European Hotel Sector Review of 2007

20

Russell Kett Managing Director HVS – London Amsterdam – 16 January 2008 European Hotel Sector Review of 2007

description

European Hotel Sector Review of 2007. Russell Kett Managing Director HVS – London Amsterdam – 16 January 2008. Key Trends for European Hotels. Occupancy and room rate Hotel valuation Transactions. Europe – Still the RevPAR King. Seasonally Adjusted RevPAR. $115. $103. $99. €87. $64. - PowerPoint PPT Presentation

Transcript of European Hotel Sector Review of 2007

Russell KettManaging Director

HVS – London

Amsterdam – 16 January 2008

European Hotel Sector Review of 2007

Key Trends for European Hotels

● Occupancy and room rate● Hotel valuation● Transactions

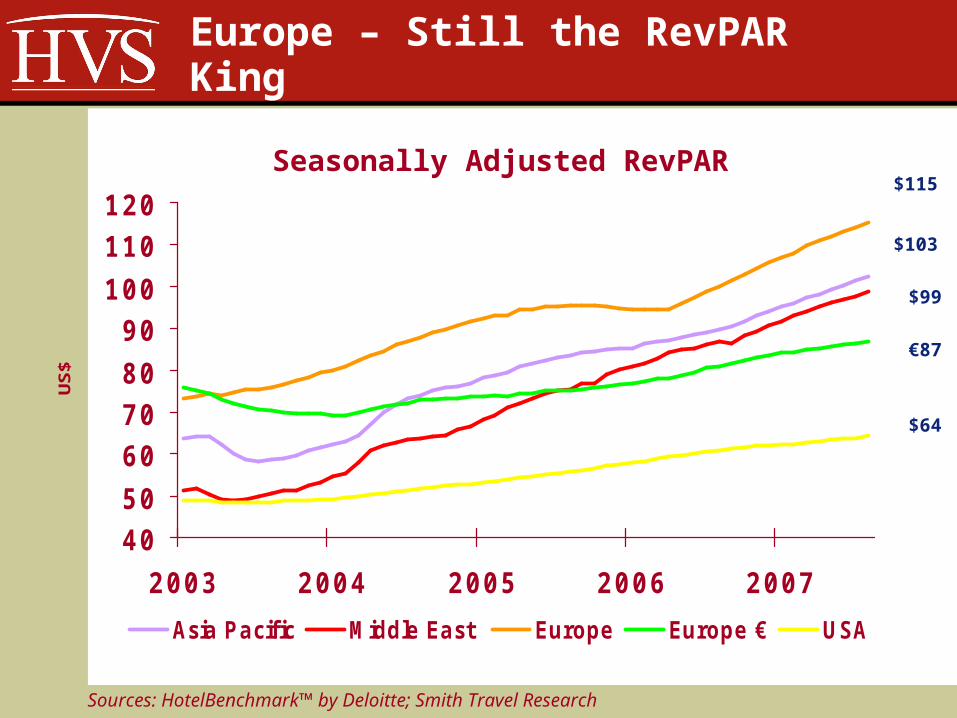

Europe – Still the RevPAR King

405060708090

100110120

2003 2004 2005 2006 2007

US$

Asia Pacific Middle East Europe Europe € USA

Sources: HotelBenchmark™ by Deloitte; Smith Travel Research

Seasonally Adjusted RevPAR$115

$103

$99

$64

€87

European hotel occupancy %

0

10

20

30

40

50

60

70

80

90

A'damB'lo

naBerl

in

Bruss

els

Genev

a

London

Paris

Milan

Rome

200520062007e

European hotel ADR €

0

50

100

150

200

250

A'damB'lo

naBerl

in

Bruss

els

Genev

a

London

Paris

Milan

Rome

200520062007e

Hotel RevPAR 2006-07 YTD Nov (€)

0% to -10% 0%-5% 5%-10% 10% -15% 15%-20%

Frankfurt Amsterdam Athens Barcelona

Prague Berlin Geneva Brussels

Rome Budapest Madrid Lisbon

Dublin Paris London

Milan Moscow

Stockholm

Vienna

WarsawSource: HotelBenchmarkTM Zurich

Key Trends for European Hotels

● Occupancy and room rate● Transactions● Hotel valuation

Hotel investment volumes (€m)

Source: HVS International Research

—

5,000

10,000

15,000

20,000

25,000

1999 2000 2001 2002 2003 2004 2005 2006Single Asset Transactions Portfolio Activity

European single asset transactions

Source: HVS International Research

-500

1,0001,5002,0002,5003,0003,5004,0004,5005,0005,5006,0006,500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

€ Milli

ons (

Appr

oxim

ate)

0

20

40

60

80

100

120

140

160

Numb

er of

Tran

sacti

ons

€ Millions Number of Transactions

Buyer categories 2006 (€m)

Source: HVS International Research

Private Equity, 5,178

Hotel Operator, 6,864

Undisclosed, 137High-Net-Worth Individual, 585

Real Estate Investor, 3,448

Hotel Investment Company, 2,789

Institutional Investor, 1,277

Key portfolio transactions – 2006

Portfolio Buyer Price €m Room €

Hilton Group Hilton Hotels Corp 4,767 --

Marriott (47 UK) Delek 1,671 195,000

De Vere (35 UK) Alternative Hotel Gp 1,073 229,000

Travelodge (229 UK) Dubai Int’l Capital 977 57,000

Starwood (5 Europe) Host Hotels 762 291,000

Hospitality Europe (8) Blackstone Group 650 201,000

Key portfolio transactions – 2007

Portfolio Buyer Price €m Room €

Hilton Hotels Corp (2,800 hotels) Blackstone Group 19,043 --

Marriott (47 UK) Quinlan Private 1,619 190,500

Jury’s Inns (20 UK, Eire) Quinlan Private 1,165 241,000

Accor (91 Germany) Moorpark 863 72,000

Scandic Hotels (132) EQT 833 --

Accor (30 UK) Land Securities 711 142,000

Key single asset transactions – 2006

Hotel Buyer Price €k Room €

Hotel Lancaster, Paris – 60 rooms Hospes Hotels 48,000 800,000

Four Seasons, Milan – 118 rooms Statuto Group 200,000 1,695,000

Hotel Arts, Barcelona – 483 rooms Host Hotels 417,000 863,000

Great Eastern, London – 267 rooms

Global Hyatt / JER Partners 217,200 813,000

Marriott Park Lane, London – 157 rooms Bahrain Royal Family 151,400 964,300

Blakes Hotel, London – 49 rooms Sir Mark Weinberg 33,400 681,400

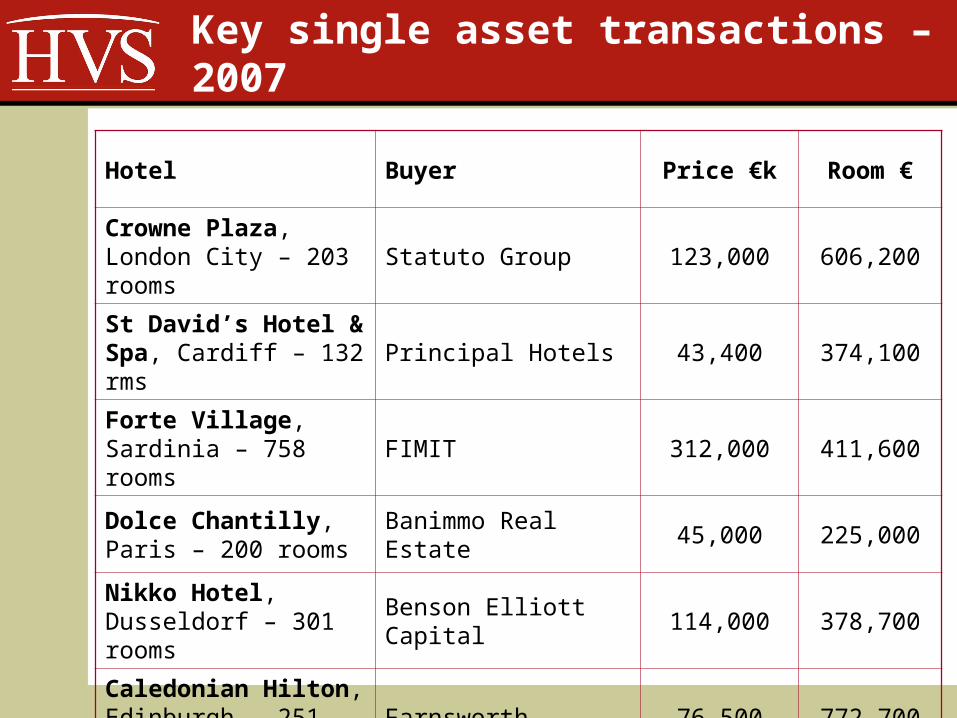

Key single asset transactions – 2007

Hotel Buyer Price €k Room €

Crowne Plaza, London City – 203 rooms Statuto Group 123,000 606,200

St David’s Hotel & Spa, Cardiff – 132 rms Principal Hotels 43,400 374,100

Forte Village, Sardinia – 758 rooms FIMIT 312,000 411,600

Dolce Chantilly, Paris – 200 rooms Banimmo Real Estate 45,000 225,000

Nikko Hotel, Dusseldorf – 301 rooms Benson Elliott Capital 114,000 378,700

Caledonian Hilton, Edinburgh – 251 rooms Farnsworth 76,500 772,700

Key Trends for European Hotels

● Occupancy and room rate● Transactions● Hotel valuation

Value trends – winners & ‘losers’ 2006

Moscow

Amster

damLisb

on

Warsaw

Madrid

Berlin

Budape

st

Athens

Prague

Hambur

g

-10%

-5%

0%

5%

10%

15%

20%

25%

2006

Values – Top 10 European cities €/room

2005 2006London 516,100 London 576,700Paris 484,500 Paris 528,200Milan 415,800 Milan 467,000Zurich 376,000 Zurich 413,800Geneva 340,100 Geneva 365,800Rome 288,500 Edinburgh 319,600Edinburgh 285,200 Rome 311,000Amsterdam 261,000 Amsterdam 304,000Prague 248,800 Moscow 290,500Moscow 241,200 Prague 252,300

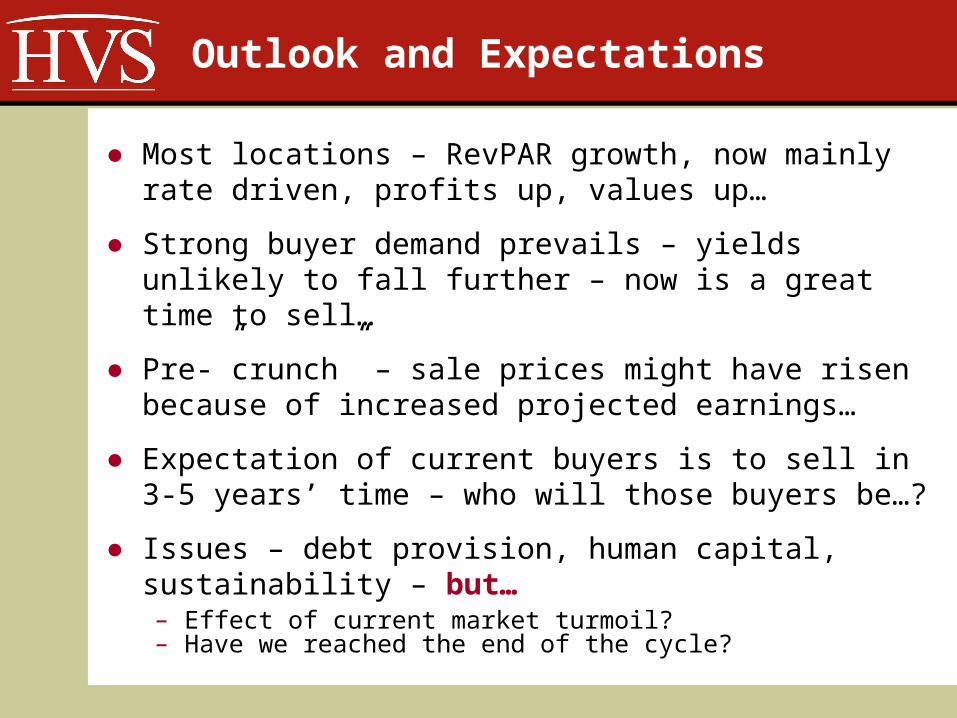

Outlook and Expectations

● Most locations – RevPAR growth, now mainly rate driven, profits up, values up…

● Strong buyer demand prevails – yields unlikely to fall further – now is a great time to sell…

● Pre-”crunch” – sale prices might have risen because of increased projected earnings…

● Expectation of current buyers is to sell in 3-5 years’ time – who will those buyers be…?

● Issues – debt provision, human capital, sustainability – but…– Effect of current market turmoil? – Have we reached the end of the cycle?

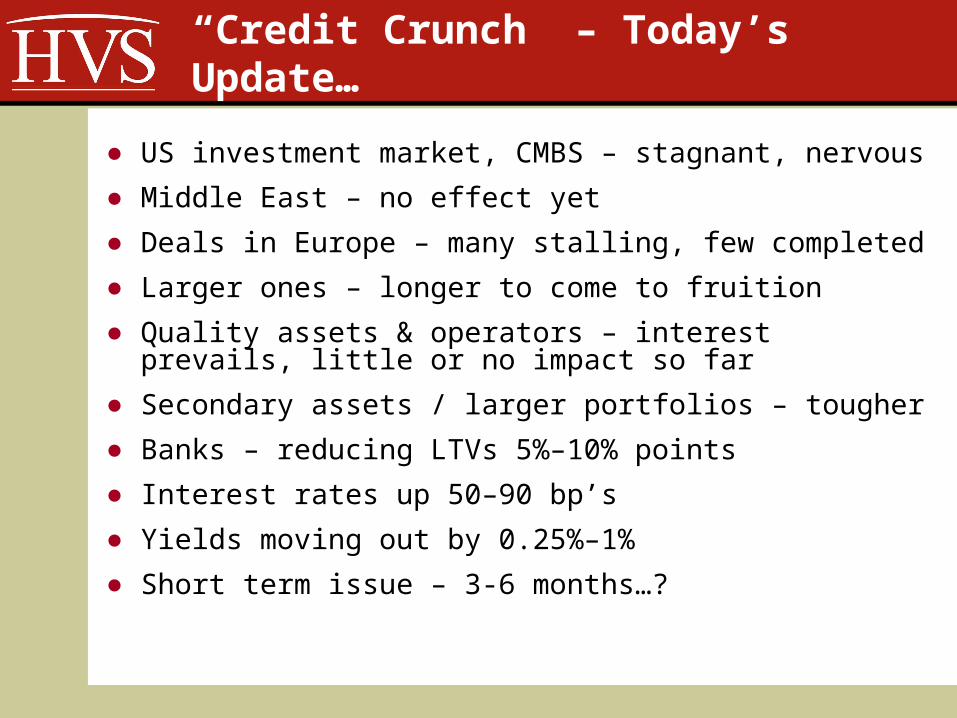

“Credit Crunch” – Today’s Update…

● US investment market, CMBS – stagnant, nervous● Middle East – no effect yet● Deals in Europe – many stalling, few completed● Larger ones – longer to come to fruition● Quality assets & operators – interest prevails, little or

no impact so far● Secondary assets / larger portfolios – tougher● Banks – reducing LTVs 5%–10% points● Interest rates up 50–90 bp’s● Yields moving out by 0.25%–1%● Short term issue – 3-6 months…?

Thank you!

Russell KettManaging DirectorHVS International

7-10 Chandos StreetCavendish SquareLondon W1G 9DQ

Tel: 020 7878 7700Fax: 020 7878 7799