Enhancing Financial Wellbeing Through Voluntary...

27

Conduent Human Resource Services Enhancing Financial Wellbeing Through Voluntary Benefits January 26, 2017

Transcript of Enhancing Financial Wellbeing Through Voluntary...

Conduent Human Resource Services

Enhancing Financial Wellbeing

Through Voluntary Benefits January 26, 2017

Today’s Speakers

Ruth Hunt Principal

Engagement

Tom Kelly Principal

Voluntary Benefits

January 26, 2017 2

• Employee financial landscape

• Role of voluntary benefits in financial

wellbeing

• Making voluntary benefits work

• Questions?

3

Agenda

Employee Financial Landscape

Muscle Tension/

Back Pain

51%

31%

Migraines/

Headaches

44%

15%

Insomnia/

Sleep Trouble

39%

17%

High Blood

Pressure

33%

26%

Severe

Anxiety

29%

4%

Stomach

Ulcers

27%

8%

Severe

Depression

23%

4%

Heart

Attacks

6%

3%

• Seven out of ten under

stress

• 48% under financial stress

• One in five skipped work

• 61% impact on performance

• 75% are living paycheck to

paycheck

• 69% have less than $1,000 in

savings

People with high levels of financial stress

People with low levels of financial stress

Sources: AP-AOL Health Poll: Debt Stress: The Toll Owing Money Takes on the Body.

The American Psychology Association; PricewaterhouseCoopers, LLC; American Institute of Certified Public Accountants; Society for Human Resource Management; and Gallup.

2016 Retirement Confidence Survey, Employee Benefit Research Institute

CareerBuilder 2016 Survey January 26, 2017 4

Financial Stress in the Workplace

Source: Conduent 2016 Financial Wellbeing & Voluntary Benefits Survey.

HR leaders are “extremely concerned” or “very

concerned” about impact on financial wellbeing

71%

71%

68%

67%

67%

65%

65%

64%

64%

64%

64%

57%

Retire When Ready

Unexpected Medical Expenses

Long-Term Care/ Elder Care

Absorb Financial Shock

Right Amount of Life/Disability

Access to Financial Advice

Address Legal Issues

Reduce 401(k) Loans

Day-to-Day Expenses

Save for College

Improve Credit

Payoff Student Loans

55% Of companies are either working on implementing

financial wellbeing strategies, or plan to in the next

3 years.

78% Of employers view voluntary benefits as being

“extremely effective” or “very effective” in supporting

employee financial wellbeing.

January 26, 2017 5

Source: Conduent 2016 Financial Wellbeing & Voluntary Benefits Survey.

Top Resources Offered to Support Financial Wellbeing Future Emphasis on Voluntary Benefits

43% 43%

13%

1%

They will be part of ourstrategy.

They will be one of our threehighest priorities.

We will keep track of them,but not focus on them.

They will not be a topic weplan to spend much time on.

76%

41%

39%

36%

36%

35%

32%

31%

29%

26%

25%

24%

22%

19%

15%

Voluntary Benefits

Financial Health Assessment

Employee Workshops on Financial Topics

Financial Education Material

Retirement Planning Tools/Calculators

Money Management/Budgeting Tools

Personal Financing Guidance

Financial Wellbeing Vendor(s)

Retirement Modeling Tools

Access to Personal Financial Planners

Interactive Retirement/Investment Games

Integrated Recordkeeping Tools/Services

Retirement Drawdown Strategies

EAP

Robo-Investing

January 26, 2017 6

Financial Stress in the Workplace

Workforce 2017

5 Generations Working Together

Silents Baby Boomers Generation X Millennials Generation Z

Financial

Outlook

• Concerned with keeping what

they’ve accumulated through

proper distribution strategies

• Worry about having enough

money for retirement

• Worry about covering medical

expenses in retirement

• Concerned about long-term

care and estate issues

• Impacted by chronic and

catastrophic illnesses

• Parents report greater stress

• Ages 35-54 have delayed

paying bills more often than

other groups to help manage

finances

• Highest legal needs (wills, real

estate, etc.)

• Pregnancy cost a top medical

concern

• Underinsured with life and

disability

• Highest financial stress

• 74% say money is top worry

• 33% use credit to pay for

items they can’t afford

• 42% have student loans (78%

of these say it impacts their

ability to reach other financial

goals)

• Want discounts and

convenience programs

• Benefit needs include portable

benefits, forced savings,

financial education

• Younger employees are most

stressed by “budgeting”

• Spend more time at work on

personal finances

2% 29% 33% 35%

1%

Sources include the American Psychology Association; PricewaterhouseCoopers, LLC; American Institute of Certified Public Accountants; Society for Human Resource Management; and Gallup.

January 26, 2017 7

Employee View: The Four Pillars of Financial Success

Spend Smarter

Save More

Invest Better

Protect Wisely

“I can manage my daily finances,

absorb a financial shock”

“I’m on track to meet

my financial goals”

“I am able to enjoy life…

Throughout my lifetime”

Concepts from the Consumer Financial Protection Bureau.

January 26, 2017 8

The Role of Voluntary Benefits: Spend Smarter, Save More, Protect Wisely

A well designed voluntary benefit

offering complements and

enhances existing benefit programs

while helping to support employees’

health, wealth and security needs.

Programs are typically employee paid and payroll deducted.

Financial

Wellbeing Health

• Accident

• Critical Illness

• Hospital Indemnity

• Limited Medical

• Telemedicine

• Dental

• Vision

Wealth

• Short-Term Disability

• Long-Term Disability

• Life Insurance (Term/Permanent)

• Long-Term Care

• Financial Wellness

Security

• Legal

• Identity Theft Protection

• Auto & Home Insurance

• Pet Insurance

• Payroll Purchasing

• Student Loan Refinancing

• Discounts

• Mortgages/Personal Loans

January 26, 2017 9

It Starts with Your Priorities

Financial

Wellbeing

Business/HR Priorities

• Employee Engagement

• Attraction and Retention

• Benefit Cost Containment

• Financial Stability of Workforce

• Improve Productivity

• Decrease 401(k) & 403(b) loans

Employee Financial Wellbeing = Employer Financial Wellbeing

January 26, 2017 10

Health Strategy

Spend Smarter/Protect Wisely

Voluntary Benefits Most Likely to Offer in Next 1-2 Years*

43%

48%

54%

Hospital Indemnity

Accident Coverage

Critical Illness

Hospital Indemnity Accident Plan Critical Illness

Increased employee deductible and coinsurance cost

Out-of-pocket expense

Lower Employee Out-of-Pocket Risk

Employers “Agreed” or “Strongly Agreed” Supplemental Medical Achieved the Following Goals for HDHP Strategy:

Conduent Voluntary Benefits & Financial Well-being Survey, March 2016.

January 26, 2017 11

78% Participation in HDHP

79% Employees Satisfaction with HDHP

78% Employee Cost Savings

88% Employer Cost Savings

Health Strategy

Spend Smarter/Protect Wisely

Note: Assumes employee coverage in CDH Plan: $1,500 deductible, 20% coinsurance, $5,600 out-of-pocket maximum = $3,200.

Employee chooses:

Hospital Indemnity Insurance

Jen has baby via conventional delivery.

Employee incurred expenses for services in and out of the hospital. In addition

to what the medical plan pays, Hospital Indemnity benefits are paid directly to

the employee.

Overall hospitalization charges before deductible and copay applied: $10,000

Employee Financial Impact

Employee Medical Out of Pocket* ($3,200)

Annual Premium Payment

of Hospital Indemnity Plan ($250)

Hospital Plan Benefit Payment to Employee ($2,200 admission and $200/day for 3-day stay)

$2,800

Net Employee Out of Pocket:

With Hospital Indemnity Coverage

Without Hospital Indemnity Coverage

($650)

($3,200)

January 26, 2017 12

Health Strategy

Spend Smarter/Protect Wisely

Note: Assumes employee coverage in CDH Plan: $1,500 deductible, 20% coinsurance, $5,600 out-of-pocket maximum = $2,200.

Employee chooses: Accident Insurance

James breaks his leg and is rushed to the emergency room. (Estimated cost: $5,000)

Employee incurred expenses for services in and out of ER. In addition to what

the core plan paid, Accident benefits were paid directly to the employee.

Employee Financial Impact

Employee Medical Out of Pocket* ($2,200)

Annual Premium Payment

of Accident Plan ($135)

Accident Plan Benefit Payment to Employee $2,200

Net Employee Out of Pocket:

With Accident Coverage

Without Accident Coverage

($135)

($2,200)

Ambulance $100

ER Treatment/X-ray $250

Broken Leg $1,500

Crutches $125

Follow-up Treatment (3 visits) $150

Physician Treatment (3 visits) $75

Total Cash Benefits $2,200

January 26, 2017 13

Wealth Strategy

Protect Wisely

1. LIMRA, “Facts from LIMRA: Life Insurance Awareness Month

2. U.S. Department of Health and Human Services. longtermcare.gov.

3. National Funeral Directors Association (NFDA)

More than 50% of employees expect survivors to have trouble

covering everyday expenses if the employee were to die tomorrow1

Needs persist long after the kids have graduated college or the

mortgage has been paid off

70% of Americans 65 years old and older will need LTC assistance2

Average U.S. funeral costs between $7,000 and $10,0003

Term Life Insurance

Permanent Life Insurance

Long-Term Care Insurance

Retiree Life Insurance

January 26, 2017 14

Wealth Strategy

Protect Wisely

Group LTD plus

Supplemental DI

Group LTD

Standard LTD policies could

leave some of your high earners

with only 15% to 45% of their

pre-disability income

January 26, 2017 15

Security Strategy

Spend Smarter, Protect Wisely

Solution: Voluntary Purchasing Program

Financial Education

• Financial assessments and goal-setting

• Broad financial education

• Personalized, unbiased coaching

• Ongoing measurement of participation and progress

• Free credit report

Cash/Debt Management • Manageable payments through payroll deductions

• Easy qualification – no credit check required

• No overspending, typically limited to 6% of annual salary

Employee Engagement • Incentives for engagement

• Financial education portal with budgeting/learning tools

• Custom dashboard for key engagement metrics

Example: Meet Amber

Amber needs to buy a new refrigerator. She’s low on cash, and

her credit score is below prime.

What are Amber’s options?

70M Do not qualify for prime

credit and can’t turn to

friends and family for

help.

69% Do not have at least

$1,000 in emergency

savings.

21% Of 401(k) savers have an

outstanding loan against

their account.

January 26, 2017 16

Harris Poll on behalf of Purchasing Power, Nov. 19-23, 2015

PWC Employee Financial Wellness Survey, 2015 Results

Employee Benefit Research Institute, 401(k) Plan Asset Allocation, Account Balances, and Loan Activity

Subprime

Credit Rent-to-Own Title Loans Payday

Loans Bounced

Checks

25-41% 91% 300% 400% 17,000% Average

APR

Sources: 1December 3, 2015 CFPB report on The Consumer Credit Market

2http://scholarship.kentlaw.iit.edu/cgi/viewcontent.cgi?article=3993&context=cklawreview

3http://www.responsiblelending.org/other-consumer-loans/car-title-loans/research-analysis/CRL-Car-Title-exec.pdf

4http://www.consumerfinance.gov/askcfpb/1567/what-payday-loan.html

5http://files.consumerfinance.gov/f/201403_cfpb_report_payday-lending.pdf

6http://www.consumerfinance.gov/about-us/newsroom/cfpb-finds-small-debit-purchases-lead-to-expensive-overdraft-charges/

7https://s3.amazonaws.com/files.consumerfinance.gov/f/201306_cfpb_whitepaper_overdraft-practices.pdf

Security Strategy

Save More/Spend Smarter/Protect Wisely

Multi-Year Strategy May

Include • Student Loan Refinancing

• Mortgage Program

• Purchasing Program

• Personal Loans

• Identity Theft Protection

• Financial Planning

• Concierges Services

• Employee Discount Mall

• Auto, Home and Rental Insurance

• Pet Insurance Millennials

• Highest financial stress; 74% say money is top worry

• 33% use credit to pay for items they can’t afford

• 42% have student loans (78% of these say it impacts

their ability to reach financial goals)

• Want discounts and convenience programs

• Have challenges establishing credit and

buying homes

• Pets are the new family!

January 26, 2017 17

2% 29% 33% 35%

1%

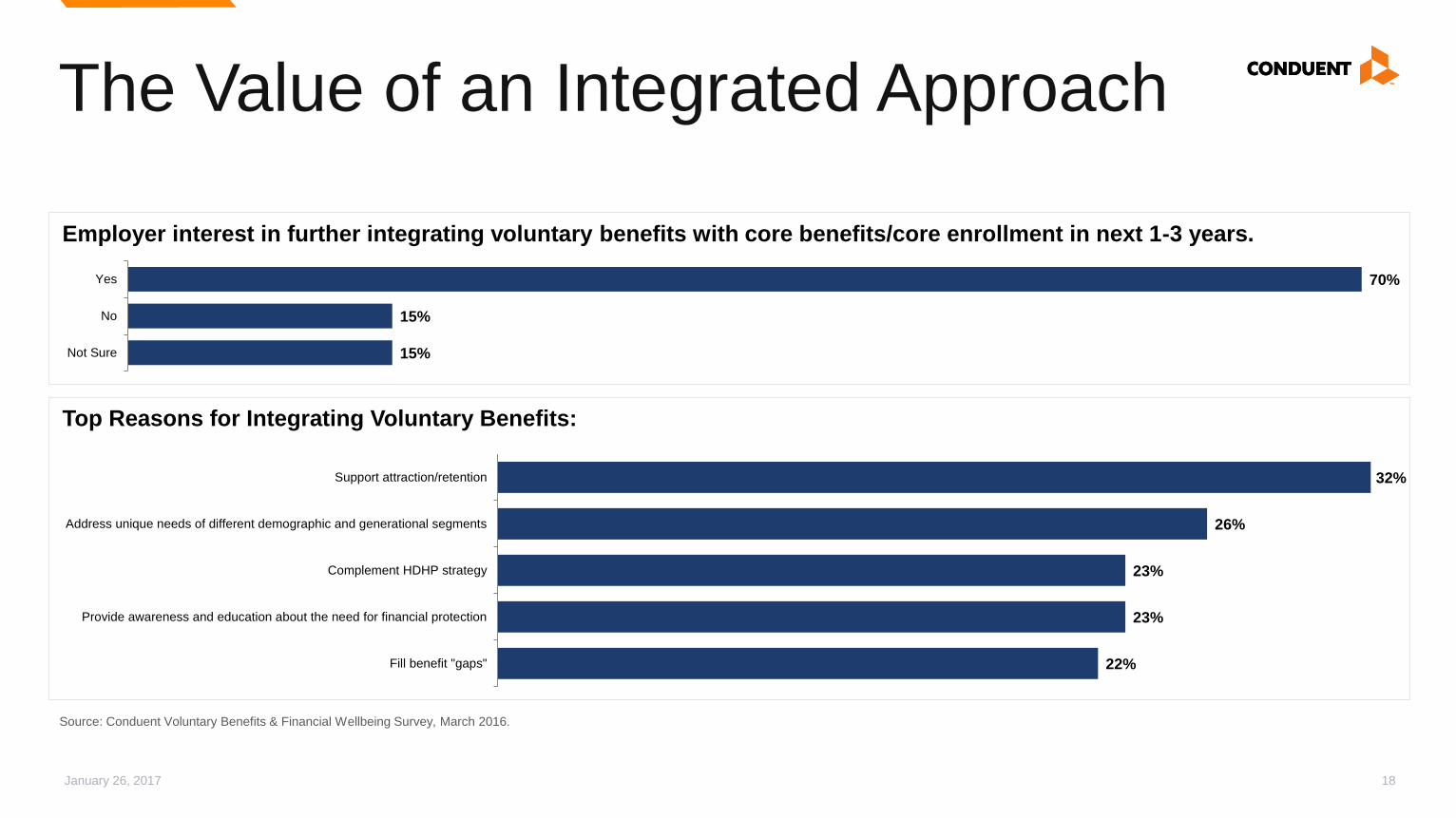

The Value of an Integrated Approach

Source: Conduent Voluntary Benefits & Financial Wellbeing Survey, March 2016.

Employer interest in further integrating voluntary benefits with core benefits/core enrollment in next 1-3 years.

70%

15%

15%

Yes

No

Not Sure

Top Reasons for Integrating Voluntary Benefits:

32%

26%

23%

23%

22%

Support attraction/retention

Address unique needs of different demographic and generational segments

Complement HDHP strategy

Provide awareness and education about the need for financial protection

Fill benefit "gaps"

January 26, 2017 18

The Value of an Integrated Approach

January 26, 2017 19

Company ABC Goal Results

Consistency • Establish consistent

voluntary benefits strategy

• Successfully harmonized voluntary benefits for over 100,000 employees

• Improved rates/underwriting

• Implemented platform and communication identity and channels

Value

Proposition &

Member

Experience

• Move VBs from an after-

thought to an integrated

part of the EVP

• Support total wellbeing

• Promote engagement and

enhanced consumerism

• Integrated with the annual enrollment process

• Aligned VB communication plan with EVP and wellbeing strategy

• Paired together like benefits (voluntary and core) during enrollment

• Increased participation in supplemental medical by over 570%

• HSA contributions rose by $116; those electing VB increased $359

Administrative

Simplicity

• Enable ease of

communication and

explanation, online

navigation, enrollment and

administration

• Successfully launched two phases of voluntary benefits

• Centralized and streamlined management of partners

• Integrated data from all vendors

• Consolidated confirmation statements (elections and deductions)

• Developed and documented administrative process flows

• Developed consolidated payroll/remittance process

Action

Orientation

• Drive engagement and

participation

• Enrolled over 20,170 across all plans

• Achieved strong participation across age groups

• Shifted average salary of purchasers from lower to mid salary levels,

demonstrating increased understanding of value across pay levels

Clients Moving from

Non-Integrated Strategy

to Integrated Strategy

Participation by policy count

after transition:

3-5x higher participation

Lessons Learned in VB Communications

January 26, 2017 20

With providers: “Partner” but customize • Co-brand where possible; if ERISA concerns, emphasize choice and use disclaimers

• Leverage vendor communications but customize to your message and integrate, e.g., leverage teachable moments at open

enrollment but also promote periodically

• Make it easy with technology – and don’t forget the spouse at home

Know your audience: Push solutions, not just products • Gather data: audience demographics, benefit elections, survey and focus group research (consider pre-testing) to prioritize

product needs and design communication strategy

• Consider “what if” scenarios to help varying employees/situations visualize personal value

• Monitor data and response for future updates

For management: Build the business case • Financial wellbeing is more than retirement and 401(k) savings plans

• Long-term saving isn’t possible without short-term financial management

• Addressing financial wellbeing also enhances physical and mental/emotional wellbeing

• Voluntary benefits can move from an “afterthought” or “add-on” to a valued part of our EVP

Examples: Branding and Messaging Strategies

Protection Appeal: Get covered; worry less

To drive understanding, perceived value, security and wellbeing

Total Rewards Appeal: Get more; something for all

Wellbeing Appeal: Get a better life

January 26, 2017 21

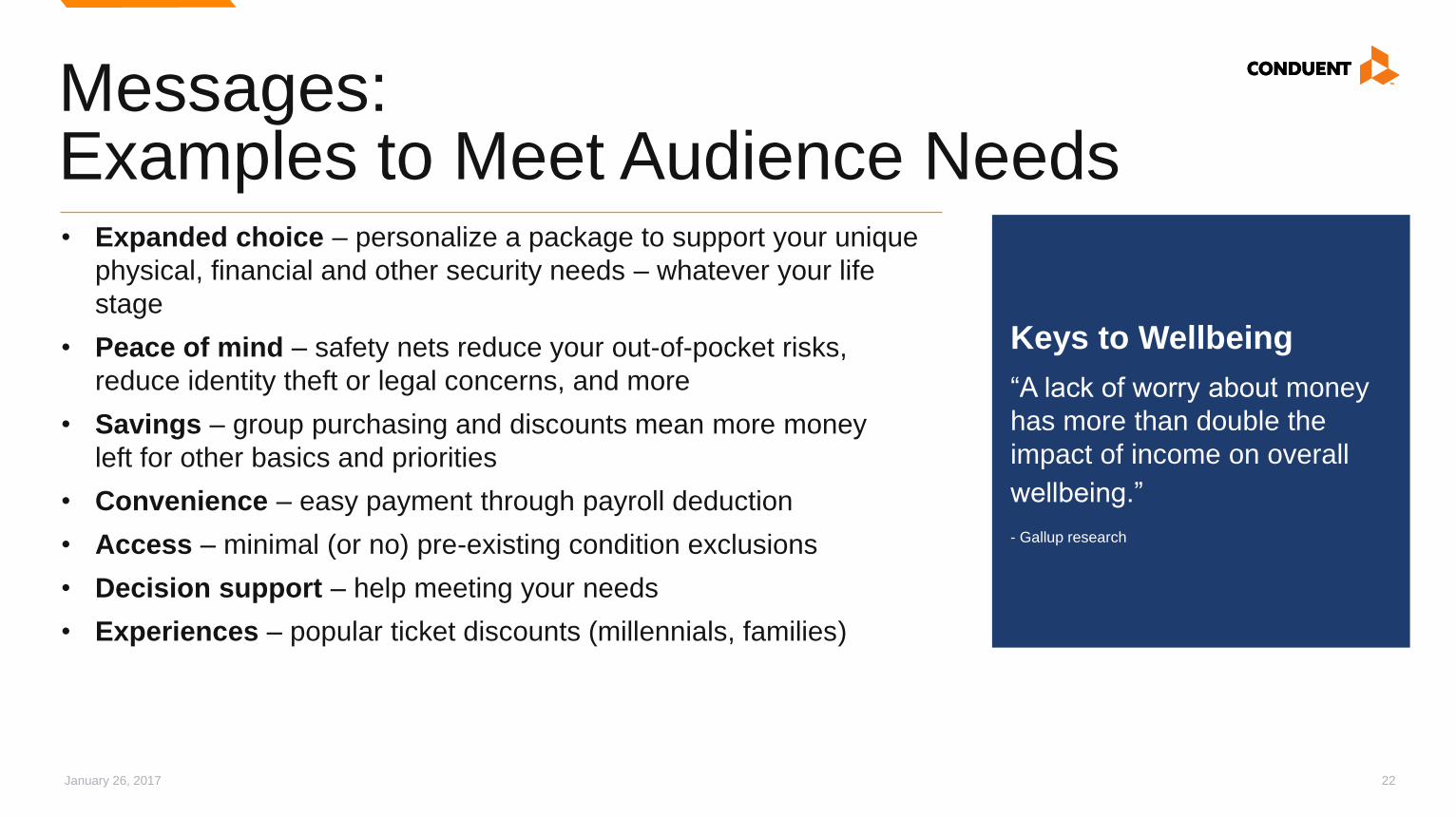

Messages: Examples to Meet Audience Needs • Expanded choice – personalize a package to support your unique

physical, financial and other security needs – whatever your life

stage

• Peace of mind – safety nets reduce your out-of-pocket risks,

reduce identity theft or legal concerns, and more

• Savings – group purchasing and discounts mean more money

left for other basics and priorities

• Convenience – easy payment through payroll deduction

• Access – minimal (or no) pre-existing condition exclusions

• Decision support – help meeting your needs

• Experiences – popular ticket discounts (millennials, families)

January 26, 2017 22

Keys to Wellbeing

“A lack of worry about money

has more than double the

impact of income on overall

wellbeing.”

- Gallup research

Tactic: Financial Wellbeing Assessment • Decision support quiz educates

while self-assessing wellbeing

needs

• Scoring can recommend

solutions and invite further

exploration

January 26, 2017 23

Scenarios Support Decision-Making

January 26, 2017 24

New supplemental medical

plans introduced

• All with no pre-existing condition limitations

• Goal to show how new plans complement the

medical plans

Enrollment results

• Consumer-driven health plan elections

doubled; HSA contributions also rose

• Supplemental plan elections

– 20% Hospital Indemnity

– 25% Accident

– 15% Critical Illness

In Closing

• Voluntary benefits play a key role in supporting total wellbeing

• Providing the right personalized mix of voluntary benefits to meet specific health, wealth and security

needs supports both employee and employer financial being

• In order to achieve desired results, create a truly integrated benefit experience for the employee and

employer including design, enrollment, communications, and administration

January 26, 2017 25

Ruth Hunt Principal

Engagement

612.805.2387

Tom Kelly Principal

Voluntary Benefits

515.330.7476

Questions?

January 26, 2017 26

© 2017 Conduent Business Services, LLC. All rights reserved. Conduent and Conduent Agile Star are trademarks of Conduent Business Services, LLC in the United States and/or other countries. BRXXXXX