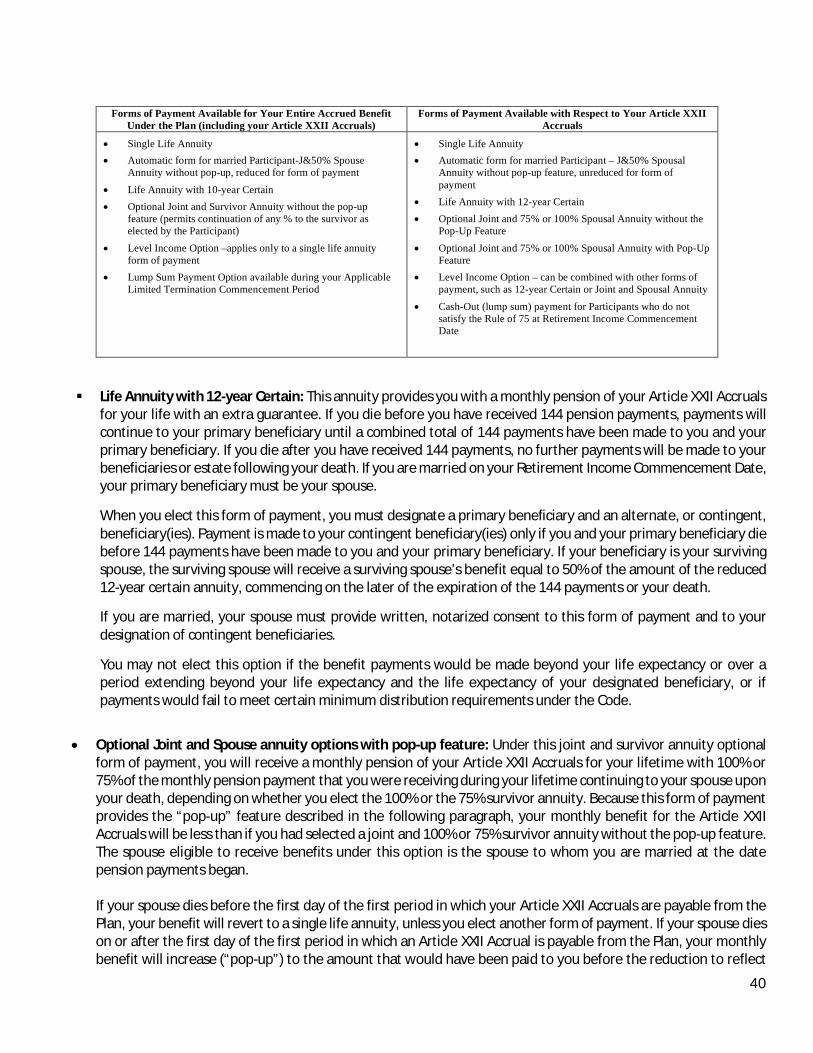

ENTERGY CORPORATION RETIREMENT PLAN

67

Effective July 1, 2021 Summary Plan Description ENTERGY CORPORATION RETIREMENT PLAN for Non-Bargaining Employees

Transcript of ENTERGY CORPORATION RETIREMENT PLAN

Effective July 1, 2021

Summary Plan Description

ENTERGY CORPORATIONRETIREMENT PLANfor Non-Bargaining Employees

i

This Summary Plan Description summarizes and explains in plain language key provisions of the Entergy CorporationRetirement Plan for Non-Bargaining Employees, as amended through June 30, 2021 (the “Plan”) and the benefits providedpursuant to the Plan for certain non-bargaining employees of the Participating Companies.

The Plan itself is more comprehensive and is written in more technical language to comply with federal law.

If you have any questions that this Summary Plan Description does not answer, you should read the Plan itself or contactthe Plan Administrator. See Section 16, ERISA Rights, beginning on page 61 regarding how you can get a copy or inspectthe Plan document. REMEMBER THAT THE PLAN ITSELF, AND NOT THE SUMMARY PLAN DESCRIPTION, IS WHATALWAYS CONTROLS YOUR BENEFITS.

The following information concerning the Plan is very important to you as a Plan Participant:

Plan Name: Entergy Corporation Retirement Plan forNon-Bargaining Employees

Plan Sponsor: Entergy Corporation

Corporate Address: 639 Loyola Avenue New Orleans, LA 70113

Employer I.D. No.: 72-1229752

Plan Administrator: Employee Benefits Committeec/o Entergy Corporation639 Loyola AvenueNew Orleans, LA 70113504-576-4000

Trustee: JP Morgan Chase Bank, N. A.One Chase Manhattan PlazaNew York, NY 10015

Company: Any System Company that adopts the Entergy Corporation Retirement Plan forNon-Bargaining Employees

Legal Agent: The person designated as the agent for service of legal process is the:

SecretaryEntergy Corporation639 Loyola AvenueNew Orleans, LA 70113

Legal process may also be made upon the Trustees or the Plan Administrator.

Plan Year: January 1 through December 31

Plan Number: 004

Participating Company: Any System Company that adopts the Entergy Corporation Retirement Plan forNon-Bargaining Employees. A complete list of the Participating Companies is available bycalling the Entergy Pension Resource Center at 1-855-523-3772 (toll free).

System Company: Entergy Corporation, any corporation 80 percent or more of whose stock (based on votingpower or value) is owned, directly or indirectly, by Entergy Corporation, and any partnershipor trade or business which is 80 percent or more controlled, directly or indirectly, by EntergyCorporation.

ii

TableofContentsSection 1: Introduction ....................................................................................................................................... 1

Section 2: Entering the Plan................................................................................................................................ 3Who Is Eligible ................................................................................................................................................. 3When You Join the Plan ................................................................................................................................... 3

Section 3: Service ............................................................................................................................................... 4Benefit Service ................................................................................................................................................. 4Vesting Service ................................................................................................................................................ 4Service If You Become Disabled....................................................................................................................... 5Break in Service ............................................................................................................................................... 5Leave of Absence Rules ................................................................................................................................... 6

Section 4: Transfers & Reemployment ................................................................................................................ 7Transfer from Covered Employment ................................................................................................................. 7Transfer to Covered Employment ..................................................................................................................... 7

Section 5: When You Can Retire ......................................................................................................................... 8Normal Retirement Date ................................................................................................................................... 8Early Retirement Date ...................................................................................................................................... 8Deferred Retirement Date................................................................................................................................. 8

Section 6: How Your Pension is Calculated .......................................................................................................... 9Normal Retirement Pension .............................................................................................................................. 9Early Retirement Pension ............................................................................................................................... 10Deferred Retirement Pension ......................................................................................................................... 11Terminated Vested Pension ........................................................................................................................... 12Deferring Commencement of Your Pension .................................................................................................... 13Grandfathered Benefits .................................................................................................................................. 13Service under Prior Employer’s Plan............................................................................................................... 14Earnings ......................................................................................................................................................... 14Suspension of Benefits ................................................................................................................................... 15

Section 7: How Your Pension Will Be Paid ......................................................................................................... 17Normal Payment Method ................................................................................................................................ 17Spousal Consent Requirements ..................................................................................................................... 17Optional Payment Methods ............................................................................................................................ 18Small Amount Lump-Sum Payments .............................................................................................................. 20Limited Termination Commencement Period .................................................................................................. 21How to Commence Your Pension ................................................................................................................... 23When Your Pension Will Be Paid .................................................................................................................... 26

Section 8: Survivor Benefits .............................................................................................................................. 27Pre-Retirement Spouse’s Death Benefit.......................................................................................................... 27Commencement at Normal Retirement Date................................................................................................... 27Commencement at Early Retirement Date ...................................................................................................... 27If Death Occurs After Early Retirement Eligibility ............................................................................................. 28Commencement During Applicable LTC Period .............................................................................................. 28

iii

Payment of the Pre-Retirement Spouse’s Death Benefit ................................................................................. 28

Section 9: Grandfathered Benefits and Options for Gulf States Utilities Company Employees’ TrusteedRetirement Plan Participants ............................................................................................................................ 29

Normal Retirement Pension ............................................................................................................................ 29Early Retirement Pension ............................................................................................................................... 30Vested Pension .............................................................................................................................................. 30Disability Retirement Benefits ......................................................................................................................... 31Pop-Up Provision ........................................................................................................................................... 32

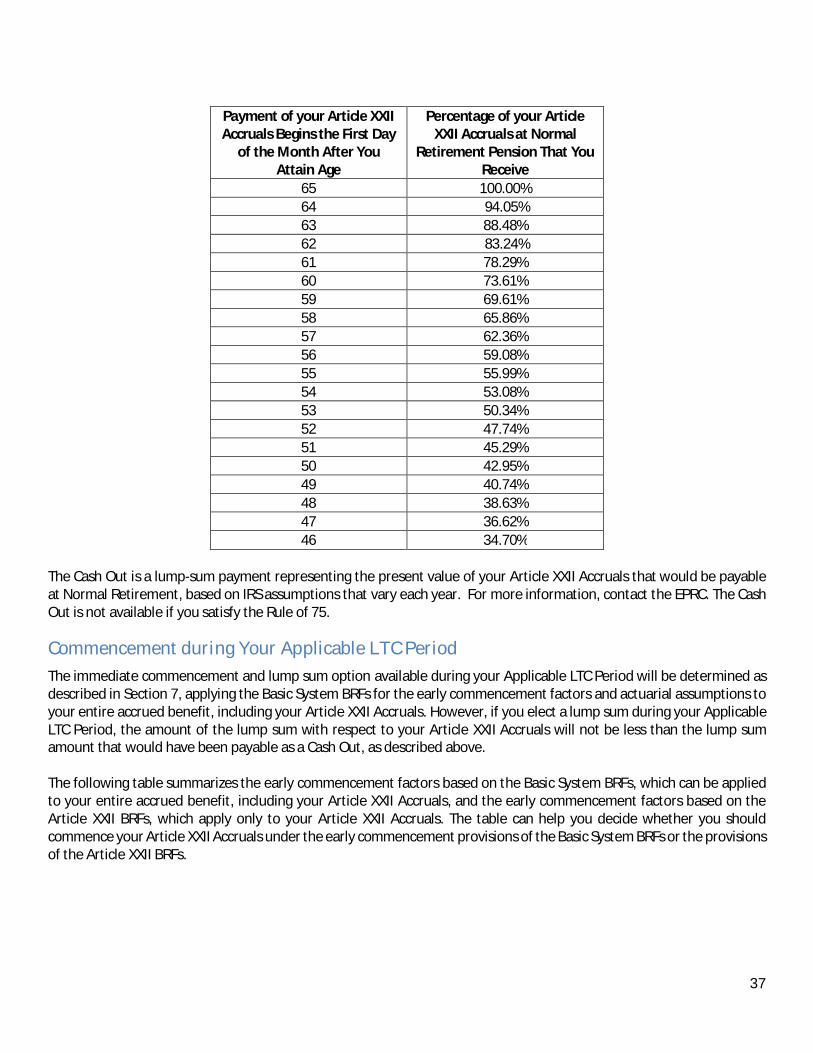

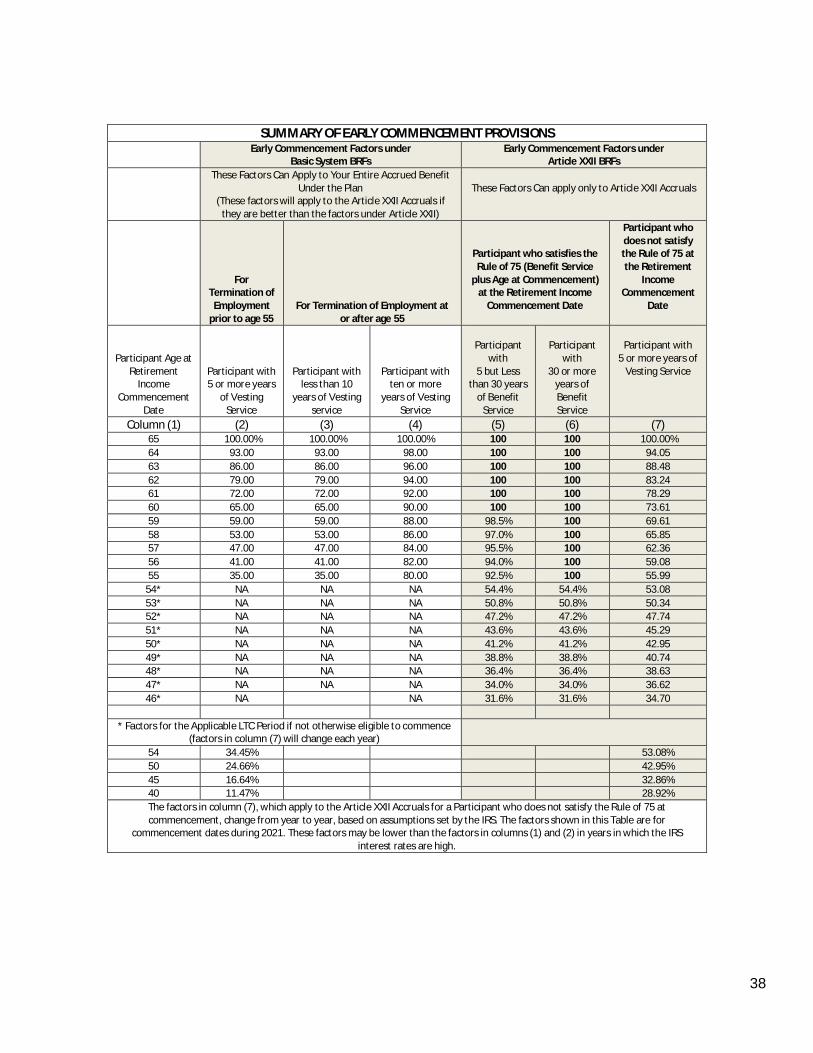

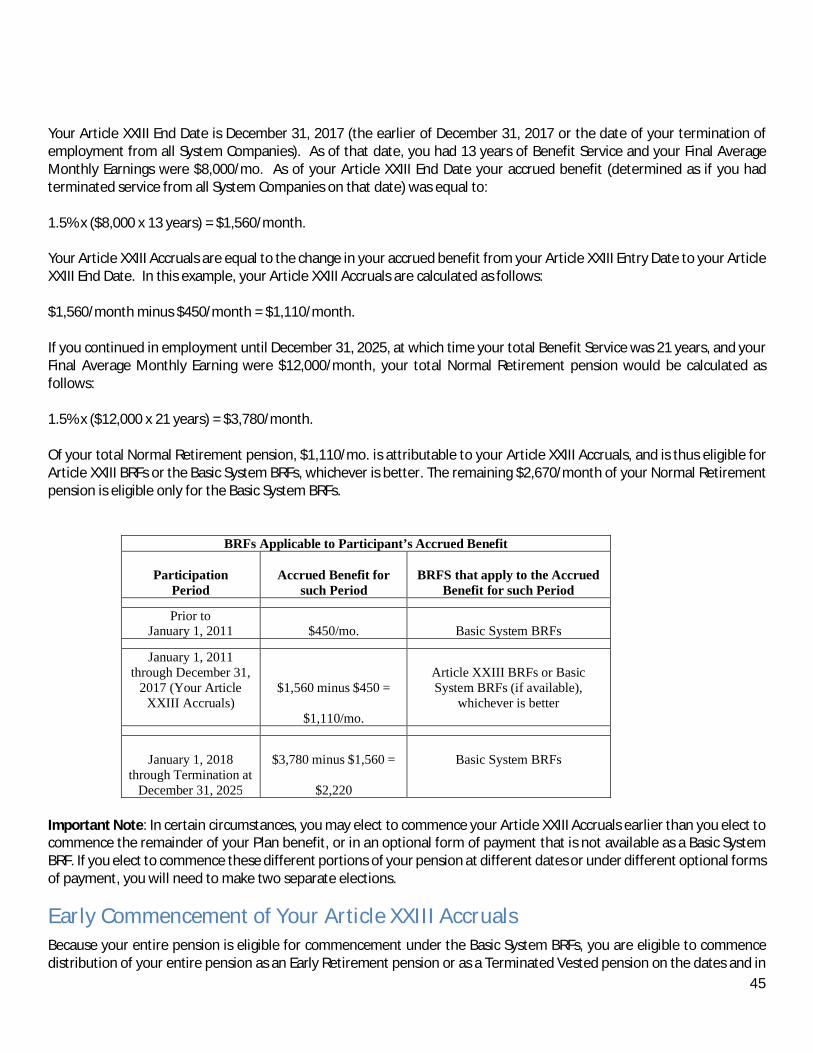

Section 10: Special Provisions For Article XXII Participants .............................................................................. 33Normal Retirement Pension – Your Article XXII Accruals ................................................................................ 33Early Commencement of Your Article XXII Accruals ....................................................................................... 35Disability Retirement Benefits ......................................................................................................................... 39Optional Forms of Payment ............................................................................................................................ 39Survivor Benefits ............................................................................................................................................ 42

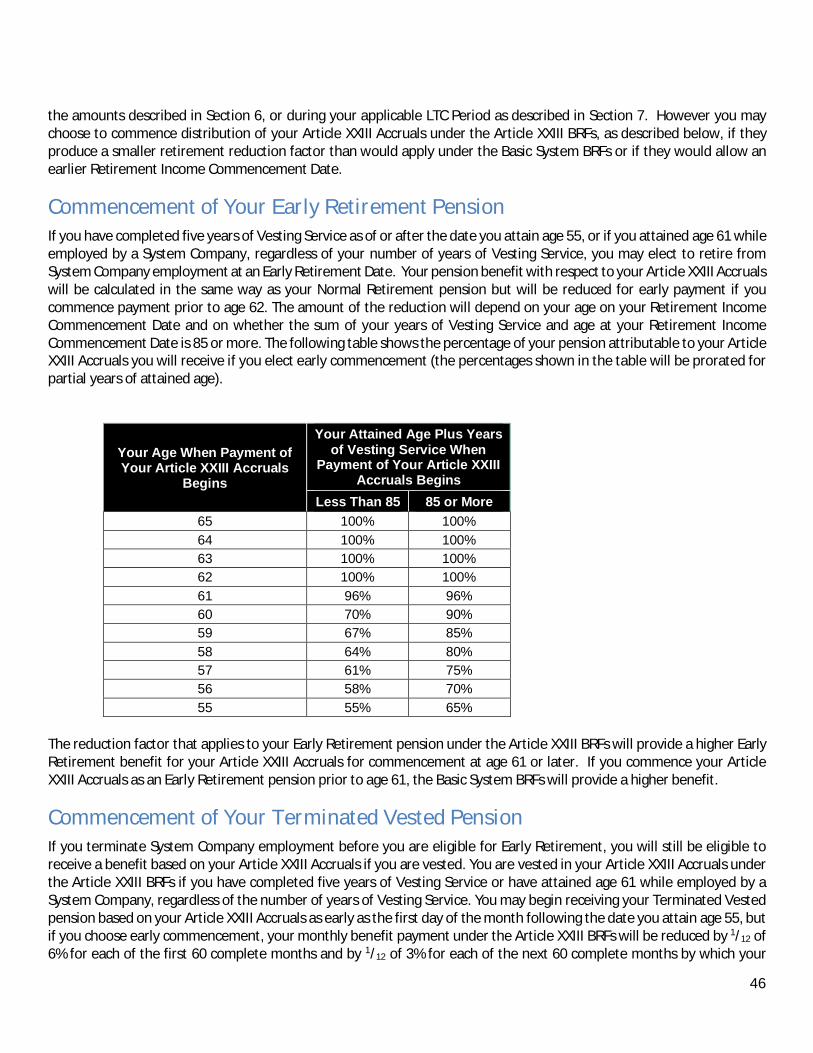

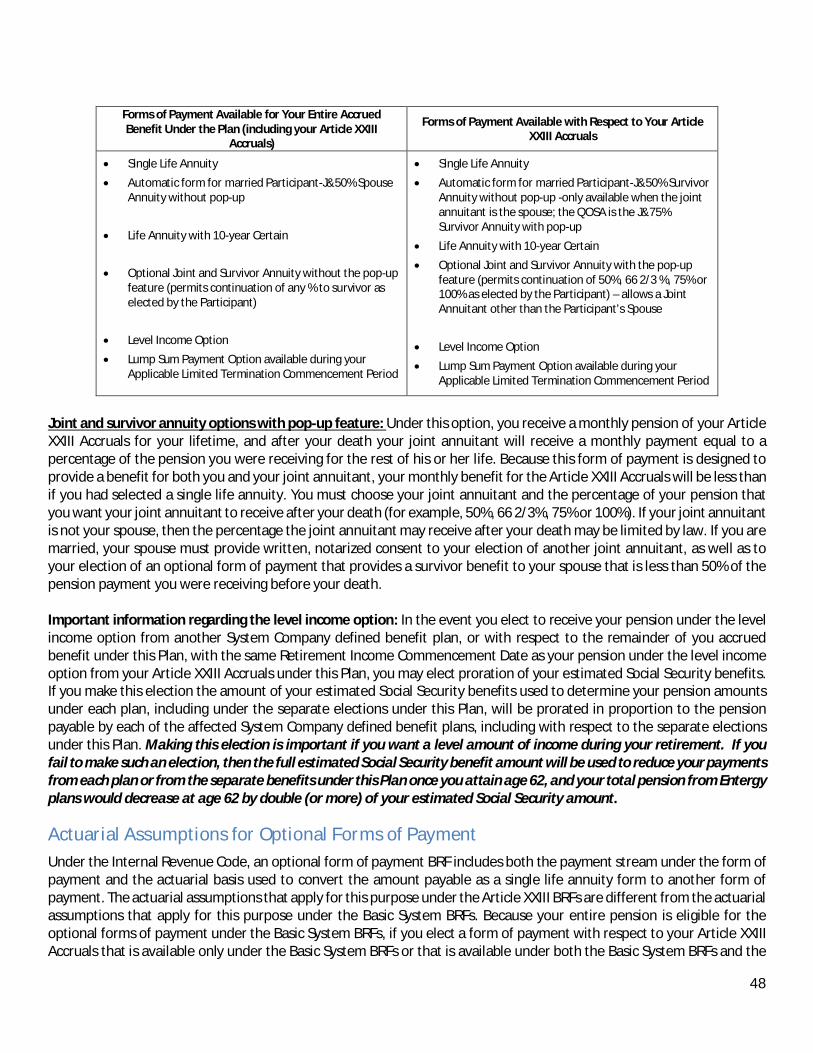

Section 11: Special Provisions for Article XXIII Participants .............................................................................. 44Normal Retirement Pension – Your Article XXIII Accruals ............................................................................... 44Early Commencement of Your Article XXIII Accruals ...................................................................................... 45Commencement of Your Early Retirement Pension ........................................................................................ 46Commencement of Your Terminated Vested Pension ..................................................................................... 46Commencement during the Applicable LTC Period ......................................................................................... 47Deferred Commencement of Your Article XXIII Accruals ................................................................................. 47Optional Forms of Payment ............................................................................................................................ 47Survivor Benefits ............................................................................................................................................ 49

Section 12: Claims for Benefits ......................................................................................................................... 50Requesting Benefits ....................................................................................................................................... 50If a Request Is Denied – Non-Disability Claims ............................................................................................ 50Additional Procedures for Disability Claims .................................................................................................. 51Special Timing Rules for Disability Claims ................................................................................................... 51Denial of Disability Claim .............................................................................................................................. 52Appeal Following Denial of Disability Claim ................................................................................................. 53Final Authority of Claims Appeal Administrator ............................................................................................ 53Mailing Address for All Claims and Appeals ................................................................................................. 54Importance of Exhausting Administrative Remedies........................................................................................ 54Time to File Suit ............................................................................................................................................. 54

Section 13: Plan Insurance ................................................................................................................................ 55

Section 14: Loss of Benefits .............................................................................................................................. 56

Section 15: Other Provisions ............................................................................................................................ 58Post-Retirement Medical Benefits ................................................................................................................... 58Plan Amendment or Termination .................................................................................................................... 58Assignment of Benefits ................................................................................................................................... 58Employment Rights ........................................................................................................................................ 58Guarantees under the Plan ............................................................................................................................. 58Mergers, Consolidations or Transfers ............................................................................................................. 59

iv

Maximum Retirement Benefits ........................................................................................................................ 59Top-Heavy Provisions .................................................................................................................................... 59Right to Recover Excess Payments ................................................................................................................ 59Duty to Furnish Information and Documents ................................................................................................... 59Plan Cost and Trust Fund ............................................................................................................................... 59Plan Sponsor and Plan Administrator ............................................................................................................. 60Administration Agent ...................................................................................................................................... 60

Section 16: ERlSA Rights ................................................................................................................................... 61ERISA Rights ................................................................................................................................................. 61Conflict with the Plan and/or Trust .................................................................................................................. 62

1

1

Section1:IntroductionThis booklet summarizes and explains in plain language the key provisions of the Entergy Corporation Retirement Planfor Non-Bargaining Employees, as amended through June 30, 2021 (the “Plan”) and describes how the Plan operates.Whenever this Summary Plan Description refers to “the Plan,” the reference is to the Entergy Corporation RetirementPlan for Non-Bargaining Employees. References in lower case to “the plan” mean a different plan.

In addition, this Summary Plan Description explains the determination of benefits under the Plan on or after July 1, 2021.If you stopped working as an eligible non-bargaining employee for a Participating Company before July 1, 2021 and donot return to employment as an eligible non-bargaining employee of a System Company employer, the provisions of thePlan in effect at the time you stopped working will apply for the determination of your benefit. Those provisions aredescribed in the Summary Plan Description, including any Summaries of Material Modifications, in effect at the time youractive participation in the Plan ended.

Certain groups of employees have special grandfathered benefits, including minimum benefit provisions or certain specialbenefits, rights and features. Those employees were previously provided with Summary Plan Descriptions describing theprovisions applicable to their group. Please refer to “Grandfathered Benefits” on page 13 of this Summary Plan Descriptionor call the Entergy Pension Resource Center (“EPRC”) to determine if you belong to a group of employees that is entitledto a grandfathered benefit. In addition, a small group of Participants, referred to in this Summary Plan Description asArticle XXII or Article XXIII Participants, are entitled to certain special benefits, rights and features, described in Sections10 and 11, with respect to a portion of their benefits under the Plan. These Article XXII and Article XXIII Participants arenamed in the Plan as part of a Compliance Statement received from the Internal Revenue Service (“IRS”). All Article XXIIand Article XXIII Participants were previously notified of their designation in the Plan as an Article XXII Participant or anArticle XXIII Participant, as applicable, and were provided with information regarding these special benefits, rights andfeatures.

If there is an inconsistency or conflict between this Summary Plan Description and the formal Plan document, or anyomission from or ambiguity in the terms of the Summary Plan Description, the Plan document will control.

Here are some highlights of the Plan:

§ You are not required to contribute to the Plan in order to participate.

§ You are 100% vested in your benefit under the Plan after five years of Vesting Service with any SystemCompany or, if earlier, at the time you attain age 65 while employed by a System Company.

§ Your pension usually begins when you attain age 65, but you may begin receiving a reduced pension as earlyas age 55 (or in some cases, as early as age 50 with respect to certain frozen grandfathered benefits).

§ If you terminate employment with all System Companies after December 31, 2017 you may elect to beginreceiving a reduced pension on a commencement date that is within the Limited Termination CommencementPeriod that applies to you (“ Applicable LTC Period “) which may be earlier than age 55. You may also elect tohave your pension paid as a lump sum, if your termination occurs after December 31, 2017 and yourcommencement date is during your Applicable LTC Period. Your Applicable LTC Period extends from the dayafter your termination of employment to the 1st day of the 12th month following the first day of the calendarmonth immediately following your termination date. See “Limited Termination Commencement Period” inSection 7.

2

2

§ Your spouse will receive a part of your pension if you die after you are vested and before pension paymentscommence, even if you no longer work for a Participating Company. Benefits available to your spouse afterpension payments commence will depend on the form of payment you selected for your pension at the timeyou commenced pension payments. In accordance with federal law, your “spouse” for all Plan purposes isdefined as the person to whom you are lawfully married under applicable law.

If you have any questions about the Plan, please contact the EPRC for more information.

ResourcesWhen you have questions or need assistance, you can contact the EPRC in one of the following ways:

Resource How to Contact

Entergy PensionResource Center

Contact the EntergyPension ResourceCenter when:

You have questionsabout your benefits.

You want to apply tocommence yourpension.

Online

http://digital.alight.com/entergy

Phone

1-855-523-3772

For the hearing impaired, TDD: Contact your local telephone service provider whowill contact the EPRC to assist with communication.

Fax

1-847-554-1792

U.S Mail

Entergy Pension Resource CenterDept 03207PO Box 64117The Woodlands TX 77387-4117

Overnight Mail

Entergy Pension Resource CenterDept 032078770 New Trails DriveThe Woodlands TX 77381

3

3

Section2:EnteringthePlan

Who Is EligibleYou are eligible to participate in the Plan if you meet all of the following requirements:

§ You are employed by a Participating Company,

§ You are not covered by a collective bargaining agreement,

§ Your most recent date of hire or rehire into System Company employment was prior to July 1, 2014, and

§ Prior to July 1, 2014, you were not excluded from participation in every System Company defined benefit plan.

Effective July 1, 2019, you will also be eligible to participate in the Plan if you are an Affected Plan III Employee. You arean Affected Plan III Employee if while you were a participant in Entergy Corporation Retirement Plan III (“Plan III”) youtransferred on or after March 1, 2019 from a position as an Employee of a System Company at Indian Point NuclearGenerating Unit 2 or Indian Point Nuclear Generating Unit 3 (collectively, "IPEC") to a position as a non-bargainingEmployee of a Participating Company at a work location other than IPEC. Your eligibility to participate in the Plan willbegin as of the date of your transfer, provided you meet the other requirements for eligibility, but not prior to July 1, 2019.

You are not eligible to participate in the Plan if you are classified by a System Company as a leased employee, independentcontractor or consultant, even if you are in fact a common-law employee of a System Company.

You are not eligible to accrue benefits under this Plan while you are accruing benefits under any other System Companydefined benefit plan, or if you are a “Retirement Contribution Eligible Employee” under the Savings Plan of EntergyCorporation and Subsidiaries VI or a “Defined Company Contribution Eligible Employee” under the Savings Plan of EntergyCorporation and Subsidiaries VII. You also are not eligible to participate in this Plan if you are eligible to participate in theSavings Plan of Entergy Corporation and Subsidiaries VIII or the Savings Plan of Entergy Corporation and Subsidiaries IX.

When You Join the Plan

You are eligible to participate in the Plan on the later of the date you attain age 21 or the date you become an eligiblenon-bargaining employee.

The terms “eligible employee” or “active Participant” as used in this Summary Plan Description mean an employee whocontinues to meet the eligibility requirements for participation in the Plan set forth above.

4

4

Section3:Service

Benefit ServiceBenefit Service is used to calculate your pension and is generally equal to the period in which you are an active Participantin the Plan. Benefit Service is counted in years, months and days and is earned while you are eligible to participate in thePlan. For Plan purposes, Benefit Service is limited to 40 years. It starts from the date you become a Participant and endson the earlier of (i) the date you are no longer an eligible employee because you transfer to a position not eligible underthe Plan, or (ii) your last day of employment. For Benefit Service purposes, your last day of employment is the earlier of:

§ The date you quit, are discharged or retire from all Participating Companies, or

§ The first anniversary of the first day you are absent from active employment with all Participating Companiesfor any reason.

Benefit Service may also include service you earned under a prior employer’s defined benefit plan. Please refer to thesections “Grandfathered Benefits” and “Service under Prior Employer’s Plan” beginning on page 13 of this Summary PlanDescription or call the EPRC to determine if this provision applies to you.

Benefit Service is also governed by the Break in Service, leave of absence and transfer rules.

Your Benefit Service will also include the period between your last day of employment and your rehire date if you arerehired by a Participating Company within 12 months of your last day of employment and the date of your rehire is priorto July 1, 2014.

Benefit Service shall also include the period of an approved leave of absence of up to two years, to the extent not alreadyincluded in the above determination.

Special rules apply if you were hired before July 1, 1976 and you were under age 30 at your date of hire, or if you werehired before 1985 and you were under age 25 at your date of hire.

In addition, any period of service during which you failed to make a contribution required by this Plan, by another SystemCompany defined benefit plan, or by any prior plan in which you participated is excluded from Benefit Service.

Vesting Service

Vesting Service determines whether you are entitled to a benefit under the Plan. Vesting Service is counted in years,months and days from your date of hire (or the date you reach age 18, if later) until your last day of employment with allSystem Companies. Vesting Service is also governed by the Break in Service, leave of absence and transfer rules. However,any period of service during which you failed to make a contribution required by this Plan, by another System Companydefined benefit plan, or by any prior plan in which you participated is excluded. You become vested in — that is, earn apermanent right to — your benefit under this Plan once you complete five years of Vesting Service with a System Company,or when you reach age 65 while employed by a System Company (whichever occurs first).

For purposes of determining your Vesting Service, your last day of employment is the earlier of:

§ The date you quit, are discharged or retire from System Company employment, or§ The first anniversary of the first day you are absent from active employment with a System Company for any

reason.

5

5

Your Vesting Service will also include the period between your last day of employment and your rehire date if you arerehired by a System Company within 12 months of your last day of employment. Vesting Service shall also include theperiod of an approved leave of absence of up to two years, to the extent not already included in the above determination.

Vesting Service may also include service you earned under a prior employer’s defined benefit plan. Vesting Service doesnot include service with a Reciprocating Company as described in Appendix G of Entergy Corporation Retirement Plan IIfor Non-Bargaining Employees or Entergy Corporation Retirement Plan IV for Bargaining Employees. Please refer to thesections “Grandfathered Benefits” and “Service under Prior Employer’s Plan” beginning on page 13 of this Summary PlanDescription or call the EPRC to determine if this provision applies to you.

Service If You Become Disabled

If you become disabled while working as an eligible employee for a Participating Company, your service will be affectedby whether you are receiving long term disability (“LTD”) benefits under the Entergy Corporation Companies’ Benefits PlusLong Term Disability Plan or any other Participating Company-sponsored long-term disability plan (collectively referred toas the “LTD Plan”).

If you are entitled to receive LTD benefits under the LTD Plan when you become permanently disabled, you may continueto earn Benefit Service and Vesting Service until the earliest of:

§ The date you commence your pension payments from the Plan,§ The last day of the month in which you cease to be eligible to receive an LTD benefit from the LTD Plan, or§ The date you die.

When you commence your pension, it will be based on all the Benefit Service (up to a maximum of 40 years) you earnedwhile you were an active employee and while you were receiving LTD Plan benefits from the LTD Plan.

If you elect to receive the grandfathered Disability Retirement Benefit described in Section 9, you will not accrue BenefitService under the Plan during the period in which you are receiving Disability Retirement Benefits, regardless of whetheror not you are receiving benefits from the LTD Plan. If you are an Article XXII Participant, you should refer to Section 10.

Break in Service

If you have a period of at least 12 consecutive months during which you are not paid or entitled to pay by a SystemCompany for an hour of service, you are considered to have a “Break in Service.” For purposes of determining whetheryou have a Break in Service, the 12 consecutive month period begins after the date that is treated as your last day ofemployment for determining Vesting Service. See the discussion under “Vesting Service” on page 4.

If you return to work with a System Company after a Break in Service:

§ Your prior Vesting Service and Benefit Service will be restored if:- You had a vested interest in your benefit under the Plan before your Break in Service, or- You had fewer than five consecutive one year Breaks in Service.

§ Your prior Vesting Service and Benefit Service will not be restored if:- You were not vested under the Plan, and- You were absent for five or more consecutive one year Breaks in Service.

6

6

Your “Break in Service” shall be determined in accordance with the Break in Service rules under the Plan or prior plans atthe time such Break in Service occurred. Also, you will not receive Vesting Service and Benefit Service for any period thathas not been restored under the Break in Service rules of any other System Company defined benefit plan in which youwere a participant.

If you had a Break in Service under a prior plan before January 1, 1976, as determined under the Break in Service rules ofsuch prior plan, you will not receive Vesting Service and Benefit Service for your period of employment before that Breakin Service.

Leave of Absence Rules

Breaks in Service will not begin while you are on an approved leave of absence of up to two years. (The period duringwhich you are receiving LTD benefits under the LTD Plan is not considered an approved leave of absence for this purpose.)

If you are away from work because of a maternity or paternity leave, the 12-consecutive month period beginning on thefirst anniversary of the first day of such leave will not constitute a Break in Service. For purposes of the Plan, maternity orpaternity leave includes time you are absent from work due to:

§ Pregnancy,§ The birth of your child,§ Placement of a child with you in connection with adoption, and/or

§ The care of your child immediately after birth or placement for adoption.

If you are absent from a Participating Company for a period of Qualified Service in the Uniformed Services of the UnitedStates, as defined in the Uniformed Services Employment and Reemployment Rights Act of 1994 (USERRA), and you returnto employment with a Participating Company within the time limit following such service, as prescribed under USERRA,you may be entitled to certain rights and protections concerning Plan benefits and service credit. Contact the EPRC formore information.

7

7

Section4:Transfers&Reemployment

Transfer from Covered EmploymentIf you are an active Participant in the Plan and you transfer from covered employment to a position in which you are nolonger an eligible employee under the Plan (for example, because of a transfer to another System Company, a bargainingposition, or a non-bargaining position not eligible under the Plan) or for any other reason you no longer meet all of theeligibility requirements described in Section 2 for coverage under the Plan, the Earnings used to calculate your benefitswill be frozen as of your date of transfer or the date you no longer meet the eligibility requirements for coverage underthe Plan, and you will no longer accrue years of Benefit Service under the Plan following the transfer. You are eligible tocontinue to accrue Vesting Service after your transfer date, as long as you remain employed by a System Company.

Transfer to Covered EmploymentIf after transferring from covered employment under the Plan, you subsequently return to covered employment, or if youhave not previously been an active Participant in the Plan and you transfer to a position covered by the Plan or you wererehired into employment covered by the Plan before July 1, 2014, you will be covered by the Plan features described inthis Summary Plan Description if you meet all of the eligibility requirements described in Section 2. The following ruleswill apply in determining your benefits under the Plan:

§ Your prior service with a System Company will be included in the determination of Vesting Service under thePlan, using the rules of this Plan, and

§ Your service and earnings that were earned during a period in which you were an employee of a SystemCompany and an active participant in another System Company defined benefit plan prior to your transfer orreemployment may be included in the determination of Benefit Service and Earnings under this Plan, usingthe rules of this Plan (as if you were a Participant in this Plan during those prior years of participation inanother Entergy plan).

Your benefit under the Plan will be offset by any benefits earned prior to your transfer or reemployment, based on rulesdescribed in the Plan.

Under the transfer and reemployment rules outlined above, you will not receive more than a total of one year of VestingService and/or Benefit Service under all plans, including this Plan during any one year of employment service. In addition,the definition of earnings and benefit service may differ among System Company defined benefit plans and this may affectthe way your benefit is calculated. Vesting Service and/or Benefit Service taken into account for a former employee whobegins employment covered by the Plan will reflect the Break in Service rules of this Plan for such services performedwhile an active Participant in this Plan and the break in service rules of the other System Company defined benefit plansin which such employee formerly participated for the services performed while an active participant in the other SystemCompany defined benefit plans.

Under the Plan, certain exceptions may apply to the recognition of earnings and prior service. If you have any questionsabout transfers or reemployment and the impact to your benefit, please contact the EPRC.

8

8

Section5:WhenYouCanRetireThere are three types of retirement under the Plan: normal, early and deferred retirement. Each type of retirement isbased on your age and the circumstances of your retirement.

Please note that to be eligible for retiree coverage under Entergy’s employee health and welfare plans (the EntergyCorporation Companies’ Benefits Plus Medical, Dental, Vision and Life Insurance Plans and the Entergy CorporationCompanies’ Retiree Health Plan), you must satisfy all of the eligibility requirements for “eligible retired participants” andretiree coverage in the applicable Entergy employee health and welfare plans, including retiring directly from employmentwith a System Company and immediately commencing your pension under this Plan. For questions about eligibilityrequirements for retiree health and welfare coverage, you must contact Employee Support Center at 1-844-ETR-WORK(844-387-9675). Entergy has the right in its sole discretion to amend or terminate retiree health and welfare benefits atany time. Failure to meet the eligibility requirements for retiree health and welfare coverage does not impact your abilityto begin receiving your pension under the Plan on any of the dates outlined below.

If you terminate employment from all System Companies after December 31, 2017, you should also be aware of theLimited Termination Commencement Period (“LTC Period”) provision, under which you are permitted to commence yourpension prior to age 55, and to elect payment of your pension in a lump sum instead of an annuity form of payment. Totake advantage of the LTC Period provision of the Plan, you must commence your pension no later than the end of yourApplicable LTC Period. Your Applicable LTC Period extends from the day after your termination of employment to the 1st

day of the 12th month following the first day of the calendar month immediately following your termination date. See“Limited Termination Commencement Period” in Section 7.

Normal Retirement DateYour Normal Retirement Date is the day you attain age 65. You are entitled to your Normal Retirement pensioncommencing on the first day of the month following your Normal Retirement Date. If you wish, you may defercommencement of your pension. See “Deferring Commencement of Your Pension” beginning on page 13.

Early Retirement DateIf you have completed 10 years of Vesting Service as of or after the date you attain age 55, you may elect to retire fromSystem Company employment at an Early Retirement Date. You may request that your pension commence on the firstday of any month after reaching your Early Retirement Date; however, your pension will be reduced for paymentscommencing before your Normal Retirement Date. If you wish, you may defer commencement of your pension. See“Deferring Commencement of Your Pension” beginning on page 13.

If you were a participant in the Gulf States Utilities Company Employees’ Trusteed Retirement Plan and you have at least10 years credited service at your termination of employment date, you may retire as early as age 50 if you meet certainrequirements. Refer to Section 9 for more information regarding these requirements. If you are an Article XXII or XXIIIParticipant, you should refer to Section 10 or Section 11, as applicable.

Deferred Retirement DateIf you continue to work past age 65 you will continue to accrue benefits based on the Plan’s benefit formula, as long asyou continue to satisfy the eligibility requirements outlined in Section 2. Your Deferred Retirement pension will commenceon the first day of the month following your termination of employment from all System Companies, unless you elect todefer commencement. See “Deferring Commencement of Your Pension” beginning on page 13 for more information.

9

9

Section6:HowYourPensionisCalculatedThis Plan is a defined benefit plan. This means your monthly pension is calculated under a definite formula. The amountcalculated under the formula is based on a single life annuity. All pensions payable under the Plan, and the forms ofpensions payable under certain circumstances, are subject to certain limits established by the Internal Revenue Code (the“Code”).

Normal Retirement PensionYour monthly pension at your Normal Retirement Date is calculated as follows:

1.5% x Final Average Monthly Earnings x Benefit Service (up to 40 years).

If you are an Affected Plan III Employee, your Normal Retirement pension will be the greater of: (i) the amountcalculated under the above formula, including both your prior Entergy service and your post-transfer service under thisPlan, or (ii) the amount calculated by adding your Normal Retirement pension earned under Plan III to the NormalRetirement pension calculated under the above formula taking into account only your post-transfer service.

If you are an Article XXII or XXIII Participant, you should refer to Section 10 or Section 11, as applicable.

Final Average Monthly EarningsIf your employment date (or your adjusted hire date, if later) with a System Company is prior to May 1, 2002 and you wereemployed by Entergy Arkansas, Inc. or its successor entity, Entergy Arkansas LLC, or Entergy Operations, Inc. at ArkansasNuclear One on or after May 1, 2002, your Final Average Monthly Earnings is the average of your monthly Earnings for the60 months in which your Earnings were the highest during the 120 months immediately before the earliest of:

§ Your retirement from, or termination of employment with Entergy Arkansas, Inc. or its successor entity,Entergy Arkansas, LLC, or Entergy Operations, Inc. at Arkansas Nuclear One,

§ Your death, or

§ The date you are no longer eligible to be an active Participant in the Plan.

If the conditions described above apply and you have less than 60 months of earnings, your Final Average Monthly Earningsis the average of your monthly Earnings for all months during your total period of service.

If the conditions described above do not apply, then your Final Average Monthly Earnings is the average of your monthlyEarnings for the 60 consecutive months in which your Earnings were the highest during the last 120 months immediatelybefore the earliest of:

§ Your retirement from, or termination of employment with, a Participating Company,

§ Your death, or

§ The date you are no longer eligible to actively participate in the Plan.

If you worked less than 60 months, your Final Average Monthly Earnings is the average of your monthly Earnings for yourtotal period of service.

In computing your Final Average Monthly Earnings, no more than 10 three-pay-period months will be included in any 60-month period. In addition, no more than five annual bonuses and associated supplemental payments, or if paid morefrequently, the equivalent of five annual bonuses and associated supplemental payments, will be included in any 60-month period.

10

10

Special rules apply if you are disabled for at least 120 months immediately prior to your Retirement IncomeCommencement Date.

In addition, your Earnings will be equal to $0 for each month in which you are absent from employment and are not paidby a System Company, if such months are not during a Break in Service. If you do incur a Break in Service, the monthsduring the Break in Service will not be included in the calculation of your Final Average Monthly Earnings.

The pension computed under this formula is reduced by the amount of any pension that you may have earned under anyother qualified defined benefit plan of a System Company prior to your becoming an active Participant in the Plan.

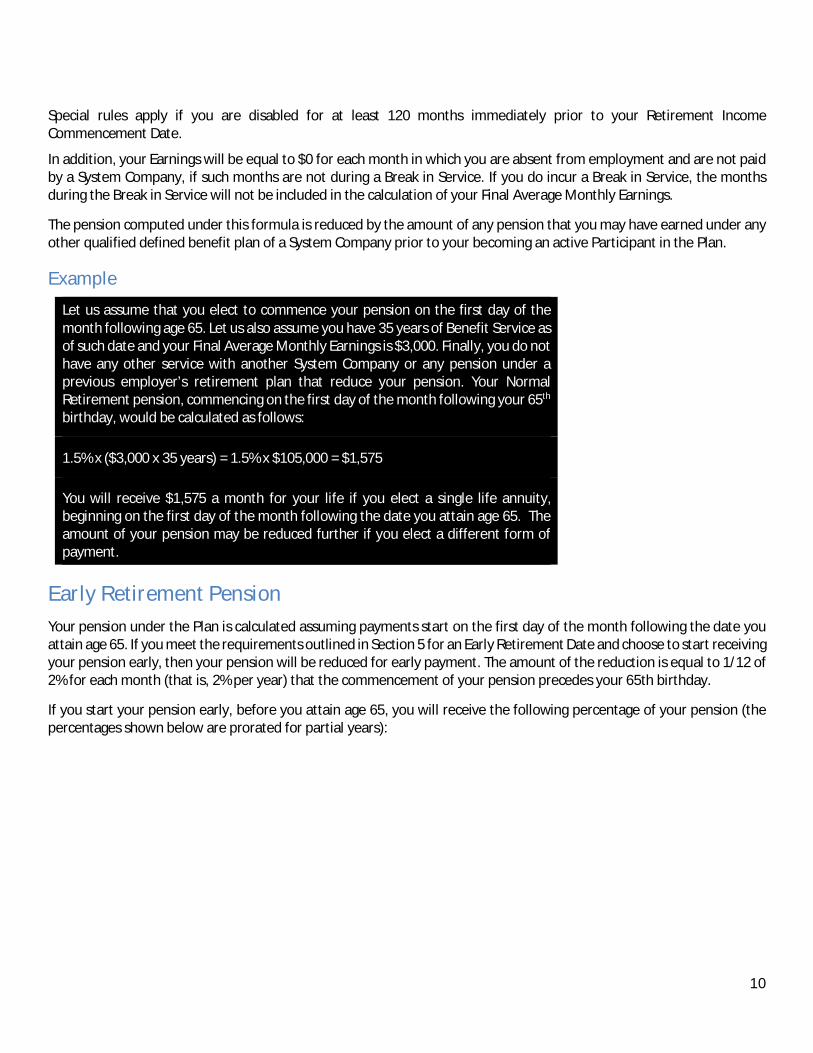

ExampleLet us assume that you elect to commence your pension on the first day of themonth following age 65. Let us also assume you have 35 years of Benefit Service asof such date and your Final Average Monthly Earnings is $3,000. Finally, you do nothave any other service with another System Company or any pension under aprevious employer’s retirement plan that reduce your pension. Your NormalRetirement pension, commencing on the first day of the month following your 65th

birthday, would be calculated as follows:

1.5% x ($3,000 x 35 years) = 1.5% x $105,000 = $1,575

You will receive $1,575 a month for your life if you elect a single life annuity,beginning on the first day of the month following the date you attain age 65. Theamount of your pension may be reduced further if you elect a different form ofpayment.

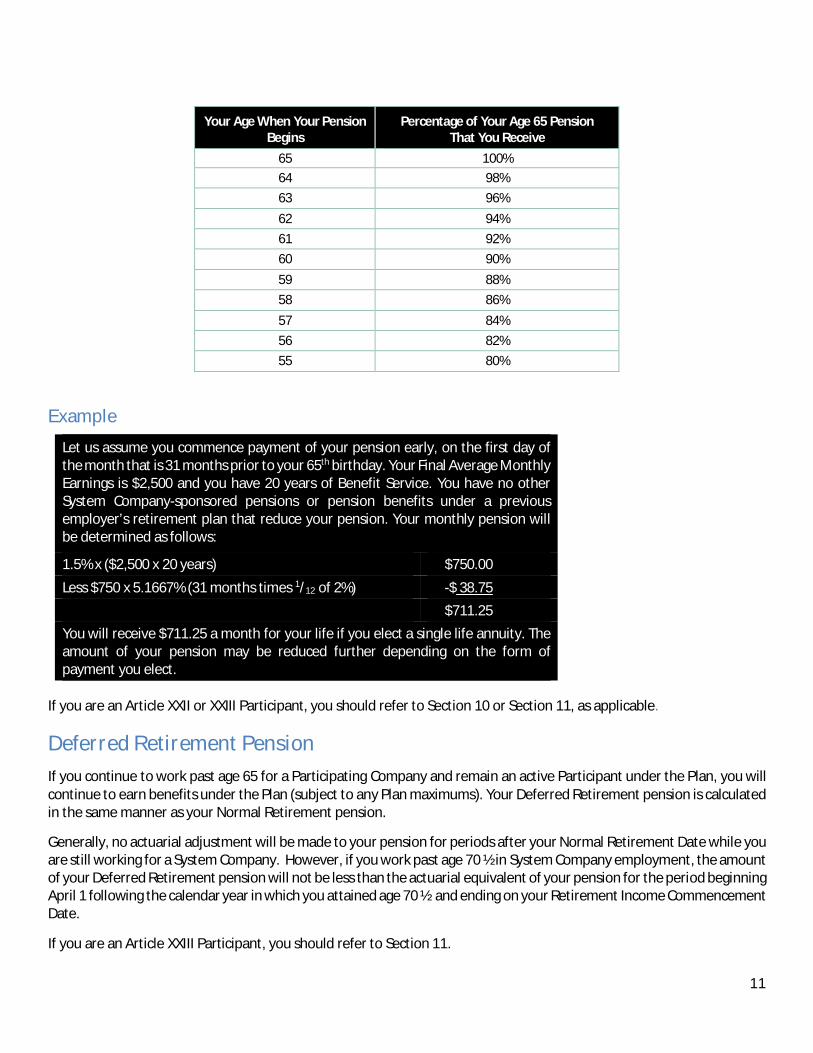

Early Retirement PensionYour pension under the Plan is calculated assuming payments start on the first day of the month following the date youattain age 65. If you meet the requirements outlined in Section 5 for an Early Retirement Date and choose to start receivingyour pension early, then your pension will be reduced for early payment. The amount of the reduction is equal to 1/12 of2% for each month (that is, 2% per year) that the commencement of your pension precedes your 65th birthday.

If you start your pension early, before you attain age 65, you will receive the following percentage of your pension (thepercentages shown below are prorated for partial years):

11

11

Your Age When Your PensionBegins

Percentage of Your Age 65 PensionThat You Receive

65 100%64 98%63 96%62 94%61 92%60 90%59 88%58 86%57 84%56 82%55 80%

ExampleLet us assume you commence payment of your pension early, on the first day ofthe month that is 31 months prior to your 65th birthday. Your Final Average MonthlyEarnings is $2,500 and you have 20 years of Benefit Service. You have no otherSystem Company-sponsored pensions or pension benefits under a previousemployer’s retirement plan that reduce your pension. Your monthly pension willbe determined as follows:

1.5% x ($2,500 x 20 years) $750.00

Less $750 x 5.1667% (31 months times 1/12 of 2%) -$ 38.75$711.25

You will receive $711.25 a month for your life if you elect a single life annuity. Theamount of your pension may be reduced further depending on the form ofpayment you elect.

If you are an Article XXII or XXIII Participant, you should refer to Section 10 or Section 11, as applicable.

Deferred Retirement PensionIf you continue to work past age 65 for a Participating Company and remain an active Participant under the Plan, you willcontinue to earn benefits under the Plan (subject to any Plan maximums). Your Deferred Retirement pension is calculatedin the same manner as your Normal Retirement pension.

Generally, no actuarial adjustment will be made to your pension for periods after your Normal Retirement Date while youare still working for a System Company. However, if you work past age 70 ½ in System Company employment, the amountof your Deferred Retirement pension will not be less than the actuarial equivalent of your pension for the period beginningApril 1 following the calendar year in which you attained age 70 ½ and ending on your Retirement Income CommencementDate.

If you are an Article XXIII Participant, you should refer to Section 11.

12

12

You may elect to commence your Deferred Retirement pension on the first day of the month following your terminationof employment from all System Companies. If you wish, you may elect to defer commencement of your pension. See“Deferring Commencement of Your Pension” beginning on page 13. Keep in mind that if you defer commencement beyondthe end of your Applicable LTC Period, you will permanently lose your eligibility for the lump sum option under the Plan.See “Limited Termination Commencement Period” in Section 7.

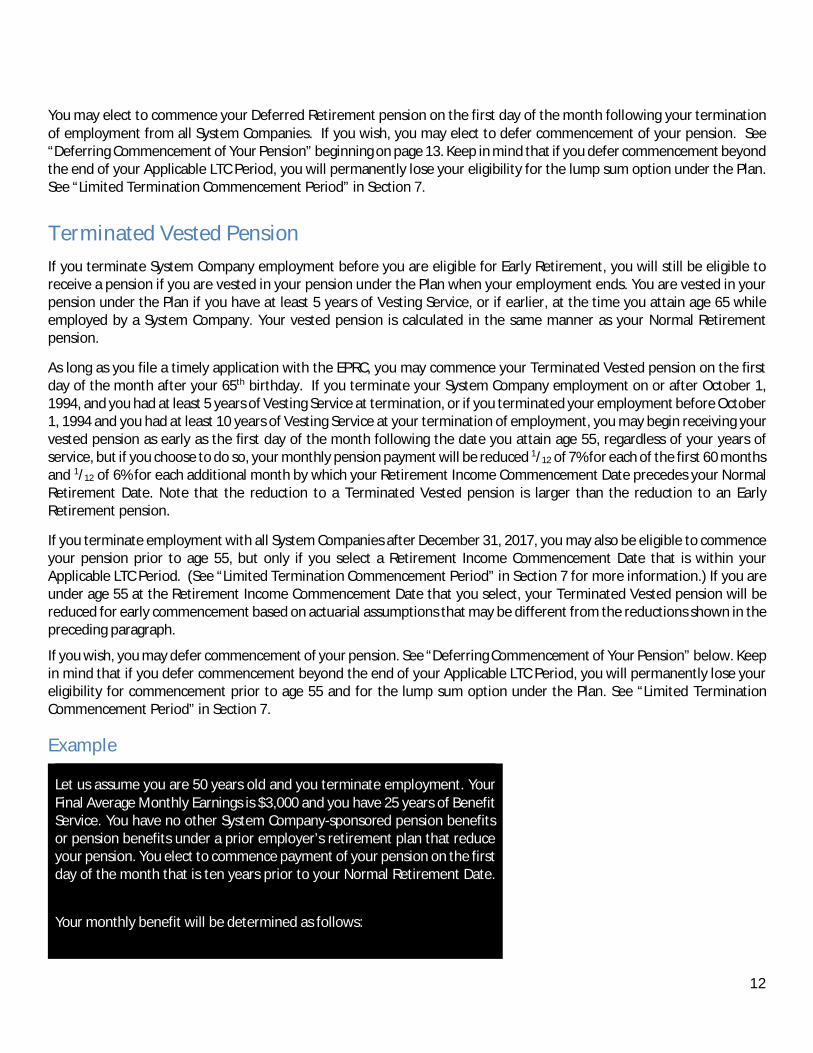

Terminated Vested PensionIf you terminate System Company employment before you are eligible for Early Retirement, you will still be eligible toreceive a pension if you are vested in your pension under the Plan when your employment ends. You are vested in yourpension under the Plan if you have at least 5 years of Vesting Service, or if earlier, at the time you attain age 65 whileemployed by a System Company. Your vested pension is calculated in the same manner as your Normal Retirementpension.

As long as you file a timely application with the EPRC, you may commence your Terminated Vested pension on the firstday of the month after your 65th birthday. If you terminate your System Company employment on or after October 1,1994, and you had at least 5 years of Vesting Service at termination, or if you terminated your employment before October1, 1994 and you had at least 10 years of Vesting Service at your termination of employment, you may begin receiving yourvested pension as early as the first day of the month following the date you attain age 55, regardless of your years ofservice, but if you choose to do so, your monthly pension payment will be reduced 1/12 of 7% for each of the first 60 monthsand 1/12 of 6% for each additional month by which your Retirement Income Commencement Date precedes your NormalRetirement Date. Note that the reduction to a Terminated Vested pension is larger than the reduction to an EarlyRetirement pension.

If you terminate employment with all System Companies after December 31, 2017, you may also be eligible to commenceyour pension prior to age 55, but only if you select a Retirement Income Commencement Date that is within yourApplicable LTC Period. (See “Limited Termination Commencement Period” in Section 7 for more information.) If you areunder age 55 at the Retirement Income Commencement Date that you select, your Terminated Vested pension will bereduced for early commencement based on actuarial assumptions that may be different from the reductions shown in thepreceding paragraph.

If you wish, you may defer commencement of your pension. See “Deferring Commencement of Your Pension” below. Keepin mind that if you defer commencement beyond the end of your Applicable LTC Period, you will permanently lose youreligibility for commencement prior to age 55 and for the lump sum option under the Plan. See “Limited TerminationCommencement Period” in Section 7.

Example

Let us assume you are 50 years old and you terminate employment. YourFinal Average Monthly Earnings is $3,000 and you have 25 years of BenefitService. You have no other System Company-sponsored pension benefitsor pension benefits under a prior employer’s retirement plan that reduceyour pension. You elect to commence payment of your pension on the firstday of the month that is ten years prior to your Normal Retirement Date.

Your monthly benefit will be determined as follows:

13

13

If you are an Article XXII or XXIII Participant, you should refer to Section 10 or Section 11, as applicable.

Deferring Commencement of Your PensionYou are not required to begin receiving your pension on the first day of the month following your 65th birthday (or the firstday of the month immediately following your later termination of employment). You may instead choose to defercommencement to a later date. However, you must commence your benefit no later than April 1st of the calendar yearfollowing the later of the year in which you terminate employment with all System Companies or attain age 72. (If youattained age 70 ½ prior to January 1, 2020, you may not defer commencement beyond the April 1st following the later ofthe year in which you terminate employment with all System Companies or attained age 70 ½.) If you fail to commenceyour benefit by that date, you will be required to pay an excise tax equal to 50% of the minimum distribution requiredunder the Code.

If you elect to defer commencement to a date later than the first of the month following your Normal Retirement Date,your benefit will be actuarially increased, but no retroactive Retirement Income Commencement Date will be permitted.

In addition, if you fail to commence your pension on the first day of the month following your Normal Retirement Date,you will be deemed to have elected to defer commencement of your pension. In that case, your pension will begin afteryou have contacted the EPRC and completed the application (see the section “How to Commence Your Pension” beginningon page 23).

If you defer commencement of your pension to a date after your Applicable LTC Period, you will permanently lose eligibilityfor commencement prior to age 55 and eligibility to elect the lump sum form of payment. See “Limited TerminationCommencement Period” in Section 7.

Special rules for calculating the actuarial increase apply if you continue working beyond your Normal Retirement Date.See the section “Deferred Retirement Pension” beginning on page 11.

Grandfathered BenefitsIf you participated in the Gulf States Utilities Company Employees’ Trusteed Retirement Plan, you may be eligible forgrandfathered benefits or recognition of additional service, as described in Section 9 of this Summary Plan Description.

You may be eligible for grandfathered benefits and recognition of additional service if you participated in the Gulf StatesUtilities Company Employees’ Trusteed Retirement Plan, the Retirement Plan of Arkansas Power & Light Company, theMississippi Power & Light Company Employees’ Retirement Income Plan, the Louisiana Power & Light CompanyRetirement Income Plan, and the Retirement Income Plan of Entergy Corporation, Entergy Services, Inc., Electec, Inc.,System Energy Resources, Inc., System Fuels, Inc., and Entergy Operations, Inc. If you were covered by one of these plans,you were previously provided with a summary plan description describing the grandfathered benefits and provisionsregarding recognition of prior service.

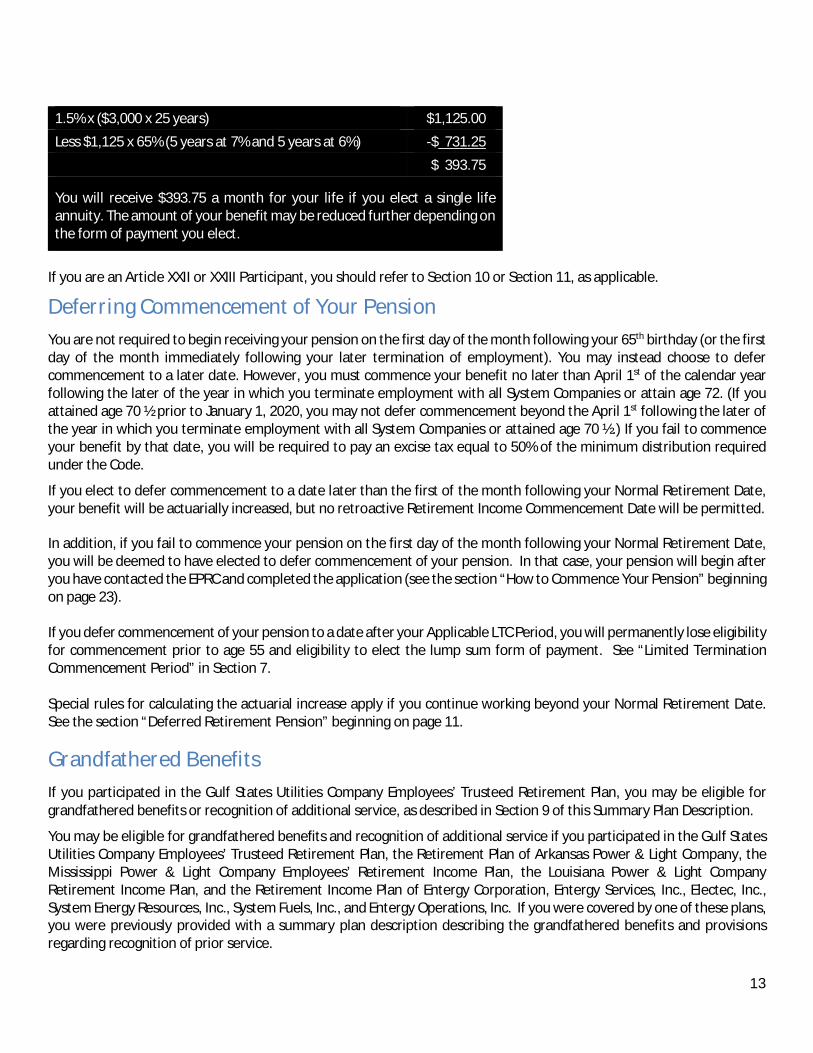

1.5% x ($3,000 x 25 years) $1,125.00

Less $1,125 x 65% (5 years at 7% and 5 years at 6%) -$ 731.25

$ 393.75

You will receive $393.75 a month for your life if you elect a single lifeannuity. The amount of your benefit may be reduced further depending onthe form of payment you elect.

14

14

Please contact the EPRC to determine your eligibility for grandfathered benefits and an explanation of their provisions.

Service under Prior Employer’s PlanAs discussed on page 4, Vesting Service under this Plan will generally take into account service under a prior employer’sretirement plan if individuals who became employees of a System Company as part of a purchase and sale agreementwere granted recognition of such service under the agreement.

In addition, if you participated in any of the following prior employer’s plans, you may be eligible to have your service andpay that were covered by such plan included for determining your Benefit Service and Earnings under this Plan:

§ The Boston Edison Retirement Plan, or

§ The Vermont Yankee Nuclear Power Corporation Final Average Pay Pension Plan for Management Employees, or theVermont Yankee Nuclear Power Corporation Retirement Plan for Local Union 300 of the International Brotherhood ofElectrical Workers. However, this Plan does not recognize service attributable to employment with a ReciprocatingCompany for inactive or former participants in Appendix G of Entergy Corporation Retirement Plan II for Non-Bargaining Employees or Entergy Corporation Retirement Plan IV for Bargaining Employees.

Please contact the EPRC for an explanation of any special service recognition provisions that apply to you.

EarningsIn general, “Earnings” means your base rate of pay for a standard 40-hour workweek, less any pre-tax salary deferrals toa non-qualified plan, plus bonuses and associated supplemental pay, if any, paid (i) in calendar years beginning on andafter January 1, 1995 under the TeamSharing Program, the Management Incentive Plan, and the Sales Incentive Plan; (ii)in calendar years beginning on and after January 1, 1997 in accordance with the Network Manager Incentive Plan and theWholesale Trader Incentive Plan; (iii) in calendar years beginning on and after January 1, 1999, in accordance with theCustomer Service Incentive Plan; (iv) in calendar years beginning on and after January 1, 2003, in accordance with theExempt Incentive Plan; and (v) in calendar years beginning on and after January 1, 2021, in accordance with theOperational Supervisor Incentive Plan, but excluding overtime payments, all other bonuses, and all other forms ofpayment.

If you are a part-time employee, Earnings includes your regular monthly earnings received (including vacation pay) thatwere paid by a System Company, and includes any before-tax contributions made to the Savings Plan of EntergyCorporation and Subsidiaries, or any other Code Section 401(k) plan sponsored by a System Company, to a Section 125cafeteria plan, and/or to a Section 132(f)(4)) qualified transportation fringe benefit program, plus bonuses and associatedsupplemental pay, if any, received (i) in calendar years beginning on and after January 1, 1995 under the TeamSharingProgram, the Management Incentive Plan, and the Sales Incentive Plan; (ii) in calendar years beginning on and afterJanuary 1, 1997, in accordance with the Network Manager Incentive Plan and the Wholesale Trader Incentive Plan; (iii) incalendar years beginning on and after January 1, 1999, in accordance with the Customer Service Incentive Plan; (iv) incalendar years beginning on and after January 1, 2003, in accordance with the Exempt Incentive Plan; and (v) in calendaryears beginning on and after January 1, 2021, in accordance with the Operational Supervisor Incentive Plan, but excludingovertime payments, all other bonuses, and all other forms of payment.

If you were employed at one of the following Entergy entities and were hired prior to the dates indicated:

§ Entergy Arkansas, Inc., or its successor entity, Entergy Arkansas, LLC, if you have an employment date (oradjusted hire date, if later) prior to May 1, 2002,

15

15

§ Entergy Louisiana, Inc., or its successor entity, Entergy Louisiana, LLC, if you have an employment date (oradjusted hire date, if later) prior to January 1, 2005 (but only for periods prior to October 1, 2015),

§ Entergy New Orleans, Inc., or its successor entity, Entergy New Orleans, LLC, if you have an employment date (oradjusted hire date, if later) prior to January 1, 2005,

§ Entergy Operations, Inc. located at Arkansas Nuclear One if you have an employment date (or adjusted hiredate, if later) prior to May 1, 2002,

§ Entergy Operations, Inc. located at Waterford III Steam Generation Station if you have an employment date (oradjusted hire, if later) prior to January 1, 2005, or

§ Entergy Louisiana, LLC (formerly Entergy Louisiana Power, LLC), if on September 30, 2015 you were an Employeeof Entergy Louisiana, LLC, the successor entity to Entergy Louisiana, Inc., and you have an employment date (oradjusted hire date, if later) prior to January 1, 2005 (but only for periods on or after October 1, 2015),

then your Earnings during the period in which you were employed by these entities will include overtime pay. However,if you transfer to another entity (and continue to be an active Participant in the Plan), your benefit will be determined asthe greater of (i) a benefit reflecting only Benefit Service and Earnings, including overtime, for the period overtime isincluded in your Earnings, or (ii) a benefit reflecting all of your Benefit Service, and Earnings for your entire period ofBenefit Service, but excluding overtime for all years.

Subject to the rules of this Plan, Earnings may also include amounts you earned while you were a participant in a prioremployer’s defined benefit plan. Please refer to “Grandfathered Benefits” and “Service under Prior Employer’s Plan”beginning on page 13 of this Summary Plan Description or call the EPRC to determine if this provision applies to you.

If you become disabled and are receiving LTD benefits under the LTD Plan, Earnings for your period of disability will bebased on your Earnings last in effect before you became disabled, except that bonuses and associated supplemental payand/or overtime that were included in such Earnings will not be included. However, any eligible bonuses and associatedsupplemental payments (as described in the preceding paragraphs) will be included if you actually receive these paymentswhile you are eligible for LTD benefits.

In the case of a Participant who is a Full-Time Employee and absent from work for an authorized leave of absence withpay, Earnings will be included at the base rate of pay last in effect prior to commencement of the leave of absence, for aperiod not exceeding two years.

Earnings above a specific maximum, as set annually by the IRS, are not considered when calculating Plan benefits (for2021, the maximum is $290,000).

Earnings shall not include amounts earned while employed by a non-Participating Company except during a period ofservice prior to your participation in this Plan during which you were an active participant in a System Company definedbenefit plan covering employees of such non-Participating Company. The definition of earnings may differ among SystemCompany defined benefit plans, so that the amounts taken into account under this Plan for your prior service may not bethe same as the amounts that were taken into account under a prior plan.

Suspension of BenefitsIf you leave the employ of all System Companies and start receiving annuity payments and are later rehired by a SystemCompany as an employee, your annuity payments from the Plan may be suspended after your reemployment. Yourpayments will be suspended for calendar months in which you complete 40 or more hours of service with the SystemCompanies. If you receive an annuity payment from the Plan for any month following your reemployment during whichyou complete 40 or more hours of service with System Companies, including the first month of your reemployment, if

16

16

applicable, you will be required to repay these amounts to the Plan. If the amounts are not repaid, the payments youreceive when you retire again will be reduced by the actuarial equivalent of any amounts that were not repaid to the Plan.

If you were rehired into a position covered by the Plan prior to July 1, 2014 and continue to meet the eligibilityrequirements described in Section 2, your Earnings and Benefit Service earned after your rehire will be used in therecalculation of your pension when you retire again.

Your recalculated pension will be offset by the actuarial equivalent (using the Plan’s actuarial factors) of any pensionpayments received prior to your reemployment, but your pension will not be less than the pension you were receivingprior to your reemployment (except as may be required to recover payments you received during months in which yourpension was suspended, as described above).

You will be required to make a new election with respect to the form of payment in which you will receive your pensiononce payments resume.

Your pension payments will also be “suspended” if you continue to work past your Normal Retirement Date. You willcontinue to be eligible to accrue benefits (subject to the provisions of the Plan), but in general, no actuarial adjustmentfor late commencement will be made to your pension. However, as indicated in the discussion regarding a DeferredRetirement pension, if you work past age 70 ½ in System Company employment, the amount of your Deferred Retirementpension will not be less than the actuarial equivalent of your benefit for the period beginning April 1 following the calendaryear in which you attained age 70 ½ and ending on your Retirement Income Commencement Date.

The EPRC will notify you if any of the suspension of benefits provisions described above apply to you.

17

17

Section7:HowYourPensionWillBePaidThe Plan offers several methods for payment of your pension. You should choose the method that best suits your needs.Your normal form of payment depends on your marital status when your pension payments begin. If you prefer, you mayelect (with your spouse’s consent, if applicable) one of the optional forms of payment. If you terminate employment withall System Companies after December 31, 2017 and are interested in receiving your pension in the form of a lump suminstead of an annuity, or electing commencement prior to age 55, you have only a limited time following your terminationof employment to make this election. In all cases, your commencement elections must be made within a specified timeperiod before your selected Retirement Income Commencement Date. Based on various factors such as interest rateassumptions and life expectancy tables, all optional forms of payment are approximately equal in value. If you are anArticle XXII or XXIII Participant, you should refer to Section 10 or Section 11, as applicable.

Normal Payment MethodYour normal payment method depends upon your marital status on your Retirement Income Commencement Date.

§ If you are single, your pension will be paid as a single life annuity. You will receive a monthly pension for yourlifetime and no pension payments will be made after your death.

§ If you are married, your pension will be paid as a joint and 50% survivor annuity. You will receive monthlypension payments for your lifetime, and after your death your surviving spouse will receive a monthlypayment equal to 50% of the pension payment you were receiving for the rest of his or her life. The spouseeligible to receive benefits under this option is the spouse to whom you are marred on your RetirementIncome Commencement date.

Because a joint and survivor annuity is payable for two lifetimes, your pension will be actuarially reduced, based onyour age and the age of your spouse on your Retirement Income Commencement Date.

Spousal Consent RequirementsIf you are married on your Retirement Income Commencement Date and want to select an optional form of payment thatprovides a survivor benefit that is less than 50% (for example, you elect a single life annuity, or the life annuity with a 10-year certain option), or you wish to designate someone other than your spouse as your beneficiary or your joint annuitant,your spouse must provide written, notarized consent to such an election. Your spouse must consent not only to the formof payment, but also to the specific individual named as your joint annuitant or beneficiary.

The waiver by your spouse of the normal form of payment described above may be made only during the 90-day periodbefore your Retirement Income Commencement Date, and may also be revoked during this same period. It may not berevoked after your Retirement Income Commencement Date.

Unless a Qualified Domestic Relations Order (QDRO) (see page 56) requires otherwise, your spouse’s consent is notrequired if your spouse cannot be located through reasonable means, or if you are legally separated (within the meaningof local law) and you have a court order to such effect. If your spouse is not legally competent to give consent to yourelection, your spouse’s legal guardian, even if the guardian is the Participant, may give consent.

Please contact the EPRC for information on providing appropriate documentation if one of the special circumstancesregarding spousal consent described above applies to you.

18

18

Optional Payment MethodsIf you prefer, you may elect one of the optional forms of payment described in this section. If you die before the first dayof the first period in which a pension is payable from the Plan, your election will be cancelled and any pension payable willbe subject to the survivor benefit rules discussed in Section 8. However, if the survivor annuity payable to your survivingspouse under the optional form you elected is higher than the amount your spouse would receive as a pre-retirementspouse’s death benefit, your spouse will receive the higher amount. Note that if you terminate employment with allSystem Companies after December 31, 2017 and commence your pension prior to age 55 during your Applicable LTCPeriod and are not otherwise eligible to commence at that time, certain annuity forms of payment will not be available toyou. See “Limited Termination Commencement Period” below.

Optional Joint and Survivor AnnuityUnder this option, you will receive a monthly pension for your lifetime, and after your death your joint annuitant willreceive a monthly payment equal to a percentage of the pension payment you were receiving for the rest of his or herlife. You choose your joint annuitant and the percentage of your pension that you want your joint annuitant to receiveafter your death (for example, 25%, 331/3%, 50%, 60%, 662/3%, 75%, 90% or 100%). If your joint annuitant is not yourspouse, then the percentage you may continue after your death may be limited by law. If you are married, your spousemust provide written, notarized consent to your election of another joint annuitant as well as to your election of anoptional form of payment that provides a survivor benefit to your spouse that is less than 50% of the pension paymentyou were receiving before your death.

If your joint annuitant dies before the first day of the first period in which your pension is payable from the Plan, yourpension will revert to the normal form of payment, unless you elect another form of payment. If your joint annuitant dieson or after the first day of the first period in which a pension is payable from the Plan, your pension will continue in thesame manner until your death and no additional benefits will be payable to your estate or anyone else following yourdeath. You will not be allowed to elect a new joint annuitant to receive any portion of your pension following your death.

If you were a participant in the Gulf States Utilities Company Employees’ Trusteed Retirement Plan, you may be eligible fora special pop-up provision from the Plan if your pension commences in the form of a joint and survivor annuity prior toyour joint annuitant’s actual death. Please refer to Section 9 for more detail.

Life Annuity with 10-Year Certain OptionThis annuity provides a monthly pension for your life with an extra guarantee. If you die before you have received 120pension payments, payments will continue to your primary beneficiary until a combined total of 120 payments have beenmade to you and your primary beneficiary. If you die after you have received 120 payments, no further payments will bemade to your beneficiaries or your estate or to anyone else following your death.

When you elect this form of payment, you must designate a primary beneficiary and an alternate, or contingent,beneficiary(ies). Payment is made to your contingent beneficiary(ies) only if you and your primary beneficiary die before120 payments have been made to you and your primary beneficiary. Again, if you are married, your spouse must providewritten, notarized consent to this form of payment and, if your primary beneficiary is not your spouse, your designationof another beneficiary.

Single Life AnnuityUnder this form of payment, you receive a monthly pension for your lifetime. When you die, payments stop. Again, if youare married, your spouse must provide written, notarized consent to your election of a single life annuity.

19

19

Level Income OptionIf you elect to commence your pension payments before age 62, you may elect the level income payment option. Thisprovides a larger monthly pension to you before age 62 (the age at which you become eligible for Social Security benefits)and then automatically reduces your monthly pension amount by your estimated monthly Social Security benefit onceyou attain age 62 — thus providing you with a consistent level of income from your Retirement Income CommencementDate until your death. (Note: You may have one or two months where the total income is not level because of the SocialSecurity payment time schedule.) The reduction at age 62 occurs whether or not you actually apply for Social Securitybenefits.

Again, if you are married, your spouse must provide written, notarized consent to your election of the level incomepayment option.

This option is not available to you if the amount that would be payable under this option prior to age 62 is equal to or lessthan your estimated Social Security benefit payable at age 62. Also, this form of payment may be restricted under IRSrules depending on the funded status of the Plan.

Example

Let us assume that you are entitled to a single life annuity of $1,350 per month payableat age 55 and that your estimated monthly Social Security benefit payable at age 62 is$800. An adjustment to your pension amount is calculated by applying an actuarialfactor to your estimated Social Security benefit to produce an actuarially equivalentstream of payments. The adjusted Social Security amount in this example is equal to($800 x 0.48 = $384).

To compute the amounts payable under the level income option, subtract theadjusted Social Security amount ($384) from the single life annuity payable at age 55,and then add back the age 62 estimated Social Security benefit amount ($1,350 - $384+ $800 = $1,766). This is the amount of your pension that would be payable beginningat age 55 and until you reach age 62.

Once you attain age 62, subtract the estimated Social Security benefit ($800) from thelevel income benefit ($1,766). You will receive a pension of $966 per month, for therest of your life.

In the event you elect to receive your pension from another System Company defined benefit plan under the level incomepayment option with the same Retirement Income Commencement Date as your pension from this Plan under the levelincome payment option, you may elect proration of your estimated Social Security benefits. If you make this election theamount of your estimated Social Security benefits used to determine your pension amounts under each plan will beprorated in proportion to the pension payable by each of the affected System Company defined benefit plans. Making thiselection is important if you want a level amount of income during your retirement. If you fail to make such an election,then the full estimated Social Security benefit amount will be used to reduce your payments from each plan once youattain age 62, and your total pension from Entergy plans would decrease at age 62 by double (or more) of your estimatedSocial Security amount.

Because this form of payment is based on your estimated Social Security benefit, you must submit an estimate of yourSocial Security benefit to the EPRC when you commence your pension. This estimate can be obtained from the SocialSecurity Administration (visit www.ssa.gov). Keep in mind, this option does not provide for any survivor benefits.

20

20

Lump Sum Option – Available Only during Your Applicable LTC PeriodUnder this option, you receive your pension in a single lump sum payment, with no benefit payable to anyone followingyour death. This option is only available to you if you terminate employment with all System Companies after December31, 2017, and only if you commence your pension within your Applicable LTC Period. If you are married, your spousemust provide written, notarized consent to your election of the lump sum form of payment. If you fail to commenceyour pension within your Applicable LTC Period, you permanently forfeit your eligibility to elect the lump sum form ofpayment. See “Limited Termination Commencement Period” below for more details. The lump sum payable under theLTC Period provision of the Plan will be equal to the present value, as of the lump sum commencement date, of thedeferred monthly pension payments that you could otherwise elect to receive as a single life annuity if you delayed thestart of your pension to your Normal Retirement Date. If you are eligible to commence your pension as of your selectedRetirement Income Commencement Date without regard to the LTC Period provision of the Plan, the lump sum amountwill be equal to the present value, as of the lump sum commencement date, of the immediate monthly pension paymentsthat you could elect to receive under the Plan as a single life annuity commencing on your selected Retirement IncomeCommencement Date, if this amount is greater than the present value described in the preceding sentence. The actuarialassumptions used to determine the present value will be based on the mortality table prescribed by the IRS underInternal Revenue Code section 417(e) and the three-segment interest rates under section 417(e) for the month of Augustof the calendar year immediately preceding the calendar year in which the Retirement Income Commencement Datefalls.

You (or your surviving spouse or alternate payee under a QDRO, if applicable) may elect to have the lump sum paymentpaid to you or directly rolled over to another eligible retirement plan of your choice.

Small Amount Lump-Sum PaymentsIf the actuarial present value of your vested pension is $1,000 or less when you retire, die or otherwise terminateemployment with a System Company, you (or your surviving spouse, if applicable) will automatically receive your pension(or pre-retirement spouse’s death benefit, if applicable) in a single lump-sum payment as soon as practicable thereafter.The actuarial value of such benefit is based on certain assumptions about life expectancy and interest rates, as requiredby law. A pension that is payable as a small-amount lump sum payment is not eligible for commencement under the LTCPeriod provision described in the following section of this Summary Plan Description.

However, if the single lump sum payment amounts to at least $200 then you (or your surviving spouse, if applicable) mayelect to have the lump sum payment paid to you or directly rolled over to another eligible retirement plan of your choice.You (or your surviving spouse, if applicable) will be provided with a detailed explanation of the rollover procedures at thattime. If you (or your surviving spouse, if applicable) do not make a timely election you will automatically receive yourpension in a single lump sum cash payment.

If you were rehired before July 1, 2014 after receiving a lump-sum payment of your pension and you continue to meet allof the eligibility requirements discussed in Section 2, your pension upon subsequent termination of employment will bebased on all of your Benefit Service and Vesting Service, but your pension will be reduced to take into account the valueof the pension attributable to the lump-sum amount you already received.

If the single-sum actuarial present value of your pension is more than $1,000, your pension will be paid under the normalpayment method or, if you so elect, one of the optional payment methods. You may also be eligible for commencementunder the LTC Period provision described in the following subsection of this Summary Plan Description.

21

21