Evaluating the Effectiveness of Environmental Policies Using Financial Data …€¦ · ·...

47

1 Evaluating the Effectiveness of Environmental Policies Using Financial Data Series Minhua Yang, Vikash Ramiah, Imad Moosa † and Yu He School of Commerce, University of South Australia † School of Economics, Finance and Marketing, RMIT University The corresponding author: Dr. Vikash Ramiah UniSA Business School 37-43 North Terrace, City West Adelaide, South Australia 5000 Australia Tel: +61 8 8302 7572 Fax: +61 8 8302 0992 Email: [email protected] Acknowledgements This paper was presented at the CAFS 5 th Annual Finance Research Colloquium which was organised by the University of South Australia on 2 December 2015, the INFINITI 2016 Conference at Trinity College Dublin, the 2016 Multinational Finance Society 23 rd Annual Conference which was held at the Stockholm Business School in June 2016 and at Tianjin Academy of Environmental Studies in September 2017. The authors wish to thank the discussants and the anonymous referees, as well as Michael Gangemi, Jeremy Gabe, Ilke Onur and the remaining participants for their comments and support. We thank Tianjin Academy of Environmental Studies for their financial support. Any remaining errors are our own.

Transcript of Evaluating the Effectiveness of Environmental Policies Using Financial Data …€¦ · ·...

1

Evaluating the Effectiveness of Environmental Policies Using Financial Data Series

Minhua Yang, Vikash Ramiah, Imad Moosa† and Yu He

School of Commerce, University of South Australia

†School of Economics, Finance and Marketing, RMIT University

The corresponding author:

Dr. Vikash Ramiah UniSA Business School 37-43 North Terrace, City West Adelaide, South Australia 5000 Australia Tel: +61 8 8302 7572 Fax: +61 8 8302 0992 Email: [email protected]

Acknowledgements

This paper was presented at the CAFS 5th Annual Finance Research Colloquium which was organised by the University of South Australia on 2 December 2015, the INFINITI 2016 Conference at Trinity College Dublin, the 2016 Multinational Finance Society 23rd Annual Conference which was held at the Stockholm Business School in June 2016 and at Tianjin Academy of Environmental Studies in September 2017. The authors wish to thank the discussants and the anonymous referees, as well as Michael Gangemi, Jeremy Gabe, Ilke Onur and the remaining participants for their comments and support. We thank Tianjin Academy of Environmental Studies for their financial support. Any remaining errors are our own.

2

Evaluating the Effectiveness of Environmental Policies Using Financial Data Series

Abstract

This research explores the factors that determine the effectiveness of environmental regulation in the United States and Australia. Unlike prior literature that uses direct performance measures such as carbon emissions, we use financial data to determine effectiveness. We utilize the concept of green effect to develop effectiveness scores following each policy announcement and then identify the factors that determine the effectiveness scores. Leadership (narcissism and presidency tenure of political leaders) and fundamental factors (size, profitability, capital expenditure and leverage) are used to explain the effectiveness of environmental policies. Similar to the emerging literature in environmental finance, we find that abnormal returns are associated with environmental regulation, and we add to this literature by showing how a higher proportion of effectiveness in polluting sectors is achieved when less narcissistic leaders are in power.

JEL classification: G02, G14, G18, Q56.

Key Words: Environmental Policies, Green Effects, Narcissism, Effectiveness Scores,

Environmental Finance.

- 3 -

1. Introduction

When the Kyoto Protocol on climate change came into force in February 2005 a number of

countries agreed to commit to the reduction of greenhouse gas (GHG) emissions, leading to

the adoption of environmental policies that would achieve this objective. This has given rise

to a series of stringent environmental regulations and a debate on the effectiveness of these

policies. The emerging environmental finance literature shows that the effects of green

policies on stock markets are tangible and that regulations are not achieving their desired

effects in the sense that major polluting firms are not affected negatively whereas

environmentally-friendly businesses are affected negatively (in terms of negative abnormal

returns following the introduction of policies). It should be noted that such evidence is

circumstantial as there is no direct measure of effectiveness based on financial data. Although

the environmental economics literature provides direct measures (for example, carbon

emission levels) these are lagging, as opposed to leading indicators (for instance stock

prices). Leading indicators provide policy-makers with feedback on what the market expects

to happen if these policies were to be implemented and offer policy makers a leeway to adjust

their policies to achieve a higher level of effectiveness prior to the enforcement of regulation.

Furthermore, existing environmental economics/finance/accounting literature fails to provide

an explanation as to why the desired effects on stock returns are not achieved. In view of this

discussion, this study expands on and extends previous research and identifies factors that

contribute to the success of environmental policies as measured by the effectiveness scores

post the Kyoto Protocol.

The political will of leaders and governments is an important determinant of the adoption of

environmental regulation. For instance, George W. Bush used a cost–benefit analysis

argument to discourage the adoption of stringent environmental policies, stating that the

- 4 -

benefits from the implementation of stringent policies were unknown, and consequently there

was a need for further study before these policies could be implemented (Kraft, 2007).

Barack Obama, on the other hand, promised to tackle climate change in his first mandate and

formulated a strong view in favour of environmental protection. In Australia there has been a

long political discussion on the adoption of a Carbon Pollution Reduction Scheme (CPRS), as

former Prime Minister Tony Abbott has moved away from a carbon tax (also referred to as

carbon pricing) by introducing the Direct Action Plan (DAP). Given that governments around

the world are considering the effects of climate change and implementing policies to protect

the environment, this provides a practical justification for this research.

Although the knowledge related to political will and the implementation of green policies has

been accepted, it is unclear on politicians’ behavioural attributes, which may or may not

affect the effectiveness of green policies. One unique contribution of this research is that we

investigate whether or not narcissistic political leaders are more effective in implementing

environmental policies. Narcissism is regarded as a focus as this factor has distinctive

features that make it relevant for the effective implementation of environmental policies. This

is because narcissistic individuals undertake actions continuously to strengthen their self–

image and maintain their ideal ego (Buss and Chiodo, 1991; Campbell and Foster, 2007),

implying that narcissistic leaders seek to manifest themselves when large stakes are involved

(for instance, the adoption and implementation of policies). In fact, the literature on strategic

management and environmental psychology confirms the connection between narcissism and

the pro–environmental behaviour. Other factors that determine the effectiveness of

environmental policies, such as presidency tenure and financial fundamentals (size, capital

expenditure, profitability and leverage), are also investigated. Adopting various tests, we

provide strong empirical evidence to demonstrate that narcissism, presidency tenure and

- 5 -

financial fundamentals are major determinants of the effectiveness of implementing

environmental policies.

This study combines environmental finance, traditional finance and behavioural finance to

explore the effectiveness of environmental regulation in the United States and Australia.

These two countries are chosen as the evidence indicates “green effects” in terms of abnormal

returns around the announcements of certain green policies (Veith et al., 2009; Ramiah et al.,

2013; Ramiah et al., 2015a), with abnormal returns being a key component of the proposed

effectiveness measure. The remainder of our paper is organized as follows. Section 2 reviews

the literature on environmental finance, environmental economics, narcissism, traditional

finance, and related background. Section 3 describes the data and methodology. Section 4

reports the empirical results, and Section 5 concludes the paper.

2. Literature Review and Theoretical Background

One segment of the applied economics literature1 advocates for the need to test for the

effectiveness of green policies as the direct measures such as carbon dioxide emissions

(United Nations Energy Statistics Yearbook, 1983 and 1984), nitrous oxide emissions

(Pachauri and Reisinger, 2007), temperature (Barreca, 2012; Dergiades et al., 2016) and

production of methane (U.S. Environmental Protection Agency, 2014) are not sufficient.

However, because of physical constraints, there are often lagging effects in terms of when

environmental policies emerge and when direct impacts take place as the physical

environment uses methods of laboratory analysis and surveys to investigate the effectiveness

of policies achieved by individual firms or groups of ordinary individuals (Moosa and

Ramiah, 2014). Nevertheless, researchers in this field fail to investigate the effectiveness of

1 See Auffhammer et al. (2009), Cason and Gangadharan (2013) and Cole et al. (2013).

- 6 -

these policies after considering the behavioural characteristics of political leaders who are

enforcing the policies. This paper contributes to the literature in two ways: (i) we provide an

additional explanation as to how narcissism and the tenure of political leaders affect the

implementation of green policies; and (ii) we use financial market data as a leading indicator.

Stock market data is considered to be superior compared to lagging indicators as it provides a

preview of what market participants’ perceptions are (analysts’ forecasts in terms of how they

perceive the cost and revenue functions of a firm will be affected if the policy was to be

implemented) when preliminary announcements about the policies are made prior to the

implementation date.

The emerging environmental finance literature suggests that abnormal returns are associated

with the announcements of green policies, which is referred to as “green effects” (Pham et al.,

2015; Ramiah et al., 2015b; Ramiah et al., 2016). The literature suggests that polluting

sectors are expected to experience negative abnormal returns when stringent green policies

are announced (Kahn and Knittel, 2003) as environmental costs that come along worsen

performance (Vernon, 1992; Kinnaman et al., 2014; Kolstad, 2014). Nevertheless, the

empirical evidence paints a different picture as it shows that environmental regulation fails to

achieve the desired effects, given that stringent policies neither have negative impacts on

polluting sectors nor positive impacts on environmentally-friendly sectors. Veith et al. (2009)

offer a possible explanation for the non–negative abnormal returns experienced by a polluting

sector (electricity firms) by showing that polluting firms tend to pass rising costs on to

consumers. Ramiah et al. (2013) report similar findings for the Australian market. Although

these studies provide circumstantial evidence for ineffectiveness, they fail to provide a direct

measure to quantify effectiveness that can be applied to all sectors, which would provide

- 7 -

justification for the development of a new methodology (effectiveness scores based on

financial data).

We observe a relationship between personality and environmental concern, which includes

concern for self, other people and the biosphere, implying a potential link between

personality and the successful implementation of environmental policies (Schultz, 2002).

Political leaders are often criticised for being narcissistic ̶ a personality that can potentially

impact political decisions, including decisions on environmental policies (Rosenthal and

Pittinsky, 2006; Winter, 2011). Narcissism, which was first introduced by Sigmund Freud, is

regarded as a sort of personality disorder that results from individuals’ experiences (Kohut,

1966). It can be defined as a “pervasive pattern of grandiosity in fantasy or behaviour, need

for admiration, and lack of empathy, beginning by early adulthood and present in a variety of

contexts” (American Psychiatric Association, 1994). The literature suggests a positive

relationship between narcissism and the implementation of policies. For instance, after

studying the long-term association between leadership and narcissism, Rosenthal and

Pittinsky (2006) conclude that narcissistic leaders (CEOs) have charisma, power and vision–

three great attributes to achieve excellence (firm performance). They contend that narcissistic

leaders (i) possess outstanding leadership styles, which inspire followers efficiently; (ii) have

grandiose belief systems; and (iii) focus on projects they are undertaking. It is apparent from

this literature that narcissistic leaders are more effective in swinging political decisions in the

way they want. The implication for environmental policies is that if a political leader cares

for the environment then the leader will ensure the successful implementation of stringent

environmental policies (and vice versa). According to Bergman et al. (2014), narcissism is

related significantly to lower levels of environmental ethics. Similarly, Dunbar (2011)

suggests that narcissism negatively affects pro–environmental behaviour. One conclusion that

- 8 -

can be drawn from this literature is that narcissism contributes to an inappropriate sense of

environmental protection and may be a factor that results in ineffective implementation in

this area. To address this contrast of connections between narcissism and implementation of

environmental policies, this paper contributes to the literature by attempting to find out

whether narcissistic leaders are more or less effective when it comes to the implementation of

pro–environmental policies.

Another factor that may affect leadership and further determines the effectiveness of green

policies is presidency tenure, as House et al. (1991) state that this factor determines

presidential motives, behavioural charisma and presidential performance. Similarly in the

financial field, Chen et al. (2006) indicate that the tenure of CEOs is associated with

corporate strategy and performance. Based on these findings, we add presidency tenure as an

explanatory variable in our model.

The literature documents the finding that abnormal returns (and cumulative abnormal returns)

are affected by financial fundamentals such as firm size, capital expenditure, profitability and

leverage (Keim, 1983; Chan, 1990; Dhaliwal et al., 1991; Abarbanell and Bushee, 1998;

Chung et al., 1998; Hull, 1999; Dische, 2002). For instance, it has been found that (i) firm

size affects abnormal returns (Keim, 1983); (ii) capital expenditure announcements impact

future earnings and abnormal returns negatively (Chan, 1990; Abarbanell and Bushee, 1998;

Chung et al., 1998); (iii) a positive relationship exists between profitability as measured by

earnings and abnormal returns (Dische, 2002); and (iv) leverage impacts abnormal returns

(Dhaliwal et al., 1991; Hull, 1999).

- 9 -

Among these financial fundamentals, capital expenditure provides a unique feature in that it

may affect abnormal returns both positively and negatively. The reaction between stock price

and capital expenditure decisions is based on the quality of investment opportunities. For

instance, firms increase (decrease) capital expenditure on valuable investments, resulting in

positive (negative) abnormal returns, while increases (decreases) of capital expenditure on

valueless ones lead to negative (positive) abnormal returns (Chung et al., 1998). This leads us

to believe in the existence of a U–shape relationship between capital expenditure and

abnormal returns, although there is a lack of empirical evidence to support this relationship.

Thus, we conclude that these fundamentals may influence the green effects in terms of

abnormal returns.

In addition, we find that these financial fundamentals have the potential to influence the

effectiveness of green policies. The previous literature documents that fundamental

characteristics influence the effectiveness of green policies in terms of the air quality directly

or through firm performance indirectly (Robinson, 1982; Opler et al., 1994; Campello, 2006;

Gangadharan, 2006; González, 2009; Offenberg, 2009; Margaritis et al., 2010; Henner et al.,

2011). For instance, González (2009) indicates that environmental costs amount to around 10%

of capital expenditure for certain firms, which determines whether or not these firms or

sectors can afford environmental costs as they have been under enormous pressure to use low

carbon emission equipment. Therefore, a positive relationship between capital expenditure

and the effectiveness of green policies is expected. What we draw from the literature is that it

is important to have fundamental characteristics as explanatory variables.

3. Data and Methodology

- 10 -

This study examines announcements of environmental policies in the United States and

Australia over the period 1989–2015. In total, 978 announcements of environmental policies

are sourced from websites of the United States Environmental Protection Agency2and the

Department of Environment in Australia3. Market data for 1131 listed firms are collected

from Datastream. Following Simonton (1988), the data used to measure narcissism are

collected manually from transcripts of political leaders’ speeches and autobiographies.

3.1. Measuring the Effectiveness of Environmental Policies (The Dependent Variable)

We develop four processes concerning the measurement of the effectiveness of

environmental policies. These processes are: (i) identifying a policy as stringent or lax; (ii)

determining whether a sector is a polluter or environmentally-friendly; (iii) estimating

abnormal returns and cumulative abnormal returns around the announcements dates of

environmental policies; and (iv) developing effectiveness scores based on abnormal returns

and cumulative abnormal returns.

The first process of measuring effectiveness involves the categorization of environmental

policies as either stringent or lax. A stringent (lax) policy is defined in terms of reducing

carbon emissions. The next process is to categorize firms or sectors as either polluters or

environmentally-friendly, using two definitions to identify polluters. The first definition is

based on the maximum4 amount of emissions of greenhouse gases permitted. A sector is

classified as a polluter if its emissions are higher than 25,000 metric tons or more per year of

GHG in the United States and is more than 50 kilotons of GHG for 2010–2011 and onwards

in Australia. The second definition is based on the manufacturing processes of different

sectors or firms to identify the processes that release certain pollutants, which vary across 2 http://www3.epa.gov/ 3 https://www.environment.gov.au/ 4 Maximum emission figures are extracted from Kauffmann, Less and Teichmann (2012).

- 11 -

sectors. To be specific, a sector is classified as a polluter if it is found to (i) use or release any

of the specified pollutants, (ii) emit certain GHG, and (iii) produce harmful types of waste or

pollute water.5

Table 1 lists examples of pollutants that are used or released by a selection of sectors based

on definition two. For example, we can see from Table 1 that the sector of food beverage and

tobacco produces water, air and food pollution. Table 2 sketches how sectors are categorized

as either polluters (for example, electricity) or environmentally-friendly (for example, banks)

based on the two definitions. The second definition appears to be more precise as it

recognizes more polluters after considering the pollutants, which in turn solves the issue of

why certain green policies are not achieving their desired effects. Consequently, the second

definition is selected when a conflict occurs in the classification of sectors following the two

definitions (for example, see the beverage sector in Table 2). It should be noted that only

selected sectors are shown in tables 1 and 2 for the purpose of brevity.

The third process of measuring effectiveness is based on abnormal returns and cumulative

abnormal returns around the announcement dates of environmental policies. Daily returns for

each sector are calculated as the first natural logarithmic difference of the underlying stock

price index for all individual firms. The event study methodology of Brown and Warner

(1985) is adopted. Expected returns over the previous 260 days ̶are calculated via the capital

asset pricing model (CAPM) of Sharpe (1964) and Lintner (1965). Following Watts (1978),

we define abnormal returns as the difference between actual and expected returns. We

calculate cumulative abnormal returns with various event windows, which is a widely

5 Note that the two categorization schemes do not necessarily provide the same result. For instance, based on the level of emissions, the beverage sector may not be classified as a polluter but it is categorized as a polluter based on the pollutants used in the production process.

- 12 -

accepted procedure in the finance literature, including windows such as (-1, +1), (-5, +5), and

(-10, +10) (Cheung et al., 2006; Peng et al., 2011; Liu and Tian, 2012). The various windows

allow us to capture any leakage and/or any delayed response. Average industry abnormal

returns are calculated by grouping individual firms’ abnormal returns and cumulative

abnormal returns into different sectors.

The fourth process of measuring the effectiveness of environmental policies involves

developing effectiveness scores, representing one of the methodological contributions of this

paper. The underlying assumption is that stringent policies affect the cost and/or revenue

function of a firm, unless the firm is protected by another piece of regulation. This process

involves the examination of abnormal returns or cumulative abnormal returns of listed firms

(i) within sector (j) on the days when environmental policies (g) are announced. For a

stringent policy (gs) to be regarded as effective, it must generate either positive abnormal

returns for environmentally-friendly firms or negative abnormal returns for polluters. The

proportion of firms where the policy is effective is measured as

(1)

where ESjg is the effectiveness score for sector j following the announcement of policy g,

NEjg refers to the number of firms where the policy is effective6 within a sector, and Nj refers

to the total number of firms in sector j. Standard t–statistics of the effectiveness scores are

calculated to measure statistical significance. The reverse is expected for lax policies (gl). We

rank the effectiveness scores, which take a value between 0 to 17, and set three categories of

effectiveness: a score of 0 implies ineffectiveness, scores between 0.4 and 0.6 (inclusive)

imply moderate effectiveness, and a score of 1 is regarded as the most effective. The 1131

6 Effectiveness is achieved when environmentaly-friendly firms experience positive abnormal returns and the reverse is expected for the polluting firms following the announcement of a stringent policy. 7 Using a survey methodology, Bürer and Wüstenhagen (2009) developed environmental effectiveness scores for renewable energy policy, with values falling within the range 1 ̶5.

- 13 -

firms are organized under three categories (polluters, environmentally-friendly and mixed8),

so that the effectiveness scores for these three groups are calculated.

3.2. The Explanatory Variables

According to the literature review, it is important to consider explanatory variables such as

leadership (narcissism and presidency tenure) and fundamental industry characteristics (size,

profitability, capital expenditure and leverage). These variables are explained in turn.

3.2.1. Leadership–Narcissism and Presidency Tenure

One strand of the literature suggests that narcissism is a product of materialism and that it has

a negative impact on pro-environmental behaviour (Dunbar, 2011; Bergman et al., 2014).

Another strand of the literature states that narcissism contributes to leadership and further

influences such behaviour (Rosenthal and Pittinsky, 2006). This paper extends the literature

by investigating how narcissism affects effectiveness scores (which is also an implicit test for

the relationship between narcissism and the green effect).

Three measures of narcissism can be found in the academic literature, the details of which are

presented in the appendix. In this paper, narcissism is mainly proxied by a ratio of ‘I’ to ‘We’

where the data is manually collected from 2515 speeches. This procedure is used by Raskin

and Shaw (1988) who argue that narcissistic individuals tend to use the personal pronoun of

the first singular ‘I’ more than the personal pronoun of the first person plural ‘We’ during

their speeches and interviews. Kashima and Kashima (1998) support this conclusion and

show that the number of personal pronouns of the first singular used is correlated with

different conceptions of individuals. The ratio of ‘I’ to ‘We’ as a proxy for narcissism has

8 Mixed sectors are those with both polluting and environmentally friendly firms.

- 14 -

been adopted in earlier studies such as Chatterjee and Hambrick (2007) in management and

Aktas et al. (2013, 2016) in finance. When the ratio of ‘I’ to ‘We’ is greater than one, it

implies that a political leader exhibits narcissistic behaviour, and the higher the ratios, the

more narcissistic the political leader is. The alternative outcome implies a reverse personality

of narcissism, such as self-abasement.

It is worthwhile mentioning that culture is related to the use of personal pronouns (Kashima

and Kashima, 1998). We test correlation between culture and narcissism by using the

methodology developed by Hofstede (1983).9 Hiel et al. (2004) and Zavala et al. (2009)

contend that collective narcissism (right–wing authoritarianism and maladaptive personality)

usually exists as a sort of ideology of groups of political leaders. Thus, a party–centred

dummy is added as an explanatory variable to test the correlation and relationship with

leaders’ narcissistic personality. Other factors that may influence narcissism include duration

and pronoun–drop language in that residents in certain countries tend to use other words to

replace the personal pronoun of the first singular, which may reduce the accuracy of this

measure of narcissism. For instance, ‘I’ is often replaced by other words such as ‘We’ or

other pronoun–drop language in certain countries. Kashima and Kashima (1998) indicate that

this pronoun-drop language issue is related to collective culture and exists in few countries

such as China, Japan and Turkey. However, English, as the official language of the United

States and Australia, does not belong to the pronoun–drop language, thus the influence of

pronoun–drop language on narcissism can be excluded and avoided in this study. Following

the literature, we believe that the relationship between narcissism and its determinants can be

tested in the following manner (refer to appendix for an elaborate discussion).

9 According to Hofstede (1983), six dimensions of national culture-power distance, uncertainty avoidance, individualism/collectivism, masculinity/femininity, long/short term orientation and indulgence/restraint can be used to describe the cultural aspects of individuals or countries.

- 15 -

α (2)

Following Hofstede (1983) individualism is used to measure culture. We expect that (i)

individualism (culture) affects narcissistic behaviour positively; (ii) the longer the leaders are

in power, the more narcissistic they are (House et al., 1991; Rosenthal and Pittinsky, 2006);

and (iii) leaders from the right–wing parties, as measured by the party-centred dummy, are

expected to be more narcissistic (Hiel et al., 2004; Zavala et al., 2009).

Moreover, according to House et al. (1991), presidency tenure determines behavioural

charisma, presidential motives and related performance. Loewenstein et al. (2001) and

Hartley and Phelps (2012) support this proposition by arguing that leaders who stay in office

twice are prone to less stress in their second tenure as they do not suffer the pressure of re–

election, but their performance may deteriorate in the later stage of the tenure as their stress

level rises. Accordingly, we hypothesize that leaders who stay on longer devote themselves to

a successful implementation of environmental policies. Therefore, we adopt presidency

tenure as an explanatory variable to explain green effects and effectiveness scores where we

capture tenure with a dummy variable, second time in office (STO), which takes a value of 1

when leaders successfully win the second election and zero when leaders fail to serve a

second tenure.

3.2.2. Finance Fundamentals

According to the traditional finance literature, fundamental characteristics (such as size, value

and growth) affect financial performance. Within the emerging environmental finance

literature, the influence of finance fundamentals has not been explored. Nonetheless, the

environmental economics literature suggests that fundamental characteristics tend to affect

- 16 -

the quality of greenhouse gas emission following the implementation of environmental

policies, implying the need to control for finance fundamentals. We contribute to the

literature by attempting to find out if green effects and effectiveness scores are explained by

fundamental characteristics such as size, profitability, capital expenditure and leverage. The

size factor is represented by the logarithm of individual firm’s market value; profitability is

measured by the return on assets (ROA); capital expenditure (CAPEX) is calculated as the

ratio of capital expenditure to the value of common stock; and leverage is captured by the

debt to equity ratio.

3.3. Fundamental Analysis of Environmental Policies

The green effects (in terms of abnormal returns and cumulative abnormal returns) and

effectiveness scores following the announcement of environmental regulation are

investigated using fundamental characteristics.

3.3.1. Determinants of Green Effects

We postulate that the abnormal returns and cumulative abnormal returns associated with

environmental regulation are a function of the narcissistic behaviour of political leaders,

presidency tenure and fundamental characteristics (size, capital expenditure, profitability and

leverage). Hence

, , 3

, , 4

- 17 -

where , and are respectively the abnormal returns and cumulative abnormal

returns for each country c (United States and Australia) and for each sector j following

environmental policy announcements g. refers to two variables, narcissism

and the presidency tenure for each political leader p. The ratio of ‘I’ to ‘We’ is calculated

from data collected manually from 2015 speeches. As narcissism may affect leaders’ work

performance positively or negatively, as suggested by Rosenthal and Pittinsky (2006), we

expect either positive or negative relationship between narcissism and green effects.

Presidency tenure is a dummy variable that characterizes political stability which boosts

investors’ confidence, leading to positive abnormal returns. Consequently, we hypothesize a

positive relationship between tenure and green effects. Fundamental factors include size,

profitability, capital expenditure and leverage. We expect a positive relationship between

profitability and abnormal returns (Dische, 2002); a negative relationship with size (Keim,

1983) and leverage (Dhaliwal et al., 1991; Hull, 1999); and a mixed relationship for capital

expenditure (Chung et al., 1998).

3.3.2. Determinants of the Effectiveness of Green Policies

The effectiveness scores are explained by the following general model:

, , 5

where is the effectiveness scores calculated from both abnormal returns and cumulative

abnormal returns. We hypothesize (i) a mixed relationship with narcissism (Rosenthal and

Pittinsky, 2006; Dunbar, 2011); (ii) a positive relationship with presidency tenure (House et

al., 1991; Loewenstein et al., 2001; Hartley and Phelps, 2012); (iii) a positive relationship

with size, profitability, capital expenditure (Robinson, 1982; González, 2009); and (iv) a

- 18 -

negative relationship with leverage as highly levered firms has a strong commitment to

paying interest costs which in turn may lead to a deferral of environmental costs.

The analysis is based on cross-sectional data from two countries covering 62 sectors 10

(including 26709 firm-year observations). Before conducting the regression analysis, we

carry out a panel unit root test using the Fisher-Augmented Dickey-Fuller statistic with drift

and trend. The results show that all variables are stationary at the 1% and 5% significance

levels. Following González (2009), we assume that (i) various sectors react differently to new

announcements, and (ii) political leaders play pivotal roles in the implementation of these

policies. From an econometric point of view, this implies the need to control for the fixed

effects of sectors and leaders when equations 3, 4 and 5 are estimated. The Hausman test is

used to find out if fixed effects within the panel dominate random effects, obtaining results

that confirm our expectation and that of González (2009). Both correlation and variance

inflation factors tests reveal the absence of multicollinearity. A modified Wald test is used to

check for heteroscedasticity whereas the Huber-White sandwich estimators are used to

control for the standard errors.

4. Empirical Results

The empirical results are presented in the following order. We start with the summary

statistics of abnormal returns, effectiveness scores, and the variables used to represent

leadership and fundamental characteristics. The second part shows the results of the four

processes we use to calculate the effectiveness scores. The final part explains effectiveness

scores and green effects using various factors.

10 Combining Australia and United States

- 19 -

4.1 Summary Statistics

Table 3 displays the summary statistics of effectiveness scores, AR, CAR, narcissism, size,

profitability, capital expenditure (CAPEX), leverage and second time in office (STO). This

includes the number of observations (Obs), mean, minimum and maximum values. For

instance, the mean effectiveness scores (Effectivea) for the United States is 0.4390, indicating

that on average around 44% of the firms within an industry react to environmental policies in

the expected manner. We observe a similar proportion (labelled “moderate effective” in this

study as the proportion is between 0.4 and 0.6) regardless of the event window. In addition,

when the analysis is conducted for Australia, we find that on the average effectiveness score

is around 0.39, which is statistically lower than that of the United States (t statistics for the

test for difference is 11.81), implying that environmental policies are more effective in the

United States. The range of abnormal return (AR) is between -15.02% (minimum) and 13.72%

(maximum), whereas the range for the cumulative abnormal return (CARc) for the event

window (-5, 5) is between -43.81% and 32.85%. We use the evidence of abnormal returns to

confirm the existence of green effects. The mean of narcissism in the United States (1.27) is

higher than that of Australia (0.96), showing that American leaders are more narcissistic than

Australian leaders. The fundamental characteristics are higher for the United States, perhaps a

reflection of a larger economy. Furthermore, the mean of second time in office (STO) in the

United States (0.3630) is higher than that in Australia (0.2669), which shows that on average

American political leaders stay on longer.

4.2. Effectiveness of Environmental Policies

The first process of measuring the effectiveness of environmental policies is to categorize

these policies as either stringent or lax—99% of the policies are found to be stringent. The

second process enables us to detect 12 environmentally friendly sectors, 42 polluting sectors

- 20 -

and 8 mixed sectors that fall into both categories (examples of these sectors are commercial

and professional services, consumer discretionary, financials and real estate).

4.2.1. The Green Effects

The third process involves the calculation of abnormal returns and cumulative abnormal

returns around the announcement of environmental policies. The results reported in Table 4

indicate that green effects do exist in the United States as environmental policies affect

polluting (P) sectors effectively, resulting in negative abnormal returns (AR) for sectors such

as airlines (-0.06%), automobile (-0.02%), food products (-0.01%) and transportation (-

0.01%). Nevertheless, other polluting sectors experience positive abnormal returns—for

instance, the household durables sector experiences a positive abnormal return (0.06%). On

the other hand, most of the environmentally-friendly sectors experience positive returns,

including diversified financials (0.03%) and information technology (0.02%), implying

profitable opportunities for investors. Cumulative abnormal returns (CAR) for three event

windows are also calculated. The results suggest that green effects tend to be more evident

with longer window periods, reinforcing the notion of green effects. For example, the green

effect detected in the airline sector is -0.06% for the CAR (-1, +1) window and expands to -

0.76% for the CAR (-10, +10) window. Our findings are consistent with those of Pham et al.

(2015), Ramiah et al. (2015b) and Ramiah et al. (2016).

Previous studies tend to use anecdotal evidence on green effects to conclude whether

environmental policies achieve their goals (Veith et al., 2009; Ramiah et al., 2013; Ramiah et

al., 2015a). These studies look at whether major polluting firms (electricity) are negatively

affected by stringent policies and whether environmentally-friendly businesses are affected

positively. The results presented in Table 4 allow us to make such an assessment. For

- 21 -

example, the Australian energy sector (polluter) is positively affected whereas the banking

sector (environmentally-friendly sector) is negatively affected in terms of abnormal returns.

Such evidence can be interpreted to imply that environmental policies are not achieving their

goals in Australia. However, abnormal returns do not represent a direct measure, and this is

why we propose the effectiveness scores.

4.2.2. Effectiveness Scores

The fourth process creates effectiveness scores for each sector by finding out whether or not

the desired outcomes of green policies are achieved. We expect polluters to be negatively

affected (captured by negative abnormal returns) and environmentally-friendly businesses are

positively affected by stringent policies (where the reverse is expected for lax policies). More

specifically, we calculate the proportion of firms where the desired effects are achieved.

Effectiveness scores measured by abnormal returns and cumulative abnormal returns are

calculated for all sectors. Table 5 shows that the mean of effectiveness scores measured by

abnormal return for all sectors are 0.4389 and 0.3933 for the United States and Australia

respectively after estimating 26709 (21060 for United States) observations as shown in Table

3. This implies that environmental regulation in the United States is more effective than

Australia. We find similar occurrences across sectors, polluters and environmentally-friendly

sectors. For instance, the effective scores are higher for the United States for (i) polluters

(0.4629 vs 0.3955), (ii) environmentally-friendly (0.4212 vs 0.3658), and (iii) mixed sectors

(0.4194 vs 0.3833). The results reported in Table 5 imply that room for improvement exists

with respect to the effectiveness of environmental regulation as effectiveness scores are far

away from 100% in both countries (although the United States achieves a higher level of

effectiveness). Thus, we suggest that the government may carry out schemes for polluters and

- 22 -

boost the incentives for environmentally-friendly sectors to implement green policies more

effectively.

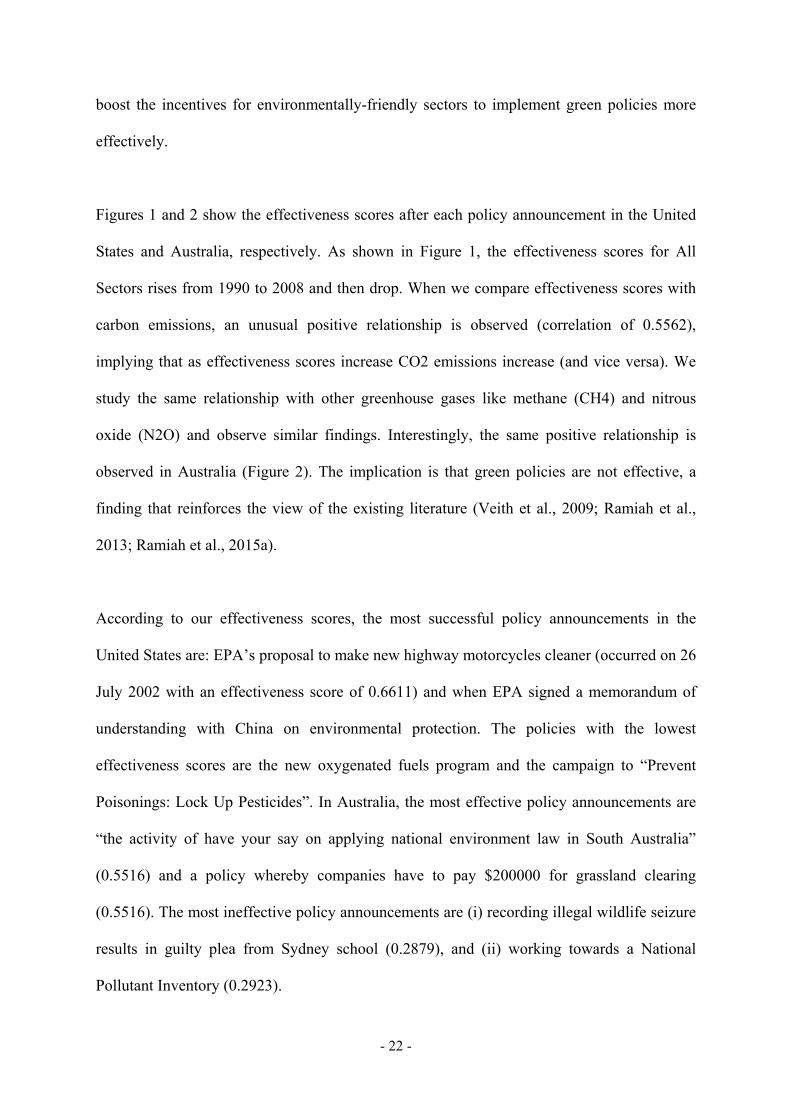

Figures 1 and 2 show the effectiveness scores after each policy announcement in the United

States and Australia, respectively. As shown in Figure 1, the effectiveness scores for All

Sectors rises from 1990 to 2008 and then drop. When we compare effectiveness scores with

carbon emissions, an unusual positive relationship is observed (correlation of 0.5562),

implying that as effectiveness scores increase CO2 emissions increase (and vice versa). We

study the same relationship with other greenhouse gases like methane (CH4) and nitrous

oxide (N2O) and observe similar findings. Interestingly, the same positive relationship is

observed in Australia (Figure 2). The implication is that green policies are not effective, a

finding that reinforces the view of the existing literature (Veith et al., 2009; Ramiah et al.,

2013; Ramiah et al., 2015a).

According to our effectiveness scores, the most successful policy announcements in the

United States are: EPA’s proposal to make new highway motorcycles cleaner (occurred on 26

July 2002 with an effectiveness score of 0.6611) and when EPA signed a memorandum of

understanding with China on environmental protection. The policies with the lowest

effectiveness scores are the new oxygenated fuels program and the campaign to “Prevent

Poisonings: Lock Up Pesticides”. In Australia, the most effective policy announcements are

“the activity of have your say on applying national environment law in South Australia”

(0.5516) and a policy whereby companies have to pay $200000 for grassland clearing

(0.5516). The most ineffective policy announcements are (i) recording illegal wildlife seizure

results in guilty plea from Sydney school (0.2879), and (ii) working towards a National

Pollutant Inventory (0.2923).

- 23 -

4.3. Fundamental Analysis

4.3.1. Factors Influencing the Effectiveness of Environmental Policies

Table 6 presents the factors that influence the effectiveness of green policies. In the United

States, we find four factors with explanatory power (narcissism, size, profitability and

CAPEX). Narcissistic behaviour is negatively related to the effectiveness score—for instance,

when narcissistic behaviour is increased by one unit, effectiveness scores decline by 0.012

when effectiveness is measured by CAR (-5,+5). This finding is consistent with those of

Dunbar (2011) and Bergman et al. (2014) who argue that narcissism tends to lead to lower

environmental ethics. A negative relationship is observed for capital expenditure and

profitability (to a lesser degree). For CAPEX, the result implies that as capital expenditure

goes up, effectiveness scores decline (unfortunately due to data limitations we cannot identify

capital spending on green methods of production). Furthermore, we find an inverse

relationship between profitability and effectiveness scores, a finding that is consistent with

the literature (Gangadharan, 2006). With regards to size, we observe a positive relationship

indicating that the larger the sector, the better it is at implementing environmental policies.

This provides support for the argument put forward by González (2009), which revolves

around firms that follow high environmental standards.

For Australia, three factors influence the effectiveness of environmental policies (size, capital

expenditure and second time in office). According to our results, political leaders who serve a

second tenure contribute to the effectiveness of environmental policies as we observe a

positive relationship (similar to House et al., 1991; Loewenstin, 2001; Hartley and Phelps,

2012). Furthermore, we find a positive relationship with size and capital expenditure

(consistent with Robinson, 1982; González, 2009).

- 24 -

4.3.2. Factors Determining the Green Effects

Another contribution of this paper is the identification of the factors that determine green

effects. Table 7 exhibits the factors that influence green effects when measured by abnormal

returns and cumulative abnormal returns. In the United States, we find three such factors:

narcissism, size and second time in office. Narcissism and second time in office are positively

related to green effects, implying that the narcissistic political leaders in their second tenure

tend to create investment opportunities in terms of generating green effects. This is consistent

with the proposition that narcissistic behaviour comes with great attributes to achieve

excellence in terms of firm performance, as suggested by Rosenthal and Pittinsky (2006) and

Chen et al. (2006) who argue that the tenure of leaders (although CEOs in this case) is

associated with firms’ performance. Our findings suggest a small firm size effect in that a

negative relationship is observed when it comes to green effects (consistent with Keim, 1983).

The evidence observed in Australia indicates that narcissism, size and leverage are important

factors. We find a negative relationship with leverage, implying that as leverage rises, less

green effects are observed (similar to Dhaliwal et al. 1991; Hull, 1999).

5. Conclusion

One objective of environmental regulation is to reduce greenhouse gas emissions in order to

tackle the problems of climate change. Following the implementation of the Kyoto Protocol

on climate change, countries around the world have been implementing a series of green

policies to address the problem of climate change. Although most environmental policies are

stringent, certain lax policies tend to relax previous regulations. One problem that the world

faces in regards to environmental regulation is that we do not know how these policies affect

financial markets—for instance, investors’ perspectives on stock market returns. This paper

- 25 -

contributes to this discussion by using a unique methodology to estimate the effectiveness of

environmental policies as well as the effect of environmental policies on stock markets in

terms of realized returns. The feasibility of a proxy of narcissism is tested and we find that

leaders’ narcissistic personality influences the effectiveness of environmental policies. We

conclude that the effective score model is a superior methodology to evaluate the

effectiveness of environmental policies and that there is major room for improvement in this

endeavour.

- 26 -

Appendix: Empirical Results Related to Narcissism

We posit that leadership influences green effects and the effectiveness of environmental

policies through two factors: narcissism and presidency tenure. In this appendix we provide

details as to how we estimate three proxies for narcissism.11 The first proxy, which is known

as the narcissistic personality inventory (NPI), has been developed by Raskin and Hall (1979)

by conducting surveys. The measure consists of 223 items describing the characteristics of

narcissistic personality disorder, including (i) grandiose sense of individual’s self-importance;

(ii) preoccupation with fantasies of unlimited success and power; (iii) exhibitionism; and (iv)

entitlement expecting special favours without assuming reciprocal responsibilities.

The other two measures of narcissism have been developed by Raskin and Shaw (1988) and

by Chatterjee and Hambrick (2007). Raskin and Shaw (1988) argue that in their speeches and

interviews, narcissistic individuals tend to use the personal pronoun of the first singular ‘I’

more than the personal pronoun of the first person plural ‘We’. Therefore, the ratio of ‘I’ to

‘We’ is used as another proxy for narcissism. There is positive correlation between the

second proxy and NPI, which remains valid after controlling for other personalities (Raskin

and Shaw, 1988). Kashima and Kashima (1998) support this finding and show that the

number of personal pronouns of the first singular used is correlated with different

conceptions of individuals. Chatterjee and Hambrick (2007) use salary packages as proxies of

narcissism, suggesting that narcissistic individuals believe that they are so outstanding that

they deserve better salary packages than others.

We have carried out our narcissistic analysis on the second proxy. One criticism of the

narcissism ratio is that leaders’ speeches may be written by others within the office/parties of

11 It should be noted that the use of proxies is widely accepted in finance and examples of these studies are Black et al. (1972), Mayers (1973) and Lee et al. (2002).

- 27 -

the political leader. We respond to this argument by suggesting that political leaders approve

the wording used in their speeches. Another criticism of this approach is that political leaders

may exhibit various narcissistic behaviour patterns in various stages of their lives. To address

the issue, we examine other speeches given by the same politicians when they are not in

office to find out if there are major differences. Another robustness test is to calculate the ‘I’

to ‘We’ ratio from autobiographies (Simonton, 1988). The third robustness test is to compare

the salary packages of presidents (or prime ministers) with those of the second in charge

(Chatterjee and Hambrick, 2007), where larger differences are expected for narcissistic

leaders.

It is worthwhile mentioning that the determinants of narcissism are investigated in this paper,

including culture (Kashima and Kashima, 1998), duration and the party centre dummy.

Culture is measured by following the methodology developed by Hofstede (1983). The

results suggest that this proxy is accurate as it can be used to measure narcissistic behaviour

and the reverse aspect of narcissism. Table A1 shows that half of the leaders exhibit

narcissistic behaviour in the United States as the narcissism ratios calculated for the

presidents are greater than one; while almost all narcissism ratios calculated for leaders in

Australia are less than one, implying that most of the political leaders are not narcissistic,

except for John Howard. The descriptive statistics in Table A1 show that leaders who come

from the Republican Party are more narcissistic than those who come from the Democratic

Party. Factors that affect narcissism are also investigated in this appendix (Table A2). The

party-centred dummy positively influences narcissistic behaviour, which indicates that

leaders from a right–wing party tend to be more narcissistic, a finding that is consistent with

the results of Zavala et al. (2009) and Hiel et al. (2004).

- 28 -

Robustness tests are used to test the potential criticism of this proxy. Table A3 presents the

results of first robustness test and lists narcissism ratios when leaders are/are not in power.

These political leaders appear to be more narcissistic post their candidature as shown in Table

A3. Narcissism ratios calculated from ‘I’ and ‘We’ statements collected from their

autobiographies and biographies are adopted as the second robustness test. Interestingly, the

results from autobiographies tend to be different from their biographies whereby we detect

higher levels of narcissism in autobiographies than biographies. Furthermore, the narcissism

levels detected by using this approach are higher than the levels in speeches. A third

robustness test is adopted by comparing leaders’ salary packages, national average annual

income (NAAI) and salary packages of the second chair. Leaders’ salaries are found to be

much more than the NAAI and those of the second chair. However, the results of this analysis

are inconclusive (or not applicable) as the salaries of political leaders are found to be

regulated by the government (which is different for CEOs of private firms).

- 29 -

References

Abarbanell, J. S., Bushee, B. J., (1998). Abnormal returns to a fundamental analysis strategy.

The Accounting Review 73(1), 19-45.

Aktas, N., Bodt, E. D., Roll, R., (2013). MicroHoo: Deal failure, sector rivalry, and sources

of overbidding. Journal of Corporate Finance 19(1), 20-35.

Aktas, N., Bodt, E. D., Roll, R., (2016). CEO narcissism and the takeover process: From

private initiation to deal completion. Journal of Financial and Quantitative Analysis

51(1), 113-137.

Americcan Psychiatric Association. (1994). Diagnostic and Statistical Manual of Mental

Disorders (4th Edition). Washington, DC: Author.

Auffhammer, M., Bento, A. M., Lowe, S. E., (2009). Measuring the effects of the Clean Air

Act Amendments on ambient PM10 concentrations: The critical importance of a

spatially disaggregated analysis. Journal of Environmental Economics and

Management 58(1), 15-26.

Barreca, A. I., (2012). Climate change, humidity, and mortality in the United States. Journal

of Environmental Economics and Management 63(1), 19-34.

Bergman, J. Z., Westerman, J. W., Bergman, S. M., Westerman, J., Daly, J. P., (2014).

Narcissism, materialism, and environmental ethics in business students. Journal of

Management Education 38(4), 489-510.

Black, F., Jensen, M. C., Scholes, M., (1972). The capital asset pricing model: Some

empirical tests. Studies in the theory of capital markets 79-121.

Brown, S. J., Warner, J. B., (1985). Using daily stock returns: The case of event studies.

Journal of Financial Economics 14(1), 3-31.

- 30 -

Bürer, M. J., Wüstenhagen, R., (2009). Which renewable energy policy is a venture

capitalist’s best friend? Empirical evidence from a survey of international cleantech

investors. Energy Policy 37(12), 4997-5006.

Buss, D. M., Chiodo, L. M., (1991). Narcissistic acts in everyday life. Journal of Personality

59(2), 179-215.

Campbell, W. K., Foster, J. D., (2007). The narcissistic self: Background, and extended

agency model, and ongoing controversies. The Self, Frontiers of Social Psychology.

New York, Psychology Press.

Campello, M., (2006). Debt financing: Does it boost or hurt firm performance in product

markets? Journal of Financial Economics 82(1), 135-172.

Cason, T., Gangadharan, L., (2013). Empowering neighbors versus imposing regulations: An

experimental analysis of pollution reduction schemes. Journal of Environmental

Economics And Management 65(3), 469-484.

Chan, S. H., (1990). Corporate research and development expenditures and share value.

Journal of Financial Economics 26(2), 255-276.

Chatterjee, A., Hambrick, D. C., (2007). It's all about me: Narcissistic Chief Executive

Officers and their effects on company strategy and performance. Administrative

Science Quarterly 52(3), 351-386.

Chen, G., Firth, M., Gao, D. N., Rui, O. M., (2006). Ownership structure, corporate

governance, and fraud: Evidence from China. Journal of Corporate Finance 12(3),

424-448.

Cheung, Y. L., Rau, P. R., Stouraitis, A., (2006). Tunneling, propping, and expropriation:

Evidence from connected party transactions in Hong Kong. Journal of Financial

Economics 82(2), 343-386.

- 31 -

Chung, K. H., Wright, P., Charoenwong, C., (1998). Investment opportunities and market

reaction to capital expenditure decisions. Journal of Banking and Finance 22(1), 41-

60.

Cole, M. A., Elliott, R. J. R., Okubo, T., Zhou, Y., (2013). The carbon dioxide emissions of

firms: A spatial analysis. Journal of Enviornmental Economics and Management

65(2), 290-309.

Dergiades, T., Kaufmann, R. K., Panagiotidis, T., (2016). Long-run changes in radiative

forcing and surface temperature: The effect of human activity over the last five

centuries. Journal of Enviornmental Economics and Management 76(1), 67-85.

Dhaliwal, D. S., Lee, K. J., Fargher, N. L., (1991). The association between unexpected

earnings and abnormal security returns in the presence of financial leverage.

Contemporary Accounting Research 8(1), 20-41.

Dische, A., (2002). Dispersion in analyst forecasts and the profitability of earnings

momentum strategies. European Financial Management 8(2), 211-228.

Dunbar, E., (2011). The green sheen: Are attitudes really predictive of proenvironmental

behavior? Social Sciences. Paper 24.

Gangadharan, L., (2006). Environmental compliance by firms in the manufacturing sector in

Mexico. Ecological Economics 59(4), 477-486.

González, P. D. R., (2009). The empirical analysis for the determinants for environmental

technology change: A research agenda. Ecological Economics 68(3), 861-878.

Hartley, C. A., Phelps, E. A., (2012). Anxiety and decision-making. Biological psychiatry

72(2), 113-118.

Henner, M. L., Powell, R. G., (2011). Firm size, takeover profitability, and the effectiveness

of the market for corporate control: Does the absence of anti-takeover provisions

make a difference? Journal of Corporate Finance 17(3), 418-437.

- 32 -

Hiel, A. V., Mervielde, I., Fruyt, F. D., (2004). The relationship between maladaptive

personality and right wing ideology. Personality and Individual Difference 36(2),

405-417.

Hofstede, G., (1983). National cultures in four dimensions: A research-based theory of

cultural differences among nations. International Studies of Management &

Organization 13(1), 46-74.

House, R. J., Spangler, W. D., Woycke, J., (1991). Personality and charisma in the U.S.

presidency: A psychological theory of leader effectiveness. Administrative Science

Quarterly 36(3), 364-396.

Hull, R. M., (1999). Leverage ratios, sector norms, and stock price reaction: An empirical

investigation of stock-for-debt transactions. Financial Management 28(2), 32-45.

Kahn, S., Knittel, C. R., (2003). The impact of the Clean Air Act Amendments of 1990 on

electric utilities and coal mines: Evidence from the stock market. Working Paper 118,

Centre for the Study of Energy Markets, University of California – Berkeley.

Kashima, E. S., Kashima, Y., (1998). Culture and language: The case of cultural dimensions

and personal pronoun use. Journal of Cross-Cultural Psychology 29(3), 461-486.

Kauffmann, C., Less, C. T., Teichmann, D., (2012). Corporate greenhouse gas emission

reporting: A stocktaking of government schemes. OECD Working Papers on

International Investment, No. 2012/1.

Keim, D. B., (1983). Size-related anomalies and stock return seasonality: Further empirical

evidence. Journal of Financial Economics 12(1), 13-32.

Kinnaman, T. C., Shinkuma, T., Yamamoto, M., (2014). The socially optimal recycling rate:

Evidence from Japan. Journal of Enviornmental Economics and Management 68(1),

54-70.

- 33 -

Kohut, H., (1966). Forms and transformations of narcissism. Journal of the American

Psychoanalytic Association 14(2), 243-272.

Kolstad, C. D., (2014). Who pays for climate regulation? SIEPR Policy Brief. Stanford

Institute for Economic Policy Research.

Kraft, M. E., (2007). Environmental Policy and Politics. United States of America, Pearson

Education. Print.

Lee, W. Y., Jiang, C. X., Indro, D. C., (2002). Stock market volatility, excess returns, and the

role of investor sentiment. Jounal of Banking & Finance 26(12), 2277-2299.

Lintner, J., (1965). The valuation of risk assets and the selection of risky investments in stock

portfolios and capital budgets. Review of Economics and Statistics 47(1), 13-37.

Liu, Q., Tian, G., (2012). Controlling shareholder, expropriations and firm's leverage decision:

Evidence from Chinese non-tradable share reform. Journal of Corporate Finance 18(4),

782-803.

Loewenstein, G. F., Weber, E. U., Hsee, C. K., Welch, N., (2001). Risk as feelings.

Psychological Bulletin 127(2), 267.

Margaritis, D., Psillake, M., (2010). Capital structure, equity ownership and firm

performance. Journal of Banking & Finance 34(3), 621-632.

Mayers, D., (1973). Nonmarketable assets and the determination of capital asset prices in the

absence of a riskless asset. Journal of Business 46(2), 258-267.

Moosa, I., Ramiah, V., (2014). The Costs and Benefits of Environmental Regulation.

Cheltenham, Edward Elgar.

Offenberg, D., (2009). Firm size and the effectiveness of the market for corporate control.

Journal of Corporate Finance 15(1), 66-79.

Opler, T. C., Titman, S., (1994). Financial distress and corporate performance. Journal of

Finance 49(3), 1015-1040.

- 34 -

Pachauri, R. K., Reisinger, A., (2007). Contribution of Working Groups I, II and III to the

Fourth Assessment Report of the Intergovernmental Panel on Climate Change.

Intergovernmental Panel on Climate Change, Geneva, Switzerland.

Peng, V. Q., Wei, K. C. J., Yang, Z., (2011). Tunneling or propping: Evidence from

connected transactions in China. Journal of Corporate Finance 17(2), 306-325.

Pham, H. N. A., Ramiah, V., Moosa, I., (2015). Are European Environmental Regulations

Excessive? MFS Conference, Greece.

Ramiah, V., Martin, B., Moosa, I., (2013). How does the stock market react to the

announcement of green policies? Journal of Banking and Finance 37(5), 1747–1758.

Ramiah, V., Morris, T., Moosa, I., Gangemi, M., Puican, L., (2016). The effects of

announcement of green policies on equity portfolios: Evidence from the United

Kingdom. Managerial Auditing Journal 31(2), 138-155.

Ramiah, V., Pichelli, J., Moosa, I. (2015a). Environmental regulation, the Obama effect and

the stock market: Some empirical results. Applied Economics 47(7), 725-738.

Ramiah, V., Pichelli, J., Moosa, I. (2015b). The effects of environmental regulation on

corporate performance: A Chinese perspective. Review of Pacific Basin Financial

Markets and Policies 18(4).

Raskin, R. N., Hall, C. S., (1979). A narcissistic personality inventory. Psychological Reports

45(2), 590-590.

Raskin, R., Shaw, R., (1988). Narcissism and the use of personal pronouns. Journal of

Personality 56(2), 393-404.

Robinson, R. B. Jr., (1982). The importance of “Outsiders” in small firm strategic planning.

The Academy of Management Journal 25(1), 80-93.

Rosenthal, S. A., Pittinsky, T. L., (2006). Narcissistic leadership. The Leadership Quarterly

17(6), 617-633.

- 35 -

Schultz, P. W., (2002). The structure of environmental concern: Concern for self, other

people, and the biosphere. Journal of Environmental Psychology 21(4), 327-339.

Sharpe, W. F., (1964). Capital asset prices: A theory of market equilibrium under conditions

of risk. Journal of Finance 19(3), 425-442.

Simonton, D. K., (1988). Presidential style: Personality, biography, and performance. Journal

of Personality and Social Psychology 55(6), 928-936.

United Nations, Department of Economic and Social Development, Energy Statistics

Yearbook. New York, United Nations Publications, 1983. Print.

United Nations, Department of Economic and Social Development, Energy Statistics

Yearbook. New York, United Nations Publications, 1984. Print.

U.S. Environmental Protection Agency, Inventory of U.S. Greenhouse Gas Emissions and

Sinks: 1990-2012. Washington, DC, National Service Center for Environmental

Publications, 2014. Print.

Veith, S., Werner, J. R., Zimmermann, J., (2009). Capital market response to emission rights

returns: Evidence from the European power sector. Energy Economics 31(4), 605-

613.

Vernon, R., (1992). Transnational corporations: Where are they coming from, where are they

headed? Transnational Corporations 1, 7–35.

Watts, R. L., (1978). Systematic ‘abnormal’ returns after quarterly earnings announcements.

Journal of Financial Economics 6(2), 127-150.

Winter, D. G., (2011). Philosopher-king or polarizing politician? A personality profile of

Barack Obama. Political Psychology 32(6), 1059-1081.

Zavala, D. A. G., Cichocka, A., Eidelson, R., Jayawickreme, N., (2009). Collective

narcissism and its social consequences. Journal of Personality and Social Psychology

97(6),1074-1096.

- 36 -

37

Table 1: Pollutants Used across Selected Sectors Sector Examples of Pollutants Used across Certain Sectors

Auto Parts Using toxic substances and contaminants in this sector

Automobiles Surface-treatment process: Waste acid, heavy metal ions Painting and baking varnish will release dutrex If coal is utilized during the manufacturing process, the

solid waste also can be another pollution source. Automobile & Parts Waste pollution and toxic substances

Cons. Durables & App. Consumer durables: Releases toxic substances Printing process leads to water pollution and releases toxic

substances. This applies to the apparel sector. Tex. & Luxury Goods Water pollution and toxic substances Hotels & Restaurants Hotels and other service sectors lead to pollution,

including noise pollution, fumes, smoke and odor pollution, light pollution of advertising signs, decorative lights and outdoor LED, and water pollution, etc.

Leisure Equipment Water pollution, solid wastes and air pollution Multiline Retail Waste pollution Retailing Waste pollution Food Beverage & Tob. Water, air and food pollution Energy Water pollution and air pollution Energy Equ. & Service Water pollution, air pollution and solid wastes Oil & Gas Products Water pollution and air pollution Real Estate Air, noise, water pollution and solid wastes Building Products Air, noise, water pollution and solid wastes Cons. & Engineering Air, noise, water pollution and solid wastes Biotechnology Releasing chemical wastes. Health care Such services assist individuals to maintain their health.

Revenues and stock returns of these sectors decrease when individuals are healthier.

Waste pollution Pharmaceuticals Waste pollution Aerospace & Defense These sectors generate dust, sulfured, nitrogen oxides, and

carbon monoxide and lead to solid wastes, water pollution and air pollution.

Air Freight & Logistics Solid wastes, water pollution and air pollution Marine Solid wastes, water pollution and air pollution Road & Rail Solid wastes, water pollution and air pollution Transportation Solid wastes, noise pollution and air pollution

38

Table 2: Classification of Selected Sectors Sector First Definition Second Definition

Polluters Environment

ally Friendly Polluters Environment

ally Friendly Automobile and Parts Yes Yes

Banks Yes Yes Beverage Yes Yes

Chemical Yes Yes

Construction and Material Yes Yes

Electricity Yes Yes

Electrical Equipment Yes Yes Financial Services Yes Yes Telecommunications Yes Yes

Food and Drug Retailers Yes Yes

Food Producers Yes Yes

Forestry and Papers Yes Yes

Multi–Utilities Yes Yes

Healthcare Equipment Yes Yes

Household Goods Yes Yes

Life Insurance Yes Yes Media Yes Yes Mining Yes Yes

Mobile Telecommunication Yes Yes

Non–Life Insurance Yes Yes Oil and Gas Producers Yes Yes

Personal Goods Yes Yes

Pharmaceutical Yes Yes

Real Estate Yes Yes Software Yes Yes Travel Leisure Yes Yes

39

Table 3: Summary Statistics and t–Test of Difference in Means between the United States and Australia

United States Australia t-Test of Difference

United States vs. Australia Variable Obs Mean Min Max Obs Mean Min Max Difference t–Statistics Effectivea 21060 0.4390 0.0000 1.0000 5645 0.3933 0.0000 1.0000 0.0457*** 11.81 Effectiveb 21060 0.4379 0.0000 1.0000 5645 0.3919 0.0000 1.0000 0.0460*** 11.84 Effectivec 21060 0.4364 0.0000 1.0000 5645 0.3944 0.0000 1.0000 0.0421*** 10.83 Effectived 21060 0.4367 0.0000 1.0000 5645 0.3926 0.0000 1.0000 0.0441*** 11.36 AR 20956 0.0000 -0.1502 0.1372 5645 -0.0001 -0.2884 0.0981 0.0001 0.58 CARb 20956 0.0001 -0.3128 0.2290 5645 -0.0001 -0.3333 0.3107 0.0002 0.61 CARc 20956 -0.0001 -0.4381 0.3285 5645 -0.0008 -0.7196 0.3590 0.0007 1.07 CARd 20956 -0.0001 -0.4081 0.5264 5645 -0.0009 -0.5902 0.6128 0.0007 0.89 Narcissism 21060 1.2761 0.1400 3.1021 5649 0.9618 0.2418 2.1749 0.3143*** 34.85 Size 20956 9.4553 4.1151 11.5785 5649 8.0387 2.9069 11.1595 1.4166*** 93.20 Profitability 20956 0.1917 -0.1083 9.5217 5554 0.0738 -2.6138 4.3626 0.1180*** 11.02 CAPEX 20956 1.8119 -0.3682 18.9747 5554 0.7410 -0.5024 38.1557 1.1690*** 37.24 Leverage 20956 0.9581 -50.5763 94.6910 5554 0.6429 -5.5668 19.3112 0.2171*** 2.97 STO 21060 0.3630 0.0000 1.0000 5649 0.2669 0.0000 1.0000 0.0960*** 13.55

*** indicates the significance at the 1% level. a, b, c, d refers to the event window (0,0), (-1, +1), (-5, +5) and (-10, +10).

40

Table 4: American and Australian Green Effects AR CARa CARb CARc United States Airlines (P) -0.06 -0.06 -0.37 -0.76 Automobiles (P) -0.02 0.02 -0.04 -0.00 Banks (E) -0.08 -0.16 -0.32 -0.58 Diversified Financials (E) 0.03 0.08 0.12 0.12 Electrical Equipment (P) 0.01 0.02 -0.04 -0.09 Food Products (P) -0.01 -0.03 0.13 0.15 Household Durables (P) 0.06 0.11 0.02 0.03 Information Technology (E) 0.02 0.03 -0.08 -0.05 Paper Packaging (P) 0.04 0.12 0.13 0.13 Telecommunications Services (P) -0.00 -0.04 -0.06 -0.02 Transportation (P) -0.01 0.03 -0.10 -0.21 Australia Automobiles (P) 1.19 0.14 0.86 0.25 Banks (E) -0.68 -0.08 -0.19 -0.27 Household Durables (P) -0.99 -0.32 -0.46 0.02 Diversified Financials (E) 0.66 -0.10 -0.10 -0.49 Diversified Industries (P) -0.25 -0.04 0.44 0.70 Energy (P) 0.87 -0.06 -0.02 -0.42 Food Beverage and Tobacco (P) -0.18 0.16 -0.04 -0.14 Information Technology (E) 2.16 0.24 0.44 0.33 Insurance (E) 1.09 0.09 -0.11 0.12 Media (M) 0.16 -0.08 0.06 0.33 Paper Packaging (P) -0.22 0.01 -0.54 0.04 Technique Hardware & Equity (P) 6.58 -0.10 -1.32 -0.92 Telecommunications Services (P) -1.53 -0.16 -0.51 -0.75 Transportation (P) 0.04 -0.11 -0.17 -1.05 Utilities (P) -0.71 0.08 -0.24 -0.10

a, b, c refers to the event window (-1, +1), (-5, +5) and (-10, +10) respectively. P=Polluter, E=Environmentally Friendly and M=mixed sector.

41

Table 5: Robustness of Effectiveness Scores Using AR United States Australia All Sectors 0.4389* 0.3933 (1.69) (1.58)

Polluters 0.4629*** 0.3955*** (4.56) (5.56) Food Products 0.4718** 0.2667* (2.25) (1.74) Healthcare 0.4716** 0.3225*** (2.29) (2.79) Household Durable 0.4752** 0.5556 (1.98) (1.11) Paper Packaging 0.4907 0.4846 (1.27) (1.34) Telecommunication Services 0.4960* 0.4247** (1.89) (2.41) Transportation 0.4376** 0.4130** (2.05) (2.11) Utilities 0.5006* 0.4259 (1.79) (1.44) Technical Hardware and Equity N/A 0.1173 N/A (0.55)

Environmentally Friendly Sectors 0.4212*** 0.3658*** (3.65) (3.80) Bank 0.4710* 0.3652** (1.74) (2.12) Information Technology 0.3585** 0.4105 (2.14) (1.59) Insurance 0.4295** 0.3563* (2.07) (1.94)

Mixed Sectors 0.4194*** 0.3833*** (2.59) (5.95) Media 0.3652*** 0.4040*** (2.58) (4.17) Real Estate 0.4520* 0.4105*** (1.95) (2.78) *, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

42

Table 6: Factors Affecting Effectiveness Scores. (t statistics in parentheses)

United States Australia Effectivea Effectiveb Effectivec Effectived Effectivea Effectiveb Effectivec Effectived Narcissism -0.0085 -0.0105* -0.0120** -0.0143** 0.0051 0.0080 0.0046 -0.0130 (-1.50) (-1.85) (-2.11) (-2.47) (0.33) (0.55) (0.30) (-0.85) Size 0.0252*** 0.0259*** 0.0291*** 0.0295*** 0.0307*** 0.0255*** 0.0397*** 0.0459*** (5.60) (5.64) (6.38) (6.43) (3.78) (3.26) (5.06) (6.04) Profitability 0.0005 -0.0038 -0.0063*** -0.0042* 0.0018 0.0032 0.0007 0.0029 (0.23) (-1.54) (-2.65) (-1.72) (0.37) (0.61) (0.13) (0.63) CAPEX -0.0029** -0.0031** -0.0053*** -0.0039*** 0.0068*** 0.0065*** 0.0063*** 0.0098*** (-2.30) (-2.41) (-4.12) (-3.13) (4.69) (4.82) (4.30) (6.96) Leverage 0.0000 0.0004 0.0004 0.0009*** -0.0055** -0.0010 0.0005 -0.0039 (0.17) (1.19) (1.36) (2.95) (-2.15) (-0.34) (0.21) (-1.14) STO 0.0068 0.0074 0.0032 -0.0055 0.0538*** 0.0624*** 0.0810*** 0.0687***

(1.42) (1.52) (0.67) (-1.14) (4.45) (5.28) (6.78) (5.84) Fixed-Effects Leaders Yes Yes Yes Yes Yes Yes Yes Yes Sectors Yes Yes Yes Yes Yes Yes Yes Yes R-squared 0.0772 0.0762 0.0769 0.0786 0.0962 0.0948 0.1108 0.1021

a, b, c, d refer to the dependent variable when measured by AR, CAR (-1, +1), CAR (-5, +5) and CAR (-10, +10) respectively. *, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

43

Table 7: Factors affecting Green Effects (t statistics in parentheses) United States Australia AR CARa CARb CARc AR CARa CARb CARc Narcissism 0.0004* 0.0010** 0.0021*** 0.0036*** 0.0030*** 0.0008 0.0116*** 0.0174*** (1.68) (2.37) (2.72) (3.35) (4.02) (0.68) (4.07) (4.22) Size 0.0003 -0.0010* -0.0053*** -0.0091*** 0.0001 0.0002 -0.0040*** -0.0054*** (1.08) (-1.94) (-5.39) (-6.31) (0.17) (0.32) (-2.95) (-2.80) Profitability 0.0002 0.0004 0.0009 0.0010 0.0002 0.0003 0.0032** 0.0030 (0.72) (1.26) (1.57) (1.38) (0.38) (0.28) (2.03) (1.61) CAPEX -0.0001 -0.0001 0.0002 0.0004 0.0002 0.0000 -0.0003 -0.0010** (-1.08) (-0.62) (0.52) (1.02) (1.39) (0.02) (-0.81) (-2.21) Leverage 0.0000 0.0000 -0.0001 -0.0003*** -0.0001 -0.0006** -0.0012** -0.0014* (1.38) (0.31) (-1.30) (-3.21) (-0.72) (-2.04) (-2.26) (-1.88) STO 0.0001 0.0009** 0.0041*** 0.0070*** 0.0005 -0.0005 -0.0012 0.0009

(0.68) (2.35) (5.76) (7.22) (0.85) (-0.53) (-0.56) (0.29) Fixed-Effects Leaders No Yes Yes Yes No Yes No Yes Sectors Yes Yes Yes Yes Yes No Yes Yes R-squared 0.0018 0.0024 0.0075 0.0132 0.0121 0.0079 0.0217 0.0180

a, b, c refers to the event window of (-1, +1), (-5, +5) and (-10, +10) respectively. *, **, and *** indicate significance at the 10%, 5%, and 1% levels, respectively.

- 44 -

Table A1: Descriptive Statistics of Narcissism Ratios When Leaders are in Power

Period Party Mean Median SD US

George H. Bush 1989-1993 Republican 2.0944 1.3750 2.6967 Bill Clinton 1993-2001 Democratic 0.5261 0.4881 0.3372

George W. Bush 2001-2009 Republican 1.2335 1.0458 0.8428 Barack Obama 2009-2015 Democratic 0.7526 0.6748 0.5524

Australia

Paul Keating 1991-1996 Labor 0.5659 0.4737 0.1543 John Howard 1996-2007 Liberal 1.1628 0.9857 0.8228 Kevin Rudd 2007-2010 Labor 0.6004 0.5000 0.3383 Julia Gillard 2010-2013 Labor 0.7528 0.6079 0.6302 Kevin Rudd 2013-2013 Labor 0.6004 0.5000 0.3383 Tony Abbott 2013-2015 Liberal 0.6096 0.5000 0.5852

45

Table A2: Factors Affecting Narcissism Panel A. Correlation between Narcissism and Related Factors Correlation Narcissism Culture (Individualism) -0.0212 Duration 0.1319 Party–Centred Dummy 0.5956 Panel B. Regression between Narcissism and Related Factors Independent Variable Coefficients Culture (Individualism) -0.0032 t statistics (-1.14) Duration -0.0240 t statistics (-1.04) Party–Centred Dummy 0.7626 t statistics (5.01)

R-squared 0.3917

- 46 -

Table A3: Narcissism Ratios Calculated for Leaders Before, During and Post Candidature US Australia

George H. Bush

Bill Clinton

George W. Bush

Barack Obama

Paul Keating

John Howard

Kevin Rudd

Julia Gillard

Tony Abbott