MSc Financial Markets Financial Markets and Regulation MSc Finance Financial Markets and Crises

1

EUROPEAN COMMISSION Directorate General Financial Stability, Financial Services and Capital Markets Union FINANCIAL MARKETS Securities Markets

Brussels, 18 February 2015

CONSULTATION DOCUMENT REVIEW OF THE PROSPECTUS DIRECTIVE

Disclaimer

This document is a working document of the Commission services for consultation and does not prejudge the final form of any future decision to be taken by the Commission.

You are invited to comment on the views reflected in this paper. These views are only an indication of the approach the Commission services may take and are not a final policy position nor do they constitute a formal proposal by the European Commission.

The responses to this consultation will provide important guidance to the Commission when preparing, if considered appropriate, a formal Commission proposal.

In replying to these questions, please indicate the expected impact described in each section of this paper on your activities or the activities of firms in your jurisdiction, including estimates of administrative or compliance costs. Please also state reasons for your answers and provide, to the extent possible, evidence supporting your views.

If need be, files with additional information can be uploaded using the button at the end of the consultation page. In order to assist in the evaluation of your contribution, we would appreciate if you could maintain the structure of this questionnaire and indicate clearly the question you are responding to in any additional material you might want to provide.

You are invited to reply to this online questionnaire by 13 May 2015 at the latest. Responses will be published on the following website unless requested otherwise: http://ec.europa.eu/finance/consultations/2015/prospectus-directive/index_en.htm.

2

Commission Services Consultation In the following document, "the Directive" refers to Directive 2003/71/EC of 4 November 2003 on the prospectus to be published when securities are offered to the public or admitted to trading and amending Directive 2001/34/EC, as subsequently amended by Directive 2008/11/EC of 11 March 2008, by Directive 2010/73/EU of 24 November 2010, by Directive 2010/78/EU of 24 November 2010, by Directive 2013/50/EU of 22 October 2013 and by Directive 2014/51/EU of 16 April 2014 (Omnibus II). "Issuers" refers to issuers, offerors or persons asking for the admission to trading, as the case may be. All references to "the proportionate disclosure regime" relate to the minimum disclosure requirements set out in Articles 7(2)(e) and (g) of the Directive and Chapter IIIa of Commission Regulation (EC) No 809/2004 of 29 April 2004 implementing Directive 2003/71/EC of the European Parliament and of the Council as regards information contained in prospectuses as well as the format, incorporation by reference and publication of such prospectuses and dissemination of advertisements, as subsequently amended (the "Implementing Regulation") and the corresponding Annexes. In the context of this consultation "prospectus framework" means the legal framework created by the Directive and the Implementing Regulation. I. Introduction The Prospectus Directive 2003/71/EC has applied since July 2005. The Directive, together with its Implementing Regulation n°809/2004, lays down the rules governing the prospectus that must be made available to the public when a company makes an offer or an admission to trading of transferable securities on a regulated market in the EU. The prospectus contains information about the offer, the issuer and the securities, and has to be approved by the competent authority of a Member State before the beginning of the offer or the admission to trading of the securities. Two key objectives underpin the Directive: • Investor and consumer protection. A prospectus is a standardised document which, in

an easily analysable and comprehensible form, should contain all information which is necessary to enable investors to make an informed assessment of the issuer and the securities offered or admitted to trading on a regulated market.

• Market efficiency. A prospectus aims at facilitating the widest possible access to capital

markets by companies across the EU. The Directive sought to achieve this through requiring a common form and content of the prospectus and introducing an EU wide passport: a prospectus approved by the competent authority of one Member State should be valid for the entire Union without additional scrutiny by the authorities of other Member States.

Following a review, the Directive was amended in November 2010 in the following areas: (i) investor protection was strengthened by improving the quality and effectiveness of disclosures and by facilitating comparison between products through the summary; (ii) efficiency was increased by reducing administrative burdens for issuers through various proportionate disclosure regimes (including for small and medium-sized enterprises (SMEs), companies with reduced market capitalisation and rights issues), a recalibration of the thresholds below which no prospectus is required and some further harmonisation of technical details in certain areas (withdrawal rights). The review of the Directive in the context of the Commission's action plan for a Capital Markets Union The prospectus is the gateway into capital markets for firms seeking funding, and most firms seeking to issue debt or equity must produce one. It is crucial that it does not act as an

3

unnecessary barrier to the capital markets. It should be as straightforward as possible for companies (including SMEs) to raise capital throughout the EU. The Commission is required to assess the application of the Directive by 1 January 2016 but given the importance of making progress towards a Capital Markets Union, has decided to bring the review forward. The review will seek to ensure that a prospectus is required only when it is truly needed, that the approval process is as smooth and efficient as possible, the information that must be included in prospectuses is useful and not burdensome to produce and that barriers to seeking funding across borders are reduced.

The review of the Prospectus Directive is featured in the Commission Work Programme for 2015, as part of the Regulatory Fitness and Performance Programme (REFIT)1. Shortcomings of the Directive and objectives of the review There are several potential shortcomings of the prospectus framework today. The process of drawing up a prospectus and getting it approved by the national competent authority is often perceived as expensive, complex and time-consuming, especially for SMEs and companies with reduced market capitalisation. Member States have applied differently the flexibility in the Directive to exempt offers of securities with a total value below EUR 5 000 000: the requirement to produce a prospectus kicks in at different levels across the EU. There are indications that prospectus approval procedures are in practice handled differently between Member States. Prospectuses have become overly long documents, which has brought into question the effectiveness of the Directive from an investor protection perspective. The objective of the review of the Directive is to reform and reshape the current prospectus regime in order to make it easier for companies to raise capital throughout the EU and to lower the associated costs, while maintaining effective levels of consumer and investor protection. The Directive also needs to be updated to reflect market and regulatory developments including the development of multilateral trading facilities (MTFs), creation of SME growth markets and organised trading facilities (OTFs), and the introduction of key information documents for packaged retail and insurance-based investment products (PRIIPs) under Regulation (EU) No 1286/2014. This public consultation seeks to identify the needs of market users with regard to prospectuses concerning scope, form, content, comparability, the approval process, liability and sanctions. In addition, interested parties should provide feedback about the aspects which unduly hinder access to capital markets for issuers, and which, if amended, could reduce administrative burden without undermining investor protection. Questions: (1) Is the principle, whereby a prospectus is required whenever securities are admitted to trading on a regulated market or offered to the public, still valid? In principle, should a prospectus be necessary for:

- admission to trading on a regulated market - an offer of securities to the public?

1 See http://ec.europa.eu/atwork/pdf/cwp_2015_refit_actions_en.pdf.

4

Should a different treatment should be granted to the two purposes (i.e. different types of prospectus for an admission to trading and an offer to the public). If yes, please give details. (2) In order to better understand the costs implied by the prospectus regime for issuers: a) Please estimate the cost of producing the following prospectus

- equity prospectus - non-equity prospectus - base prospectus - initial public offer (IPO) prospectus

b) What is the share, in per cent, of the following in the total costs of a prospectus:

- Issuer's internal costs: [enter figure]% - Audit costs: [enter figure]% - Legal fees: [enter figure]% - Competent authorities' fees: [enter figure]% - Other costs (please specify which): [enter figure]%

What fraction of the costs indicated above would be incurred by an issuer anyway, when offering securities to the public or having them admitted to trading on a regulated market, even if there were no prospectus requirements, under both EU and national law? (3) Bearing in mind that the prospectus, once approved by the home competent authority, enables an issuer to raise financing across all EU capital markets simultaneously, are the additional costs of preparing a prospectus in conformity with EU rules and getting it approved by the competent authority are outweighed by the benefit of the passport attached to it? II. ISSUES FOR DISCUSSION The current prospectus framework provides issuers with several tools initially intended to make the procedure of drawing up prospectuses more flexible and to lower the associated costs (proportionate disclosure regime, incorporation by reference, base prospectus, tripartite prospectus). However, the prospectus framework is seen today by some as burdensome and not effective at facilitating access to capital markets, in particular for SMEs and companies with lower market capitalisation. These fundamental aspects of the Directive under review are grouped under the following headings: - A. When a prospectus is needed: the scope of the requirement to prepare a

prospectus;

- B. What information a prospectus should contain: the contents of a prospectus and the responsibility attaching to it;

- C. How prospectuses are approved: the role of national competent authorities in the approval process of prospectuses, the equivalence of third-country prospectus regimes.

When a prospectus is needed

5

This consultation requests respondents' views on a possible recalibration of the obligation for issuers to draw up a prospectus, based on the existing exemption thresholds, as well as the favourable treatment granted to debt issuers using high denominations per unit. Views are also welcome on whether a prospectus should be required for secondary issuances and for the admission of securities to trading on MTFs. What information prospectuses should contain The consultation seeks feedback on ways to expand the existing tools that were intended to introduce some flexibility in the drawing up of a prospectus and enhance their effectiveness to the benefit of issuers, striking an appropriate balance between effective investor protection and the alleviation of administrative burden. The consultation also suggests ways to introduce more flexibility in the process of raising capital by clarifying the relationship in the prospectus approval process with the marketing phase. To avoid the tendency towards lengthier prospectuses and return to the original purpose of a prospectus (providing investors with easily analysable and comprehensible information necessary for an informed assessment of an issuer and its securities), views are sought on the usefulness of the prospectus summary, as well as on possible limitations which could be introduced on prospectuses. As the length of a prospectus is to a certain extent linked to the liability incurred by those who prepare it, the question of the liability regime is raised, as well as the sanctions regime. Finally this paper invites comments on certain issues already addressed in the amending Directive 2010/73/EU – e.g. the prospectus exemption for employee share schemes, the determination of the home Member State for issues of non-equity securities, the clarification of legal concepts - with a view to ensuring that the amendments introduced have achieved their objectives. A. When a prospectus is needed A.1. Adjusting the current exemption thresholds The scope of the Directive is currently determined by a number of quantitative thresholds which exempt certain types of public offers from the prospectus requirement. Given recent developments in financial markets, such as investment-based crowdfunding, these thresholds as well as the non-harmonised area of offers below EUR 5 000 000, need to be reassessed. The thresholds concern small offers, offers of debt securities by small credit institutions, offers targeting a very limited number of retail investors and offers where the denomination per unit of the securities or the minimum "entry ticket" are so high that they would not normally be accessible to retail investors. These thresholds are:

• EUR 5 000 000: any offer of securities with a total consideration in the EU below this amount falls outside the scope of the Directive (Article 1(2)(h)). Member States are free to have national rules in place that impose disclosure requirements (wholly or partly inspired from, if not analogous to, a prospectus under the Directive) to such offers.

• EUR 75 000 000: any offer or admission to trading of non-equity securities, issued in

a continuous or repeated manner by credit institutions, with a total consideration in the EU below this amount falls outside the scope of the Directive (Article 1(2)(j)). This provision essentially relates to small credit institutions issuing (non-hybrid) bonds, debentures or notes.

6

• 150 persons: any offer of securities addressed to a number of natural or legal persons per Member State below this number, other than qualified investors is exempted from the requirement to produce a prospectus (Article 3(2)(b)). Offers which are addressed solely to qualified investors (i.e. "professional investors" under MIFID) are also exempted (Article 3(2)(a)).

• EUR 100 000: any offer of securities whose denomination per unit is equal or above

this value, or where investors are subject to a minimum individual investment equal or above this value, is exempted from the requirement to produce a prospectus (Article 3(2)(c) & (d)).

These thresholds were raised significantly by Directive 2010/73/EC (from respectively EUR 2 500 000, EUR 50 000 000, 100 persons and EUR 50 000). Stakeholders' views would be helpful to assess whether the thresholds are still appropriate today or if any further quantitative adjustment would be desirable and if more harmonisation is required, bearing in mind that Member States are currently free to implement national regimes for offers with a total consideration below EUR 5 000 000. This is particularly relevant in the context of investment-based crowdfunding, the development of which might be discouraged in those Member States where the prospectus requirement applies below the EUR 5 000 000 threshold. Furthermore, the Directive applies only to ‘securities’ as defined in Article 2(1)(a).2 Thus, securities which do not fall into that definition are subject to either no or national, non-harmonised prospectus requirements. Questions (4) The exemption thresholds in Articles 1(2)(h) and (j), 3(2)(b), (c) and (d), respectively, were initially designed to strike an appropriate balance between investor protection and alleviating the administrative burden on small issuers and small offers. Should these thresholds be adjusted again so that a larger number of offers can be carried out without a prospectus? If yes, to which levels? Please provide reasoning for your answer.

a) the EUR 5 000 000 threshold of Article 1(2)(h): - Yes, from EUR 5 000 000 to EUR [enter monetary figure] - No - Don't know/no opinion Textbox: [ justification ]

b) the EUR 75 000 000 threshold of Article 1(2)(j):

- Yes, from EUR 75 000 000 to EUR [enter monetary figure] - No - Don't know/no opinion Textbox: [ justification ]

c) the 150 persons threshold of Article 3(2)(b)

- Yes, from 150 persons to [enter figure] persons - No;

2 Transferable securities as defined by MIFID with the exception of money market instruments having a maturity of less than 12 months. For these instruments national legislation may be applicable.

7

- Don't know/no opinion Textbox: [ justification ]

d) the EUR 100 000 threshold of Article 3(2)(c) & (d)

- Yes, from EUR 100 000 to EUR [enter monetary figure] - No - Don't know/no opinion Textbox: [ justification ]

(5) Would more harmonisation be beneficial in areas currently left to Member States discretion, such as the flexibility given to Member States to require a prospectus for offers of securities with a total consideration below EUR 5 000 000?

Yes No Other areas: Don't know/no opinion

Textbox: [ justification ] (6) Do you see a need for including a wider range of securities in the scope of the Directive than transferable securities as defined in Article 2(1)(a)? Please state your reasons.

Yes No Don't know/no opinion

Textbox: [ justification ] (7) Can you identify any other area where the scope of the Directive should be revised and if so how? Could other types of offers and admissions to trading be carried out without a prospectus without reducing consumer protection?

Yes [text box] No Other areas: Don't know/no opinion

Textbox: [ justification ] A.2. Creating an exemption for "secondary issuances" under certain conditions A company which already has a class of securities admitted to trading on a regulated market is known to the market through the prospectus it prepared and got approved on that occasion. Until now, a proportionate disclosure regime exists only for ‘rights issues’, i.e. any issue of statutory pre-emption rights which allow for the subscription of new shares and is addressed only to existing shareholders, but there is no alleviation of prospectus requirements for secondary issuances in general. It may be argued that there is less of a need to require a prospectus for secondary issuances, because, once the class of securities is admitted to trading on a regulated market, the disclosure regimes under Regulation (EU) 596/2014 (Market Abuse Regulation, "MAR") and Directive 2004/109/EC (Transparency Directive, "TD") provide the necessary information for purchasers. On that basis, a range of options could be envisaged to alleviate the prospectus burden for subsequent admissions to trading or offers of the same class of fungible securities. These could include: - raising the exemption for secondary issues of Article 4(2)(a) from 10% to at least 20%;

8

- granting a prospectus exemption to rights issues (i.e. cases where the issuer has not disapplied the statutory pre-emptive rights);

- granting a prospectus exemption to any secondary admission to trading or public offers of securities that are fungible with securities already listed, for which a prospectus has been approved within a certain time frame (e.g. 3 years).

In the case of MTFs, where the admission of securities to trading is not currently subject to a prospectus, a similar kind of exemption could be devised to target offers to the public of a class of securities which has already been offered to the public over a certain period of time to be defined (e.g. 3 years). Since the Transparency Directive does not apply to MTFs, this exemption may need to be conditional on the existence of appropriate market rules regarding periodic financial reporting by issuers. Questions (8) Do you agree that while an initial public offer of securities requires a full-blown prospectus, the obligation to draw up a prospectus could be mitigated or lifted for any subsequent secondary issuances of the same securities, providing relevant information updates are made available by the issuer?

Yes No Don't know/no opinion

Textbox: [ justification ] (9) How should Article 4(2)(a) be amended in order to achieve this objective ? Please state your reasons.

The 10% threshold should be raised to [enter figure]% The exemption should apply to all secondary issuances of fungible securities, regardless of their proportion with respect to those already issued No amendment Don't know/no opinion

Textbox: [ justification ] (10) If the exemption for secondary issuances were to be made conditional to a full-blown prospectus having been approved within a certain period of time, which timeframe would be appropriate?

[ ] years There should be no timeframe (i.e. the exemption should still apply if a prospectus was approved ten years ago) Don't know/no opinion

Textbox: [ justification ] A.3. Extending the prospectus to admission to trading on an MTF The requirement for establishing a prospectus applies to admission of securities to trading on a regulated market and to offers of securities to the public. However, admissions to trading on MTFs are not covered by the Directive and therefore no level playing field exists between the different MTFs within the EU. The current principle of requiring a prospectus only for public offers and admissions to regulated markets was first set out in Directive 2003/71/EC at a time when the concept of MTF did not exist yet, as Directive 2004/39/EC (MIFID) was only finalised one year later. Today there are more than 150 registered MTF operating in the EU. Some of these MTF which focus on small and medium-sized companies may in the future adopt the label 'SME

9

growth markets" recently created under MIFID II (Directive 2014/65/EU). Companies whose securities are traded on such MTFs are currently required to produce a prospectus where they offer securities to the public, unless an exemption applies. On the contrary, no prospectus is required for the mere admission to trading of securities on these MTF, unlike for admissions to trading on regulated markets. In practice, companies seeking admission of their securities to trading on a MTF will usually produce an admission document or offering circular, pursuant to the specific market rules of the MTF at the national level. Thus, no level playing field exists across the EU and issuers may face different levels of disclosure requirements depending on the MTF where the admission to trading of their securities is sought. Disclosure rules applying to MTFs are more flexible than rules applying to regulated markets, however some benefit may exist in harmonising the disclosure requirements for admissions to trading of securities on an MTF (including SME growth markets) across the EU. This could be achieved by extending the scope of the Directive to such markets, while granting the corresponding prospectuses the benefit of using the proportionate disclosure regime (if necessary, with revised, less onerous minimum requirements). Such a harmonisation would be coherent with recent developments of MAR and MIFID II which brought MTFs into scope alongside regulated markets. Questions: (11) Do you think that a prospectus should be required when securities are admitted to trading on an MTF? Please state your reasons.

Yes, on all MTFs Yes, but only on those MTFs registered as SME growth markets No Don't know/no opinion

Textbox: [ justification ] (12) Were the scope of the Directive extended to the admission of securities to trading on MTFs, do you think that the proportionate disclosure regime (either amended or unamended) should apply? Please state your reasons.

Yes, the amended regime should apply to all MTFs Yes, the unamended regime should apply to all MTFs Yes, the amended regime should apply but not to those MTFs registered as SME growth markets Yes, the unamended regime should apply but not to those MTFs registered as SME growth markets Yes, the amended regime should apply but only to those MTFs registered as SME growth markets Yes, the unamended regime should apply but only to those MTFs registered as SME growth markets No Don't know/no opinion

Textbox: [ justification ] A.4. Exemption of prospectus for certain types of closed-ended alternative investment funds (AIFs) At present, multiple layers of disclosure requirements for certain types of closed-ended alternative investment funds may create overlaps in the information to be disclosed to investors.

10

The current Directive provides that units of open-ended collective investment schemes are out of its scope, and that offers of securities addressed solely to qualified investors (i.e. professional investors as defined under MIFID) are exempted from the obligation to draw up a prospectus. It follows that units or shares of closed-ended collective investment schemes, to the extent that they are considered as transferable securities, may be within the scope and required to have a prospectus approved if they are offered to more than 150 persons per Member State other than qualified investors. This may be the case in particular for European venture capital funds (EuVECA) or European social entrepreneurship funds (EuSEF) to the extent that they are of the closed-ended type and sold to the so-called "high-net-worth individuals" (as defined under Article 6(1) of both corresponding Regulations)3. In the case of the future European long term investment funds (ELTIF), the Regulation establishing them, for which a political agreement was found in November 2014, imposes a prospectus to be drawn up for all ELTIFs, including where those are structured as investment funds of the closed-ended type. There might be therefore instances in which these alternative investment funds (AIFs) would have to comply cumulatively with the requirements to (i) publish a prospectus (the minimum content of which is set out in Annex I and XV of the Implementing Regulation), (ii) draw up a key information document (KID) pursuant to the PRIIPS Regulation and (iii) disclose to investors the information listed in the relevant sectorial legislation (Art. 13 of the EuVECA Regulation, Art. 14 of the EuSEF Regulation, Art. 23 of AIFMD). Despite the fact that these funds are sometimes allowed not to disclose a second time the information that is already featured in the prospectus, these multiple layers of disclosure requirements may create overlaps between the various information to be disclosed to investors under each of them e.g. investment strategy and objectives, leverage, valuation procedures. Given that EuVECAs, EuSEFs, and ELTIFs have specifically been created in order to channel capital into long-term assets and projects and small and medium-sized enterprises, views are welcome as to the extent to which the disclosure regime is appropriate and contributes to the achievement of that goal, or, for those investment vehicles, provides investors with little additional benefit. Questions: (13) Should future European long term investment funds (ELTIF), as well as certain European social entrepreneurship funds (EuSEF)4 and European venture capital funds (EuVECA)5of the closed-ended type and marketed to non-professional investors, be exempted from the obligation to prepare a prospectus under the Directive, while remaining subject to the bespoke disclosure requirements under their sectorial legislation and to the PRIIPS key information document? Please state your reasoning, if necessary by drawing comparisons between the different sets of disclosure requirements which cumulate for these funds.

Yes, such an exemption would not affect investor/consumer protection in a significant way No, such an exemption would affect investor/consumer protection

3 Investors that commit to investing a minimum of 100,000 € and state in writing that they are aware of the risks associated with the envisaged commitment or investment. 4 Established under Regulation (EU) No 346/2013 of the European Parliament and of the Council of 17 April 2013 on European social entrepreneurship funds (OJ L 115, 25.4.2013, p. 18) 5 Established under Regulation (EU) No 345/2013 of the European Parliament and of the Council of 17 April 2013 on European venture capital funds (OJ L 115, 25.4.2013, p. 1)

11

Don't know/no opinion Textbox: [ justification ] A.5. Extending the exemption for employee share schemes A prospectus exemption is granted for offers of securities by a firm to its employees (employee shares scheme, "ESS"), providing a document is made available containing information on the number and nature of securities and the reasons for and details of the offer (Article 4(1)(e)). However, a private company established outside the EU wishing to offer its securities to its employees in the EU as part of an ESS is still required to prepare a prospectus. The reasoning behind this is that an ESS represents a very particular kind of offer in so far as employees of an issuer do not have the same information needs as normal investors, and therefore a full prospectus brings little added value in terms of investor protection. While Directive 2003/71/EC only granted this exemption to issuer listed on an EU regulated market, Directive 2010/73/EU extended it to ESS launched by any EU company, listed or not, and to non-EU issuers provided their securities are admitted to trading on an EU regulated market or on a third-country market, in which case an equivalence decision by the Commission regarding the third-country market is required. The level playing field was only partially achieved: a private company established outside the EU wishing to offer its securities to its employees in the EU as part of an ESS is still required to prepare a prospectus. This might deprive EU employees of non-EU, non-listed companies from the opportunity to invest in their employer's securities, as their employer might refrain from launching an ESS due to the administrative burden of preparing a full prospectus. Accordingly, some EU employees might be disadvantaged relative to others. Question (14) Is there a need to extend the scope of the exemption provided to employee shares schemes in Article 4(1)(e) to non-EU, private companies ? Please explain and provide supporting evidence.

Yes No Don't know/no opinion

Textbox: [ justification ] A.6. Balancing the favourable treatment of issuers of debt securities with a high denomination per unit, with liquidity on the debt markets Under both the Prospectus and Transparency Directives, a system of exemption thresholds currently create incentives for issuers to issue debt securities with a high denomination per unit, namely above EUR 100 000. Such a high threshold might create an incentive to only issue in larger denominations, which as a consequence may inhibit liquidity on the secondary market for corporate bonds and limit the issuance of debt securities in smaller denominations: • under Directive 2003/71/EC, there is a prospectus exemption in Art. 3(2) for issuers of

securities (debt or equity) with a denomination per unit of at least EUR 100 000: this exemption only applies to public offers while there is no such prospectus exemption in

12

case of admission of securities to trading on a regulated market. The Implementing Regulation 809/2004 contains schedules for issuers of debt securities with a denomination per unit of at least EUR 100 000 (Annexes IX & XIII in particular) which are to be used for admission prospectuses. Such schedules are lighter than those for debt securities with a denomination per unit below EUR 100 000 (Annexes IV & V). In addition, issuers drawing up an admission prospectus for non-equity securities having a denomination of at least EUR 100 000 are not required to provide a summary and benefit from a more flexible language regime. Therefore, the incentive for debt issuers to denominate their debt securities above EUR 100 000 per unit is (i) either less information to disclose if the securities are admitted to trading, (ii) or no prospectus at all if no admission is sought.

• likewise, under Directive 2004/109/EC, a person issuing exclusively debt securities

admitted to trading on a regulated market, the denomination per unit of which is at least EUR 100 000 is exempted from the obligation to publish annual and half-yearly financial reports (Art. 8(1)(b)).

In both Directives, the threshold in terms of denomination per unit was raised from EUR 50 000 to EUR 100 000 by the amending Directive 2010/73/EU, as there was evidence that the EUR 50 000 threshold no longer reflected the distinction between retail and professional investors in terms of investment capacity, since it appeared that even retail investors were making investments of more than EUR 50 000 in a single transaction. Views are sought as to whether such a high threshold creates an incentive to only issue in larger denominations, and whether this may inhibit liquidity on the secondary market for corporate bonds, in which case a recalibration of the thresholds or of the incentives attached thereto might be desirable. Question (15) Do you consider that the system of exemptions granted to issuers of debt securities above a denomination per unit of EUR 100 000 under the Prospectus and Transparency Directives may be detrimental to liquidity in corporate bond markets? If so, what targeted changes could be made to address this without reducing investor protection? Yes No Don't know/no opinion Textbox: [ justification ] If you have answered yes, do you think that:

(a) the EUR100 000 threshold should be lowered? - Yes, to EUR [enter monetary figure] - No - Don't know/no opinion - Textbox: [ justification ] (b) some or all of the favourable treatments granted to the above issuers should be

removed? - Yes, please indicate to what extent : [ ] - No - Don't know/no opinion - Textbox: [ justification ]

13

(c) the EUR 100 000 threshold should be removed altogether and the current exemptions should be granted to all debt issuers, regardless of the denomination per unit of their debt securities?

- Yes - No - Don't know/no opinion - Textbox: [ justification ]

B. The information a prospectus should contain B.1. Proportionate disclosure regime Following the previous review of the Directive, a proportionate disclosure regime was introduced for certain types of issues and issuers, however, this lighter prospectus regime does not seem to have delivered its intended effect and is apparently not widely used in practice by issuers in most Member States. The proportionate disclosure regime is currently available under Article 7(2)(e) and (g) for rights issues (i.e. offers of shares to existing shareholders who can either subscribe those shares or sell the right to subscribe for the shares), offers by SMEs and companies with reduced market capitalisation (as defined in Article 2(1)(f) and (t)), and offers of non-equity securities referred to in Article 1(2)(j) of Directive 2003/71/EC issued by credit institutions6 to improve the efficiency of pre-emptive issues of equity securities and adequately to take account of the size of issuers, without prejudice to investor protection. The regime consists in a set of simplified schedules featured in the Implementing Regulation n°809/2014, for each of the above, with minimum disclosure requirements that are lighter than those applying to regular offers. It seems however that the proportionate disclosure regime has not delivered its intended effect and is not widely used in practice by issuers in most Member States, mainly because it is still perceived as too burdensome. Questions (16) In your view, has the proportionate disclosure regime (Article 7(2)(e) and (g)) met its original purpose to improve efficiency and to take account of the size of issuers? If not, why?

Yes No Don't know/no opinion

Textbox: [ justification ] (17) Is the proportionate disclosure regime used in practice, and if not what are the reasons? Please specify your answers according to the type of disclosure regime.

a) Proportionate regime for rights issues - Yes - No - Don't know/no opinion

6 Such offers are normally exempted from the prospectus requirement under Article 1(2)(j). The proportionate disclosure regime may however be used by credit institutions who voluntarily choose to opt for the prospectus regime of the Directive.

14

- Textbox: [ justification ] b) Proportionate regime for small and medium-sized enterprises and companies

with reduced market capitalisation - Yes - No - Don't know/no opinion - Textbox: [ justification ]

c) Proportionate regime for issues by credit institutions referred to in Article 1(2)(j) of Directive 2003/71/EC - Yes - No - Don't know/no opinion - Textbox: [ justification ]

(18) Should the proportionate disclosure regime be modified to improve its efficiency, and how? Please specify your answers according to the type of disclosure regime.

a) Proportionate regime for rights issues Textbox: [ ] b) Proportionate regime for small and medium-sized enterprises and companies

with reduced market capitalisation Textbox: [ ] c) Proportionate regime for issues by credit institutions referred to in Article

1(2)(j) of Directive 2003/71/EC Textbox: [ ]

(19) If the proportionate disclosure regime were to be extended, to whom should it be extended?

To types of issuers or issues not yet covered? Please specify: [text box] To admissions of securities to trading on an MTF, supposing those are brought into the scope of the Directive? Please specify: [text box] Other. Please specify: [text box] Don't know/no opinion

Textbox: [ justification ] B.2. Creating a bespoke regime for companies admitted to trading on SME growth markets Directive 2014/65/EU on markets in financial instruments ("MIFID II") created the status of "SME growth markets", It needs to be assessed whether a tailor-made prospectus regime would be beneficial for the development of these markets. "SME growth markets" is an optional label which an MTF may obtain by registering with its competent authority, provided inter alia that at least 50% of the issuers whose securities are traded on such an MTF are "SMEs", as defined by MIFID II as companies with a market capitalisation below EUR 200 000 000. In order to further foster and promote the use of SME growth markets by making them attractive for investors and issuers, and providing a lessening of administrative burdens and further incentives for SMEs and companies with reduced market capitalisation to access capital markets through SME growth markets, a bespoke prospectus regime for SMEs and companies with reduced market capitalisation admitted to trading on these new markets could be considered.

15

At the very least, this could consist in making the proportionate disclosure regime described in Annex XXV to XXVIII of the implementing Prospectus Regulation available to all SMEs, as defined under MIFID II, thereby raising from EUR 100 000 000 to EUR 200 000 000 the capitalisation limit included in the definition of "company with reduced market capitalisation" of the Directive. More radically, the establishment of a simplified set of schedules in the implementing Prospectus Regulation, i.e. less detailed than the current Annexes XXV to XXVIII, could be envisaged and these schedules could become the default content for any prospectus to be prepared by an SME or a company with reduced market capitalisation admitted to trading on an SME growth market when offering securities to the public. Questions (20) Should the definition of "company with reduced market capitalisation" (Article 2(1)(t)) be aligned with the definition of SME under Article 4(1)(13) of Directive 2014/65/EU by raising the capitalisation limit to EUR 200 000 000?

Yes No Don't know/no opinion

Textbox: [ justification ] (21) Would you support the creation of a simplified prospectus for SMEs and companies with reduced market capitalisation admitted to trading on an SME growth market, in order to facilitate their access to capital market financing?

Yes No, the higher risk profile of SMEs and companies with reduced market capitalisation justifies disclosure standards that are as high as for issuers listed on regulated markets. Don't know/no opinion

Textbox: [ justification ] (22) Please describe the minimum elements needed of the simplified prospectus for SMEs and companies with reduced market capitalisation admitted to trading on an SME growth market. Textbox: [ justification ] B.3. Making the "incorporation by reference" mechanism more flexible and assessing the need for supplements in case of parallel disclosure of inside information Both the Transparency Directive and the Market Abuse Directive 2003/6/EC oblige issuers to disclose certain types of information to the public. Thus, it needs to be assessed whether duplication in the prospectus and in the supplement respectively could be avoided. The "incorporation by reference" mechanism allows for information that has already been published and approved or filed with the relevant authority in accordance with the Prospectus or Transparency Directives to be used for the purpose of a prospectus by including only a reference therein. Incorporation by reference facilitates the procedure of drawing up a prospectus and lowers the costs for issuers without lowering investor protection. This mechanism could potentially be extended to other types of regulated information, as ESMA's current work on the draft regulatory technical standards (RTS) under Directive 2014/51/EU (Omnibus II) on incorporation by reference has shown.

16

Questions: (23) Should the provision of Article 11 (incorporation by reference) be recalibrated in order to achieve more flexibility? If yes, please indicate how this could be achieved (in particular, indicate which documents should be allowed to be incorporated by reference)?

Yes No Don't know/no opinion

Textbox: [ justification ] (24) (a) Should documents which were already published/filed under the Transparency Directive no longer need to be subject to incorporation by reference in the prospectus (i.e. neither a substantial repetition of substance nor a reference to the document would need to be included in the prospectus as it would be assumed that potential investors have anyhow access and thus knowledge of the content of these documents)? Please provide reasons.

Yes No Don't know/No opinion

Textbox [justification] (b) Do you see any other possibilities to better streamline the disclosure requirements of the Prospectus Directive and the Transparency Directive?

Yes No Don't know/No opinion

Textbox [justification] (25) Article 6(1) Market Abuse Directive obliges issuers of financial instruments to inform the public as soon as possible of inside information which directly concerns the said issuers; the inside information has to be made public by the issuer in a manner which enables fast access and complete, correct and timely assessment of the information by the public. Could this obligation substitute the requirement in the Prospectus Directive to publish a supplement according to Article 17 without jeopardising investor protection in order to streamline the disclosure requirements between Market Abuse Directive and Prospectus Directive?

Yes No Don't know/No opinion

Textbox [justification] (26) Do you see any other possibility to better streamline the disclosure requirements of the Market Abuse Directive and the Prospectus Directive?

Yes No Don't know/No opinion

Textbox [justification] B.4. Reassessing the objectives of the prospectus summary and addressing possible overlaps with the key information document required under the PRIIPs Regulation

17

The prospectus summary is one of the three components of a prospectus (alongside the registration document and the securities note). Its purpose is to provide the key information relating to the securities and their issuer in a concise manner and in non-technical language, in order to help investors in their investment decision and to enable them to compare similar securities. Nonetheless, the summary regime, as reformed by Directive 2010/73/EU, may not have fully achieved its objectives and needs to be assessed in the light of the PRIIPs regulation. The summary regime may not have fully achieved its objectives when it was reformed by Directive 2010/73/EU. The summary of the prospectus was supposed to be short, simple, clear and easy for investors to understand. As a key source of information for retail investors in particular, it was supposed to focus on key information that investors need for their investment decisions and, thanks to its standardised format, to allow comparisons between similar products. Views are welcome as to whether room for improvement exists, in particular with regard to the comparability of summaries and their interaction with the final terms of a base prospectus. Questioning the purpose of the prospectus summary seems all the more relevant as the Regulation on key information documents for packaged retail and insurance-based investment products ("PRIIPS Regulation") will apply from 31 December 2016. Under this Regulation, the manufacturer of any packaged investment product7 marketed to retail investors will be under the obligation to draw up and publish a three-page key information document (KID) for that product and the persons advising or selling the product will have to provide such KID to retail investors before they buy it. As certain packaged investment products (e.g. convertible bonds, structured notes, shares of closed-ended collective investment schemes, asset-backed securities) may be securities falling in the scope of the Directive, their offer to the public or admission to trading on a regulated market may require the simultaneous production of a KID under PRIIPS and a prospectus under the Directive (unless an exemption applies). Indeed, Article 3(1) of the PRIIPS Regulation clarifies that both disclosure requirements apply in a cumulative way. When this happens, there might be a partial overlap between some of the information listed in Article 8(3) of the PRIIPS Regulation that are required to be featured in the KID and some of the information required to be featured in the summary of the prospectus, as listed in Annex XXII of the Prospectus Regulation. The revision of the Prospectus Directive gives an opportunity to deal with such overlaps between the KID and the prospectus summary in order to prevent unnecessary duplication of information. More fundamentally, the PRIIPS KID is designed to provide retail investors with standardised information about a broad range of investment opportunities in order to enable them to understand and compare the key features and risks of such products. Its aim is therefore largely overlapping with that of the prospectus summary. As the KID cannot exceed three sides of A4-sized paper, whereas the prospectus summary is limited to 7% of the length of the prospectus or 15 pages, whichever is the longer, the KID will most likely be the shorter of the two documents, and the probability that investors may read it is higher. Questions

7 Defined as "an investment (…) where, regardless of the legal form of the investment, the amount repayable to the retail investor is subject to fluctuations because of exposure to reference values or to the performance of one or more assets which are not directly purchased by the retail investor".

18

(27) Is there a need to reassess the rules regarding the summary of the prospectus? (Please provide suggestions in each of the fields you find relevant)

a) Yes, regarding the concept of key information and its usefulness for retail investors

b) Yes, regarding the comparability of the summaries of similar securities c) Yes, regarding the interaction with final terms in base prospectuses d) No. e) Don't know/no opinion

Textbox: [ justification ] (28) For those securities falling under the scope of both the packaged retail and insurance-based investment products (PRIIPS) Regulation8, how should the overlap of information required to be disclosed in the key investor document (KID) and in the prospectus summary, be addressed?

a) By providing that information already featured in the KID need not be duplicated in the prospectus summary. Please indicate which redundant information would be concerned : [textbox]

b) By eliminating the prospectus summary for those securities. c) By aligning the format and content of the prospectus summary with those of

the KID required under the PRIIPS Regulation, in order to minimise costs and promote comparability of products

d) Other: [textbox] e) Don't know/no opinion

Textbox: [ justification ] B.5. Imposing a length limit to prospectuses A trend towards overly long prospectuses has been observed, especially since the adoption of Directive 2010/73/EU. Views are welcome as to whether prospectuses of excessive length still suit the information purpose: to convey key information on the issuer and the securities on offer in order to aid investors in their investment decision. Yet, while there is currently a length limit to the prospectus summary, there is none for the prospectus as a whole. Imposing a length limit to the entire prospectus could be considered, but may prove ineffective if the surplus information is then channelled into supplements. An alternative approach could consist in setting specific limits (not necessarily in terms of number of pages) to certain sections of the prospectus. For instance, the disclosure of risk factors, which is sometimes viewed as responsible for the size inflation of prospectuses, could be made subject to limitations by setting a maximum limit to the number of risk factors that may be presented and therefore requiring issuers to mention only the key risks most relevant to them. Questions (29) Would you support introducing a maximum length to the prospectus? If so, how should such a limit be defined?

Yes, it should be defined by a maximum number of pages and the maximum should be [ figure] pages Yes, it should be defined using other criteria, for instance: [textbox] No

8 Regulation (EU) No 1286/2014 of the European Parliament and of the Council of 26 November 2014 on key information documents for packaged retail and insurance-based investment products (PRIIPs) (OJL 352, 9.12.2014, p. 1)

19

Don't know/no opinion Textbox: [ justification ] (30) Alternatively, are there specific sections of the prospectus which could be made subject to rules limiting excessive lengths? How should such limitations be spelled out?

Textbox: [ ] B.6. Liability and sanctions The Directive aligns liability and sanctions only to a limited degree, as evidenced in ESMA's report on "Comparison of liability regimes in Member States in relation to the Prospectus Directive" (ESMA/2013/619). Thus, there might be a need to further harmonise liability and sanctions to create a level playing field within the EU. Article 6 governs the responsibility/civil liability attaching to the prospectus which attaches at least to the issuer or its administrative, management or supervisory bodies, the offeror, the person asking for the admission to trading on a regulated market or the guarantor, as the case may be. A specific liability regime exists for summaries: namely no civil liability attaches to any person solely on the basis of the summary, including any translation thereof, unless it is misleading, inaccurate or inconsistent, when read together with the other parts of the prospectus, or it does not provide, when read together with the other parts of the prospectus, key information in order to aid investors when considering whether to invest in such securities. Fundamental provisions regarding sanctions are laid down in Articles 25 and 26. Without prejudice to the right of Member States to impose criminal sanctions and without prejudice to their civil liability regime, Member States are required to ensure, in conformity with their national law, that the appropriate administrative measures can be taken or administrative sanctions be imposed against the persons responsible, where there is a breach of the national rules implementing the Directive. Member States shall ensure that these measures are effective, proportionate and dissuasive. Furthermore, Member States shall provide that the competent authority may disclose to the public every measure or sanction that has been imposed for breaches of the national provisions transposing this Directive, unless the disclosure would seriously jeopardise the financial markets or cause disproportionate damage to the parties involved. The right to appeal against decisions taken under the Directive is also provided for. There may be a case for upgrading the prospectus sanctioning regime to the one recently introduced in the amended Transparency Directive and MIFID II, by defining more precisely the types of sanctions which Member States and their competent authorities should have the power to impose as a minimum, the circumstances which they should take into account when applying those sanctions, as well as measures concerning the publication of sanctions and the mechanisms to enable reporting of potential infringements of the Directive. Questions: (31) Do you believe the liability and sanctions regimes the Directive provides for are adequate? If not, how could they be improved? Yes No No opinion • the overall civil liability regime of Article 6 • the specific civil liability regime for

prospectus summaries of Article 5(2)(d)

20

and Article 6(2) • the sanctions regime of Article 25 Textbox: [ justification ] (32) Have you identified problems relating to multi-jurisdiction (cross-border) liability with regards to the Directive? If yes, please give details.

Yes No Don't know/no opinion

Textbox: [ justification ] C. How prospectuses are approved C.1. Streamlining further the approval process of prospectuses by national competent authorities (NCAs) Currently, scrutiny and approval procedures are handled differently across Member States. Thus, there might be room for improving the approval process to make it more transparent and more flexible for the issuers seeking to react quickly to market windows and to market their securities. According to Article 2(1)(q) of the Directive, “approval” is defined as "[…] the positive act at the outcome of the scrutiny of the completeness of the prospectus by the home Member State’s competent authority including the consistency of the information given and its comprehensibility." Provisions regarding the approval are contained in Article 13, in particular the timeframe allocated to NCAs to carry out their review of a prospectus, from the moment a complete draft prospectus is submitted by the issuer (10 days for regular submissions, 20 days for IPO submissions). Scrutiny and approval procedures are handled differently across Member States due to different national procedural administrative law, supervisory practices and liability regimes. More consistent approaches to procedural provisions may be needed in order to ensure a level playing field, in particular, but not limited to, the methods of the scrutiny carried out by the NCAs prior to approval. Furthermore, views are sought on ways to make the scrutiny and approval process more transparent to the public and more flexible for the issuers seeking to react quickly to market windows. For example, this could be achieved by making public the first draft prospectus filed with the NCA for review and by explicitly allowing the issuer to carry out certain marketing activities in relation to the offer or the admission to trading, going beyond advertising (see Article 15), in the period between the first submission of a draft prospectus and the approval of its final version. Such a provision may bring additional flexibility to issuers in so far as it would allow them to gauge the appetite of potential investors on the basis of a draft prospectus. It would not however endanger investor protection as no legally-binding purchase or subscription would take place until the prospectus has received formal approval by the competent authority. Lastly, the decision to admit securities to trading on a regulated market is currently distinct from the approval of the prospectus required for such an admission. Since in practice the admission decision is often the responsibility of either the firm operating the exchange or an ad hoc listing authority, it follows that the admission decision and the prospectus approval might eventually be handled by two different entities, depending on the Member State. This is true in particular in Member States where Directive 2001/34/EC on the admission of

21

securities to official stock exchange listing and on information to be published on those securities (the "Listing Directive") is applied to regulated markets, in which case the admission decision is the responsibility of the competent authority appointed by Member States under the Listing Directive and follows a process set out therein. In any case, the benefits of having both decisions handled by the same authority should be assessed in order to simplify the process of first admission to trading on a regulated market. Questions: (33) Are you aware of material differences in the way national competent authorities assess the completeness, consistency and comprehensibility of the draft prospectuses that are submitted to them for approval? Please provide examples/evidence.

Yes No Don't know/no opinion

Textbox: [ justification ] (34) Do you see a need for further streamlining of the scrutiny and approval procedures of prospectuses by NCAs? If yes, please specify in which regard.

Yes No Don't know/no opinion

Textbox: [ justification ] (35) Should the scrutiny and approval procedure be made more transparent to the public? If yes, please indicate how this should be achieved.

Yes No Don't know/no opinion

Textbox: [ justification ] (36) Would it be conceivable to allow marketing activities by the issuer in the period between the first submission of a draft prospectus and the approval of its final version, under the premise that no legally binding purchase or subscription would take place until the prospectus is approved? If yes, please provide details on how this could be achieved.

Yes No Don't know/no opinion

Textbox: [ justification ] (37) What should be the involvement of NCAs in relation to prospectuses? Should NCAs:

a) review all prospectuses ex ante (i.e. before the offer or the admission to trading takes place)

b) review only a sample of prospectuses ex ante (risk-based approach) c) review all prospectuses ex post (i.e. after the offer or the admission to trading

has commenced) d) review only a sample of prospectuses ex post (risk-based approach) e) Other f) Don't know/no opinion

Please describe the possible consequences of your favoured approach, in particular in terms of market efficiency and invest protection.

22

Textbox: [ justification ] (38) Should the decision to admit securities to trading on a regulated market (including, where applicable, to the official listing as currently provided under the Listing Directive), be more closely aligned with the approval of the prospectus and the right to passport? Please explain your reasoning, and the benefits (if any) this could bring to issuers.

Yes No Don't know/no opinion

Textbox: [ justification ] (39) (a) Is the EU passporting mechanism of prospectuses functioning in an efficient way? What improvements could be made?

Yes No Don't know/no opinion

Textbox: [ justification ] (b) Could the notification procedure set out in Article 18, between NCAs of home and host Member States be simplified (e.g. limited to the issuer merely stipulating in which Member States the offer should be valid, without any involvement from NCAs), without compromising investor protection?

Yes No Don't know/no opinion

Textbox: [ justification ] C.2. Extending the base prospectus facility The approval procedure for base prospectuses is more flexible than the standard regime and issuers who are eligible to use it find that this flexibility addresses their need for swift and timely access to capital markets, but it is at present limited to certain types of non-equity issues. Whereas the base prospectus itself is approved by the NCA, its final terms are subject to a distinct, more flexible treatment with regard to their publication and the role of the NCA. Indeed, because they only contain a limited amount of new information, and their corresponding base prospectus has already been approved and published, final terms are just filed with the NCA, not approved by it, and they just need to be made available to the public where possible before the beginning of the public offer. The option to draw up a base prospectus is currently only available for non-equity securities issued under an offering programme (in which case the base prospectus remains valid for a period of up to 12 months) or issued in a continuous or repeated way by credit institutions (in which case it remains valid until no more of the securities concerned are issued). Furthermore, it should be expressly clarified in the Directive whether a base prospectus can be drawn up as a tripartite prospectus or not. Views are sought as to how to make the EU base prospectus facility accessible to more issuers and more types of issuances, and on how to bring additional flexibility to it.

23

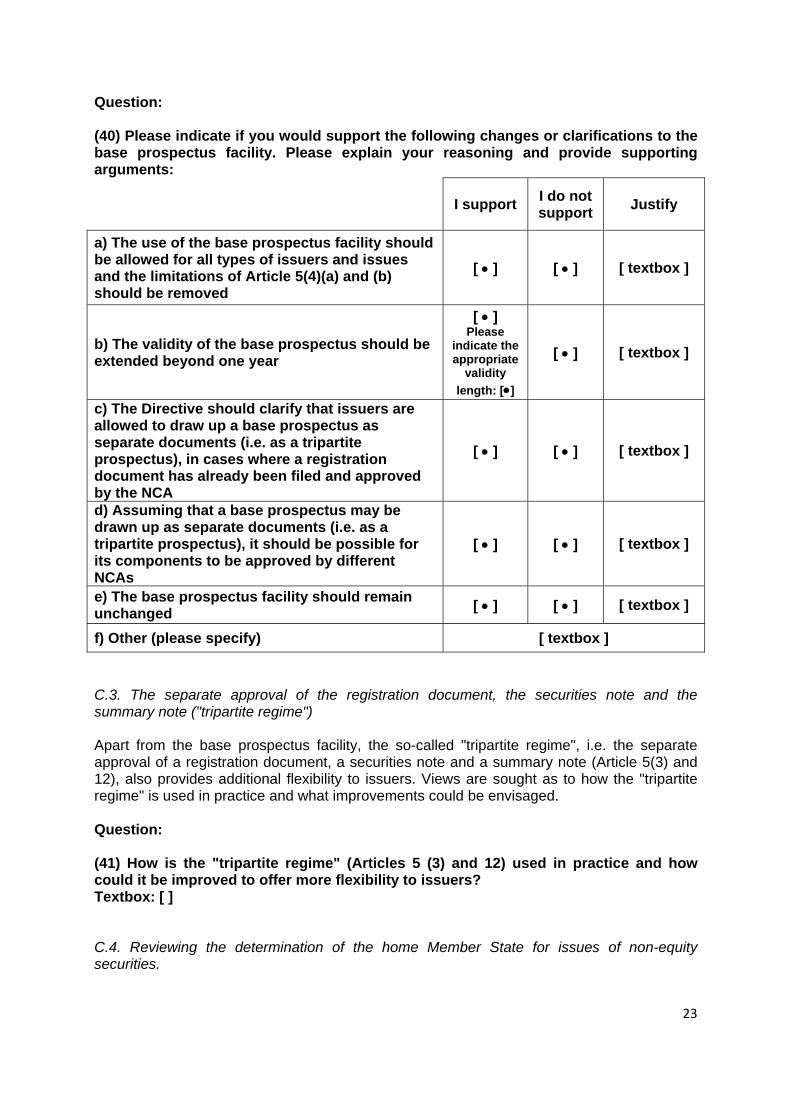

Question: (40) Please indicate if you would support the following changes or clarifications to the base prospectus facility. Please explain your reasoning and provide supporting arguments:

I support I do not support Justify

a) The use of the base prospectus facility should be allowed for all types of issuers and issues and the limitations of Article 5(4)(a) and (b) should be removed

[ • ] [ • ] [ textbox ]

b) The validity of the base prospectus should be extended beyond one year

[ • ] Please

indicate the appropriate

validity length: [•]

[ • ] [ textbox ]

c) The Directive should clarify that issuers are allowed to draw up a base prospectus as separate documents (i.e. as a tripartite prospectus), in cases where a registration document has already been filed and approved by the NCA

[ • ] [ • ] [ textbox ]

d) Assuming that a base prospectus may be drawn up as separate documents (i.e. as a tripartite prospectus), it should be possible for its components to be approved by different NCAs

[ • ] [ • ] [ textbox ]

e) The base prospectus facility should remain unchanged [ • ] [ • ] [ textbox ]

f) Other (please specify) [ textbox ] C.3. The separate approval of the registration document, the securities note and the summary note ("tripartite regime") Apart from the base prospectus facility, the so-called "tripartite regime", i.e. the separate approval of a registration document, a securities note and a summary note (Article 5(3) and 12), also provides additional flexibility to issuers. Views are sought as to how the "tripartite regime" is used in practice and what improvements could be envisaged. Question: (41) How is the "tripartite regime" (Articles 5 (3) and 12) used in practice and how could it be improved to offer more flexibility to issuers? Textbox: [ ] C.4. Reviewing the determination of the home Member State for issues of non-equity securities.

24

Issuers of certain types of non-equity securities can choose which Member State should act as the home Member State (and thus approve the prospectus). This right to choose might have led to unnecessary complexity and supervisory divergence. Article 2(1)(m)(ii) of Directive 2003/71/EC allows an issuer to choose its home Member State for issues of non-equity securities with a denomination per unit above 1,000 € as well as for issues of certain non-equity securities giving the right to acquire transferable securities or to receive a cash amount, as a consequence of a conversion or exercise of right. In such cases, the home Member State may be chosen between (i) the Member State where the issuer has its registered office, (ii) the Member State where the debt is going to be admitted to trading on a regulated market, or (iii) the Member State where the debt is offered to the public. No such choice exists for non-equity securities whose denomination per unit is below 1,000 €, in which case the home Member State is the one where the issuer has its registered office. It has been argued that the dual regime for the determination of the home Member State for non-equity securities, built around the threshold of 1,000 € for the denomination per unit, creates unnecessary complexity for issuers of non-equity securities as it may result in there being different home Member States for an issuer's various products. Question: (42) Should the dual regime for the determination of the home Member State for non-equity securities featured in Article 2(1)(m)(ii) be amended? If so, how?

a) No, status quo should be maintained. b) Yes, issuers should be allowed to choose their home Member State even for

non-equity securities with a denomination per unit below EUR 1 000. c) Yes, the freedom to choose the home Member State for non-equity securities

with a denomination per unit above EUR 1 000 (and for certain non-equity hybrid securities) should be revoked.

Textbox: [ justification ] C.5. Moving to an all-electronic system for the filing and publication of prospectuses Prospectuses are made available to the public either in printed or electronic form, but no comprehensive all-electronic system exists today. Thus, it should be assessed whether creating a single database that would operate as a unique entry point for both investors and persons producing and filing prospectuses across the EU Member States would be beneficial. The Directive provides that the prospectus, once approved by the relevant NCA, shall be made available to the public by the issuer and such publication is possible either in printed form (Article 14(2)(a) and (b)) or in electronic form (Article 14(2)(c) to (e)). It is questionable whether keeping the printed form among the options for making a prospectus available to the public still makes sense today, given the advances in technology and the progress in internet access over the past years. If most investors can be presumed to have access to the Internet, the rules may be simplified by providing that issuers and offerors need only post their prospectus to a website in order to fulfil their publication requirements. Of course, the obligation for the issuer to provide a paper copy free of charge upon request by investors (Article 14(7)), would still be retained in order not to create discrimination between investors. Regarding the filing of prospectuses and their accessibility by investors on a cross-border basis, it is worth referring to the developments introduced by the revised Transparency Directive in 2013. Directive 2013/50/EU created a web portal, operated by ESMA, to serve as a European electronic access point to regulated information of issuers listed on regulated

25

markets. It will start to operate in 2018 and will be interconnected with the officially appointed mechanisms for the central storage of regulated information of each Member State. Based on that example, it should be assessed whether creating a single, centralised, EU database that would operate as a unique entry point for both investors and persons producing and filing prospectuses across the 28 Member States, could bring benefits in facilitating effective cross-border access to information and streamlining the process of prospectus filing by issuers, while maintaining a high standard of investor protection. Questions: (43) Should the options to publish a prospectus in a printed form and by insertion in a newspaper be suppressed (deletion of Article 14(2)(a) and (b), while retaining Article 14(7), i.e. a paper version could still be obtained upon request and free of charge)?

Yes No Don't know/no opinion

Textbox: [ justification ] (44) Should a single, integrated EU filing system for all prospectuses produced in the EU be created? Please give your views on the main benefits (added value for issuers and investors) and drawbacks (costs)?

Yes No Don't know/no opinion

Textbox: [ justification ] (45) What should be the essential features of such a filing system to ensure its success? Textbox: [ ] C.6. Equivalence of third-country prospectus regimes The current Directive lacks a single equivalence regime for prospectuses drawn up in accordance with the legislation of third countries, which might hinder cross-border investment flows. Assessments are currently made by each national authority for each third-country prospectus on a case-by-case basis, under the provision of Article 20. So far, the Commission has not used its empowerment to adopt delegated acts establishing general EU-wide equivalence criteria for third-country prospectuses. In 2011, ESMA published a Statement concerning a framework for third-country equity prospectuses (ESMA/2011/36, revised under ESMA/2013/317) that essentially would allow a third country prospectus to have a "wrap" added to it so that the resulting document meets the requirements of the Directive. However, this framework has only been applied to one third country so far and, in any event, it has no binding force on NCAs when approving a third country prospectus. An equivalence regime could be developed and applied for all third countries. A general equivalence decision could be taken for each third country by the Commission, subject to the assessment that the requirements of the third country prospectus regime are equivalent to those of the Directive in that they achieve the same outcome in terms of investor protection. Questions:

26

(46) Would you support the creation of an equivalence regime in the Union for third country prospectus regimes? Please describe on which essential principles it should be based.

Yes No Don't know/no opinion

Textbox: [ justification ]

(47) Assuming the prospectus regime of a third country is declared equivalent to the EU regime, how should a prospectus prepared by a third country issuer in accordance with its legislation be handled by the competent authority of the Home Member State defined in Article 2(1)(m)(iii)?

a) Such a prospectus should not need approval and the involvement of the Home Member State should be limited to the processing of notifications to host Member States under Article 18

b) Such a prospectus should be approved by the Home Member State under Article 13

c) Don't know/no opinion Textbox: [ justification ]

----- Final questions: (48) Is there a need for the following terms to be (better) defined, and if so, how:

a) "offer of securities to the public" Yes No Don't know/no opinion Textbox: [ justification ]

b) "primary market" and "secondary market"? Yes No Don't know/no opinion Textbox: [ justification ]

(49) Are there other areas or concepts in the Directive that would benefit from further clarification?

No, legal certainty is ensured Yes, the following should be clarified: [ ] Don't know/no opinion

Textbox: [ justification ] (50) Can you identify any modification to the Directive, apart from those addressed above, which could add flexibility to the prospectus framework and facilitate the raising of equity or debt by companies on capital markets, whilst maintaining effective investor protection? Please explain your reasoning and provide supporting arguments.

Yes No Don't know/no opinion

Textbox: [ justification ]

27

(51) Can you identify any incoherence in the current Directive's provisions which may cause the prospectus framework to insufficiently protect investors? Please explain your reasoning and provide supporting arguments.

Yes No Don't know/no opinion

Textbox: [ justification ]

* * *