Equity part1

42

EQUITY EQUITY Part 1 Part 1 Financial Accounting and Reporting 1 - Pearson

-

Upload

kim-rae-ki -

Category

Education

-

view

85 -

download

0

Transcript of Equity part1

EQUITY EQUITY Part 1Part 1

Financial Accounting and Reporting 1 - Pearson

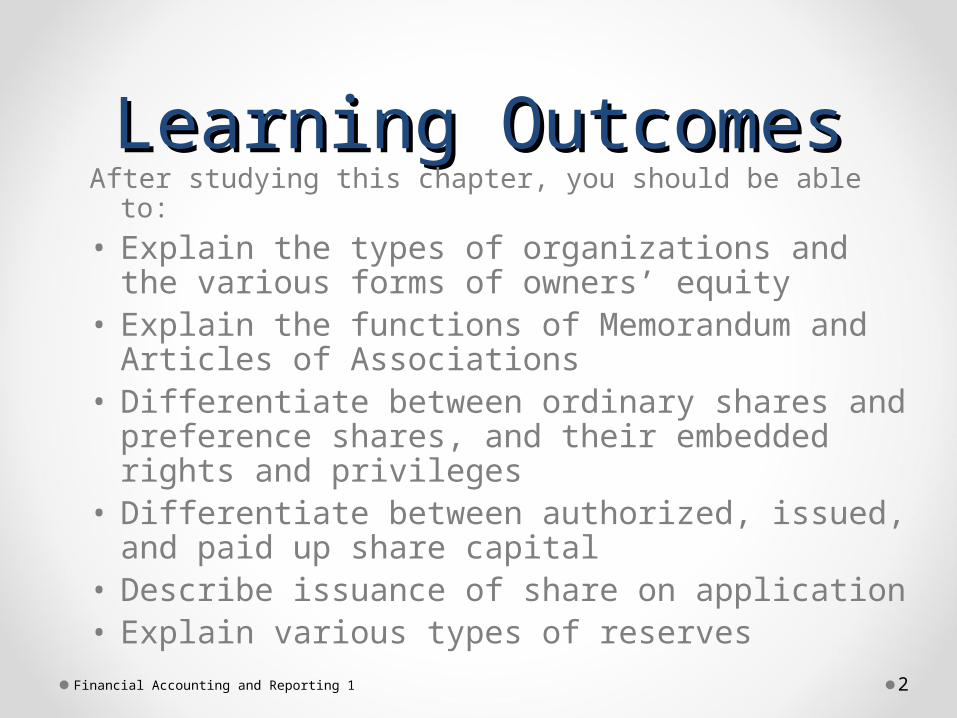

Learning OutcomesLearning OutcomesAfter studying this chapter, you should be able to:

• Explain the types of organizations and the various forms of owners’ equity

• Explain the functions of Memorandum and Articles of Associations

• Differentiate between ordinary shares and preference shares, and their embedded rights and privileges

• Differentiate between authorized, issued, and paid up share capital

• Describe issuance of share on application• Explain various types of reserves Financial Accounting and Reporting 1 2

Owners’ EquityOwners’ Equity

Investment made by owners in a business or organization

Investment made by owners in a business or organization

Financial Accounting and Reporting 1 3

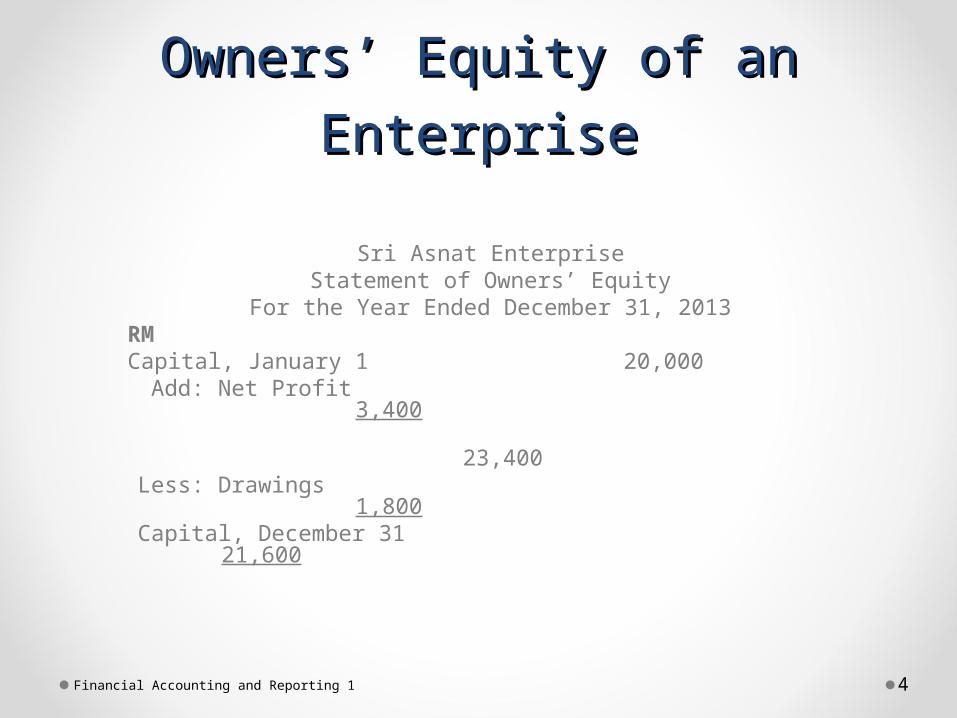

Owners’ Equity of an Owners’ Equity of an

EnterpriseEnterprise

Sri Asnat EnterpriseStatement of Owners’ Equity

For the Year Ended December 31, 2013RM

Capital, January 1 20,000 Add: Net Profit 3,400

23,400 Less: Drawings

1,800 Capital, December 31 21,600

Financial Accounting and Reporting 1 4

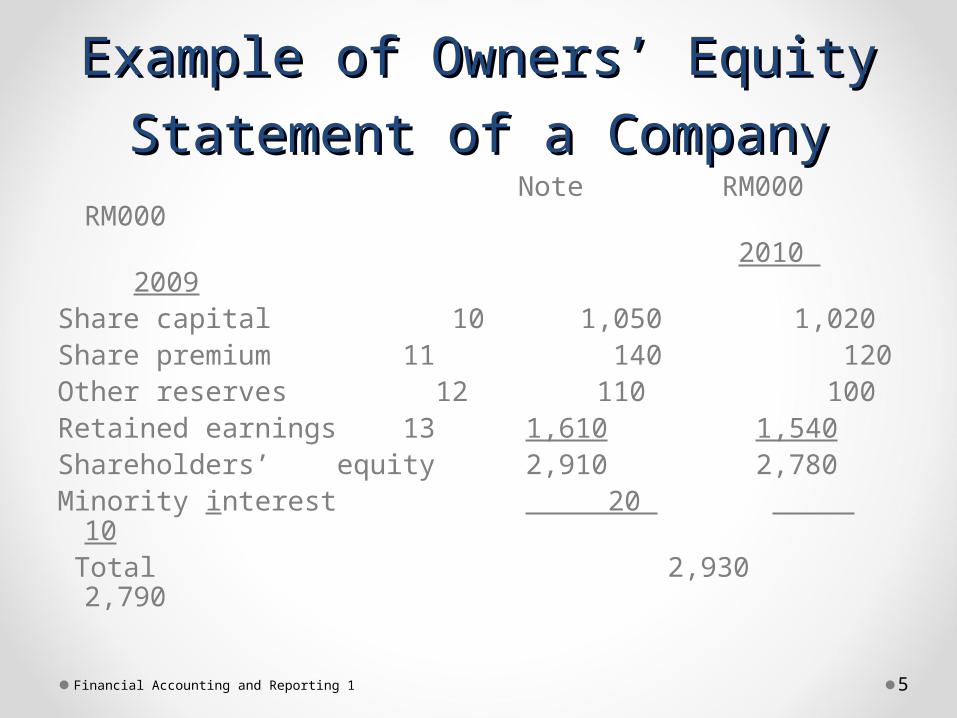

Example of Owners’ Equity Example of Owners’ Equity

Statement of a CompanyStatement of a Company Note RM000 RM000 2010

2009Share capital 10 1,050 1,020Share premium 11 140 120Other reserves 12 110 100Retained earnings 13 1,610 1,540Shareholders’ equity 2,910 2,780Minority interest 20 10 Total 2,930

2,790Financial Accounting and Reporting 1 5

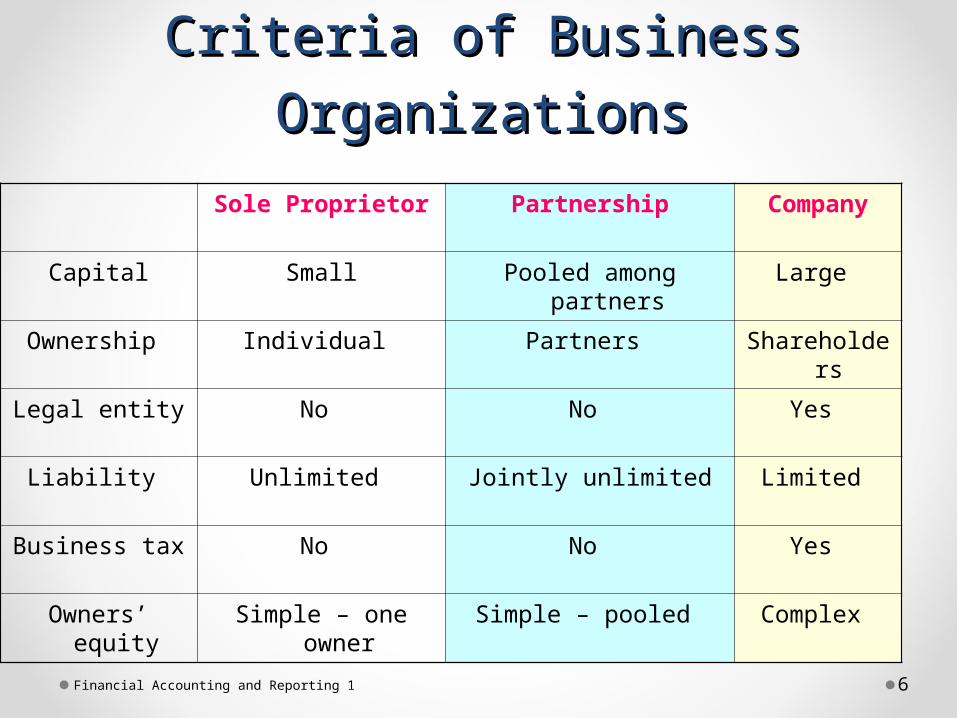

Criteria of Business Criteria of Business

OrganizationsOrganizations

Sole Proprietor Partnership Company

Capital Small Pooled among partners

Large

Ownership Individual Partners Shareholders

Legal entity No No Yes

Liability Unlimited Jointly unlimited Limited

Business tax No No Yes

Owners’ equity

Simple – one owner

Simple – pooled Complex

Financial Accounting and Reporting 1 6

Financial Accounting and Reporting 1 7

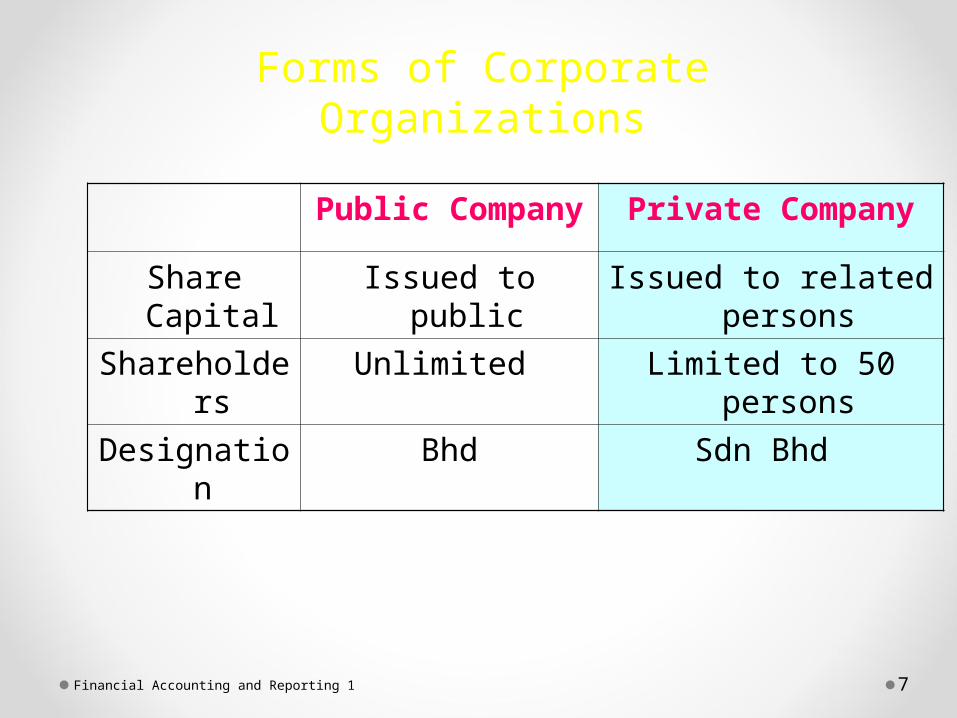

Forms of Corporate OrganizationsForms of Corporate Organizations

Public Company Private Company

Share Capital Issued to public Issued to related persons

Shareholders Unlimited Limited to 50 persons

Designation Bhd Sdn Bhd

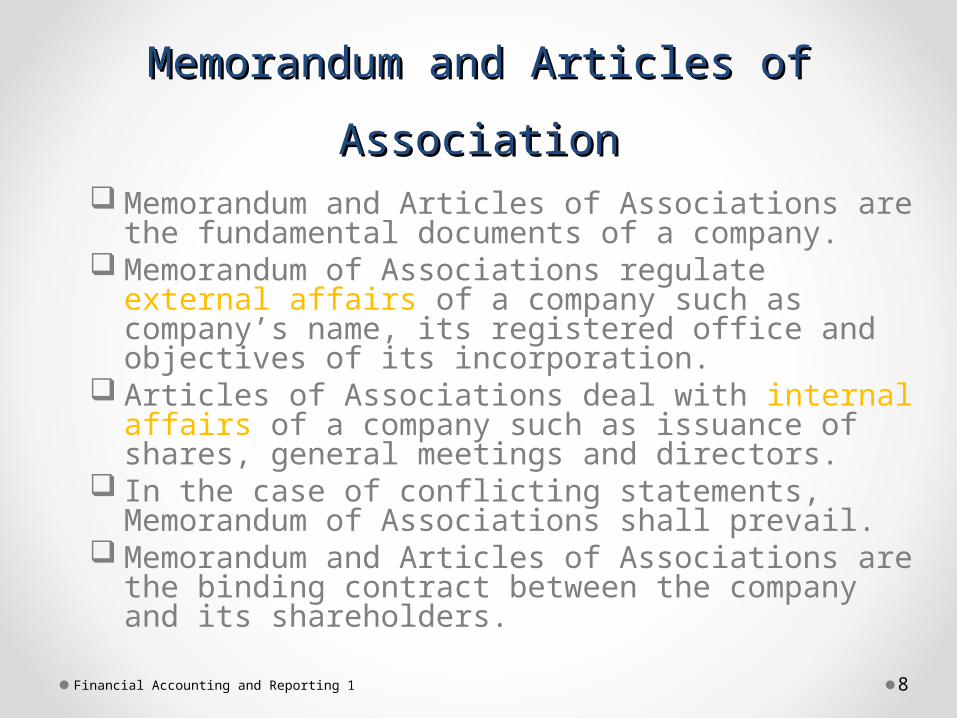

Memorandum and Articles of Memorandum and Articles of

AssociationAssociation Memorandum and Articles of Associations are

the fundamental documents of a company. Memorandum of Associations regulate external

affairs of a company such as company’s name, its registered office and objectives of its incorporation.

Articles of Associations deal with internal affairs of a company such as issuance of shares, general meetings and directors.

In the case of conflicting statements, Memorandum of Associations shall prevail.

Memorandum and Articles of Associations are the binding contract between the company and its shareholders.

Financial Accounting and Reporting 1 8

Share Capital Share Capital StructureStructure

Generated from the amount of authorized share capital that being issued and paid, valued at nominal price. Two main forms of share capital:o Ordinary shares o Preference shares

Financial Accounting and Reporting 1 9

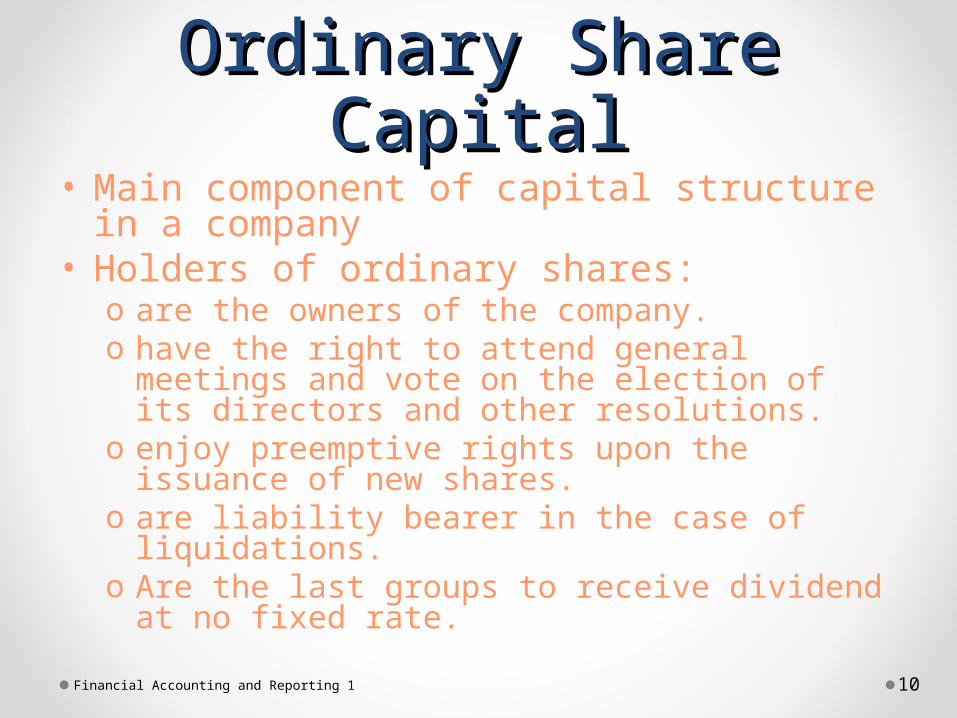

Ordinary Share Ordinary Share CapitalCapital

• Main component of capital structure in a company

• Holders of ordinary shares:o are the owners of the company.o have the right to attend general meetings and

vote on the election of its directors and other resolutions.

o enjoy preemptive rights upon the issuance of new shares.

o are liability bearer in the case of liquidations.o Are the last groups to receive dividend at no

fixed rate.

Financial Accounting and Reporting 1 10

Financial Accounting and Reporting 1 11

Preference Share CapitalPreference Share Capital

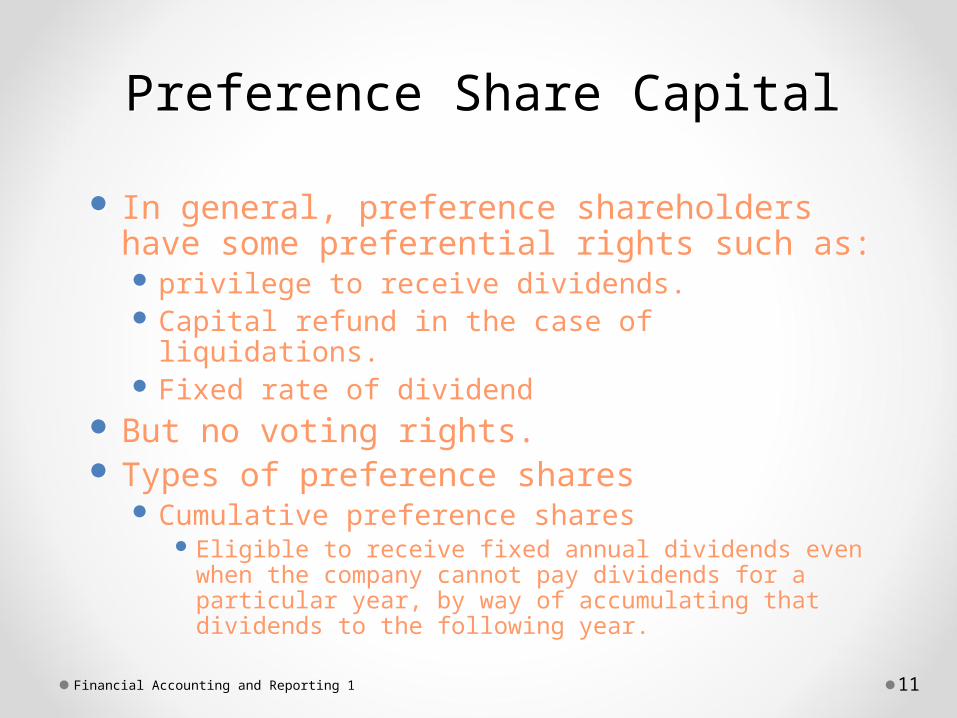

In general, preference shareholders have some preferential rights such as: privilege to receive dividends. Capital refund in the case of liquidations. Fixed rate of dividend

But no voting rights. Types of preference shares

Cumulative preference shares Eligible to receive fixed annual dividends even

when the company cannot pay dividends for a particular year, by way of accumulating that dividends to the following year.

In general, preference shareholders have some preferential rights such as: privilege to receive dividends. Capital refund in the case of liquidations. Fixed rate of dividend

But no voting rights. Types of preference shares

Cumulative preference shares Eligible to receive fixed annual dividends even

when the company cannot pay dividends for a particular year, by way of accumulating that dividends to the following year.

Preference Share CapitalPreference Share Capital

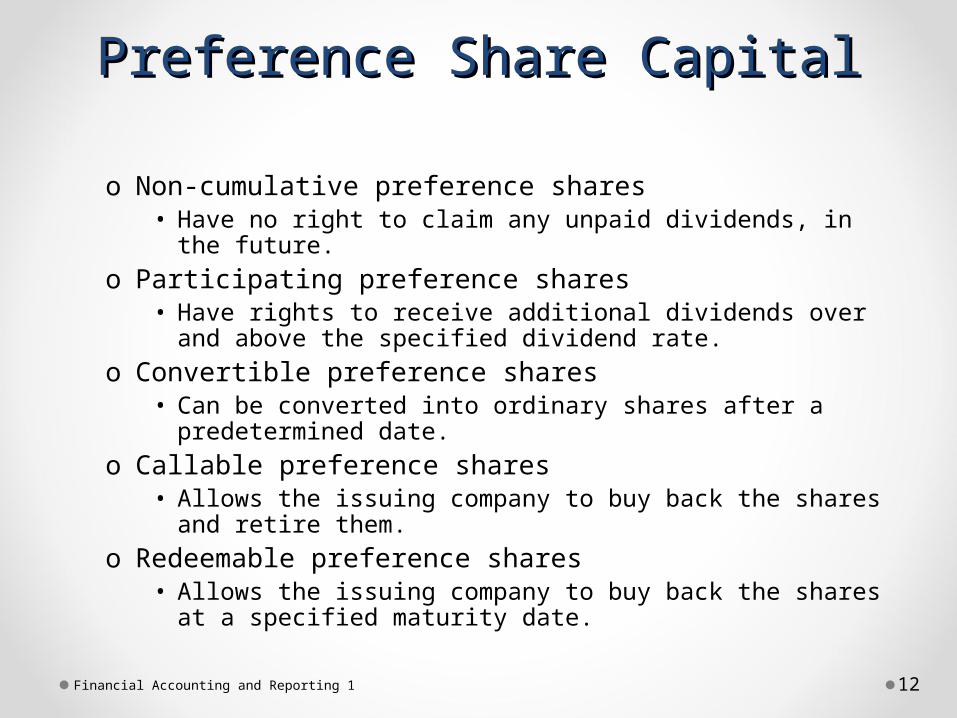

o Non-cumulative preference shares• Have no right to claim any unpaid dividends, in the future.

o Participating preference shares• Have rights to receive additional dividends over and above

the specified dividend rate. o Convertible preference shares

• Can be converted into ordinary shares after a predetermined date.

o Callable preference shares• Allows the issuing company to buy back the shares and

retire them.o Redeemable preference shares

• Allows the issuing company to buy back the shares at a specified maturity date.

Financial Accounting and Reporting 1 12

Authorized Share Authorized Share CapitalCapital

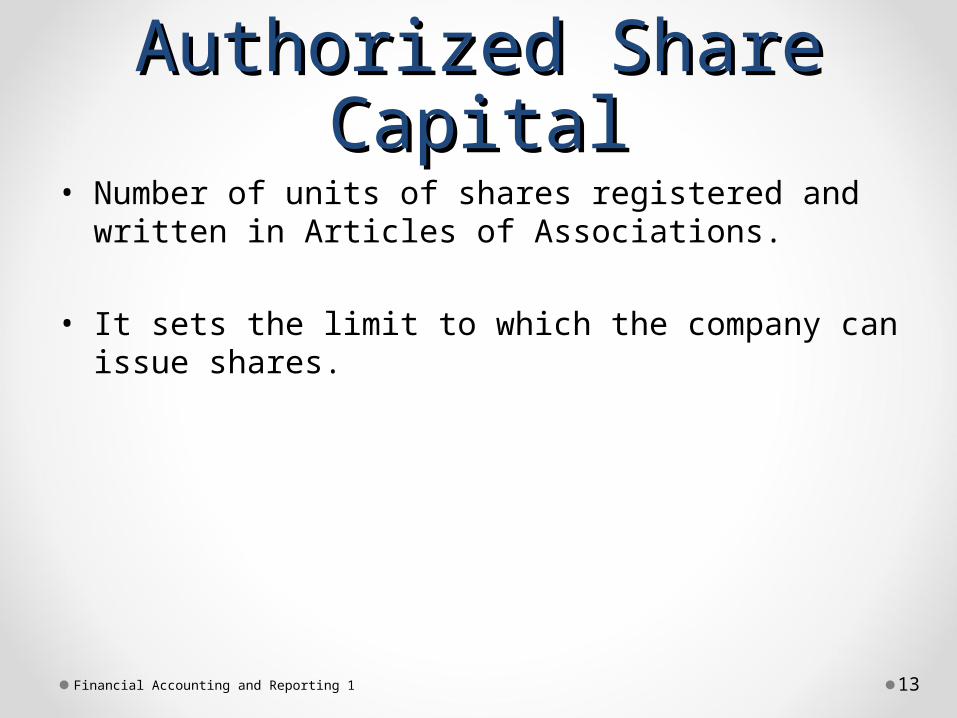

• Number of units of shares registered and written in Articles of Associations.

• It sets the limit to which the company can issue shares.

Financial Accounting and Reporting 1 13

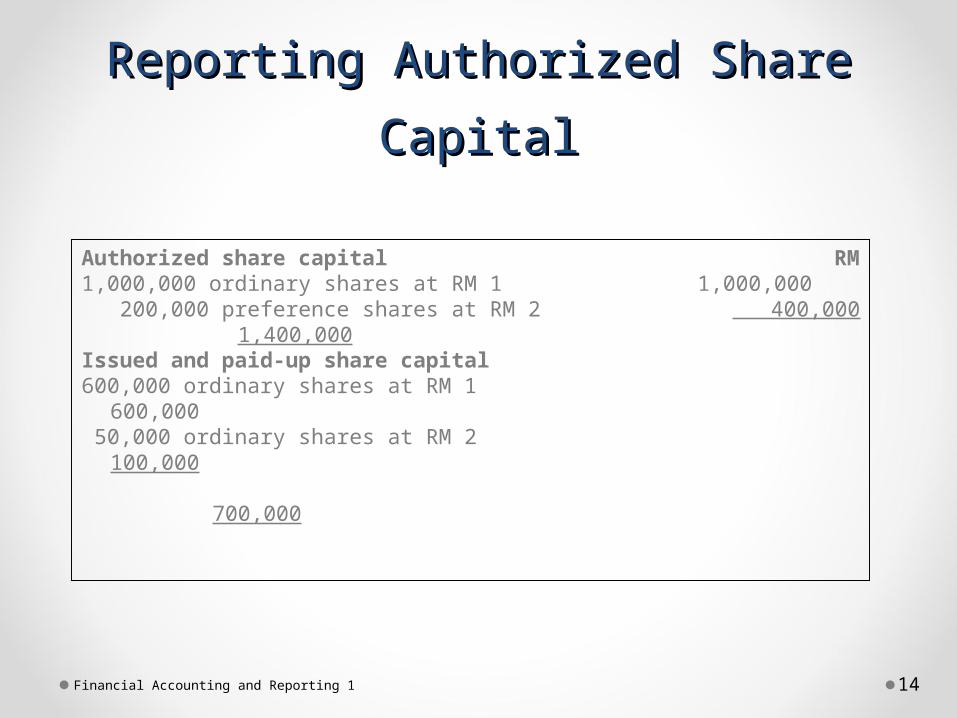

Reporting Authorized Share Reporting Authorized Share

CapitalCapital

Authorized share capital RM1,000,000 ordinary shares at RM 1 1,000,000 200,000 preference shares at RM 2 400,000

1,400,000Issued and paid-up share capital600,000 ordinary shares at RM 1 600,000 50,000 ordinary shares at RM 2 100,000 700,000

Financial Accounting and Reporting 1 14

Financial Accounting and Reporting 1 15

Issued Share CapitalIssued Share Capital

Company invites the public to buy shares.

Anybody who is interested to buy the shares will express his interest by applying to the company with full payment for the shares.

Shares will be allotted to successful applicants, while unsuccessful applicants will be refunded.

The total shares allotted are known as issued share capital.

Company invites the public to buy shares.

Anybody who is interested to buy the shares will express his interest by applying to the company with full payment for the shares.

Shares will be allotted to successful applicants, while unsuccessful applicants will be refunded.

The total shares allotted are known as issued share capital.

ExampleExample Assume Medaniaga Bhd issues 40,00 shares

at RM 1 each during the year ended 31 December 2008. The applications are received with full payment on October 31, 2008 for 100,000 shares. The shares are subsequently allotted on December 31, 2008 to the successful applicants, while unsuccessful applicants are refunded at the same date. The entries to record the transactions are as follows:

Financial Accounting and Reporting 1 16

Journal EntriesJournal Entries

Financial Accounting and Reporting 1 17

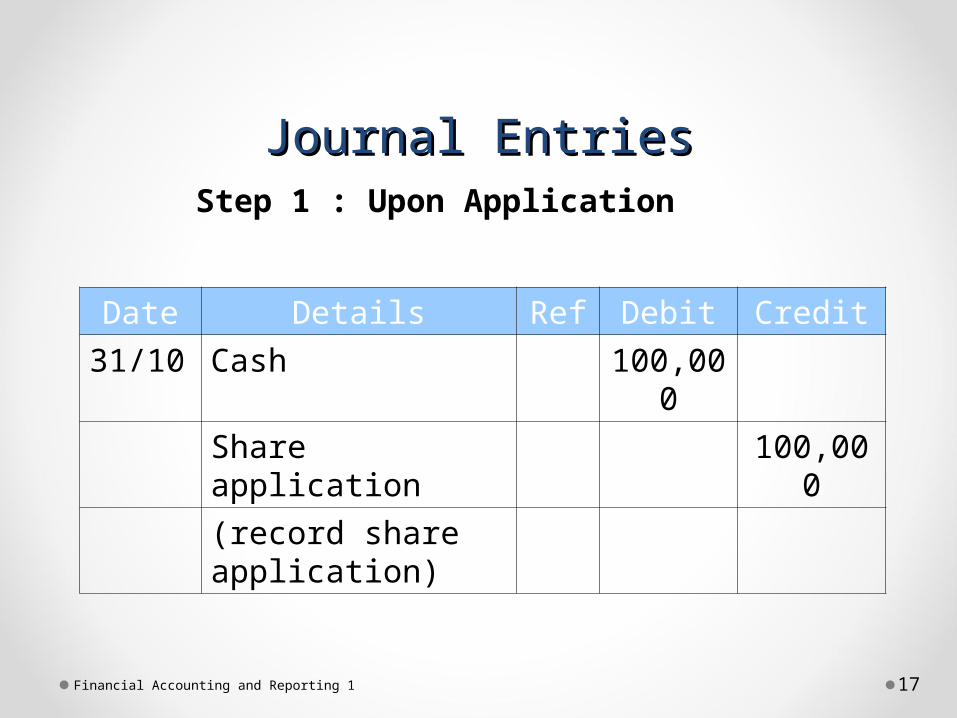

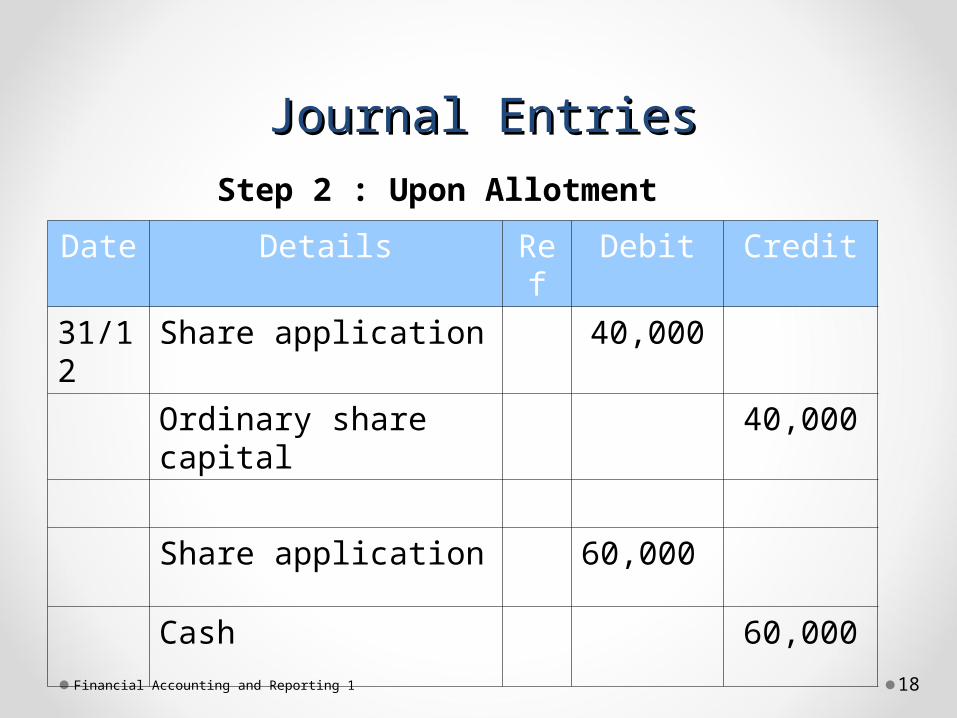

Step 1 : Upon Application

Date Details Ref Debit Credit

31/10 Cash 100,000

Share application 100,000

(record share application)

Journal EntriesJournal Entries

Date Details Ref Debit Credit

31/12 Share application 40,000

Ordinary share capital 40,000

Share application 60,000

Cash 60,000

Financial Accounting and Reporting 1 18

Step 2 : Upon Allotment

Financial Accounting and Reporting 1 19

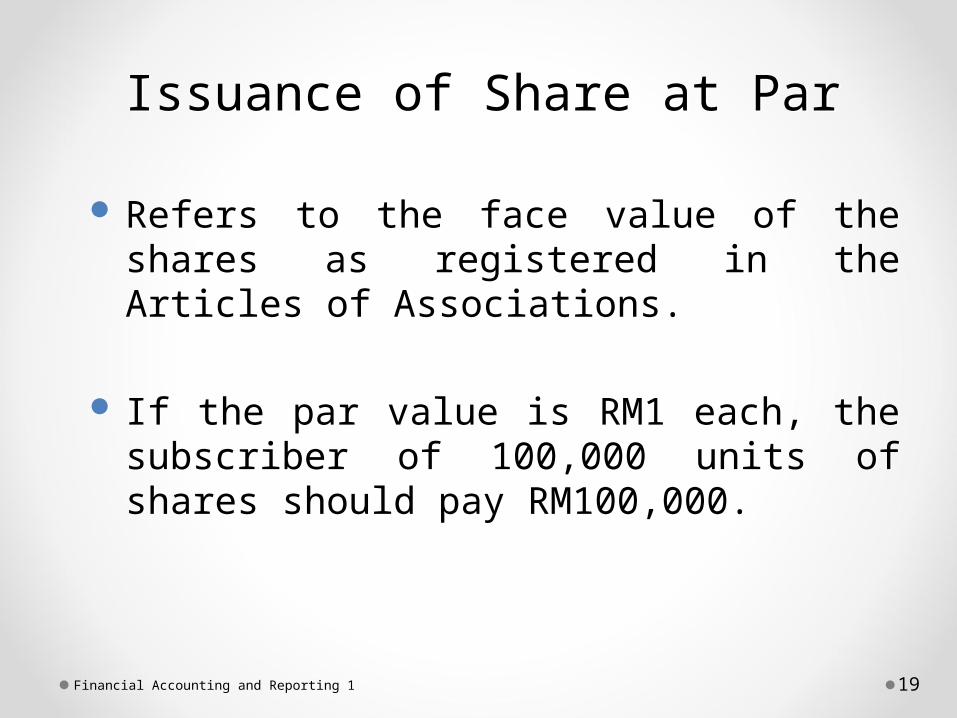

Issuance of Share at ParIssuance of Share at Par

Refers to the face value of the shares as registered in the Articles of Associations.

If the par value is RM1 each, the subscriber of 100,000 units of shares should pay RM100,000.

Refers to the face value of the shares as registered in the Articles of Associations.

If the par value is RM1 each, the subscriber of 100,000 units of shares should pay RM100,000.

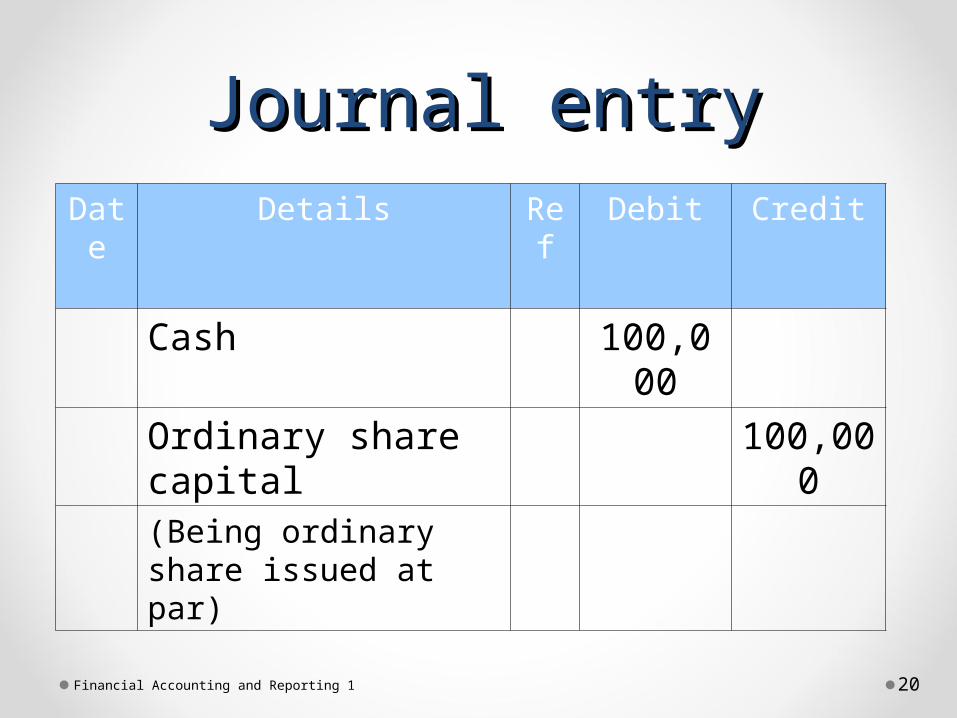

Journal entryJournal entryDate Details Ref Debit Credit

Cash 100,000

Ordinary share capital 100,000(Being ordinary share issued at par)

Financial Accounting and Reporting 1 20

Financial Accounting and Reporting 1 21

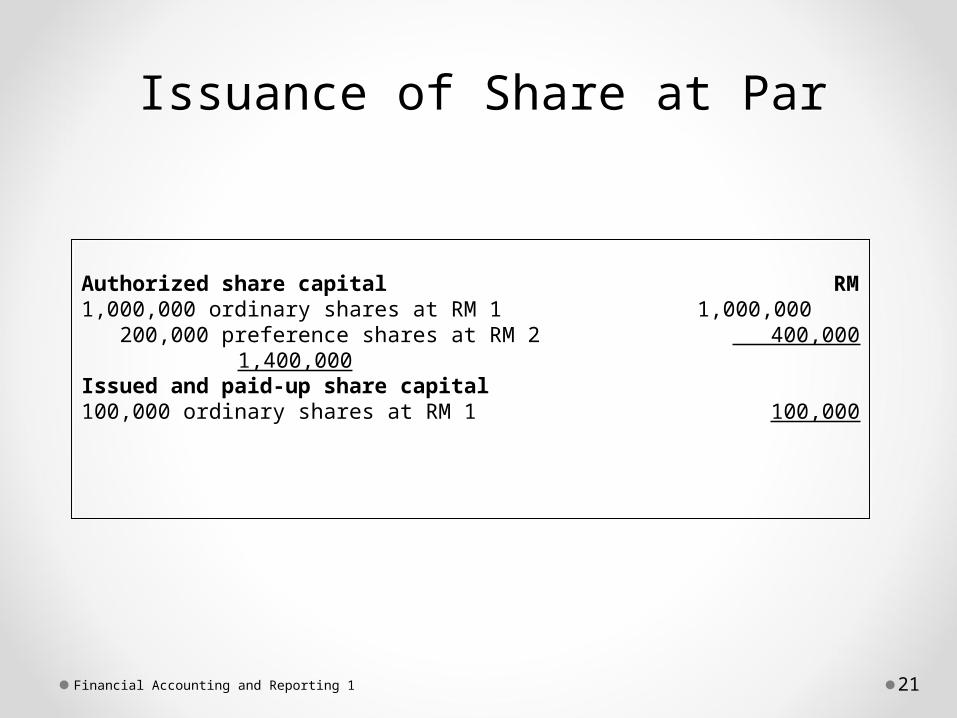

Issuance of Share at ParIssuance of Share at Par

Authorized share capital RM1,000,000 ordinary shares at RM 1 1,000,000 200,000 preference shares at RM 2 400,000

1,400,000Issued and paid-up share capital100,000 ordinary shares at RM 1 100,000

Authorized share capital RM1,000,000 ordinary shares at RM 1 1,000,000 200,000 preference shares at RM 2 400,000

1,400,000Issued and paid-up share capital100,000 ordinary shares at RM 1 100,000

Financial Accounting and Reporting 1 22

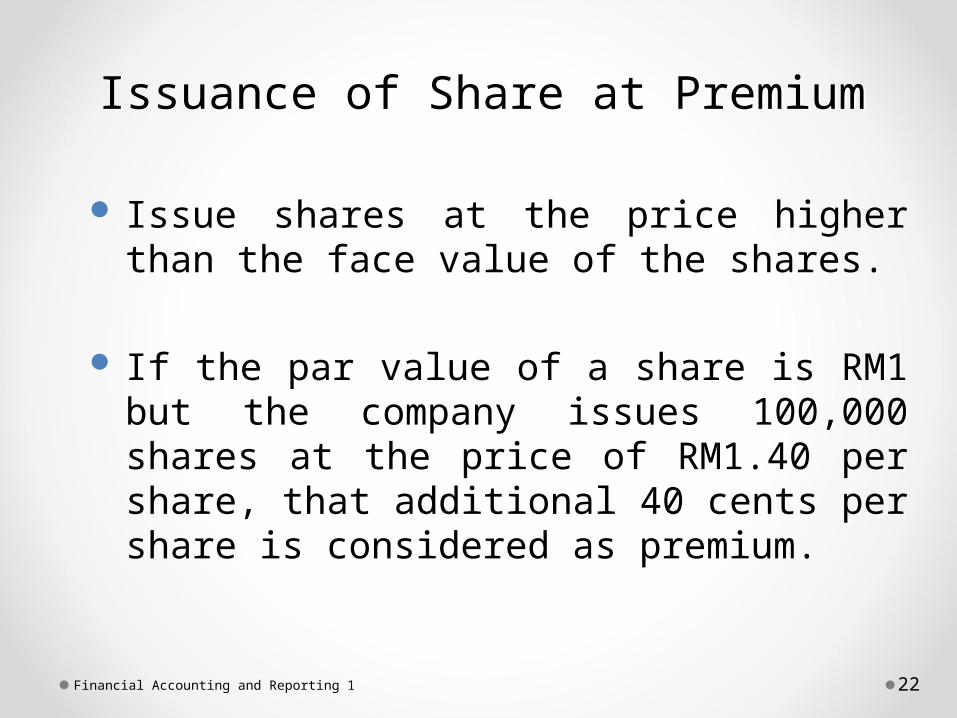

Issuance of Share at PremiumIssuance of Share at Premium

Issue shares at the price higher than the face value of the shares.

If the par value of a share is RM1 but the company issues 100,000 shares at the price of RM1.40 per share, that additional 40 cents per share is considered as premium.

Issue shares at the price higher than the face value of the shares.

If the par value of a share is RM1 but the company issues 100,000 shares at the price of RM1.40 per share, that additional 40 cents per share is considered as premium.

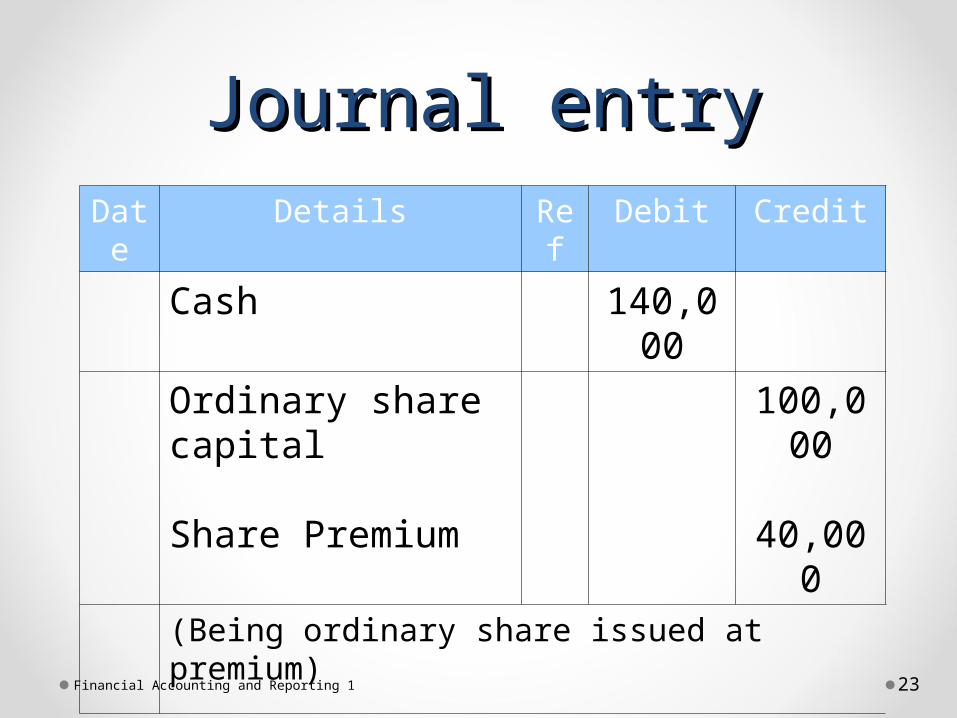

Journal entryJournal entryDate Details Ref Debit Credit

Cash 140,000

Ordinary share capital

Share Premium

100,000

40,000(Being ordinary share issued at premium)

Financial Accounting and Reporting 1 23

Financial Accounting and Reporting 1 24

Issuance of Share at PremiumIssuance of Share at Premium

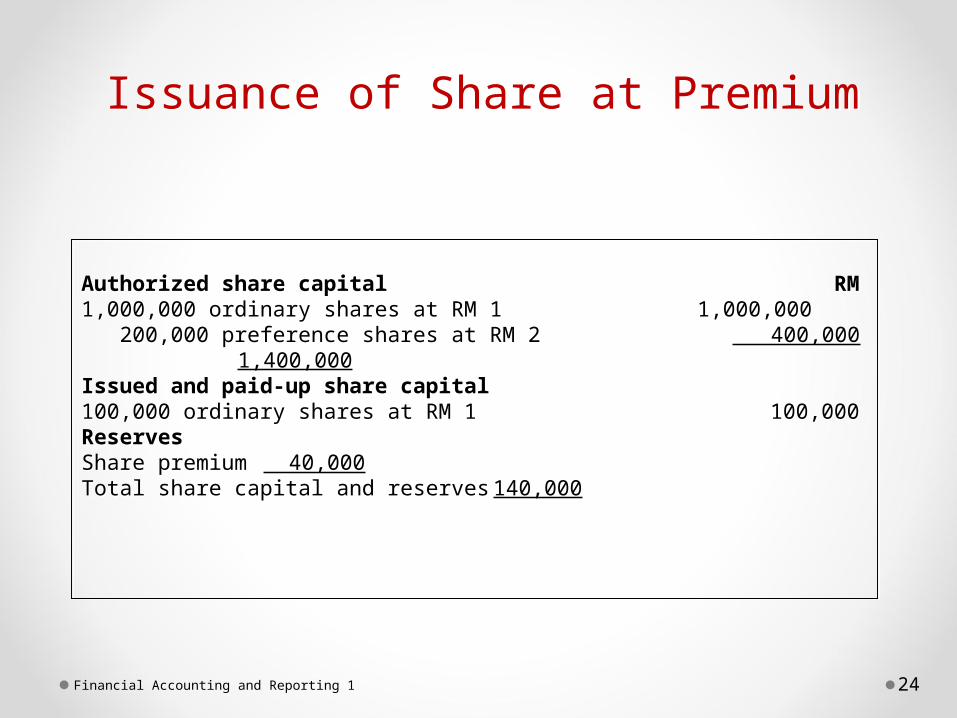

Authorized share capital RM1,000,000 ordinary shares at RM 1 1,000,000 200,000 preference shares at RM 2 400,000

1,400,000Issued and paid-up share capital100,000 ordinary shares at RM 1 100,000 ReservesShare premium 40,000Total share capital and reserves 140,000

Authorized share capital RM1,000,000 ordinary shares at RM 1 1,000,000 200,000 preference shares at RM 2 400,000

1,400,000Issued and paid-up share capital100,000 ordinary shares at RM 1 100,000 ReservesShare premium 40,000Total share capital and reserves 140,000

Financial Accounting and Reporting 1 25

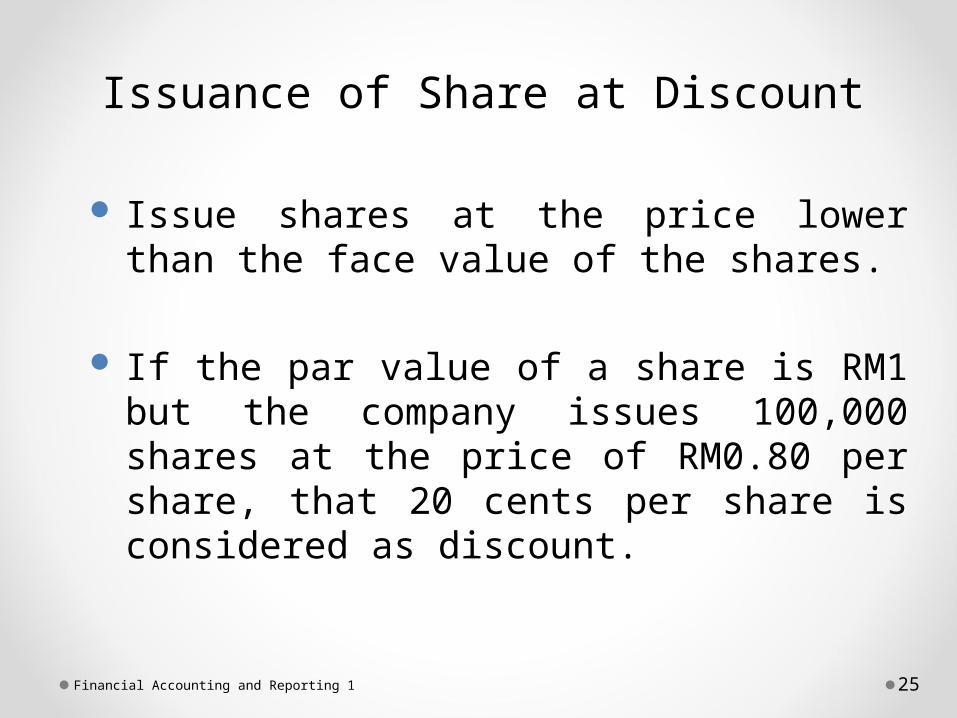

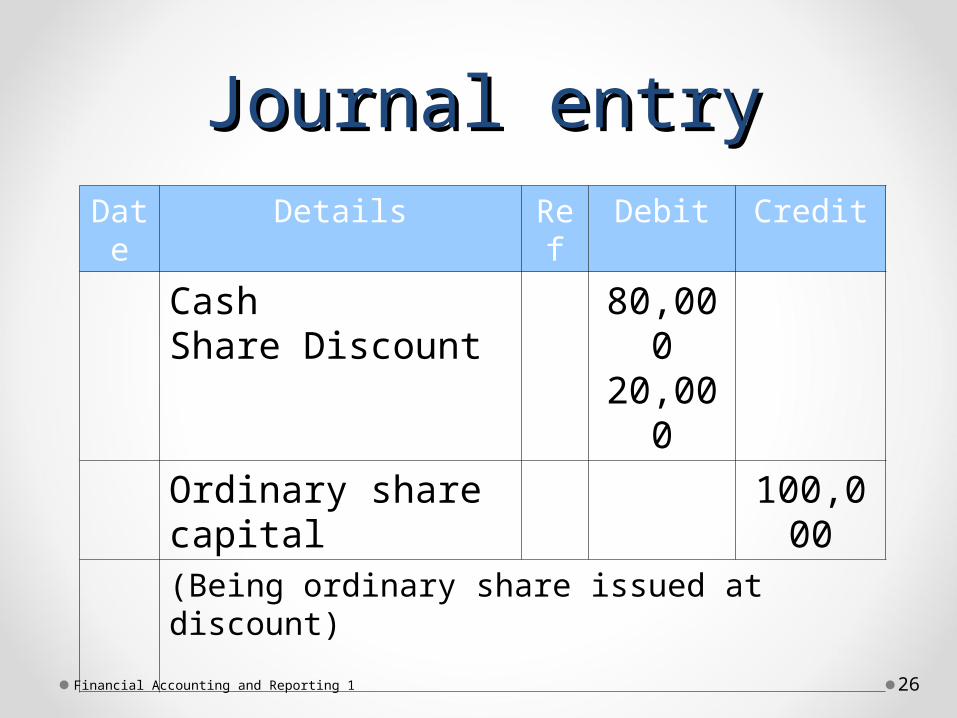

Issuance of Share at DiscountIssuance of Share at Discount

Issue shares at the price lower than the face value of the shares.

If the par value of a share is RM1 but the company issues 100,000 shares at the price of RM0.80 per share, that 20 cents per share is considered as discount.

Issue shares at the price lower than the face value of the shares.

If the par value of a share is RM1 but the company issues 100,000 shares at the price of RM0.80 per share, that 20 cents per share is considered as discount.

Journal entryJournal entryDate Details Ref Debit Credit

CashShare Discount

80,00020,000

Ordinary share capital 100,000

(Being ordinary share issued at discount)

Financial Accounting and Reporting 1 26

Financial Accounting and Reporting 1 27

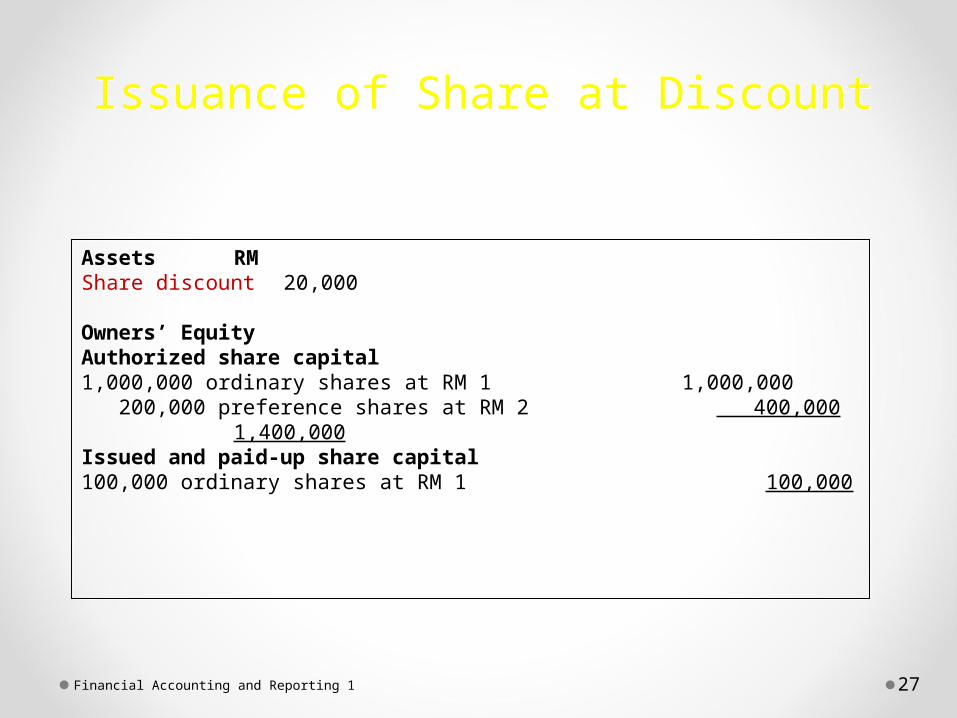

Issuance of Share at DiscountIssuance of Share at Discount

Assets RMShare discount 20,000

Owners’ EquityAuthorized share capital 1,000,000 ordinary shares at RM 1 1,000,000 200,000 preference shares at RM 2 400,000

1,400,000Issued and paid-up share capital100,000 ordinary shares at RM 1 100,000

Assets RMShare discount 20,000

Owners’ EquityAuthorized share capital 1,000,000 ordinary shares at RM 1 1,000,000 200,000 preference shares at RM 2 400,000

1,400,000Issued and paid-up share capital100,000 ordinary shares at RM 1 100,000

ReservesReserves

• Part of owners’ equity• Comprise of capital reserve and revenue

reserve.

Financial Accounting and Reporting 1 28

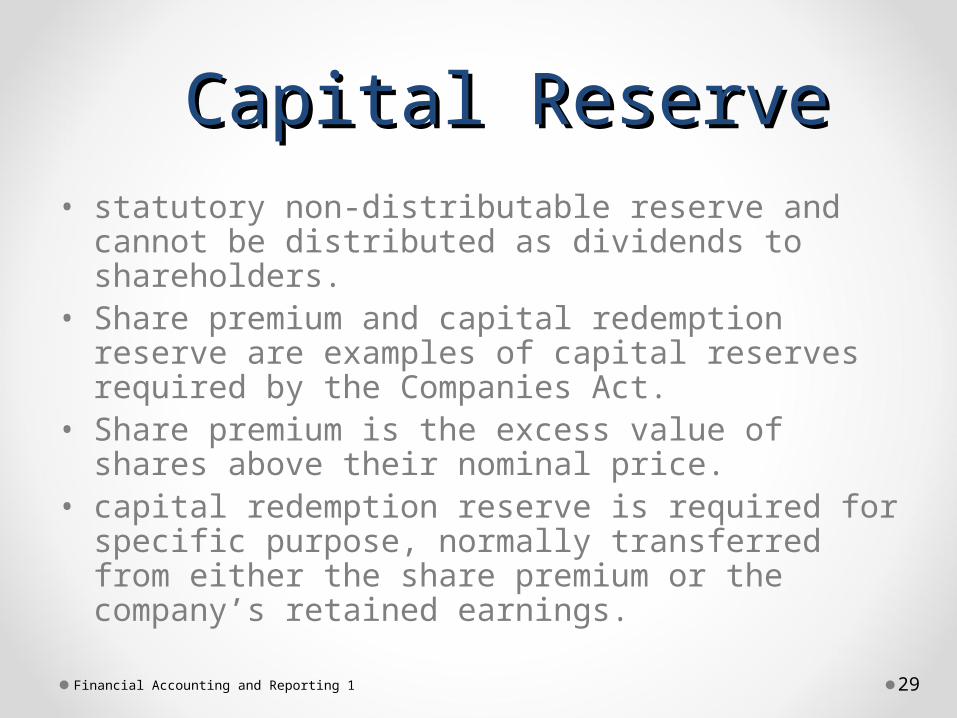

Capital ReserveCapital Reserve• statutory non-distributable reserve and cannot be

distributed as dividends to shareholders.• Share premium and capital redemption reserve

are examples of capital reserves required by the Companies Act.

• Share premium is the excess value of shares above their nominal price.

• capital redemption reserve is required for specific purpose, normally transferred from either the share premium or the company’s retained earnings.

Financial Accounting and Reporting 1 29

Financial Accounting and Reporting 1 30

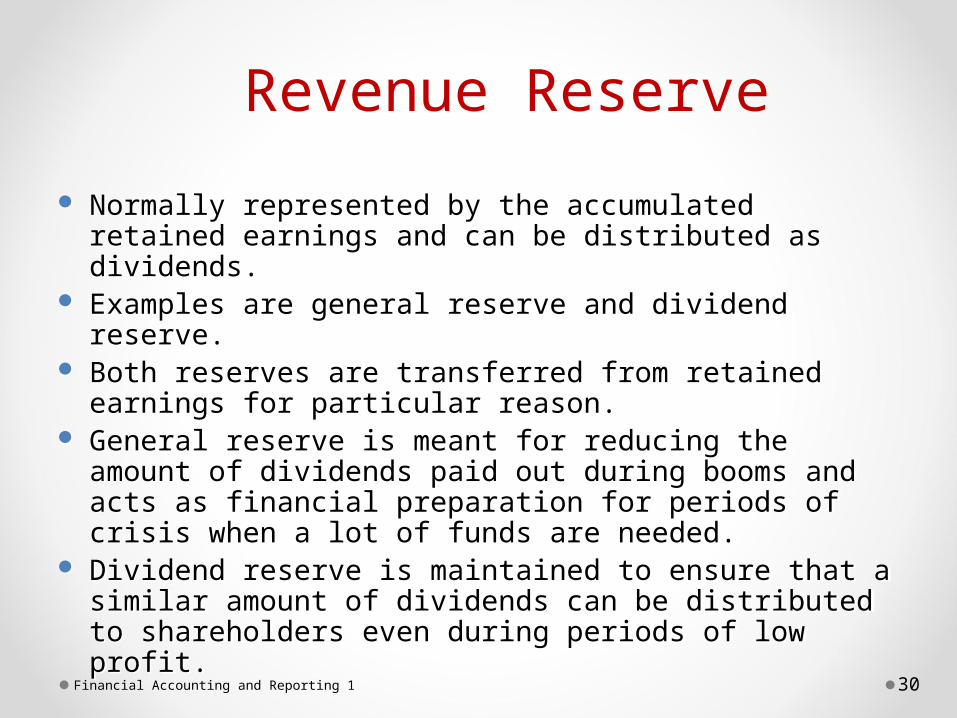

Revenue ReserveRevenue Reserve

Normally represented by the accumulated retained earnings and can be distributed as dividends.

Examples are general reserve and dividend reserve.

Both reserves are transferred from retained earnings for particular reason.

General reserve is meant for reducing the amount of dividends paid out during booms and acts as financial preparation for periods of crisis when a lot of funds are needed.

Dividend reserve is maintained to ensure that a similar amount of dividends can be distributed to shareholders even during periods of low profit.

Normally represented by the accumulated retained earnings and can be distributed as dividends.

Examples are general reserve and dividend reserve.

Both reserves are transferred from retained earnings for particular reason.

General reserve is meant for reducing the amount of dividends paid out during booms and acts as financial preparation for periods of crisis when a lot of funds are needed.

Dividend reserve is maintained to ensure that a similar amount of dividends can be distributed to shareholders even during periods of low profit.

Shares Issued with Other Securities

Two methods of allocating proceeds:

Proportional method.

Incremental method.

LO 3 Explain the accounting procedures for issuing shares.

EquityEquityEquityEquity

LO 3

EquityEquityEquityEquity

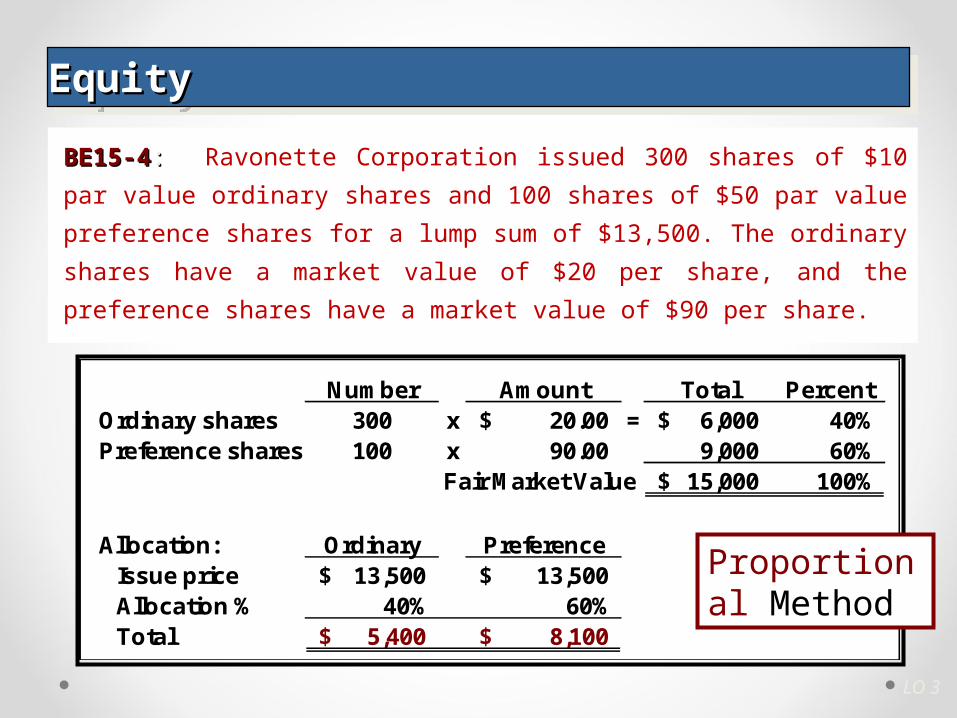

Number Amount Total PercentOrdinary shares 300 x 20.00$ = 6,000$ 40%Preference shares 100 x 90.00 9,000 60%

Fair Market Value 15,000$ 100%

Allocation: Ordinary PreferenceIssue price 13,500$ 13,500$ Allocation % 40% 60%Total 5,400$ 8,100$

Proportional Method

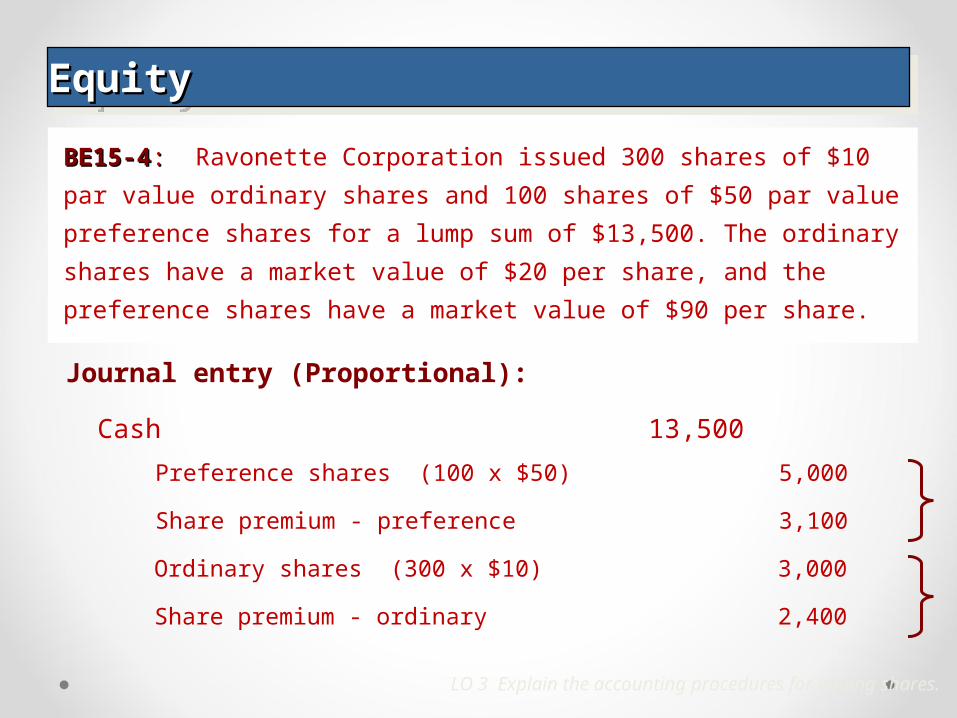

BE15-4BE15-4: : Ravonette Corporation issued 300 shares of $10 par value

ordinary shares and 100 shares of $50 par value preference shares for

a lump sum of $13,500. The ordinary shares have a market value of

$20 per share, and the preference shares have a market value of $90

per share.

LO 3 Explain the accounting procedures for issuing shares.

EquityEquityEquityEquity

Cash 13,500

Preference shares (100 x $50) 5,000

Journal entry (Proportional):

Share premium - preference 3,100

Ordinary shares (300 x $10) 3,000

Share premium - ordinary 2,400

BE15-4BE15-4: : Ravonette Corporation issued 300 shares of $10 par value

ordinary shares and 100 shares of $50 par value preference shares for

a lump sum of $13,500. The ordinary shares have a market value of

$20 per share, and the preference shares have a market value of $90

per share.

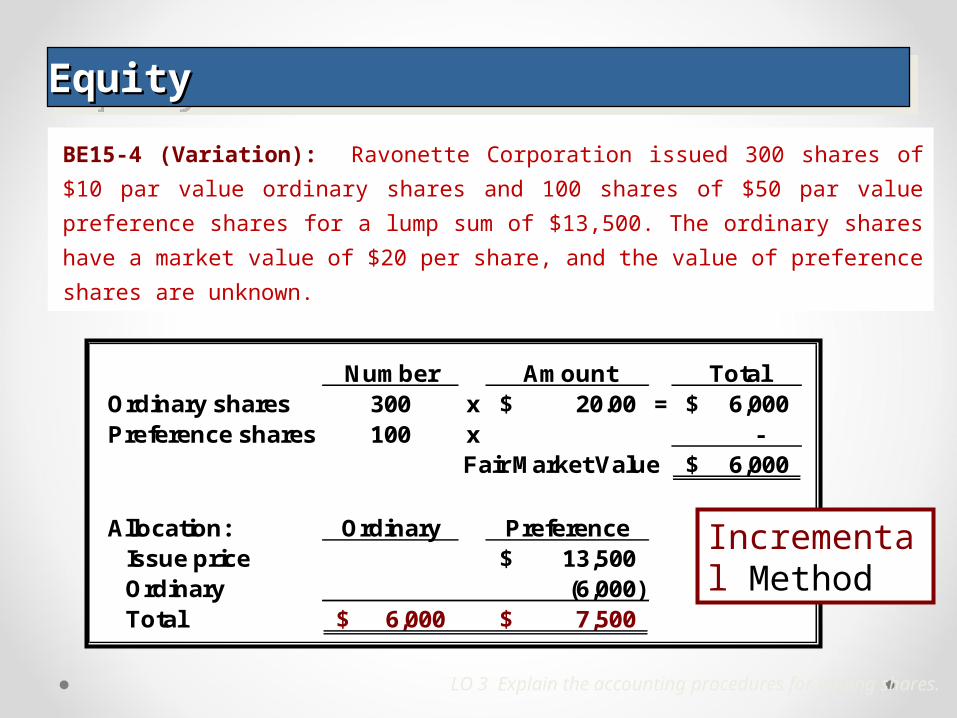

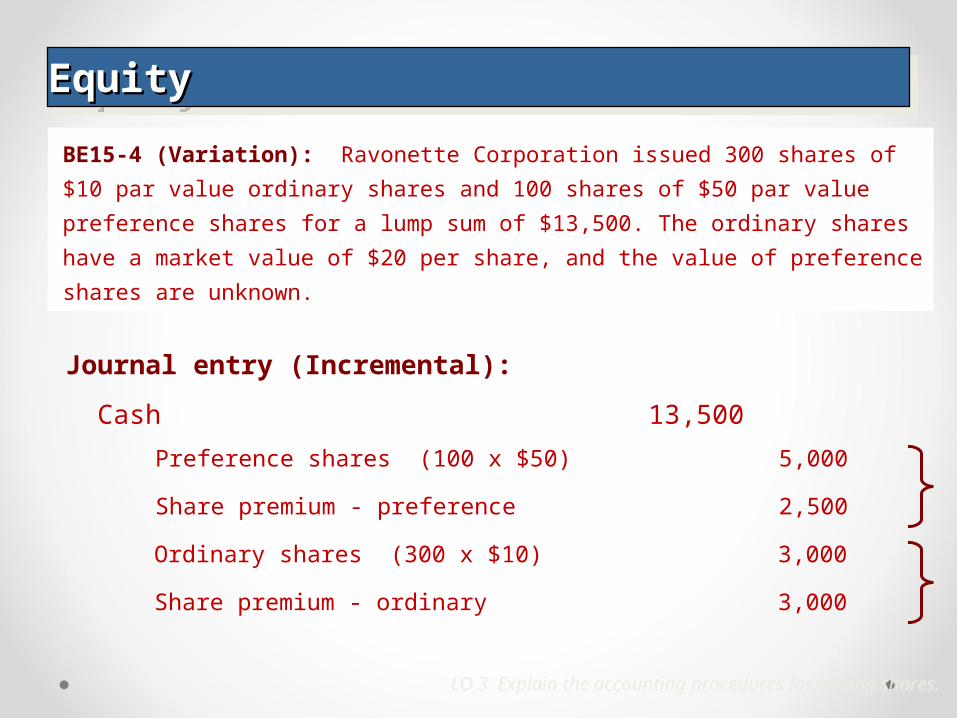

BE15-4 (Variation): Ravonette Corporation issued 300 shares of $10

par value ordinary shares and 100 shares of $50 par value preference

shares for a lump sum of $13,500. The ordinary shares have a market

value of $20 per share, and the value of preference shares are unknown.

LO 3 Explain the accounting procedures for issuing shares.

EquityEquityEquityEquity

Number Amount TotalOrdinary shares 300 x 20.00$ = 6,000$ Preference shares 100 x -

Fair Market Value 6,000$

Allocation: Ordinary PreferenceIssue price 13,500$ Ordinary (6,000) Total 6,000$ 7,500$

Incremental Method

LO 3 Explain the accounting procedures for issuing shares.

EquityEquityEquityEquity

Cash 13,500

Preference shares (100 x $50) 5,000

Journal entry (Incremental):

Share premium - preference 2,500

Ordinary shares (300 x $10) 3,000

Share premium - ordinary 3,000

BE15-4 (Variation): Ravonette Corporation issued 300 shares of $10

par value ordinary shares and 100 shares of $50 par value preference

shares for a lump sum of $13,500. The ordinary shares have a market

value of $20 per share, and the value of preference shares are unknown.

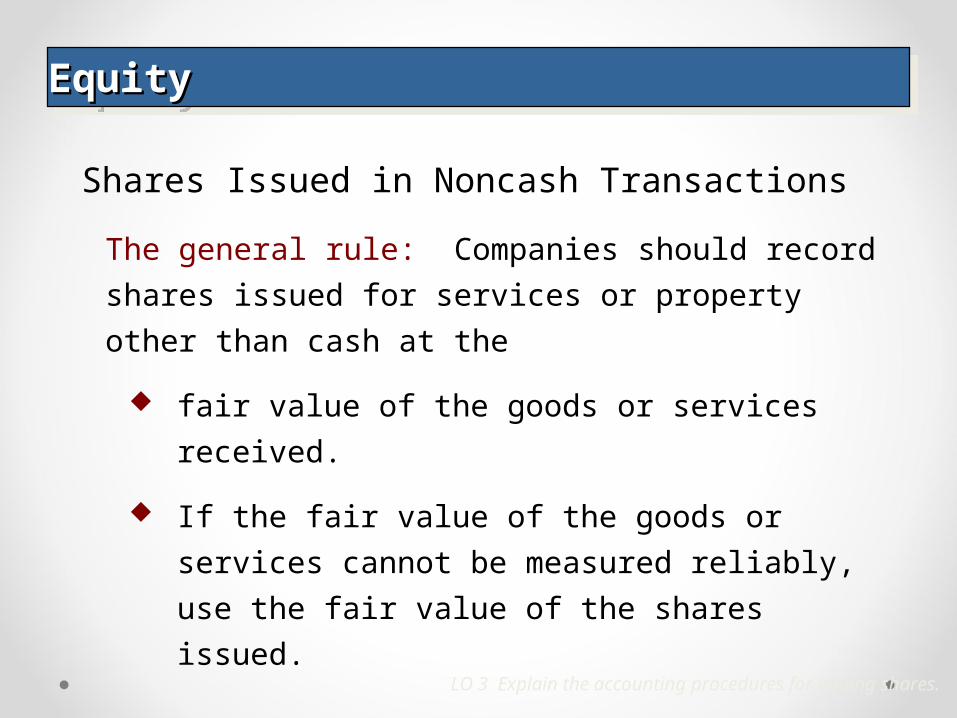

Shares Issued in Noncash Transactions

The general rule: Companies should record shares

issued for services or property other than cash at the

fair value of the goods or services received.

If the fair value of the goods or services cannot be

measured reliably, use the fair value of the shares

issued.

LO 3 Explain the accounting procedures for issuing shares.

EquityEquityEquityEquity

LO 3 Explain the accounting procedures for issuing shares.

EquityEquityEquityEquity

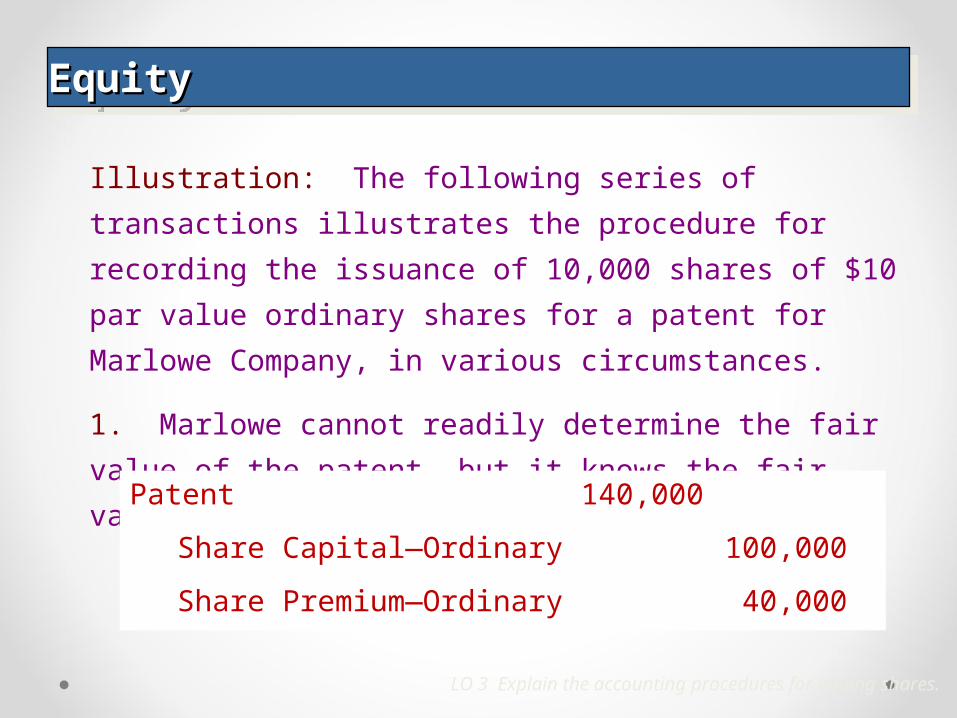

Illustration: The following series of transactions illustrates the

procedure for recording the issuance of 10,000 shares of $10

par value ordinary shares for a patent for Marlowe Company,

in various circumstances.

1. Marlowe cannot readily determine the fair value of the

patent, but it knows the fair value of the shares is $140,000.

Patent 140,000

Share Capital—Ordinary 100,000

Share Premium—Ordinary 40,000

LO 3 Explain the accounting procedures for issuing shares.

EquityEquityEquityEquity

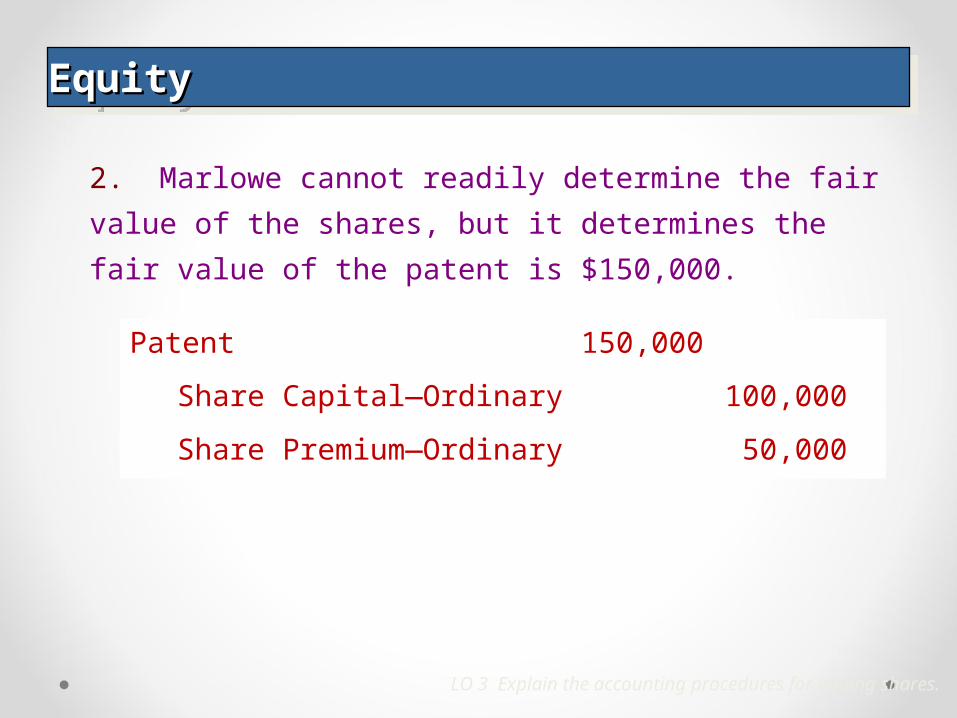

2. Marlowe cannot readily determine the fair value of the

shares, but it determines the fair value of the patent is

$150,000.

Patent 150,000

Share Capital—Ordinary 100,000

Share Premium—Ordinary 50,000

Financial Accounting and Reporting 1 39

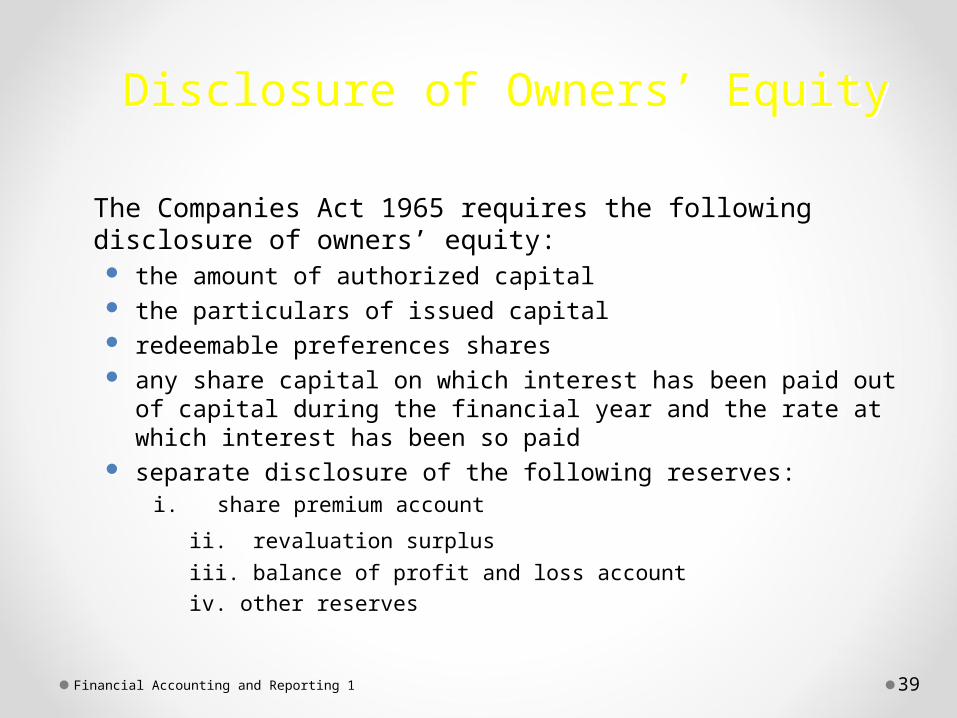

Disclosure of Owners’ EquityDisclosure of Owners’ Equity

The Companies Act 1965 requires the following disclosure of owners’ equity: the amount of authorized capital the particulars of issued capital redeemable preferences shares any share capital on which interest has been paid out of capital

during the financial year and the rate at which interest has been so paid

separate disclosure of the following reserves:i. share premium account

ii. revaluation surplus

iii. balance of profit and loss accountiv. other reserves

The Companies Act 1965 requires the following disclosure of owners’ equity: the amount of authorized capital the particulars of issued capital redeemable preferences shares any share capital on which interest has been paid out of capital

during the financial year and the rate at which interest has been so paid

separate disclosure of the following reserves:i. share premium account

ii. revaluation surplus

iii. balance of profit and loss accountiv. other reserves

Financial Accounting and Reporting 1 40

Disclosure of Owners’ EquityDisclosure of Owners’ Equity

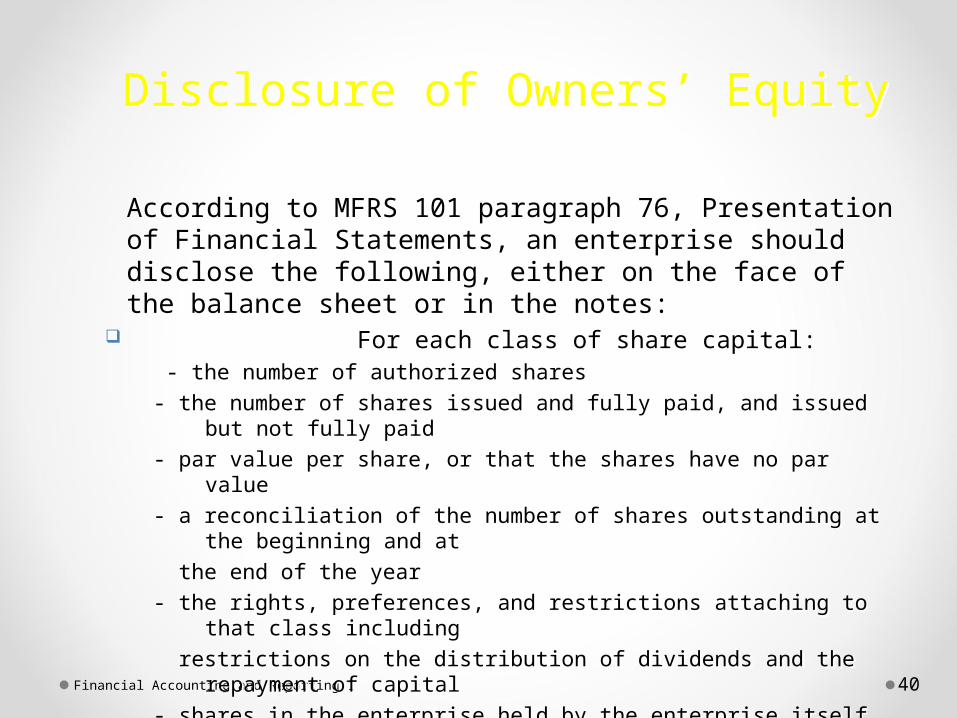

According to MFRS 101 paragraph 76, Presentation of Financial Statements, an enterprise should disclose the following, either on the face of the balance sheet or in the notes:

For each class of share capital: - the number of authorized shares- the number of shares issued and fully paid, and issued but not fully

paid- par value per share, or that the shares have no par value- a reconciliation of the number of shares outstanding at the

beginning and at the end of the year- the rights, preferences, and restrictions attaching to that class

including restrictions on the distribution of dividends and the repayment of

capital- shares in the enterprise held by the enterprise itself or by

subsidiaries or associates of the enterprise- shares reserved for issuance under options and sales contracts,

including the terms and amounts.

According to MFRS 101 paragraph 76, Presentation of Financial Statements, an enterprise should disclose the following, either on the face of the balance sheet or in the notes:

For each class of share capital: - the number of authorized shares- the number of shares issued and fully paid, and issued but not fully

paid- par value per share, or that the shares have no par value- a reconciliation of the number of shares outstanding at the

beginning and at the end of the year- the rights, preferences, and restrictions attaching to that class

including restrictions on the distribution of dividends and the repayment of

capital- shares in the enterprise held by the enterprise itself or by

subsidiaries or associates of the enterprise- shares reserved for issuance under options and sales contracts,

including the terms and amounts.

Financial Accounting and Reporting 1 41

Disclosure of Owners’ EquityDisclosure of Owners’ Equity

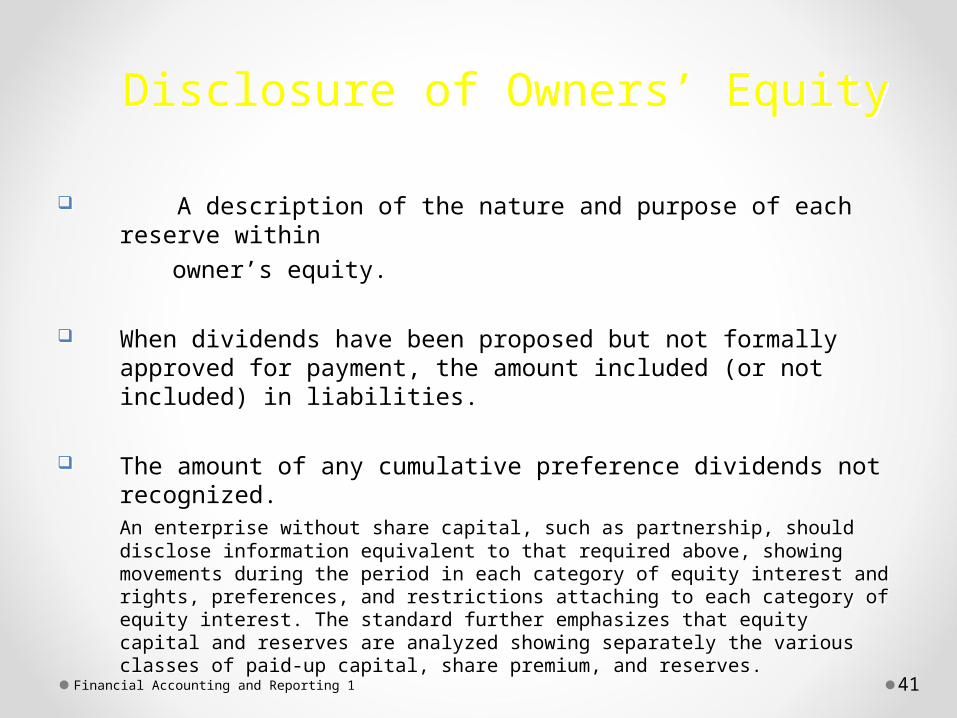

A description of the nature and purpose of each reserve within

owner’s equity.

When dividends have been proposed but not formally approved for payment, the amount included (or not included) in liabilities.

The amount of any cumulative preference dividends not recognized.An enterprise without share capital, such as partnership, should disclose information equivalent to that required above, showing movements during the period in each category of equity interest and rights, preferences, and restrictions attaching to each category of equity interest. The standard further emphasizes that equity capital and reserves are analyzed showing separately the various classes of paid-up capital, share premium, and reserves.

A description of the nature and purpose of each reserve within

owner’s equity.

When dividends have been proposed but not formally approved for payment, the amount included (or not included) in liabilities.

The amount of any cumulative preference dividends not recognized.An enterprise without share capital, such as partnership, should disclose information equivalent to that required above, showing movements during the period in each category of equity interest and rights, preferences, and restrictions attaching to each category of equity interest. The standard further emphasizes that equity capital and reserves are analyzed showing separately the various classes of paid-up capital, share premium, and reserves.

ConclusionConclusion • Owners’ equity represents the ownership

of a company.• Owners’ equity of a company normally

arises from the investment of shareholders and retained earnings.

• It is mandatory for a company to report owners’ equity on the balance sheet as highlighted in FRS 101, Presentations of Financial Statements.

Financial Accounting and Reporting 1 42