Europe: Energy: Oil & Gas - E&P

60

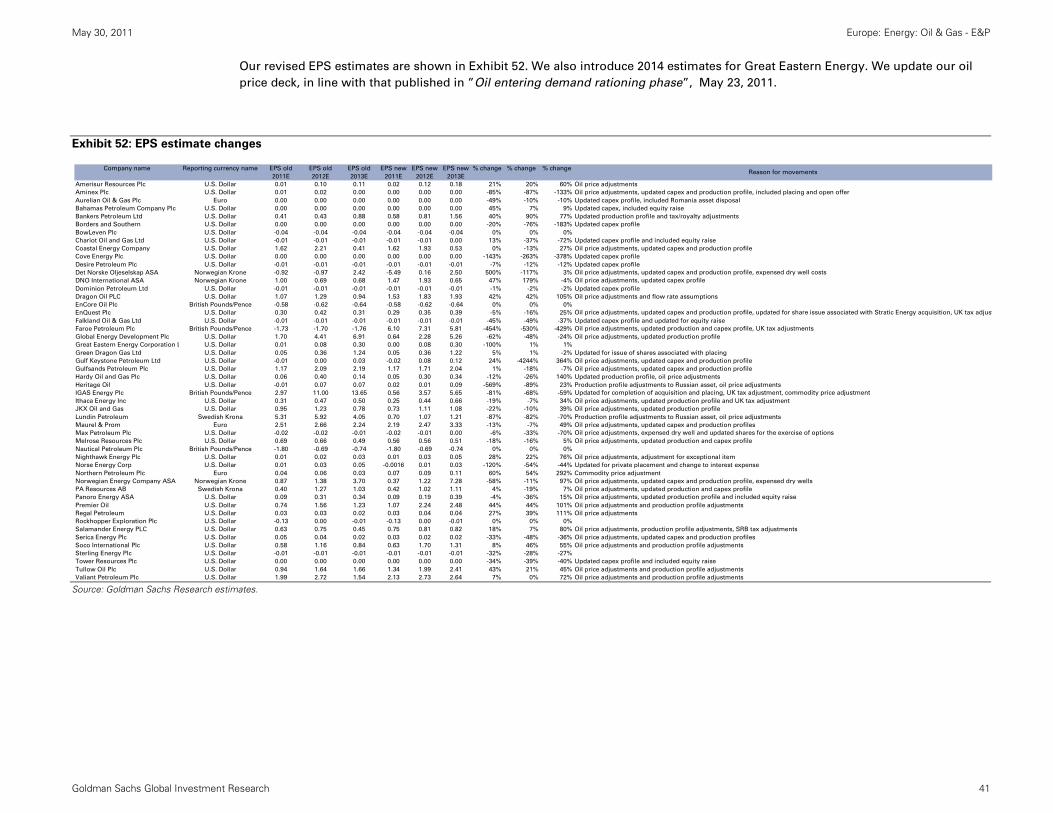

May 30, 2011 Europe: Energy: Oil & Gas - E&P Equity Research 5 themes and 17 companies to generate alpha in an industry in transformation E&P - seek exposure to five key themes We highlight five themes that we believe will drive share price performance in the E&P sector; high-impact, frontier exploration; unconventional gas; unconventional liquids; explorers with a strong core value; and NOC-driven M&A. We highlight 17 companies that we believe provide the most attractive exposure to these themes. Frontier exploration increasingly attractive We highlight five E&P stocks with high re-rating potential from exploration in new basins. We expect the majors and NOCs to show increasing appetite for these types of assets after a decade of poor exploration performance. Unconventional gas in deficit markets Increasing gas prices and new technical advances benefit unconventional gas producers in countries fighting for less dependency on foreign gas imports. Stocks we believe will benefit from this theme include Conviction Buy Aurelian. Unconventional liquids Technological progress being made in established unconventional liquid/oil shale plays in the US could be levered to new basins and countries; we highlight two stocks that should benefit from this trend, including Conviction Buy Panoro. Balanced exploration We identify five stocks with high-impact exploration supported by core values that mitigate downside risk of exploration failure. Bowleven and Rockhopper (Conviction Buys) screen well. NOC-driven M&A We see NOCs as the most price-insensitive buyers and believe that high materiality and exposure to new technologies drive such activity. Rating changes We upgrade Noreco and Maurel and Prom to Buy (from Neutral). We upgrade DNO and Encore Oil to Neutral (Sell). We downgrade Salamander, Det Norske and Coastal Energy to Neutral (Buy), and downgrade Premier to Sell (Neutral). ACTION RATINGS & UPSIDE TO 12-MONTH PRICE TARGETS Source: Datastream, Goldman Sachs Research estimates. Coverage View: Attractive Christophor Jost +44(20)7774-0014 [email protected] Goldman Sachs International The Goldman Sachs Group, Inc. does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification, see the end of the text. Other important disclosures follow the Reg AC certification, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S. Ruth Brooker +44(20)7774-6842 [email protected] Goldman Sachs International Michele della Vigna, CFA +44(20)7552-9383 [email protected] Goldman Sachs International Henry Tarr +44(20)7552-5981 [email protected] Goldman Sachs International The Goldman Sachs Group, Inc. Global Investment Research Upside to TP Market Cap (USDmn) Conviction Buy Rockhopper 241% 901 Aurelian 181% 411 Panoro 154% 261 Bowleven 107% 1074 Buy Global Energy Development 189% 37 BPC 168% 316 Northern Petroleum 164% 173 Max Petroleum 159% 164 Falkland Oil & Gas 140% 192 PA Resources 132% 418 Nighthawk Energy 125% 36 Dominion 117% 146 Igas 117% 187 Nautical Petroleum 112% 470 Cove Energy 108% 691 Aminex Plc 104% 100 Great Eastern Energy 97% 771 Borders and Southern 96% 392 Noreco 96% 523 Green Dragon 95% 1718 Maurel & Prom 89% 2604 Bankers Petroleum 89% 1950 Sell Premier Oil 22% 3578 Hardy Oil 22% 241 Lundin Petroleum 14% 4315

Transcript of Europe: Energy: Oil & Gas - E&P

May 30, 2011

Europe: Energy: Oil & Gas - E&P

Equity Research

5 themes and 17 companies to generate alpha in an industry in transformation

E&P - seek exposure to five key themes

We highlight five themes that we believe will

drive share price performance in the E&P sector;

high-impact, frontier exploration; unconventional

gas; unconventional liquids; explorers with a

strong core value; and NOC-driven M&A. We

highlight 17 companies that we believe provide

the most attractive exposure to these themes.

Frontier exploration increasingly attractive

We highlight five E&P stocks with high re-rating

potential from exploration in new basins. We

expect the majors and NOCs to show increasing

appetite for these types of assets after a decade of

poor exploration performance.

Unconventional gas in deficit markets

Increasing gas prices and new technical advances

benefit unconventional gas producers in countries

fighting for less dependency on foreign gas

imports. Stocks we believe will benefit from this

theme include Conviction Buy Aurelian.

Unconventional liquids

Technological progress being made in established

unconventional liquid/oil shale plays in the US

could be levered to new basins and countries; we

highlight two stocks that should benefit from this

trend, including Conviction Buy Panoro.

Balanced exploration

We identify five stocks with high-impact

exploration supported by core values that mitigate

downside risk of exploration failure. Bowleven

and Rockhopper (Conviction Buys) screen well.

NOC-driven M&A

We see NOCs as the most price-insensitive buyers

and believe that high materiality and exposure to

new technologies drive such activity.

Rating changes

We upgrade Noreco and Maurel and Prom to Buy

(from Neutral). We upgrade DNO and Encore Oil

to Neutral (Sell). We downgrade Salamander, Det

Norske and Coastal Energy to Neutral (Buy), and

downgrade Premier to Sell (Neutral).

ACTION

RATINGS & UPSIDE TO 12-MONTH PRICE TARGETS

Source: Datastream, Goldman Sachs Research estimates.

Coverage View: Attractive

Christophor Jost +44(20)7774-0014 [email protected] Goldman Sachs International

The Goldman Sachs Group, Inc. does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification, see the end of the text. Other important disclosures follow the Reg AC certification, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

Ruth Brooker +44(20)7774-6842 [email protected] Goldman Sachs International Michele della Vigna, CFA +44(20)7552-9383 [email protected] Goldman Sachs International

Henry Tarr +44(20)7552-5981 [email protected] Goldman Sachs International

The Goldman Sachs Group, Inc. Global Investment Research

Upside to TP Market Cap (USDmn)Conviction BuyRockhopper 241% 901Aurelian 181% 411Panoro 154% 261Bowleven 107% 1074BuyGlobal Energy Development 189% 37BPC 168% 316Northern Petroleum 164% 173Max Petroleum 159% 164Falkland Oil & Gas 140% 192PA Resources 132% 418Nighthawk Energy 125% 36Dominion 117% 146Igas 117% 187Nautical Petroleum 112% 470Cove Energy 108% 691Aminex Plc 104% 100Great Eastern Energy 97% 771Borders and Southern 96% 392Noreco 96% 523Green Dragon 95% 1718Maurel & Prom 89% 2604Bankers Petroleum 89% 1950SellPremier Oil 22% 3578Hardy Oil 22% 241Lundin Petroleum 14% 4315

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 2

Table of contents

Five themes to play in the E&P sector 3

Frontier exploration set to be a major theme in late 2011/early 2012. Industry appetite for frontier exploration provides additional benefits for explorers. 5

Rising gas prices, energy security and production ramp-ups to drive outperformance in unconventional gas 10

Unconventional liquids – de-risking of assets and potential M&A the key driver 15

Free exploration options remain a compelling investment case 18

M&A – Materiality and technical access a further potential driver of NOC activity 19

Thematic summary for E&P universe 21

Oil price sensitivity and the E&Ps; higher fiscal risk, but lower commercial thresholds; maintaining US$100/bl in our valuations 22

E&P screens; updating target prices and ratings 27

Medium-term exploration & balanced explorers still top performing exploration screens 34

Portfolio update for the E&Ps 38

North Sea performance weak on tax change; Falklands and Kurdistan remain weak 40

Maurel & Prom (MAUP.PA): Core value and ‘free’ exploration exposure; up to Buy 43

Noreco (NOR.OL): Core value combined with ‘free’ Norwegian exploration option; Buy 44

Premier Oil (PMO.L): Company’s strengths already in the price, down to Sell. 45

DNO international (DNO.OL): Underperformance & political de-risking of KRG, Neutral 46

Salamander Energy (SMDR.L): Downgrading to Neutral after recent outperformance 48

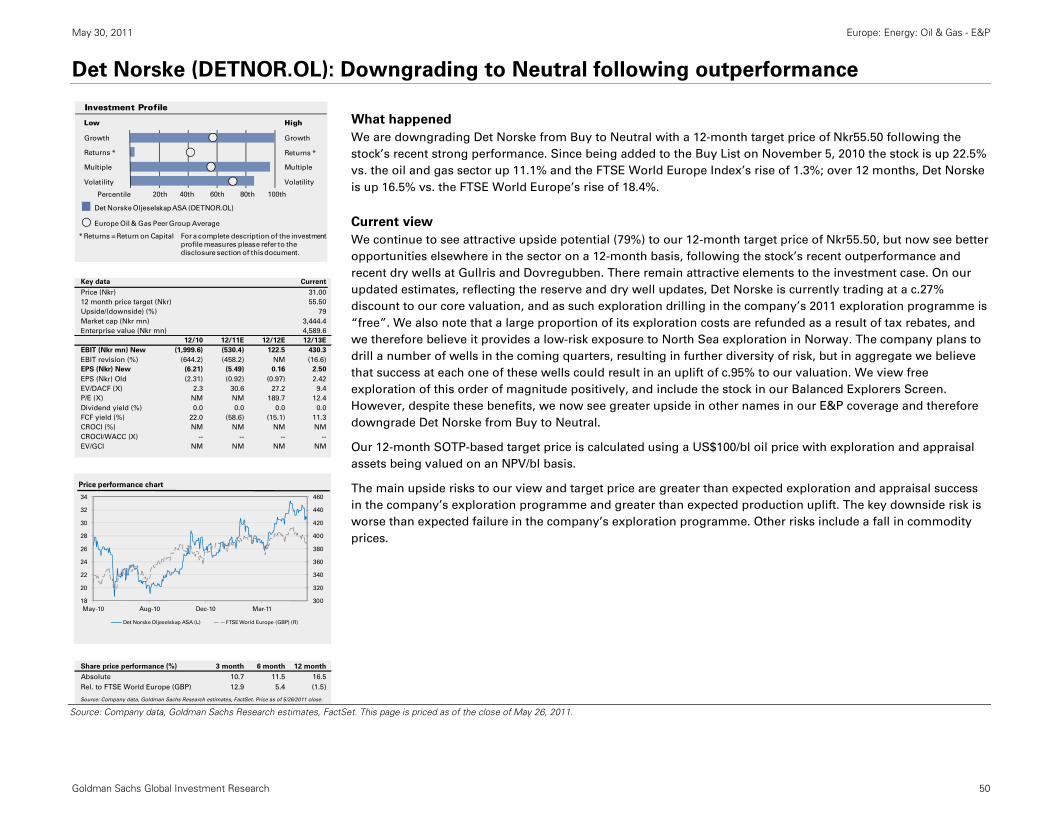

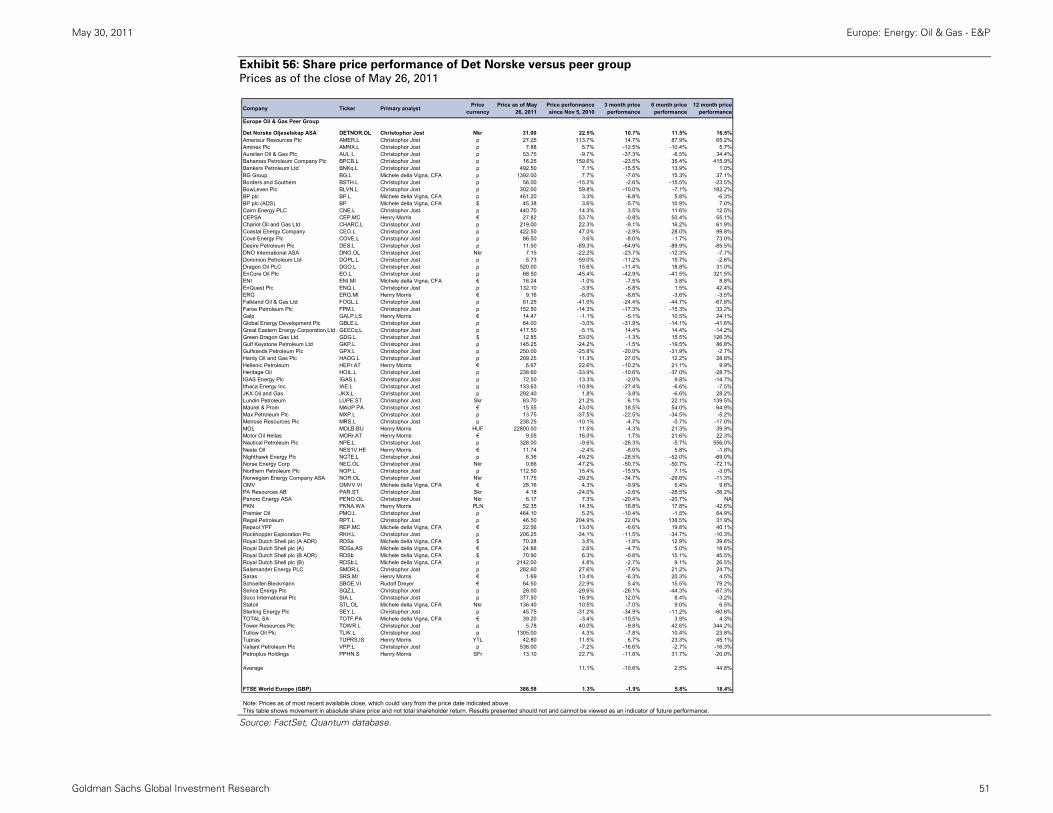

Det Norske (DETNOR.OL): Downgrading to Neutral following outperformance 50

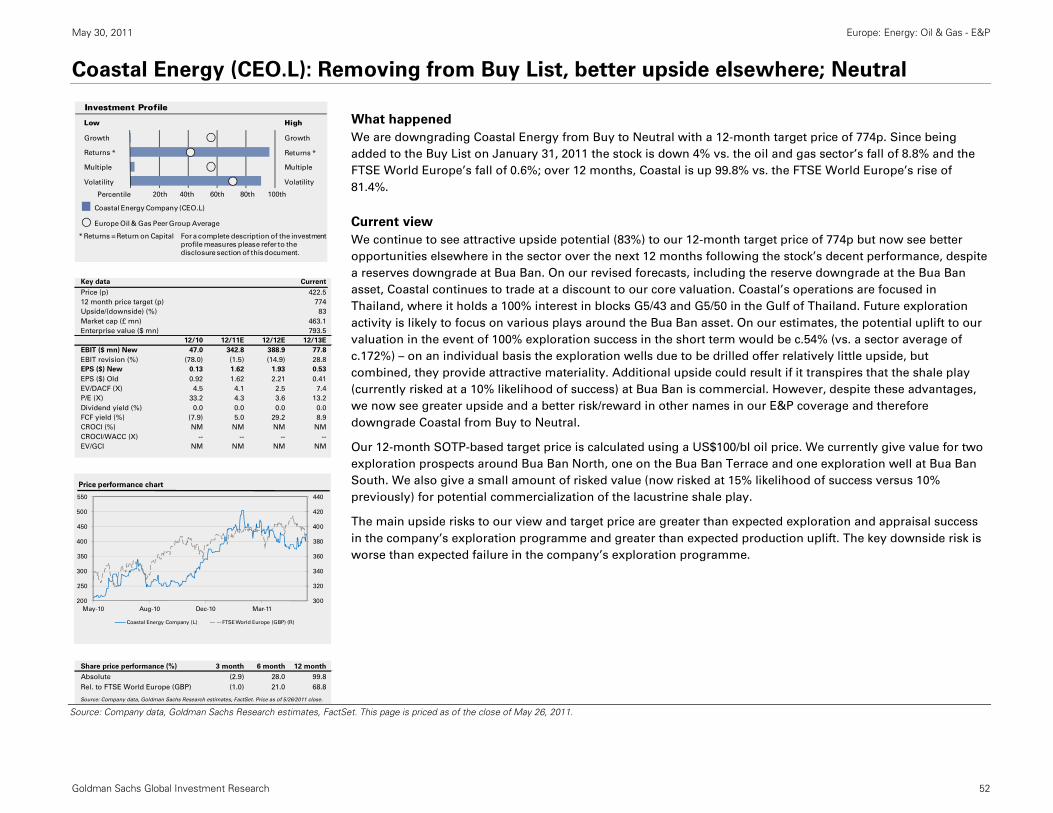

Coastal Energy (CEO.L): Removing from Buy List, better upside elsewhere; Neutral 52

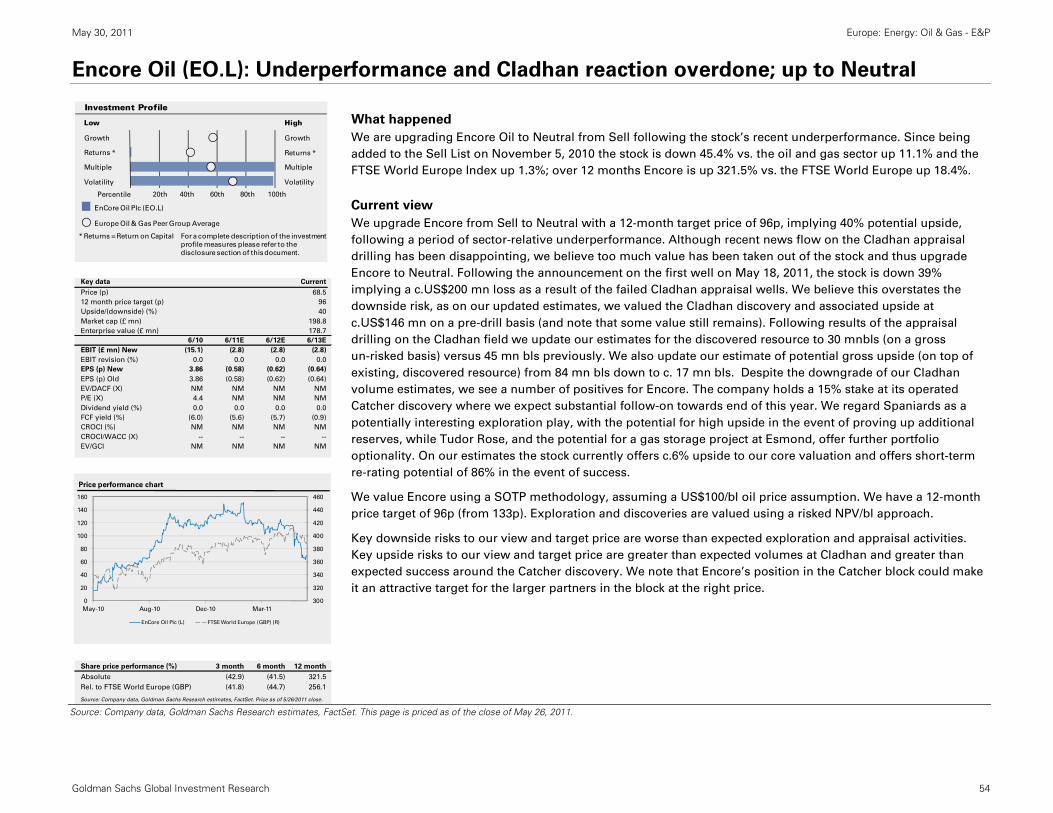

Encore Oil (EO.L): Underperformance and Cladhan reaction overdone; up to Neutral 54

Prices in this report are as of the close of May 25, 2011 unless stated otherwise.

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 3

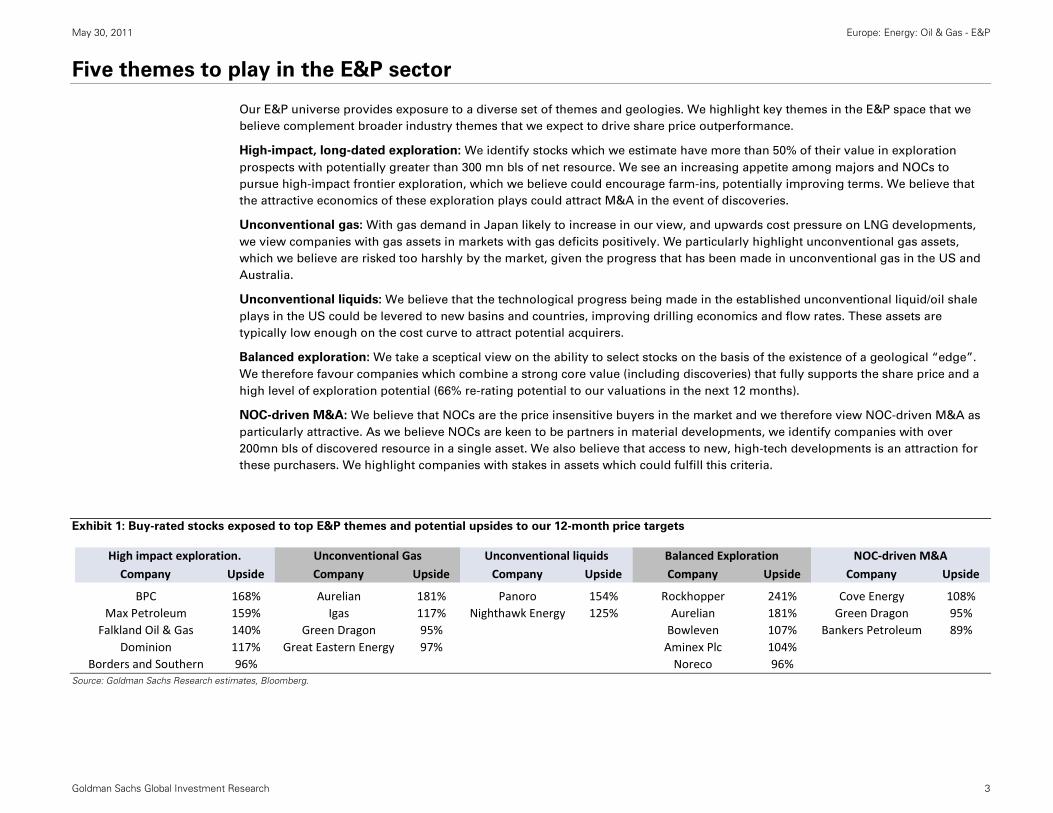

Five themes to play in the E&P sector

Our E&P universe provides exposure to a diverse set of themes and geologies. We highlight key themes in the E&P space that we

believe complement broader industry themes that we expect to drive share price outperformance.

High-impact, long-dated exploration: We identify stocks which we estimate have more than 50% of their value in exploration

prospects with potentially greater than 300 mn bls of net resource. We see an increasing appetite among majors and NOCs to

pursue high-impact frontier exploration, which we believe could encourage farm-ins, potentially improving terms. We believe that

the attractive economics of these exploration plays could attract M&A in the event of discoveries.

Unconventional gas: With gas demand in Japan likely to increase in our view, and upwards cost pressure on LNG developments,

we view companies with gas assets in markets with gas deficits positively. We particularly highlight unconventional gas assets,

which we believe are risked too harshly by the market, given the progress that has been made in unconventional gas in the US and

Australia.

Unconventional liquids: We believe that the technological progress being made in the established unconventional liquid/oil shale

plays in the US could be levered to new basins and countries, improving drilling economics and flow rates. These assets are

typically low enough on the cost curve to attract potential acquirers.

Balanced exploration: We take a sceptical view on the ability to select stocks on the basis of the existence of a geological “edge”.

We therefore favour companies which combine a strong core value (including discoveries) that fully supports the share price and a

high level of exploration potential (66% re-rating potential to our valuations in the next 12 months).

NOC-driven M&A: We believe that NOCs are the price insensitive buyers in the market and we therefore view NOC-driven M&A as

particularly attractive. As we believe NOCs are keen to be partners in material developments, we identify companies with over

200mn bls of discovered resource in a single asset. We also believe that access to new, high-tech developments is an attraction for

these purchasers. We highlight companies with stakes in assets which could fulfill this criteria.

Exhibit 1: Buy-rated stocks exposed to top E&P themes and potential upsides to our 12-month price targets

Source: Goldman Sachs Research estimates, Bloomberg.

Company Upside Company Upside Company Upside Company Upside Company Upside

BPC 168% Aurelian 181% Panoro 154% Rockhopper 241% Cove Energy 108%Max Petroleum 159% Igas 117% Nighthawk Energy 125% Aurelian 181% Green Dragon 95%

Falkland Oil & Gas 140% Green Dragon 95% Bowleven 107% Bankers Petroleum 89%Dominion 117% Great Eastern Energy 97% Aminex Plc 104%

Borders and Southern 96% Noreco 96%

Balanced Exploration NOC‐driven M&AHigh impact exploration. Unconventional Gas Unconventional liquids

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 4

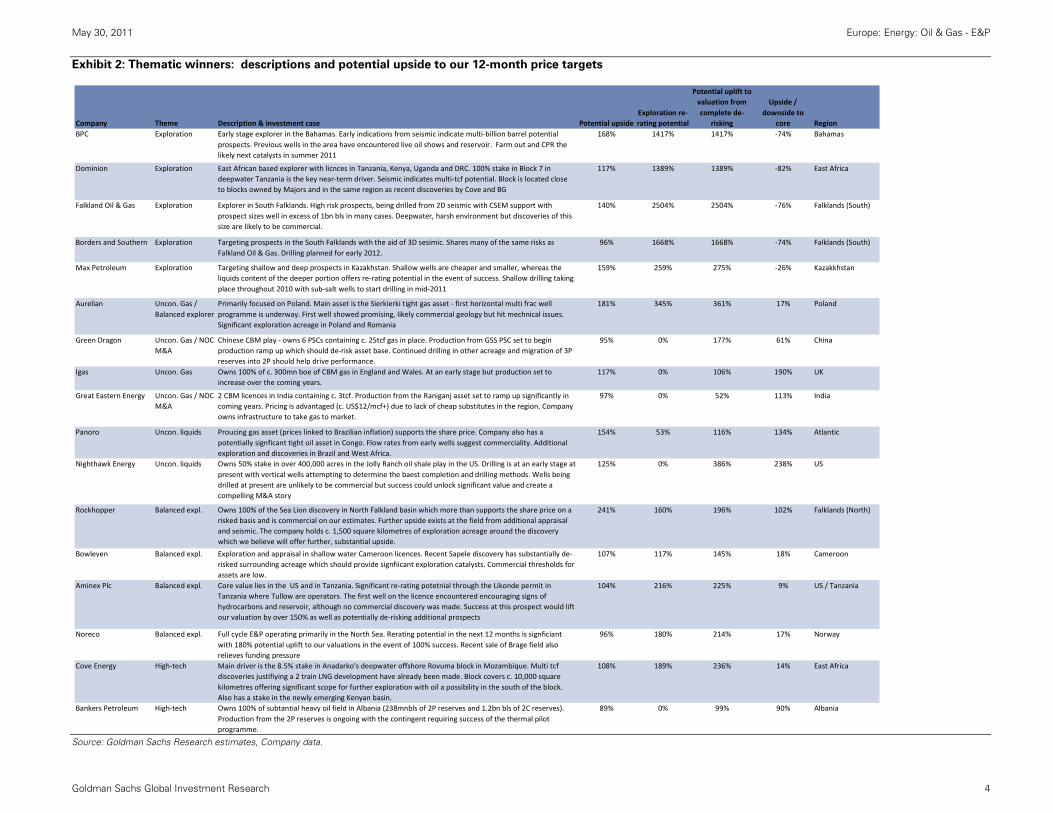

Exhibit 2: Thematic winners: descriptions and potential upside to our 12-month price targets

Source: Goldman Sachs Research estimates, Company data.

Company Theme Description & investment case Potential upsideExploration re‐rating potential

Potential uplift to valuation from complete de‐

risking

Upside / downside to

core RegionBPC Exploration Early stage explorer in the Bahamas. Early indications from seismic indicate multi‐billion barrel potential

prospects. Previous wells in the area have encountered live oil shows and reservoir. Farm out and CPR the likely next catalysts in summer 2011

168% 1417% 1417% ‐74% Bahamas

Dominion Exploration East African based explorer with licnces in Tanzania, Kenya, Uganda and DRC. 100% stake in Block 7 in deepwater Tanzania is the key near‐term driver. Seismic indicates multi‐tcf potential. Block is located close to blocks owned by Majors and in the same region as recent discoveries by Cove and BG

117% 1389% 1389% ‐82% East Africa

Falkland Oil & Gas Exploration Explorer in South Falklands. High risk prospects, being drilled from 2D seismic with CSEM support with prospect sizes well in excess of 1bn bls in many cases. Deepwater, harsh environment but discoveries of this size are likely to be commercial.

140% 2504% 2504% ‐76% Falklands (South)

Borders and Southern Exploration Targeting prospects in the South Falklands with the aid of 3D sesimic. Shares many of the same risks as Falkland Oil & Gas. Drilling planned for early 2012.

96% 1668% 1668% ‐74% Falklands (South)

Max Petroleum Exploration Targeting shallow and deep prospects in Kazakhstan. Shallow wells are cheaper and smaller, whereas the liquids content of the deeper portion offers re‐rating potential in the event of success. Shallow drilling taking place throughout 2010 with sub‐salt wells to start drilling in mid‐2011

159% 259% 275% ‐26% Kazakkhstan

Aurelian Uncon. Gas / Balanced explorer

Primarily focused on Poland. Main asset is the Sierkierki tight gas asset ‐ first horizontal multi frac well programme is underway. First well showed promising, likely commercial geology but hit mechnical issues. Significant exploration acreage in Poland and Romania

181% 345% 361% 17% Poland

Green Dragon Uncon. Gas / NOC M&A

Chinese CBM play ‐ owns 6 PSCs containing c. 25tcf gas in place. Production from GSS PSC set to begin production ramp up which should de‐risk asset base. Continued drilling in other acreage and migration of 3P reserves into 2P should help drive performance.

95% 0% 177% 61% China

Igas Uncon. Gas Owns 100% of c. 300mn boe of CBM gas in England and Wales. At an early stage but production set to increase over the coming years.

117% 0% 106% 190% UK

Great Eastern Energy Uncon. Gas / NOC M&A

2 CBM licences in India containing c. 3tcf. Production from the Raniganj asset set to ramp up significantly in coming years. Pricing is advantaged (c. US$12/mcf+) due to lack of cheap substitutes in the region. Company owns infrastructure to take gas to market.

97% 0% 52% 113% India

Panoro Uncon. liquids Proucing gas asset (prices linked to Brazilian inflation) supports the share price. Company also has a potentially signficant tight oil asset in Congo. Flow rates from early wells suggest commerciality. Additional exploration and discoveries in Brazil and West Africa.

154% 53% 116% 134% Atlantic

Nighthawk Energy Uncon. liquids Owns 50% stake in over 400,000 acres in the Jolly Ranch oil shale play in the US. Drilling is at an early stage at present with vertical wells attempting to determine the baest completion and drilling methods. Wells being drilled at present are unlikely to be commercial but success could unlock significant value and create a compelling M&A story

125% 0% 386% 238% US

Rockhopper Balanced expl. Owns 100% of the Sea Lion discovery in North Falkland basin which more than supports the share price on a risked basis and is commercial on our estimates. Further upside exists at the field from additional appraisal and seismic. The company holds c. 1,500 square kilometres of exploration acreage around the discovery which we believe will offer further, substantial upside.

241% 160% 196% 102% Falklands (North)

Bowleven Balanced expl. Exploration and appraisal in shallow water Cameroon licences. Recent Sapele discovery has substantially de‐risked surrounding acreage which should provide signfiicant exploration catalysts. Commercial thresholds for assets are low.

107% 117% 145% 18% Cameroon

Aminex Plc Balanced expl. Core value lies in the US and in Tanzania. Significant re‐rating potetnial through the Likonde permit in Tanzania where Tullow are operators. The first well on the licence encountered encouraging signs of hydrocarbons and reservoir, although no commercial discovery was made. Success at this prospect would lift our valuation by over 150% as well as potentially de‐risking additional prospects

104% 216% 225% 9% US / Tanzania

Noreco Balanced expl. Full cycle E&P operating primarily in the North Sea. Rerating potential in the next 12 months is signficiant with 180% potential uplift to our valuations in the event of 100% success. Recent sale of Brage field also relieves funding pressure

96% 180% 214% 17% Norway

Cove Energy High‐tech Main driver is the 8.5% stake in Anadarko's deepwater offshore Rovuma block in Mozambique. Multi tcf discoveries justifiying a 2 train LNG development have already been made. Block covers c. 10,000 square kilometres offering significant scope for further exploration with oil a possibility in the south of the block. Also has a stake in the newly emerging Kenyan basin.

108% 189% 236% 14% East Africa

Bankers Petroleum High‐tech Owns 100% of subtantial heavy oil field in Albania (238mnbls of 2P reserves and 1.2bn bls of 2C reserves). Production from the 2P reserves is ongoing with the contingent requiring success of the thermal pilot programme.

89% 0% 99% 90% Albania

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 5

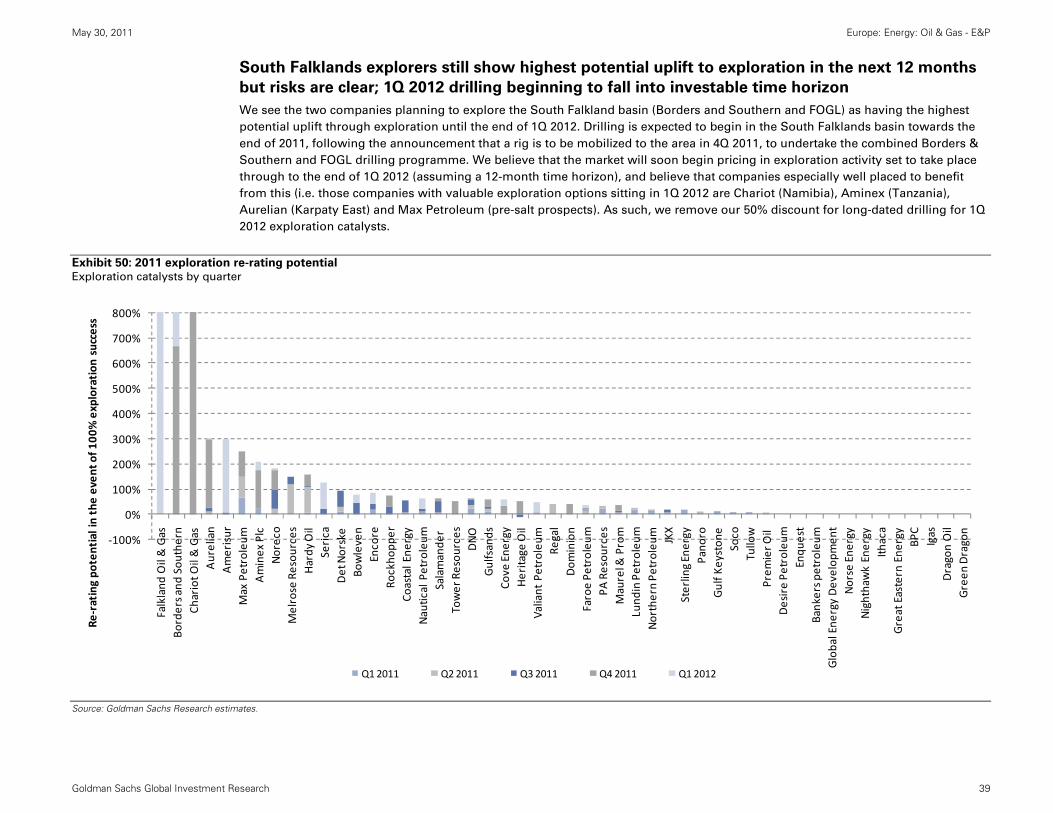

Frontier exploration set to be a major theme in late 2011/early 2012. Industry appetite for

frontier exploration provides additional benefits for explorers

Potentially major new basins to be tested in the next 18 months; vast re-rating potential

In the next 12-18 months, a number of companies in our coverage are expected to drill potentially transformational wells in new,

frontier basins. Risks are clearly high, but volumes are significant, especially for the companies involved, and success could re-rate

stocks and open up new basins. The key new basins we identify in our coverage universe are Namibia (Tower and Chariot), the

South Falklands Basin (Borders and Southern and FOGL) and the Bahamas (BPC). We also note that Max Petroleum (Kazakhstan)

and Dominion (Tanzania) are due to drill very large prospects in areas with previous successes in finding hydrocarbons.

Exhibit 3: Exploration re-rating potential by time period

Source: Goldman Sachs Research estimates.

‐500%

0%

500%

1000%

1500%

2000%

2500%

3000%

Falkland

Oil & Gas

Tower Resou

rces

Borders and

Sou

thern

Chariot O

il & Gas

BPC

Dom

inion

Sterling Energy

Northern Pe

troleu

mDesire Pe

troleu

mPA

Resou

rces

Serica

Amerisur

Aurelian

Hardy

Oil

Max Petroleum

Aminex

Plc

Cove

Ene

rgy

Noreco

Rockho

pper

Melrose Resou

rces

Bowleven

Det Norske

Encore

Coastal Ene

rgy

Nautical Petroleum

Salamande

r DNO

Gulfsands

Pano

roValiant Petroleum

Regal

Heritage

Oil

Faroe Pe

troleu

mMaurel &

Prom

Lund

in Petroleum JKX

Gulf K

eyston

eSoco

Tullow

Prem

ier O

il Enqu

est

Bankers p

etroleum

Global Ene

rgy Develop

men

tNorse Ene

rgy

Nighthawk Energy

Ithaca

Great Eastern Ene

rgy

Igas

Dragon Oil

Green

Dragon

Re‐rating po

tential in the even

t of 1

00% exploration

success

Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Rest of 2012

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 6

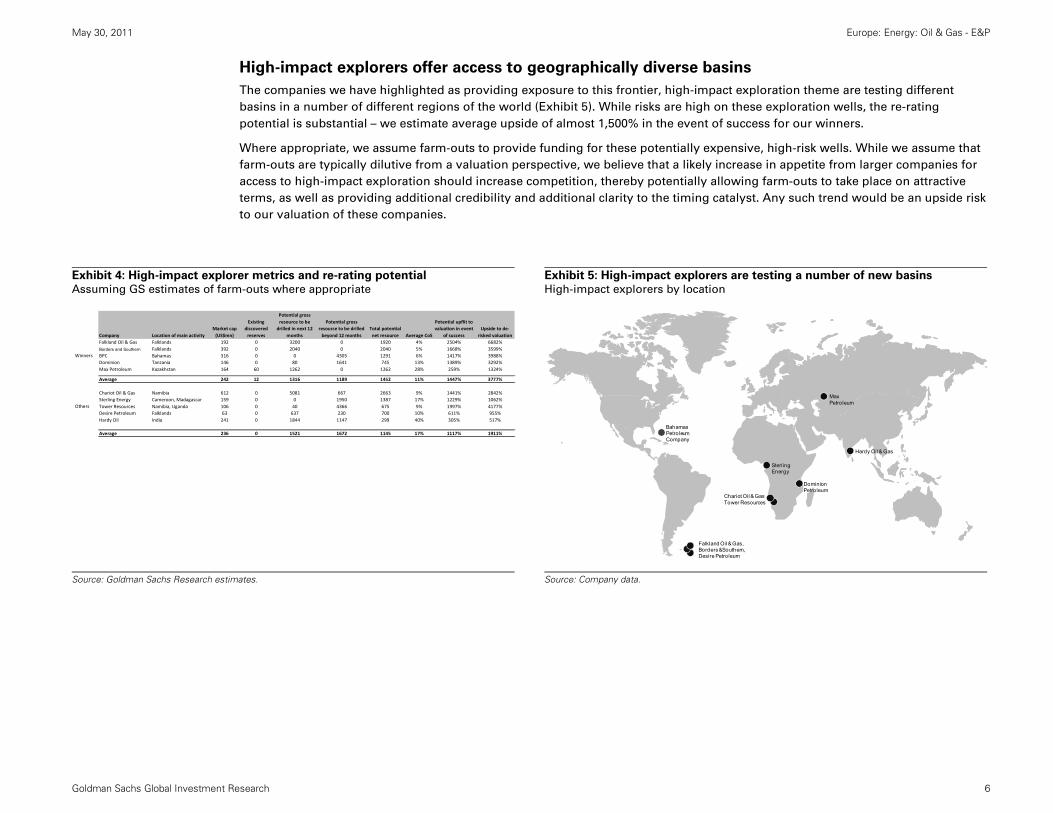

High-impact explorers offer access to geographically diverse basins

The companies we have highlighted as providing exposure to this frontier, high-impact exploration theme are testing different

basins in a number of different regions of the world (Exhibit 5). While risks are high on these exploration wells, the re-rating

potential is substantial – we estimate average upside of almost 1,500% in the event of success for our winners.

Where appropriate, we assume farm-outs to provide funding for these potentially expensive, high-risk wells. While we assume that

farm-outs are typically dilutive from a valuation perspective, we believe that a likely increase in appetite from larger companies for

access to high-impact exploration should increase competition, thereby potentially allowing farm-outs to take place on attractive

terms, as well as providing additional credibility and additional clarity to the timing catalyst. Any such trend would be an upside risk

to our valuation of these companies.

Exhibit 4: High-impact explorer metrics and re-rating potential Assuming GS estimates of farm-outs where appropriate

Exhibit 5: High-impact explorers are testing a number of new basins High-impact explorers by location

Source: Goldman Sachs Research estimates.

Source: Company data.

Company Location of main activityMarket cap (US$mn)

Existing discovered reserves

Potential gross resource to be drilled in next 12

months

Potential gross resource to be drilled beyond 12 months

Total potential net resource Average CoS

Potential upflit to valuation in event

of successUpside to de‐

risked valuationFalkland Oil & Gas Falklands 192 0 3200 0 1920 4% 2504% 6682%Borders and Southern Falklands 392 0 2040 0 2040 5% 1668% 3599%BPC Bahamas 316 0 0 4305 1291 6% 1417% 3988%Dominion Tanzania 146 0 80 1641 745 13% 1389% 3292%Max Petroleum Kazakhstan 164 60 1262 0 1262 28% 259% 1324%

Average 242 12 1316 1189 1452 11% 1447% 3777%

Chariot Oil & Gas Namibia 612 0 5081 667 2663 9% 1441% 2842%Sterling Energy Cameroon, Madagascar 159 0 0 1950 1387 17% 1229% 1062%Tower Resources Namibia, Uganda 106 0 40 4366 675 9% 1997% 4177%Desire Petroleum Falklands 63 0 637 230 700 10% 611% 955%Hardy Oil India 241 0 1844 1147 299 40% 305% 517%

Average 236 0 1521 1672 1145 17% 1117% 1911%

Winners

Others

Bahamas Petroleum Company

Falkland Oil & Gas, Borders &Southern, Desire Petroleum

Max Petroleum

Dominion Petroleum

Chariot Oil & GasTower Resources

Hardy Oil & Gas

Sterling Energy

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 7

High-impact exploration to become increasingly attractive to the industry

Based on our Top 330 analysis, most of the discoveries that have been made over the last five years have been made in the deep

offshore, with Brazil dominating, followed by GoM and Ghana. Onshore discoveries of substantial size have typically been limited to

Kurdistan and Uganda. Notably, the more traditional areas of exploration (shallow GoM, Nigeria, Angola) that are typically the

provinces of the majors, have been increasingly less relevant – it has been new frontiers that has driven this exploration. The result

has been a relative lack of success with the drill bit for the larger companies, with majors having found less than other companies

each year since 2003. With exploration budgets at the major’s looking set to increase, we believe this trend is set to reverse, and

believe that competition for attractive, high-impact acreage is likely to increase, thereby improving potential farm-out terms.

Exhibit 6: A pick up in recent exploration success has been led by frontier

basins Oil reserves discovered each year in giant fields (Top 330 projects) – 2000 includes

15 bn bls from Kashagan

Exhibit 7: Majors’ reliance on established basins has not been effective Top 330 oil reserves discovered by company type

Source: Company data, Goldman Sachs Research estimates.

Source: Company data, Goldman Sachs Research estimates.

0

5,000

10,000

15,000

20,000

25,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Traditional offshore Onshore traditional Onshore frontier Offshore frontier0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010mn bls

Major Other NOC

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 8

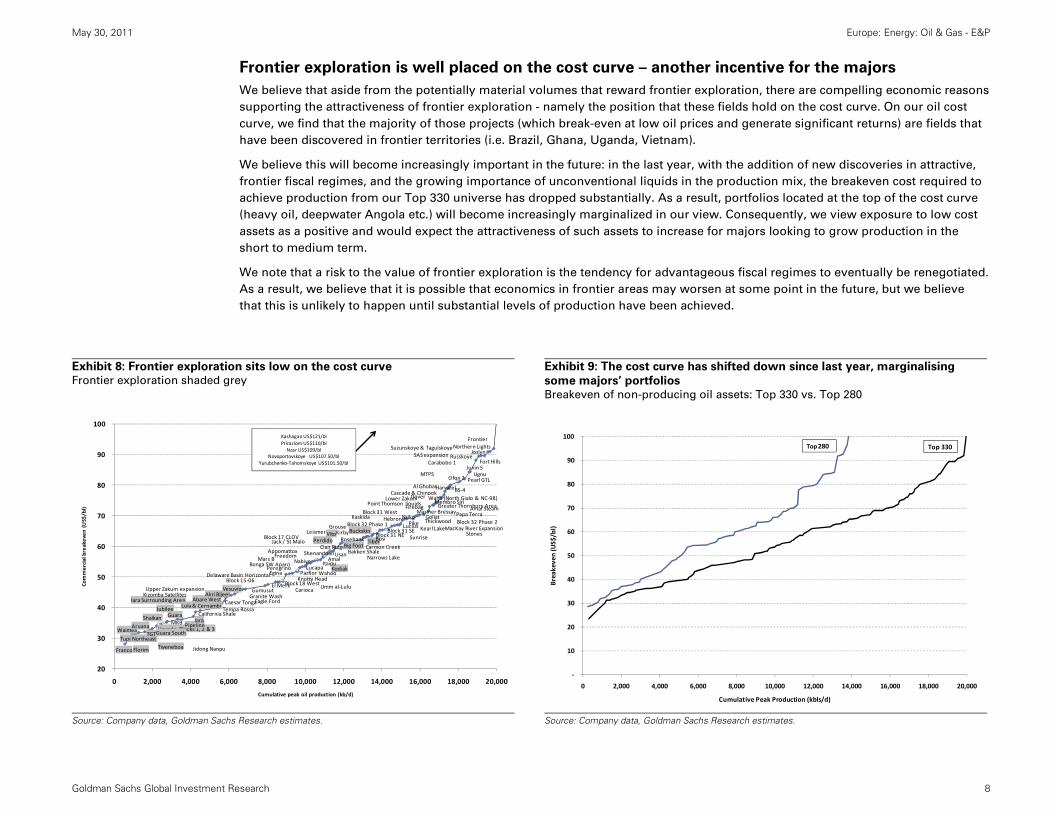

Frontier exploration is well placed on the cost curve – another incentive for the majors

We believe that aside from the potentially material volumes that reward frontier exploration, there are compelling economic reasons

supporting the attractiveness of frontier exploration - namely the position that these fields hold on the cost curve. On our oil cost

curve, we find that the majority of those projects (which break-even at low oil prices and generate significant returns) are fields that

have been discovered in frontier territories (i.e. Brazil, Ghana, Uganda, Vietnam).

We believe this will become increasingly important in the future: in the last year, with the addition of new discoveries in attractive,

frontier fiscal regimes, and the growing importance of unconventional liquids in the production mix, the breakeven cost required to

achieve production from our Top 330 universe has dropped substantially. As a result, portfolios located at the top of the cost curve

(heavy oil, deepwater Angola etc.) will become increasingly marginalized in our view. Consequently, we view exposure to low cost

assets as a positive and would expect the attractiveness of such assets to increase for majors looking to grow production in the

short to medium term.

We note that a risk to the value of frontier exploration is the tendency for advantageous fiscal regimes to eventually be renegotiated.

As a result, we believe that it is possible that economics in frontier areas may worsen at some point in the future, but we believe

that this is unlikely to happen until substantial levels of production have been achieved.

Exhibit 8: Frontier exploration sits low on the cost curve Frontier exploration shaded grey

Exhibit 9: The cost curve has shifted down since last year, marginalising

some majors’ portfolios Breakeven of non-producing oil assets: Top 330 vs. Top 280

Source: Company data, Goldman Sachs Research estimates.

Source: Company data, Goldman Sachs Research estimates.

20

30

40

50

60

70

80

90

100

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 20,000

Commercial breakeven

(US$/bl)

Cumulative peak oil production (kb/d)

Kashagan US$121/blPrirazlom US$110/blNasr US$109/bl

Novoportovskoye US$107.50/blYurubchenko‐Tahomskoye US$101.50/bl

Uganda, Blocks 1, 2 & 3

Franco

Waimea

Florim TweneboaTupi Northeast

TGTAruana

Shaikan

Guara South

Jubilee

Jidong Nanpu

Iara Surrounding Area

GuaraMKB Pipeline

Kizomba Satellites

IaraCalifornia Shale

Upper Zakum expansion

Lula & CernambiTempa Rossa

Abare WestAkri Bijeel

Caesar Tonga

Vesuvio

Block 15‐06

Granite WashGumusut

Eagle Ford

El Merk

Delaware Basin HorizontalPeregrino

Mars B

Egina

Carioca

Bonga SW Aparo

Block 18 West

Pazflor

FreedomAppomattox

Lucapa

Knotty Head

NabiyeKodiak

Wahoo

Umm al‐Lulu

Itaipu

Block 17 CLOVJack / St Malo

Clair Ridge

AmalShenandoah

VitoGrouse

Kirby

Usan

RosebankCarmon Creek

Leismer

Perdido

Bakken Shale

Kaskida

Buckskin

Narrows Lake

Big FootTiber

Block 32 Phase 1Block 31 SE

BosiBlock 31 NE Sunrise

Block 31 WestHebron

LuciusPike

Point Thomson liquids

Block 32 Phase 2Nsiko

Kearl Lake

Mariner BressayGoliatThickwood

Dover

Firebag

MacKay River Expansion

Waha (North Gialo & NC‐98)Greater Thornbury Area

Cascade & Chinook

Stones

Amal SteamPapa Terra

Lower ZakumMembro Siri

Al Ghubar

MTPS

Harweel

Ofon 2

Carabobo 1

BS‐4

Pearl GTL

Junin 5Ugnu

Fort HillsRusskoye

Northern LightsSuzunskoye & TagulskoyeJoslynSAS expansion

Frontier

‐

10

20

30

40

50

60

70

80

90

100

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 20,000

Breakeven (US$/bl)

Cumulative Peak Production (kbls/d)

Top 330Top 280

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 9

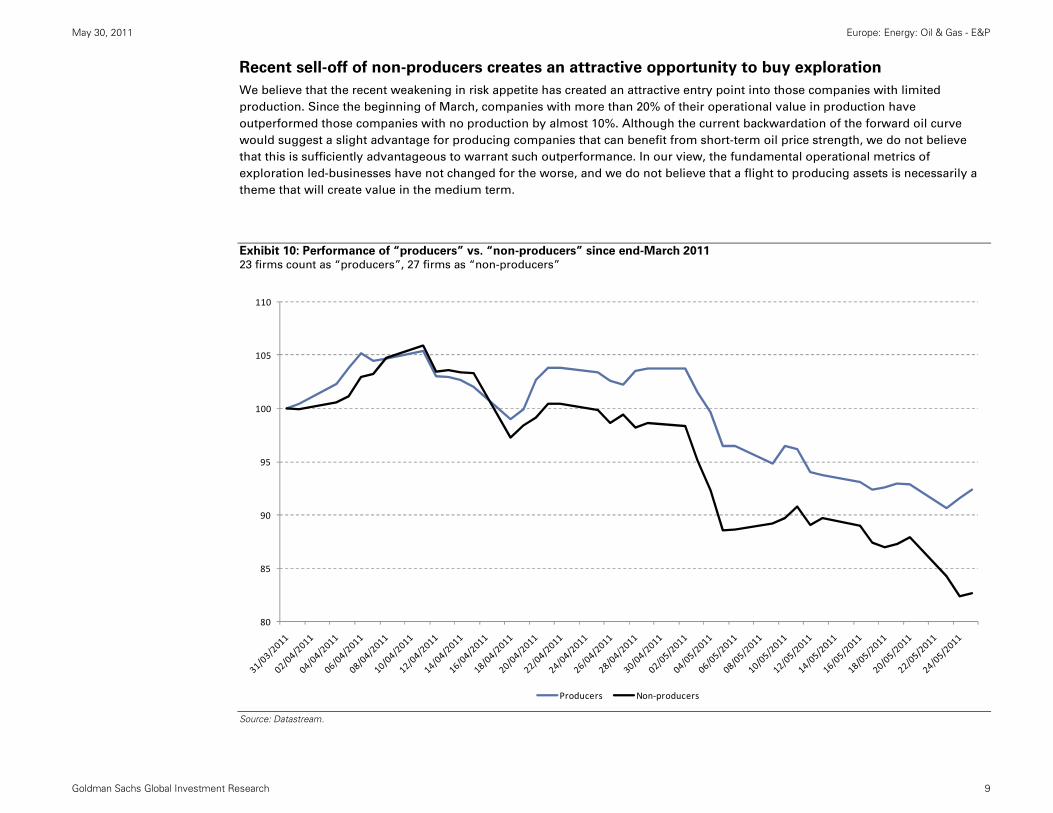

Recent sell-off of non-producers creates an attractive opportunity to buy exploration

We believe that the recent weakening in risk appetite has created an attractive entry point into those companies with limited

production. Since the beginning of March, companies with more than 20% of their operational value in production have

outperformed those companies with no production by almost 10%. Although the current backwardation of the forward oil curve

would suggest a slight advantage for producing companies that can benefit from short-term oil price strength, we do not believe

that this is sufficiently advantageous to warrant such outperformance. In our view, the fundamental operational metrics of

exploration led-businesses have not changed for the worse, and we do not believe that a flight to producing assets is necessarily a

theme that will create value in the medium term.

Exhibit 10: Performance of “producers” vs. “non-producers” since end-March 2011 23 firms count as “producers”, 27 firms as “non-producers”

Source: Datastream.

80

85

90

95

100

105

110

Producers Non‐producers

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 10

Rising gas prices, energy security and production ramp-ups to drive outperformance in

unconventional gas

We are positive on gas price exposure in countries with substantial gas deficits, as we believe LNG prices (likely to remain the global

determinant of marginal gas prices in importing markets) will remain strong or strengthen further in the medium term, providing

increased tightness on global markets. As a result, we view companies exposed to gas importing markets, where LNG is likely to be

the marginal fuel positively.

While we believe that the current situation in Japan is likely to put upward pressure on demand, we also see structural pressures on

cost in the supply base providing support to global gas prices. We believe that the marginal costs of projects being brought on line

will remain a key determinant of prices in the long term. Floating LNG projects remain the marginal cost area within LNG in our

view, but there are a number of projects with imminent sanction dates that require US$13/mcf or more to reach an 11% cost of

capital on our estimates, such as Gladstone LNG, Arrow LNG or Evans Shoal.

Exhibit 11: Marginal Top 330 gas fields require over US$12/mcf

Breakeven of non-producing gas assets

Source: Goldman Sachs Research estimates.

‐

2

4

6

8

10

12

14

16

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 20,000

Commercial breakeven

(US$/m

cf)

Cumulative peak gas production (kboe/d)

Shizhuang

Haynesville ShalePinedale Tight Gas

Horn River ShaleFayetteville Shale

LNG is the maringal asset type, providing support for medium term global prices at c. US$13/mcf+

Raniganj

SierkierkiUK CBMi Unconventional gas breaks

even low down on the cost curve, partly as a result of its proximity to local markets

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 11

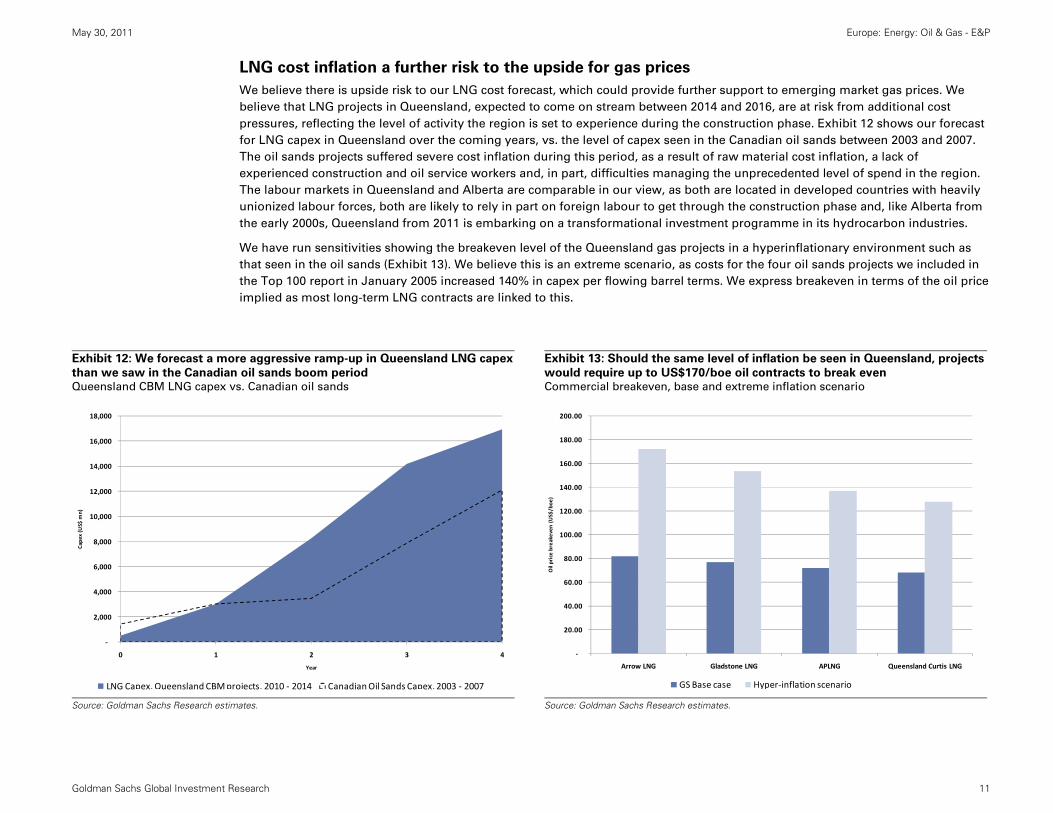

LNG cost inflation a further risk to the upside for gas prices

We believe there is upside risk to our LNG cost forecast, which could provide further support to emerging market gas prices. We

believe that LNG projects in Queensland, expected to come on stream between 2014 and 2016, are at risk from additional cost

pressures, reflecting the level of activity the region is set to experience during the construction phase. Exhibit 12 shows our forecast

for LNG capex in Queensland over the coming years, vs. the level of capex seen in the Canadian oil sands between 2003 and 2007.

The oil sands projects suffered severe cost inflation during this period, as a result of raw material cost inflation, a lack of

experienced construction and oil service workers and, in part, difficulties managing the unprecedented level of spend in the region.

The labour markets in Queensland and Alberta are comparable in our view, as both are located in developed countries with heavily

unionized labour forces, both are likely to rely in part on foreign labour to get through the construction phase and, like Alberta from

the early 2000s, Queensland from 2011 is embarking on a transformational investment programme in its hydrocarbon industries.

We have run sensitivities showing the breakeven level of the Queensland gas projects in a hyperinflationary environment such as

that seen in the oil sands (Exhibit 13). We believe this is an extreme scenario, as costs for the four oil sands projects we included in

the Top 100 report in January 2005 increased 140% in capex per flowing barrel terms. We express breakeven in terms of the oil price

implied as most long-term LNG contracts are linked to this.

Exhibit 12: We forecast a more aggressive ramp-up in Queensland LNG capex

than we saw in the Canadian oil sands boom period Queensland CBM LNG capex vs. Canadian oil sands

Exhibit 13: Should the same level of inflation be seen in Queensland, projects

would require up to US$170/boe oil contracts to break even Commercial breakeven, base and extreme inflation scenario

Source: Goldman Sachs Research estimates.

Source: Goldman Sachs Research estimates.

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0 1 2 3 4

Cape

x (US$

mn)

Year

LNG Capex, Queensland CBM projects, 2010 ‐ 2014 Canadian Oil Sands Capex, 2003 ‐ 2007

‐

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

Arrow LNG Gladstone LNG APLNG Queensland Curtis LNG

Oil price breakeven (US$/boe

)

GS Base case Hyper‐inflation scenario

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 12

Gas price leverage hard to come by in the E&P universe

Obtaining exposure to this theme is not as easy as one may think in the E&P universe, with oil by far the most important commodity

as a driver of the universe. Gas as a commodity represents only 17% of the operational value of the E&P companies under our

coverage. Exposure is, however, significant for certain stocks. We would highlight Great Eastern (North East India), IGas (UK), Green

Dragon (China), JKX (Ukraine), Dominion (LNG), Cove (LNG), Northern Petroleum (Netherlands), Aurealian (Poland) and Hardy

(India) as stocks with significant gas exposure to markets where a net deficit exists. Although companies such as Panoro, Premier

and Salamander have significant exposure to gas, we note that prices are fixed for significant portions of their volumes.

We have identified companies with over 40% of their value in markets with gas deficits, and where prices are not fixed by contracts

or the government, and show the impact on our valuations of a 25% increase in gas prices. We note that a 25% increase to our gas

price assumptions would not take prices above the US$13/mcf we see as the marginal cost for Queensland LNG projects apart from

in the case of Great Eastern, where competing fuels are LPG / fuel oil more than LNG.

Exhibit 14: Exposure to gas in attractive locations is not a common theme

among European E&Ps Gas price exposure by value

Exhibit 15: Potential increase to valuation from a 25% increase in gas prices

in deficit markets Revised gas prices take Poland to c.US$12/mcf, the UK to US$12.5/mcf, India (KG

basin) to US$10/mcf, Chinese bucket price after downstream / midstream margins

to US$13/mcf

Source: Goldman Sachs Research estimates.

Source: Goldman Sachs Research estimates.

0%

20%

40%

60%

80%

100%

120%

Great Eastern Ene

rgy

Igas

Green

Dragon

JKX

Hardy

Oil

Regal

Cove

Ene

rgy

Dom

inion

Aurelian

Northern Pe

troleu

mMelrose Resou

rces

Pano

roSalamande

r Prem

ier O

il Aminex

Plc

Ithaca

Serica

Heritage

Oil

PA Resou

rces

Noreco

Chariot O

il & Gas

Faroe Pe

troleu

mTower Resou

rces

Encore

Dragon Oil

Tullow

Coastal Ene

rgy

Nautical Petroleum

Lund

in Petroleum

Det Norske

Valiant Petroleum

Maurel &

Prom

Nighthawk Energy

Sterling Energy

Gulfsands

Enqu

est

Rockho

pper

DNO

Norse Ene

rgy

Bowleven

Bankers p

etroleum

Borders and

Sou

thern

Amerisur

Desire Pe

troleu

mFalkland

Oil & Gas

Global Ene

rgy …

Gulf K

eyston

eMax Petroleum BPC

Soco

% of value

attribu

te to gas by

region

Western Europe gas Emerging market gas LNG Eastern Europe gas

0%

5%

10%

15%

20%

25%

30%

35%

40%

Regal Great Eastern Energy

Igas Green Dragon Aurelian JKX Northern Petroleum Hardy Oil

Upside to valuation

from a 25%

increase in

gas prices

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 13

Unconventional gas assets over-risked in our view; breakevens are low and production ramp ups /

flow tests should begin to challenge bearish assumptions

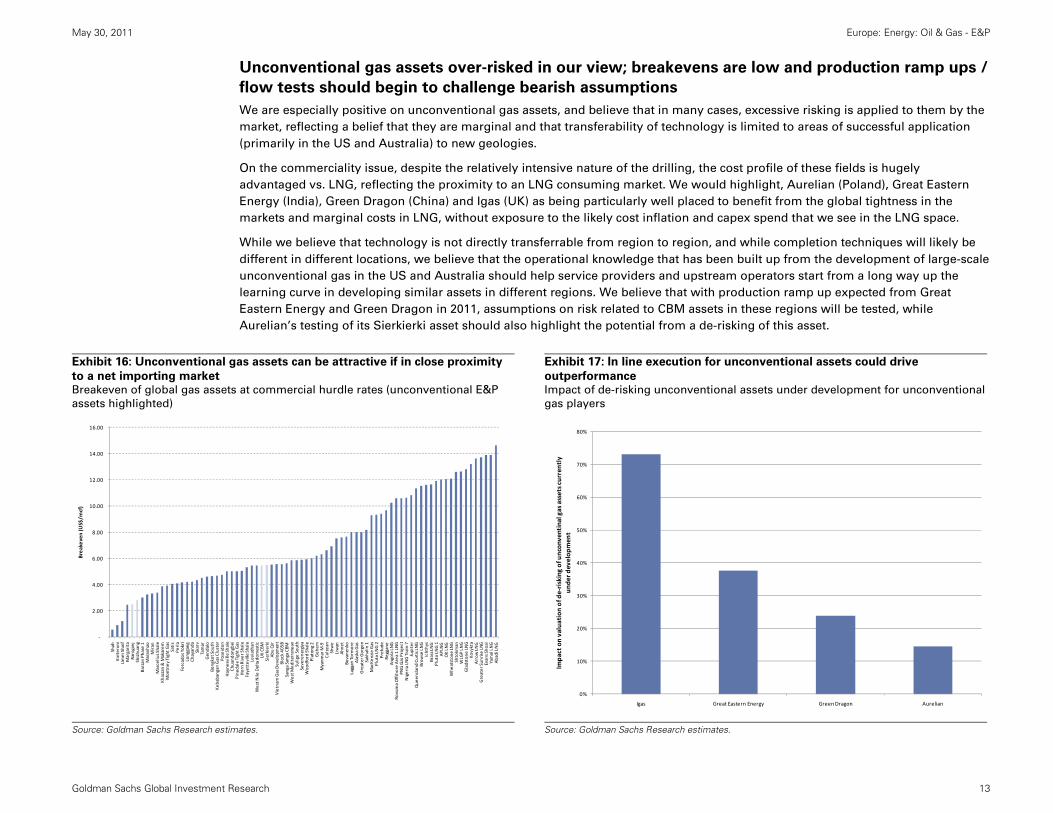

We are especially positive on unconventional gas assets, and believe that in many cases, excessive risking is applied to them by the

market, reflecting a belief that they are marginal and that transferability of technology is limited to areas of successful application

(primarily in the US and Australia) to new geologies.

On the commerciality issue, despite the relatively intensive nature of the drilling, the cost profile of these fields is hugely

advantaged vs. LNG, reflecting the proximity to an LNG consuming market. We would highlight, Aurelian (Poland), Great Eastern

Energy (India), Green Dragon (China) and Igas (UK) as being particularly well placed to benefit from the global tightness in the

markets and marginal costs in LNG, without exposure to the likely cost inflation and capex spend that we see in the LNG space.

While we believe that technology is not directly transferrable from region to region, and while completion techniques will likely be

different in different locations, we believe that the operational knowledge that has been built up from the development of large-scale

unconventional gas in the US and Australia should help service providers and upstream operators start from a long way up the

learning curve in developing similar assets in different regions. We believe that with production ramp up expected from Great

Eastern Energy and Green Dragon in 2011, assumptions on risk related to CBM assets in these regions will be tested, while

Aurelian’s testing of its Sierkierki asset should also highlight the potential from a de-risking of this asset.

Exhibit 16: Unconventional gas assets can be attractive if in close proximity

to a net importing market Breakeven of global gas assets at commercial hurdle rates (unconventional E&P

assets highlighted)

Exhibit 17: In line execution for unconventional assets could drive

outperformance Impact of de-risking unconventional assets under development for unconventional

gas players

Source: Goldman Sachs Research estimates.

Source: Goldman Sachs Research estimates.

‐

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Shah

Kinteroni

Umm Shaif

Margarita

Raniganj

Shizhu

ang

Barzan

Phase 1

Maranhao

Miran

Marcellu

s Shale

Khazzan & Makarem

Mon

tney

Tight Gas

Satis

Perla

Forcados Yokri

Longgang

Chayanda

Skarv

Tamar

Gen

dalo

Bongkot Sou

thKe

babangan

Gas Cluster

Poseidon

Hayne

sville Shale

Chuand

ongbei

Pine

dale Tight Gas

Horn River Shale

Fayetteville Shale

Leviathan

West N

ile Delta dom

estic

UK CB

MSierkierki

Abu Qir

Vietnam Gas Development

Block 40

5BSanga Sanga CB

MWest M

editerranean

Sulige South

Severenergiya

Woo

dford Shale

Platon

g 2

Geh

emMyanm

ar M

‐9Cu

lzean

Shwe

Liwan

Ahne

tBo

vane

nko

Laggan

Tormore

Alaska Gas

Greater Gorgon

Sakhalin 1

MacKe

nzie Gas

Pluto LN

G 2

Prelud

eRe

ggane

Angola LNG

Rovuma Offsho

re Area 1 LN

GPN

G Gas Project

Nigeria LNG Train 7

Jupiter

Que

ensland Cu

rtis LN

GBrow

se LNG

Ichthys

Brass LNG

Pluto LN

G 1

APLN

GOK LN

GWhe

atston

e LN

GShtokm

anWLG

P LN

GGladstone

LNG

Kovykta

Arrow LNG

Greater Sun

rise LNG

Evans Sho

alYamal LNG

Abadi LNG

Brea

keven (US$

/mcf)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Igas Great Eastern Energy Green Dragon Aurelian

Impact on

valua

tion

of d

e‐risking of u

ncon

ventinal gas assets currently

und

er develop

men

t

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 14

We expect performance of unconventional assets to improve, in line with US shale assets

We believe that these unconventional assets will begin to improve drilling economics through time, in line with the trend that we

have seen in more established basins in the US. We believe that this expected improvement is likely to drive further performance

and help de-risk the unconventional assets in our coverage further.

Exhibit 18: The “legacy” and emerging shale plays in the US have seen material improvement in drilling economics over time Average initial production rates and days to drill (excludes completion and tie in time)

Source: Chesapeake Energy, Devon Energy, Southwestern Energy.

Barnett/Fayetteville Shale annual averages based on data from CHK/DVN and CHK/SWN respectively

Haynesville Shale and Granite Wash annual averages based on data from CHK

Average IP rate

Average drilling days

0

5

10

15

20

25

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2,400

2007 2008 2009 2010

Average drilling days in the B

arnett Shale

Aver

age

IP ra

te in

the

Bar

nett

Shal

e, M

Mcf

/d

Average IP rate

Average drilling days

40

42

44

46

48

50

52

54

56

58

4,700

5,200

5,700

6,200

6,700

7,200

7,700

8,200

8,700

2007 2008 2009

Average drilling days in the H

aynesville Shale

Ave

rage

IP ra

te in

the

Hay

nesv

ille

Shal

e, M

Mcf

/d

Average IP rate

Average drilling days

15

16

17

18

19

20

21

22

23

24

25

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

2007 2008 2009 2010

Average drilling days in the

Fayetteville Shale

Aver

age

IP ra

te in

the

Faye

ttevi

lle

Shal

e, M

Mcf

/d

Average IP rate

Average drilling days

0

10

20

30

40

50

60

1,600

2,600

3,600

4,600

5,600

6,600

7,600

8,600

2007 2008 2009 2010

Average drilling days in the G

ranite Wash

Aver

age

IP ra

te in

the

Gra

nite

W

ash,

MM

cf/d

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 15

Unconventional liquids – de-risking of assets and potential M&A the key driver

As with the levels of risking we see in unconventional gas assets, we believe that a similarly high risking is applied to

unconventional liquids outside the more established basins in the US (such as the Bakken, Eagle Ford, Granite Wash etc.). Again,

while we believe that the drilling techniques perfected in these basins are unlikely to be able to applied directly to different

geologies, we believe that the experience in these basins serves to help the process of unlocking the potential of new basins. We

also note that the trend is for well performance to improve through time, as more is learnt about the optimal way in which to drill

and complete wells, and therefore we expect to see incremental improvements from these assets at an early stage of development.

As shown in Exhibits 19 and 20, drilling efficiencies also tend to improve, with times to drill, and costs decreasing through time.

Exhibit 19: Flow rates in the the Bakken Shale have gradually increased

through time Initial production rates for wells in tier 1 of the Bakken Shale

Exhibit 20: North Dakota monthly implied spud-to-spud days and average rig

count

Source: Company data.

Source: North Dakota Oil & Gas Commission. Goldman Sachs Research estimates.

1.00

1.50

2.00

2.50

3.00

3.50

1 2 3 4 5 6 7 8 9 1011121314151617181920212223242526272829303132333435363738394041424344454647484950515253545556575859

IP rates (kbo

pd)

IP rates from tier 1 Bakken shale assets Linear (IP rates from tier 1 Bakken shale assets)

0

20

40

60

80

100

120

140

160

180

20

25

30

35

40

45

50

55

60

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Average R

ig CountSp

ud-t

o-sp

ud D

ays

Rig count Implied Spud-to-spud days

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 16

Flow rates and costs key to unlocking value

We highlight Panoro (with its low permeability MKB asset in Congo) and Nighthawk (with its oil shale Jolly Ranch play in the US) as

companies with exposure to unconventional liquids assets at an early stage of development. We believe that a de-risking of these

assets could result in substantial upside from current levels. While we note that risk remains around these assets (especially for

Nighthawk, which has only drilled one well to date that we would consider commercial), we believe that the heavy risk factors that

we apply to these assets account for this uncertainty.

We believe there is significant further upside to be realized from both these assets from:

A de-risking of the assets as drilling continues;

The potential to improve flow rates;

The potential for drilling efficiencies to improve and, subsequently, for costs to come down.

In the event of de-risking these plays, we see significant re-rating potential for both Panoro and Nighthawk (Exhibit 22). We see the

key to de-risking these unconventional assets and determining value as the flow rates that can be achieved by the wells.

Exhibit 21: Assumed flow rates per well

Exhibit 22: Increased flow rates, more efficient drilling and de-risking of

unconventional liquid assets have the potential to re-rate Panoro and

Nighthawk Potential uplift to valuation as percentage of market cap

Source: Company data, Goldman Sachs Research estimates.

Source: Goldman Sachs Research estimates.

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.00

0.10

0.20

0.30

0.40

0.50

0.60

1 2 3 4 5 6 7 8 9 10

kbop

d

kbop

d

Assumed MKB flow rates (Panoro ‐ LHS) Assumed Jol ly ranch vertical flow rates (Nighthawk ‐ RHS)

‐100%

100%

300%

500%

700%

900%

1100%

0%

20%

40%

60%

80%

100%

120%

De‐risking 50% higher IP rate (no risking changes) Drop in costs by 50%

Potential value

add

ed as % of m

arket cap (Nighthawk)

Panoro (LHS) Nighthawk (RHS)

100% de‐risking IP rates 50% higher Costs 50% down

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 17

Unconventional liquids set for M&A in the future

We note that the majors are conspicuously absent from unconventional liquids at present. Despite the presence of some majors in

the Eagle Ford shale (i.e. Shell, Statoil) the only two majors with significant exposure to the unconventional liquids plays in the US

are Exxon and Conoco.

We note that Panoro’s and Nighthawk’s operations are at an early stage, and that further drilling and de-risking is required before

these are likely to screen as potential M&A targets. Nonetheless, we believe the early results at Panoro’s MKB fields are very

encouraging. Nighthawk’s Jolly Ranch asset has greater risk in our view, but as Exhibit 23 shows, in the event of the company

proving the geology of the play, the potential upside based on US deal metrics from similar assets could be substantial.

Exhibit 23: Majors are generally under-represented in unconventional liquidsNPV of unconventional liquids resource as % of EV (as at April 6, 2011)

Exhibit 24: The size of the prize for unlocking new plays is substantial Oil shale transaction implications for Nighthawk

Source: Goldman Sachs Research estimates, Bloomberg.

Source: Company data, Goldman Sachs Research estimates, Wyoming Land Auction data.

0%

10%

20%

30%

40%

50%

60%

70%

NPV

201

1 of uncon

ventional liquids portfolio as a % of 20

11 EV

Buyer Seller Date Asset 000 acres Price (US$mn) 000' US$ / acre Implied Nighthawk value Implied upsideHigh Bid Wyoming lease sale 4/9/10 Niobrara 0.6 3.8 5.9 1195 3248%Hess Marathon 28/7/10 Bakken 85.0 445.0 5.2 1060 2870%XTO Headington 15/7/08 Bakken 352.0 1800.0 5.1 1035 2801%High Bid Wyoming lease sale 9/7/10 Niobrara 0.3 1.0 3.2 647 1712%High Bid Wyoming lease sale 12/5/10 Niobrara 0.6 1.9 3.0 606 1598%Northern Oil Windsor bakken 1/6/09 Bakken 3.0 7.3 2.4 491 1276%El Paso UoT lease sale 23/9/10 Wolfcamp 123.1 180.0 1.5 294 723%Rex Energy Private company 30/6/10 Niobrara 18.7 18.7 1.0 200 461%Hilcorp Energy Lucas Energy 5/7/10 Eagle Ford 9.525 8.9 0.9 187 423%

Average 2.9 577.5 1518%

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 18

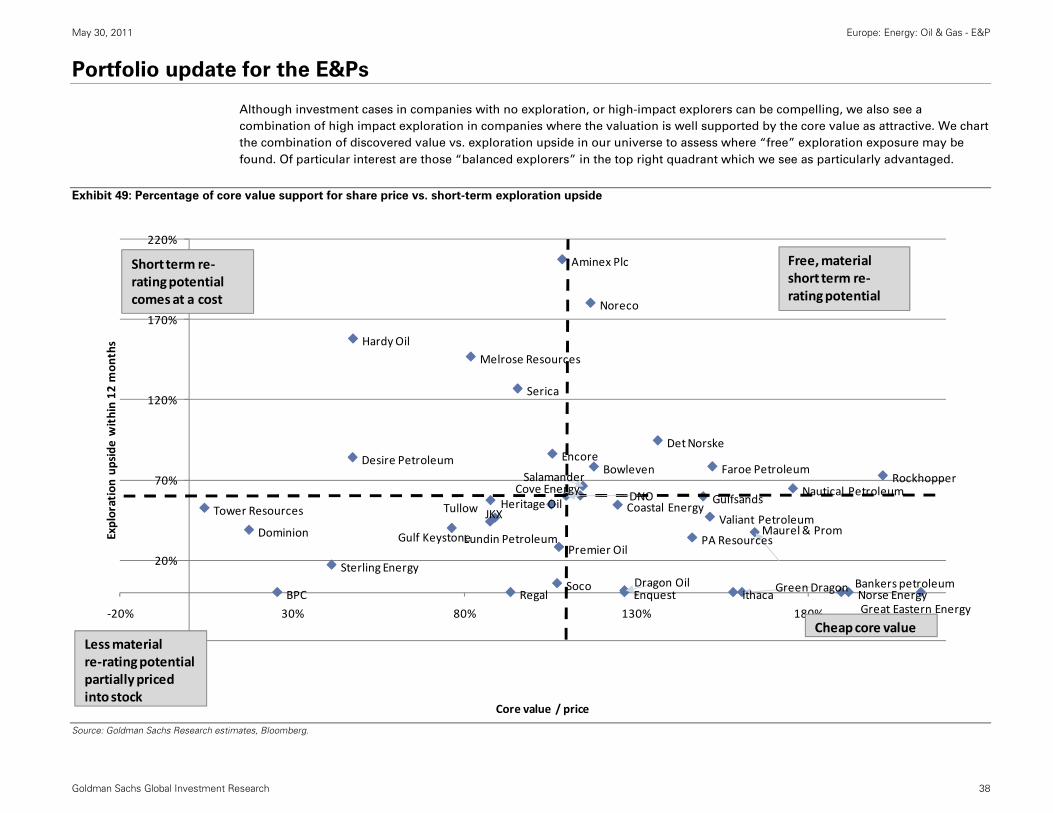

Free exploration options remain a compelling investment case

Since we expanded our universe of stocks on November 5, 2010, a key theme of ours has been identifying those companies in

which the value of their cash, production and discoveries supports the share price, but which also contain material exploration

upside – essentially providing re-rating potential through exploration that does not need to be paid for in the share price. Since

November, these companies have outperformed our coverage by c.10%.

We believe that these companies offer a compelling mix of value and exploration upside, and therefore highlight those companies

in our universe which we estimate have re-rating potential of over 66% in the next six months, combined with a share price that is

fully supported by cash, production, developments and risked discoveries. Of particular interest, in our view, are Bowleven and

Rockhopper, due to the de-risked nature of their exploration.

Exhibit 25: Balanced explorers have performed well since November 2010 Balanced explorers vs. E&P coverage

Exhibit 26: Exploration re-rating potential with core value support is an

attractive combination 6-month re-rating potential vs. upside / downside to core value (+discoveries)

Aurelian has 314% re-rating potential and 17% upside to core valuation, Amerisur has 297% and 3%.

Source: IHS Herold.

Source: Goldman Sachs Research.

90

95

100

105

110

115

120

125

130

135

140

08/11/2010 08/12/2010 08/01/2011 08/02/2011 08/03/2011 08/04/2011 08/05/2011

Balanced explorers E&P universe

‐30%

20%

70%

120%

170%

220%

‐20% 30% 80% 130% 180%

Exploration upside w

ithin 12 m

onths

Core value / price

Free, material short term re‐rating potential

Short term re‐rating potential comes at a cost

Less material re‐ratingpotential partially priced into stock

Cheap core value

Aminex Plc

Faroe PetroleumBowleven

Noreco

Det Norske

Salamander Rockhopper

Encore

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 19

M&A – Materiality and technical access a further potential driver of NOC activity

We believe that M&A remains a key theme in the industry. However, with NOC’s the most price insensitive buyers, in our view, we

believe that isolating M&A likely to be driven by NOCs is the most attractive way to play this theme.

We believe that larger assets are likely to be attractive to NOCs and therefore consider companies with discovered resource of

greater than 200 mn bls in a single block / asset to screen attractively in this regard (Exhibit 28).

In recent years, we have also seen an increasing bias towards NOC purchases of complex assets. We believe that this is in large part

inspired by a desire to develop technical skills, through exposure to highly skilled operators, pushing back the technological

boundaries of the industry. We would expect this trend to continue, with a number of “gaps” remaining in the portfolios of NOCs.

We have assessed which companies could provide a possible entry point into such assets. In our view, there are a number in our

coverage that provide exposure to what we regard as technical asset types. Companies with particularly high exposure include a

number of early stage CBM operators, such as and Green Dragon (China). Cove Energy represents an interesting potential entry into

a deepwater LNG scheme, while Bankers offers a high level of exposure to heavy oil developments. Tullow also offers exposure to

deepwater expertise.

Exhibit 27: NOC transactions have been highly focused on technical assets

NOC deals in high-tech win zones since 2006

Exhibit 28: Materiality a key concern for NOCs Percentage of value lying in assets of 200 mn bls or more. Assets exposed to

technical frontiers are highlighted.

Source: Goldman Sachs Research.

Source: Goldman Sachs Research estimates.

Heavy Oil DW Brazil DW West AfricaUnconventional gas / liquids LNG

CNOOCOML 130 (Akpo, Egina), 2006

Eagle Ford, 2010Wyoming, Colorado, 2011 Curtis LNG, 2010

Gazprom Sakhalin II, 2006KNOC CRTHE, 2009 Eagle Ford, 2011ONGC BC‐10, 2006

PetroChina MacKay River & Dover, 2009

Encana Cutbank Ridge gas assets, 2011 Arrow Energy, 2010

Petronas Mauritania, 2007 Gladstone LNG, 2008PTTEP Kai Kos Dehseh, 2010

RelianceMarcellus, 2010Eagle Ford, 2010

RosneftSinochem Peregrino, 2010

Sinopec

Northern Lights, 2009Tanganyika, 2008Syncrude, 2010 Repsol Brasil, 2010

Block 15, 17, 18/06, 2006

0%

20%

40%

60%

80%

100%

120%

Bankers petroleum

Dragon Oil Green Dragon Gulf Keystone Cove Energy Tullow Heritage Oil

% value

in assets over 200

mn bls

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 20

NOC interest could be a material value driver

We are especially attracted towards M&A that could potentially involve NOCs as we note that recent deals involving NOCs as the

acquirers have been done at significantly higher prices than those that have attracted IOC attention. We believe that this is a

function of the IOCs typically looking to buy assets at commercial costs of capital (to generate value), while the NOCs’ deal

rationales are often more strategic. Exhibit 29 shows the discount rates implied by recent deals, with NOC’s paying discount rates of

8% or lower in order to secure assets.

Exhibit 30 shows the re-rating potential from those companies that we believe could attract NOC attention either as a result of the

large materiality, or as a result of the technical nature of the asset if we use an 8% discount rate to value those assets we view as

attractive.

Exhibit 29: NOC acquisitions have been more price insensitive driving

potentially greater returns Implied discount rates of recent deals

Exhibit 30: Deals done at NOC costs of capital could see significant upside to

current valuations Highlighted companies screen attractively for both materiality and technical

access

Source: IHS Herold.

Source: Goldman Sachs Research.

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

Peregrino Athabasca Oil Sands

Corporation assets

Dana * Block 32 -Marathon

stake

Jack/St Malo Mariner** Uganda, blocks 1 & 3

(ENI & Heritage)

Dragon

Dis

coun

t rat

e im

plie

d by

dea

l at l

ong

run

oil p

rice

NOC acquirersIOC acquirers

NOC acquirer but with controlling stake

* Excluding exploration value** Assuming 80% development risking

Average WACC for sector per GS valuations

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Cove Energy Dragon Oil Gulf Keystone Green Dragon Bankers petroleum Heritage Oil Tullow

Uplift to

valaution

at NOC valuations

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 21

Thematic summary for E&P universe

In this report we have highlighted as thematic winners only those stocks on which we have a Buy rating. In Exhibit 31 we show

where all our coverage sits in relation to our five key themes, regardless of rating.

Exhibit 31: Thematic exposure of entire E&P coverage universe

Source: Goldman Sachs Research estimates.

Company Upside Company Upside Company Upside Company Upside Company Upside Company Upside

BPC 168% Aurelian 181% Panoro 154% Rockhopper 241% Cove Energy 108% Global Energy Development 189%Max Petroleum 159% Igas 117% Nighthawk Energy 125% Aurelian 181% Green Dragon 95% Northern Petroleum 164%

Falkland Oil & Gas 140% Green Dragon 95% Bowleven 107% Bankers Petroleum 89% PA Resources 132%Dominion 117% Great Eastern Energy 97% Aminex Plc 104% Aminex Plc 104%

Borders and Southern 96% Noreco 96% Nautical Petroleum 112%Maurel & Prom 89%

Sterling Energy 82% JKX 40% Faroe Petroleum 82% Gulf Keystone 85% Gulfsands 78%Chariot Oil & Gas 81% Regal 32% Det Norske 81% Heritage Oil 55% Norse Energy 79%Tower Resources 72% Hardy Oil 22% Salamander 79% Dragon Oil 35% Serica 75%Desire Petroleum 48% Amerisur 60% Tullow 32% Coastal Energy 82%

Hardy Oil 22% Encore 38% Valiant Petroleum 64%Ithaca 52%DNO 64%Soco 34%

Melrose Resources 28%Enquest 28%

Premier Oil 22%Lundin Petroleum 14%

Balanced Exploration NOC‐driven M&A Others

Thematic, buy rated winners

Thematic exposure already in price (netural & sell rated stocks)

High impact exploration. Unconventional Gas Unconventional liquids

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 22

Oil price sensitivity and the E&Ps; higher fiscal risk, but lower commercial thresholds;

maintaining US$100/bl in our valuations

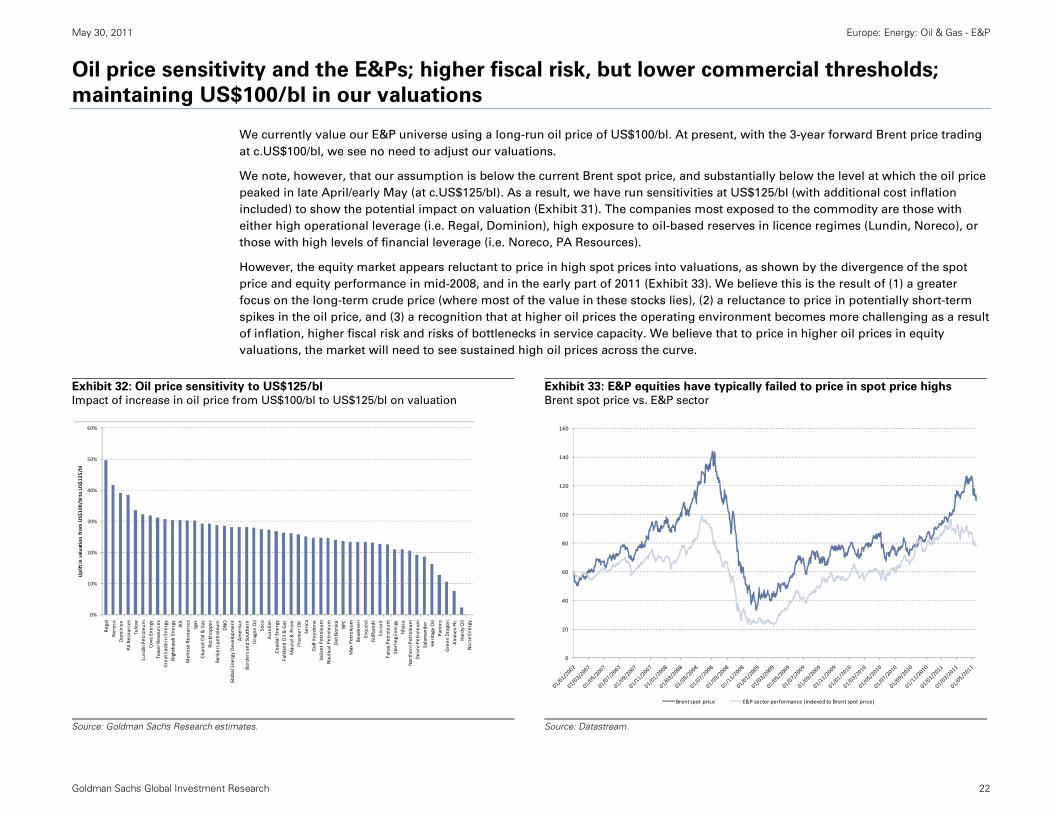

We currently value our E&P universe using a long-run oil price of US$100/bl. At present, with the 3-year forward Brent price trading

at c.US$100/bl, we see no need to adjust our valuations.

We note, however, that our assumption is below the current Brent spot price, and substantially below the level at which the oil price

peaked in late April/early May (at c.US$125/bl). As a result, we have run sensitivities at US$125/bl (with additional cost inflation

included) to show the potential impact on valuation (Exhibit 31). The companies most exposed to the commodity are those with

either high operational leverage (i.e. Regal, Dominion), high exposure to oil-based reserves in licence regimes (Lundin, Noreco), or

those with high levels of financial leverage (i.e. Noreco, PA Resources).

However, the equity market appears reluctant to price in high spot prices into valuations, as shown by the divergence of the spot

price and equity performance in mid-2008, and in the early part of 2011 (Exhibit 33). We believe this is the result of (1) a greater

focus on the long-term crude price (where most of the value in these stocks lies), (2) a reluctance to price in potentially short-term

spikes in the oil price, and (3) a recognition that at higher oil prices the operating environment becomes more challenging as a result

of inflation, higher fiscal risk and risks of bottlenecks in service capacity. We believe that to price in higher oil prices in equity

valuations, the market will need to see sustained high oil prices across the curve.

Exhibit 32: Oil price sensitivity to US$125/bl Impact of increase in oil price from US$100/bl to US$125/bl on valuation

Exhibit 33: E&P equities have typically failed to price in spot price highs Brent spot price vs. E&P sector

Source: Goldman Sachs Research estimates.

Source: Datastream.

0%

10%

20%

30%

40%

50%

60%

Regal

Noreco

Dom

inion

PA Resou

rces

Tullow

Lund

in Petroleum

Cove

Ene

rgy

Tower Resou

rces

Great Eastern Ene

rgy

Nighthawk Energy JKX

Melrose Resou

rces

Igas

Chariot O

il & Gas

Rockho

pper

Bankers p

etroleum DNO

Global Ene

rgy Develop

men

tAmerisur

Borders and

Sou

thern

Dragon Oil

Soco

Aurelian

Coastal Ene

rgy

Falkland

Oil & Gas

Maurel &

Prom

Prem

ier O

il Serica

Gulf K

eyston

eValiant Petroleum

Nautical Petroleum

Det Norske

BPC

Max Petroleum

Bowleve

nEnqu

est

Gulfsan

dsEncore

Faroe Pe

troleu

mSterling Energy

Ithaca

Northern Pe

troleu

mDesire Pe

troleu

mSalamande

r Heritage

Oil

Pano

roGreen

Dragon

Aminex

Plc

Hardy

Oil

Norse Ene

rgy

Uplift in valuation

from US$10

0/bl to

US$12

5/bl

0

20

40

60

80

100

120

140

160

Brent spot price E&P sector performance (indexed to Brent spot price)

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 23

Oil prices and commerciality - fiscal risk increases under higher oil prices

Higher oil prices do not necessarily result in higher valuations as they can also cause countries to adjust their fiscal regimes to

effectively tax away outsized returns gained through access to a country’s hydrocarbons. We believe that three factors are worthy of

consideration in assessing whether a country is at risk of adjusting its fiscal terms:

High returns for producers in the country. Countries need to ensure that companies continue activities and therefore low

returns are likely to reduce the likelihood of fiscal changes;

A low existing tax rate. If a government’s fiscal take is already high, a relatively large proportion of profits will go to the

government in any case and the possible delta by which to move the tax take is more limited

Assets are already producing. We believe there is less incentive to avoid changing the fiscal terms as oil companies in the

country will have already sunk substantial costs and will be less able to simply halt development. Most frontier areas remain at

lower tax rates until production begins (with Israel’s recent tax rise being a notable exception).

We show in Exhibits 33 and 34 the returns vs. tax take at US$85/bl (the 5-year forward price through most of 2009/2010) and at

US$110/bl. We believe in a sustained high oil price environment, tax rates in many countries to the right of the line in Exhibit 35 will

be at risk of change, although those countries with an immature or emerging industry may be reluctant to make changes to fiscal

regimes until production has been established.

Exhibit 34: High P/Is and low tax rates put outsized returns at risk Country tax rates vs. PIs for pre-sanction and under development projects

Exhibit 35: Higher oil price may lead to further tax increases Country tax rates vs. PI at US$110/bl

Source: Goldman Sachs Research estimates.

Source: Goldman Sachs Research estimates.

20%

30%

40%

50%

60%

70%

80%

90%

100%

1.00x 1.50x 2.00x 2.50x 3.00x 3.50x

Ove

rall

tax

take

PI ratio

Low returns and / or high existing tax rates limit chance

of fiscal renegotiation

High returns and relatively low existing tax rates increase risk of fiscal renegotiation

Algeria

Angola

Australia

Bolivia

Brazil

Canada

China

Congo

Egypt

Ghana

Indonesia

Iraq

Israel

Italy

Kazakhstan

LibyaMalaysia

Mozambique

Myanmar

Nigeria

Norway

Oman

Papua New Guinea

Peru

Qatar

Russia

Thailand

UAE

Uganda

UK

US

Venezuela

Vietnam

Israel - Top 280

UK - Top 280

20%

30%

40%

50%

60%

70%

80%

90%

100%

1.00x 1.50x 2.00x 2.50x 3.00x 3.50x

Ove

rall

tax

take

@ U

S$1

10/b

l

PI ratio @ US$110/bl

Low returns and / or high existing tax rates limit

chance of fiscal renegotiation

High returns and relatively low existing tax rates increase risk of fiscal

renegotiation

Algeria

Angola

Australia

Bolivia

Brazil

Canada

China

Congo

Egypt

Ghana

Indonesia

Iraq

Israel

Italy

KazakhstanLibya

Malaysia

Mozambique

Myanmar

Nigeria

Norway

Oman

Papua New Guinea

Peru

QatarRussia

Thailand

UAE

UK

US

VenezuelaVietnam

Uganda:PI 3.52x,

73%

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 24

Commercial thresholds drop at higher oil prices which should also drive de-risking

The other major impact of an increased oil price environment is that it allows commercialization of previously unattractive assets.

Although valuations of marginal assets increase at higher oil prices, we believe that there is rarely an additional increase in the

valuations equity markets ascribe to more marginal assets as a result of reductions in the commerciality risk at higher oil prices.

We highlight the North Falklands Basin as an asset where the market regards commerciality with a degree of scepticism as a result

of its relative isolation. Although we believe that these concerns are substantially overdone (with the use of FPSOs limiting the need

for major infrastructure in the area), we note that in the current oil price environment, concerns should be receding; at the current oil

price, even costs of over US$30/bl are comfortably commercial using a 15% hurdle rate. We do not believe that the market has fully

accounted for this impact in more marginal basins in our coverage, and we believe that projects perceived as marginal have seen

little de-risking in this higher oil price environment.

Exhibit 36: Higher oil prices should drive de-risking of more marginal assets IRR and NPV/bl of North Falklands asset at differing cost and oil price assumptions (assuming US$16/bl opex costs)

Source: Goldman Sachs Research estimates.

NPV12/bl US$70 US$85 US$100 US$115 US$130 IRR US$70 US$85 US$100 US$115 US$130$10 7.67 11.33 14.99 18.64 22.30 $10 50% 65% 79% 91% 102%$15 4.88 8.54 12.2 15.85 19.51 $15 29% 41% 52% 62% 71%$20 2.02 5.68 9.33 12.99 16.65 $20 18% 27% 36% 45% 53%$25 ‐0.84 2.81 6.47 10.13 13.78 $25 10% 18% 26% 33% 40%$30 ‐3.63 0.03 3.68 7.34 11.00 $30 5% 12% 19% 25% 31%

Uncommercial at 12% hurdle rate Uncommercial at 12% hurdle rateUncommercial at 15% hurdle rate Uncommercial at 15% hurdle rate

Oil price Oil price

F&D per barrel

F&D per barrel

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 25

Adjustment to long-term exploration discount

We previously applied a 50% discount to medium-term drilling catalysts, reflecting uncertainties with long-dated catalysts (timing of

drilling, resource updates following additional seismic, lack of CPRs, etc.). Following further analysis of the performance of stocks

into drilling campaigns, we note that performance into a major catalyst is far from uniform, with many stocks outperforming up to

two years before the campaign. Catalysts, such as the booking of rigs, CPRs etc., however continue to drive shares. As a result, we

remove the blanket discount we had previously used and replace it with asset-specific discounts to account for specific uncertainties

in the build up to drilling. We also apply these discounts to high-impact exploration prospects being drilled in the next 12 months,

where these prospects represent greater than 50% of a company’s valuation. We now adjust our chances of success for the

following:

Lack of 3D seismic over prospects, 15% discount to chance of success (CoS);

Lack of CPR, 20% discount to CoS;

Lack of rig booked, 10% discount to CoS.

Exhibit 37: Chariot Oil has outperformed steadily into drilling in Namibia…

Chariot Oil’s share price performance vs. E&P universe

Exhibit 38: …while much of Desire’s outperformance came over 12 months

before Desire’s share price performance vs. E&P universe

Source: Datastream.

Source: Datastream.

‐100%

0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

Seismic acquired (no sizes)

Increase in prospective resources

CPR (small decrease in prospective resource)

Nimrod structure identified

‐100%

‐50%

0%

50%

100%

150%

200%

250%

Farm in partner announced

Liz well dryRig booked

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 26

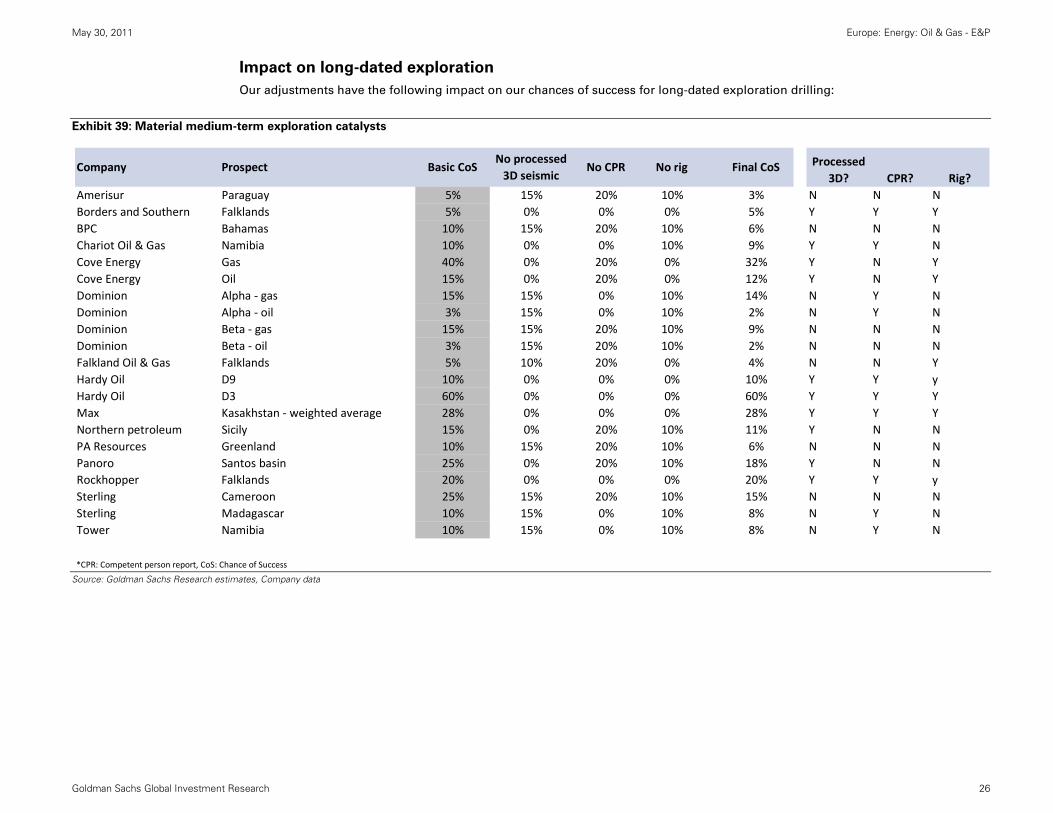

Impact on long-dated exploration

Our adjustments have the following impact on our chances of success for long-dated exploration drilling:

Exhibit 39: Material medium-term exploration catalysts

Source: Goldman Sachs Research estimates, Company data

Company Prospect Basic CoSNo processed 3D seismic

No CPR No rig Final CoS Processed 3D? CPR? Rig?

Amerisur Paraguay 5% 15% 20% 10% 3% N N NBorders and Southern Falklands 5% 0% 0% 0% 5% Y Y YBPC Bahamas 10% 15% 20% 10% 6% N N NChariot Oil & Gas Namibia 10% 0% 0% 10% 9% Y Y NCove Energy Gas 40% 0% 20% 0% 32% Y N YCove Energy Oil 15% 0% 20% 0% 12% Y N YDominion Alpha ‐ gas 15% 15% 0% 10% 14% N Y NDominion Alpha ‐ oil 3% 15% 0% 10% 2% N Y NDominion Beta ‐ gas 15% 15% 20% 10% 9% N N NDominion Beta ‐ oil 3% 15% 20% 10% 2% N N NFalkland Oil & Gas Falklands 5% 10% 20% 0% 4% N N YHardy Oil D9 10% 0% 0% 0% 10% Y Y yHardy Oil D3 60% 0% 0% 0% 60% Y Y YMax Kasakhstan ‐ weighted average 28% 0% 0% 0% 28% Y Y YNorthern petroleum Sicily 15% 0% 20% 10% 11% Y N NPA Resources Greenland 10% 15% 20% 10% 6% N N NPanoro Santos basin 25% 0% 20% 10% 18% Y N NRockhopper Falklands 20% 0% 0% 0% 20% Y Y ySterling Cameroon 25% 15% 20% 10% 15% N N NSterling Madagascar 10% 15% 0% 10% 8% N Y NTower Namibia 10% 15% 0% 10% 8% N Y N

*CPR: Competent person report, CoS: Chance of Success

May 30, 2011 Europe: Energy: Oil & Gas - E&P

Goldman Sachs Global Investment Research 27

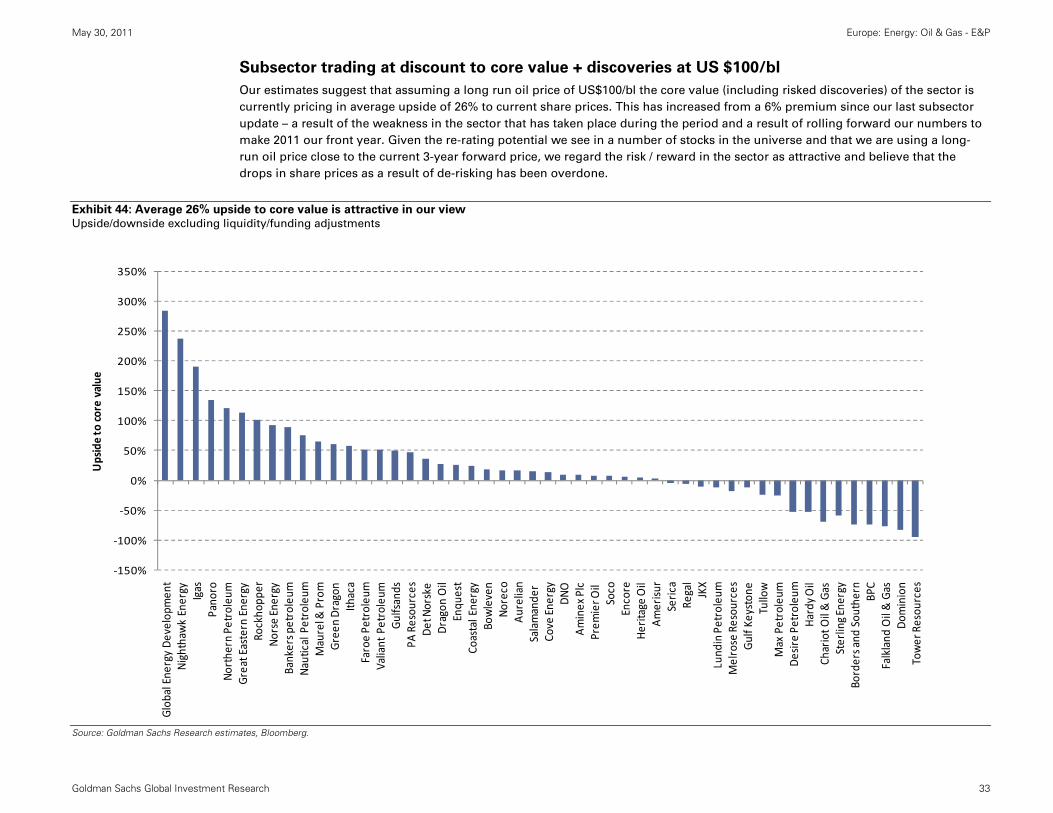

E&P screens; updating target prices and ratings

We make several adjustments to the valuations of the companies in our coverage, reflecting recent newsflow. As in our last

sub-sector publication on January 31, 2011, we use a US$100/bl oil price to value the E&Ps, broadly in line with the forward curve

and our 2011 oil price estimates. Our target prices imply average potential upside for the sector of 88%, (26% excluding exploration

value) and hence we retain our Attractive coverage view. We also update for movements in fx.

Exhibit 40: Target prices and ratings changes (sorted by upside potential to 12-month target price) % change from previous, does not include the impact of the roll-forward.

Source: Bloomberg, Goldman Sachs Research estimates. *Conviction List member.

# CompanyMarket cap (USDmn)

Current price

Previous target price

Updated target price (not rolled forward)

Updated target price (with roll‐forward)

New potential upside to target price

% change from

previous

Upside / downside to core value

12‐month re‐rating potential Old rating New rating Currency