European Airline Capacity – Winter 2013/14 Boeing...

30

BOEING is a trademark of Boeing Management Company. Copyright © 2014 Boeing. All rights reserved. European Airline Capacity – Winter 2013/14 Boeing Commercial Airplanes Network, Fleet and Schedule Strategic Planning Module 20: 14 March 2014 Istanbul Technical University Air Transportation Management M.Sc. Program

-

Upload

truongthien -

Category

Documents

-

view

218 -

download

2

Transcript of European Airline Capacity – Winter 2013/14 Boeing...

BOEING is a trademark of Boeing Management Company. Copyright © 2014 Boeing. All rights reserved.

European Airline Capacity – Winter 2013/14 Boeing Commercial Airplanes

Network, Fleet and Schedule

Strategic Planning

Module 20: 14 March 2014

Istanbul Technical University

Air Transportation Management

M.Sc. Program

Copyright © 2014 Boeing. All rights reserved. Boeing Proprietary

World Regional Definitions

COPYRIGHT © 2014 THE BOEING COMPANY

Executive Summary Scheduled capacity to/from/within Europe up 5.3% YoY (by ASKs), led by

Turkish, Norwegian, LCCs. Air France, IAG cutting back on intra-Europe capacity.

− Europe ASKs expanding yet still lags global ASK growth (7.6%) − Turkish, Norwegian continue rapid expansion with double-digit ASK growth

Flag carriers cutting intra-Western Europe frequencies for the winter while Turkish, Norwegian, and Ryanair expand

− Despite ASK capacity growth, frequency growth flat as increases by Turkish (23%), LCCs are offset by Lufthansa (-4%), Air France/KLM (-17%), IAG (-13%) cuts

Europe-Middle East continues to be fastest growing regional flow at 10%+

− All regional flows positive, or near positive, YoY growth after volatile 2013

Istanbul Ataturk Airport posting 8% YoY capacity growth; now 4th largest airport by seat capacity

− Spain and Italy continue to face challenges; Madrid, Rome, Barcelona airports are biggest losers

Focus Carrier Section includes Lufthansa, Ryanair, Air France / KLM, British Airways/Iberia(IAG),and Air Berlin Supplemental focus section: European airline financials 3rd quarter earnings

3 Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

COPYRIGHT © 2014 THE BOEING COMPANY

Europe Capacity Report: Included Nations

4

YoY Change – Total Offered Seats • Green –expanding capacity • Red – declining capacity

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

COPYRIGHT © 2014 THE BOEING COMPANY

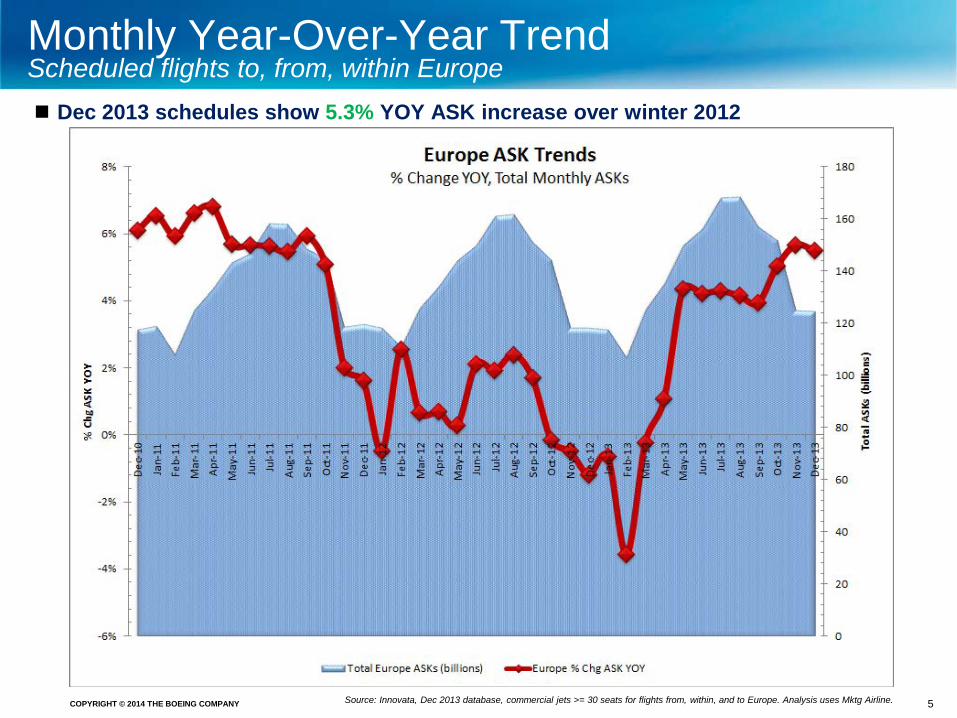

Monthly Year-Over-Year Trend Scheduled flights to, from, within Europe Dec 2013 schedules show 5.3% YOY ASK increase over winter 2012

5 Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

COPYRIGHT © 2014 THE BOEING COMPANY

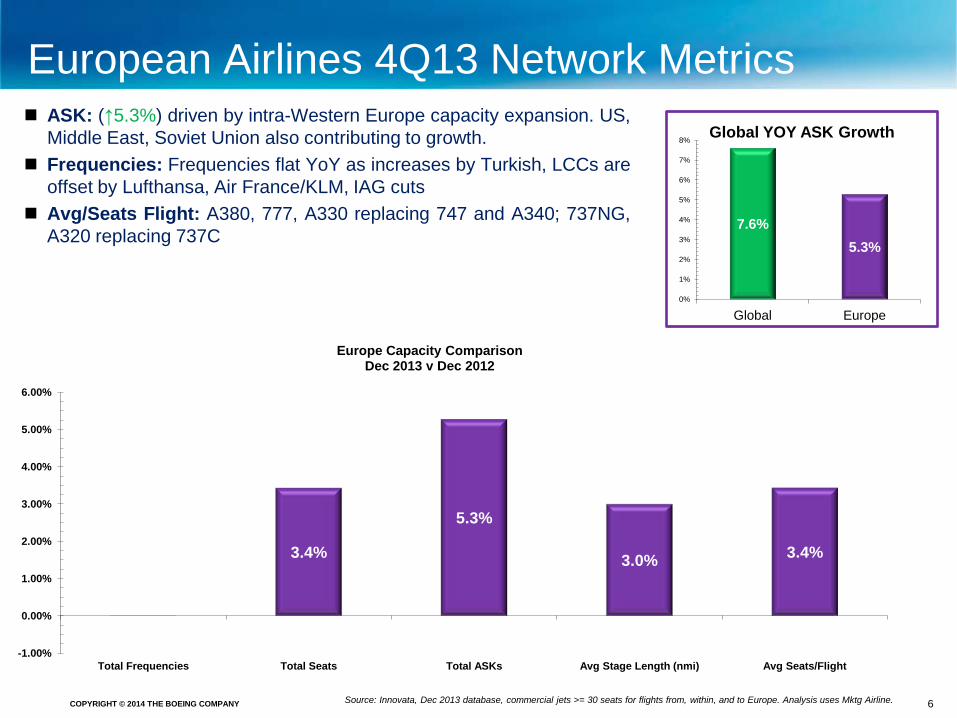

European Airlines 4Q13 Network Metrics ASK: (↑5.3%) driven by intra-Western Europe capacity expansion. US,

Middle East, Soviet Union also contributing to growth. Frequencies: Frequencies flat YoY as increases by Turkish, LCCs are

offset by Lufthansa, Air France/KLM, IAG cuts Avg/Seats Flight: A380, 777, A330 replacing 747 and A340; 737NG,

A320 replacing 737C

6

0.4%

2.1% 3.4%

+1.6%

0.0%

3.4%

5.3%

3.0% 3.4%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Total Frequencies Total Seats Total ASKs Avg Stage Length (nmi) Avg Seats/Flight

Europe Capacity Comparison Dec 2013 v Dec 2012

7.6% 5.3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Global Europe

Global YOY ASK Growth

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

COPYRIGHT © 2014 THE BOEING COMPANY

-

500

1,000

1,500

2,000

2,500

3,000

3,500

LUFTHANSA AIR FRANCE IAG TURKISH AIRLINES

RYANAIR EASYJET EMIRATES NORWEGIAN AIR SHUTTLE

UNITED AIRLINES

SAS SCANDINAVIAN

AIRLINES

Wee

kly

ASK

s (M

illio

ns)

Dec 13 ASK (per week) Change (neg)

Dec 13 ASK (per week) Change (pos)

Dec 12 ASK (per week)

Europe Capacity Comparison - ASKs Dec 2013 vs. Dec 2012 weekly available-seat-kilometers (ASKs)

European capacity up (ASKs ↑5.3%); intra-Europe capacity shifting away from AF, IAG Turkish Airlines moves to 4th largest operator (by ASKs) after 19% YoY capacity increase

7

4% 42%

3%

9%

2%

0%

-2%

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

7%

3%

19%

↓W. Europe -17% ↑ Carribbean – 46%

↑ Africa – 11% ↑ C. America – 35%

↓E. Europe -28%

↑ former Soviet– NEW ↑ Africa – 14%

↑ Mid East – 5% ↓W. Europe -35%

↑ W. Europe– 34% ↑ US – NEW

↑ SE Asia– NEW

↑ W. Europe – 19% ↑ US – 26%

↑ Japan – 73% ↑ India – 50%

↑ SE Asia – 28% ↑ India – 50%

*Key drivers of change by airline, ranked by impact ↑ Europe - Region – %chg ↓Europe - Region -%chg

↑ W. Europe – 3% ↓Japan - 21%

↑ Canada – 25% ↓Asia - 9%

↑ W. Europe – 9% ↑ Africa – 102% ↓E. Europe -5%

↓W. Europe -7% ↓S. America -14% ↓Carribbean -31%

↑ India– 22% ↑US – 3%

COPYRIGHT © 2014 THE BOEING COMPANY

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

LUFTHANSA AIR FRANCE IAG RYANAIR EASYJET TURKISH AIRLINES

SAS SCANDINAVIAN

AIRLINES

NORWEGIAN AIR SHUTTLE

FLYBE AIR BERLIN

Tota

l Wee

kly

Flig

hts

Dec 12 Flights (per week) Dec 13 Flights (per week) change (pos) Dec 13 Flights (per week) change (neg)

Europe Capacity Comparison - Frequencies Dec 2013 vs. Dec 2012 weekly flights

Biggest Increases: Middle East (Arkia, Turkish), former Soviet Union (Ukraine, Aeroflot), Africa (Ryanair, Thomson,

RAM), United States (BA, Norwegian), Western Europe (Airlinair, Turkish, Germanwings)

Biggest Decreases: Western Europe (LH, AF, IAG)

8

0%

-4%

-5%

-13%

3% 23%

20%

-17%

-2%

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

7%

↓W. Europe – (2,063) flights/wk

↓W. Europe – (1164) flights/wk

↑ W. Europe – 139 flights/wk

↓W. Europe – (1,173) flights/wk

↓W. Europe – (137) flights/wk

↑ W. Europe – 481 flights/wk

↑ W. Europe – 161 flights/wk ↓E. Europe – (46) flights/wk ↑ Africa– 72

flights/wk

↓W. Europe – (107) flights/wk

↑ W. Europe – 889 flights/wk

↑ Middle East – 52 flights/wk

*Key drivers of change by airline, ranked by impact

↑ Europe - Region – chg flights/week ↓Europe - Region -chg flights/week

COPYRIGHT © 2014 THE BOEING COMPANY

Regional Capacity by Flow

9

Europe-Middle East continues to be the fastest growing regional flow ~10% Transatlantic flows strengthening over 2013

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

COPYRIGHT © 2014 THE BOEING COMPANY

Change in Regional Seat Capacity by Flow YOY change (December) in weekly seats deployed, by region

10

Capacity expanding in all regional flows; Turkish a key driver

↑ Turkish 18% ↑ Norwegian 18% ↑ Pegasus 24% ↑ Vueling 11% ↑ Germanwings 75% ↓Air France -18% ↓Iberia -22%

↑ Wizz Air 8% ↑ Lufthansa 10% ↑ Turkish 17% ↑ Austrian 7% ↑ EasyJet 7% ↓ Ryanair -6% ↓LOT -19%

↑LOT 8% ↑ Air Baltic 42% ↑ JAT 69% ↑ Bulgaria 25% ↓Czech -23%

↑ United 4% ↑ British 5% ↑ American 11% ↑ Air France 8% ↑ Turkish 23% ↓ Virgin -9% ↓ Iberia -7%

↑ Emirates 5% ↑ Qatar 17% ↑Turkish 13% ↑ Etihad 22% ↑ Arkia 51% ↑ Saudia 27% ↓ Lufthansa -5% ↓ El Al -15%

↑ RAM 27% ↑ Ryanair 104% ↑ Easyjet 15% ↓Air Algerie -19% ↓Tunisair -8% ↓Egyptair -10%

↑ Air China 3% ↑ GUN 7% ↑ Turkish 15% ↓KLM-5%

↑ Turkish 28% ↑ JAL 15% ↑ Malaysia 11% ↓Korean -12%

↑ KLM 11% ↓Iberia -16% ↓Lufthansa -5% ↓TAM-9%

Intra-Europe (LgSm) Transcontinental (LgSm)

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

COPYRIGHT © 2014 THE BOEING COMPANY

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

A320 737NG 737C E-Jet 757 Other 777 A330 767 747 A340 A380 787 A300/310

Tota

l Sea

ts (

in th

ousa

nds)

Dec 13 Seats (per week) (000s) Dec 12 Seats (per week) (000s)

Europe Fleet Dynamics December YoY Fleet Change by Total Available Weekly Seats

Single Aisle Twin Aisle

• Single-Aisle (↑5.1%): 737NG growth outpacing A320 (↑4%) but total market share largely unchanged

• Twin-Aisle (↑5.2%): Boeing takes 3% of Airbus twin-aisle market share compared to December 2012 with 777/787s entering fleets and A340 leaving fleets faster than 747s

4%

10%

-8% -6% 4% 1% -5%

641%

14% 6%

-19%

10%

6% -2%

A320 ↑ Turkish 34% ↑ Lufthansa 13% ↑ Germanwings 51% ↑ SAS 125% ↓Iberia -25% ↓Air France -9% ↓ Alitalia -11%

A330 ↑ Iberia NEW ↓ Qatar -28% ↑ Etihad 8% ↑ Turkish 28%

737C ↑ Meridana 232% ↑ KLM 7% ↑ Transavia 94% ↓SAS -78% ↓Lufthansa -21% ↓ British -38%

737NG ↑ Pegasus 27% ↑ Norwegian 23% ↑ Sunexpress 210% ↑ Thomson NEW ↑ SAS 10% ↓Austrian -100%

A380 ↓ Lufthansa -33% ↑ Thai 1300% ↑ British NEW ↓ Singapore -14% ↓ Korean -100%

747 ↑ Lufthansa 31% ↓Thai -45% ↓ Cathay -81%

777 ↑ Turkish 103.4% ↑ Emirates 18% ↑ AF/KLM 18% ↑ American 46% ↑ Cathay 73% ↓ANA -44%

787 ↑ Qatar ↑ Thomson ↑ Jetairfly ↑ Norwegian ↑ LAN ↑ Air India ↑ British ↑ Royal Brunei ↑ Aeromexico ↑ China Southern ↑ Ethiopian ↑ JAL ↑ ANA ↑ LOT

E-Jet ↑ Air Dolomiti NEW ↑ Lufthansa 8% ↑ Airlinair NEW ↑ Alitalia 23% ↑ Air Europa 28% ↓Air France -17%

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

A340 ↓Iberia -35% ↓Emirates -91%

COPYRIGHT © 2014 THE BOEING COMPANY

Europe Fleet Dynamics – Market Share Old-generation, out of production airplanes leaving fleets

SINGLE-AISLE OEM Market share shift (share shift Dec YoY):

• Airbus - 53.5% (↓0.4%)

• E-Jet - 5.8% (↑0.3%)

• 737NG, A320 expanding; 737C exiting fleets

TWIN-AISLE OEM Market share (share shift Dec YoY):

• Airbus - 43% (↓3.2%)

• Boeing – 57% (↑ 3.3%) Fleet market share by available seats (share shift Dec YoY):

• A330, A380, 777 expanding

• 777 – 30.1% (↑2.4%)

• A330 – 24.8% (↑0.2%)

• A380 – 5.3% (0%)

• 787 - 3.2% (↑2.7%)

• A340, 747 exiting fleets

• 747 – 11.5% (↓1.2%)

• A340 – 11.2% (↓3.4%)

• Boeing - 36.6% (↑0.7%)

• CRJ - 3.4% (↓0.3%)

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

COPYRIGHT © 2014 THE BOEING COMPANY

Top 15 Europe Airports Ranked by size (December 2013 available originating seat capacity)

13

Total Europe seat capacity ↑ 3.4% in December year-over-year Istanbul Ataturk Airport continues strong year-over-year capacity growth (↑ 8%); 4th largest by Seat Capacity Frankfurt may be feeling pressure from Istanbul, Middle East Spain, Italy capacity down amidst continued uncertainty

Ranked largest to smallest, by seats

Source: Innovata, Dec 2013 database, commercial jets >= 30 seats for flights from, within, and to Europe. Analysis uses Mktg Airline.

3%

6%

-2%

8%

5% 4%

-12%

-6% -4%

4% 3%

8%

4%

-1%

4%

-15%

-10%

-5%

0%

5%

10%

Top 15 European Airports YoY Change in Seat Capacity

(Dec13 v. Dec12)

COPYRIGHT © 2014 THE BOEING COMPANY

Top 50 Intra-Europe City Pairs By weekly seats December 2013

14

*Data: capstats *sector is defined as one aircraft movement from Point A to Point B.

COPYRIGHT © 2014 THE BOEING COMPANY

Intra-European Market Analysis by Country

15

*Data: capstats *sector is defined as one aircraft movement from Point A to Point B.

As of Dec. 2013

COPYRIGHT © 2014 THE BOEING COMPANY

Domestic Market Analysis by Country

16

*Data: capstats *sector is defined as one aircraft movement from Point A to Point B.

As of Dec 2013

COPYRIGHT © 2014 THE BOEING COMPANY

Alliance Capacity Metrics

17 *Data:capstats/Innovata *sector is defined as one aircraft movement from Point A to Point B.

As of Dec. 2013

COPYRIGHT © 2014 THE BOEING COMPANY

Europe - Focus Carriers

18

Europe Focus Carriers • LCCs

• Ryanair

• Air Berlin

• Lufthansa

• Air France/KLM

• IAG

COPYRIGHT © 2014 THE BOEING COMPANY

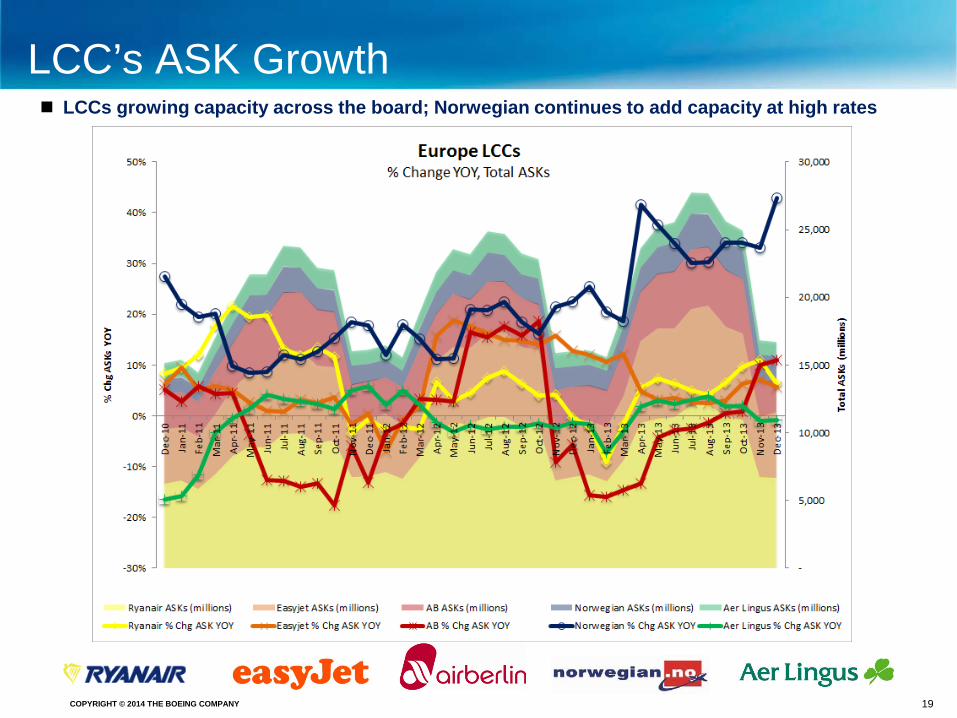

LCC’s ASK Growth

19

LCCs growing capacity across the board; Norwegian continues to add capacity at high rates

COPYRIGHT © 2014 THE BOEING COMPANY

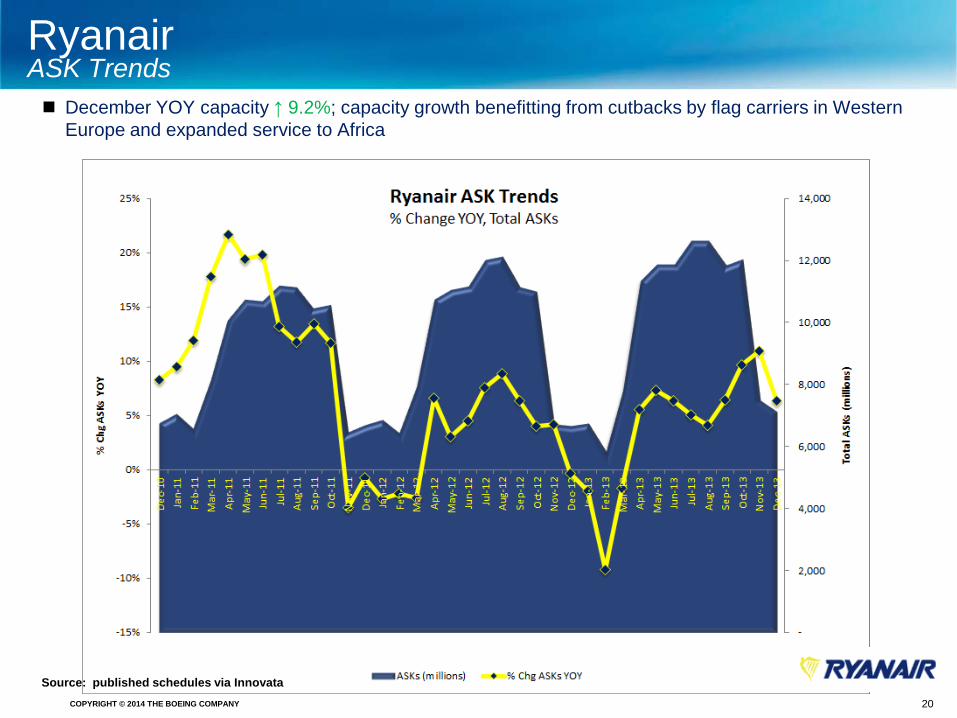

Ryanair ASK Trends December YOY capacity ↑ 9.2%; capacity growth benefitting from cutbacks by flag carriers in Western

Europe and expanded service to Africa

Source: published schedules via Innovata 20

COPYRIGHT © 2014 THE BOEING COMPANY

Ryanair Network Metrics – Dec 2013 v Dec 2012 YoY

21

Source: published schedules via Innovata

ASK growth driven by new intra-Western Europe and Africa routes

2.7% 2.7%

9.2%

6.4%

0.0% 0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Total Frequencies Total Seats Total ASKs Avg Stage Length (nmi) Avg Seats/Flight

COPYRIGHT © 2014 THE BOEING COMPANY

Air Berlin ASK Trends

December schedules ↑ 12.6% YOY; AB aiming to cut costs 15% over the next two years “Turbine 2013” reducing fleet, focusing on short and medium-haul segments in core markets

o Expanding intra-Western Europe, US capacity; cutting Africa capacity

Source: published schedules via Innovata 22

COPYRIGHT © 2014 THE BOEING COMPANY

Air Berlin Network Metrics – Dec 2013 v Dec 2012 YoY

23

6.6%

8.7%

12.6%

3.2% 1.9%

0%

2%

4%

6%

8%

10%

12%

14%

Total Frequencies Total Seats Total ASKs Avg Stage Length (nmi) Avg Seats/Flight

ASK growth driven by routes to Germany, US, Turkey, and Spain

COPYRIGHT © 2014 THE BOEING COMPANY

Lufthansa ASK Trends December YOY schedules up 3.5% as European markets strengthen in second half

Source: published schedules via Innovata 24

COPYRIGHT © 2014 THE BOEING COMPANY

Lufthansa Group Network Metrics – Dec 2013 v Dec 2012 YoY

25

Source: published schedules via Innovata

Intra-Europe: capacity in Germany, Spain, Poland, UK; cutting capacity in Italy, Switzerland

International: growing capacity to Russia, Israel; cutting capacity in US, Korea, Iran, Thailand

-3.8%

5.2% 3.5%

2.1%

9.4%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Total Frequencies Total Seats Total ASKs Avg Stage Length (nmi) Avg Seats/Flight

COPYRIGHT © 2014 THE BOEING COMPANY

Air France / KLM ASK Trends

Source: published schedules via Innovata 26

December YOY schedules ↑ 3% even as AF restructures capacity domestically (Western Europe: AF -17% reduction, KLM 8% expansion)

COPYRIGHT © 2014 THE BOEING COMPANY

-15.2%

-6.7%

3.0%

11.5% 9.9%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Total Frequencies Total Seats Total ASKs Avg Stage Length (nmi) Avg Seats/Flight

Air France / KLM Network Metrics – Dec 2013 v Dec 2012 YoY

27

Source: published schedules via Innovata

AF/KLM contracting in both Western and Eastern Europe while expanding in the Caribbean and

Central America, driven by Air France

AF expanding in SE Asia and Africa, KLM expanding in South America

COPYRIGHT © 2014 THE BOEING COMPANY

IAG (British Airways, Iberia) ASK Trends IAG December YOY schedules down 2.3% as BA growth offset by continued IB restructuring to focus on improving unit

revenues Iberia cutting capacity in all other markets except Eastern Europe…major drivers are in Western Europe (-21%), South

America (-16%), Caribbean (-100%) British Airways expanding in most markets except relatively small cuts to Japan, SE Asia, and Middle East…key capacity

growth markets are US (5%), Western Europe (4%), India (22%), and China + Asia (15%)

Source: published schedules via Innovata 28

COPYRIGHT © 2014 THE BOEING COMPANY

IAG Network Metrics – Dec 2013 v Dec 2012 YoY

29

Source: published schedules via Innovata

Large single-aisle capacity reductions by Iberia driving down ASKs, increasing average stage length

-12.6%

-8.3%

-2.3%

9.5%

5.0%

-15%

-10%

-5%

0%

5%

10%

15%

Total Frequencies Total Seats Total ASKs Avg Stage Length (nmi) Avg Seats/Flight

COPYRIGHT © 2014 THE BOEING COMPANY 30

Questions?