Evaluation of Stationary Fuel Cell Deployments, Costs, and ... · Evaluation of Stationary Fuel...

25

NREL is a national laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable Energy, operated by the Alliance for Sustainable Energy, LLC. Evaluation of Stationary Fuel Cell Deployments, Costs, and Fuels 2013 Fuel Cell Seminar and Energy Exposition Keith Wipke (presenter) for Chris Ainscough, Jennifer Kurtz, Michael Peters, Genevieve Saur October 23, 2013 Columbus, Ohio NREL/PR-5400-60903 STA32-1

Transcript of Evaluation of Stationary Fuel Cell Deployments, Costs, and ... · Evaluation of Stationary Fuel...

NREL is a national laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable Energy, operated by the Alliance for Sustainable Energy, LLC.

Evaluation of Stationary Fuel Cell Deployments, Costs, and Fuels

2013 Fuel Cell Seminar and Energy Exposition Keith Wipke (presenter) for Chris Ainscough, Jennifer Kurtz, Michael Peters, Genevieve Saur

October 23, 2013 Columbus, Ohio

NREL/PR-5400-60903 STA32-1

2

Technology Validation at NREL

• Confirmation of component and system technical targets • Evaluation, optimization, and demonstration in integrated

energy systems • National Fuel Cell Technology Evaluation Center (NFCTEC)

Photo by Dennis Schroeder, NREL Figures and illustrations: NREL

3

www.nrel.gov/hydrogen/proj_tech_validation.html

NFCTEC Analysis Approach

National Fuel Cell Technology Evaluation Center

NFCTEC

Analysis and reporting of real-world operation data

4

Major Ramp-Up of Fuel Cell Stationary System Deployments Began in 2010

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

50

100

150

200

250

300

Total = 295 units

Cumulative Deployment Count by Year*Pr

ojec

t Cou

nt

TotalCHPElectric Only

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

50

100

150

Total = 121 MW

Cap

acity

[MW

]

Cumulative Capacity by Year*

TotalCHPElectric Only

NREL cdp_stat_01Created: Sep-25-13 9:08 AM | Data Range: 2001Q2-2013Q2 *Data from the California SGIP.

Majority of deployments and nearly all capacity is electric only

5

Contractual Status of Stationary Fuel Cell Systems in Deployment

3%

5%

15%

69%

Deployment Count By Status*

Other Categories: ICF ReviewICF InspectionRRF Technical ReviewRRF ReservedPPM Technical ReviewICF Technical Review

Definitions: RRF = Reservation Request Form, is the first step in the SGIP incentive claim process.PPM = Proof of Project Milestone; the applicant must prove progress and committment to the project.ICF = Incentive Claim Form is the step where the appliant, after meeting all SGIP requirements requests payment of the incentive.PBI = Performance Based Incentive is the way in which the incentive is paid out over time based on performance of the system.

OtherICF Pending PaymentPayment PBI in ProcessPPM ConfirmedPayment Completed

NREL cdp_stat_02Created: Sep-25-13 9:21 AM | Data Range: 2001Q2-2013Q2 *Data from the California SGIP.

New projects since 2011 receiving the performance-based incentive

Payment Completed

6

Stationary Fuel Cell System Count and Capacity by Fuel Type (ALL Fuel Cell Systems)

5%10%

12%

74%

Site Count by Fuel Type*

Biomass

Digester Gas

Landfill Gas

Natural Gas

4%

17%

14%

65%

Installed Capacity by Fuel Type

NREL cdp_stat_04Created: Sep-27-13 10:12 AM | Data Range: 2001Q2-2013Q2

Includes Status Categories:CompletedAdvancementPending PaymentPayment CompletedICF InspectionICF Pending PaymentICF ReviewICF Technical ReviewPayment PBI in ProcessPPM ConfirmedPPM Technical ReviewRRF ReservedRRF Technical Review

Total Capacity: 121 MWTotal Sites: 295

Installations by Fuel Type(All Fuel Cell Systems)

Definitions: RRF = Reservation Request Form, is the first step in the SGIP incentive claim process.PPM = Proof of Project Milestone; the applicant must prove progress and committment to the project.ICF = Incentive Claim Form is the step where the appliant, after meeting all SGIP requirements requests payment of the incentive.PBI = Performance Based Incentive is the way in which the incentive is paid out over time based on performance of the system. *Data from the California SGIP.

Natural gas is the most-used fuel. However, renewable fuels make up one-third of capacity.

7

Installations By Fuel Type (CHP Fuel Cells Only)

1%

99%

Site Count by Fuel Type*

Digester Gas

Natural Gas

18%

82%

Installed Capacity by Fuel Type

NREL cdp_stat_20Created: Sep-27-13 10:12 AM | Data Range: 2001Q2-2013Q2

Includes Status Categories:CompletedAdvancementPending PaymentPayment CompletedICF InspectionICF Pending PaymentICF ReviewICF Technical ReviewPayment PBI in ProcessPPM ConfirmedPPM Technical ReviewRRF ReservedRRF Technical Review

Total Capacity: 8 MWTotal Sites: 71

Installations by Fuel Type(CHP Fuel Cell Systems)

Definitions: RRF = Reservation Request Form, is the first step in the SGIP incentive claim process.PPM = Proof of Project Milestone; the applicant must prove progress and committment to the project.ICF = Incentive Claim Form is the step where the appliant, after meeting all SGIP requirements requests payment of the incentive.PBI = Performance Based Incentive is the way in which the incentive is paid out over time based on performance of the system. *Data from the California SGIP.

Nearly all CHP systems use natural gas.

8

Fuel Type Capacity (All Systems)

Biomass Digester Gas Landfill Gas Natural Gas0

100

200

300

400

500

600

700

800

900

1000

Inst

alle

d C

apac

ity (k

W)

Installation Capacity Statistics by Fuel Type*

NREL cdp_stat_05Created: Sep-27-13 10:17 AM | Data Range: 2001Q2-2013Q2

75% Percentile

Median

25% Percentile

Mean

*Data from the California SGIP.

Natural gas systems have a wide range of sizes. Digester systems tend to be the largest.

9

Installation Capacity by Fuel Type (CHP Fuel Cells)

Digester Gas Natural Gas0

100

200

Inst

alle

d C

apac

ity (k

W)

Installation Capacity Statistics by Fuel Type (CHP)*

NREL cdp_stat_21Created: Sep-27-13 1:33 PM | Data Range: 2001Q2-2013Q2

75% Percentile

Median

25% Percentile

Mean

Insufficientdata toprotect

anonymity

*Data from the California SGIP.

Natural gas CHP has a few large deployments (large mean, small 25–75 percentiles)

10

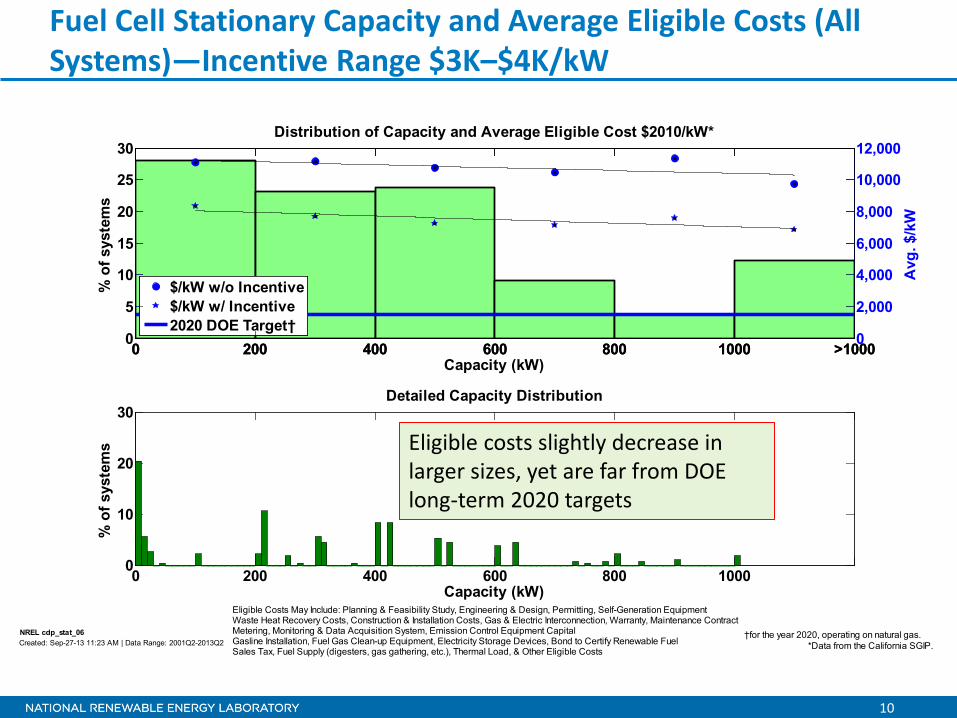

Fuel Cell Stationary Capacity and Average Eligible Costs (All Systems)—Incentive Range $3K–$4K/kW

0 200 400 600 800 1000 >10000

5

10

15

20

25

30Distribution of Capacity and Average Eligible Cost $2010/kW*

Capacity (kW)

% o

f sys

tem

s

0 200 400 600 800 1000 >10000

2,000

4,000

6,000

8,000

10,000

12,000

Avg

. $/k

W

$/kW w/o Incentive$/kW w/ Incentive2020 DOE Target†

0 200 400 600 800 1000 0

10

20

30

Capacity (kW)

% o

f sys

tem

s

Detailed Capacity Distribution

NREL cdp_stat_06Created: Sep-27-13 11:23 AM | Data Range: 2001Q2-2013Q2

†for the year 2020, operating on natural gas.*Data from the California SGIP.

Eligible Costs May Include: Planning & Feasibility Study, Engineering & Design, Permitting, Self-Generation EquipmentWaste Heat Recovery Costs, Construction & Installation Costs, Gas & Electric Interconnection, Warranty, Maintenance ContractMetering, Monitoring & Data Acquisition System, Emission Control Equipment CapitalGasline Installation, Fuel Gas Clean-up Equipment, Electricity Storage Devices, Bond to Certify Renewable FuelSales Tax, Fuel Supply (digesters, gas gathering, etc.), Thermal Load, & Other Eligible Costs

Eligible costs slightly decrease in larger sizes, yet are far from DOE long-term 2020 targets

11

Distribution of Capacity and Eligible Cost (CHP FC Only)

0 200 400 600 800 1000 >10000

20

40

60

80

Distribution of Capacity and Average Eligible Cost $2010/kW (CHP Fuel Cell)*

Capacity (kW)

% o

f sys

tem

s

0 200 400 600 800 1000 >10000

2,000

4,000

6,000

8,000

10,000

12,000

Avg

. $/k

W

$/kW w/o Incentive$/kW w/ Incentive2020 DOE Target†

0 200 400 600 800 1000 0

20

40

60

Capacity (kW)

% o

f sys

tem

s

Detailed Capacity Distribution

NREL cdp_stat_22Created: Sep-27-13 11:23 AM | Data Range: 2001Q2-2013Q2

†for the year 2020, operating on natural gas.*Data from the California SGIP.

Eligible Costs May Include: Planning & Feasibility Study, Engineering & Design, Permitting, Self-Generation EquipmentWaste Heat Recovery Costs, Construction & Installation Costs, Gas & Electric Interconnection, Warranty, Maintenance ContractMetering, Monitoring & Data Acquisition System, Emission Control Equipment CapitalGasline Installation, Fuel Gas Clean-up Equipment, Electricity Storage Devices, Bond to Certify Renewable FuelSales Tax, Fuel Supply (digesters, gas gathering, etc.), Thermal Load, & Other Eligible Costs

Economies of scale are better for CHP systems

12

Distribution of Stationary Fuel Cell Install Cost With and Without Incentives

0

20

40

60

80

0

1000

20

00

3000

40

00

5000

60

00

7000

80

00

9000

1000

011

000

1200

013

000

1400

015

000

1600

017

000

1800

019

000

2000

021

000

proj

ect c

ount

Price without incentives [$2010/kW]

Installed Eligible Cost Per kW*Adjusted To 2010 Dollars

Avg = $10,412 $/kW

CurrentDOE 2020 Target

0

20

40

60

0

1000

20

00

3000

40

00

5000

60

00

7000

80

00

9000

1000

011

000

1200

013

000

1400

015

000

1600

017

000

1800

019

000

2000

021

000

proj

ect c

ount

Price with incentives [$2010/kW]

Avg = $6,896 $/kW

CurrentDOE 2020 Target

NREL cdp_stat_07Created: Sep-27-13 12:16 PM | Data Range: 2001Q2-2013Q2 *Data from the California SGIP.

Eligible Costs May Include: Planning & Feasibility Study, Engineering & Design, Permitting, Self-Generation EquipmentWaste Heat Recovery Costs, Construction & Installation Costs, Gas & Electric Interconnection, Warranty, Maintenance ContractMetering, Monitoring & Data Acquisition System, Emission Control Equipment CapitalGasline Installation, Fuel Gas Clean-up Equipment, Electricity Storage Devices, Bond to Certify Renewable FuelSales Tax, Fuel Supply (digesters, gas gathering, etc.), Thermal Load, & Other Eligible Costs

Average incentives are $3,500/kW historically; fuel cell incentives are now set to decrease 10% per year.

13

Stationary Fuel Cell Install Cost Over Time With and Without Incentives

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

5

10

15

20

25

Ave

rage

$20

10/W

of In

stal

led

Cap

acity

Average Eligible Cost $2010/W Trend for Overall Deployments*

Without IncentiveWith IncentiveDOE 2020 Target

0

5

10

15

20

25

200120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

13

Capacity < 500 kW

Ave

rage

$20

10/W

of In

stal

led

Cap

acity

0

5

10

15

20

25

200120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

13

500 kW <= Capacity < 1000 kW

0

5

10

15

20

25

200120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

13

Capacity >= 1000 kW

NREL cdp_stat_08Created: Sep-25-13 9:08 AM | Data Range: 2001Q2-2013Q2 *Data from the California SGIP.

Eligible Costs May Include: Planning & Feasibility Study, Engineering & Design, Permitting, Self-Generation EquipmentWaste Heat Recovery Costs, Construction & Installation Costs, Gas & Electric Interconnection, Warranty, Maintenance ContractMetering, Monitoring & Data Acquisition System, Emission Control Equipment CapitalGasline Installation, Fuel Gas Clean-up Equipment, Electricity Storage Devices, Bond to Certify Renewable FuelSales Tax, Fuel Supply (digesters, gas gathering, etc.), Thermal Load, & Other Eligible Costs

Eligible costs are generally increasing over time (inflation adjusted), driven by the sub-MW size range

14

Stationary Fuel Cell Install Cost by Fuel Type With and Without Incentives

Biomass Digester Gas Landfill Gas Natural Gas2000

4000

6000

8000

10000

12000

$201

0/kW

of In

stal

led

Cap

acity

Eligible Cost $2010/kW of Installed Capacity by Fuel Type*

Avg. Without IncentiveAvg. With Incentive

NREL cdp_stat_09Created: Sep-25-13 9:09 AM | Data Range: 2001Q2-2013Q2

75% Percentile

Median

25% Percentile

Mean

*Data from the California SGIP.

Eligible Costs May Include: Planning & Feasibility Study, Engineering & Design, Permitting, Self-Generation EquipmentWaste Heat Recovery Costs, Construction & Installation Costs, Gas & Electric Interconnection, Warranty, Maintenance ContractMetering, Monitoring & Data Acquisition System, Emission Control Equipment CapitalGasline Installation, Fuel Gas Clean-up Equipment, Electricity Storage Devices, Bond to Certify Renewable FuelSales Tax, Fuel Supply (digesters, gas gathering, etc.), Thermal Load, & Other Eligible Costs

Digester systems have the lowest costs in both mean and 25 percentile

15

Total Incentive Spending ($2010) per kW by Year

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

20

40

60

80

100

120

140

Cap

acity

[MW

]

Year2000

2500

3000

3500

4000

4500

5000

5500

Ince

ntiv

e Sp

endi

ng ($

2010

) Per

kW

Inst

alle

d

Total Incentive ($2010) per kW by Year*

NREL cdp_stat_11Created: Sep-25-13 9:09 AM | Data Range: 2001Q2-2013Q2 *Data from the California SGIP.

Deployments are continuing to increase in an era of decreasing incentives

16

Average System Size Installed Per Year (kW)

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

100

200

300

400

500

600

700

800

Ave

rage

Sys

tem

Siz

e In

stal

led

Per Y

ear (

kW)

Year

Average System Size Installed Per Year (kW)*

Overall Average Capacity = 471 kW

NREL cdp_stat_12Created: Sep-25-13 9:09 AM | Data Range: 2001Q2-2013Q2 *Data from the California SGIP.

2013 has seen the third largest average system size 1 2

3

17

Installed Annual Capacity by Fuel Type

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

10

20

30

40

50

60

Year

Tota

l Ann

ual I

nsta

lled

Cap

acity

(MW

)

Installed Fuel Type By Year*

BiomassDigester GasLandfill GasNatural Gas

NREL cdp_stat_13Created: Sep-25-13 9:09 AM | Data Range: 2001Q2-2013Q2 *Data from the California SGIP.

Rule change in 2011 requiring directed biogas to be in state, and a lack of its availability (it’s all being used already) has led to dominance of natural gas

18

Comparing FC to Other Distributed Generation (DG): Distribution of Capacity by Equipment Type

0 200 400 600 800 1000 1200 1400 1600 1800 2000 >20000

50

100

150

200

250

300Distribution of Capacity by Equipment Type*

Capacity (kW)

Tota

l # o

f Sys

tem

s

Fuel Cell CHPFuel Cell ElectricGas TurbineInternal CombustionMicroturbinePressure Reduction Turbine

NREL cdp_stat_14Created: Sep-30-13 1:57 PM | Data Range: 2010Q10-2013Q2 *Data from the California SGIP.

Fuel cells represent about one-third of installed generation capacity in most size bins in SGIP

19

Comparing FC to Other DG: Average Eligible Cost by Equipment Type

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

5

10

15

20

25

Ave

rage

$20

10/W

of In

stal

led

Cap

acity

Average Eligible Cost $2010/W Trend for Overall Deployments*Without Incentives

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

5

10

15

20

25

Average Eligible Cost $2010/W Trend for Overall Deployments*With Incentives

Ave

rage

$20

10/W

of In

stal

led

Cap

acity

Fuel Cell CHPFuel Cell ElectricGas TurbineInternal CombustionMicroturbinePressure Reduction Turbine

NREL cdp_stat_15Created: Sep-30-13 1:57 PM | Data Range: 2010Q10-2013Q2 *Data from the California SGIP.

Eligible Costs May Include: Planning & Feasibility Study, Engineering & Design, Permitting, Self-Generation EquipmentWaste Heat Recovery Costs, Construction & Installation Costs, Gas & Electric Interconnection, Warranty, Maintenance ContractMetering, Monitoring & Data Acquisition System, Emission Control Equipment CapitalGasline Installation, Fuel Gas Clean-up Equipment, Electricity Storage Devices, Bond to Certify Renewable FuelSales Tax, Fuel Supply (digesters, gas gathering, etc.), Thermal Load, & Other Eligible Costs

Without incentives, fuel cells have a cost disadvantage compared to other technologies

20

Average Eligible Cost for Biogas Sources

0 200 400 600 800 1000 >10000

2000

4000

6000

8000

10000

12000

Average Eligible Cost $2010/kW Biogas Source*Without Incentives

System Size (kW)

$201

0/kW

of In

stal

led

Cap

acity

DirectedOnsite

0 200 400 600 800 1000 >10000

2000

4000

6000

8000

Average Eligible Cost $2010/kW Biogas Source*With Incentives

System Size (kW)

$201

0/kW

of In

stal

led

Cap

acity

DirectedOnsite

NREL cdp_stat_16Created: Sep-30-13 1:57 PM | Data Range: 2010Q10-2013Q2 *Data from the California SGIP.

Eligible Costs May Include: Planning & Feasibility Study, Engineering & Design, Permitting, Self-Generation EquipmentWaste Heat Recovery Costs, Construction & Installation Costs, Gas & Electric Interconnection, Warranty, Maintenance ContractMetering, Monitoring & Data Acquisition System, Emission Control Equipment CapitalGasline Installation, Fuel Gas Clean-up Equipment, Electricity Storage Devices, Bond to Certify Renewable FuelSales Tax, Fuel Supply (digesters, gas gathering, etc.), Thermal Load, & Other Eligible Costs

Directed biogas systems tend to cost more than onsite sources

21

Mean Time Between Stoppage (For Any Reason)

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000 11000 12000 13000 140000

5

10

15

20

25

30

35

40

% o

f Uni

ts

Mean Time (hr) between Stoppages

Mean Time Between Stoppage (hours)*

NREL cdp_stat_17Created: Sep-30-13 1:57 PM | Data Range: 2010Q10-2013Q2

Overall Mean = 2742 hours

*Data from outside the SGIP.

22

Mean Unit Lifetime Electrical Efficiency (%HHV)

10 15 20 25 30 35 40 450

5

10

15

20

25

30

35

% o

f Uni

ts

Mean Unit Electrical Efficiency (% HHV)

Unit Lifetime Mean Electrical Efficiency (HHV)*†

NREL cdp_stat_18Created: Sep-30-13 2:04 PM | Data Range: 2010Q10-2013Q2

Overall Mean = 27 %

†Includes startup, shutdown, transient and partial power operation *Data from outside the SGIP.

Efficiency includes startup, shutdown, transients, and part

load

23

Mean Unit Lifetime Availability

40 45 50 55 60 65 70 75 80 85 90 95 1000

5

10

15

20

25

30

35

40

% o

f Uni

ts

Mean Unit Availability (%)

Unit Mean Availability*

NREL cdp_stat_19Created: Sep-30-13 1:57 PM | Data Range: 2010Q10-2013Q2

Overall Mean = 93 %

*Data from outside the SGIP.

Availability includes stoppages for all

reasons, including customer request

24

Conclusions

• Stationary fuel cell deployments are accelerating despite decreasing incentives

• Current SGIP incentives make FC systems more competitive with other distributed generation systems

• Lack of available directed biogas in CA has caused new SGIP installations to be natural gas

• Cost curves need to begin going down (not up) to accommodate decreasing incentives

• NREL will continue to update results as new data are available

25

Acknowledgements

This project was supported by the Technology Validation subprogram of the U.S. Department of Energy’s Fuel Cell Technologies Office.