ETFs as a source of Income · ETFs as a source of Income June 2013 ... Retail Investors Websites...

15

ETFs as a source of Income June 2013 PRESENTED BY GARETH STOBIE

Transcript of ETFs as a source of Income · ETFs as a source of Income June 2013 ... Retail Investors Websites...

ETFs as a source of Income

June 2013

PRESENTED BY GARETH STOBIE

Introduction to Grindrod Bank’s ETF suite:

Tax efficient, 7.48%

No long term growth to income stream

Preference

Shares

6.95% taxable

Long term growth to income stream

Property

Grindrod: Exchange Traded Products

Your share of the South African listed property market

Liquid and cost effective

Growing income stream > 6%

Tangible investment secured by ‘bricks and mortar’

Regulated and transparent

Historical performance

PROPTRAX : PROPERTY ETFs

(20)

(10)

0

10

20

30

40

50

60

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Income Price

Average annual income

return 11.01

Listed Property Returns and How They are

Derived?

Average annual returns: 26.08 percent

Average annual income: 11.01 percentage points or 43 percent of total return

Source: I-Net

Scorecard

SA Short Rates + Notwithstanding recent spike in bond yields,

generally low yields set to continue

SA Property Fundamentals 0

Industrial and retail doing well

Office continues to struggle

Forecast 6-8% pa distribution grow next 2-3 years

SA Valuations 0 Recent pull-back healthy for the market but yields

remain below historical average

Funding + Extremely low funding rates available to property

companies

Demand / Supply for SA

Listed Property 0

REIT legislation to be positive for sector

Numerous new issuances pose some supply side

risk but the issues remain over-subscribed

TOTAL + 2 Mildly positive outlook

Property Prospects

Investment Portfolio Portfolio with Property

Stocks 60.00% 50.00%

Bonds 30.00% 30.00%

Cash 10.00% 10.00%

Listed Property 0.00% 10.00%

100.00% 100.00%

10 Years, annualized

Return 16.80% 17.33%

Risk 10.40% 9.78%

Risk vs. Return : An Investors Quandary?

SAPY TEN

Index SAPY Customized, top ten

equally weighted

Yield(1) 6.78% 7.12%

Size R108m R141m

Share PTXSPY PTXTEN

1 Year(2) 26.0% 21.9%

3 Year(2) 21.6% n/a

PTX TEN & SAPY

Source: I-Net

(1) As at 14 June 2013

(2) Source: SIM. Performance annualised, gross of fees

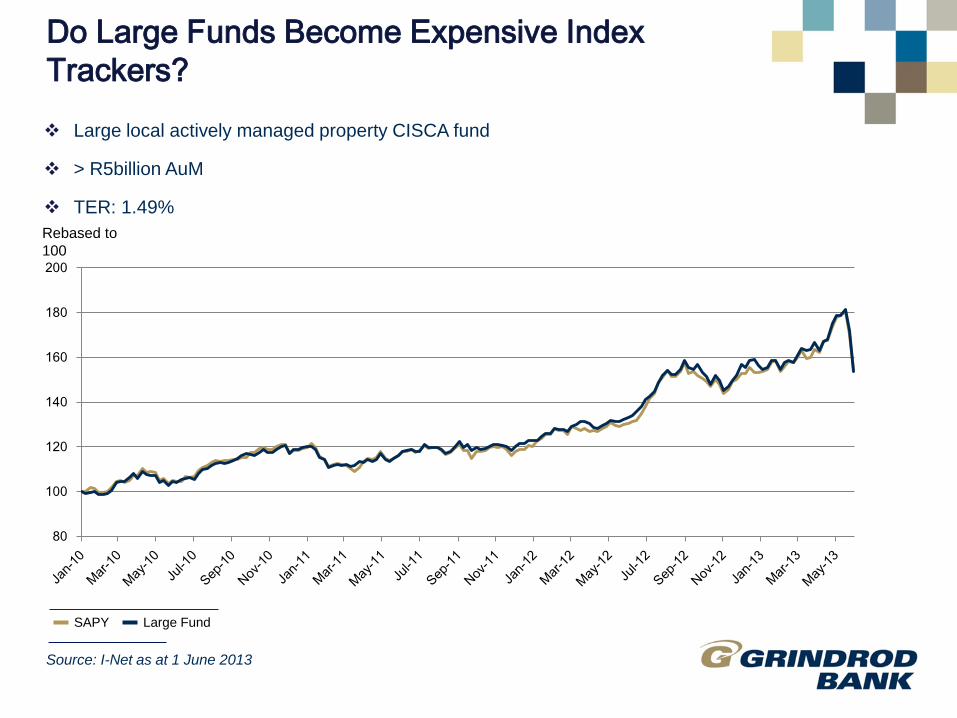

Do Large Funds Become Expensive Index

Trackers?

Large local actively managed property CISCA fund

> R5billion AuM

TER: 1.49%

SAPY Large Fund

80

100

120

140

160

180

200

Rebased to

100

Source: I-Net as at 1 June 2013

SA’s Preference share ETF

Hybrid investment: part Equity, part Debt

High yielding 7.48% fixed income investment

Significant pick-up in after tax yields relative to cash

Tax efficient (max DWT @ 15%)

Comparable to bonds and cash but must invest > 12 months

Very attractive after surprising pull back in valuations

Prefs vs. Cash since start of Financial Crisis

90

100

110

120

130

140

150

160

170

Jul-0

8

Sep-0

8

No

v-0

8

Jan-0

9

Ma

r-0

9

Ma

y-0

9

Jul-0

9

Sep-0

9

No

v-0

9

Jan-1

0

Ma

r-1

0

Ma

y-1

0

Jul-1

0

Sep-1

0

No

v-1

0

Jan-1

1

Ma

r-1

1

Ma

y-1

1

Jul-1

1

Sep-1

1

No

v-1

1

Jan-1

2

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Sep-1

2

No

v-1

2

Jan-1

3

Ma

r-1

3

Ma

y-1

3

J251T STFIND

53%

23%

Rebased to

100

On an after tax basis the J251 has outperformed the Stefi

Source: I-Net as at 07 June 2013

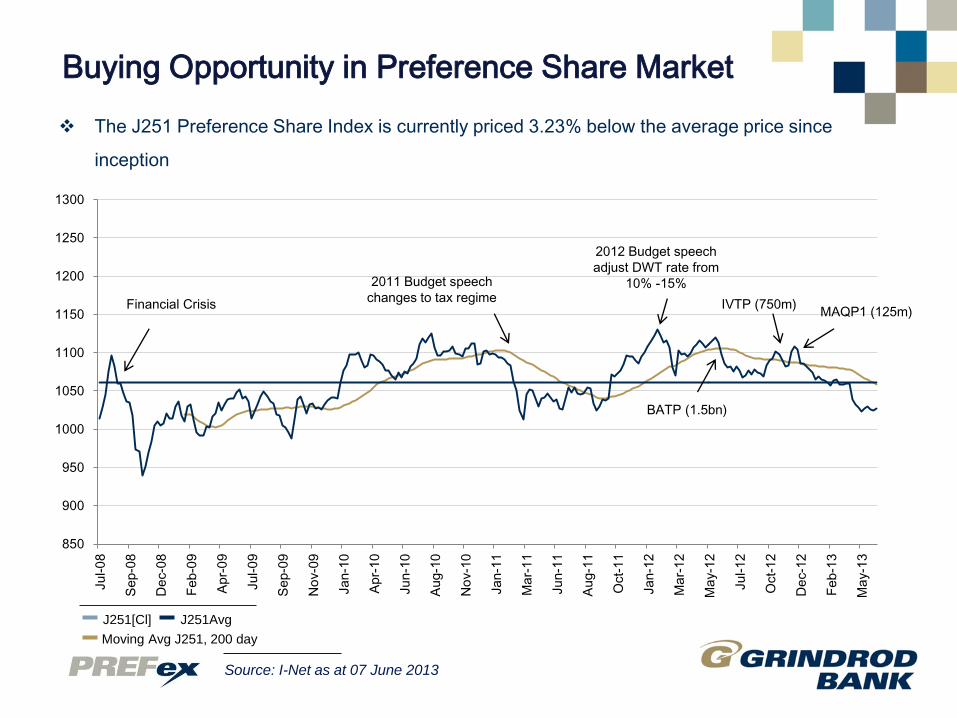

Buying Opportunity in Preference Share Market

Source: I-Net as at 07 June 2013

850

900

950

1000

1050

1100

1150

1200

1250

1300

Jul-0

8

Sep-0

8

De

c-0

8

Feb

-09

Apr-

09

Jul-0

9

Sep-0

9

No

v-0

9

Jan-1

0

Apr-

10

Jun-1

0

Aug-1

0

No

v-1

0

Jan-1

1

Ma

r-1

1

Jun-1

1

Aug-1

1

Oct-

11

Jan-1

2

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Oct-

12

De

c-1

2

Feb

-13

Ma

y-1

3

2011 Budget speech

changes to tax regime

2012 Budget speech

adjust DWT rate from

10% -15%

BATP (1.5bn)

IVTP (750m) MAQP1 (125m)

Financial Crisis

J251Avg

Moving Avg J251, 200 day

J251[Cl]

The J251 Preference Share Index is currently priced 3.23% below the average price since

inception

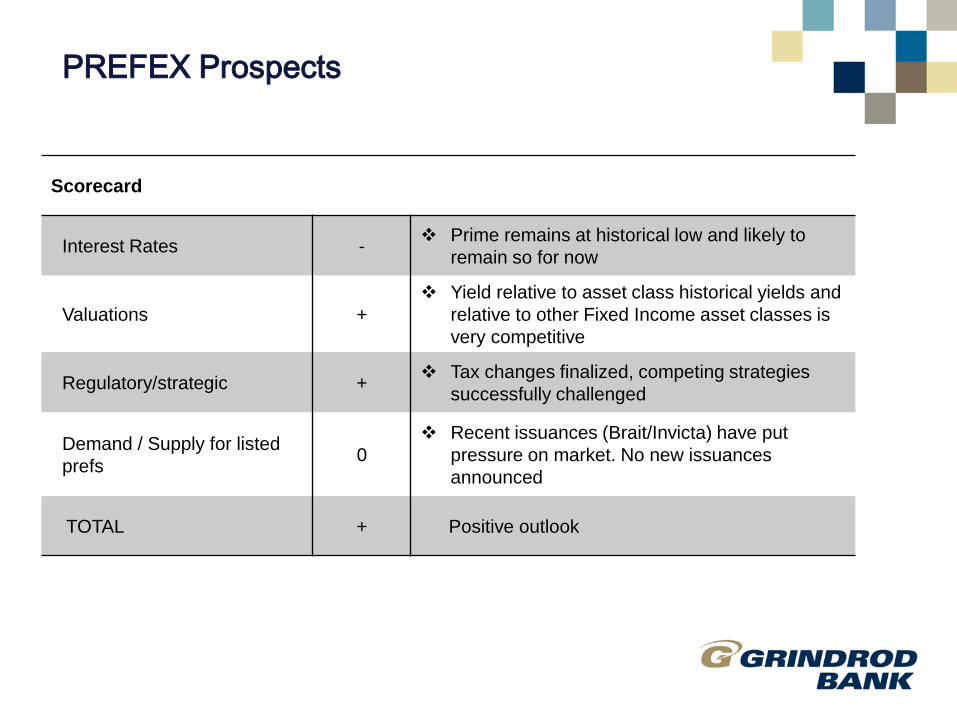

Scorecard

Interest Rates - Prime remains at historical low and likely to

remain so for now

Valuations +

Yield relative to asset class historical yields and

relative to other Fixed Income asset classes is

very competitive

Regulatory/strategic + Tax changes finalized, competing strategies

successfully challenged

Demand / Supply for listed

prefs 0

Recent issuances (Brait/Invicta) have put

pressure on market. No new issuances

announced

TOTAL + Positive outlook

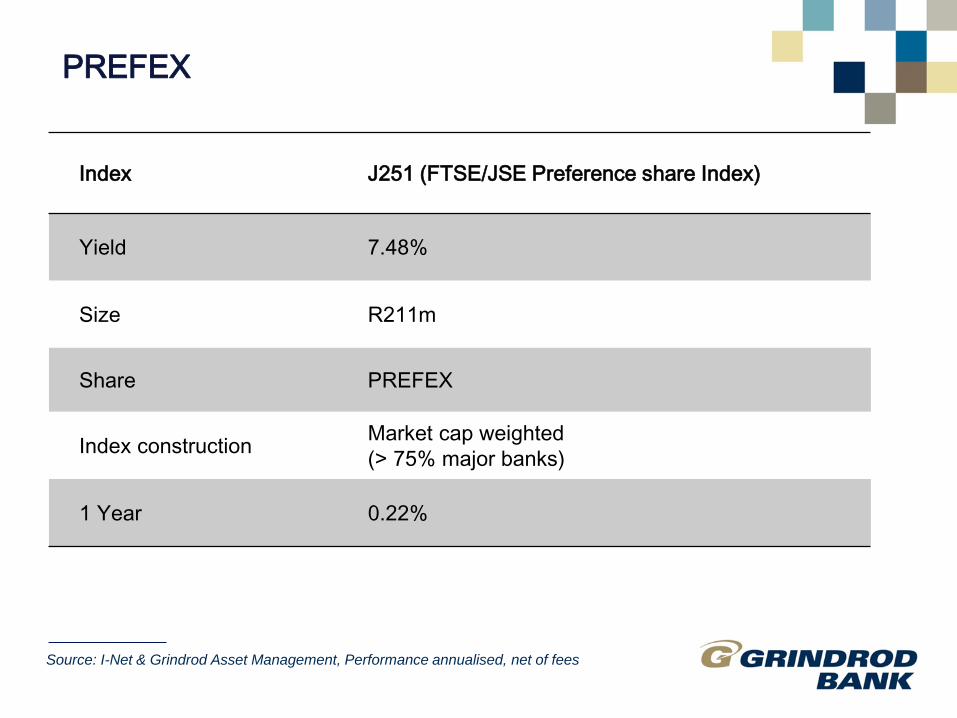

PREFEX Prospects

Source: I-Net & Grindrod Asset Management, Performance annualised, net of fees

Index J251 (FTSE/JSE Preference share Index)

Yield 7.48%

Size R211m

Share PREFEX

Index construction Market cap weighted

(> 75% major banks)

1 Year 0.22%

PREFEX

Source: Source: BlackRock as at end of 2012

Core: Broad diversification by closely mirroring asset

class benchmarks

Consistent performance relative to a benchmark

Low costs

Improved risk management

Satellite: Precise exposure to a wide range of discrete

market sectors, specific styles or market capitalisations indices

Exposure to selected market segments at low costs

Eliminating security selection or manager selection risk

14

ETF Usage Example: Core Satellite Strategy

Grindrod Securities Capital Markets

Taryn Mulligan

Telephone: +27 (0)31 333 6633

Fax: +27 (0)31 571 0505

Email: [email protected]

Chris Rule

Telephone: +27 (0)11 459 1846

Fax: +27 (0)11 388 2341

Email: [email protected]

Retail Investors Websites

Retail investors can transact through the etfSA

Investor Scheme

Telephone: 0861 3837 21

Website: www.etfsa.co.za

www.proptrax.co.za

www.grindrodsecurities.co.za

www.grindrodbank.co.za

Contact