European Data Centre Market - FStech · CB Richard Ellis | Page 3 Total Market Retail Colocation...

23

Andrew Jay Head of EMEA Technology Practice Group CB Richard Ellis Data Centre Real Estate Market Update Supply and Demand in the Face of Recession 1 st December 2008

Transcript of European Data Centre Market - FStech · CB Richard Ellis | Page 3 Total Market Retail Colocation...

Andrew JayHead of EMEA Technology Practice GroupCB Richard Ellis

Data Centre Real Estate Market UpdateSupply and Demand in the Face of Recession1st December 2008

CB Richard Ellis | Page 2

Agenda

Market Positioning

Demand

Supply

Pricing

Conclusions

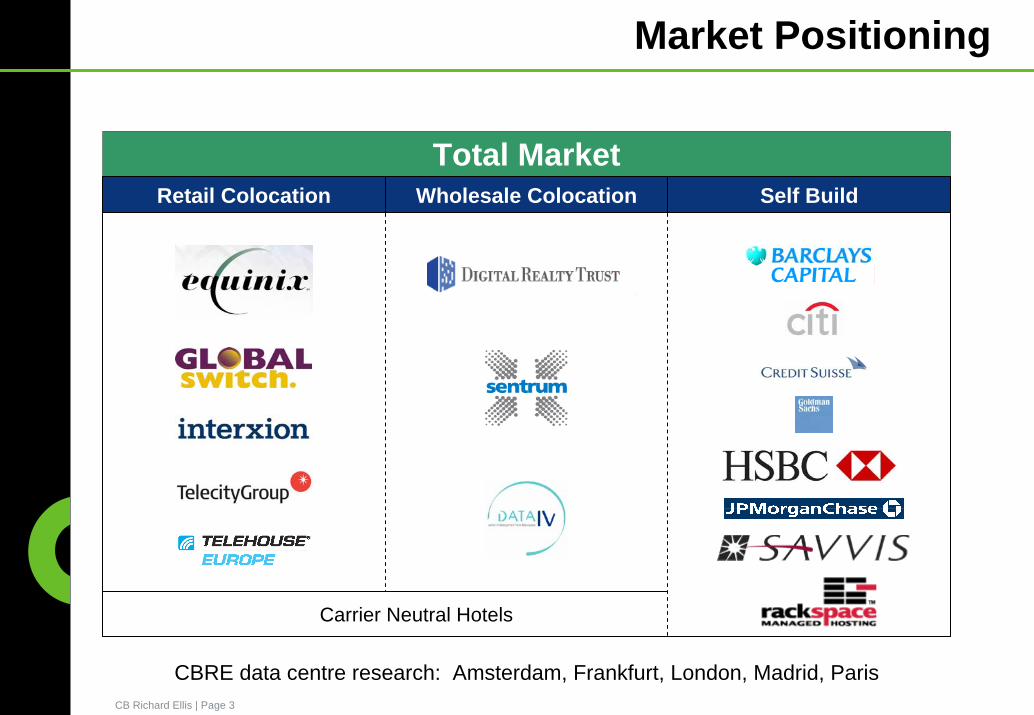

CB Richard Ellis | Page 3

Total MarketRetail Colocation

Market Positioning

Wholesale Colocation Self Build

CBRE data centre research: Amsterdam, Frankfurt, London, Madrid, Paris

Carrier Neutral Hotels

CB Richard Ellis | Page 4

Demand

Existing facilities no longer fit for purpose– Insufficient power/cooling to accommodate new (blade)

technology

– Pressure to use space for people

– Requirement for Zero Downtime – 2N specification

– Landlord conflict to limit data centre plant

Increasing reliance on IT

Expansion of IT equipment

Data centre consolidation initiatives

Internal Drivers

Source: CBRE research

CB Richard Ellis | Page 5

Demand

Terrorist threat or catastrophic event – 9/11

Statutory and regulatory pressures on business continuity (PAS 56) and disaster recovery (FSA regulations)

Corporate Governance – Sarbanes Oxley

Meeting criteria for insurance purposes

Meeting client expectations

External Drivers

Source: CBRE research

CB Richard Ellis | Page 6

Demand

Total Market Take-up

Source: CBRE research

0

20

40

60

80

100

120

140

160

180

Amsterdam Frankfurt London Madrid Paris Total

Thou

sand

m²

2005 2006 2007 2008 Q1/Q2

CB Richard Ellis | Page 7

Demand

Total Market Take-up

Source: CBRE research

Amsterdam Frankfurt London Madrid Paris Total

Thou

sand

m²

2005 2006 2007 2008 Projection

0

20

40

60

80

100

120

140

160

180

CB Richard Ellis | Page 8

DemandTake-up by Market Type & Sector

* Projected take-up

Source: CBRE research

Wholesale Colocation Model– Real estate model

– Variety of product offerings

– Modular bespoke fitout is contract led

– FM services are optional

– No managed services

– Pricing is driven by return on build cost

0

20

40

60

80

100

120

140

160

180

2001 2002 2003 2004 2005 2006 2007 2008 *

Thou

sand

m²

Self Build

Wholesale Colocation

Retail Colocation

CB Richard Ellis | Page 9

60%

8%

32%

54%

15%

31%

64%15%

21%Corporate

Systems Integrator

Technology & Telecoms200555,000 m²

200664,000 m²

2007158,000 m²

DemandTake-up by Market Type & Sector

Source: CBRE research

2008152,000 m²(projection)

66%9%

25%

2009

?

* Projected take-up

0

20

40

60

80

100

120

140

160

180

2001 2002 2003 2004 2005 2006 2007 2008 *

Thou

sand

m²

Self Build

Wholesale Colocation

Retail Colocation

CB Richard Ellis | Page 10

DemandTake-up By Market Type

Company Location Market Type FloorArea (m²)

Adapt London Retail Colocation 1,500

BT London Wholesale Colocation 2,000

Paris

Paris

German Bank London Wholesale Colocation 4,000

Petrochemical Company London Wholesale Colocation 2,000

US Investment Bank London Self Build 15,000

SAVVIS London Self Build 6,000

Rackspace London Self Build 5,000

IBM Retail Colocation 1,000

AT&T Retail Colocation 400

Source: CBRE research

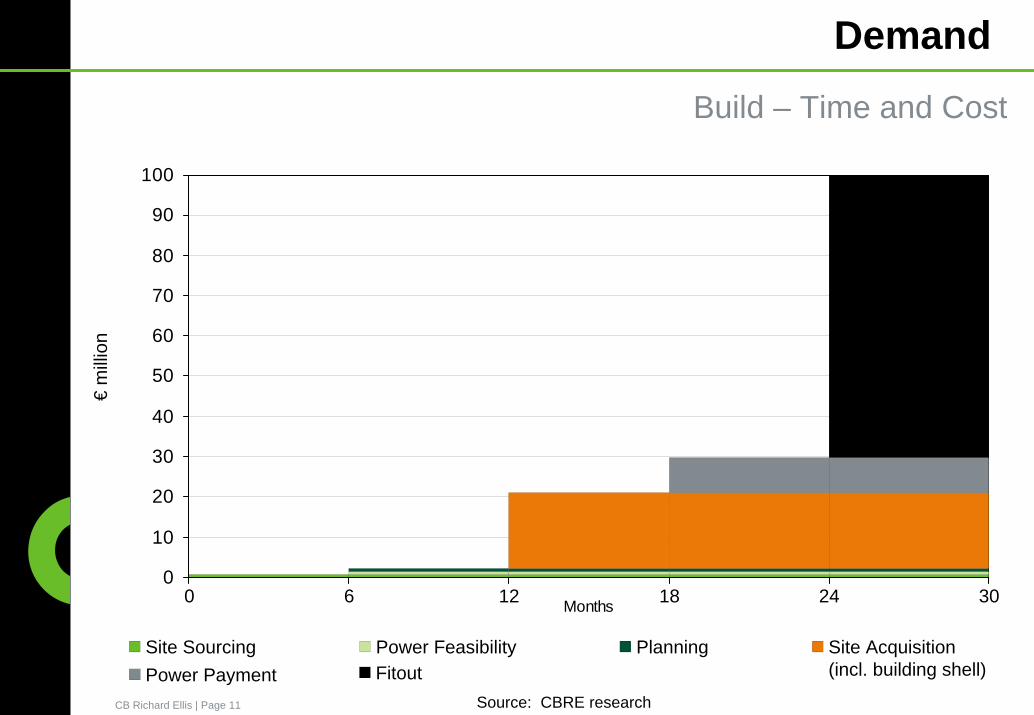

CB Richard Ellis | Page 11

Demand€

milli

onBuild – Time and Cost

Site Sourcing Power Feasibility Planning Site Acquisition(incl. building shell)Power Payment Fitout

6 18 2412 300

Source: CBRE research

0

10

20

30

40

50

60

70

80

90

100

Months

CB Richard Ellis | Page 12

-0.5

0

0.5

1

1.5

2

Credit Crunch: LIBOR % aboveBank of England base rate

2008 2009 2010

Demand

Demand Pipeline

2005 2006 2007

projection

1 321. Bear Stearns collapse – credit

market closes

2. Banks write down toxic debt

3. Lehman Brothers collapse -Armageddon

Source: CBRE research

0

50

100

150

200

250

Thou

sand

m²

CB Richard Ellis | Page 13

New Supply (planned)

Demand (actual)

Demand and Supply

Credit Crunch Impact

Source: CBRE research

New Supply

New Supply (actual)DemandDemand (projected)

0

100

200

300

400

500

60020

05 Q

1

2005

Q2

2005

Q3

2005

Q4

2006

Q1

2006

Q2

2006

Q3

2006

Q4

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

-0.5

0

0.5

1

1.5

2Th

ousa

nd m

²

CB Richard Ellis | Page 14

Supply

London Colocation Market

Existing colocation facilitiesat 1 Jan 200519 facilities, 160,000 m²

60 km aroundcentral London

Source: CBRE research

CB Richard Ellis | Page 15

London Colocation Market

Supply

60 km aroundcentral London

Existing colocation facilitiesat 1 Jan 200519 facilities, 160,000 m²

New supply (pre-crunch)2005 to 201035 facilities, 406,900 m²

Source: CBRE research

CB Richard Ellis | Page 16

London Colocation Market

Supply

60 km aroundcentral London

Existing colocation facilitiesat 1 Jan 200519 facilities, 160,000 m²

New supply (pre-crunch)2005 to 201035 facilities, 406,900 m²

64% reduction in proposed new floor space

New supply (actual)2005 to 201017 facilities, 145,900 m²

Source: CBRE research

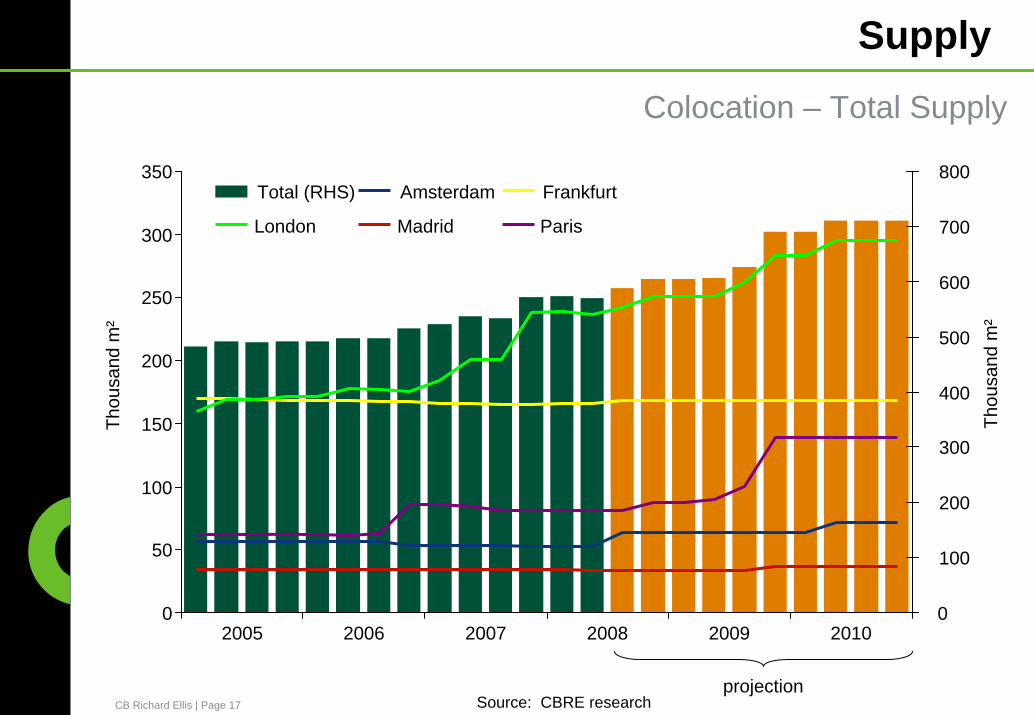

CB Richard Ellis | Page 17

Supply

Colocation – Total Supply

2005 2006 2007 2008 20102009

Source: CBRE researchprojection

0

50

100

150

200

250

300

350

Thou

sand

m²

0

100

200

300

400

500

600

700

800

Thou

sand

m²

Total (RHS) Amsterdam Frankfurt

London Madrid Paris

CB Richard Ellis | Page 18

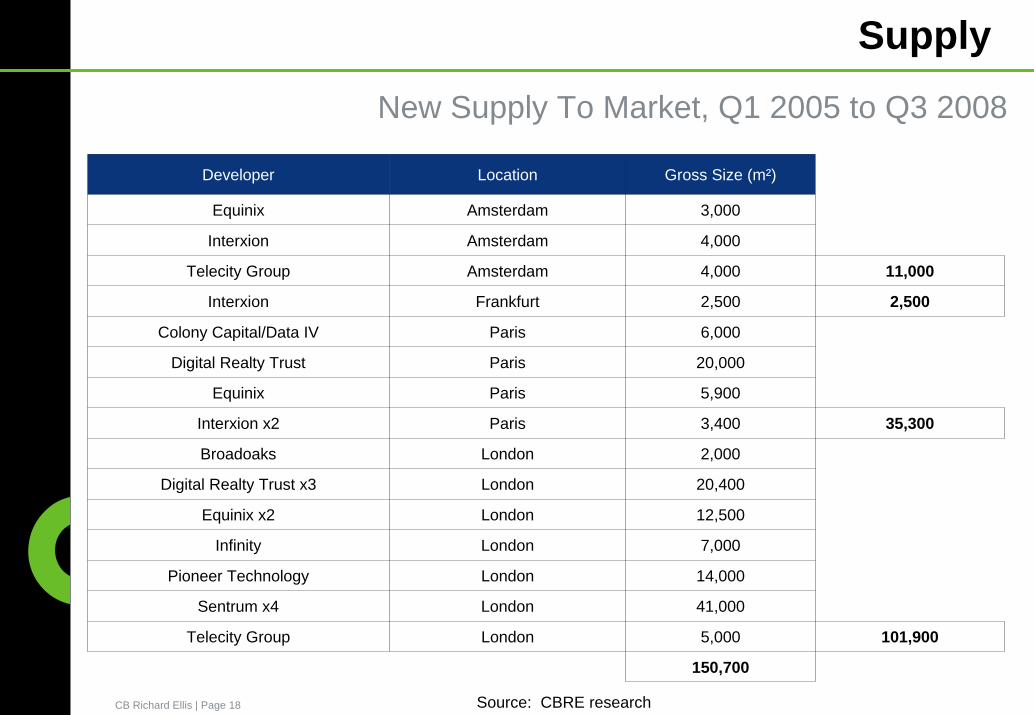

Supply

New Supply To Market, Q1 2005 to Q3 2008

Developer Location Gross Size (m²) City Total (m²)

Equinix Amsterdam 3,000

11,000

2,500

Colony Capital/Data IV Paris 6,000

Digital Realty Trust Paris 20,000

Equinix Paris 5,900

Interxion x2 Paris 3,400 35,300

101,900

Interxion Amsterdam 4,000

Telecity Group Amsterdam 4,000

Sentrum x4 London 41,000

Interxion Frankfurt 2,500

Broadoaks London 2,000

Digital Realty Trust x3

Telecity Group London 5,000

150,700

20,400

12,500

7,000

14,000

London

Equinix x2 London

Infinity London

Pioneer Technology London

Source: CBRE research

CB Richard Ellis | Page 19

Supply

Future Supply Pipeline from Q4 2008 to Q1 2010

Developer Location Gross Size (m²) City Total (m²)

8,000 8,000

3,000

51,000

Sentrum London 10,000

44,000

Interxion Madrid 3,000

Colony Capital/Data IV Paris 18,000

Digital Realty Trust Paris 10,000

Equinix Paris 10,000

Global Switch Paris 10,000

Telecity Group Paris 3,000

Equinix London 10,000

12,000

Telehouse London 12,000

106,000

Global Switch Amsterdam

e-shelter London

Source: CBRE research

CB Richard Ellis | Page 20

Supply

Vacancy Rates

2005 2006 2007 20092008

Source: CBRE researchprojection

0%

10%

20%

30%

40%

50%

60% Overall AmsterdamFrankfurt LondonMadrid Paris

CB Richard Ellis | Page 21

Pricing

Pricing trending towards € per kW

Retail Pricing– €2,900 - €3,500+ per m² pa (1,250 Watts per m²) - €2,560 per kW per annum

Wholesale Pricing– €1,800 - €2,400 per m² pa (1,250 Watts per m²) - €1,680 per kW per annum

Rents driven by– SPECIFICATION

– Power density

– Level of service provided

– Supply and demand (by market and building)

Colocation Pricing

Source: CBRE research

CB Richard Ellis | Page 22

Conclusions

Underlying demand drivers remain – increased reliance on IT and need for increased processing power

Credit Crunch has had relatively minor impact on Demand compared to Supply

Capital constraints mean less opportunities to self build – OPEX solutions preferred

BEWARE – fragile supply and demand dynamics

CB Richard Ellis | Page 23

Questions ?

Thank you

If you wish to receive the quarterly CBRE data centre research bulletin, please email [email protected]