Environment, Social & Governance Evaluation in … to affect a Company’s valuation and ... •...

30

Environment, Social & Governance Evaluation in Acquisition Diligence October 29, 2015

Transcript of Environment, Social & Governance Evaluation in … to affect a Company’s valuation and ... •...

Environment, Social & Governance Evaluation in

Acquisition Diligence October 29, 2015

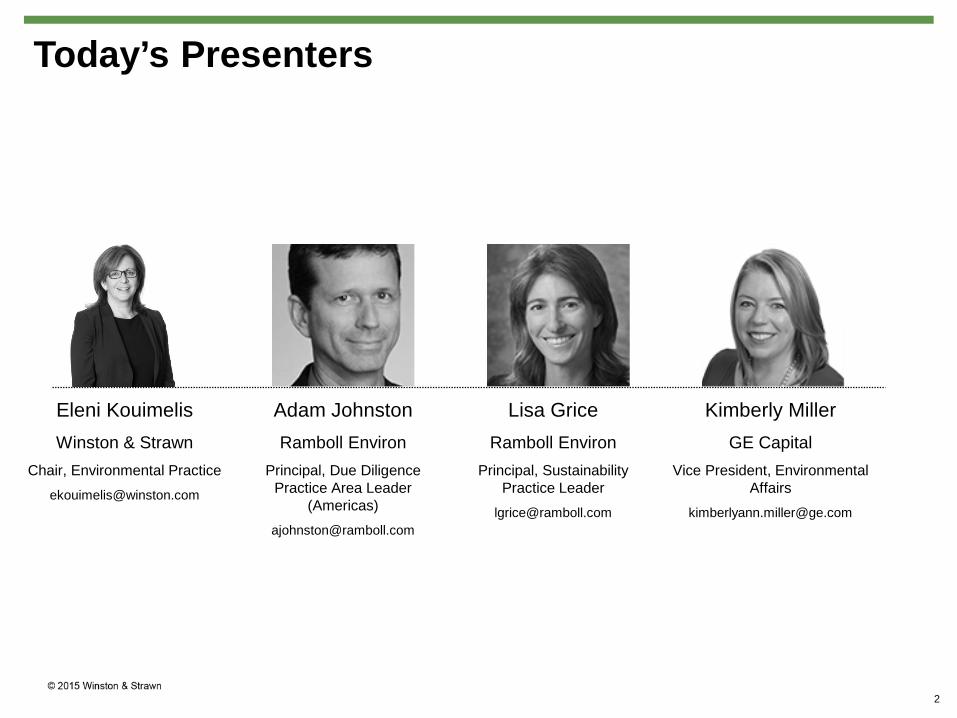

Today’s Presenters

Adam Johnston Ramboll Environ

Principal, Due Diligence Practice Area Leader

(Americas) [email protected]

Kimberly Miller GE Capital

Vice President, Environmental Affairs

Lisa Grice Ramboll Environ

Principal, Sustainability Practice Leader

Eleni Kouimelis Winston & Strawn

Chair, Environmental Practice [email protected]

2

3

WHAT IS ENVIRONMENTAL, SOCIAL AND GOVERNANCE EVALUATION?

• Often referred to as “ESG” or “sustainability” services

• Helps evaluate management of sustainability risks and opportunities in operations, supply chain and products

• Relates to a wide range of topics with the potential to affect a Company’s valuation and public perception

• Used to encompass criteria used in socially responsible investing

4

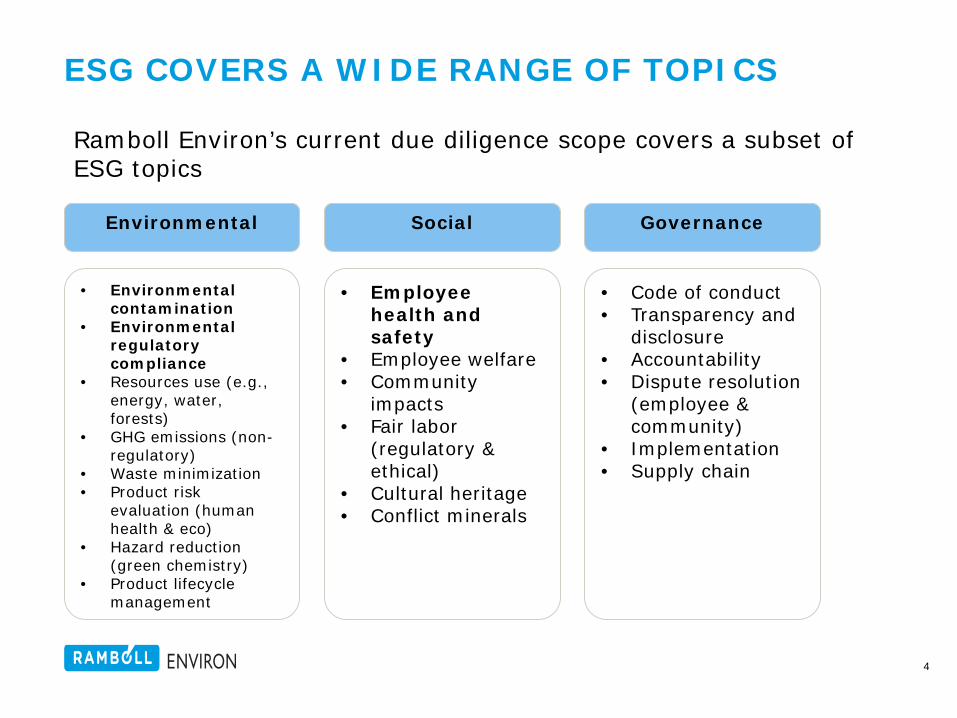

ESG COVERS A WIDE RANGE OF TOPICS

Environmental

• Environmental contamination

• Environmental regulatory compliance

• Resources use (e.g., energy, water, forests)

• GHG emissions (non-regulatory)

• Waste minimization • Product risk

evaluation (human health & eco)

• Hazard reduction (green chemistry)

• Product lifecycle management

• Employee health and safety

• Employee welfare • Community

impacts • Fair labor

(regulatory & ethical)

• Cultural heritage • Conflict minerals

• Code of conduct • Transparency and

disclosure • Accountability • Dispute resolution

(employee & community)

• Implementation • Supply chain

Social Governance

Ramboll Environ’s current due diligence scope covers a subset of ESG topics

5

ESG IN THE NEWS

“Tesla to Use North American Material Amid Pollution Worry” Bloomberg, March 31, 2014

“Target to increase minimum wage to $9 an hour, matching rivals WalMart and TJ Maxx” Reuters, March 19, 2015

“Mining company BHP Billiton to pay $25 million to settle SEC anti-bribery charges” Associated Press, May 20, 2015

“Danone Raises Mengniu Stake Amid China Food Safety Concerns” Bloomberg, February 12, 2014

“Indian officials order Coca-Cola plant to close for using too much water” The Guardian, June 18, 2014

6

ESG IN VALUE CREATION

Risk management

Business opportunities and competitive advantage

Government regulation

Corporate reputation and brand

Customer and investor demand

External pressures (e.g., NGOs)

Employee interests

7

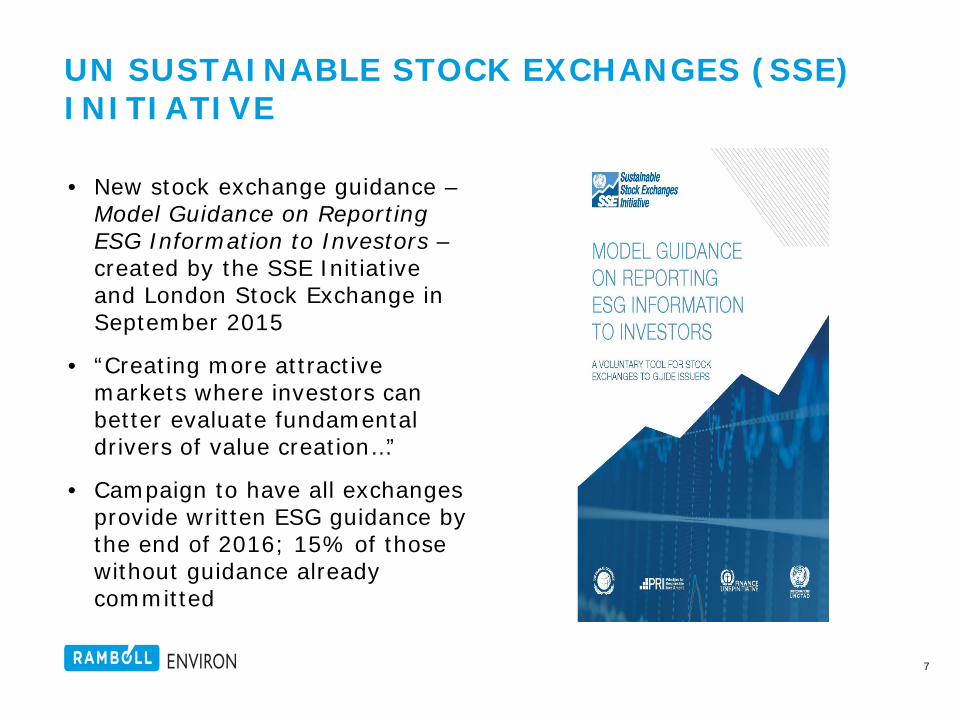

UN SUSTAINABLE STOCK EXCHANGES (SSE) INITIATIVE

• New stock exchange guidance – Model Guidance on Reporting ESG Information to Investors – created by the SSE Initiative and London Stock Exchange in September 2015

• “Creating more attractive markets where investors can better evaluate fundamental drivers of value creation…”

• Campaign to have all exchanges provide written ESG guidance by the end of 2016; 15% of those without guidance already committed

8

GROWING INTEREST IN ESG BY PRIVATE EQUITY FIRMS • Almost 90% of PE firms surveyed

in 2013 and 2014 said that they planned to increase their attention on ESG issues in the future, up from around 55% in 2012

Source: PitchBook 2015 survey

• 68% of those planning divestitures, mergers, or IPOs in the next year said they will evaluate ESG considerations

Source: PricewaterhouseCoopers 2013 survey

• There are more than 150 private equity signatories to the Principles for Responsible Investment (PRI)

Source: PricewaterhouseCoopers/UNPRI 2012 survey

Environmental, Social, and Governance Due Diligence • Deal context

• Fast paced and competitive process

• Identify and quantify material ESG liabilities • Negotiate and document risk allocation • Lenders requiring ESG reviews

9

Sustainability Reports

• “A sustainability report is an organizational report that gives information about economic, environmental, social and governance performance.” (Global Reporting Initiative (GRI) definition)

• The most widely adopted framework is the GRI Sustainability Reporting Framework

10

Sustainability Reporting Value Add

11

Issues With Sustainability Reporting

• Weak or unreasonable goals • Lack of or mismanaged data • Discounting feedback • Failure to follow guidelines • Under or over reporting • Thinking short-term • Inadvertent greenwashing

12

14

RAMBOLL ENVIRON’S SCREENING-LEVEL APPROACH TO ESG DUE DILIGENCE

Focus review on corporate-level awareness and written policies and plans 1 Target broadly applicable ESG topics (e.g., energy use, product stewardship), as well as sector-specific issues, as appropriate 2 Recognize importance of typical due diligence timeframes and budgets 3 Maintain flexibility to modify approach depending on the needs of the client and type of target 4

15

WHAT WE COVER: SECTOR-NEUTRAL ESG TOPICS

Environmental

• Environmental Management System (EMS)

• Energy and Greenhouse Gas (GHG) Management

• Water Use and Impact

• Biodiversity and Ecosystems

• Climate Risk and Resilience

• Waste and Materials Use

• Product Stewardship – Environmental Topics

• Human Capital/Employee Welfare

• Stakeholder Engagement

• Employee Health and Safety

• Human Rights • Product

Stewardship – Social Topics

• Ethics • Supply Chain • ESG Management

Framework • ESG/Sustainability

Reporting

Social Governance

In addition to those areas covered during a standard due diligence review, Ramboll Environ covers the following additional topics:

16

WHAT WE COVER: SECTOR-SPECIFIC ESG TOPICS

• Assessment also includes “sector-specific” ESG topics

• Sector-specific topics identified based on:

1) Ramboll Environ experience and professional judgment within the given industry

2) Publicly available information on industry-specific material topics

• Topics may overlap with sector-neutral ESG topics

17

EXAMPLE SECTOR-SPECIFIC ESG TOPICS: OIL & GAS EXPLORATION & PRODUCTION

Environmental

• Environmental Management System (EMS)

• Energy and Greenhouse Gas (GHG) Management

• Water Use and Impact

• Biodiversity and Ecosystems

• Climate Risk and Resilience

• Waste and Materials Use

• Product Stewardship – Environmental Topics

• Air Quality

• Human Capital/Employee Welfare

• Stakeholder Engagement/Community Relations

• Employee Health and Safety and Emergency Management

• Human Rights, Security and Rights of Indigenous Peoples

• Product Stewardship – Social Topics

• Business Ethics & Payments Transparency

• Supply Chain • ESG

Management Framework

• ESG/Sustainability Reporting

• Reserves Valuation & Capital Expenditures

Social Governance

Bolded items are those considered potentially material topics

18

EXAMPLE SECTOR-SPECIFIC ESG TOPICS: CHEMICALS MANUFACTURING

Environmental

• Environmental Management System (EMS)

• Energy, Feedstock Management, and Greenhouse Gas (GHG) Management

• Water Use and Impact • Biodiversity and Ecosystems • Climate Risk and Resilience • Waste and Materials Use • Product Stewardship of

Chemicals and GMOs • – Environmental Topics • Air Quality • Product Design for Use-

Phase Efficiency

• Human Capital/Employee Welfare

• Stakeholder Engagement

• Employee Health and Safety

• Human Rights • Product

Stewardship of Chemicals and GMOs – Social/Safety Topics

• Ethics • Supply Chain • ESG Management

Framework • ESG/Sustainability

Reporting • Political Spending

Social Governance

Bolded items are those considered potentially material topics

19

RAMBOLL ENVIRON ESG DUE DILIGENCE REVIEW PROCESS

Client dialogue Gather client’s expectations about most important ESG topics to cover

Written questionnaire Develop customized list of questions for sector-neutral and sector-specific ESG topics

Telephone interview Follow up on questionnaire responses with an interview of appropriate ESG corporate personnel

Document and database review Review ESG documents provided by Company and publically available databases

Report Summary of Company’s awareness and management of pertinent ESG topics

20

COMPARISON OF SCREENING LEVEL DD REVIEW TO FOCUSED ESG ASSESSMENT

Outcomes of Screening-Level Review • Multidisciplinary review of

Company’s involvement with 16+ ESG topics

• Corporate awareness of individual ESG topics and their relevance to Company operations

• Level of Company’s sophistication: Breadth of understanding across

multiple ESG topics

Depth of understanding within a given topic

Outcomes of Focused Assessment • Based on the results of the

screening-level review, assessment focuses on most pertinent and material ESG topics

• Where does the Company stand with respect to its competitors in the same industry (i.e., benchmarking)?

• Identification of potential risks and opportunities of material ESG areas

21

EXAMPLE POST-TRANSACTION SERVICES Ramboll Environ has a multidisciplinary team with the expertise to complete a focused review of individual ESG topics after the due diligence phase and recommend possible follow-up actions to mitigate risks and pursue opportunities

Examples of our capabilities to create value out of the identified risks and opportunities include:

• Develop strategies and tactics for specific sustainability/ESG topics; e.g. climate resilience plan, water risk assessments, product lifecycle assessment

• Complete operational efficiency inventories (greenhouse gas, energy, water, and/or waste), audits and improvement plans

• Develop meaningful supplier ESG surveys and plans

• Prepare or review sustainability reporting (per GRI, CDP, UNGC)

• Develop sustainability metrics, and data collection and tracking tools

• Create effective management systems for ESG/Sustainability

22

FOR MORE INFORMATION

Adam Johnston, Principal

Christine Ng, Manager

Lisa Grice, Principal

Kelly Guyton, Manager

User Perspective – Case Study

• Borrower: Garment designer and distributor

• U.S. Operations low risk – leased office and warehouses

• Manufacturing outsourced to 12, 3rd party manufacturers in China

• Pre Loan Diligence: – Desktop review of warehouse

locations – Review of Company “Supplier

Code of Conduct”

23

Situation

• Administrative Agent

• Distressed Debt/Restructuring

• Exploring potential to convert debt to equity

24

Pre Loan Diligence

• Desktop environmental review of warehouse locations

• Review of Supplier Code of Conduct

25

Supplier Code of Conduct

“ We audit our suppliers to ensure they comply with our Code of Conduct including sections on forced and child labor. Our auditing program evaluates all factories, and their subcontractors.”

26

CSR Diligence Scope of Work

CSR Audits were at 3 supplier locations. Selection Criteria:

• Mfg capacity largely dedicated to borrower manufacturing

• Supplier critical to continued operation

• Supplier was not used to manufacture “big name” garments

27

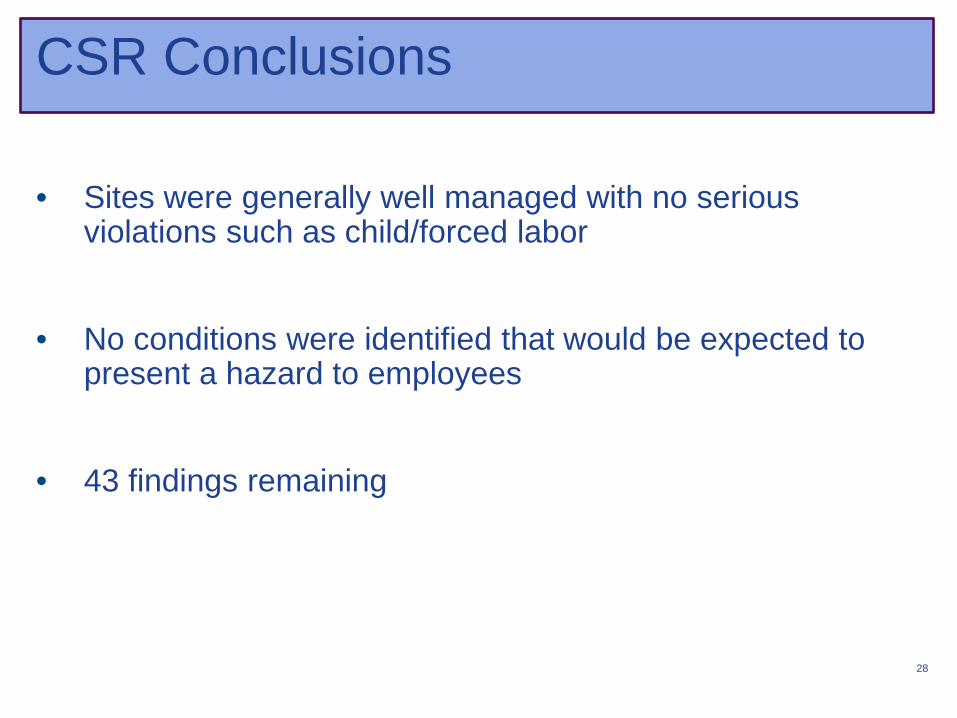

CSR Conclusions

• Sites were generally well managed with no serious violations such as child/forced labor

• No conditions were identified that would be expected to present a hazard to employees

• 43 findings remaining

28

CSR Conclusions – Priority Findings

1. Employees are not correctly compensated for all overtime in certain circumstances

2. Employees are paid “by the piece” instead of on an hourly basis at one supplier location

3.Certain permits relating to kitchen operations and other environmental/business operations were outstanding

29

Resolution of remaining findings

• GE shared the findings of the Environ review with company management

• Clauses related to management accountability for environmental matters and CSR reviews at 3rd party auditors were added to the shareholders agreement as a measure to ensure that management maintains CSR audit protocols going forward

30

Resolution of remaining findings

• GE shared the findings of the Environ review with company management

• Clauses related to management accountability for environmental matters and CSR reviews at 3rd party auditors were added to the shareholders agreement as a measure to ensure that management maintains CSR audit protocols going forward

31