European Health & Fitness Market Study 2016 … development is one of the main forces shaping the...

24

European Health & Fitness Market Study 2016 Karsten Hollasch, Deloi&e

Transcript of European Health & Fitness Market Study 2016 … development is one of the main forces shaping the...

EuropeanHealth&FitnessMarketStudy2016KarstenHollasch,Deloi&e

The European Health & Fitness Market Report 2016 Karsten Hollasch

2016 Deloitte

21%

18%

9% 8% 8%

5% 5% 4% 3% 3%

16%

5,615

4,830

2,393 2,152 2,130

1,292 1,260 1,090

871 813

4,218

0

1,000

2,000

3,000

4,000

5,000

6,000

UK Germany France Italy Spain Netherlands Russia Turkey Poland Switzerland Others

Tota

l rev

enue

s (€

m)

The European fitness market was worth €26.7bn in 2015, with the top 5 countries representing almost two thirds

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 3

Sources: EuropeActive/Deloitte, DSSV/DHfGP/Deloitte, The Leisure Database

Top 10 European health and fitness markets by revenues (2015) Market size (€m), Share of total market (%)

64% of total European market 20% of total European market

2016 Deloitte

Germany

United Kingdom

France

Italy Spain

Russia

Poland

NetherlandsTurkey

Sw eden

0%

1%

2%

3%

4%

5%

6%

7%

8%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Cha

nge

in m

embe

rshi

p (in

%)

Penetration rate (% of total population)

Germany and the UK strengthened their positions as the largest European markets in terms of membership

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 4

Sources: EuropeActive/Deloitte, DSSV/DHfGP/Deloitte, The Leisure Database

Top 10 European health and fitness markets by membership (2015) Penetration rate (% of total population), Change in membership (%), Total membership (bubble size)

Above-average membership growth Below-average membership growth

Average penetration rate of top 10 markets

Average growth of top 10 markets

Question I: Which of the following factors are correlated with fitness market penetration? 1. General physical activity of the population 2. Real GDP per capita 3. The degree of urbanisation 4. All of the above 5. None of the above

2016 Deloitte

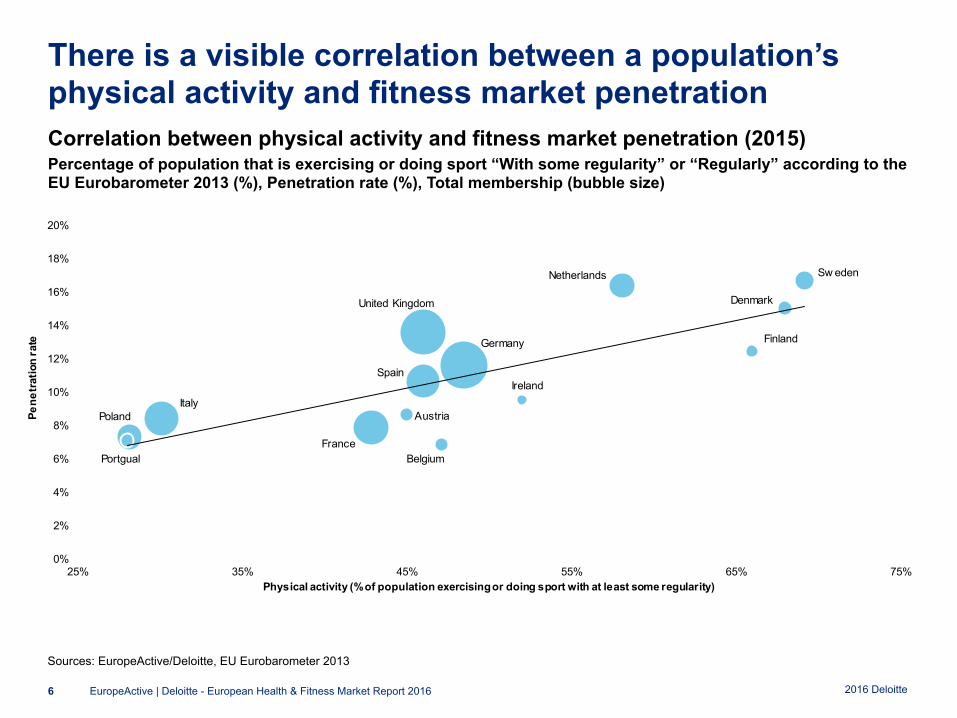

There is a visible correlation between a population’s physical activity and fitness market penetration

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 6

Sources: EuropeActive/Deloitte, EU Eurobarometer 2013

Correlation between physical activity and fitness market penetration (2015) Percentage of population that is exercising or doing sport “With some regularity” or “Regularly” according to the EU Eurobarometer 2013 (%), Penetration rate (%), Total membership (bubble size)

Austria

Belgium

Denmark

Finland

France

Germany

IrelandItaly

Netherlands

Poland

Portgual

Spain

Sw eden

United Kingdom

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

25% 35% 45% 55% 65% 75%

Pene

trat

ion

rate

Physical activity (% of population exercising or doing sport with at least some regularity)

2016 Deloitte

Real GDP per capita and the degree of urbanisation help explain fitness market penetration

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 7

Sources: EuropeActive/Deloitte, Eurostat, The World Bank

Correlation of real GDP per capita and urbanisation with fitness market penetration (2015) Real gross domestic product per capita (in €), Penetration rate (%), Total membership (bubble size)

Urbanisation of 80% or more Urbanisation of less than 80%

Note: The urban population, as stated by The World Bank, refers to people living in urban areas as defined by national statistical offices. It is calculated using World Bank population estimates and urban ratios from the United Nations World Urbanization Prospects.

Austria

Belgium

Denmark

Finland

France

Germany

Ireland

Italy

Netherlands

Norw ay

Poland Portgual

Russia

Spain

Sw eden

Sw itzerland

Turkey

United Kingdom

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000

Pene

trat

ion

rate

Real GDP per capita (€)

Question II: What correlation is there between market concentration (membership share of top 5 operators) and the average membership fees in a country? 1. Higher concentration = Higher membership fees 2. Higher concentration = Lower membership fees 3. No correlation

2016 Deloitte

Markets with a higher market share of top 5 operators tend to have lower average membership fees

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 9

Sources: EuropeActive/Deloitte, Eurostat

Impact of market concentration on PPP-adjusted monthly membership fees (2015) Market share of top 5 operators in terms of membership (%), PPP-adjusted average monthly membership fees incl. VAT (in €), Total membership (bubble size)

Austria

Belgium

Denmark

Finland

France

Germany

Ireland

ItalyNetherlands Norw ay

Poland

PortgualSpain

Sw eden

Sw itzerland

United Kingdom

0

20

40

60

0% 20% 40% 60% 80%

PPP-

adju

sted

ave

rage

mon

thly

gro

ss m

embe

rshi

p fe

es (€

)

Market share of top 5 operators in terms of membership

2016 Deloitte

In Denmark and Belgium, the leading operators represent more than 50% of all members

Notes: 1) Membership figures for Alex Fitness (Russia), Basic-Fit (Belgium), Fitness World (Denmark) and McFIT/High5 (Germany) based on professional judgement; Sources: EuropeActive/Deloitte, Company information

30% to 49%

15% to 29%

50% and more

Less than 15%

Share of top 5 operators and selected market leaders by membership

Leading operator by membership

Market share

(%)

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 10

18%

55%

11%

8%

27%

6%

10%

53%

2016 Deloitte

The fastest-growing fitness operators in 2015 came largely from the low-cost sector

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 11

Non-franchise operation Fully or partly a franchise operation

Selected top 30 European health and fitness operators by membership (2015) Change in membership (%), Revenue per member per month (€), Total membership (bubble size)

Notes: 1) Revenue figures for clever fit, INJOY and Mrs.Sporty, Change in membership for Basic-Fit as well as revenue and membership figures for FitX, McFIT/High5, SportCity/Fit For Free and Virgin Active based on professional judgement; 2) Migros figures only include Swiss business; 3) Nuffield figures do not include corporate fitness and wellbeing centres Sources: EuropeActive/Deloitte, Company information

clever f it

David Lloyd Leisure

McFIT/High5

Pure Gym

SportCity/Fit For Free

Xercise4Less

Fitness First

Health & Fitness Nordic

Actic

Nuffield Health

FitX

INJOY

Keep CoolKieser Training L'Orange Bleue

Migros

Mrs.Sporty

Russian Fitness Group

The Gym Group

Virgin Active

Basic-Fit

0

25

50

75

100

-10% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Reve

nue

per m

embe

r per

mon

th (€

)

Change in membership (in %)

2016 Deloitte

After a total of 24 fitness transactions from 2011 to 2013, 19 M&A activities were recorded in both 2014 and 2015

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 12

Change in ownership by investor type (2015)

Sources: Mergermarket, Bloomberg, Company information, Deloitte analysis

Strategic investors

Financial investors

Founders / Private

shareholders Private

shareholders

Strategic investors

Financial investors

2016 Deloitte

The five leading commercial equipment manufacturers accounted for about 72% of the global market in 2015

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 13

Leading manufacturers’ share of global commercial fitness equipment market (in %)

Sources: EuropeActive/Deloitte, Company information

Estimated global commercial (B2B) market

2016 Deloitte

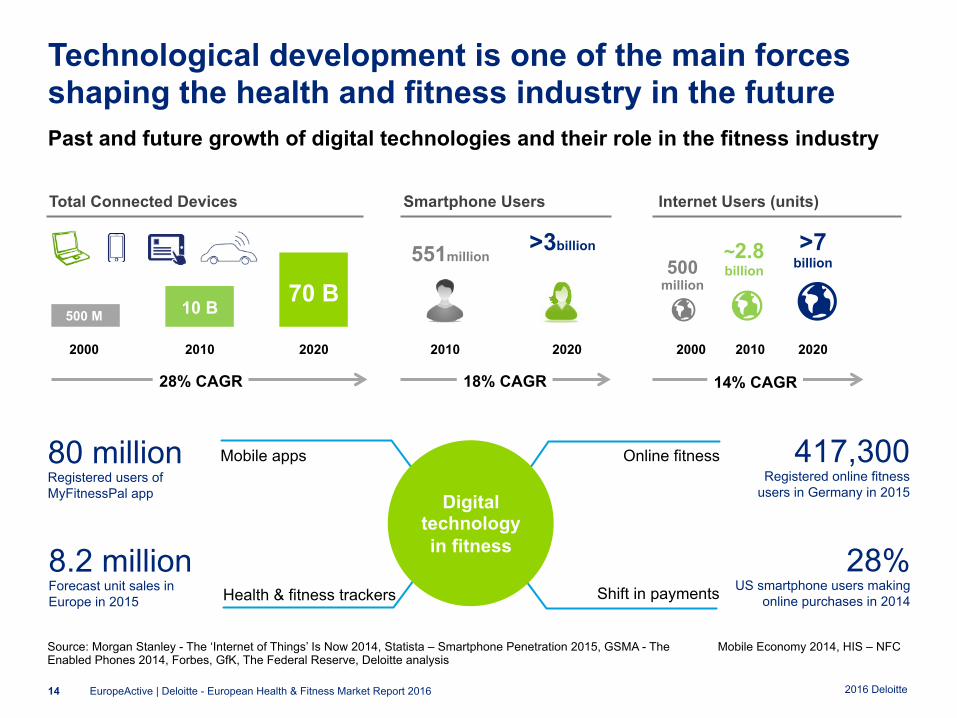

Technological development is one of the main forces shaping the health and fitness industry in the future

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 14

Past and future growth of digital technologies and their role in the fitness industry

Source: Morgan Stanley - The ‘Internet of Things’ Is Now 2014, Statista – Smartphone Penetration 2015, GSMA - The Mobile Economy 2014, HIS – NFC Enabled Phones 2014, Forbes, GfK, The Federal Reserve, Deloitte analysis

Mobile apps

Health & fitness trackers

Online fitness

Shift in payments

Digital technology in fitness

417,300 Registered online fitness

users in Germany in 2015

8.2 million Forecast unit sales in Europe in 2015

28% US smartphone users making

online purchases in 2014

80 million Registered users of MyFitnessPal app

500 M

2000

10 B

2010

70 B

2020 2010 2020

551million >3billion

2000 2020

500 million

2010

~2.8 billion

>7 billion

28% CAGR 18% CAGR 14% CAGR

Total Connected Devices Smartphone Users Internet Users (units)

Thank you for your attention.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/de/UeberUns for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, financial advisory and consulting services to public and private clients spanning multiple industries; legal advisory services in Germany are provided by Deloitte Legal. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 225,000 professionals are committed to making an impact that matters.

2016 Deloitte

BACKUP

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 17

2016 Deloitte

A major macro-economic trend to consider is the increasing age of the European population

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 18

Division of age groups in % of total population (EU-27), 2011 vs. 2060

Sources: Eurostat, Deloitte analysis

Mean age group

Mean age group

6 4 2 0 2 4 6

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80-84

85+

% of total population

Age

Male Female

Mean age groupMean age group

5 3 1 1 3 5

0-4

5-9

10-14

15-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65-69

70-74

75-79

80-84

85+

% of total population

Age

Male Female

2016 Deloitte

Detailed research led to a comprehensive picture of the European health and fitness market

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 19

Methodology

What we have done And what we achieved

Interviews with selected industry experts

Questionnaire for major chain operators

Online questionnaire in twelve different languages for individual club operators

General research work

Identification of individual and chain operators in 18 countries

Educated assessment of industry’s state and development

Detailed information on major European operators

Data of more than 1,000 individual clubs in 13 countries

Insights in existing market reports, data on equipment industry, M&A activity

Detailed club databases on national level

2016 Deloitte

Leading Operator Rankings/Profiles

Recent Mergers & Acquisitions

Perspectives on the Market

Corporate Wellbeing

Content (1/2)

The EuropeActive/Deloitte market report examines the European fitness industry from various perspectives

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 20

New

2016 Deloitte

Innovation in the Fitness Industry

Snapshot of the Equipment

Industry Eurobarometer Top Market

Overview/Profiles

Content (2/2)

New

The EuropeActive/Deloitte market report examines the European fitness industry from various perspectives

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 21

2016 Deloitte

Specialised product offerings and digitalisation are two of the main trends shaping the fitness industry

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 22

Trends and drivers of the fitness industry

Source: Deloitte analysis

Product offerings • Polarisation of market segments • Special interest concepts • Flexible membership concepts

Macro-economic development • National economy • Demographic change • Change in values

Digitalisation & Media • Online fitness clubs • Fitness apps • Social media

Management challenges • Employee management • Franchise • Revenue and cost management

Stakeholders • Investors • Health insurers & politics • Other interest groups

Fitness industry

2016 Deloitte

Most European club operators expect to grow in 2016; Polish clubs are again the most optimistic Expected increase in revenues for 2016 (in %)

Source: EuropeActive/Deloitte

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 23

41.7%

33.3%36.1%

44.4%45.2%41.0%

57.1%

50.0%55.1%

60.7%

40.9%

54.5%

33.3%

4.2%15.7%

14.8%

8.9%12.9%

17.9%

5.7%15.4%

12.2%

10.7%

32.6%

22.7%

44.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

BelgiumFranceRussiaItalyAustriaFinlandIrelandTurkeyNetherlandsSpainPortugalSwedenPoland

Increase 2.5-7.5% Increase >7.5%

2016 Deloitte

After a total of 24 fitness transactions from 2011 to 2013, 19 activities were recorded in both 2014 and 2015

EuropeActive | Deloitte - European Health & Fitness Market Report 2016 24

Selected transactions in the health and fitness industry (2015)

Sources: Mergermarket, Bloomberg, Company information, Deloitte analysis

# Date Company Country Seller Bidder1 Jan 2015 Condizione PL Patrycja Bartnicka-Irndorfer Fitness World

2 Feb 2015 MeridianSpa DE Private investor(s) AFINUM

3 Feb 2015 Form Developpement FR Philippe Ducos Ekkio Capital

4 Mar 2015 Total Fitness UK Co-op Bank / Barclays Ventures NorthEdge Capital / RooGreen Ventures

5 Apr 2015 Virgin Active UK CVC Capital Partners Brait Private Equity

6 May 2015 Fitness World DK Henrik Rossing FSN Capital

7 May 2015 LA Fitness UK Royal Bank of Scotland Pure Gym

8 May 2015 basefit.ch CH Stefan Lüben Verium AG

9 Jun 2015 Aspria DE Ares Management Cofinimmo Group

10 Jul 2015 easyFit CH Private investor(s) basefit.ch

11 Jul 2015 FITmade CH Private investor(s) basefit.ch

12 Nov 2015 Viva Gym ES Magenta Partners Bridges Ventures

13 Nov 2015 The Gym Group UK Phoenix Equity Partners / Bridges Ventures IPO

14 Nov 2015 Pure Gym UK Pure Gym DW Fitness

15 Nov 2015 L’Appart Fitness FR Patrick Mazerot L’Appart Fitness

16 Dec 2015 1Rebel UK 1Rebel Crow dfunding

17 Dec 2015 Physic Club CH Christian Matthey Let's Go Fitness

18 Dec 2015 HealthCity FR 3i Group Ekkio Capital

19 Dec 2015 Ingesport / Go Fit ES Corpfin Capital Mutua Madrileña