European Commission Directorate General Economic and Financial Affairs Using BCS data for tracking...

20

European Commission Directorate General Economic and Financial Affairs Using BCS data for tracking q-o-q GDP growth Andreas Reuter Business and consumer surveys and short-term forecast (ECFIN A4.2)

-

Upload

ruth-harrell -

Category

Documents

-

view

219 -

download

0

Transcript of European Commission Directorate General Economic and Financial Affairs Using BCS data for tracking...

European CommissionDirectorate General Economic and Financial Affairs

Using BCS data for tracking q-o-q GDP growth

Andreas ReuterBusiness and consumer surveys and

short-term forecast (ECFIN A4.2)

2

Outline

2. Relative weaknesses of the Economic Sentiment Indicator (ESI)

4. Improving the ESI's tracking performance of q-o-q GDP growth

step a: re-constructing the ESI based on "best-performing" survey questions

step b: an ESI with amplified changes

3. Refresher on ESI Construction Method

1. Introduction: the Economic Sentiment Indicator (ESI)

3

1. Introduction: the Economic Sentiment Indicator (ESI)

Added value: timeliness (complementing delayed quantitative statistics)

high frequency

Purpose of the ESI: summarising developments in all 5 sectors covered by DG

ECFIN's Business and Consumer Surveys (BCS):

services

tracking GDP growth at Member State, EU and euro-area level

industry

construction

retail trade consumers

4

ESI is excellent in tracking GDP growth y-o-y…

2. Relative Weaknesses of the Economic Sentiment Indicator (ESI)

03/1

996

03/1

997

03/1

998

03/1

999

03/2

000

03/2

001

03/2

002

03/2

003

03/2

004

03/2

005

03/2

006

03/2

007

03/2

008

03/2

009

03/2

010

03/2

011

03/2

012

70.00

75.00

80.00

85.00

90.00

95.00

100.00

105.00

110.00

115.00

120.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

ESI (quarterly levels)GDP growth (quarterly, y-o-y, euro area, rhs)

0.92

0.87

0.68

Correlations:

coincident

leading 1

leading 2

However…

5

ESI is less convincing in tracking GDP growth q-o-q…

2. Relative Weaknesses of the Economic Sentiment Indicator (ESI)

06/1

995

06/1

997

06/1

999

06/2

001

06/2

003

06/2

005

06/2

007

06/2

009

06/2

011

70

80

90

100

110

120

-3

-2

-1

0

1

2

ESI (quarterly levels)

GDP growth (quarterly, q-o-q, euro area, rhs)

06/1

995

06/1

997

06/1

999

06/2

001

06/2

003

06/2

005

06/2

007

06/2

009

06/2

011

30

35

40

45

50

55

60

65

-3

-2

-1

0

1

2

PMI (quarterly levels)

GDP growth (quarterly, q-o-q, euro area, rhs)

06/1

995

06/1

997

06/1

999

06/2

001

06/2

003

06/2

005

06/2

007

06/2

009

06/2

011

96

97

98

99

100

101

102

103

-3

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

OECD Composite Leading Indicator (quarterly levels)

GDP growth (quarterly, q-o-q, euro area, rhs)

PMI

0.71 0.87 0.67

0.46 0.65 0.38

0.19 0.37 0.05

Correlations:

coincident

leading 1

leading 2

ESI OECD CLI

2 quarters delay

downturn signalled with:

1 quarter delay

quickness of recovery underestimated

6

ingredients: balance series of 15 survey questions

Effect: values >100 indicate above-average

economic sentiment

3. Refresher on ESI Construction Method

The questions are: seasonally adjusted standardised

allocating weights per sector: Industry: 40% ; Services: 30% ; Consumers: 20% ; Construction: 5% ; Retail Trade: 5%

calculation of arithmetic mean of weighted balances

standardisation of the ESI and: addition of 100 multiplication by 10

Effect: comparability of balance series in

terms of mean and volatility no series dominates development of

ESI due to a higher amplitude

individual indu question has weight of 13,3% (=40% weight / 3 questions)

2/3 of observations will be in the interval [90 ; 110]

(assuming normality)

% of positive answers minus % of negative answers

7

4. Improving the ESI's tracking performance of q-o-q GDP growth

step a: re-constructing the ESI based on "best-performing" survey questions

1. Correlation of all individual survey questions with i) reference series, ii) q-o-q GDP growth:

quarterly averages of balance series

for industry:Gross Value Added in Manufacturingfor services:Gross Value Added in Servicesfor consumers:Household and NPISH final consumption expenditurefor construction:Gross Value Added in Construction

for retail trade:Household and NPISH final consumption expenditure

8

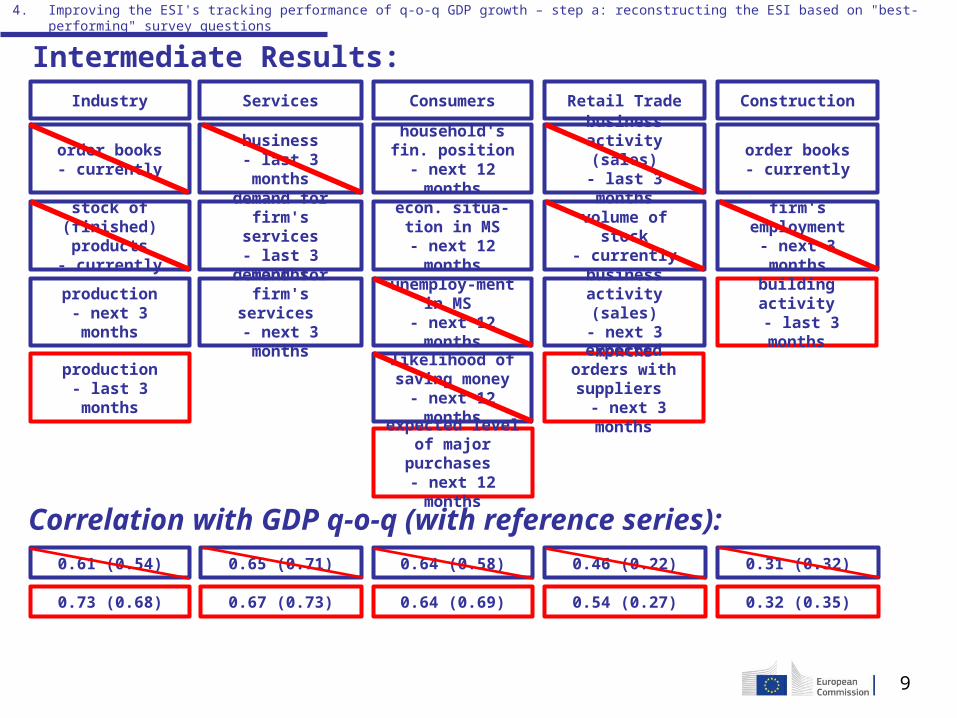

2. Construction of 3 new sector-specific Confidence Indicators (CIs):

CIs summarise overall perceptions / expectations at individual sector level

4. Improving the ESI's tracking performance of q-o-q GDP growth – step a: reconstructing the ESI based on "best-performing" survey questions

calculation: arithmetic mean of (seasonally adjusted) balances for specific questions

questions included in sectoral CIs are also the ones used to construct the ESI

1. CI based on the 2 best performing questions (reg. correlation with reference series & GDP q-o-q)

2. CI based on the 3 best performing questions (reg. correlation with reference series & GDP q-o-q)

3. CI based on all forward-looking questions of the respective sector

3. For each sector: selection of the best CI (reg. correlation with reference series & GDP q-o-q)

9

Intermediate Results:

4. Improving the ESI's tracking performance of q-o-q GDP growth – step a: reconstructing the ESI based on "best-performing" survey questions

Industry Services Retail TradeConsumers

order books- currently

business- last 3 months

business activity (sales)

- last 3 months

household's fin. position

- next 12 months

stock of (finished) products

- currently

demand for firm's services

- last 3 months

volume of stock- currently

econ. situa-tion in MS

- next 12 months

production- next 3 months

demand for firm's services

- next 3 months

business activity (sales)

- next 3 months

unemploy-ment in MS

- next 12 months

likelihood of saving money

- next 12 months

Construction

order books- currently

firm's employment- next 3 months

production- last 3 months

expected level of major purchases - next 12 months

expected orders with suppliers

- next 3 months

building activity - last 3 months

0.61 (0.54) 0.65 (0.71) 0.46 (0.22)0.64 (0.58)

0.73 (0.68) 0.67 (0.73) 0.54 (0.27)0.64 (0.69)

0.31 (0.32)

0.32 (0.35)

Correlation with GDP q-o-q (with reference series):

10

4. Re-construction of the ESI, using the set of questions of the new CIs:

4. Improving the ESI's tracking performance of q-o-q GDP growth – step a: reconstructing the ESI based on "best-performing" survey questions

Slight improvements…

03/1

996

12/1

996

09/1

997

06/1

998

03/1

999

12/1

999

09/2

000

06/2

001

03/2

002

12/2

002

09/2

003

06/2

004

03/2

005

12/2

005

09/2

006

06/2

007

03/2

008

12/2

008

09/2

009

06/2

010

03/2

011

12/2

011

09/2

012

60

70

80

90

100

110

120

-03

-02

-01

00

01

ESI with new questions (quarterly levels)ESI (quarterly levels)GDP growth (quarterly, q-o-q, euro area, rhs)

Turning points:modified ESI records 0-change in quarter where GDP-downturn starts, while the ESI still signals a rise

Amplitude:modified ESI records steeper downward slope than ESI, being more in line with GDP-growth

modified ESI

0.71 0.77 8 %

0.46 0.51 12%

0.19 0.25 30%

Correlations:

coincident

leading 1

leading 2

ESI improvement

11

step b: an ESI with amplified changes

Intuition of the approach:

4. Improving the ESI's tracking performance of q-o-q GDP growth

Comparable changes in the ESI should be taken more "seriously", when reflected by many survey questions.

Example:

Indu

stry

Q1

Indu

stry

Q5

Servic

es Q

2

Servic

es Q

3

Consu

mpt

ion Q

2

Consu

mpt

ion Q

4

Consu

mpt

ion Q

9

Retail

Q3

Retail

Q4

Const

ruct

ion Q

1

Const

ruct

ion Q

3

-2

-1.5

-1

-0.5

0

0.5

change in 1999Q1 (compared to previous quarter)change in 2000Q4 (compared to previous quarter)

Change in modified ESI: -1.8

Change in modified ESI: -2

Instead:change in ESI should be-2*x (with x > 1)

standard deviation of balance series

>>>> change in ESI should be multiplied, if a critical amount of questions changes in the same direction

We propose: 8 (out of 11) questions We propose: multiplication by 3

12

Calculation of the new method:

4. Improving the ESI's tracking performance of q-o-q GDP growth – step b: an ESI with amplified growth

1. Sum all standardised weighted questions per quarter:

2. Calculate the (modified) ESI:

Variable is called: ZNEW

sum of weighted standardised questions (per quarter)

13

4. Improving the ESI's tracking performance of q-o-q GDP growth – step b: an ESI with amplified growth

3. Calculate the absolute change of ZNEW per quarter:

4. Calculate for each quarter a variable taking value 1 if >=8 questions go up / go down :

Variable is called: ZNEW change

(trigger variable)

Variable is called: ZNEW change (amplified)

5. Re-calculate "ZNEW change" mutiplying it by 3 (only in case the "trigger variable" has value 1):

sum of weighted standardised questions (per quarter)

14

4. Improving the ESI's tracking performance of q-o-q GDP growth – step b: an ESI with amplified growth

6. Re-calculate ZNEW, adding "ZNEW change (amplified)" of quarter t to "ZNEW" of quarter t-1:

Variable is called: ESINEW (amplified change)

Variable is called:

ZNEW (amplified)

7. Standardise "ZNEW (amplified)" and thus obtain a new ESI with amplified change:

15

4. Improving the ESI's tracking performance of q-o-q GDP growth – step b: an ESI with amplified growth

Results:

03/1

996

03/1

997

03/1

998

03/1

999

03/2

000

03/2

001

03/2

002

03/2

003

03/2

004

03/2

005

03/2

006

03/2

007

03/2

008

03/2

009

03/2

010

03/2

011

03/2

012

60

70

80

90

100

110

120

-3

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

current ESI (quarterly levels)

ESINEW - amplified change (quarterly levels)

PMI (quarterly levels, rescaled to long-term mean of 100)

GDP growth (quarterly, q-o-q, euro area, rhs)

improvements:

compared to current ESI:

compared to PMI:

"micro"-volatility of GDP better captured

2008-downturn announced by steeper slope (more in line with GDP)

2009-upswing reflected with steeper slope (in line with GDP)

"micro"-volatility of GDP better captured

better leading properties

time-period current ESI PMIESINEW (ampl.)

increase compared to current ESI

increase compared to

PMI

98Q3 – 02Q1 0.58 (0.28) 0.74 (0.54)0.76 (0.52) 31% (85%) 4% (-4%)

02Q2 – 07Q1 0.79 (0.64) 0.86 (0.63)0.85 (0.69) 8% (8%) -1% (10%)

07Q2 – 12Q2 0.74 (0.39) 0.89 (0.61)0.91 (0.73) 23% (87%) 2% (18%)

98Q3 – 07Q1 0.64 (0.41) 0.79 (0.58)0.79 (0.58) 25% (41%)

98Q3 – 12Q2 0.75 (0.49) 0.87 (0.65)0.90 (0.73) 20% (51%)

0% (0%)

3% (12%)

Correlation with GDP growth q-o-q (in brackets: leading 1 correlations)

16

Conclusion: BCS data can be used to construct indicator tracking q-o-q

GDP growth satisfactorily

key of the approach: consider not only the (average) values of the balance series, but also the amount of series moving up/down

approach is still in its infancy and needs further testing

17

4. Improving the ESI's tracking performance of q-o-q GDP growth – step b: an ESI with amplified growth

Shortcomings of the approach

Is it possible to apply the same construction method to monthly data?

Calculations are done with quarterly averages of BCS questions

>>>> indicator could only be published once a quarter

technically yes !

Will quarterly averages of the resulting monthly ESI-series remain well-correlated with q-o-q GDP growth?

yes: even slightly higher correlations with GDP q-o-q

correlation of the two quarterly ESI series is at 0.97

However…

18

4. Improving the ESI's tracking performance of q-o-q GDP growth – step b: an ESI with amplified growth – Shortcomings of the approach

Problem of constructing ESI with amplified changes for monthly data:

too high volatility

1/1/

1996

1/1/

1997

1/1/

1998

1/1/

1999

1/1/

2000

1/1/

2001

1/1/

2002

1/1/

2003

1/1/

2004

1/1/

2005

1/1/

2006

1/1/

2007

1/1/

2008

1/1/

2009

1/1/

2010

1/1/

2011

1/1/

2012

55

65

75

85

95

105

115

125

ESINEW - amplified changes (monthly levels) current ESI (monthly levels)

Sep 2009: in upswing-period, ESINEW with amplified changes drops by 10 points (=1 standard deviation)

19

4. Improving the ESI's tracking performance of q-o-q GDP growth – step b: an ESI with amplified growth – Shortcomings of the approach

If amplification is applied in t-1, but not in t, ESI will usually suggest a drop in sentiment in t (also in case the underlying data continues the upward/downward trend of t-1)

Source of volatility (note: amplifying changes does not only increase the amplitude of the series, but also its volatility):

Jan Feb Mar Apr94

96

98

100

102

104

106

unamplified ESIESI (amplified change): assuming 8 questions go up in Feb

+2 +2 +2

+2*3 = +6

This additional volatility improves the fit of our quarterly series, but renders the monthly series TOO volatile.

Main reason for this difference: criterion for amplification is more restrictive in case of quarterly set-up:

for quarterly: >= 8 questions must have gone up/down over 3 months-period (amplification in 63% of quarters)

for monthly: >= 8 questions must have gone up just one month (amplification in 73% of the months)

20

4. Improving the ESI's tracking performance of q-o-q GDP growth – step b: an ESI with amplified growth – Shortcomings of the approach

Solution: When multiplying change of t (compared to t-1), the

resulting amplified change should be added to ESI for month t, but also ESI of t+1 and t+2 (1/3 of the change respectively should be added).

Approach smoothens the monthly curve substantially…

4/1/

1996

4/1/

1997

4/1/

1998

4/1/

1999

4/1/

2000

4/1/

2001

4/1/

2002

4/1/

2003

4/1/

2004

4/1/

2005

4/1/

2006

4/1/

2007

4/1/

2008

4/1/

2009

4/1/

2010

4/1/

2011

4/1/

2012

55

65

75

85

95

105

115

125

ESINEW - amplified changes (monthly levels)ESINEW - amplified changes distributed over 3 months (monthly levels)

When constructing quarterly averages, correlations with q-o-q GDP growth remain high.