E.ON Roadshow March 2017 from long-term customer relations built on satisfaction and trust ~15% >6...

39

March 2017 E.ON Roadshow

Transcript of E.ON Roadshow March 2017 from long-term customer relations built on satisfaction and trust ~15% >6...

March 2017

E.ON Roadshow

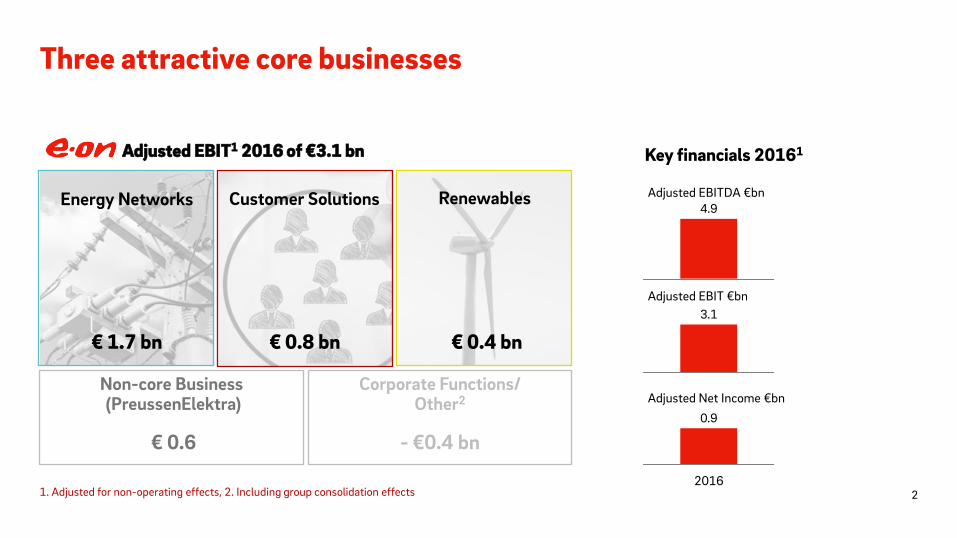

Three attractive core businesses

2

Adjusted EBITDA €bn

Adjusted EBIT €bn

Adjusted Net Income €bn

Adjusted EBIT1 2016 of €3.1 bn

4.9

3.1

0.9

2016

Corporate Functions/ Other2

- €0.4 bn

Non-core Business (PreussenElektra)

€ 0.6

€ 1.7 bn € 0.4 bn € 0.8 bn

Key financials 20161

1. Adjusted for non-operating effects, 2. Including group consolidation effects

Energy Networks Customer Solutions Renewables

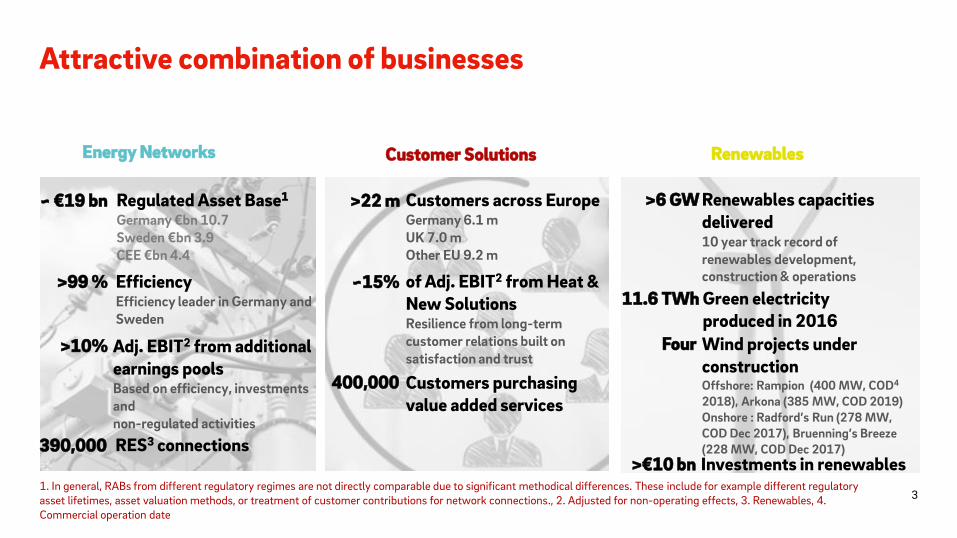

Attractive combination of businesses

1. In general, RABs from different regulatory regimes are not directly comparable due to significant methodical differences. These include for example different regulatory asset lifetimes, asset valuation methods, or treatment of customer contributions for network connections., 2. Adjusted for non-operating effects, 3. Renewables, 4. Commercial operation date

Energy Networks Renewables Customer Solutions

~ €19 bn Regulated Asset Base1 Germany €bn 10.7 Sweden €bn 3.9 CEE €bn 4.4

Efficiency Efficiency leader in Germany and Sweden

>99 %

Adj. EBIT2 from additional earnings pools Based on efficiency, investments and non-regulated activities

>10%

>22 m Customers across Europe Germany 6.1 m UK 7.0 m Other EU 9.2 m

Customers purchasing value added services

400,000

of Adj. EBIT2 from Heat & New Solutions Resilience from long-term customer relations built on satisfaction and trust

~15%

>6 GW Renewables capacities delivered 10 year track record of renewables development, construction & operations

Wind projects under construction Offshore: Rampion (400 MW, COD4 2018), Arkona (385 MW, COD 2019) Onshore : Radford’s Run (278 MW, COD Dec 2017), Bruenning’s Breeze (228 MW, COD Dec 2017)

Four

Green electricity produced in 2016

11.6 TWh

RES3 connections 390,000 Investments in renewables

>€10 bn

3

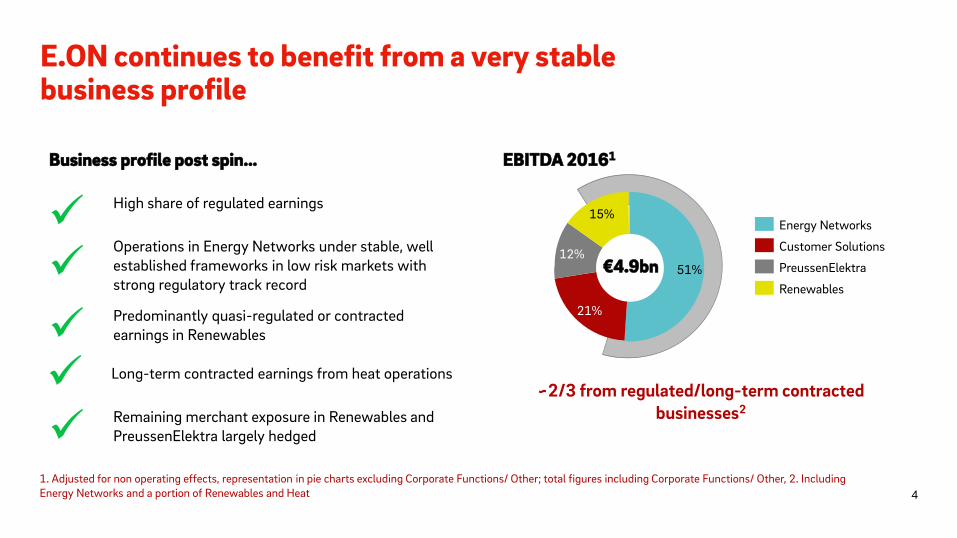

E.ON continues to benefit from a very stable business profile

Business profile post spin…

High share of regulated earnings

Predominantly quasi-regulated or contracted earnings in Renewables

Remaining merchant exposure in Renewables and PreussenElektra largely hedged

Operations in Energy Networks under stable, well established frameworks in low risk markets with strong regulatory track record

Long-term contracted earnings from heat operations

EBITDA 20161

~2/3 from regulated/long-term contracted businesses2

1. Adjusted for non operating effects, representation in pie charts excluding Corporate Functions/ Other; total figures including Corporate Functions/ Other, 2. Including Energy Networks and a portion of Renewables and Heat

51%

15%

12%

21%

Energy Networks

Customer Solutions

PreussenElektra

Renewables

€4.9bn

4

Solid delivery of full year 2016 targets

EBIT1 and EBITDA1 at top end of full year guidance

Adj. Net Income1 at the upper end of the guidance range

Dividend proposal: €0.21/share

Efficiency program initiated - securing sustainable competitiveness

Focus on disciplined capital allocation - CAPEX spending reduced

Uniper spin-off and KFK law led to high extraordinary effects and total reported IFRS loss of €16.0 bn in 2016

Highlights

904

Adj. Net Income1 EBIT1

3.112

EBITDA1

4.939

2016 key figures

1. Adjusted for non operating effects

€ m

2016 Outlook range

2.700-3.100

600 - 1.000

4.600 - 5.000

5

KFK implementation in final stages

6

Status / Next steps Total payment amount for E.ON confirmed

2.00.2

10.0

7.8

Premium1 Provisions Payment amount1

Provision for interest costs

€ bn

• German legislative process completed

• Law approved by Bundestag and Bundesrat in December 16

• State aid approval by the EU Commission expected in Q2 17

• Additional contract finalized

• Nuclear operators are dropping storage-related legal claims and moratorium court cases

• Signing of contract expected closely after law enters into force

• Payment planned around 1st July 2017

• Financing of premium via capital measures

• Financing of base amount via liquidity on balance sheet and bond issues (up to €3 bn) as well as Commercial Paper (CP)

1. Excluding €0.2 bn for minority shareholders

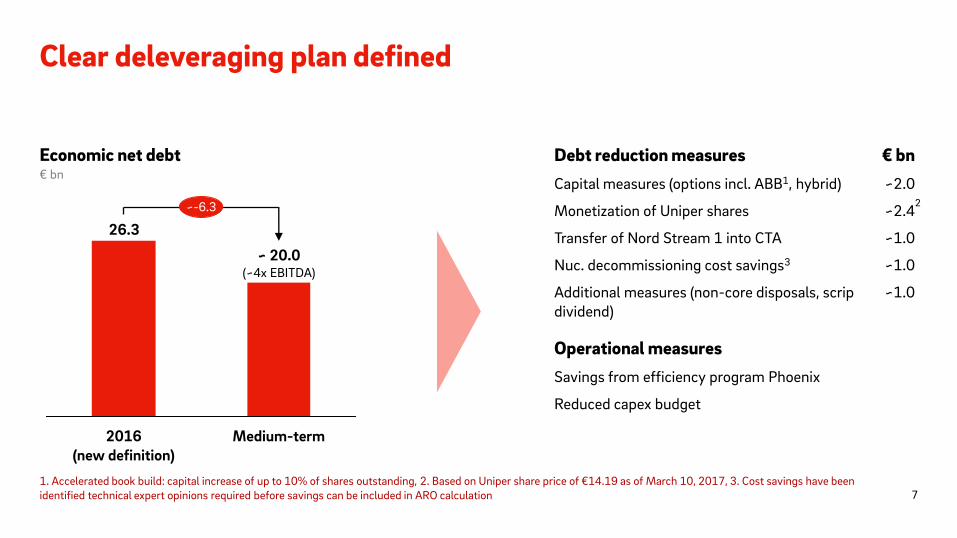

Clear deleveraging plan defined

Economic net debt Debt reduction measures

Capital measures (options incl. ABB1, hybrid)

Monetization of Uniper shares

Transfer of Nord Stream 1 into CTA

Nuc. decommissioning cost savings3

Additional measures (non-core disposals, scrip dividend)

Operational measures

Savings from efficiency program Phoenix

Reduced capex budget

€ bn

26.3

~ 20.0 (~4x EBITDA)

2016 (new definition)

~-6.3

Medium-term

€ bn

~2.0

~2.4

~1.0

~1.0

~1.0

1. Accelerated book build: capital increase of up to 10% of shares outstanding, 2. Based on Uniper share price of €14.19 as of March 10, 2017, 3. Cost savings have been identified technical expert opinions required before savings can be included in ARO calculation

2

7

Efficiency program Phoenix: Securing sustainable competitiveness

Principles Scope Targets, status, and next steps

Competitive services 4

Business empowerment 1

Lean management holding 2

Divisional steering 3

1.2

Costs in scope of Phoenix

4.1

Total E.ON

5.3

Controllable cost1 baseline

€ bn

• Phoenix target: €400 m EBIT contribution p.a. from 2018 onwards

• About €300 m from central overhead & support functions

• Restructuring of pension plans & other measures deliver ~€100 m

• Status/ Next steps

• 100% of target measures identified

• First measures being implemented

• Negotiations with workers’ council in Q2 2017

8

1. Controllable Costs include operational costs that management can meaningfully influence, such as material expenses, consultancy and personnel expenses. Margin-effective components such as fuel costs as well as cost item that are largely uncontrollable by the management are not included.

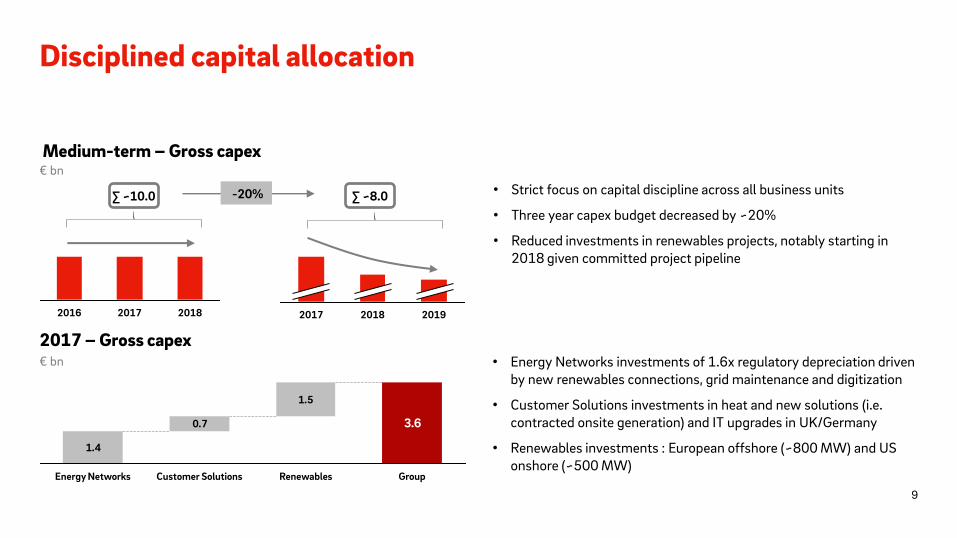

Disciplined capital allocation

Medium-term – Gross capex

• Strict focus on capital discipline across all business units

• Three year capex budget decreased by ~20%

• Reduced investments in renewables projects, notably starting in 2018 given committed project pipeline

2017 – Gross capex

2018 2017 2016

-20%

2019 2018 2017

1.4

0.7

1.5

3.6

Group Renewables Customer Solutions Energy Networks

€ bn

€ bn • Energy Networks investments of 1.6x regulatory depreciation driven by new renewables connections, grid maintenance and digitization

• Customer Solutions investments in heat and new solutions (i.e. contracted onsite generation) and IT upgrades in UK/Germany

• Renewables investments : European offshore (~800 MW) and US onshore (~500 MW)

∑ ~10.0 ∑ ~8.0

9

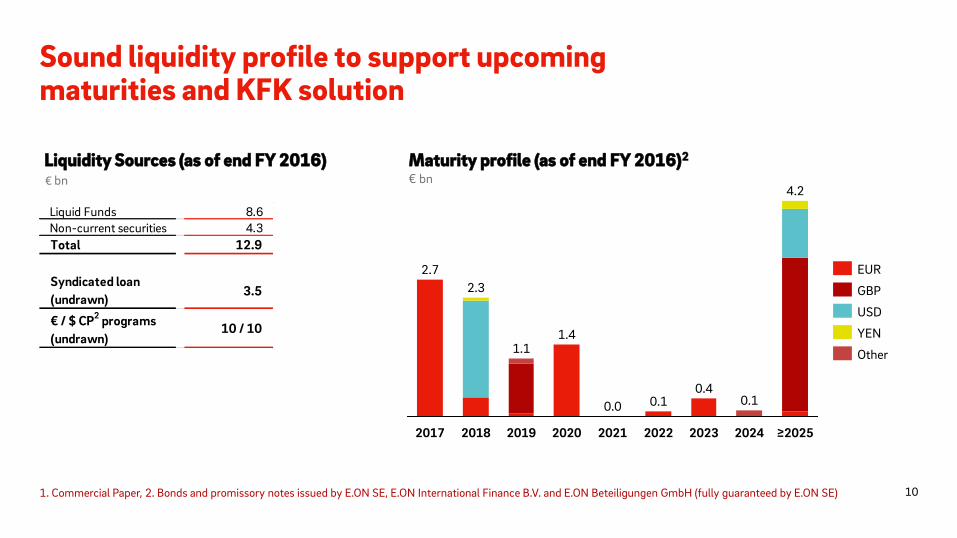

Sound liquidity profile to support upcoming maturities and KFK solution

Liquidity Sources (as of end FY 2016) Maturity profile (as of end FY 2016)2

€ bn

2022 2021

2.7

2020

2.3

2019

1.1

2018 2017

0.1 0.0

1.4

2024 2023

0.4

4.2

≥2025

0.1

€ bn

Other

YEN

USD

GBP

EUR

1. Commercial Paper, 2. Bonds and promissory notes issued by E.ON SE, E.ON International Finance B.V. and E.ON Beteiligungen GmbH (fully guaranteed by E.ON SE) 10

Liquid Funds 8.6

Non-current securities 4.3

Total 12.9

Syndicated loan

(undrawn)3.5

€ / $ CP2 programs

(undrawn) 10 / 10

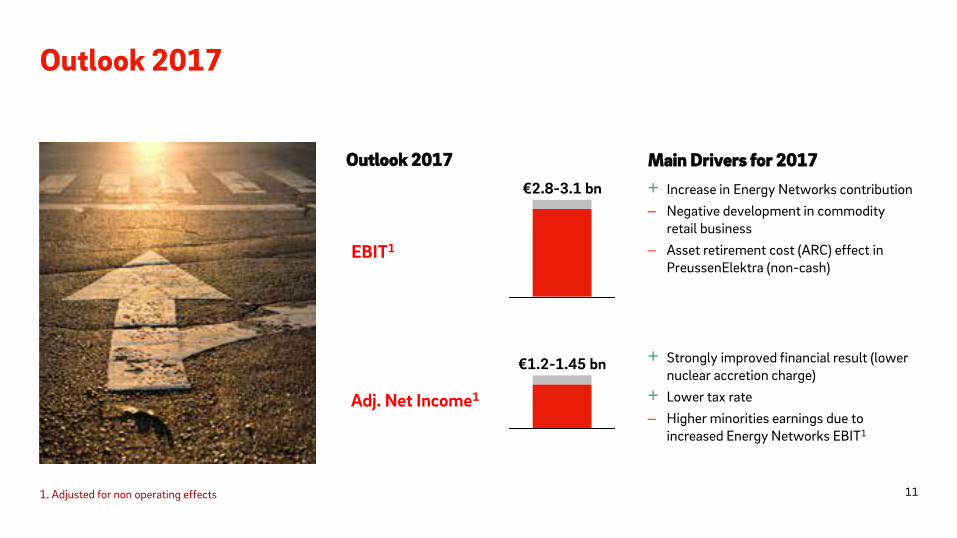

Outlook 2017

EBIT1

Adj. Net Income1

Outlook 2017

1. Adjusted for non operating effects

€2.8-3.1 bn

€1.2-1.45 bn

+ Increase in Energy Networks contribution

– Negative development in commodity retail business

– Asset retirement cost (ARC) effect in PreussenElektra (non-cash)

Main Drivers for 2017

+ Strongly improved financial result (lower nuclear accretion charge)

+ Lower tax rate

– Higher minorities earnings due to increased Energy Networks EBIT1

11

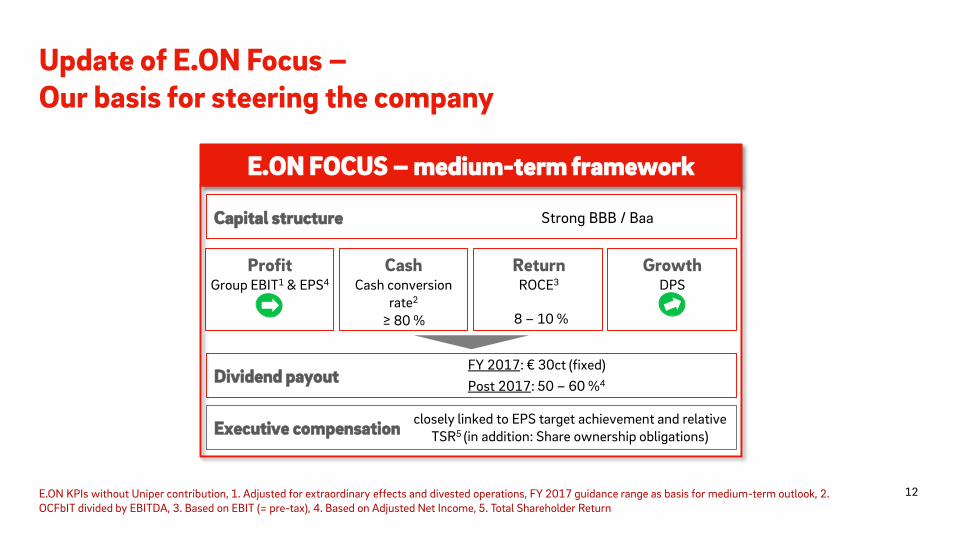

Executive compensation

Profit Group EBIT1 & EPS4

Cash Cash conversion

rate2 ≥ 80 %

Return ROCE3

8 – 10 %

Growth DPS

Capital structure Strong BBB / Baa

Dividend payout FY 2017: € 30ct (fixed)

Post 2017: 50 – 60 %4

E.ON FOCUS – medium-term framework

closely linked to EPS target achievement and relative TSR5 (in addition: Share ownership obligations)

Update of E.ON Focus – Our basis for steering the company

E.ON KPIs without Uniper contribution, 1. Adjusted for extraordinary effects and divested operations, FY 2017 guidance range as basis for medium-term outlook, 2. OCFbIT divided by EBITDA, 3. Based on EBIT (= pre-tax), 4. Based on Adjusted Net Income, 5. Total Shareholder Return

12

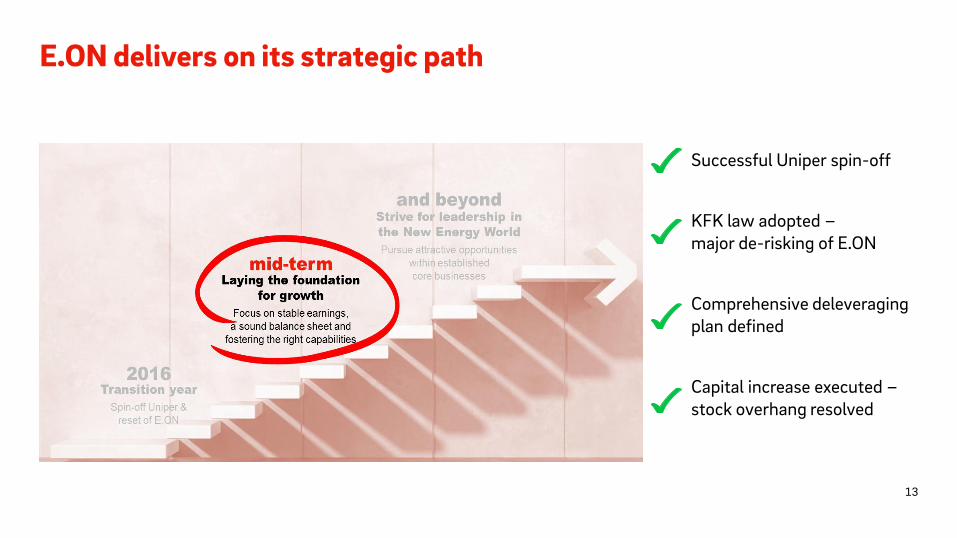

E.ON delivers on its strategic path

13

Successful Uniper spin-off

KFK law adopted – major de-risking of E.ON

Comprehensive deleveraging plan defined

Capital increase executed – stock overhang resolved

Appendix

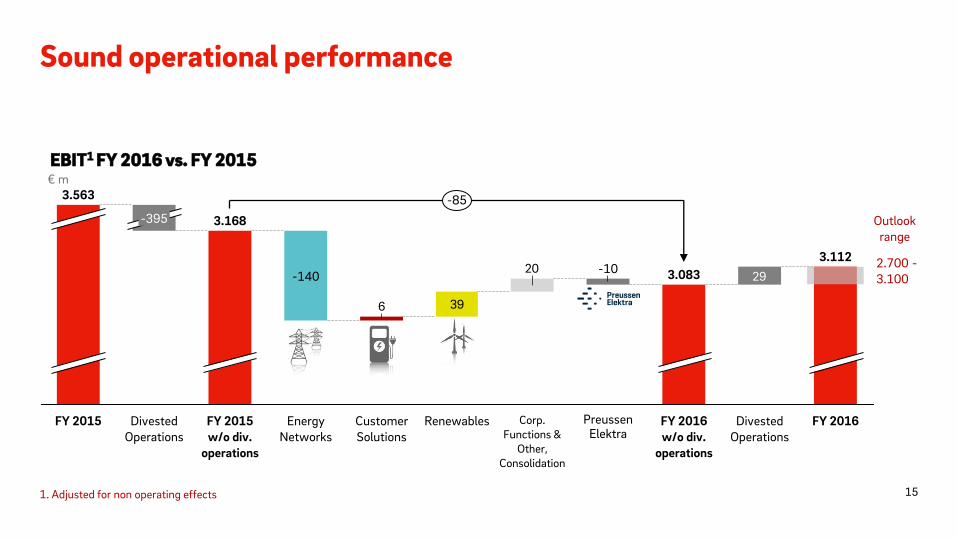

Sound operational performance

2920

396

-85

FY 2016 w/o div.

operations

Divested Operations

3.112

FY 2016

3.083

Preussen Elektra

-10

Corp. Functions &

Other, Consolidation

Renewables Customer Solutions

Energy Networks

-140

FY 2015 w/o div.

operations

3.168

Divested Operations

-395

FY 2015

3.563

EBIT1 FY 2016 vs. FY 2015 € m

1. Adjusted for non operating effects

2.700 -3.100

Outlook range

15

Adjusted Net Income and EPS up by ~10%

EPS (€ per share)

FY 2016 € m

0.46 904Adjusted

Net Income1

Minorities -278

Tax expense -478

Profit before Taxes1

1.660

Other interest expenses

-838

Interest on fin. assets/

liabilities2

-614

Group EBIT1 3.112

Improvement vs. previous year due to bond repayment in January

Slightly weaker than previous year; mainly driven by lower construction interest capitalization

Tax rate of 29% (FY 2015: 34%)

Slightly lower on YoY basis

Underlying net income (excl. divested operations) increased by ~10% YoY

1. Adjusted for non operating effects, 2. Without accretion of nuclear provisions 16

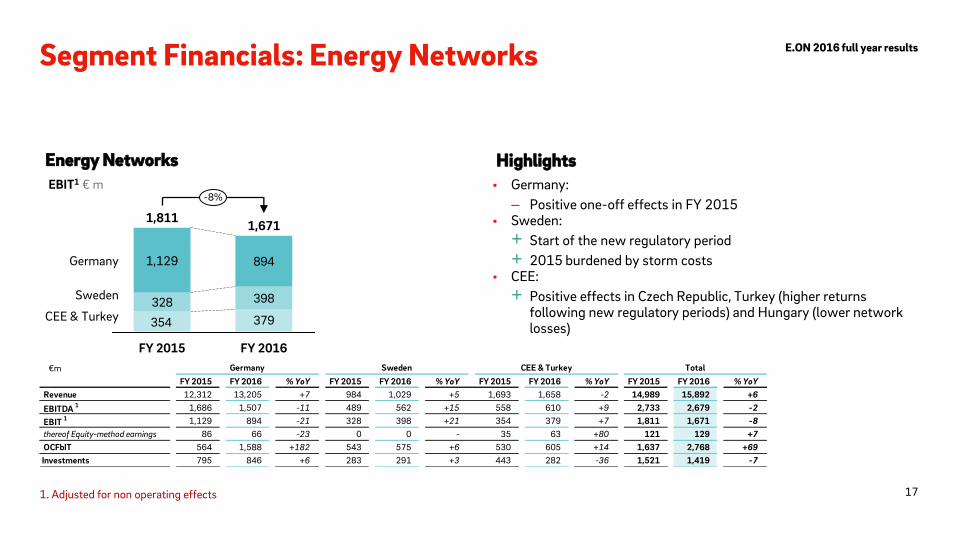

Segment Financials: Energy Networks

• Germany:

– Positive one-off effects in FY 2015 • Sweden:

+ Start of the new regulatory period

+ 2015 burdened by storm costs • CEE:

+ Positive effects in Czech Republic, Turkey (higher returns following new regulatory periods) and Hungary (lower network losses)

Energy Networks Highlights

328 398

379354

894

Sweden

CEE & Turkey

-8%

Germany

FY 2016

1,671

FY 2015

1,811

1,129

1. Adjusted for non operating effects

EBIT1 € m

€m

FY 2015 FY 2016 % YoY FY 2015 FY 2016 % YoY FY 2015 FY 2016 % YoY FY 2015 FY 2016 % YoY

Revenue 12,312 13,205 +7 984 1,029 +5 1,693 1,658 -2 14,989 15,892 +6

EBITDA 1 1,686 1,507 -11 489 562 +15 558 610 +9 2,733 2,679 -2

EBIT 1 1,129 894 -21 328 398 +21 354 379 +7 1,811 1,671 -8

thereof Equity-method earnings 86 66 -23 0 0 - 35 63 +80 121 129 +7

OCFbIT 564 1,588 +182 543 575 +6 530 605 +14 1,637 2,768 +69

Investments 795 846 +6 283 291 +3 443 282 -36 1,521 1,419 -7

TotalGermany Sweden CEE & Turkey

17

E.ON 2016 full year results

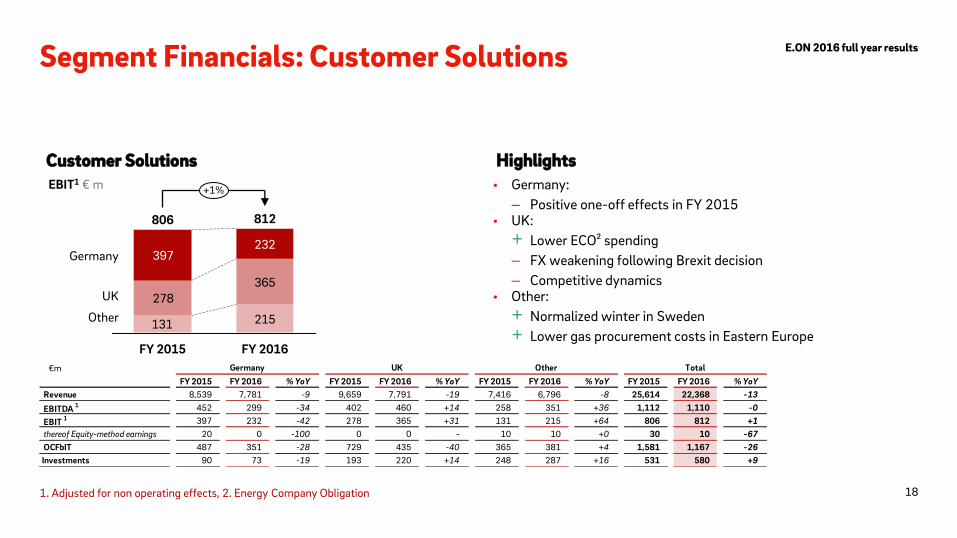

Segment Financials: Customer Solutions

Customer Solutions Highlights

• Germany:

– Positive one-off effects in FY 2015 • UK:

+ Lower ECO² spending

– FX weakening following Brexit decision

– Competitive dynamics • Other:

+ Normalized winter in Sweden

+ Lower gas procurement costs in Eastern Europe 215

278365

397232

131

+1%

Other

UK

Germany

FY 2016

812

FY 2015

806

EBIT1 € m

1. Adjusted for non operating effects, 2. Energy Company Obligation

€m

FY 2015 FY 2016 % YoY FY 2015 FY 2016 % YoY FY 2015 FY 2016 % YoY FY 2015 FY 2016 % YoY

Revenue 8,539 7,781 -9 9,659 7,791 -19 7,416 6,796 -8 25,614 22,368 -13

EBITDA 1 452 299 -34 402 460 +14 258 351 +36 1,112 1,110 -0

EBIT 1 397 232 -42 278 365 +31 131 215 +64 806 812 +1

thereof Equity-method earnings 20 0 -100 0 0 - 10 10 +0 30 10 -67

OCFbIT 487 351 -28 729 435 -40 365 381 +4 1,581 1,167 -26

Investments 90 73 -19 193 220 +14 248 287 +16 531 580 +9

TotalUKGermany Other

18

E.ON 2016 full year results

• Offshore:

+ Positive contribution from Humber & Amrumbank, book gain from Arkona stake sale (Q2 2016)

– Negative effects from lower wind yields & adverse FX development following Brexit decision

• Onshore:

– Positive one-off effects in FY 2015 (incl. book gains)

– Lower prices in FY 2016, phase-out of UK LEC scheme

Segment Financials: Renewables

Renewables Highlights

189

202338

92

+10%

Offshore/Other

Onshore/Solar

FY 2016

391 430

FY 2015

EBIT1 € m

1. Adjusted for non operating effects

€m

FY 2015 FY 2016 % YoY FY 2015 FY 2016 % YoY FY 2015 FY 2016 % YoY

Revenue 957 728 -24 524 629 +20 1,481 1,357 -8

EBITDA 1 422 308 -27 328 488 +49 750 796 +6

EBIT 1 189 92 -51 202 338 +67 391 430 +10

thereof Equity-method earnings 16 15 -6

OCFbit 563 699 +24

Investments 1,010 1,070 +6

Onshore Wind / Solar Offshore Wind / Others Total

19

E.ON 2016 full year results

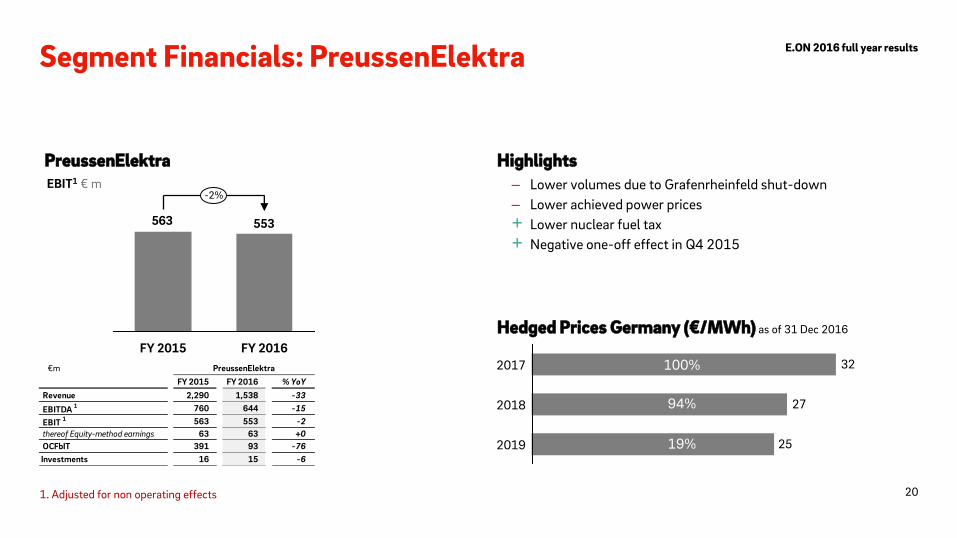

Segment Financials: PreussenElektra

PreussenElektra Highlights

553563

FY 2016

-2%

FY 2015

– Lower volumes due to Grafenrheinfeld shut-down

– Lower achieved power prices

+ Lower nuclear fuel tax

+ Negative one-off effect in Q4 2015

25

27

32

2019

2018

2017

Hedged Prices Germany (€/MWh) as of 31 Dec 2016

100%

94%

19%

EBIT1 € m

1. Adjusted for non operating effects

€m

FY 2015 FY 2016 % YoY

Revenue 2,290 1,538 -33

EBITDA 1 760 644 -15

EBIT 1 563 553 -2

thereof Equity-method earnings 63 63 +0

OCFbIT 391 93 -76

Investments 16 15 -6

PreussenElektra

20

E.ON 2016 full year results

+ Germany: lower maintenance costs, one-time regulatory effects

+ Sweden: power tariff increase

+ CEE: positive regulatory periods in Czech Republic, Turkey; new regulatory period in Hungary

+ Onshore/Offshore: normalized wind yields across portfolio

– Offshore: non-recurring book gain in 2016

Segment Outlook 2017

EBIT 2016 Drivers for 2017

Renewables

Customer Solutions

2017

Energy Networks

1,671

812

430

– Germany: competitive dynamics

– UK: impact of CMA resolution and Brexit; competitive dynamics

– Other EU: normalization of seasonal effects & procurement costs

€ m

21

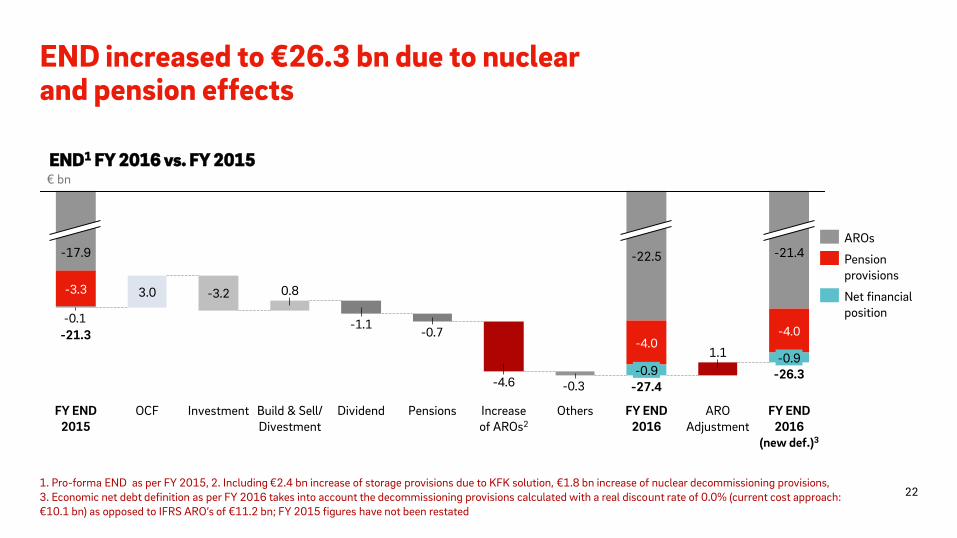

END increased to €26.3 bn due to nuclear and pension effects

-0.3-4.6

-0.7-1.1

-3.2

-4.0-4.0

-3.3

-0.1

ARO Adjustment

1.1

FY END 2016

-27.4 -0.9

-22.5

Others Investment

-17.9

0.8

-21.3

FY END 2015

Build & Sell/ Divestment

Dividend OCF Increase of AROs2

Pensions

3.0

FY END 2016

(new def.)3

-26.3 -0.9

-21.4

€ bn

END1 FY 2016 vs. FY 2015

1. Pro-forma END as per FY 2015, 2. Including €2.4 bn increase of storage provisions due to KFK solution, €1.8 bn increase of nuclear decommissioning provisions, 3. Economic net debt definition as per FY 2016 takes into account the decommissioning provisions calculated with a real discount rate of 0.0% (current cost approach: €10.1 bn) as opposed to IFRS ARO’s of €11.2 bn; FY 2015 figures have not been restated

Net financial position

Pension provisions

AROs

22

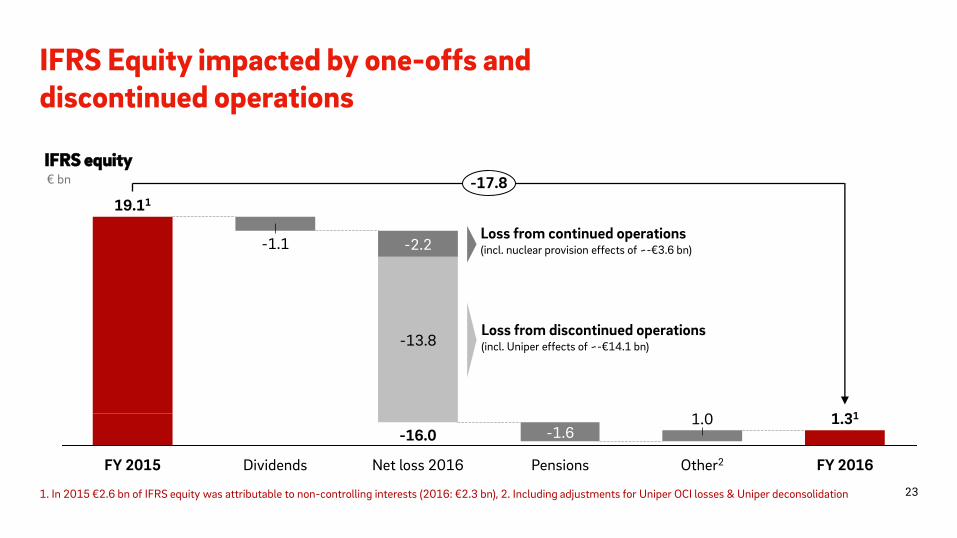

IFRS Equity impacted by one-offs and discontinued operations

1.0

Other2 Pensions

-1.6

Net loss 2016

-16.0

-13.8

-2.2

Dividends

-17.8

1.31

-1.1

FY 2015

19.11

FY 2016

IFRS equity € bn

Loss from continued operations (incl. nuclear provision effects of ~-€3.6 bn)

Loss from discontinued operations (incl. Uniper effects of ~-€14.1 bn)

1. In 2015 €2.6 bn of IFRS equity was attributable to non-controlling interests (2016: €2.3 bn), 2. Including adjustments for Uniper OCI losses & Uniper deconsolidation 23

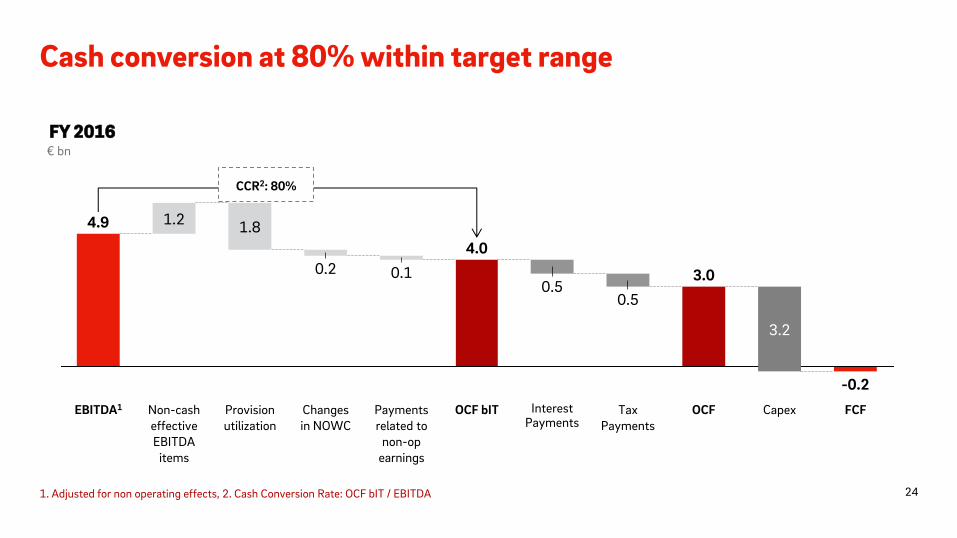

Cash conversion at 80% within target range

FY 2016 € bn

Capex

-0.2

FCF

3.2

OCF Interest Payments

0.5

OCF bIT

4.0

Payments related to

non-op earnings

0.1

Changes in NOWC

0.2

Provision utilization

1.8

Non-cash effective EBITDA

items

1.2

EBITDA1

0.5

Tax Payments

3.0

4.9

CCR2: 80%

1. Adjusted for non operating effects, 2. Cash Conversion Rate: OCF bIT / EBITDA 24

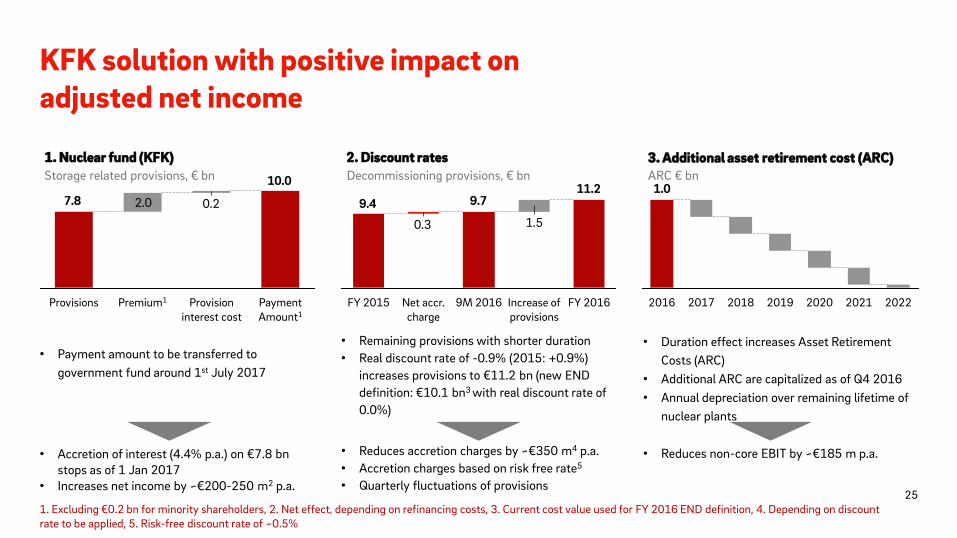

KFK solution with positive impact on adjusted net income

• Payment amount to be transferred to

government fund around 1st July 2017

• Accretion of interest (4.4% p.a.) on €7.8 bn stops as of 1 Jan 2017

• Increases net income by ~€200-250 m2 p.a.

1. Nuclear fund (KFK) 2. Discount rates 3. Additional asset retirement cost (ARC)

2.0 0.2

10.0

7.8

Payment Amount1

Provision interest cost

Premium1 Provisions

1. Excluding €0.2 bn for minority shareholders, 2. Net effect, depending on refinancing costs, 3. Current cost value used for FY 2016 END definition, 4. Depending on discount rate to be applied, 5. Risk-free discount rate of ~0.5%

11.29.79.4

1.50.3

FY 2016 Increase of provisions

9M 2016 Net accr. charge

FY 2015

Storage related provisions, € bn

• Remaining provisions with shorter duration

• Real discount rate of -0.9% (2015: +0.9%)

increases provisions to €11.2 bn (new END

definition: €10.1 bn3 with real discount rate of

0.0%)

• Reduces accretion charges by ~€350 m4 p.a.

• Accretion charges based on risk free rate5

• Quarterly fluctuations of provisions

1.0

2022 2021 2020 2019 2018 2017 2016

ARC € bn

• Duration effect increases Asset Retirement

Costs (ARC)

• Additional ARC are capitalized as of Q4 2016

• Annual depreciation over remaining lifetime of

nuclear plants

• Reduces non-core EBIT by ~€185 m p.a.

Decommissioning provisions, € bn

25

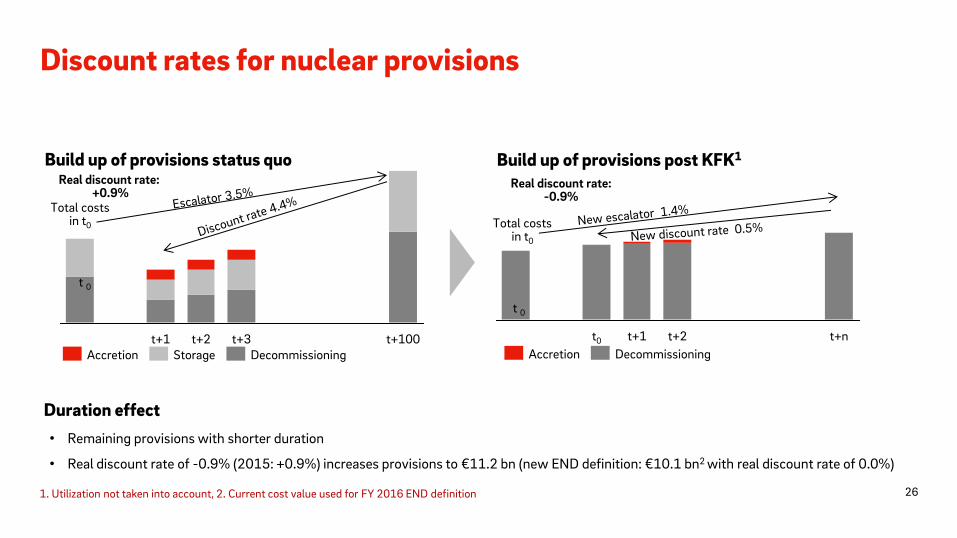

Discount rates for nuclear provisions

Build up of provisions status quo

t+3 t+100 t+2 t+1 Storage Accretion Decommissioning

Real discount rate: +0.9%

Build up of provisions post KFK1

t+2 t+1 t+n t0

Accretion Decommissioning

Real discount rate: -0.9%

• Remaining provisions with shorter duration

• Real discount rate of -0.9% (2015: +0.9%) increases provisions to €11.2 bn (new END definition: €10.1 bn2 with real discount rate of 0.0%)

Duration effect

Total costs in t0 Total costs

in t0

t 0

t 0

26 1. Utilization not taken into account, 2. Current cost value used for FY 2016 END definition

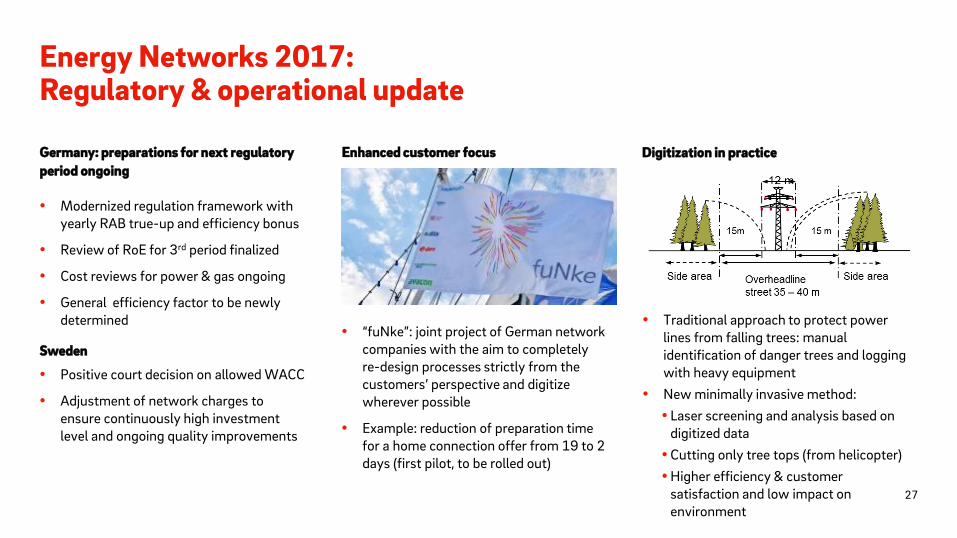

Digitization in practice

Energy Networks 2017: Regulatory & operational update

Germany: preparations for next regulatory

period ongoing

Enhanced customer focus

Modernized regulation framework with yearly RAB true-up and efficiency bonus

Review of RoE for 3rd period finalized

Cost reviews for power & gas ongoing

General efficiency factor to be newly determined

“fuNke”: joint project of German network companies with the aim to completely re-design processes strictly from the customers’ perspective and digitize wherever possible

Example: reduction of preparation time for a home connection offer from 19 to 2 days (first pilot, to be rolled out)

Traditional approach to protect power lines from falling trees: manual identification of danger trees and logging with heavy equipment

New minimally invasive method:

Laser screening and analysis based on digitized data

Cutting only tree tops (from helicopter)

Higher efficiency & customer satisfaction and low impact on environment

27

Sweden

Positive court decision on allowed WACC

Adjustment of network charges to ensure continuously high investment level and ongoing quality improvements

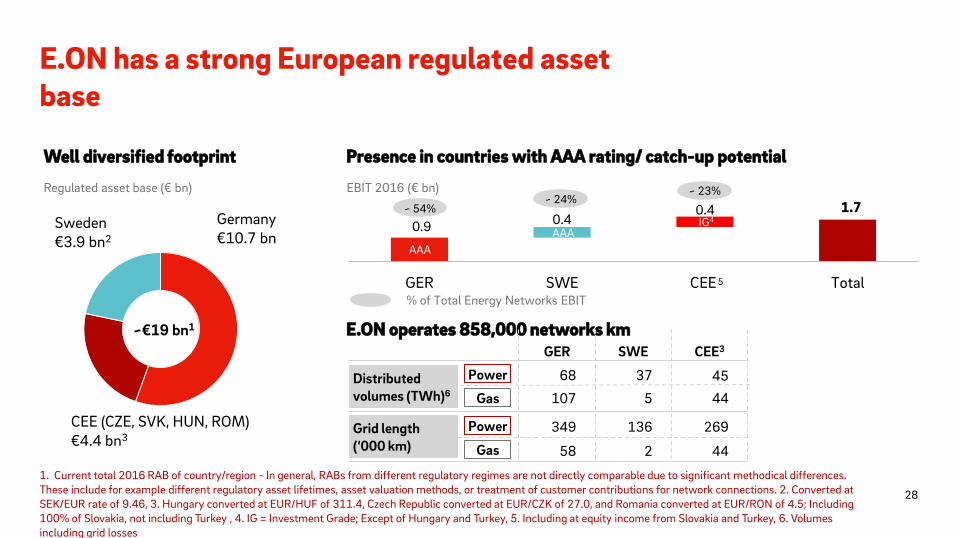

E.ON has a strong European regulated asset base

0.9 0.4 0.4

GER SWE CEE Total

IG4

E.ON operates 858,000 networks km

Presence in countries with AAA rating/ catch-up potential

CEE (CZE, SVK, HUN, ROM)

€4.4 bn3

Sweden €3.9 bn2

Germany €10.7 bn

~€19 bn1

EBIT 2016 (€ bn)

1.7 ~ 54% ~ 24%

~ 23%

% of Total Energy Networks EBIT

AAA

Well diversified footprint

5

Regulated asset base (€ bn)

68

107

349

58

Power

Gas

Power

Gas

37

5

136

2

269

44

45

44

GER SWE

Distributed volumes (TWh)6

Grid length (‘000 km)

CEE3

1. Current total 2016 RAB of country/region - In general, RABs from different regulatory regimes are not directly comparable due to significant methodical differences. These include for example different regulatory asset lifetimes, asset valuation methods, or treatment of customer contributions for network connections. 2. Converted at SEK/EUR rate of 9.46, 3. Hungary converted at EUR/HUF of 311.4, Czech Republic converted at EUR/CZK of 27.0, and Romania converted at EUR/RON of 4.5; Including 100% of Slovakia, not including Turkey , 4. IG = Investment Grade; Except of Hungary and Turkey, 5. Including at equity income from Slovakia and Turkey, 6. Volumes including grid losses

28

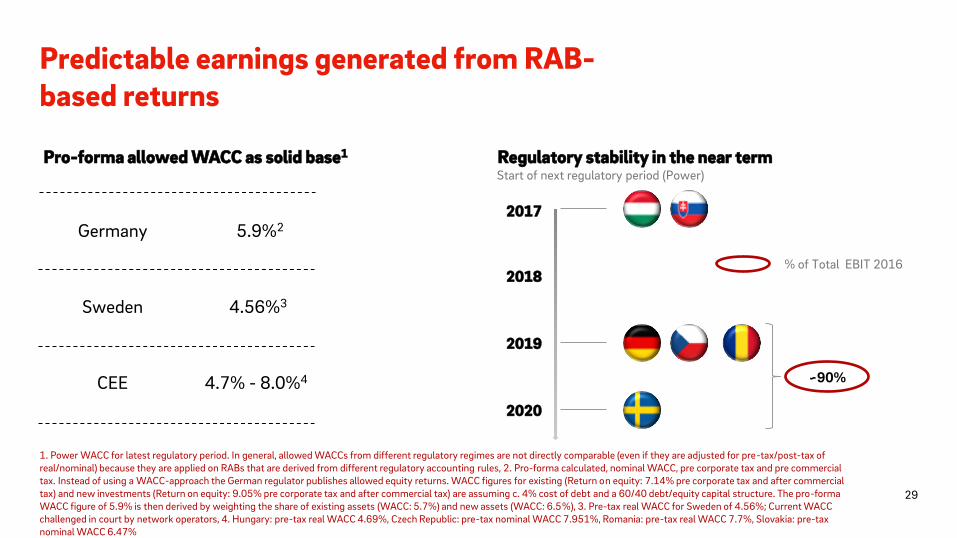

AAA

Predictable earnings generated from RAB-based returns

Start of next regulatory period (Power)

2017

2019

2018

2020

Germany 5.9%2

Sweden 4.56%3

CEE 4.7% - 8.0%4

% of Total EBIT 2016

Pro-forma allowed WACC as solid base1 Regulatory stability in the near term

~90%

1. Power WACC for latest regulatory period. In general, allowed WACCs from different regulatory regimes are not directly comparable (even if they are adjusted for pre-tax/post-tax of real/nominal) because they are applied on RABs that are derived from different regulatory accounting rules, 2. Pro-forma calculated, nominal WACC, pre corporate tax and pre commercial tax. Instead of using a WACC-approach the German regulator publishes allowed equity returns. WACC figures for existing (Return on equity: 7.14% pre corporate tax and after commercial tax) and new investments (Return on equity: 9.05% pre corporate tax and after commercial tax) are assuming c. 4% cost of debt and a 60/40 debt/equity capital structure. The pro-forma WACC figure of 5.9% is then derived by weighting the share of existing assets (WACC: 5.7%) and new assets (WACC: 6.5%), 3. Pre-tax real WACC for Sweden of 4.56%; Current WACC challenged in court by network operators, 4. Hungary: pre-tax real WACC 4.69%, Czech Republic: pre-tax nominal WACC 7.951%, Romania: pre-tax real WACC 7.7%, Slovakia: pre-tax nominal WACC 6.47%

29

Customer Solutions 2017: Introducing new solutions

E.ON Aura: PV & storage B2B Large: continuously gaining traction

All-in-one solution including PV, battery, energy management app, service & guarantee package and green electricity tariffs

Successful launch and scaling up across Germany

Introduction of virtual storage product E.ON SolarCloud

10x increase in unit sales in 2016 Target 2017: 10-15% market share

E-mobility: gearing up

Significant sales growth with tailor-made energy solutions (on-site generation, energy efficiency, flexibility, storage,…)

Diversified portfolio of customers (auto suppliers, tires, chemical, retail,…)

Innovative solutions like e.g. fuel cells & battery storage

2017 ambition: new contracts with several hundred million in total revenues

Established dedicated unit to take leading role in developing Europe’s charging infrastructure

E.ON has extensive experience in e-mobility market leader in Denmark (2,500 charging points)

Data-based development of services for further markets

Partnerships with car rental company Sixt and e-mobility specialists 30

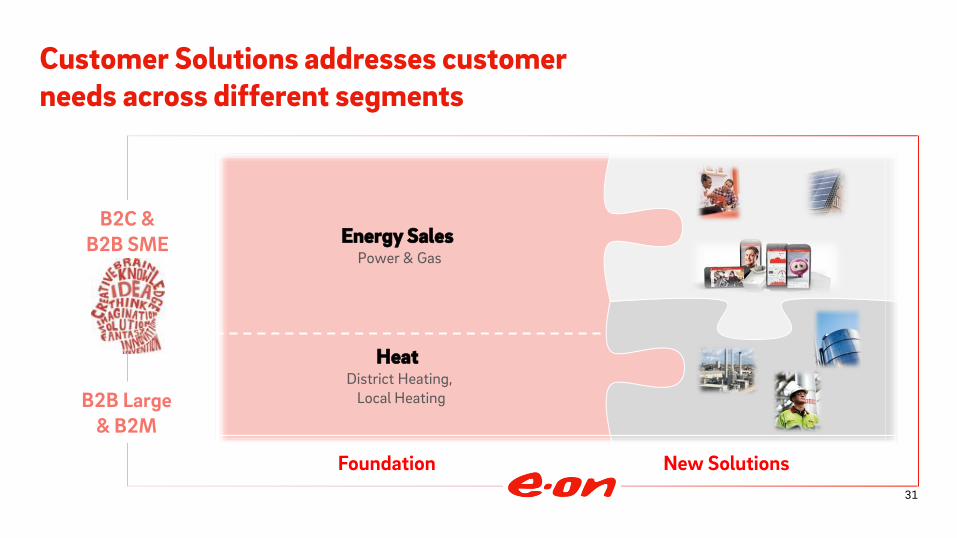

Customer Solutions addresses customer needs across different segments

Energy Sales Power & Gas

Heat District Heating,

Local Heating

Foundation New Solutions

B2B Large & B2M

B2C & B2B SME

31

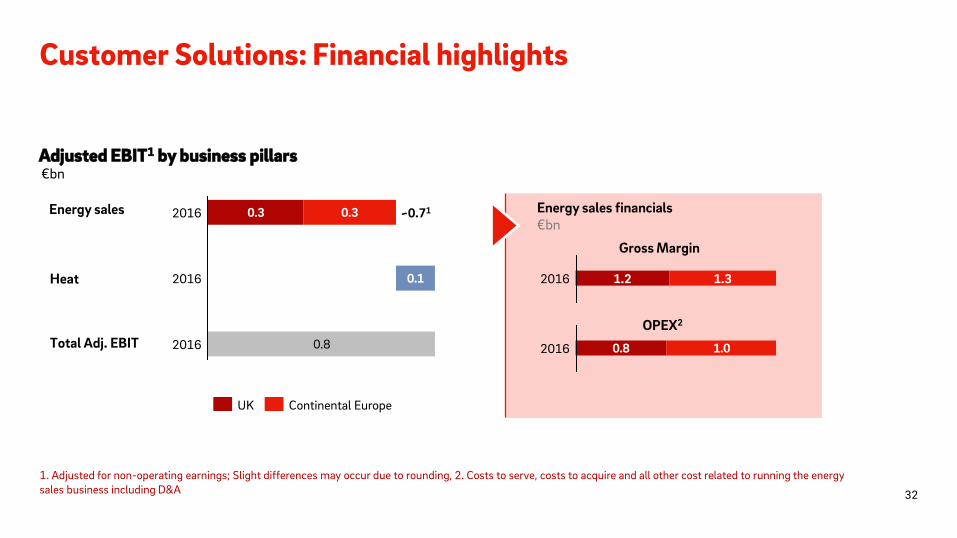

Customer Solutions: Financial highlights

Energy sales

Adjusted EBIT1 by business pillars

Heat

0.3

0.8

0.3

0.1

2016

2016

2016 ~0.71

Total Adj. EBIT

Energy sales financials

1.2 1.3 2016

Gross Margin

0.8 1.02016

OPEX2

Continental Europe UK

€bn

€bn

1. Adjusted for non-operating earnings; Slight differences may occur due to rounding, 2. Costs to serve, costs to acquire and all other cost related to running the energy sales business including D&A 32

Renewables 2017: Build-out fully on track

Rampion (400 MW in UK)

Installations of 116 mono-pile foundations completed

On time and within budget for completion in 2018

Arkona (385 MW in Germany)

Installation of 60 wind turbine foundations planned for 2017

Expected to be fully operational in 2019

US Onshore

US Storage

Radford’s Run (278 MW in Illinois)

Bruenning’s Breeze (228 MW in Texas)

Both farms scheduled to be in commercial operation in December 2017

E.ON actively developing projects in fast-growing energy storage market

Iron Horse (10 MW/2.5 MWh): first grid-scale project to support grid stability in Arizona (planned COD in H1 2017)

Texas Wave: two further projects (10 MW/5 MWh) in Texas on track to be completed in late 2017

Europe Offshore

Repowering projects started in Germany & UK

Won 57 MW auction in Italy with 20 years tariff of €66/ MWh

Europe Onshore

33

E.ONs capabilities in most attractive technologies and markets

Technology Geography Business model

• Focus on Onshore wind, off-shore wind & utility-scale PV

• Strong E.ON capabilities and experience

• Capture trends in line with E.ON’s capabilities / markets

Wind Onshore

PV

Wind Offshore

• Focus on Europe & North America

• Stable countries / low-risk

• Still attractive returns achieved

• Integrated renewables player

• Portfolio optimization strategy, bringing:

- Scale advantages

- Maintain capabilities

- Value creation

- Reduce cluster risk

1

34

Highlights

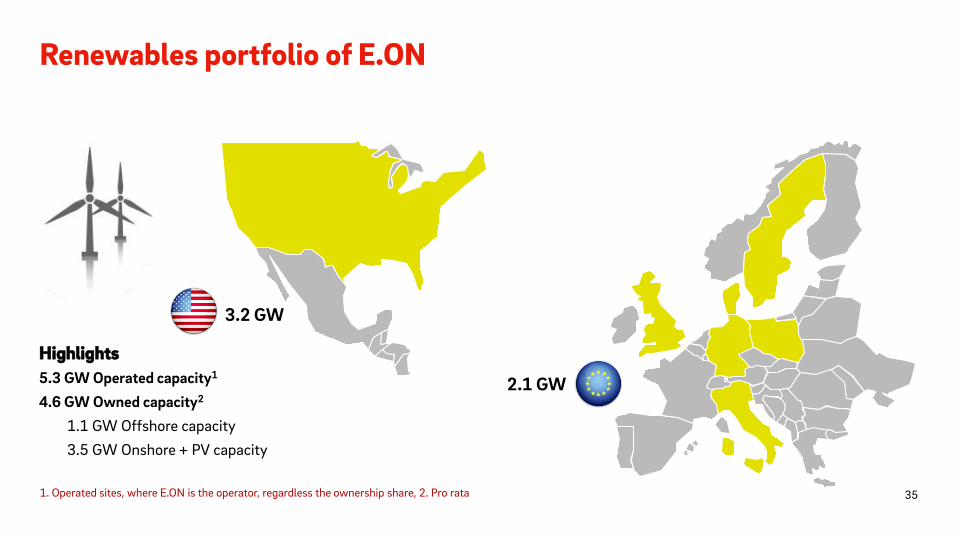

5.3 GW Operated capacity1

4.6 GW Owned capacity2

1.1 GW Offshore capacity

3.5 GW Onshore + PV capacity

Renewables portfolio of E.ON

1. Operated sites, where E.ON is the operator, regardless the ownership share, 2. Pro rata

2.1 GW

3.2 GW

35

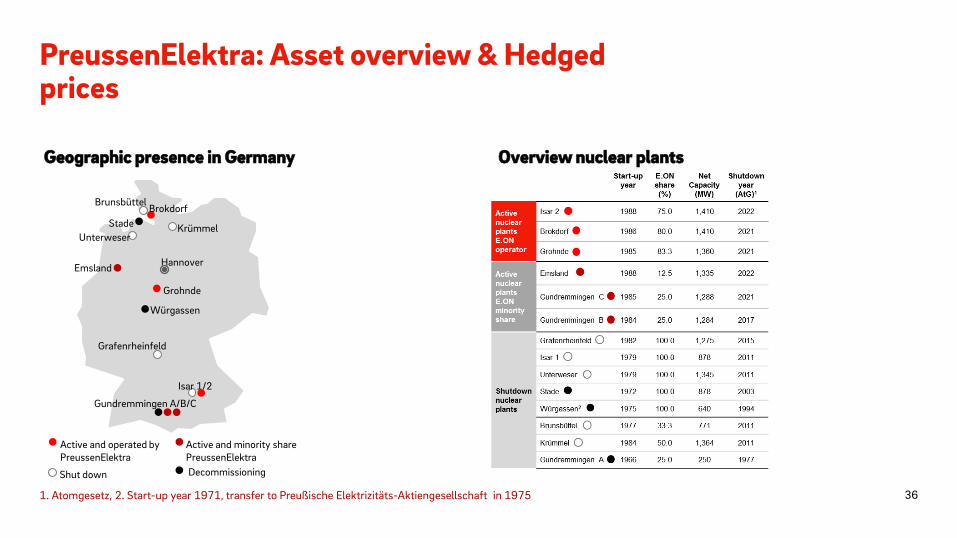

PreussenElektra: Asset overview & Hedged prices

36

Decommissioning Shut down

Active and operated by PreussenElektra

Active and minority share PreussenElektra

Brunsbüttel Brokdorf

Stade

Unterweser Krümmel

Hannover Emsland

Grohnde

Würgassen

Grafenrheinfeld

Isar 1/2

Gundremmingen A/B/C

Geographic presence in Germany Overview nuclear plants

1. Atomgesetz, 2. Start-up year 1971, transfer to Preußische Elektrizitäts-Aktiengesellschaft in 1975 36

Stringent incentive plan for the Management Board

KPI

Relative TSR1

EPS & individual performance

Cap

200% of target value

200% of target value

Calculation

TSR development relative to STOXX Europe 600 Utilities over 4 years

EPS × individual performance multiplier

Long-Term Incentive

Short-Term Incentive

Share Ownership Guidelines

Board members obliged to acquire E.ON shares equaling 150 – 200% of annual base salary

1. Total Shareholder Return 37

Martina Burger T +49 (201) 184 28 07

Manager Investor Relations [email protected]

Conny Ripphahn T +49 (201) 184 28 34

Manager Investor Relations [email protected]

E.ON Investor Relations contacts

T +49 (201) 184 2806 [email protected]

Dr. Stephan Schönefuß T +49 (201) 184 28 22

Manager Investor Relations [email protected]

Alexander Karnick T+49 (201) 184 28 38

Vice President Investor Relations [email protected]

Florian Floßmann T+49 (201) 184 28 33

Head of Investor Relations [email protected]

38

Rouven Fleischer T +49 (201) 184 72 30

Debt Investor Relations [email protected]

Financial calendar & important links

Financial calendar

May 9, 2017 Interim Report I: January – March 2017

May 10, 2017 2017 Annual Shareholders Meeting

August 9, 2017 Interim Report II: January – June 2017

November 8, 2017 Interim Report III: January – September 2017

March 14, 2018 Annual Report 2017

Important links

Presentations http://www.eon.com/en/investors/presentations.html

Annual Reports http://www.eon.com/en/investors/financial-publications/annual-report.html

Interim Reports http://www.eon.com/en/investors/financial-publications/interim-report.html

Shareholders Meeting http://www.eon.com/en/investors/shareholders-meeting.html

Creditor Relations http://www.eon.com/en/investors/presentations/bonds.html

39