European Bank for Reconstruction and Development · Investments in primary agriculture...

29

European Bank for Reconstruction and Development The Leading Private Sector Investor in Western Balkans Belgrade, 20 th April 2011

Transcript of European Bank for Reconstruction and Development · Investments in primary agriculture...

European Bank for Reconstruction and Development

The Leading Private Sector Investor in Western Balkans

Belgrade, 20th April 2011

Structure of Presentation

1. Introduction to EBRD

2. Financing with EBRD

3. EBRD and Agribusiness

4. Crisis Response and Beyond

5. EBRD contact

6. Questions and Answers

1. Introduction to EBRD

What is the EBRD?

International financial institution owned by 61 countries and two inter-governmental institutions. Capital base of EUR 30 billion with capital increase approved in Zagreb in May 2010.

Operates through the Head Office in London and Resident Offices in 30 countries of operation.

Works in both the public and private sectors.

Financing is provided directly or through financial intermediaries.

What are the EBRD’s objectives?

Support economic growth in its countries of operation.

Promote entrepreneurship, competition and privatisation.

Promote adoption of strong corporate governance, including environmental sensitivity.

Promote foreign direct investment and mobilise domestic capital.

Provide technical assistance.

EBRD’s cumulative investments amount to EUR 62.0 billion up to the Dec 2010

The EBRD is the largest single investor in the region and mobilizes significant foreign direct investment beyond its own financing.

As of the end of December 2010, the Bank had cumulative commitments of € 60.0 billion.

Private sector > 74% of EBRD portfolio

Debt 77%, Equity 23% of EBRD portfolio

Investments in 2010 – EUR 9.0 billion from EUR 7.9 billion in 2009

2010 investments in WB – EUR 1 billion

Cumulative commitments (billions €)

048

12162024283236404448525660

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

Unaudited as at 30 September 2010

2. Financing with EBRD

The EBRD offers a variety of different financing instruments

Senior, subordinated, convertible

Long term

Working capital

Fixed / floating interest rates

Major (USD, EUR) and local currencies (e.g. Romania, Russia, Poland)

Political risk guarantees

Common / preferred shares

Mezzanine financing

Exclusively minority participations (up to 35%)

“Portage Equity“

In-house syndication unit

Lender of record

EBRD‘s Preferred creditor status attracts other financiers

LoansLoans EquityEquity SyndicationSyndication

Financing requirementsFinancing requirements How to obtain finance?How to obtain finance?

EBRD financing requires careful upfront risk assessment and a clear investment strategy

Ensure appropriate returns by carefully

assessing the risks:Management strength and strategyClear business plan and project costsTransparency of operationsDisclosed identity of final shareholders

and corporate structure Identified and limited tax liability riskRecourse to subsidiaries generating

profits and holding assets

Ensure appropriate returns by carefully

assessing the risks:Management strength and strategyClear business plan and project costsTransparency of operationsDisclosed identity of final shareholders

and corporate structure Identified and limited tax liability riskRecourse to subsidiaries generating

profits and holding assets

Provide EBRD with an overview of

proposed investmentCommitment to cooperation

clarify role of EBRD mandate to initiate transaction mutual understanding of corporate

integrity issuesProject / business plan, market

analysis, strategy, ownership structure,

financial analysis, risk assessment Exit strategy

Provide EBRD with an overview of

proposed investmentCommitment to cooperation

clarify role of EBRD mandate to initiate transaction mutual understanding of corporate

integrity issuesProject / business plan, market

analysis, strategy, ownership structure,

financial analysis, risk assessment Exit strategy

3. EBRD and Agribusiness

EBRD and Agribusiness

Agribusiness

• From 2000, the EBRD has invested EUR 6.5 billion in over 422 projects in the Agribusiness sector.

• 2010: 63 projects signed with EUR 836 million committed investments vs. 59 projects with EUR 639 million in 2009.

• One of the largest sector teams within the EBRD with 33 bankers in London and Resident Offices accounting for around 40% of the projects in the EBRD’s corporate sector portfolio.

• Client network of leading global and regional players.

Agribusiness Strategy

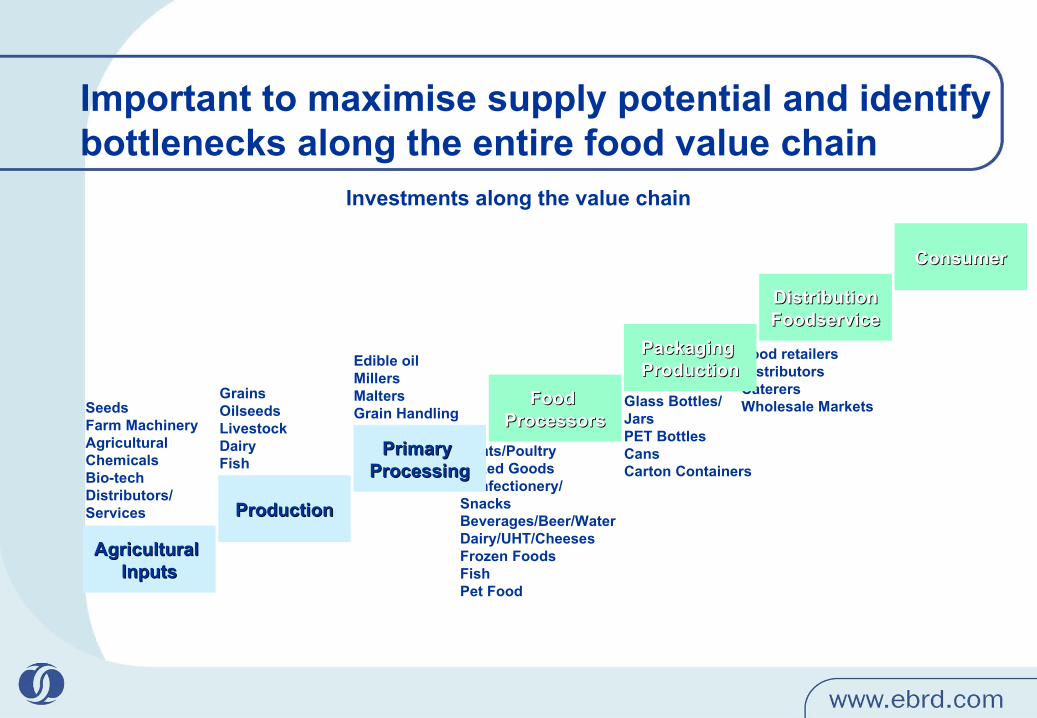

• All activities along the food and drink production chain are included

• Rather focused on increasing demand than supply.

• Downstream investments are mainly in vertical integrated companies with positive spill-over effects to primary agriculture.

• Indirect support to smaller farmers and food enterprises via SME credit lines.

• As a result, EBRD has a conservative approach towards direct land investments.

Primary & secondary processing

Packaging & distribution

Retail &Food Service

Downstream Upstream

Agricultural inputs

& production

ConsumerConsumer

SeedsFarm MachineryAgricultural ChemicalsBio-techDistributors/Services

GrainsOilseedsLivestockDairyFish

Edible oilMillersMaltersGrain Handling

Meats/PoultryBaked GoodsConfectionery/SnacksBeverages/Beer/WaterDairy/UHT/CheesesFrozen FoodsFishPet Food

Food retailersDistributorsCaterersWholesale MarketsGlass Bottles/

JarsPET BottlesCansCarton Containers

Primary Primary ProcessingProcessing

ProductionProduction

Agricultural Agricultural InputsInputs

DistributionDistributionFoodserviceFoodservice

Packaging Packaging ProductionProduction

Food Food ProcessorsProcessors

Important to maximise supply potential and identify bottlenecks along the entire food value chain

Investments along the value chain

Developing appropriate strategies in dealing with market Developing appropriate strategies in dealing with market challengeschallenges

Retail consolidationRetail consolidation is happening but competition is healthy: higher is happening but competition is healthy: higher competition in retail will create larger choices for suppliers and consumers competition in retail will create larger choices for suppliers and consumers and help fight food inflation and help fight food inflation (like in UK in 1Q2011).(like in UK in 1Q2011). Still highly fragmented Still highly fragmented (Serbia 25m2/per capita, BiH 10m2/per capita, Croatia 150m2/per capita)(Serbia 25m2/per capita, BiH 10m2/per capita, Croatia 150m2/per capita)

Regional expansion:Regional expansion: higher growth opportunities in western Balkan higher growth opportunities in western Balkan countries including higher brand recognition (ex-YU legacy) then in the countries including higher brand recognition (ex-YU legacy) then in the EU as well as understanding of consumer preferences – establishing EU as well as understanding of consumer preferences – establishing early entrance – subsidiaries or JV. early entrance – subsidiaries or JV.

Strong processorsStrong processors are the key to a healthy sector; as they provide a are the key to a healthy sector; as they provide a sustainable market for agricultural products.3sustainable market for agricultural products.3

Moving closer to primary agriculture-Moving closer to primary agriculture- A better legal and institutional A better legal and institutional framework is a must for farmers to get the financing they need – as a framework is a must for farmers to get the financing they need – as a result of EBRD – introduction of warehouse receipts financing. result of EBRD – introduction of warehouse receipts financing.

EBRD and Agribusiness: sector views

Branded food and beverages producers with clear regional Branded food and beverages producers with clear regional expansion strategies expansion strategies - Projects with: Somboled (Serbia), Tikves (FYR Macedonia), Brcko (BiH), Marbo Projects with: Somboled (Serbia), Tikves (FYR Macedonia), Brcko (BiH), Marbo

(Serbia), Grand (Serbia), Droga Kolinska (Slovenia), Stark (Serbia), Atlantic Group (Serbia), Grand (Serbia), Droga Kolinska (Slovenia), Stark (Serbia), Atlantic Group (Croatia), Agrokor (Croatia), Dukat (Croatia) etc,(Croatia), Agrokor (Croatia), Dukat (Croatia) etc,

Growing local and international retailersGrowing local and international retailers- Projects with Idea (Serbia), VF Komerc (Bosnia and Herzegovina), Voli Projects with Idea (Serbia), VF Komerc (Bosnia and Herzegovina), Voli

(Montenegro), Kaufland (regional), Billa (regional), Spar (Croatia), (Montenegro), Kaufland (regional), Billa (regional), Spar (Croatia),

Processors such as edible oil, meat and juice producersProcessors such as edible oil, meat and juice producers - - Projects with Victoria Group (Serbia), Boni (Bulgaria), Nectar (Serbia)Projects with Victoria Group (Serbia), Boni (Bulgaria), Nectar (Serbia)

Investments in primary agricultureInvestments in primary agriculture (MK/Agroinvest Ukraine, CHS Romania, (MK/Agroinvest Ukraine, CHS Romania, Serbia and Hungary)Serbia and Hungary)

EBRD and Agribusiness: sector views Recognised strategies of sub-sectors

Extensive experience in cooperating with the leading Agribusiness and FMCG corporates of the entire food chain. We are working with local and international clients with many follow on projects.

Agribusiness Clients

Western Balkans Agribusiness Strategy An overview

Western Balkans: important region for agribusiness.

Countries standing out: Serbia and Croatia

Western Balkans made 13 % total agribusiness in 2010.

10 transactions in 2010 and 13 in 2009 as a crisis tool.

Trademark deals in 2010: Atlantic Group and WHR in Serbia

In Turkey, the Bank had two projects in 2010: Noble Turkey and Ulker.

Agribusiness portfolio – Western Balkans

Victoria Group (EUR 40m, Serbia; agribusiness)

Spar (EUR 25m, Croatia; retail)

Žitoluks (EUR 3.7m, FYR Macedonia; bakery)

Konzum BiH (EUR 50m, BiH; retail)

Bimal (EUR 4m, BiH; edible oil)

Zdravje (EUR 1m, FYR Macedonia; dairy)

Agribusiness team transactions in 2009 in cooperation with the EBRD offices in the region

VF Komerc (EUR 1.25m, BiH; retail) Devolli (EUR 6m, Serbia (Kosovo);

food and beverage) Albi (EUR 5m, Serbia (Kosovo); retail) Tikveš (EUR 2.5m, FYR Macedonia;

wine) Mesopromet (EUR 2m, Montenegro;

meat processing) Voli (EUR 4m, Montenegro; retail) Vitaminka (EUR 0.8m, FYR

Macedonia; food)

Agribusiness portfolio – Western Balkans

Atlantic Group Equity (EUR 27.5m, Croatia)

Atlantic Group Debt (EUR 30m, Croatia)

Bingo (EUR 3.7m, BiH)

MIK Sveti Nikola (EUR 1.6m, FYR Macedonia)

Pestova (EUR 0.5m, Kosovo (under 1244))

Agribusiness team transactions in 2010 in cooperation with the EBRD offices in the region

Societe Generale WHR (EUR 20m, Serbia)

Albi (EUR 1.6m, Kosovo (under 1244))

Haxhijaha (EUR 0.9m, Kosovo (under 1244))

Banca Intesa WHR (EUR 10m, Serbia)

CHS Regional facility (EUR 13.4m, Serbia)

Agribusiness Portfolio Serbia

2006 2007 2008 2009 2010

Deals Somboled EUR 10m

(cross border)

Stark EUR 10m

(cross border)

MladostSid EUR 10m

(working capital)

Victoria Group EUR 45m

(working capital/EE)

Nectar EUR 10m (expansion)

Agroinvest EUR 10m

(cross-border)

Idea EUR 70m

(restructuring/ retail)

Victoria Group EUR 40m

(restructuring/ working capital)

Societe Generale WHR EUR 20m

Banca Intesa WHR EUR 10m

(commodity backed financing)

CHS EUR 13.4m

(working capital)

Total EUR 30m EUR 65m EUR 70 EUR 40m EUR 43.4m

-# 3 3 1 1 3

Agribusiness Portfolio Croatia

2006 2007 2008 2009 2010

Deals Agrokor EUR 110m

(restructuring/ cross border)

Dukat/Somboled EUR 10m

(restructuring/ cross border)

Getro EUR 28.8m

(restructuring)

Idea/Agrokor – EUR 70m

(cross-border)

Spar EUR 25m

(expansion)

Konzum EUR 50m

(cross-border)

Atlantic Group EUR 27.5m

Atlantic Group EUR 30m

(acquisition finance)

Total EUR 120m EUR 28.8m EUR 70m EUR 75m EUR 57.5m

-# 2 1 1 2 2

4. Crisis Response and Beyond

EBRD Crisis Response and Beyond…

EBRD is providing financing to the local corporate companies through loan financing, equity and quasi-equity participations and guarantees. Also the Bank is providing loans for financing of industrial energy efficiency projects. Minimum financing of EUR 1 million.

In response to the crisis, the Bank remains committed to:– support its existing private sector clients as well as to financing

commercially viable private sector projects with both local and foreign investors;

– provide long-term funding to local banks for on-lending to private SMEs; and

– continue to provide financing for infrastructure projects in the transport, power and municipal sectors.

EBRD Crisis Response and Beyond…

Crisis has hit the region hard:

– Liquidity and working capital issues

– Consumer purchasing power went down (cca 12%) with changed consumer preferences (lower retail basket by, focus on economy segment products, private label)

– Banks are focusing only on “first-tier” larger companies without appetite for significant new long term lending, further liming growth

– Limited expansion projects (new capital investments), but more focus on regional consolidation (sale of Delta Maxi to Delhazie Group, Droga Kolinska to Atlantic Group, Tus to IDEA, ongoing processes for Mercator, Fructal etc.)

EBRD Crisis Response and Beyond…

To alleviate lack of long-term funds in the WB region:

– EBRD is providing long term funding for Balance Sheet restructuring and improving maturity profiles

– EBRD offers long term debt with repayments in line with “cash flows” of companies, equity and quasi equity instruments etc.

– Co-financing with local and international commercial banks operating in the region to increase their risk appetite for long term lending in region (e.g. preferred creditor status etc.)

… and what to focus on in the WB region

Co-financing larger projects with commercial banks

Risk Sharing schemes with local banks in financing post harvest operations using harvest as security (Warehouse Receipts) like in Serbia

Risk Sharing schemes with local banks/leasing companies in financing agricultural equipment using equipment as security (currently exploring in Serbia)

Equity/quasi investments on its own or in co-operation with private equity funds or strategic investors not willing to take region risk from the outset

… and what to focus on in the WB region

Serbia, together with Romania, Russia, Ukraine and Kazakhstan is classified as strategically important country for grain sourcing

As a result, in addition to Warehouse Receipts (WHR), the Bank is working with Ministry of Agriculture of Serbia on preparing the legal ground for adoption of Crop Receipts (instrument used in Brazil for security for lending based on future crop)

Today, in Brazil there is USD 20bln per year pre-financing using crop receipts The Bank believes this will increase liquidity and investments in agriculture sector

Lack of agronomists & relevant experts across the agribusiness value chain, problem in primary agriculture is evident through substantially lower yields (potential co-operation with European Commission from their funds once Serbia and other WB countries obtain access to rural component of instrument for pre-accession assistance linked to candidate status)

Contact

Miljan ŽdraleSenior BankerEBRD London, Banking DivisionIndustry, Commerce and Agribusiness GroupAgribusiness (FMCG/Food Retail) TeamTel.: +44 207 338 6000 Fax: + 44 207 338 [email protected]

Questions and Answers

The time is always right for all kind of questions…