EU SUSTAINABLE ENERGY WEEK ADVANCING ENERGY …

17

EU SUSTAINABLE ENERGY WEEK ADVANCING ENERGY EFFICIENCY FINANCE For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. Murray Birt DWS Senior ESG Strategist IIGCC Property Working Group Co-Chair Brussels – 12 June 2019

Transcript of EU SUSTAINABLE ENERGY WEEK ADVANCING ENERGY …

EU SUSTAINABLE ENERGY WEEK

ADVANCING ENERGY EFFICIENCY FINANCE

For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors.

Murray BirtDWS Senior ESG StrategistIIGCC Property Working Group Co-ChairBrussels – 12 June 2019

DWS IN A NUTSHELL

/ 2

Source: DWS AuM breakdown as at March 30, 2019. Images for illustrative purposes only

AUM BY ASSET CLASS AUM BY GEOGRAPHY

Germany43%

EMEA(ex Germany)

25%

Americas27%

APAC5%

AUM BY CLIENT TYPE

Retail45%

Institutional55%

A diversified business with strong responsible investing leadership

€704bn €704bn €704bn

RESPONSIBLE INVESTING

Track-record Award winning Climate focused Energy efficiency

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

Active Fixed

Income33%

Active Equity12%

Active SQI10%

Active Multi Asset7%Cash

8%Passive

18%

Alternatives12%

HOW INSTITUTIONAL INVESTORS CAN TARGET ENERGY EFFICIENCY

/ 3

Source: EEEF March 2019; DWS December 2018; GRESB 2018

Directly…Type of investment DWS example Market status

Direct energy efficiency project funds Investment manager for European Energy Efficiency fund – public sector buildings www.eeef.eu for EC/EIB

€158.5m active investmentscumulative 420k CO2 savings

There are a few other impact investment funds that directly target energy efficiency improvements

Private equity funds that target companies with new energy efficient and other technologies

China clean energy and environment fund (CEEF) - Raising and deploying capital

Private equity investors do target companies with new energy efficiency technologies

Real estate funds that target energyefficiency improvements

Seven of our largest direct real estate funds received Green Star from GRESB in 2018

€13.4bn of green labelled buildings as of December 2018

US energy reduction target set in 2010, met 3 years early (2016)

First energy reduction target begun in the UK in 2017

Additional energy reduction targets in Europe being established in 2019

903 property companies and funds participated in GRESB real estate sustainability assessment in 2018, representing USD 3.6 trillion in gross asset value

Represents 61% of major developed market listed real estate indices

~70% of these real estate investors had some sort of energy reduction target

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

HOW INSTITUTIONAL INVESTORS CAN TARGET ENERGY EFFICIENCY

/ 4

Source: DWS May 2019; Ceres March 2019; HSBC June 2019; CBI Sept 2018

Indirectly…Type of investment DWS example Market status

Public equity thematic funds (listed companies)

Actively managed Sustainable Development Goals fund

Climate tech fund

ESG low-carbon passive funds (ETFs)

HSBC: Globally, number of building energy efficiency technology related companies rose from 225 in 2010-11 to 410 in 2017-18;

14% have a market-cap greater than USD5bn.

Investor engagement / influence with companies, encouraging green policiesand CAPEX

Participation in Climate Action 100+

Strongest track-record for the last 6 years voting in favour of US climate related AGM resolutions. Many direct engagements with companies (see DWS Corporate Governance report)

300+ investors with €33 trillion in assets are participating in Climate Action 100+, encouraging companies to take stronger action

ESG bonds and Green bonds – refinancing

Green bond fund

Investing in green bonds for institutional clients

Energy efficient buildings are a small portion of overall green bond issuance (CBI Sept 2018)

Thought leadership / client education / policy engagement

Founding member and now steering group member of Energy Efficiency Financial Institutions Group (EEFIG)

Engaged policy makers on Clean Energy Package through Institutional Investors Group on Climate Change (IIGCC)

DWS client research reports include a focus on energy efficiency

Presenting at EU Sustainable Energy Week!

Policies strengthened but energy efficiency investment is still roughly flat (EuroACEMarch 2019)

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

PROBLEM #1

/ 5

Source: DWS analysis June 2019; Recurve June 2019; EnergyPro Sept 2018

Lack of connection with energy and financial marketsEnergy efficiency is mostly financed by a combination of individual savings, consumer loans and government

subsidy, unlike virtually any other part of the energy system.

The way we deliver EE (incentive programs funded by governments and utilities – EE obligations), and value energy efficiency is disconnected from the way we plan and manage our energy system. Verification is

expensive and takes too much time.

Energy supply companies cannot invest in or contract for the reduction in energy use in the same way that they currently invest in or contract for renewable energy.

Energy network companies cannot contract for the reduction in energy use as an alternative to network upgrades.

There are too few EE focused private sector financial institutions.

Creating a way for energy supply and network companies to measure energy efficiency with sufficient granularity could enable contracts for portfolios of energy efficiency projects

i.e. revenue which can be used for customer market based incentives for EuroPACE, EE mortgages etc and improved returns for investors/financiers

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

PROBLEM #2

/ 6

Source: California Energy Commission 2018; Stanford University May 2019 https://www.eurekalert.org/pub_releases/2019-05/su-1rd051719.php ; Recurve June 2019Picture for illustrative purposes only. Forecasts are based on assumptions, estimates, views and hypothetical models or analyses, which might prove inaccurate or incorrect.

Traditional ‘deemed’, annual average carbon reduction from energy efficiency and renewable energy will increasingly diverge from actual carbon reduction…risk of a ‘diesel-gate’ moment for EE and RE100?Stanford University report – May 2019: “Current methods of estimating greenhouse gas emissions use yearly averages, even though the carbon content of electricity on the grid can vary significantly over the course of a day in some locations.

By 2025, the use of yearly averages in California could overstate the greenhouse gas reductions associated with solar power by more than 50% when compared to hourly averages.”

“Two buildings that use the same kWh per month can have very different carbon footprints depending on when they consume energy and where they are located on the grid.” – Recurve June 2019

Using hourly [or more frequent] data is the best way to measure the environmental benefit of renewables [and energy efficiency – DWS], and this will become increasingly true wherever renewable generation is growing."

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

ADDRESSING THE PROBLEMS: MEASURING & VALUING THE TRUE ENERGY MARKET BENEFITS OF ENERGY EFFICIENCY Helping the benefits of smart meters to become real

Source: Recurve June 2019; www.recurve.com/open-source/how-it-worksCalTrack June 2019 www.caltrack.org/caltrack-history.htmlPicture for illustrative purposes only. Forecasts are based on assumptions, estimates, views and hypothetical models or analyses, which might prove inaccurate or incorrect.

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

Standard weights and measures are essential to any market, but is largely absent in EE

Estimating the counterfactual (what energy use would have been) is mostly standard practice in large non-residential EE projects. (M&V Measurement and Verification)

Estimates follow M&V standards but there is substantial subjectivity on how savings are calculated – different answers possible if calculations are done by different people on the same project.

Metered energy efficiency takes M&V principles and embeds them in an automated software platform. Combines smart meter with weather data in a fixed, open source method

Taking a portfolio approach across home retrofit projects can give a highly accurate evaluation of the weather-normalised savings…projects exceed/under-perform

Managing EE as a portfolio In 2012, California started to create a set of empirically tested methods to standardize the way normalized meter-based changes in energy consumption are measured and reported

This approach is transforming energy efficiency practices in California, Oregon, Washington, New York and other US states

/ 7

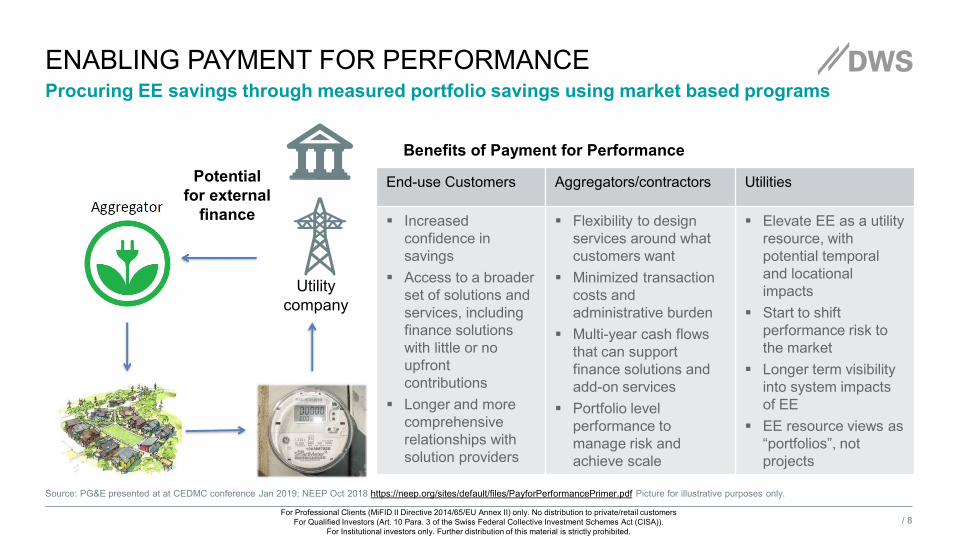

ENABLING PAYMENT FOR PERFORMANCE

/ 8

Source: PG&E presented at at CEDMC conference Jan 2019; NEEP Oct 2018 https://neep.org/sites/default/files/PayforPerformancePrimer.pdf Picture for illustrative purposes only.

Procuring EE savings through measured portfolio savings using market based programs

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

Utility company

Potential for external

finance

End-use Customers Aggregators/contractors Utilities

Increased confidence in savings

Access to a broader set of solutions and services, including finance solutions with little or no upfront contributions

Longer and more comprehensive relationships with solution providers

Flexibility to design services around what customers want

Minimized transaction costs and administrative burden

Multi-year cash flows that can support finance solutions and add-on services

Portfolio level performance to manage risk and achieve scale

Elevate EE as a utility resource, with potential temporal and locational impacts

Start to shift performance risk to the market

Longer term visibility into system impacts of EE

EE resource views as “portfolios”, not projects

Benefits of Payment for Performance

A NEW COMPONENT TO SMART FINANCE FOR SMART BUILDINGS

/ 9

Source: DWS June 2019; EnergyPro Sept 2018. For illustrative purposes only.

Potential next steps for Europe

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

1. Build on EU’s partnership with California to establish knowledge exchange, cooperation and high level public/private missions: Advanced Energy Efficiency Measurement and Finance Partnership

2. As part of more regular & structured private sector participation in EE Concerted Action, incorporate metered EE & P4P into Member State discussions on policy implementation

3. Start to pilot, then require metered EE and P4P within utility obligation schemes (EED Article 7) with rapid start EU support, followed by H2020 and other programme support

4. Incorporate metered EE & P4P into EU policy/program development, discussions with utilities, networks, smart grid/meters

5. Start to pilot, then require metered EE and P4P on all EE projects supported by EU / EIB

6. Convene finance led, EE expert industry group to assess adoption of CalTRACK in Europe

7. Assess potential for adding metered EE & P4P into EU funding for emerging economies with improving EE policy frameworks

APPENDIX

Name of speaker / Name of event / Date / 10

RESPONSIBLE INVESTMENT RESEARCH OVERVIEW

“Highly Commended”Sustainable Finance Report #2,

June 2017

Source: DWS, November 2018; Savvy Investor June 2017; Investment Week 2018https://dws.com/solutions/esg/research/For illustrative purposes only. Savvy Investor is the world’s leading resource hub for institutional investors. They curate the best pensions and investment white papers from around the world. The Savvy Investor Awards are judged on the basis of the quality and readability of the paper and its appeal to their institutional investor audience. No fee was paid to be considered for the award. Investment Week Awards are designed to highlight investment research services that demonstrate knowledge, innovation, engagement, clarity and transparency. No fee was paid to be considered for the award.

The task of the ESG thematic research team is to support clients and investment teams to understand and consider major sustainability risks and opportunities in their everyday business

DWS finalist for Best ESG

Research Team

DWS finalist for Best ESG Fund Management Group,

Best ESG Research Team &Best Thought Leadership Paper

(physical risk)

/ 11

DEVELOPMENT TIMELINE OF METERED EE AND PAYMENT FOR PERFORMANCE (P4P)

/ 12

Source: https://www.caltrack.org/caltrack-history.html ; https://www.recurve.com/blog ; https://www.greentechmedia.com/search/results?keywords=matt%2520golden

2012: California Public Utilities Commission (CPUC) decides to broaden allowable software under home Energy Upgrade California program

2013-present – continuous development of CalTRACK - a set of empirically tested methods to standardize the way normalized meter-based changes in energy consumption are measured and reported.

Spring 2015 – California experts and PG&E advocate for Payment for Performance

October 2015 – California passes SB350/AB802 –includes CPUC authorisation for investor owned utilities to run meter based energy savings programs

December 2015 – regulation authorising PG&E to undertake P4P

2016 – CPUC ruling allowing metered EE M&V framework; PG&E whole building testing of reliability of billing estimates

Nov 2016 – PG&E issues first RfP for residential EE payment for performance

July 2017 – PG&E awards first two P4P contracts

Nov 2017 – PG&E issues second RfP for residential P4P

California leadership

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

WHAT ARE THE BENEFITS?

/ 13

Source: Recurve March 2019; Home Energy Analytics presented at CEDMC conference Jan 2019;Picture for illustrative purposes only. Forecasts are based on assumptions, estimates, views and hypothetical models or analyses, which might prove inaccurate or incorrect.

Happy customers, robust data for contractors, utility companies & regulators, lower carbon emissions, more economic activity

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

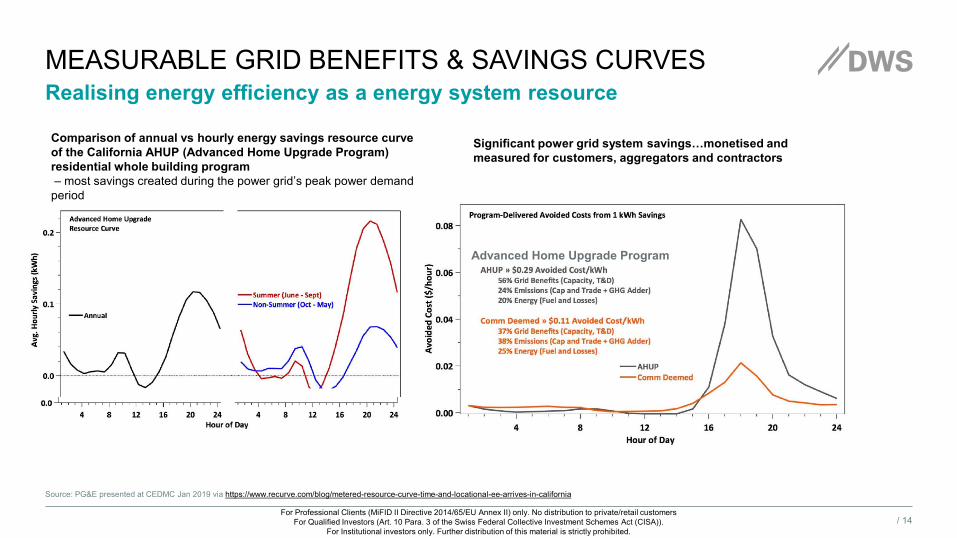

MEASURABLE GRID BENEFITS & SAVINGS CURVES

/ 14

Source: PG&E presented at CEDMC Jan 2019 via https://www.recurve.com/blog/metered-resource-curve-time-and-locational-ee-arrives-in-california

Realising energy efficiency as a energy system resource

Advanced Home Upgrade Program

For Professional Clients (MiFID II Directive 2014/65/EU Annex II) only. No distribution to private/retail customersFor Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

For Institutional investors only. Further distribution of this material is strictly prohibited.

Comparison of annual vs hourly energy savings resource curve of the California AHUP (Advanced Home Upgrade Program) residential whole building program– most savings created during the power grid’s peak power demand

period

Significant power grid system savings…monetised and measured for customers, aggregators and contractors

DISCLAIMERS (1/2)

/ 15

Issued in the UK by DWS Investments UK Limited. DWS Investments UK Limited is authorised and regulated by the Financial Conduct Authority.

Any reference to “DWS”, “Deutsche Asset Management” or “Deutsche AM” shall, unless otherwise required by the context, be understood as a reference to DWS Investments UK Limited including any of its parent companies, any of its or its parents affiliates or subsidiaries and, as the case may be, any investment companies promoted or managed by any of those entities.

This document is a “non-retail communication” within the meaning of the FCA's Rules and is directed only at persons satisfying the FCA’s client categorisation criteria for an eligible counterparty or a professional client. This document is not intended for and should not be relied upon by a retail client.

This document is intended for discussion purposes only and does not create any legally binding obligations on the part of DWS Group GmbH & Co. KGaA and/or its affiliates (DWS). Without limitation, this document does not constitute an offer, an invitation to offer or a recommendation to enter into any transaction. When making an investment decision, you should rely solely on the final documentation relating to the transaction and not the summary contained herein. DWS is not acting as your financial adviser or in any other fiduciary capacity in relation to this transaction. The transaction(s) or products(s) mentioned herein may not be appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understand the transaction and have made an independent assessment of the appropriateness of the transaction in the light of your own objectives and circumstances, including the possible risks and benefits of entering into such transaction. For general information regarding the nature and risks of the proposed transaction and types of financial instruments please go to https://www.db.com/company/en/risk-disclosures.htm. You should also consider seeking advice from your own advisers in making this assessment. If you decide to enter into a transaction with DWS, you do so in reliance on your own judgment.

Although information in this document has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness, and it should not be relied upon as such. All opinions and estimates herein, including forecast returns, reflect our judgment on the date of this document and are subject to change without notice and involve a number of assumptions which may not prove valid.

Any opinions expressed herein may differ from the opinions expressed by Deutsche Bank AG and/or any other of its affiliates (DB). DB may engage in transactions in a manner inconsistent with the views discussed herein. DB trades or may trade as principal in the instruments (or related derivatives), and may have proprietary positions in the instruments (or related derivatives) discussed herein. DB may make a market in the instruments (or related derivatives) discussed herein.

DWS SPECIFICALLY DISCLAIMS ALL LIABILITY FOR ANY DIRECT, INDIRECT, CONSEQUENTIAL OR OTHER LOSSES OR DAMAGES INCLUDING LOSS OF PROFITS INCURRED BY YOU OR ANY THIRD PARTY THAT MAY ARISE FROM ANY RELIANCE ON THIS DOCUMENT OR FOR THE RELIABILITY, ACCURACY, COMPLETENESS OR TIMELINESS THEREOF.

This document has been prepared without consideration of the investment needs, objectives or financial circumstances of any investor. Before making an investment decision, investors need to consider, with or without the assistance of an investment adviser, whether the investments and strategies described or provided by DWS, are appropriate, in light of their particular investment needs, objectives and financial circumstances. Furthermore, this document is for information/discussion purposes only and does not constitute an offer, recommendation or solicitation to conclude a transaction and should not be treated as giving investment advice.

DWS does not give tax or legal advice. Investors should seek advice from their own tax experts and lawyers, in considering investments and strategies suggested by DWS. Investments with DWS are not guaranteed, unless specified.

FOR PROFESSIONAL CLIENTS ONLY

DISCLAIMERS (2/2)

/ 16

Investments are subject to various risks, including market fluctuations, regulatory change, counterparty risk, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you may not recover the amount originally invested at any point in time. Furthermore, substantial fluctuations of the value of the investment are possible even over short periods of time.

This document contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models and hypothetical performance analysis. The forward looking statements expressed constitute the author’s judgment as of the date of this material. Forward looking statements involve significant elements of subjective judgments and analyses and changes thereto and/or consideration of different or additional factors could have a material impact on the results indicated. Therefore, actual results may vary, perhaps materially, from the results contained herein. No representation or warranty is made by DWS as to the reasonableness or completeness of such forward looking statements or to any other financial information contained herein. The terms of any investment will be exclusively subject to the detailed provisions, including risk considerations, contained in the offering documents.

This document may not be reproduced or circulated without our written authority. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, including the United States, where such distribution, publication, availability or use would be contrary to law or regulation or which would subject DWS to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

© DWS Investments UK Limited June 2019.

Disclaimer – EMEA - The following document is intended as marketing communication. Important Information

DWS is the brand name under which DWS Group GmbH & Co. KGaA and its subsidiaries operate their business activities. Clients will be provided DWS products or services by one or more legal entities that will be identified to clients pursuant to the contracts, agreements, offering materials or other documentation relevant to such products or services.

The information contained in this document does not constitute investment advice.

All statements of opinion reflect the current assessment of DWS Investments UK Limited and are subject to change without notice.

Forecasts are not a reliable indicator of future performance. Forecasts are based on assumptions, estimates, opinions and hypothetical performance analysis, therefore actual results may vary, perhaps materially, from the results contained here.

Past performance, [actual or simulated], is not a reliable indication of future performance.

The information contained in this document does not constitute a financial analysis but qualifies as marketing communication. This marketing communication is neither subject to all legal provisions ensuring the impartiality of financial analysis nor to any prohibition on trading prior to the publication of financial analyses.

This document and the information contained herein may only be distributed and published in jurisdictions in which such distribution and publication is permissible in accordance with applicable law in those jurisdictions. Direct or indirect distribution of this document is prohibited in the USA as well as to or for the account of US persons and persons residing in the USA.

DWS Investment International GmbH. As of: June 2019

RISK FACTORS

/ 17

Investments are subject to various risks, including market fluctuations, regulatory change, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you may not recover the amount originally invested at any point in time. Furthermore, substantial fluctuations of the value of the investment are possible even over short periods of time. An investment in infrastructure involves high degree of risk, including possible loss of principal amount invested, and is suitable only for sophisticated investor who can bear such losses. The operation and cash flows of infrastructure debt obligors may depend, in some cases to a significant extent, upon prevailing market prices for commodities such as oil, gas, coal, electricity, steel or concrete. Investments in commodities are subject to risk, including possible loss of invested capital. The price of commodities (e.g. raw industrial materials such as gold, copper and aluminum) may be subject to substantial fluctuations over short periods of time and may be affected by unpredictable international monetary and political policies. Additionally, valuations of commodities may be susceptible to such adverse global economic, political or regulatory movements, regulatory changes, economic changes and adverse political or financial factors could have a significant impact on performance. An investment in real estate involves a high degree of risk, including possible loss of principal amount invested, and is suitable only for sophisticated investors who can bear such losses. The value of shares/units and their derived income may fall or rise. Investment in real estate may be or become nonperforming after acquisition for a wide variety of reasons. Nonperforming real estate investment may require substantial workout negotiations and/or or restructuring. Environmental liabilities may pose a risk such that the owner or operator of real property may become liable for the costs of removal or remediation of certain hazardous substances released on, about, under, or in its property. Additionally, to the extent real estate investments are made in foreign countries, such countries may prove to be politically or economically unstable. Finally, exposure to fluctuations in currency exchange rates may affect the value of a real estate investment. Investments in Real Estate are subject to various risks, including but not limited to the following:— Adverse changes in economic conditions including changes in the financial conditions of tenants, buyer and sellers, changes in the availability of debt financing, changes in interest rates, real estate tax rates and other operating expenses;— Adverse changes in law and regulation including environmental laws and regulations, zoning laws and other governmental rules and fiscal policies;— Environmental claims arising in respect of real estate acquired with undisclosed or unknown environmental problems or as to which inadequate reserves have been established;— Changes in the relative popularity of property types and locations;— Risks and operating problems arising out of the presence of certain construction materials; and— Currency / exchange rate risks where the investments are denominated in a currency other than the investor’s home currency