ETHICAL CONSUMERISM AN OPPORTUNITY FOR INDIAN HANDCRAFTED AND HANDLOOM TEXTILE SECTORS

Upload

noorani-biswasCategory

view

100download

1

1

ETHICAL CONSUMERISM: AN OPPORTUNITY FOR INDIAN HANDCRAFTED AND HANDLOOM TEXTILE SECTORS

RESEARCH PROJECT

BY

NOORANI BISWAS

12DFT0025

2

INDEX

SL.NO. CHAPTER PAGE

1 TITLE, OBJECTIVE AND RESEARCH METHODOLOGY 3

CHAPTER PLAN

2 INTRODUCTION TO ETHICAL CONSUMERISM 4

3 GREEN AND ETHICAL FASHION 5

4 ETHICAL ALTERNATIVES IN FASHION 6

5 GLOBAL INNOVATION FOR SUSTAINABILITY: TEXTILE AND APPAREL INDUSTRY 8

6 PURCHASE BEHAVIOUR TOWARDS ETHICAL PRODUCTS 10

7 SURVEY RESULTS 12

8 ECOLABELS, INTERNATIONAL ORGANISATIONS FOR CERTIFICATION OF SUSTAINABLILITY AND ECOLABELS IN TEXTILE AND APPAREL INDUSTRY 16

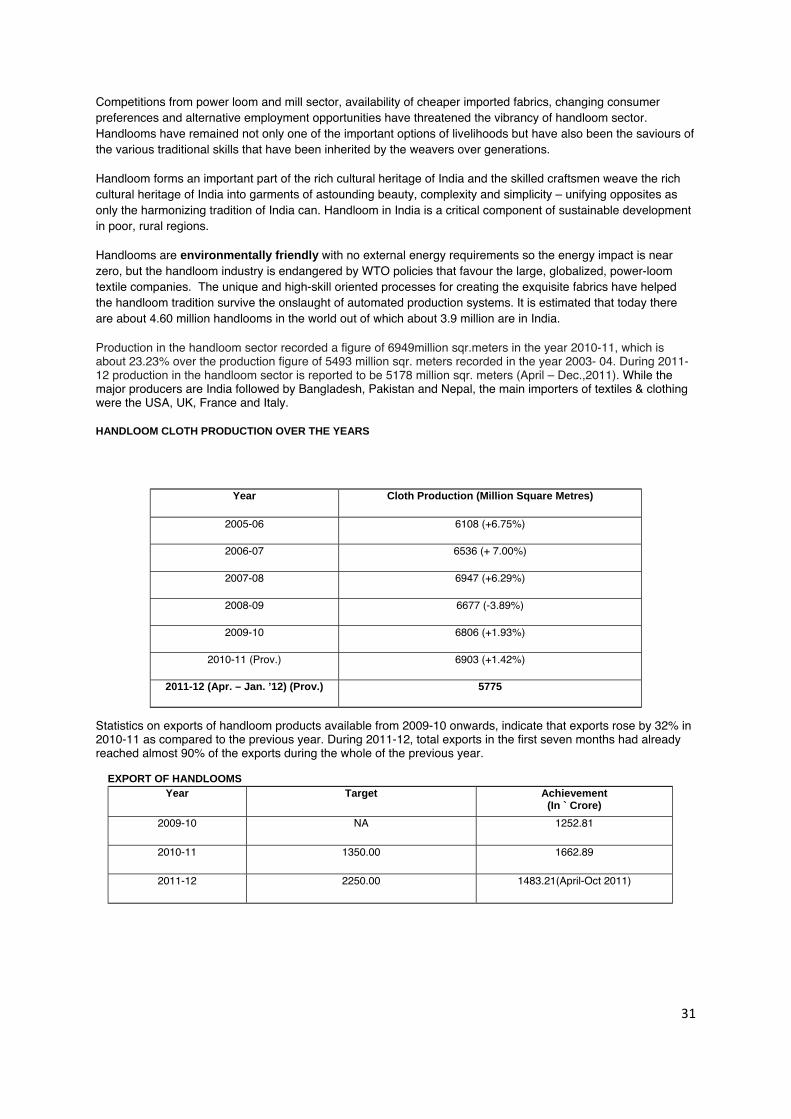

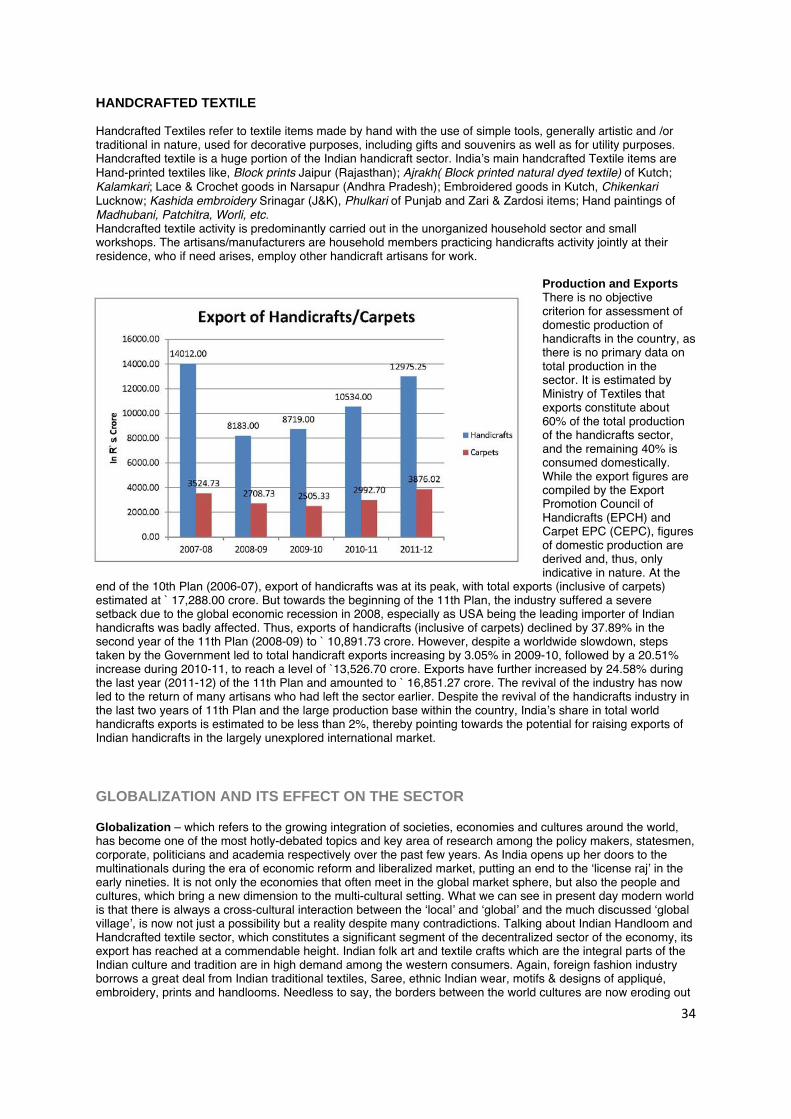

9 INTRODUCTION: INDIAN HANDLOOM AND HANDCRAFTED TEXTILE SECTOR 30

10 GLOBALIZATION AND ITS EFFECT ON THE SECTOR 34

11 GOVERNMENT STEPS TO SUPPORT THE HANDLOOM AND HANDCRAFTED TEXTILE SECTOR 37

12 MAJOR CHALLENGES FACING THE HANDLOOM SECTOR 44

13 MAJOR CHALLENGES FACING THE HANDICRAFTS SECTOR 46

14 ETHICAL STAND OF INDIAN HANDLOOM AND HANDCRAFTED TEXTILE SECTOR 48

15 ETHICAL CERTIFICATION ORGANIZATIONS IN INDIA

50

16 PERCEPTION OF ETHICAL CONSUMERS TOWORDS HANDCRAFTED AND HANDLOOM TEXTILE PRODUCTS

52

17 OPPORTUNITIES TO HANDCRAFT AND HANLOOM TEXTILE PRODUCER DUE TO ETHICAL CONSUMERISM

52

18 CHALLENGES TO HANDCRAFT AND HANLOOM TEXTILE PRODUCER DUE TO ETHICAL CONSUMERISM

53

19 CONCLUSION 53

20 BIBLIOGRAPHY 54

3

TITLE

ETHICAL CONSUMERISM: AN OPPORTUNITY FOR INDIAN HANDCRAFTED AND HANDLOOM TEXTILE SECTORS

OBJECTIVE

The main objective is firstly, to closely analyse the consumer activism of ethical sourcing, which is creating awareness among consumers to buy products which is ethical, in the sense of socially responsible, environment friendly and economical. How Ethical consumerism is effecting on the purchase of green and ethical product?

Secondly, to research the current scenario of Indian handcrafted and handloom textile sectors in Globalization.

And thirdly, to analyse the opportunities created by the ethical consumerism for the Indian Handcrafted and Handloom textile sectors, which can be leveraged in its growth.

RESEARCH METHODOLOGY

Primary Data Collection: Customer survey to analyse the mentality of Indian youth towards Ethical product. Indian exporters and market demand survey through questioners.

Secondary Data Collection: Articles, books, research document, Case studies, etc.

4

CHAPTER PLAN

Introduction to Ethical consumerism Ethical Consumerism is a type of consumer activism practiced through 'positive buying' in that ethical products are favoured, or 'moral boycott', that is negative purchasing and company-based purchasing. An increasing number of people make their consumption decisions on the basis of ethical values, such as environmentally friendly products and production methods, labour standards (wage rates and working conditions), and human rights. Ethical consumerism is a growing phenomenon that underpins ethical trade activities. The term "ethical consumer", now used generically, was first popularised by the UK magazine the Ethical Consumer, first published in 1989. Ethical Consumer magazine's key innovation was to produce 'ratings tables,' inspired by the criteria-based approach of the then emerging ethical investment movement. Ethical Consumer's ratings tables awarded companies negative marks (and from 2005 overall scores) across a range of ethical and environmental categories such a 'animal rights', 'human rights' and 'pollution and toxics', empowering consumers to make ethically informed consumption choices and providing campaigners with reliable information on corporate behaviour. Consumption is not a straightforward process. When we buy a commodity we are also responsible for the process it goes through to reach us. Under what conditions was an item of clothing or a new computer manufactured? Were workers paid fair wages? Were they exposed to harmful substances during the production process? Which products and which companies do I want to support with my purchases? Do I buy food in a supermarket, around the corner at a local vendor or at a weekly outdoor market? How will the product ultimately perish – will its destruction lead to polluting the earth, water or air? The term “ethical consumption” refers to selective consumption based on awareness of the environmental, social and economic aspects of consumption.

5

GREEN AND ETHICAL FASHION

People around the world have become more concerned about environmental (ʻgreenʼ) issues. They worry about climate change, greenhouse gas emissions, fuel prices, and the impact that products may have on the environment. Public awareness of the escalating problems due to diminishing natural resources is helping focus attention on the need to adopt sustainable and healthy lifestyles. This scenario has fuelled the latest trend of ethical fashion.

Sustainable clothing and green eco fashion have entered mainstream consumer consciousness with a barrage of recent media attention. Itʼs now hip to show off your green and ethical credentials and the fashion industry has joined the party.

But what really is sustainable clothing and is it different from eco or organic clothing? While concepts of “sustainable clothing” and “organic clothing” share many similarities, they have different roots and history. Where organic clothing grew and evolved out of the organic agriculture movement, sustainable clothing is a product of the environmental movement. They are both working towards the same ends but one has the feel of the farm and the other has the feel of the lab. One of the most apparent differences between the organic approach and the sustainable approach is the emphasis that the sustainable approach places on reuse and recycling of manufactured products.

Improving a corporationʼs sustainability footprint and reducing environmental impact is about more than just recycling materials. It requires a more holistic corporate approach that includes reusing environmentally-friendly packaging, reducing manufacturing and operational waste and pollution, improving building energy efficiency and reducing energy consumption, moving towards the use of renewable energy, improving shipping and transportation efficiencies, and designing sustainability into the products and services that are sold to the public.

TEXTILE ECOLOGY

To analyse the sustainability and ethicalness of a Textile product, we need to analyse the life cycle assessment of textile or Textile ecology. Textile ecology consists of four sectors: production ecology, human ecology, performance ecology and disposal ecology.

Production ecology It examines the impact of production processes on people and environment, e.g. occupational health and safety, material, water and energy consumption, waste water and waste treatment as well as generation of dust and noise. Human ecology Human ecology deals with the impact of textiles and their chemical ingredients on the health and well-being of humans. Performance ecology Performance ecology comes in at the usage phase of textile products. It examines the environmental impact of washing, cleaning and caring for textiles. Disposal ecology Analyses the problems connected with disposal, reuse, recycling and removal (thermal recycling or landfill) of textiles.

6

ETHICAL ALTERNATIVES IN FASHION Organic Cotton Cotton might appear to be the best choice for people looking for natural clothing but it is the worldʼs most heavily sprayed crop, around 150g of pesticide and fertilizer might be used to grow the cotton for a single T –shirt, and cotton farmerʼs account for 10% of all pesticides used. In developing countries, poor untrained and ill-equipped farmers are often expected to use some of the most hazardous pesticides available. The alternative of farming organically without the use of pesticides, is more difficult but it saves lives and improve health. Many have seen for themselves the effects of chemical farming – soil erosion and loss of soil nutrients, loss of nutrition in food, and human diseases resulting from the chemicals that inevitably seep into the water table, go directly to the users blood stream, which consequently affect's the body's organs and tissues, all the reasons for the urgent demand for organic foods and farming. Besides the naturally soft organic cotton fabric is a lot more comfortable to use and is available at competitive prices. Organic cotton textiles have evolved from being a niche product for the environment-conscious consumers to emerging as a highly fashionable product sold in major fashion boutiques and renowned fashion houses. Organic cotton is the cotton produced without employing chemical fertilizers and pesticides on plants that are not modified genetically. The organic production of cotton provides benefits not only for the environment and human health, but also for the socio-economic situation of farmers. The market is currently in evolving stage and is projected to expand significantly in the near term. India, Syria, and Turkey account for more than 85% of the global organic cotton production .The United States represents the leading consumer of organic cotton and eco-textiles. The nation accounts for 40% of the organic cotton consumption in apparel products.

Organic Wool Despite the fact that wool is a natural fibre, its processing is far from being eco friendly. Conservative woolmaking process creates adverse results in the environment and livestock health. Animals are subjected to synthetic pesticides, synthetic hormones, or genetic engineering. Organic wool has been produced using eco-friendly methods. It comes from sheep bred under holistic environment, in natural and healthy conditions. Organic wool is cleaned using biodegradable cleaning agents. Processing of raw wool and converting them into fabric isdone without exposure to harsh chemicals. Organic woollen clothes are non allergenic, and hence can be worn by people with chemical sensitivities. Adopting sustainable options in the entire value chain is one of the driving forces of the textile sector today.Smart innovations are the main influencing factor for the development of sustainable textiles. Organic and Peace Silk Silk, the “Queen of Fibre”. Darling of the haute couture set for the luxurious feel and drape. Even though silk is a natural fibre, but how organic, sustainable, ethical and healthy is silk? The finest, most desirable silk comes from the mulberry silkworm, which is actually a caterpillar and not a worm. Known as the Bombyx mori by entomologists. Bombyx mori moth eats only mulberry leaves. One acre of mulberry trees produces enough foliage to feed silkworms that create 178 pounds of cocoons which can beunravelled into 35 pounds of raw silk. The mulberry leaves are a renewable and sustainable crop as the treesproduce year after year. One mature mulberry tree will produce enough foliage for 100 silkworms. The raw silk threads are produced easily to comply with emerging sustainable and organic standards for silk and be manufactured into silk eco-fashion and organic clothing, except for this a 3 inch ethical problem – the Bombyx mori silkworm that is gassed, steamed, or boiled alive to prevent them from escaping from their cocoon as a mothby dissolving a hole in the silk cocoon. To make one pound of the finest silk, 2600 silkworms must die.Fortunately there is an ethical alternative to this, some silk manufactures doesnʼt kill the worms inside the cocoonand let them come out of it. Silk from the damaged cocoon are then spun into yarn like cotton, instead of reeling.This type of silk is known as Vegetarian silk or Peace silk. The Bombyx mori silkworm is not the only silkworm that spins a silk cocoon that can be used to produce silkfabric for silk clothing. There are many species of wild silk caterpillars that produce silk cocoons used in theproduction of silk fabrics, sometimes called “wild silks” or “peace silks” because the silk caterpillars are allowed tolive complete and natural lives in the wild without being sacrificed for fashion. Some of the wild silkworms which are domesticated are Eri, Muga, Tussar. Most wild silkworms are multivoltine, which means that they producecocoons several times during the year rather than just once a year like the Bombyx mori. One of the highly desirable properties of the Bombyx mori silk fibres due to the unique structure of their fibroin protein is their exceptional ability to absorb dyes; wild silk caterpillars secrete a slightly different protein structure and their silk fibres tend to not accept dyes as well, is one reason for the brilliance and luster of dyed silk fabrics.

7

Cellulosic Fibres Rayon, modal and lyocell are produced from renewable cellulosic plants such as beech trees, pine trees, and bamboo. All three fibers are biodegradable. Specifically, Lenzing Viscose® and Lenzing Modal® are produced from sustainably harvested beech trees and Tencel® from sustainably harvested eucalyptus trees. Eucalyptus grows quickly and without irrigation, pesticides, fertilizers or genetic manipulation; it can also be planted on marginal land that cannot be used for food crops. The fiber yield per acre from the trees used in the Lenzing fibers is up to ten times higher than that of cotton. Also, cotton needs up to 20 times more water.

However, there are many manufacturers of rayon. Even with the advancements that have been made over time, most rayon manufacturing processes in use today are not considered environmentally friendly. In fact, they use a range of polluting chemicals and heavy metals. On the other hand, lyocell manufacturing, and that of Tencel® in particular, is an extremely environmentally friendly process and the friendliest of these three fibres.

Since regenerated fibres do not qualify for organic certification, other recognized eco standards that review the entire process chain for growing and harvesting the trees through the manufacturing and treatment processes must be applied to these fibres. One such award that has been given to Lenzing for Tencel® is the European Eco-Label, which addresses compliance with high environmental standards for production and products.

As early as 1963, Lenzing started recycling the chemicals from pulp production after the company switched from the calcium bisulphite method to an environmentally friendly magnesium bisulphite method. The revolutionary aspect of Tencel® manufacturing is the recovery and reuse of up to 99.8 percent of the solvent and the remaining emissions are broken down in biological water treatment plants. In fact, the solvent is not acidic, does not remain in the fibre, and has been proven harmless in dermatological and toxicological tests.

Finally, we need to remember that much of the total environmental impact of textile goods comes from their care. With lyocell fabrics, there is no need for fabric softener or whitening agents, and energy and water use can be decreased due to shorter washing machine cycles. So with this knowledge and careful shopping for respected eco-friendly labels, you can buy textiles from manufactured fibres that can be considered to be green.

Bio based alternatives

Cotton and polyester, together, account for over 80% of the world clothing output. They have dominated the market because they were available in abundance and cheap, but they both have sustainability issues in their different ways. According to a report in Eco Textiles, a full life cycle analysis can show an accurate assessment of the environment al impact of any fibre. Among the issues, the growing of crops for raw material using land, which could be for food, is questionable, and that includes cotton and corn (for bio plastics). The polyester industry believes that viable alternative will be available with advances in renewable energytechnology. Textiles made from biopolymers derived from renewable materials (such as corn) are likely toincrease in the coming years, reducing dependence on oil based polymers. Biopolymers are biodegradable, and their inherent properties make them suitable for protecting from moisture, increasing shelf life, and easier to dispense. DuPont has expansion plans for its sorona biopolymer into textiles, while producers such as Proctorand Gamble have committed to replace 25% of their non-renewable materials by renewable or recycled alternatives by 2020.

Natural Dyes More chemicals are used in the making of textiles which are carcinogenic in nature. Textile industry is currently concerned about the use of natural dyes sourced from plants, minerals, and animals. Vegetable dyes are found in most of the plant tissues. Litchens are rich source of vegetable dyes. Other plants such as onion, mango, pomegranate, etc are also rich in dye content. Secretions of insects such as lucca, cochineal, and kermes are used for dye extracts. As far as mineral dyes are concerned, oxides of iron, tin, and antimony are used along with vegetable or insect dyes. Natural dyes not only release medicinal properties but also improve the aesthetic value of the product. They are unique, and eco-friendly.

8

GLOBAL INNOVATION FOR SUSTAINABILITY: TEXTILE AND APPAREL INDUSTRY

Global awareness and demand for sustainability has spurred industries to develop process and systems to bring sustainable and ethical principles. Companies are focusing that, the need of their consumers are met without much damage to the environment. During the past few years, with the wake of global warming effects, sustainability has gained increased importance among businesses. New methods are applied in business practices to reduce pollution by better utilization of raw materials, and also to improve financial results. Technological improvements help to foster sustainable business practices.

Sustainability is recognised as a major concern throughout the textile and garment industry. Innovative solution has not only improved production at each stage of the textile and garment chain, but also save on costs, energy, chemical inputs, water and waste, ultimately reduces emission. Innovative technologies are designed, developed, and marketed around the world. The speed of innovation has increased and technological landscape is going through rapid changes, reversing the negative effects of the textile industry.

INNOVATION IN DYE AND FINISHING TECHNIQUES

Textile sector use a lot of water in fabric dyeing and finishing traditionally. There is a strong need to reduce the use of water in these processes to achieve sustainability. New technologies for sustainable solutions for dyeing and finishing were evident in international fairs like ITMA, a vast international textile machinery fair held every four years (in Barcelona 2011).

Denim Industry: Fading and trashing denim jeans is enduringly popular, as well as posing a health risk for workers. Until now, it has been done most often through blasting a spray of sand at a garment to remove the top surface of the fabric, which then becomes fade and abraded with washing for a pre-worn look. But, this process is potentially hugely damaging to the health of textile workers, who can inhale air borne dust. Prompted by health concerns, some major denim brands have now banned suppliers from sandblasting denims, which is a significant step. Laser technologies can create the ʻusedʼ effects on denim without using any water, or any unhealthy techniques. The laser maps out the washing details etching them into the surface of the denim to imitate real aging and worn effects. The systems allow for savings in energy, water, chemicals, and it is infinitely faster. Between 100 and 200 jeans can be produced per hour, while manual scraping produces only 10 units per hour, sandblasting 30 and spraying 60.

Spanish company Jeanologia, which has long been a pioneer in the development of laser for textiles and making machines for laundering denim since 1985. The company has been developing advanced techniques both wet and dry denim garment processing. Washing denim jeans is one of the most polluting activities in the apparel industry. According to Jeanologia, in terms of usage, one pair of jeans uses 70 litres water, 1.5 kwatt of electricity, and 150gms chemicals. But by using a different method of finishing to achieve the ʻusedʼ look, says Jeanologia, this can be reduced to 20 litres water, 1.0 kw and 50gms chemicals. Laser engraving is a safe, quick and eco-friendly way to achieve the aging effects of wear, without using chemicals. Now marketing its third version of the guided laser system, which can also replicate the use of chemical bleaching; output is up to 4,000 pairs of jeans a day. Jeanologia has also created the ʻWaterlessʼ G2 Washing Machine – its latest development to debut in 2012. This is a unique eco-washing machine, which allows the washing of jeans and shirts with vintage finishing, without using water or chemicals. How it works is: air from the atmosphere is transformed into a blend of active oxygen and ozone called ʻPlasmaʼ, which is used to age garments. The plasma is then transformed into purified air before it is returned to the atmosphere.

Italian company Tonello Garment Finishing Technologies introduced G1 N2 Nitrogen Dyeing Machine, offers eco friendly washing and dyeing by allowing the dyeing process to be carried out in a nitrogen atmosphere, thereby drastically reducing the use of chemical products, ensuring a cleaner and safer work environment and guaranteeing sustainable economic saving as well as improved stability in dying process. ʻWaterlessʼ dyeing is another technology, which dyes fabric with absolutely no water at all, being taken up by big sports brands including Puma and Adidas.

9

Branded DryDye are developed by the Yeh Group in Thailand, DryDye are dyed using only CO2 and high pressure, a form of dyeing which lowers chemical inputs and reduces energy and dye stuffs, and uses no water at all.

Sustainable Enzymes are proteins catalyzing chemical reactions. They are applied during the preparation, after dyeing and finishing stages of textile manufacturing to facilitate modification of textiles. Repeated water washes, or chemical reducing agents were traditionally used which leaves behind harsh chemicals. New sustainable enzyme technology facilitates in shorter process time, milder process conditions, improving the finishing of textiles, results in cost-effective innovation and most importantly is environmentally friendly. Applications of sustainable enzymes offer sustainable advantages for eco-scouring in the pre-treatment of cotton fabrics. This process results in 30% of water saving, and 60% of energy saving compared with the standard processes. It also enhances the quality and brightness of fabrics after dyeing.

RECYCLING: A SUSTAINABLE INNOVATION

We think of natural products as being more sustainable, but it is recycled products, which are actually proving to be more immediately accessible and viable, whether from recycled synthetic materials or recycled natural fibres such as wool. Giving new life to materials, destined for landfill, is a neat solution. And, more are taking up recycle fibres, as a response to market demand for social awareness and responsibility.

Plastic bottles into polyester: Recycled polyester, which comes mainly from drink bottles, is really gaining ground. In just a year Newlife, the recycled polyester yarn from Filatura Miroglio, made from plastic bottles collected and transformed entirely in Italy, has grown into a commercial reality, and is now being made into fabric available from for instance Boselli E. &C. and Tessitura Virgilio Taina, as well as in fabric ranges from Pontetorto, Becagli and Klopman, primary for performance sportswear applications. The Newlife recycled fibre is a “complete and certified system of recycled polyester filament yarns coming 100% from post consumer bottles, sourced, processed into polymer through a mechanical process, not a chemical one, and spun into yarn, completely and exclusively made in Italy.” The Newlife Process is the first of its kind, and leading the way in sustainable innovation for the textile yarn industries, with a unique supply chain approach.

Fishing nets into nylon yarns: Most of the nylon (polyamide) being recycled comes from damaged fishing nets. Recycled nylon yarn has been developed by Italian synthetic fibre producer Aquafil, which is already being used by circular jersey knitters Carvio and Jersey Lomallina to develop line of sustainable sportswear fabrics. The new branded Econyl yarn is a 100% recycled hollow polyamide, made from post consumer discarded products such as fishing net, old carpets and plastic from cars, which would otherwise be dump into the landfill. This has turned into a new polymer and then yarn for the production of new generation of ultra light comfortable high performance fabrics.

Jute sacks into Starbuck interior: While on the subject of recycling, another new fabric with an unusual raw material is WoJo fabric for Starbucks interior. This is made from recycled jute coffee sacks mixed with wool, made by UK firm Camira with yarn developed by Wools of New Zealand.

Recycle fibre into new fabric: Around 40 companies under a new label, Cardato Regenerated CO2 neutral, are recycling used fabrics and its fibre into new fabrics. The city of Prato, equipped with a purification system, recycles 22000 tons of textiles a year, which are sorted for different end uses. It is mainly the woollen articles that are destined for fraying and spinning once again into production of fabrics for clothing. This is either turned into wadding or mixed with virgin wool, which has longer fibres, to be able to spin the yarn. Among many commercial fabrics already being produced, Furpile, a member of the Cardato Group, is upcycling regenerated wool to make a jersey flannel.

10

PURCHASE BEHAVIOUR TOWARDS ETHICAL PRODUCTS

People do think and care about ethical, social, environmental, and health concerns and would purchase a green product over an environmentally problematic product. But consumers will only buy an ethical product if it doesnʼt cost more, comes from a brand they know and trust, can be purchased at stores where they already shop, doesnʼt require a significant change in habits to use, and has the same level of quality, performance, and endurance as the less-social alternative. Letʼs understand how social consumption fits into our general understanding of consumption behaviour.

GENERAL SURVEY ON ETHICAL CONSUMERISM

During the last 25 years, there has been debate about the value of corporate social responsibility (csr), particularly as it relates to the rise of "ethical consumers." these are shoppers who base purchasing decisions on whether a product's social and ethical positioning—for example, its environmental impact or the labor practices used to manufacture it—aligns with their values.

Many surveys purport to show that even the average consumer is demanding so-called ethical products, such as fair trade–certified coffee and chocolate, fair labor–certified garments, cosmetics produced without animal testing, and products made through the use of sustainable technologies. Yet when companies offer such products, they are invariably met with indifference by all but a selected group of consumers.

Is the consumer a cause-driven liberal when surveyed, but an economic conservative at the checkout line? Is the ethical consumer little more than a myth? Although many individuals bring their values and beliefs into purchasing decisions, when we examined actual consumer behaviour, we found that the percentage of shopping choices made on a truly ethical basis proved far smaller than most observers believe, and far smaller than is suggested by the anecdotal data presented by advocacy groups.

The trouble with the data on ethical consumerism is that the majority of research relies on people reporting on their own purchasing habits or intentions, whether in surveys or through interviews. But there is little if any validation of what consumers report in these surveys, and individuals tend to dramatically overstate the importance of social and ethical responsibility when it comes to their purchasing habits. As noted by John Drummond, ceo of corporate culture, a csr consultancy, "most consumer research is highly dubious, because there is a gap between what people say and what they do."

The purchasing statistics on ethical products in the marketplace support this assertion. Most of these products have attained only niche market positions. The exceptions tend to be relatively rare circumstances in which a multinational corporation has acquired a company with an ethical product or service, and invested in its growth as a separate business, without altering its other business lines (or the nature of its operations). For example, unilever's purchase of ben & jerry's homemade inc. Allowed for the expansion of the ben & jerry's ice cream franchise within the united states, but the rest of unilever's businesses remained largely unaffected.

Companies that try to engage in proactive, cause-oriented product development often find themselves at a disadvantage: either their target market proves significantly smaller than predicted by their focus groups and surveys, or their costs of providing ethical product features are not covered by the prices consumers are willing to pay. (for a different perspective on these issues, see "the power of the post-recession consumer," by john gerzema and michael d'antonio, s+b, spring 2011.) Consumers are aware of a great deal about the issues, and agree that good practices involving labor, the environment, and intellectual property are important to society. But most did not consider such issues to be relevant to them personally. Indeed, they often stated that someone other than the individual consumer should be responsible: the law ("the government should protect the environment"), the competitive market ("it's too bad, but all sneaker companies do this"), the companies themselves ("advertising should let us know about this"), or the overall system ("i cannot do anything, so why bother thinking about it?").

Another key finding is that most people will not sacrifice product function for ethics. When faced with a choice of good ethical positioning and bad product functionality or good product functionality and bad ethical positioning, individuals overwhelmingly chose the latter. They revealed an astounding reluctance to consider ethical product features as anything but secondary to their primary reasons for purchasing the products in question.

Contrary to other research that has typecast ethical consumers demographically or by their responses to surveys of values, we find little difference between people who take into consideration social aspects of products and those who do not. For example, it has been commonly assumed in the popular media that Europeans, with their strong tradition of social democracy, are more socially aware than Americans bred on notions of self-sufficiency and individualism. However, we found only weak support for this idea.

11

Simplistic notions about differences influenced by gender, education, income, culture, domicile, basic values, and so on proved similarly unfounded. It is often assumed that individuals from emerging-market countries are significantly less sensitive to social issues, being more concerned about economic development. Again, the reality is more complex; individuals' responses were more nuanced. It is found that although those from Germany, the United States, or china might rationalize their ethical consumption (or lack of it) differently, the purchase behaviours being justified are remarkably similar.

Proponents of ethical consumerism want to believe that people's socially oriented choices are somehow different—perhaps made at a higher level of consciousness—from their general product choices. This is a delusion. Product ethics are more important only when individuals, comparing such ethics to all the other things that have value to them, determine that they are more important. And research shows that for many people, this is seldom the case.

To some, this will sound like heresy. How can it possibly be that the cost of a bar of soap is more important than knowing that it won't pose an ecological hazard? Whatever the moral merits of the issue, for many ordinary people in ordinary circumstances, the cost does matter more. Even a factor like the color of a running shoe matters more, to most people, than the conditions under which the shoe was made.

The emergence of a true ethical consumer base is a long way from being a reality. Although some consumers today do take into consideration the social aspects of their purchasing behavior and care about a company's csr policies, most do not care enough to pay a higher price. Looking ahead, however, social consumption may have the potential to become a mass-market phenomenon. In fact, we see a parallel between the current ethical consumer market and the early days of e-commerce in the mid-1990s. As internet usage expanded and capabilities and security grew more sophisticated, consumers learned to integrate technology into their daily lives. Now, amazon and myriad other online destinations have made e-commerce an integral part of the shopping (and banking) culture.

RISE OF ETHICAL CONSUMERISUM THROUGH AWARNESS

Socially responsible consumption today is a nascent skill. Individuals do not necessarily know how to translate descriptions of ethical activity into judgment. (For example, what is a "good" labor practice? How much of a difference does an "ethical" sneaker purchase make in improving labor conditions?) Nor do they have any reason to trust in the verifiers, which are often the corporations themselves, or biased third-party organizations.

For more ethically oriented consumption to really take hold, the consumer needs to become a knowledgeable participant, not a reader of labels. Rather than relying on traditional market research techniques, firms need to help their existing and future consumers become more socially conscious in their purchasing. This will require giving consumers more tangible, reliable information about the health, social, and environmental benefits of their products and services, in the context of the many choices consumers have to make. Product labels will have to explain why a certain company's production footprint, packaging techniques, or ingredients are better than those of the competition—and have that superiority verified, ideally by independent sources that are accessible through the web or social media, conceivably through a shopper's smartphone.

Bit by bit, this type of information is becoming more available, and people are starting to bring their values not just to the survey but to the checkout counter. But that movement will be gradual, and such behaviour is still far from being second nature. It is possible that 10 or 20 years from now people will be purchasing ethically as a matter of habit, but corporations (along with third-party information providers) must first make the social merit of their products and services tangible to the pragmatic consumers who dominate the market.

This article was originally published by strategy+business magazine and was adapted from devinney, auger, and eckhardt's book, the myth of the ethical consumer (Cambridge university press, 2010).

12

SURVEY RESULTS

With an aim to collect primary data for this research project, two surveys has been taken, firstly survey on Consumer behaviour and secondly on Ethical business.

SURVEY RESULTS OF CONSUMER BEHAVIOUR

The survey on consumer behaviour results the core reality of the consumer behaviour in todayʼs ethical activism. The result is not unlike other survey results on ethical consumerism conducted in different part of the world before. Ethical consumers are not from another planet. They are the same consumer as before with basic needs, a consumer, which desire for primary feature in a product like use, quality, and cost. Ethical consumers have evolved from these consumers with sense of responsibility towards themselves, their surroundings and care for their planet. Though the basic desired features of a product remained primary, and the ethical features are still secondary in their desired products. Letʼs see what the survey suggests:

On asking the participants to arrange a list of product features according to their preference while buying a product: Utility, Quality and Cost were the top 3 preference whereas Environment friendly, Fair trade and Child labour free were last 3 preferences out of 10 product features. Around 46.7% of participants gave first preference to Utility and 76.6% of respondent opted Child labour free as least preferred feature while buying a product. This clearly indicates that consumers prefer primary features first.

On asking for preference of ethical features while buying an ethical product: 42.9% gave first preference to Environment friendly product, 32.1% gave first preference to Healthy products and 46.4% gave least preference to fair wages to labour. Consumers first take care of themselves in the environment then care about others related in the product supply chain. Ethical feature will be accepted as primary features only if it relate to or benefit the consumers directly.

30% admitted that they never bought any ethical product. This shows they are not aware of the ethical consumerism nor they have accessibility to ethical products and hence not motivated to buy ethical products.

93% said they would buy ethical product if it is affordable. Though some research claims that, consumers are willing to pay more to buy ethical product, but is very little in number who actually buy ethical products at more price than other similar products.

The survey also shows that 36.7% admitted that they would prefer an unethical product with good product features over an ethical product with less product features. This makes clear that ethical products cannot ignore the competition faced from product & design innovation and technological up gradation. The ethical products will survive in a market only if it provides same or better product features than the similar products present in the market at an affordable price.

About 62.1% said they will look for authentic eco-labels or certification while buying an ethical product. And about 27.6% said they will rely upon the company, offering ethical product. Consumers feel it is companyʼs responsibility to promote their ethical features in product as only 10.3% of the participants said they will take proactive steps to find out the ethicalness of the product themselves. Hence if a company is dealing in ethical product it should get authentic certification or eco-labels to attract ethical consumers and promote its ethical activities to make the consumer aware of their products.

51.7% preferred to buy ethical products from nearby shops over shopping online or buying from store at a long distance from home. The degree of accessibility of ethical product will also affect in the purchase of ethical products.

13

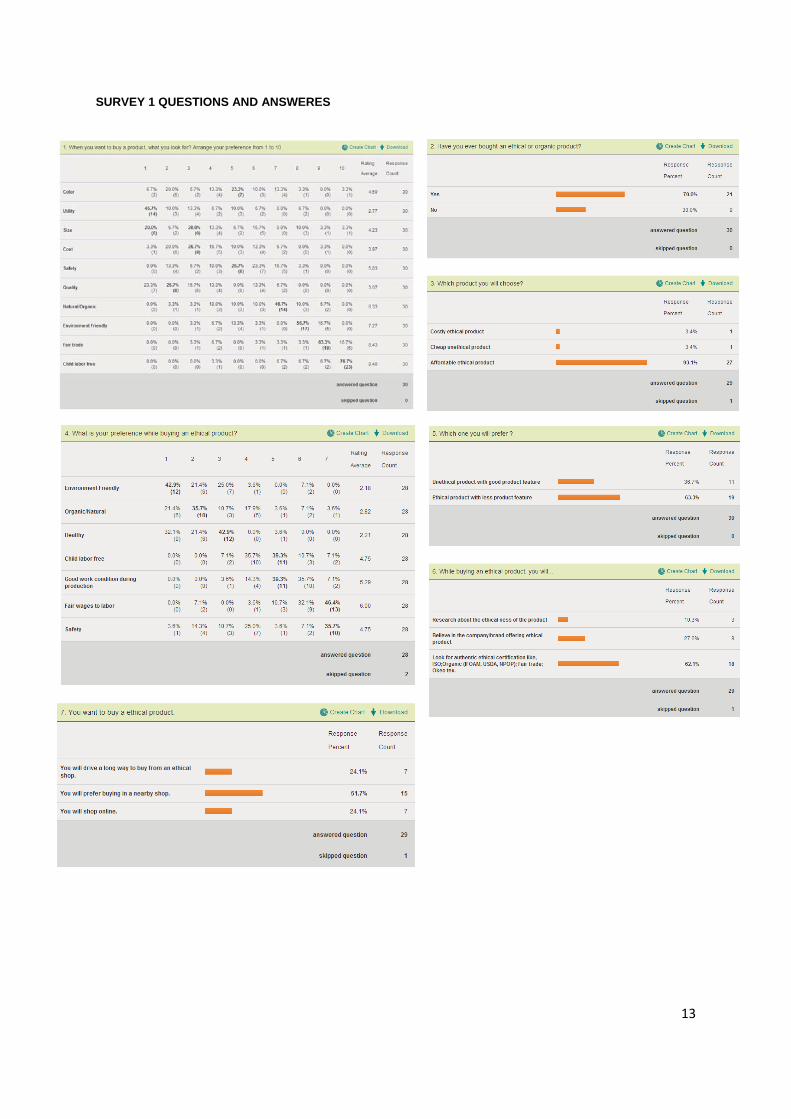

SURVEY 1 QUESTIONS AND ANSWERES

14

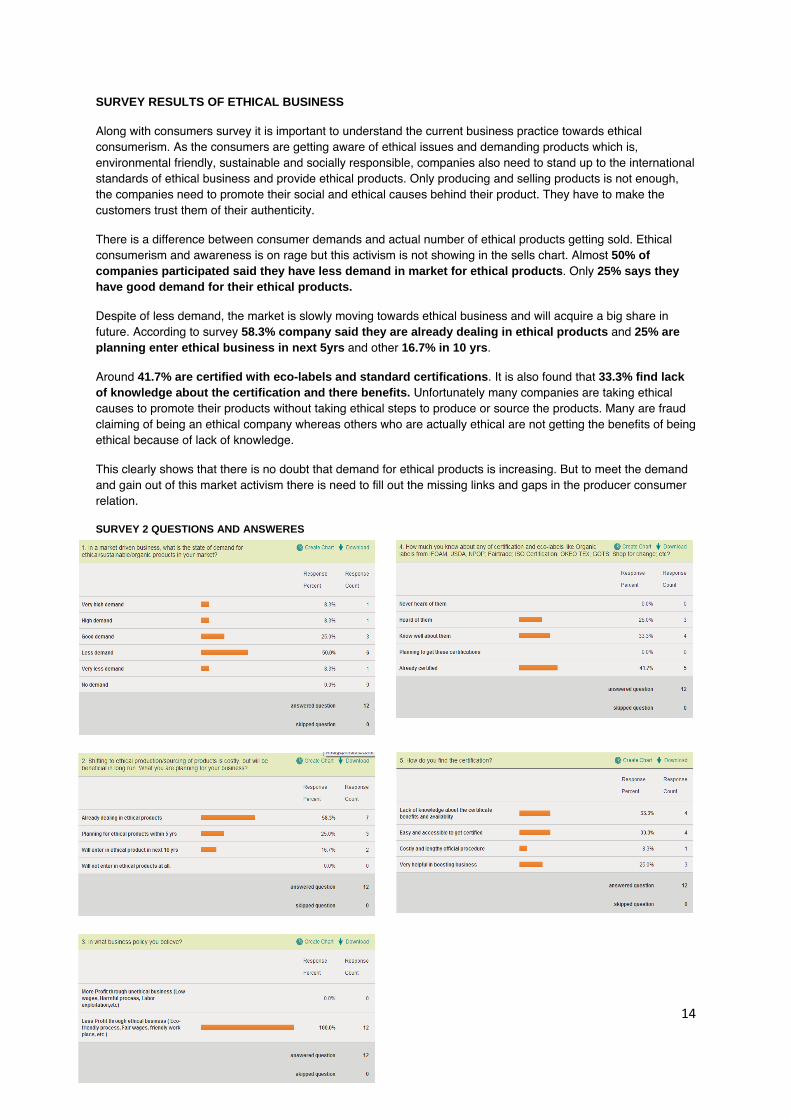

SURVEY RESULTS OF ETHICAL BUSINESS

Along with consumers survey it is important to understand the current business practice towards ethical consumerism. As the consumers are getting aware of ethical issues and demanding products which is, environmental friendly, sustainable and socially responsible, companies also need to stand up to the international standards of ethical business and provide ethical products. Only producing and selling products is not enough, the companies need to promote their social and ethical causes behind their product. They have to make the customers trust them of their authenticity.

There is a difference between consumer demands and actual number of ethical products getting sold. Ethical consumerism and awareness is on rage but this activism is not showing in the sells chart. Almost 50% of companies participated said they have less demand in market for ethical products. Only 25% says they have good demand for their ethical products.

Despite of less demand, the market is slowly moving towards ethical business and will acquire a big share in future. According to survey 58.3% company said they are already dealing in ethical products and 25% are planning enter ethical business in next 5yrs and other 16.7% in 10 yrs.

Around 41.7% are certified with eco-labels and standard certifications. It is also found that 33.3% find lack of knowledge about the certification and there benefits. Unfortunately many companies are taking ethical causes to promote their products without taking ethical steps to produce or source the products. Many are fraud claiming of being an ethical company whereas others who are actually ethical are not getting the benefits of being ethical because of lack of knowledge.

This clearly shows that there is no doubt that demand for ethical products is increasing. But to meet the demand and gain out of this market activism there is need to fill out the missing links and gaps in the producer consumer relation.

SURVEY 2 QUESTIONS AND ANSWERES

15

WORLD’S MOST ETHICAL COMPANIES

The Ethisphere Institute, a New York City think tank, has announced its sixth annual list of the Worldʼs Most Ethical Companies 2012. Highlights include Starbucks (NASDSAQ:SBUX) and General Electric (NYSE:GE) among the 23 companies that have been named for six years running since Ethisphere first launched the rankings. New additions include Intel (NASDAQ:INTC), Hasbro (NYSE:HAS), Kimberly-Clark (NYSE:KMB),L’Oreal (PINK:LRLCF), Honeywell (NYSE:HnON), Time Warner (NYSE:TWX), Alcoa (NYSE:AA),CostCo (NYSE:COST) and Kellogg’s (NYSE:K), among others. The 2012 list includes a record 145 companies, up from 110 in 2011. Also of note is that this year 43 of the companies listed are from outside the U.S. Including two from India, Tata Steel and Wipro that have been rated most ethical by the institute.

Worldʼs Most Ethical Companies 2012 in Apparel Comme Il Faut Israel Gap Inc USA Patagonia USA Timberland USA

Ethisphereʼs Worldʼs Most Ethical Companies ranking provides companies a chance to be recognized for their efforts in ethics and compliance. The winners of the Worldʼs Most Ethical Companies are the standouts. Each of these companies will have materially higher scores versus their competitors. They are the companies who force other companies to follow their leadership or fall behind. These are the companies who use ethical leadership as a profit driver. And each of these companies embody the true spirit of Ethisphereʼs credo, ʻGood. Smart. Business. Profit.ʼ

16

ECOLABELS

How do consumers and institutional buyers know if something is ʻgreenʼ or ʻeco-friendlyʼ? As environmental qualities are often imperceptible in the final product, producers need to make them visible to consumers. Many ecolabels and eco-certification schemes have been launched to validate green claims, guide green purchasing, and improve environmental performance standards. Done well, ecolabels and eco-certifications can provide an effective baseline within industry sectors by encouraging best practice and providing guidelines that companies must meet in order to meet a certified standard. Demand for products with ecolabels is growing, though confusion about which companies are truly environmentally responsible persists.

Several large companies and government agencies have recently announced or improved their green- or eco-purchasing policies, notably Wal-Mart, Office Depot, Mars, Dow, Dell and the US Federal Government. In order to meet their policies, these large-scale institutional purchasers need standards, detailed information, and proof that a product is green.

The ecolabel and eco-certification landscape is currently fragmented and often confusing to institutional buyers as well as individual consumers. Marketplace confusion has grown and continues to grow due to competing claims on what makes a product ʻgreenʼ, especially when there are two or more competing schemes for the same sector or product. Some ecolabels are regionally specific, while others are global; and some have stricter criteria than others. Compounding the problem is a lack of good quality standardized and comparable information worldwide. According to a European market research study (OECD, 2006), marketing, consumer confusion and competition between similar schemes has caused low market penetration for some ecolabels.

It is very important for manufacturers and sellers to choose ecolabel which is globally accepted and meets global quality standards. It should get certification which is known and appreciated by their specific market.

According to ecolabelindex, there are around than 103 ecolabels on textiles products and textile raw materials, which provides certification and labelling for eco-friendly and sustainable products in various countries. We will focus on the ecolabels with international standards which is beneficial for Indian textile industry.

INTERNATIONAL ORGANISATIONS FOR CERTIFICATION OF SUSTAINABLILITY AND ECOLABELS IN TEXTILE AND APPAREL INDUSTRY

INTERNATIONAL ORGANIZATION FOR STANDARDIZATION

ISO (International Organization for Standardization) is the worldʼs largest developer of voluntary International Standards. International Standards give state of the art specifications for products, services and good practice, helping to make industry more efficient and effective. Developed through global consensus, they help to break down barriers to international trade. ISO International Standards ensure that products and services are safe, reliable and of good quality. For business, they are strategic tools that reduce costs by minimizing waste and errors and increasing productivity. They help companies to access new markets, level the playing field for developing countries and facilitate free and fair global trade.

Some of the important sustainable and ethical standards:

• ISO 9000 Quality management The ISO-9000 series of standards evolved by the international standards organisation has been accepted worldwide as the norm assuring high quality of goods. The ISO-9000 is also the hallmark of a good quality oriented system for suppliers and manufacturers. It identifies the basic principles underlying quality, and specifies the procedures and criteria to be followed to ensure that what leaves the manufacture/supplierʼs premises fully meets the customerʼs requirements. The ISO- 9000 series of standards are basically quality assurance standards and not product standards. ISO-9000 spells out how a company can establish, document and maintain an effective and economic quality control system which will demonstrate to the customer that the company is committed to quality. The series of standards aims at the following: 1. Increased customer confidence in the company,

17

2. A shift from a system of inspection, to one of quality management, 3. Removing the need for multiple assessment of suppliers, 4. Gaining management commitment, 5. Linking quality to cost-effectiveness, 6. Giving customers what they need. The implementation of ISO-9000 standards involves: 1. Management education, 2. Writing a quality policy, 3. Nominating a quality representative, 4. Identify responsibilities, 5. Identifying business process, 6. Writing a quality manual, 7. Writing procedures, 8. Writing work instructions. It is thus clear that the ISO-9000 series of standards constitute of concept of Total Quality Management (TQM)

• ISO 14000 Environmental management

ISO -14000 is the first series of International standards on environmental management system issued by ISO. The main purpose of the ISO 14000 series is to promote more effective and efficient environmental management is organizations, 1.e. management that is systems-based, flexible and cost-effective. ISO 14001 provides the elements for an effective environmental management system which can be integrated into other management requirements. The system enables an organization to establish and assess the effectiveness of procedures for setting environmental policies and objectives, achieving conference with these objectives and demonstrating such conformance. ISO 14001 series specifies the requirements for certification and self declaration of enterpriseʼs environmental management system. Compliance with the standards will give exporting enterprises a competitive edge. For enterprises in developing countries, the ISO 14000 series of standards represent on opportunity for technology transfer and a source of guidance for introducing and adopting an environmental management system based on best universal practices. The whole ISO-14000 family provides management tools for organizations to control their environmental aspects and to improve their environmental performance. Together, these tools can provide significant tangible economic benefits, including: 1. Reduced raw material/resource use, 2. Reduced energy consumption; 3. Improved process efficiency; 4. Reduced waste generation and disposal costs; and 5. Utilization of recoverable resources. In India, export and trading houses that have acquired certification to ISO 9000, ISO 14000 or the equivalent internationally recognised certification of quality are granted Star Export House status on achievement of a lower threshold limit.

• ISO 50001 Energy management Using energy efficiently helps organizations save money as well as helping to conserve resources and tackle climate change. ISO 50001 supports organizations in all sectors to use energy more efficiently, through the development of an energy management system (EnMS). ISO 50001 is based on the management system model of continual improvement also used for other well-known standards such as ISO 9001 or ISO 14001. This makes it easier for organizations to integrate energy management into their overall efforts to improve quality and environmental management.

ISO 50001:2011 provides a framework of requirements for organizations to:

1. Develop a policy for more efficient use of energy 2. Fix targets and objectives to meet the policy 3. Use data to better understand and make decisions about energy use 4. Measure the results 5. Review how well the policy works, and 6. Continually improve energy management.

18

• ISO 26000 Social responsibility Business and organizations do not operate in a vacuum. Their relationship to the society and environment in which they operate is a critical factor in their ability to continue to operate effectively. It is also increasingly being used as a measure of their overall performance. ISO 26000 provides guidance on how businesses and organizations can operate in a socially responsible way. This means acting in an ethical and transparent way that contributes to the health and welfare of society. ISO 26000:2010 provides guidance rather than requirements, so it cannot be certified to unlike some other well-known ISO standards. Instead, it helps clarify what social responsibility is, helps businesses and organizations translate principles into effective actions and shares best practices relating to social responsibility, globally. It is aimed at all types of organizations regardless of their activity, size or location. The standard was launched in 2010 following five years of negotiations between many different stakeholders across the world. Representatives from government, NGOs, industry, consumer groups and labour organizations around the world were involved in its development, which means it represents an international consensus.

INTERNATIONAL FEDERATION OF ORGANIC AGRICULTURE MOVEMENTS The International Federation of Organic Agriculture Movements (IFOAM) is the worldwide umbrella organization for the organic agriculture movement, uniting more than 750 member organizations in 108 countries. It declares its mission to be as follows: IFOAM's mission is leading, uniting and assisting the organic movement in its full diversity. Their goal is “the worldwide adoption of ecologically, socially and economically sound systems that are based on the principles of Organic Agriculture." Among its wide range of activities, IFOAM maintains an organic farming standard, and an organic accreditation and certification service.

IFOAM actively participates in international agricultural and environmental negotiations with the United Nations and multilateral institutions to further the interests of the organic agricultural movement worldwide, and has observer status or is otherwise accredited by the following international institutions:

ECOSOC Status with the United Nations General Assembly The Food and Agriculture Organization of the United Nations (FAO) United Nations Conference on Trade and Development (UNCTAD) Codex Alimentarius Commission (FAO and World Health Organization) United Nations Environment Program (UNEP) The Organization for Economic Cooperation and Development (OECD) International Labor Organization of the United Nations (ILO) International Organization for Standardization (ISO)

According to the One World Trust's Global Accountability Report 2008 which assessed a range of organisations in areas such as transparency, stakeholder participation and evaluation capacity, "IFOAM is the highest scoring international NGO, and at the top of the 30 organisations this year with a score of 71 percent".

IFOAM and Standards and Certification

IFOAM's Organic Guarantee System (OGS) is designed to

a) Facilitate the development of organic standards and third-party certification worldwide and to

b) Provide an international guarantee of these standards and organic certification.

In recent years IFOAMʼs OGS approach underwent some significant changes. With the establishment and spreading of organic standards and certification around the world a number of new challenges appeared. Especially smallholder farmers in developing countries struggle with

a) the multitude of standards they are expected to farm conform with and

b) with high certification costs and considerable administrative expenditures.

IFOAM had a breakthrough in the development and adoption of approaches to address these certification problems. The IFOAM Basic Standards and the Accreditation Criteria are two of the main components of the OGS.

19

IFOAM Family of Standards

In the framework of a multi-year collaboration IFOAM developed together with his UN partners: the Food and Agriculture Organization (FAO) and the United Nations Conference on Trade and Development (UNCTAD), a set of standard requirements that functions as an international reference to assess the quality and equivalency of organic standards and regulations. It is known as the COROS (Common Objectives and Requirements of Organic Standards) The vision is that the Family of Standards will contain all organic standards and regulations equivalent to the COROS. Instead of assessing each standard against each other the Family of Standards can be used as a tool to simplify equivalence assessment procedures while ensuring a high level of integrity and transparency. The Family of Standard Program started in January 2011. One year later about 50 standards worldwide are approved.

EUROPEAN UNION (EU)

The European Union bases its organic farming program on the EC 834/2007, which establishes the legal framework for all levels of production, distribution, control and labelling of organic products which may be offered and traded in this region.

EU Organic Certification

The EU organic logo guarantees that the product in question complies with the common European organic food standards. Consumers buying products bearing this logo can be confident that at least 95% of the product's ingredients have been organically produced, the product complies with the rules of the official inspection scheme, the product has come directly from the producer or preparer in a sealed package and that the product bears the name of the producer, the preparer or vendor and the name or code of the inspection body. The hope is that in the long term the EU logo will be able to solve the trade problems that the organic food sector faces today. This certification is also given to organic cotton which fulfils the organic standards of EU.

USDA ORGANIC The U.S. Department of Agriculture has put in place a set of national standards that products labelled must meet, whether it is grown in the United States or imported from other countries. Organic meat, poultry, eggs, and dairy products come from animals that are given no antibiotics or growth hormones. Organic food, cotton is produced without using most conventional pesticides; fertilizers made with synthetic ingredients or sewage sludge; bioengineering; or ionizing radiation.

NATIONAL ORGANIC PROGRAM (NOP)

Information for International Trade Partners The United States has trade arrangements with several nations to facilitate the exchange of organic products. These arrangements provide additional market opportunities for USDA organic producers. Consumers also benefit from a wider range of organic products year-round. The National Organic Program works with the Foreign Agricultural Service and Office of the United States Trade Representative to establish international trade arrangements. Trade opportunities for USDA organic operations vary by an operationʼs physical location: United States Trade Partners: European Union | Canada | Taiwan | Japan India, Israel, Japan, New Zealand Trade Partner: United States The National Organic Program is committed to protecting organic integrity through the following activities:

• Audits of certifying agents to ensure appropriate monitoring of organic products • Annual on-site inspections of approximately 30,000 organic operations by certifying agents

20

• Residue testing program to verify that prohibited pesticides arenʼt being applied to organic crops • Compliance and enforcement activities, including suspending or revoking organic certificates for regulatory

non-compliance • Issue-based investigations (e.g. country- or commodity-specific)

International Trade Policies: India The United States has a recognition agreement with India. Recognition agreements allow a foreign government to accredit certifying agents in that country to the USDA organic standards. These foreign certifying agents are authorized to certify organic farms and processing facilities, ensuring that USDA organic products meet or exceed all USDA organic standards. These products can then import for sale in the United States. Scope. This agreement covers all USDA organic products produced in India and certified by an Indian government-accredited certifying agent. Production Requirements. USDA organic regulations Documentation. Standard United States import documentation Overview: Importing and Exporting Organic Products (PDF) Labelling. Products produced under the agreement must meet all USDA organic labelling requirements. USDA Organic Seal

HOW TO CERTIFY AN ORGANIC PRODUCT UNDER USDA In order to label a product organic, as USDA (United States Department of Agriculture) certified, meaning it has met the requirements of the USDA NOP (National Organic Program) standards. Even when not grown in the United States, the cotton must still meet USDAʼs NOP standards in order to be labelled as such. The requirements include: • Retailers and brands require documentation from growers providing that they have met stringent

requirements at every stage of processing, starting at farm level.

• Production practices must comply with the NOP National List of Allowed Synthetic and Prohibited Non-Synthetic Substances.

• Proof must be available on demand. • Transgenic cotton varieties are not acceptable in organic certification.

The USDA NOP standards are written for organic cotton fibres and not the end products. As per the USDA: "Although the NOP has no specific fibre or textile processing and manufacturing standards, it may be possible for fibres grown and certified to NOP crop/livestock standards to be processed and manufactured into textile and other products which meet NOP standards." Only textile products certified to the NOP production and processing standards are eligible to be labelled as “100 percent organic” and “organic”. "100 percent organic": • 100 percent organic fibre content. • Only organic processing aids. • USDA Organic seal may be displayed on final product, in marketing materials, and in retail displays in

proximity to certified products only. • All operations producing, handling, processing and manufacturing the final product must be certified.

21

GOTS (THE GLOBAL ORGANIC TEXTILE STANDARD) The Global Organic Textile Standard (GOTS) was developed through collaboration by leading standard setters with the aim of defining requirements that are recognised world-wide and that ensure the organic status of textiles from harvesting of the raw materials through environmentally and socially responsible manufacturing all the way to labelling in order to provide credible assurance to the consumer. Since its introduction in 2006 the Global Organic Textile Standard has already demonstrated its practical feasibility. Supported by the growth in consumption of organic fibres and by the remarkable demand for unified processing criteria from the industry and retail sector, it has gained universal recognition, enabling processors and manufacturers to supply their organic textiles with one certification accepted in all major markets. With the introduction of the logo and labelling system the GOTS is already visible not only on the shelves of natural textile shops but large-scale retailers and brand dealers as well. This is a milestone in consumer recognition and a strong acknowledgement of our reliable quality assurance concept.

The Global Organic Textile Standard (GOTS) is the world's leading textile processing standard for organic fibres, including ecological and social criteria, backed by independent certification of the entire textile supply chain.

Version 3.0 was published on 1 March 2011, six years after the introduction of the initial version. High ecological and social requirements as well as global practicability and verifiability were taken into consideration in the revision work in order to achieve reliable and transparent criteria.

AIM

The aim of the standard is to define globally recognised requirements that ensure the organic status of textiles, from harvesting of the raw materials through environmentally and socially responsible manufacturing all the way to labelling in order to provide credible assurance to the end consumer. Textile processors and manufacturers should be able to export their organic fabrics and garments with one certification accepted in all major markets.

CRITERIA The consensus of the International Working Group was that a clear and unambiguous understanding of the content required the Global Organic Textile Standard itself to focus on compulsory criteria only. The standard covers the processing, manufacturing, packaging, labelling, trading and distribution of all textiles made from at least 70% certified organic natural fibres. The final products may include but are not limited to: fibre products, yarns, fabrics, clothes and home textiles. The standard does not set criteria for leather products.

FIBRE PRODUCTION

The key criteria for fibre production can be identified as:

• Organic certification of fibres on the basis of recognised international or national standards (e.g. IFOAM, EEC 834/2007, USDA NOP)

• Certification of fibres from conversion period is possible if the applicable farming standard permits such certification

22

• A textile product carrying the GOTS label grade ʻorganicʼ must contain a minimum of 95% certified organic fibres whereas a product with the label grade ʻmade with organicʼ must contain a minimum of 70% certified organic fibres

PROCESSING AND MANUFACTURING

Key criteria for processing and manufacturing include:

Environmental Criteria

• At all processing stages organic fibre products must be separated from conventional fibre products and must be clearly identified

• All chemical inputs (e.g. dyes, auxiliaries and process chemicals) must be evaluated and meet basic requirements on toxicity and biodegradability/eliminability

• Ban on critical inputs such as toxic heavy metals, formaldehyde, aromatic solvents, functional nano particles, genetically modified organisms (GMO) and their enzymes

• The use of synthetic sizing agents is restricted; knitting and weaving oils must not contain heavy metals • Bleaches must be based on oxygen (no chlorine bleaching) • Azo dyes that release carcinogenic amine compounds are prohibited • Discharge printing methods using aromatic solvents and plastisol printing methods using phthalates and

PVC are prohibited • Restrictions for accessories (e.g. no PVC, nickel or chrome permitted, all polyester must be post-consumer

recycled from 2014 onwards) • All operators must have an environmental policy including target goals and procedures to minimise waste

and discharges • Wet-processing units must keep full records of the use of chemicals, energy, water consumption and waste

water treatment, including the disposal of sludge. The waste water from all wet-processing units must be treated in a functional waste water treatment plant.

• Packaging material must not contain PVC. From 1 January 2014 onwards, any paper or cardboard used in packaging material, hang tags, swing tags etc. must be post-consumer recycled or certified in accordance with FSC or PEFC

Technical Quality and Human Toxicity Criteria

• Technical quality parameters must be met (such as rubbing, perspiration, light and washing fastness and shrinkage values)

• Raw materials, intermediates, final textile products as well as accessories must meet stringent limits in regard to unwanted residues

Minimum Social Criteria

All processors and manufacturers must meet minimum social criteria based on the key norms of the International Labour Organisation (ILO). They must implement social compliance management with defined elements to ensure that the social criteria can be met. The applicable key conventions of the International Labour Organization (ILO) listed must be used as the relevant basis for interpretation for adequate implementation and assessment of the following social criteria topics.

• Employment is freely chosen C29 - Forced Labour Convention C105 - Abolition of Forced Labour Convention

• Freedom of association and the right to collective bargaining are respected C87 - Freedom of Association and Protection of the Right to Organise Convention C98 - Right to Organise and Collective Bargaining Convention

23

C135 - Workers' Representatives Convention C154 - Collective Bargaining Convention

• Working conditions are safe and hygienic C155 - Occupational Safety and Health Convention

• Child labour must not be used C138 - Minimum Age Convention C182 - Worst Forms of Child Labour Convention

• Living wages C95 - Protection of Wages Convention C131 - Minimum Wage Fixing Convention

• Working hours are not excessive C1 - Hours of Work (Industry) Convention C14 - Weekly Rest (Industry) Convention C30 - Hours of Work (Commerce and Offices) Convention C106 - Weekly Rest (Commerce and Offices) Convention

• No discrimination is practised C100 - Equal Remuneration Convention C111 - Discrimination (Employment and Occupation) Convention

• Regular employment is provided C158: Termination of Employment Convention C175: Part-time Work Convention C177: Homework Convention C181 Private Employment Agencies Convention

• Harsh or inhumane treatment is prohibited C29 - Forced Labour Convention C105 - Abolition of Forced Labour Convention

HOW TO BECOME A CERTIFIED

Textile processing, manufacturing and trading entities can apply for certification in accordance with the Global Organic Textile Standard. Entities that wish to become certified are requested to contact an appropriate GOTS approved certification body. These are entrusted with implementation of the GOTS quality assurance system and are able to provide information about the related procedures and timeline from the initial request through the inspection and certification process. They will be able to offer individual cost estimates for certification based on the operatorʼs location, size, fields of operation and other relevant factors.

In principle all GOTS-approved certifiers are entitled to offer related inspection and certification services worldwide and each applicant may choose its certification body. Some certifiers operate local offices or work with local representatives in various countries while others coordinate all services through their head offices. There are limitations regarding the accredited scope for which a certifier may offer GOTS certification. Certifiers of textile supply chain operators may be accredited to the following scopes:

• Certification of mechanical textile processing and manufacturing operations and their products (scope 1) • Certification of wet-processing and finishing operations and their products (scope 2) • Certification of trading operations and related products (scope 3)

APLLICABILITY OF THE CERTIFICATION SYSTEM

The applicability of the GOTS certification system starts with the first processing step in the textile supply chain. In the cotton supply chain ginning is considered to be the first processing step, whereas the wool supply chain processing normally starts with scouring.

Organic fibre production is not directly covered by the GOTS certification system as GOTS does not set standards for organic fibre cultivation itself. Instead, cultivation of organic fibres is under the scope of the governmental organic farming standards (e.g. the EEC Organic Regulation or the USDA NOP). Organic fibres certified according to these recognised international or national legal standards are the accepted raw material inputs for the GOTS processing and manufacturing chains.

The GOTS quality assurance system is based on on-site inspection and certification of the textile processing and trade chain. In particular operators from post-harvest handling through garment-making as well as traders up to the wholesale stage have to undergo an annual on-site inspection cycle and must hold a valid certification as a prerequisite for final products (sold to retailers) to be labelled as GOTS-certified.

Processors and manufacturers that receive a GOTS operational certification have demonstrated to the assigned certifier that they are able to work in compliance with all applicable GOTS criteria in the fields of operations and for the product groups shown on their certificate. They may then accept orders for GOTS-compliant processing /

24

manufacturing in their certified scope. Accordingly certified exporters-, importers and traders are authorised to trade GOTS textile products within the scope of the certification they have attained.

Entities that receive a GOTS operational certificate are free to advertise their certified status on the market. They must however avoid the impression that all of their products are certified, if this is not the case and ensure that no confusion arises between certified and non-certified products in any marking, publications and advertising. They also become listed in the public GOTS data base on this website.

ELEMENTS OF THE INSPECTION

Generally a company that is participating in the GOTS certification scheme needs to comply with all criteria of the standard. The assigned certifier makes use of appropriate inspection methods which may include but are not limited to the following key elements:

• Review of bookkeeping in order to verify flow of GOTS goods (input/output reconciliation, mass balance calculation and trace back lots and shipments). This is a key aspect of the inspection of any operation that sells/trades GOTS goods.

• Assessment of the processing and storage system through visits to the applicable facilities • Assessment of the separation and identification system and identification of areas of risk to organic integrity • Inspection of the chemical inputs (dyes and auxiliaries) and accessories used and assessment of their

compliance with the applicable criteria of the GOTS • Inspection of the waste water (pre-) treatment system of wet processors and assessment of its performance. • Check on minimum social criteria (possible sources of information: interview with management, confidential

interviews with workers, personnel documents, physical on-site inspection, unions/stakeholders) • Verification of the operator's risk assessment of contamination and residue testing policy potentially including

sample drawing for residue testing either as random sampling or in case of suspicion of contamination or non-compliance.

OEKO-TEX®

The OEKO-TEX® Standard was introduced at the beginning of the 1990s as a response to the needs of the general public for textiles which posed no risk to health. "Poison in textiles" and other negative headlines were widespread at this time and indiscriminately branded all chemicals across the board used in textile manufacturing as negative and dangerous to health. In order to become OEKO-TEX® certified, a product must undergo rigorous testing to determine if it is free from harmful substances which are prohibited or regulated by law, and chemicals which are known to be harmful to health. Additional parameters are included as a precautionary measure to safeguard health. In principle, the more intensively a textile comes into contact with the skin, the stricter the human ecological requirements it must fulfil.

Before introduction of the OEKO-TEX® Standard there was neither a reliable product label for the assessment of the human ecological quality of textiles for consumers nor a uniform safety standard for manufacturers in the textile and clothing industry allowing practical assessment of potential harmful substances in textile products. The Austrian Textile Research Institute (ÖTI)and the German Hohenstein Research Institute have therefore jointly developed the OEKO-TEX® Standard 100 on the basis of their existing test standards.

The Oeko-Tex Association is an independent, third-party certifier that offers two certifications for textiles: Oeko-Tex 100 (for products) and Oeko-Tex 1000 (for production sites/factories). Products satisfying the criteria for Oeko-Tex 100 and produced in a OekoTex 1000 certified facility may use the Oeko-Tex 100+ mark, which is simply a combination of the two.

OEKO-TEX® Standard 100

The OEKO-TEX® Standard 100 is an independent testing and certification system for textile raw materials, intermediate and end products at all stages of production. Examples for items eligible for certification: Raw and dyed/finished yarns, raw and dyed/finished fabrics and knits, ready-made articles (all types of clothing, domestic and household textiles, bed linen, terry cloth items, textile toys and more).

25

Criteria Testing for harmful substances includes:

• illegal substances • legally regulated substances • known harmful (but not legally regulated) chemicals • as well as parameters for health care In their entirety the requirements clearly exceed existing national legislation.

Laboratory tests and product classes OEKO-TEX® testing for harmful substances always focuses on the actual use of the textile. The more intensive the skin contacts of a product, the stricter the human ecological requirements to be met.

Accordingly there are four product classes: • Product class I:

Textile items for babies and toddlers up to 3 years (clothing, toys, bed linen, terry cloth items etc.) • Product class II:

Textiles used close to the skin (underwear, bed linen, T-shirts etc.) • Product class III:

Textiles used away from the skin (jackets, coats etc.) • Product class IV:

Furnishing materials (curtains, table cloths, upholstery materials etc.)

Some of the specific items tested for include:

• Banned MAK amines in specific AZO dyes • Other carcinogenic and allergenic dyes • Formaldehyde • Pesticides • Extractable heavy metals and heavy metals in digested samples • pH value, color fastness, and odors

Certification The requirement for certification of textile products according to OEKO-TEX® Standard 100 is that all components of an item have to comply with the required criteria without exception – that means in addition to the outer material also sewing threads, linings, prints etc. as well as non-textile accessories such as buttons, zip fasteners, rivets etc.

OEKO-TEX® Standard 1000

OEKO-TEX® Standard 1000 is a testing, auditing and certification system for environmentally friendly operations in the textile and clothing industry.

On the basis of criteria which are updated annually the standard allows an objective assessment of the achieved environmental balance and social acceptability at the respective site of the company. The aim is the continuing improvement of operational environmental performance and working conditions. Criteria • Product certification according to OEKO-TEX® Standard 100 • Compliance with national legislation • Adherence to strict guidelines regarding waste water purification and exhaust emissions/environmentally

friendly waste management • Use of environmentally compatible technologies, chemicals and dyes (e.g. omission of chlorine bleach) • Optimised use of energy and materials • Proof of a quality and environmental management system • Workplace hygiene and occupational safety (low noise and dust pollution, provision of required protective

measures etc.) • Satisfaction of social criteria (ban against child labour, no discrimination/forced labour, performance-based

pay, regulated work and holiday times etc.) Certification

26