eOne PowerPoint Presentation · Investor overview. 1. A leading global entertainment group. ......

19

Entertainment One Investor overview

Transcript of eOne PowerPoint Presentation · Investor overview. 1. A leading global entertainment group. ......

Entertainment OneInvestor overview

1

A leading global entertainment groupeOne sources, selects and sells entertainment content across all media platforms globally. We offer investors an attractive and risk-mitigated way to benefit from the long-term trend

of rising consumer demand for film, television and family content

Strategy

2

3

Building the leading talent-driven entertainment company

Live events Licensing

Virtual reality

Music supervision

Artist mgmt

Production

4

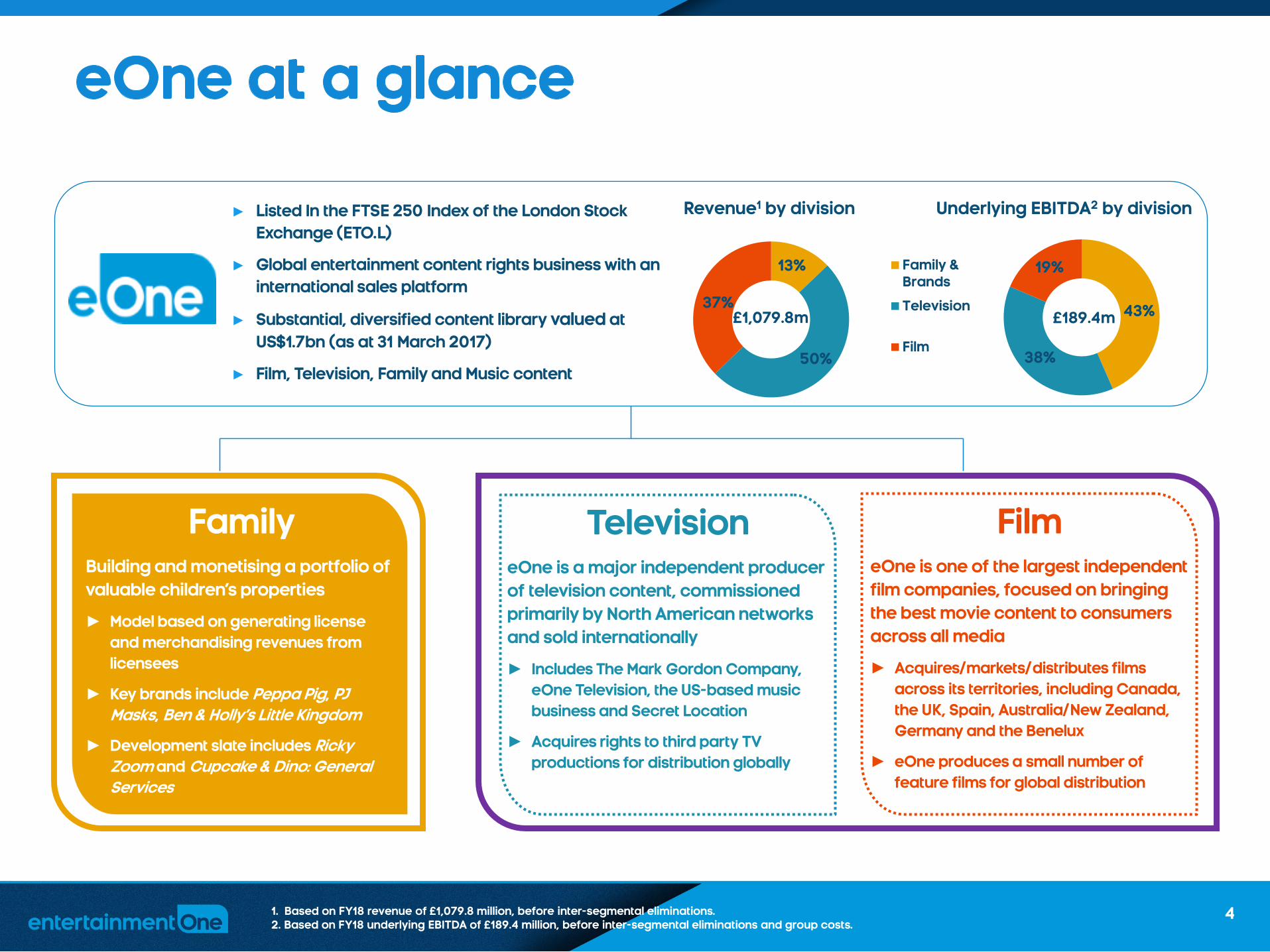

► Listed In the FTSE 250 Index of the London Stock Exchange (ETO.L)

► Global entertainment content rights business with an international sales platform

► Substantial, diversified content library valued at US$1.7bn (as at 31 March 2017)

► Film, Television, Family and Music content

1. Based on FY18 revenue of £1,079.8 million, before inter-segmental eliminations.2. Based on FY18 underlying EBITDA of £189.4 million, before inter-segmental eliminations and group costs.

Revenue1 by division Underlying EBITDA2 by division

Family &Brands

Television

Film

Film eOne is one of the largest independent film companies, focused on bringing the best movie content to consumers across all media

► Acquires/markets/distributes films across its territories, including Canada, the UK, Spain, Australia/New Zealand, Germany and the Benelux

► eOne produces a small number of feature films for global distribution

Television eOne is a major independent producer of television content, commissioned primarily by North American networks and sold internationally

► Includes The Mark Gordon Company, eOne Television, the US-based music business and Secret Location

► Acquires rights to third party TV productions for distribution globally

FamilyBuilding and monetising a portfolio of valuable children’s properties

► Model based on generating license and merchandising revenues from licensees

► Key brands include Peppa Pig, PJ Masks, Ben & Holly’s Little Kingdom

► Development slate includes Ricky Zoom and Cupcake & Dino: General Services

37%

19%

38%

43%

50%

13%

£189.4m£1,079.8m

5

Film

Family & Brands

TV

► International sales presence

► 500 broadcaster relationships across

cable, broadcast, pay-TV, digital

► 150 territories

► 1500+ L&M licences globally

► US$2.4bn retail sales in FY18 and growing

► SVOD, AVOD, live shows and theme park

revenues growing

► One of the largest global independent

distributors

► Strong production partnerships

► 6 international Film territories

► Relationships across all parts of the Film

value chain

► Transitioning from acquisition

to production activities

► 140 theatrical releases

planned for FY19

► £170m investment in content

for FY19

► Peppa Pig generated FY18

retail revenues of $1.3bn

► China is a major opportunity

► PJ Masks building traction

► A leading indie TV producer

► Prime-time scripted drama

and unscripted reality

► Over £350m investment in

content for FY19

Broad and growing content portfolio Global sales capability

6

mitigates individual title riskInvestment in… a broad content portfolio…

FY18: 144 theatrical releases

40,000+ Film and TV titles

FY18: 887 half hours of TV content

4,500+ hours of TV content

► Diversified, not reliant on hits

► Around 50% of Film revenues derived from library each year

► Delivering consistent portfolio return on investment

► Portfolio valued at US$1.7bn

► FY18: £438m invested in content

7

As at 31 March 2018, the overall value of the Group’s independent content library increased to US$2.0 billion

- The annual independent library valuation of the Group's library assets has increased, driven by continued growth in value of titles in Film & Television, continued growth in Family & Brands and improvement in the value of music assets

- The valuation was completed in September 2018 and takes into account the impact of the £57.0 million one-off charge largely relating to impairment of certain assets in the film distribution business

- Key valuation assumptions consistent year-on-year

- No significant change in Divisional split

Another year of growth

Key assumptions 30 September 2018

30 September 2017

Discount rate 7.2% 7.9%

Admin & OH rate 6.0% 6.0%

FX rates:

CAD 0.78 0.81

GBP 1.40 1.40

EUR 1.23 1.20

AUD 0.77 0.80

65

0

80

1

1,0

00

1,5

00

1,7

00

2,0

00

0

500

1000

1500

2000

2500

2013 2014 2015 2016 2017 2018

US$m

2018

US$2,000mEst

8

9

Half year financial highlightsRevenue £404.9m Stable

Strong growth in Family & Brands offset by lower Film & Television

EBITDA1 £60.1m 10% Includes approximately £2m costsavings

EBITDA margin 14.8% 1.6ptsGreater proportion of Group EBITDA from high margin Family & Brands

EPS2 6.1p 1.0p

Free cash outflow3 £88.1m £21.5m

Net debt £433.0m £120.2m Reflects MGC transaction £72m

Library valuation US$2.0bn US$0.3bn

10

Revenue growth in Family & Brands offset by lower Film & Television

Period-on-Period Divisional Revenue Bridge

£m 2018 2017 Change

Family & Brands 76.0 58.7 29%

Film & Television 331.5 356.5 (7%)

Theatrical 19.1 23.5 (19%)

Transactional 33.2 60.9 (45%)

Broadcast and Licensing 174.9 145.2 20%

Production and Other 76.5 103.9 (26%)

Music 27.8 23.4 19%

Eliminations - (0.4) 100%

Total Divisional Revenue 407.5 415.2 (2%)

Group Eliminations (2.6) (2.5) (4%)

Total Group Revenue 404.9 412.7 (2%)

£415.2m £407.5m

£17.3m £25.0m

2017 Family & Brands Film & Television 2018

Group revenue 2%– Family & Brands growth driven by strong SVOD and AVOD

revenues for Peppa Pig, significant growth from PJ Masks and new show Cupcake & Dino: General Services

– Film & Television decline due to lower theatrical, transactional and production and other revenue driven by fewer releases and deliveries and accelerated decline in the home entertainment market

– Partly offset by strong film and television SVOD revenue, higher television broadcast revenue and music growth

Foreign exchange– Translation impact of stronger pound sterling against the US,

Canadian and Australian dollars – underlying revenue flat on a constant currency basis

11

Growth driven by Family & Brands partly offset by lower Film & Television

Period-on-Period EBITDA Bridge

£54.5m

£60.1m

£10.6m

£0.5m

£0.1m

£5.6m

2017 Family & Brands Film & Television Group Elims Centre 2018

Group EBITDA 10%– Family EBITDA growth from strong performance of PJ Masks and

Peppa Pig– Film & Television lower revenue and title mix partly offset by cost

savings of approximately £2m– Greater proportion of Group EBITDA from Family & Brands

improving Group EBITDA margin %

Foreign exchange– Translation impact of stronger pound sterling against the US,

Canadian and Australian dollars had minimal impact – underlying EBITDA growth on a constant currency basis was also 10%

£m 2018 2017 Change

Family & Brands 47.2 36.6 29%

Film & Television 17.1 22.7 (25%)

Total Divisional EBITDA 64.3 59.3 8%

Group Eliminations 0.3 (0.2) 250%

Centre (4.5) (4.6) 2%

Total Group EBITDA 60.1 54.5 10%

EBITDA Margin % 14.8% 13.2% 160bps

12

Impacted by working capital outflows

Adjusted cash outflow higher than prior period by £25.2 million– Good cash generation in Family & Brands driven by revenue growth, with higher working capital outflow compared to prior period due to timing

of certain SVOD deals towards latter part of period and higher accrued income relating to increased royalty performance in the last quarter– Film & Television adjusted cash outflow was higher than the prior period due to higher working capital outflow owing to decrease in payables

driven by timing of payments in film distribution territories, reduction in deferred income, in particular, due to delivery of How It Ends and cash flow relating to intercompany trading with Film & Television production financing

Free cash outflow of £88.1 million, after interest, tax and capex– Driven by higher adjusted cash outflow and higher interest due to higher debt levels partly offset by lower tax payments due to timing

2018 2017

£mFamily &

BrandsFilm &

TelevisionCentre &

Elims TotalFamily &

BrandsFilm &

TelevisionCentre &

Elims Total

Underlying EBITDA (exc. Production) 47.0 14.0 (4.2) 56.8 36.9 18.0 (4.8) 50.1

Amortisation of investment in acquired content rights - 35.7 - 35.7 - 50.8 - 50.8

Investment in acquired content rights - (64.5) - (64.5) - (86.9) - (86.9)

Amortisation of investment in productions 1.4 57.1 (0.3) 58.2 1.1 21.2 - 22.3

Investment in productions, net of grants (2.5) (50.6) 0.3 (52.8) (3.2) (32.9) 0.2 (35.9)

Working capital (19.0) (67.4) (4.1) (90.5) (8.6) (23.7) - (32.3)

Adjusted cash flow 26.9 (75.7) (8.3) (57.1) 26.2 (53.5) (4.6) (31.9)

Capital expenditure (1.7) (1.5)

Tax paid (14.6) (21.7)

Net interest paid (14.7) (11.5)

Free cash flow (88.1) (66.6)

13

£m 2018 2017

Net debt (433.0) (312.8)

Net debt higher than prior period:– Higher opening net debt due to impact of MGC transaction

(£72.1m)– Free cash outflow £21.5m higher offset by lower one-off items

Full year leverage expected to be around 1.8x

14

FY19 Guidance

May 2018 Guidance Nov 2018 Guidance

Family & BrandsFY19 FY19

Investment in acquired content and productions £13.5 million £13.5 million

Film & Television FY19 FY19

Investment in productions, Television £309.0 million £275.0 million

Investment in acquired content, Television £45.0 million £45.0 million

Investment in productions, Film £70.0 million £50.0 million

Investment in acquired content, Film £100.0 million £90.0 million

Investment in acquired content and production, Other £5.0 million £10.0 million

Half hours produced/acquired, Television Over 1,000 Over 1,000

No. of theatrical releases 140 120

No. of unique theatrical releases 80 60

FY19 FY19

Amortisation of acquired intangibles £37.0 million £39.0 million

One-off items £7.0 million £65.0 million

Adjusted effective tax rate 20.0% 20.0%

Weighted average number of shares - diluted 481 million

Net debt to Group EBITDA leverage 1.8x 1.8x

Summary

15

16

Robust EBITDA performance, strong margin growth

Family & Brands performing well, driven by multiple revenue streams

• Growth in digital platform sales, experiential revenues developing

• Ricky Zoom broadcast debut in spring/summer 2019

Film & Television experiencing revenue mix changes as industry evolves

• Film slate transition continues as planned as home entertainment market decline accelerates

• High demand for quality television content, exciting pipeline of development projects

• Strong SVOD and television broadcast sales

• Solid growth in Music set to continue

Robust development pipeline for Film & Television to drive future growth

On track to deliver £13-15 million of annualised cost savings by the end of FY20

Independent valuation of the library increased to US$2.0 billion

Full year financial performance anticipated to be in line with management expectations

17

1. Underlying EBITDA (referred to as “EBITDA” herein) is operating profit before one-off items, amortisation of acquired intangibles, depreciation and amortisation of software, share-based payment charge, and tax, finance costs and depreciation related to joint ventures. Underlying EBITDA is reconciled to operating profit in the "Other Financial Information” section of the Interim Announcement.

2. Adjusted profit before tax is the reported measure before amortisation of acquired intangibles, share-based payment charge, tax, finance costs and depreciation related to joint ventures, operating one-off items and finance one-off items. Adjusted diluted earnings per share is adjusted for the tax effect of these items and other one-off tax items.

3. Free cash flow is calculated from cash flows associated with the net debt of the Group. It excludes cash flows associated with production activities funded using production financing. Free cash flow is adjusted cash flow less capital expenditure, net interest paid and tax paid. It is measured excluding one-off items. Adjusted cash flow is underlying EBITDA (excluding EBITDA related to production financing), amortisation of acquired content rights, investment in acquired content rights, amortisation of investment in productions, investment in productions (net of grants) and working capital.

18

This confidential presentation (including any oral information, question and answer session and any other document or materials distributed at or in connection with this presentation) (the “Presentation”) has been prepared by Entertainment One Ltd. (the “Company”), and contains confidential information regarding the Company, its business and operations and members of its group (the “Group”). It is provided for the exclusive use of the persons provided with the Presentation, and the Presentation and any further confidential information made available to any recipient, either verbally or in writing, must be held in complete confidence and without prejudice to the aforesaid, such information and documents containing such information may not be reproduced, used or in any way disclosed without the prior written consent of the Company.

This Presentation is not intended to form the basis of any investment activity or decision, and should not be considered as a recommendation by the Company that any recipient should acquire any interest in the share capital or in any other interest in the Company. It does not constitute or form part of and should not be relied upon in connection with any offer or invitation to sell or issue, or a solicitation of an offer or invitation to purchase or subscribe for, any securities or other interests in the Company or any related entity and no legal relations shall be created by its issue.

The contents of this Presentation have not been approved for distribution in the UK by an authorised person for the purposes of Section 21 of the Financial Services and Markets Act 2000 (“FSMA”). This Document may only be communicated or caused to be communicated in the UK to: (1) persons authorised to carry on a regulated activity (“Authorised Persons”) under FSMA; (2) persons otherwise having professional experience in matters relating to investments and qualifying as investment professionals under Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”); (3) persons qualifying as high net worth individuals under Article 48 of the Order; (4) persons qualifying as high net worth companies or unincorporated associations under Article 49 of the Order; or (5) to any other person to whom this Document may otherwise lawfully be communicated or caused to be communicated, including the recipients (“Relevant Persons” ).

The distribution of the Presentation in certain jurisdictions may be restricted by law and therefore persons into whose possession this document comes should inform themselves about and observe such restrictions. Any person who receives this Presentation in violation of such restrictions should not act upon it and should return it to the Company immediately. The Presentation is not directed to, or intended for distribution or use by any persons or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction. In particular, this Presentation (and the information contained in it) is not for release, publication or distribution, directly or indirectly, in the United States (or for the account of any "U.S. Person" as defined in Regulation S under the US Securities Act 1933), Australia, New Zealand, Canada, Japan or South Africa. Persons into whose possession this Presentation comes should inform themselves about and observe such restrictions.