Enhancing the Development Impact of Remittances Policy...

66

June 2006 Document of the World Bank Report No. 35771-TJ Tajikistan Policy Note Poverty Reduction and Economic Management Unit Europe and Central Asia Enhancing the Development Impact of Remittances Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

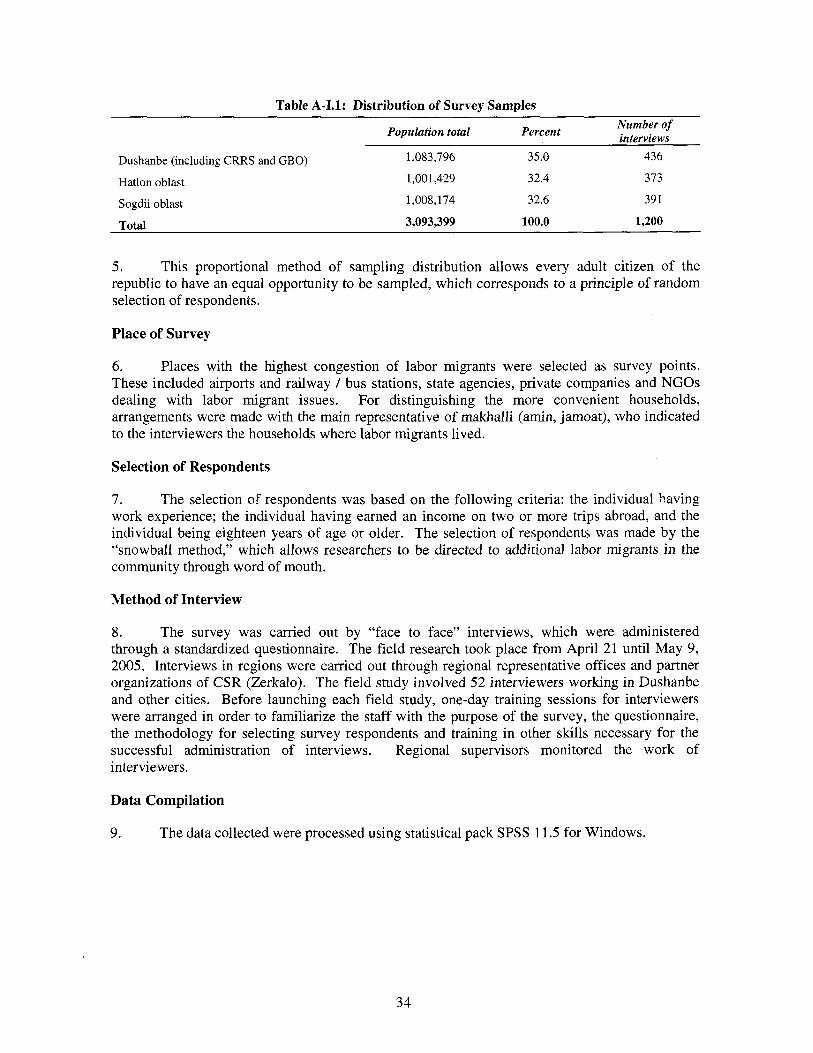

Transcript of Enhancing the Development Impact of Remittances Policy...

June 2006

Document of the World Bank

Report No. 35771-TJ

TajikistanPolicy Note

Poverty Reduction and Economic Management UnitEurope and Central Asia

Report N

o. 35771-TJTajikistan

Policy Note

Enhancing the Development Impact of RemittancesPub

lic D

iscl

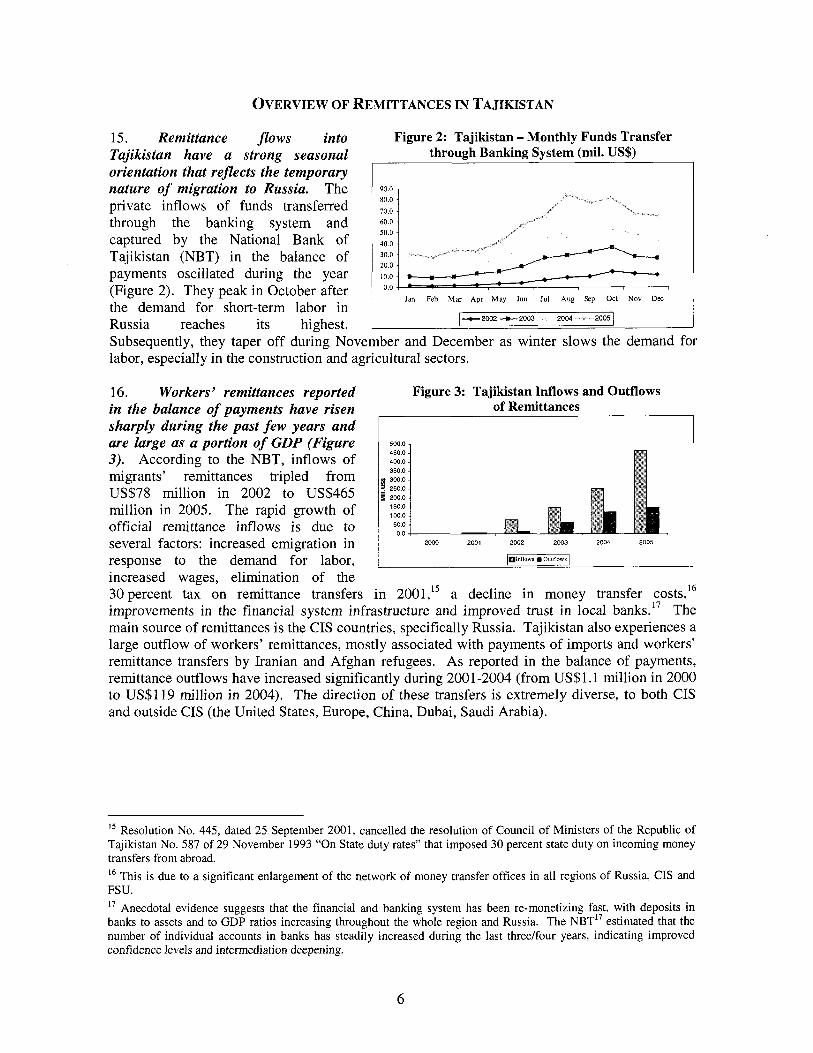

osur

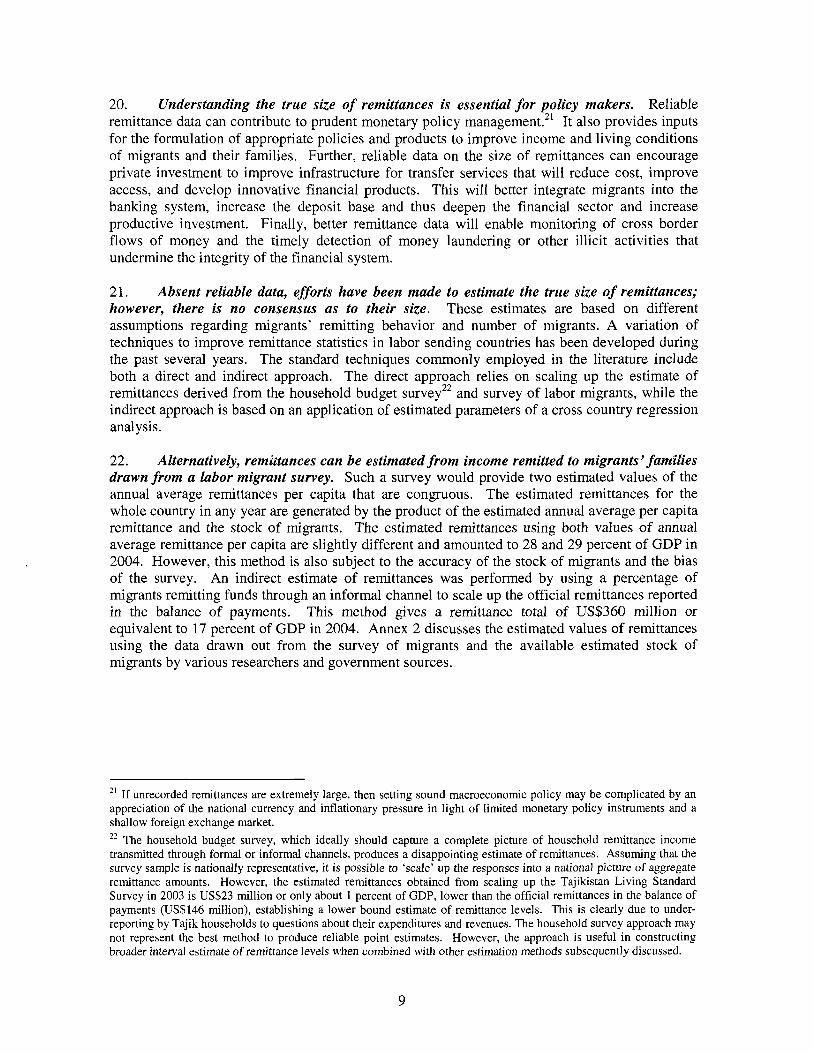

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

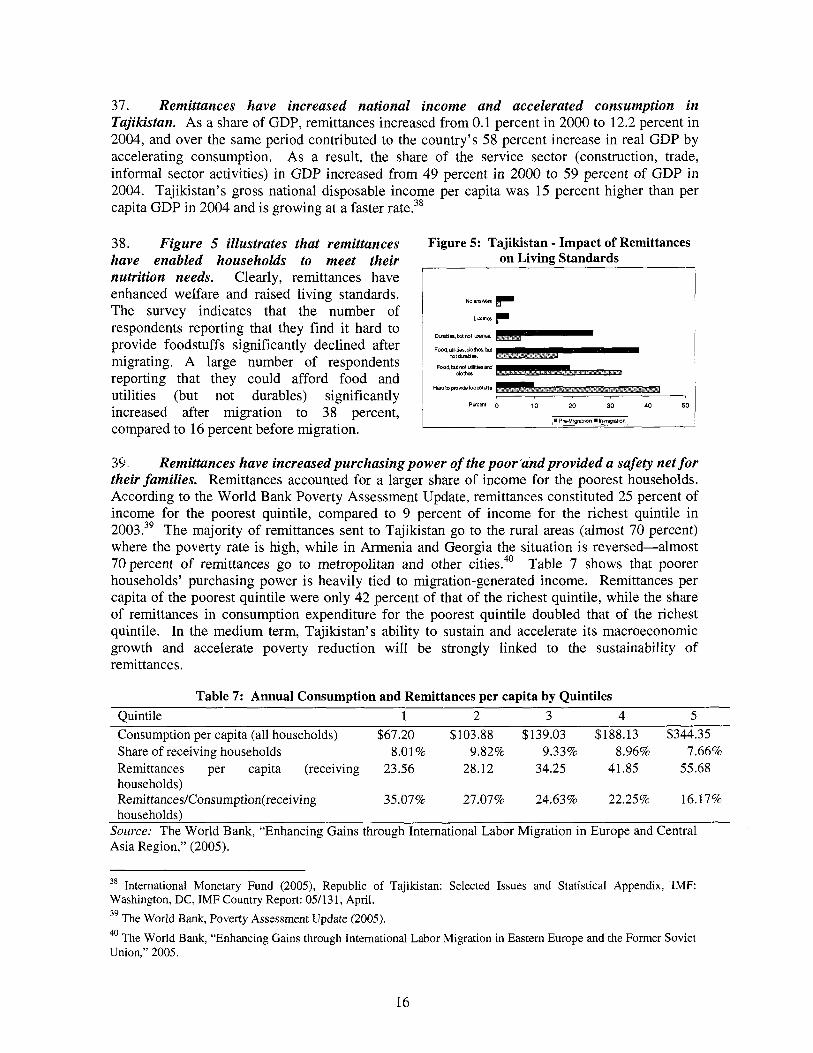

utho

rized

TABLE OF CONTENT

ACKNOWLEDGEMENTS ......................................................................................................... V

EXECUTIVE SUMMARY ....................................................................................................... vi1

I . I1 .

I11 . I V .

V .

V I .

INTRODUCTION ............................................................................................................... 1

BACKGROUND .................................................................................................................. 2

MIGRATION IN TAJIKISTAN ................................................................................................... 2 WHO ARE THE MIGRANTS? ................................................................................................... 4 OVERVIEW OF REMITTANCES IN TAJIKISTAN ....................................................................... 6

ALTERNATIVE ESTIMATES OF REMITTANCES ..................................................... 7 TRANSFER METHOD, USES, AND IMPACT OF REMITTANCES IN TAJIKISTAN ..................................................................................................................... 11 TRANSFER METHODS OF REMITTANCES ............................................................................. 11 USES OF REMITTANCES IN TAJIKISTAN ............................................................................... 14 IMPACTS OF REMITTANCES IN TAJIKISTAN ......................................................................... 15

ENHANCING THE DEVELOPMENTAL IMPACT OF REMITTANCES- LlSSONS LEARNED FROM INTERNATIONAL EXPERIENCE ........................... 18

MEASURES TO MOBILIZE REMITTANCES INTO THE BANKING SYSTEM .............................. 18 USING MICRO-FINANCE INSTITUTIONS TO MOBILIZE REMIlTANCES ................................. 20 MEASURES TO MOBILIZE COLLECTIVE REMIITANCES ....................................................... 21 LESSONS LEARNED .............................................................................................................. 24

ENHANCING DEVELOPMENT IMPACT- WHAT CAN TAJIKISTAN DO? ...... 25

Overarching Policies to Enhance the Development Impact of Remittances .................. 25 RECOMMENDATIONS ........................................................................................................... 25

Improvements of Business Environment ................................................................... 25 Strengthening Financial Intermediaries ................................................................... 25

Policies Measures to Improve the Welfare of Tajik Migrants Abroad ..................... 28

Improving Information Dissemination and Statistics on Remittances and Migration .................................................................................................................................. 27

AREAS FOR FURTHER STRENGTHENING AND RESEARCH .................................................... 30

ANNEX I: A SUMMARY OF MIGRANT SURVEY ............................................................. 33

ANNEX 11: ESTIMATION OF REMITTANCE FLOWS INTO TAJIKISTAN ................. 35

ANNEX 111: TRANSFER OF REMITTANCES TO TAJIKISTAN ..................................... 39

ANNEX IV: MONEY TRANSFER SYSTEM IN TAJIKISTAN .......................................... 45

ANNEX V: MICROFINANCE INSTITUTIONS IN TAJIKISTAN ..................................... 51

REFERENCES ............................................................................................................................ 53

iii

LIST OF TABLES

Tab Tab Tab Tab Tab Tab Tab Tab Tab Tab Tab Tab Tab

‘le 1: Tajikistan Migration Flows (thousand persons) ............................................. 3 #le 2: Tajikistan’s Demographic Profile .................................................................... 4 lle 3: Financial Snapshot of a Taj ik Migrant ............................................................ 5

l e 5: ECA’s Largest Developing Country Recipients of Remittances. 2003 ......... 7 lle 4: Tajikistan Balance of Payments ....................................................................... 7

Ile 6: Correlation between Methods of Transfer and Transport Mode ............... 11 Ile 7: Annual Consumption and Remittances per capita by Quintiles ................. 16 de A-1.1: Distribution of Survey Samples ............................................................... 34

Ile A-11.2: Choice of Remittance Channel by Taj ik Migrants .............................. 37 de A-111.1: Money Transfer Systems in Tajikistan ................................................ 41

de A-IV.l: Pricing of Money Gram Remittance Services ..................................... 46

de A-11.1: Estimated Remittances ........................................................................... 36

de A-111.2: Selected Indicators of Financial System (in thousand Somoni) ........ .44

LIST OF FIGURES

Figure 1: Migration of Skil led Workers in Eastern Europe and the Former Soviet Union ......................................................................................................... 5

Figure 3: Tajikistan Inflows and Outflows of Remittances .......................................... 6

Figure 5: Tajikistan - Impact of Remittances on Living Standards .......................... 16 Figure 6: Employment Sector for Taj ik Migrants ....................................................... 17

Figure A-111.1: Fund Transfers through various Commercial Banks in 2004 (% of Total Transfers) ..................................................................................................... 39

Figure 2: .............................................................................................................................. 6

Figure 4: Tajikistan Uses of Remittances (% of Respondents) .................................. 14

Figure 7: Remittance Securitization Structure ............................................................ 22

LIST OF BOXES

Box 1: Official Estimate of Remittances ......................................................................... 8 Box 2: Estimate of Remittances through Informal Channels ..................................... 10 Box 3: Cross-selling by Taj ik Commercial Banks ....................................................... 12 Box 4: Tajikistan’s Banking System ............................................................................. 13 Box 5: Benefits of Involvement of MFIs in Remittances ............................................. 21 Box A-111.1: Tajikistan’s ATMs and PTMs .................................................................. 43 Box A-IV.l: Sending and Receiving Money via Western Union ................................ 46

i v

ACKNOWLEDGEMENTS

This Policy Note i s part o f the Country Economic Memorandum for Tajikistan. The analysis i s based on the survey o f migrants conducted by Tajikistan’s Sociological Research Center (Zerkalo) from April through May 2005, the findings o f several missions that visited Tajikistan between February through July 2005, and the extensive review o f international experience on migration and remittances.

The Policy Note i s prepared by a team comprising Jariya Hoffman (task team leader, ECSPE), Bryce Ramsey-Quillin (ECAVP), Carlo Segni (ECSPS), and Paul Jacobs (summer intern). The team wishes to thank the Government of Tajikistan for the constructive discussions and inputs provided during and after the various missions. The team i s particularly grateful for the inputs provided by Faizullo Kholboboev (State Adviser to the President on Economic Policy), Mr. M. Alimardonov (NBT Chairman), Mr. Jamshed Yusupov (Head, Monetary Policy and Statistics Department, NBT) Mr. Asadullo Gafurov (Head, BOP Division, NBT), Mr. Anvar Babaev (Head State Migration Service, Ministry o f Labor and Social Protection), Mr. Asoev Umed Abdulloevich (Head, Department for Labor Market and Population Employment), Mr. Halimjon Rahimov (Director, Tajik Labor Export Agency-Tojikhofijakor, Ministry o f Labor and Social Protection), Mr. Fattoh Saidov (Head, Visa and Registration and Passport Affair Division, Ministry of Interior), Samandar Haidarovich Khaidarov (Head Foreign Economic Activities and Forex Operations, AgroInvestBank), Mr. Umed Davlatzod (First Deputy Chairman, Orionbank), Mrs. Larisa Loginova (First Deputy Chairman, Tojiksodirotbonk), Mr. Muzaffar Zaripov (Director IOM-OSCE Information Resource Center for labor migrants), Aziz Sharipov (Chief, International Relations Department Kafolatbank), Ms. Saodat Olimova (Head, Social Service Scientific Research Center “Shark), Mr. Kahramon Bakozoda (Sociological Research Center, Zerkalo), Alastair Watson (Chief Operating Officer, the First MicroFiannceBank), Michael Schneider (Manager, Project “Support o f Microfinance Services in rural areas,” GTZ), Shamsiddin Gulov (Branch Director, International Micro-Loan-Fund “IMON’)), Mahmoud Naderi (Chief o f Mission, IOM) and Mr. Phillip Wanners (Swiss Forum for Migration and Population Studies, Switzerland). The author would l ike to express her gratitude to the Swiss Government for i t s generosity in providing financing support through the Consultant Trust Fund for the survey o f migrants in Tajikistan.

The Note i s drawn upon several background papers contributed by Bryce Ramsey-Quillin and Paul Jacob (Estimation o f Remittances), Carlo Segni (Transfer Channels and Costs and Micro-finance Institutions), and Paul Jacobs (Review o f International Experience) provided in Annex 11-IV. I t benefits from discussions with Ali Mansoor and Bryce Ramsey-Quillin and insightful and constructive comments from the peer reviewers, Dilip Ratha and John Litwack.

This report was prepared under the general guidance and advice of Cheryl Gray, Carlos Felipe Jaramillo, Samuel K. Otoo, Deborah L. Wetzel, Dennis de Tray, Annette Dixon, Cevdet Denizer, Sudharshan Canagarajah, L i l ia Burunciuc, and Ashad Sayed. Bryce Ramsey-Quillin and Ali Mansoor kindly provided overall guidance and advice as well as shared the survey data from the ECA migration study. The report also benefited from valuable suggestions and inputs received at different stages o f preparation from Sudharshan Canagarajah, Jakob von Weizsacker, Samuel Munzele Maimbo, Raul Hernandez-Coss, Utkir Umarov, and Aziz Khaidarov. Paul Jacobs provided valuable and excellent assistance in analyzing the migrant survey database and

conducting the literature review. Processing assistance from Dammika Somasundaram and Zakia Nekaien-Nowrouz i s gratefully acknowledged. Helpful logistical assistance was also received from Munira Salieva, Janna Yusonova, Takhmina Jumaeva and Zarina Shukurova.

v i

EXECUTIVE SUMMARY

1. Since i t s transition to a market economy in 1991, Tajikistan has experienced high levels o f out migration. The motivations for this migration, however, have evolved over time. Early emigration was motivated by war and the conflicts following independence, while more recent migration has been provoked by economic factors influenced by demand and supply factors. An increase in the demand for labor driven by a decline in the working age population in Russia as well as strong economic growth in Russia, combined with slow job growth and the low wage level in Tajikistan, have encouraged the emigration o f Tajiks.

2. Who are these migrants and how many are they? A migration survey conducted in May 2005, shows that the average migrant i s a male ethnic Tajik, with an average age of 34 years, married and with 5 dependents. The majority o f migrants have secondary education or vocational training. Most are unemployed or grapple with a low wage level that i s insufficient to meet basic household needs. They travel alone and mainly head for Russia for an average o f 14 months and then return to Tajikistan. While in Russia, most Tajik migrants work in the construction, services, and manufacturing sectors. Given the dearth and unreliability o f migration statistics, the true number o f Tajiks l iving outside the country i s unknown and a large number o f them are undocumented migrants. One official estimate suggests the number was about 421,000 in 2004, while other estimates indicate numbers up to 1.2 mil l ion Tajiks l iving overseas.

3. What i s all the mor: remarkable about Tajik migrants i s that they are the source of a large volume of funds that are being sent back to their home country in amounts so significant that they have now become an important source of economic growth for Tajikistan. In fact, the level of remittances ranks second after aluminum and ahead o f cotton if considered as an export o f labor services in 2004, and towers over those o f official development assistance as well as foreign direct investment. These inflows have a strong seasonal orientation that reflects, in particular, the temporary nature o f migration to Russia. Between 2000 and 2004, official estimated remittances increased from 0.1 percent to 12 percent of GDP. In addition to employment opportunities in Russia (and in other host countries), the reasons that official remittance transfers have increased since 2000 include the removal o f the 30 percent tax that had been levied on such transfers, reduction in money transfer costs, improvements in the financial system’s infrastructure, and improved trust in local banks.

4. Though already large, i t i s widely agreed that the true size of remittance flows are unquestionably larger than the official balance of payment estimates. Alternative methods of estimating remittances produce widely different numbers depending on the estimation methodology used. For example, the estimate based on the Liv ing Standard Survey i s even lower than the official estimate, which clearly undershoots the true mark. An estimate based on a micro-survey of returned migrants suggests that remittances could amount to 28 percent of GDP, although the finding i s contentious because o f the unreliability o f migrant statistics and the biases o f the survey methodology. Alternatively, one regression-based estimate suggests that remittances could be as high as 21 percent o f GDP.

5. Remittance transfers to Tajikistan are relatively efficient as measured by the simplicity of operation, cost and speed. The most widely used transfer mode among Tajik migrants i s the money transfer system (cash-to-cash transfer) that operates in partnership with Tajik commercial banks (about 70 percent o f all operations). These require no documents from senders, and have a

fee that averages anywhere from 1.5 to 5 percent o f the amount sent (which i s charged to senders in host countries and i s considered relatively low compared to similar systems in countries such as Mexico and Philippines). Competition among banks and money transfer operators have driven rates down, and even a global company l ike Western Union was obliged to lower costs in Tajikistan. Recipients can withdraw cash in a short time (within a day in Dushanbe), and in several currencies (US$, Pound Sterling, Ruble, Euro, and Somoni). Remittances sent through the banking system (account to account transfer) are insignificant due to high transfer costs (that includes a fee o f 3 percent paid by both senders and receivers, and the exchange rate spread o f 2- 3 percent), limited access to the banking system, and lack o f bank accounts abroad and at home. Despite i t s extensive network in the rural areas, transfer through the post office system i s inefficient due to high fees (10-12 percent) and very slow speed (2-3 weeks). I t i s estimated that about 30 percent of migrants send remittances through informal channels, depending mostly on personal courier, friends, and acquaintances.

6. Remittances to Tajikistan are highly significant as they have become a source o f income for many low income families to meet basic needs and thereby help reduce poverty. They are clearly welfare enhancing for households who benefit from these flows. The survey o f Tajik migrants suggests that the financial situation o f Tajik migrants and their families improve after migration. Their income overseas i s ten times what they earned in Tajikistan before migration (US$274 per month compared with a pre-migration income of US$30 per month), o f which about 48 percent i s remitted to Tajikistan. Remittance recipients earmark funds for consumption, home repair, education and health, and savings. ’ Consequently, they have contributed to short-term economic growth and poverty alleviation through increased domestic demand that leads to increased employment, income and output. At present, their contribution to longer term growth through investments in productive activities i s limited by the low level o f migrants’ income and an unfavorable business environment that constrains the development o f small and medium enterprises (SMEs). However, their contribution to funding the education and health needs o f families i s arguably a contribution to investment in human capital that can yield benefits both in the near- and medium-term.

7. From a macro perspective, the international literature shows that large inflows o f remittances can also lead to a real appreciation o f the exchange rate, which can fuel imports and worsen the country’s export competitiveness. Further, they may increase the vulnerability of recipient countries to host countries’ migration policies and business cycles. Such macroeconomic impacts have implications for long-term economic growth and thus deserve a comprehensive analysis. To mitigate the potential negative impacts and to enhance their longer term positive impact, the government o f Tajikistan i s seeking appropriate policies on how to further enhance the use o f remittances beyond increasing the standards o f living and welfare o f household recipients. This Note attempts to bring them into focus and to suggest measures for the government to consider enhancing the development impact of remittances.

8. The report contains a review o f the latest international policy experiments to enhance the development impact o f remittances; however, many o f these experiments, unfortunately, have either not been properly evaluated or are more relevant for middle income countries, where financial sectors are more developed. This Note considers some o f the most relevant international experience concerned with enhancing the development impact o f remittances. Such experience i s instructive and suggests that there are indeed a variety of policy instruments that can be effective in mobilizing remittances into the banking system and channeling their use for more productive purposes.

v i i i

9. The conclusion o f this analysis i s that policies need to be designed for Tajikistan’s specific needs. After considering the international experience and Tajikistan’s particular conditions, the note assesses the potential for replication of the most successful o f these policies that were applied elsewhere to the case o f Tajikistan. For example, to meet specific development objectives, collective remittances have been mobilized by the Home Town Associations (HTAs) in several Latin American countries and matched by government funds (known in Mexico as Three-for-One). The experience o f matching funds that has been piloted in Tajikistan by UNDP in collaboration with the I O M i s considered inconclusive and i t i s too early to evaluate the program’s development impact.

10. The Note considers those policies that would increase remittance inflows and enhance the development impact o f remittances, increase welfare and broaden the safety net for migrants and their families. I t recommends a set o f policies aimed at optimizing their positive impacts by improving the investment climate, and the role of financial intermediaries. I t also offers a second set o f policy recommendations that focuses entirely on bilateral negotiations, especially with Russia, concerning the rights of Tajik migrants, and resident and work permits when working in host countries. Finally, the report explains the importance o f improving the quality o f migrant and remittance statistics to improve the understanding o f their impact and as an aid in the designing o f appropriate policies.

11. impact o f remittances, the Tajik authorities could focus on the following:

In terms o f policies that can be implemented unilaterally to enhance the development

(a) Encouraging a pro-business environment, This requires maintaining a stable macro- economy and simplifying the licensing and inspection regimes.

(b) Enhancing the role o f financial intermediaries for mobilizing savings and investment resulting from remittances. Such policies include:

Encourage entry o f foreign banks into Tajikistan to foster modernization and technological improvements, as well as to further increase public t rust and confidence in the banking system;

Cross-selling o f financial products by commercial banks to migrants as incentives for keeping their savings in the banking system;

Promote healthy competition of commercial banks to further reduce transfer fees, especially wire transfers charged by commercial banks;

Improving public information dissemination related to financial services by both the government and commercial banks; and

Integrating MFIs into the remittance services to mobilize remittance savings from un-banked migrants in the rural areas and channel them towards productive investment including small business and agricultural projects.

(c) In the near-term, efforts should be undertaken to improve the quality and coverage of statistics on migration and remittances, including estimating informal transfers o f remittances in the balance o f payments and improving household budget surveys.

i x

12. In terms o f policies designed to increase remittance inflows that are not fully under the control of the Tajik authorities. The Note outlines the potential benefits of a proactive engagement in bilateral diplomatic negotiations with Russia to remove obstacles to migration. The main aim o f such negotiations should be to:

(a) Protect the right o f undocumented Tajik migrants on Russian territory; (b) Simplify the registration process o f resident permits for Tajik migrants; and (c) Lower the cost to Russian employers when hiring foreign workers.

X

I. INTRODUCTION

1. Remittances have played an important role as one o f the drivers o f Tajikistan's robust economic growth during the past several years. The volume o f official remittances has significantly increased since 2001 and now represent close to 12 percent o f GDP (2004). Remittances have become the most important source o f external financing for the balance of payments, have increased incomes, and as a result helped reduce poverty. Emigration- particularly seasonal migration to Russia-has become an alternative poverty coping measure chosen by the poor. According to the 2003 Tajikistan's Liv ing Standard Survey, remittances and other transfers made up about 10 percent o f average household income in 2003, ranking i t the second source o f cash income following wages.'

2. Recognizing their importance, the Tajikistan authorities have sought to sustain remittance flows. In order to increase the quantity o f legal migration, temporary worker agreements have been signed bilaterally with key receiving countries (Russia, Kyrgyz Republic). A 30 percent tax on remittance transfers was eliminated and commercial banks were allowed to partner with foreign money transfer operators to provide low cost transfer services to migrants. The Ministry o f Labor and Social Protection established an employment agency to provide employment services including information on vacancies, training, and orientation for workers choosing to live abroad,

3 . However, anecdotal evidence indicates that migrants are not sufficiently integrated into the Tajikistan financial system, much less that o f the destination countries. Most do not have bank accounts at home or abroad, and as a result remittances are mostly transferred through money transfer systems on a cash to cash basis. They are immediately withdrawn in cash once reaching Tajikistan in order to meet basic needs. If there are savings, they prefer to keep them at home because of a lack o f trust in the banking system. This leads to inadequate integration of migrants and their families into the financial system, thus limiting access to financial services and products that could smooth consumption and provide additional investment for income generation activities.

4. The survey o f Tajik migrants found that the majority o f remittances are used to fund basic household consumption, while an insignificant amount o f remittances are spent on productive investment. Most migrants come from poor, rural areas and the bulk o f international remittances appear to fund basic consumption and some investment and saving at the margin. Although this pattern o f remittance use i s common around the world, i t i s recognized that the development impact o f investment can be greater than consumption expenditure. To maximize the potential impact o f remittances, the Tajik authorities have expressed keen interest in receiving guidance on how to further encourage their use for greater productive investment.

5. For remittances to have an impact beyond an income effect, two conditions must be met. First, households must have surplus income after all subsistence needs have been met. Second, investment policies and institutions must create the incentives to encourage households to save any surplus income in the formal, financial sector or invest in businesses. In the case o f Tajikistan, i t i s not yet clear whether households have large of amounts o f surplus income. However, efforts could be made to improve the investment climate not only to encourage greater

' The World Bank, Poverty Assessment Update (June 2004).

savings and investment from remittance income at the margin, but also to take greater advantage of Tajikistan’s migrant population. Improved policies to encourage higher levels o f remittances wi l l facilitate greater trade and migration complementarities, and provide more opportunities for migrants to use the financial and human capital built abroad back home.

6. (i) to expand knowledge o f the size of remittances, their sending mechanisms (especially through formal channels), and their use; and (ii) to propose policy recommendations to enhance the development impact o f remittances. The Note benefits from a recently completed study (Tajikistan’s Trade Diagnostic Study) and from the World Bank’s ongoing Study on “Enhancing Gains through International Labor Migration in Europe and Central Asia,” and the 2005 Global Economic Prospect featuring “International Migration and Remittances.”2 The survey o f Tajik migrants conducted by the Zerkalo3 during April-May 2005 for the migration study in the ECA region provides insights to Tajikistan’s migration and remittances. I t provides demographic characteristics and economic behavior o f migrants, thus enabling the computation of economic and financial parameters underpinning the analysis. Finally, reviewing the international experience o f other selected labor sending countries around the world provides lessons that can be drawn for the Tajik government in designing relevant policy measures aiming to enhance the development impact o f remittances.

This Policy Note has two main objectives:

7. Section Two provides background on migration and remittances related to Tajikistan. Section Three discusses the estimation o f remittance size and data issues. Section Four examines the transfer channels o f remittances (their cost, access, and speed), their use, and the impact o f remittances. The analysis highlights impediments to the efficiency o f remittance transfer services through formal channels, examines the use o f remittances by recipient households in Tajikistan, and identifies impacts of remittances on the economy. Section Five discusses the international experience o f other selected migrant-sending countries in using various instruments to enhance the development impact of remittances. The section draws some o f the key lessons learned from the international experience that could be considered in the Tajik context. The final section recommends policies to enhance the development impact o f remittances taking into account the Tajik context and identifies topics for further research.

The Note i s organized into six sections, including this Introduction.

11. BACKGROUND

MIGRATION IN TAJIKISTAN

8. Tajikistan’s transition to a market economy has been challenging. The implementation o f structural reforms was delayed by the multi-year civi l war that broke out after independence in 1991 and did not commence until 1997. The country inherits a difficult geography - i t i s land- locked, resource poor, mountainous and faces an unfavorable geo-political backdrop bordered by Afghanistan and Uzbekistan. The civil war contributed to the deterioration o f the physical infrastructure and an already weak institutional capacity. Despite strong economic growth, averaging 9.6 percent over 2000-2004, Tajikistan remains the poorest economy in Central Asia with a per capita GDP o f US$310 in 2004. Poverty has fallen somewhat, but remains high at

The World Bank, 2005. Enhancing Gain through International Labor Migration in Europe and Central Asia. The Zerkalo i s a Sociological Research Center in Tajikistan that carried out the survey of 1,200 migrants financed by

the World Bank’s ECA Migration Study during April-May 2005. The survey i s based on the same set of questionnaire that was designed for 6 countries that were case studies for the World Bank Study. Based on the survey results, Zerkalo prepared a report entitled “Assessment of Standard of Living of Labor Migrants.”

2

64percent and income inequality has widened since 1999.4 Lackluster job growth due to demographic factors combined with delayed structural reform makes i t difficult for the population to find employment and earn sufficient income to meet basic needs, especially in the rural areas. A good segment o f the population has found i t s way out o f poverty through international migration, primarily to various parts of Russia.

9. International migration in Tajikistan i s a relatively new phenomenon relative to other labor exporting countries around the world, especially Mexico, Philippines and South Asian countries (India, Pakistan, Sri Lanka, and Bangladesh). Prior to independence in 199 1, Tajikistan’s migration was considered internal within the former Soviet Union. The eruption o f ethnic conflict, followed by a multi-year c iv i l war that began in 1991, then liberalization o f migration after independence and economic transition, all resulted in a large f low of international migration. Based on the available official migration data reported by the State Statistical Committee, about 41 1,623 persons left Tajikistan during 1991-2004, o f which 68 percent left during 1991-95 (Table 1). They were mostly non-ethnic Tajik (Russian, Jews, Crimea Tartars, Ukrainians, Kazakhs, and German) and their main destination

Table 1: Tajikistan Migration Flows (thousand persons)

Arrived Departed Migration inflows

(+Youtflows (-) 1991 74.9 101.3 -26.4 1992 51.3 146.0 -94.7 1993 71.4 146.1 -74.7 1994 43.3 88.9 -45.6 1995 37.1 74.9 -37.8 1996 26.1 53.7 -27.6 1997 20.8 37.1 -16.3 1998 16.9 32.3 -15.4 1999 14.7 28.8 -14.1 2000 14.5 28.2 -13.7 2001 16.7 29.1 -12.4 2002 17.7 30.2 -12.5 2003 16.9 27.9 -1 1.0 2004 15.2 24.7 -9.4

Source: State Statistical Committee.

countries were Russia, Uzbekistan, Germany, Kazakhstan, Israel, and the Kyrgyz Republic. However, emigration declined sharply in 1997 and leveled o f f during the 1998-2004 period as the political and economic situation gradually normalized.

10. The pattern of Tajikistan’s migration in recent years has evolved. Whi le international migration had been driven by ethnic conflict and civ i l war, recent emigration has been driven by economic factors, both on the demand and supply sides. The demand factors-demographic crisis in Russia due to a declining and aging population5 and continued economic growth in Russia-generated significant demand for labor, especially in the service sector. The supply factors in Tajikistan included a low wage level, high unemployment6 due to s k i l l mismatches and slow job growth relative to labor force g r ~ w t h , ~ all of which provided great incentives for workers to seek opportunities outside the country. A free visa regime between Tajikistan and the

According to the World Bank 2003 Poverty Assessment Update, the inequality o f consumption expenditure increased from 0.33 in 1999 to 0.36 in 2003.

Russia’s natural rate o f increase (-0.6 percent) ranks the second lowest in the world after Ukraine (-0.8 percent). Population in Russia declined to 143.5 million (December 2004) from 145.2 million (2002) due to natural causes, a low birth rate and emigration. The World Population Data Sheet projects that Russia’s population wil l decline to 119 million by 2050. According to a demographic forecast for 2050 the share o f population in the working age group (between 16 and 55 for females and 60 for males) wi l l be close to 50 percent, which i s considerably lower than 61 percent according to Census 2002 but s im i la r to the Census 1939 with difference in higher proportion of old population, 34 percent in 2050 compared to 9 percent in 1939 (Andreev and Vishnevsky, 2004).

The World Bank’s Poverty Assessment Update estimated the unemployment rate at 30 percent compared to the official rate of 2.2 percent (September 2004). ’ Tajikistan’s working population represents 55 percent o f total population.

3

CIS countries and Russia, combined with a shared cultural background and language, facilitated easy entry and exit for the Tajik migrants. The main destination countries were, and continue to be, Russia and Kazakhstan. Today’s emigration i s characterized as “temporary” as confirmed by responses to the 2005 migrant survey in Tajikistan where 90 percent o f migrants reported that they had no intention o f settling abroad. According to the State Migration Services, most migrants are from Khatlon, RRS, and Sogd regions.

11. Much of the migration from Tajikistan is undocumented. Despite restrictive migration policy and tight administrative control in Russia, migrants have overcome these barriers. Based on self-determination o f legality* by the survey’s respondents, about 4.2 percent of the migrants surveyed were categorized as legal; all others (most o f whom carried only a passport) were deemed irregularhllegal migrants. The number o f illegal Tajik in Russia i s unknown but large as the Ministry o f Labor and Social Protection reported that only 10 percent o f migrants work legally in Russia.’ A free visa regime and weak enforcement enable migrants to cross borders and bribe their way into Russia. Tajik migrants in Russia are considered illegal” because they fail to obtain residence permits upon their registration as foreign citizens within 72 hours upon arrival in the country or they do not have employment permits. Russia s t i l l maintains internal administrative controls, including the registration system, a legacy o f propiska.” Most jobs in Moscow are only open to residents o f the city and the Moscow region even though i t i s against Russia’s Constitution. Although a lack o f legal status makes Tajik migrants vulnerable to bribes and extortion, the survey on income of migrants proves that they are s t i l l better o f f than in their home country.

WHO ARE THE MIGRANTS?

12. Table 2: Tajikistan’s Demographic Profile demographic characteristics o f Tajik migrants. Ethnic Taj ik 81%

average age o f 34 years, married, and have Male 86%

Table 2 provides a summary o f the

They are mainly ethnic Tajik, male, with an Married 72%

5 dependents. The travel alone and mainly Average age 34 head for Russia 1Y where they find job Average No. Of

No. Of months in migration (median) Source: Zerkalo’s Survey, M a y 2005

5 9 opportunities, a common culture and language,

and existing social network^.'^ The cost o f travel i s relatively low at about US$200 per trip by plane or train. Their main motivation to migrate i s higher income to provide food and necessities for their families back in Tajikistan. About 49percent of migrants remain abroad for 9 months. This profile i s s i m i l a r to that o f Mexico, except for the level o f education. The f low o f circular Mexican migrant laborers heading to the United States i s mostly made up of males (94.4 percent), between the ages o f 25 and 34

T h i s i s based on the respondents’ answers whether they camed a series o f documents (asylum papers or a work permit

Tajikistan Media Monitoring, March 10,2006. and passport) with them when they traveled abroad.

lo The Report on “Combating Trafficking in Human, Its Consequences and forms of Forced Labor in Central Asian Countries and Russian Federation,” estimated that about 15-18 percent of Tajik migrants legally reside in Russia. ” In the Soviet Union, the propiska or resident permit system required persons to register before being allowed to migrate to a new location. Though this system did not completely capture all migration flows, i t was a useful tool in tracking migration flows.

Destination cities in Russia are Moscow, St. Petersburg, Ekaterinburg, Novosibirsk, Chelyabinsk, and Krasnoyarsk. l3 A detailed demographic profile of migrants i s documented in “Migration and Return--The Case Study of Tajikistan,” The World Bank, ECA Migration Study, 2005. T h i s profile i s consistent with data provided by the State Migration Service.

4

(37.3 percent), with fewer years o f schooling than the national average for Mexico, married (57.9 percent) and are the head of the household (65.1 per~ent) . ’~

13. The lack of legal residence and work permits oblige Tajik migrant workers to accept unskilled and low paid jobs. A recent OECD study found that Tajikistan had one o f the highest levels o f out-migration o f skilled workers in the region (Figure 1). The Zerkalo survey found that one-third o f migrants had secondary andor technical education. Despite their education, about 62 percent o f Tajik migrants appeared to be employed in the construction sector.

Figure 1: Migration of Skilled Workers in Eastern Europe and the Former Soviet Union

7

0 5 10 15 20 25 30 35 40 45 50

Expatnates that are highly skilled (% of total expatriates) 1

Source: OECD.

14. Migration has clearly improved the financial situation of Tajik migrants and their families. Table 3 provides a snapshot Premigrat ion $30 o f the financial status o f a typical migrant $274 based on self reporting from the survey. $9 1 Overall, migration increased the income o f migrants 10 times compared to what they earned in Tajikistan (US$274 per month compared with pre-migration income o f US$30 per month). About 48 percent o f this income i s remitted to families in Tajikistan, thus resulting in an average monthly income o f about US$131 per household. Remittances have enabled families back home to afford food, clothes and utilities to a much greater degree.

Table 3: Financial Snapshot of a Tajik Migrant Average monthly income (excluding Unemployed)

During migration Post migration Saving/Income 0.0 15 Remittances/Income 0.476

Source: Zerkalo

l4 The data i s based on the ENEFNEU Survey (Encuesta Nacional de Migracidn a la Frontera Norte y a 10s Estados Unidos) carried out by the Centro Nacional de Informacidn y Estadisticas del Trabajo to obtain an accurate estimate of Mexican workers in the United States and their socio-economic characteristics. See Germin A. Zirate-Hoyos, 1999. “A New View of Financial Flows from Labor Migration: A Social Accounting Matrix Perspective,” E.I.A.L. Vol. 10, No. 2, July-December 1999.

5

OVERVIEW OF REMITTANCES IN TAJIKISTAN

sharply during the past few years and are hrge as a portion of GDP (Figure 3). According to the NBT, inflows o f migrants’ remittances tripled from US$78 million in 2002 to US$465 million in 2005. The rapid growth o f official remittance inflows i s due to several factors: increased emigration in response to the demand for labor,

15. Remittance flows into Tajikistan have a strong seasonal orientation that reflects the temporary nature of migration to Russia. The private inflows o f funds transferred through the banking system and captured by the National Bank o f Tajikistan (NBT) in the balance of payments oscillated during the year (Figure 2). They peak in October after the demand for short-term labor in Russia reaches i t s highest.

5000

4 0 0 0

3 0 0 0

~ 2 0 0 0

450 0

350 0

2 2 5 0 0

50 0 0 0

2005 2003 2044 2000 2001 2002

innows O U ~ O W S

Figure 2: Tajikistan - Monthly Funds Transfer through Banking System (mil. US$)

90 0 80 0 70 0 60 0 50 0 40 0 30 0 20 0 10 0 0 0

Jan Feb Mar Apr May Iun Iu l Aug Sep Oct NOV Dec

- c 2 0 0 2 + 2003 2004 2005

Subsequently, they taper of f during November and December as winter slows the demand for labor, especially in the construction and agricultural sectors.

l5 Resolution No. 445, dated 25 September 2001, cancelled the resolution of Council o f Ministers of the Republic of Tajikistan No. 587 of 29 November 1993 “On State duty rates” that imposed 30 percent state duty on incoming money transfers from abroad. l6 T h i s i s due to a significant enlargement o f the network o f money transfer offices in all regions of Russia, CIS and FSU. l7 Anecdotal evidence suggests that the financial and banking system has been re-monetizing fast, with deposits in banks to assets and to GDP ratios increasing throughout the whole region and Russia. The NBT17 estimated that the number o f individual accounts in banks has steadily increased during the last three/four years, indicating improved confidence levels and intermediation deepening.

6

17. Remittances play an important role in the balance of payments. Table 4 shows that if labor services are considered as exports, migrants' remittance inflows rank second after aluminum and ahead o f cotton fiber. They accounted for nearly one-third o f merchandise exports and financed about 70 percent o f the trade deficit fueled by imports induced by increased income associated with remittances since 2000. Remittances also tower above foreign direct investment and other transfers generated by official development aid flows. In 2005, gross remittance inflows doubled the stock o f Tajikistan's inter-national reserves.

18. International comparisons of remittance recipients, as a share of GDP, shows that Tajikistan ranked the fourth among the largest remittance recipient countries in the ECA region in 2003. Table 5 shows that Moldova, Bosnia and Albania rank the first, second, and third, respectively. According to the revised official statistics, remittances to Tajikistan accounted for 11 percent of GDP, compared to an aggregate o f 14 percent of GDP for all high emigration countries. In nominal terms, Tajikistan's remittance receipts rank the

Table 4: Tajikistan Balance of Payments 2000 2001 2002 2003 2004 2005

Trade Balance Exports of which: Aluminum

Imports Cotton

-23 -125 -125 -204 -151 -319 788 652 699 799 1088 1107 424 398 399 430 563 563

92 71 128 193 162 144 811 777 824 1003 1239 1426

Service Balance 4 -8 -36 -54 -89 -117

Net Transfer 37 131 184 329 236 432 of which: Net Migrants' Remittances 0 -1 65 82 133 321

Inflows 1 4 78 146 252 465 outflows -1 -5 -13 -64 -119 -144

Current Account Balance -18 -74 -34 -19 -82 -79 Financing: Net Public Sector Borrowing 39 6 14 32 -169 50 FDI 24 9 22 32 272 55 Changes in Reserves 1 -9 21 35 -54 -41 Others 46 -68 23 80 -33 -15

Stock of Internatonal Reserves 87 96 96 135 189 224 Memorandum items: Gross RemittanceslExports 0% 1% 11% 18% 23% 42% Gross Remittancesmrade Deficit 3% 3% 63% 72% 167% 146% Gross RemittancesFDI 3% 47% 356% 456% 93% 852% Gross Remittmemet Borrowing 2% 70% 560% 456% -149% 932% Gross Remittmces/Gross Reserves 1% 4% 82% 108% 133% 207%

Net Income -36 -72 -57 -90 -78 -75

Sources: National Bank of Tajikistan and IMF.

Table 5: ECA's Largest Developing Country Recipients of Remittances, 2003 Remittances Migrants GDP Remittances Remittances

Mill. US$ in Mill. Mill. US$ per migrant % of GDP

Moldova 465 1 1,566 603 29.70% 785 23.20% Bosnia and Herzegovina 1,178 2 5,072

1 4,411 986 20.20% Albania 889 133 11.10% Tajikistan 146 1 1,313

Kyrgyz Republic 108 1 1,539 163 7.00% 247 6.60% 189 6.20% Armenia 168 1 2,700

Macedonia, FYR 171 0 3,565 548 4.80%

High Emigration

Georgia 246 1 3,737

REGIONAL AGGREGATES South Asia 27,127 14 817,617 1,883 3.30%

17,049 13 524,755 1,327 320% Middle East and North Africa 6,026 8 327,117 731 1.80% Sub Saharan Africa

Latin America 34,425 31 1,987,349 1,114 1.70% 12,406 5 1 887,472 231 1.30% ECA

East and Southeast Asia 24,997 21 8,065,940 1,182 0.30% 173,103 177 33,527,651 980 0.50% WORLD

Source: The World Bank, "Enhancing Gains through International Labor Migration in Europe and Central Asia" (2005).

second lowest (US$146 million) after the Kyrgyz Republic (US$lOS million).

111. ALTERNATIVE ESTIMATES OF REMITTANCES

19. Despite the importance of remittances, there is great uncertainty regarding their actual levels and growth rates. There i s no consensus on the true size o f remittances. Remittances are private transfers and are notoriously difficult for any government to monitor and measure as unknown amounts are transmitted through informal channels, including carrying by self and friends or through intermediaries. In general, official remittance statistics shown in the balance of

7

payments” around the world are grossly under-reported. A recent World Bank survey o f central banks found that 75 percent do not attempt to estimate the amounts at all.19 Tajikistan’s official estimate, for example, excludes remittances sent through informal channels. I t i s well known that a large number of Tajik migrants work illegally abroad and travel back to Tajikistan with their earned salaries in cash or send money through informal channels. They do not trust the banking system or cannot access official money transfer systems because they are abroad illegally and do not have access to foreign bank accounts. Moreover, they may well find i t more convenient and cost effective to bring money back home with them directly rather than pay intermediaries as a large number o f Tajik migrants work abroad on a short-term seasonal bask2’

____

Box 1: Official Estimate of Remittances The Global Economic Prospects 2006 defines remittances as the total sum o f workers’ remittances, compensation o f employees and migrant transfers. The Tajikistan’s balance o f payments, however, records only workers’ remittances and omits the remainder due to a lack o f information.

The estimate o f workers’ remittances i s based on fund transferred through the banking system (wire transfer, travelers check, money orders, and money transfer system) that i s reported periodically by commercial banks. The NBT conducted two surveys o f migrants twice a year. This has enabled the NBT to differentiate migrants’ transfers from export receipts. Previously, NBT classified all single transfers o f more than US$l,OOO plus 50 percent o f transfers between US$l,OOO and US$3,000 as migrants’ transfers; while all single transfers o f more than US$3,000 and 50 percent o f transfers between US$l,OOO and US$3,000 are export receipts. This method yields the ratio o f workers’ remittances to export receipts o f 60:40. The inflows o f workers’ remittances in the balance of payments were estimated at US$252 and US$380 million, respectively in 2004 and 2005, compared to total fund transferred through the banking system o f US$430 and US$664 million during the same period. The official estimate o f Tajikistan’s workers’ remittance inflows now accounts for 12 percent in 2004 and 17 percent o f GDP in 2005.

The NBT i s currently improving the above estimation methodology by calculating the ratio of migrants’ transfer to exports directly from the surveys in stead o f using all single transfers (over and above US$3,000). The surveys in 2005 indicated that the share o f migrants’ transfers in total bank transfers has increased to 70-75 percent. Source: World Bank Staff.

The Technical Sub-Group on the Movements of Persons (TSG), chaired by UN Statistics Division with membership from central banks, international and national statistics organizations recommended that workers’ remittances in the balance of payments be replaced by a new component “personal transfer.” T h i s includes all current transfer in cash or in kinds received by resident households to or from other non-resident households. A new aggregate, “personal remittances” should be reported in the balance of payments as a memorandum item including current and capital transfer both in cash and in kind made or received by resident households to or from non-resident households, and net compensation of employees from persons working abroad for a short period of time (less than one year). l9 Martinez, JosC de Luna (2005). Workers’ Remittances to Developing Countries: A Survey with Central Bank on Selected Public Policy Issues, Washington, DC: World Bank, Mimeo. *’ Three main types of Tajik labor migrants are distinguished-permanent, seasonal, and shuttle. Permanent migrants, hired under formal working contacts or informal working relationships, remain in host countries for more than one year. Seasonal labor migrants, usually unskilled workers travel individually or in groups to Russia throughout March to November to work mostly in construction, mining or agriculture, and are mostly employed under informal contractual agreements. Shuttle workers travel individually or in groups and more periodically than seasonal workers for short period of times under established and de facto labor networks. These types of workers are relatively more skilled than seasonal workers. Also these workers tend to travel with cash rather then sending money through formal channels.

18

8

20. Understanding the true size of remittances is essential for policy makers. Reliable remittance data can contribute to prudent monetary policy managernent.’l I t also provides inputs for the formulation of appropriate policies and products to improve income and l iving conditions of migrants and their families. Further, reliable data on the size o f remittances can encourage private investment to improve infrastructure for transfer services that w i l l reduce cost, improve access, and develop innovative financial products. This wi l l better integrate migrants into the banking system, increase the deposit base and thus deepen the financial sector and increase productive investment. Finally, better remittance data w i l l enable monitoring o f cross border flows o f money and the timely detection o f money laundering or other i l l ic i t activities that undermine the integrity o f the financial system.

21. Absent reliable data, efforts have been made to estimate the true size of remittances; however, there is no consensus as to their size. These estimates are based on different assumptions regarding migrants’ remitting behavior and number o f migrants. A variation of techniques to improve remittance statistics in labor sending countries has been developed during the past several years. The standard techniques commonly employed in the literature include both a direct and indirect approach. The direct approach relies on scaling up the estimate of remittances derived from the household budget survey2* and survey o f labor migrants, while the indirect approach i s based on an application o f estimated parameters of a cross country regression analysis.

22. Alternatively, remittunces can be estimated from income remitted to migrants’ families drawn from a labor migrant survey. Such a survey would provide two estimated values of the annual average remittances per capita that are congruous. The estimated remittances for the whole country in any year are generated by the product o f the estimated annual average per capita remittance and the stock o f migrants. The estimated remittances using both values o f annual average remittance per capita are slightly different and amounted to 28 and 29 percent o f GDP in 2004. However, this method i s also subject to the accuracy of the stock o f migrants and the bias o f the survey. An indirect estimate o f remittances was performed by using a percentage of migrants remitting funds through an informal channel to scale up the official remittances reported in the balance o f payments. This method gives a remittance total o f US$360 million or equivalent to 17 percent o f GDP in 2004. Annex 2 discusses the estimated values of remittances using the data drawn out from the survey o f migrants and the available estimated stock of migrants by various researchers and government sources.

21 If unrecorded remittances are extremely large, then setting sound macroeconomic policy may be complicated by an appreciation of the national currency and inflationary pressure in light of limited monetary policy instruments and a shallow foreign exchange market. 22 The household budget survey, which ideally should capture a complete picture o f household remittance income transmitted through formal or informal channels, produces a disappointing estimate of remittances. Assuming that the survey sample i s nationally representative, i t i s possible to ‘scale’ up the responses into a national picture of aggregate remittance amounts. However, the estimated remittances obtained from scaling up the Tajikistan Living Standard Survey in 2003 i s US$23 million or only about 1 percent of GDP, lower than the official remittances in the balance of payments (US$146 million), establishing a lower bound estimate of remittance levels. T h i s i s clearly due to under- reporting by Tajik households to questions about their expenditures and revenues. The household survey approach may not represent the best method to produce reliable point estimates. However, the approach i s useful in constructing broader interval estimate o f remittance levels when combined with other estimation methods subsequently discussed.

9

23. The recent estimation method of remittances is based on regression analysis.23 A recent World Bank and IMF study conducted a regression panel that sought to predict remittance levels with respect to a number o f explanatory variables-including workers’ income, predicted costs o f sending remittances through informal channels, effect o f dual exchange regime, net errors and omissions (capital flight). Applying the estimated parameters to Tajikistan, i t results in remittance inflows equivalent to 22 to 30 percent of GDP in 2004, where the lower estimate corresponds to reducing the fee o f remittances transferred through informal channels to 5 percent, and the higher estimate corresponds to reducing the cost to 2 percent.

24. The foregoing discussions on the estimation of remittances single out the need to improve the quality of statistics on migration and remittances in Tajikistan. In January 2004, the State Migration Committee introduced the Migration Registration Card24 to monitor international migration. However, the statistics are likely underestimated because o f misreporting caused by weak capacity in data processing and compilation, and weak administrative control by the State Border Control Committee responsible for collecting cards from travelers. The National Bank o f Tajikistan could improve the coverage o f the remittance by providing detailed remittances sent through various channels including informal channels. The statistics from the latter sources can be captured through a survey o f migrants. According to the survey o f the central banks in 40 countries, 10 o f them (Costa Rica, Ecuador, El Salvador, Honduras, Indonesia, Mexico, Moldova, Nicaragua, Peru, and Russia) have developed tools to measure the volume o f remittance inflows that occur through informal channels.25 In these countries, information i s normally collected through surveys o f migrants visiting their home country and/or household surveys.

Box 2: Estimate of Remittances through Informal Channels

The Moldovan National Bank’s procedures for recording migrant’s remittances in the Balance of Payments does record some transfer through informal channels. In addition to the standard practice o f obtaining remittances transfer data from banks, the central bank monitors foreign exchange transactions made at bureaus de change and in the purchase o f goods in which foreign currencies are often used (e.g., automobiles). In this way, the Bank i s able to pick up some o f the funds that move into the country from abroad but are not sent through formal channels.

Ecuador and Honduras conduct surveys o f migrants at the country’s main points o f entry (usually airports) every year, especially during holiday seasons when the inflow o f migrant visitors reaches its peak (e.g., Christmas and New Year, Easter, Chinese New Year).26

I

El Salvador conducts household surveys every year to estimate the total volume that they receive in remittances either through formal or informal channels.

Sources: The World Bank, Moldova: Opportunities for Accelerated Growth- A Country Economic Memorandum, 2005. JosC de Luna Martinez (2005). 1

23 Freund, Caroline and Nikola Spatafora (2005),” Remittances: Costs, Determinants, and Informality,” Washington, DC: World Bank and IMF. 24 The card includes information on purpose, terms of departure, and estimated duration of trip. 25 Jost de Luna Martinez, Workers’ Remittances to Developing Countries: A Survey with Central Banks on Selected Public Policy Issues, the World Bank (2005). 26 The survey did not assess the scope, methodology and adequacy of the surveys conducted by this group of countries. T h i s i s an issue that deserves much more attention in the future.

10

IV. TRANSFER METHOD, USES, AND IMPACT OF REMITTANCES IN TAJIKISTAN

TRANSFER METHODS OF REMITTANCES

25. The Policy Note now turns to examine the main methods of transferring remittances in Tajikistan. Remittances “flow” to Tajikistan via both formalz7 and informalz8 channels. Table 6 shows that about 70 percent o f migrants interviewed remitted money through a formal channel, the remaining remitted through informal channels. Due to the low level o f the average remittance and the amount o f money transfer per migrant, i t i s quite common that remittances are pooled and transferred to Tajikistan in a single transaction by individuals residing in the sending co~n t ry . ’~

26. informal channels is driven by and Transport Mode

electronic uavments and banks,

The choice between formal and Table 6: Correlation between Methods of Transfer

transaction cost, level of trust in Mode of Transport Methods of Transfer Automobile Plane Train

2% 10% 13% 3% 20% 20% 0% 1% 1%

preference fo; cash, level of education and skill. A low transaction cost postofices

Operators

(transfer fee), increased confidence in the Friends/Acquaintan=s 3% 10% 12% 0% 0% 1%

cash, and a high level o f education and 10% 42% 48% banking system, weak preference for ~ ~ ~ n T ~ ’ ~ ~ & ~ ~ 0% 1% 1%

skilled migrants likely promote the Use Of

formal transfer channels through the banking system. There are also preferences related to proximity and accessibility o f migrants an2 relatives to banks and other intermediaries. Although the cost o f sending cash through personal courier and friends i s zero, the risk o f carrying cash i s high for Tajik migrants due to informal payments to Russian, Uzbek and Tajik customs and immigration officers, particularly for those who travel by train and car that cross multiple borders. The majority o f migrants traveling by plane (74 percent) and by train (71 percent) send money through official channels, while only a small number o f migrants used informal channels to remit funds (Table 6).

Source: Zerkalo, Migration Survey Report, Tajikistan 2005.

27. The most popular method of formal transfer among migrants is through money transfer systems because they are relatively cheap, fast and they require no bank accounts. Money transfer systems have become a preferred mode to remit funds to Tajikistan among migrants. About 60 percent o f respondents who remitted through formal channels chose money transfer operators, while 36 percent chose bank transfers. There are a number o f money transfer

’’ Formal channels include banks and specialized money transfer systems, and the postal system. Banks and money transfer systems form the financial system infrastructure in the recipient country. The postal system in Tajikistan supports the financial system infrastructure, although i t does not provide savings or other payments services. Non-bank financial institutions do not play any role in this segment, given the nature o f their business and their chronic underdevelopment. Microfinance institutions, although relatively developed and active in Tajikistan, do not yet intermediate in the remittances segment, due to their limitation from providing basic financial services and their inability to access the payments system.

z8 Informal channels include personal carrier of cash through the borders by self or friends, or pool their earnings and transfer them through trustworthy travelers, who in turn take care o f the delivery to workers’ and migrants’ relatives. T h i s i s quite common in Tajikistan, mainly due to the l ow density o f the average remittance and money transfer per migrant. Pooling in fact helps abate transaction costs, as some remittance service providers, and especially banks, charge flat fees irrespective o f the amounts sent. 29 Pooling in fact helps abate transaction costs, as some remittance service providers, and especially banks, charge flat fees irrespective o f the amounts. The same individuals organize the distribution o f remittances to migrant relatives in the respective recipient country.

11

systems operating in Tajikistan and they all integrate into the banking system through partnerships and contract agreements. They operate from the premises o f commercial banks and share fees almost equally. Most transfers through money transfer systems are made on a cash-to- cash basis. Competition among the money transfer systems helps drive down the cost of transfers. (Details on transfer fees and speed o f these systems operating in Tajikistan are described in Annex 3.) B y contrast, inter-bank money transfers (account-to-account) are infrequently used among migrants because of difficulties in opening bank accounts and foreign exchange regulations limiting the amount that can be transferred. The Zerkalo survey (2005) indicates that only 18 percent o f migrants have bank accounts because their illegal status l i m i t s access to the banking system in host countries. Transfers through post offices are insignificant due to high cost (10-12 percent) and slow speed (2-3 weeks) despite their extended outreach into rural areas. (Annex 2 provides details on transfer channels and costs for remitting funds by Taj ik migrants.)

28. Informal channels for transferring remittances include self-carrier, friends and acquaintances due to the zero cost of transfer or their illegal status. For example, illegal Tajik migrants residing in Russia do not leave their residence to go to commercial banks to transfer funds for fear of harassment by Russian police and deportation. Instead, they send money to friends or acquaintances that in turn w i l l carry or transfer funds and distribute them to their families back home. According to the survey, about 26 percent o f migrants sent money to their families in Tajikistan through friends.

29. In addition, anecdotal evidence shows that some banks have formalized business relationships with a number o f Tajik individuals permanently residing in Russia involved in providing labor opportunities for seasonal and shuttle migrants. These individuals are generally trustworthy and well known by Russian employers and Tajik workers. Together with providing job opportunities, they also provide remittance services by sending- receiving- distributing remittances through their bank accounts in both Russia and Tajikistan. They work against a commission, the value o f which remains unknown. The benefits o f these business relationships are significant: migrants find temporary jobs and a secure and accessible way to send money to their relatives all the while addressing cultural and language barriers when i t comes to dealing with Russian money transfer systems and banks. Tajik banks build these relationships in order to expand the client base, profit from remittance commissions, and increase the average value of remittances and thus decrease the transaction cost for the bank. This i s because banks and money transfer commissions and fees are in most cases based on a percentage of the transferred amount, irrespective o f the value o f the transaction. As a result, the higher the value of the remittance, the less paper work and fixed costs for the bank and the money transfer system.

Box 3: Cross-selling by Tajik Commercial Banks

Some commercial banks have slowly begun to sell financial products to migrants. In general, Tajik banks are neither particularly focused on, nor capable of, servicing remittances. A few banks with a more extensive branch network in the country (AIB, Orion Bank, Tajiksodirot and Eskhata Bank) have just begun targeting migrants and remittances as an important element o f their business. Two Tajik banks have so far established specialized units to provide a range of banking services other than simple savings to migrant clients and their relatives (including small loans).

12

30. Tajikistan’s formal transfer system for remittances is e f l~ ient ,~ ’ especially through the money transfer operators. The country has been successful in reducing cost by removing a transfer tax and creating an enabling environment that promotes competition among banks in partnership with the money transfer systems. Further, the exchange rate spread i s insignificant due to no restrictions on cash withdrawal in foreign currencies. The analysis of financial infrastructure, costs, speed, and outreach discussed in Annex I1 reveals that money transfer operators offer high speed services at a relatively low cost.‘ Senders are not required to have bank accounts and only need to show an ID card if they use cash-to-cash or cash-to-account transfers. The cost of transfer that i s paid entirely by remitters in sending countries to money transfer operators i s relatively low (between 1.5 percent and 5 percent o f the remitted amount), compared to other countries.31

3 1. Disbursement of remittances mostly takes place in Dushanbe at locations where commercial banks operate. The low density o f the rural economy, weak communication infrastructure, and low profit for retail banking in the regions and rural areas l im i t s the outreach o f banks. Two commercial banks, A B and Amonat, have the largest branch networks in the country, with about 80 branches each. Amonat bank, in particular, plays a critical role in delivering fiscal and quasi-fiscal payments in the rural areas (almost on a monopolistic basis); however, i t s technology i s cumbersome. Only 10 percent o f the branches are connected to headquarters, which makes i t impossible to consolidate bank accounts on a daily basis. Most transfers are made on a cash-to-cash basis because of, in part, a low level o f thrust in the banking system due to prior unstable macro-economic environment, the effects o f banks failures and closures and the three mandatory monetary conversions during the last decade, which sharply eroded savings (Box 4).

Box 4: Tajikistan’s Banking System

The level o f development o f the Tajik banking sector i s relatively low compared to other countries in the FSU and the CIS. I t i s currently undergoing a profound stabilization and consolidation process that has resulted in the exit o f insolvent banks and the divestiture o f KreditInvest from AIB bank. Consequently, asset quality, the overall capitalization o f banks, and the capital adequacy ratio have improved, and non-performing loans have declined. Although the banking sector i s growing rapidly in terms o f credit to the private sector, i t s t i l l faces a lack o f long-term financing, an inadequate deposit base, and low capacity to intermediate their capital base.

The banking sector includes 14 banks, with only one bank fully owned by the state, Amonat Bank (former savings bank). There i s only one foreign commercial bank operating in the country, and one microfinance bank fully owned by the Aga Khan Foundation (established in 2003). The sector remains concentrated, with four large banks (Orion Bank, AIB, Tajiksodirot and Amonat Bank) controlling 70 percent o f assets, 80 percent o f household deposits and 70 percent o f credits to the economy. The economy i s highly dollarized and the inter-bank market i s not yet developed to acceptable standards, mainly due to weakness in monetary policy management, lack o f a government securities market, high degree o f dollarization and lack o f trust among bankers.

30 An efficient transfer service i s characterized by low transfer costs, increased speed, and better access. 31 Bank charges in the Philippines, exclusive of the foreign exchange spread and recipient charge, range from about US$5 for a transfer from a foreign account to a branch account in a single bank, to about US$16 which may include courier services (Kevin Mellyn, “Worker Remittances as a Development Tool Opportunity for the Philippines, p. 12 (June, 2003). The average cost of transfer money from the US. to Mexico was 7.3 percent in February 2004.

13

USES OF REMITTANCES IN TAJIKISTAN

32. According to the survey of migrants by Zerkalo, most recipients used funds for purposes of consumption, education, health, home repair and savings. Nearly one-half o f respondents (47 percent) indicated that they used remittances for c o n s ~ m p t i o n , ~ ~ 22 percent used remittances for education and health care, 15 percent for home repair, and 10 percent for saving. These findings show that about 37 percent o f respondents uscd remittances for personal investment

Figure 4: Tajikistan Uses of Remittances (% of Respondents)

, . . 0% 5% 10% 15% E3% 25% 30% 35% 4% 45% 50%

(human capital and home repair), while only 3 percent o f respondents used remittances for income generation activities and asset accumulation. Unfortunately, further insight i s limited as information on the share o f these expenditures in total remittance use i s not available from the survey.

33. The level of income dictates the type of spending. Given a low level o f income o f about US$131 per month (based on estimates o f remittances a migrant transfers to his family in Tajikistan), a Tajik household with 5 dependents w i l l likely spend the majority o f their income- including remittances-on priority expenditures (consumption and other basic needs). For this reason, i t i s unlikely that any significant amount of funds wi l l be left over for productive investment. However, an increase in income after several years o f working abroad tends to lower the marginal propensity to consume, thus increasing the scope for recipients to use remittances for productive investment, and more so given a favorable business environment. This includes income generation activities in rural areas, small and medium businesses, and bank deposits that wi l l be invested indirectly.

34. However, migrants’ ability to save and invest is limited by several factors. Bank saving deposits are discouraged due to a lack o f t rust in the banking system33 and a low level o f interest rate. As remittances reach Tajikistan, they are mostly withdrawn in cash in various currencies (U.S. Dollar, Russian Ruble, Euro, and Somoni) and typically kept at home “under the mattress” or used to accumulate assets (car, house, and land). The NBT survey indicated that 82 percent of respondents were not ready to deposit remitted funds in the banking system and 62 percent said that they needed money for current household consumption and business transaction^.^^ Only small amounts are converted into savings in the banking system; however, deposits in commercial banks has increased in recent years (deposits by individuals doubled from 1 percent in 2002 to 2 percent o f GDP in 2005 and deposits by legal entity and individuals increased from 4 percent in 2002 to 7 percent o f GDP in 2005).

-

Consumption i s defined as the sum of expenditures on food and clothing, purchases o f goods, social activities, charity, and paying off debts. 33 T h i s i s due to the prior unstable macro-economic environment, the effects o f bank failures and closures and the three mandatory monetary conversions during the last decade. All this resulted in people’s savings being sharply devalued and eroded. 34 IMF, “Labor Migration and Remittances” in Tajikistan--Selected Issues and Statistical Appendix, March, 2005.

32

14

35. Similarly, an unfavorable business environment in Tajikistan hinders the use of remittances for investment, specifically, for income generation activities in rural areas and for small businesses in urban areas. According to an IFC survey o f the business environment in Tajikistan (2003), the majority o f SMEs found that administrative procedures are overly complex (such as access to external financing, foreign trade operations, taxation, inspection, and licensing procedure^).^^ The regulatory system i s non-transparent, application of the tax code i s uneven, licensing, inspection, standardization and certification are excessive, and harassment and corruption are frequent. Although the Business Environment Enterprise Performance Survey (BEEPS) in 2005 shows that the overall environment for doing business in Tajikistan has improved (compared to 2002); there remain serious problems regarding access to land, title or leasing o f land, business licensing and permits, labor regulations, s k i l l and education o f workers, judiciary functions, and street crime, thefts and disorders. In relation to CIS countries, doing business in Tajikistan i s worse of f in several areas including judiciary function, business licensing and permits, tax administration, transport and electricity. The access to land problem discourages remittance recipients from using funds for income generation activities in the agriculture sector. Similarly, the business licensing, permits and inspection problems limit new business entries, thus limiting the use o f remittances to a few choices including accumulating personal wealth and home repairs. The Government has recently amended the law on licensing that significantly reduced the number of activities subject to licensing, and adopted a law on micro-finance to support access o f SMEs to finance; however, much remains to be done to further improve the business environment.

IMPACTS OF REMITTANCES IN TAJIKISTAN

36. The extent to which remittances will have a maximum impact on the economy depends largely on how they are used. I t i s widely recognized that remittances provide a source of foreign exchange for financing the current account deficit, which i s associated with increased income of recipient households fueling domestic consumption and imports. The long-term developmental impact o f remittances, however, depends on the type o f remittance spending, Le., consumption versus investment. This i s important because remittances can help reduce poverty and fuel high rates o f household savings and investment. If remittance income i s spent on consumption, the impact w i l l be short-term through a spill-over effect transmitted through a multiplier. Consumption spending raises the effective demand for local goods and services and fuels imports. Future consumption w i l l therefore depend on future remittances. On the other hand, if remittances are invested directly or indirectly (through bank deposits) for the development o f local infrastructure, income generation activities and small and medium businesses, they w i l l increase capital and generate a future income stream to finance future consumption. This wi l l contribute to long-term economic growth3’ and reduce the vulnerability o f recipients to a sharp falloff in remittances and to potential remittance decay.