European Insolvency Procedures - 2010 Edition

99

European Insolvency Procedures - 2010 Edition

Transcript of European Insolvency Procedures - 2010 Edition

European InsolvencyProcedures - 2010 Edition

© Clifford Chance LLP, July 2010

ContentsChapter Page

European Regulation on Insolvency Proceedings . . . . . . . . . . . . . . . . . . . . . . . 4

England & Wales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

France . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Italy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Luxembourg . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Belgium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Germany . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Spain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

The Netherlands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Poland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

The Czech Republic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

The Slovak Republic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Romania . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

Ukraine . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

Hungary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

Insolvency and Restructuring Trends in Europe - Summary Table

Automatic Stay and Rescue Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

Cram Down of Creditors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

Position of Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

Personal Liability of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

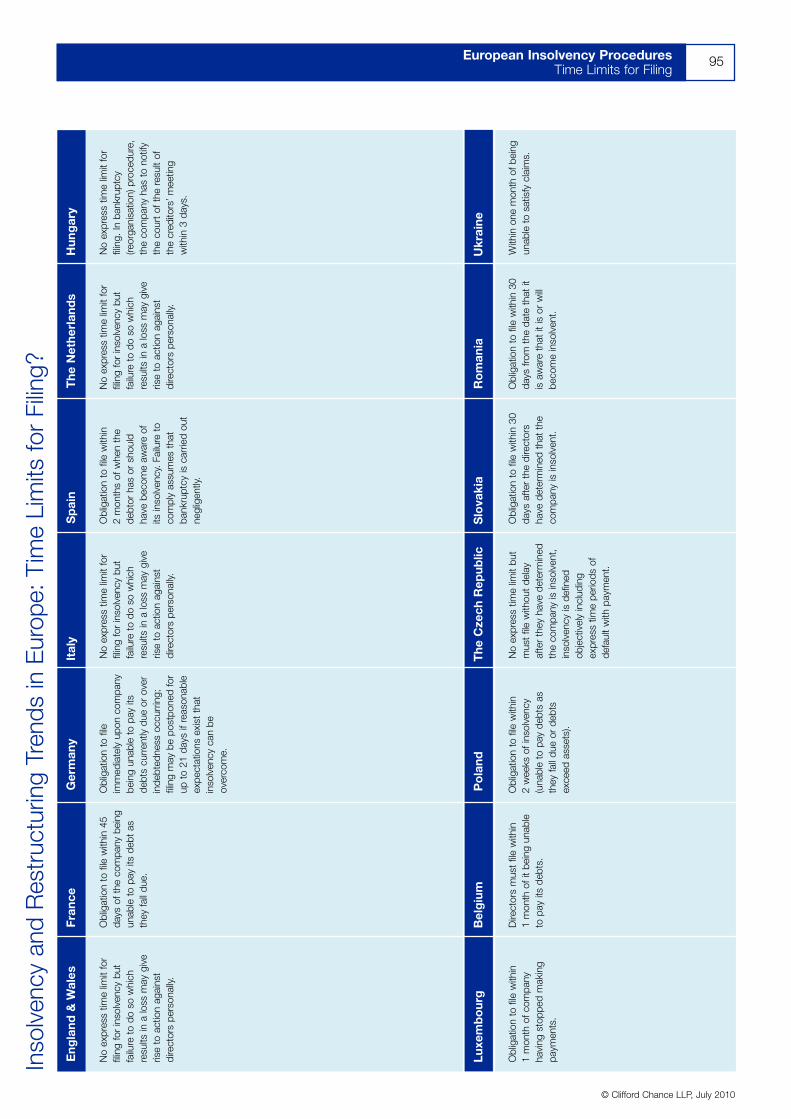

Time Limits for Filing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

New Reforms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

Clifford Chance Contacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

European Insolvency ProceduresContents

IntroductionThis note primarily focuses on theinsolvency considerations and legislationin specific European jurisdictions.However, before considering theindividual jurisdictions, it is important torecognise the influence of the pan-European legislation.

The European Regulation on InsolvencyProceedings (Council Regulation1346/2000) (“the Regulation”) came intoeffect on 31 May 2002. It applies to allEU member states except Denmark(including the European countries thathave joined the EU since that date.)

The Regulation does not provide uniformsubstantive law provisions for membersof the European Union. The purpose ofthe Regulation is primarily to codify howa member state should determinewhether it has jurisdiction to openinsolvency proceedings, whilst alsoimposing a uniform approach to thegoverning law which is applicable tothose proceedings. Once these factorshave been determined, the proceduralrules of the member state in whichproceedings are opened will generallyapply. The Regulation also provides forthe automatic recognition of insolvencyproceedings throughout the EU.

ScopeThe Regulation applies to all collectiveinsolvency proceedings which entail thepartial or total divestment of a debtorand the appointment of a liquidator orsimilar insolvency officeholder. TheRegulation primarily applies to

corporates and individuals within themember states. This encompassesvarious corporate entities such astrading companies, special purposevehicles and group treasury companies.Its scope of application is confined toparties with their centre of main interestswithin a member state of the EU. (Ittherefore applies to entities whose placeof incorporation may be outside of theEU, but whose centre of main interestsis within a member state.)

The Regulation does not apply toentities who do not have their centre ofmain interests within a member state.The extent to which insolvencyproceedings from outside of the EU arerecognised, depends upon the domesticlegislation and practice of eachparticular member state. (See theseparate sections for individual memberstates.)

The Regulation does not apply to banks,credit institutions, insurance companies,investment undertakings which holdfunds or securities for third parties, orcollective investment schemes. Thereorganisation and winding up of creditinstitutions is addressed in CouncilDirective 2001/24 and the reorganisationand winding up of insuranceundertakings is addressed in CouncilDirective 2001/17. These two directivesare beyond the scope of this note.

JurisdictionThe primary jurisdiction for insolvencyproceedings, as provided by theRegulation, is the court of the memberstate where the debtor’s centre of main

interests is located. In the case of acompany or other legal person, in theabsence of proof to the contrary, there is a rebuttable presumption that this iswhere the registered office of thecompany is located.

The Regulation allows for the courts incountries other than the home state toopen “territorial” insolvency proceedingsor, after the commencement of mainproceedings “secondary” proceedings,in the event that such debtor possessesan establishment in the territory of suchother member state. The applicable lawof such territorial or secondaryinsolvency proceedings will be the law of that other member state. However,territorial insolvency proceedings orsecondary insolvency proceedings arelimited in scope to the debtor’s assets in that member state and so will notextend beyond the member state wherethey are opened. Furthermore, under theRegulation, secondary proceedings arelimited to winding-up proceedings.

Governing LawThe Regulation imposes a unified codefor the governing law which, inconjunction with the mandatory regimeof jurisdiction rules, aims to enable thosewho have dealings with a debtor whosecentre of main interests is within the EUto identify with greater certainty thesubstantive legal provisions by whichtheir rights will be determined in theevent of the debtor’s insolvency. Thegeneral rule is that the law applicable to the insolvency proceedings and itseffects shall be that of the member state within the territory in which such

European Insolvency ProceduresEuropean Regulation on Insolvency Proceedings

© Clifford Chance LLP, July 2010

4

Key Elements:

n Effective since May 2002

n To promote recognition and co-operation between different insolvency regimes of individual member states within the EU

n Unified code for governing law rules

n Concept of “centre of main interests” to determine opening of main proceedings

n Jurisdiction for the opening of territorial or secondary proceedings

n Carve outs include rights in rem and rights of set-off

n Differences in legal regimes for individual member states to remain

The European Insolvency Regulation

European Insolvency Procedures

proceedings are opened.

So, unless secondary or territorialproceedings can be initiated as well, the law of the home state is likely todominate. Once the proceedings areopened the specific jurisdictionalconsiderations set out in the latter partof this note assume relevance.

The Regulation recognises that there willbe cases where strict adherence to thegeneral rule will interfere with the rulesunder which transactions are carried outin other member states, and thereforethe general rule is subject to a numberof exceptions and carve outs.

These exceptions include ‘rights in rem’including rights of security (to includeholders of floating security over afluctuating pool of assets), rights of set-off permitted by the law applicable tothe insolvent debtor’s claim, rights undera reservation of title clause, contractsrelating to immovable property, rules ofpayment systems and financial markets,contracts of employment, etc.

Disagreements BetweenMember StatesDifferent jurisdictions may interpret theRegulation in ways inconsistent witheach other. This has been apparent fromthe case law which has been generatedsince the introduction of the Regulation,which has primarily focused on thedetermination of an entity’s centre ofmain interests. No guidance is given inthe Regulation itself. Different memberstates’ interpretation of what constitutesthe centre of main interests has resultedin main proceedings being opened inmore than one member state. This issomething that the Regulation wasdesigned to avoid.

Any disagreement between memberstates as to where the centre of maininterests is located would ultimately haveto be resolved by the European Court ofJustice (“ECJ”).

Reference to The EuropeanCourt of JusticeThe first significant reference was madein 2004 to the ECJ in respect of the Irishincorporated subsidiary of the Parmalat

group, Eurofood IFSC (“Eurofood”). Inrelation to that company, a difference ofinterpretation led to two different courtsasserting that the centre of maininterests for Eurofood was in theirrespective jurisdictions. The Irish courtconsidered that Eurofood’s centre ofmain interests was in Ireland, based onthe following: it was incorporated inIreland and subject to the fiscal andregulatory controls there; the day to dayadministration was carried out in Irelandwhere the company’s accounts werealso maintained; the company’s boardmeetings took place in Ireland; and, thecreditor’s perception was that the centreof main interests was in Ireland.

The Italian courts asserted that thecentre of main interests was in Italy,based on the following: the companywas merely a conduit for the financialpolicy of the Italian parent; its exclusivepoint of reference was to the Italianparent; its operating office was in Italy;and, the central management functionwas carried out in Italy. The IrishSupreme Court referred a number ofquestions in relation to this issue to theEuropean Court. The ECJ held that theregistered office presumption could only

be rebutted if there were factorsascertainable by those dealing with thecompany that objectively establishedthat its administration was conductedelsewhere.

The ECJ further held that thepresumption could not be rebuttedsimply by producing evidence that theheadquarters of the parent company(that has the ability to make or influenceeconomic choices for its subsidiary) waselsewhere. It is to be noted that theburden of proof is placed on thoseseeking to rebut the presumption thatthe location of the registered officedetermining the centre of main interestsis a high one.

Discrepancies in the interpretation of theRegulation (in respect of extending amember state court’s jurisdiction) may in some circumstances result in forumshopping, something the Regulation wasdesigned to prevent. On a positive note,there have been examples where theRegulation has been used to facilitatepan-European restructurings byimplementing local compositions in main proceedings.

© Clifford Chance LLP, July 2010

5

IntroductionThis section is designed to provide ageneral outline of the main corporateinsolvency procedures in England andWales. Most of the legislation relevant toinsolvency is contained in the InsolvencyAct 1986 (the “Act”) and the InsolvencyRules 1986 as amended by theEnterprise Act 2002 (the “EA 2002”).

The main procedures encountered incorporate insolvencies are administrativereceivership, administration andliquidation. We also consider very brieflycompany voluntary arrangements andschemes of arrangement pursuant tothe Companies Act 2006. We considereach of these procedures in turn, thelegal basis for challenges to antecedenttransactions, and the personal liability ofdirectors.

Receivership andAdministrative ReceivershipAdministrative receiverThis is a receiver appointed over all orsubstantially all of the assets andundertakings of the company pursuantto a debenture which includes a floatingcharge. It is not technically an insolvencyprocedure, it is an enforcementmechanism used by a secured lendermost notably at a time when a companyis actually insolvent.

The introduction of the EA 2002 brought about substantial insolvency law reforms. The most significant reformwas the prohibition of the appointmentof administrative receivers by debentureholders other than pursuant to floatingcharges created prior to 15 September2003 and certain other exceptions. Theexceptions to the prohibition mean thatthe administrative receivership regime

will still be used as an enforcementmechanism.

Function and duties of receiverThe main function of the receiver is torealise the assets subject to the charge.His duty is to obtain the best pricereasonably obtainable at the time ofrealisation. The receiver owes hisprimary duty to his appointor, but alsohas subsidiary duties of good faith toguarantors of the company’s debts and to the company. He has very littleresponsibility to the unsecured creditorsof the company and is entitled to act inwhat he considers to be the bestinterests of his appointor.

The powers of the receiverThese derive from two sources:

(a) express powers granted in thedebenture or charge under which he is appointed; and

(b) statute, as an administrative receiverhas the extensive powers conferredby schedule 1 of the Act. It shouldbe noted that schedule 1 does not apply to fixed charge receivers,who have to rely on the expresspowers in the charge under whichthey were appointed and the limitedstatutory powers in the Law ofProperty Act 1925.

Power to sell charged propertyThe most significant of the powers of an administrative receiver is the powerto dispose of charged property. Anadministrative receiver has wide powersto dispose of charged property and maydo so by public auction or by privateagreement. This is generally on suchterms as he sees fit. The assets may besold separately or as part of a sale of

the business as a whole. However, sincethe receiver will generally sell without anywarranty or other recourse, the price hecan obtain for assets is generally lessthan that which would be obtained in anormal sale by the company.

Fixed charge receiverThis is a receiver appointed under a fixedcharge (i.e. a specific security interestover specific property). His role is torealise security and he is known as a“bare receiver” or “fixed charge receiver”.

AdministrationAdministration is principally a procedureintended to rescue companies which are or may become insolvent. Theprocedure has been streamlined by theEA 2002. A company can be placed intoadministration by way of an applicationto the court for an administration ordermade by either: the company; or itsdirectors; or by a creditor (includingcontingent and prospective creditors); orin certain circumstances by a clerk of aMagistrates Court. Administration mayalso be commenced without the needfor a court order initiated by the filing ofrequisite notices by: the holder of aqualifying floating charge as defined byparagraph 14 of schedule B1 of the Act;or the company; or its directors.

The overriding purpose of anadministration is to rescue a companyas a going concern. If this is notreasonably practicable, then anadministrator may perform his functionswith a view to achieving a better resultthan would be achieved if the companywere wound up. Again if this is notreasonably practicable, he may realisethe property in order to make adistribution to one or more secured orpreferential creditors.

European Insolvency ProceduresEngland & Wales

© Clifford Chance LLP, July 2010

6

Key Elements:

n Limited application of administrative receivership regime

n Administration procedure with focus on company rescue

n Practical guidance for lenders and shadow directors

n Ranking of claims in different procedures

England & Wales

European Insolvency ProceduresEngland & Wales

Effect of administrationAdministration creates a moratoriumduring which no insolvency proceedingsor other legal proceedings, includingenforcement of security, can be takenwithout the consent of the administratoror the permission of the court.

The effect of this moratorium is toenable the administrator sufficientbreathing space to formulate proposalsfor rescuing the company, or in theevent that this does not prove possible,an orderly realisation of the company’sassets.

Qualifying charge holder has choice of administratorA qualifying floating charge holder has the power to choose the identity of anadministrator, whether by making theappointment himself (if the floating chargeis enforceable) or by intervening in anapplication to court. An administratorappointed by a qualifying charge holderowes a duty to act in the best interests of the general body of creditors, notsimply his appointor. A qualifying floatingcharge holder may also be able to blockthe appointment of an administrator incertain circumstances by appointing anadministrative receiver (see above).

Powers of an administratorThe powers vested in the administratorare extensive. He is authorised to do allsuch things as may be necessary for themanagement of the affairs, business andproperty of a company. He may dismissdirectors. Also, powers of directorswhich might interfere with the exerciseby the administrator of his powers willonly be exercisable with his consent.Most importantly, an administrator hasthe power to sell the assets of thecompany, even if they are subject tosecurity (see below). He also has thepower to make distributions to thecreditors of the company (in the instanceof distributions to unsecured creditors,he must first obtain the permission ofthe court).

Property subject to fixed chargeWhere the property which theadministrator seeks to dispose of issubject to a fixed charge, or is propertyheld by the company under a hirepurchase agreement, the administrator

is first required either to obtain the leaveof the court (who will need to be satisfiedthat the disposal is likely to promote thelegitimate purposes of the administration)or the consent of the charge holder.

It will be a condition of the courtpermitting the disposal of propertysubject to a fixed charge or hirepurchase agreement that the netproceeds of the disposal must beapplied by the company first towardsmeeting the debt of the secured creditor.The administrator must sell the assets at “market value”, failing which he willhave to make up the deficiency to thesecured creditor.

Property subject to a floating chargeIf the security, as created, took the formof a floating charge, the administrator isfree to deal with and dispose of theproperty without permission of thecharge holder and without the sanctionof the court. The floating charge holder’sclaims transfer to the proceeds of saleof the charged property but his claimsrank after (a) administration liabilities, (b)costs and expenses of the administrator,and (c) claims of preferential creditors.

Importantly the administrator is entitledto use floating charge assets to fund thecontinuation of the business during theadministration. This is one of thereasons why administrators sometimeschallenge the legal nature of fixedcharges (i.e. contending the charge tobe floating rather than fixed).

LiquidationThere are two forms of liquidation,namely:

(a) winding-up by the court (sometimescalled compulsory winding-up); and

(b) voluntary winding-up.

Winding-up by the courtA compulsory liquidation begins by awinding-up order of the court made on the presentation of a petition by acreditor, the company, its directors, or a shareholder.

Grounds for a winding-up orderA company may be wound-up by thecourt in a number of circumstances

although the two most common are:

(a) that the company is unable to pay itsdebts; or

(b) that the court considers that it is justand equitable that the companyshould be wound-up.

Although it is unusual for a solventcompany to be wound-up by the court,it can happen in certain circumstanceson the ‘just and equitable’ ground. Forinstance where minority shareholders are being unfairly treated or where thereare, for example, only two shareholdersneither of whom has effective controland who cannot agree how the affairs of the company should be conducted.Winding-up is, however, an extremeremedy and minority shareholders whoare being unfairly treated are usuallybetter advised to seek alternativeremedies under section 994 of theCompanies Act 2006 which gives thecourt a broad discretion so that it can,for example, order the purchase of aminority shareholder’s shares.

Inability of a company to pay debtsA company is deemed unable to pay itsdebts if:

(a) a creditor, to whom the company isindebted in a sum exceeding £750then due, has served on thecompany a written demand (knownas a statutory demand) requiring thecompany to pay the sum so due,and the company has for threeweeks neglected to pay the sum or to secure or compound for it tothe reasonable satisfaction of thecreditor; or

(b) a judgment against the company is unsatisfied; or

(c) it is proved to the satisfaction of thecourt that the company is unable topay its debts as they fall due.

A company is also deemed unable to pay its debts if it is proved to thesatisfaction of the court that the value of the company’s assets is less than the amount of its liabilities, taking intoaccount its contingent and prospectiveliabilities.

© Clifford Chance LLP, July 2010

7

In order to obtain a winding-up order itmay not be necessary for a creditor tohave served a statutory demand on thecompany or to have an unsatisfiedjudgment debt, if it has other evidenceto demonstrate that the company isinsolvent.

Provisional liquidationAfter the presentation of a petition,where the company’s property is indanger or where it is alleged that those in control of the company aremisappropriating or wasting thecompany’s assets, an application maybe made by any creditor or contributoryor by the company itself for theappointment of a provisional liquidator,and the court in a proper case will, at any time before the making of awinding-up order, appoint one.

Duties and powers of the liquidatorThe liquidator in a compulsory liquidationis an officer of the court and subject atall times to the control of the court. He is responsible to the creditors for theconduct of the liquidation and remainsso responsible until his release asliquidator. The functions of a liquidator in a compulsory liquidation are to ensure that the company’s assets aregot in, realised and distributed to thecompany’s creditors, and to pay anysurplus to the persons entitled to it. Theliquidator or the provisional liquidator (asthe case may be) takes into his custody,or into his control, all the property towhich the company is or appears to be entitled. The powers of the directorscease. The liquidator has very broadpowers some of which may only beexercised with the sanction either of thecourt or of the liquidation committee ofcreditors. However, the liquidator onlyhas a limited power to carry on thebusiness (to the extent necessary tocollect and realise the assets) and inpractice it is relatively unusual for aliquidator to achieve a sale of thebusiness as a going concern.

Power of disclaimerIn addition to his general powers aliquidator has a special power todisclaim onerous property. It is importantto note that the power to disclaimapplies to any unprofitable contract orany other property of the company

which is unsaleable, or is not readilysaleable, or is such that it may give riseto liability to pay money or perform anyother onerous act. Property subject toonerous burdens may be disclaimedeven though it is not actually unsaleable.The most typical exercise of disclaimeris in respect of a low value leasehold.The effect of disclaimer is that iteffectively terminates the rights andliabilities of the company on the propertydisclaimed but does not affect the rightsand liabilities of any other person. Anyinterested party is entitled to request theliquidator to decide whether he intendsto disclaim and can apply to the court tohave the disclaimed property vested inhim. A person suffering loss or damageas a result of the liquidator exercising hisstatutory power of disclaimer, will havean unsecured claim for any loss ordamage in the liquidation.

Secured creditors may enforce rightsAlthough liquidation has the effect ofsuspending legal proceedings againstthe company, liquidation does notoverride the rights of secured creditorswho remain free to enforce their security and to retain the proceeds ofenforcement in priority to the claims of unsecured creditors.

Unsecured creditors are generally paidpari passu, although preferentialcreditors, as defined by section 386 andschedule 6 of the Act, have a priorityover general unsecured creditors and

there is a limited class of deferredcreditors.

Voluntary winding-upThere are two types of voluntarywinding-up, a members’ voluntarywinding-up and a creditors’ voluntarywinding-up, the essential differencebeing that the former applies to solventcompanies and the latter to insolventcompanies. Accordingly voluntaryliquidation is not always an insolvencyprocedure. Members’ voluntary winding-up is often used to effect a corporatereorganisation or reconstruction.

Powers of the liquidatorOne consequence of both members’and creditors’ voluntary liquidation isthat the powers of the directors cease.The liquidator has a number of powersset out in the Act some of which, in thecase of a creditors’ voluntary liquidation,must be exercised with the sanction of a liquidation committee appointed bycreditors, and some of which require the sanction of the court. There are also a number of enabling provisionswhich entitle the liquidator to, forexample, apply to the court for guidanceon questions arising in the winding-up.As with a compulsory liquidation, theliquidator’s general function is to realisethe assets and to pay creditors inaccordance with their entitlements (andthe liquidator in a voluntary winding-upalso has a similar power regarding thedisclaimer of onerous property). The

European Insolvency ProceduresEngland & Wales

© Clifford Chance LLP, July 2010

8

European Insolvency ProceduresEngland & Wales

order of priority of debts is the same asin a compulsory liquidation.

Company VoluntaryArrangementsA Company Voluntary Arrangement(“CVA”) might take the form of a rescueplan or may simply be used to facilitatea distribution to creditors. The objectiveof such arrangements is to binddissenting creditors to the proposals.

The Insolvency Act 2000 introduced,amongst other things, a new regime for CVAs of small companies which areeligible for a moratorium period of up tothree months when a CVA is proposedby its directors. A small company is onewhich currently satisfies at least two ofthe following three requirements:turnover of not more than £6.5m; assetsof not more than £3.26m; and less than50 employees. Although the moratoriumis only available to small companies, aCVA can be used by the directors of anycompany to come to an arrangementwith its creditors. For larger businessesthat do not qualify for the smallcompany moratorium, the administrationprocess (which has the benefit of amoratorium) may be used in conjunctionwith a CVA.

There are a number of exceptions andcertain companies will not be treated as eligible for a moratorium, for example,insurance companies, banks, andbuilding societies. During the moratorium,amongst other things, security cannot be enforced and proceedings cannot becommenced or continued against thecompany or its property except with theconsent of the court. Again, the effect ofthis moratorium is to allow a companytime to formulate a proposal so that itcan come to an arrangement with itscreditors.

The arrangement proposalThe proposal cannot affect the rights of secured creditors to enforce theirsecurity without the concurrence of thecreditors concerned; this effectivelygives the secured creditors a veto on an arrangement if it affects their rights. A meeting may not approve a proposalunder which a preferential debt of thecompany is to be paid otherwise than

in priority to non-preferential debts,unless the preferential creditor consentsto such a change in priority. In order for the proposal to be approved morethan one half majority in value of theshareholders and more than threequarters in value of the creditors mustvote in favour of the CVA. (Although ifthe decisions of the creditors and theshareholders differ, the decision of thecreditors will prevail subject to the rightof a member to apply to the court.)

Schemes of ArrangementThis is not an insolvency procedure buta mechanism contained in Part 26:sections 895-901 of the Companies Act2006 which allows the court to sanctiona “compromise or arrangement” that hasbeen agreed between the relevant classor classes of creditors or members andthe company.

A scheme of arrangement bindsmembers or creditors within a class,including unknown creditors who fallwithin a class of creditors. The power of the majority to bind a minority in theclass operates regardless of anycontractual restrictions (e.g.requirements for amendments andvariations set out in the loan documentwhich governed the debt beingcompromised.) For the scheme to beapproved there needs to be a majority innumber, representing three quarters invalue, in each class of those voting forthe scheme.

A scheme of arrangement requires thesanction of the court to summon ameeting or meetings of the relevantclass or classes of creditors ormembers. Assuming the scheme hasbeen approved by the requisite majorityof creditors at the meetings, the courtshould sanction the scheme itself.

Challenges to AntecedentTransactionsTransactions at an undervalue: section 238 of the ActAn administrator or liquidator may applyto the court to set aside transactionsentered into at an undervalue within two years of the onset of insolvency. For this purpose a transaction is at anundervalue if it constitutes a gift or if the

value of the consideration received (inmoney or moneys worth) is significantlyless than the consideration provided bythe company.

It is a defence to a challenge undersection 238 to show that the companywas solvent at the time it entered intothe relevant transaction or that it wasentered into in good faith and that therewere reasonable grounds for thinkingthe transaction would benefit thecompany. Although historically the viewof the court was that granting securitydid not deplete a company’s assets and therefore did not constitute anundervalue, secured creditors should be aware that following the Court ofAppeal’s decision in Hill v SpreadTrustee Company Limited [2006] EWCA542, the grant of security may now bethe subject of a challenge as atransaction at an undervalue.

Preferences: section 239 of the ActAn administrator or liquidator may applyto set aside transactions which occurred within six months of the onsetof insolvency (this period is extended to two years for transactions involvingconnected parties) which had the effectof putting the creditor, surety orguarantor in a better position in theliquidation than would otherwise havebeen the case and where the companywas influenced by a desire to producethat (i.e. preferential) effect. A companymust have been influenced in deciding to give the preference by a desire toproduce the effect of putting the creditorin a better position. If this desire ismissing the security will not beinvalidated. It is a defence to a challengeunder section 239 to show that thecompany was solvent at the relevanttime (taking account of the effect of therelevant transaction, act or omission).

Transactions defrauding creditors(section 423)Under section 423 of the Act the courtmay, on the application of the liquidatorof a company (or with the leave of thecourt, on the application of a “victim ofthe transaction” even if the company isnot in liquidation), set aside a transactionentered into by the company “at anundervalue” if the company entered intothe transaction for the purpose of

© Clifford Chance LLP, July 2010

9

putting assets beyond the reach of aperson who is making, or may at sometime make, a claim against it or ofotherwise prejudicing the interests ofsuch a person in relation to the claimwhich he is making or may make. It isnot a condition of the making of such an order that the company was insolvent at the time of the transaction.

A transaction at an undervalue is defined under section 423 of the Act insubstantially the same terms as undersection 238 of the Act (i.e. lackof/inadequate consideration). Theprincipal differences are:

(a) To set aside a transaction undersection 423, the court must besatisfied that it was entered into for the purpose of putting assetsbeyond the reach of creditors orotherwise prejudicing the interest of creditors.

(b) The remedy is available not only toadministrators and liquidators, butalso to “a victim of the transaction”.

(c) There is no requirement that thecompany be subject to a formalinsolvency proceeding.

Avoidance of floating charges: section 245 of the ActA charge, which as created was afloating charge, entered into by acompany within 12 months (the period isextended to two years if the transactionwas in favour of a connected party) ofthe onset of insolvency is invalid exceptto the extent of any new moneyadvanced (or the value of goods orservices provided) or the dischargereduction of indebtedness which occursat the same time or on or after thecreation of the charge.

It is a defence to a challenge undersection 245 to show that the companywas solvent when it entered into thecharge.

Extortionate credit transactions:section 244 of the ActAn administrator or liquidator maychallenge credit transactions enteredinto within three years of the onset ofinsolvency if, having regard to the risk

accepted by the counterparty, the terms were such as to require “grosslyexorbitant” payments (whetherunconditionally or in certaincircumstances) or if the terms of thetransaction otherwise “grosslycontravened” ordinary principles of fairdealing.

Personal Liability for DirectorsDirectors can incur civil and criminalliability for the debts of an insolventcompany in a number of ways under theAct. For this purpose, director includes,any person in accordance with whosedirections the appointed directors areaccustomed to act.

The principal areas of risk for directorsare breach of duty, fraudulent tradingand wrongful trading.

Breach of duty: section 212 of the ActThis section enables the court on theapplication of a liquidator, creditor orshareholder to make an order requiringany officer of the company (or anyperson who has taken part in thepromotion, formation or management of the company), liquidator oradministrative receiver who has mis-applied or mis-appropriated orwrongfully retained money or property of the company or been guilty ofmisfeasance or breach of any fiduciaryduty, to repay or restore the mis-appliedor mis-appropriated or wrongfullyretained property or contribute to thecompany’s assets by way ofcompensation for breach of duty.

Fraudulent trading: section 213 of the ActThis section enables a liquidator to applyfor contributions from any persons (i.e.not just directors and shadow directors)who were knowingly parties to thecarrying on of business with the intent todefraud creditors. The section requires“actual dishonesty involving, accordingto current notions of fair trading amongcommercial men, real moral blame”.

The facts supporting a claim undersection 213 will also render every personknowingly party to the carrying on of thebusiness with intent to defraud creditors

liable to criminal penalties under section993 of the Companies Act 1985.

Wrongful trading: section 214 of the Act A liquidator may apply to the court forcontributions towards the assets of thecompany from any person who heldoffice as a director (this includes shadowdirectors) from the point at which thatperson “knew or ought to haveconcluded that there was no reasonableprospect of avoiding insolventliquidation”.

It is a defence to a challenge undersection 214 for a director to show thatfrom the point that he knew or ought tohave known that insolvent liquidationwas unavoidable he “took every stepwith a view to minimising the potentialloss to the company’s creditors”. Thismay include directors initiatinginsolvency proceedings.

It should be noted that resigning doesnot necessarily enable a director toavoid liability under section 214 and thatunder section 214 there is no need toprove an intention to defraud creditors.

Part 10 of the Companies Act 2006codifies the duties of directors. Itprovides a list of seven general dutiesaimed to provide greater clarity todirectors, and also a non-exhaustive listof factors that directors must take intoaccount when exercising their duties. In particular the factors include a duty to consider not just shareholders, butemployees, suppliers, consumers andthe environment. The statement ofduties in the Companies Act 2006 is not comprehensive. In particular, it doesnot include the duty which is owed tocreditors when the company is insolventor on the verge of insolvency, thoughthis is preserved.

The Companies Act 2006 also containsa new procedure for enforcement ofdirectors’ duties by shareholders onbehalf of the company although theclaimant must show a prima facie casebefore being given permission toproceed with a claim. In practice therehas not been any increase in litigation todate against directors as a result of thesechanges to the legislation.

European Insolvency ProceduresEngland & Wales

© Clifford Chance LLP, July 2010

10

European Insolvency ProceduresEngland & Wales

Lender LiabilityGenerally speaking, the risk in Englandof lenders being held liable to pay theircustomers’ debts is small. The principalrisk for a lender, however, arises where it is found to be acting as a shadowdirector of a company that becomesinsolvent. In such circumstances it isconceivable that a lender may be madeliable to make a contribution to aninsolvent company’s assets for wrongfultrading under section 214 of the Act.

“Shadow Director” is defined in section251 of the Act as meaning “...a personin accordance with whose directions orinstructions the directors of thecompany are accustomed to act (but sothat a person is not deemed a shadowdirector by reason only that the directorsact on advice given by him in aprofessional capacity.)”

Consequences of being a shadow directorA liquidator or creditor of an insolventcompany might seek to pursue a lenderon the basis that it is a shadow director.As previously mentioned, a lender maybe made liable to make a contribution to an insolvent company’s assets forwrongful trading where it is held to be a shadow director of that company.Wrongful trading occurs from the pointin time that a reasonable director oughtto have concluded that the companywould not avoid insolvent liquidation.From that point on the directors,including shadow directors, run the riskof being ordered to contribute to thecompany’s assets in its liquidation.

Defences available to lendersOne line of defence for a lender accusedof shadow directorship lies in thewording of the definition. The directorsof the insolvent company are required to be accustomed to act in accordancewith directions or instructions receivedfrom the shadow director. The word“accustomed” implies that there hasbeen a course of dealings between theparties. If the lender has a constantpresence in the company, for examplewhere the lender has appointed acompany doctor who is exercisingmanagement authority, the position maybe different. The key to the definition isthe idea that it is the shadow director,

not the board of directors, who isexercising the management discretion of the company.

Practical advice for lendersThere is no authority as to what activitiesare safe for a lender to conduct. Thisquestion remains largely unanswered bythe courts. Although yet to be tested bythe courts, lenders to a company infinancial difficulty may be entitled to takeaction to protect their interests, such assending in an investigating team;demanding a reduction in the overdraft;demanding security or further security;calling for information, valuations of fixedassets, accounts, cash flow forecasts,etc; requesting the customer’sproposals for the reduction of theoverdraft, including the submission of abusiness plan, schedule of proposedsales, etc; advising on the desirability ofstrengthening management, and seekingfresh capital. In doing all these things thelenders may well expect their demandsto be met, firstly because they are likelyto be commercially sensible, andsecondly because the customer has nooption if it wants its facility continued.This should not be sufficient toconstitute the lenders being regarded as shadow directors.

So long as the lenders can be viewed tobe merely setting out what conditionsattach to their continued support theyshould not incur liability. Crucially, thedecision as to whether to continue

trading in the face of these conditions,or to cease trading or go into liquidationrests with the directors.

Recent pensions legislation may alsoaffect a lenders’ liability where there is a defined benefit pension scheme.Lenders should take care not to become“connected with” or associates of aborrower with such a scheme, as doingso could put them at risk of incurringobligations under financial support orcontribution notices issued by thePension’s Regulator. One of the tests of whether a lender is connected orassociated is the ability to control onethird of the voting rights in a relevantborrower. Security over shares therefore,needs to be carefully drafted to avoid alender being liable.

GuaranteesGuarantees are available in mostcircumstances, e.g. downstream (parentto subsidiary), upstream (subsidiary toparent) and cross-stream (betweensister companies within a group).

Corporate benefit issues need to beaddressed especially in the context ofupstream and cross-stream guarantees.

A guarantee is a secondary obligation by a third party relating to a primaryobligation by a contracting party (i.e. aborrower under a loan agreement). If theprimary obligation is altered, discharged

© Clifford Chance LLP, July 2010

11

or fails the guarantee may not beenforceable. Usually the documentcontaining a guarantee will also containa direct indemnity as an independentprimary obligation. This should surviveeven if the guarantee is not enforceable.

A guarantee must be in writing to beenforceable.

Generally speaking, if security orguarantees are granted at the time aloan is drawn, and at that time it is notcontemplated that the company willbecome insolvent, the requisite desire toprefer the creditor/guarantor is usuallymissing and therefore it should notconstitute a preference (see above).

Following the Court of Appeal thedecision in Hill v Spread TrusteeCompany Limited the granting ofsecurity/guarantee may be challengedas a transaction at an undervalue (seeabove).

PrioritySecurity usually ranks by order ofcreation, but to preserve the priorityposition, notice may need to be given.For some assets registration is requiredin an asset register and security will rankby date of registration.

Subject to the rights of the creditors toagree their relative priority, the order forpayment of claims depends upon thetype of insolvency procedure.

Broadly speaking in the context ofreceivership from the charged assets,rank as follows:

(a) Holders of security which ranks priorto the security under which thereceiver is appointed;

(b) Holders of security (from theproceeds of which the receiver willrecover costs, remuneration andexpenses (as prescribed in thecharge appointing the receiver));

(c) Preferential creditors (ranks ahead offloating charge only, fixed chargestake priority);

(d) Unsecured creditors up to amaximum of £600,000 if the

company’s net property is £10,000or more (ranks ahead of floatingcharge only, fixed charges takepriority);

(e) Holders of a floating charge;

(f) Any surplus is payable tosubsequent charge holders (if any) or to the company or its liquidator.

A recent amendment to the law has beenmade which affects the priority of thecosts and expenses of a liquidation. Ithas the effect of making the expenses of a liquidation rank ahead of a floatingcharge. The change in priority waseffective from 6 April 2008 and applies toall liquidations commenced after that datewhere there are insufficient unsecuredassets to meet the payment of liquidationexpenses. Claims in a liquidation after 6April 2008 will rank as follows:

(a) Holders of fixed charge security(usually dealt with outside of theliquidation process);

(b) Costs and expenses of theliquidation in accordance with theorder stipulated by the enactinglegislation;

(c) Preferential creditors;

(d) Unsecured creditors up to amaximum of £600,000 if thecompany’s net property is £10,000or more (payable out of floatingcharge assets);

(e) Holders of floating charge;

(f) Unsecured creditors;

(g) Post liquidation interest on debts;

(h) Deferred creditors;

(i) Shareholders (only if there is asurplus after the debts are paid).

Claims in administration rank as follows:

(a) Fixed charge security;

(b) Costs and expenses of theadministration in accordance withthe order stipulated by the enactinglegislation;

(c) Preferential creditors;

(d) Unsecured creditors up to amaximum of £600,000 if thecompany’s net property is £10,000or more;

(e) Holder of a floating charge;

(f) Unsecured creditors;

(g) Post administration interest ondebts;

(h) Deferred creditors;

(i) Shareholders (only if there is asurplus after the debts are paid).

New Money LendingNormally lenders will insist on additionalsecurity or priority (ahead of debtsincurred prior to the proceedings) beforeany new monies are advanced tocompanies after the opening of anyinsolvency proceedings.

Recognition of ForeignInsolvency Proceedings Within the EUThe Regulation applies, see first part ofthis note.

Recognition of foreign insolvencyproceedings outside of the EUThe Model Law On Cross BorderInsolvency promoted by UNCITRAL was adopted in Great Britain on 4 April2006 in the form of the Cross BorderInsolvency Regulations in 2006. Thisextends the English court’s ability torecognise foreign insolvencyproceedings outside of the EU, tojurisdictions such as the US. In additionto the Cross Border InsolvencyRegulations 2006 there are statutoryprovisions allowing the English court toexercise its jurisdiction if the foreignentity has a sufficient connection withEngland (section 221 of the Act) or if aspecific request for assistance is madeby the court from one of the territoriesspecified in section 426 of the Act(largely commonwealth countries).

Further, a recent House of Lordsdecision in the case of McGrath andothers v Riddell and others [2008]

European Insolvency ProceduresEngland & Wales

© Clifford Chance LLP, July 2010

12

European Insolvency ProceduresEngland & Wales

UKHL21 held that pursuant to section426 of the Act, the English Court coulddirect the remittal of assets realised in anEnglish liquidation to another jurisdictionand absent any manifest injustice tocreditors, the English Court has theability to make an order, even if theeffect of that order will facilitate theapplication of an insolvency regimewhich differs from English insolvencylaw. Where remittal is to a jurisdictionwhose court cannot make a requestpursuant to section 426, the EnglishCourt’s inherent jurisdiction may onlyfacilitate a transfer where the foreigncourt’s rules do not infringe theprinciples of English insolvency law.

Under the general principles of comity,foreign proceedings may also berecognised, and in a recent PrivyCouncil decision (which as a matter ofEnglish law is persuasive but notbinding), Cambridge Gas TransportCorporate v The official committee ofunsecured creditors of NavigatorHoldings Plc and others [2006] UKPC26,it was held that it was not necessary toopen ancillary proceedings in the Isle of Man, to facilitate the implementation of a US plan of reorganisation.

© Clifford Chance LLP, July 2010

13

This section is designed to provide ageneral outline of the main pre-insolvency proceedings and insolvencyproceedings in France.

The legislation applying to the insolvencyand pre-insolvency proceedings of allprivate legal entities (limited liabilitycompanies, unlimited liability companies,partnerships, trade unions, etc.),individuals conducting a commercialbusiness, craftsmen, farmers and otherpersons running an independentprofessional activity, including thosehaving a regulated status (e.g. lawyers,doctors etc.), is contained in Book VI ofthe French Commercial Code. Therelevant proceedings are:

n mandat ad hoc;

n conciliation;

n safeguard proceedings;

n rehabilitation proceedings; and

n judicial liquidation.

The objectives of French insolvency laware (i) the preservation of the business,(ii) the preservation of jobs and (iii) thepayment of creditors.

The legislation applying to insolvencyproceedings of individuals who do no not fall within the scope of Book VI of the French Commercial Code (e.g.employees) and to insolvencyproceedings of credit institutions, financialinstitutions and insurance companies isnot described in this section.

The European Regulation on InsolvencyProceedings (the “EUIR”) applies, with

respect to private international lawissues, where the debtor in theinsolvency proceedings is not a creditinstitution, an investment company or aninsurance company and the “centre ofmain interests” (the “COMI”) of thedebtor is within the territory of a memberstate of the EU. For cases which do notfall within the scope of the EUIR (e.g. thecompany’s COMI is outside the EU), therules of private international lawessentially stem from French precedents.

Consensual Pre-insolvencyProceedingsPre-insolvency procedures under Frenchlaw are mandat ad hoc and conciliationproceedings. they are intended tofacilitate negotiations between the debtorand its main creditors, with a view toreaching an agreement and avoiding theopening of insolvency proceedings.

Debts may only be restructured on aconsensual basis in pre-insolvencyproceedings, and creditors who refuseto negotiate or to participate in theproceedings will not be affected by anycompromise or arrangement reached bythe debtor and its other creditors inthose proceedings. However, it shouldbe mentioned that under French generalcivil law, French courts have a generaldiscretion to impose a grace period ofup to two years on any creditor: inpractice, the availability of this discretioncan be used as a tool to encouragedissenting creditors to participate in thediscussions.

Mandat ad hocA debtor that is facing any type ofdifficulties (but which is not insolvent yet,

i.e. which is still able to pay all its dueand payable debts with its immediatelyavailable assets) may file a petition withthe president of the local court havingjurisdiction to obtain an order appointinga mediator / advisor called a mandatairead hoc to the debtor. His appointmentinitiates the pre-insolvency proceedingscalled mandat ad hoc.

The mandataire ad hoc assists thedebtor in its negotiations with thirdparties (e.g. creditors, employees) and / or helps the debtor assessing its situation (e.g. whether the opening of insolvency proceedings would beappropriate).

The debtor remains in charge of runningits business. The mandataire ad hocdoes not have the power to interfere inthe management of the business.

Mandat ad hoc is not an insolvencyproceeding. The existence of a mandatad hoc is confidential, and will bedisclosed only to those parties withwhom negotiations need to beconducted. Creditors are not barred fromtaking legal action against the debtor to recover their claims, but, in practice,they do not usually try to do so.

The debtor may suggest to the court the name of the mandataire ad hoc itwould like to see appointed. Thissuggestion is usually followed by thecourt. Mandataires ad hoc are generallychosen from the register of insolvencyadministrators.

The ability of the mandataire ad hoc tohelp the debtor in its negotiations comesfrom the fact that he is an independent,

European Insolvency ProceduresFrance

© Clifford Chance LLP, July 2010

14

Key Elements:

Considers:

n Consensual pre insolvency proceedings: mandat ad hoc and conciliation

n Formal insolvency proceedings: safeguard proceedings, rehabilitation proceedings and judicial liquidation

n Creditors’ ranking

n Challenge to antecedent transactions

n Liabilities and sanctions

France

European Insolvency ProceduresFrance

court-appointed third party, havingsignificant experience of companiesfacing financial difficulties. In particular,he is able to explain to the creditors thatthey also have an interest in finding aconsensual solution with the debtor bydescribing the potential consequencesof insolvency proceedings if anagreement is not found. The mandatairead hoc usually sends written reports tothe president of the court, on aconfidential basis.

ConciliationConciliation is available to debtors thatare facing actual or foreseeable legal,economic or financial difficulties, andthat are either (a) not insolvent (i.e. arestill able to pay all their due and payabledebts with their immediately availableassets); or (b) insolvent but have been insuch a position for a period of less than45 days.

Conciliation is very similar to mandat adhoc. In particular:

The debtor can request the appointmentof the conciliator (“conciliateur”) by filinga petition with the president of the localcourt having jurisdiction. The conciliatorwill assist the debtor in its negotiationswith third parties (e.g. creditors,employees) and / or help the debtorassess its situation (e.g. whether theopening of insolvency proceedingswould be appropriate).

The debtor remains in charge of runningits business. The conciliator does nothave the power to interfere in themanagement of the business.

Conciliation is not an insolvencyproceeding. The existence of aconciliation is confidential, and will bedisclosed only to those parties withwhom negotiations need to beconducted. Creditors are not barred fromtaking legal action against the debtor to recover their claims, but, in practice,they do not usually try to do so.

The debtor may suggest to the court thename of the conciliator it would like tosee appointed. This suggestion isusually followed by the court.Conciliators are generally chosen fromthe register of insolvency administrators.

The ability of the conciliator to help thedebtor in its negotiations comes from thefact that he is an independent, court-appointed third party, having significantexperience of companies facing financialdifficulties. In particular, he is able toexplain to the creditors that they alsohave an interest in finding a consensualsolution with the debtor by describingthe potential consequences of insolvencyproceedings if an agreement is notfound. The conciliator usually sendswritten reports to the president of thecourt, on a confidential basis.

The main differences with mandat adhoc are the following:

(i) The conciliator can only beappointed for a maximum of 4months and this period may only beextended by 1 month in exceptionalcircumstances (i.e. a maximum of 5months), unlike the mandataire adhoc whose length of office is at thediscretion of the president of thecourt.

(ii) The debtor cannot enter conciliationagain within three months of thetermination of the earlier conciliation.

(iii) If the parties reach an agreement(the “Conciliation Agreement”), suchagreement can either beacknowledged by an order of thepresident of the court (“accord de

conciliation constaté”), or approvedby a formal judgment of the court,upon request of the debtor (“accordde conciliation homologué”).

In practice, debtors frequently combinethe use of mandat ad hoc andconciliation: they first request theopening of a mandat ad hoc (the lengthof which is very flexible) and, when theybelieve that they are about to reach anagreement with their creditors, theypetition the president of the court toconvert the mandat ad hoc intoconciliation. Once in conciliation they will be able to seek acknowledgement of the Conciliation Agreement by thepresident of the court or its approval bya judgment of the court.

Acknowledgement by the president ofthe court. If the Conciliation Agreementis simply acknowledged by an order ofthe president of the court, it remainsconfidential.

Approval by judgment of court.Alternatively, approval of the ConciliationAgreement by a formal judgment givescomfort to the parties thereto in that, ifthe debtor subsequently goes intoinsolvency proceedings:

(i) lenders making new money and/orsuppliers making trade creditavailable to the debtor under theConciliation Agreement will benefit

© Clifford Chance LLP, July 2010

15

from a priority ranking in thoseinsolvency proceedings; and

(ii) the court may not fix the startingdate of the Hardening Period (seeChallenge to AntecedentTransactions section below) at a dateearlier than the date on which theapproval judgment became final.

The drawback of approval by way of ajudgment is that confidentiality is lost.

Formal InsolvencyProceedings: GeneralOverviewUnder French law, a debtor isconsidered to be insolvent (“en état de cessation des paiements”) when it is unable to meet its due and payabledebts with its immediately availableassets (being cash plus assets that can be immediately realised for cash).

The debtor must file a petition with a view to opening a RehabilitationProceedings (“redressement judiciaire”)or a Judicial Liquidation (“liquidationjudiciaire”) within 45 days of the datewhen it became insolvent (unless it haselected to enter conciliation within suchtime frame). A petition can also be made by an unpaid creditor, by thepublic prosecutor or by the court of itsown motion.

The law further allows the filing of apetition for Safeguard Proceedings(“procédure de sauvegarde”) thattriggers an automatic stay of paymentsand is aimed at recovery if the debtorestablishes that, although not insolvent,he is facing difficulties which he isunable to overcome on its own. If thedebtor is insolvent, this procedure willnot be available to him.

Safeguard Proceedings, RehabilitationProceedings, or Judicial Liquidation arecollectively referred to below as“Insolvency Proceedings” with eachbeing an “Insolvency Proceeding”.

Insolvency officers Insolvency Proceedings are essentiallycourt-driven proceedings where most ofthe key decisions are made orauthorised by the court.

In an Insolvency Proceeding, aninsolvency judge (“juge-commissaire”) isappointed by the court in the judgmentopening the proceedings. He is incharge of taking certain decisions (e.g.admitting claims against the insolvencyestate) and authorising certaintransactions (e.g. authorising entry intoagreements that are not within theordinary course of business; authorisingthe sale of assets). However, the courtitself retains jurisdiction over keydecisions in the proceedings, inparticular (i) the adoption of a SafeguardPlan or a Rehabilitation Plan, (ii) the saleof the business as a going concernpursuant to a Sale-of-Business Plan, (iii) the termination of the InsolvencyProceedings, (iv) claims against thedebtor (e.g. for mismanagement) andagainst third parties (e.g. claw-backactions). The public prosecutor isconsulted by the court before it takessuch key decisions, but the court is notobliged to adopt his position. The publicprosecutor is also entitled to initiatecertain legal actions.

In Safeguard Proceedings andRehabilitation Proceedings, anadministrator (“administrateur judiciaire”)(selected from the register of insolvencyadministrators) is generally appointed bythe court to assist, supervise or, underexceptional circumstances, replace thedebtor in the management of thebusiness. However, it is possible for thecourt not to appoint an administrator ifthat does not seem necessaryconsidering the size of the estate of thedebtor. In parallel, the court alsoappoints a representative of thecreditors (“mandataire judiciaire”)(selected from the list of registeredmandataires judiciaires) who is in chargeof (i) receiving and verifying the proofs ofclaims, (ii) initiating legal actions onbehalf of the creditors as a whole (e.g.claims against the directors of theinsolvent company), and (iii) moregenerally, defending the general interestof creditors.

In Judicial Liquidation, a judicialliquidator (“liquidateur judiciaire”)(selected from the list of registeredmandataires judiciaires) is appointed bythe court. He represents the debtor andhe is also entitled to initiate legal actions

on behalf of the creditors as a whole.He also receives and verifies the proofsof claims.

Up to five creditors can be appointed ascontrollers (“contrôleur”) if they sorequest. This appointment gives themprivileged access to information, and theyare entitled to initiate legal actions onbehalf of the creditors as a whole if thecreditors’ representative fails to do so.

Purpose of insolvency lawFrench insolvency law is aimedessentially at the preservation of theenterprise and of employment (byrescue of the company or of thebusiness of the company) and to alesser extent the repayment of thecreditors.

The possible outcomes of InsolvencyProceedings are as follows:

(i) If recovery is possible, the court willpermit the debtor to prepare either a “Safeguard Plan” (in the case ofSafeguard Proceedings) or a“Rehabilitation Plan” (in the case ofRehabilitation Proceedings) which ineach case will provide the measuresnecessary for the rehabilitation andcontinuation of the operations of thedebtor.

(ii) If the debtor is unable to prepare a viable Safeguard Plan orRehabilitation Plan, the court canorder the sale of the business as a going concern (free of debts, and including employees and keycontracts) to a third party (who mustbe independent from the debtor), ina so-called “Sale-of-Business Plan”(“plan de cession”).

(iii) If recovery is manifestly impossible,the court must order the opening ofa Judicial Liquidation.

Outcome of Safeguard Proceedingsand Rehabilitation ProceedingsThe process for implementing aSafeguard or Rehabilitation Plan isessentially as follows:

(i) In both Rehabilitation and SafeguardProceedings, after verifying theeligibility of the debtor to enter the

European Insolvency ProceduresFrance

© Clifford Chance LLP, July 2010

16

European Insolvency ProceduresFrance

relevant proceedings, the courtorders the commencement of a time period during which the debtorcontinues to operate its businessunder the protection of the courtwhilst its financial and businesssituation is assessed and anarrangement with creditors issought. This time period is known as the observation period (“périoded’observation”). The observationperiod may initially last for up to 12months and may be extended sothat its maximum total duration is 18 months.

(ii) The proposed restructuring of thedebt must be approved, whereapplicable, by creditors’ committees(see below). Each creditor committeeacts by a majority of two thirds ofcreditors present and such majorityis empowered to approve acompromise and/or a repaymentschedule that is binding on theirmembers.

(iii) If there are no creditors’ committeesor if the proposed restructuring ofthe debt is not approved by thecreditors’ committees, the court mayimpose a rescheduling of the debtwhich cannot exceed 10 years (15years for agricultural businesses).The court is not empowered toreduce a debt at its own initiative.

(iv) Alternatively, at the hearing for entryinto Safeguard Proceedings orRehabilitation Proceedings the courtmay decide that recovery isimpossible, and order that JudicialLiquidation be opened in respect ofthe debtor. The court can orderJudicial Liquidation either (i) from thebeginning of the relevant InsolvencyProceedings without allowing anobservation period where the debtoris insolvent and any recovery isobviously impossible, or (ii) at anytime during the observation period ifit becomes obvious that recovery isimpossible.

Outcome of a Judicial LiquidationIn a Judicial Liquidation, the debtor’sassets are realised and the proceedsfrom those realisations are distributedamong the creditors on a pro rata basis

subject to the order of prioritiesprescribed by legislation.

The court may approve a “Sale-of-Business Plan” if it determines that thedebtor’s business can be realised as agoing concern. Under such a plan thecourt may approve the sale of all or partof the business and assets of thedebtor, as a going concern, preserving a certain number of employmentpositions.

If the court considers that no sale of thebusiness as a going concern is likely totake place, the assets can be realisedpiecemeal.

Automatic stay of payments and otherrestrictions on rights of creditorsDuring Insolvency Proceedings, therights of the creditors are restricted, interalia, as follows:

(i) subject only to very limitedexceptions, the debtor may notrepay any debts incurred prior tothe insolvency judgment;

(ii) as a principle, the commencementof Safeguard Proceedings orRehabilitation Proceedings freezes alllegal actions of creditors to enforce a payment obligation incurred priorto the insolvency judgment or toenforce security over the assets ofthe bankrupt debtor. However thereare some limited exceptions to thisrule even during an observationperiod; and some secured creditorsrecover their right to enforce theirsecurity if the debtor is placed inJudicial Liquidation;

(iii) contracts cannot be terminated for reasons originating prior to the insolvency judgment, andclauses providing for termination or acceleration in the event ofinsolvency are of no effect;

(iv) insolvency officers have the power to choose which agreementsentered into by the debtor prior tothe insolvency judgment shouldcontinue. Contracts which aninsolvency officer elects to continuemust be performed in accordancewith their terms;

(v) creditors must prove their claimsarising prior to the judgment openingInsolvency Proceedings within 2months (4 months for creditorsresiding outside of France) from thedate of publication of such judgmentin the designated legal gazette.Where the creditor has failed to fileits proof of debt in a timely manner, it will not be allowed to participate inthe distribution of proceeds. Certainpost-judgment claims must also beproved;

(vi) the right to set off reciprocal debtswith the insolvent debtor is limited to “related debts” (“créancesconnexes”) i.e. debts which arose in the framework of the samecontract (or, to a certain extent, fromthe same group of contracts); and

(vii) when the Insolvency Proceedingsare closed and there is a shortfallbetween the assets of the debtorand its liabilities, the remedies of thecreditors to obtain repayment are, as a general principle, extinguishedeven if their claims were not satisfiedin full. This is subject to certainexceptions e.g. fraud, “insolvencysecond offenders”, etc.

Safeguard ProceedingsSafeguard Proceedings are onlyavailable to debtors which, although notinsolvent, establish that they are facingdifficulties (usually financial) which theycannot overcome. The purpose ofSafeguard Proceedings is to facilitate a restructuring of the debtor while itsdifficulties are still at an early stage in the framework of formal proceedings.

The judgment opening the proceedingsstays all individual claims of creditors,irrespective of their rank, subject only to very limited exceptions such asenforcement of retention of title clauses,set-off of related debts, rights ofretention attached to certain securityinterests. The judgment opens anobservation period of a maximumduration of six months, renewable once,and exceptionally twice, for thepurposes of preparing and submitting to the approval of the court a SafeguardPlan restructuring the debts and the

© Clifford Chance LLP, July 2010

17

business. The judgment approving theplan ends the observation period.

The court appoints an administrator toassist and supervise the debtor, but therationale is to allow sufficient flexibility toenable the management of the debtor to remain in possession. The debtor hasthe option of nominating anadministrator for the court to approve.

In contrast to Rehabilitation andLiquidation Proceedings, SafeguardProceedings do not provide for simplifiedredundancy procedures, and theredundancy regime is the same as for a non-distressed business. SafeguardProceedings are therefore moreappropriate for financial restructuringsand debt work-outs (e.g. over-leveragedsituations, distressed LBOs, etc.) ratherthan industrial reorganisations requiringnot only debt restructuring but alsobroad scale redundancies.

However, if a redundancy scheme isneeded, and if the debtor is not in aposition to finance the cost of itsimplementation, a state-organisedinsurance scheme will provide thenecessary financing to the debtor,subject to certain criteria and limitations.The repayment of the advances madeby the insurance scheme must be made within a limited period of time,which is to be agreed with the insurancescheme, and is generally one to twoyears after the approval by the court of the Safeguard Plan.

Safeguard Proceedings provide for the creation of at least two creditors’committees, if the debtor (a) has morethan 150 employees or (b) has aturnover of more than €20,000,000 and (c) its accounts are certified by astatutory auditor or carried out by acertified public accountant. Nevertheless,the Insolvency Judge can decide tocreate committees even though thethresholds are not met.

The first committee is comprised ofcreditors who are the main suppliers of goods and services. The secondcommittee is comprised of creditors that are credit institutions and“assimilated” institutions in particularbanks, local public credit institutions,

finance companies (“sociétésfinancières”) or special purpose financialinstitutions, the assignees of bank debtthat occurred prior or after the openingof proceedings (e.g. hedge funds), aswell as any entity granting credit oradvances in favour of the debtor. If thereare bondholders, a “third” committeecomprising all bondholders (“assembléeunique des obligataires”) must approvethe plan that has been voted by the twocreditors’ committees.

The powers of the committees aremainly to approve or reject the debtor’srestructuring proposal. The debtor has a wide flexibility in structuring suchproposals. In particular, these proposalsmay include the debt being written off orthe partial closure or disposal of thebusiness. The draft Safeguard Plan canprovide for the rescheduling of the debtsof the members of the committees overa period longer than ten years, andthere is no requirement that the debt bereduced by a certain amount within acertain period. Since reform legislationwas passed in 2008, the plan canprovide for debt-for-equity swaps incertain circumstances. The law providessufficient scope to treat creditors of asame committee differently if theobjective economic situation so requires.Creditors can make counter proposalsto the debtor and to the administrator,but the debtor has no obligation to takethem into consideration when submittingthe plan to the committees.

Within each committee, approval isachieved by a majority of two thirds invalue of creditors present who voted onthe plan. Dissenting creditors are boundby the decision of that majority. Each ofthe creditors’ committees must haveapproved the plan before it will beadopted by the court. After havingdiscussed with the debtor and theadministrator, the committees must takea decision on the proposed Safeguardor Rehabilitation plan within 20 to 30days following the submission of theproposals by the debtor. The decision of the committees on the Safeguardplan must take place within 6 monthsfollowing the opening of the SafeguardProceedings or RehabilitationProceedings. If all creditors’ committeeshave not approved a Safeguard Planwithin this 6-month period, they nolonger have any role in the proceeding.

In parallel, non-committee creditors areconsulted individually on the options forthe payment of their claims (e.g.reduction of the debt with shorterdeferral or full repayment over a longerperiod). The court cannot impose areduction of the debt on creditorsrefusing the debtor’s proposals, but onlya rescheduling or deferral of payment.The rescheduling cannot exceed tenyears. After the second year, theminimum annual instalment is 5% of thetotal liabilities (except in the case ofagricultural businesses).

European Insolvency ProceduresFrance

© Clifford Chance LLP, July 2010

18

European Insolvency ProceduresFrance

State creditors (such as the taxadministration) are not members of anyof the creditors’ committees. They mayhowever waive or reduce their debt.Rescheduling of their debt can also beimposed, under the conditionsmentioned above.

After approval of the Safeguard Plan bythe committees, and before sanctioningthe plan, the court must satisfy itself thatthe interests of all the creditors (whichincludes minority committee creditors)are sufficiently protected. After thesanction of the Safeguard Plan by thecourt, all members of the committeesare bound by the plan. At the sametime, the court acknowledges anywaiver of debts granted by non-committee creditors and/or orders arescheduling or deferral of payment oftheir claims.

If all creditors’ committees have notapproved a draft Safeguard Plan within 6months of the opening of the SafeguardProceedings, or if the Court has refusedto sanction the draft Safeguard Plan, allcreditors are consulted individually on theoptions for the payment of their claims(according to the rules described abovefor consultation of non-committeecreditors).

At any time during the observationperiod, the court can convert theSafeguard Proceedings into eitherRehabilitation Proceedings or JudicialLiquidation, if it is shown that the debtorwas actually in a state of cessation ofpayments when it applied for SafeguardProceedings, or if the debtor finds itself in a state of cessation of paymentsafter the opening of the SafeguardProceedings. At the request of thedebtor, the court also may order theconversion of Safeguard Proceedingsinto Rehabilitation Proceedings if theadoption of a Safeguard Plan appearsimpossible and if the termination of theSafeguard Proceedings would lead,without doubt and rather quickly, to thedebtor’s insolvency.

Rehabilitation ProceedingsRehabilitation Proceedings are availableto debtors that are insolvent but whosebusiness appears viable.

Such proceedings are commenced by a judgment, which is rendered either atthe debtor’s request or upon request ofan unpaid creditor, of the publicprosecutor, or of the court itself. Itshould be stressed that the debtor has a duty to file a petition with a view to theopening Rehabilitation Proceedings or of a Judicial Liquidation within 45 daysof the date when it became insolvent(unless it has elected to enterconciliation within such time frame).

Most of the organisational provisions ofSafeguard Proceedings apply toRehabilitation Proceedings (in particularthe limitations imposed on the rights ofthe creditors). The administrator isrequired to make an assessment of thecompany’s financial situation, thecauses of that situation and the potentialsolutions e.g. whether the businessshould be continued under aRehabilitation Plan (similar to aSafeguard Plan), assigned in whole or in part to a third party or put intoliquidation. Depending on the scope ofhis duties, as determined by the court,the administrator may either assist orreplace the debtor in the managementof its business and assets.

As in Safeguard Proceedings:

(i) the observation period can last forup to 12 months with an exceptionaladditional extension of 6 monthsupon request of the publicprosecutor (i.e. a maximum of 18months);

(ii) the creditors’ committees areconsulted and can compromise thedebt of their members in the samemanner as with the SafeguardProceedings; and

(iii) if the creditors’ committees do notapprove the proposals of the debtorfor the reorganisation of the debt inthe framework of a RehabilitationPlan, all creditors are consultedeither individually or collectively onthe options for the payment of theirclaims (see above).

The law provides for expeditedredundancy procedures in the case of Rehabilitation Proceedings. If the

debtor is not in a position to finance the redundancies, a state organisedinsurance system provides thenecessary financing, subject to certaincriteria.

For a Rehabilitation Plan to be approvedby the court, the debtor must show thatits recovery scheme is viable, and on thebasis of the past and forecastedoperations’ accounts, that the debtor willbe able to generate sufficient operationalprofits to repay the rescheduled liabilitiesand finance its day-to-day operationsand business plan.

A significant difference betweenRehabilitation Proceedings andSafeguard Proceedings is that, if thedebtor proves unable to prepare a viableRehabilitation Plan, the court mayimpose the sale of part or all of thebusiness as a going concern, under aSale-of-Business Plan (see below). If thisroute is taken, the administrator makesa call for tender, and the court choosesthe offer that best meets the three goalsprovided for by the law.

At any time during the observationperiod, the court can order the JudicialLiquidation of the debtor, if the businessappears not to be viable.