highlights probability of

fraud / error

Special Mention – RSF

•Types of errors / frauds it can unearth

•Data Entry mistakes

•Fat Finger errors

•Wrong coding with masters

•Capital Asset written off in expense

•Excess payments in payroll

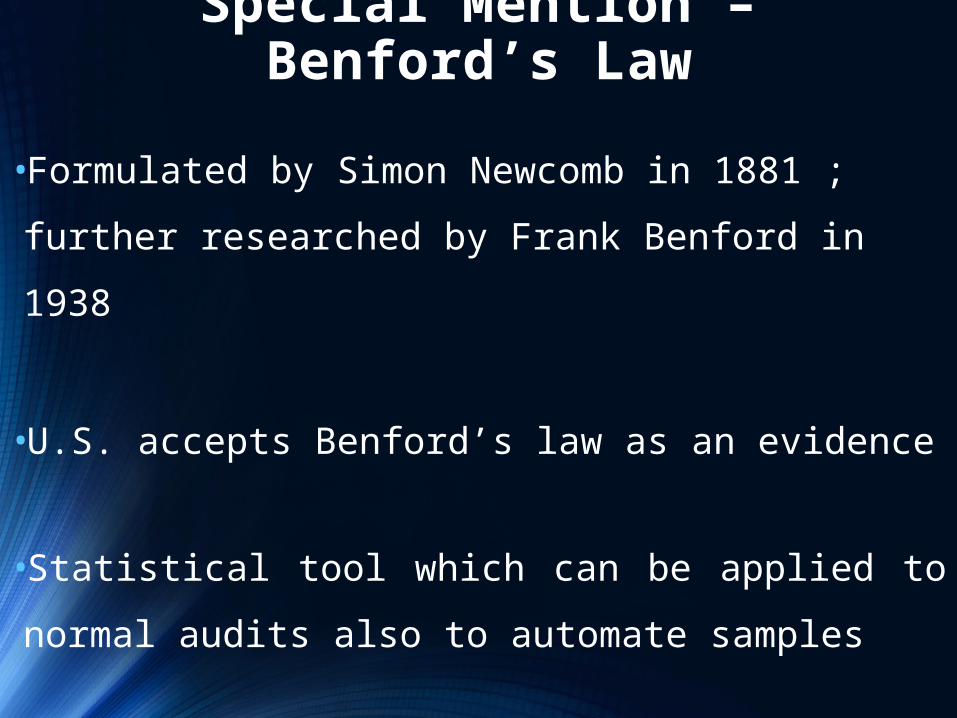

Special Mention – Benford’s Law

•Formulated by Simon Newcomb in 1881 ;

further researched by Frank Benford in 1938

•U.S. accepts Benford’s law as an evidence

•Statistical tool which can be applied to

normal audits also to automate samples

Special Mention – Benford’s Law

Special Mention – M-score

•Theory propounded by Prof. Beneish

•Stipulates the accuracy of financial statements based on certain ratios

•Ratios such as •Sales to receivables and Sales Growth Index•Gross margin Index•Asset Quality Index•Depreciation Index

Special Mention – M-score

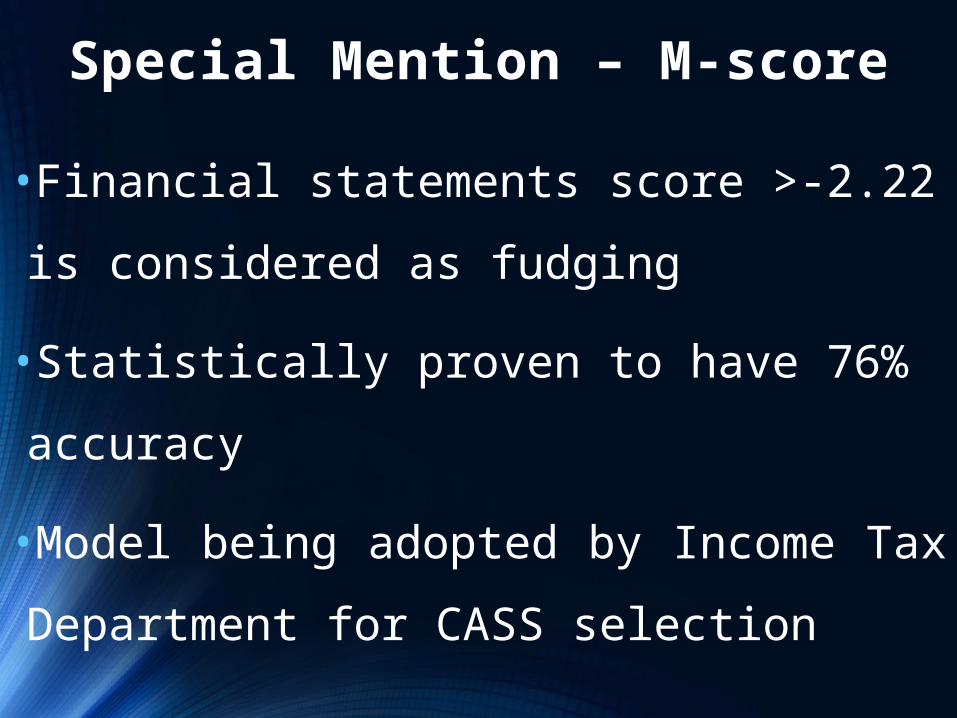

•Financial statements score >-2.22 is

considered as fudging

•Statistically proven to have 76% accuracy

•Model being adopted by Income Tax

Department for CASS selection

Excel Limitations

•Absence of Log

•Not admissible in court

•Involves slight complexity in applying

•Data size limitation / Instability

•Risk of Hidden data

There are no small frauds … They just didn't get sufficient time !

THANK YOU

CA. DHRUV [email protected]

![(5) C n & Excel Excel 7 v) Excel Excel 7 )Þ77 Excel Excel ... · (5) C n & Excel Excel 7 v) Excel Excel 7 )Þ77 Excel Excel Excel 3 97 l) 70 1900 r-kž 1937 (filllß)_] 136.8cm 136.8cm](https://static.fdocuments.in/doc/165x107/5f71a890b98d435cfa116d55/5-c-n-excel-excel-7-v-excel-excel-7-77-excel-excel-5-c-n-.jpg)