eveloping a risk appetite for Dutch pension funds · PDF file05.05.2013 ·...

21

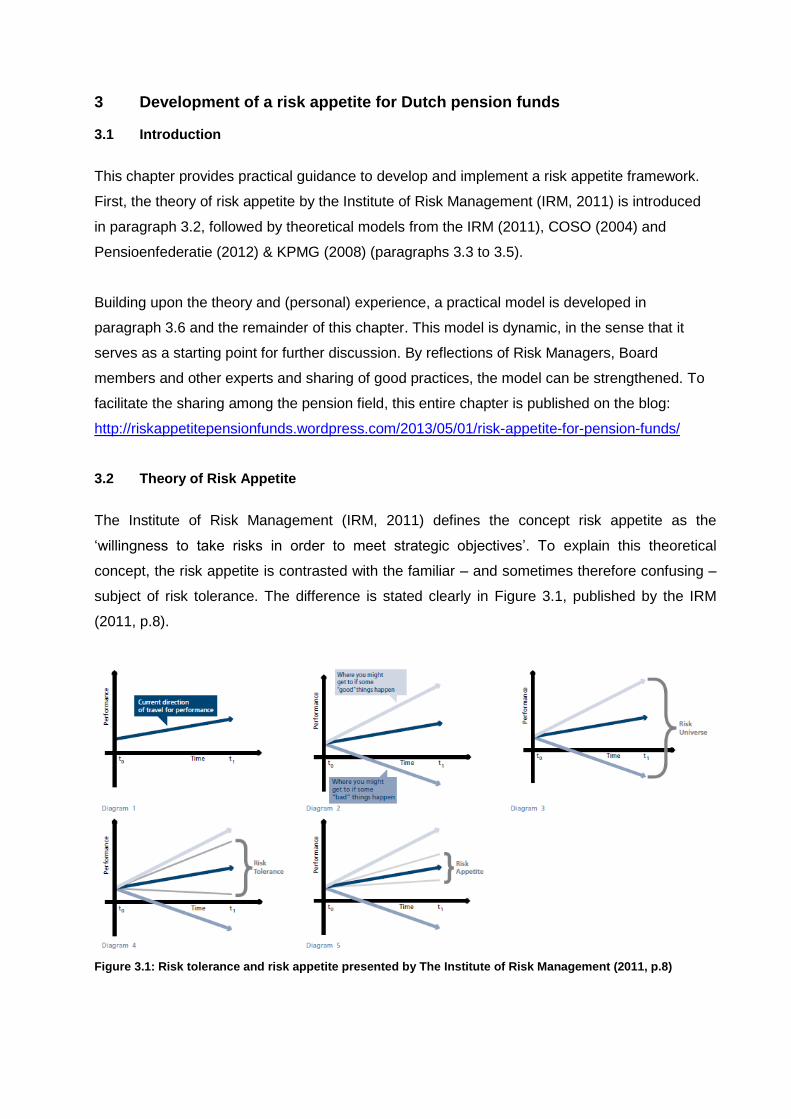

3 Development of a risk appetite for Dutch pension funds 3.1 Introduction This chapter provides practical guidance to develop and implement a risk appetite framework. First, the theory of risk appetite by the Institute of Risk Management (IRM, 2011) is introduced in paragraph 3.2, followed by theoretical models from the IRM (2011), COSO (2004) and Pensioenfederatie (2012) & KPMG (2008) (paragraphs 3.3 to 3.5). Building upon the theory and (personal) experience, a practical model is developed in paragraph 3.6 and the remainder of this chapter. This model is dynamic, in the sense that it serves as a starting point for further discussion. By reflections of Risk Managers, Board members and other experts and sharing of good practices, the model can be strengthened. To facilitate the sharing among the pension field, this entire chapter is published on the blog: http://riskappetitepensionfunds.wordpress.com/2013/05/01/risk-appetite-for-pension-funds/ 3.2 Theory of Risk Appetite The Institute of Risk Management (IRM, 2011) defines the concept risk appetite as the „willingness to take risks in order to meet strategic objectives‟. To explain this theoretical concept, the risk appetite is contrasted with the familiar – and sometimes therefore confusing – subject of risk tolerance. The difference is stated clearly in Figure 3.1, published by the IRM (2011, p.8). Figure 3.1: Risk tolerance and risk appetite presented by The Institute of Risk Management (2011, p.8)

Transcript of eveloping a risk appetite for Dutch pension funds · PDF file05.05.2013 ·...

3 Development of a risk appetite for Dutch pension funds

3.1 Introduction

This chapter provides practical guidance to develop and implement a risk appetite framework.

First, the theory of risk appetite by the Institute of Risk Management (IRM, 2011) is introduced

in paragraph 3.2, followed by theoretical models from the IRM (2011), COSO (2004) and

Pensioenfederatie (2012) & KPMG (2008) (paragraphs 3.3 to 3.5).

Building upon the theory and (personal) experience, a practical model is developed in

paragraph 3.6 and the remainder of this chapter. This model is dynamic, in the sense that it

serves as a starting point for further discussion. By reflections of Risk Managers, Board

members and other experts and sharing of good practices, the model can be strengthened. To

facilitate the sharing among the pension field, this entire chapter is published on the blog:

http://riskappetitepensionfunds.wordpress.com/2013/05/01/risk-appetite-for-pension-funds/

3.2 Theory of Risk Appetite

The Institute of Risk Management (IRM, 2011) defines the concept risk appetite as the

„willingness to take risks in order to meet strategic objectives‟. To explain this theoretical

concept, the risk appetite is contrasted with the familiar – and sometimes therefore confusing –

subject of risk tolerance. The difference is stated clearly in Figure 3.1, published by the IRM

(2011, p.8).

Figure 3.1: Risk tolerance and risk appetite presented by The Institute of Risk Management (2011, p.8)

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 2

To explain the picture, the IRM states that the expected performance of a company is shown in

Diagram 1. In the case of a pension fund, one might think of the performance of the funding

ratio. Since the performance of a portfolio is uncertain or so to say stochastic, the expected

future outcomes show variability (Diagram 2). The fan of all possible good and bad future

outcomes is shown in Diagram 3, and is called the risk universe (IRM, 2011, p.8). It is assumed

that the risk tolerance of an organization lies within the risk universe. The risk tolerance is

described by the IRM as „the lines in the sand beyond which the organisation will not move

without prior board approval‟ (Diagram 4, IRM, 2011, p.14). In terms of a pension fund, the risk

tolerance can e.g. indicate the maximum loss the fund is willing to take with respect to a certain

asset clas, or the portfolio as a whole. Where risk tolerance is seen as the line a pension fund

must not cross, the risk appetite is seen as the risk the pension funds actually strives for, or

actively decides to get exposed to in order to meet its return proposition. Typically it is assumed

that the risk appetite is smaller than the risk tolerance (Diagram 5, IRM, 2011, p.14). This last

point is in my opinion open for debate. In the recent financial crisis we have seen that Dutch

pension funds crossed the barriers of their risk tolerance. This might have been the result of a

risk appetite which is bigger than the risk tolerance and/or this might have been the

consequence of not explicitly knowing and defining the risk appetite in the first place.

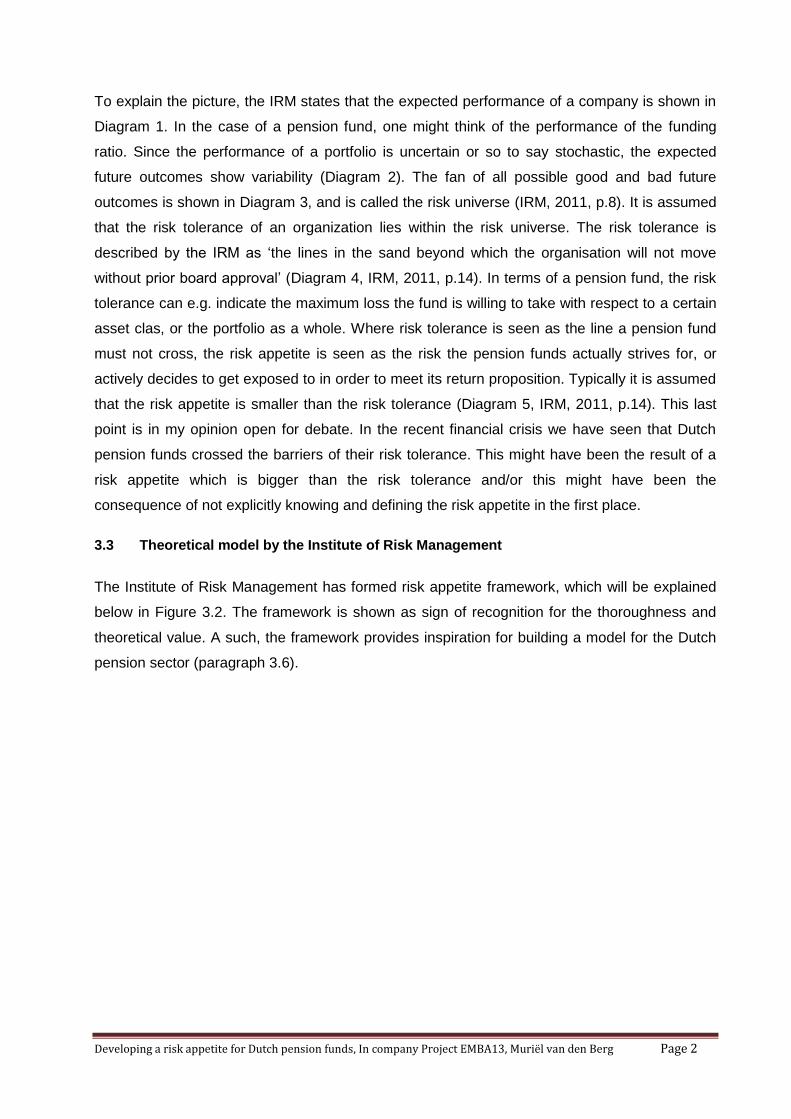

3.3 Theoretical model by the Institute of Risk Management

The Institute of Risk Management has formed risk appetite framework, which will be explained

below in Figure 3.2. The framework is shown as sign of recognition for the thoroughness and

theoretical value. A such, the framework provides inspiration for building a model for the Dutch

pension sector (paragraph 3.6).

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 3

Figure 3.2: Building blocks of risk appetite framework by the IRM (IRM, 2011, p.16).

Working from outside-in, several characteristics of the model – which will be used to developing

a model for Dutch pension funds – are summarized below.

The model recognizes the importance of risk capacity (the ability to carry risks) and the

risk maturity of an organization. The IRM stresses that a risk appetite is not „one size fits

all‟ (IRM, 2011, p.17) and that there is no use in developing a sophisticated risk appetite

when the organizational maturity to manage the risk appetite is low.

The IRM states that risk management maturity can be measured on four dimensions: the

business context, processes, systems and culture (IRM, 2011, p.19). The dynamics of

risk maturity imply an equal dynamic nature of the risk appetite.

From the inner building blocks it is shown that risk appetite is set at strategic, tactical

and operational levels (IRM, 2011, p17), and it indicates that embedding risk appetite

throughout the organization is one of the bigger challenges.

The IRM stresses the importance of measuring the risk appetite. This is the only way to

give meaning to the concept risk appetite. The IRM states that risk measurement will

predominantly take place at operational level, where risk taking decisions are set at the

strategic level (IRM, 2011, p.17).

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 4

3.4 Enterprise Risk Management model by COSO

A very well-known Enterprise Risk Management model is developed by the Committee of

Sponsoring Organizations of the Treadway Commission (COSO, 2004). The COSO cube is

presented in Figure 3.3.

Figure 3.3: The COSO cube (COSO, 2004)

COSO forms the basis of Risk Management for many Dutch pension funds (Pensioenfederatie,

2012). Although, in practice the pension funds have started building their risk management

bottom-up, by identifying risks, assessing risks, controls, and implementing monitoring &

reporting activities. The missing link between current risk management in practice and future

risk management is at the top of the pyramid: strategy/setting risk appetite, linking the

operational risk management frameworks to strategy. This is a key level in the COSO-cube

shown in Figure 3.3, marked as „internal environment‟. According to COSO (2004), the tone of

the organization is determined in the internal environment and here the risk appetite is set.

3.5 Clover Leaf model of Atos and Integral Risk Management by Pensioenfederatie/KPMG

The models of the IRM (2011) and COSO (2004) put emphasis on embedding the risk appetite

throughout the organization, and draw the attention to setting a risk appetite at the strategic

level. In addition to these models it is worthwhile to mention two models of organizational

effectiveness, which focus on the relation between strategic goals and operational design

(Figures 3.4 and 3.5).

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 5

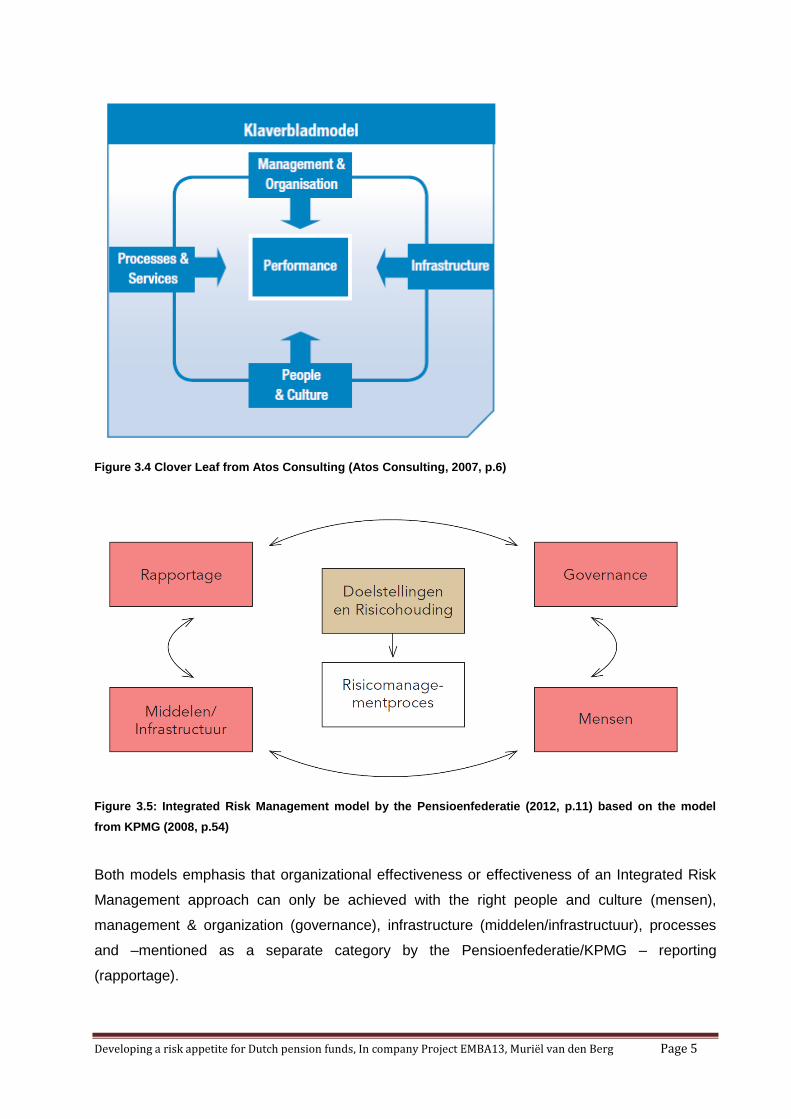

Figure 3.4 Clover Leaf from Atos Consulting (Atos Consulting, 2007, p.6)

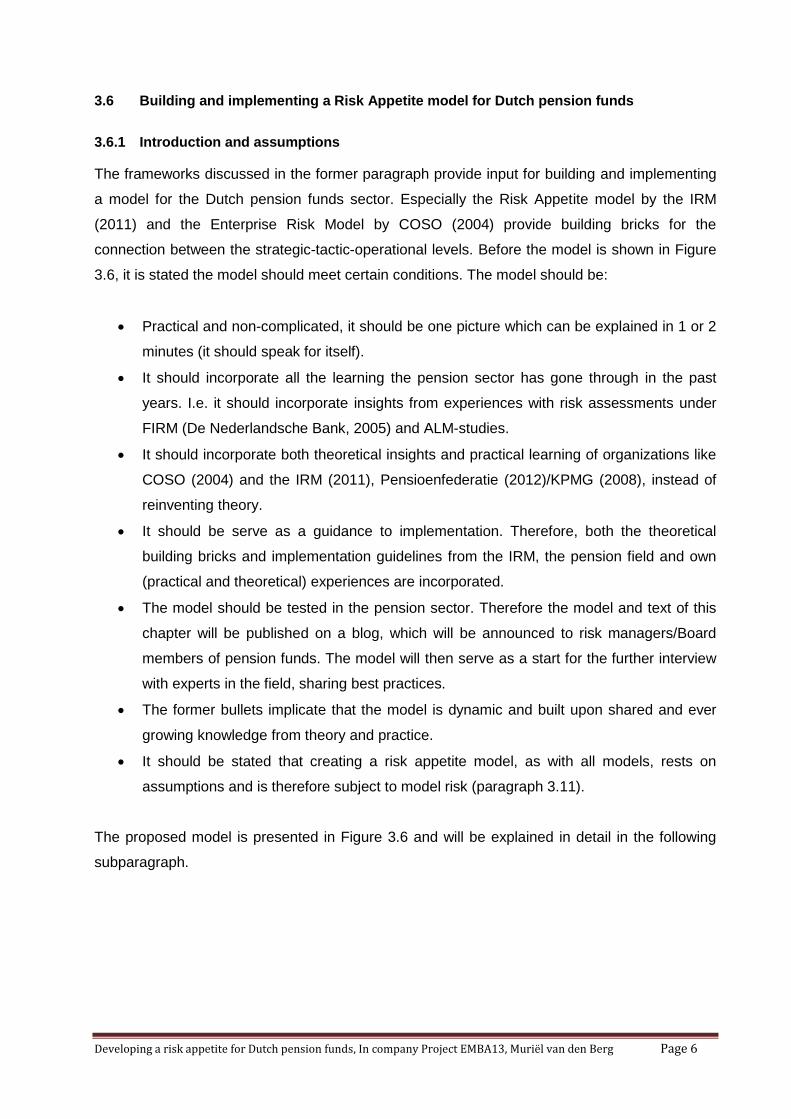

Figure 3.5: Integrated Risk Management model by the Pensioenfederatie (2012, p.11) based on the model

from KPMG (2008, p.54)

Both models emphasis that organizational effectiveness or effectiveness of an Integrated Risk

Management approach can only be achieved with the right people and culture (mensen),

management & organization (governance), infrastructure (middelen/infrastructuur), processes

and –mentioned as a separate category by the Pensioenfederatie/KPMG – reporting

(rapportage).

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 6

3.6 Building and implementing a Risk Appetite model for Dutch pension funds

3.6.1 Introduction and assumptions

The frameworks discussed in the former paragraph provide input for building and implementing

a model for the Dutch pension funds sector. Especially the Risk Appetite model by the IRM

(2011) and the Enterprise Risk Model by COSO (2004) provide building bricks for the

connection between the strategic-tactic-operational levels. Before the model is shown in Figure

3.6, it is stated the model should meet certain conditions. The model should be:

Practical and non-complicated, it should be one picture which can be explained in 1 or 2

minutes (it should speak for itself).

It should incorporate all the learning the pension sector has gone through in the past

years. I.e. it should incorporate insights from experiences with risk assessments under

FIRM (De Nederlandsche Bank, 2005) and ALM-studies.

It should incorporate both theoretical insights and practical learning of organizations like

COSO (2004) and the IRM (2011), Pensioenfederatie (2012)/KPMG (2008), instead of

reinventing theory.

It should be serve as a guidance to implementation. Therefore, both the theoretical

building bricks and implementation guidelines from the IRM, the pension field and own

(practical and theoretical) experiences are incorporated.

The model should be tested in the pension sector. Therefore the model and text of this

chapter will be published on a blog, which will be announced to risk managers/Board

members of pension funds. The model will then serve as a start for the further interview

with experts in the field, sharing best practices.

The former bullets implicate that the model is dynamic and built upon shared and ever

growing knowledge from theory and practice.

It should be stated that creating a risk appetite model, as with all models, rests on

assumptions and is therefore subject to model risk (paragraph 3.11).

The proposed model is presented in Figure 3.6 and will be explained in detail in the following

subparagraph.

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 7

Figure 3.6: A practical model to determine and implement a risk appetite for pension funds

3.6.2 Overview of the model

From Figure 3.6 the following observations are made:

The Risk Appetite is embedded in the organization, at strategic, tactic and operational

level. At strategic level, the focus is more on setting a risk appetite and on operational

level it is more concerned with monitoring/reporting, conform the theoretical model of the

IRM (2011).

As stated before, the learning the pension field has gone through with respect to ALM-

studies and risk assessments is taken into account when developing a risk appetite

(input).

A necessary and integral part of forming a risk appetite – or more general to implement a

successful (Risk Management) strategy – is the organizational culture. This is a two-way

process. The tone at the top and cascading of the organizational culture ánd bottom-up

signaling contribute to (reform of) the organizational culture.

The link between forming and implementing a risk appetite and financial/economic

outcomes (e.g. losses; performance indicators) and technical outcomes (e.g. adequacy

of systems and procedures) is explicitly shown in the model. The measurements of

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 8

financial/economic and technical outcomes provide feedback to the setting and

implementation of the risk appetite at strategic-tactic-operational levels.

These feedback loops indicate that setting and implementing a risk appetite is a

continuous and context specific process. This statement is comparable with the IRM

framework, that place the organization in the ever changing environment (IRM, 2011,

p.16).

The bits and pieces of the model will be discussed in the remainder of this chapter.

3.7 Strategic level: developing a risk appetite

The risk appetite is developed at the strategic level. Input to set the risk appetite can come from

guidance from the IRM (2011), and past experience from the pension field with developing risk

assessment frameworks and ALM-studies.

3.7.1 Guidance from the IRM to facilitate a strategic discussion of the risk appetite

In their guidance paper Risk Appetite and Tolerance, the IRM (2011) provides a list of 25

practical questions to discuss with the Board (IRM, 2011, p.10). These questions cover:

The background of the risk appetite: which risks does the Board want to take/to avoid?

Are the strategic objectives of the organization clearly defined (IRM, 2011, p.10).

Designing a risk appetite: does the Board have insight in the capabilities, risk maturity

and risk culture of the organization (IRM, 2011, p.10). This will be discussed further in

paragraph 3.10.

Constructing a risk appetite: is the Board addressing all relevant risks (IRM, 2011, p.10).

The recommendations 2 to 5 (paragraph 3.7) show how to detect relevant risks and how

to discuss them with the Board.

Implementing a risk appetite: one of the questions is, whether the views of external

stakeholders are taken into account (IRM, 2011, p.10). The important relation between

the Board and its subcontractors will be discussed in paragraph 3.8.

Governing a risk appetite: an important question here is whether the Board has a risk

committee to oversee the development and monitoring of the risk appetite framework

(IRM, 2011, p.10). This will be discussed further 3.12 (the role of the risk manager).

Final thoughts: Here the question is addressed what the Board should do/change in the

future, hereby stressing the ongoing dynamic character of the risk appetite (IRM, 2011,

p.10).

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 9

The former questions are not limitative. It is worthwhile to read the guidance paper by the IRM

(2011) in depth to get inspired.

Recommendation 1: When developing a risk appetite, guidance questions by e.g. the IRM

(2011) facilitate the Board discussions.

3.7.2 Build on experience with risk assessment frameworks

In this report, it might be suggested that pension funds are not that far with implementing a risk

appetite. It is true that many funds are in the early days of developing an appetite (chapters 1

and 2). On the other hand, pension funds have spend an enormous amount of time to develop a

risk assessment framework (chapters 1 and 2). The risk assessment and risk

measurement/monitoring phase the funds have gone through can be seen as the first and most

important step to develop a risk appetite later on. First of all, from no risk management to

implementing a risk assessment framework requires that „the tone at the top‟ has changed

already towards risk mindedness. Assessing the risks, means that pension funds at least have

developed a feeling about the most important financial and non-financial risks. Getting from the

assessment framework to a risk appetite, in my opinion only requires two extra steps. First, the

risk tolerance boundaries per assets class and on portfolio level should be set (see Figure 3.1,

IRM, 2011). Funds now know which risks they take, and in some extent they discuss the

desirability of these risks. They determine whether they avoid, transfer, mitigate, reinsure

certain risks. And they make qualitative and quantitative impact analyses (see chapters 1 and

2). The extra mile is, to translate the chance*impact analyses – which is descriptive – into the

perceived ability of the fund to bear the risk. The second step is then to discuss, which risk is

actively desired – taking into account the tolerance levels.

Recommendation 2: Use the risk assessment framework – qualitative and/or quantitative

chance*impact analysis of risk categories – to discuss the ability and desirability to bear risks.

3.7.3 Build on experience with ALM-studies:

When taking into account financial risks the former advice is already followed by many pension

funds. When pension fund Boards discuss the feasibility of the (new) pension contract, they use

ALM-studies as a forecasting tool. The (personal) experience is that performing ALM-studies

and interpreting output from ALM-studies can be quite a technical exercise. Pension fund

Boards typically hire ALM-consultants to perform ALM-studies upon the Board‟s request.

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 10

ALM-consultants are merely specialists in quantitative risk management and typically have a

background in econometrics/mathematics/physics. The typical Board member of a pension

funds might struggle to consume this technical information and has an even more difficult task

to challenge the consultants. Since being „in control‟ and acting as a „countervailing‟ party are

important requirements a modern Board member should meet (e.g. De Nederlandsche Bank,

2011), practical knowledge of ALM-studies – especially where this contributes to forming an

opinion about the risk appetite – is a necessity.

To give the Board guidance when using ALM-studies as an instrument for developing a risk

appetite, two practical advices can be given. First of all, the right questions – which relate risk-

return decisions to the strategic goals – should be asked. ALM-consultants, or risk managers

directly working for the Board can guide an ALM-session. Fiduciary asset managers who have

their own ALM-departments can contribute from a technical point of view. However, the Board

should always take into account that they are in charge, and should assure itself that it can

operate independent and „countervailing‟ towards advising parties.

Typical questions an ALM-session should cover, could be:

What is the desired pension outcome the Board pursues. Which nominal or real pension

would they guarantee with xx% certainty? Which is the minimum pension outcome which

is still acceptable? This question gives insight in the risk tolerance (IRM, 2011).

What may be the maximum loss (in funding ratio or Euro‟s) the Board is willing to take?

This question also gives some insight in the risk tolerance (IRM, 2011).

What is the variability in pension outcomes that the Board accepts/pursues? It is better

to have a lower – but almost certain – pension outcome? Or is it better to have a high

pension outcome with a reasonable chance, and a very low pension outcome with some

chance? This question provides insight in the risk appetite (IRM, 2011).

What is the sensitivity of pension outcomes due to economic/demographic risks in

normal and stressed economies? This question provides insight in the effects of

changing parameters and create awareness of the power and limitations of models.

Another method, to make pension fund Boards aware of the effect of risk-return decisions on

the height and variability of pension outcomes, are ALM-simulations or ALM-games. Several

pension funds or academic researchers have developed these games. An easy way to develop

a relative simple ALM-model is @Risk, a build-in statistical tool for Microsoft Excel (see e.g.

Albright and Wilson, 2012 for access to @Risk). A stylistic picture of @Risk, representing a

funding ratio of a pension fund experiencing two shocks due to increasing life expectancy

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 11

(which is no longer applicable in the future new pension contract, where liabilities will be

adjusted for increasing life expectancy), is shown in Figure 3.7.

Figure 3.7: A stylistic example of modeling shocks in life expectancy with @Risk.

From this paragraph, two recommendations are derived:

Recommendation 3: Actively involve pension fund Boards when discussing ALM-studies, ask

open and concrete questions to discover the boundaries of the risks a pension fund can absorb

(risk tolerance) and as next step try to find a an optimum of the desired variability and expected

height of pension outcomes (developing a risk appetite).

Recommendation 4: Actively involve pension fund Board in developing ALM-studies, to increase

awareness of risk-return characteristics and the relation between risk-return profiles and the

desirability to take risk (set the risk appetite)

3.7.4 Stress tests en (stress) scenario’s and Emerging Risks

ALM-studies form an important tool to give insights in risk-return profiles and show differences

in risk-return patterns in different economies. In addition to these insights, pension funds should

focus on (adverse) outcomes of stress test and stress scenarios on the funding ratio. The

search for stress tests and stress scenarios should capture both financial and non-financial

events. Several articles proclaim the need for focusing on new – emerging risks – instead of

what is already known (e.g. PwC, 2009).

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 12

A handy tool to improve scenario thinking can be found in books on Strategic Management, e.g.

Johnson et al. (2011). To summarize some of the insights, a first step in developing a strategy

could be, to focus on expected external developments (risks) regarding economics, politics,

social/demography, ecological, technological and law/regulations, which may affect pension

funds. This structured approach is known as a PESTEL or PESTLE analysis (e.g. Johnson et

al., 2011; Hopkin, 2012; Andersen, 2007). Practical guidance to decide on relevant emerging

risks can be found in publications of the World Economic Forum (2012). After a first assessment

of many risks (long list), the pension fund Board can decide to rank a short list of risk scenario‟s,

which could be quantified (impact analysis).

After the PESTEL-session – focusing on the unknown risks rather than sticking to the known

risks – the pension fund Board can summarize which threats and opportunities it foresees and

which risks it is willing to take to achieve the funds‟ objectives. This analysis (SWOT, e.g.

Johnson et al., 2011; Andersen, 2007) is an important exercise to decide on the future strategy

on the fund – in which the risk appetite should be embedded.

Recommendation 5: when discussing future risks, pension fund Board should focus on multiple

angles (PESTEL), and search for unknown risk scenario‟s. A number of scenario‟s should be

ranked by the Board, and the impact of these scenarios should be quantified and serve as input

to the SWOT and future strategy (e.g. Andersen, 2007; Johson et al., 2011; Hopkin, 2012).

3.8 Tactic and operational level: implementing systems and procedures and monitoring/reporting

To form a risk appetite an organization should at least be able to identify risks, measure risks,

monitor risks and report about risks (IRM, 2011, p.19). This implies a certain quality of the

processes, systems, people/culture and governance in the organization. The willingness to take

risk should be reflected in the strategic decisions, operations management and culture of the

organization. This was shown in the Clover Leaf Model in Figure 3.4 (Atos Consulting, 2007)

and the Pensioenfederatie (2012)/KPMG (2008) model in Figure 3.5. It is exactly along these

angles, that risk maturity of organizations can be measured (IRM, 2011, p.19). The importance

of an organizational culture – within the Board and within subcontractors – is discussed in

paragraph 3.10. The essence of governance and organization & management at the strategic

level was covered in paragraph 3.6. In this eight paragraph, the focus will be on the relation

between systems & processes in relation to the organizational strategy.

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 13

And precisely in that important aspect, the situation of a pension fund differs from most

organizations. In most organizations, the implementing/monitoring is part of the primary

process. Dutch pension funds have a different structure, where the pension fund Board is

actively in charge of the strategy/setting the risk appetite. The implementation of the day-to-day

processes and systems is generally outsourced to subcontractors, on behalf of the pension fund

Board. In managing a risk appetite, which should be embedded in the strategic-tactic-

operational levels, this structure can be quite a challenge. The pension fund Board should guide

that the subcontractor manages/oversees the implementation of the risk appetite and provides

feedback on a regular base. Formally, the Board has an Service Level Agreement (SLA) with its

subcontractor(s). As part of the service agreement the Board receives regular information about

e.g. development of the asset portfolio and liabilities, reports regarding the expected economic

developments and developments of financial and non-financial risk factors, risk monitoring

(financial & non financial), information about breaches, incidents and compliance issues. And

the pension fund Board generally receives assurance reports on controls (ISAE3402 reports)

from its subcontractor(s). For a discussion, how „to stay in control‟, see e.g. Bisschop et al.

(2011).

Since for most pension funds, there is a division between Board and subcontractor, and the risk

appetite should be embedded throughout all organizational levels, the connection between

strategy and tactic/operations level with respect to the risk appetite is crucial. Pension funds

Boards and contractors should take time to discuss the risk appetite set by the Board. And they

should both be convinced that the desired risk appetite can be implemented and monitored.

Otherwise a feedback loop in the model of Figure 3.6 indicates that either processes should be

adapted, either the risk appetite should be (slightly) altered.

Recommendation 6: Pension fund Boards and subcontractors should discuss the risk appetite

set by the Board. The Board should convince itself that the risk appetite is implemented and

monitored conform their specifications and the Board should regularly get feedback on risk

measures, risk developments, and the quality of systems & processes managed by the

subcontractor(s).

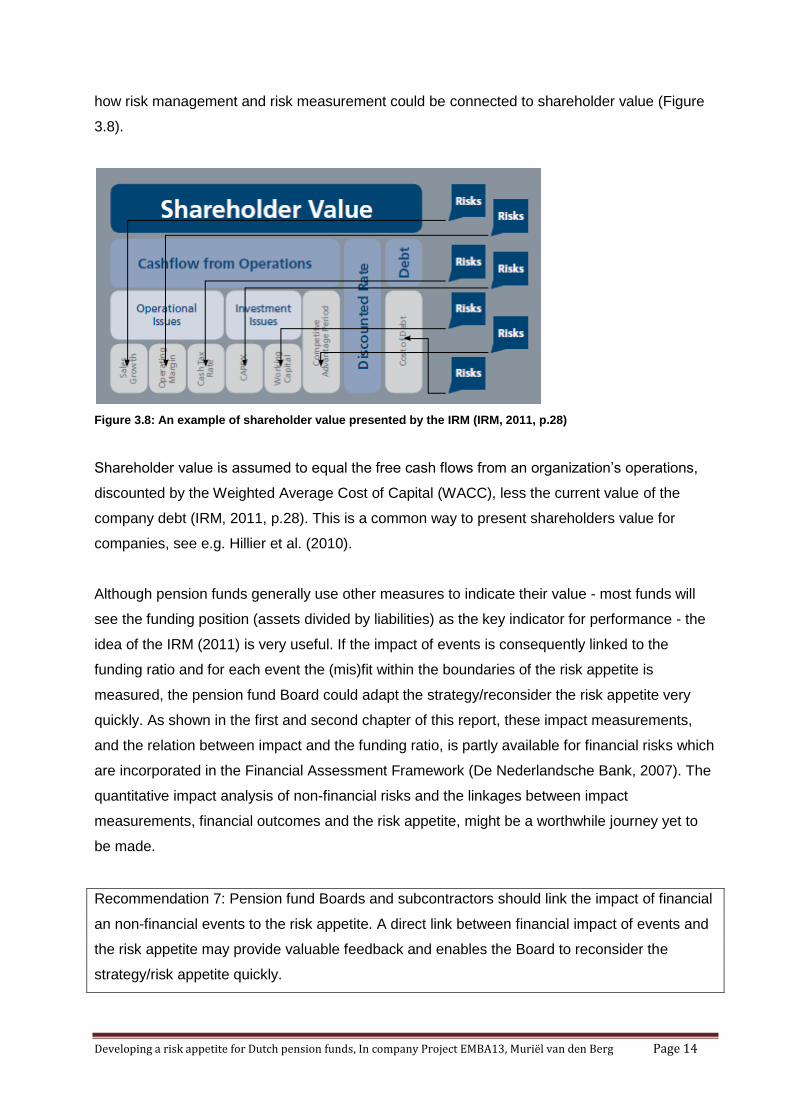

3.9 Financial outcomes

Financial outcomes of an organization should be related to strategic goals and operations. An

embedded risk appetite implies, that (financial) outcomes should also be related to the risk

management framework of an organization. The IRM (2011, p.28) shows several examples,

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 14

how risk management and risk measurement could be connected to shareholder value (Figure

3.8).

Figure 3.8: An example of shareholder value presented by the IRM (IRM, 2011, p.28)

Shareholder value is assumed to equal the free cash flows from an organization‟s operations,

discounted by the Weighted Average Cost of Capital (WACC), less the current value of the

company debt (IRM, 2011, p.28). This is a common way to present shareholders value for

companies, see e.g. Hillier et al. (2010).

Although pension funds generally use other measures to indicate their value - most funds will

see the funding position (assets divided by liabilities) as the key indicator for performance - the

idea of the IRM (2011) is very useful. If the impact of events is consequently linked to the

funding ratio and for each event the (mis)fit within the boundaries of the risk appetite is

measured, the pension fund Board could adapt the strategy/reconsider the risk appetite very

quickly. As shown in the first and second chapter of this report, these impact measurements,

and the relation between impact and the funding ratio, is partly available for financial risks which

are incorporated in the Financial Assessment Framework (De Nederlandsche Bank, 2007). The

quantitative impact analysis of non-financial risks and the linkages between impact

measurements, financial outcomes and the risk appetite, might be a worthwhile journey yet to

be made.

Recommendation 7: Pension fund Boards and subcontractors should link the impact of financial

an non-financial events to the risk appetite. A direct link between financial impact of events and

the risk appetite may provide valuable feedback and enables the Board to reconsider the

strategy/risk appetite quickly.

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 15

3.10 Risk culture

3.10.1 Observations from the Dutch pension field

The aspect of „risk culture‟ is very important when developing a proper risk appetite. Some

years ago, a study by Frijns (2010) had a massive impact in pension funds Board rooms. The

study concluded that Board Members of pension funds fail to take into account all stakeholders‟

interest when taking investment decisions. Instead of focusing on risk-return profiles, their

primary concern is expected returns (Frijns et al., 2010). An „asset only‟ view was accepted in a

pre-crisis environment. The post-crisis „risk-return‟ view – which requires a sudden and massive

reform of the organizational culture - still has to take root. Pension funds‟ Board

members/investors have to change their world view and adapt their behavior. Changing a risk

culture is a huge project, which requires Board time (and willingness!) and resources (IRM,

2012). In terms of Organizational Behavior, it is expected that the current corporate culture of

pension funds probably tends to be competitive and low emphasis on social responsibility, or

“aggressive” (McShane and Von Glinow, 2010, p. 419) and that an effective corporate culture to

implement a risk appetite probably is more oriented towards achieving stability, or more “rule-

oriented” (McShane and VonGlinow,2010, p.419)1.

3.10.2 Guidance on measuring Risk Culture by the IRM

The IRM stresses the importance of risk culture, as one of the four angles which measures the

risk maturity of the organization (IRM, 2011, p.19). The IRM defines the risk culture as „the

extent to which the board (and its relevant committees), management, staff and relevant

regulators understand and embrace the risk management systems and processes of the

organisation‟ (IRM, 2011, p.19). It states that the tone of the risk culture should be set from the

top of the organization, since behavior of top management will cascade through the

organization (IRM, 2011, p.19).

Both in the guidance paper regarding Risk Appetite and Risk Tolerance (IRM, 2011) and in a

separate paper on Risk Culture (2012), the IRM introduces the model by Hindson (2010)

(Figure 3.9).

1 McShane and Von Glinow refer to information they used from C.A. O‟Reilly III, J. Chatman, D.F. Caldwell, People and

Organizational Culture: a profile comparison approach to assessing person-organization fit. In: Academy of Management Journal 34, no. 3 (1991), pp. 487-518.

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 16

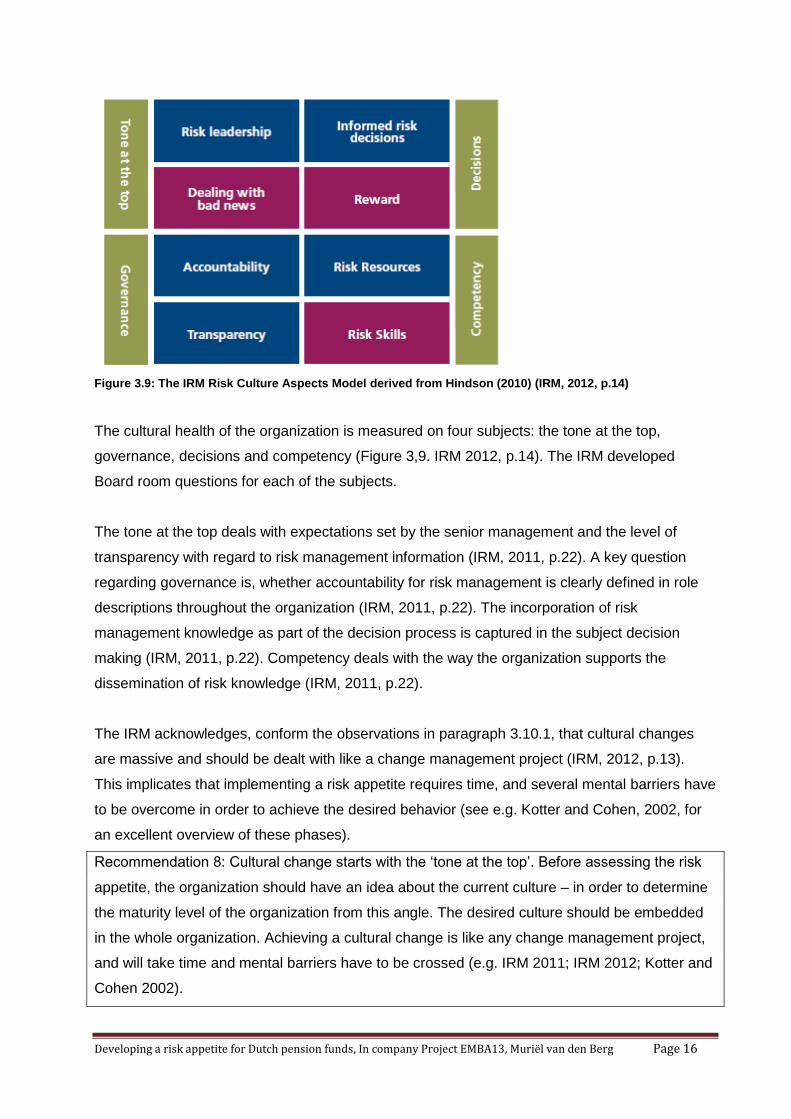

Figure 3.9: The IRM Risk Culture Aspects Model derived from Hindson (2010) (IRM, 2012, p.14)

The cultural health of the organization is measured on four subjects: the tone at the top,

governance, decisions and competency (Figure 3,9. IRM 2012, p.14). The IRM developed

Board room questions for each of the subjects.

The tone at the top deals with expectations set by the senior management and the level of

transparency with regard to risk management information (IRM, 2011, p.22). A key question

regarding governance is, whether accountability for risk management is clearly defined in role

descriptions throughout the organization (IRM, 2011, p.22). The incorporation of risk

management knowledge as part of the decision process is captured in the subject decision

making (IRM, 2011, p.22). Competency deals with the way the organization supports the

dissemination of risk knowledge (IRM, 2011, p.22).

The IRM acknowledges, conform the observations in paragraph 3.10.1, that cultural changes

are massive and should be dealt with like a change management project (IRM, 2012, p.13).

This implicates that implementing a risk appetite requires time, and several mental barriers have

to be overcome in order to achieve the desired behavior (see e.g. Kotter and Cohen, 2002, for

an excellent overview of these phases).

Recommendation 8: Cultural change starts with the „tone at the top‟. Before assessing the risk

appetite, the organization should have an idea about the current culture – in order to determine

the maturity level of the organization from this angle. The desired culture should be embedded

in the whole organization. Achieving a cultural change is like any change management project,

and will take time and mental barriers have to be crossed (e.g. IRM 2011; IRM 2012; Kotter and

Cohen 2002).

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 17

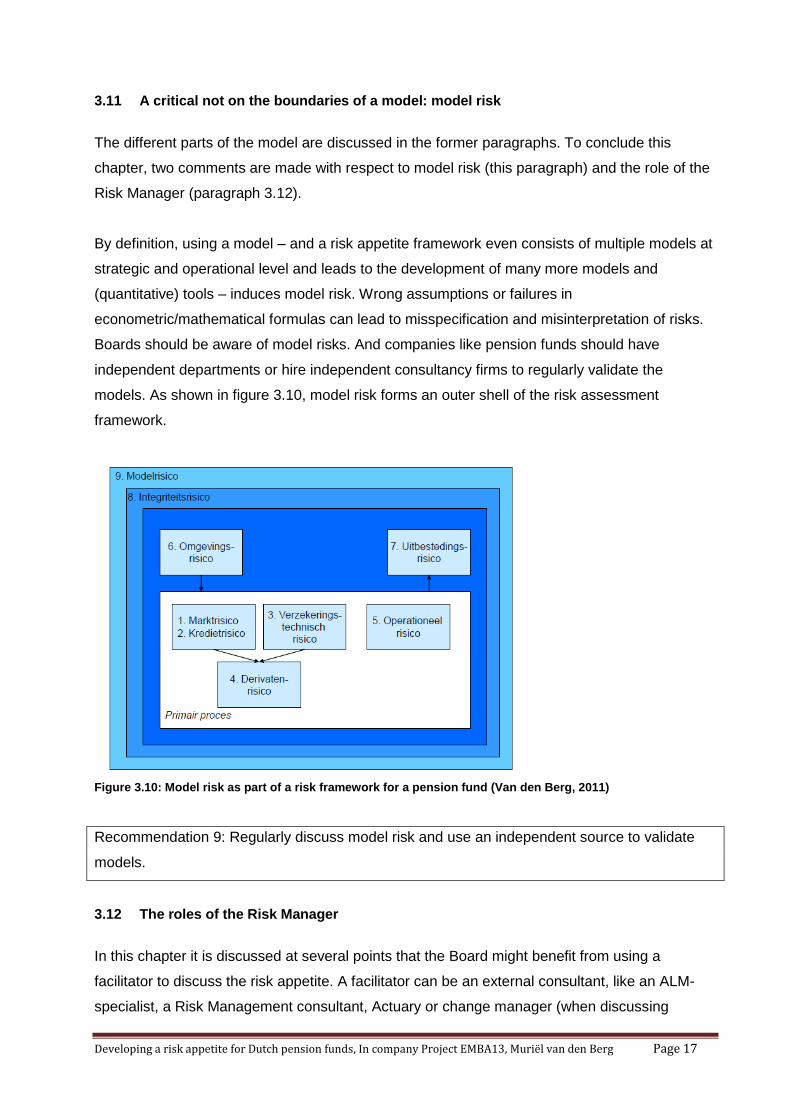

3.11 A critical not on the boundaries of a model: model risk

The different parts of the model are discussed in the former paragraphs. To conclude this

chapter, two comments are made with respect to model risk (this paragraph) and the role of the

Risk Manager (paragraph 3.12).

By definition, using a model – and a risk appetite framework even consists of multiple models at

strategic and operational level and leads to the development of many more models and

(quantitative) tools – induces model risk. Wrong assumptions or failures in

econometric/mathematical formulas can lead to misspecification and misinterpretation of risks.

Boards should be aware of model risks. And companies like pension funds should have

independent departments or hire independent consultancy firms to regularly validate the

models. As shown in figure 3.10, model risk forms an outer shell of the risk assessment

framework.

Figure 3.10: Model risk as part of a risk framework for a pension fund (Van den Berg, 2011)

Recommendation 9: Regularly discuss model risk and use an independent source to validate

models.

3.12 The roles of the Risk Manager

In this chapter it is discussed at several points that the Board might benefit from using a

facilitator to discuss the risk appetite. A facilitator can be an external consultant, like an ALM-

specialist, a Risk Management consultant, Actuary or change manager (when discussing

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 18

culture and maturity of the organization). A Risk Manager, working directly for the Board could

also facilitate and guide discussions regarding risk management. In all instances, there is one

golden rule. The Board can be facilitated, however the Board must ensure that it is in charge,

i.e. it is „countervailing‟ against the external or internal advisors (e.g. De Nederlandsche Bank,

2011).

When discussing the practical, operational side of implementing a risk management framework,

it was already stated that the bulk of the job is probably done at the subcontractor‟s. The Board

should be countervailing towards the subcontractor. As shown in paragraph 3.8, the Board and

the subcontractor have a professional relation, recorded in e.g. a Fiduciary Management

agreement. The service provided by the subcontractor is covered in the Service Level

Agreement (SLA).

However, the pension fund Board should not only be countervailing towards the subcontractor,

they should also guarantee/gather proof, that the Risk Management department within the

subcontractor‟s organization (second line of defense) is independent from the Line Managers,

who are responsible for the daily risk management activities (first line of defense) (see e.g. the

position paper of the Institute of Internal Auditors, 2013).

Recommendation 10: Besides being countervailing towards the subcontractor(s), the Board

should convince itself, that countervailing power is embedded in the subcontractor‟s

organization by means of the three lines of defense model (e.g. Institute of Internal Auditors,

2013).

3.13 Conclusion

In this chapter, a model for developing and implementing a risk appetite for Dutch pension funds

is introduced. As stated in the introduction, this model is preliminary, in the sense that it is built

on theoretical knowledge and some (personal) practical insights. The model should develop

over time through contributions and experience from Board members, Risk Managers,

Consultants and other experts in the field of pensions.

This chapter will be shared on a blog, which is especially created to reach this goal.

http://riskappetitepensionfunds.wordpress.com/2013/05/01/risk-appetite-for-pension-funds/

The author cordially invites the field to actively add, amend and criticize the model in Figure 3.6

and share best practices.

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 19

Literature Chapter 3:

Albright, S.C. and W.L. Winston (2012). Management Science Modeling (4th edition). Canada:

South-Western, Cengage Learning.

Andersen, T.J. (2007). Strategic Risk Management: Outlining the Countours of the ‘New Risk

Management’ paradigm. In: Public Forrum, May 2007.

Atos Consulting (2007). Transformaties in de verzekeringsmarkt. Een onderzoek naar de

toekomstige verzekeraar en zijn consument. White paper. Atos Consulting, Utrecht. Available

at:http://www.gertjanschop.com/sitebuildercontent/sitebuilderfiles/modelklaverbladmodelartikelat

os.pdf (accessed 2 May 2013).

Bisschop, O. et al. (2011). Uitbesteding ‘in control’. In: Gids voor uitbesteding, onder redactie

van F. Klopper et al. Pensioen Bestuur & Management dossierreeks nr. 6. Epse: Petersen

Consult B.V..

COSO (2004). Enterprise Risk Management. Integrated framework. Executive summary.

Available at: http://www.coso.org/documents/coso_erm_executivesummary.pdf (accessed 19

February 2013).

De Nederlandsche Bank (2005). Handboek FIRM. Amsterdam: De Nederlandsche Bank.

Available at: http://www.edmondhalley.nl/resources/images/Handboek%20FIRM.pdf (accessed

18 February 2013).

De Nederlandsche Bank (2007). Financieel Toetsingskader voor Pensioenfondsen. Amsterdam:

De Nederlandsche Bank. Available at: http://www.toezicht.dnb.nl/2/2/50-202556.jsp (accessed

18 February 2013).

De Nederlandsche Bank (2011). Resultaten beleggingsonderzoeken 2010. Amsterdam: De

Nederlandsche Bank. Available at:

http://www.dnb.nl/binaries/DNB%20beleggingsonderzoek%202010_tcm46-251479.pdf

(accessed 18 February 2013).

Frijns, J.M.G., J.A. Nijssen en L.J.R. Sholtens (2010). Pensioen: “onzekere zekerheid”. Een

analyse van het beleggingsbeleid en het risicobeheer van de Nederlandse pensioenfondsen.

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 20

Eindhoven/‟s Gravenhage/Winsum: Commissie beleggingsbeleid en risicobeheer. Available at:

http://docs.minszw.nl/pdf/129/2010/129_2010_3_13883.pdf (accessed 18 February 2013).

Hillier, D., S.A. Ross, R.W. Westerfield, J. Jaffe and B.J. Jordan (2010). Corporate Finance

(First European Edition). Berkshire: McGraw-Hill.

Hindson, A. (2010). Developing a risk culture. In: Risk Management Professional, December

2010.

Hopkin, P. (2012). Fundamentals of Risk Management. Understanding, evaluating and

implementing effective risk management. London: the Institute of Risk Management.

Institute of Internal Auditors (2013). The Three Lines of Defense in Effective Risk Management

and Control. IIA position paper. Florida: Institute of Internal Auditors. Available at:

https://na.theiia.org/standards-

guidance/Public%20Documents/PP%20The%20Three%20Lines%20of%20Defense%20in%20E

ffective%20Risk%20Management%20and%20Control.pdf (Accessed 3 May 2013).

Institute of Risk Management (2011). Risk appetite & tolerance guidance paper. Published by

the Institute of Risk Management, London. Available online at:

http://theirm.org/publications/documents/IRMRiskAppetiteFullweb.pdf (accessed 29 January

2013).

Institute of Risk Management (2012). Risk Culture. Under the microscope guidance for Boards.

Published by the Insitute of Risk Management, London. Available online at:

http://www.theirm.org/documents/Risk_Culture_A5_WEB15_Oct_2012.pdf (accessed 31

January 2013).

Johnson, G., R. Whittington and K. Scholes (2011). Exploring Strategy, text & cases (9th

Edition). UK: Pearson Education Limited.

KPMG (2008). De pensioenwereld in 2009. Published by KMPG Advisory N.V.

Available at: http://dev.omvleewordwide.nl/wp-

content/uploads/2013/01/Pensioenwereld_2009.pdf (Accessed 3 May 2013).

Kotter, J.P. and D.S. Cohen (2002). The Heart of Change. Real-life stories of how people

change their organizations. Boston: Harvard Business Review Press.

Developing a risk appetite for Dutch pension funds, In company Project EMBA13, Muriël van den Berg Page 21

McShane, S.L. and M.A. Von Glinow, 2010 (5th edition). Organizational Behavior. New York,

McGraw-Hill.

Pensioenfederatie (2012). Integraal risicomanagement. Handreiking integraal

risicomanagement voor pensioenfondsen. Den Haag: Pensioenfederatie. Available at:

http://www.pensioenfederatie.nl/Document/Publicaties/Servicedocumenten/Risicomanagement_

DEF.pdf (accessed 18 February 2013).

PwC (2009 ). Exploring emerging risks. Published by PwC.

Available at: http://www.pwc.com/gx/en/research-publications/pdf/pwcglobalriskserm.pdf

(accessed 2 May 2013).

Van den Berg, M.N. (2011). Effectief risicomanagement bij pensioenfondsen: een mix van tools

en soft skills. In: De Actuaris, november 2011.

World Economic Forum (2012). Global Risks 2012 (seventh edition), an initiative of the risk

response network. Geneva: World Economic Forum.