Venezolanos reaccionan ante ofensivas declaraciones de Maduro

Upload

rosanna-cobbCategory

view

213download

0

Europe meets the America’sHow to structure your investment in Aruba

www.pwc.com/dutch-caribbean May 6, 2013

Hans RuiterRachel Vieira Maduro

Europe meets the America'sPwC 2

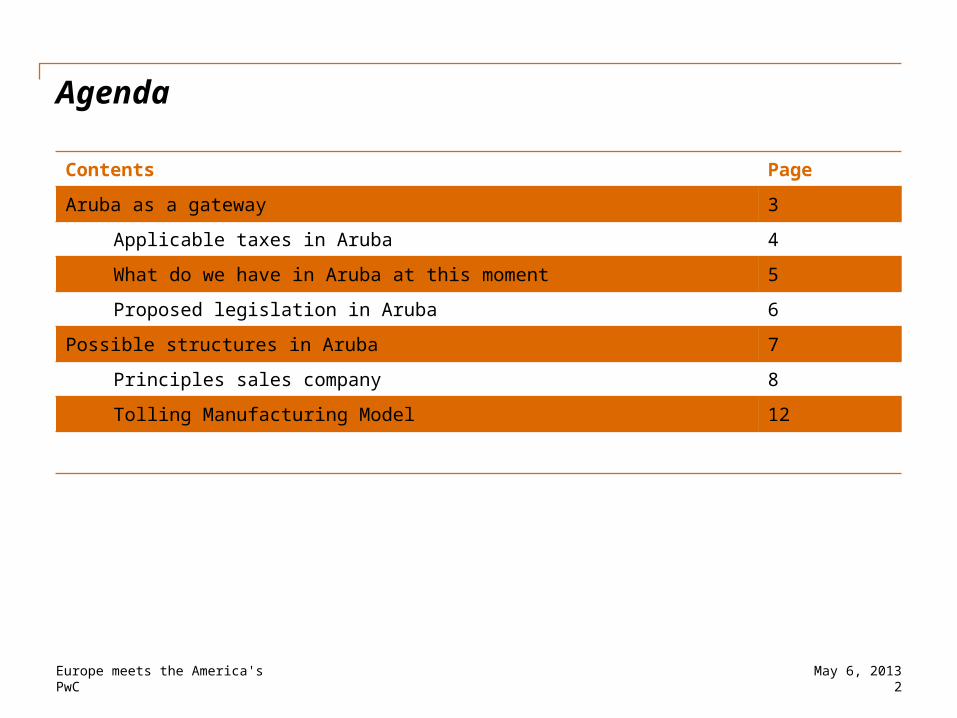

Agenda

Contents Page

Aruba as a gateway 3

Applicable taxes in Aruba 4

What do we have in Aruba at this moment 5

Proposed legislation in Aruba 6

Possible structures in Aruba 7

Principles sales company 8

Tolling Manufacturing Model 12

May 6, 2013

Europe meets the America's3PwC

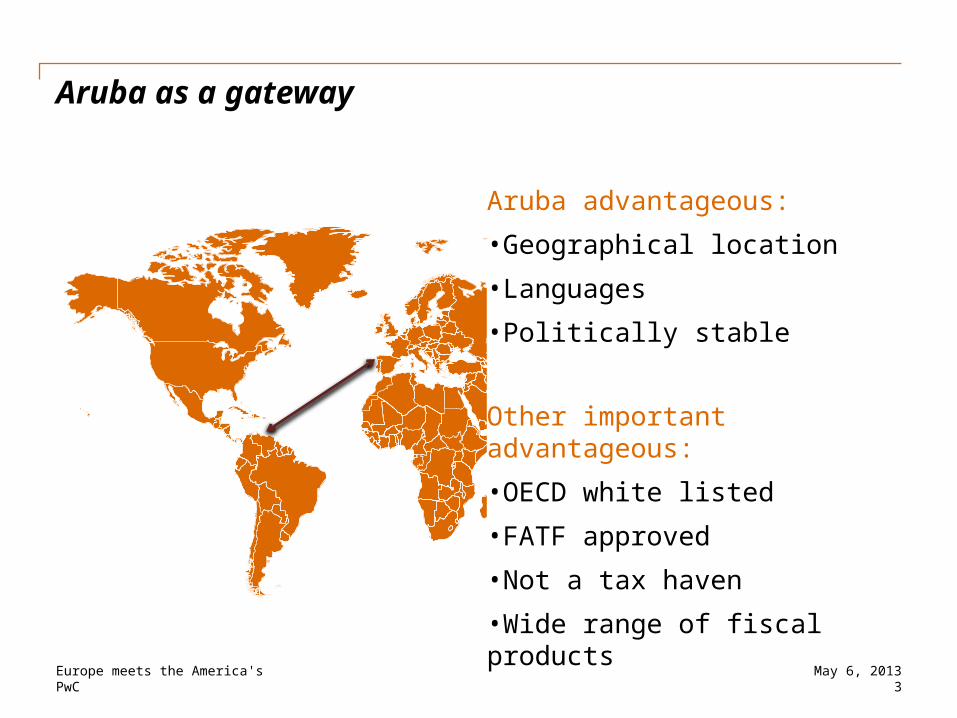

Aruba as a gateway

May 6, 2013

Aruba advantageous:

•Geographical location

•Languages

•Politically stable

Other important advantageous:

•OECD white listed

•FATF approved

•Not a tax haven

•Wide range of fiscal products

Europe meets the America's4PwC

Applicable taxes in Aruba

28% profit tax

10% dividend withholding tax

1.5% turnover tax (VAT/IVA) (export exempted)

1.3% FEC on payments abroad

Income and wage tax

May 6, 2013

Europe meets the America'sPwC 5

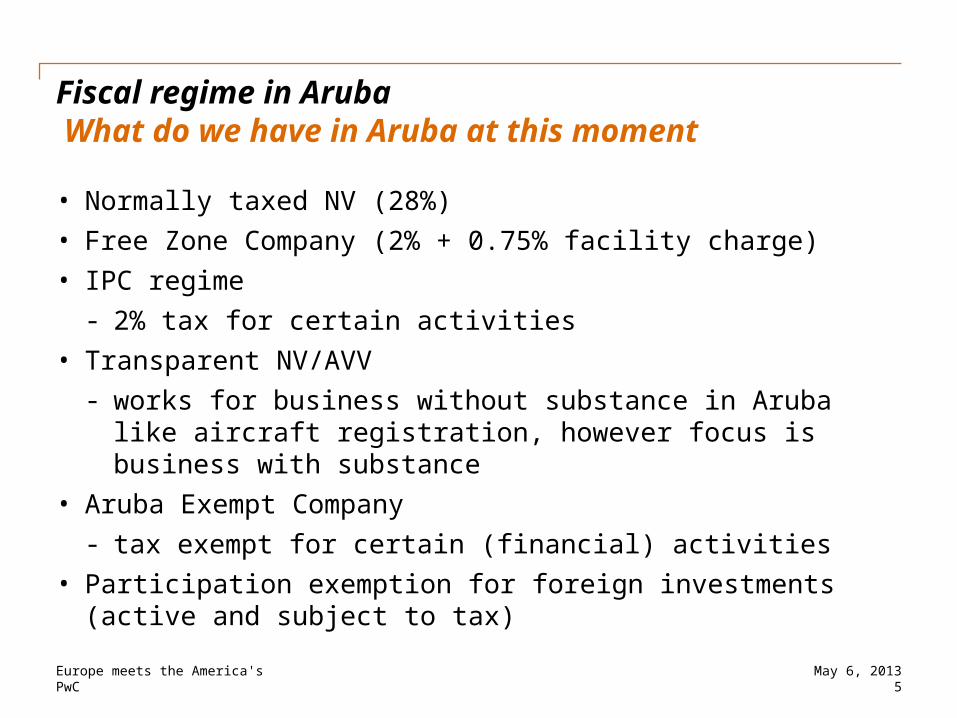

Fiscal regime in Aruba What do we have in Aruba at this moment

• Normally taxed NV (28%)• Free Zone Company (2% + 0.75% facility charge)• IPC regime

- 2% tax for certain activities• Transparent NV/AVV

- works for business without substance in Aruba like aircraft registration, however focus is business with substance

• Aruba Exempt Company- tax exempt for certain (financial) activities

• Participation exemption for foreign investments (active and subject to tax)

May 6, 2013

Europe meets the America's6PwC

Fiscal regime in Aruba Proposed legislation in Aruba

• Free Zone regime adjusted

- no dividend withholding tax

• Tax Zone San Nicolas

- 2%/10%/15% tax on profit

- no dividend withholding tax

- no FEC

• Expat regulation

- relief on high income tax for temporary employees from abroad

• IPC regime adjusted

- activities to be further determined

- profit tax rate of 10%/12%/15%

- no dividend withholding taxMay 6, 2013

Europe meets the America's7PwC

Possible structures in ArubaInbound Investment Structures

•Principal Sales Company

•Tolling Manufacturing Model

May 6, 2013

Europe meets the America's8PwC

Possible structures in Aruba Principal Sales Company

May 6, 2013

Europe meets the America'sPwC 9

Possible structures in Aruba Principal Sales Company

Objectives

• Concentrate profits in low tax jurisdiction: 2% profit tax, instead of higher percentage in your country

• Move all of the mayor sales activities and related risks into one principal sales company in Aruba

•Minimize scope of local foreign representatives

•Language, security, time zone and culture

May 6, 2013

Europe meets the America's10PwC

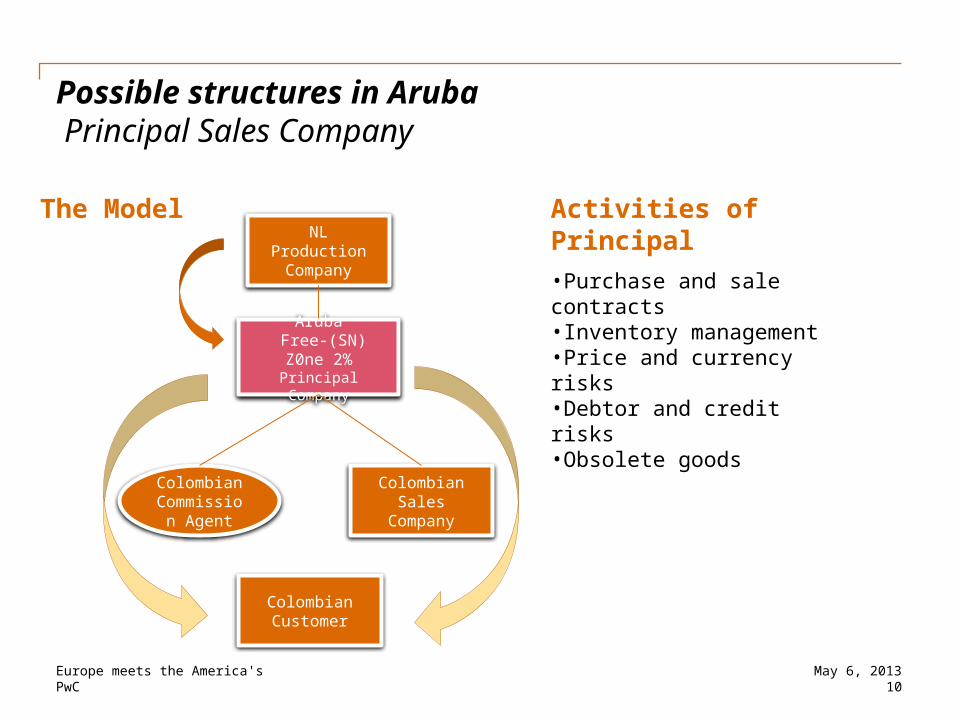

Possible structures in Aruba Principal Sales Company

Activities of Principal•Purchase and sale contracts•Inventory management•Price and currency risks•Debtor and credit risks•Obsolete goods

May 6, 2013

The ModelNL Production

Company

Aruba Free-(SN) Z0ne

2%Principal Company

ColombianCommissio

n Agent

Colombian Sales

Company

Colombian Customer

Europe meets the America's11PwC

Possible structures in Aruba Principal Sales Company

May 6, 2013

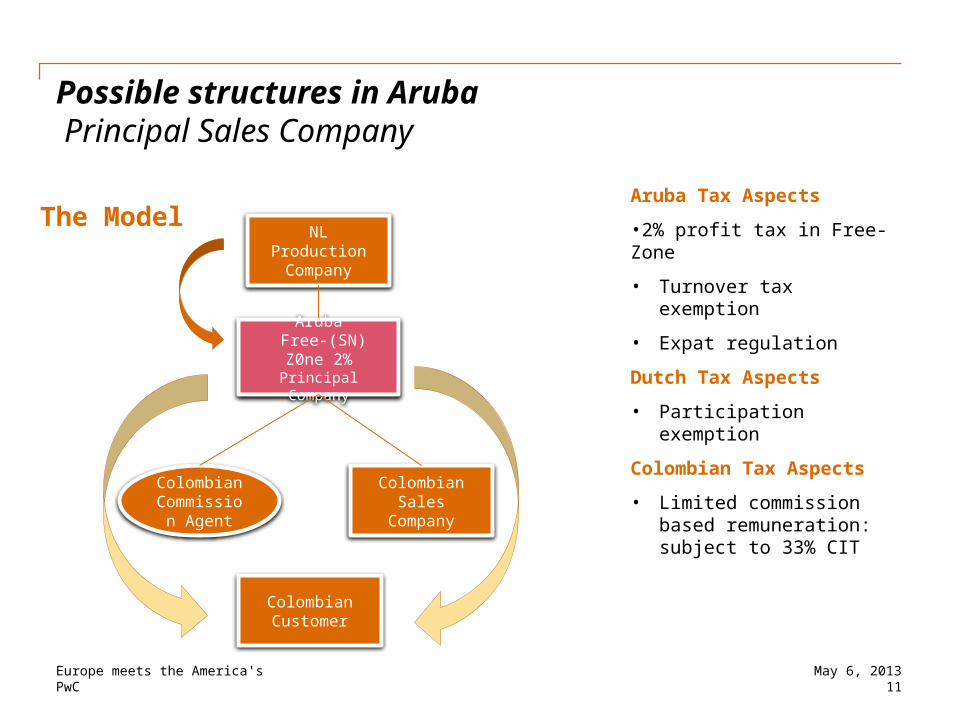

The ModelAruba Tax Aspects

•2% profit tax in Free-Zone

• Turnover tax exemption

• Expat regulation

Dutch Tax Aspects

• Participation exemption

Colombian Tax Aspects

• Limited commission based remuneration: subject to 33% CIT

NL ProductionCompany

Aruba Free-(SN) Z0ne

2%Principal Company

ColombianCommissio

n Agent

Colombian Sales

Company

Colombian Customer

Europe meets the America'sPwC 12

Possible structures in Aruba Principal Sales Company

Conditions and Characteristics

• Organize the model up front for new activities

• Substance requirements

• Adequate transfer pricing documentation to prevent double taxation

• If possible up front tax agreements confirming the transfer pricing policy, in particular in Principal jurisdiction

• The Principal jurisdiction: excellent reputation, low tax on profits, stable tax regime and beneficial expat taxation regulation

May 6, 2013

Europe meets the America's13PwC

Possible structures in Aruba Tolling Manufacturing Model

May 6, 2013

Europe meets the America'sPwC 14

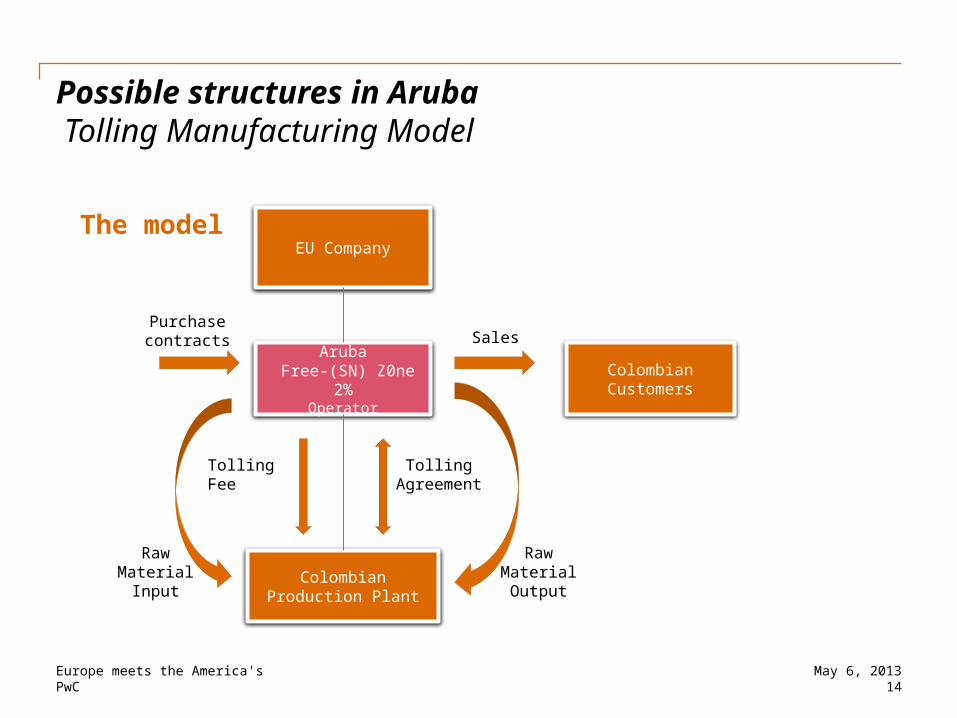

Possible structures in Aruba Tolling Manufacturing Model

May 6, 2013

EU Company

Aruba Free-(SN) Z0ne

2%Operator

Colombian Production Plant

Tolling Fee

Tolling Agreement

Colombian Customers

Sales

Purchase contracts

Raw Material

Input

Raw MaterialOutput

The model

Europe meets the America's15PwC

Possible structures in Aruba Tolling Manufacturing Model

Aruba Tax – Project Management

• 2% profit tax in Free-Zone

• Turnover tax exemption

• Expat regulation

• No WHT on tolling fee

Colombian Tax – Project Company

• Profit calculated on cost-plus basis and subject to 33% profit tax

May 6, 2013

Europe meets the America'sPwC 16

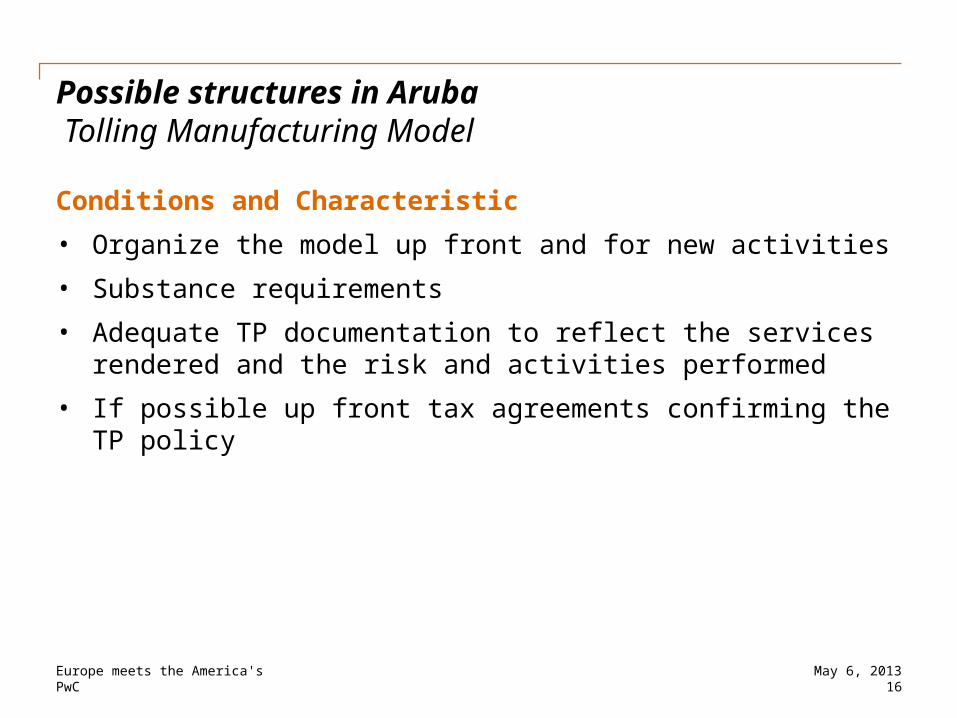

Possible structures in Aruba Tolling Manufacturing Model

Conditions and Characteristic

• Organize the model up front and for new activities

• Substance requirements

• Adequate TP documentation to reflect the services rendered and the risk and activities performed

• If possible up front tax agreements confirming the TP policy

May 6, 2013

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC Dutch Caribbean, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2013 PwC Dutch Caribbean. All rights reserved. In this document, “PwC” refers to PwC Dutch Caribbean which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

Sharing knowledge and creating value…

For more information please contact PwC Aruba:Hans Ruiter ([email protected])Rachel Vieira Maduro ([email protected])