Europe & Israel 1Q15 VC Trends Review

40

Venture Capital in Europe & Israel Venture Investment Data: First Quarter, 2015 Prepared by Gil Dibner @gdibner blog: yankeesabralimey Marsaxlokk Harbor, Malta, population 4,000

-

Upload

gil-dibner -

Category

Technology

-

view

5.564 -

download

0

Transcript of Europe & Israel 1Q15 VC Trends Review

Venture Capital in Europe & Israel Venture Investment Data: First Quarter, 2015

Prepared by Gil Dibner @gdibner blog: yankeesabralimey Marsaxlokk Harbor, Malta, population 4,000

The data • Around the middle of last year, I decided I wasn’t happy with available data sources on VC

rounds in Europe & Israel, and that I’d need to build my own • The data in this report consists entirely of data I’ve gathered manually based on publically

available, free sources • No paid data sources or API calls were harmed in the making of this dataset, every

investment was manually classified • This allows analysis of some aspects of the data I consider important – aspects that don’t

appear in other data sources • Seed investment is still under-reported, but I got a bit better at capturing it in the fourth

quarter. Rounds smaller than $500K are generally excluded from this analysis • The analysis is limited to ICT categories and excludes life sciences • The analysis excludes Turkey and FSU countries • I’m converting EUR and GBP into USD using monthly average exchange rates

2 @gdibner blog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

Monthly pace of venture investment • During the nine months

ended March, 2015, there were 596 reported venture investments across Europe & Israel

• A total of $6.487B was invested in Europe & Israel during this period, an average of $721M per month

• During these nine months, January, February, and March were each – in turn – record-breaking months

• March saw $998M invested across 103 rounds

@gdibner blog: yankeesabralimey 3

493565

644 625562

725

903971 998

42 30 50 79 73 5292 75 103

0

200

400

600

800

1,000

1,200

Jul Aug Sep Oct Nov Dec Jan Feb Mar

Qtr3 Qtr4 Qtr1

2014 2015

Num

ber o

f inv

estm

ents

VC Investments in Europe & Israel, July 2014 - March 2015

Invested amount (US $M) Number of investments

Syndicate for European & Israeli Enterprise Companies

Quarterly pace of venture investment • The first quarter of 2015 saw

a significant uptick in activity over the third and fourth quarters of 2014

• In 1Q15, over $2.8B was invested across 270 companies in Europe & Israel

4 @gdibner blog: yankeesabralimey

1,7031,912

2,872122

204

270

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

50

100

150

200

250

300

Qtr3 Qtr4 Qtr1

2014 2015

Amou

nt in

vest

ed (U

S $M

)

Num

ber o

f inv

estm

ents

VC Investments in Europe & Israel

Invested amount (US $M) Number of investments

Syndicate for European & Israeli Enterprise Companies

Mega-rounds skew the investment totals • This analysis breaks down VC

investments into brackets by size: • Seed (less than $2M) • Early venture ($2-8M) • Venture ($8-20M) • Growth ($20-100M) • Mega ($100M+)

• Five mega-rounds took place in Europe in the first quarter:

• Taboola, an Israeli content-recommendation company, raised $117M in February

• Sigfox, a French wireless network for IoT, raised $115M in February

• WorldRemit, a British money transfer company raised $100M in February

• Simplivity, an Israeli enterprise systems company, raised $175M in March

• Financial Force, a British ERP SaaS provider, raised $110M in March

• Even adjusting for mega-rounds, 1Q is still significantly above the previous two quarters

5 @gdibner blog: yankeesabralimey

98 57 92 121 120 102 85 82 118118

60168 109 76 127 169 226 161

171 342 26

366340 229

613

153

387

0

200

400

600

800

1,000

1,200

Jul Aug Sep Oct Nov Dec Jan Feb Mar

Qtr3 Qtr4 Qtr1

2014 2015

Amou

nt In

vest

ed (U

S $M

)

Pace of VC Investment in Europe and Israel

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8) Seed (.5-2)

Syndicate for European & Israeli Enterprise Companies

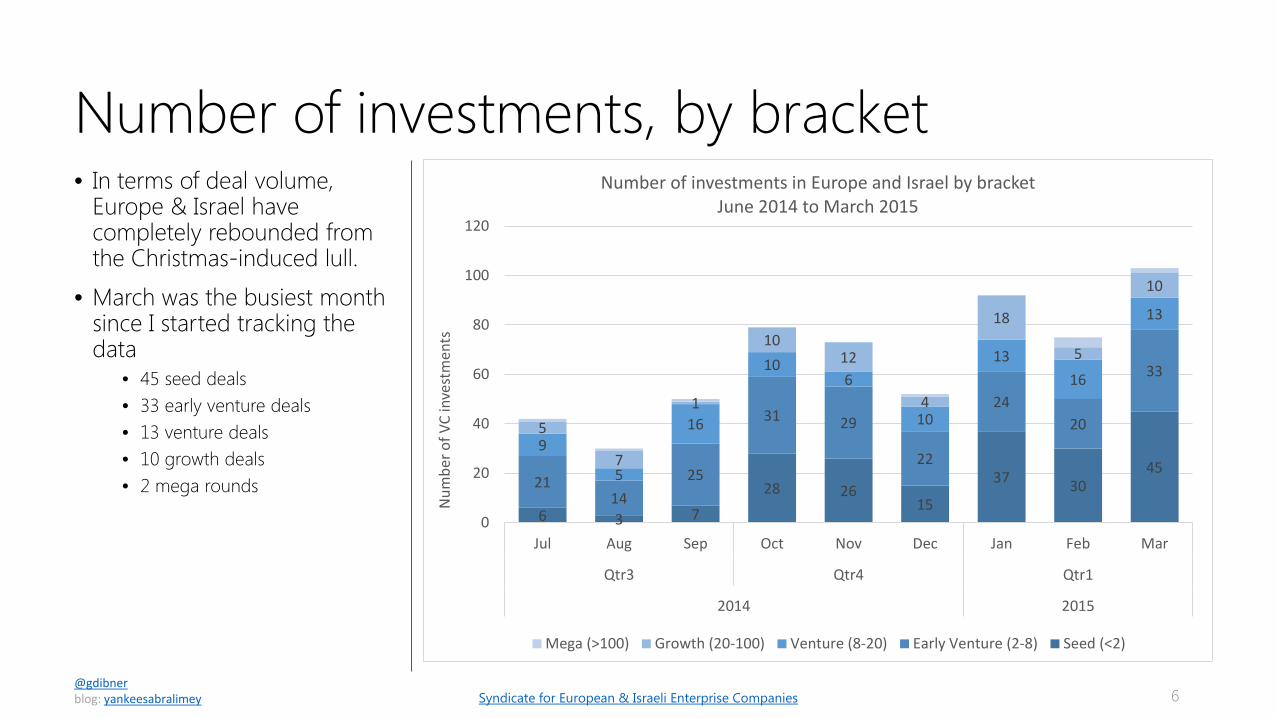

Number of investments, by bracket • In terms of deal volume,

Europe & Israel have completely rebounded from the Christmas-induced lull.

• March was the busiest month since I started tracking the data

• 45 seed deals • 33 early venture deals • 13 venture deals • 10 growth deals • 2 mega rounds

6 @gdibner blog: yankeesabralimey

6 3 7

28 2615

37 3045

2114

25

31 29

22

2420

33

9

5

16

106

10

1316

13

5

7

1

1012

4

18

5

10

0

20

40

60

80

100

120

Jul Aug Sep Oct Nov Dec Jan Feb Mar

Qtr3 Qtr4 Qtr1

2014 2015

Num

ber o

f VC

inve

stm

ents

Number of investments in Europe and Israel by bracketJune 2014 to March 2015

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8) Seed (<2)

Syndicate for European & Israeli Enterprise Companies

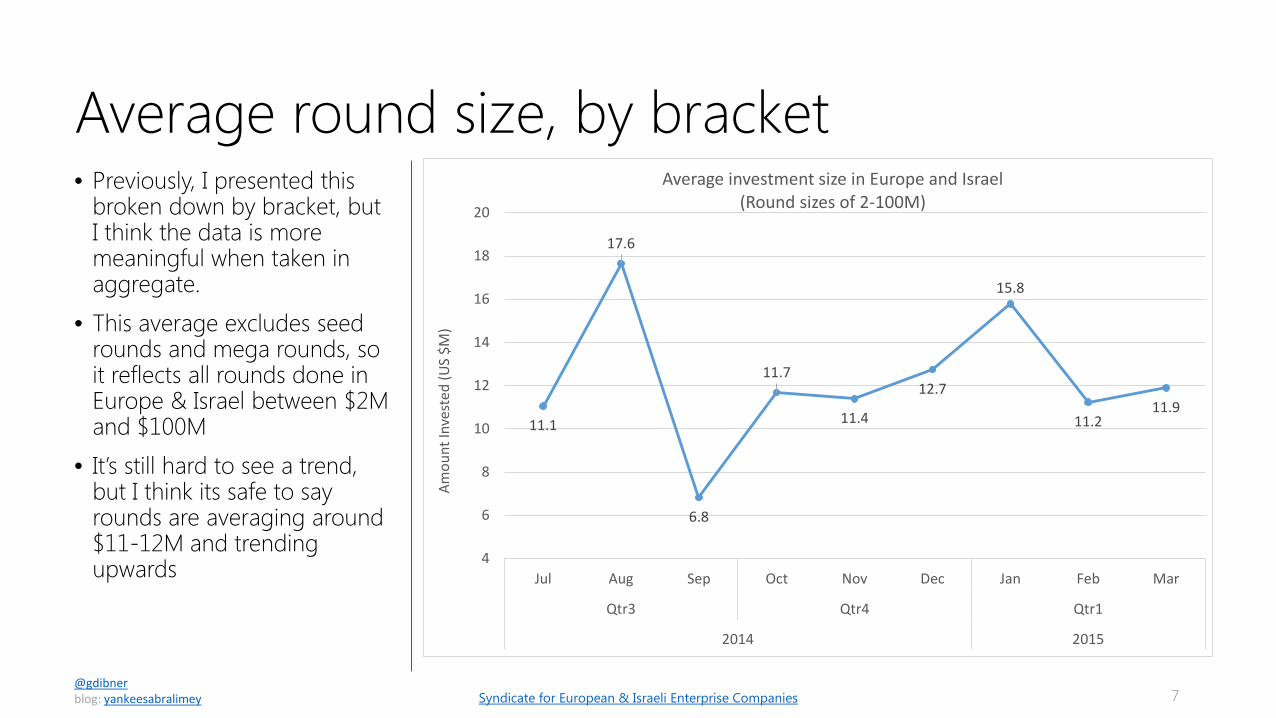

Average round size, by bracket • Previously, I presented this

broken down by bracket, but I think the data is more meaningful when taken in aggregate.

• This average excludes seed rounds and mega rounds, so it reflects all rounds done in Europe & Israel between $2M and $100M

• It’s still hard to see a trend, but I think its safe to say rounds are averaging around $11-12M and trending upwards

7 @gdibner blog: yankeesabralimey

11.1

17.6

6.8

11.7

11.4

12.7

15.8

11.211.9

4

6

8

10

12

14

16

18

20

Jul Aug Sep Oct Nov Dec Jan Feb Mar

Qtr3 Qtr4 Qtr1

2014 2015

Amou

nt In

vest

ed (U

S $M

)

Average investment size in Europe and Israel(Round sizes of 2-100M)

Syndicate for European & Israeli Enterprise Companies

Total venture investment by country, 2H 2014 • The UK overtook Israel to

regain its position as the country with the largest amount of VC activity in 1Q15

• Germany, France, and Sweden rounded out the rest of the top five

8 @gdibner blog: yankeesabralimey

930.1834.6

537.6233.0

88.952.750.6

38.934.3

23.417.2

7.85.43.83.42.72.51.31.00.90.90.60.3

UKIsrael

GermanyFrance

SwedenSpain

DenmarkNetherlandsSwitzerland

EstoniaFinland

BelgiumItaly

NorwayLatvia

IrelandPolandAustria

PortugalIcelandSerbia

LithuaniaGreece

0 100 200 300 400 500 600 700 800 900 1,000

Total VC investment volume by country, 1Q15 (US $M)

Syndicate for European & Israeli Enterprise Companies

Total venture investment by country, 3Q & 4Q 2014 • To get a better sense of VC

volumes in various countries, this analysis excludes mega-rounds

• UK venture activity skyrocketed in 1Q15, doubling that of 3Q14

• Investment volume in Israel stayed roughly flat from a record-breaking 4Q

• Investment volume in Germany continued to show strong increases

• France & Sweden both declined slightly, but France held on to its fourth place slot

9 @gdibner blog: yankeesabralimey

Israel, 315.2

Israel, 567.5

Israel, 542.6

UK, 369.0

UK, 262.9

UK, 720.1

Germany, 180.2

Germany, 284.4Germany, 388.6

France, 29.3

France, 163.3

France, 118.0Sweden, 74.4 Sweden, 123.2 Sweden, 88.9

Qtr3 Qtr4 Qtr10

100

200

300

400

500

600

700

800

Tota

l VC

inve

stm

ent (

US

$M)

Total VC investment, 3Q14 - 1Q15 (top 5 countries, excluding mega-rounds)

Syndicate for European & Israeli Enterprise Companies

Average venture round sizes, by country • Looking across all VC deals in

the second half of 2014, it’s possible to draw some conclusions about the funding environments in various countries

• This analysis excludes mega-rounds and rounds less than $2M

• UK & Ireland companies raised the largest round sizes on average in 1Q, a significant jump from 4Q

• DACH startups seem to raise consistently large rounds on average

10 @gdibner blog: yankeesabralimey

Benelux, 10.6

Benelux, 4.7

Benelux, 7.2

DACH, 18.0

DACH, 14.9DACH, 14.4

France, 3.7

France, 5.6

Iberia, 10.4

Iberia, 7.2

Iberia, 14.1

Israel, 11.6

Israel, 15.9

Israel, 12.1

Nordic, 7.7

Nordic, 11.5Nordic, 11.4

UK & Ireland, 11.9

UK & Ireland, 18.9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Qtr3 Qtr4 Qtr1

2014 2015

Aver

age

roun

d siz

e (U

S $M

)

Average investment size in Europe and Israel (rounds of $2-20M)

Syndicate for European & Israeli Enterprise Companies

Total venture investment by region, 3Q14 to 1Q15 • When VC investments across

Europe are aggregated into regions, Israel, DACH, UK & Ireland, the Nordics, and France are the clear and consistent leaders

• Benelux, Iberia, Southern Europe, and Eastern Europe do produce meaningful VC investments (Adyen, Prezi, and many others), but the volumes are still low

11 @gdibner blog: yankeesabralimey

Israel, 315.2Israel, 567.5

Israel, 834.6UK & Ireland, 399.0

UK & Ireland, 262.9

UK & Ireland, 932.8

DACH, 532.2 DACH, 290.2

DACH, 573.2

Nordic, 124.0 Nordic, 219.3

Nordic, 188.6

France, 129.3 France, 163.3

France, 233.0

Benelux, 284.9Iberia, 168.1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Qtr3 Qtr4 Qtr1

2014 2015

Tota

l VC

inve

stm

ent (

US

$M)

Total VC investment by region

Israel UK & IrelandDACH NordicFrance BeneluxIberia East. Eur.South. Eur.

Syndicate for European & Israeli Enterprise Companies

Rounds by bracket & country • To get a better sense of deal

volume, this analysis excludes seed deals which are often poorly reported

• Excluding seed deals, Israel led the region in the number of VC deals reported

• The UK and France followed • Interestingly, France and the

UK saw an equal number of early venture and growth deals, but the UK saw 13 “venture deals” compared to only 5 in France

12 @gdibner blog: yankeesabralimey

17 15 15 158

4

18

13

52

3

9

9

9

3

2

2

0

5

10

15

20

25

30

35

40

45

50

Israel UK &Ireland

DACH France Nordic Benelux Iberia East. Eur. South. Eur.

Num

ber o

f inv

estm

ents

Number of investments in Europe and Israel by bracket, 1Q 2015

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

Syndicate for European & Israeli Enterprise Companies

Investment by region, by bracket • In 1Q, UK & Ireland led in

terms of total VC dollars invested, even with mega-rounds included

• Israeli was in second place, DACH was third

• Excluding Sigfox’s $115M, France came in fifth; including it would catapult France ahead of the Nordics

13 @gdibner blog: yankeesabralimey

74 70 46 28 45

165 235

63 49

460226

308

82

210

292

149

115

0

100

200

300

400

500

600

700

800

900

1,000

UK &Ireland

Israel DACH Nordic France Iberia Benelux South. Eur. East. Eur.

Tota

l am

ount

inve

sted

(US

$M)

Investment in Europe and Israel by bracket by region, 1Q 2015(ranked excluding mega-rounds)

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8) Seed (<2)

Syndicate for European & Israeli Enterprise Companies

Participation rate of US VC firms, by bracket • US VC firms are increasingly

active in the European and Israeli VC markets

• Over the past nine months, US VC firms participated in 16% of the venture rounds in Europe

• US VCs participated in only 5% of seed rounds, 11% of early venture rounds, and 24% of venture rounds

• As a company moves from bracket to bracket, the chance of US VC participation doubles with each bracket change

14 @gdibner blog: yankeesabralimey

5% 11%24%

44%

80%

95% 89%76%

56%

20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Seed (.5-2) Early Venture (2-8) Venture (8-20) Growth (20-100) Mega (>100)

Tota

l am

ount

inve

sted

(US

$M)

Did US VC firms participate in European VC rounds? (3Q14-1Q15)

No Yes

Syndicate for European & Israeli Enterprise Companies

Rate of participation by US firms is declining • As the pace of European and

Israeli VC investment increased, the rate of participation by US firms did not keep pace

• Within rounds of between $2M and $20M, US VC participation dropped from 24% of rounds in October to just 11% of rounds in March

15 @gdibner blog: yankeesabralimey

10% 5%17%

24%17% 16% 19%

8% 11%

90% 95%83%

76%83% 84% 81%

92% 89%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul Aug Sep Oct Nov Dec Jan Feb Mar

Qtr3 Qtr4 Qtr1

2014 2015

Tota

l am

ount

inve

sted

(US

$M)

Did US VC firms participate in European VC rounds? (3Q14-1Q15)

No Yes

Syndicate for European & Israeli Enterprise Companies

Participation of US VC firms by country • In 1Q, US VCs firms were

active in 10 different European countries, down from 12 in 4Q

• US VC firms were most active in Israel, where they participated in 15 investment rounds

• The UK saw 10 investments with US VC participation, double the number in 4Q

16 @gdibner blog: yankeesabralimey

15 104

43 49

28

13 11 11 100

10

20

30

40

50

60

70

Isra

el UK

Germ

any

Spai

n

Denm

ark

Switz

erla

nd

Net

herla

nds

Swed

en

Irela

nd

Aust

ria

Num

ber o

f VC

inve

stm

ents

In which countries are US VCs most active?1Q, 2015

No US VC involved US VC involved

Syndicate for European & Israeli Enterprise Companies

Dimension Categories Explanation/Example

1. Target market Consumer, SMB, Enterprise, Government, Telecom, OEM

What sort of customer does the company target?

2. Vertical market

Adtech, Communications, Data, Development, Durables, Education, Electronics, Employment, Energy, Fashion, Financial, Food, Gaming, Health, HMI, Industrial, Infrastructure, Lifestyle, Logistics, Marketing, Media, Productivity, Real Estate, Security, Sports, Storage, Transportation, Travel, Water

What type of problem does the company solve?

3. Business model Commerce, Components, Content, Marketplace, SaaS, Semiconductors, Services, Software, Systems,

How does the company make money? What are customers paying for?

Combined segment descriptor Consumer + Travel + Marketplace AirBnB has built a travel-related marketplace for consumers 17

Three-dimensional approach to sector mapping

• The increase in venture investment activity was seen across both consumer and enterprise

• Consumer deal volume increased 65% from 4Q14 to 1Q15

• Enterprise deal volume increased only 20% during the same period

• SMB-oriented and OEM-oriented investment volume declined

18 @gdibner blog: yankeesabralimey

475 595980

494

794

951

78

133

122

78

114

47

0

500

1,000

1,500

2,000

2,500

Qtr3 Qtr4 Qtr1

2014 2015

Tota

l VC

inve

stm

ents

(US

$M)

European & Israeli venture financing by target market3Q14 to 1Q15 (in US $M)

Government

Telecom

OEM

SMB

Enterprise

Consumer

What target markets are attracting the most VC investment in Europe & Israel?

Syndicate for European & Israeli Enterprise Companies

• Last quarter ’s trend reversed itself, with consumer-oriented companies accounting for 43% of all VC investment in Europe & Israel, up from 31%

• Enterprise dropped from 55% to 47%

• Other categories declined, with SEM, OEM, and Government-oriented companies nearly disappearing from the deal volumes

19 @gdibner blog: yankeesabralimey

The return of consumer investment

54%

31%43%

29%55%

47%

5% 7%5%6%7%

0%10%20%30%40%50%60%70%80%90%

100%

Qtr3 Qtr4 Qtr1

2014 2015

Tota

l VC

inve

stm

ents

(US

$M)

European & Israeli venture financing by target market3Q14 to 1Q15 (in US $M)

Government Telecom OEM SMB Enterprise Consumer

Syndicate for European & Israeli Enterprise Companies

Breakdown by region & target market • The Israeli VC landscape

continued to be dominated by non-consumer companies

• The DACH region saw a return to the dominance of consumer-oriented companies in VC financing

• Sigfox’s massive round meant that the majority of VC dollars flowing into France went into the telecom space – clearly an anomaly

• The Nordics seemed to echo Israel’s emphasis on enterprise

• UK dealflow was split almost evenly

20 @gdibner blog: yankeesabralimey

464

80

504

55 50

407

670

64

80122

60

46

115

0

100

200

300

400

500

600

700

800

900

1,000

UK & Ireland Israel DACH France Nordic Iberia Benelux

Tota

l am

ount

inve

sted

(US

$M)

Investment in Europe and Israel by target market by country1Q, 2015 (US $M)

Government Telecom OEM SMB Enterprise Consumer

Syndicate for European & Israeli Enterprise Companies

Distribution of investment rounds by country • Across Europe & Israel, 47%

of VC investment rounds were in consumer companies in 1Q, up from 41% in 4Q

• Israel and Nordics were the only geographies to see a majority of investment rounds happen into non-consumer companies – for Israel that’s normal, for the Nordic’s it’s a reversal

• Most other European markets saw 50-60% of rounds go into consumer companies

21 @gdibner blog: yankeesabralimey

26%

37%

52%

53%

56%

57%

67%

76%

100%

60%

47%

36%

29%

39%

41%

33%

18%

7%

9%

12%

3%

3%

6%

5%

7%

6%

6%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Israel

Nordic

France

Benelux

UK & Ireland

DACH

South. Eur.

Iberia

East. Eur.

Investment in Europe and Israel by target market by country1Q 2015 (Number of investments)

Consumer Enterprise SMB OEM Telecom Government

Syndicate for European & Israeli Enterprise Companies

Seed and growth swing back to consumer • Unlike last quarter, a clear

majority of both growth deals and seed deals were in consumer-oriented companies

22 @gdibner blog: yankeesabralimey

59%

44%

43%

66%

31%

47%

57%

28%

5%

5%

6%

4%

4%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Seed (<2)

Early Venture (2-8)

Venture (8-20)

Growth (20-100)

Investment in Europe (excluding Israel) by target market by stage bracket 1Q 2015 (Number of investments)

Consumer Enterprise SMB OEM Government

Syndicate for European & Israeli Enterprise Companies

DACH investors shift back to consumer • DACH is clearly a region with

a record of strong consumer-oriented investment

• In 4Q14 this began to change, but this trend may not be long-lived

• 1Q15 saw a majority of investments in DACH go into consumer companies

23 @gdibner blog: yankeesabralimey

100%

67%60%

40%

13%

57% 60%

33%

73%

17%20%

40%88%

43% 40%

67%

20%20%

10%

7%17%

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

Investment in DACH by target market by stage bracketJuly 2014 to March 2015 (Number of investments)

OEM SMB Enterprise Consumer

Syndicate for European & Israeli Enterprise Companies

The Nordics shift towards the enterprise… • The Nordic region saw pretty

diverse investment patterns in 3Q14 and 4Q14, but in 1Q15 there was a clear shift towards the enterprise

• Interestingly, but not surprisingly, OEM-oriented deals seemed to disappear from the landscape almost entirely

24 @gdibner blog: yankeesabralimey

40%25%

67%

83%

50%64%

20%

50%38%

60%

50%

17%42%

27%

60%

50%

38%

8%

10% 14%25%

17% 17%9% 10% 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

Investment in the Nordics by target marketJuly 2014 to March 2015 (Number of investments)

OEM SMB Enterprise Consumer

Syndicate for European & Israeli Enterprise Companies

…especially in terms of dollars invested • When we look at dollars

investment as opposed to the number of investments, the trend in the Nordics is even clearer

• Interestingly, but not surprisingly, OEM-oriented deals seemed to disappear from the landscape almost entirely (from 40% in August to just 4% in March)

25 @gdibner blog: yankeesabralimey

32%

11%

72% 75%

44%52%

44%

20%12%

68%

49%

6%55%

24%54%

80%

72%

12%

40%

21% 25% 24%

4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

Investment in the Nordics by target marketJuly 2014 to March 2015 (Total US $M invested)

OEM SMB Enterprise Consumer

Syndicate for European & Israeli Enterprise Companies

About 40% of French VC deals were enterprise… • In France, the ratio of

enterprise deals to consumer deals seems roughly constant from September 2014 to March 2015

26 @gdibner blog: yankeesabralimey

100% 100%

50% 46% 58%

50% 62% 60%

46%

38% 38%

33% 50% 31% 40%

46%

15% 8% 13% 8% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul Aug Sep Oct Nov Dec Jan Feb Mar

Qtr3 Qtr4 Qtr1

2014 2015

VC Investment in France by target market July 2014 to March 2015 (Number of investments)

OEM SMB Enterprise Consumer

Syndicate for European & Israeli Enterprise Companies

…but money increasingly flows to enterprise • When the data is presented

by the amount of dollars, it becomes clear that more and more of French VC dollars are flowing towards enterprise-oriented companies

27 @gdibner blog: yankeesabralimey

100% 100%

59%44%

65%77%

33% 31%19%

23%46% 10%

23%

64% 69%

74%

10%25%

18%3% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

VC Investment in France by target marketJuly 2014 to March 2015 (Number of investments)

OEM SMB Enterprise Consumer

Syndicate for European & Israeli Enterprise Companies

• 4Q saw a reshuffling of popular verticals

• Market, lifestyle, adtech and infrastructure were the most often funded verticals across Europe & Israel

• Finance dropped to the fifth slot

28 @gdibner blog: yankeesabralimey

Marketing displaced finance as the top vertical

Marketing, 20

Lifestyle, 18

Adtech, 17Infrastructure, 17 Financial, 15

Electronics, 14

Employment, 13

Security, 11

Travel, 11

Communications, 10

Productivity, 10

Development, 10

Health, 10

Logistics, 10Data, 9

Education, 9Fashion, 9Payments, 6Gaming, 5

ERP, 5

European & Israeli venture financing by target market1Q 2015 (number of investments)

Syndicate for European & Israeli Enterprise Companies

• Enterprise and SMB marketing companies were the most popular category of investment across Europe & Israel

• Various consumer lifestyle companies were the second-most popular category

• Adtech, despite falling dramatically out of favor in the US, took the third slot

• Infrastructure companies (mostly for the enterprise) took the fourth slot

• Fintech was dominated by consumer companies

29 @gdibner blog: yankeesabralimey

Health

Development

Productivity

Logistics

Communicati…

Security

Travel

Employment

Electronics

Financial

Infrastructure

Adtech

Lifestyle

Marketing

0 5 10 15 20 25

European & Israeli venture financing by target market1Q, 2015 (number of investments, top 10 verticals)

ConsumerEnterpriseSMBOEMTelecomGovernment

Which verticals for which segments?

Syndicate for European & Israeli Enterprise Companies

• Not surprisingly, enterprise infrastructure and security were the most popular categories for investment in Israel

• Adtech took the third spot • Consumer communications

companies and enterprise marketing companies were two other popular categories

30 @gdibner blog: yankeesabralimey

A closer look at Israeli venture in 1Q15

Health

Education

ERP

Lifestyle

Payments

Financial

Development

Marketing

Productivity

Communications

Adtech

Security

Infrastructure

0 1 2 3 4 5 6 7 8 9

Israeli venture financing by target market1Q, 2015 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

Telecom

Syndicate for European & Israeli Enterprise Companies

• In 1Q15, the most popular vertical in the UK was consumer fintech

• Adtech was the second most popular vertical

• Consumer fashion and consumer durables were also popular categories for UK VCs in 1Q

31 @gdibner blog: yankeesabralimey

Consumer fintech led the UK

Infrastructure

Lifestyle

Logistics

Music

Marketing

Security

Real Estate

Communications

Durables

Travel

Fashion

Employment

Health

Adtech

Financial

0 1 2 3 4 5 6 7

UK venture financing by target market1Q, 2015 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

Syndicate for European & Israeli Enterprise Companies

• In terms of dollars invested during 1Q15, services (31%) and commerce (18%) were the leaders

• Software and SaaS came in third and fourth, respectively

• Marketplace business models took fourth place, with 10% of invested capital

• Physical products (systems, components, and semiconductors) accounted for only 4% of total investment combined, down from 14% in 4Q14

32 @gdibner blog: yankeesabralimey

Services, 666, 31% Commerce, 389, 18%

Software, 374, 18%

SaaS, 332, 16%

Marketplace, 206, 10%

Media, 57, 3%

Systems, 49, 2%

Components, 18, 1%

Semiconductors, 15, 1%

European & Israeli venture financing by target market1Q, 2015 (in US $M) (excluding mega-rounds)

Service models led the pack in 1Q

Syndicate for European & Israeli Enterprise Companies

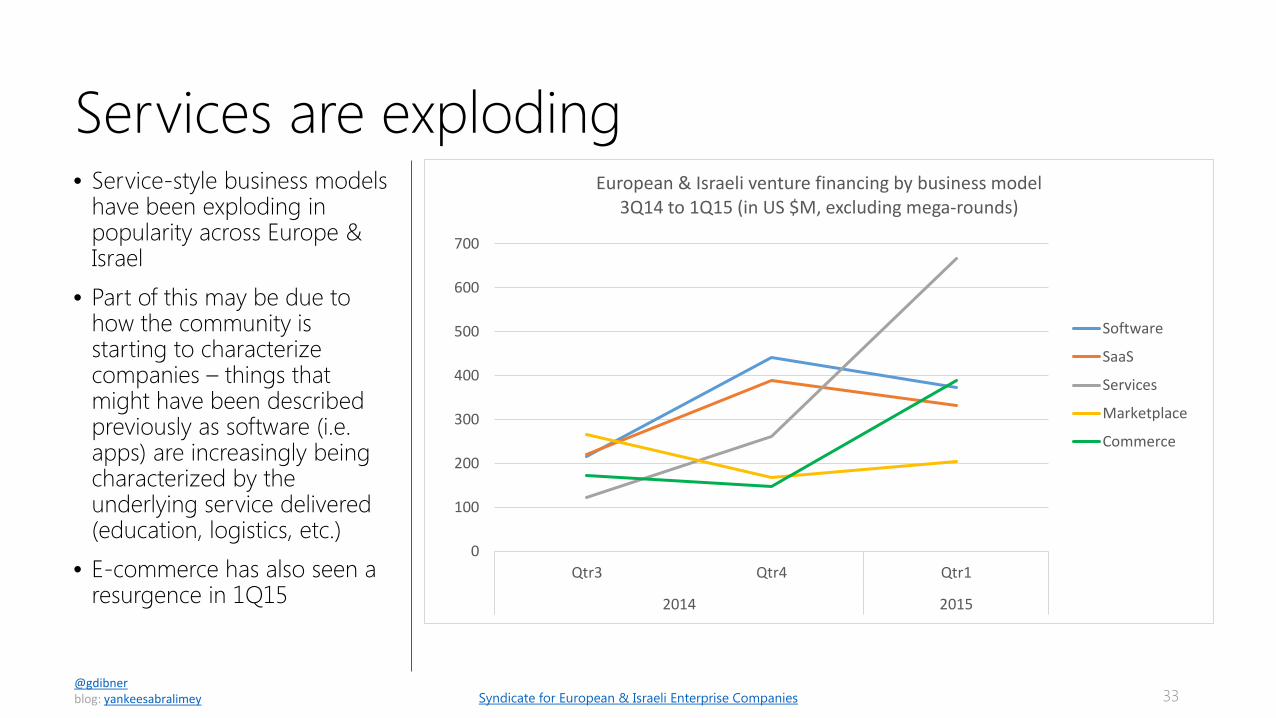

• Service-style business models have been exploding in popularity across Europe & Israel

• Part of this may be due to how the community is starting to characterize companies – things that might have been described previously as software (i.e. apps) are increasingly being characterized by the underlying service delivered (education, logistics, etc.)

• E-commerce has also seen a resurgence in 1Q15

33 @gdibner blog: yankeesabralimey

Services are exploding

0

100

200

300

400

500

600

700

Qtr3 Qtr4 Qtr1

2014 2015

European & Israeli venture financing by business model3Q14 to 1Q15 (in US $M, excluding mega-rounds)

Software

SaaS

Services

Marketplace

Commerce

Syndicate for European & Israeli Enterprise Companies

US VCs focused on SaaS, software, and services • US VC firms investing in

Europe & Israel continued to focus mainly on SaaS, software, and services

• Last quarter, no commerce-oriented companies in Europe or Israel attracted US VC interest – this quarter US VCs backed five companies in that category

• Components, and semiconductors attracted almost no interest from local VCs, and no interest at all from US VCs

• Marketplaces attracted US VCs in only two cases

34 @gdibner blog: yankeesabralimey

12 11 7 5 2 2

46 47 54

17 25 2118

0

10

20

30

40

50

60

70

Services Software SaaS Commerce Marketplace Systems Media Components Semiconductors

VC Investments in Europe & Israel1Q, 2015 (number of investments)

No US VC involved US VC involved

Syndicate for European & Israeli Enterprise Companies

• Enterprise marketing SaaS was the most popular segment for VC investment in 1Q15 with 17 investments across the region

• Consumer electronics systems was the second most popular segment, with 11 investments

• The UK was the clear leader in consumer financial services.

• Israel completely dominated the enterprise security software segment

35 @gdibner blog: yankeesabralimey

0 2 4 6 8 10 12 14 16 18

Consumer Employment Marketplace

Enterprise Development SaaS

Enterprise Infrastructure Software

Enterprise Development Software

Enterprise Adtech Services

Enterprise Data Software

Consumer Lifestyle Commerce

Consumer Lifestyle Media

Enterprise Employment SaaS

Consumer Fashion Commerce

Consumer Education Services

Enterprise Security Software

Consumer Financial Services

Consumer Electronics Systems

Enterprise Marketing SaaS

Number of VC investments

Investment in Europe & Israel by segment by country1Q15 (segments with 5 or more investments)

UK & Ireland IsraelNordic DACHFrance BeneluxIberia South. Eur.East. Eur.

Enterprise marketing & consumer electronics

Syndicate for European & Israeli Enterprise Companies

• Across Europe & Israel, US VC firms invested in 21 enterprise companies, 11 consumer companies, and 1 SMB company

• In the consumer space, US VC interest was concentrated on UK services companies and DACH commerce companies

36 @gdibner blog: yankeesabralimey

0 1 2 3 4 5 6 7 8 9 10

SaaS

Media

Commerce

Services

Marketplace

Systems

SaaS

Services

Software

SMB

Cons

umer

Ente

rpris

e

US VC Investments in Europe and Israel by end market, business model, & country, 1Q 2014

Israel

UK & Ireland

DACH

Iberia

Nordic

What business models attract US VC investments?

Syndicate for European & Israeli Enterprise Companies

Focus on dev tools: everywhere you look • Over the past nine months,

22 dev tooling companies raised VC money across Europe & Israel

• These companies were distributed across ten countries

• Israel led the pack with 6; UK and the Netherlands each saw 3, Germany and Estonia each saw 2

37 @gdibner blog: yankeesabralimey

0

1

2

3

4

5

6

7

Jul Sep Oct Nov Dec Jan Feb Mar

2014 2015

Num

nber

of i

nves

tmen

t

Development tools VC investment in Europe and Israel3Q14 to 1Q15, Number of investments

Ireland France Latvia Norway Sweden

Estonia Germany Netherlands UK Israel

Syndicate for European & Israeli Enterprise Companies

Focus on services: what’s behind the boom • 49 services-oriented

companies raised VC financing across Europe & Israel in 1Q15

• Finance, education, and communications were the most popular verticals for consumer-oriented services companies

• Adtech was the only services vertical with significant enterprise investment

38 @gdibner blog: yankeesabralimey

0 2 4 6 8 10 12 14

Entertainment

Lifestyle

Social

Music

Infrastructure

Logistics

Payments

Communications

Adtech

Education

Financial

Services-oriented VC investment in Europe and Israelby vertical and target market, 1Q 2015 (top 10 verticals)

Consumer Enterprise SMB Telecom

Syndicate for European & Israeli Enterprise Companies

Focus on enterprise SaaS: verticals by country • Marketing remained in the

top spot within enterprise SaaS, but data dropped from second place to fifth

• Employment and HR-related SaaS offerings were the second-most popular category within enterprise SaaS

• Development tooling SaaS offerings were the third most popular category

• Enterprise infrastructure, the fourth most popular category, saw only Israeli companies get funded

39 @gdibner blog: yankeesabralimey

0 5 10 15 20

LogisticsProductivity

TravelCRM

CommunicationsSecurity

HealthDataERP

AdtechInfrastructureDevelopmentEmployment

Marketing

Enterprise SaaS VC investment in Europe and Israelby vertical by country, 1Q 2015 (number of investments)

Israel FranceUK GermanyDenmark EstoniaSweden NetherlandsLithuania NorwayAustria Ireland

Syndicate for European & Israeli Enterprise Companies

Based in , I was previously a partner at . Before that, I helped run the European seed program for . I moved to London after seven years in during which I worked as a VC with and . I’m originally from . My VC investments include and . Angel investments include and three more that haven’t been announced yet. If you found this useful, I hope you’ll subscribe to my blog.

40

Gil Dibner To invest in the best European & Israeli enterprise startups,

consider backing me on here. Lots of exciting stuff in the

pipeline – and you’ll be in pretty good company.