European Insurers Insurance The Magnificent Seven ... · The Magnificent Seven; Initiating on...

116

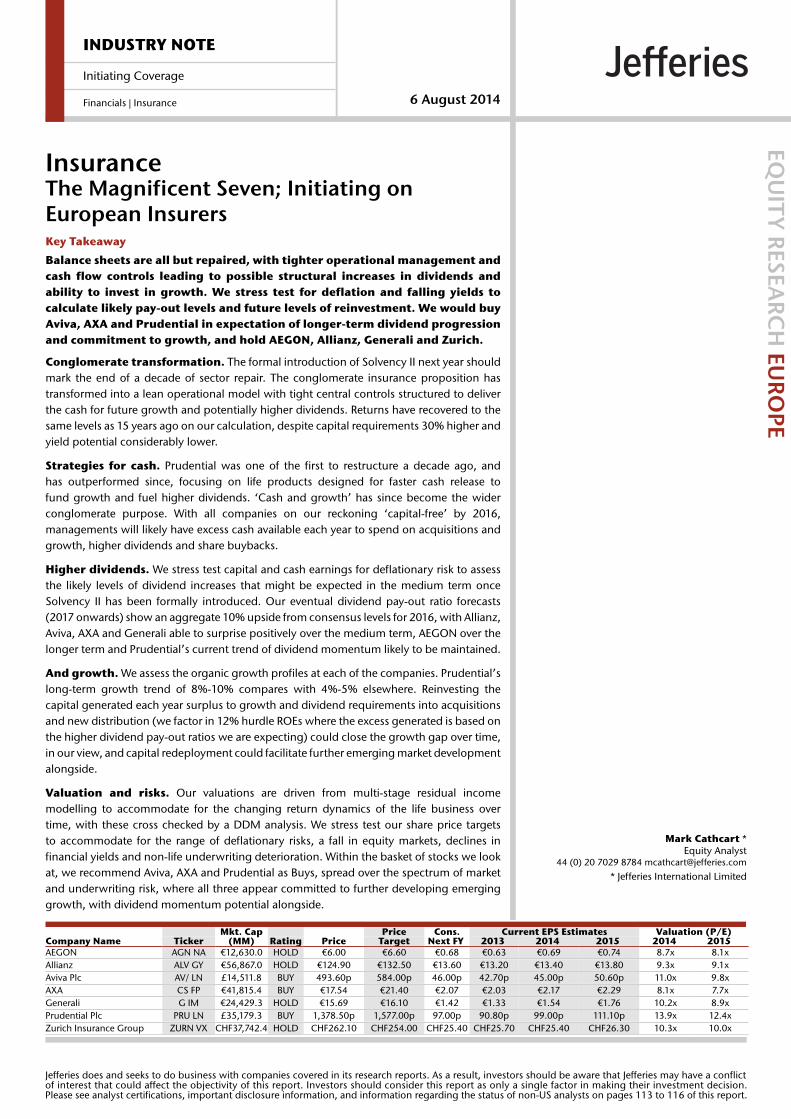

Mkt. Cap Price Cons. Current EPS Estimates Valuation (P/E) Company Name Ticker (MM) Rating Price Target Next FY 2013 2014 2015 2014 2015 AEGON AGN NA €12,630.0 HOLD €6.00 €6.60 €0.68 €0.63 €0.69 €0.74 8.7x 8.1x Allianz ALV GY €56,867.0 HOLD €124.90 €132.50 €13.60 €13.20 €13.40 €13.80 9.3x 9.1x Aviva Plc AV/ LN £14,511.8 BUY 493.60p 584.00p 46.00p 42.70p 45.00p 50.60p 11.0x 9.8x AXA CS FP €41,815.4 BUY €17.54 €21.40 €2.07 €2.03 €2.17 €2.29 8.1x 7.7x Generali G IM €24,429.3 HOLD €15.69 €16.10 €1.42 €1.33 €1.54 €1.76 10.2x 8.9x Prudential Plc PRU LN £35,179.3 BUY 1,378.50p 1,577.00p 97.00p 90.80p 99.00p 111.10p 13.9x 12.4x Zurich Insurance Group ZURN VX CHF37,742.4 HOLD CHF262.10 CHF254.00 CHF25.40 CHF25.70 CHF25.40 CHF26.30 10.3x 10.0x INDUSTRY NOTE Initiating Coverage Financials | Insurance 6 August 2014 Insurance The Magnificent Seven; Initiating on European Insurers EQUITY RESEARCH EUROPE Mark Cathcart * Equity Analyst 44 (0) 20 7029 8784 [email protected] * Jefferies International Limited Key Takeaway Balance sheets are all but repaired, with tighter operational management and cash flow controls leading to possible structural increases in dividends and ability to invest in growth. We stress test for deflation and falling yields to calculate likely pay-out levels and future levels of reinvestment. We would buy Aviva, AXA and Prudential in expectation of longer-term dividend progression and commitment to growth, and hold AEGON, Allianz, Generali and Zurich. Conglomerate transformation. The formal introduction of Solvency II next year should mark the end of a decade of sector repair. The conglomerate insurance proposition has transformed into a lean operational model with tight central controls structured to deliver the cash for future growth and potentially higher dividends. Returns have recovered to the same levels as 15 years ago on our calculation, despite capital requirements 30% higher and yield potential considerably lower. Strategies for cash. Prudential was one of the first to restructure a decade ago, and has outperformed since, focusing on life products designed for faster cash release to fund growth and fuel higher dividends. ‘Cash and growth’ has since become the wider conglomerate purpose. With all companies on our reckoning ‘capital-free’ by 2016, managements will likely have excess cash available each year to spend on acquisitions and growth, higher dividends and share buybacks. Higher dividends. We stress test capital and cash earnings for deflationary risk to assess the likely levels of dividend increases that might be expected in the medium term once Solvency II has been formally introduced. Our eventual dividend pay-out ratio forecasts (2017 onwards) show an aggregate 10% upside from consensus levels for 2016, with Allianz, Aviva, AXA and Generali able to surprise positively over the medium term, AEGON over the longer term and Prudential’s current trend of dividend momentum likely to be maintained. And growth. We assess the organic growth profiles at each of the companies. Prudential’s long-term growth trend of 8%-10% compares with 4%-5% elsewhere. Reinvesting the capital generated each year surplus to growth and dividend requirements into acquisitions and new distribution (we factor in 12% hurdle ROEs where the excess generated is based on the higher dividend pay-out ratios we are expecting) could close the growth gap over time, in our view, and capital redeployment could facilitate further emerging market development alongside. Valuation and risks. Our valuations are driven from multi-stage residual income modelling to accommodate for the changing return dynamics of the life business over time, with these cross checked by a DDM analysis. We stress test our share price targets to accommodate for the range of deflationary risks, a fall in equity markets, declines in financial yields and non-life underwriting deterioration. Within the basket of stocks we look at, we recommend Aviva, AXA and Prudential as Buys, spread over the spectrum of market and underwriting risk, where all three appear committed to further developing emerging growth, with dividend momentum potential alongside. Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 113 to 116 of this report.

Transcript of European Insurers Insurance The Magnificent Seven ... · The Magnificent Seven; Initiating on...

Mkt. Cap Price Cons. Current EPS Estimates Valuation (P/E)Company Name Ticker (MM) Rating Price Target Next FY 2013 2014 2015 2014 2015 AEGON AGN NA €12,630.0 HOLD €6.00 €6.60 €0.68 €0.63 €0.69 €0.74 8.7x 8.1xAllianz ALV GY €56,867.0 HOLD €124.90 €132.50 €13.60 €13.20 €13.40 €13.80 9.3x 9.1xAviva Plc AV/ LN £14,511.8 BUY 493.60p 584.00p 46.00p 42.70p 45.00p 50.60p 11.0x 9.8xAXA CS FP €41,815.4 BUY €17.54 €21.40 €2.07 €2.03 €2.17 €2.29 8.1x 7.7xGenerali G IM €24,429.3 HOLD €15.69 €16.10 €1.42 €1.33 €1.54 €1.76 10.2x 8.9xPrudential Plc PRU LN £35,179.3 BUY 1,378.50p 1,577.00p 97.00p 90.80p 99.00p 111.10p 13.9x 12.4xZurich Insurance Group ZURN VX CHF37,742.4 HOLD CHF262.10 CHF254.00 CHF25.40 CHF25.70 CHF25.40 CHF26.30 10.3x 10.0x

INDUSTRY NOTE

Initiating Coverage

Financials | Insurance 6 August 2014

InsuranceThe Magnificent Seven; Initiating onEuropean Insurers

EQU

ITY R

ESEARC

H EU

ROPE

Mark Cathcart *Equity Analyst

44 (0) 20 7029 8784 [email protected]

* Jefferies International Limited

Key Takeaway

Balance sheets are all but repaired, with tighter operational management andcash flow controls leading to possible structural increases in dividends andability to invest in growth. We stress test for deflation and falling yields tocalculate likely pay-out levels and future levels of reinvestment. We would buyAviva, AXA and Prudential in expectation of longer-term dividend progressionand commitment to growth, and hold AEGON, Allianz, Generali and Zurich.

Conglomerate transformation. The formal introduction of Solvency II next year shouldmark the end of a decade of sector repair. The conglomerate insurance proposition hastransformed into a lean operational model with tight central controls structured to deliverthe cash for future growth and potentially higher dividends. Returns have recovered to thesame levels as 15 years ago on our calculation, despite capital requirements 30% higher andyield potential considerably lower.

Strategies for cash. Prudential was one of the first to restructure a decade ago, andhas outperformed since, focusing on life products designed for faster cash release tofund growth and fuel higher dividends. ‘Cash and growth’ has since become the widerconglomerate purpose. With all companies on our reckoning ‘capital-free’ by 2016,managements will likely have excess cash available each year to spend on acquisitions andgrowth, higher dividends and share buybacks.

Higher dividends. We stress test capital and cash earnings for deflationary risk to assessthe likely levels of dividend increases that might be expected in the medium term onceSolvency II has been formally introduced. Our eventual dividend pay-out ratio forecasts(2017 onwards) show an aggregate 10% upside from consensus levels for 2016, with Allianz,Aviva, AXA and Generali able to surprise positively over the medium term, AEGON over thelonger term and Prudential’s current trend of dividend momentum likely to be maintained.

And growth. We assess the organic growth profiles at each of the companies. Prudential’slong-term growth trend of 8%-10% compares with 4%-5% elsewhere. Reinvesting thecapital generated each year surplus to growth and dividend requirements into acquisitionsand new distribution (we factor in 12% hurdle ROEs where the excess generated is based onthe higher dividend pay-out ratios we are expecting) could close the growth gap over time,in our view, and capital redeployment could facilitate further emerging market developmentalongside.

Valuation and risks. Our valuations are driven from multi-stage residual incomemodelling to accommodate for the changing return dynamics of the life business overtime, with these cross checked by a DDM analysis. We stress test our share price targetsto accommodate for the range of deflationary risks, a fall in equity markets, declines infinancial yields and non-life underwriting deterioration. Within the basket of stocks we lookat, we recommend Aviva, AXA and Prudential as Buys, spread over the spectrum of marketand underwriting risk, where all three appear committed to further developing emerginggrowth, with dividend momentum potential alongside.

Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflictof interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 113 to 116 of this report.

Executive Summary The conglomerate proposition has vastly improved: corporate governance,

franchise focus, and an attractive cash and return profile despite the higher

capital demands from Solvency II. Prudential has demonstrated to the market

over the past decade the benefits of investing in growth with products

designed to quickly release the cash, and has been extensively re-rated

because of it. With the wider conglomerate insurance sector on the cusp of

capital recovery, we explore the prospects for growth and higher dividend

pay-out ratios at the other companies. We assess earnings growth potential,

both organic and acquired, and stress test for deflation to construct the likely

pay-out levels for each company. Our Buy-rated stocks – Aviva, AXA and

Prudential – are spread over the spectrum of market and underwriting risk,

where all three appear committed to emerging growth, with dividend

momentum potential alongside.

In this note, we initiate coverage on seven major European insurers, with Buy

ratings on Aviva, AXA and Prudential, and Hold ratings on AEGON, Allianz,

Generali and Zurich.

Sector repair. The formal introduction of Solvency II next year will mark the

denouement of a decade of sector repair for a group of companies that, after years of

mega acquiring, had found themselves woefully undercapitalised in the sequence of

financial collapses that followed. See Appendix, The Conglomer-creation.

Operational transformation. Today the conglomerate insurance proposition has

transformed, a lean operational model with tight central controls structured specifically to

deliver the cash in the form of dividends, with life products designed for faster cash

release to fund future growth. See later section, Corporate Assessment, for a full overview.

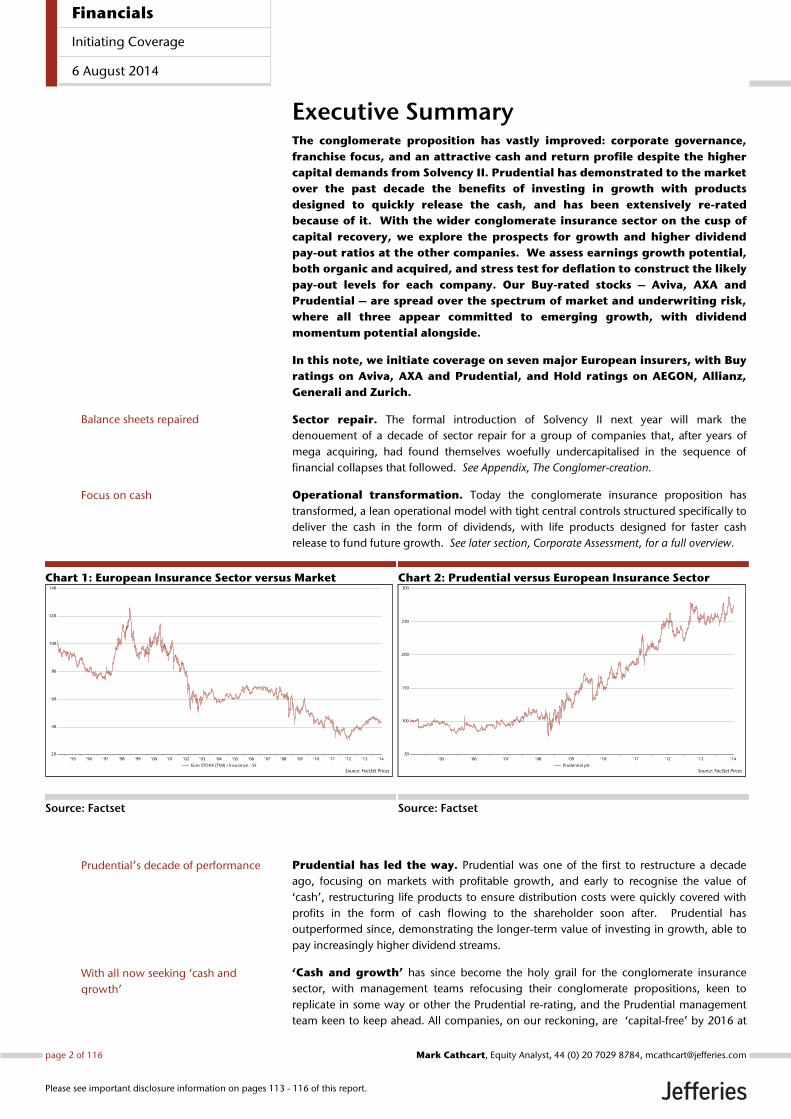

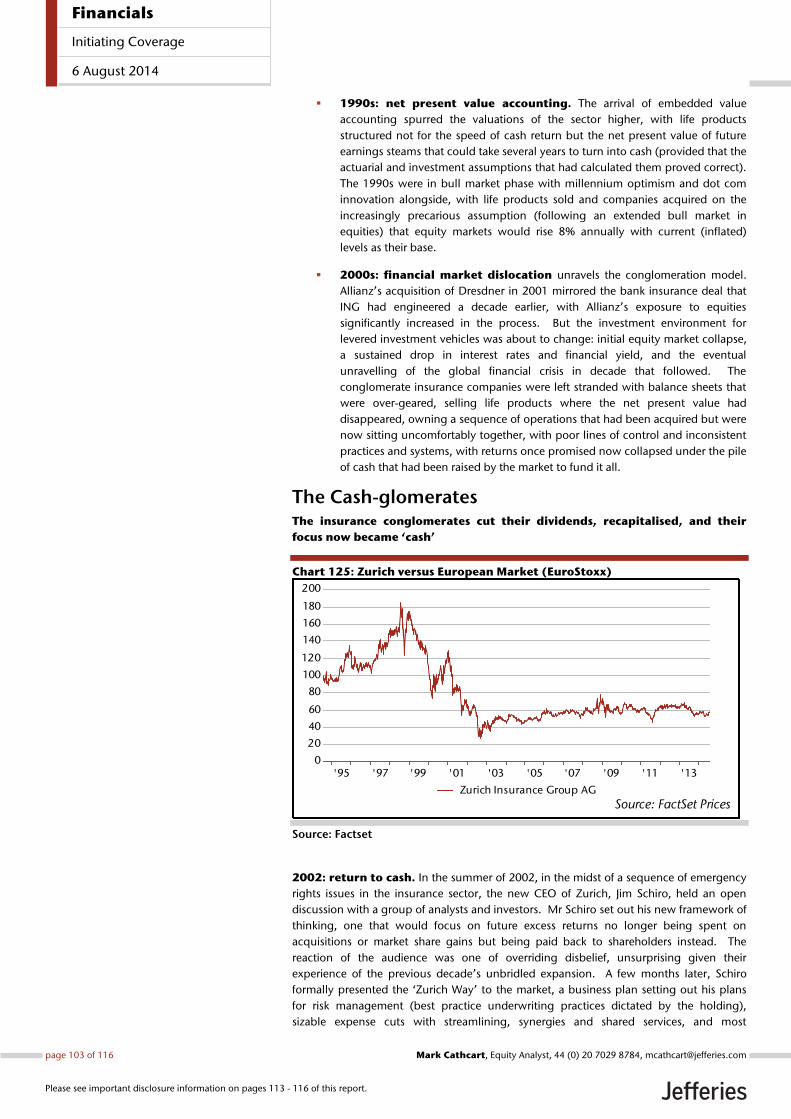

Chart 1: European Insurance Sector versus Market

Source: Factset

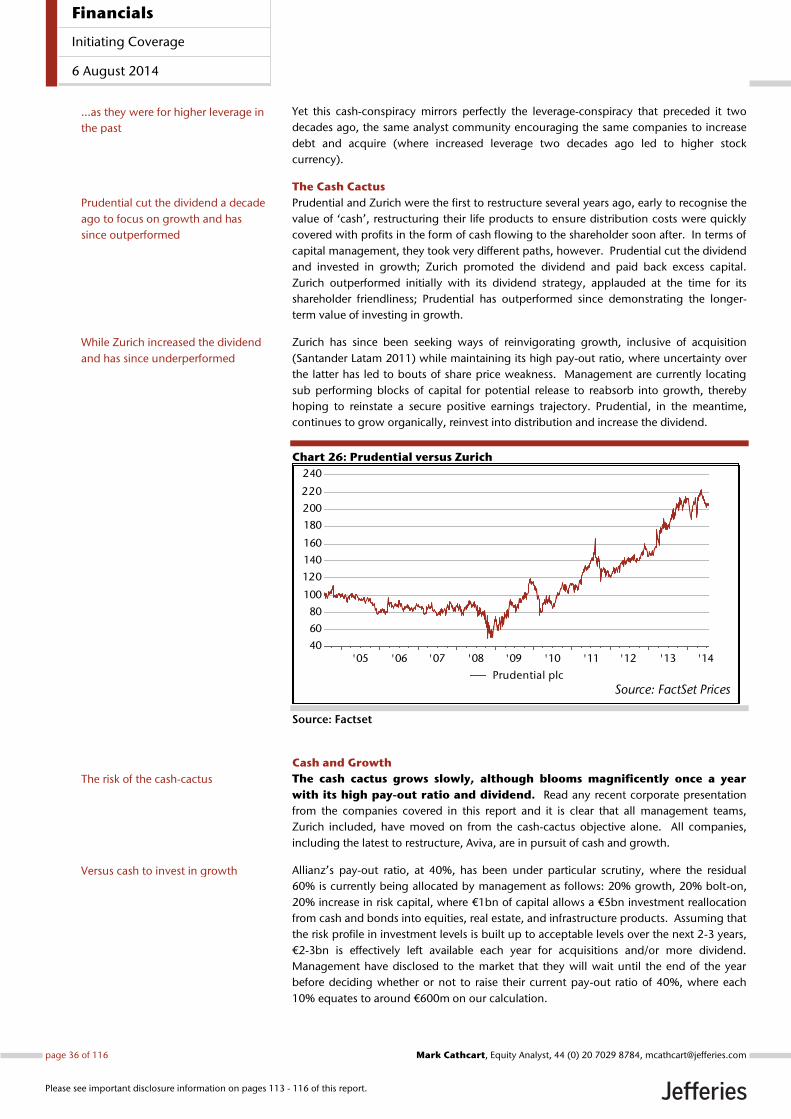

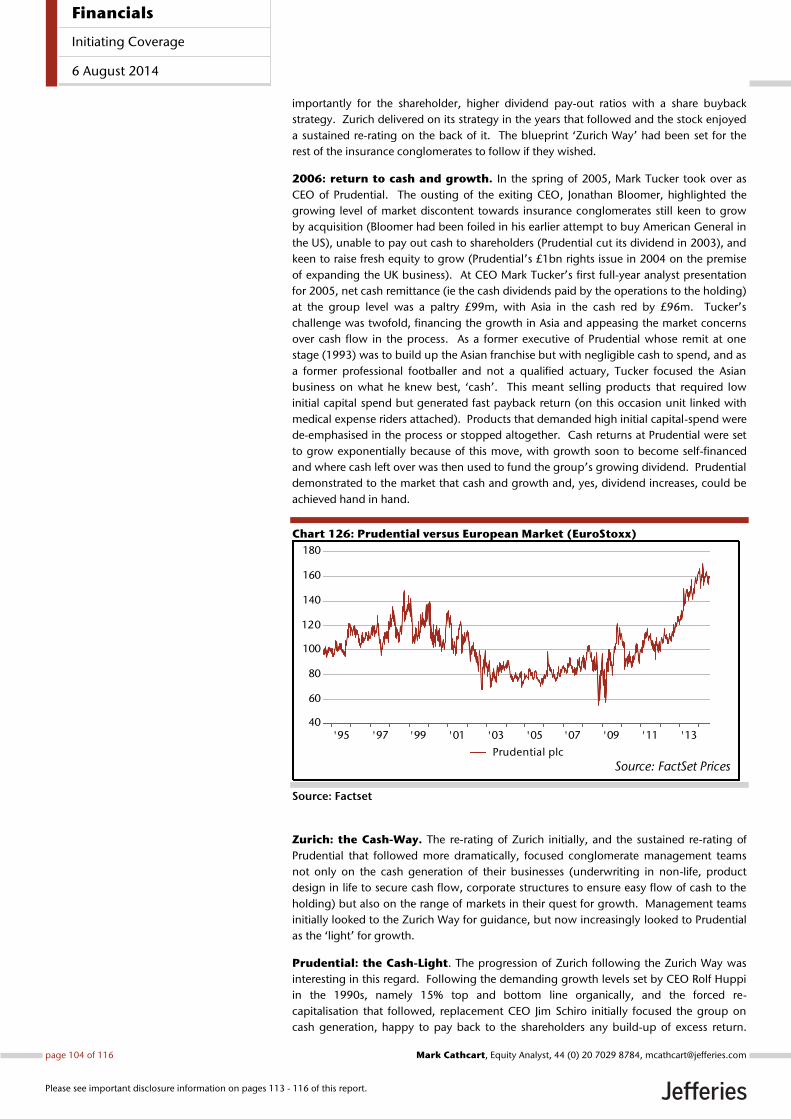

Chart 2: Prudential versus European Insurance Sector

Source: Factset

Prudential has led the way. Prudential was one of the first to restructure a decade

ago, focusing on markets with profitable growth, and early to recognise the value of

‘cash’, restructuring life products to ensure distribution costs were quickly covered with

profits in the form of cash flowing to the shareholder soon after. Prudential has

outperformed since, demonstrating the longer-term value of investing in growth, able to

pay increasingly higher dividend streams.

‘Cash and growth’ has since become the holy grail for the conglomerate insurance

sector, with management teams refocusing their conglomerate propositions, keen to

replicate in some way or other the Prudential re-rating, and the Prudential management

team keen to keep ahead. All companies, on our reckoning, are ‘capital-free’ by 2016 at

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '1420

40

60

80

100

120

140

Source: FactSet PricesEuro STOXX (TMI) / Insurance - SS

'05 '06 '07 '08 '09 '10 '11 '12 '13 '1450

100

150

200

250

300

Source: FactSet PricesPrudential plc

Balance sheets repaired

Focus on cash

Prudential’s decade of performance

With all now seeking ‘cash and

growth’

Financials

Initiating Coverage

6 August 2014

page 2 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

the latest with free cash generated no longer required to shore up capital or pay down

debt, available instead for acquisitions and growth alongside dividends and share

buybacks. See later sections, Corporate Assessment: Growth, Cash, Dividend.

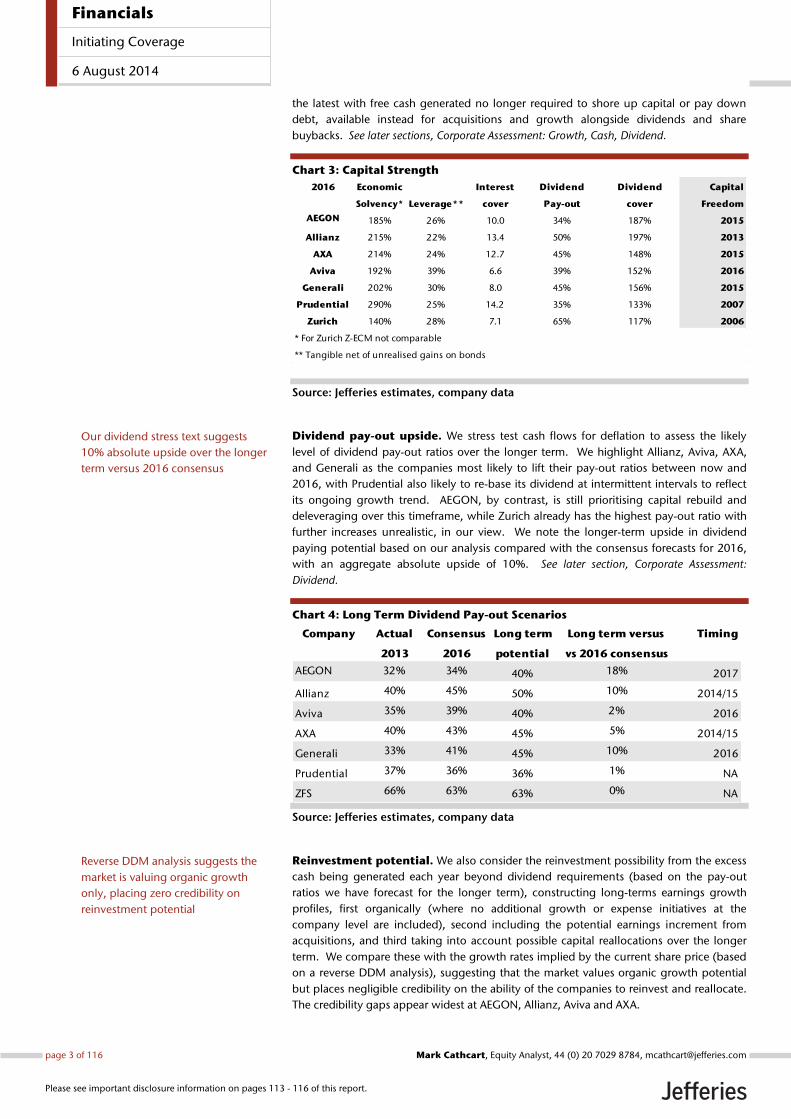

Chart 3: Capital Strength

Source: Jefferies estimates, company data

Dividend pay-out upside. We stress test cash flows for deflation to assess the likely

level of dividend pay-out ratios over the longer term. We highlight Allianz, Aviva, AXA,

and Generali as the companies most likely to lift their pay-out ratios between now and

2016, with Prudential also likely to re-base its dividend at intermittent intervals to reflect

its ongoing growth trend. AEGON, by contrast, is still prioritising capital rebuild and

deleveraging over this timeframe, while Zurich already has the highest pay-out ratio with

further increases unrealistic, in our view. We note the longer-term upside in dividend

paying potential based on our analysis compared with the consensus forecasts for 2016,

with an aggregate absolute upside of 10%. See later section, Corporate Assessment:

Dividend.

Chart 4: Long Term Dividend Pay-out Scenarios

Source: Jefferies estimates, company data

Reinvestment potential. We also consider the reinvestment possibility from the excess

cash being generated each year beyond dividend requirements (based on the pay-out

ratios we have forecast for the longer term), constructing long-terms earnings growth

profiles, first organically (where no additional growth or expense initiatives at the

company level are included), second including the potential earnings increment from

acquisitions, and third taking into account possible capital reallocations over the longer

term. We compare these with the growth rates implied by the current share price (based

on a reverse DDM analysis), suggesting that the market values organic growth potential

but places negligible credibility on the ability of the companies to reinvest and reallocate.

The credibility gaps appear widest at AEGON, Allianz, Aviva and AXA.

2016 Economic Interest Dividend Dividend Capital

Solvency* Leverage** cover Pay-out cover Freedom

AEGON 185% 26% 10.0 34% 187% 2015

Allianz 215% 22% 13.4 50% 197% 2013

AXA 214% 24% 12.7 45% 148% 2015

Aviva 192% 39% 6.6 39% 152% 2016

Generali 202% 30% 8.0 45% 156% 2015

Prudential 290% 25% 14.2 35% 133% 2007

Zurich 140% 28% 7.1 65% 117% 2006

* For Zurich Z-ECM not comparable

** Tangible net of unrealised gains on bonds

Company Actual Consensus Long term Long term versus Timing

2013 2016 potential vs 2016 consensus

AEGON 32% 34% 40% 18% 2017

Allianz 40% 45% 50% 10% 2014/15

Aviva 35% 39% 40% 2% 2016

AXA 40% 43% 45% 5% 2014/15

Generali 33% 41% 45% 10% 2016

Prudential 37% 36% 36% 1% NA

ZFS 66% 63% 63% 0% NA

Our dividend stress text suggests

10% absolute upside over the longer

term versus 2016 consensus

Reverse DDM analysis suggests the

market is valuing organic growth

only, placing zero credibility on

reinvestment potential

Financials

Initiating Coverage

6 August 2014

page 3 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

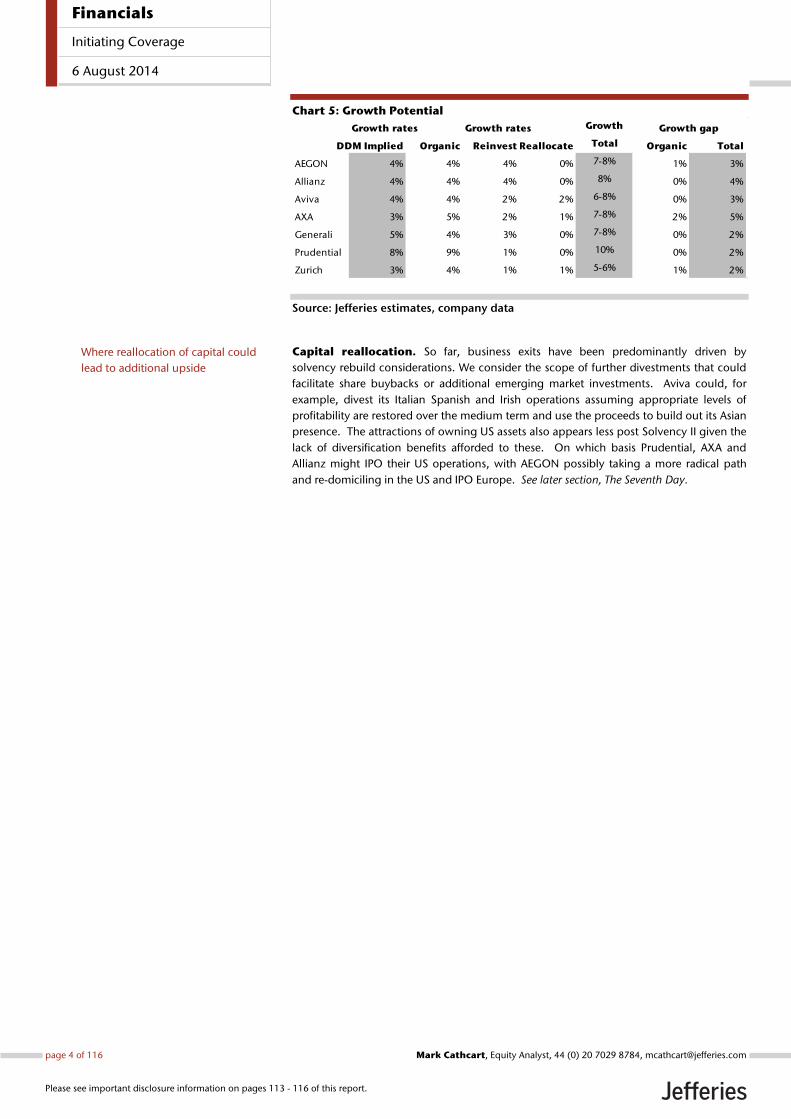

Chart 5: Growth Potential

Source: Jefferies estimates, company data

Capital reallocation. So far, business exits have been predominantly driven by

solvency rebuild considerations. We consider the scope of further divestments that could

facilitate share buybacks or additional emerging market investments. Aviva could, for

example, divest its Italian Spanish and Irish operations assuming appropriate levels of

profitability are restored over the medium term and use the proceeds to build out its Asian

presence. The attractions of owning US assets also appears less post Solvency II given the

lack of diversification benefits afforded to these. On which basis Prudential, AXA and

Allianz might IPO their US operations, with AEGON possibly taking a more radical path

and re-domiciling in the US and IPO Europe. See later section, The Seventh Day.

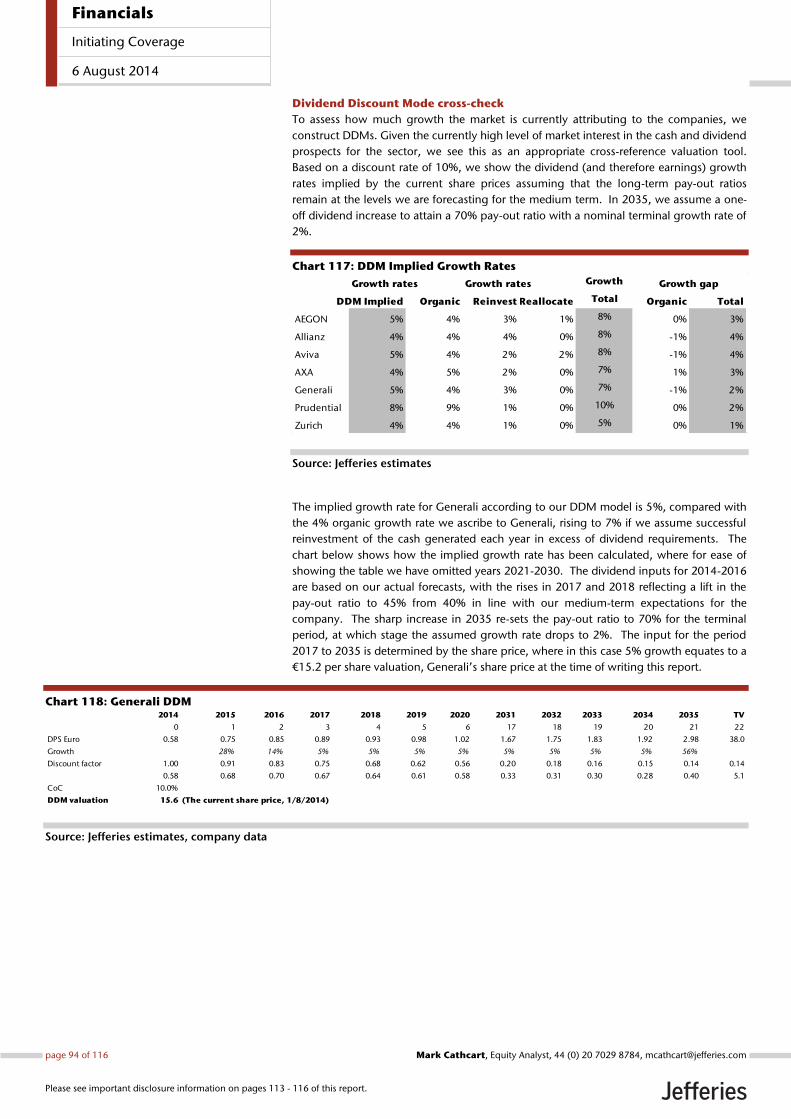

Growth rates Growth rates Growth Growth gap

DDM Implied Organic Reinvest Reallocate Total Organic Total

AEGON 4% 4% 4% 0% 7-8% 1% 3%

Allianz 4% 4% 4% 0% 8% 0% 4%

Aviva 4% 4% 2% 2% 6-8% 0% 3%

AXA 3% 5% 2% 1% 7-8% 2% 5%

Generali 5% 4% 3% 0% 7-8% 0% 2%

Prudential 8% 9% 1% 0% 10% 0% 2%

Zurich 3% 4% 1% 1% 5-6% 1% 2%

Where reallocation of capital could

lead to additional upside

Financials

Initiating Coverage

6 August 2014

page 4 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

Recommendations To participate in the potential re-rating of the conglomerates in the run up to the

completion of Solvency II, we focus our conglomerate recommendations on companies

where dividend and growth strategies are likely to lead to longer-term re-ratings. To

reflect the uncertain economic outlook (deflation versus reflation), our recommendations

are spread across the spectrum of financial market risk.

Below we summarise our recommendations, with emphasis on the Buy-rated names:

Aviva, AXA and Prudential.

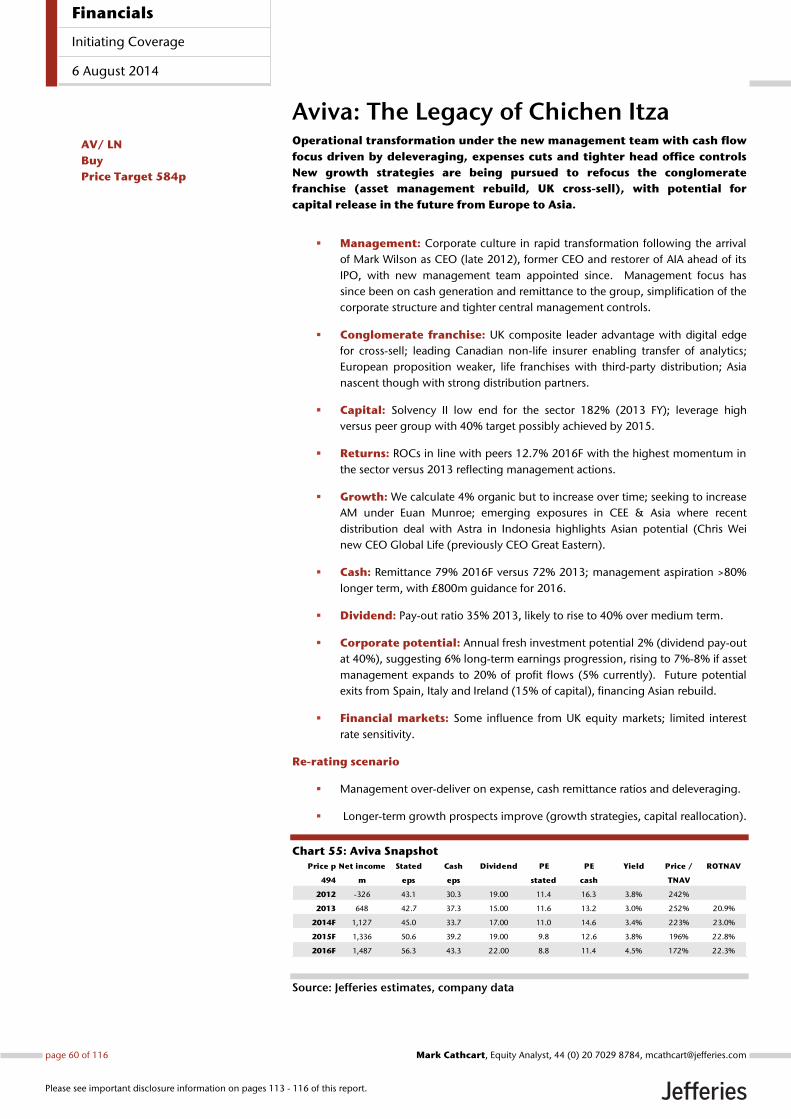

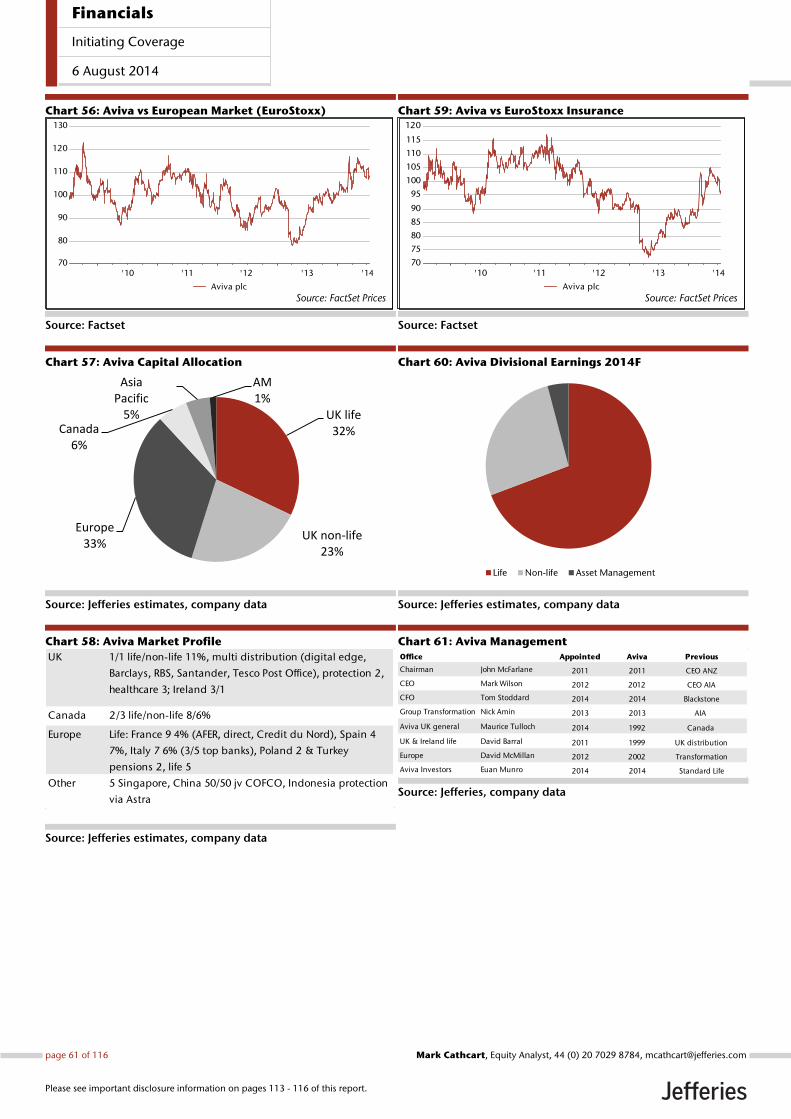

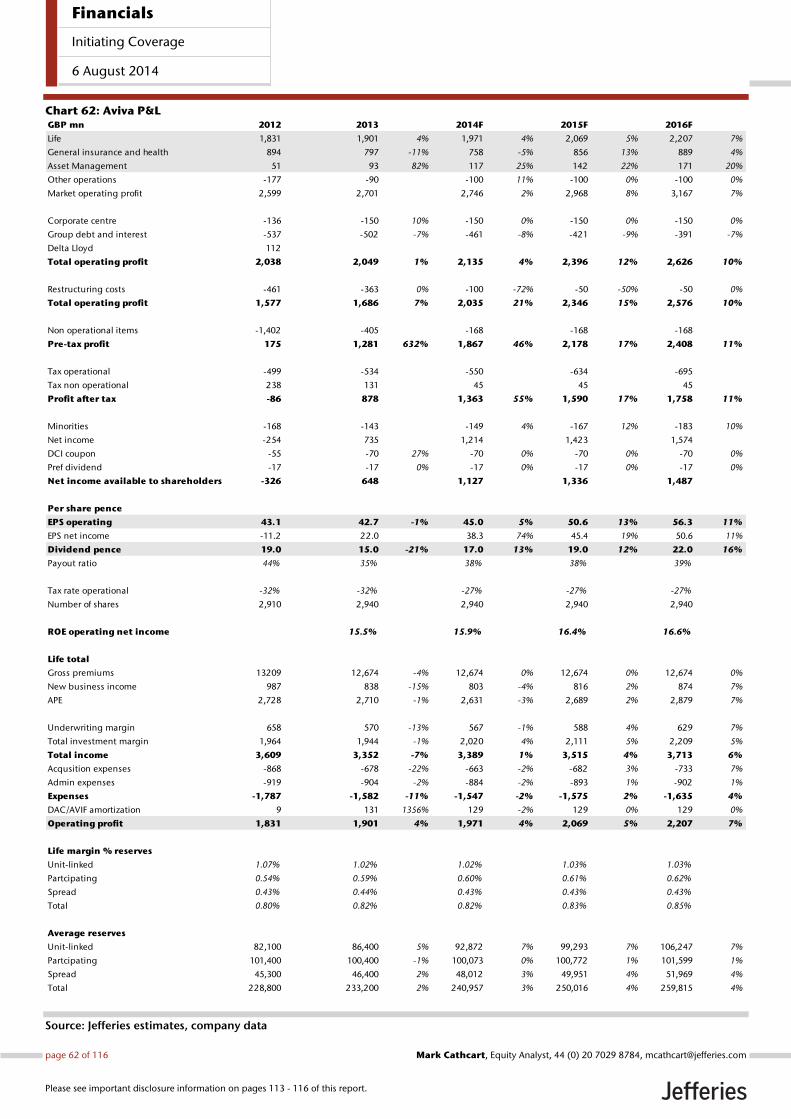

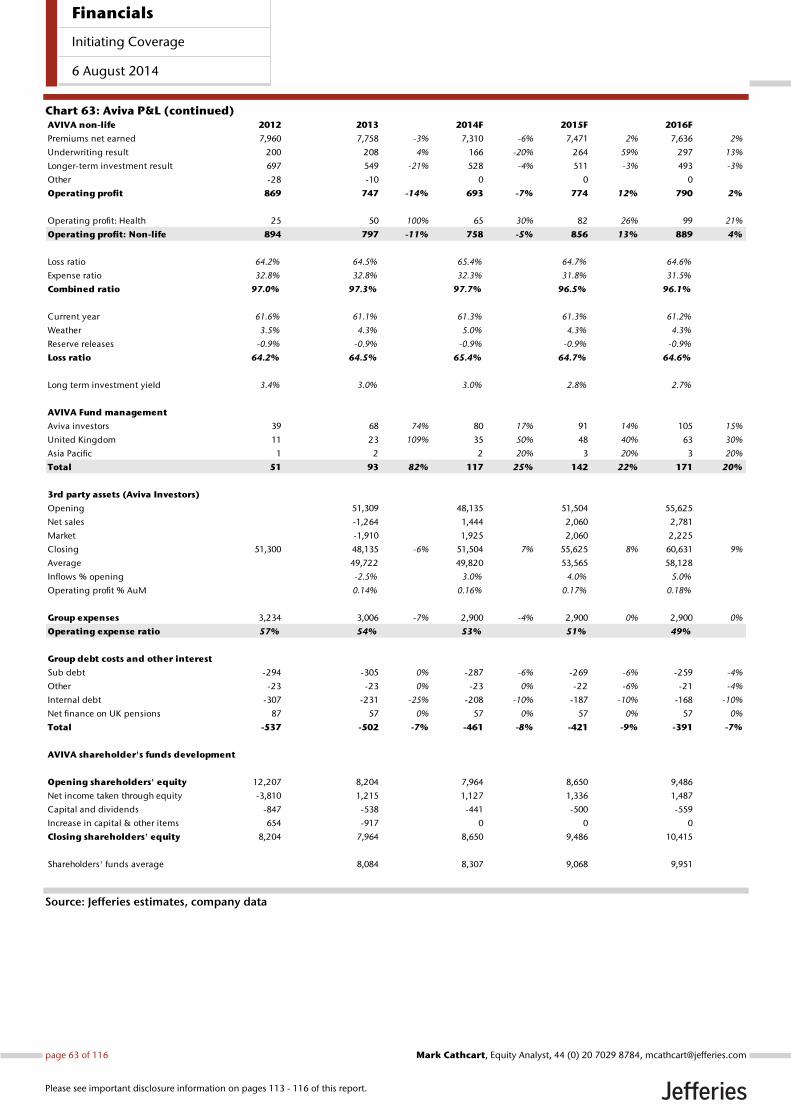

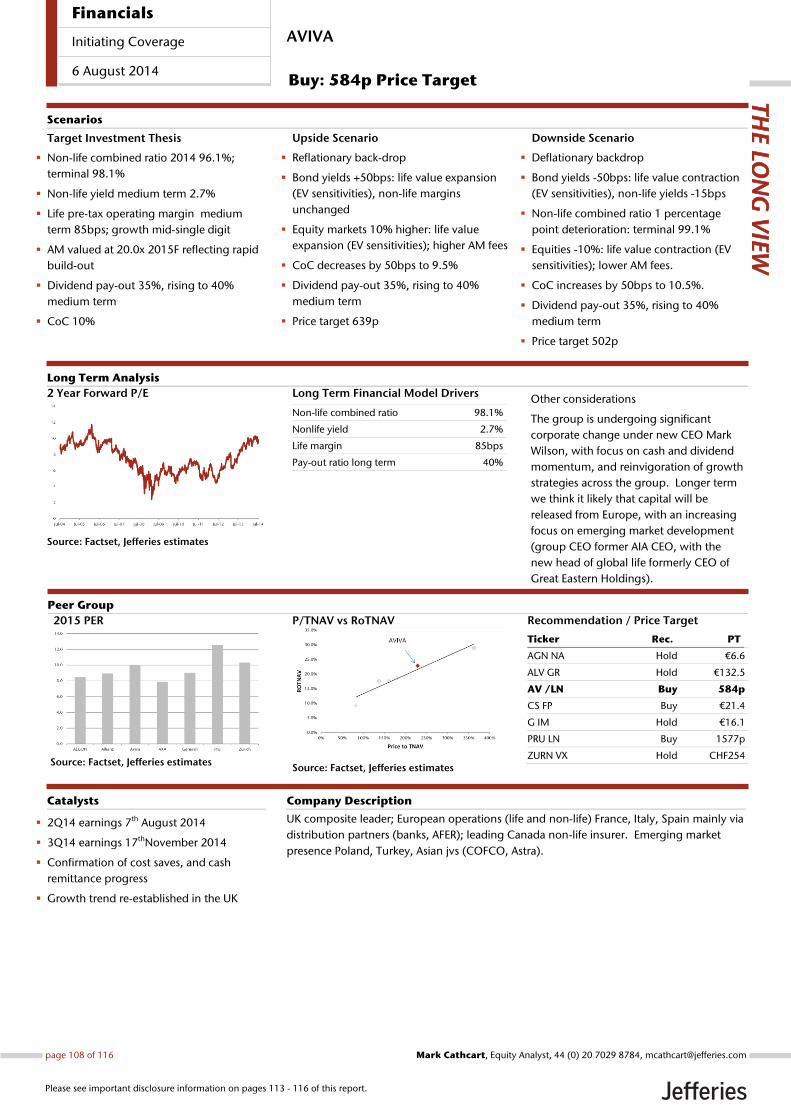

Aviva – Buy, Price Target 584p

We see dividend momentum shorter term driven by operational overhaul,

increasing cash remittance, and possible growth resurfacing in the core

business. Wider scale capital reallocation is likely over the longer term, in

our view, leading to an increasing emerging growth profile and longer-term

dividend momentum.

Aviva’s corporate culture has rapidly transformed following the arrival

of Mark Wilson as CEO (late 2012), former CEO and restorer of AIA ahead of its

IPO with a new management team appointed since. Initial focus has been on

cash generation and remittance to the group, simplification of the corporate

structure and tighter central management controls, where management’s target

of a group expense ratio of sub-50% for 2016 (53% 2013) suggests further

efficiency drives across the group.

The organic growth profile of the group is gaining momentum, with

management confident of a return to UK growth driven by their unique

composite leadership and IT edge (app and web facilitating sales), where cross-

sell stands at just 1.2, and asset management rebuild under Euan Munroe. The

distribution agreements across Europe have also been refocused and

strengthened.

CEO Mark Wilson underlined at the recent Investor Day that the £800m cash

earnings guidance for 2016 at the holding was for future dividends.

Our forecasts assume that 75% of this amount will eventually be set aside for

dividend (likely timeframe 2017), equating to a 40% pay-out ratio on operating

EPS, albeit with upside risk. This would leave £250-300m annual for investment

in growth, which if successfully reinvested on a 12% ROE would benefit

earnings growth by 2% annually on our calculation.

The key area of interest for us, however, is capital reallocation and the £2bn-

plus (10%-15% of group capital) that could be released from eventual sales of

Italy, Spain and Ireland (likely time horizon 2016-17). With the group CEO

formerly CEO at AIA, and the global life CEO formerly CEO of Great Eastern

Holdings, further investment in Asia (jvs and distribution deals) seems the

most likely home for this capital. Capital redeployment over the longer term

could see the group’s long-term earnings growth potential rising to 8% (versus

the 4% we calculate for the group as-is), where the dividend pay-out ratio will

likely sit in the 40%-45% range (versus 35% currently).

Factoring the current share price into our DDM, where we assume that the full

£800m will not be paid out until the dividend for 2018, suggests that the market

is valuing Aviva on a long-term growth rate of 4%, in line with its base-case

organic profile. Our price target of 584p is based on an eventual 40% pay-

out ratio and assumes long-term growth of 6% (rather than 8%), allowing for

risk to margins where we assume a 2 percentage point deterioration in the

combined ratio over time (see Aviva’s Long View at the end of this report for

more detail).

Buy recommendations spread across

the spectrum of economic risk

Tighter controls over expense and

cash generation driven by new CEO

UK growth potential

Dividend momentum

Longer-term capital reallocation

potential from Europe to Asia

Share price upside based on our

growth and dividend expectations

Financials

Initiating Coverage

6 August 2014

page 5 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

Downside risks are continued underwriting downturn in UK non-life, limited

cross-sell progress within the UK, further weakening of European distribution,

and failure to deliver on the operational improvements with cash earnings

disappointing in the process.

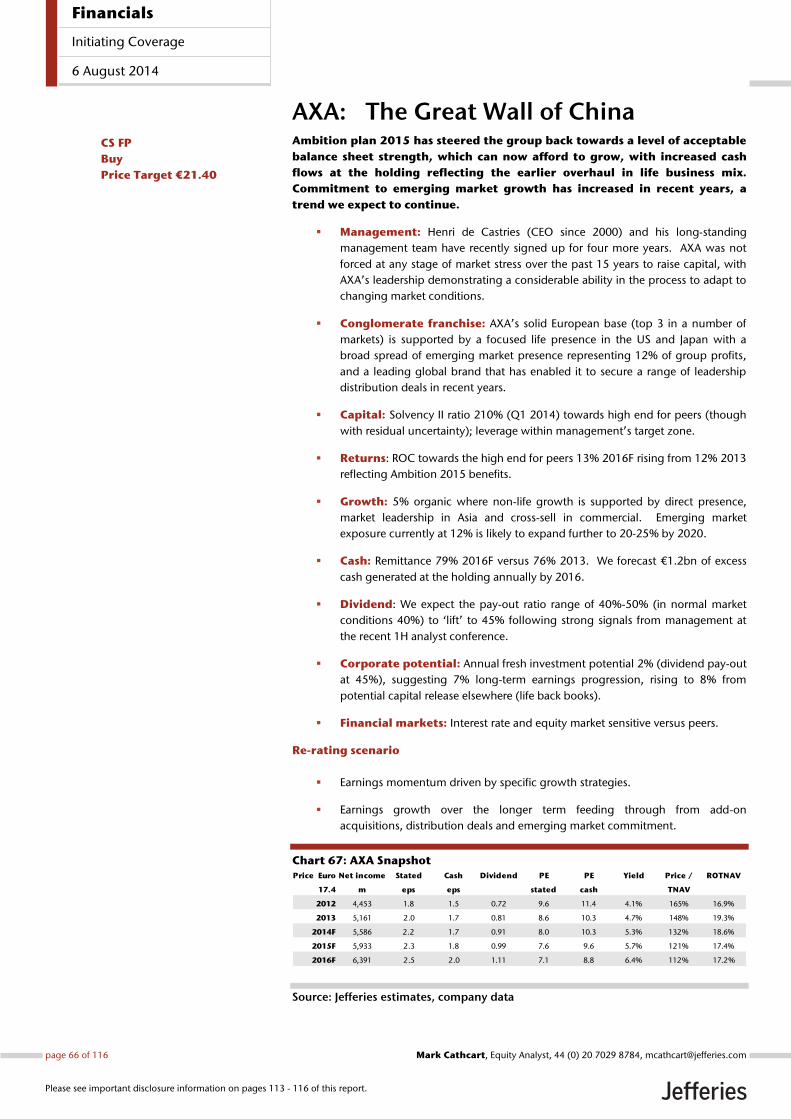

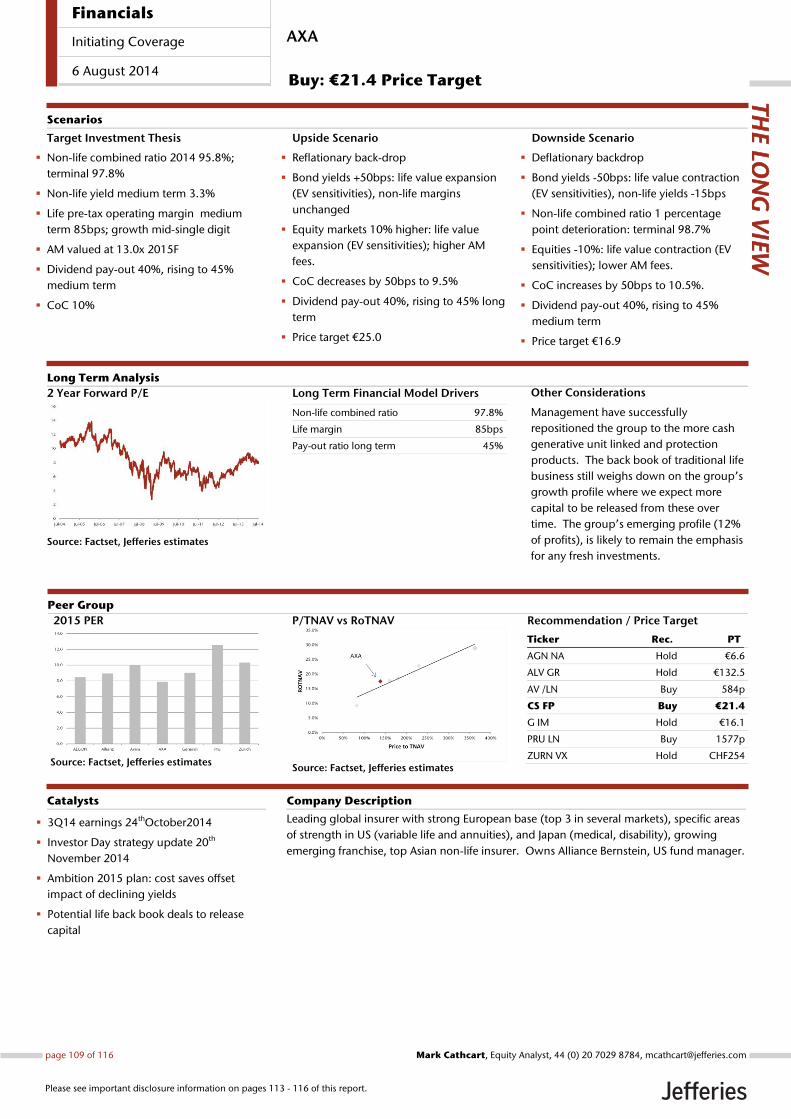

AXA – Buy, Price Target €21.4

Ambition 2015 has steered the group back towards a level of acceptable

balance sheet strength, which can now afford to grow, with increased cash

flows at the holding reflecting the successful overhaul in life business mix.

The current valuation fails to accommodate for the longer-term growth

profile of the group, with commitment to the emerging market build likely to

continue, in our view.

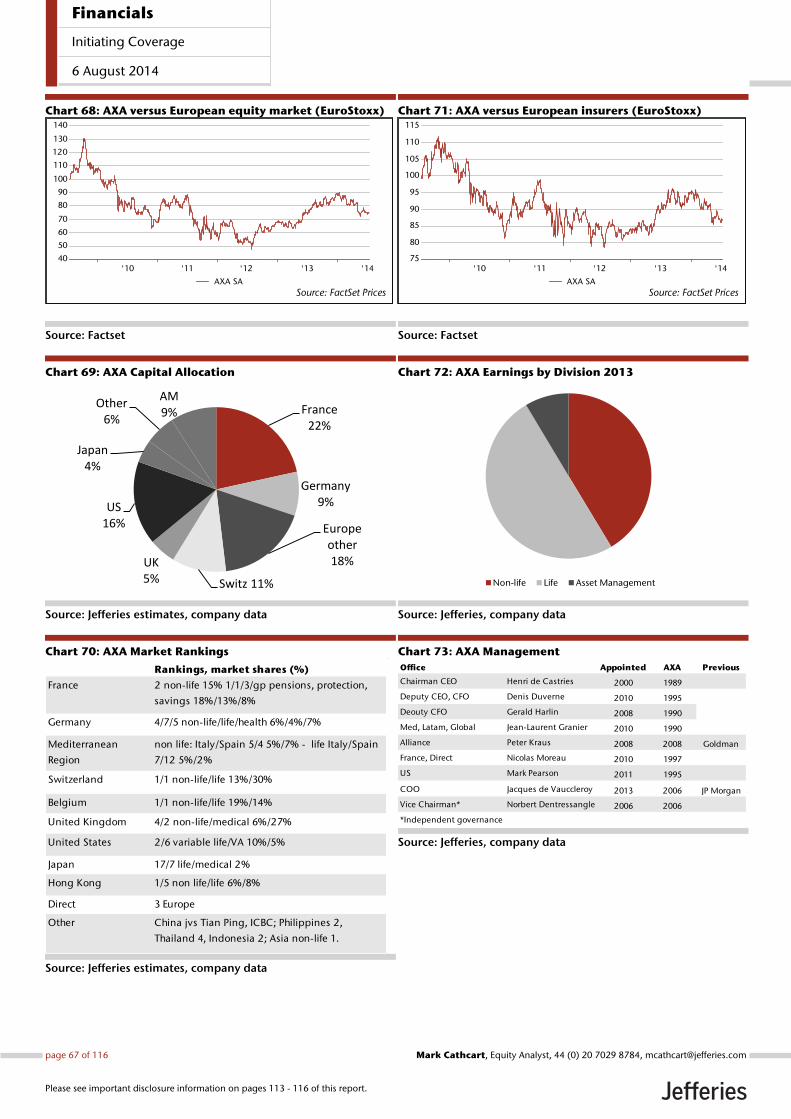

AXA’s solid European base (top 3 in a number of markets) is supported by a

focused life presence in the US and Japan, with a broad spread of emerging

market presence, and a leading global brand that has enabled it to secure a

range of leadership distribution deals in recent years. The management team

under Henri de Castries have recently signed up for four more years having

successfully restructured the balance sheet since the financial crisis,

repositioning the life portfolio to lower capital intensive unit-linked and

protection lines.

Ambition 2015 targeted a 2.5x increase in the growth contribution to group

earnings from a 5% base. At 12% for full year 2013, AXA’s commitment to

emerging growth expansion continues, where management have recently

expressed interest in the corporate insurance assets of the Brazilian bank Itau

Unibanco. Later next year AXA’s objectives for Ambition 2020 will possibly be

set out, with a further doubling of growth contribution to earnings quite likely

to be included. Successful execution would see AXA more than halfway towards

Prudential’s emerging growth profile by 2020.

We expect the dividend level to rise by 30% over the next three years,

with an increase in the pay-out ratio from 40% to 45% by 2016. This would

still leave €1bn of excess cash at the holding each year for growth reinvestments

(on a 12% ROE equates to close to 3% of earnings on our calculation), where

there might also be scope for additional capital release from the life back books.

We also consider the possibility of an IPO of its US life and annuity division (see

later section, Seventh Day, for a more detailed rationale), which would free up

around 15% of group capital on our calculation.

Factoring the current share price into our DDM, where we assume an increase in

the dividend pay-out ratio to 45% for 2016, suggests that the market is valuing

AXA on a long-term growth rate of 4%, below our base-case organic profile at

5%. Our price target of €21.4 is based on an eventual 45% pay-out ratio and

assumes long-term growth of 5% allowing for risk to margins, where we assume

a 2 percentage point deterioration in the combined ratio over time (please see

AXA’s Long View at the end of this report for more details). AXA is on the lowest

PER of the conglomerates (2015F 7.6X vs 8.8X ex Prudential), and highest cash

earnings yield (2015F 10.4% vs 9.5% ex Prudential).

Downside risks are underwriting downturn in European non-life, life margin

compression from falling yields, thwarted progress in building up the emerging

market profile, further falls in European and US bond yields, and falling equity

markets.

Strong management, powerful

franchise, leading brand

Emerging market commitment likely

to grow

Medium-term dividend momentum

driven by likely higher pay-out ratio

Share price fails to accommodate for

growth potential in our view

Financials

Initiating Coverage

6 August 2014

page 6 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

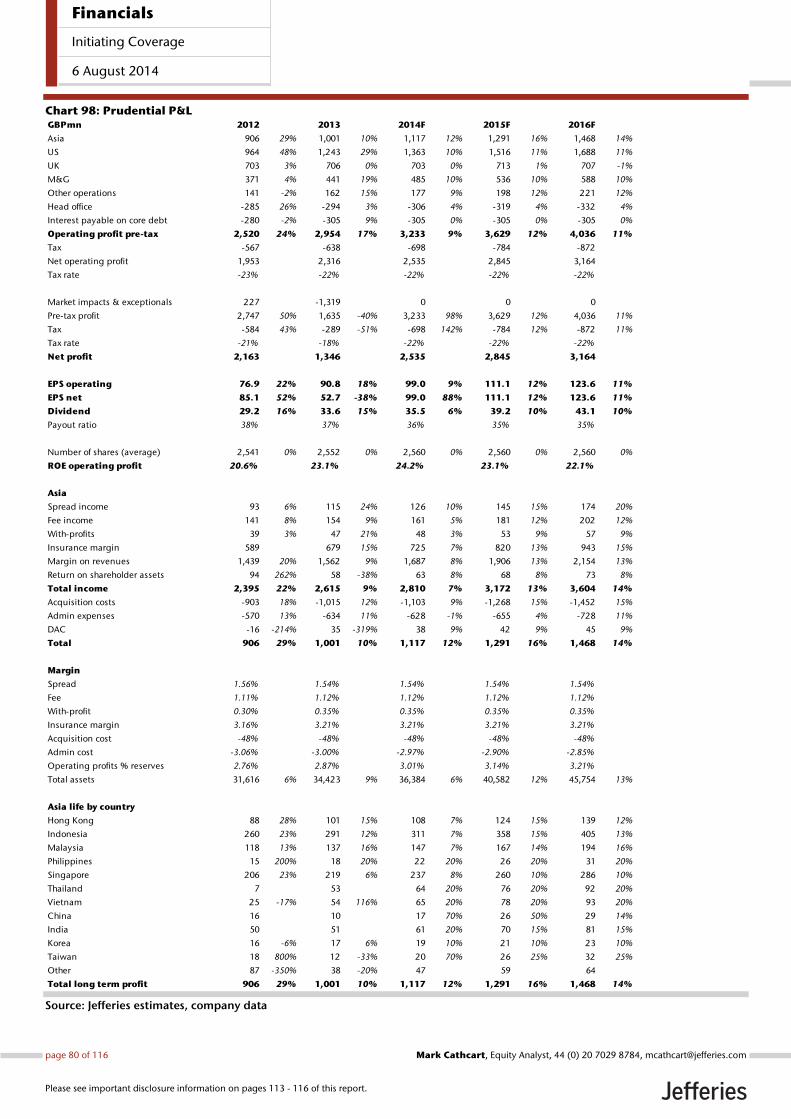

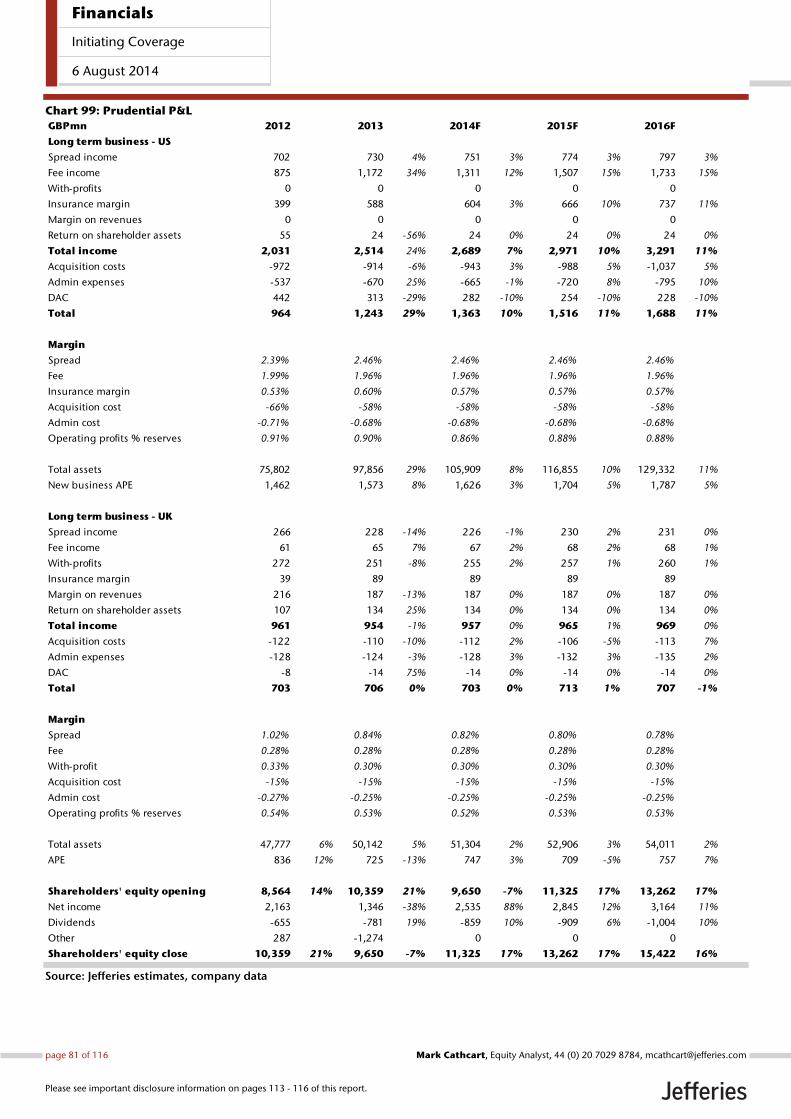

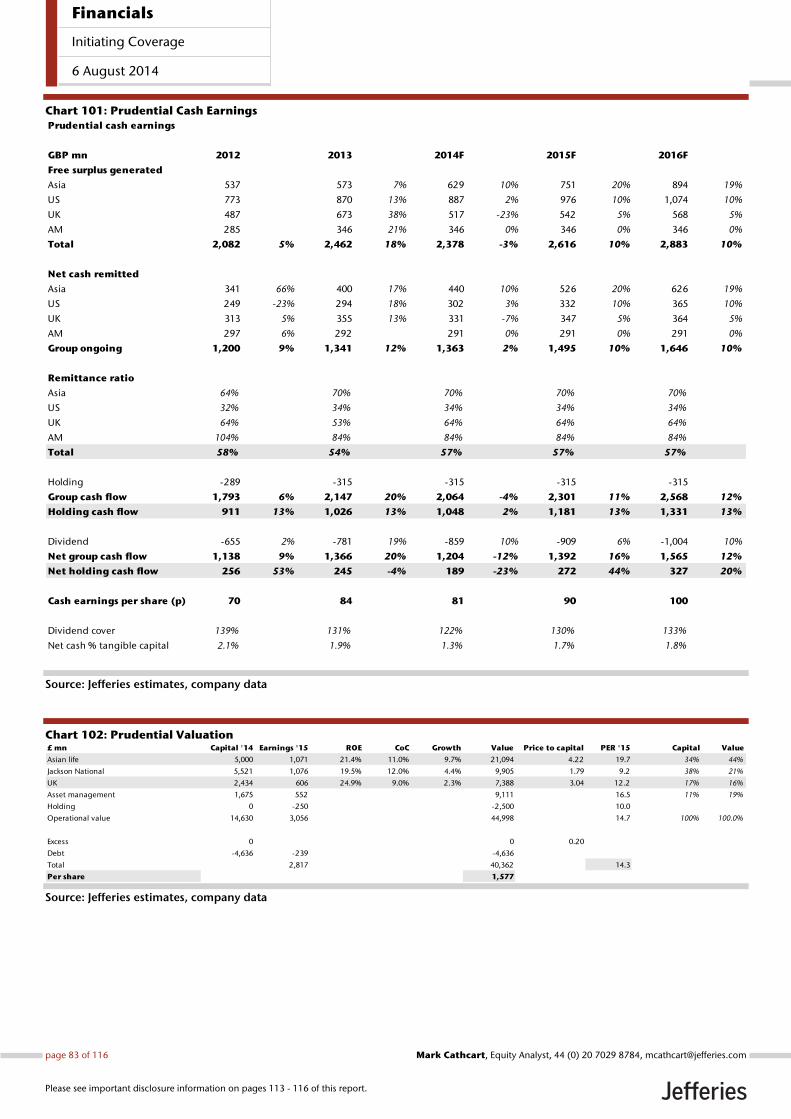

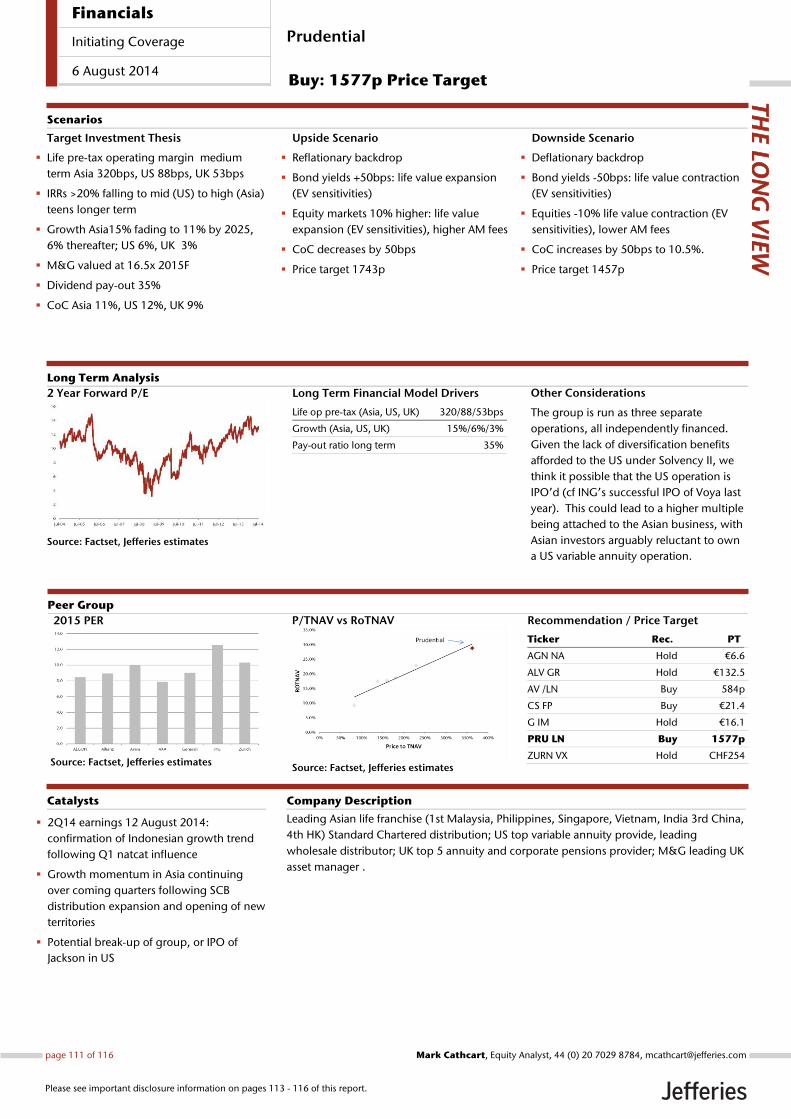

Prudential – Buy, Price Target 1577p

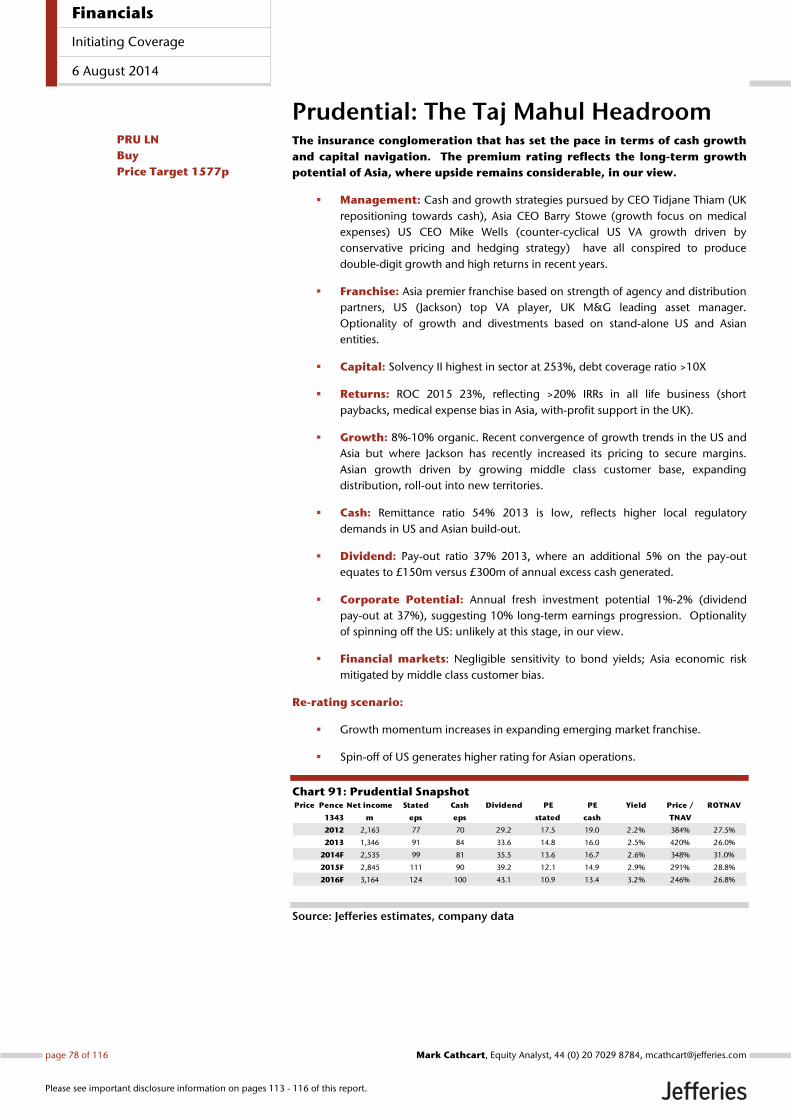

The insurance conglomeration that has set the pace in terms of cash

generation and capital navigation. The premium rating reflects the long-

term growth potential of Asia, where upside remains considerable, in our

view, and where dividend rebases are likely to continue as a result.

The cash and growth strategies pursued in the UK (repositioning towards

cash), Asia (growth focus on medical expenses to emerging middle class) and

US (counter-cyclical US VA growth driven by conservative pricing and hedging

strategy) have all conspired to produce double-digit growth and high

returns in recent years. Prudential now benefits from the leading Asian

franchise based on both distribution strength and geographic spread, leadership

in US variable annuities (market share and efficiency), and a UK franchise backed

by M&G, the leading UK asset manager.

Solvency II is the strongest in the sector at 253% (2013 FY), with ROCs the

highest of the conglomerates by some margin; we forecast 23% for 2015,

reflecting >20% IRRs in all life business (short paybacks, medical expense bias in

Asia, with-profit support in the UK).

The recent convergence of growth trends in the US and Asia has fuelled

momentum but where Jackson has recently increased its pricing to secure

margins. We expect the longer-term growth focus to be firmly on Asia,

where agency distribution continues to grow at double-digit rates, and where

Standard Chartered is also broadening (customer penetration still only 3%),

with new initiatives in Hong Kong and Singapore, India and China in the process

of opening, and with other markets to follow. Specifically, in Thailand

(undeveloped by Prudential’s standards but the second largest SE Asian

economy), distribution was secured last year via auto finance leader Thanachart.

Crucially, the growth trend in Prudential’s core health product shows no signs

of abating. Out-of-pocket medical expenses stand at 30%-60% across the

regions, according to management, versus 10% in the US/UK. Above all,

Prudential’s customer base, the middle class, is expected to grow to 135m by

2030 vs 45m 2012 (vs Prudential’s 2m customers). And beyond Asia, the

African continent now appears to be in Prudential’s sights.

Prudential’s clean corporate structure, with no internal debt, Asia with its own

holding structure, US life with no diversification benefits likely under Solvency II,

and management commentary on business optionality all point to at least the

possibility of a break-up of the group at some stage in the future, if

not a straight sale or IPO of Jackson. We note the successful IPO of Voya

(US life insurer) from ING last year. Asian investors are possibly less willing to

own Prudential given the difficulties in understanding the UK and US businesses.

With Jackson sold, the Asian business could then re-rate, possibly to a premium

to AIA based on a qualitative assessment between the two.

Factoring the current share price into our DDM, where we expect dividend

momentum to reflect earnings growth, but with no dividend pay-out increase,

suggests that the market is valuing Prudential on a long-term growth rate of

8.5% based on a CoC of 10%. Asian exposure arguably demands a higher risk

premium, but Prudential versus the conglomerate sector has limited exposure

to financial market risks, where roughly half of the Asian business is US$

denominated, and where the Asian premium mix should prove defensive

in any economic downturn (affordability of products to the bourgeoning middle

class). The PER for 2016F at 11.3x fails to accommodate for the group’s growth

profile and capital optionality, in our view. Our price target of 1577p

values the group on a PER 2016F of 12.7x, equating to a 10% long-term

growth rate on our DDM analysis. Please see Prudential’s Long View at the end

of this report for more detail.

Highest return and growth profile of

the conglomerates

The strongest on Solvency II

Asian upside remains considerable,

in our view

US IPO a possibility

Share price fails to accommodate for

the double-digit growth potential

Financials

Initiating Coverage

6 August 2014

page 7 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

Downside risks are regulatory changes in Asia undermining Prudential’s

product offering, Asian downturn deflating growth expectations, unfavourable

policyholder behaviour decreasing the expected value of Jackson’s annuity

portfolio, and further changes to government regulation of life and pensions

sales in the UK impacting margins and volumes.

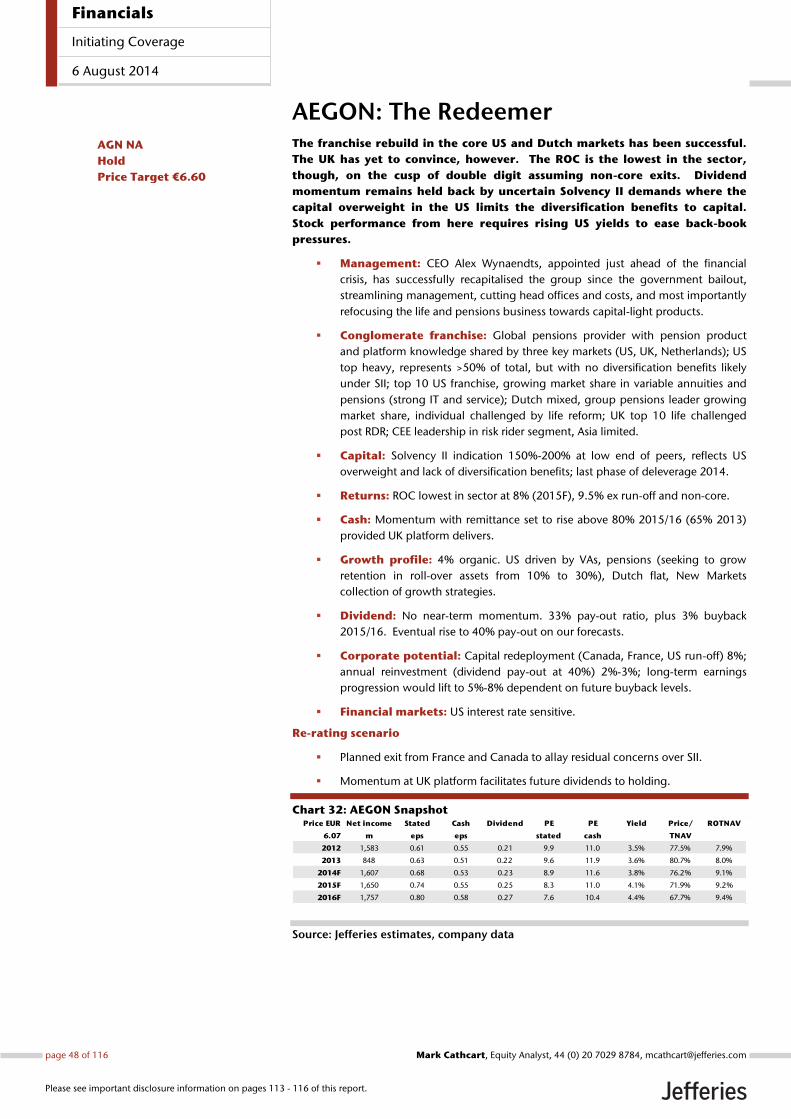

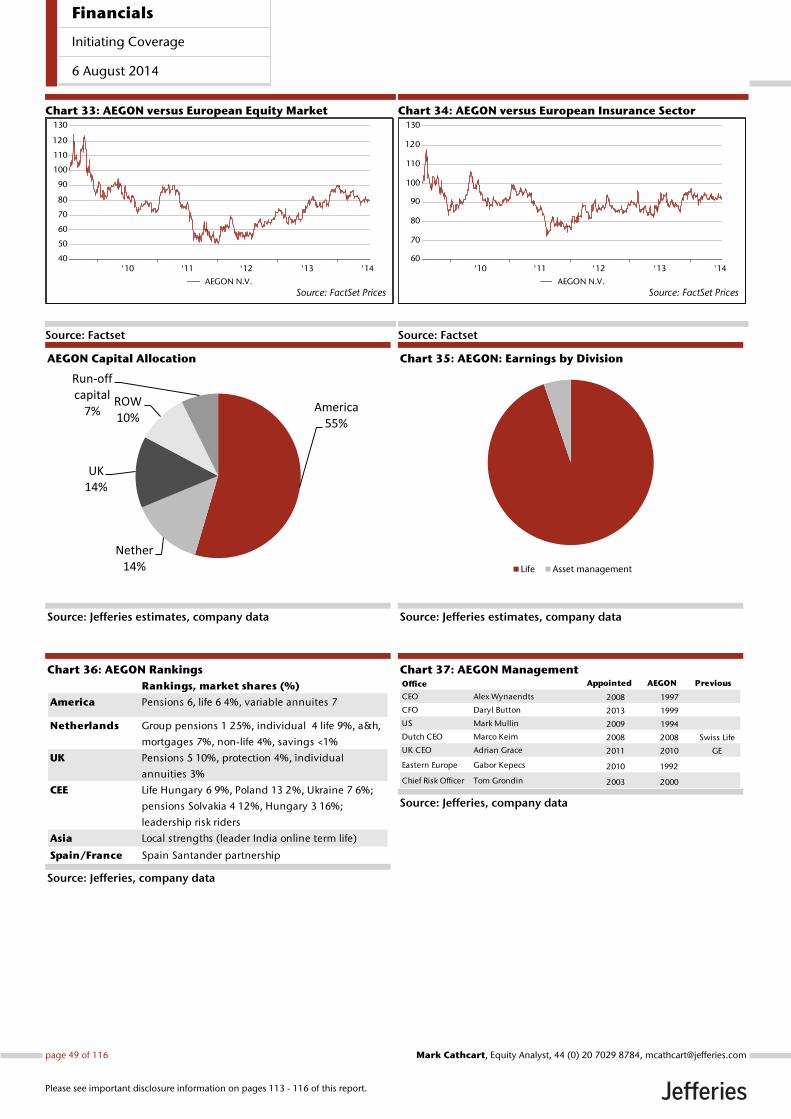

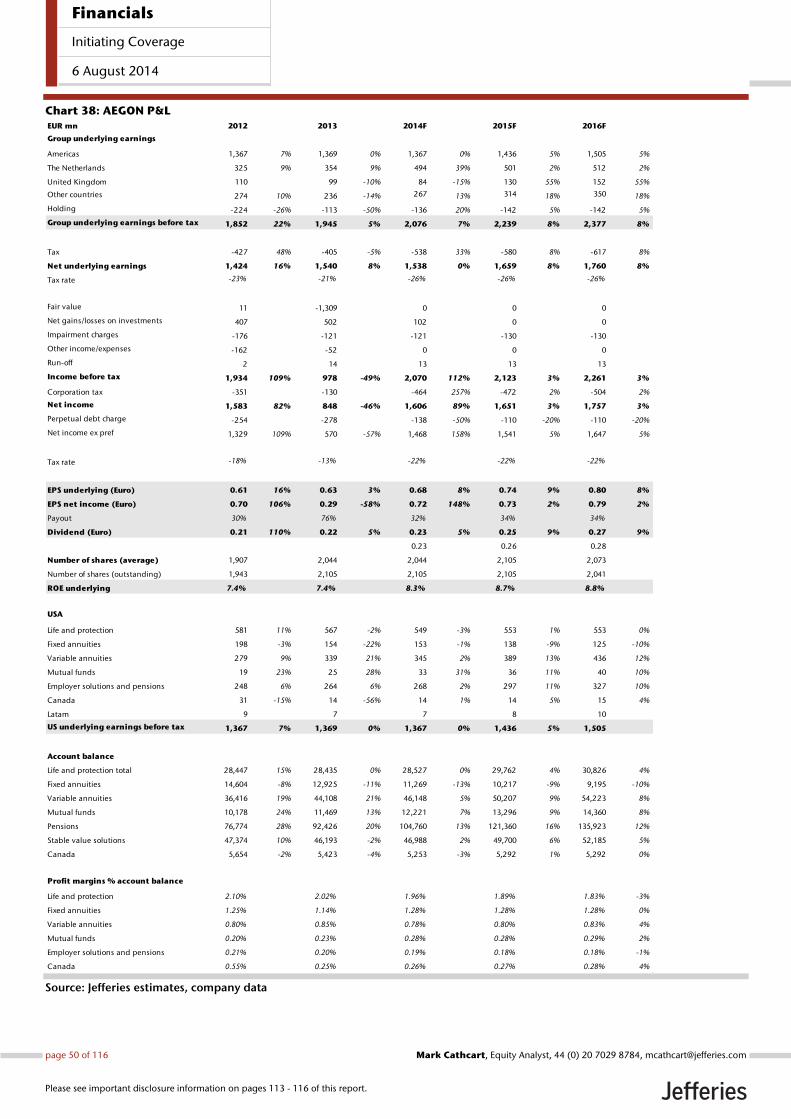

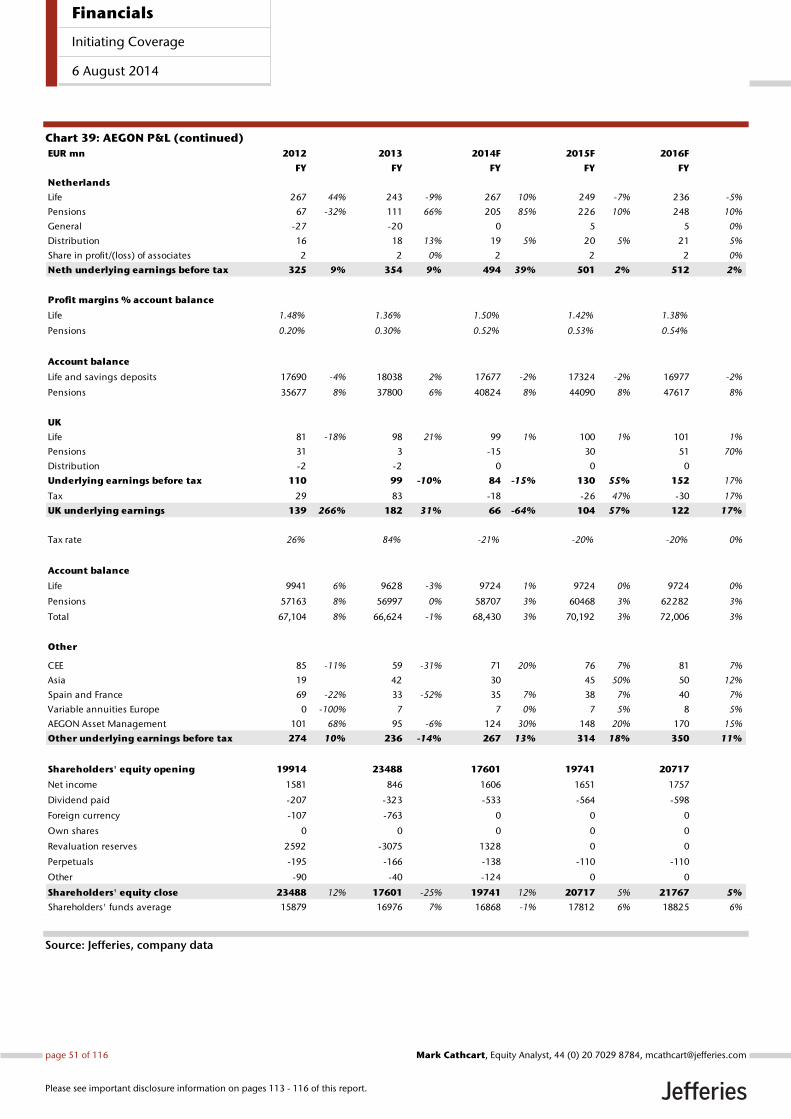

AEGON – Hold, Price Target €6.6

The improving return and growth profile of the group reflects extensive cost cutting and

portfolio repositioning in the core markets (US, Netherlands and UK), where successful

exit of non-core in France and Canada should secure an ROE of above 10% on our

calculation. ROCs still remain the lowest in the sector, however, reflecting the drag from

life back books with guarantees and extensive hedging costs, and continued sub

profitability in the UK, where critical mass has yet to be achieved in its new platform. The

indicative Solvency II range (150%-200%) is also at the low end for the sector, with the

mid-point of 175% comparing with typically 200% elsewhere. This reflects the US

overweight and absence of diversification benefits afforded to these assets under the new

capital regime, with dividend momentum likely to remain constrained longer than

elsewhere within the sector because of this, where the stock dividend yield at 4.4% for

2016 is at the low end for the sector. Risks to our Hold thesis are: a rise in US yields

leading to improving margins, an increased likelihood of selling the non-core run-off

books, faster capital replenishment, and dividend hikes earlier than expected; UK platform

momentum securing appropriate levels of returns; and (unlikely in our view), a re-

domiciling of the business to the US, and IPO of the European assets.

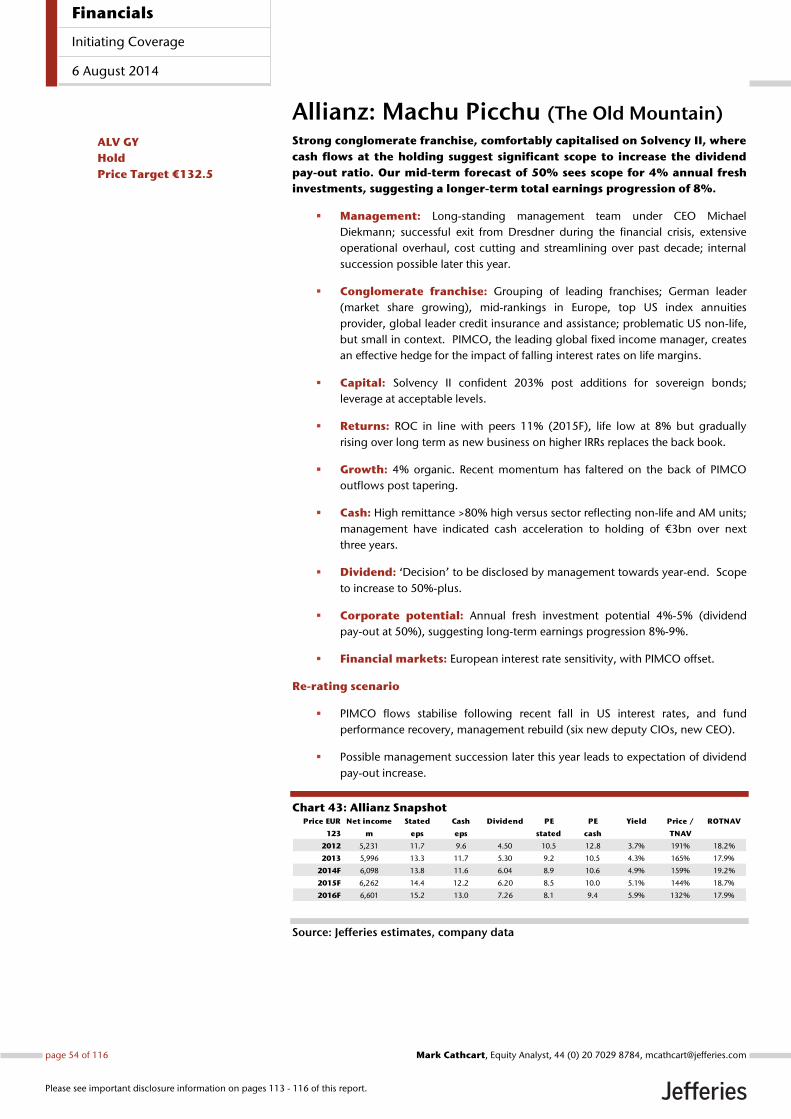

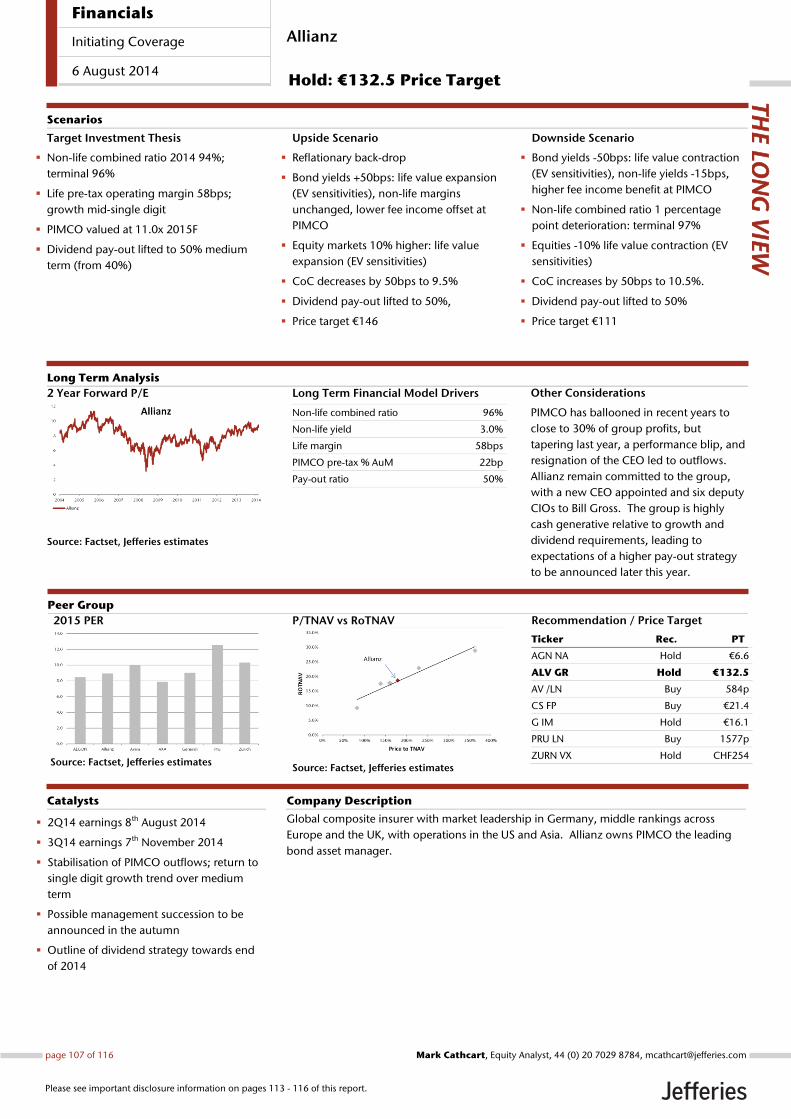

Allianz – Hold, Price Target €132.5

Strong cash flows relative to current growth and dividend requirements are likely to fuel

market expectation of pay-out increases over time (we expect a 50% pay-out ratio by

2016), where the market seems to be placing limited value on the group’s reinvestment

potential. Clarification of capital strategy is expected later this year. PIMCO outflows

have been weighing on the group’s rating in recent months following US tapering, a blip

in fund performance last year and the resignation of the CEO. We anticipate stabilisation

of outflows and a gradual return to a growth trend reflecting recent fund performance

recovery, and management rebuild (six new deputy CIOs appointed alongside CIO Bill

Gross, and a new CEO, former COO). Our €132.5 price target is based on a 50% pay-out

ratio and gives some benefit for reinvestment potential for the excess capital generation.

Risks to our thesis are continued outflows at PIMCO, underwriting downturn in European

non-life, and life margin compression from falling yields.

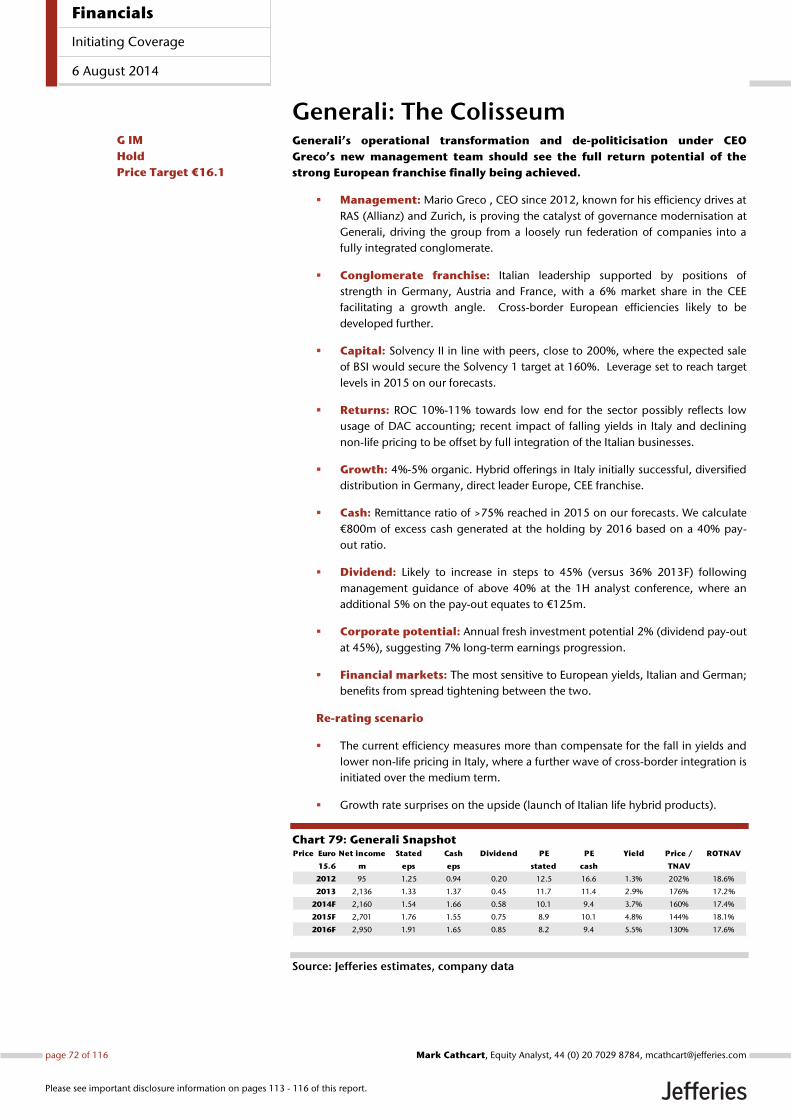

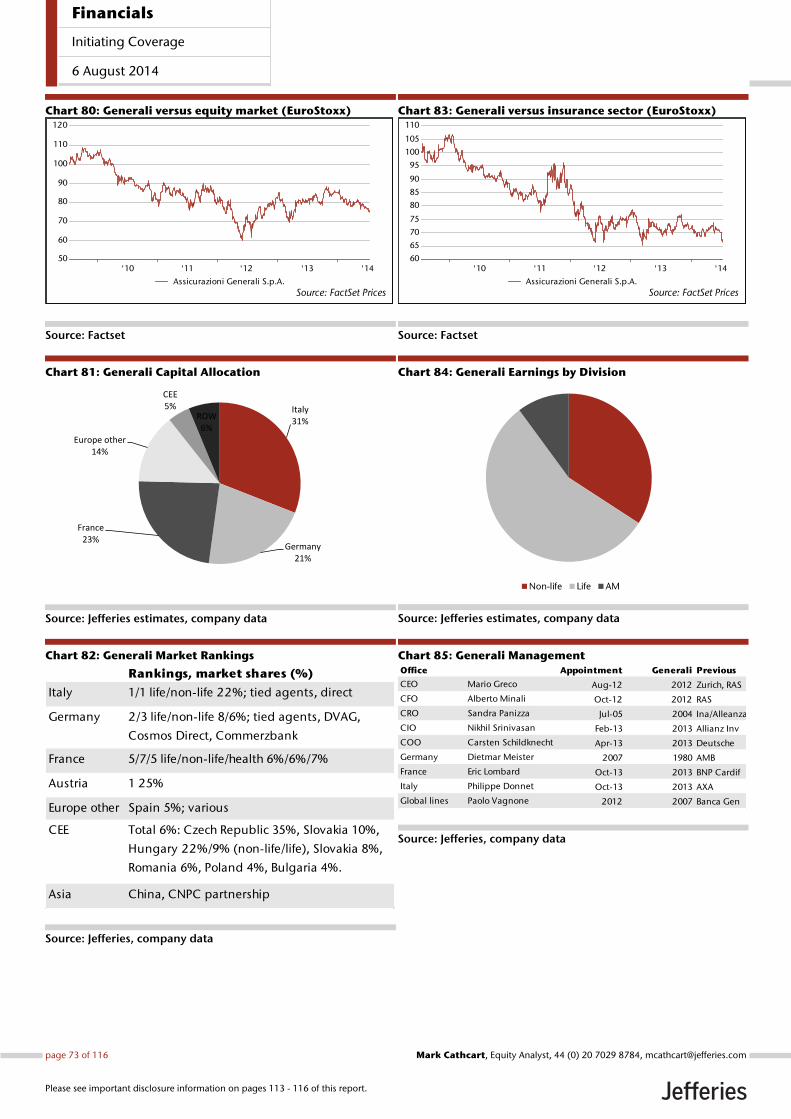

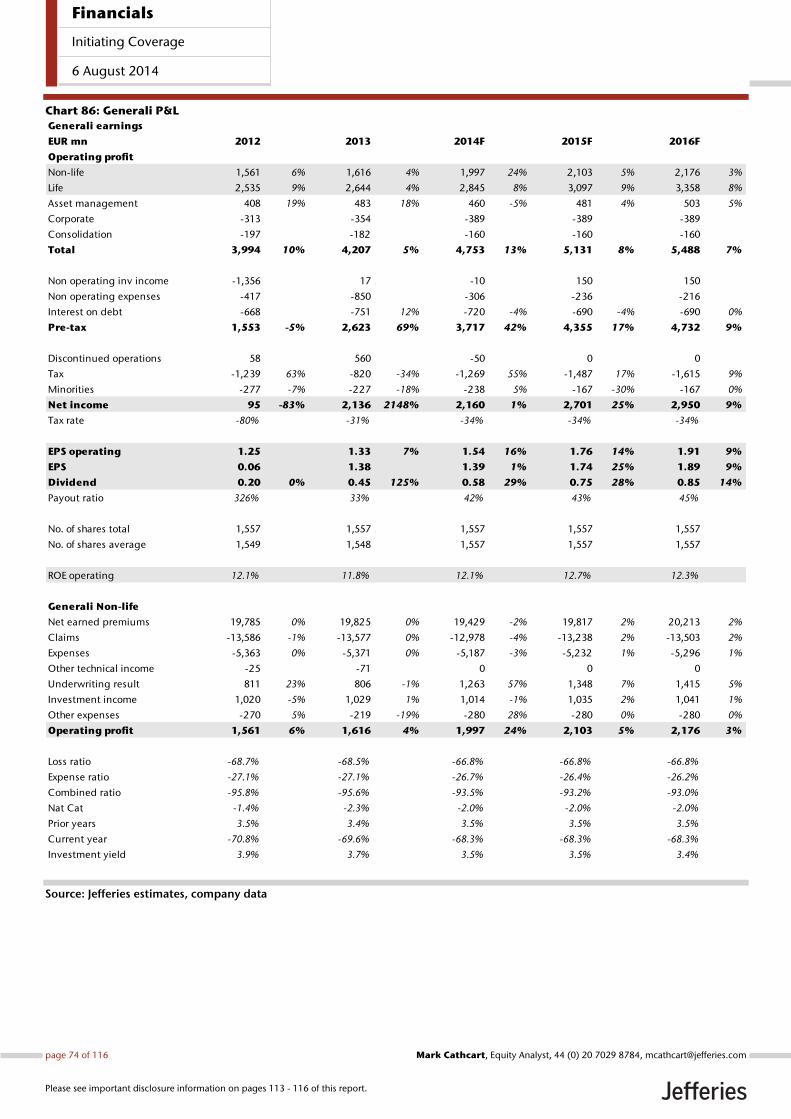

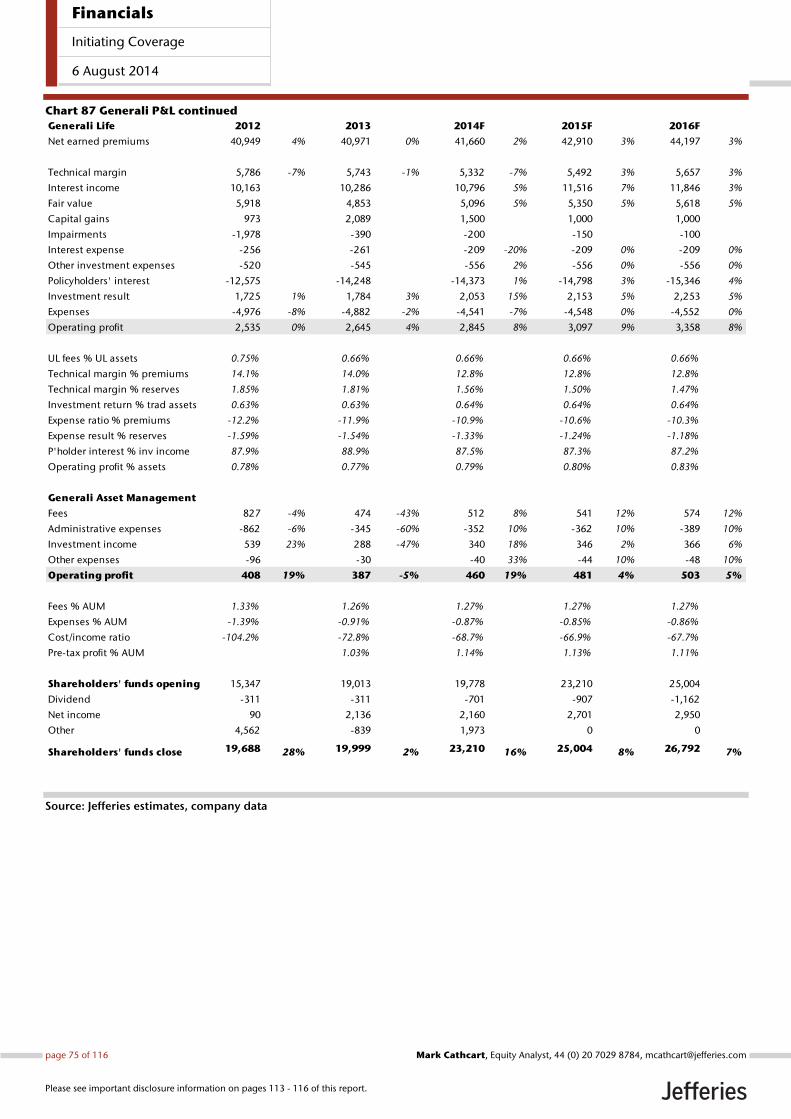

Generali – Hold, Price Target €16.1

Modernisation and de-politicisation under CEO Mario Greco and his new management

team are major positives for the group’s rating. Improving efficiency on the back of wide-

scale integration, higher domestic growth rates driven by the tied agents diversifying their

sales into non-traditional life products, and capital repair following the recent sale of BSI

have given management confidence to point to a higher dividend pay-out ratio in the

future (above 40% vs 36% 2013). Generali is the most exposed of the conglomerates to

falling yields in Italy and Germany, however, where falling domestic auto rates may begin

to affect profit momentum. Risks to our thesis are a sooner-than-expected move to 45%

pay-out ratio (our long-term forecast), additional expense cuts more than offsetting

margin pressures and reversal of the recent bond yield declines. The stock is underpinned

at current levels by its high free cash yield (9.6% 2016F vs 10.1% sector ex Pru).

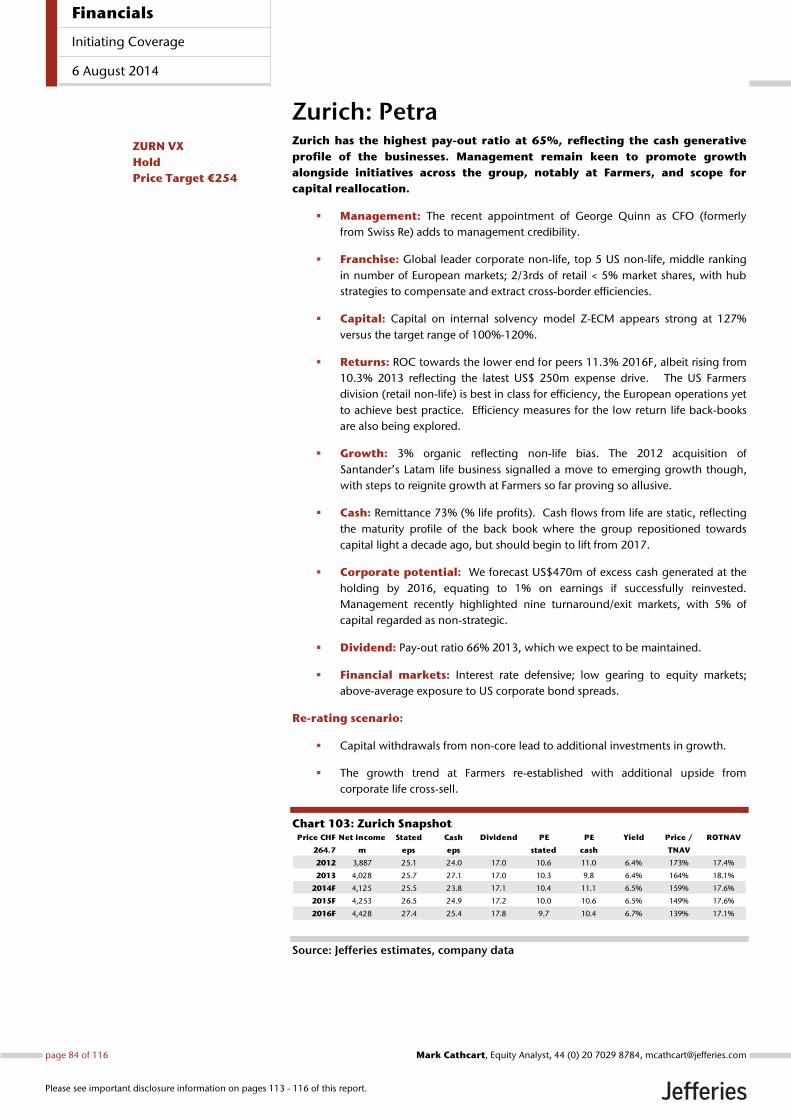

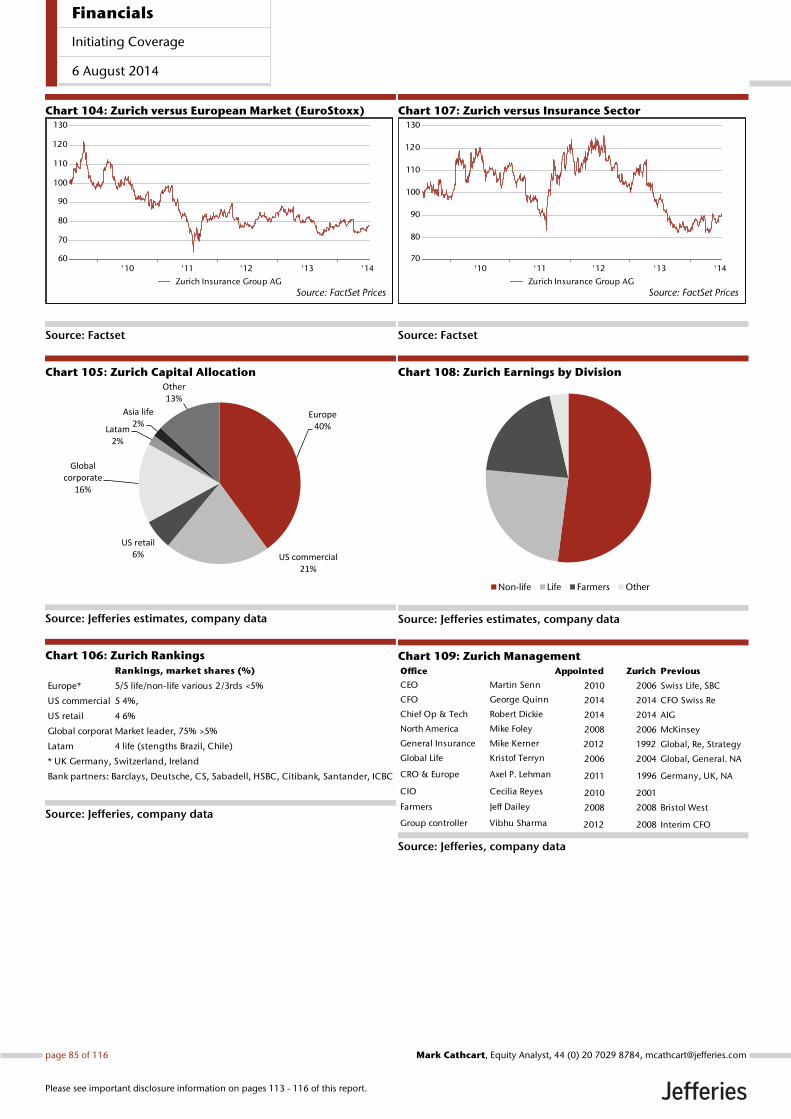

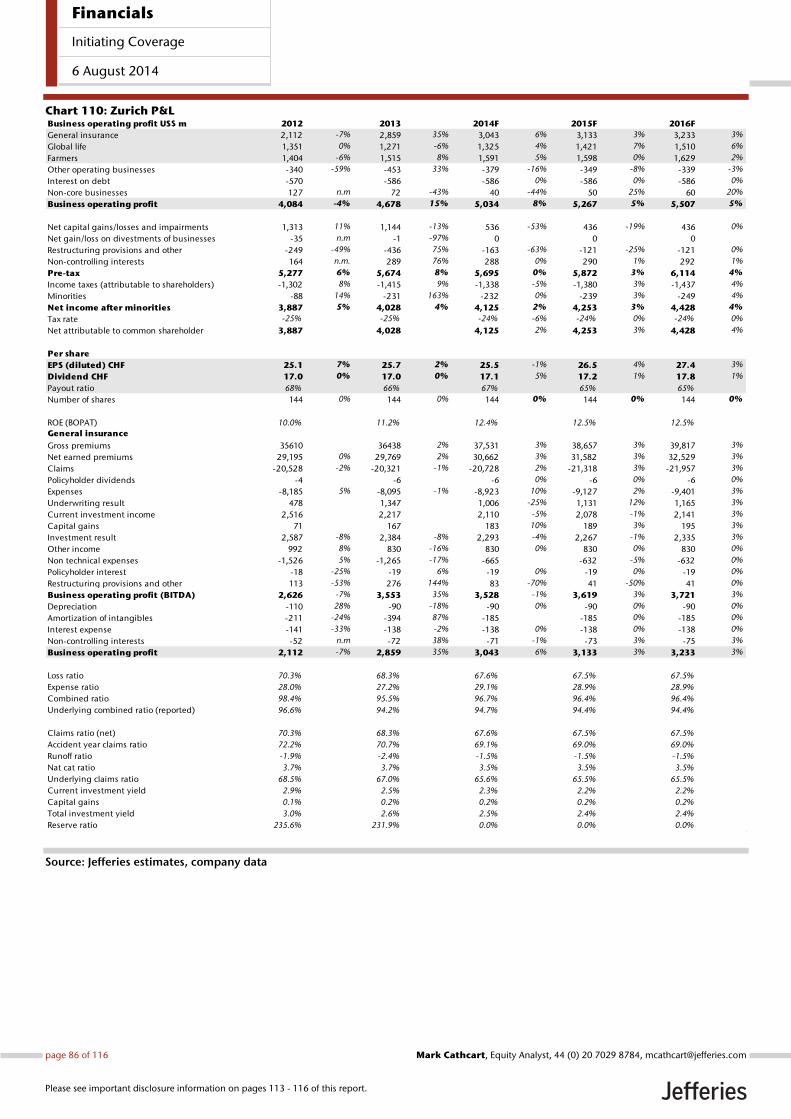

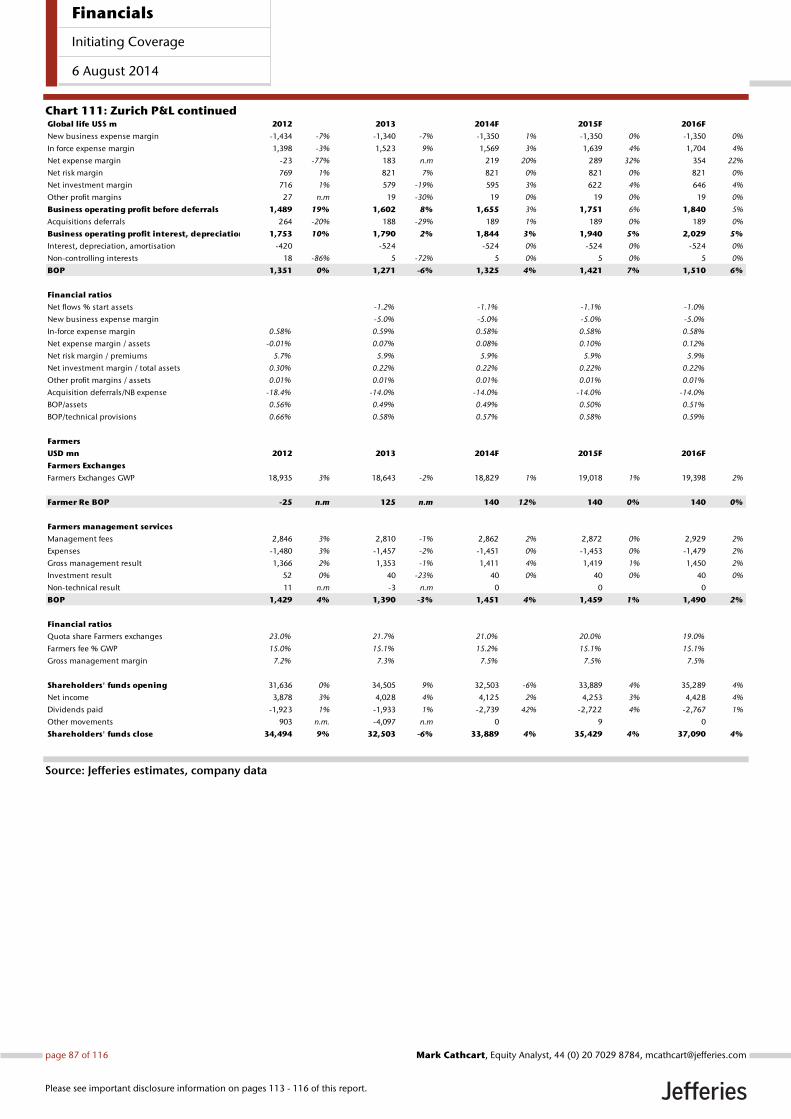

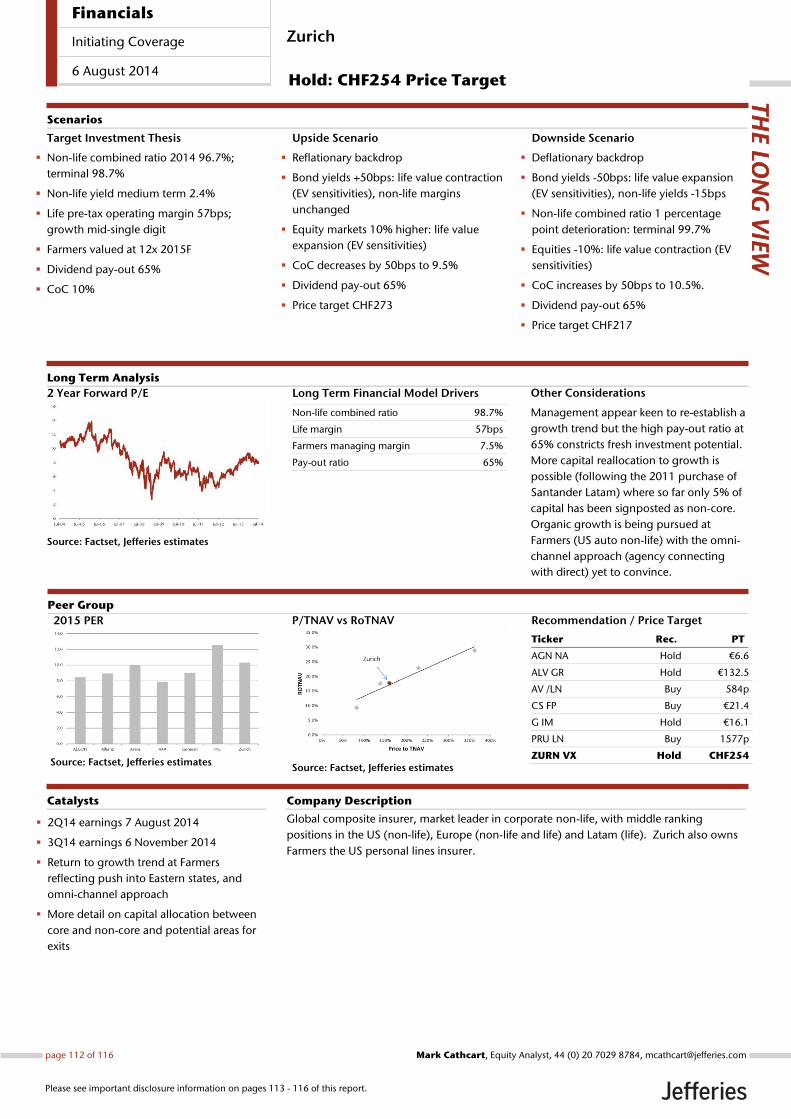

Zurich – Hold, Price Target CHF254

Dividend upside is limited by an already high pay-out ratio (65%) and low earnings

growth profile (overweight non-life, where Farmers omni-channel approach has yet to

convince in the face of direct competition). Non-core sales are also expected to be small,

with guidance at 5% of total capital. The stock does, however, benefit from strong yield

underpin (2016F 6.7%) and is economically defensive. Risks to our thesis include a

convincing growth trend being established at Farmers, and additional capital release (life

back books for example) fuelling expectations of more emerging market roll-out.

Dividend upside considerable;

PIMCO trajectory less certain

Significant cost cutting under new

management team, but drag of

falling yields and lower domestic

auto rates

Dividend pay-out already high,

growth potential limited

Solvency II at the low end for the

sector constrains dividend

momentum for the medium term

Financials

Initiating Coverage

6 August 2014

page 8 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

Valuation Our formal share price targets are driven from a traditional multi-period

residual return model. However, to reflect the increased emphasis on

dividends within the sector we use reverse dividend discount modelling to

assess the growth rates implied by the current share price and also by our

share price targets.

We flex our valuations for deflationary/reflationary scenarios. For reflation, we

assume a 10% increase in equity markets and a 50bps upward shift in bond yields; for

deflation, the opposite but also specifically take into account the likely deterioration in

non-life profitability. In a deflationary cycle, non-life earnings would possibly take a

double hit, from lower reinvestment rates (we have assumed 15bps for the 50bps decline

in bond yields to reflect the offset of asset diversification) and from likely falling prices

with customers more price conscious. We note the current combination in Italy of falling

bond yields and declining rates for auto insurance.

Chart 6 shows the share price (the line across the bars), the current share price target (the

division between red and grey), and the share price targets on deflationary and

reflationary scenarios. Those companies towards the left are the most at risk from

deflation, but those that would be most advantaged by a move to reflation. Those to the

right are the more economically defensive stocks. The additional downside in a

deflationary cycle from non-life, and the decline in traditional spreads as yield potential

gets closer to the long-term guarantees leads to asymmetric risk at both ends of the chart,

Zurich (non-life) and AXA (life).

For a full explanation of how our share price targets are derived, please see Appendices 2,

3 and 4: Valuation, Financial Market Influence and Recent Conglomerate Performance. The

last of these sections strips out financial market impact on share price moves since the

beginning of the year to assess the stock specific re-ratings/de-ratings.

Chart 6: Share Price Target Flex: Deflation/Reflation Scenarios

Source: Jefferies estimates, company data

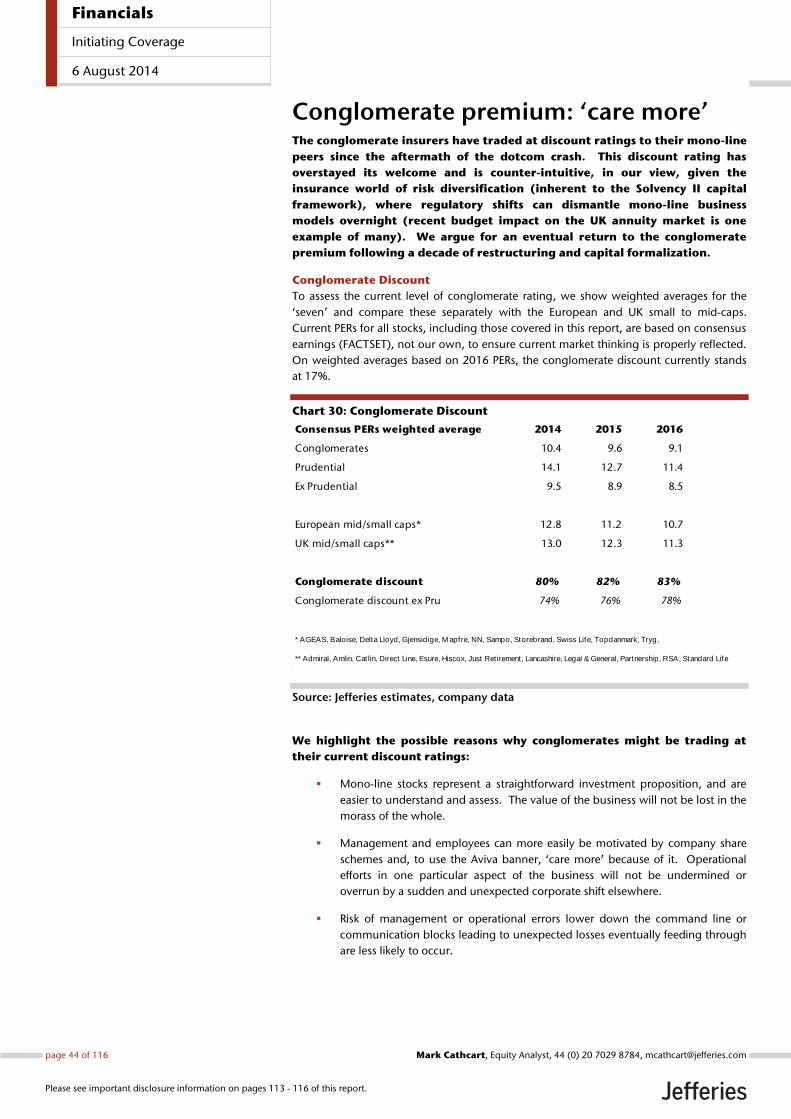

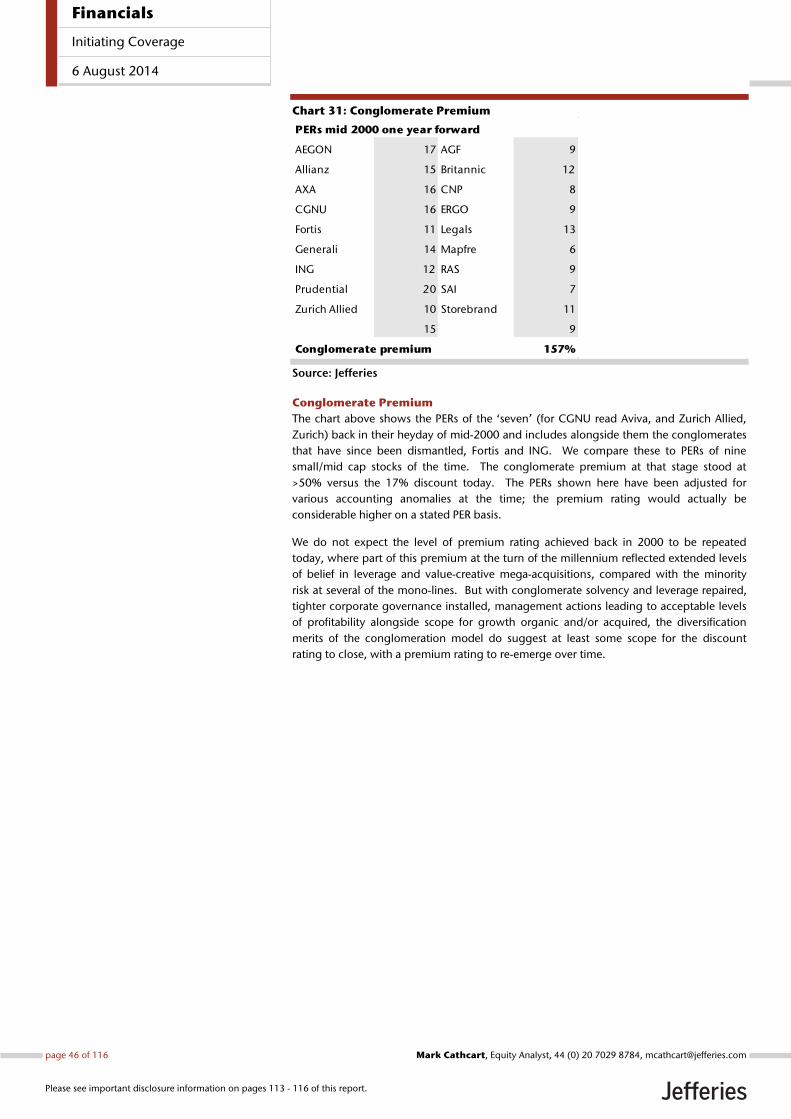

The conglomerates are currently trading at a 17% discount to the small/mid -cap insurers

on a consensus PER basis (2016F) where a premium rating appears more appropriate

given their range of growth strategies in an uncertain regulatory world. Please see later

section, The Conglomerate Premium, for arguments as to why a premium rating might

become attached to these stocks over the longer-term horizon (post Solvency II and GSII)

not seen since the early part of 2001.

80

90

100

110

120

130

140

150

AXA Generali AEGON Allianz Aviva Prudential Zurich

Min PT : Base PT range Base PT : Max PT range Share price

We flex our share price targets for

deflation and reflation

With asymmetric risk to the

downside

The conglomerate discount at 17%

appears harsh given the uncertain

regulatory world for the mono-line

insurers

Financials

Initiating Coverage

6 August 2014

page 9 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

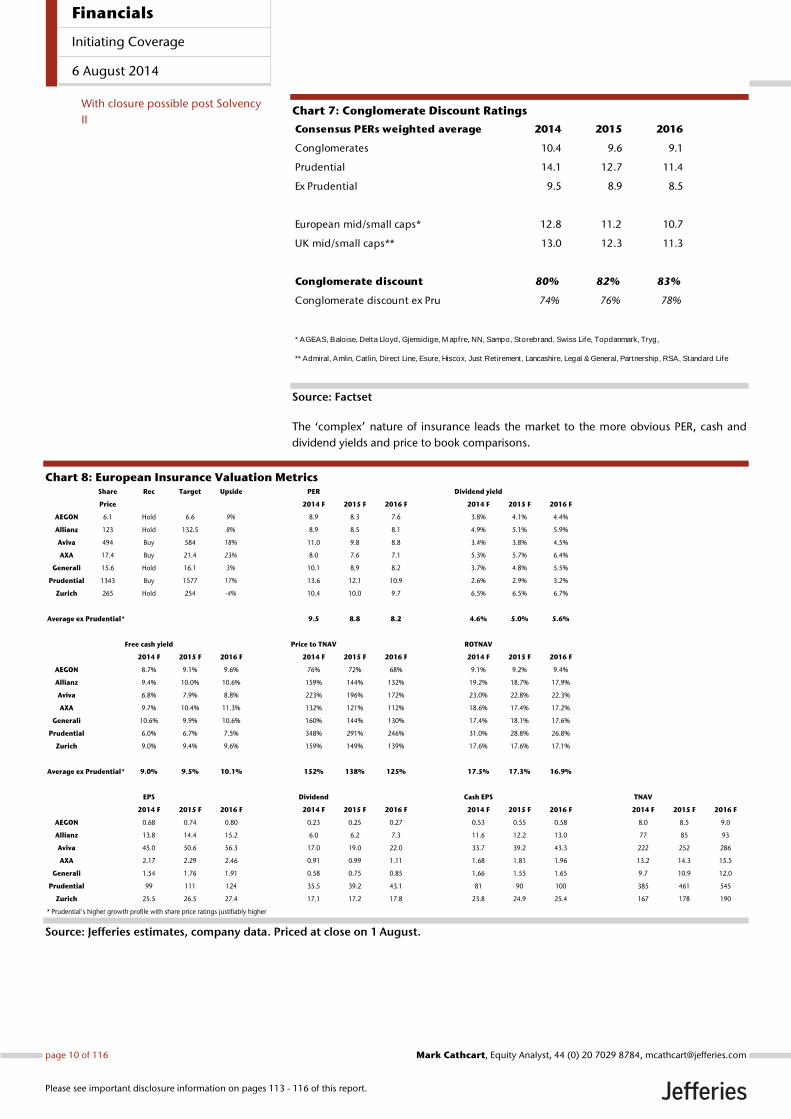

Chart 7: Conglomerate Discount Ratings

Source: Factset

The ‘complex’ nature of insurance leads the market to the more obvious PER, cash and

dividend yields and price to book comparisons.

Chart 8: European Insurance Valuation Metrics

Source: Jefferies estimates, company data. Priced at close on 1 August.

Consensus PERs weighted average 2014 2015 2016

Conglomerates 10.4 9.6 9.1

Prudential 14.1 12.7 11.4

Ex Prudential 9.5 8.9 8.5

European mid/small caps* 12.8 11.2 10.7

UK mid/small caps** 13.0 12.3 11.3

Conglomerate discount 80% 82% 83%

Conglomerate discount ex Pru 74% 76% 78%

* AGEAS, Baloise, Delta Lloyd, Gjensidige, M apfre, NN, Sampo, Storebrand, Swiss Life, Topdanmark, Tryg,

** Admiral, Amlin, Catlin, Direct Line, Esure, Hiscox, Just Retirement, Lancashire, Legal & General, Partnership, RSA, Standard Life

Share Rec Target Upside PER Dividend yield

Price 2014 F 2015 F 2016 F 2014 F 2015 F 2016 F

AEGON 6.1 Hold 6.6 9% 8.9 8.3 7.6 3.8% 4.1% 4.4%

Allianz 123 Hold 132.5 8% 8.9 8.5 8.1 4.9% 5.1% 5.9%

Aviva 494 Buy 584 18% 11.0 9.8 8.8 3.4% 3.8% 4.5%

AXA 17.4 Buy 21.4 23% 8.0 7.6 7.1 5.3% 5.7% 6.4%

Generali 15.6 Hold 16.1 3% 10.1 8.9 8.2 3.7% 4.8% 5.5%

Prudential 1343 Buy 1577 17% 13.6 12.1 10.9 2.6% 2.9% 3.2%

Zurich 265 Hold 254 -4% 10.4 10.0 9.7 6.5% 6.5% 6.7%

Average ex Prudential* 9.5 8.8 8.2 4.6% 5.0% 5.6%

Free cash yield Price to TNAV ROTNAV

2014 F 2015 F 2016 F 2014 F 2015 F 2016 F 2014 F 2015 F 2016 F

AEGON 8.7% 9.1% 9.6% 76% 72% 68% 9.1% 9.2% 9.4%

Allianz 9.4% 10.0% 10.6% 159% 144% 132% 19.2% 18.7% 17.9%

Aviva 6.8% 7.9% 8.8% 223% 196% 172% 23.0% 22.8% 22.3%

AXA 9.7% 10.4% 11.3% 132% 121% 112% 18.6% 17.4% 17.2%

Generali 10.6% 9.9% 10.6% 160% 144% 130% 17.4% 18.1% 17.6%

Prudential 6.0% 6.7% 7.5% 348% 291% 246% 31.0% 28.8% 26.8%

Zurich 9.0% 9.4% 9.6% 159% 149% 139% 17.6% 17.6% 17.1%

Average ex Prudential* 9.0% 9.5% 10.1% 152% 138% 125% 17.5% 17.3% 16.9%

EPS Dividend Cash EPS TNAV

2014 F 2015 F 2016 F 2014 F 2015 F 2016 F 2014 F 2015 F 2016 F 2014 F 2015 F 2016 F

AEGON 0.68 0.74 0.80 0.23 0.25 0.27 0.53 0.55 0.58 8.0 8.5 9.0

Allianz 13.8 14.4 15.2 6.0 6.2 7.3 11.6 12.2 13.0 77 85 93

Aviva 45.0 50.6 56.3 17.0 19.0 22.0 33.7 39.2 43.3 222 252 286

AXA 2.17 2.29 2.46 0.91 0.99 1.11 1.68 1.81 1.96 13.2 14.3 15.5

Generali 1.54 1.76 1.91 0.58 0.75 0.85 1.66 1.55 1.65 9.7 10.9 12.0

Prudential 99 111 124 35.5 39.2 43.1 81 90 100 385 461 545

Zurich 25.5 26.5 27.4 17.1 17.2 17.8 23.8 24.9 25.4 167 178 190

* Prudential's higher growth profile with share price ratings justifiably higher

With closure possible post Solvency

II

Financials

Initiating Coverage

6 August 2014

page 10 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

Risks Aside from the economic risks outlined above (falling investment yields, equity market

decline, widening corporate bond spreads), and the specific workings of deflation and

reflation leading to decreased/increased demand for products and higher/lower claims,

there are the insurance risks. These include the rating cycle in non-life, where price

aggregators might force a secular decline in pricing power; a sudden and unexpected

escalation in non-life claims; longevity and mortality risks, where people live longer or

shorter than assumed in pricing assumptions; and distribution shifts, where cheaper forms

of customer access (Apps, internet) undermine the traditional agency structures. There

are also the regulatory risks to contend with, which might impact product relevance (tax

breaks removed, annuity rules changed) and distribution channels (UK RDR for example).

Financials

Initiating Coverage

6 August 2014

page 11 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

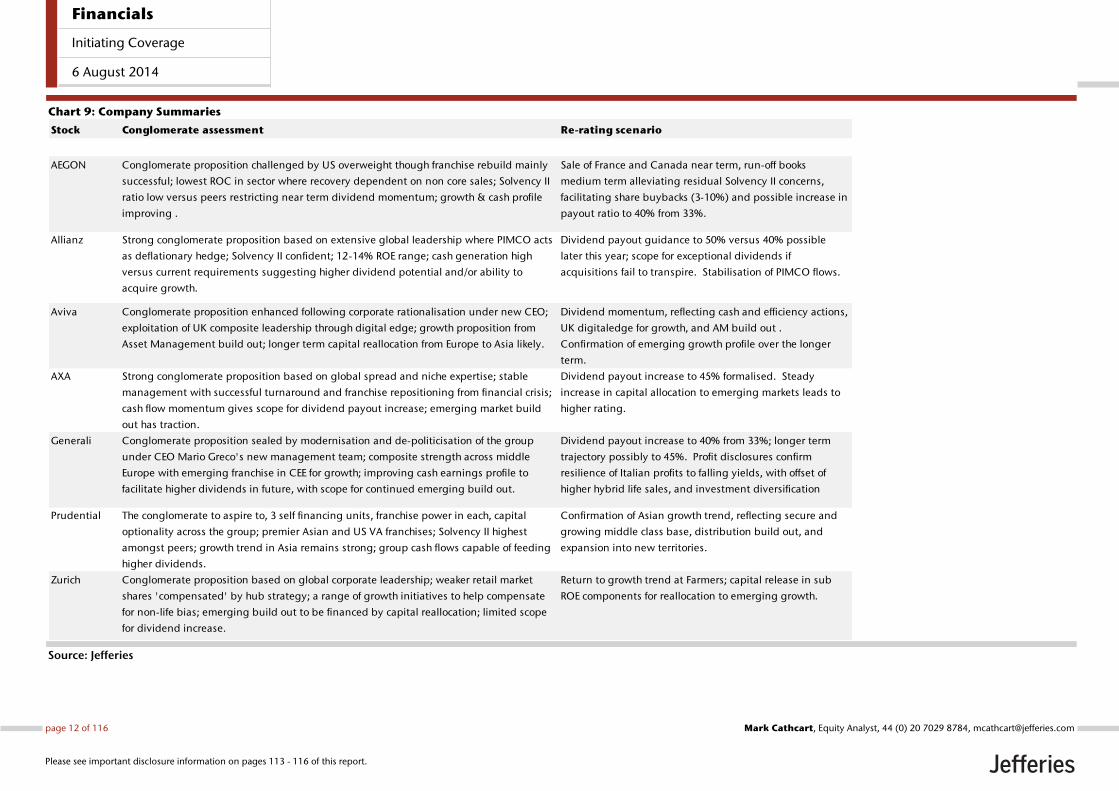

Chart 9: Company Summaries

Source: Jefferies

Stock Conglomerate assessment Re-rating scenario

AEGON Conglomerate proposition challenged by US overweight though franchise rebuild mainly

successful; lowest ROC in sector where recovery dependent on non core sales; Solvency II

ratio low versus peers restricting near term dividend momentum; growth & cash profile

improving .

Sale of France and Canada near term, run-off books

medium term alleviating residual Solvency II concerns,

facilitating share buybacks (3-10%) and possible increase in

payout ratio to 40% from 33%.

Allianz Strong conglomerate proposition based on extensive global leadership where PIMCO acts

as deflationary hedge; Solvency II confident; 12-14% ROE range; cash generation high

versus current requirements suggesting higher dividend potential and/or ability to

acquire growth.

Dividend payout guidance to 50% versus 40% possible

later this year; scope for exceptional dividends if

acquisitions fail to transpire. Stabilisation of PIMCO flows.

Aviva Conglomerate proposition enhanced following corporate rationalisation under new CEO;

exploitation of UK composite leadership through digital edge; growth proposition from

Asset Management build out; longer term capital reallocation from Europe to Asia likely.

Dividend momentum, reflecting cash and efficiency actions,

UK digitaledge for growth, and AM build out .

Confirmation of emerging growth profile over the longer

term.

AXA Strong conglomerate proposition based on global spread and niche expertise; stable

management with successful turnaround and franchise repositioning from financial crisis;

cash flow momentum gives scope for dividend payout increase; emerging market build

out has traction.

Dividend payout increase to 45% formalised. Steady

increase in capital allocation to emerging markets leads to

higher rating.

Generali Conglomerate proposition sealed by modernisation and de-politicisation of the group

under CEO Mario Greco's new management team; composite strength across middle

Europe with emerging franchise in CEE for growth; improving cash earnings profile to

facilitate higher dividends in future, with scope for continued emerging build out.

Dividend payout increase to 40% from 33%; longer term

trajectory possibly to 45%. Profit disclosures confirm

resilience of Italian profits to falling yields, with offset of

higher hybrid life sales, and investment diversification

Prudential The conglomerate to aspire to, 3 self financing units, franchise power in each, capital

optionality across the group; premier Asian and US VA franchises; Solvency II highest

amongst peers; growth trend in Asia remains strong; group cash flows capable of feeding

higher dividends.

Confirmation of Asian growth trend, reflecting secure and

growing middle class base, distribution build out, and

expansion into new territories.

Zurich Conglomerate proposition based on global corporate leadership; weaker retail market

shares 'compensated' by hub strategy; a range of growth initiatives to help compensate

for non-life bias; emerging build out to be financed by capital reallocation; limited scope

for dividend increase.

Return to growth trend at Farmers; capital release in sub

ROE components for reallocation to emerging growth.

Financials

Initiating Coverage

6 August 2014

page 12 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

Report outline

Corporate Assessment…………………………………………………….………………………………14

Corporate governance has transformed: simplified reporting lines,

centralised underwriting and expense controls, with cash flows streamlined to

the holding. Following the recent overhauls at Aviva and Generali, all

companies have now ‘modernised’.

The conglomerate proposition has gained definition, with non-core

exits and franchise rebuilds leading to a sequence of groups with rationalised

geographic presence and global offerings of expertise.

Solvency II is set for formal introduction next year. All ‘seven’ appear

comfortably capitalised on our analysis (AEGON at the lower end) and able to

withstand a deflationary shock

Returns have recovered to double-digit levels despite the significantly higher

level of capital requirements imposed, where the profitability drag from the life

back book should decline further over time.

Prudential has set the growth aspiration for the rest of the sector. The

conglomerate growth profile appears low single digit, but with a range of

growth strategies in place to lift this higher.

Cash has become the key attraction for the sector, with product

transformation in life leading to faster cash release, and corporate restructuring

leading to higher cash flows to the holding.

Increases in the dividend pay-out ratios are likely over the medium term

even in a deflationary backdrop.

Growth investment potential; reallocate capital to emerging growth.

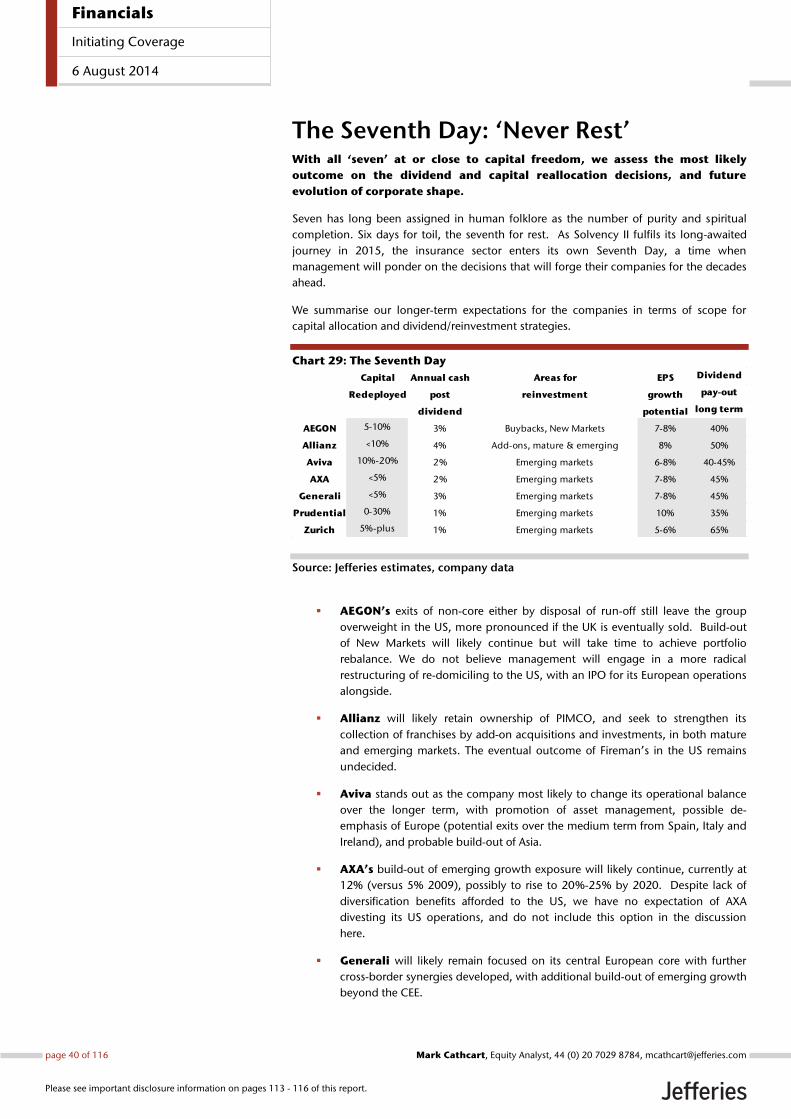

The Seventh Day……………………………………………………….…………………………………….40

We consider the likely cash and capital strategies for each of the companies,

and long-term scope for higher dividend pay-outs and earnings growth.

Conglomerate Premium………………………………………………………………………….…..…44

The larger-cap conglomerate insurers trade at a 17% discount to the small/mid-

caps, unmerited in our view given the diversification benefits that should be

afforded to the valuation if not the capital.

Company Sections: Brief overviews, p&l, cash flow, solvency, ROCs & valuation……..47

Appendices: Valuation, Financial Markets, Recent Performance, History…....90

We allocate capital using a factor-based approach, and value the companies on

a multi-stage residual income basis.

We cross check the longer-term growth rates and dividend paying

capacity suggested by our analysis with current market expectations

implied by the current share price using dividend discount modelling,

where the market unsurprisingly appears to be factoring in only limited

expectations of dividend growth.

We stress test valuations for deflationary and reflationary trends recognising

the asymmetric risk to the downside.

Recent share price performance driven by markets, and company specifics.

The Conglomer-creation: A historical overview on conglomeration and

leverage of the past that led to the last decade of capital and operational repair

The Long Views on each stock…………………………………………………………………..…….106

2) Conglomerate Franchise

3) Capital

4) Returns

5) Growth

6) Cash

7) Dividend

Corporate Assessment

The Seventh Day

The Conglomerate Premium

The Seven Insurance Wonders

Appendices:-

Appendix 1 Capital Allocation

Appendix 2 Valuation

The Long View

Appendix 4 Recent Performance

Appendix 3 Financial Markets

1) Corporate Will

Appendix 5 The Conglomer-creation

Financials

Initiating Coverage

6 August 2014

page 13 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

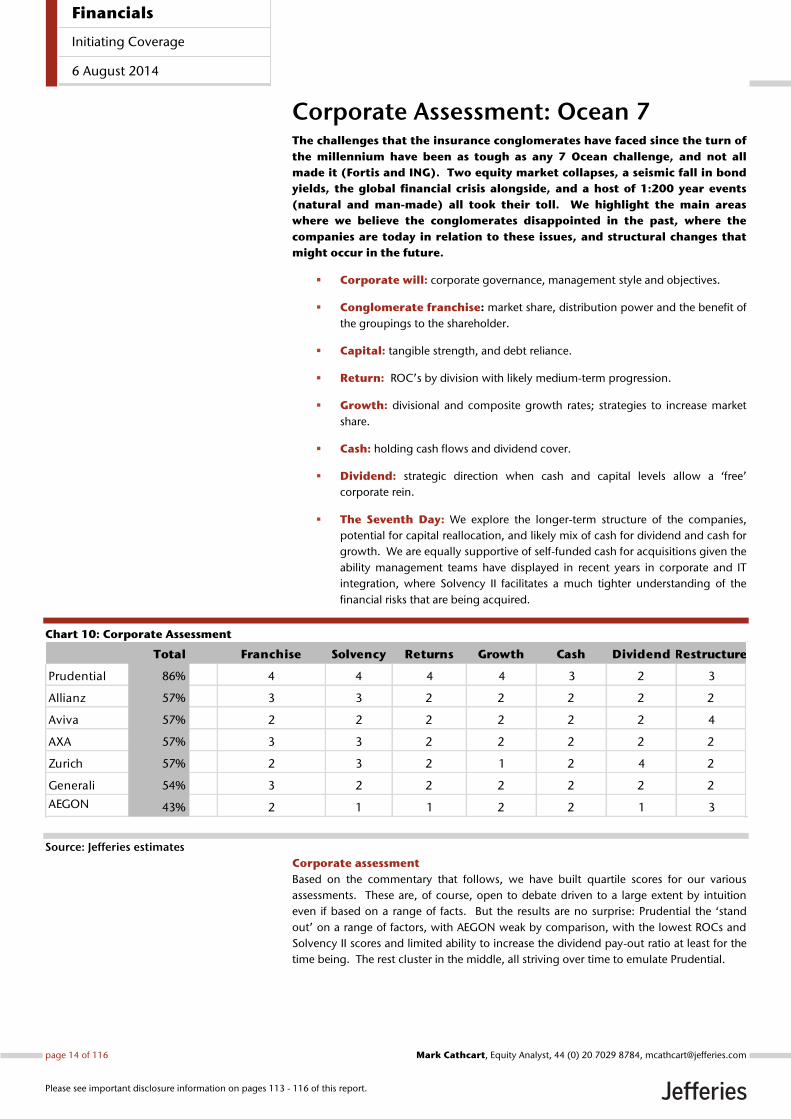

Corporate Assessment: Ocean 7 The challenges that the insurance conglomerates have faced since the turn of

the millennium have been as tough as any 7 Ocean challenge, and not all

made it (Fortis and ING). Two equity market collapses, a seismic fall in bond

yields, the global financial crisis alongside, and a host of 1:200 year events

(natural and man-made) all took their toll. We highlight the main areas

where we believe the conglomerates disappointed in the past, where the

companies are today in relation to these issues, and structural changes that

might occur in the future.

Corporate will: corporate governance, management style and objectives.

Conglomerate franchise: market share, distribution power and the benefit of

the groupings to the shareholder.

Capital: tangible strength, and debt reliance.

Return: ROC’s by division with likely medium-term progression.

Growth: divisional and composite growth rates; strategies to increase market

share.

Cash: holding cash flows and dividend cover.

Dividend: strategic direction when cash and capital levels allow a ‘free’

corporate rein.

The Seventh Day: We explore the longer-term structure of the companies,

potential for capital reallocation, and likely mix of cash for dividend and cash for

growth. We are equally supportive of self-funded cash for acquisitions given the

ability management teams have displayed in recent years in corporate and IT

integration, where Solvency II facilitates a much tighter understanding of the

financial risks that are being acquired.

Chart 10: Corporate Assessment

Source: Jefferies estimates

Corporate assessment

Based on the commentary that follows, we have built quartile scores for our various

assessments. These are, of course, open to debate driven to a large extent by intuition

even if based on a range of facts. But the results are no surprise: Prudential the ‘stand

out’ on a range of factors, with AEGON weak by comparison, with the lowest ROCs and

Solvency II scores and limited ability to increase the dividend pay-out ratio at least for the

time being. The rest cluster in the middle, all striving over time to emulate Prudential.

Total Franchise Solvency Returns Growth Cash Dividend Restructure

Prudential 86% 4 4 4 4 3 2 3

Allianz 57% 3 3 2 2 2 2 2

Aviva 57% 2 2 2 2 2 2 4

AXA 57% 3 3 2 2 2 2 2

Zurich 57% 2 3 2 1 2 4 2

Generali 54% 3 2 2 2 2 2 2

AEGON 43% 2 1 1 2 2 1 3

Financials

Initiating Coverage

6 August 2014

page 14 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

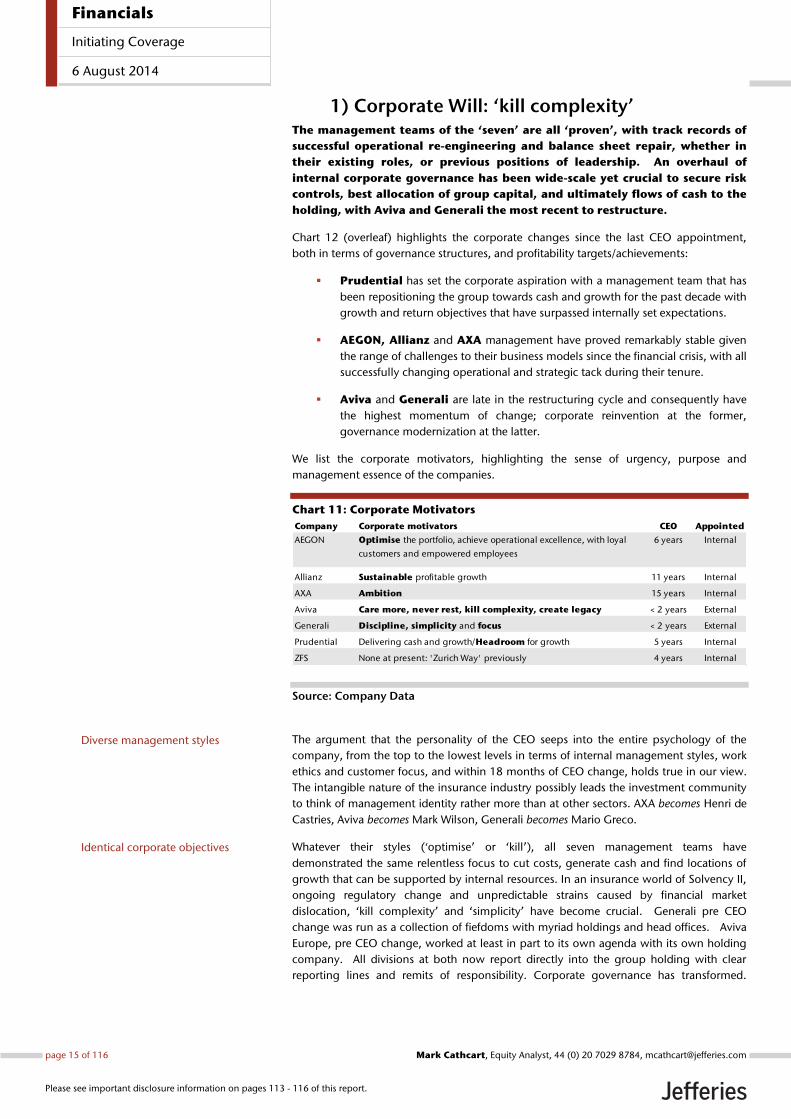

1) Corporate Will: ‘kill complexity’ The management teams of the ‘seven’ are all ‘proven’, with track records of

successful operational re-engineering and balance sheet repair, whether in

their existing roles, or previous positions of leadership. An overhaul of

internal corporate governance has been wide-scale yet crucial to secure risk

controls, best allocation of group capital, and ultimately flows of cash to the

holding, with Aviva and Generali the most recent to restructure.

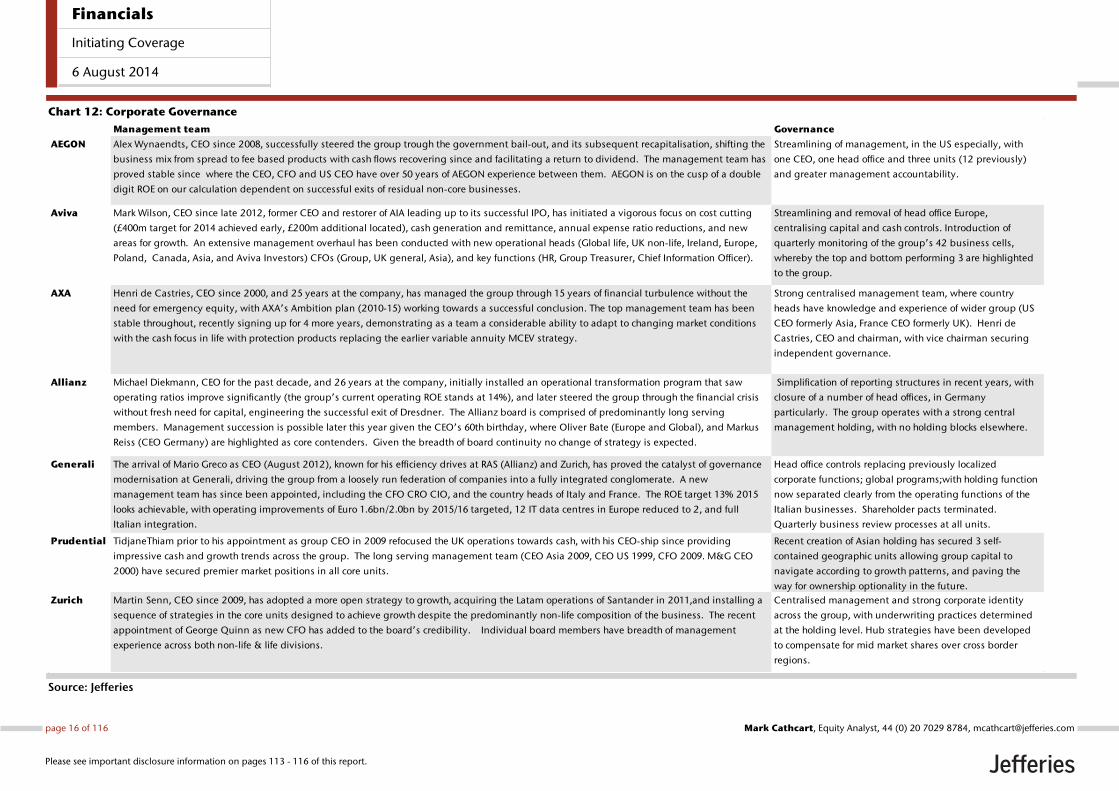

Chart 12 (overleaf) highlights the corporate changes since the last CEO appointment,

both in terms of governance structures, and profitability targets/achievements:

Prudential has set the corporate aspiration with a management team that has

been repositioning the group towards cash and growth for the past decade with

growth and return objectives that have surpassed internally set expectations.

AEGON, Allianz and AXA management have proved remarkably stable given

the range of challenges to their business models since the financial crisis, with all

successfully changing operational and strategic tack during their tenure.

Aviva and Generali are late in the restructuring cycle and consequently have

the highest momentum of change; corporate reinvention at the former,

governance modernization at the latter.

We list the corporate motivators, highlighting the sense of urgency, purpose and

management essence of the companies.

Chart 11: Corporate Motivators

Source: Company Data

The argument that the personality of the CEO seeps into the entire psychology of the

company, from the top to the lowest levels in terms of internal management styles, work

ethics and customer focus, and within 18 months of CEO change, holds true in our view.

The intangible nature of the insurance industry possibly leads the investment community

to think of management identity rather more than at other sectors. AXA becomes Henri de

Castries, Aviva becomes Mark Wilson, Generali becomes Mario Greco.

Whatever their styles (‘optimise’ or ‘kill’), all seven management teams have

demonstrated the same relentless focus to cut costs, generate cash and find locations of

growth that can be supported by internal resources. In an insurance world of Solvency II,

ongoing regulatory change and unpredictable strains caused by financial market

dislocation, ‘kill complexity’ and ‘simplicity’ have become crucial. Generali pre CEO

change was run as a collection of fiefdoms with myriad holdings and head offices. Aviva

Europe, pre CEO change, worked at least in part to its own agenda with its own holding

company. All divisions at both now report directly into the group holding with clear

reporting lines and remits of responsibility. Corporate governance has transformed.

Company Corporate motivators CEO Appointed

AEGON Optimise the portfolio, achieve operational excellence, with loyal

customers and empowered employees

6 years Internal

Allianz Sustainable profitable growth 11 years Internal

AXA Ambition 15 years Internal

Aviva Care more, never rest, kill complexity, create legacy < 2 years External

Generali Discipline, simplicity and focus < 2 years External

Prudential Delivering cash and growth/Headroom for growth 5 years Internal

ZFS None at present: 'Zurich Way' previously 4 years Internal

Diverse management styles

Identical corporate objectives

Financials

Initiating Coverage

6 August 2014

page 15 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

Chart 12: Corporate Governance

Source: Jefferies

Management team Governance

AEGON Alex Wynaendts, CEO since 2008, successfully steered the group trough the government bail-out, and its subsequent recapitalisation, shifting the

business mix from spread to fee based products with cash flows recovering since and facilitating a return to dividend. The management team has

proved stable since where the CEO, CFO and US CEO have over 50 years of AEGON experience between them. AEGON is on the cusp of a double

digit ROE on our calculation dependent on successful exits of residual non-core businesses.

Streamlining of management, in the US especially, with

one CEO, one head office and three units (12 previously)

and greater management accountability.

Aviva Mark Wilson, CEO since late 2012, former CEO and restorer of AIA leading up to its successful IPO, has initiated a vigorous focus on cost cutting

(£400m target for 2014 achieved early, £200m additional located), cash generation and remittance, annual expense ratio reductions, and new

areas for growth. An extensive management overhaul has been conducted with new operational heads (Global life, UK non-life, Ireland, Europe,

Poland, Canada, Asia, and Aviva Investors) CFOs (Group, UK general, Asia), and key functions (HR, Group Treasurer, Chief Information Officer).

Streamlining and removal of head office Europe,

centralising capital and cash controls. Introduction of

quarterly monitoring of the group’s 42 business cells,

whereby the top and bottom performing 3 are highlighted

to the group.

AXA Henri de Castries, CEO since 2000, and 25 years at the company, has managed the group through 15 years of financial turbulence without the

need for emergency equity, with AXA’s Ambition plan (2010-15) working towards a successful conclusion. The top management team has been

stable throughout, recently signing up for 4 more years, demonstrating as a team a considerable ability to adapt to changing market conditions

with the cash focus in life with protection products replacing the earlier variable annuity MCEV strategy.

Strong centralised management team, where country

heads have knowledge and experience of wider group (US

CEO formerly Asia, France CEO formerly UK). Henri de

Castries, CEO and chairman, with vice chairman securing

independent governance.

Allianz Michael Diekmann, CEO for the past decade, and 26 years at the company, initially installed an operational transformation program that saw

operating ratios improve significantly (the group’s current operating ROE stands at 14%), and later steered the group through the financial crisis

without fresh need for capital, engineering the successful exit of Dresdner. The Allianz board is comprised of predominantly long serving

members. Management succession is possible later this year given the CEO’s 60th birthday, where Oliver Bate (Europe and Global), and Markus

Reiss (CEO Germany) are highlighted as core contenders. Given the breadth of board continuity no change of strategy is expected.

Simplification of reporting structures in recent years, with

closure of a number of head offices, in Germany

particularly. The group operates with a strong central

management holding, with no holding blocks elsewhere.

Generali The arrival of Mario Greco as CEO (August 2012), known for his efficiency drives at RAS (Allianz) and Zurich, has proved the catalyst of governance

modernisation at Generali, driving the group from a loosely run federation of companies into a fully integrated conglomerate. A new

management team has since been appointed, including the CFO CRO CIO, and the country heads of Italy and France. The ROE target 13% 2015

looks achievable, with operating improvements of Euro 1.6bn/2.0bn by 2015/16 targeted, 12 IT data centres in Europe reduced to 2, and full

Italian integration.

Head office controls replacing previously localized

corporate functions; global programs;with holding function

now separated clearly from the operating functions of the

Italian businesses. Shareholder pacts terminated.

Quarterly business review processes at all units.

Prudential TidjaneThiam prior to his appointment as group CEO in 2009 refocused the UK operations towards cash, with his CEO-ship since providing

impressive cash and growth trends across the group. The long serving management team (CEO Asia 2009, CEO US 1999, CFO 2009. M&G CEO

2000) have secured premier market positions in all core units.

Recent creation of Asian holding has secured 3 self-

contained geographic units allowing group capital to

navigate according to growth patterns, and paving the

way for ownership optionality in the future.

Zurich Martin Senn, CEO since 2009, has adopted a more open strategy to growth, acquiring the Latam operations of Santander in 2011,and installing a

sequence of strategies in the core units designed to achieve growth despite the predominantly non-life composition of the business. The recent

appointment of George Quinn as new CFO has added to the board’s credibility. Individual board members have breadth of management

experience across both non-life & life divisions.

Centralised management and strong corporate identity

across the group, with underwriting practices determined

at the holding level. Hub strategies have been developed

to compensate for mid market shares over cross border

regions.

Financials

Initiating Coverage

6 August 2014

page 16 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

2) Conglomerate franchise: ‘focus’ Insurance conglomerates have been gaining definition across the sector since

the financial crisis through non-core exits and focus on strengths. Prudential

is the corporate paradigm for now, though we note the ongoing

improvements elsewhere, where franchise rebuilds have been required in a

number of core markets.

The conglomerate proposition

Prudential the paradigm franchise: number one rankings (UK asset management,

US variable annuities, the market leading Asian franchise) with brand strengths that can

each generate their own momentum: ‘M&G’ and ‘Prudential’ in the UK, ‘Jackson’ in the

US, with the ‘Prudential’ brand on bill boards and neon lights across vast swathes of Asia

as visible as any Coca Cola. The UK has purposefully been pared back in product base to

form a cash generator for the group; Asia is building its own franchise power feeding

earnings growth to the group level, self-funding, and where success in Indonesia is

inspiring distribution partners to team up with Prudential elsewhere (most recently

Thanachart in Thailand); Jackson is an expert in drawdown annuity products, relevant to

the UK division post annuity budget changes, and arguably de-risks the group to any

negative economic development in Asia post tapering, with any rise in US interest rates

accompanying the tapering trend increasing Jackson’s economic value.

We assess the conglomerate proposition at the other six. Chart 12 sets out the

conglomerate propositions of the other companies aside from Prudential: global

leadership (Allianz non-life, AXA insurance, Zurich corporate), core strengths (AEGON

pensions and retirement savings for example), and cross-border efficiencies (Generali

most notably).

In the same chart, we address the conglomeration challenges, highlighting the two that

are most likely to impact share price ratings currently:

AEGON ‘US heavy’: Solvency II will most likely disallow diversification benefits

for US businesses (>50% of the total). Earlier attempts to grow Europe to

compensate stalled (UK RDR dislocation, CEE pension rule changes), but are

likely to be reinvigorated post capital repair.

Allianz’s PIMCO rationale: Profits from the global leader in bond asset

management have increased to close to 30% of group total in recent years.

Profit streams at PIMCO rise as interest rates fall with fees increasing on rising

bond values, a trend that neatly offsets the negative impact of falling yields on

life guarantees in the European portfolio. PIMCO outflows have proved

problematic over the past year, following US tapering and the bond markets

sell-off, exacerbated by a performance blip in Bill Gross’s core fund, and the

resignation of the group CEO earlier this year. Allianz remain committed to

PIMCO as its in-house asset manager, and has responded by significant fund

diversification over the past year, and management strengthening (the

appointment of six new deputy CIO’s alongside Bill Gross as CIO, with the new

CEO former COO).

The franchise collection

Market shares and rankings for each of the companies are listed on a by-country basis in

the later company sections, with customer segmentation and product focus highlighted

within countries where relevant. Non-core sales have been especially helpful in this

regard (AEGON US reinsurance, Allianz Dresdner, Aviva Amerus, AXA UK life, Generali US

reinsurance & Migdal Israel, Prudential Egg, Zurich Scudder & Converium).

Financial market moves (falling bond yields impacting spread-based products with

guarantees), regulatory changes (UK budget impact on UK annuities for example), and

distribution shifts (migration to direct and internet from traditional agency) can lead to

product lines becoming suddenly unprofitable and business models that risk redundancy.

Non-core exits

Franchise rebuilds

Financials

Initiating Coverage

6 August 2014

page 17 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

We highlight the core threats that each company has faced under current management

teams and the effectiveness of the response. AEGON and AXA have been noteworthy in

this regard with wide-scale product overhaul successfully achieved post financial crisis.

Aviva is currently reinvigorating its business proposition across its core markets.

AEGON: The group has required a sequence of franchise rebuilds: in the US

from spread-based products (fixed annuities, GICs) to fee income (variable

annuity, pensions funds) to compensate for low interest rates; in the UK from

IFA to platform distribution post RDR dislocation; and in the Dutch market an

increased focus on corporate pensions where individual life is being eroded by

increased competition from the banks following regulatory change. The US

rebuild has proved remarkably successful with notable momentum in the fee-

driven components of VA and pensions; the Dutch group pension business has

further consolidated its market leadership, where AEGON Bank and Knab (on-

line banking) should help preserve individual life rankings; the UK has yet to

convince, however, where the platform strategy designed to offset IFA

dependency is in the final phase of build-out.

Allianz: Reliance on tied agency distribution in Germany, where Allianz is

market leader, has been a perennial concern, but where brand strength, a range

of innovative products in life (Perspective and Index) and modular packaging in

non-life has so far maintained if not enhanced market shares.

Aviva: Market shares in UK life and non-life have been steadily falling in recent

years from mid-teens to closer to 10%. The new management team are

confident of a return to growth over the next 12 months, with their

technological edge, market leading app, website that gives customer access to

all Aviva products, and purchase ability. The planned build-out of Aviva

Investors under new management, with Euan Munroe seeking to replicate his

success of GARs at Standard Life with AIMs, should also help the UK proposition.

AXA: The life offering has transformed across the group over the past five years,

from traditional savings to unit linked and protection, with the US VA offering

successfully overhauled in the process. The build-out of emerging growth has

also been notable (12% of group profits more than doubling since 2009).

Generali: The Italian life business is in the process of refocusing sales away

from traditional savings to hybrid products with unit-linked elements under the

new management team. Initial signs of momentum following this year’s

product launch bode well.

Prudential: Asian focus on unit-linked investment policies with health and

protection riders (CEO Asia Barry Stowe was head of health at AIA before his

arrival in 2006) has successfully located the core insurance need of the growing

middle classes, driving substantial growth in recent years. The US annuity

business in the mean-time has benefited from above-market growth in variable

annuities thanks to its conservative hedging programme ahead of the financial

crisis. The move towards cash focused life a decade ago in the UK, as well as

Asia and the US, has been inspirational to the rest of the sector.

Zurich: Farmers management in the US has recently adopted an ‘omni’ sales

approach (agencies and direct working in connection) to combat loss of market

share to the direct writers in their core auto business.

Financials

Initiating Coverage

6 August 2014

page 18 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

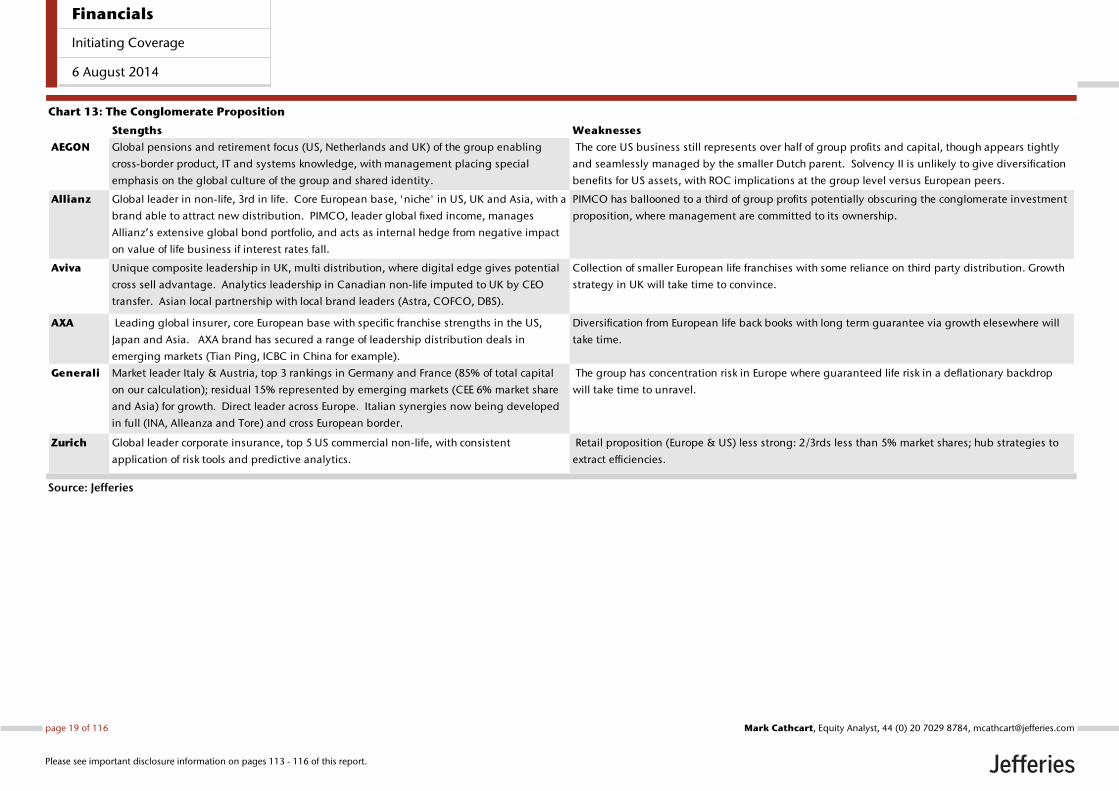

Chart 13: The Conglomerate Proposition

Source: Jefferies

Stengths Weaknesses

AEGON Global pensions and retirement focus (US, Netherlands and UK) of the group enabling

cross-border product, IT and systems knowledge, with management placing special

emphasis on the global culture of the group and shared identity.

The core US business still represents over half of group profits and capital, though appears tightly

and seamlessly managed by the smaller Dutch parent. Solvency II is unlikely to give diversification

benefits for US assets, with ROC implications at the group level versus European peers.

Allianz Global leader in non-life, 3rd in life. Core European base, 'niche' in US, UK and Asia, with a

brand able to attract new distribution. PIMCO, leader global fixed income, manages

Allianz’s extensive global bond portfolio, and acts as internal hedge from negative impact

on value of life business if interest rates fall.

PIMCO has ballooned to a third of group profits potentially obscuring the conglomerate investment

proposition, where management are committed to its ownership.

Aviva Unique composite leadership in UK, multi distribution, where digital edge gives potential

cross sell advantage. Analytics leadership in Canadian non-life imputed to UK by CEO

transfer. Asian local partnership with local brand leaders (Astra, COFCO, DBS).

Collection of smaller European life franchises with some reliance on third party distribution. Growth

strategy in UK will take time to convince.

AXA Leading global insurer, core European base with specific franchise strengths in the US,

Japan and Asia. AXA brand has secured a range of leadership distribution deals in

emerging markets (Tian Ping, ICBC in China for example).

Diversification from European life back books with long term guarantee via growth elesewhere will

take time.

Generali Market leader Italy & Austria, top 3 rankings in Germany and France (85% of total capital

on our calculation); residual 15% represented by emerging markets (CEE 6% market share

and Asia) for growth. Direct leader across Europe. Italian synergies now being developed

in full (INA, Alleanza and Tore) and cross European border.

The group has concentration risk in Europe where guaranteed life risk in a deflationary backdrop

will take time to unravel.

Zurich Global leader corporate insurance, top 5 US commercial non-life, with consistent

application of risk tools and predictive analytics.

Retail proposition (Europe & US) less strong: 2/3rds less than 5% market shares; hub strategies to

extract efficiencies.

Financials

Initiating Coverage

6 August 2014

page 19 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

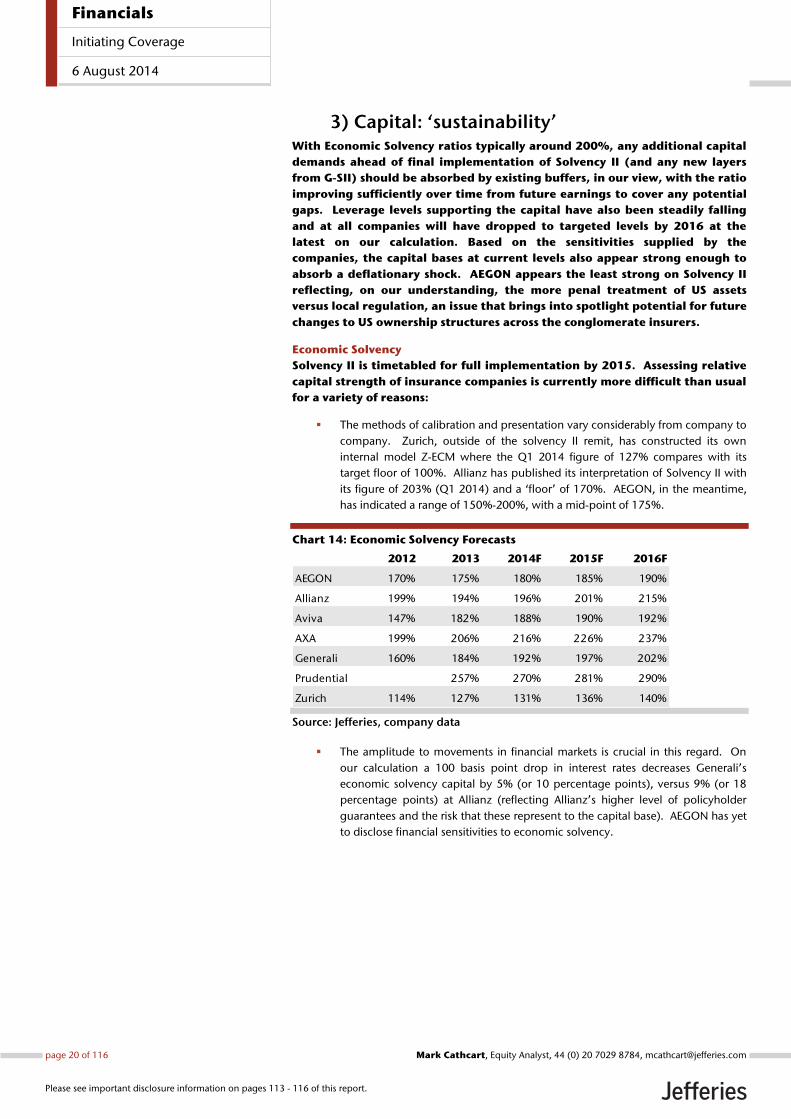

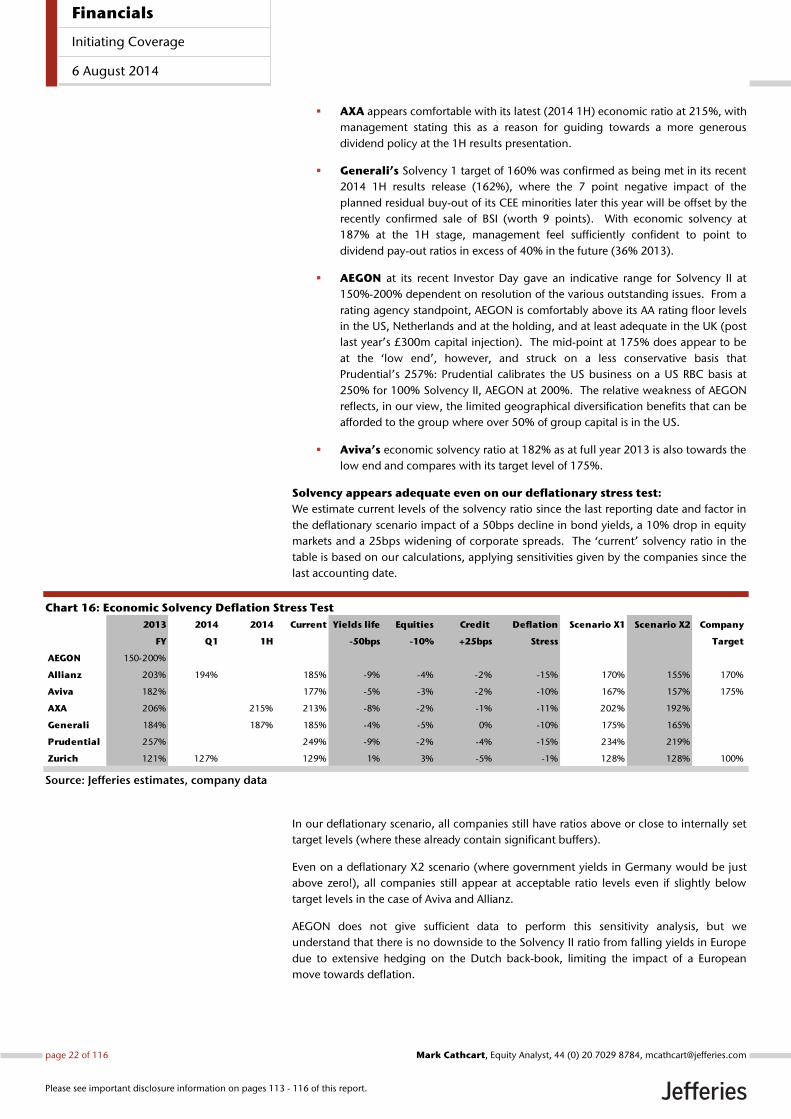

3) Capital: ‘sustainability’ With Economic Solvency ratios typically around 200%, any additional capital

demands ahead of final implementation of Solvency II (and any new layers

from G-SII) should be absorbed by existing buffers, in our view, with the ratio

improving sufficiently over time from future earnings to cover any potential

gaps. Leverage levels supporting the capital have also been steadily falling

and at all companies will have dropped to targeted levels by 2016 at the

latest on our calculation. Based on the sensitivities supplied by the

companies, the capital bases at current levels also appear strong enough to

absorb a deflationary shock. AEGON appears the least strong on Solvency II

reflecting, on our understanding, the more penal treatment of US assets

versus local regulation, an issue that brings into spotlight potential for future

changes to US ownership structures across the conglomerate insurers.

Economic Solvency

Solvency II is timetabled for full implementation by 2015. Assessing relative

capital strength of insurance companies is currently more difficult than usual

for a variety of reasons:

The methods of calibration and presentation vary considerably from company to

company. Zurich, outside of the solvency II remit, has constructed its own

internal model Z-ECM where the Q1 2014 figure of 127% compares with its

target floor of 100%. Allianz has published its interpretation of Solvency II with

its figure of 203% (Q1 2014) and a ‘floor’ of 170%. AEGON, in the meantime,

has indicated a range of 150%-200%, with a mid-point of 175%.

Chart 14: Economic Solvency Forecasts

Source: Jefferies, company data

The amplitude to movements in financial markets is crucial in this regard. On

our calculation a 100 basis point drop in interest rates decreases Generali’s

economic solvency capital by 5% (or 10 percentage points), versus 9% (or 18

percentage points) at Allianz (reflecting Allianz’s higher level of policyholder

guarantees and the risk that these represent to the capital base). AEGON has yet

to disclose financial sensitivities to economic solvency.

2012 2013 2014F 2015F 2016F

AEGON 170% 175% 180% 185% 190%

Allianz 199% 194% 196% 201% 215%

Aviva 147% 182% 188% 190% 192%

AXA 199% 206% 216% 226% 237%

Generali 160% 184% 192% 197% 202%

Prudential 257% 270% 281% 290%

Zurich 114% 127% 131% 136% 140%

Financials

Initiating Coverage

6 August 2014

page 20 of 116 , Equity Analyst, 44 (0) 20 7029 8784, [email protected] Cathcart

Please see important disclosure information on pages 113 - 116 of this report.

Chart 15: Economic Solvency Sensitivities %

Source: Jefferies estimates

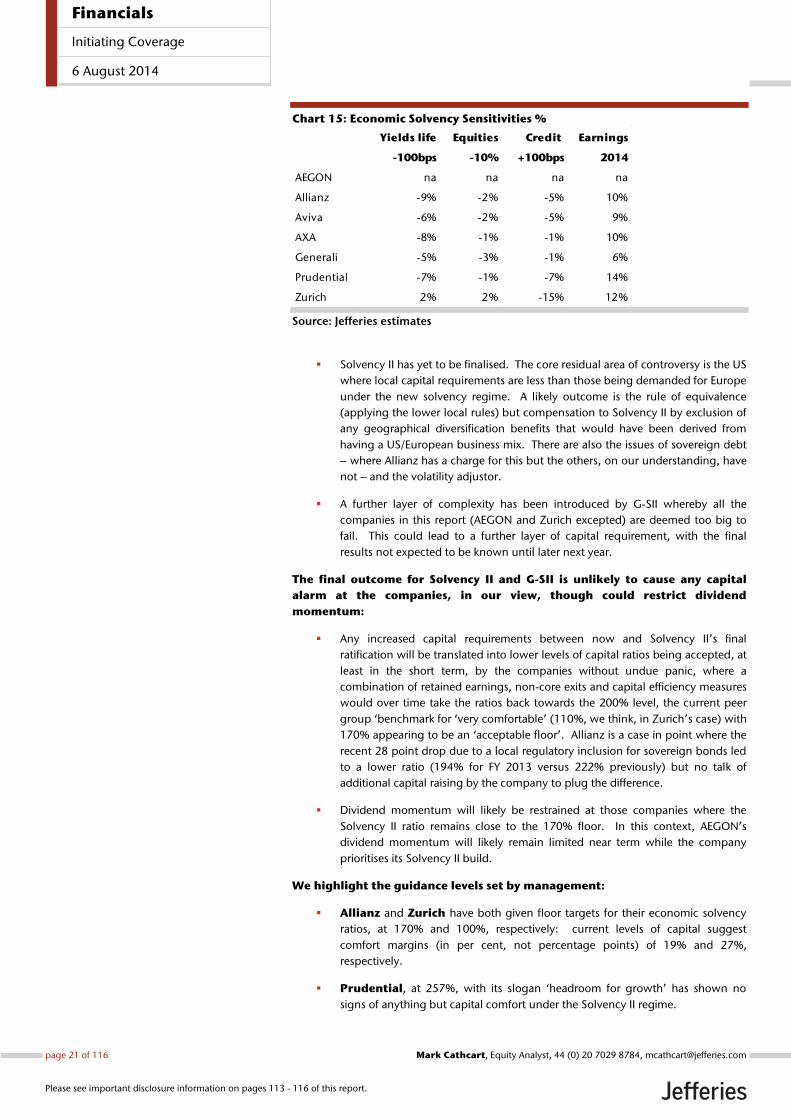

Solvency II has yet to be finalised. The core residual area of controversy is the US

where local capital requirements are less than those being demanded for Europe

under the new solvency regime. A likely outcome is the rule of equivalence

(applying the lower local rules) but compensation to Solvency II by exclusion of

any geographical diversification benefits that would have been derived from

having a US/European business mix. There are also the issues of sovereign debt

– where Allianz has a charge for this but the others, on our understanding, have

not – and the volatility adjustor.

A further layer of complexity has been introduced by G-SII whereby all the