Estate and Fiduciary Income Tax Planning for S...

31

1 BNY MELLON WEALTH MANAGEMENT Estate and Fiduciary Income Tax Planning for S Corporations Jeremiah W. Doyle IV Senior Vice President BNY Mellon Wealth Management Boston, MA [email protected] BNY MELLON WEALTH MANAGEMENT Agenda • Introduction • S corporation taxation • Reporting Income on the death of a shareholder • Eligible shareholder • Basis adjustment at death • Estate as shareholder • Election of estate FYE • Trusts as eligible shareholder – Grantor trust – Testamentary trust – Voting trust – QSST – ESBT • S corporation distributions to trust or estate – TAI v. DNI

-

Upload

truonglien -

Category

Documents

-

view

217 -

download

1

Transcript of Estate and Fiduciary Income Tax Planning for S...

1

BNY MELLON WEALTH MANAGEMENT

Estate and Fiduciary Income Tax Planning for S Corporations

Jeremiah W. Doyle IV

Senior Vice President

BNY Mellon Wealth Management

Boston, MA

BNY MELLON WEALTH MANAGEMENT

Agenda

• Introduction

• S corporation taxation

• Reporting Income on the death of a shareholder

• Eligible shareholder

• Basis adjustment at death

• Estate as shareholder

• Election of estate FYE

• Trusts as eligible shareholder

– Grantor trust

– Testamentary trust

– Voting trust

– QSST

– ESBT

• S corporation distributions to trust or estate – TAI v. DNI

2

BNY MELLON WEALTH MANAGEMENT

Agenda (cont.)

• S corporation – who pays the tax?

• S corporations and PALs

• S corporations – taxation of distributions

• Funding issues

BNY MELLON WEALTH MANAGEMENT

Introduction

• S corporations are flow-through entities like partnerships but they generally follow C corporation rules for distributions, redemptions and sales of stock

• Only certain persons and entities are eligible to own S corporation stock

• Unlike partnerships which can make a §754 election to adjust the inside basis of assets upon the death of a partner, a S corporation cannot do so

3

BNY MELLON WEALTH MANAGEMENT

S Corporation - Taxation

• Beneficiary’s income determined on a pro-rata basis (per share, per day)

• Decedent’s 1040 reports income from beginning of year to D/D

– No IRD

• Successor in interest reports income from day after D/D to end of year

BNY MELLON WEALTH MANAGEMENT

Reporting Income on the Death of a Shareholder

• Income, losses, deductions and credits determined on daily basis, using a per-day, per share allocation

• Decedent’s final 1040 includes a pro rata share of the income, loss and other items of the S corporation determined as of date of death.

– Since the decedent reports his pro rata share of S corporation income thru the end of the year, there is no IRD

• Exception: if the S corporation at the date of the decedent’s death had a right to an item that would have been IRD if held by the decedent directly, the decedent’s pro-rata share of that item is IRD to the recipient of the decedent’s stock

– The portion of the value of the stock attributable to IRD is not entitled to a step-up in basis

• Estate recognizes a pro rata share through the end of the corporation’s taxable year.

4

BNY MELLON WEALTH MANAGEMENT

Reporting Income on the Death of a Shareholder - Election

• If a shareholder “terminates his interest” in the S corporation during the year, the S corporation, with the consent of the affected shareholders, may elect to close the taxable year and treat the year as if it consisted of two taxable years, the first of which ends with the date of termination.

• If the corporation’s income, deductions and other items did not accrue ratably during the year, making this election could be beneficial

• All shareholders must consent to the election.

– Example: Decedent in high tax bracket for the year from other sources but the S corporation suffered a loss during the period preceding the decedent’s death, the election could result in substantial tax savings

BNY MELLON WEALTH MANAGEMENT

S Corporation - Taxation

• Special allocation rule under §1377(a)(2) for “termination of interest”

• Share of income computed as if taxable year consisted of 2 taxable years, the first of which ends on the D/D

– Special allocation valuable if income, deductions did not accrue ratably during the year

5

BNY MELLON WEALTH MANAGEMENT

S Corporation – Special Allocation

6/30 D/D

6/30 D/D

S Corporation earns $365 for the year

$181

($100)

$184

$465

Regular Method:

Special Allocation:

BNY MELLON WEALTH MANAGEMENT

Compare: Death of Partner

• Just the opposite of an S corporation

• Default method: interim closing of the books

– Share of income computed as if taxable year consisted of 2 taxable years, the first of which ends on the D/D

• Alternatively, the partners may agree to the pro-ration method i.e. allocation to each partner a fraction of partnership income for the entire year regardless of when the income was earned or the expenses incurred

6

BNY MELLON WEALTH MANAGEMENT

Death of Shareholder

• Death of shareholder does not terminate S election

• Where the stock ends up after the death of a shareholder presents an estate planning problem

• If the stock is distributed to an ineligible shareholder, the S election is terminated

BNY MELLON WEALTH MANAGEMENT

Eligible Shareholders

• Generally, only individuals and certain entities are eligible S corporation shareholders

– Individual i.e. U.S. residents

– Estates

– Certain trusts

– Certain tax exempt organizations

7

BNY MELLON WEALTH MANAGEMENT

Eligible Shareholders• A single member LLC that is disregarded for tax purposes is a

permitted S corporation shareholder as long as the underlying owner is a permitted shareholder.

• An IRA may not hold S stock

• As of 1/1/98 qualified plans and charities described in §§401(a) or 501(c)(3) and exempt from taxation under §501(a) may be S corporation shareholders

– S corporation income as well as any gain on the sale of S stock is taxed as UBTI to the qualified plan and charity

• ESOPs are exempt from the UBTI rules

• Private foundations are subject to a 10% excise tax (increasing to 200% if the stock is not disposed of by year-end) on “excess business holdings” when they, together with any “disqualified persons” own more than 20% of the voting stock of an incorporated business.

BNY MELLON WEALTH MANAGEMENT

Eligible Shareholders

• S corporation stock held by an ineligible shareholder terminates the S election

– Any suspended PALs remain suspended until the stock is disposed of or the corporation makes another S election.

– A new S election is not permitted until the 5th taxable year following the year in which the termination occurred.

– If the corporation converted from a C to an S corporation within the last 10 years, the 10 year holding period for built-in gain starts over again.

– Relief from S corporation termination is available but it is not automatic. It must be requested via a PLR for which the IRS charges a $11,500 user fee.

8

BNY MELLON WEALTH MANAGEMENT

Estate as Shareholder

• An estate may hold S stock indefinitely, subject only to prolonged administration rules

– No requirement that PR elect to continue S election

• Estates may elect S status for corporations that were not operated as a S corporation by the decedent prior to the decedent’s death. Rev. Rul. 92-83, 1992-2 C.B. 36.

– If decedent died within 2 ½ months of the beginning of the C corporation’s taxable year, a retroactive S election can be made and have the pre-death income taxed on the decedent’s final 1040

• An estate tax deduction is available for the income taxes paid on such income

BNY MELLON WEALTH MANAGEMENT

Estate as Shareholder

• The estate, not its beneficiaries, is the S corporation shareholder

– Thus, the following disqualified beneficiaries that could not own S corporation stock could receive the benefit of S corporation status during the administration of the estate:

• Non-resident aliens

• Complex and sprinkle trusts with multiple beneficiaries (absent a QSST or ESBT election)

• Charitable split interest trusts

– Executor may want to keep stock in estate and keep estate open ALAP if stock would otherwise be distributed to an ineligible shareholder

– §6166 election would allow estate to remain open until estate completes payment of FET i.e. up to 15 years

– Thus, probate avoidance may not be advantageous for beneficiaries who are ineligible S corporation shareholders

9

BNY MELLON WEALTH MANAGEMENT

Election of Estate FYE

• Estate as a S corporation shareholder allows for a deferral of recognition of S corporation income– Example: Estate with November 30 FYE doesn’t have to recognize

December 31 FYE S corporation income until the following November 30 FYE

• Two year exemption of estates from estimated tax payments may be beneficial

12/31

11/30

S Corp

Estate

BNY MELLON WEALTH MANAGEMENT

Trusts as Eligible S Shareholders

• In addition to estates, only certain trusts are eligible S corporation shareholders

– Grantor Trust

– Grantor Trust after owner’s death* – 2 years beginning with D/D

– Testamentary Trust* – 2 years after transfer of assets to trust

– Voting Trust

– QSST

– ESBT

• In all cases, the trust must be a domestic trust

*May continue as eligible S corporation shareholder by electing QSST or ESBT status

10

BNY MELLON WEALTH MANAGEMENT

S Corporation - Trusts

• LE/GTPOA marital trust under §2056(b)(5) is eligible S corporation shareholder due to grantor trust status

• QTIP trust under §2056(b)(7) is not an eligible S corporation shareholder unless a QSST or ESBT election is made

• A GRAT is an eligible S corporation shareholder assuming it is drafted as a wholly owned grantor trust.

• A QRT that makes a §645 election

– Election lasts for 2 years if no estate tax return is required (thus, no additional time to hold S stock) or 6 months after the final determination of the estate tax liability if an estate tax return is required to be filed.

• QDOT under §2056A cannot qualify as a QSST unless the spouse/beneficiary becomes a U.S. citizen

• §2503(c) trust qualifies as a QSST as long as the trustee distributes or is required to distribute the income at least annually to the beneficiary

• CRAT or CRUT cannot qualify as a QSST

BNY MELLON WEALTH MANAGEMENT

S Corporation – Grantor Trusts

• Must be a wholly owned grantor trust

• A grantor trust is an eligible S corporation shareholder for up to 2 years from the grantor’s death.

– During this period, the estate is treated as the shareholder for eligibility purposes.

– However, the S corporation income is reported by the trust, not the estate.

• Note that anytime after the grantor’s death the grantor trust can elect to be a QSST or an ESBT if it otherwise qualifies.

11

BNY MELLON WEALTH MANAGEMENT

S Corporation – Grantor Trusts

• Termination of grantor trust at owner’s death

– If trust distributes outright, determine if distributees are qualified to hold S stock

• If distributees are corporation, p/ship, ineligible trust or foreign individual or the number of S/H exceeds 100, S election automatically terminated

– If trust continues after owner’s death, trust is eligible S/H for 2 years• Trust would also be eligible S/H if it qualified as a QSST or ESBT

BNY MELLON WEALTH MANAGEMENT

S Corporation – Voting Trusts

• Created to exercise voting control over the stock

• The beneficial owners of the trust are treated as the owners of their portion of the trust – they must be citizens or residents of the U.S.

• Requirements of a voting trust:

– Written trust agreement entered into by the S/H must delegate the right to vote to one or more trustees

– All distributions with respect to the stock must be paid to or on behalf of the beneficial owners of the stock

– The title and possession of the stock must be delivered to the beneficial owners upon the termination of the trust

– The trust must terminate under its terms or by state law on or before a specific date or event. Reg. 1.1361-(1)(h) (1)(v).

12

BNY MELLON WEALTH MANAGEMENT

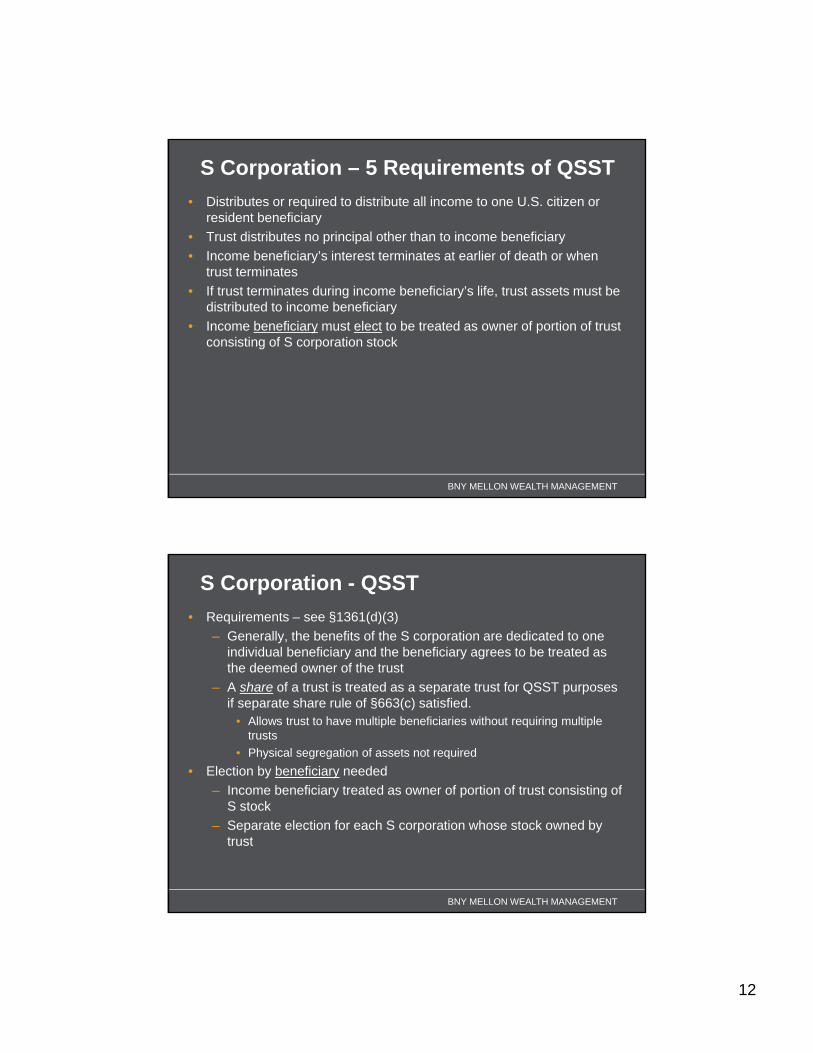

S Corporation – 5 Requirements of QSST

• Distributes or required to distribute all income to one U.S. citizen or resident beneficiary

• Trust distributes no principal other than to income beneficiary

• Income beneficiary’s interest terminates at earlier of death or when trust terminates

• If trust terminates during income beneficiary’s life, trust assets must be distributed to income beneficiary

• Income beneficiary must elect to be treated as owner of portion of trust consisting of S corporation stock

BNY MELLON WEALTH MANAGEMENT

S Corporation - QSST

• Requirements – see §1361(d)(3)

– Generally, the benefits of the S corporation are dedicated to one individual beneficiary and the beneficiary agrees to be treated as the deemed owner of the trust

– A share of a trust is treated as a separate trust for QSST purposes if separate share rule of §663(c) satisfied.

• Allows trust to have multiple beneficiaries without requiring multiple trusts

• Physical segregation of assets not required

• Election by beneficiary needed

– Income beneficiary treated as owner of portion of trust consisting of S stock

– Separate election for each S corporation whose stock owned by trust

13

BNY MELLON WEALTH MANAGEMENT

QSST Election

• Election causes beneficiary to be treated as owner of portion of trust consisting of S corporation stock as if beneficiary owned the trust under §678.

• If a QSST sells the S corporation stock, the trust rather than the beneficiary of the QSST recognizes the gain or loss. Reg. 1.1361-1(j)(8).

• Election made separately for each S corporation owned by the trust

• Generally, election must be made within two months and 16 days after S corporation is transferred to trust or, if trust holds stock of corporation that makes an S election, after the S election is effective.

• Once made, election is treated as made for successive beneficiaries unless such a beneficiary affirmatively refuses to consent to the election within two months and 15 days of becoming a current income beneficiary

– Note: an income beneficiary of a QSST has a right that direct shareholders of an S corporation do not have i.e. the right to terminate an S election individually

• A special QSST election procedure is available for an ESBT that converts to a QSST

BNY MELLON WEALTH MANAGEMENT

QSST – Death of Income Beneficiary

• If income beneficiary dies and the trust continues to hold S stock but the trust doesn’t qualify as a QSST, grantor trust or ESBT, then for 2 years after the income beneficiary’s death, the estate is treated as the S shareholder for eligibility purposes.

– Within the 2 years the trust must dispose of the stock to an eligible S/H or make an ESBT election to avoid termination of the S election

• Even though the estate is treated as the S/H for eligibility purposes, the trust is treated as the S/H for purposes of reporting the tax items on the Form K-1.

14

BNY MELLON WEALTH MANAGEMENT

S Corporation – ESBT §1361(e) -Requirements

• All beneficiaries of the trust must be individuals, estates, charitable organizations described in §§170(c)(2)-(5) or governmental organizations described in §170(c)(1).

• No interest in the trust may be acquired by purchase i.e. it must be acquired by gift, bequest or transfer in trust.

• The trustee must elect ESBT treatment

BNY MELLON WEALTH MANAGEMENT

S Corporation – ESBT §1361(e) -Beneficiaries

• A government organization may not be a potential current beneficiary (PCB)

• A beneficiary generally includes any person who has a present, remainder or reversionary interest in the trust.

• A beneficiary doesn’t include a person whose interest is so remote as to be negligible

• A beneficiary does not include a person in whose favor a power of appointment can be exercised until the power is actually exercised in favor of that person.

• CRATs and CRUT are excluded by statute for eligibility as ESBT shareholders

• A CLAT may be an S shareholder.

15

BNY MELLON WEALTH MANAGEMENT

S Corporation – ESBT §1361(e) -Beneficiaries

• The S election will terminate if an ESBT has a potential current beneficiary (PCB) that is an ineligible shareholder or the number of shareholders exceeds 100.– If so, the trust has 1 year from the terminating event to dispose of

the S stock to avoid loss of the S election.• A PCB is any beneficiary who is entitled to, or in the discretion of any

person may receive, a distribution from the principal or income of the trust.– It does not include a person who only holds a future interest in the

trust– It doesn’t include a person who is only entitled to receive a

distribution after a specified time or when a specified event occurs until the time arrives or event occurs.

BNY MELLON WEALTH MANAGEMENT

S Corporation – ESBT §1361(e)

• Election needed by trustee• Portion of ESBT that consists of S corporation stock is separate trust

for income tax purposes– ESBT share taxable on S corporation income at highest trust

income tax rate (currently 35/%)• Long-term capital gains taxed at the capital gain rate that applies

(currently 15% for most LTCG)

– Normal Subchapter J rules do not apply to S corporation portion– ESBT allows trust to have 2 or more beneficiaries, accumulate

income, make discretionary distributions of both income and principal among the beneficiaries

• Cost for distribution flexibility is higher income tax on S corporation’s income

16

BNY MELLON WEALTH MANAGEMENT

S Corporation – Basis Adjustment at Death

• Stock of S corporation get a new basis at death equal to FMV under §1014

• It also gets an automatic long-term holding period under §1223(11)

• The inside basis of the assets owned by the S corporation does not get any basis adjustment– Thus, the decedent’s successor to the S corporation stock will be

required to report any built in gain or loss when the S corporation sells its assets

• However, a partnership can make a §754 election to adjust the inside basis of partnership assets with respect to a deceased partner.

BNY MELLON WEALTH MANAGEMENT

Death of a Partner – Basis

• Partner’s basis in p/ship interest is separate and distinct from p/ship’s own basis in the underlying assets of the p/ship

• Basis of deceased partner’s partnership interest is its FMV as of the D/D or the A/V date

• Partnership does not receive new basis for partnership assets upon death of a partner

• Consider the §754 election

17

BNY MELLON WEALTH MANAGEMENT

Mary Ann Ginger

BNY MELLON WEALTH MANAGEMENT

Death of a Partner – Basis

• Ginger and Mary Ann, form a partnership

• Buy a apartment building for $100,000

• Building appreciates to $1,000,000

• Ginger dies

• $500,000 gets included in Ginger’s estate for FET purposes

• Ginger’s basis in her partnership interest is $500,000

• The partnership’s basis in the bldg is $100,000

18

BNY MELLON WEALTH MANAGEMENT

Death of a Partner – Basis (cont.)

• Ginger’s successor-in-interest sells her partnership interest for $500,000

– No gain or loss

– $500,000 proceeds less $500,000 basis stepped-up to FMV as of D/D

BNY MELLON WEALTH MANAGEMENT

Death of a Partner – Basis (cont.)

• Partnership sells the apartment building for $1,000,000

– Partnership’s gain is $900,000 ($1,000,000 proceeds less p/ship $100,000 basis in the bldg)

– Ginger’s successor-in-interest distributive share of the gain on the sale is $450,000 ($900,000 gain divided between the two partners)

– Note that if Ginger had owned her one-half interest in the property outright rather than in partnership, her estate would have a basis in the apartment building of $500,000 and would not have had to recognize a gain on the sale

19

BNY MELLON WEALTH MANAGEMENT

Death of a Partner – Basis (cont.)

• Note the problem

– Sale of partnership interest – no gain to Ginger’s successor-in-interest

– Sale of underlying asset of partnership (apartment building) -$450,000 gain to Ginger’s successor-in-interest

• The amount of gain is determined by whether the partnership interest is sold or the partnership’s underlying asset is sold

• Inequitable result depending on the structure of the transaction

BNY MELLON WEALTH MANAGEMENT

Death of a Partner – Basis (cont.)

• §754 election allows p/ship to elect to adjust the basis of the underlying asset of the p/ship to eliminate the disparity

• Election may be made on the death of a partner

• Election is made by the partnership

• Must be made by due date for p/ship return for the year in which the partner dies

• Requires separate accounting for deceased partner and all other partners

20

BNY MELLON WEALTH MANAGEMENT

Death of a Partner – Basis (cont.)

• Election is made• Sale of underlying partnership asset• Proceeds $1,000,000 less $50,000 surviving partner’s basis less

$500,000 deceased partner’s basis as a result of the §754 election equals $450,000 gain– Surviving partner reports entire $450,000 gain– Deceased partner’s successor in interest reports no gain

• Result: same tax treatment regardless of whether p/ship interest or p/ship’s underlying assets sold

BNY MELLON WEALTH MANAGEMENT

Death of a Partner – Basis (cont.)

• Alternative option if p/ship won’t make §754 election

• §732(d) – any property distributed from the p/ship to the estate within 2 years of the partner’s death gets a basis equal to the FET value

21

BNY MELLON WEALTH MANAGEMENT

S Corporation Distributions to Trust or Estate – TAI v. DNI

• An entity is any form of conducting business except sole proprietorships e.g. corporation, partnership, LLC, RIC, REIT, CTF

• Cash receipts from entities are income unless they are deemed in liquidation. 1997 UPIA §401– If an entity (1) indicates the distribution is in partial liquidation or (2)

distributes more than 20% of its gross assets (as of the year end), the distribution is deemed to be in liquidation

– If deemed to be in liquidation, the receipt is considered principal

– Cash received in partial liquidation is not taken into account as a distribution in partial liquidation to the extent it does not exceed the amount of income tax the trustee must pay on taxable income of the entity that distributes the money

– Distributions between 10% and 20% of gross assets• Use §104 power to adjust to credit to principal e.g. sale of business

assets or proceeds of a loan

BNY MELLON WEALTH MANAGEMENT

S Corporation Distributions to Trust or Estate – TAI v. DNI

• S corporation has gross assets of $500,000

• Distributes $95,000 in property to trust– Allocated to principal because it was distributed in property

• Instead distributes $95,000 in cash to trust– Allocated to income because it is less than 20% of total assets

• Instead distributes $115,000 of cash to trust– Allocated to principal because it is greater than 20% of total assets

22

BNY MELLON WEALTH MANAGEMENT

S Corporation Distributions to Trust or Estate – TAI v. DNI

• Note: how the income is reported on the Schedule K-1 does not control how the items is allocated for TAI purposes.

BNY MELLON WEALTH MANAGEMENT

S Corporation Distributions to Trust or Estate – TAI v. DNI

• Complications occur where shareholder’s share of cash is less than the shareholder’s distributive share of the S corporation’s taxable income

• UPIA §401 – cash receipts from entity constitute TAI• Estate or trust may not have received enough in cash distributions to

carryout all of the DNI attributable to the S corporation’s taxable income

• Schedule K-1 reports taxable income– K-1 amount used in calculating estate or trust’s DNI

23

BNY MELLON WEALTH MANAGEMENT

S Corporation Distributions to Trust or Estate – TAI v. DNI

• Example: S corporation, which is owned 100% by a simple trust, has $100,000 of taxable income but only distributes $40,000 in cash to the trust. The S corporation stock is the only asset of the trust.

• $40,000 of cash distributions constitutes the trust accounting income (TAI) of the trust per UPIA §401.

• The trust TAI of $40,000 is distributed to and taxed to the beneficiary.• The $100,000 of taxable income from the S corporation flows thru to

the trust and is added to the DNI of the trust.– The trust takes a distribution deduction of $40,000 for the TAI

distributed to the beneficiary.– The remaining $60,000 of DNI is accumulated and taxed at the

trust level.

BNY MELLON WEALTH MANAGEMENT

S Corporation

Trust

Beneficiary

TAI DNI

$100,000

$40,000

$40,000

$40,000 Cash

distribution

$100,000

$100,000

$40,000

$40,000 Cash

distribution

DNI

DNI

$60,000 Trapped

24

BNY MELLON WEALTH MANAGEMENT

S Corporation – Who Pays the Tax?

• Generally, the estate or trust pays tax on the S corporation taxable income and is able to claim a deduction for distributions to the beneficiaries.

• In the case of a QSST, the beneficiary pays the tax on the trust’s share of S corporation income.

– The beneficiary may owe the tax even though the S corporation doesn’t distribute any income to the QSST.

– UPIA §506 allows a fiduciary to make adjustments between income and principal to rectify this problem.

• In the case of an ESBT, the ESBT pays the tax and may not pass any of the taxable income to the beneficiary.

BNY MELLON WEALTH MANAGEMENT

S Corporation – Passive Activity Loss

• Four PAL issues with trusts and estates:

– PALs deducted by trust or estate on complete taxable disposition of S corporation stock. §469(g)(1).

– On death of an S corporation shareholder – PAL deducted on decedent’s final 1040 to extent PAL exceeds the basis step-up. §469(g)(2).

• Death of S/H is not a complete disposition in a taxable transaction because death itself is not a taxable transaction.

– On distribution of PAL property to a beneficiary – unused PAL added to beneficiary’s basis of the activity. §469(j)(12).

– On gift of PAL activity – PAL added to donee’s basis. §469(j)(6).

25

BNY MELLON WEALTH MANAGEMENT

Taxation of Distributions – No E & P

• Distributions of cash from S corporation generally tax-free to the extent they don’t exceed the S/H’s adjusted stock basis

• The distribution reduces the S/H’s basis in his stock.

• Distribution in excess of basis result in a taxable gain on the sale of an asset.

• Stock basis is determined as of the end of the corporation’s tax year.

BNY MELLON WEALTH MANAGEMENT

Taxation of Distributions – No E & P

• Distributions of appreciated property from S corporation is a deemed sale of the assets at its FMV.

• The S corporation recognizes gain as if it had sold the assets and the gain passes through to the shareholders

• A “built-in gain tax” may also apply it the corporation was formerly a C corporation and made its S election less than 10 years ago with the appreciated property.

– The “built-in gains tax” can be avoided by waiting 10 years from the date of the S election to dispose of appreciated property owned at the time of the S election.

26

BNY MELLON WEALTH MANAGEMENT

Taxation of Distributions – No E & P

• Example: Estate owns 100% of S corporation.

• Estate’s basis in the stock is $100,000

• S corporation has no E & P

• Distributes building worth $100,000 with $30,000 basis to the estate.

• Corporation recognizes a $70,000 gain which passes through to the estate.

• The $70,000 gain increases the estate’s stock basis to $170,000 ($100,000 + $70,000)

• The $100,000 distribution is tax-free because it does not exceed the estate’s stock basis.

BNY MELLON WEALTH MANAGEMENT

Taxation of Distributions – E & P

• The order of distributions:

– The accumulated adjustment account (AAA) comes out first. It is a tax-free distribution to the extent of the S/H’s basis in the S stock

– Any excess AAA over the S/H’s basis is tax as capital gain.

– Distributions in excess of the AAA are taxed as a dividend to the extent of the corporation’s E & P.

– Distributions in excess of the AAA and E & P are tax-free to the extent of any remaining stock basis.

– Any remaining distributions are capital gain

27

BNY MELLON WEALTH MANAGEMENT

Taxation of Distributions – E & P

• Example:

– Estate owns 100% of stock of a S corporation

– Estate’s basis in the stock is $100,000

– The corporation has AAA of $50,000 and E & P of $25,000

– The S corporation redeems the estate for $200,000

– The distribution is characterized as follows:• Tax-free AAA limited to basis: $50,000

• Dividend $25,000

• Tax-free recovery of remaining basis $50,000

• Capital gain $75,000

BNY MELLON WEALTH MANAGEMENT

Funding Issues

• Four issues when transferring S stock to a beneficiary:

– How to allocate the S corporation income between the estate or other transferor and the beneficiary or other transferee

– Is gain or loss recognized on the funding?

– Is there recognition of IRD?

– Is the beneficiary (transferee) an eligible S corporation S/H?

28

BNY MELLON WEALTH MANAGEMENT

Funding Issues – Allocating Income

• How to allocate the S corporation income between the estate or other transferor and the beneficiary or other transferee:

– Default method: S/H report on a per-share, per-day basis i.e. income is allocated 1/365th per day x the S/H percentage ownership x the number of days of ownership of the S corporation stock

– Alternative method: if a S/H terminates his interest in the corporation and all the affected S/H agree, the S corporation can allocate the income before and after the transfer as if the S corporation had two separate tax years – one tax year before the transfer and one tax year after the transfer

– The estate (transferor) reports it share of S corporation income up to the date of transfer and the beneficiary reports its share of income after the transfer

BNY MELLON WEALTH MANAGEMENT

Funding Issues – Allocating Income

• How to allocate the S corporation income between the estate or other transferor and the beneficiary or other transferee:

– Specific bequests – treated as a transfer directly from the decedent to the beneficiary.

• The decedent reports the income up to the date of death and the legatee reports the income after death

29

BNY MELLON WEALTH MANAGEMENT

Funding Issues – Gain or Loss on Funding

• Funding a pecuniary bequest with appreciated S corporation stock will cause the estate (transferor) to recognize gain in the amount of the FMV of the S corporation stock over its basis.

• Transfers of appreciated S corporation stock to fund a specific bequest or a residuary bequest will not result in the recognition of gain or loss.

BNY MELLON WEALTH MANAGEMENT

Agenda

• Introduction

• S corporation taxation

• Reporting Income on the death of a shareholder

• Eligible shareholder

• Basis adjustment at death

• Estate as shareholder

• Election of estate FYE

• Trusts as eligible shareholder

– Grantor trust

– Testamentary trust

– Voting trust

– QSST

– ESBT

• S corporation distributions to trust or estate – TAI v. DNI

30

BNY MELLON WEALTH MANAGEMENT

Agenda (cont.)

• S corporation – who pays the tax?

• S corporations and PALs

• S corporations – taxation of distributions

• Funding issues

BNY MELLON WEALTH MANAGEMENT

Thank You!

31

BNY MELLON WEALTH MANAGEMENT

Park the car in Harvard yard.