ESTIMATING CASH FLOWSadamodar/pdfiles/eqnotes/dcfcf.pdf · 114 Steps in Cash Flow Estimation ¨...

39

ESTIMATING CASH FLOWS Cash is king… Aswath Damodaran 113

Transcript of ESTIMATING CASH FLOWSadamodar/pdfiles/eqnotes/dcfcf.pdf · 114 Steps in Cash Flow Estimation ¨...

ESTIMATINGCASHFLOWS

Cashisking…

Aswath Damodaran 113

114

StepsinCashFlowEstimation

¨ Estimatethecurrentearningsofthefirm¤ Iflookingatcashflowstoequity,lookatearningsafterinterest

expenses- i.e.netincome¤ Iflookingatcashflowstothefirm,lookatoperatingearningsafter

taxes

¨ Considerhowmuchthefirminvestedtocreatefuturegrowth¤ Iftheinvestmentisnotexpensed,itwillbecategorizedascapital

expenditures.Totheextentthatdepreciationprovidesacashflow,itwillcoversomeoftheseexpenditures.

¤ Increasingworkingcapitalneedsarealsoinvestmentsforfuturegrowth

¨ Iflookingatcashflowstoequity,considerthecashflowsfromnetdebtissues(debtissued- debtrepaid)

Aswath Damodaran

114

115

MeasuringCashFlows

Cash flows can be measured to

All claimholders in the firm

EBIT (1- tax rate) - ( Capital Expenditures - Depreciation)- Change in non-cash working capital= Free Cash Flow to Firm (FCFF)

Just Equity Investors

Net Income- (Capital Expenditures - Depreciation)- Change in non-cash Working Capital- (Principal Repaid - New Debt Issues)- Preferred Dividend

Dividends+ Stock Buybacks

Aswath Damodaran

115

116

MeasuringCashFlowtotheFirm:Threepathwaystothesameendgame

Aswath Damodaran

116

Where are the tax savings from interest expenses?

AccountingEarnings,FlawedbutImportant

CashFlowsI117

Aswath Damodaran

118

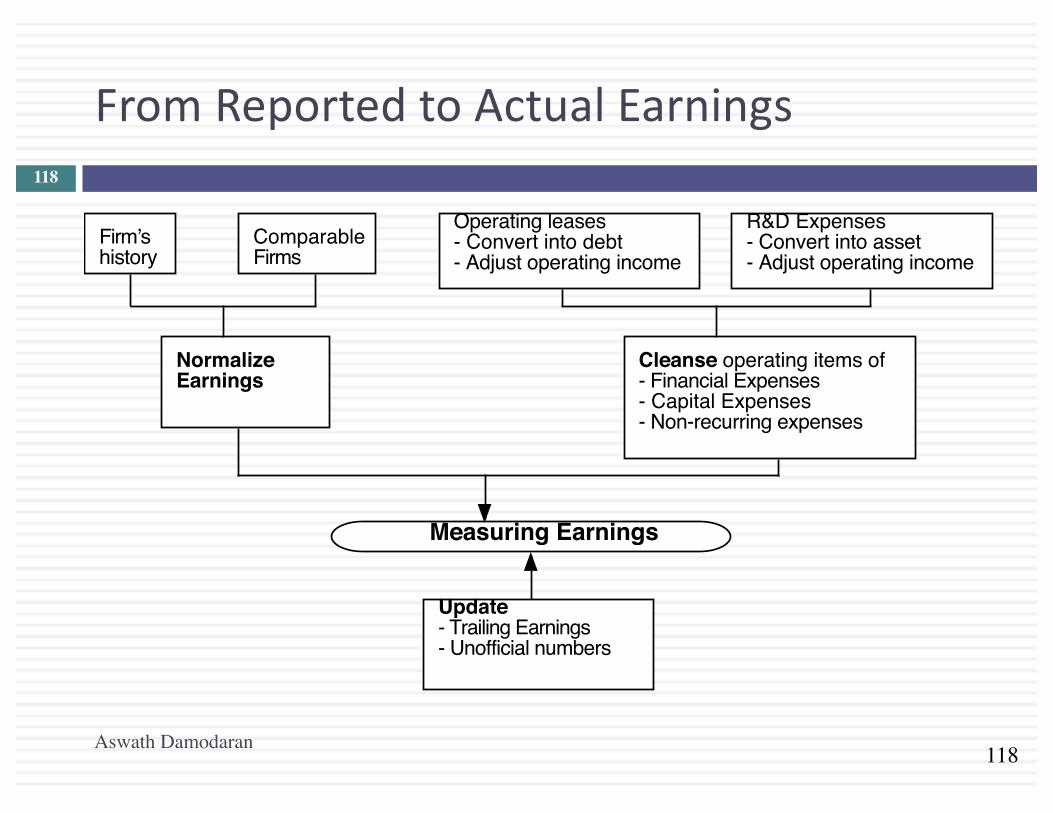

FromReportedtoActualEarnings

Update- Trailing Earnings- Unofficial numbers

Normalize Earnings

Cleanse operating items of- Financial Expenses- Capital Expenses- Non-recurring expenses

Operating leases- Convert into debt- Adjust operating income

R&D Expenses- Convert into asset- Adjust operating income

Measuring Earnings

Firmʼs history

Comparable Firms

Aswath Damodaran

118

119

I.UpdateEarnings

¨ Whenvaluingcompanies,weoftendependuponfinancialstatementsforinputsonearningsandassets.Annualreportsareoftenoutdatedandcanbeupdatedbyusing-¤ Trailing12-monthdata,constructedfromquarterlyearningsreports.¤ Informalandunofficialnewsreports,ifquarterlyreportsareunavailable.

¨ Updatingmakesthemostdifferenceforsmallerandmorevolatilefirms,aswellasforfirmsthathaveundergonesignificantrestructuring.

¨ Timesaver:Togetatrailing12-monthnumber,allyouneedisone10Kandone10Q(examplethirdquarter).UsetheYeartodatenumbersfromthe10Q.Forexample,togettrailingrevenuesfromathirdquarter10Q:¤ Trailing12-monthRevenue=Revenues(inlast10K)- Revenuesfromfirst3

quartersoflastyear+Revenuesfromfirst3quartersofthisyear.

Aswath Damodaran

119

120

II.CorrectingAccountingEarnings

¨ Makesurethattherearenofinancialexpensesmixedinwithoperatingexpenses¤ Financialexpense:Anycommitmentthatistaxdeductiblethatyouhaveto

meetnomatterwhatyouroperatingresults:Failuretomeetitleadstolossofcontrolofthebusiness.

¤ Example:OperatingLeases:Whileaccountingconventiontreatsoperatingleasesasoperatingexpenses,theyarereallyfinancialexpensesandneedtobereclassifiedassuch.Thishasnoeffectonequityearningsbutdoeschangetheoperatingearnings

¨ Makesurethattherearenocapitalexpensesmixedinwiththeoperatingexpenses¤ Capitalexpense:Anyexpensethatisexpectedtogeneratebenefitsover

multipleperiods.¤ R&DAdjustment:SinceR&Disacapitalexpenditure(ratherthanan

operatingexpense),theoperatingincomehastobeadjustedtoreflectitstreatment.

Aswath Damodaran

120

121

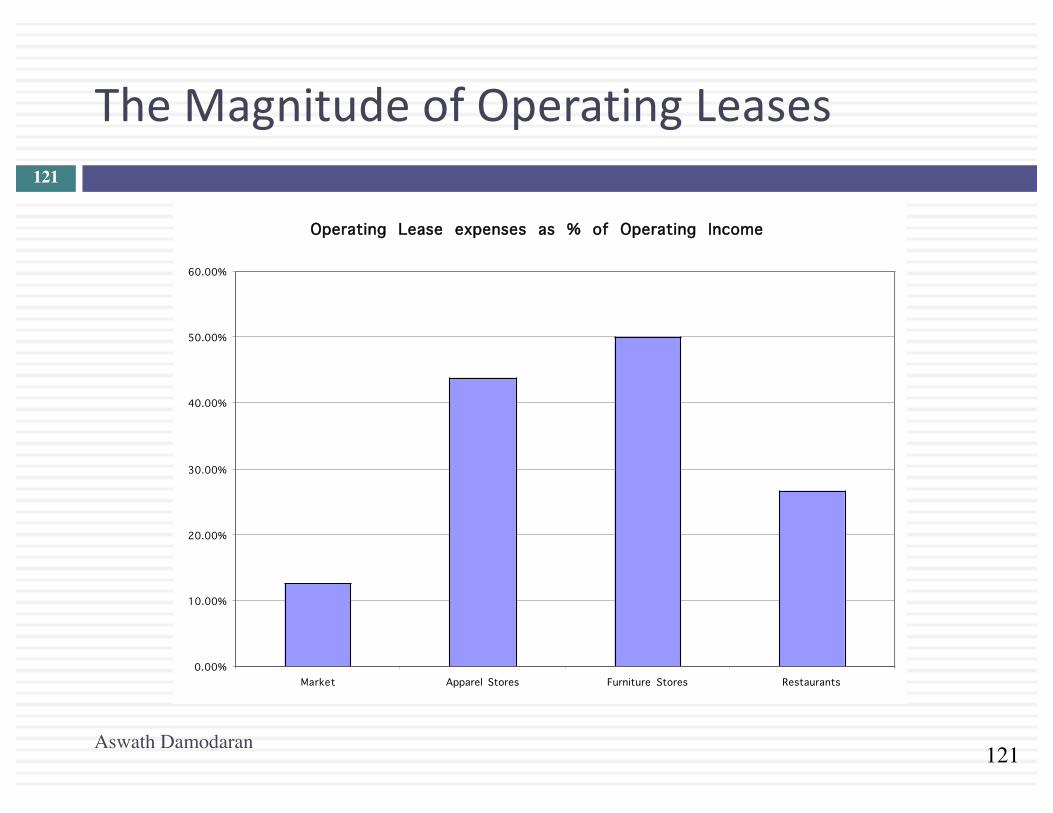

TheMagnitudeofOperatingLeases

Operating Lease expenses as % of Operating Income

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Market Apparel Stores Furniture Stores Restaurants

Aswath Damodaran

121

122

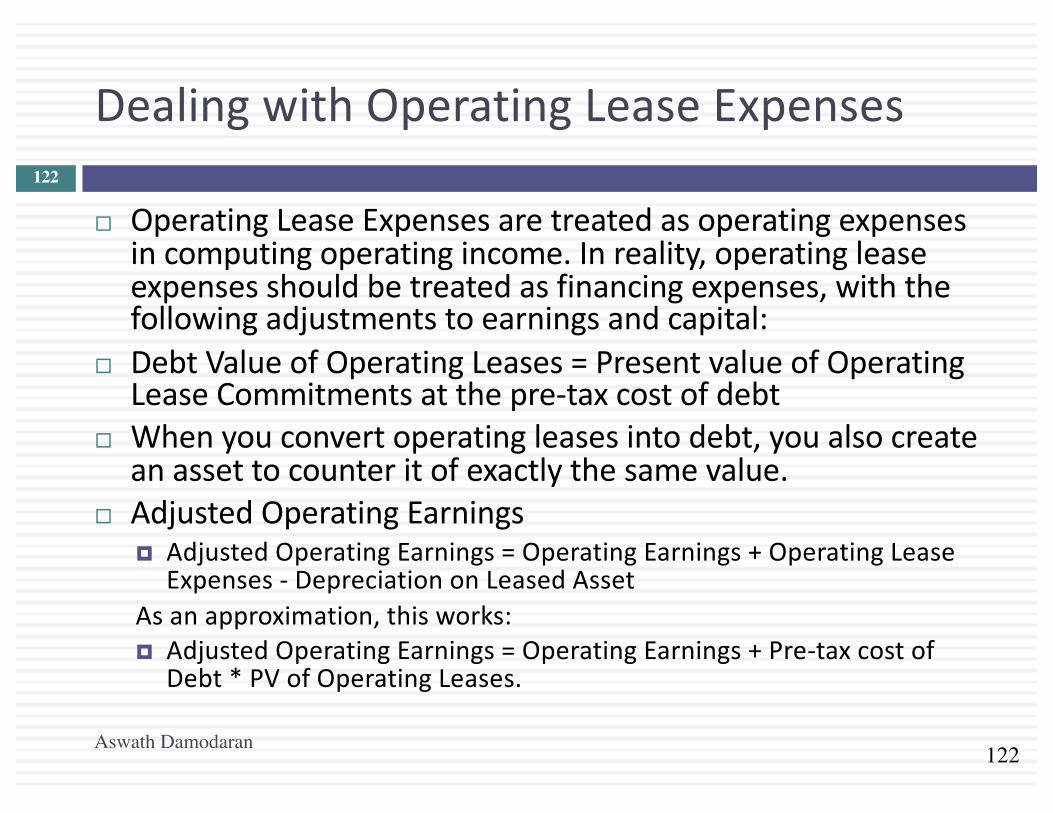

DealingwithOperatingLeaseExpenses

¨ OperatingLeaseExpensesaretreatedasoperatingexpensesincomputingoperatingincome.Inreality,operatingleaseexpensesshouldbetreatedasfinancingexpenses,withthefollowingadjustmentstoearningsandcapital:

¨ DebtValueofOperatingLeases=PresentvalueofOperatingLeaseCommitmentsatthepre-taxcostofdebt

¨ Whenyouconvertoperatingleasesintodebt,youalsocreateanassettocounteritofexactlythesamevalue.

¨ AdjustedOperatingEarnings¤ AdjustedOperatingEarnings=OperatingEarnings+OperatingLease

Expenses- DepreciationonLeasedAssetAsanapproximation,thisworks:¤ AdjustedOperatingEarnings=OperatingEarnings+Pre-taxcostof

Debt*PVofOperatingLeases.

Aswath Damodaran

122

123

OperatingLeasesatTheGapin2003

¨ TheGaphasconventionaldebtofabout$1.97billiononitsbalancesheetanditspre-taxcostofdebtisabout6%.Itsoperatingleasepaymentsinthe2003were$978millionanditscommitmentsforthefuturearebelow:

Year Commitment(millions) PresentValue(at6%)1 $899.00 $848.112 $846.00 $752.943 $738.00 $619.644 $598.00 $473.675 $477.00 $356.446&7 $982.50eachyear $1,346.04¨ DebtValueofleases= $4,396.85(Alsovalueofleasedasset)¨ DebtoutstandingatTheGap=$1,970m+$4,397m=$6,367m¨ AdjustedOperatingIncome=StatedOI+OLexp thisyear- Deprec’n

=$1,012m+978m- 4397m/7=$1,362million(7yearlifeforassets)¨ ApproximateOI=$1,012m+$4397m(.06)=$1,276m

Aswath Damodaran

123

124

TheCollateralEffectsofTreatingOperatingLeasesasDebt

! Conventional!Accounting! Operating!Leases!Treated!as!Debt!Income!Statement!

EBIT&&Leases&=&1,990&0&Op&Leases&&&&&&=&&&&978&EBIT&&&&&&&&&&&&&&&&=&&1,012&

!Income!Statement!EBIT&&Leases&=&1,990&0&Deprecn:&OL=&&&&&&628&EBIT&&&&&&&&&&&&&&&&=&&1,362&

Interest&expense&will&rise&to&reflect&the&conversion&of&operating&leases&as&debt.&Net&income&should¬&change.&

Balance!Sheet!Off&balance&sheet&(Not&shown&as&debt&or&as&an&asset).&Only&the&conventional&debt&of&$1,970&million&shows&up&on&balance&sheet&&

Balance!Sheet!Asset&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&Liability&OL&Asset&&&&&&&4397&&&&&&&&&&&OL&Debt&&&&&4397&

Total&debt&=&4397&+&1970&=&$6,367&million&

Cost&of&capital&=&8.20%(7350/9320)&+&4%&(1970/9320)&=&7.31%&

Cost&of&equity&for&The&Gap&=&8.20%&After0tax&cost&of&debt&=&4%&Market&value&of&equity&=&7350&

Cost&of&capital&=&8.20%(7350/13717)&+&4%&(6367/13717)&=&6.25%&&

Return&on&capital&=&1012&(10.35)/(3130+1970)&&&&&&&&&&=&12.90%&

Return&on&capital&=&1362&(10.35)/(3130+6367)&&&&&&&&&&=&9.30%&

&

Aswath Damodaran

124

125

TheMagnitudeofR&DExpenses

R&D as % of Operating Income

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Market Petroleum Computers

Aswath Damodaran

125

126

R&DExpenses:OperatingorCapitalExpenses

¨ AccountingstandardsrequireustoconsiderR&Dasanoperatingexpenseeventhoughitisdesignedtogeneratefuturegrowth.Itismorelogicaltotreatitascapitalexpenditures.

¨ TocapitalizeR&D,¤ SpecifyanamortizablelifeforR&D(2- 10years)¤ CollectpastR&Dexpensesforaslongastheamortizablelife¤ SumuptheunamortizedR&Dovertheperiod.(Thus,iftheamortizablelifeis5years,theresearchassetcanbeobtainedbyaddingup1/5thoftheR&Dexpensefromfiveyearsago,2/5thoftheR&Dexpensefromfouryearsago...:

Aswath Damodaran

126

127

CapitalizingR&DExpenses:SAP

¨ R&Dwasassumedtohavea5-yearlife.Year R&DExpense Unamortized AmortizationthisyearCurrent 1020.02 1.00 1020.02-1 993.99 0.80 795.19 €198.80-2 909.39 0.60 545.63 €181.88-3 898.25 0.40 359.30 €179.65-4 969.38 0.20 193.88 €193.88-5 744.67 0.00 0.00 €148.93Valueofresearchasset= €2,914millionAmortizationofresearchassetin2004 = €903millionIncreaseinOperatingIncome=1020- 903= €117million

Aswath Damodaran

127

128

TheEffectofCapitalizingR&DatSAP

! Conventional!Accounting! R&D!treated!as!capital!expenditure!Income!Statement!

EBIT&&R&D&&&=&&3045&.&R&D&&&&&&&&&&&&&&=&&1020&EBIT&&&&&&&&&&&&&&&&=&&2025&EBIT&(1.t)&&&&&&&&=&&1285&m&

!Income!Statement!EBIT&&R&D&=&&&3045&.&Amort:&R&D&=&&&903&EBIT&&&&&&&&&&&&&&&&=&2142&(Increase&of&117&m)&EBIT&(1.t)&&&&&&&&=&1359&m&

Ignored&tax&benefit&=&(1020.903)(.3654)&=&43&Adjusted&EBIT&(1.t)&=&1359+43&=&1402&m&(Increase&of&117&million)&Net&Income&will&also&increase&by&117&million&&

Balance!Sheet!Off&balance&sheet&asset.&Book&value&of&equity&at&3,768&million&Euros&is&understated&because&biggest&asset&is&off&the&books.&

Balance!Sheet!Asset&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&&Liability&R&D&Asset&&&&2914&&&&&Book&Equity&&&+2914&

Total&Book&Equity&=&3768+2914=&6782&mil&&Capital!Expenditures!

Conventional&net&cap&ex&of&2&million&Euros&

Capital!Expenditures!Net&Cap&ex&=&2+&1020&–&903&=&119&mil&

Cash!Flows!EBIT&(1.t)&&&&&&&&&&=&&1285&&.&Net&Cap&Ex&&&&&&=&&&&&&&&2&FCFF&&&&&&&&&&&&&&&&&&=&&1283&&&&&&

Cash!Flows!EBIT&(1.t)&&&&&&&&&&=&&&&&1402&&&.&Net&Cap&Ex&&&&&&=&&&&&&&119&FCFF&&&&&&&&&&&&&&&&&&=&&&&&1283&m&

Return&on&capital&=&1285/(3768+530)& Return&on&capital&=&1402/(6782+530)&

Aswath Damodaran

128

129

III.One-TimeandNon-recurringCharges

¨ Assumethatyouarevaluingafirmthatisreportingalossof$500million,duetoaone-timechargeof$1billion.Whatistheearningsyouwoulduseinyourvaluation?a. Alossof$500millionb. Aprofitof$500million

¨ Wouldyouranswerbeanydifferentifthefirmhadreportedone-timelossesliketheseonceeveryfiveyears?a. Yesb. No

Aswath Damodaran

129

130

IV.AccountingMalfeasance….

¨ Thoughallfirmsmaybegovernedbythesameaccountingstandards,thefidelitythattheyshowtothesestandardscanvary.Moreaggressivefirmswillshowhigherearningsthanmoreconservativefirms.

¨ Whileyouwillnotbeabletocatchoutrightfraud,youshouldlookforwarningsignalsinfinancialstatementsandcorrectforthem:¤ Incomefromunspecifiedsources- holdingsinotherbusinessesthatare

notrevealedorfromspecialpurposeentities.¤ Incomefromassetsalesorfinancialtransactions(foranon-financialfirm)¤ Suddenchangesinstandardexpenseitems- abigdropinS,G&AorR&D

expensesasapercentofrevenues,forinstance.¤ Frequentaccountingrestatements¤ Accrualearningsthatrunaheadofcashearningsconsistently¤ Bigdifferencesbetweentaxincomeandreportedincome

Aswath Damodaran

130

131

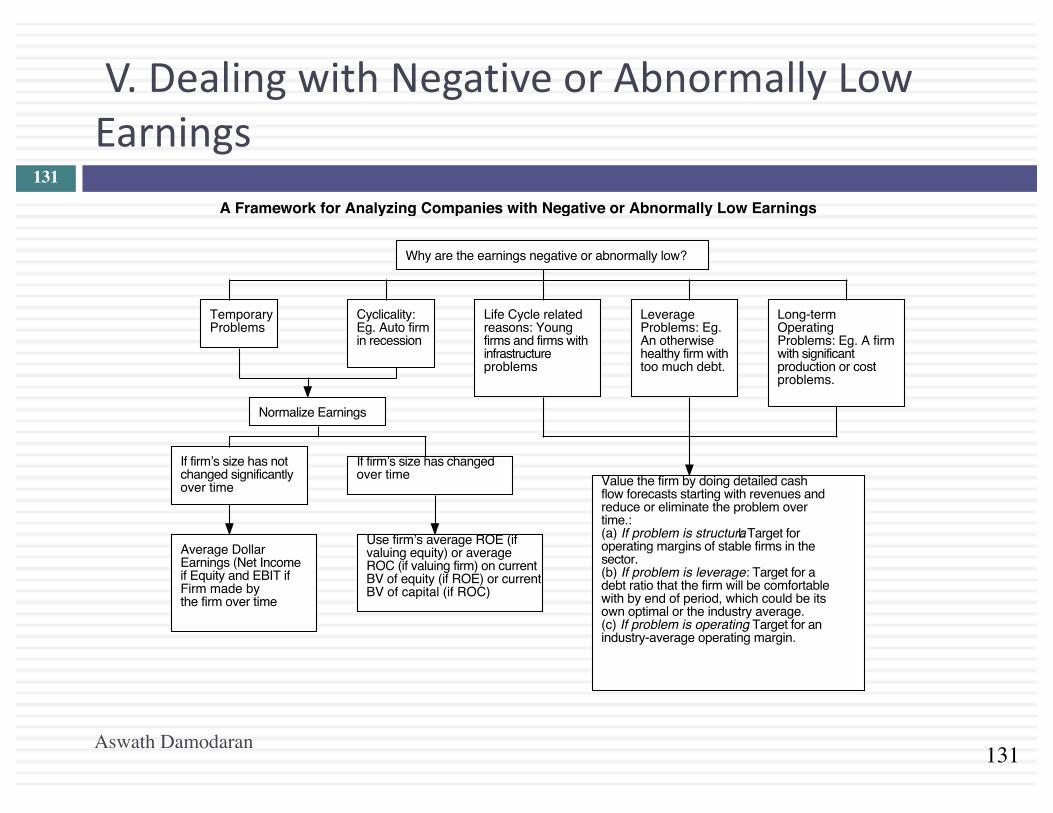

V.DealingwithNegativeorAbnormallyLowEarnings

A Framework for Analyzing Companies with Negative or Abnormally Low Earnings

Why are the earnings negative or abnormally low?

TemporaryProblems

Cyclicality:Eg. Auto firmin recession

Life Cycle related reasons: Young firms and firms with infrastructure problems

LeverageProblems: Eg. An otherwise healthy firm with too much debt.

Long-termOperatingProblems: Eg. A firm with significant production or cost problems.

Normalize Earnings

Value the firm by doing detailed cash flow forecasts starting with revenues and reduce or eliminate the problem over time.:(a) If problem is structural: Target for operating margins of stable firms in the sector.(b) If problem is leverage: Target for a debt ratio that the firm will be comfortable with by end of period, which could be its own optimal or the industry average.(c) If problem is operating: Target for an industry-average operating margin.

If firmʼs size has notchanged significantlyover time

Average DollarEarnings (Net Income if Equity and EBIT if Firm made bythe firm over time

If firmʼs size has changedover time

Use firmʼs average ROE (if valuing equity) or average ROC (if valuing firm) on current BV of equity (if ROE) or current BV of capital (if ROC)

Aswath Damodaran

131

TaxesandReinvestment

CashFlowsII132

Aswath Damodaran

133

Whattaxrate?

¨ Thetaxratethatyoushoulduseincomputingtheafter-taxoperatingincomeshouldbea. Theeffectivetaxrateinthefinancialstatements(taxes

paid/Taxableincome)b. ThetaxratebasedupontaxespaidandEBIT(taxespaid/EBIT)c. Themarginaltaxrateforthecountryinwhichthecompany

operatesd. Theweightedaveragemarginaltaxrateacrossthecountriesin

whichthecompanyoperatese. Noneoftheabovef. Anyoftheabove,aslongasyoucomputeyourafter-taxcostof

debtusingthesametaxrate

Aswath Damodaran

133

134

TheRightTaxRatetoUse

¨ Thechoicereallyisbetweentheeffectiveandthemarginaltaxrate.Indoingprojections,itisfarsafertousethemarginaltaxratesincetheeffectivetaxrateisreallyareflectionofthedifferencebetweentheaccountingandthetaxbooks.

¨ Byusingthemarginaltaxrate,wetendtounderstatetheafter-taxoperatingincomeintheearlieryears,buttheafter-taxtaxoperatingincomeismoreaccurateinlateryears

¨ Ifyouchoosetousetheeffectivetaxrate,adjustthetaxratetowardsthemarginaltaxrateovertime.¤ Whileanargumentcanbemadeforusingaweightedaverage

marginaltaxrate,itissafesttousethemarginaltaxrateofthecountry

Aswath Damodaran

134

135

ATaxRateforaMoneyLosingFirm

¨ Assumethatyouaretryingtoestimatetheafter-taxoperatingincomeforafirmwith$1billioninnetoperatinglossescarriedforward.Thisfirmisexpectedtohaveoperatingincomeof$500millioneachyearforthenext3years,andthemarginaltaxrateonincomeforallfirmsthatmakemoneyis40%.Estimatetheafter-taxoperatingincomeeachyearforthenext3years.

Year1 Year2 Year3EBIT 500 500 500TaxesEBIT(1-t)Taxrate

Aswath Damodaran

135

136

NetCapitalExpenditures

¨ Netcapitalexpendituresrepresentthedifferencebetweencapitalexpendituresanddepreciation.Depreciationisacashinflowthatpaysforsomeoralot(orsometimesallof)thecapitalexpenditures.

¨ Ingeneral,thenetcapitalexpenditureswillbeafunctionofhowfastafirmisgrowingorexpectingtogrow.Highgrowthfirmswillhavemuchhighernetcapitalexpendituresthanlowgrowthfirms.

¨ Assumptionsaboutnetcapitalexpenditurescanthereforeneverbemadeindependentlyofassumptionsaboutgrowthinthefuture.

Aswath Damodaran

136

137

Capitalexpendituresshouldinclude

¨ Researchanddevelopmentexpenses,oncetheyhavebeenre-categorizedascapitalexpenses.Theadjustednetcapexwillbe¤ AdjustedNetCapitalExpenditures=NetCapitalExpenditures+

Currentyear’sR&Dexpenses- AmortizationofResearchAsset¨ Acquisitionsofotherfirms,sincethesearelikecapital

expenditures.Theadjustednetcapexwillbe¤ AdjustedNetCapEx=NetCapitalExpenditures+Acquisitionsofother

firms- Amortizationofsuchacquisitions¨ Twocaveats:

1.Mostfirmsdonotdoacquisitionseveryyear.Hence,anormalizedmeasureofacquisitions(lookingatanaverageovertime)shouldbeused

2.Thebestplacetofindacquisitionsisinthestatementofcashflows,usuallycategorizedunderotherinvestmentactivities

Aswath Damodaran

137

138

Cisco’sAcquisitions:1999

Acquired MethodofAcquisition PricePaidGeoTel Pooling $1,344Fibex Pooling $318Sentient Pooling $103AmericanInternet Purchase $58SummaFour Purchase $129ClarityWireless Purchase $153Selsius Systems Purchase $134PipeLinks Purchase $118Amteva Tech Purchase $159

$2,516

Aswath Damodaran

138

139

Cisco’sNetCapitalExpendituresin1999

CapExpenditures(fromstatementofCF)=$584mil- Depreciation(fromstatementofCF) =$486milNetCapEx(fromstatementofCF)=$98mil+R&Dexpense =$1,594mil- AmortizationofR&D =$485mil+Acquisitions =$2,516milAdjustedNetCapitalExpenditures =$3,723mil

¨ (Amortizationwasincludedinthedepreciationnumber)

Aswath Damodaran

139

140

WorkingCapitalInvestments

¨ Inaccountingterms,theworkingcapitalisthedifferencebetweencurrentassets(inventory,cashandaccountsreceivable)andcurrentliabilities(accountspayables,shorttermdebtanddebtduewithinthenextyear)

¨ Acleanerdefinitionofworkingcapitalfromacashflowperspectiveisthedifferencebetweennon-cashcurrentassets(inventoryandaccountsreceivable)andnon-debtcurrentliabilities(accountspayable)

¨ Forfirmsinsomesectors,itistheinvestmentinworkingcapitalthatisthebiggerpartofreinvestment.

Aswath Damodaran

140

141

WorkingCapital:GeneralPropositions

1. Working Capital Detail: While some analysts break downworking capital into detail (inventory, deferred taxes,payables etc.), it is a pointless exercise unless you feel thatyou can bring some specific information that lets youforecast the details.

2. Working Capital Volatility: Changes in non-cash workingcapital from year to year tend to be volatile. So, building ofthe change in the most recent year is dangerous. It is betterto either estimate the change based on working capital as apercent of sales, while keeping an eye on industry averages.

3. Negative Working Capital: Some firms have negative non-cash working capital. Assuming that this will continue intothe future will generate positive cash flows for the firm andwill get more positive as growth increases.

Aswath Damodaran

141

142

VolatileWorkingCapital?

Amazon Cisco MotorolaRevenues $1,640 $12,154 $30,931Non-cashWC -$419 -$404 $2547%ofRevenues -25.53% -3.32% 8.23%Changefromlastyear $(309) ($700) ($829)Average:last3years -15.16% -3.16% 8.91%Average:industry 8.71% -2.71% 7.04%

MyPredictionWCas%ofRevenue 3.00% 0.00% 8.23%

Aswath Damodaran

142

Fromthefirmtoequity

CashFlowsIII143

Aswath Damodaran

144

DividendsandCashFlowstoEquity

¨ Inthestrictestsense,theonlycashflowthataninvestorwillreceivefromanequityinvestmentinapubliclytradedfirmisthedividendthatwillbepaidonthestock.

¨ Actualdividends,however,aresetbythemanagersofthefirmandmaybemuchlowerthanthepotentialdividends(thatcouldhavebeenpaidout)¤ managersareconservativeandtrytosmoothoutdividends¤ managersliketoholdontocashtomeetunforeseenfuturecontingenciesandinvestmentopportunities

¨ Whenactualdividendsarelessthanpotentialdividends,usingamodelthatfocusesonlyondividendswillunderstatethetruevalueoftheequityinafirm.

Aswath Damodaran

144

145

MeasuringPotentialDividends

¨ Someanalystsassumethattheearningsofafirmrepresentitspotentialdividends.Thiscannotbetrueforseveralreasons:¤ Earningsarenotcashflows,sincetherearebothnon-cashrevenuesand

expensesintheearningscalculation¤ Evenifearningswerecashflows,afirmthatpaiditsearningsoutas

dividendswouldnotbeinvestinginnewassetsandthuscouldnotgrow¤ Valuationmodels,whereearningsarediscountedbacktothepresent,will

overestimatethevalueoftheequityinthefirm¨ Thepotentialdividendsofafirmarethecashflowsleftoverafter

thefirmhasmadeany“investments” itneedstomaketocreatefuturegrowthandnetdebtrepayments(debtrepayments- newdebtissues)¤ Thecommoncategorizationofcapitalexpendituresintodiscretionaryand

non-discretionarylosesitsbasiswhenthereisfuturegrowthbuiltintothevaluation.

Aswath Damodaran

145

146

EstimatingCashFlows:FCFE

¨ CashflowstoEquityforaLeveredFirmNetIncome- (CapitalExpenditures- Depreciation)- Changesinnon-cashWorkingCapital- (PrincipalRepayments- NewDebtIssues)=FreeCashflowtoEquity

¨ Ihaveignoredpreferreddividends.Ifpreferredstockexist,preferreddividendswillalsoneedtobenettedout

Aswath Damodaran

146

147

EstimatingFCFEwhenLeverageisStable

NetIncome- (1- DR)(CapitalExpenditures- Depreciation)- (1- DR)WorkingCapitalNeeds=FreeCashflowtoEquity

DR=Debt/CapitalRatioForthisfirm,

¤ Proceedsfromnewdebtissues=PrincipalRepayments+d(CapitalExpenditures- Depreciation+WorkingCapitalNeeds)

¨IncomputingFCFE,thebookvaluedebttocapitalratioshouldbeusedwhenlookingbackintimebutcanbereplacedwiththemarketvaluedebttocapitalratio,lookingforward.

Aswath Damodaran

147

148

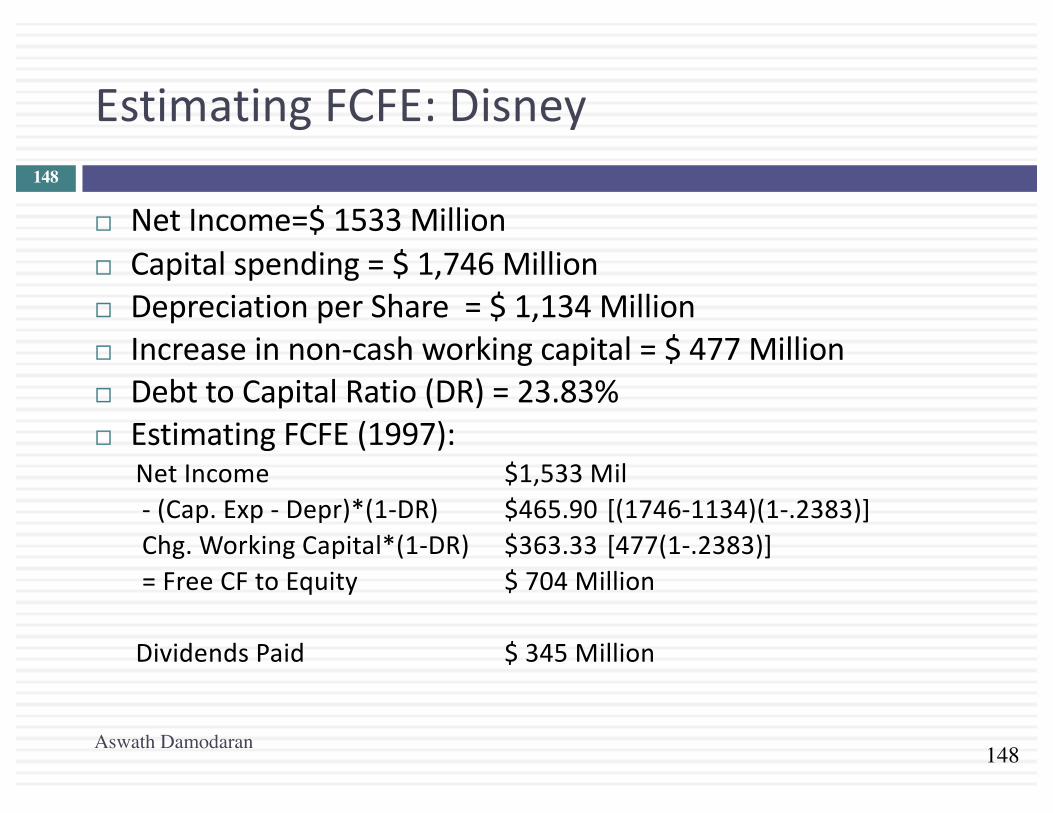

EstimatingFCFE:Disney

¨ NetIncome=$1533Million¨ Capitalspending=$1,746Million¨ DepreciationperShare=$1,134Million¨ Increaseinnon-cashworkingcapital=$477Million¨ DebttoCapitalRatio(DR)=23.83%¨ EstimatingFCFE(1997):

NetIncome $1,533Mil- (Cap.Exp - Depr)*(1-DR) $465.90[(1746-1134)(1-.2383)]Chg.WorkingCapital*(1-DR) $363.33 [477(1-.2383)]=FreeCFtoEquity $704Million

DividendsPaid $345Million

Aswath Damodaran

148

149

FCFEandLeverage:Isthisafreelunch?

Debt Ratio and FCFE: Disney

0

200

400

600

800

1000

1200

1400

1600

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Debt Ratio

FCFE

Aswath Damodaran

149

150

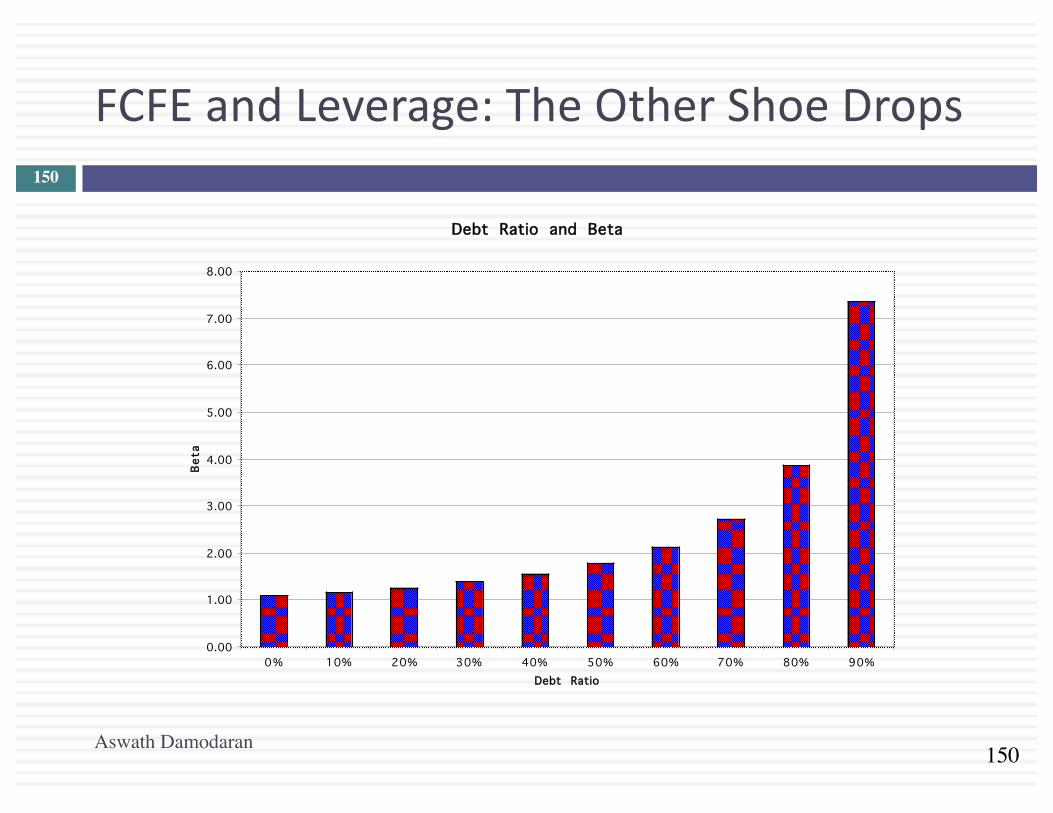

FCFEandLeverage:TheOtherShoeDrops

Debt Ratio and Beta

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%Debt Ratio

Beta

Aswath Damodaran

150

151

Leverage,FCFEandValue

¨ Inadiscountedcashflowmodel,increasingthedebt/equityratiowillgenerallyincreasetheexpectedfreecashflowstoequityinvestorsoverfuturetimeperiodsandalsothecostofequityappliedindiscountingthesecashflows.Whichofthefollowingstatementsrelatingleveragetovaluewouldyousubscribeto?a. Increasingleveragewillincreasevaluebecausethecashfloweffects

willdominatethediscountrateeffectsb. Increasingleveragewilldecreasevaluebecausetheriskeffectwillbe

greaterthanthecashfloweffectsc. Increasingleveragewillnotaffectvaluebecausetheriskeffectwill

exactlyoffsetthecashfloweffectd. Anyoftheabove,dependinguponwhatcompanyyouarelookingat

andwhereitisintermsofcurrentleverage

Aswath Damodaran

151