Ewa Siemion cala praca

142

Contents: Introduction...................................................3 Chapter 1: Introduction to the idea of the capital market......6 1.1. Introduction............................................6 1.2. The classification of financial markets.................6 1.3. The role of the capital market and the purpose which it serves......................................................12 1.4. The functions of the Capital Market....................15 1.5. Types of financial investment..........................19 1.5.1. Equities............................................20 1.5.2. Fixed-income securities.............................21 1.5.3. Derivatives.........................................22 1.5.4. Money and foreign exchange..........................23 1.6. The economy and the markets............................25 Chapter 2: The idea of index shares...........................27 2.1. .............................................Introduction 27 2.2. .............................................FTSE indices 28 Chapter 3: The changes of indices.............................38 3.1. .............................................Introduction 38 3.2. .................................................FTSE 100 38 3.2.1. January – December 2007.............................38 3.2.2. January – December 2008.............................39 3.2.3. January – December 2009.............................40 3.2.4. January 2007 – December 2009........................42 3.3. FTSE 250...............................................44 3.3.1. January – December 2007.............................44 3.3.2. January – December 2008.............................45

-

Upload

ewa-siemion -

Category

Documents

-

view

73 -

download

1

Transcript of Ewa Siemion cala praca

Contents:Introduction....................................................................................................................................3

Chapter 1: Introduction to the idea of the capital market...............................................................6

1.1. Introduction....................................................................................................................6

1.2. The classification of financial markets...........................................................................6

1.3. The role of the capital market and the purpose which it serves...................................12

1.4. The functions of the Capital Market............................................................................15

1.5. Types of financial investment......................................................................................19

1.5.1. Equities.................................................................................................................20

1.5.2. Fixed-income securities........................................................................................21

1.5.3. Derivatives...........................................................................................................22

1.5.4. Money and foreign exchange...............................................................................23

1.6. The economy and the markets......................................................................................25

Chapter 2: The idea of index shares.............................................................................................27

2.1. Introduction..................................................................................................................27

2.2. FTSE indices................................................................................................................28

Chapter 3: The changes of indices...............................................................................................38

3.1. Introduction..................................................................................................................38

3.2. FTSE 100......................................................................................................................38

3.2.1. January – December 2007....................................................................................38

3.2.2. January – December 2008....................................................................................39

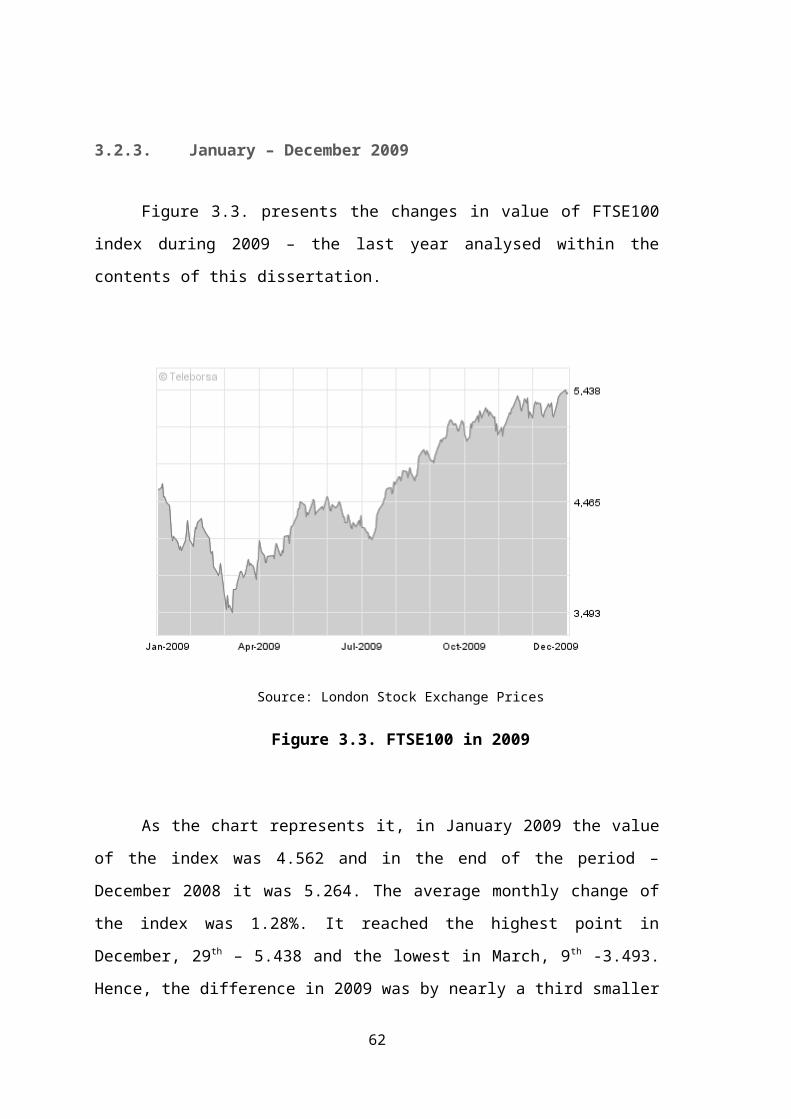

3.2.3. January – December 2009....................................................................................40

3.2.4. January 2007 – December 2009...........................................................................42

3.3. FTSE 250......................................................................................................................44

3.3.1. January – December 2007....................................................................................44

3.3.2. January – December 2008....................................................................................45

3.3.3. January – December 2009....................................................................................46

3.3.4. January 2007 – December 2009...........................................................................47

3.4. FTSE All-Share............................................................................................................49

3.4.1. January – December 2007....................................................................................49

3.4.2. January – December 2008....................................................................................50

3.4.3. January – December 2009....................................................................................52

3.4.4. January 2007 – December 2009...........................................................................53

3.5. Annual analysis............................................................................................................55

3.5.1. January – December 2007....................................................................................55

3.5.2. January – December 2008....................................................................................56

3.5.3. January – December 2009....................................................................................57

Chapter 4: The changes of indices and the economic indicators.................................................59

4.1. Introduction..................................................................................................................59

4.2. Gross Domestic Product...............................................................................................59

4.2.1. The idea of GDP and its changes in 2007-2009...................................................59

4.2.2. FTSE 100 and GDP..............................................................................................61

4.2.3. FTSE 250 and GDP..............................................................................................63

4.2.4. FTSE All-Share and GDP....................................................................................63

4.3. Pound Sterling Exchange Rate.....................................................................................65

4.3.1. GBP/EUR exchange rate and its changes in 2007-2009......................................65

4.3.2. GBP/EUR and FTSE 100.....................................................................................68

4.3.3. GBP/EUR and FTSE 250.....................................................................................69

4.3.4. GBP/EUR and FTSE All-Share...........................................................................70

4.4. Unemployment Rate.....................................................................................................71

4.4.1. The idea of unemployment rate and its changes in 2007-2009............................71

4.4.2. Unemployment rate and FTSE 100......................................................................75

4.4.3. Unemployment rate and FTSE 250......................................................................76

4.4.4. Unemployment rate and FTSE All-Share............................................................77

4.5. Interest Rate..................................................................................................................78

4.5.1. The idea of interest rate and its changes in 2007-2009........................................78

4.5.2. Interest rate and FTSE 100...................................................................................82

4.5.3. Interest rate and FTSE 250...................................................................................83

4.5.4. Interest rate and FTSE All-Share.........................................................................84

Summary......................................................................................................................................85

Bibliography.................................................................................................................................87

Literature..................................................................................................................................87

Press.........................................................................................................................................88

The Internet..............................................................................................................................88

Appendix 1: FTSE 100 constituents (December 2009):..............................................................89

Appendix 2: FTSE 250 constituents (December 2009):..............................................................90

Appendix 3: FTSE All-Share constituents (December 2009):.....................................................93

2

Introduction

The stock market is meant to be the reflection of the state of the economy in a

given country. By observing the situation in the market one should be able to judge

whether the economy is expanding, in recession or experiencing a boom. The decision

to explore the British stock market was based on my residency in the United Kingdom

as well as the phenomenon of Britain being one of the western countries that seemed to

have suffered most from the consequences of the American Credit Crunch.

FTSE indices have been chosen as a subject of the study, in view of the fact that

they stand for the biggest companies present on the British market. FTSE All-Share

covers 98% of total market capitalisation. FTSE 100 stands for the 100 most valuable

companies and FTSE 250, correspondingly, for 250. They also cover all the sectors of

the market from retail to steel industry, which gives a full picture.

Moreover, the reason for choosing the three-year period of time- 2007-2009 was

its attractiveness; after a rather steady 2007 one could observe a major change in 2008

and slow recovery of the economy beginning the end of 2009. This period enables a

researcher to show and analyse all stages of the business cycle: expansion, contraction,

recession and boom.

Furthermore, the aim of this thesis is to observe and describe how indices

changed in 2007-2009, to explore the similarities and differences in their behaviour as

well as check the rank of correlation between indices and four chosen economic

indicators: Gross Domestic Product, Great Britain Pound exchange rate, unemployment

rate and interest rate. In order to show how strong the relationship between the four

chosen variables is, Pearson’s correlation coefficient has been used.

What is more, in order to conduct the study, literary resources as well as

newspapers and the Internet have been used. To explore the very idea of financial

market, including capital market, one focused on work by Blake, Chamber, Clarke, Fell,

McInish, and Midgley. These authors describe the nature, significance, function as well

as the division of financial market which id the field of my research. In order to present

the division of FTSE indices and their role and significance, Vaitilingam’s [2001] work

has been reviewed and updated according to the information provided by the Financial

Times Stock Exchange website. Barry’s work, as well as another book by Vaitilingam

[2004], was very helpful to analyse the data and relate the indices to the chosen

economic indicators. What I also did find helpful in understanding the data was

Financial Times itself. It describes the economical issues on daily basis and is edited by

specialists, i.e. Bank of England governor, Mervyn King.

Worth mentioning is also a short description of what information is covered by

each of the four chapters. Chapter 1 describes the very idea of financial market,

including capital market. First, it focuses on the division of financial markets presented

briefly according to Blake’s [1990] classification. Moreover, it also explains the idea of

equilibrium and the phenomenon of bid-offer spread present in the market. Furthermore,

it focuses on the role of the capital market- explains who the participants are and how

the cost of capital can be influenced. Later, one can explore the functions of the capital

market, such as creating liquidity, allocating and rationing funds, pricing of shares, as

well as providing a barometer of a company’s success. Besides, types of financial

investment, like equities, fixed-income securities, derivatives and foreign exchange are

enumerated and briefly described. Finally, it presents the idea of how the economy of a

given country is related to the situation of the market; main economical crises are also

briefly described.

The second chapter focuses on the idea of index shares, especially FTSE indices,

presenting their division and significance to the British economy. After presenting the

FTSE UK Index Series family tree, it describes the following components briefly: FTSE

100, FTSE 250, FTSE 350, FTSE SmallCap, FTSE All-Share, FTSE Fledging, FTSE

All-Small as well as FTSE AIM. Moreover, it shows how the daily changed of indices

enumerated above are presented in Financial Times. Lastly, this chapter described the

way of classifying categories of businesses into certain sectors.

The next chapter shows the changes in value of the three chosen FTSE indices:

FTSE 100, FTSE 250 and FTSE All-Share. What is taken into consideration is the price

they had at the beginning and in the end of a given year, as well as their highest and

lowest values they reached over the analysed period. The rate of average monthly

change has also been measured for the whole period as well as for each year separately.

4

Next, the dynamics of change for each index is calculated and presented by separate

charts.

Finally, the last chapter discusses the correlation between indices and four major

economic indicators. First, it described the idea of GDP and how it changed in the

United Kingdom over the three years. It is also mentioned that the dynamics of its

changes can be used to identify the phase of business cycle that the economy is

currently in. The relationship between GDP and FTSE indices is also examined.

Similarly, GBP/EUR exchange rate and its change is also introduced and analysed. This

part of the chapter also explains how the value of currency is influenced by the state of

economy. The relationship between the exchange rate and chosen indices is also

measured. Moreover, the focus is moved onto unemployment rate which also says a lot

about the economy of a given country. It is explained why unemployment rises when

the market is facing problems as well as why it does not fall immediately after the

market starts recovering. The level of correlation between the number of people seeking

for work and the value of FTSE indices is also calculated. Finally, the chapter finishes

its analysis by concentrating on interest rate and its significance in reading the state of

the economy in the UK. It is explained how the government reacts to the situation in the

market by fulfilling its monetary policy.

5

Chapter 1: Introduction to the idea of the capital market

1.1. Introduction

The nature of this section is purely introductory to the topic of financial markets

yet essential for understanding how the capital market works and what its significance

is. This chapter presents the very idea of financial markets and the possible way of

classifying them as well as focuses on the role and functions of the capital market itself.

Later, the types of financial investment are also presented and briefly described. It also

introduces essential terms used in discussing the capital market.

1.2. The classification of financial markets

An organised financial market is a place where, or a system through which,

securities are created and transferred.

Financial markets can be classified in a number of ways. The division made by

Blake [1990, p. 16-35], which is crucial to understanding the functions and subjects of

financial market, is presented below:

- physical v. over-the-counter

- continuous v. call markets

- money v. capital markets

- primary v. secondary markets

- stock v. flow markets

A financial market does not have a physical location. Shares, bonds and money

market instruments are traded over-the-counter using a system of computer screens and

telephones together with the Internet. Only financial futures and financial options are

still traded in a physical market, the former, at LIFFE (the London International

Financial Futures Exchange) and the latter, at LTOM (the London Traded Options

Market), on the floor of the ISE (the International Stock Exchange).

Most markets operate on a continuous basis during opening hours, implying that

trading can take place at any time that the markets ape open. Examples here are the

markets for shares, bonds and money market instruments. However, as Blake [1990, p.

17] points out, some markets trade at specific times during opening hours. Such markets

are known as call markets because the securities are ‘called’ for trading. There has to be

sufficient time between calls to allow offers to buy and sell securities to accumulate and

so make trading worthwhile. Examples here are the pit trading of financial futures and

financial options.

Markets can also be classified according to their maturity of the securities traded

in them. A major distinction is usually drawn between money markets and capital

markets which are the subject of this dissertation. Money markets deal in securities

with less than one year to maturity, whereas capital markets deal in securities with

more than one year to maturity. Examples of money market instruments are Treasury

bills, commercial bills, commercial paper, bankers’ acceptances and negotiable

certificates of deposits. Examples of capital market instruments are bonds with more

than one year to maturity and shares.

An important distinction can also be drawn between primary and secondary

markets. Blake [1990, p. 19] reminds that the primary market is the new issues

market. When an investment bank brings a new company to flotation, its shares are

issued on the primary market (as an initial public offer). If this company subsequently

decides to gear up by issuing bonds, these are also floated on the primary market.

Similarly, if a company decides to expand using either equity finance or bond finance,

the additional shares or bonds are floated on the primary market (known as a secondary

public offer). As Chamber [2004, p.72] claims, the most difficult problem facing an

investment bank involved in a new issue is deciding on the offer price of the issue. If

the offer price is too low and there is an excess demand for the new shares or bonds,

then the issuing company will not be satisfied because it could have raised additional

revenue from the issue. But if the offer price is too high and there is insufficient demand

7

for the new shares of bonds, then the investment bank as underwriter will be involved in

often considerable losses. The important point about the primary market is that the

initial price of the security is set rather than determined by the market, unless the

security is issued through a tender offer or by auction.

The secondary market, according to Blake [1990, p. 21], is the market in which

existing securities are subsequently traded. There are two main reasons why individuals

transact in the secondary market: information-motivated reasons and liquidity-

motivated reasons. Information-motivated investors believe that they have superior

information about a particular security than other market participants. This information

leads them to believe that the security is not being correctly priced by the market. If the

information leads them to believe that the security is currently underpriced, and

investors with access to such information will want to buy the security. On the other

hand, if the information is incorrect, the security will be currently overpriced, and such

investors will want to sell their holdings of the security. Liquidity- motivated investors,

on the other hand, transact in the secondary market because they are currently in a

position of either excess or insufficient liquidity. Investors with surplus cash holdings

(e.g. as a result of an inheritance) will buy securities, whereas investors with insufficient

cash (e.g. to purchase a car) will sell securities.

The prices of securities in the secondary market are determined by the market-

makers in those securities. Precisely how those prices are determined can be seen once

we have discussed the final way in which securities markets can be classified, namely as

stock or flow markets. This classification leads us directly to the concept of

equilibrium. Once a security has been issued, it exists in the market-place until it

matures and is redeemed. Although a security can be sold, it can be sold only to

someone who is willing to buy it. Clearly, it is impossible for everyone to sell their

holdings of a particular security. Therefore there is a market for the entire stock of a

particular security, and there is also a market for the flow purchases and sales of that

security over time. These are shown in Fig. 1.1 the left-hand diagram, which shows the

stock market, indicates a fixed stock supply and a downward-sloping stock demand.

The lower the price of the security, the higher the stock demand. The right-hand

diagram shows the flow market per unit of time. If the time period is a day, for example,

the diagram indicates a downward-sloping daily demand curve and an upward-sloping

daily supply curve for the security. Equilibrium in the stock market is defined as the

8

situation in which the entire stock supply of the security is voluntarily held. This occurs

when the stock market price of the security is Pe. Equilibrium in the flow market is

defined as the situation in which the flow supply of the security on the market equals

the flow demand. This occurs when the flow market price of the security is Pe. Overall

equilibrium occurs when both the stock and flow markets are simultaneously in

equilibrium. This occurs when the stock and flow market equilibrium prices are

identical. Out of equilibrium, prices will adjust to clear both markers.

Source: Blake [1990, p. 23]

Figure 1.1. The stock and flow markets for a security

Figure 1.2 shows the equilibrium price, but this is never actually observed in the

market-place. What is observed are transaction prices, and these take into account the

bid-offer spread of the market-makers. The transaction price at which a market-maker

buys securities is the bid price and the transaction price at which he sells securities is

the offer price. The difference between the two is the bid-offer spread. If there is more

than one market-maker, then the difference between the highest bid price and the lowest

offer price is known as the market bid-offer spread or the touch. The equilibrium price

lies within the touch, as Fig. 1.2 shows for the flow market.

9

Source: Blake [1990, p. 25]

Figure 1.2. The bid-offer spread

What determines the bid-offer spread? This can be answered when one examines

the role of a market-maker. In an organised financial market, the role of a recognised

market-maker is to provide continuous and effective two-way prices (i.e. both bid and

offer prices) in all market conditions. In short, the market-maker has the responsibility

of keeping an orderly market. To do this effectively, he or she must hold an inventory of

securities to smooth out price fluctuations. The market-maker must be compensated for

holding these inventories, and the bid-offer spread is the way in which the market-

maker receives his compensation. The bid-offer spread will be determined to

compensate the market-maker for the cost of and risk to the capital that he or she has

tied up in the inventory of securities. The total compensation to the market-makers is

given by the shaded area in Fig 1.2, i.e. (PS –PB)Q.

The costs and risks of market-making depend on such characteristics of the

market as its breadth, depth and resilience. They also depend on the ratio of

information-motivated investors to liquidity-motivated investors.

A market for a particular security is said to have breadth if it has a substantial

volume of both buy and sell orders at the equilibrium price, i.e. if it has a good two-way

flow of orders. Markets with few buyers and sellers are called thin markets. A security

will be regarded as highly liquid if the market for than security has substantial breadth.

Market-makers in a broad market will operate with lower bid-offer spreads than those in

10

a thin market, because broad markets provide a bigger volume of business and are also

less risky.

Source: Blake [1990, p. 26]

Figure 1.3. A broad, deep market

A market for a security is said to have depth if it has a continuous flow of buy

and sell orders at prices above and below the equilibrium price. This means that both

the flow demand curve and the flow supply curve must be continuous at prices above

and below the equilibrium price. It also means that both the demand curve and the

supply curve must be highly elastic, (e.g. quite flat), at prices around the equilibrium

price. If these conditions hold, then only small changes in the price of the security will

be required to restore equilibrium should a sudden imbalance between buy and sell

orders arise. In short, price changes will be continuous in deep markets. In shallow

markets, on the other hand, the flow demand and supply curves are either discontinuous

or highly inelastic (steep). In such markets price changes will be both highly variable

and discontinuous (i.e. they will jump a great deal). Price changes will be smaller in

deep markets than in shallow markets. Therefore there is less risk of market-makers

incurring losses on their inventories as a result of sudden large adverse price movements

in deep markets compared with shallow markets. As a result, market-makers’ spreads

will be lower in deep markets than in shallow markets. A security will be regarded as

11

highly reversible if the market for that security has substantial depth. Figure 1.3 shows a

broad, deep market, while Fig. 1.4 shows a thin, shallow market.

Source: Blake [1990, p. 27]

Figure 1.4. A thin, shallow market

A market is said to be resilient if the flow of buy and sell orders does not dry up

whenever the price changes. If price changes do not reduce the flow of orders, then the

market-makers will not be faced with an inventory of unsaleable securities, and as a

result they will be willing to charge lower spreads.

Summarising, one can see that bid-offer spread will be lower the broader the

market, the deeper the market, and the more resilient the market.

1.3. The role of the capital market and the purpose which it serves

A market provides a focus on activities of buyers and sellers of a particular

commodity or service. In the course of the dealings the price or series of prices is

settled. The participants in the United Kingdom capital market include businessmen,

central and local government, financial intermediaries such as insurance companies and

12

pension funds, and private investors. According to Midgley [1977, p. 1], the capital

market has no confined location: it is in progress all over the land, wherever suppliers

and users of capital get together to do business. Much business is transacted over the

telephone or the Internet, so that there need be no geographical site at all for certain

activities. However, parts of the market are concentrated in certain well-known centres,

the most renowned of these being the Stock Exchange at 33 Throgmorton Street in

London which deals in company securities and those issued by governments and local

authorities.

The capital market deals in funds, but as securities, for example bonds or share

certificates, are given in exchange for funds, one can equally treat it as a market dealing

in securities. The market conforms to the laws of supply and demand in the ordinary

way. Thus in demand for funds increases and the supply remains constant the price of

funds raisers (that is, the price of securities rises).

Within the capital market one can speak of the price of funds in a general way.

Midgley [1977, p.1] compares capital market to fish market to illustrate the mechanism:

in the fish market one can speak of the price of fish. But of course nobody buys just

fish; one does not ask for a pound of fish, but rather a pound of haddock or cod.

Similarly, in the capital market the buyers of funds are in practice specific about their

requirements. They may wish to raise £1 million of risk capital, or £500,000 of capital

on long-term loan, or £200,000 on bank overdraft, and so on.

The price paid for access to funds may be in the form of a fixed payment per

annum (though it may be paid in instalments, for example, twice a year) or it may be in

the form of an agreement to share profits. An example of the former circumstance is

where interest is paid to providers of loan capital; and the latter circumstance is

exemplified where dividends are paid out to shareholders. However, as Midgley [1977,

p. 26] stresses, one must hasten to add that shareholders are not rewarded only by

dividend payments: if that were the case some companies would appear to be giving a

meagre return to risk capital. Part of the return to shareholders is in the form of retained

earnings is a factor taken into consideration by the market, and if it is regarded as

sufficiently attractive the share price will rise so as to reflect this expected future

growth.

13

Moreover, the factors which could influence the cost of capital funds, or, the

reciprocal, the price of securities, must be generally reviewed. As Briston [1995, p. 34]

presents it, perhaps one of the first influences which will come to mind is the extent of

funds available from public savings. Another fairly obvious influence is the level of

demand for funds arising from plans for new forms of industrial and commercial

investment. These will provide a starting point, but in practice there are many complex

factors which exert their influence on the market. On the supply side there is of course

the flow of funds stemming from the banking system. An easy credit policy which leads

to the criterion of new bank money will lead, ceteris paribus, to a reduction in the cost

of funds. Bank credit policy, however, will not be unrelated to governmental fiscal

policy; for example, a budget deficit financed by issue of short-term securities may

encourage expansion of bank credit and thus lower the cost of funds.

In its turn governmental fiscal policy will not be immune to the behaviour of the

balance of payments and capital movements in and out of the country. A serious run-

down of a country’s reserves of foreign currencies will almost certainly be countered by

fiscal stringency and credit restrictions leading to an increase in the cost of capital.

One of the most cogent influences on the cost of funds is the attitude to liquidity

on the part of investors, that is people, institutions, etc. who purchase securities, as a

whole. If investors decide that the return to funds which they provide is too low, or in

other words the price of securities is too high, there may be a sudden and overwhelming

desire to hold cash or near-cash for the time being. This may result in a fairly rapid

slump in security prices, or, the same thing, an increase in the return to funds, that is in

the cost of capital. Conversely, investors may decide that they are too liquid and that

returns to funds are too attractive to ignore. For example, Gilbert [1999, p. 75-76]

illustrates this situation by describing what happened 25 years before; it was known that

the institutional investors (insurance companies, pension funds, investment trusts and

unit trusts) were holding large liquid balances towards the end 1974. Once security

prices began to rise in January 1975, and investors began to appreciate that the return to

funds provided was falling, they flooded the market for securities with buying orders to

such a degree that the Financial Times Actuaries All Share Index rose by over 100 per

cent within a few weeks. Looking at this dramatic change from the point of view of the

return to funds, the earnings yield on industrial ordinary shares fell from over 30 per

cent to 20 per cent within a month. The flat yield on Consols (that is a general

14

indication of the return on long-term gilt-edged securities) also fell during this short

period, though by no means so spectacularly, from 16 per cent to less than 15 per cent.

In fact, as Midgley [1977, p. 13] states, different sectors of the market for

securities are subject to different influences. The return to funds in different sectors may

move more of less rapidly over time, as noted above. It is possible too that the returns in

one sector may be rising when the returns to other sectors are falling. Thus long-term

fixed interest rates may be rising when short-term rates are falling; or the earnings yield

on industrial shares generally may be falling when that on, say, engineering shares is

rising. Generally though, apart from occasional exceptional moves against the trend, the

returns in different broad sectors of the market move together in the same direction,

though not at the same pace.

1.4. The functions of the Capital Market

The fact that the capital market, or at least that part of it represented by the Stock

Exchange, is sometimes regarded as providing a service not unlike that of a casino does

not mean that it has no important, sober and useful functions. Like any other market, the

capital market provides a means whereby suppliers and buyers can exchange a

commodity at mutually satisfactory prices. Here lies perhaps the most obvious, and

certainly the most important, of the market’s functions, according to Midgley [1997,

p.14]: that of creating liquidity. Were it not for the market most of the longer-term

securities issued by companies would be far more permanent investments in the hands

of their holders. Without an organised market, the owner of a block of ordinary shares

in a particular company who wished to dispose of his holding would have to make a

personal search for a potential buyer. He may have to advertise and/pr employ an agent;

he may have to suffer the inconvenience of a considerable delay before finally finding a

buyer, and the price agreed upon would almost certainly be much less satisfactory than

that settled in an organised market where many buyers and sellers confront each other.

As Midgley stresses [1997, p.15], without the market- endowed quality of liquidity,

company shares and debentures would be far less attractive to investors, and companies

would have difficulty in raising all the funds they needed for expansion. It is of course

15

true that a comparatively small part of company funds are raised externally from

investors at present, but this part may nevertheless be of vital importance.

Consequently, the liquidity provided by the stock market (in particular) serves the very

useful purpose of ensuring that external investors are willing to make new funds

available to business as required.

Moreover, the market not only creates liquidity through its pricing mechanism, it

also allocates and rations funds, and it operates a system of incentives and

penalties. As Briston [1995, p. 74] suggests, the market prices funds for borrowers and

suppliers according to their different requirements. For large, efficient companies,

which can offer sound securities subject to the minimum or risk, the rate for borrowing

will be comparatively low. For smaller companies, which cannot give the same

assurance of safety, the rate will be higher. Furthermore, the shares of a successful

company with good growth prospects will be priced much higher in the market than

those of a similar-sized company with a poor record and uncertain growth prospects.

One effect of this is that potential growth companies in expanding industries tend to

have much lower earnings and dividend yields than companies, with uninspired

management in declining industries. In short, the ‘super-companies’, as Briston [1995,

p. 78] calls them, can raise funds by equity share issues with the minimum immediate

obligation in terms of cash outflow to the providers of capital; while the companies

which lack investor confidence will issue securities subject to the maximum obligation

in terms of annual cash returns to investors. The market is thus conferring a

considerable advantage on the more efficient companies.

The market pricing of shares has further repercussion on companies other than

its effect on the allocation of funds. Share-price movements operate so as to provide

both sticks and carrots for those who manage quoted companies. The mechanisms are

various. One fairly obvious form of discipline to management is that exercised by

shareholders who are dissatisfied with the trend in the share price. For some, usually

small quoted companies, the holdings of certain individual shareholders are sufficiently

large for them to take direct action, such as removing directors from the board. In the

case of lager companies, the holdings are often so widely spread that no individual, or

group of individuals, holds sufficient shares to exercise power, and the directors, in such

circumstances, although themselves holding only a small fraction of total voting shares,

can retain full control in the absence of any concerted opposition. This situation is not

16

all-pervasive among large companies. Sometimes ginger groups are set up to act on

behalf of the mass of individual shareholders. Moreover, in most large companies

institutional shareholders now hold between one-third and one-half of the equity shares

via their separate investment protection committees or their combined institutional

shareholders committee ma act as a disciplining force. However, as Midgley points out

[1997, p.16], it has to be said that in spite of some notable successes, such forms of

direct action tend to have been brought to bear too late to avoid the damage which they

sought to avert. This does not mean, incidentally, that shareholders must remain

powerless in terms of direct influence; rather, it may be argued that more effective and

permanent methods of representation must be forged.

Share price movements frequently provide incentives and penalties on a

personal basis for top managers of large companies. Many directors have large

shareholdings, and thus have a personal incentive to work to promote the efficiency of

the company and hence upgrade the value of their own stake. Nowadays, even if

managers have not the wealth to acquire a large holding of shares by direct personal

investment, they may profit from share-incentive or stock-option schemes. Such scheme

may vary in detail according to the circumstances operative at the time of their

introduction and are prone to the taxation policy of the government of the day.

Fundamentally, the idea is that chosen directors and executives, who can influence the

profitability of the company, are given the right to subscribe at some time in the future

to the shares of their company, but at the current day’s price. In this way they have a

strong incentive to work for increased profits, which, if sufficiently meritorious in

relation to results of other companies, will lead to a higher share price. Participants to

the scheme can then exercise their options and sell their shares, thus enjoying a capital

gain – the reward for their efforts. The scheme will be subject to various restrictions to

avoid undue dilution of capital. For example, participants may be prevented from

selling their shares within a stipulated period from allotment; there will be limitations to

the total amount of shares issued under a scheme, and also to the shares issued to any

individual; or a profit target may be built into the scheme, with the effect that

participants can only gain if the target is achieved and other shareholders get some

benefit from company growth.

As Briston presents it [1998, p.81], share-incentive schemes involved a

consideration of which managers should be entitled to benefit and to what extent.

17

Inevitably, the right will tend to be made available in relation to the degree of

importance in the management hierarchy. This may mean that a particular executive

who has made a substantial entrepreneurial contribution, but who is fairly low down in

the hierarchy, is not adequately compensated by a share-incentive scheme. However,

one means of compensation may be open to them, although it is a means which is

generally frowned upon, that is, profiting from dealing in shares on the basis of inside

knowledge. The arguments against this are fairly well known, although the practice, in a

variety of forms, is probably less uncommon than some London apologists would care

to admit. Broadly, insider trading is said to put outsiders at a disadvantage, to allow

insiders to profit at the expense of share-holders who are unaware of the inside

information, and to undermine confidence on the part of the investing public.

Nevertheless, the case for insider trading as a means of rewarding the modern

company entrepreneur has been cogently made. It has been argued that because insider

trading in company stocks does not suppress long-term trends, it does little harm to

long-term outside investors. As for short-term outside speculators, such losses as they

might make as a result of selling (or buying) before inside information becomes

generally known would probably have been made anyway. More importantly, it is

argued that the possibility of dealing in the company’s own shares provides incentives

for anyone who makes an entrepreneurial contribution: that it can reward company

entrepreneurs in a more precise manner than bonus or incentive schemes; that it rewards

regardless of status, and yet ensures that all investors gain as well as entrepreneurs.

Whether or not such arguments are given serious weight, they do at least illustrate

theoretically how company executives might be motivated to work harder and more

imaginatively for the company in response to the possibility of making gains from share

price movements stemming from their own efforts.

There are two more reasons for thinking that share price movements exert an

influence on company management. One is that the share price barometer provides a

rough and ready indicator of the success of company management. A share price which

is falling more than those of rival companies (or not rising as fast) may be thought to

cast a reflection on management efficiency, and managers are unlikely to be insensitive

to the view that share price movements have a bearing on their competence.

18

If some thick-skinned managers are immune to the aspersions or their efficiency

implicit in a falling share price, they may be more open to influence by a pressure more

germane to their pockets and power positions than to their public image. Again, the

pressure derives from share price movements, but here we refer to the view that the

depressed share price of a company which has had a poor profits record will make it

vulnerable to a takeover bid, and that the possibility of dismissal or reduced status and

prospects may act as a spur to management to do better. However, it must be said that

empirical evidence provides only meagre support for the proposition that a company

which is relatively cheap in terms of the relationship between its equity stock market

price and the book value of its equity assets is in practice much more vulnerable to a

takeover bid than a company which has a high valuation ratio of this sort. Even if the

spur provided by falling share prices, and the possibility of takeover depends more on

fear than fact for many companies, the stock market may still be exerting a useful

influence favouring company efficiency.

To sum up, the capital market supports the whole basis of business undertaken

by joint-stock limited companies. By providing a means of converting long-term

investments into liquid funds, it gives a foundation of confidence to the process of

saving an investment. The pricing process for securities not only leads to the allocation

of funds to those companies which can make best use of them, it also provides penalties

and inventiveness to managers, both directly and indirectly, and even threatens to

operate through the takeover mechanism to put the management of inefficient

companies into more competent hands.

1.5. Types of financial investment

In this section the types of financial investments are being presented according

to the division made by McInish [2000]. First the focus is directed onto equities, than

fixed-income securities, derivatives, money, and foreign exchange. All of those

instruments are briefly described.

19

1.5.1. Equities

Equities are securities representing capital contributed to the firm for which

there is no legal obligation to repay. Once they have fully paid the purchase price for

their shares, investors can lose only the amount of their investment and cannot be called

upon to put up additional funds. This limited liability is a major advance in modern

finance that has resulted in a significant increase in the ability of firms to raise capital.

As McInish [2000, p. 11] points out, the advantage of this system from the point of view

of investors can be seen in the case of the insurance firm Lloyds of London, which is

organised as a series of partnerships. Major losses due to the hurricanes and other

insured risks resulted in calls on the partners, called ‘names’, for millions of British

pounds in additional capital, resulting in the bankruptcy of many names. Many of the

names in the USA sought court protection from the requirement to contribute additional

capital.

Equities include all types of stock issued by the firm. Shares of common stock

represent ownership interests in a firm. The owners of stock are called ‘stockholders’ or

‘shareholders’. Common stock represents ownership of the residual claim on the

earnings and assets of the firm after the firm has paid its other commitments. The

shareholders are the owners of the firm. They run the firm through an elected board of

directors. Of course, the shareholders are not the only investors in the firm, as McInish

[2000, p. 14] stresses. Many firms borrow money, becoming debtors, and those lending

the money become creditors of the firm. But the creditors make their decisions on how

much to lend the firm and what rate of interest to charge with full knowledge that

operating decisions are in the hands of the board of directors and the firm’s officers and

managers.

Another equity security is preferred stock, which has a claim to earnings and,

typically, also assets that is superior to or ahead of that of the common stock, but that

comes after all other obligations of the firm. Many issues of preferred stock have a fixed

dividend payment that is specified in the form’s documents such as the corporate charter

or by-laws. This specified dividend payment does not generally represent a legally

enforceable claim against the firm, but firms are often required to give certain privileges

to preferred stockholders if the specified dividends are not met. As McInish [2000, p.

20

16] enumerates, these privileges may include the right to receive any back dividends

owed before the common stockholders can receive any dividends and the right to elect

some or all of the members of the board of directors. Because many preferred stock

issues have the right to receive fixed dividend payments and no more, preferred stock is

often regarded as being a fixed-income security.

A warrant is a security issued by a firm that gives the holder the right to acquire

stock in the issuing firm, or sometimes in another firm, at a stated price for a specified

period of time. Warrants are often issued in combination with other securities such as

common stock or bonds which will be discussed later in this chapter. Traditionally, as

McInish [2000, p. 17] mentions, warrants have been considered as equities, and the

funds raised from the sale of warrants are part of the firm’s capital.

A right is a short-term warrant that is distributed to the holders of a firm’s

common stock as a dividend. Each right entitles the owner to purchase an asset,

typically the common stock of the firm distributing the right, at a price that is less than

the current market price of the firm’s common stock. The goal is to have the

stockholders exercise the right so that the firm can increase its equity. Rights offerings

are a popular way of rising equity in many countries, including the United Kingdom,

which is the subject of my dissertation, and Japan. As McInish [2000, p. 21] points out,

they were also popular in the USA at one time, but their use has declined sustainability

in the end of 1990s.

1.5.2. Fixed-income securities

Fixed-income securities are securities that promise to make payments of

specified amounts to investors at specified dates. As it was mentioned before preferred

stock is often a fixed-income security. But most fixed-income securities are debt

instruments. A bond is a security which is evidence of debt issued by firms and

governmental bodies, including nations and their subdivisions and international

organizations such as the World Bank (the International Bank for Reconstruction and

Development), that requires that the issuer make one or more payments to the owner. A

money market instrument is a debt obligation with an initial maturity date of less than

21

one year. Capital market instruments have lives of one year and more. Money market

instruments are traded in the money market, in contrast to the market for bonds,

equities, and warrants, which are traded in the capital market.

1.5.3. Derivatives

A derivative, according to McInish [2000, p. 25] is a contract that specifies the

conditions under which each party transfers assets, including cash, to the other during

the life of the contract. While the derivative contract specifies how the amounts to be

transferred are to be determined, at least some of the amounts are intended to be

uncertain. The contract may involve cash payments or the transfer of real or financial

assets. The types of items that may be transferred or that may be the basis for

calculating cash payments are highly varied and include:

- commodities such as precious metals (silver, gold, platinum), agricultural

products (corn, soybeans, live cattle, pork bellies), and industrial commodities

(gasoline, heating oil, lumber);

- equities and equity indexes;

- currencies;

- debt instruments;

- other derivatives;

- price indexes or other type of pricing arrangements such as the movement over

time of the US Consumer Price Index, freight rates, or insurance claims.

This definition encompasses the six types of derivatives examined in this chapter:

options, futures, forwards, swaps, warrants, and rights. While warrants are considered

equities, they also have the characteristics of derivatives.

An option is a contract with a stated life in which one party acquires, in return for a

fee, the right to receive something if it is advantageous to do so. Some option contracts

provide for the payment of the cash value of the difference between an assets’s price

and a stated price. Other options allow the purchase of a real asset such as corn at s

22

predetermined price, the purchase of a financial asset such as common stock at a

predetermined price, the sale of a real asset at a predetermined price.

Futures are standardised contracts in which on party acquires the right to receive

and the other the obligation to deliver a specified amount and type of an asset at a

specified future date at a price stated in the contract. Some futures contracts call for one

party to pay the liquidating value of the contract to the other party rather than for the

delivery of an asset in exchange for cash. Non-standardised contracts similar to futures

contracts, except that the terms are individually negotiated on a bilateral basis, are

called forward contracts.

A swap is a contract evidenced by a single document in which two parties agree to

exchange one or more periodic payments based on the value of change in value of

something specified in the contract. The payments that are exchanged can be based on

any number of items, including interest rated and exchange rates. Depending on the

terms of the swap, one party’s payments can be fixed while the other’s fluctuate, or both

parties’ payments may fluctuate. The terms for many types of swaps have become

standard so that the market price can be determined from usual information vendors.

Warrants were defined previously. A warrant is equity because the funds received

from the sale of a warrant do not have a definite repayment obligation. But because the

value of which is uncertain, a warrant is also a derivative as defined here.

1.5.4. Money and foreign exchange

Money is anything used as a medium of exchange. In modern economies there

are three principal types of money: coins, currency and deposits which are liabilities of

financial institutions that are generally accepted as a medium of exchange and therefore

classified as money. The trading of money of one country for that of another is called

the foreign exchange market, and the money itself is foreign exchange.

23

Governments and firms issue equities and fixed-income securities at specific

times in large quantities to raise funds. The parties to the derivative contract create

derivatives (excluding warrants) as the need to transfer risk arises. Money is created by

governments through the minting of coins and the printing of paper currency and by the

banking system through the creation of deposits that can serve as a medium of

exchange.

The most basic goals of individuals, according to McInish [2000, p. 23], is to

maximise their utility – i.e. their satisfaction. The maximisation of utility translates into

the financial goal of maximising wealth. For a firm this means maximising the wealth of

the owners. Production is the way that wealth is created in the economy. Individuals can

directly consume the production for a given year, or they can divert some of the

production for use in producing other goods and services. This diversion of production

from immediate consumption to use in facilitating additional production is called saving

or direct investment.

Direct investment is the use of resources to produce other goods and services.

But not everyone who wishes to defer consumption wants to invest directly. Instead,

some prefer to give their funds to others to invest. Financial markets are institutional

arrangements designed to facilitate the transfer of resources from those who have more

to those who have less than they wish to consume.

Financial markets and instruments contribute to the enhancement of wealth.

They increase the use of capital in the economy, and they lower the cost of transferring

capital from those with a surplus to those with a shortage.

1.6. The economy and the markets

According to Vaitilingam [2000, p.248] the economy is one of the most

important drivers of the stock market. The central economic force of interest rates, plus

the assorted effects of exchange rates, inflation, public spending and taxation, will

eventually have a say in overall valuations, whatever the temporary investment craze.

At the same time, the stock market has a major impact on the economy, both as a

forward indicator and determinant of consumer sentiment, and as a vital mechanism in

24

the management of risk encouraging the innovation and entrepreneurship that drive

economic growth.

Shares and bonds provide the essential capital that enables companies to take the

risks inherent in business. From their origins in medieval Italy, through increasing size

and sophistication in 17th- and 18th- century Amsterdam, 19th- century London and 20th-

century New York, the stock markets in which these assets traded have meant that the

business risks of new projects can be shared – from building the rail, road and aviation

infrastructure of the 19th-and 20th-century economies to building the electronic

infrastructure of the 21st-century economy. Such risk-sharing has transformed the

potential for economic growth and, in the latter part of the last century, as more and

more people have got involved in the investment process, changed fundamentally our

understanding of the relationship between risk and return.

For most of financial market history, debt finance was dominant. Until as late as

the 1950s, shares were largely in the hands of wealthy individuals. Buying and owning

shares was considered far too risky by the less well off and even by the institutions that

now dominate the investment scene; instead, they held portfolios of high-grade, long-

term bonds. But this arrangement has been swept aside in the last few decades, as

investors of all kinds have sought better returns, companies have seen the hugely

increased financing opportunities of the equity markets, and economic growth has made

enormous improvements in living standards in the developed world.

Of course, there have been bad times in the past sixty years and the stock market

has been a good leading indicator of future economic gloom. For example, the of the

period 1950-73 – often described in literature as the ‘golden age’ of economic growth in

western Europe and the United States [Vitilingam, 2000, p.249] – was clearly foretold

in the disastrous crash of 1973-4, when markets fell by over 50 per cent. The bear

market of the early 1970s clearly reflected the ominous economic events of that

unfortunate decade: sky-rocketing oil prices, the breakdown of the Bretton Woods

agreements for managing international monetary affairs, and the emergence of

persistent inflationary forces.

Many feared that these collapsing share valuations would lead to economic

disaster, just as the Great Crash of 1929 was thought to have led to the Great Depression

of the 1930s. Certainly, as Chamber [2004, p.38] states, speculative manias or ‘bubbles’

25

that culminate in self-feeding panics and eventual crashes can have widespread and

undesirable consequences in the real economy. Clearly, too, a booming market boosts

consumer sentiment, encouraging spending, reducing saving and increasing debt, and

adding further fuel to a raging economy.

But economic policy itself has a major impact on the interaction between share

values and the economy. In the 1990s, for example, cheap and easily available money

sustained the market’s upward trend. And in both the United States and the United

Kingdom, the crashes of 1987 had marginal effects on economic performance since the

monetary policy authorities in both countries were quick to cut interest rates to increase

liquidity. Similarly, the US Federal Reserve’s rate-cutting response to the global crisis

of 1997-8 seemed to be successful in restoring the good times.

This situation didn’t last for much longer than a decade though. The increasing

rates and decreasing availability of loans in the United States in 2008, widely known as

the Credit Crunch, made economies of many countries collapse, especially the US itself

and Western, Central and Eastern Europe. Some, like Hayek [2009], would call it a

natural end of the prolonged boom and others, like Minford [2010], would name

western societies victims of easy-money policy. Minford also states that for the credit

crunch shock it was 20% of borrowers that were marginal and not able to get loans on

normal basis, which meant that they had to pay interest they could not afford. The

situation led to great panic spread by the media as well, many people lost their jobs,

especially in the City. Credit Crunch forced the British government to cut their

spending, more than ever in the social sector, and raise taxes. Anxiety, panic and

terrifying statistics dominated the period of over a year, starting in the middle of 2008.

26

Chapter 2: The idea of index shares

2.1. Introduction

To begin discussing indices one has to know what they are. According to

Vaitilingam [2001, p. XV] an index is a number used to represent the changes in a set of

values between a base year and the present. Index numbers blend many different

ingredients into a single index, and measure changes in it by changes in its parts. This

involves giving appropriate weighting to the components according to their importance

in what is being measured. A weighted average is usually calculated as an arithmetic

mean, either using the same weights throughout (a base-weighted index) or adjusting

the weights as the relative importance of different components changes (a current-

weighted index). Vaitilingam also adds that base-weighted indices may have the base

shifted periodically.

Moreover, Fell [2000, p.74] adds that as well as providing information on

individual share prices, financial information sources often also report on the movement

of the value of shares as a whole by recording and commenting on share indices. A

share index records the change in the aggregate value of a particular group of shares

from a base period. For instance, the Financial Times – Stock Exchange 100 index,

otherwise known as ‘Footsie’, was started in 1984 and records the total value of the

hundred largest UK firms by market capitalisation. The index started at a value of 1000

and stands at 5,996.45 at the time of writing (January 2010). What this means is that the

top hundred firms in the UK are worth 5,996.45 times more/less than they were in 1984.

Worth mentioning is the fact that the FTSE 100 is one of the most important

share indices the UK, though there are other broader indices too, notably FTSE All

Share index, which includes around 850 UK quoted companies. Indices of European

shares are also produced by the Financial Times in conjunction with the Stock

Exchange. The FTSE Eurotop 100 index records the value of the hundred most actively

traded shares in Europe, while the Eurotop 300 is more similar to the Footsie in being

based on the 300 largest European companies by market capitalisation. Other important

indices from around the world are the Dow-Jones 30 share index and Standard and

Poor’s 500 index, which are based on American shares, and the Nikkei 225 index,

which reports movement in the Japanese market.

2.2. FTSE indices

Most widely based indices have been developed by the Financial Times, the

Stock Exchange and the Institute and Faculty of Actuaries. As of November 1995, these

have been managed by a joint company, FTSE International. These indices are

arithmetically weighted by the market capitalisation rather than being based on crude

price movements. In other words, the larger a company, the bigger the effect its price

movements will have on the index.

Source: FTSE 100 Index Factsheet

Figure 2.1 FTSE UK Index Series family tree

As Vaitilingam [2001, p. 93] states, the FTSE Actuaries share indices, and notably

the All-Share index, are the professional investor’s yardstick for the whole UK equity

28

market, for use in analysing investment strategies and as a measure of portfolio

performance. There are 39 component indices in the All-Share index relating to

different industrial sectors of the market, and nine component indices relating to

different levels of capitalisation (including the well-known Footsie). Beyond the All-

Share are the new fledgling indices, incorporating companies with a market

capitalisation below £35 million. Figure 2.1 represents the whole FTSE UK Index

Series family tree.

Furthermore, it is important to know what each index represents. The indices are

presented below according to Vaitilingam [2001, p. 95-97] description and updated

according to the official FTSE International website <http://www.ftse.com/

Indices/UK_Indices/ index.jsp> [consulted on 05.01.2011]:

Source: London Stock Exchange Prices

Figure 2.2. FTSE UK 100 5-year performance

- FTSE 100: the Footsie index was started with a base of 1,000 in January 1984 to

fill a gap in the market. At that time, the FT 30 index was calculated only

hourly, and there was demand for a constantly updated – or real-time – index in

view of both the competition from overseas and the needs of the new traded

29

options and financial futures markets. For most purposes, the Footsie has

replaced the FT 30. The index, amended quarterly, includes the 100 largest UK

companies in terms of market capitalisation – the blue chips – and represents

over 81% per cent of total UK market capitalisation. Figure 2.2. represents it’s

performance over the last 5 years.

Source: London Stock Exchange Prices

Figure 2.3. FTSE UK 250 5-year performance

- FTSE 250: an index of the next 250 companies by the market capitalisation,

those directly beneath the FTSE 100. These are companies capitalised between

£350 million and £3 billion, in total around 15 per cent of overall market

capitalisation. It is calculated two ways, one that includes and one that excludes

investment companies. Figure 2.3. represents the performance of the index

during the last 5 years.

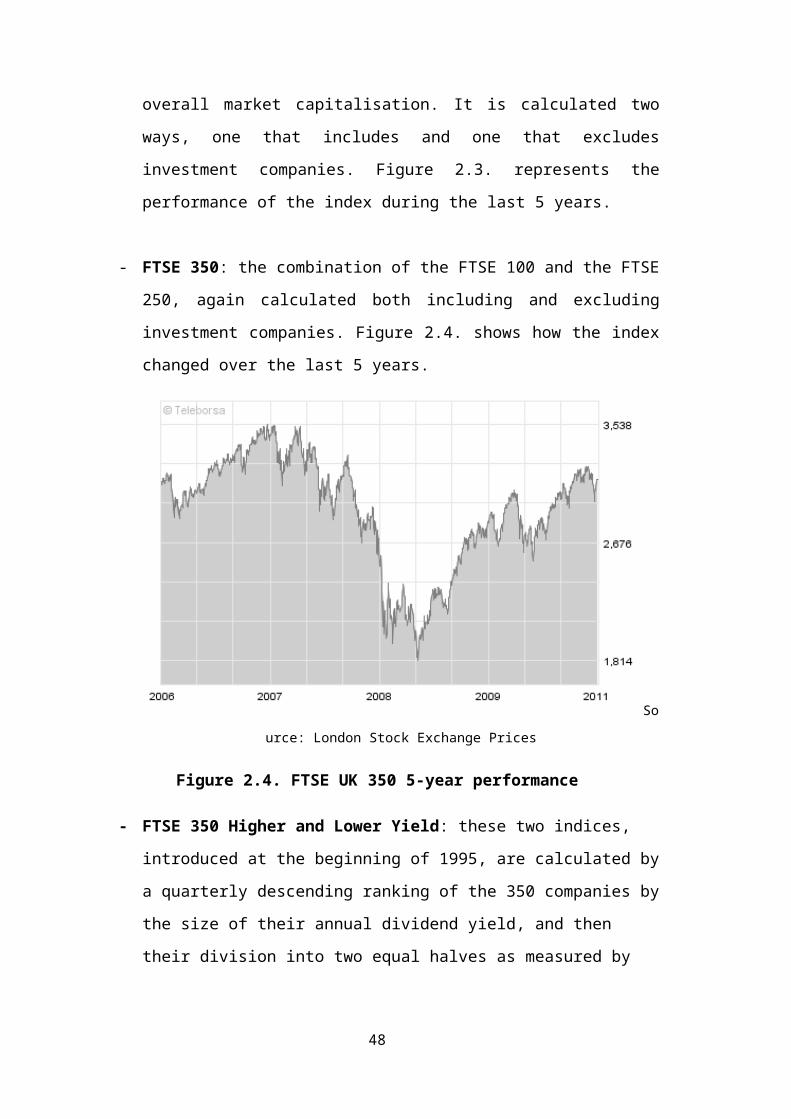

- FTSE 350: the combination of the FTSE 100 and the FTSE 250, again

calculated both including and excluding investment companies. Figure 2.4.

shows how the index changed over the last 5 years.

30

Source: London Stock Exchange Prices

Figure 2.4. FTSE UK 350 5-year performance

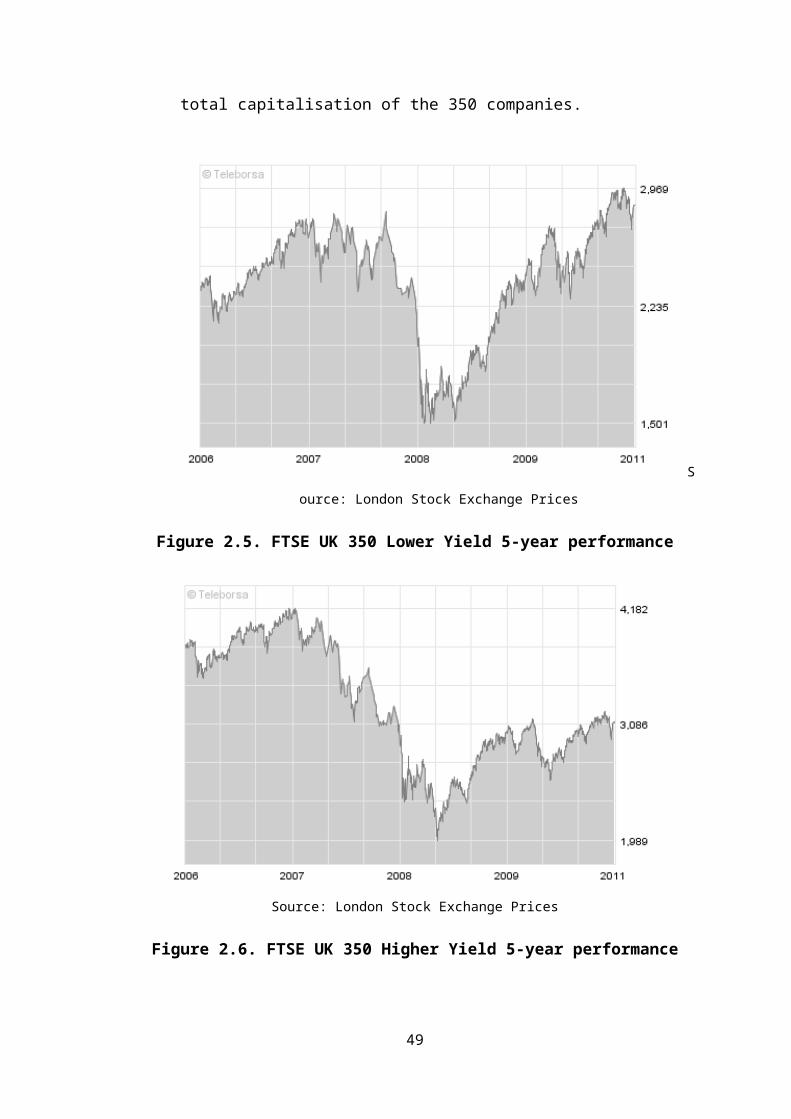

- FTSE 350 Higher and Lower Yield: these two indices, introduced at the

beginning of 1995, are calculated by a quarterly descending ranking of the 350

companies by the size of their annual dividend yield, and then their division into

two equal halves as measured by total capitalisation of the 350 companies.

Source: London Stock Exchange Prices

31

Figure 2.5. FTSE UK 350 Lower Yield 5-year performance

Source: London Stock Exchange Prices

Figure 2.6. FTSE UK 350 Higher Yield 5-year performance

- FTSE SmallCap: the 450-plus companies capitalised at up to £350 million,

which when added to the 350 make up the All-Share index. Like 250 and 350,

this index is calculated two ways.

Source: London Stock Exchange Prices

32

Figure 2.7. FTSE UK SmallCap 5-year performance

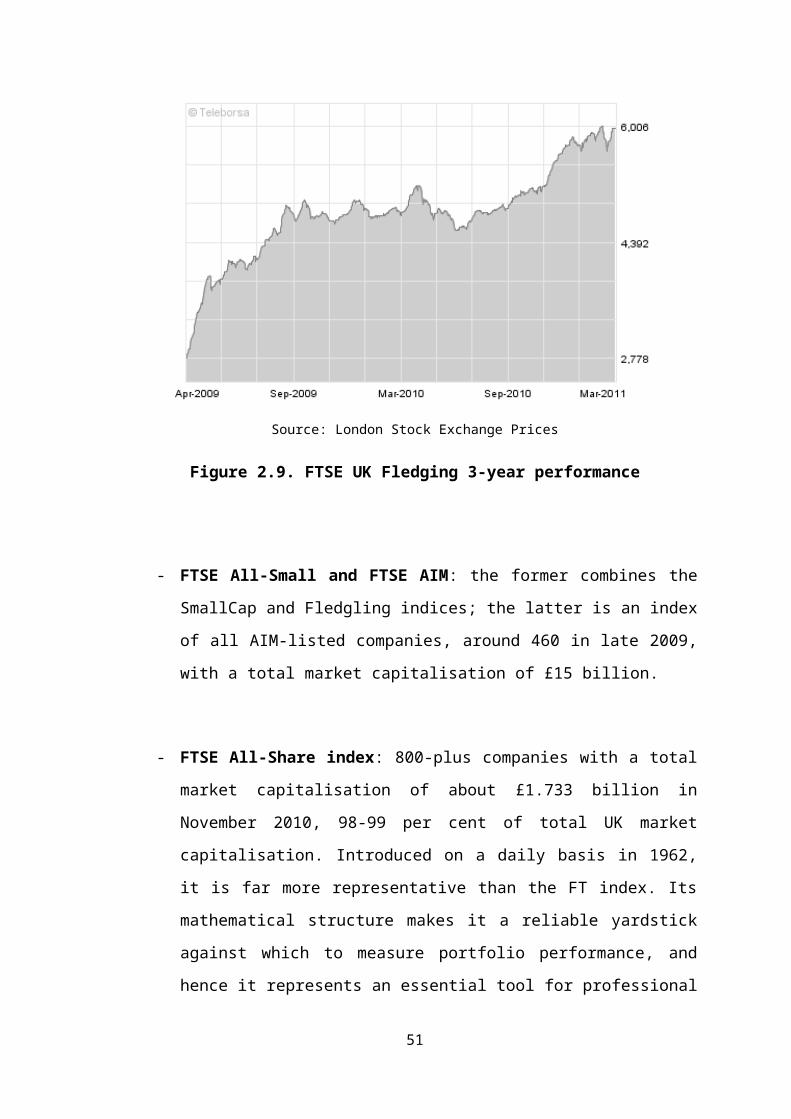

- FTSE Fledgling: another index launched at the beginning of 1995, this was

introduced to indicate the Stock Exchange’s concern for smaller companies. It

includes the over 700 companies that fail to qualify for the All-Share index

(including shares quoted on the AIM), representing 1-2 per cent of total market

capitalisation. It is calculated two ways as well. The figure below represents

how the index changed over the last 5 years.

Source: London Stock Exchange Prices

Figure 2.9. FTSE UK Fledging 3-year performance

- FTSE All-Small and FTSE AIM: the former combines the SmallCap and

Fledgling indices; the latter is an index of all AIM-listed companies, around 460

in late 2009, with a total market capitalisation of £15 billion.

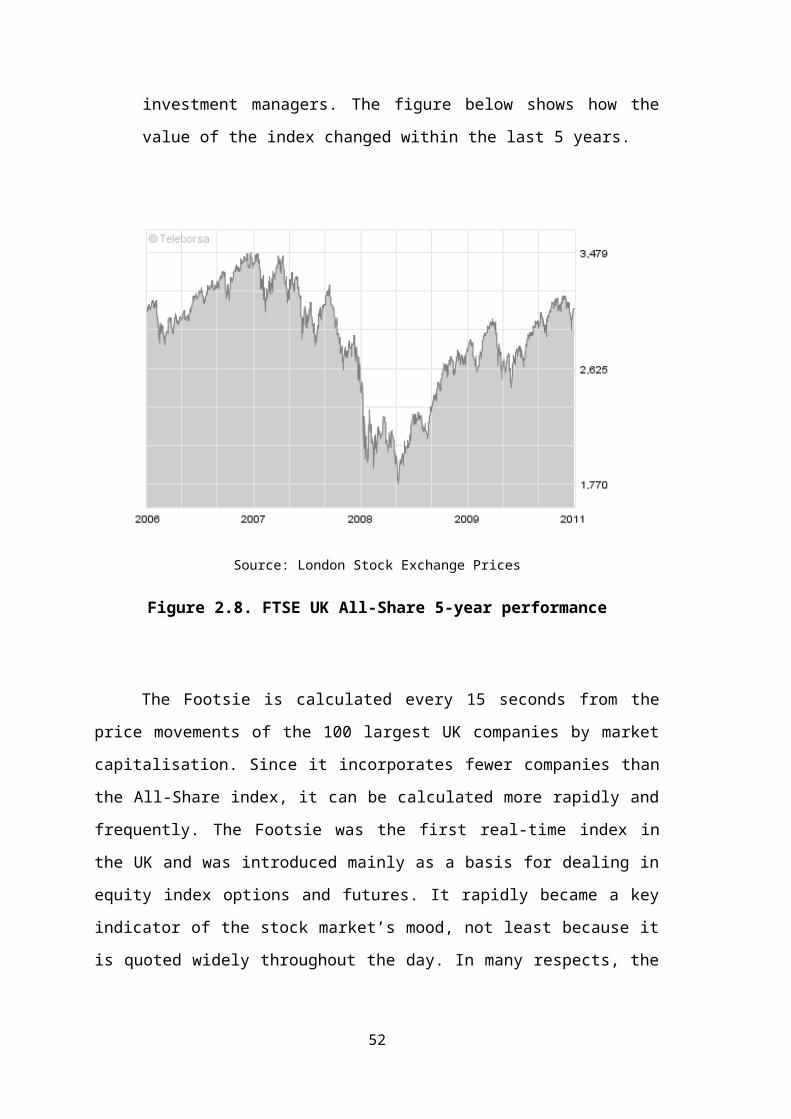

- FTSE All-Share index: 800-plus companies with a total market capitalisation

of about £1.733 billion in November 2010, 98-99 per cent of total UK market

capitalisation. Introduced on a daily basis in 1962, it is far more representative

than the FT index. Its mathematical structure makes it a reliable yardstick

33

against which to measure portfolio performance, and hence it represents an

essential tool for professional investment managers. The figure below shows

how the value of the index changed within the last 5 years.

Source: London Stock Exchange Prices

Figure 2.8. FTSE UK All-Share 5-year performance

The Footsie is calculated every 15 seconds from the price movements of the 100

largest UK companies by market capitalisation. Since it incorporates fewer companies

than the All-Share index, it can be calculated more rapidly and frequently. The Footsie

was the first real-time index in the UK and was introduced mainly as a basis for dealing

in equity index options and futures. It rapidly became a key indicator of the stock

market’s mood, not least because it is quoted widely throughout the day. In many

respects, the market thinks in terms of Footsie figures with particular points being seen

as psychological watersheds.

The FTSE 100 constituents are mostly multinationals and companies with strong

overseas interests, while the FTSE 250 are mainly strongly UK orientated companies.

As a result, the former are likely to be more influenced by overseas factors such as

34

exchange rate movements, while the latter may be influenced more by domestic factors

such as interest rate movements. Membership of both indices is reviewed every quarter

as market caps rise and fall. For the FTSE 100, any share that is 90th or higher

automatically joins the index; 111th or lower means automatic relegation.

The FTSE All-Share accurately reflects the whole market, as Vaitilingam [2001,

p. 98] states. With over 800 constituents, it has a very broad coverage, encompassing 98

per cent of the market’s aggregate capitalisation, with each company weighted

according to its market value so that a move in the price of a large company has more

effect than that of a small one. It can be used as a measure of the market’s performance

over long periods. It serves as a reliable yardstick against which to assess portfolio

performance. As a weighted arithmetic index it is designed to behave as an actual

portfolio would behave.

The breakdown into industry groups allows investors to track the performance of

particular sectors. This is of great assistance to specialist sector analysts, as well as

allowing more general investors to improve their understanding of the structure of the

market as a whole. Industrial classification is highly important since it is normally

accepted by the stock market and institutional research departments as the basis for the

analysis of companies. Correctly classifying all companies traded on the London market

is the responsibility of the FTSE Actuaries Industry Classification Committee, made up

of market practitioners, investment managers and actuaries. Figure 2.2 is an example of

how FTSE is presented daily in Financial Times.

Over time, as the structure of the UK industry has shifted, it has been necessary

to amalgamate sectors and create new ones. For example, Radio and TV, Teas and

Diamonds have gone, while Health, Media, Photography, and Electricity have been

formed. When a new group is created, its initial value is set at the level of its immediate

predecessor. In 1999, FTSE International introduced the Global Industry Classification

System, allowing comparison across national boundaries as well as across sectors and

sub-sectors. There are three levels of classification:

- Economic group, for example resources

- Industry sector, for example oil and gas

- Industry sub-sector, for example oil services or oil integrated

35

Source: Financial Times, January 26, 2011

Figure 2.9. An example of FTSE Indices presented daily in Financial Times

36

At the moment FTSE International is using Industry Classification Benchmark

(ICB) that comprises of four categories:

- Industry: basic materials

- Supersector: basic resources

- Sector: industrial materials

- Subsector: steel

Institutional investors attempt to beat the index most relevant to their portfolio.

Increasingly, investors want a set of indices that covers the entire equity capital

structure of the UK market so that they can accurately assess the performance of large,

medium and small companies within the framework of the whole market. There has also

been a growing interest in the performance of medium-sized companies since the

beginning of current century. The newer indices increase the visibility of many medium

and small companies.

The FTSE 350 provides a real-time measure covering around 90 per cent of the

UK equity market by value. The SmallCap and Fledgling indices are higher risk but

likely to boom in a recovery. They are good for the visibility and marketability of

smaller companies. Beyond the markets covered by the All-Share and Fledgling indices

is Ofex, an unregulated off-exchange dealing facility for companies not eligible for the

AIM or the index. It is offered by the broker JP Jenkins Ltd, with daily share

information published in the Financial Times.

The differentiation between Higher Yield and Lower Yield companies in the FT

350 is an interesting reflection of the decreasing importance of dividends as part of the

rewards to investors. Indeed, many of the market’s hottest stocks pay no dividends at

all, as Stowell, D.P. [2010, p.77] points out. Companies normally have relatively high

yields because investors expect their share prices to perform relatively badly. There are

three main types of high yielding stocks:

- Stodgy companies like utilities that chug along but are unlikely to produce

fireworks

- Companies in decline that are overdistributing their earnings

- Recovery shares that may or may not make it back.

37

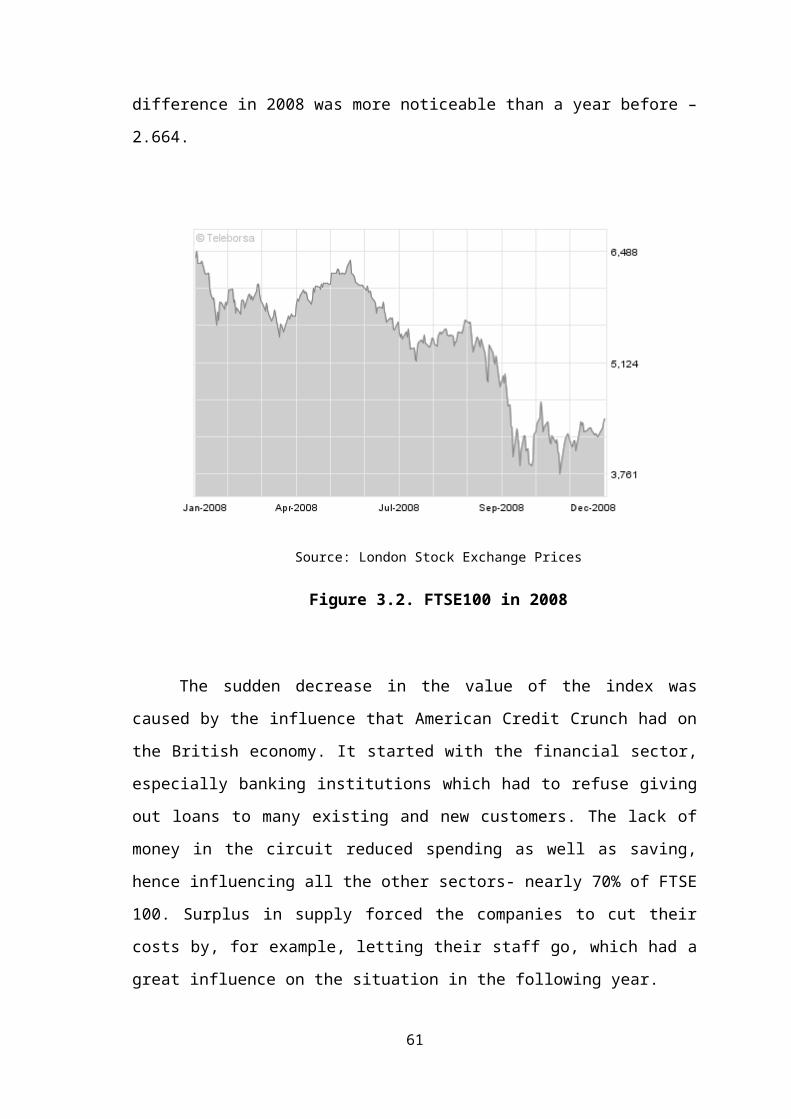

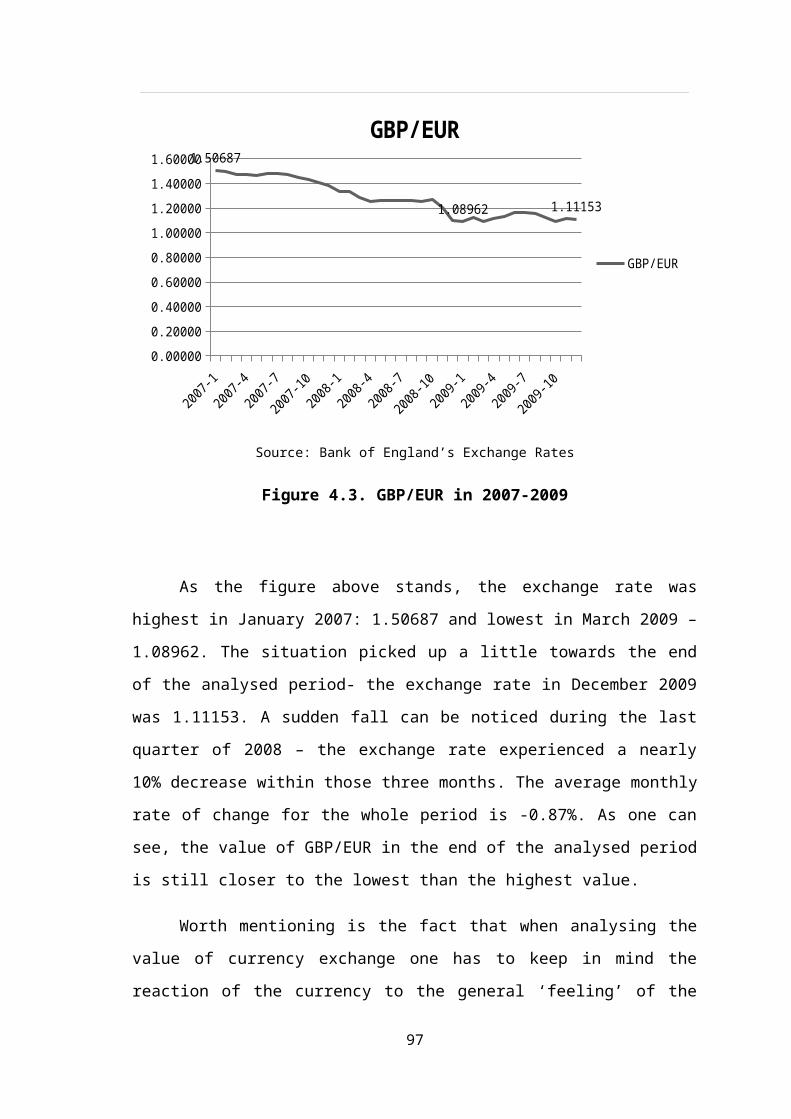

Chapter 3: The changes of indices

3.1. Introduction

This section focuses on the changes in value of analysed indices: FTSE 100,

FTSE 250 and FTSE All-Share. The changes are explored annually as well as for the

whole period of three years which this thesis covers. The choice of indices is

determined by their importance and significance to the UK market. They represent the

state of British economy as they stand for all the industries present at London Stock