Hitomi Sekine Local Government Reporting Section Division of Accounting and Reporting.

description

April 2009

Oklahoma Councilof Public Affairs

2

“I think it an object of great importance, to be kept in view and to be undertaken at a fit season, tosimplify our system of finance, and bring it within the comprehension of every member of Con-gress. … [W]e might hope to see the finances of the Union as clear and intelligible as amerchant’s books, so that every member of Congress, and every man of any mind in the Union,should be able to comprehend them, to investigate abuses, and consequently to control them.”

—President Thomas Jefferson, in a letter to Treasury Secretary Albert Gallatin, April 1, 1802

ments. They also may give important contextto information that can be gleaned fromexisting transparency initiatives.

The illustrative financial statements are notprepared in accordance with generally ac-cepted accounting principles but are preparedto illustrate how those principles might bemore useful to interested readers seeking animproved understanding of governmentperformance. The illustrative financial state-ments have not been audited, nor are theybased on audited information. These financialstatements illustrate an alternative method ofpresentation of the financial position andresults of operations of the State of Oklahoma.If the statements were prepared with theprecision required to withstand an audit, itwould require a far more exhaustive effortthan attempted by this study. Many of theamounts presented would doubtless change,and some of them almost certainly byamounts material to the financial statementsas a whole.

We cannot prosper without change

The United States faces a financial crisis, acrisis that without action is likely to overwhelmus in the next quarter century and changeforever the American experience. Withoutsignificant change, our current economicsystem cannot survive. While isolated voiceshave warned of this impending fiscal disaster,most observers and policymakers remainfixated on increasingly obsolete and irrelevantmeasures of our national debt and the valueand burden created by government activity.

For several decades, most Americans haveanticipated a retirement in which they wouldreceive a government-funded pension andgovernment assistance in meeting their healthcare bills. To receive these benefits, Ameri-cans have paid into the system. For mostpeople, the amount the federal government

Introduction

We are flying in stormy weather and we areflying blind.

A financial hurricane is building. It is biggerthan the current financial crisis launched by thesub-prime lending debacle. It is bigger thananything that has previously hit the federalgovernment. It is poised to unleash budget diffi-culties of immense dimensions.

We are flying blind because we do not under-stand our financial position or what it costs thegovernment to deliver various services. Some mayhave a sense that government spends “too much”money, but we do not know how much governmentprograms really cost, and we rarely measure thebenefits received.

The traditional methods used to measure costare methods that would land the CEO and CFO ofany public company in prison. Some things areleft off the books, especially unpleasant liabilities.In addition, current financial reporting groupscosts in ways that mask the true cost of providingservices.

The purpose of this study is to illustrate analternative way state government could report itsfinancial position and the costs of its operations.By coupling the approach outlined in this reportwith meaningful reporting on the value producedby government services, a valuable analytical toolwill emerge. Better decisions about how to allo-cate our resources and whether to increase ordecrease use of those resources should result.

The illustration of how a state government canreport its costs to the public also sets an examplefor the federal government. We can improve ourunderstanding of the nature of the problems weface and better equip ourselves to develop work-able solutions.

The illustrative financial statements in thisreport attempt to demonstrate how financialstatements that focus on cost might appear, andhow they can provide critical information notreadily available from existing financial state-

3

takes in payroll taxes for Social Security andMedicare exceeds the amount taken for incometaxes. While many observers bemoan the lack ofprudent retirement planning by those approach-ing retirement, most of those who did plan haveanticipated getting some retirement income fromSocial Security and help with medical bills fromMedicare.

However, in 2007, Medicare Part A benefitpayments began exceeding the program’s taxreceipts. By 2019, the U.S. Treasury projects thatMedicare Part A Trust Fund assets will be insuffi-cient to pay full benefits. The Treasury alsoprojects that in 2017, Social Security benefitpayments will begin to exceed the program’s taxrevenues, and that by2041, the Social SecurityTrust Fund will not haveenough assets to pay fullbenefits.1

Poor accounting and

financial reporting

practices helped cause

our problems

Not only have government accounting stan-dards played a role in masking our problems, butfailure to insist on proper accounting and report-ing has facilitated this looming crisis. For ex-ample, when we speak of the national debt, wegenerally mean only the cash borrowings of theU.S. Government. Other liabilities are not consid-ered, such as amounts due to military veteransand federal civilian government retirees forbenefits already earned. The present value ofSocial Security and Medicare benefits for whichcurrent retirees think they have paid, and uponwhich they are relying, usually escapes notice.

There are assets, such as infrastructure andparks, that offset some of these liabilities. Unfortu-nately, the magnitude of the liabilities dwarfs thevalue of any offsetting assets.

At September 30, 2007, federal debt held by thepublic, what commentators usually mean whenthey refer to the national debt, totaled approxi-mately $5.1 trillion. On the same date, the U.S.Treasury noted the net position of the federalgovernment was a negative $9.2 trillion. Theincrease was accounted for by adding $5.7 trillionin other liabilities, primarily unfunded pensionbenefits earned by service veterans and civilianfederal employees, and subtracting the book

value of $1.6 trillion in federal assets.However, what is not considered in any of these

calculations is the net present deficit of $45 trillionfor Social Security and Medicare benefits. Addingall this together, our national debt is really closerto $54 trillion than $5 trillion. Most informedobservers believe that the paltry $5 trillion is amatter of very serious national concern that couldthreaten the nation’s future prosperity. And yet, inthese serious and supposedly informed discussions,over 90 percent of the problem gets ignored.

Why are we so ill-informed and why don’t we act?

While accounting rules themselves cannotchange policy, perhaps policymakers would be

more restrained in enact-ing new benefits or moreactive in assuring thosebenefits are adequatelyfunded if voters weremore cognizant of thereal numbers. Manycitizens may have avague idea that some-

thing isn’t right with respect to federal retirementprograms, but, unfortunately, leaders in neitherthe executive nor legislative branches havesought to consistently focus attention on thisproblem.

While poor accounting standards may havefacilitated the looming crisis, improved account-ing standards, and the good information thosestandards will bring about, can play an importantrole in mitigating the consequences of our inaction.We need to make good decisions, and goodinformation is necessary for good decision making.

Focus on the state level

While the overwhelming nature of our problemsat the federal level appears to make most of thefinancial issues at the state level seem immate-rial, state governments are not without their ownproblems to which deficient accounting standardshave contributed. Oklahoma’s teacher retirementsystem is seriously underfunded. The budgetaryfocus on available cash and the focus on thebudget almost to the exclusion of other factorsoften leave us without the information we need forsound decision making.

This study looks at state government account-ing practices and proposes major changes. Itrecommends that financial statements use cost as

Oklahoma was a leader in the

transparency movement, and the state

is one of the first to maintain a

transparency website. This study was

undertaken with a view to enhancing

the benefits of transparency.

4

the principal measurement focus and demon-strates how the provision of state services looks inthis new light. In order to show how this can beaccomplished, the study provides an illustration offull accrual basis financial statements for theState of Oklahoma. However, the principlesdeveloped and illustrated here are also appli-cable to U.S. Government finances.

A brief political background

This study is about accounting and finance.The purpose of an accounting and reportingsystem is to communicate useful information. Anapproach to governmental accounting that con-flicts with American values would be worth little.While this is not an exercise in political science, itmay help to look at some of the unique features ofour political system and make certain the account-ing methods are consistent with those features.

The American system of government ushered inthe concept of government by the consent of thegoverned. This differed significantly from Europe,where the elites, not the people, made the decisions.Many Europeans came to America to escape theEuropean system, and certainly the thinking of theframers of our Constitution was infused with thephilosophy of men acting freely under the law andthe supremacy of individual rights.

What might this mean for accounting stan-dards? We should recognize that our reports arenot so much to inform the political leaders aboutthe bureaucracy, but to hold the political leadersaccountable to the citizens who elect them. Weare not ultimately governed by elites. We ulti-mately govern ourselves and delegate authority toelected officials to make policy and administer thegovernment. We reserve the right to change orwithdraw that delegation at the next election.

What is the purpose of government? Govern-ment is not a business. It does not exist to make aprofit. In America, government exists to provideservices to its citizens. This should have profoundimplications for accounting theory. Agovernment’s financial reporting should notrevolve around comparing income and expenseas in business. Neither should it revolve aroundreporting if the bureaucracy complied with the lawand the budget. Such reporting stops short ofholding the whole government accountable.

If the citizens ultimately control the governmentand the purpose of the government is to provideservices, then financial reporting should focus on

providing information about the quality and scopeof government services and the cost of providingthem. In this way, financial statements will helpcitizens hold elected officials accountable. Thoseofficials may find “internal use” financial reportshelpful in carrying out their responsibilities, butsuch reports stop short of providing the publicwith the information to which it is entitled.

Several years ago a client who was a stateofficial asked me to explain why following gener-ally accepted accounting principles was a goodthing. The audience was the chief of staff for agovernor to whom my client reported.

I explained how good financial reporting couldhelp the governor sell his program by giving thepublic more understandable information. Ipointed out that the governor could better rallypublic support if voters had a clearer understand-ing of the problems the governor faced. I showedhow generally accepted accounting principles, orGAAP, give the public a better understanding ofthe real situation. The chief of staff then looked atme incredulously and asked, “Who would want todo a stupid thing like that?!”

The experience drove home to me that not allgovernment leaders want the public to under-stand. Some are quite happy to obfuscate thefacts for their own ends. If we design accountingstandards that only serve the needs of electedofficials, we stop short of providing the type ofinformation that can be helpful in a republic. Theinformation we should communicate is: What arewe doing? What are the results? What is the cost?

There are many key issues we must address inorder to move from an accounting system thatfocuses on the budget and compliance to one thatfocuses on cost and value added. The next sectiondiscusses some of these issues.

The accounting profession has made signifi-cant progress over the last quarter century inimproving accounting standards for government.The formation of the Governmental AccountingStandards Board (GASB) and its acceptance as astandard-setter by members of the AmericanInstitute of Certified Public Accountants (AICPA)were important steps. GASB’s adoption of State-ment 34 in June 1999, which brought true accrualaccounting to entity-wide financial statements forthe first time, was also a very significant milestone.

At the same time, the profession, led by theGovernment Finance Officers Association (GFOA),has worked to improve the professionalism of

5

those charged with accounting matters in govern-ment. While technically a separate issue from thedebate over accrual accounting, GFOA’s successin asserting the need for professional accountantshas had the desirable effect of recognizing abasic tenet of a profession in government, namelythat the public interest comes first. This recogni-tion reinforces the arguments to be made forimproved financial reporting that serves those towhom government is accountable.

However, much of financial reporting by gov-ernment remains mired in outmoded practicesthat obscure the real cost of providing services.Rather than focusing on cost, the standards bywhich fund-level financial statements are preparedcontinue to focus on compli-ance, especially compliancewith the adopted budget.

Government should report

on a consolidated basis

Traditionally, governmentshave prepared stand-alonefinancial statements for various activities andthen combined those financial statements into acomprehensive report. Of course, one mightaccurately think such a report would be confusingand misleading. Government financial state-ments, even when properly prepared, are almostalways confusing and sometimes even misleading.

In the United States, governments at all levelsare established by the consent of the governedthrough elections and the delegation of power tothose elected. Financial reporting should followthis model. Those activities undertaken by electedofficials should govern both the focus and scopeof the financial statements.

Existing GAAP consider many factors in deter-mining whether to include an activity in a govern-ment financial report. These factors include notonly the ability of officials to control operations,but the degree of responsibility of the governmentfor the debt and the financial transactions of theactivity. However, financial reporting should focuson the extent to which the government exercisesits power directly. If elected officials appoint anagency’s governing board, that agency is part ofthe government entity. No other questions need beasked.

Of course, in the private sector, the subsidiariesof a parent company are consolidated and theeffect of transactions between subsidiaries is

eliminated. This provides a much clearer pictureof overall operations. The illustrative financialstatements that accompany this report follow thisprinciple and consolidate operations.

Government should have a balance sheet

In the past it could be said the balance sheetfor a government entity was a place to store dataneeded to keep the statement of revenue andexpenditure in balance. The balance sheet pro-vided little enlightening information, even to thosegenerally knowledgeable about governmentalaccounting.

The role of the balance sheet is further dimin-ished by the reluctance of political leaders to look

beyond the next election.Many elected officials feelcompelled to perform nowand let the future take careof itself. Of course, thoseelected officials may bereplaced, but the citizensstill have their government

and must depend on it for essential services.Citizens must also ultimately pay the bills, so ifthe government is running up liabilities, thegovernment’s political leaders have a responsibil-ity to inform their constituents.

Assets

Assets can provide services. Assets not onlyinclude buildings and equipment, but roads andother infrastructure improvements, such as habitatrestoration at state parks or preservation ofhistorical sites. Of course, financial assets canhelp cover costs when they are liquidated. How-ever, non-financial assets may also help coverunexpected shortfalls. When Orange County,California, worked its way out of bankruptcy in1995, the sale of the County’s landfill was thecentral ingredient that allowed the County torepay creditors without raising taxes or eliminat-ing essential services.

At the same time, interested observers may askif a government’s assets could do more good inprivate hands. Some land might be developed byprivate investors that could create jobs andbolster tax revenues. A private entity may be ableto more effectively provide resources to achieve apublic goal than the government itself. Theseinstances call for privatizing a government assetor forming a public-private partnership.

The traditional methods used to

measure the cost of government

are methods that would land

the CEO and CFO of any public

company in prison.

6

Assets are important in government, and thefinancial statements should disclose the assetsthe government owns and their value.

Liabilities

Under traditional government accounting rules,officials could provide services and delay payingfor them by incurring liabilities. For instance,legislators might reward state employees withmore generous pension benefits while failing tocurrently fund those benefits. The employees maybe happy. Those who receive the services theemployees provide may be happy. The taxpayers,who see an increase in services without highertaxes, may also be happy. Everyone may behappy, at least in the short run.

However, future taxpayers who get stuck withthe bill for servicesalready provided may beless enthusiastic. Like-wise, future employeeswho may be called uponto make more onerouscontributions to pensionplans without a corre-sponding increase in theirbenefits may also be lesssupportive.

Just like a business, agovernment should disclose on its balance sheetall the liabilities it has incurred. Some maycomplain that a liability may not have to be met ifpolicy is changed at a future date. However, amore reasonable approach is to book the liabilitywhen it is incurred and remove it if the governmentchanges the policy.

We should also distinguish between entitle-ments and liabilities. They are not the same thing.Someone may be entitled to a benefit becausethey meet certain conditions. Most welfare andsocial service programs are entitlements. Ifsomeone meets the current definition of eligibilityfor, say, food stamps, that person gets foodstamps. However, this is not a liability unless theindividual earns the benefit.

For instance, an employee provides services onbehalf of the government and, as part of compen-sation, gets credit toward a pension. The em-ployee is not only entitled to a paycheck, but theemployee has also earned a pension. Therefore, aliability exists.

A somewhat more difficult situation may exist

where the government encourages participationin certain activities in return for future benefits. Forinstance, Oklahoma promises a college scholar-ship to a student who satisfactorily completes amore rigorous high school curriculum and meetscertain other requirements. Traditionally, the statehas not booked the value of the scholarshipsearned because the state can change the pro-gram. It is also true that the student may haveacted in his or her own best interest in pursuing amore rigorous course of study.

However, the state also benefits. Students whoenter college having completed more demandingclasses in high school are more likely to succeedin college without the need for costly remedialclasses. In addition, in order to participate,students, and their families often make sacrifices

they would not otherwisemake.

Accordingly, the stateshould record a liability.The student reasonablybelieves he or she isearning the right to afuture benefit by his orher actions. If the statefails to provide the benefit,it breaks an implicitagreement with the

student.In the case of some pension plans, officials

may argue that recording a liability is unneces-sary because the government is not going tochange the plan; that is, the plan will continue inperpetuity. However, as we have seen, forces areat work that will certainly challenge the structureof government as we have known it since theGreat Depression. Increasingly, governments arelooking to the private sector to carry out functionsonce thought the exclusive domain of government.

Most politicians want to act in ways that showthey can accomplish things. Building things andstarting things attract favorable attention. Main-taining them and paying for them often get farless attention. As a result, there is a tendency tobuild new roads and new parks, even if we arenot doing adequate maintenance on those wealready have.

While proper accounting cannot eliminate thistendency, it can bolster the cause of those whowant to expand programs responsibly whilepointing out the true cost of operations. Likewise,

Not all government leaders want the

public to understand. Some are quite

happy to obfuscate the facts for their

own ends. If we design accounting

standards that only serve the needs of

elected officials, we stop short of

providing the type of information that

can be helpful in a republic.

7

when pension benefits are increased, the presentvalue of the future cost of that increase should berecognized immediately.

A similar issue exists with reporting investmentearnings. Most government pension plans aredefined benefit plans. In order to pay benefits,governments set up pension trust funds to whichthey regularly make contributions so that the trustmay invest the money and, hopefully, earn areturn that can help offset the government’seventual obligation.

Unfortunately, there is no guarantee that thetrust will earn a profit in any year, or even anyseries of years. When the government offers adefined benefit plan, the government is assumingall the risk. If the government’s investment portfo-lio declines in value, the government shouldimmediately recognize the loss.

Conversely, if the government earns superiorreturns on the investment of its pension assets, itis the primary beneficiary. The government mayreduce the size of its future contributions to thepension trust. In extreme cases, the governmentmay even take funds from the pension plan anduse those funds for other purposes.

Of course, groups representing governmentemployees and retirees want it both ways. Theywant the government to guarantee the pensionand use any profits only to pay better benefits.However, the purpose of good financial reportingis not to obtain a particular political outcome (anda conflict between an employee interest groupand taxpayers is always a political contest), but tomake sure that the parties, and especially thepublic, to whom the political leaders are respon-sible, get all the facts in an intelligible manner.

Financial statements should inform the publicabout the type and extent of the government’sassets and liabilities. The illustrative financialstatements for the State of Oklahoma for June 30,2008, demonstrate how this can be accomplished.

Reporting the real cost of government services

Corresponding to the premise that the financialstatements should report liabilities for all costsalready incurred, the financial statements shouldalso reflect the actual cost of providing govern-ment services. In technical accounting terms, thismeans reporting expense rather than reportingexpenditures.

In preparing a budget, a legislative bodyallocates available financial resources to various

activities. Political interest groups compete fortheir share of the pie. In the debate, a necessarypart of our system, the parties often refer to theamount of an appropriation as the cost of theservice. While they may make statements withgood motives, statements that equate appropria-tions or expenditures with expense are misleading.

We have already seen that political leaders,seeking to minimize the impact of the costs theiractions impose, will naturally attempt to financeprograms with future, rather than current, rev-enues. This reduces the need for current appro-priations and reduces the apparent cost of theservice the politician is championing.

There remain other techniques for passingcosts on to future legislatures.

First, the legislature may vote a pay raise thattakes effect on the last month of the coming fiscalyear. (Yes, this has happened in recent years inOklahoma.) The sitting legislators get credit forincreasing pay levels, although the benefit isdelayed by 11 months. However, the cost is notrecognized and the legislature may adjournhaving balanced the budget. Of course, the nextlegislature has the option of reducing pay levels,but this is a highly unpleasant action that winsfew votes at the next election.

The notes should disclose any unusual timingin the initiation of new pay or benefits. GAAPcurrently require the disclosure of significantsubsequent events, such as the issuance of newbonds after the end of the fiscal year. We shouldrequire similar disclosure of actions that, if notreversed, will increase costs for existing programsin future years. The illustrative financial state-ments in this report contain no such disclosurebecause the legislature did not employ thistechnique in the year ended June 30, 2008.

Proponents of increased government spendingwill point out that the timing of tax cuts usuallymeans that only a portion of any revenue loss isbudgeted in the year the tax cut takes effect.Oklahoma is on a fiscal year ending June 30.However, most taxpayers compute their taxes onthe basis of a calendar year. This leaves a six-month differential.

A tax reduction passed by the Oklahomalegislature normally takes effect the followingJanuary 1. The tax rates don’t change during thefirst half of the fiscal year for which the tax cutwas budgeted. In addition, most withholding ispaid monthly in the following month, so the

standard convention is to budget five-twelfths ofany expected revenue reduction from a tax cut inthe coming year because tax collections for thefirst seven months of the fiscal year will be on thebasis of tax rates in effect before the tax cut goesinto effect.

Of course, many proponents of bigger govern-ment often ignore the feedback effect that a taxcut, especially a reduction in tax rates on workand investment, has on revenue. A 10 percent cutin income tax rates will result in less than a 10percent reduction in tax revenues while a 10percent increase in rates is unlikely to generate a10 percent revenue gain. I have watched manyvery knowledgeable observers get surprised bythe less than expected impact of a tax rate reduc-tion and disappointed by the ability of a tax hiketo raise revenue.2

However, the point ofproponents of more spendingand higher taxes is welltaken. The financial state-ments should disclose allmaterial policy changes totake effect in future years that will impact thestate’s finances.

A second technique for reducing the appropria-tion necessary to carry out operations is to defermaintenance. If the state builds a new road,political leaders and dignitaries will gather to cuta ribbon and engage in general hoopla. When astate worker patches a pothole, repairs a guard-rail, or cuts weeds from the shoulder, the result isno hoopla and few opportunities for politicalplaudits for the elected officials.

This state of affairs has several effects. First, wetend to build things we can’t properly maintain.Professional engineers are constantly bemoaningthe lack of upkeep on our roads. When serving asstate finance director, I more than once visitedstate parks and other facilities where mainte-nance was neglected. In one instance, the ne-glected facility was an old building caring forsome of Oklahoma’s most vulnerable citizens.

I have also heard legislators plead for new orexpanded park facilities, usually in their districts,while simple upkeep was neglected at existingparks. A legislator appears to be getting some-thing done for constituents by building a new golfcourse. The cameras show up for positive photo-ops. However, if a sewer lagoon needs mainte-nance, fixing it gets little fanfare until the lagoon’s

decay reaches a crisis stage.The notes to the financial statements should

probably contain a disclosure of estimated main-tenance in coming years. The illustrative financialstatements accompanying this report do notinclude such a disclosure as I am not clear onwhat would be best. While legislators have agen-das, so do bureaucrats, even those with goodintentions. Just as the politically oriented legisla-tor likes the photo-ops that go with the dedicationof new facilities, the bureaucrat wants to encour-age increased appropriations and security for hisor her operations.

As a result, I am not confident in recommend-ing a particular manner of disclosure. However,future efforts similar to this project should con-sider including disclosure of the extent of deferred

maintenance and the reliabil-ity of the deferred mainte-nance estimates.

The cost of programs in-

cludes overhead

People realize that aprivate company, in addition to making a product,must spend resources to sell the product andmake collections on its sales. It must also keep itsbooks current, arrange for its finances, andeffectively hire, evaluate, and retain its personnel.We refer to such activities as overhead.

Yet, in government, we tend to think of suchactivities as freestanding when their real purposeis to help other agencies achieve the other agen-cies’ objectives. A private business must pay itsemployees and collect its receivables. We recog-nize this overhead as part of the cost of doingbusiness.

However, we seldom attribute the cost of theTax Commission to the agencies and programsthey serve by collecting revenues. The same istrue for other overhead functions such as thosecarried out by the Treasurer, the Auditor andInspector, the Office of State Finance, the Depart-ment of Central Services, and the Office of Per-sonnel Management.

Accordingly, the illustrative financial statementsdo not treat overhead functions as separateactivities, but allocate the cost of overhead func-tions to the programs their actions assist orregulate. A part of the cost of providing preventivehealth services is assessing and collecting thetaxes to pay for the service, hiring and processing

8

The information we should

communicate is: What are we

doing? What are the results?

What is the cost?

personnel to carry out the activities, and comply-ing with the myriad of rules and regulations thatattend government activities.

The illustrative financial statements account forevery cost that the state incurs as part of a servicethe state provides to the public.

The truth is good, smoothing things that are not

smooth is bad

When managing an investment portfolio, amanager wants profits, but also stability, espe-cially when he or she reports results. However, ifthe state takes responsibility for achieving acertain result, which it does when it maintains adefined-benefit pension plan, it is going to haveboth gains and losses to report, unless it investsso conservatively that it eliminates all risk, astrategy also likely to hold down long-term returns.

If Oklahoma loses a billion dollars on invest-ments, as it did in the year ended June 30, 2008,the financial statements should reflect that. Ofcourse, such disclosures may bring questions thatmanagers and political leaders would rather nothave to answer. They prefer to “smooth” resultsover time as a result. Rather than showing a 6percent loss in year one and a 24 percent gain inyear two, they would prefer to show a gain of 9percent in both years.

They may argue that the financial markets areinherently volatile and that the investment objec-tives of a pension plan are long-term. Both asser-tions are true and the losses of one year canusually be recovered in future years. However,there is no guarantee. Current GAAP do not requirethat current gains and losses, or even the fullextent of existing pension obligations, be includedon the face of the financial statements. The illustra-tive financial statements correct this deficiency.

Organize reporting by program rather than by fund

Consistent with the traditional focus of financialreporting in government on compliance, tradi-tional statements of activity are organized by fundor fund type. All financial resources that flowthrough the general fund are reported in a columnfor the general fund. All financial resourcesobtained through taxes that are earmarked for aspecific purpose are aggregated into anothercolumn for special revenue funds.

The value of a report on the revenues andexpenditures of a special revenue fund type isdubious. It is simply an amalgamation of several

funds that may have little in common except thatthey are funded by dedicated revenue sources.Rather than focusing on funds, the illustrativefinancial statements focus on activities andprograms.

The statements provide an overview of govern-ment activities. These statements answer thequestion, a question that current financial report-ing does not completely answer: How much do ourvarious programs cost? The Government-wideStatement of Activities also shows the extent andthe manner in which those are financed currently.

The activities of each statement are thentreated separately and broken into further detail.For instance, the Statement of Activities for PublicSafety shows the cost of separate activities:• Punishing and rehabilitating adult offenders• Preventing and correcting juvenile crime• Patrolling state highways• Investigating and resolving crimes• Prosecuting crimes• Etc.

The illustrative financial statements focus onthe cost of providing services instead of adminis-trative boundaries. While this adds a degree ofsubjective judgment, the result is reports that aremore meaningful. In assigning costs to activities,an attempt was made to assign the costs to theactivity that supposedly benefited from that cost.

For example, the Oklahoma Department ofCareer and Technology Education conductseducational programs for prison inmates. Whileadministratively these programs are carried outby an agency primarily responsible for education,these programs are also conducted in behalf ofcorrections. Therefore, the costs of the programsare included in public safety, not education,reflecting the impulse behind them.

The ability to parse the data is seeminglyinfinite. Certainly, the state could provide anotherlevel of reporting, or even two or three more levelsof additional detail, and there are instanceswhere this would be helpful. However, our pur-pose here is to illustrate how the data might bepresented to convey the cost of programs. It maybe best to leave more detailed reporting to sepa-rate reports on the details of an activity.

What is missing are the benefits derived fromthe activities. In the private sector, if we know howmuch it costs to run the business, we also want toknow how much it sold. Of course, the goal ofgovernment is not to maximize profits, but to

9

maximize the value of its services relative to thecosts incurred. Governments should combine areport on the cost of providing services, as shownin the illustrative financial statements, withinformation on the value of the services provided.

Achieving symmetry in society

Financial reporting for government shouldreflect the interaction of the government withothers. This happens normally in most privatetransactions. For instance, when business A buyssomething from business B, each usually recordsthe transaction at the same time. Business Brecords a sale while Business A records a pur-chase.

Government is not always so straightforward.It imposes taxes and then collects those taxes.With respect especially to income taxes, there aretiming differences. Consider the following.

An individual earns income. He or she hasmoney withheld for tax purposes or pays esti-mated taxes to the state. After year’s end, thetaxpayer prepares a return in which he or shecalculates the actual tax due and pays theadditional tax or files for a refund. If theindividual’s income is from a sole proprietorshipthat prepares financial statements, the financialstatements will display the estimated tax orrefund due on the income earned.

However, the state does not show the addi-tional tax to be paid on income already earned. Itshould. Just as the state should accrue expensesbased upon its activities, it should accrue rev-enue based upon the activities that give rise tothat revenue. This is not a major issue at this timein Oklahoma, but it could be, and the state needsto do the accounting right. By reporting revenuebased upon its receipt, as is the general rule atpresent, the state risks a material misstatement.

I was once an advisor to a state official facinga serious unexpected budget shortfall. An exami-nation revealed that one cause was a failure toaccount for changes in tax policy. This state hadnot required corporations to make estimatedincome tax payments until four years earlier.Because of the large impact on business, thestate phased in the new estimated paymentrequirement over three years.

The first year, the state collected all the rev-enue for the previous year plus one-third of theamount expected for the current year. Notice thatthe government created a 33 percent windfall.

The second year, the state collected two-thirds ofthe previous year’s taxes and two-thirds of thosefor the current year. There was little budgetaryimpact from year one to year two. The third year,the state collected one-third of the previous year’stax and 100 percent of the current year’s. Again,there was little disturbance. However, the fourthyear, the state collected all of the current year’stax but no tax from the previous year.

Corporate income tax revenue was downsignificantly. Corporate income tax is one of themore volatile taxes anyway, but in this year, thenormal volatility was exacerbated by faultyaccounting. By accounting for income tax andother taxes at the time the underlying transactiongiving rise to the tax occurs, a government willavoid surprises. Of course, this approach re-quires use of some estimates, but such estimatesare not particularly difficult in most situations.

A twist on the matching concept

All students in an introductory accountingcourse learn the basic concepts that underlieaccounting practice. One of those concepts ismatching. Matching means that expenses shouldbe matched with the revenue to which they giverise.

However, in government, the focus is on cost,not income, so rather than matching expense toincome, the state should match its revenues to theexpenses they fund. This is an issue with respectto infrastructure. States build roads with a combi-nation of state and federal funds. The federalgovernment makes grants to the states for roadbuilding. Generally, states should properly recordrevenue from a grant when it completes therequirements for receiving the grant. In the caseof roads, the state will usually be able to recog-nize the revenue from the grant as it builds theroads.

However, a road is a capital asset that peoplewill use for many years. The state should recog-nize the cost of the road over the period of its use,and the illustrative financial statements accom-plish this by charging depreciation over theexpected life of the road to transportation ex-pense. However, the state has long since com-pleted all steps necessary to assure its right tothe federal grant that helped build the road.

To recognize the grant as revenue when theasset that it helped purchase is capitalized anddepreciated would be misleading. Accordingly,

10

11

the illustrative financial statements displaydeferred revenue, which is then charged toexpense as the state recognizes depreciation onthe related roads. Of course, while we shouldmatch grant revenue with the expense it is meantto offset, we should also match the expense withthe service provided. The enhancements in thesefinancial statements accomplish that objective inthe case of roads by charging expense throughdepreciation as the road is used.

When is it a tax and when is it a user fee?

In the current environment, few politicians wantto be seen as favoring higher taxes. Those whodo advocate higher taxes are usually very selec-tive about those to whom the added burden willapply so that they will notbe seen as advocatinghigher taxes for the majorityof their constituents. Accord-ingly, many times we seehigher fees in lieu of highertaxes. We also see newtaxes called fees even if theperson paying the fee getslittle directly in return.Oklahoma, a state with aconstitutional limit on highertaxes without a vote of the people, increases thepressure on politicians to call a tax a fee.

In the illustrative financial statements, thegovernment-wide statement of activities limits theclassification of user fees to something other thantaxes only when the fee can legitimately be calleda sale. For instance, turnpike tolls and collegetuition are sales of government services, whiletaxes on the sale of gasoline and tobacco are not.Sales result only from the government selling aservice it creates and provides.

When the sovereign power of the state isinvolved, we have a tax. The illustrative financialstatements do distinguish fees for professionaland similar licenses, but these are, in effect, taxessince there is no realistic alternative to the gov-ernment license. In contrast, a student may attenda private college and a motorist may travel onroads that are not subject to tolls. In arriving atthe net cost of an activity, the illustrative financialstatements deduct revenue from the sale ofservices and any grants and contributions fromoutsiders in determining the activity’s net burdento taxpayers.

Common school activities

The proper classification of some activities iscertainly open to debate. The single largest itemin recent state budgets has been an appropriationfor common schools (K–12). Technically, this isassistance to local governments as each schooldistrict elects its own board that exercises admin-istrative control within the boundaries of state law.

However, the illustrative financial statementsshow this assistance as an education activity.While each school district has its own electedboard, the major decisions as to whom theschools must educate, the curriculum they follow,whom they may hire as teachers, and what theyare paid are so heavily regulated by the state thatit is a de facto state activity. The illustrative finan-

cial statements accountfor it as such.

Disclosures can also be

helpful

The notes to the finan-cial statements provideessential information toassist the readers of thefinancial statements.While there are areaswhere we could complain

that the minutiae the notes often contain are moreof a distraction, this project has not attempted tocritique the drawing of the line between what isrequired and what is not. However, there areinstances where additional disclosures may behelpful.

For example, the legislature may grant favor-able tax treatment for certain transactions itdeems in the public interest. In many cases, thesetax preferences are granted in lieu of subsidies inan attempt to fulfill a state objective. Thesepreferences, or “tax expenditures,” have a signifi-cant financial impact. Accordingly, the stateshould disclose them in its financial statements,and the illustrative financial statements do so.

Some object to the term tax expenditure as allthe government is doing is allowing someone tokeep what originally belonged to them. However,the reality of refundable credits where the creditmay exceed the amount of tax otherwise dueundermines this view. Meanwhile, when a govern-ment imposes a tax and then allows some taxpay-ers to avoid paying the tax instead of reducingtaxes for all taxpayers, the government does

It is one thing for a taxpayer

to be able to view individual

transactions of a state

agency. It is another thing

altogether to understand the

state’s financial position and

the cost of its activities.

something comparable to spending when itgrants preferences. However, the term “tax prefer-ences” is employed to avoid a controversy notdirectly relevant to this project.

The state also places restrictions on who maybe hired to work for a state agency and requiresthat certain preferences be granted to someapplicants. There is often less flexibility to hire,train, and reassign staff in government. Accord-ingly, the number of workers approaching retire-ment and similar matters are disclosed becausethe ability of the state to attract and retain quali-fied staff is important to carrying out its missions.

As previously discussed, future efforts similar tothis project may want to consider making disclo-sures about the extent of deferred maintenance.

Financial statements should be timely

Governments are notoriously tardy in publish-ing their financial statements. The federal govern-ment allows state and local governments up to 13months to submit reports under the Single AuditAct. Meanwhile, the Securities and ExchangeCommission allows publicly traded companiesonly 90 days to issue audited financial state-ments, and most sophisticated businesses canclose their books in two or three days. Quite adiscrepancy!

While some in government will blame the longtime period upon the complexity of governmentoperations, governments are no more complexthan business operations of comparable size.Most large businesses have several subsidiariesand must account for global transactions thatoccur in different currencies.

A more likely cause of the lack of urgency is thegeneral lack of interest that accompanies therelease of a government’s financial report. Fewclamor for the data, and perhaps the reason isthat they do not see the data as especially helpfulas they are currently organized. And in manycases, the data are not particularly helpful.

Financial statements should be issued andaudited no less than 90 days after the end of thefiscal year.

Transparency and financial reporting

Taxpayers are often frustrated by government’sseemingly unfathomable complexities. Recently, amovement toward transparency has sought toshed much-needed light on government opera-tions. Oklahoma was a leader in the transparency

movement, and the state is one of the first tomaintain a transparency website.

This project was undertaken with a view toenhancing the benefits of transparency. It is onematter for a taxpayer to be able to view individualtransactions of a state agency. It is anotheraltogether to understand the state’s financialposition and the cost of its activities.

The government should simply report:• This is what we do• This is the cost of doing it• These are the benefits provided• This is how we accomplished it

Transparency provides an opportunity toinvestigate the last of these disclosures, how thestate goes about trying to accomplish its objectives.The illustrative financial statements show how thestate could provide the first two items. If we canincorporate measures of service efforts andaccomplishments into the reporting process, wewill place significant tools in the hands of thosewho take seriously their responsibilities as citizens.

Those citizens, for the first time, will be able tounderstand not only what the government does,but how much it costs to do it and what the publicreceives as a result. Armed with this information,citizens can for the first time view the books oftheir government as, in Thomas Jefferson’s words,“clear and intelligible as a merchant’s books,” sothat they will be able to investigate abuses andcontrol them.

We can understand how much it costs thegovernment to provide services. Combined withreporting on services, efforts, and accomplish-ments, we can see if we are getting value for ourmoney. We will know if the government has assetsto offset its liabilities. We will know if we arepaying for the services we receive or if we aregetting services by pushing the cost off on futuregenerations. These are benefits our currentaccounting system fails to provide. If we canenlighten ourselves about our finances and getthe information needed to address a serious fiscalcrisis, we will make important progress. �

Endnotes

1 “The Federal Government’s Financial Health: A Citizen’s Guide

to the 2007 Financial Report of the United States Government,”

The Financial Management Service, A Bureau of the U.S.

Department of the Treasury, page 2.

2 See also Reed, W. Robert, “The Robust Relationship Between

Taxes and State Economic Growth,” The National Tax Journal,

March, 2008.

12

13

A W O R D A B O U T T H E I L L U S T R A T I V E F I N A N C I A L S T A T E M E N T S

face of the statements, such as subsequent events.Most items covered by existing notes generally

included with state government financial state-ments would remain under a cost-focused sce-nario. As such, the notes that currently appear inOklahoma’s financial statements are referencedbut not further addressed. However, there areadditional disclosures that should be consideredunder the approach outlined in this project. Theseadditional disclosures include a discussion of taxpreferences, sometimes called “tax expenditures,”where the government grants preferential taxtreatment. Additional disclosure may be helpfulwith regard to the government workforce as therecruitment and retention of qualified workers isoften more difficult in the government environment.

The notes to Oklahoma’s financial statementsare referenced below with explanations andexamples where changes from the existing contentare recommended. Existing GAAP may requirenotes that are excessively detailed beyond what isconstructive. However, a critique of this practice isbeyond the scope of this project.

This project focuses on the cost of governmentactivity. Elsewhere in this report, the merit ofincluding information about the value added bygovernment activity, often called “service, efforts,and accomplishments reporting,” is discussed.Including such information is beyond the scope ofthis project. However, financial statements that doinclude information about the value added bygovernment activity should include notes relatingto that information.

The illustrative financial statements that accom-pany this report are not prepared in accordance withgenerally accepted accounting principles thatcurrently apply to government. They are prepared toillustrate how generally accepted accountingprinciples in government can be more useful.

The amounts shown in the illustrative financialstatements are often taken from official statesources, including the state’s own comprehensiveannual financial report and its OpenBooks trans-parency website. Other data were acquired infor-mally from knowledgeable officials, and still otherdata presented were estimates prepared by meand the team that helped me complete this project.

The illustrative financial statements are shownonly for the purpose of discussion about financialreporting and may not fairly present the state’sfinancial position or results of operations. Thedata have not been audited or, in some cases,even independently verified and may containmaterial errors and omissions.

This project presents a new approach to finan-cial accounting for government. The project usesdata for the State of Oklahoma to prepare illustra-tive financial statements that focus on cost andaccountability of the elected government to itscitizens. The notes are an integral part of thefinancial statements. They explain the policiesused in the accounting process and provideimportant detail to aid the reader in understand-ing. The notes also provide important informationthat cannot be readily quantified, such as contin-gencies, or that would be inappropriate on the

14

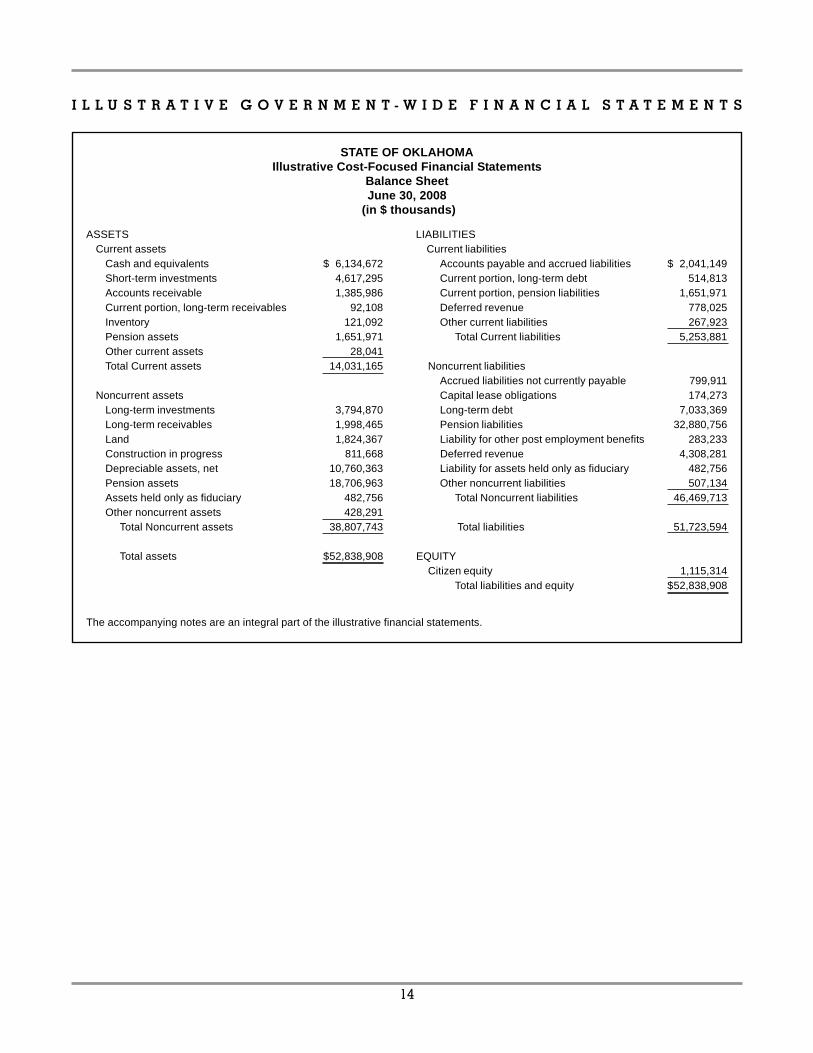

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Balance SheetJune 30, 2008

(in $ thousands)

ASSETS LIABILITIESCurrent assets Current liabilities

Cash and equivalents $ 6,134,672 Accounts payable and accrued liabilities $ 2,041,149Short-term investments 4,617,295 Current portion, long-term debt 514,813Accounts receivable 1,385,986 Current portion, pension liabilities 1,651,971Current portion, long-term receivables 92,108 Deferred revenue 778,025Inventory 121,092 Other current liabilities 267,923Pension assets 1,651,971 Total Current liabilities 5,253,881Other current assets 28,041Total Current assets 14,031,165 Noncurrent liabilities

Accrued liabilities not currently payable 799,911Noncurrent assets Capital lease obligations 174,273

Long-term investments 3,794,870 Long-term debt 7,033,369Long-term receivables 1,998,465 Pension liabilities 32,880,756Land 1,824,367 Liability for other post employment benefits 283,233Construction in progress 811,668 Deferred revenue 4,308,281Depreciable assets, net 10,760,363 Liability for assets held only as fiduciary 482,756Pension assets 18,706,963 Other noncurrent liabilities 507,134Assets held only as fiduciary 482,756 Total Noncurrent liabilities 46,469,713Other noncurrent assets 428,291

Total Noncurrent assets 38,807,743 Total liabilities 51,723,594

Total assets $52,838,908 EQUITYCitizen equity 1,115,314

Total liabilities and equity $52,838,908

The accompanying notes are an integral part of the illustrative financial statements.

I L L U S T R A T I V E G O V E R N M E N T - W I D E F I N A N C I A L S T A T E M E N T S

STATE OF OKLAHOMAIllustrative Cost-Focused Financial Statements

Statement of ActivitiesFor the Fiscal Year Ended June 30, 2008

(in $ thousands)

Grants and Burden toExpense Sales Net expense contributions taxpayers

ACTIVITYEducation $ 9,225,428 $ (3,344,613) $ 5,880,815 $ (770,411) $ 5,110,404Health and Welfare 7,091,784 (477,099) 6,614,685 (4,051,854) 2,562,831Public safety 1,435,108 (85,939) 1,349,169 (303,462) 1,045,707Transportation 928,386 (307,598) 620,788 (444,627) 176,161Public insurance 923,698 (976,805) (53,107) - (53,107)Public utilities 380,367 (471,253) (90,886) - (90,886)Assistance to local governments 328,910 (4,139) 324,771 (151,868) 172,903Natural and cultural resources 295,270 (84,214) 211,056 (107,909) 103,147General government 159,849 (66,080) 93,769 (5,252) 88,517Regulation 116,668 (6,513) 110,155 (6,918) 103,237Economic development 110,039 (11,011) 99,028 (5,424) 93,604Cost of increased pension benefitsto former employees 376,689 - 376,689 - 376,689

Total $ 21,372,196 $ (5,835,264) $15,536,932 $ (5,847,725) $ 9,689,207

TAXES and OTHER REVENUESTaxes

Individual income taxes $ 2,819,364Sales and use taxes 2,069,303Gross production taxes 1,114,950Motor vehicle taxes 604,926Corporate income taxes 552,193Fuel taxes 419,617Tobacco taxes 237,166Insurance taxes 100,778Beverage taxes 86,648Other taxes 513,020

Total taxes 8,517,965

Other revenuesLicenses and permits 197,617Income/(loss) from moneyand investments (938,310)Fines, forfeitures and miscellaneous 41,936

Total, other revenues (698,757)

Total, all sources $ 7,819,208

Burden to taxpayers fromcurrent services $ 9,689,207less: current amount of taxesand other revenues 7,819,208

Increased / (decreased) burdento taxpayers in future years $ 1,869,999

15

The accompanying notes are an integral part of the illustrative financial statements.

16

Note 1. Summary of Significant Accounting Policies

The illustrative financial statements includeseveral features that differ from existing GAAPpresentation. Most of these differences are relatedto entity definition, measurement focus, matching,intergenerational equity, and symmetry in society.

Entity definition—The illustrative financialstatements include all activities under the direc-tion, either directly or indirectly, of officials electedby the voters of Oklahoma. This includes allactivities where a board is appointed by stateelected officials or by others appointed by thoseofficials. Consistent with the fact that the state is apolitical unit accountable to its citizens, thefinancial statements report on all activity con-ducted by that unit on behalf of those who electedits decision makers.

As a result, the illustrative financial statementsdo not distinguish between general government,component units, or other relationships. If the dulyelected officials of the state can ultimately directthe operations of an agency, board, commission,or public trust, it is included as part of the illustra-tive financial statements.

Accordingly, the illustrative financial statementsrecognize indirect expenses incurred for thebenefit of other agencies as part of the expense ofproviding services through those agencies. Forinstance, in the illustrative financial statements,the cost of collecting taxes is allocated among allactivities financed by those taxes.

The illustrative financial statements alsoallocate other overhead costs among the activitiesmeant to benefit from those activities. Centralfiscal operations, personnel management, centralpurchasing, and other general managementfunctions are allocated to activities based uponappropriate criteria, such as expenditures, appro-priations, or number of personnel. This policy ismaintained even though the purpose may be toprevent misappropriation or abuse rather thanbenefit the activity charged directly.

The illustrative financial statements alsodistinguish between transfers that are truly apayment from one agency to another and trans-fers that are made on behalf of third parties. Forinstance, the Oklahoma State and EducationEmployees Group Insurance Board (OSEEGIB) isa state agency that provides insurance benefits tostate and county employees and teachers. How-

ever, state employees are not automaticallyenrolled in OSEEGIB. Rather, OSEEGIB mustcompete with several private sector providers forthe business of those it serves. The State offers itsemployees a choice between OSEEGIB and itscompetitors and withholds the cost of premiumsfrom its employees’ pay and benefit allowances. Itthen transfers the funds withheld to the providersas chosen by its employees.

When the transfer is made from the State toOSEEGIB, it is treated as an arm’s length transac-tion rather than a transfer. The State has compen-sated its employees. Separately, the State, throughOSEEGIB, has sold insurance to its employees.The transfer to OSEEGIB is treated as revenue tothe State, specifically a charge for service.

Special considerations arise when more thanone level of government funds, manages, ordelivers a service. The illustrative financial state-ments report the cost of programs primarilymanaged and delivered by the State of Okla-homa as a state activity. Funds provided by thefederal government for state activities are in-cluded in grants and contributions. Funds theState provides to local governments for servicesprimarily managed and delivered by local gov-ernment are reported as assistance to localgovernments.

The factors considered in determining whichlevel of government primarily manages anddelivers a service include which level of govern-ment is responsible for:• determining the extent of program coverage• determining eligibility to participate by estab-

lishing rules for participation• determining eligibility to participate by apply-

ing the rules to individual situations• determining the type and level of benefits

delivered• employing workers and/or contractors to

deliver services includingo establishing criteria for employees and

contractorso establishing rules that govern the firing of

employees and retaining of contractorso selecting individual employees and contractorso supervising employees and contractorsCommon schools are funded primarily by the

State of Oklahoma, although federal assistanceand local taxes are also important sources. Voters

N O T E S T O T H E I L L U S T R A T I V E C O S T- F O C U S E D F I N A N C I A L S T A T E M E N T S

17

elect local school boards, but important decisionsabout who is to be educated, the amount ofeducation services provided, the overall curricu-lum, and qualifications for teachers are made bythe State of Oklahoma apart from local schooldistricts. Accordingly, Oklahoma’s common schoolsare treated as a state function, although the finan-cial statements do not include local tax revenues.

Similarly, the activities of the Department ofCareer Technology and Education, the OklahomaConservation Commission, and the District Attor-neys Council are treated as state functions,although local districts make many decisions andprovide important funding. In all cases, thepurpose, scope, and rules are determined at thestate level, although locally accountable officialsimplement the decisions made at the state level.The illustrative financial statements do not in-clude funds provided by local sources.

However, other county activities are not treatedas state functions because the locally electedcounty officials exercise more decision-makingcontrol. However, the State provides major fund-ing for many county activities. The illustrativefinancial statements report this financing underassistance to local governments. The major areasof assistance reported include funding for countyhealth departments and county roads and bridges.

In addition, the State manages pension sys-tems for firefighters and police officers. Almost allparticipants in both systems are local governmentemployees. However, while both employees andemployers contribute to the pension plans, theState underwrites the benefits, establishes therules of participation, and sets the benefit deter-mination formulas. Increases in the unfundedliability of the systems are treated as an expenseof the state, while declines in the unfunded liabil-ity (or gains in surplus funding) are treated asrevenue to the state.

Another area of consideration is communitydevelopment. The largest program, the Commu-nity Development Block Grant, is a federallyfunded pass-through intended to spur localeconomic growth. The federal assistance isincluded in grants and contributions, while thegrants to local governments are included inassistance to local governments. However, com-munity development also includes funds appropri-ated by the state for sub-state planning districts.

There are many other instances in which astate agency will provide funds or services to a

local government on an ad hoc basis or where thelevel of funding is not significant. These situationsare all treated as an expense related to a stateactivity, although a local government may exer-cise considerable control over the managementand delivery of the ultimate service. Examples ofsuch situations are found as part of the Office ofJuvenile Affairs, the Oklahoma State Bureau ofInvestigation, the Arts Council, the Water Re-sources Board, the Department of Libraries, andmany other agencies.

Measurement focus—The illustrative financialstatements are presented using the economicresources measurement focus and the accrualbasis of accounting. Consistent with the principlesthat follow, revenue is recognized when earnedand expenses are recorded when a liability isincurred, regardless of the timing of related cashflows. Similarly, grants and similar items are recog-nized as revenue as soon as the State has met alleligibility requirements imposed by the provider.

Under existing GAAP, financial statementsprepared at the government-wide level are pre-pared using the accrual basis of accounting anda measurement focus on economic resources.However, existing GAAP use a modified accrualbasis of accounting and a measurement focus oncurrent financial resources in all general govern-ment statements below the entity level. Theillustrative financial statements make no suchdistinction. The illustrative financial statementsapply the measurement focus consistently, fromthe entity-wide financial statements to the moredetailed activity-level statements.

The illustrative financial statements also refinethe measurement focus by recognizing a liabilityto the State when others have taken action ingood faith with a reasonable expectation ofreceiving a future benefit. Therefore, when theState, in an effort to achieve a public goal, offersto pay the college tuition of high school studentswho meet certain requirements, such as taking amore rigorous set of classes than would otherwisebe required, the illustrative financial statementsrecognize a liability when students and theirparents, in good faith, sign up for the programand begin complying with its requirements. Theliability is adjusted to the extent the students areexpected to complete those requirements.

Similarly, the State also recognizes the presentvalue of pension and other post-employmentbenefits as a liability at the time they are earned

18

by state employees. This is discussed in moredetail below, under intergenerational equity.

Matching principle—The matching principle isbasic to accounting and financial reporting. Asgenerally applied in the private sector, the match-ing principle means expenses are recognizedwhen the revenue to which the expenses give isrecognized. Thus, expenses are matched torevenue and the financial statements give aclearer picture of the profitability.

However, government is not in business tomake a profit, but to provide services for thepublic good. Rather than incurring expenses toproduce revenue and profit, the governmentcollects taxes and other revenues in order to fundits services. Whereas in the private sector, thedesire for revenue drives the need for expense, ingovernment, the desire to provide services drivesthe need for revenue.

The matching principle is relevant in govern-ment. However, rather than matching expense torevenue, the illustrative financial statementsmatch revenue to expense. For example, when thefederal government provides funds for capitalimprovements such as roads, the State wouldgenerally record revenue when it has met all theeligibility requirements of the grant. This wouldusually mean building a road in compliance withthe terms of the federal assistance.

However, the road, a capital asset, will provideservice to the public over many years. In theillustrative financial statements, the State recog-nizes the expense of providing that service throughdepreciation. Accordingly, the illustrative financialstatements defer revenue from federal grants thathelp pay for road and bridge construction andrecognize it over the same period that the expenseof providing the public service is recognized.

The application of the matching principle isfurther refined by two additional principles:symmetry in society and intergenerational equity.

Symmetry in society—In the private sector,when a transaction occurs between two parties,each party will usually make correspondingaccounting entries at the same time. For instance,if X sells to Y on credit, X will record a receivableand Y will record a payable at the time the sale isexecuted. The illustrative financial statementsapply this same principle to the State’s financialstatements.

When an individual or business earns incomethat is subject to income tax, the illustrative

financial statements recognize revenue to theState. The taxpayer would recognize an expenseand a liability for any tax due at the time incomeis earned. Accordingly, the State recognizesrevenue and a receivable at the same time,regardless of when the tax is paid or due. Simi-larly, sales taxes are recognized when salessubject to the tax are made, and gross productiontaxes are recognized when oil or gas is produced.

Intergenerational equity—Intergenerationalequity measures the extent to which public offi-cials have postponed or accelerated the incidenceof cost related to program benefits. To the extentpracticable, the illustrative financial statementscharge the cost of actions taken by current offi-cials to the current time period. For instance, thepresent value of the cost of added pension orother post-employment benefits related to servicesalready performed is recognized when thosebenefits are voted in by the legislature rather thanbeing amortized over some future period.

Note 2. Deposits and Investments

No significant change is contemplated exceptthat the effect of securities lending agreements isnot displayed on the balance sheet. The notedisclosures would remain as at present.

Note 3. Receivables

The State has amounts due from numeroussources: taxpayers, the federal government, andthose purchasing state services, etc. No change iscontemplated except that income earned bytaxpayers that is subject to state income tax resultsin the State recognizing a receivable for taxrevenue at the time the taxpayer earns the income.

Note 4. Interfund Accounts and Transfers

Interfund transactions and balances, includingthose between what is currently referred to as theprimary government and component units, areeliminated. This is consistent with private sectorconsolidated reporting.

Note 5. Capital Assets

No significant change is contemplated. How-ever, one issue raised but not resolved by thisproject is the reporting of replacement cost ofcapital assets in use.

Note 6. Risk Management and Insurance

No significant change is contemplated.

19

Note 7. Operating Lease Commitments

No significant change is contemplated.

Note 8. Lessor Agreements

No significant change is contemplated. How-ever, lease agreements between different agen-cies of the State of Oklahoma are consolidated.

Note 9. Long-Term Obligations

Oklahoma’s Promise—The State Regents forHigher Education promote and administer aprogram to assist students from families withincome below $50,000 to attend college in Okla-homa. To remain eligible, the student’s familyincome cannot exceed $100,000 in the year thestudent enters college. To participate, a studentmust apply before his or her final two years ofhigh school. The student’s parent(s), custodian(s),or guardian(s) must agree to help the studentmeet the program’s requirements. The studentmust take a more rigorous curriculum than isgenerally necessary to graduate from high schoolaccording to the following schedule of requiredcourses:

4 years of English3 years of lab science3 years of mathematics3 years of history and citizenship skills2 years of foreign language or 2 years ofcomputer technology1 year additional of any of the above1 year of fine arts or speech

In addition, the student must maintain a 2.5GPA in the required courses and a cumulative 2.5GPA for high school, abstain from abusing drugsand alcohol, abstain from criminal activity, andmeet certain other requirements.

For a student who successfully completes theprogram, the State will pay the student’s collegetuition according to schedules published by theRegents for Higher Education. The programcovers only tuition and does not cover books,room and board, activities, and special fees.Students are encouraged to apply for otherfinancial aid for assistance with these other costs.

The statutes provide a mechanism to reducethe number of awards in the event that funding isinsufficient to cover anticipated costs. However,this provision is not widely discussed inOklahoma’s Promise promotional literature. Sincestudents must complete actions that they mightnot in the absence of Oklahoma’s Promise, the

very name of the program indicates the State hasobligated itself to fund the scholarships and hastherefore incurred a liability.

Approximately 28,500 Oklahoma high schoolstudents are enrolled in the Oklahoma’s Promiseprogram. The State projects the cost of tuition forthe program for the current year to be $54 million.The liability for future tuition payments for highschool students enrolled in the program and forcollege students in the program for whom addi-tional tuition payments beyond the current yearwill be made is estimated to be $313.8 million.

No other significant change is contemplatedexcept that the illustrative financial statementswould not distinguish between the obligationsrelated to governmental activities, business-typeactivities, or component units.

Note 10. Restatements of Balances

No significant change is contemplated.

Note 11. Nonrecourse Debt and Debt Guarantees

No significant change is contemplated.

Note 12. Retirement and Pension Systems

No significant change is contemplated in thenotes, but the full extent of the present value ofpension assets and pension liabilities is reportedon the balance sheet.

Note 13. Other Postemployment Benefits

No significant change is contemplated in thenotes, but the full extent of the present value ofother postemployment benefits is reported on thebalance sheet. The State does not maintainassets to offset this liability.

Note 14. On-Behalf Payments

No significant change is contemplated.

Note 15. Tax Preferences

The State levies taxes to finance many of itsactivities. As part of its system of taxation, theState grants certain tax preferences includingexemptions, credits, exclusions, deferrals, prefer-ential rates, and other provisions. In alternateyears, the Oklahoma Tax Commission attempts toestimate the amount of revenue the State wouldhave collected but for the existence of the taxpreference. The tax preferences with the largestestimated impacts on revenue as calculated bythe Oklahoma Tax Commission are listed below.

20

Preference Amount

Sales tax on sales of items used in the manufacturing process ...................................................... $1,623,110

Sales of items for the purpose of resale .............................................................................................. $1,493,000

Use of itemized and standard deductions on individual income tax ................................................. $685,506

Use of personal exemption on individual income tax .......................................................................... $137,911

Sales tax on sales to counties, municipalities, and other local governments .................................. $104,750

Sales tax on utilities for residential use ................................................................................................... $99,592

Cigarette tax on sales to Indian tribes that have compacted with the State ...................................... $96,648

Sales tax on sales to the State of Oklahoma .......................................................................................... $85,105

Motor vehicle excise tax on used motor vehicles held for sale by dealers ......................................... $70,726

Sales tax on sales of livestock, agricultural products,and certain items used in agricultural production ................................................................................. $63,905

Prorated motor vehicle excise tax on registered trucks and trailers .................................................... $63,516

Tax on sales of prescription drugs and similar items ............................................................................ $60,967

Rebate of 6/7 of gross production tax paid on oil and gas produced fromdeep wells, horizontally drilled wells, and other special wells ............................................................ $57,000

Exclusion from income tax for up to $7,500 of most government retirementand Social Security benefits ...................................................................................................................... $50,215

Use tax on livestock brought into Oklahoma for eventual sale ............................................................ $48,049

Sales tax on advertising ............................................................................................................................. $46,794

Use tax on property to be used by airlines or railroads ........................................................................ $45,706

Credit for sales tax paid by individuals with gross income of less than

$20,000 or families with less than $50,000 ............................................................................................. $37,813

Credit for income tax paid to another state on personal services income .......................................... $33,321

Income tax credit equal to 5 percent of federal earned income tax credit .......................................... $30,243

Nonrefundable income tax credit for an investment in depreciable propertyor to increase in employment .................................................................................................................... $28,680

Sales tax on food purchased with food stamps ...................................................................................... $20,731

Other tax preferences may not be includedbecause the Oklahoma Tax Commission does notcalculate an estimate of the revenue impact orhas determined that a meaningful estimatedcannot be made. The Tax Expenditures Report isprepared by the Tax Policy Division of the Okla-homa Tax Commission and is available from theCommission.

Note 16. Commitments

No significant change is contemplated.

Note 17. Litigation and Contingencies

No significant change is contemplated.

Note 18. Workforce Resources and Qualifications