European Construction Monitor 2016-2017: Growing ... · uncertainty in the economy and financial...

28

European Construction Monitor 2016-2017: Growing opportunities in local markets

Transcript of European Construction Monitor 2016-2017: Growing ... · uncertainty in the economy and financial...

European Construction Monitor2016-2017: Growing opportunities in local markets

European Construction Monitor | 2016-2017: Growing opportunities in local markets

02

European Construction Monitor is a publication edited and distributed by Deloitte.

DirectorsJurriën Veldhuizen, Partner Real Estate, Segment Leader Construction, NetherlandsNico Dijkstra, Partner Corporate Finance, Financial Advisory Services, Netherlands

Coordinated byMorsal SarwarzadehGerben SinkeCarlo SturmLaura Zegger

ContactReal Estate Department, Deloitte NetherlandsPhone: +31-88 288 3281Fax: +31-88 288 9752

March 2017

03

European Construction Monitor | 2016-2017: Growing opportunities in local markets

1. Introduction 05

2. Looking back 07

3. Going forward 14

4. Conclusion 23

5. European real estate, construction and 25 infrastructure group contacts

Contents

04

European Construction Monitor | 2016-2017: Growing opportunities in local markets

European Construction Monitor | 2016-2017: Growing opportunities in local markets

05

We are pleased to present the sixth edition of the European Construction Monitor, which looks at the latest trends and issues in mergers & acquisitions (M&A) in the European construction industry. This 2016–2017 publication complements the 2015 “European Powers of Construction” (EPoC), a Deloitte research paper examining the status of major European-listed construction companies.

Market trends: Supply chain integration and digital constructionThe trend we have seen over the last few years is that the recovery of the local construction markets in Europe has not exactly led to a likewise increase of M&A in the construction sector. In search for more revenue and profits the EU construction sector showed a significant increase in international and diversification transactions from 2012 until 2015. M&A activity over 2016 seems to break with these trends.

Compared to the total of 144 transactions in 2015, the number of transactions over 2016 has increased slightly, to 149. Both the percentage of cross-border transactions and diversification transactions dropped over 2016 – for the first time since 2012. Although the decline over 2016 is limited, the trend break indicates a renewed focus of European construction companies on local markets and their core business. Local real estate experts have noticed an increased focus on supply chain integration in the construction markets over 2016. This seems in line with the ongoing recovery of local construction markets, affiliated supply chain pressure, and construction companies focusing on increasing their revenues and profit margins in their core business on local markets. With growth being projected for most EU construction markets, we expect an increased focus on supply chain integration in the coming year.

Another noticeable trend is the increased application of digital construction across Europe. Now, as markets recover and demand for construction increases, the use and development of new technologies in the construction sector is finally growing. The pattern of the digital construction trend seems about the same in most EU construction markets: mainly larger construction companies are investing in digital construction. As continuing growth is projected in the construction sector, we expect digital construction, and foremost BIM, to finally mature in the following years.

The impact of Trump’s presidency and BrexitThis year’s monitor includes our experts’ opinions on the potential effects on the construction sector of both the Brexit and Trump’s presidency. These recent political shifts in the US and the UK are said to potentially have an impact on the European construction. However, according to our specialists both developments may cause uncertainty in the economy and financial markets, which could indirectly affect the construction markets, though neither will have a large impact on the construction sector. In contrast, the extensive investments in infrastructure expected under Trump’s presidency may benefit European construction companies. Their experience in public private partnerships and large scale projects means European construction companies should be able to benefit from these investments.

This European Construction Monitor analyses the market trends in the European construction industry by looking back and forward at the same time. In producing this outlook Deloitte has combined these analyses with the in depth, local knowledge its European member firms have of M&A, real estate, construction and infrastructure.

1. Introduction

Highlights in this publication

• M&A activity within the European construction sector continues to be relatively stable: 149 recorded transactions in 2016 compared to 144 recorded transactions in 2015.

• The average transaction value of individual transactions decreased to EUR 203 million in 2016, down from EUR 241 million in 2015.

• The share of PE transactions seems to stabilise at approximately a quarter of the total transactions: 26.8% of the transactions were PE transactions in 2016, compared to 26.4% in 2015.

• The share of diversification transactions dropped to 27.0% in 2016, down from 31.3% in 2015.

• Renewed focus of European construction companies on local markets and their core business is expected to lead to an increased focus on supply chain integration.

• Digital construction is expected to finally mature in the coming years.

• Both Brexit and Trump’s presidency are not expected to have a large impact on the European construction sector. Trump’s presidency may even lead to opportunities for EU construction companies in PPP infrastructe projects in the US.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

06

European Construction Monitor | 2016-2017: Growing opportunities in local markets

European Construction Monitor | 2016-2017: Growing opportunities in local markets

07

Building on the 2014 and 2015 editions and the continuous trend of diversification in the construction sector we have analysed the M&A activity of construction companies combined with installation, engineering and infrastructural companies involved in the construction sector. Including these in the sample size allows for a comprehensive picture of M&A activity within the construction sector as a whole.

Developments in 2015-2016In last years’ monitor we had not expected a significant change in the number of transactions for 2016. We did suggest, though, that the ongoing recovery in local construction markets might result in a slight rise of the number of transactions compared to the last few years. This seems to be holding true for 2016.

M&A activity within the European construction sector shows a slight increase over the last three years but continues to be relatively stable compared to 2015: 149 recorded transactions in 2016 compared to 144 recorded transactions in 2015.

When analysing the 2010-2016 period using the broader definition of construction, we have noticed a relatively stable level of M&A activity: the number of transactions fluctuated between 126 and 149 per year, with an average of 131. Thus, 2016 has the highest number of transactions since 2010. Extrapolating these figures, we expect the trend towards stabilisation in M&A activity to continue, resulting in approximately the same number or slightly more transactions in 2017.

The average transaction value of individual transactions decreased to EUR 203 million in 2016, down from EUR 241 million in 2015. Compared to an average value of disclosed transactions of approximately EUR 343 million in 2013, the average transaction size has dropped for the third year in a row. This does indicate that companies made smaller transactions, which are usually add-ons for their core business. This is in line with last year’s monitor, were we expected an increase in relatively small-sized transactions. Due to the ongoing recovery of most local commercial and residential construction markets, construction companies are strengthening their core business to be able to profit from the upturn in local construction markets.

The share of PE transactions seems to stabilise at approximately a quarter of the total: 26.8% of the transactions in 2016 were PE transactions compared to 26.4% in 2015. Notable is the sharp decrease in transaction size of disclosed PE transactions. The average transaction value

2. Looking back

The divestment of Bilfinger

Bilfinger SE concluded the sale of its Building and Facility segment to EQT in September 2016. The sale price amounted to approximately EUR 1.2 billion. Only weeks after the purchase EQT launched the resale of the building part of the business it had just acquired.

The European construction sector recorded 149 transactions in 2016, showing a slight increase for the third year in a row.

Figure 1: Number of transactions in the construction sector Source: Mergermarket, 2017

20100

20

60

80148 134

2011

126

2012

139

2013

127

2014

144

2015

149

2016

100

120

140

160

180

40

European Construction Monitor | 2016-2017: Growing opportunities in local markets

08

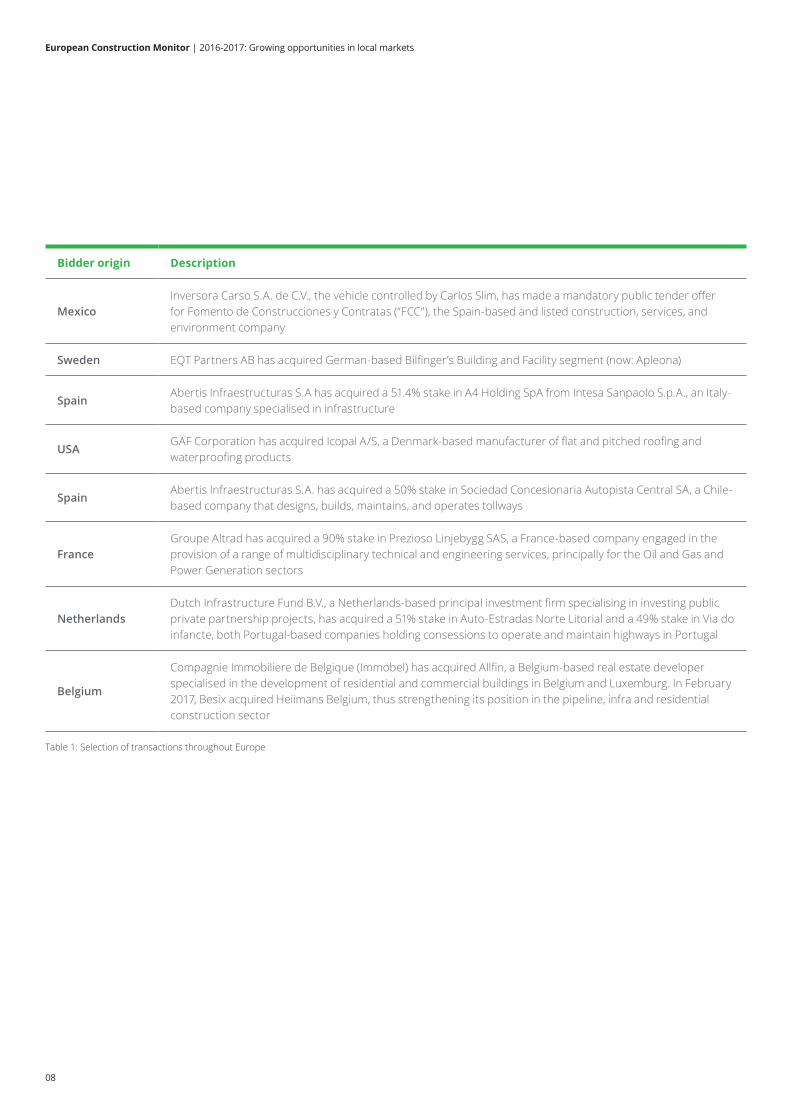

Bidder origin Description

MexicoInversora Carso S.A. de C.V., the vehicle controlled by Carlos Slim, has made a mandatory public tender offer for Fomento de Construcciones y Contratas (“FCC”), the Spain-based and listed construction, services, and environment company

Sweden EQT Partners AB has acquired German-based Bilfinger’s Building and Facility segment (now: Apleona)

SpainAbertis Infraestructuras S.A has acquired a 51.4% stake in A4 Holding SpA from Intesa Sanpaolo S.p.A., an Italy-based company specialised in infrastructure

USAGAF Corporation has acquired Icopal A/S, a Denmark-based manufacturer of flat and pitched roofing and waterproofing products

SpainAbertis Infraestructuras S.A. has acquired a 50% stake in Sociedad Concesionaria Autopista Central SA, a Chile-based company that designs, builds, maintains, and operates tollways

FranceGroupe Altrad has acquired a 90% stake in Prezioso Linjebygg SAS, a France-based company engaged in the provision of a range of multidisciplinary technical and engineering services, principally for the Oil and Gas and Power Generation sectors

NetherlandsDutch Infrastructure Fund B.V., a Netherlands-based principal investment firm specialising in investing public private partnership projects, has acquired a 51% stake in Auto-Estradas Norte Litorial and a 49% stake in Via do infancte, both Portugal-based companies holding consessions to operate and maintain highways in Portugal

Belgium

Compagnie Immobiliere de Belgique (Immobel) has acquired Allfin, a Belgium-based real estate developer specialised in the development of residential and commercial buildings in Belgium and Luxemburg. In February 2017, Besix acquired Heiimans Belgium, thus strengthening its position in the pipeline, infra and residential construction sector

Table 1: Selection of transactions throughout Europe

European Construction Monitor | 2016-2017: Growing opportunities in local markets

09

decreased to EUR 75 million in 2016, down from EUR 574 million in 2015. The amount of strategic transactions, on the other hand, continue to rise for the fourth year: of the transactions in 2016 23,5% were disclosed strategic transactions compared to 22,9% in 2015. The average transaction value increased sharply to EUR 255 million in 2016, up from EUR 59 million in 2015.

We reported a continuation of the purchase of stakes and / or acquisition of entire construction companies. These transactions were generally higher in value than add-on transactions and are often done on a cross-border and cross-continental basis. In 2016, the number of cross-border transactions remained relatively stable compared to last years’ monitors: 76 cross-border transactions in 2016 compared to 79 transactions in 2015. This also applies to the share of intercontinental transactions within the cross-border transactions: 34 transactions in 2016 compared to 37 in 2015. Although the number of cross-border and intercontinental transactions seems to stabilise and even shows a slight decrease, the international focus of European construction sector seemingly continues to be a dominant strategy of larger construction companies.

Figure 2: Percentage of diversification transactions (Source: Mergermarket, 2017)

20100%

10.0%

30.0%

25.0% 27.6%

2011

20.6%

2012

22.3%

2013

28.3%

2014

31.3%

2015

27.0%

2016

40.0%

Figure 3: Percentage of cross-border transactions (Source: Mergermarket, 2017)

20100%

10.0%

30.0%

40.0%

28.4%35.8%

2011

27.0%

2012

34.5%

2013

49.6%

2014

54.9%

2015

51.0%

2016

50.0%

60.0%

20.0%

20.0%

We noticed a slight decrease in diversification transactions compared to last year’s monitor. In 2016, 31.3% of all transactions were identified as diversification transactions, against 27.0% in 2015. Combined with the decrease in cross-border transactions, these trends indicate that construction companies are shifting their focus back to their core business within their national markets.

Turkish Renaissance saves Dutch Ballast Nedam

In December 2015/January 2016, Turkish construction company Renaissance concluded the purchase of Netherlands-based Ballast Nedam after Ballast Nedam got into a difficult financial situation. The sale price amounts to approximately EUR 117 million.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

10

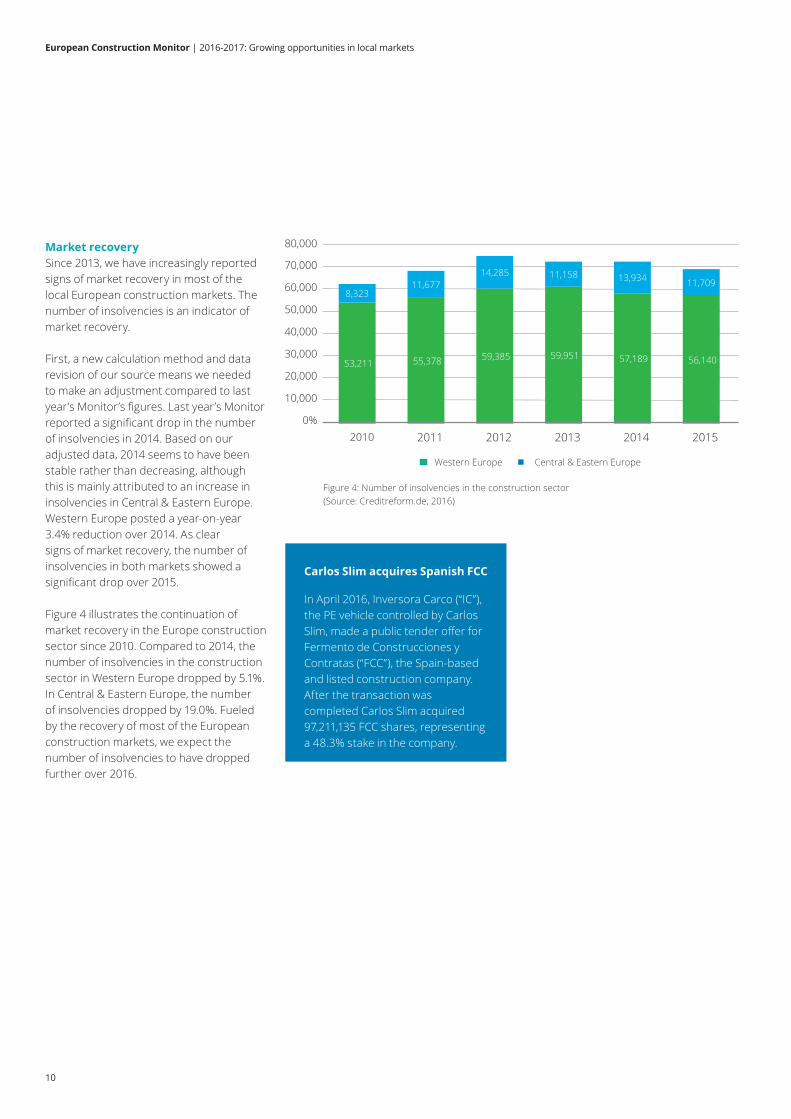

Market recoverySince 2013, we have increasingly reported signs of market recovery in most of the local European construction markets. The number of insolvencies is an indicator of market recovery.

First, a new calculation method and data revision of our source means we needed to make an adjustment compared to last year’s Monitor’s figures. Last year’s Monitor reported a significant drop in the number of insolvencies in 2014. Based on our adjusted data, 2014 seems to have been stable rather than decreasing, although this is mainly attributed to an increase in insolvencies in Central & Eastern Europe. Western Europe posted a year-on-year 3.4% reduction over 2014. As clear signs of market recovery, the number of insolvencies in both markets showed a significant drop over 2015.

Figure 4 illustrates the continuation of market recovery in the Europe construction sector since 2010. Compared to 2014, the number of insolvencies in the construction sector in Western Europe dropped by 5.1%. In Central & Eastern Europe, the number of insolvencies dropped by 19.0%. Fueled by the recovery of most of the European construction markets, we expect the number of insolvencies to have dropped further over 2016.

Carlos Slim acquires Spanish FCC

In April 2016, Inversora Carco (“IC”), the PE vehicle controlled by Carlos Slim, made a public tender offer for Fermento de Construcciones y Contratas (“FCC”), the Spain-based and listed construction company. After the transaction was completed Carlos Slim acquired 97,211,135 FCC shares, representing a 48.3% stake in the company.

Figure 4: Number of insolvencies in the construction sector (Source: Creditreform.de, 2016)

2010

53,211

8,323

55,378

11,677

2011

59,385

14,285

2012

59,951

11,158

2013

57,189

13,934

2014

56,140

11,709

20150%

10,000

30,000

40,000

50,000

60,000

70,000

80,000

20,000

Western Europe Central & Eastern Europe

European Construction Monitor | 2016-2017: Growing opportunities in local markets

11

Trend I: Supply chain integrationThe European Construction market has witnessed a significant increase of cross-border and diversification transactions over the last five years. The trends of diversification and internationalisation by European construction companies are primarily attributed to the search for revenue and profit due to the poor conditions on local markets.

Meanwhile, market conditions on the European continent recovered in the past two years. While construction volumes grew, sharply increased subcontractors’ prices continued to put pressure on operating margins. This so-called supply chain pressure results from the increased demand for construction associated with the challenge to attract sufficient labour and subcontractors with the right capabilities and capacity. Even though margins in the local construction sector have increased over 2016, supply chain pressure continues to be an issue in most European construction markets.

Both the percentage of cross-border transactions and diversification transactions dropped over 2016 – for the first time since 2012. The percentage of cross-border transactions dropped to 51.0% in 2016, down from 54.9% in 2015. The percentage of diversification transactions decreased to 27.0%, down from 31.3%. Although the declines over 2016 are limited, the trend break indicates a renewed focus of European construction companies on local markets and their core business.

Our local real estate experts increasingly observed M&A activity in local construction supply chains over the last year. Larger construction companies are targeting mid-sized and small-sized subcontractors, while at the same time European construction companies have stepped up the acquisition of suppliers and supporting services in their core business.

This focus on supply chain integration appears to be in line with the ongoing recovery of local construction markets and construction companies focusing on increasing their revenues and profit margins in their core business on local markets. As growth is projected for most EU construction markets, we expect an increased focus on supply chain integration in the coming year.

Trump’s presidency: opportunities for EU construction companies expected in PPP infrastructure projects

Our experts feel that Donald Trump’s election to the US presidency could boost the US construction market over the next couple of years, considering the proposed investments in infrastructure. A general issue with Trump’s election is the industry-wide uncertainty that comes with it. Trump is expected to deregulate the US economic sector, combined with the introduction of protectionist measures.

Our local Real Estate experts point out the possible currency related issues on the back of Trump’s presidency. Any increase in interest rates in the medium term is likely to have a negative impact on the housing market and, thus, on the demand for residential construction.

That said, the most likely way to finance Trump’s proposed infrastructure investments will be through public private partnerships, this could benefit EU construction companies. European construction companies are generally very experienced in participating in public private partnerships and working on large scale infrastructure projects. The potential benefits for EU construction companies depend on their position on the US construction market. For instance, many Spanish companies are well positioned in the US market, having acquired American peers and developed projects during the last couple of years. However, in light of the interest rate rise the FED is expected to announce shortly, the Spanish real estate experts, too, point out the uncertainty involved in the rising cost of dollar-funded new investments.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

12

Trend II: Digital constructionDespite many construction companies across Europe have defined their focus on digital construction as a core vision for their future, few of them have structurally implemented digital construction into their business over the past few years. However, when it comes to materializing this vision it is still early days. The economic downturn has meant construction companies scarcely invested in the development and adaptation of new technologies. Now, as markets recover and demand for construction is on the rise, the development and implementation of new technologies in the construction sector is finally growing.

One of the widespread innovations involves the use of drones. In Spain drones are used to supervise projects in less accessible areas.

The use of a technology known as Building Information Modelling (BIM) has particularly increased. BIM is a digital representation of a construction project and allows for the construction process to be simulated in all phases. It is an emerging technological shift within the Architecture, Engineering, Construction and Operations (AECO) industry. In a country like Finland the digital construction market matured quite fast. The 2013 Finnish BIM survey showed over half of the professionals surveyed to be

familiar with BIM or already using it. Over 90% of the respondents stated they will be using BIM by 2018. In Portugal a committee for BIM standardisation has been appointed in order to align BIM integration in the Portuguese sector. In most other European countries, including the UK and the Netherlands, BIM is a major investment area for construction companies. With several key government project owners requiring the use of technologies like BIM, in Norway the adaptation of BIM is expected to increase over 2017.

As yet not all European countries will show equal levels of maturation in terms of digital construction. Poland and Greece are two

countries where implementation of BIM is very limited. The construction companies there prefer to focus on more tangible resources like machinery and people.

The pattern of the digital construction trend seems about the same in most EU construction markets: mainly larger construction companies are investing in digital construction. As continuing growth is projected we expect digital construction, and foremost BIM, to finally mature in the following years. The question will be whether the smaller construction companies will be able to benefit from this trend or whether their inability to invest now means they will lose ground later on.

‘Brexit is considered to create uncertainty across the economy’

Just like Trump’s election, the uncertainty Brexit is considered to create across the economy may cause exchange rate issues. This market volatility will increase risk premiums, affecting the funding costs and the access construction companies have to the capital markets. Any uncertainty Brexit triggers as regards exchange rates and the debt and equity markets can, in turn, affect project funding and the financing of construction companies.

Alternatively, according to some experts Brexit may have a positive effect on any relocation of financial services firms to other European cities. Post Brexit, the cities of Paris, Dublin, Amsterdam and Frankfurt are all tipped as “the new London”, although this will not have repercussions for the construction market any time soon.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

13

European Construction Monitor | 2016-2017: Growing opportunities in local markets

14

3. Going forward

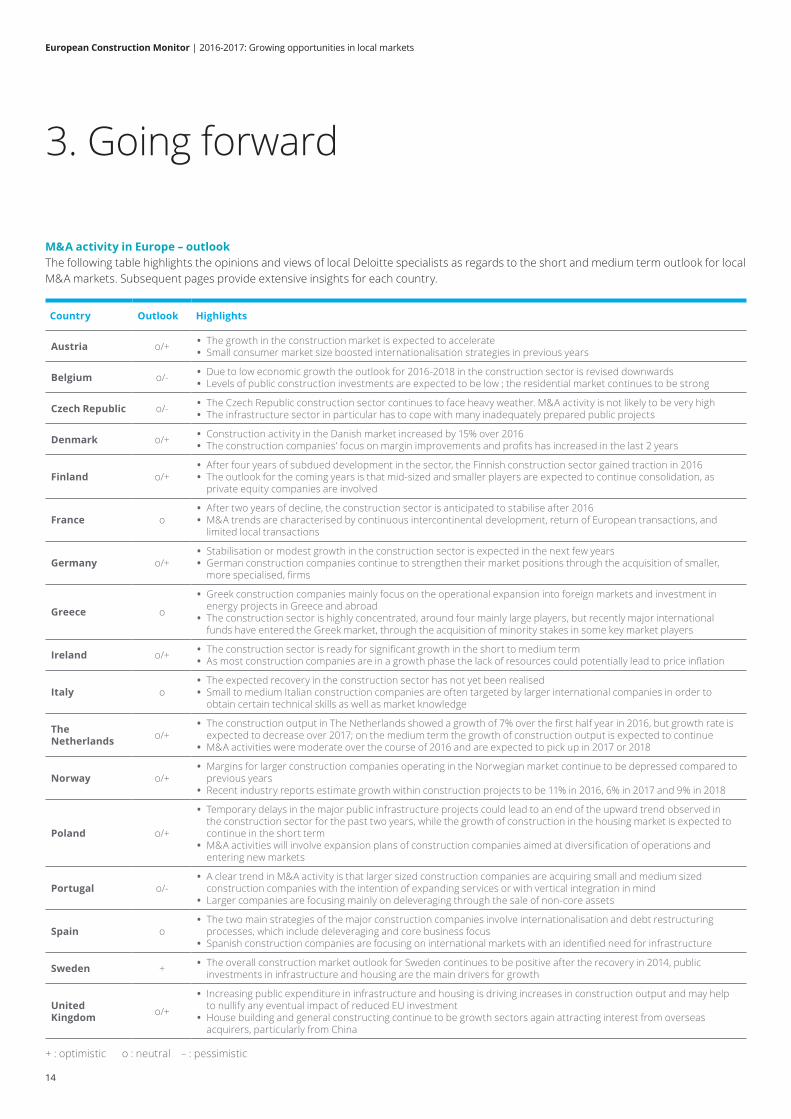

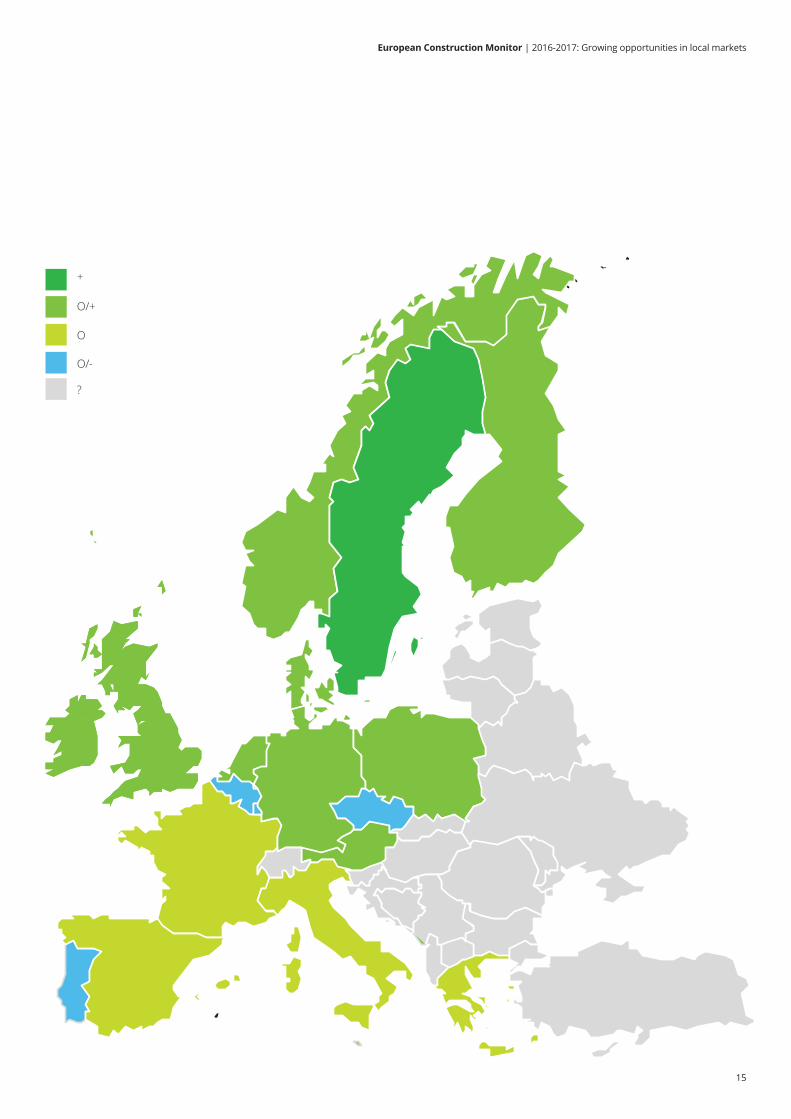

M&A activity in Europe – outlookThe following table highlights the opinions and views of local Deloitte specialists as regards to the short and medium term outlook for local M&A markets. Subsequent pages provide extensive insights for each country.

Country Outlook Highlights

Austria o/+ • The growth in the construction market is expected to accelerate • Small consumer market size boosted internationalisation strategies in previous years

Belgium o/- • Due to low economic growth the outlook for 2016-2018 in the construction sector is revised downwards • Levels of public construction investments are expected to be low ; the residential market continues to be strong

Czech Republic o/- • The Czech Republic construction sector continues to face heavy weather. M&A activity is not likely to be very high • The infrastructure sector in particular has to cope with many inadequately prepared public projects

Denmark o/+ • Construction activity in the Danish market increased by 15% over 2016 • The construction companies’ focus on margin improvements and profits has increased in the last 2 years

Finland o/+ • After four years of subdued development in the sector, the Finnish construction sector gained traction in 2016 • The outlook for the coming years is that mid-sized and smaller players are expected to continue consolidation, as

private equity companies are involved

France o • After two years of decline, the construction sector is anticipated to stabilise after 2016 • M&A trends are characterised by continuous intercontinental development, return of European transactions, and

limited local transactions

Germany o/+ • Stabilisation or modest growth in the construction sector is expected in the next few years • German construction companies continue to strengthen their market positions through the acquisition of smaller,

more specialised, firms

Greece o

• Greek construction companies mainly focus on the operational expansion into foreign markets and investment in energy projects in Greece and abroad

• The construction sector is highly concentrated, around four mainly large players, but recently major international funds have entered the Greek market, through the acquisition of minority stakes in some key market players

Ireland o/+ • The construction sector is ready for significant growth in the short to medium term • As most construction companies are in a growth phase the lack of resources could potentially lead to price inflation

Italy o • The expected recovery in the construction sector has not yet been realised • Small to medium Italian construction companies are often targeted by larger international companies in order to

obtain certain technical skills as well as market knowledge

The Netherlands o/+

• The construction output in The Netherlands showed a growth of 7% over the first half year in 2016, but growth rate is expected to decrease over 2017; on the medium term the growth of construction output is expected to continue

• M&A activities were moderate over the course of 2016 and are expected to pick up in 2017 or 2018

Norway o/+ • Margins for larger construction companies operating in the Norwegian market continue to be depressed compared to

previous years • Recent industry reports estimate growth within construction projects to be 11% in 2016, 6% in 2017 and 9% in 2018

Poland o/+

• Temporary delays in the major public infrastructure projects could lead to an end of the upward trend observed in the construction sector for the past two years, while the growth of construction in the housing market is expected to continue in the short term

• M&A activities will involve expansion plans of construction companies aimed at diversification of operations and entering new markets

Portugal o/- • A clear trend in M&A activity is that larger sized construction companies are acquiring small and medium sized

construction companies with the intention of expanding services or with vertical integration in mind • Larger companies are focusing mainly on deleveraging through the sale of non-core assets

Spain o • The two main strategies of the major construction companies involve internationalisation and debt restructuring

processes, which include deleveraging and core business focus • Spanish construction companies are focusing on international markets with an identified need for infrastructure

Sweden + • The overall construction market outlook for Sweden continues to be positive after the recovery in 2014, public investments in infrastructure and housing are the main drivers for growth

United Kingdom o/+

• Increasing public expenditure in infrastructure and housing is driving increases in construction output and may help to nullify any eventual impact of reduced EU investment

• House building and general constructing continue to be growth sectors again attracting interest from overseas acquirers, particularly from China

+ : optimistic o : neutral – : pessimistic

European Construction Monitor | 2016-2017: Growing opportunities in local markets

15

+

O/+

O/-

O

?

European Construction Monitor | 2016-2017: Growing opportunities in local markets

16

Overview per country(in alphabetical order)

o/+ AustriaAustria’s construction sector performance is expected to exhibit a positive growth rate of 1.6% in 2016 – slightly below the European average. Residential construction showed a sound performance in the first half of 2016, and a steady expansion is expected due to support through public measures in the upcoming years. Nevertheless, economic uncertainty continues to negatively affect non-residential construction. Although this sector will still be driving the industry in the upcoming years, its dynamics will significantly lower.

The relatively small consumer market size of Austria has boosted internationalisation strategies in previous years, both through organic sales and through M&A activities that were adopted by some major Austrian construction firms as an essential part of their business growth processes.

The outlook for the construction industry in Austria for the forecast period of 2016-2020 is better when compared to the industry’s performance during the last 5 year period (2011-2015). The industry’s average annual growth in real terms is expected to accelerate to 1.17% over the forecast period, up from 0.03% during the last 5-year period. This increase is projected to take place due to the anticipated recovery in regional and global economic conditions; an expected rise in government investment; as well as an improvement of both consumer and investor confidence.

o/- BelgiumThe latest economic outlook broadly confirms the low growth scenario for the Belgian economy. Growth is generally expected to remain subdued in FY16, levels of public construction investments are expected to be low, and the number of payment delays and insolvencies continues to be high.

The outlook for the 2016-2018 period was revised slightly downwards. In particular, growth is expected to cap at 1.2% in 2016. The Federal Planning Bureau estimates the 2016 – 2018 sector to grow at around 1.3% per year. M&A activity is expected to retain its highly diverse character, in line with previous years. While some construction groups aim at increasing scale through a number of acquisitions, others want to focus on their core activities. Some large construction groups have been very M&A active (e.g. CFE, Besix), but often experience difficulties in realizing the optimal synergy potential. Furthermore, the number of PE transactions in the construction industry has increased.

Driven by generally high levels of working capital in the sector, construction companies stepped up their efforts in reducing their working capital. Nevertheless, this continues to be a challenge due to industry practices and contractual obligations (mostly with governmental contracts). First of all, the contractual billing and payment conditions or milestones are not aligned with the timing of services to be rendered by the engineering cycle. One example involves the services to be performed by the engineering cycle in the initial phase of a project while, contractually, the fee may only be invoiced in subsequent phases. Secondly, a cumbersome approval process may also cause billing delays. Often this is not sufficiently considered as part of the proposal process.

o/- Czech Republic The Czech Republic construction sector continues to face heavy weather. The sector’s output has decreased over 2016. The infrastructure sector in particular has to cope with many ill-prepared public projects.

The Czech construction sector had no major M&A transactions in in 2016. Although the construction sector is on a downward slope, because the sector is still underinvested the potential for both future state and private investments is very high. M&A activity is not likely to be very high, though, as the biggest companies are already owned by international companies. The smaller ones are too insignificant for the foreign companies and unappealing for the local private equity players. Nevertheless, given that the public investment deficit forces the industry to grow in the near future, this sector might be attractive for strategic investors in the coming years. In addition, the potential prices of the companies will not be excessive.

Expansion plans of construction companies aimed at diversification of operations and entering new markets will involve M&A activities. However, the companies underline that they want to increase their presence on foreign markets primarily through export sales.

o/+ DenmarkThe Danish market has seen its activities rise by 15%. The increase is mainly due to the construction of a large number of large hospitals, private housing and private commercial buildings, spread across the country.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

17

M&A activity in the construction sector itself is very low, with very few, very small acquisitions. The real estate M&A activity, however, is high. A large number of small, medium and large transactions are taking place. The transactions have spread from Copenhagen and Aarhus to smaller Danish cities. This is expected to continue in the coming years.

The construction companies’ focus on margin improvements and profits has increased, especially in the last two years. Increased digitalisation ranks high on the agenda. Larger construction companies invest in new technologies and BIM infrastructure. The smaller and medium-sized companies are lagging behind. The investments are expected to result in efficiency gains and increased margins.

o/+ FinlandAfter four years of subdued development, the Finnish construction sector gained traction in 2016. Especially the new building construction has dragged the overall development during the recent years while renovation construction has grown steadily. The market outlook has improved from the previous years and the construction sector is forecast to grow by some 6 – 7 % in 2016. The construction market growth is expected to slow down to around 1.5% in 2017.

Urbanisation has meant the construction market activity is increasingly focused on Finnish growth cities. New building construction is experiencing solid growth and it is expected to be up by 16% from the low levels of 2015 (measured by cubic meters). The ground work of building construction is supporting the demand of infrastructure construction. Significant proportions of the Finnish asset base were built during the 70s and 80s. They will be in need of renovation in the future. Despite the significant overall repair liability, growth of the renovation construction is expected to slow down in the short-term.

The outlook for the coming years is that mid-sized and smaller players are expected to continue consolidation, as private equity companies are involved. The Finnish markets have few on-going or soon to be kicking off sales processes and some cross-border activity is expected, most of which will be inbound.

The number of construction market defaults has decreased by roughly 40% from peak levels in 2011. Currently, construction market defaults are close to 2006 levels, as the twelve-month moving average for defaulted construction companies was around 40 per month as at 11 October 2016.

o FranceThe construction sector once again decreased, by -1.6% in 2015. Still, at -3.6% the decrease was stronger in 2014. Things are anticipated to to stabilise in 2016, but the trends are different in each subsector. The residential construction will enjoy a small catch-up due to renovation works, stabilisation is expected for the non residential construction sector and the lack public sector investment is expected to result in a small but continuing decline in civil works.

M&A trends are characterized by a continuous intercontinental development of some of the largest players, mainly in America, Asia and the Middle East, whose focuses differ depending on the players and the business. What’s more, the return of European transactions with acquisitions notably in northern Europe has been announced. The key focus of the major players appears to be on energy and concessions. The difficulties faced by small and medium-sized French companies and the larger players clearly focusing on foreign developments, have resulted in a relatively quiet local market. This trend is not expected to change in the near future, although a limited number of consolidation transactions will likely take place among the small and medium-sized players.

The number of defaults in the construction section continues to be high although it slightly improved in comparison with 2015. The small and medium-sized players are significantly affected because public sector demand has fallen. The larger players benefit from their international developments.

Working capital and cash management continues to be a key focus for companies in the construction sector. This translates into increasing focus on contract financing as well as development towards less working capital intensive activities (services).

o/+ GermanyLast year’s indication of Germany’s construction market can be carried forward without major modifications: stabilisation or modest growth is expected in the next few years. Transaction activities continue to focus on acquisitions that precisely extend market power in specific areas and competencies.

The largest 2016 transaction in Germany was Bilfinger’s sale of their remaining Real Estate Business (including building) to private equity investor EQT. While EQT is planning to develop most parts of their investment, they will immediately resell the building components. In January 2017, resale of the building entities to (Swiss) Implenia was announced.

Due to a high level of demand, the residential building sector’s condition continues to be very strong, showing high workload and utilisation rates and leading to a price/earnings increase in the sector. Public spending for infrastructure has been increased significantly and is expected to maintain that higher level for the near future.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

18

A focus on acquisitions that precisely extend market power in specific areas and competencies can be observed. In some cases, takeover of competitors for shakeout reasons may be a motive. In accordance with the big number of smaller players in the German market, smaller companies are in the pipeline continuously. Time and again, major players may be subject to M&A transactions as well.

o GreeceThe Greek economy has suffered from a long term recession and real GDP has declined by more than one quarter. The prospects for short-term economic growth still remain uncertain. Based on the latest data obtained, the 2016 0.5% target primary GDP surplus set by the ESM is expected to be exceeded. On the other hand, the 2017 1.75% primary surplus target of GDP under the third economic adjustment program seems quite challenging.

Due to the economic stagnation in Greece as regards infrastructure works like concessions and PPPs, the Greek construction companies are mainly focusing on the operational expansion into foreign markets and investments in energy projects in Greece and abroad. These energy projects mainly include Renewable Energy Systems (RES) projects.

The largest infrastructure projects are about to be completed, so the construction pipeline is mainly driven by maintenance works, certain infrastructure additions, and finalisation of past projects.

Further M&A activity is expected to be anticipated in cases where the construction works finish and the projects reach their operational phase. The construction sector is highly concentrated around four mainly large players, but recently major international funds have entered the Greek market by acquiring minority stakes in some key market players.

Working capital management and lack of liquidity are still a primary concern, also given the banking system’s difficulties in bridging this gap. Operational restructuring (i.e. intra-group mergers) could be a means of improving financial positions and enhancing liquidity.

o/+ IrelandThe construction industry is continuing to grow. The lack of supply in the residential market led the government to bring in a number of provisions in order to facilitate the process of enhancing supply. Residential prices are projected to increase by 8% in 2017. Another important area of strong demand in the private sector regards the hotels and office accommodation.

In the short to medium term, the construction sector is ready for significant growth. To catch up and meet demand, the supply of residential units should increase. The demographics are favorable, the population is increasing and the underlying economy is performing strongly. This means most sectors, such as education, hospitality, tourism, health, utilities and so on, have their demands. However, the public sector capital expenditure is still relatively low. Since public finances have regained a balanced position, public spending is anticipated to increase in the coming years.

The property sector has experienced significant foreign investment in recent years. This came on the back of a deep recession and deflated property prices.

Credit and working capital continues to be a challenge. Banks are very risk adverse, leading to very low Loan to Value. Other funding entities with more aggressive tactics than the banks, have higher borrowing costs. Considering the already tight margins this could make potential developments unviable. Another issue could be that most construction companies

are in a growth phase and there will be lack of resources. This is quickly becoming an issue and may lead to price inflation.

o ItalyThe GDP is estimated to grow by 0.8% and 0.6% for the years 2016-2017. The improved economic indicators in the wider economy at the end of 2015 as well as an anticipated increase in public investments in infrastructure were expected to enhance the recovery of the Italian construction sector. However, the expected recovery has not yet been realised.

The forecasted 1% growth of construction investments in 2016 has been revised to 0.3%, the growth of construction investments is now expected to be 1.1% in 2017. The Association of Italian Construction Companies (ACNE) is forecasting a further decline in production in the construction sector of around 1.2% for 2017 (in real terms). However, the construction sector shows a few minor signs of improvement, with a reduction in the number of bankruptcies. Still, it continues to be the sector with one of the highest bankruptcy rates in the economy.

The Inter-ministerial Economic Planning Committee (CIPE) has recently approved total investments of nearly 40 billion of which 13 billion has been awarded to various construction projects. The government has stated the need to resume and increase investments in infrastructure. The presence of Italian construction companies in the international market continues to grow. International revenues accounted for 54% of the revenues generated by the major Italian construction companies surveyed. The local investments in Italian construction sector amounted to about EUR 125 billion.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

19

While Italian construction companies are generally smaller than their international competitors, they are recognized for providing leading construction services. These small to medium Italian companies are often targeted by larger international companies, which are often looking to obtain certain technical skills as well as market knowledge. These types of M&A transactions are expected to occur more in the coming years.

o/+ The NetherlandsThe production in the construction sector showed an 8.5% growth in 2015, against 7% in the first half of 2016. Like in 2015, growth is mainly driven by the recovered residential sector. Growth of investments in the commercial and infrastructure markets lag behind due to decreased public expenditure. The first half of 2016 nonetheless showed growing order books in all construction markets. The commercial sector showed the strongest growth of the order books.

Based on the decline of issued building permits in 2015, the growth rate of the construction output in the Netherlands is expected to decrease over 2017. In the medium term, 2018 2021, production in the construction sector is expected to grow. Although construction sector production has increased over 2015 and 2016, the sales volume has lagged behind. Dutch construction companies expect an average sales growth of 5.4% and an average profit growth of 7% over 2017. However, supply chain pressure continues to be a crucial issue for the larger construction companies due to the scarcity of capacity of subcontractors and suppliers.

The M&A activities are in line with recent years and were moderate over the course of 2016. Larger construction companies are repositioning themselves for future growth and profitability. Heijmans for instance was compelled to sell subsidiary Franki to the Austrian Porr in order to strengthen its financial position. VolkerWessels on the other hand publicly announced to examine IPO plans. Most larger construction companies are betting heavily on digital construction while facing scarcity of highly qualified personnel. Overall M&A activity could pick up in 2017 or be postponed to 2018.

The expected effects of Brexit for the Dutch construction market are neutral. Postponement of expansion investments by Dutch companies focused on UK markets maybe an indirect effect of Brexit.

o/+ NorwayMargins for larger construction companies operating in the Norwegian market remain depressed compared to previous years, averaging around 2% in EBIT margin for FY14 and FY15 compared to an EBIT range of 2% to 4% from FY04 to FY13. Companies focusing on consultancy and project management within the construction business are seen to achieve consistently higher margins than those focusing on construction.

According to Statistics Norway, production growth within the construction market continues to be positive, with a growth of approx. 4.8% YoY as of Q1 FY16 compared to 4.3% YoY as of Q1 FY15, while industry orders have outgrown production in FY16. Recent industry reports estimate growth within construction projects to be 11% in 2016, 6% in 2017 and 9% in 2018. The decline in railroad investments in 2017 affects the overall (expected) growth rate of 6%. Investments are projected to outgrow maintenance by 14% versus a 3% growth rate in 2016, a trend that is expected to continue in FY17 and FY18.

According to the National Transportation Plan 2018-2029 under evaluation by the Norwegian Parliament, the investment budget for road, rail and port/harbour infrastructure will be around NOK 59.7 billion per year from 2018 to 2029. The Transportation plan affirms the Norwegian state’s future investment in infrastructure. It enjoys broad bi-partisan parliamentary support, with minor discrepancies on smaller projects. However, the plan includes low-middle-high scenarios on a granular level, opening up the possibility to spend more/less than what the average sum indicates.

Deloitte expects BIM and similar technological tools to expand in use going into 2017, as several key state/government project owners have demanded BIM on new projects as of July 2016, including services delivered by subcontractors. While the state/government project owners’ endeavors to use BIM through a project’s entire lifespan, at the time of writing this report the scope of BIM demands had yet to be determined.

The Norwegian market continues to be fragmented with many small and midsized companies whose market shares are relatively high, although there are some large players as well.

Considering consolidation in the Swedish construction market, Deloitte expected Norway to experience a similar consolidation wave. However, this had yet to materialize as of time of writing. M&A transactions in the Norwegian market in 2015 and 2016 primarily involved midsize companies taken over by larger players. No large transaction occurred that considerably consolidated the market.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

20

o/+ PolandThe conditions in the construction sector differ across segments. The infrastructure segment depends on public funding and government decisions and faces the most problematic situation. The launch of the 2014-2020 EU perspective and revision of the existing national road and railway programs has caused temporary delays in the major infrastructure projects. This slowdown could lead to an end of the upward trend observed in the construction sector for the past two years. On the back of the EU 2014-2020 perspective, companies focused on the infrastructure segment will enter new markets and continue their expansion on foreign markets. Moreover, the housing construction segment has shown a strong growth in demand, which has been rising since 2014. This trend is expected to continue in the short term. In the long term, though, the termination of a government support program in 2018 and the expected heightened restriction on mortgage loan availability may lead to a slowdown in the housing construction segment.

M&A activities will involve expansion plans of construction companies aimed at diversifying operations and entering new markets. In the upcoming years, construction companies will focus on taking advantage of the increased project volume (as a result of an influx of EU funds and the launch of government housing programs) and at the same time they will focus on ensuring growth and value in the long term.

In the first half of 2016, the number of bankruptcies in the construction sector increased by 8%, mainly due to the temporary lack of contracts in the infrastructure segment caused by delays in tender procedures.

o/- PortugalThe Portuguese construction industry is still suffering from the economic downturn. In facing the drop in demand the larger companies have implemented operational strategies like restructuring staff and departments, selling non core assets and entering new markets.

The government maintains the low public spending in large infrastructure projects and no increase in public investments is forecasted. Last year saw an increase in both licensing of new residential homes and an increase in mortgage credit granted. This increase is likely to continue and is expected to slightly increase the internal demand. Even though the construction sector still leads the bankruptcies list, a few signs of recovery indicate the number of construction companies created.

Construction M&A shows a clear trend in which larger-sized construction companies are acquiring small and medium-sized construction companies with the intention to expand services or to implement vertical integration. Due to the difficulties faced by the smaller companies, the larger Portuguese construction companies are engaging in vertical integrations to streamline internal processes. The construction M&A transactions are expected to be driven by the acquisition of distressed construction and engineering companies for the coming years. This, in turn, will include private equity. The acquisition of large infrastructure assets by international funds and large international construction players is expected to be another driver.

The larger companies are mainly focusing on deleverage through the sale of non-core assets. They, too, continue to focus on international markets, especially Africa and Latin America. The economic instability in Angola has reduced demand, pushing the larger construction companies to increase their focus on Latin America and other

international markets. o SpainThe economic downturn led Spanish construction companies to divest their non-core divisions. In order to deleverage or fund their international expansion, these companies implemented a Spanish PPP portfolio rotation strategy.

The lack of government policy has slowed down the arrival of new financial investors and investments in the Spanish PPP market have been postponed. Alternatively, infrastructure funds already present in Spain have increased and consolidated their portfolios. Private equity activity focuses on higher value added assets such as parking or gymnasiums concessions. Here, the automatisation of the Spanish market allows for a build-up process to take place, while operational adjustments are easier to perform.

The two main strategies of the major construction companies in the debt restructuring processes are deleveraging and core business focus, and internationalisation. The Spanish government budget is ring-fenced for existing infrastructure maintenance. Hence, the Spanish construction companies are focusing on international markets, where an infrastructure need has been identified. Their main targets are emerging markets but mature markets such as North America are on their list, too. Infrastructure funds are becoming an active player in new Greenfield projects across the world, because in order to fund these infrastructure needs the public sector will need private sector involvement.

European Construction Monitor | 2016-2017: Growing opportunities in local markets

21

Moreover, current monetary policies have helped to increase infrastructure destined available capital seeking higher returns on their investment initially in the US, UK or France, and, as the number of competitors increase, potential returns decrease. Investors thus turn to pursuing opportunities in countries such as Spain or Italy or new geographies such as Latin America. Spanish M&A transactions will focus on the brownfield secondary market, both from an equity and a debt point of view. As the number of financial investors in Spain is increasing and the potential return is decreasing due to the competition, infrastructure funds are willing to focus their efforts on demand driven or value-added assets, where their expected return could be higher.

+ SwedenThe overall construction market outlook for Sweden continues to be positive after the recovery in 2014. Public investments in infrastructure and housing are the main drivers for growth. Over 2016 the total construction output grew by around 4.5%. Growth is expected to stabilize over 2017 and 2018, mainly due to stabilisation of the total number of permits issued for the construction of residential buildings. As pointed out last year, Sweden is facing a housing shortage – especially in the major cities. The Swedish government has announced plans to provide financial support and build 250,000 houses by 2020. New amortisation requirements are expected to lead to a more balanced housing market.

In line with last year, M&A activity on the Swedish construction market remained steady. The number of transactions recorded in 2016 matched the 2015 activity. M&A activity on the Swedish construction market predominantly involves domestic

transactions. Inbound and outbound cross border transactions are mainly recorded between Nordic countries. Of the four largest Swedish construction companies (NCC AB, Skanska AB, JM AB and Peab AB) only Skanska AB was involved in M&A activity in 2016. Skanska divested Skanska Installation to Assemblin AB.

o/+ United KingdomThe UK government is increasing infrastructure and housing public expenditure. This is driving increases in construction output and may help to nullify any eventual impact of reduced EU investment. The UK construction market as a whole is generally highly buoyant, facing quarter on quarter increases in output. However, the impact of Brexit forms an element of caution.

Infrastructure is possibly the most attractive segment and the government recently announced a major infrastructure investment program. From an M&A perspective, interest in this segment is being driven by China in order to develop a presence/foothold in areas such as nuclear, power generation, road and rail. House building and general constructing continue to be growth sectors again, attracting interest from overseas acquirers – particularly China. 2017 is expected to trigger an active M&A environment.

UK M&A has been in decline over the last few years. Large contractors have been through a period of divestment, focusing on a more efficient use of their balance sheet by divesting on the capital intensive parts/assets of their business. The trend in M&A is driving towards the acquisitions of specialist/niche contracting businesses and businesses with off-site/modular capabilities.

The larger players in the construction sector have been through a period of divestment and strengthening their balance sheets. They have consequently experienced a small performance increase. Hence, the number of defaults in this sector is low. However, the UK market is very fragmented and there have been a number of insolvencies on the smaller end of the market. This typically involved subcontractors, which have been “squeezed” by supply chain pressures. In recent times this can be seen to have reduced.

22

European Construction Monitor | 2016-2017: Growing opportunities in local markets

European Construction Monitor | 2016-2017: Growing opportunities in local markets

23

What to expectM&A activity within the European construction sector has shown a slight increase over the last three years but continues to be relatively stable: 149 recorded transactions in 2016 compared to 144 recorded transactions in 2015. Although we do not expect a sudden increase of M&A activity in the construction sector, the ongoing market recovery may result in a rise of the number of transactions over 2017 or 2018 compared to the last few years.

Overall, the M&A-trend changes in the European construction market have been insignificant. The number of cross-border and intercontinental transactions dropped to 51.0% in 2016, down from 54.9% in 2015, but the international focus of the European construction sector continues to be a dominant strategy of larger companies. A slight decrease in diversification is noticed compared to last year’s monitor. The percentage of diversification transactions decreased to 27.0%, down from 31.3%.

Although the decline in cross-border and diversification transactions was limited over 2016, the trend break indicates the first trend of this year’s monitor: the European construction companies renewed focus on local markets and core business. This trend can be attributed to better local market conditions and supply chain pressure. The past two years showed significant recovery of market conditions on the European continent. While construction volumes grew, the sharply increased prices charged by subcontractors continued to put pressure on the operating margins. This so-called supply chain pressure results from the increased demand for construction associated with the challenge to attract sufficient labour and subcontractors with

the right capabilities and capacity. Even though margins in the local construction sector have increased over 2016, supply chain pressure continues to be an issue in most European construction markets.

Over the last year our local real estate experts increasingly observed M&A activity in local construction supply chains. Not only are larger construction companies targeting mid-sized and small-sized subcontractors, an increase in the acquisition of suppliers and supporting services in core business by European construction companies can be identified. This focus on supply chain integration appears to be in line with the ongoing recovery of local construction markets and construction companies focusing on increasing their revenues and profit margins in their core business on local markets. As growth is projected for most EU construction markets, we expect an increased focus on supply chain integration in the coming year.

The second trend identified in this year’s monitor is the coming of age of digital construction. Recently, larger European Construction firms all defined their future vision around digital construction. The economic downturn led construction companies to make few investments in the development and adaptation of new technologies. Now, as markets recover and demand for construction increases, the adaptation of new technologies in the construction sector is finally growing. Especially the larger construction companies are applying – or at least slowly adapting to – BIM. On the back of the projected continued growth we expect digital construction, and foremost BIM, to mature in the following years.

In 2017 and the years beyond the European constructions sector is said to potentially be affected by Brexit and the Trump presidency. Our local real estate experts mainly point out the potential uncertainty in (global) economy and financial markets will indirectly affect the construction sector. The potential negative effects of both Brexit and the Trump presidency are expected to be limited. In contrast, European construction companies could potentially benefit from Trump’s presidency as substantial investments in infrastructure are expected. Their experience in public private partnerships and large scale projects means European construction companies could be able to benefit from these investments.

4. Conclusion

European Construction Monitor | 2016-2017: Growing opportunities in local marketsEuropean Construction Monitor | 2016-2017: Growing opportunities on local markets

24

European Construction Monitor | 2016-2017: Growing opportunities in local markets

25

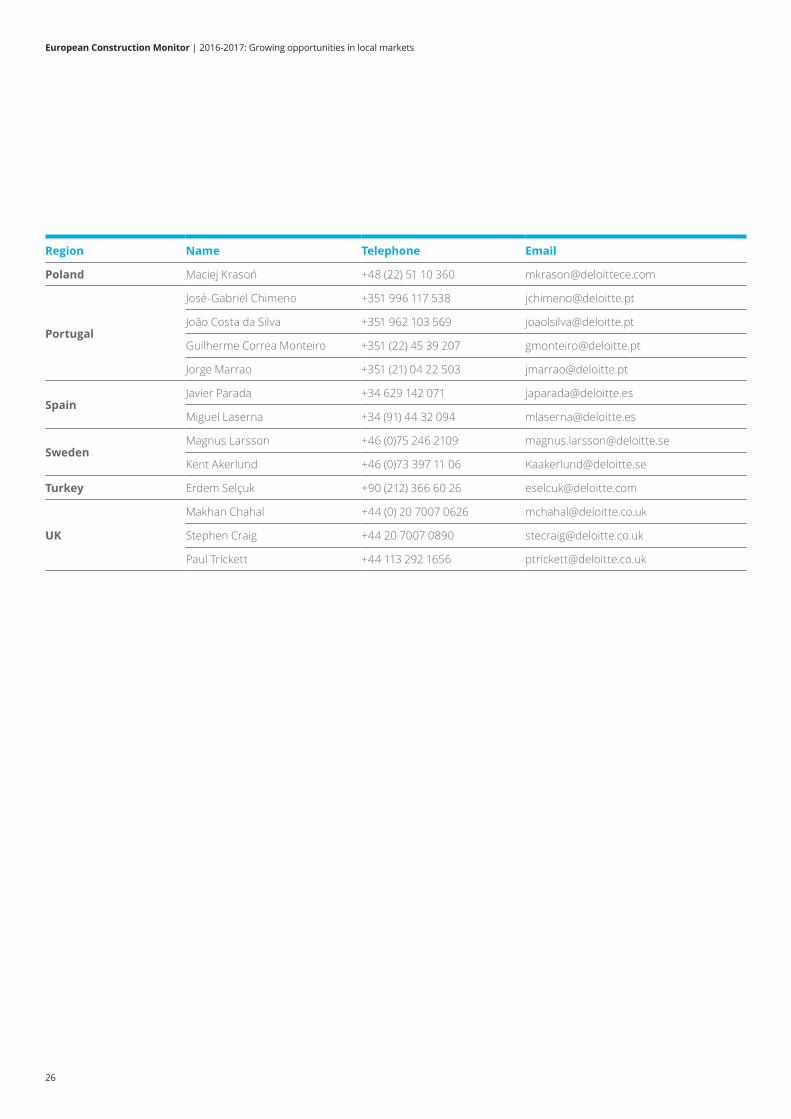

5. European real estate, construction and infrastructure group contacts

Region Name Telephone Email

EMEA Javier Parada +34 629 142 071 [email protected]

AustriaAlexander Hohendanner +43 (1) 537 00 2700 [email protected]

Nikolaus Schaffer +43 (1) 537 00 2400 [email protected]

BelgiumFrédéric Sohet +32 (4) 77 37 52 81 [email protected]

Jean-Paul Loozen +32 (2) 639 49 40 [email protected]

Central EuropeDiana Radl Rogerova +420 (246) 042 572 [email protected]

Miroslav Linhart +420 (246) 042 598 [email protected]

DenmarkThomas Frommelt +45 24 23 83 04 [email protected]

Lars Kronow +45 22 20 27 86 [email protected]

Finland Jan Söderholm +358 (0) 40 560 6018 [email protected]

France

Mansour Belhiba +33 1 55 61 54 61 [email protected]

Matthew Jiggins +33 1 40 88 86 38 [email protected]

Pascal Souchon +33 1 55 61 69 93 [email protected]

GermanyFranz Klinger +49 (89) 29036 8362 [email protected]

Michael Mueller +49 (89) 29036 8428 [email protected]

GreeceAlexis Damalas +30 (210) 678 1100 [email protected]

Dimitris Nektarios +30 (210) 678 1100 [email protected]

Ireland

Michael Flynn +353 (1) 417 2515 [email protected]

Kevin Sheehan +353 (1) 417 2218 [email protected]

Padraic Whelan +353 (1) 417 2848 [email protected]

ItalyElena Vistarini +39 (02) 833 25122 [email protected]

Kevin O’Connor +39 (02) 833 25072 [email protected]

Luxembourg Benjamin Lam +(352) 451 452 429 [email protected]

The Netherlands

Paul Meulenberg +31 (0) 88 288 1982 [email protected]

Jurriën Veldhuizen +31 (0) 88 288 1636 [email protected]

Nico Dijkstra +31 (0) 88 288 6813 [email protected]

NorwayAre Skjøy +47 907 26 899 [email protected]

Carsten V. Haukås +47 915 55 035 [email protected]

European Construction Monitor | 2016-2017: Growing opportunities in local markets

26

Region Name Telephone Email

Poland Maciej Krasoń +48 (22) 51 10 360 [email protected]

Portugal

José-Gabriel Chimeno +351 996 117 538 [email protected]

João Costa da Silva +351 962 103 569 [email protected]

Guilherme Correa Monteiro +351 (22) 45 39 207 [email protected]

Jorge Marrao +351 (21) 04 22 503 [email protected]

SpainJavier Parada +34 629 142 071 [email protected]

Miguel Laserna +34 (91) 44 32 094 [email protected]

SwedenMagnus Larsson +46 (0)75 246 2109 [email protected]

Kent Akerlund +46 (0)73 397 11 06 [email protected]

Turkey Erdem Selçuk +90 (212) 366 60 26 [email protected]

UK

Makhan Chahal +44 (0) 20 7007 0626 [email protected]

Stephen Craig +44 20 7007 0890 [email protected]

Paul Trickett +44 113 292 1656 [email protected]

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.nl/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2017 Deloitte The Netherlands