ENERGY SUBSIDIES IN THE EUROPEAN UNION - CORE · · 2017-05-03ENERGY SUBSIDIES IN THE EUROPEAN...

85

WORKING DOCUMENT OF THE EUROPEAN PARLIAMENT'S DG FOR RESEARCH. NOT YET PUBLISHED BY THE EUROPEAN PARLIAMENT. ENERGY SUBSIDIES IN THE EUROPEAN UNION Final Report Frans Oosterhuis Institute for Environmental Studies (IVM) Vrije Universiteit Amsterdam July 2001

Transcript of ENERGY SUBSIDIES IN THE EUROPEAN UNION - CORE · · 2017-05-03ENERGY SUBSIDIES IN THE EUROPEAN...

WORKING DOCUMENT OF THE EUROPEAN PARLIAMENT'S DG FOR RESEARCH.

NOT YET PUBLISHED BY THE EUROPEAN PARLIAMENT.

ENERGY SUBSIDIES IN THE EUROPEAN UNION

Final Report

Frans OosterhuisInstitute for Environmental Studies (IVM)Vrije UniversiteitAmsterdam

July 2001

2

ACKNOWLEDGEMENT

This study on energy subsidies in the EU was commissioned by the European Parliament,Directorate General for Research. The author would like to thank all those who providedvaluable suggestions and comments on earlier drafts of this report.

3

CONTENTS

SUMMARY...............................................................................................................................................................................5INTRODUCTION..................................................................................................................................................................71. METHODOLOGICAL ISSUES AND GENERAL CONSIDERATIONS.........................................................8

1.1 DEFINING AND QUANTIFYING ENERGY SUBSIDIES.................................................................................81.2 EXTERNAL COSTS AND UNCOMPENSATED DAMAGE.............................................................................91.3 THE INHERITANCE OF PAST SUBSIDIES.......................................................................................................11

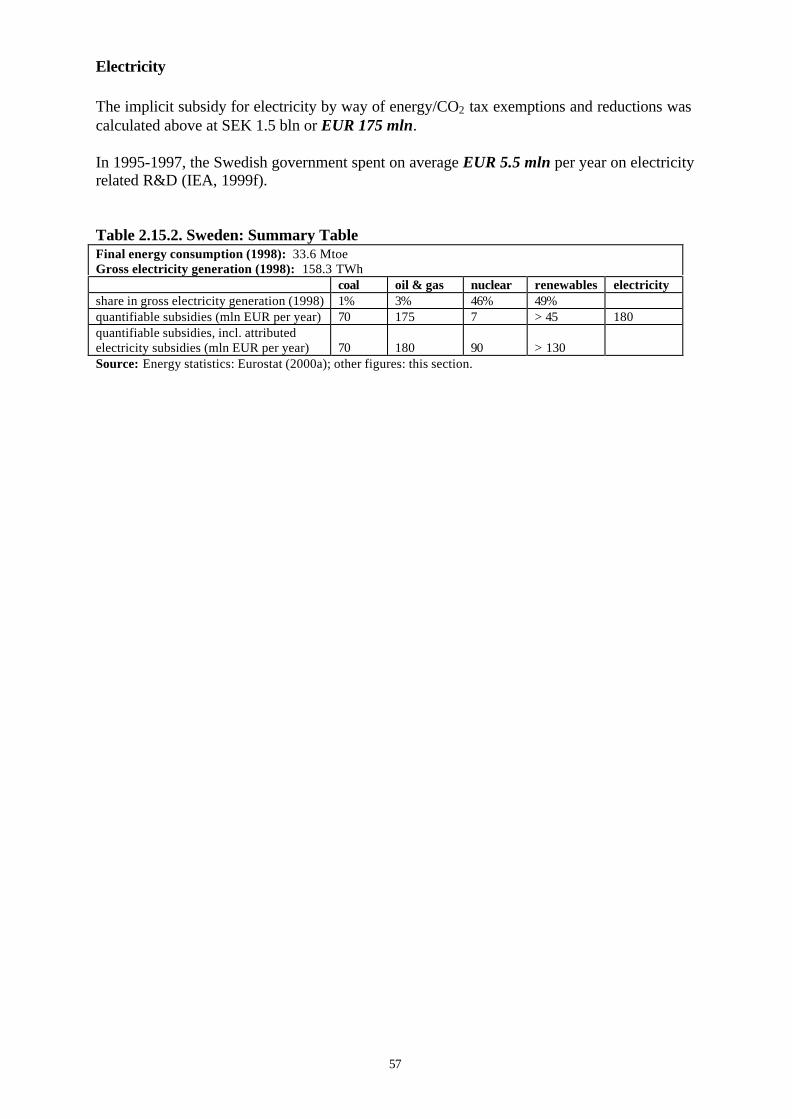

2. ENERGY SUBSIDIES IN THE EUROPEAN UNION......................................................................................... 132.1 THE EUROPEAN UNION........................................................................................................................................142.2 AUSTRIA......................................................................................................................................................................182.4 DENMARK...................................................................................................................................................................232.5 FINLAND.....................................................................................................................................................................262.6 FRANCE........................................................................................................................................................................282.7 GERMANY...................................................................................................................................................................332.8 GREECE........................................................................................................................................................................372.9 IRELAND.....................................................................................................................................................................402.10 ITALY..........................................................................................................................................................................423.11 LUXEMBOURG........................................................................................................................................................452.12 THE NETHERLANDS.............................................................................................................................................472.13 PORTUGAL...............................................................................................................................................................512.14 SPAIN..........................................................................................................................................................................532.15 SWEDEN ....................................................................................................................................................................552.16 UNITED KINGDOM................................................................................................................................................58

3. THE ACCESSION COUNTRIES .......................................................................................................................... 603.1 BULGARIA ..................................................................................................................................................................603.2 CYPRUS........................................................................................................................................................................613.3 CZECH REPUBLIC....................................................................................................................................................623.4 ESTONIA ......................................................................................................................................................................643.5 HUNGARY...................................................................................................................................................................653.6 LATVIA ........................................................................................................................................................................673.7 LITHUANIA ................................................................................................................................................................683.8 MALTA .........................................................................................................................................................................693.9 POLAND.......................................................................................................................................................................703.10 ROMANIA .................................................................................................................................................................713.11 SLOVAKIA ................................................................................................................................................................723.12 SLOVENIA ................................................................................................................................................................743.13 TURKEY.....................................................................................................................................................................75

4. CONCLUSIONS.............................................................................................................................................................. 77REFERENCES ..................................................................................................................................................................... 79APPENDIX: ABBREVIATIONS .................................................................................................................................... 85

4

5

SUMMARY

Many European governments as well as the EU itself provide financial support to varioussources of energy. Such subsidies have been introduced for a variety of reasons, includingeconomic, social, political, technological and environmental ones. However, energy subsidiesalso imply market distortions, leading to inefficiencies in the functioning of energy markets,and they may have unwanted side effects, such as reducing the attractiveness of energyconservation and renewable energy.

The present study contains a survey of energy subsidies existing in the EU and the AccessionCountries by the end of the 20th century. Lacking any ‘objective’ definition of whatconstitutes a subsidy, and lacking any ‘objective’ baseline against which the size of a subsidycan be measured, some pragmatic and sometimes arbitrary choices had to be made.Furthermore, the information needed to quantify the amounts of subsidy involved was notalways available.

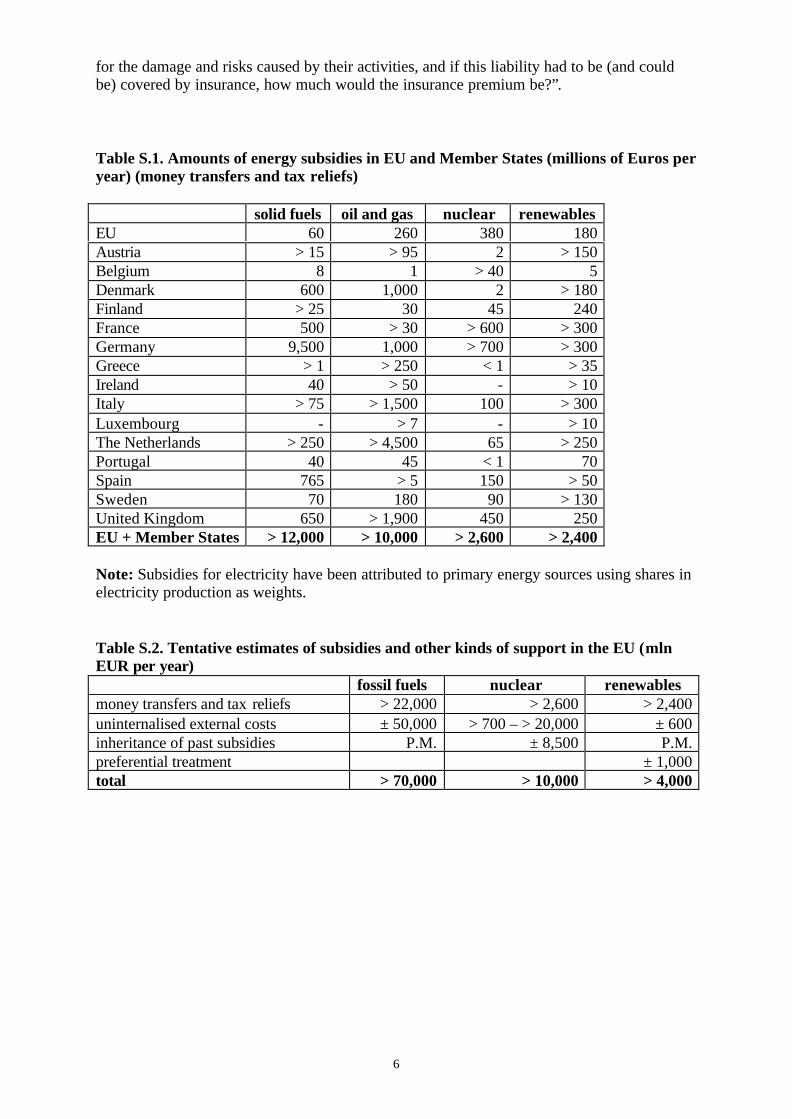

When only looking at money transfers and tax reliefs (see Table S.1), it can be concluded thatthe total amount of subsidy that the EU and its Member States give to renewable energy issubstantially lower than the amount of subsidy to fossil fuels, and probably in the same orderof magnitude of the subsidies to nuclear alone.

A major part of the identified subsidies relates to tax exemptions and reductions. There aretwo major groups: those which have been introduced for social reasons (usually reducedVAT rates for households) and those intended to protect industry against the loss ofinternational competitiveness. The latter are often accompanying the introduction of specificenergy and/or CO2 taxes. Renewable energy is subsidised directly as well as by means ofvarious fiscal arrangements. R&D subsidies play a particularly important role in the case ofnuclear energy.

Direct subsidies to coal production are declining throughout Europe, although the Germancoal subsidies remain one of the largest single subsidy items. Tax reductions and exemptionsare an important component of the subsidies to oil, gas and electricity and they tend toincrease as more countries are introducing energy tax schemes. Support for renewables is alsoincreasing, whereas subsidies to nuclear energy do not show a clear trend.

In the accession countries, especially the former centrally planned economies, subsidies aregenerally decreasing. In particular, cross subsidies from industry to households are graduallybeing phased out.

In addition to these direct and indirect subsidies, there are three important factors favouringcertain types of energy over others. Firstly, energy producers and users often do not pay forthe (full) external costs and damage (such as pollution, accidents and risks). In some cases(oil spills, nuclear accidents), international conventions provide for limited liability of theperpetrators. Secondly, ‘traditional’ energy continues to benefit from support that it hasreceived in the past, e.g. in the form of below-commercial rates of return on investments.Finally, legal arrangements provide for preferential treatment of specific types of energy(especially renewables). Although these kinds of support are much harder to translate intomoney terms, some attempts to do so have been made. A comparison with the amountsinvolved in money transfers and tax reliefs is given in Table S.2. This shows that the bias infavour of ‘traditional’ sources of energy is even stronger if these factors are taken intoaccount.

A more precise and reliable estimate of the bias against renewable energy might be achievedby means of a study to answer the question: “If energy producers and users were fully liable

6

for the damage and risks caused by their activities, and if this liability had to be (and couldbe) covered by insurance, how much would the insurance premium be?”.

Table S.1. Amounts of energy subsidies in EU and Member States (millions of Euros peryear) (money transfers and tax reliefs)

solid fuels oil and gas nuclear renewablesEU 60 260 380 180Austria > 15 > 95 2 > 150Belgium 8 1 > 40 5Denmark 600 1,000 2 > 180Finland > 25 30 45 240France 500 > 30 > 600 > 300Germany 9,500 1,000 > 700 > 300Greece > 1 > 250 < 1 > 35Ireland 40 > 50 - > 10Italy > 75 > 1,500 100 > 300Luxembourg - > 7 - > 10The Netherlands > 250 > 4,500 65 > 250Portugal 40 45 < 1 70Spain 765 > 5 150 > 50Sweden 70 180 90 > 130United Kingdom 650 > 1,900 450 250EU + Member States > 12,000 > 10,000 > 2,600 > 2,400

Note: Subsidies for electricity have been attributed to primary energy sources using shares inelectricity production as weights.

Table S.2. Tentative estimates of subsidies and other kinds of support in the EU (mlnEUR per year)

fossil fuels nuclear renewablesmoney transfers and tax reliefs > 22,000 > 2,600 > 2,400uninternalised external costs ± 50,000 > 700 – > 20,000 ± 600inheritance of past subsidies P.M. ± 8,500 P.M.preferential treatment ± 1,000total > 70,000 > 10,000 > 4,000

7

INTRODUCTION

Subsidies and other types of financial support to various sources of energy are quite commonthroughout the European Union, as well as in the countries that have applied for membership(the accession countries). These subsidies have been introduced for various reasons, such as:- ‘traditional’ energy policy considerations (security of supply, diversification,

development of domestic energy resources, competitiveness);- social and regional policy considerations (e.g. to maintain income and employment in

mining regions or to make heating fuels affordable for low-income households);- technology policy considerations (e.g. to build up a strong international position in

nuclear know-how);- environmental policy considerations (e.g. to stimulate renewable energy).

In a liberalising European energy market, the need for a ‘level playing field’ implies the needfor a critical assessment of the distortions created by existing energy subsidies. Furthermore,financial support to conventional energy sources may be barriers to achieve the EU’s policyobjectives on CO2 reduction and a higher share of renewables.

Against this background, the European Parliament has commissioned the present study,which presents a survey of existing energy subsidies in the EU, its member states and theaccession countries.

The report is structured as follows. In Chapter 1, some methodological aspects and generalconsiderations are discussed. Chapter 2 presents a review of energy subsidies in the EU andits 15 member states. The situation in the 13 accession countries is described in Chapter 3,whereas Chapter 4 contains the conclusions.

8

1. METHODOLOGICAL ISSUES AND GENERAL CONSIDERATIONS

1.1 DEFINING AND QUANTIFYING ENERGY SUBSIDIES

The fact that many governments provide substantial amounts of financial support to theproduction and consumption of energy has led to a considerable research activity in recentyears. An important reason for the interest in energy subsidies is the possible negative impacton the environment that they could have, by providing ‘perverse’ incentives – i.e., byincreasing the demand for energy in general and for polluting types of energy in particular.Another major concern, mainly expressed by economists, are the market distortions thatenergy subsidies generate, thus impeding the market mechanism to function properly, leadingto a sub-optimal allocation and restricting social welfare. Several studies have been publishedon environmentally adverse subsidies, including energy subsidies (e.g. Roodman, 1996; DeMoor and Calamai, 1997; Greenpeace, 1997; Myers and Kent, 1998; OECD, 1996, 1999b).

When trying to identify and quantify energy subsidies, one will unavoidably be confrontedwith a number of methodological and definition problems. Two of the main problems are:1. The fact that there is no fundamental difference between energy subsidies in a narrow

sense (i.e., direct payments from the public budget benefiting the supply or use of energy)and other kinds of support. Thus, all policies favouring the production or consumption of(specific kinds of) energy can in principle be seen as ‘subsidies’. Looking only at actualcash flows would lead to a limited and distorted result. However, including all policiesthat affect the supply of and demand for energy would imply an unmanageable task.Somehow, a compromise between the two extremes has to be found. The emphasis in thisreport is on subsidies involving actual money transfers (including tax relief), but attentionis also paid to other kinds of support (see Sections 1.2, 1.3 and 1.4).

2. The fact that there is no such thing as an ‘objective baseline’, i.e. an ‘ideal’ situation thatprovides a reference against which the size of a subsidy can be measured. For example,the fact that fuels are taxed more heavily when they are used for transport than when theyare used for heating could be regarded as a subsidy for the heating fuels. However, thehigher tax for the transport fuel can also be seen as a payment for the use of infrastructureand for ‘external costs’ (such as congestion and accidents). Determining whether asubsidy exists (either on the transport or the heating fuel) and what its size is wouldrequire a full assessment of these external costs, which is obviously not feasible.

The present study takes a pragmatic approach in dealing with these complexities. Rather thanstarting from a definition of energy subsidies, the demarcation line has been drawn bydescribing types of support that have remained beyond the scope of the study. Thus, thefollowing arrangements are not included as energy subsidies1:- differences in mineral oil tax rates between road traffic and other types of use of the same

fuel;- differentiations and exemptions in excise taxes on mineral oil products for road transport

(e.g., reduced rates for unleaded petrol or low-sulphur diesel);- exemptions from taxes for fuels which are used for non-energy purposes (e.g. as a

chemical feedstock);- exemptions from taxes for fuels which are used for electricity generation (if electricity is

taxed);- public money for investments that only have an indirect relationship with energy use

(e.g., in road infrastructure);

1 In some cases, they may be mentioned in the text, but they are not counted as subsidies whenestimating the order of magnitude of subsidies for particular types of energy.

9

- public money for programs related to the termination of energy production activities, in asfar as these expenditures are not part of the normal costs that should have been borne bythe operator of the activity (e.g. losses incurred due to a politically motivated earlyclosure of nuclear plants; social programs to alleviate the consequences of coal mineclosures);

- differentiations in the conditions under which energy companies can operate (lacking any‘baseline’ for these conditions), except when these conditions relate to provisions whichalso apply to other industries (thus, a lower corporate tax rate for oil and gas producingcompanies than for other companies is included as a subsidy, but differences in the state’sshare in mining profits or royalties are not);

- subsidy schemes which are not exclusively related to energy and for which the partrelated to energy could not be identified separately;

- ‘cross-subsidies’, i.e. subsidies entirely financed by other users of the same kind ofenergy;

- financial compensation, given in reaction to energy price increases (such as those givenby several governments to the transport, agriculture and fisheries sectors, followingprotests in autumn 2000);

- subsidies for energy conservation (including subsidies for combined heat and power2);- general energy subsidies which could not be allotted to a particular fuel or type of energy;- general public provisions that can be related to energy (e.g. military expenditures to

safeguard oil supplies from the Middle East, or the cost of police forces protectingnuclear transports).

Furthermore, the present report does not refer to subsidies to energy projects and investmentsoutside the EU or the accession countries. Subsidies amounting to less than EUR 1 millionper year are also excluded. The emphasis is on subsidies provided by central governments,although subsidies by regional governments are included where they play an important role inenergy policies.

Having drawn these pragmatic demarcation lines, an overview of the various energy subsidyschemes in the EU and the accession countries will be presented in the next chapters. Beforedoing so, three types of government support will be discussed that do not involve actualmoney transfers, but which can be important factors favouring particular types of energy: thenon-internalisation of external costs, the lasting impact of subsidies that have been providedin the past; and the existence of legal arrangements giving preferential treatment to certainkinds of energy.

1.2 EXTERNAL COSTS AND UNCOMPENSATED DAMAGE

An important, but largely hidden type of support to energy is the fact that energy producersand consumers often do not pay the full social cost of energy. In economic terms: the externalcost of energy remains to a large extent uninternalised. Examples of such costs are theenvironmental damage caused by oil spills or by air pollution from burning fossil fuels, thecosts of accidents (e.g. in coal mining), and the risks associated with nuclear power.Obviously, some internalisation occurs if regulations are in place which oblige the energyproducer or user to take preventive measures or to compensate the damage. However, thecosts of the uncompensated damage and risks that remain are largely borne by society as awhole rather than by the firms or individuals bringing them about. Such shifts of (potential)costs from the private to the public domain can be seen as subsidies.

2 Although subsidies to combined heat and power (CHP) are intended to be instruments of energyconservation, they can also be regarded as subsidies favouring the fuel that is being used. However, even if onetakes that vision, the subsidy could not be attributed to one particular kind of energy, because CHP can involveseveral types of fuels (though in practice the majority is fossil).

10

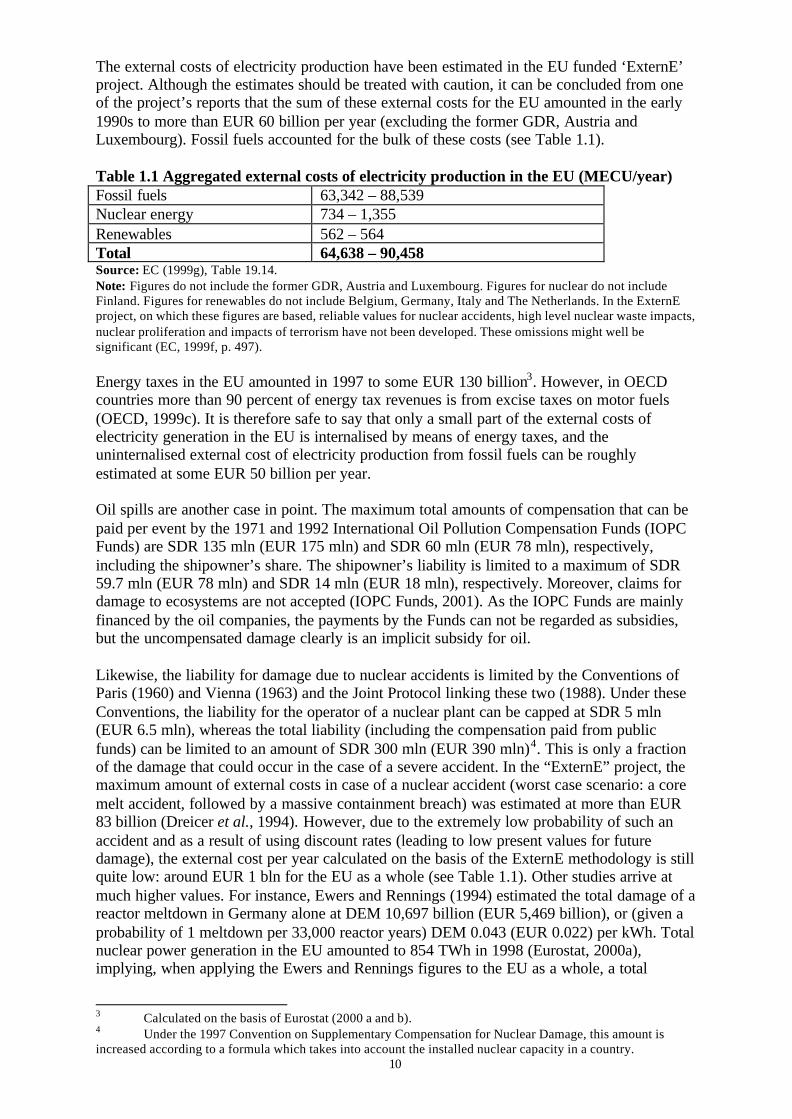

The external costs of electricity production have been estimated in the EU funded ‘ExternE’project. Although the estimates should be treated with caution, it can be concluded from oneof the project’s reports that the sum of these external costs for the EU amounted in the early1990s to more than EUR 60 billion per year (excluding the former GDR, Austria andLuxembourg). Fossil fuels accounted for the bulk of these costs (see Table 1.1).

Table 1.1 Aggregated external costs of electricity production in the EU (MECU/year)Fossil fuels 63,342 – 88,539Nuclear energy 734 – 1,355Renewables 562 – 564Total 64,638 – 90,458Source: EC (1999g), Table 19.14.Note: Figures do not include the former GDR, Austria and Luxembourg. Figures for nuclear do not includeFinland. Figures for renewables do not include Belgium, Germany, Italy and The Netherlands. In the ExternEproject, on which these figures are based, reliable values for nuclear accidents, high level nuclear waste impacts,nuclear proliferation and impacts of terrorism have not been developed. These omissions might well besignificant (EC, 1999f, p. 497).

Energy taxes in the EU amounted in 1997 to some EUR 130 billion3. However, in OECDcountries more than 90 percent of energy tax revenues is from excise taxes on motor fuels(OECD, 1999c). It is therefore safe to say that only a small part of the external costs ofelectricity generation in the EU is internalised by means of energy taxes, and theuninternalised external cost of electricity production from fossil fuels can be roughlyestimated at some EUR 50 billion per year.

Oil spills are another case in point. The maximum total amounts of compensation that can bepaid per event by the 1971 and 1992 International Oil Pollution Compensation Funds (IOPCFunds) are SDR 135 mln (EUR 175 mln) and SDR 60 mln (EUR 78 mln), respectively,including the shipowner’s share. The shipowner’s liability is limited to a maximum of SDR59.7 mln (EUR 78 mln) and SDR 14 mln (EUR 18 mln), respectively. Moreover, claims fordamage to ecosystems are not accepted (IOPC Funds, 2001). As the IOPC Funds are mainlyfinanced by the oil companies, the payments by the Funds can not be regarded as subsidies,but the uncompensated damage clearly is an implicit subsidy for oil.

Likewise, the liability for damage due to nuclear accidents is limited by the Conventions ofParis (1960) and Vienna (1963) and the Joint Protocol linking these two (1988). Under theseConventions, the liability for the operator of a nuclear plant can be capped at SDR 5 mln(EUR 6.5 mln), whereas the total liability (including the compensation paid from publicfunds) can be limited to an amount of SDR 300 mln (EUR 390 mln)4. This is only a fractionof the damage that could occur in the case of a severe accident. In the “ExternE” project, themaximum amount of external costs in case of a nuclear accident (worst case scenario: a coremelt accident, followed by a massive containment breach) was estimated at more than EUR83 billion (Dreicer et al., 1994). However, due to the extremely low probability of such anaccident and as a result of using discount rates (leading to low present values for futuredamage), the external cost per year calculated on the basis of the ExternE methodology is stillquite low: around EUR 1 bln for the EU as a whole (see Table 1.1). Other studies arrive atmuch higher values. For instance, Ewers and Rennings (1994) estimated the total damage of areactor meltdown in Germany alone at DEM 10,697 billion (EUR 5,469 billion), or (given aprobability of 1 meltdown per 33,000 reactor years) DEM 0.043 (EUR 0.022) per kWh. Totalnuclear power generation in the EU amounted to 854 TWh in 1998 (Eurostat, 2000a),implying, when applying the Ewers and Rennings figures to the EU as a whole, a total

3 Calculated on the basis of Eurostat (2000 a and b).4 Under the 1997 Convention on Supplementary Compensation for Nuclear Damage, this amount isincreased according to a formula which takes into account the installed nuclear capacity in a country.

11

external cost from nuclear accident risks for the EU of almost EUR 20 billion per year.Including the external cost of other parts of the nuclear cycle would imply still (much) higherfigures. Allowing nuclear plant operators to leave this damage largely uninsured implies animplicit subsidy (by way of unpaid insurance premiums) in the same orders of magnitude.

It can be concluded that the size of uninternalised external costs of energy is considerable,even though the estimates are largely uncertain (especially in the case of nuclear). In order toarrive at more precise figures of the implicit subsidy involved, it might be interesting tolaunch a study to answer the question: “If energy producers and users were fully liable for thedamage and risks caused by their activities, and if this liability had to be (and could be)covered by insurance, how much would the insurance premium be?”.

1.3 THE INHERITANCE OF PAST SUBSIDIES

Before the process of liberalisation and privatisation started in the EU, energy supply waswidely regarded as a ‘public service’. Energy companies were in many cases state owned andheavily regulated so as to contribute to the political objectives of governments. Although theinvisible subsidies implied in these arrangements have been substantially reduced, they havenot disappeared. Moreover, the impact of past subsidies can remain a beneficial factor forparticular types of energy for a long time, especially in case of long term investments.

For example, countries like The Netherlands and Denmark have devoted large amounts ofmoney to the creation of natural gas networks. Although the role of direct governmentsubsidies was limited, tariff regulations and fiscal facilities have played an important role.Present users of natural gas are still benefiting from these investments by paying lower pricesthan would have been the case if the infrastructure had been financed on commercial terms.

Similarly, investments in nuclear power plants have been facilitated by requiring financialrates of return well below commercial rates. Michaelis (1997) argues that, if a 10%-11%required rate of return (RRR) is taken as the benchmark for the market rate, the 5% RRRrequired by the British government in the early 1980s reduced the apparent cost of nuclear-generated electricity by approximately 1.6 pence per kWh (nearly 40%). Investment innuclear power plants has also benefited from direct subsidies. For instance, the EuropeanCommunity has contributed EUR 2.9 billion to investments in nuclear power plants since thestart of the Euratom Treaty in 1957 (EC, 2000r). Current nuclear power production stillbenefits from these capital subsidies. Assuming that for all existing nuclear capacity in theEU government investment support has led to an average cost reduction of EUR 0.01 perkWh, the effective annual subsidy (given the above mentioned nuclear power generation of854 TWh) amounts to some EUR 8.5 billion.

Renewable energy also benefits from past public investments (e.g. in large scalehydropower), but to a much lesser extent.

Another example of subsidy legacies from the past are the ‘stranded costs’ involved inprojects that would have been too risky for a commercial firm, but could be done thanks tothe ‘soft budget constraints’ of state owned or monopolistic enterprises. Examples are the fastbreeder reactors that have been closed down in Germany and France and an expensive coalgasification project in The Netherlands. With the liberalisation of the energy markets, thesecosts and the huge subsidies they imply are becoming visible.

12

1.4 PREFERENTIAL TREATMENT OF PARTICULAR TYPES OF ENERGY

Several EU governments have introduced arrangements requiring energy companies topurchase specific kinds of electricity (in particular renewables based) from independentpower producers at a fixed price. The best known example of such an arrangement is theGerman ‘Stromeinspeisungsgesetz’. Comparable arrangements exist in Austria, Greece, Italyand Spain. In March 2001, the European Court of Justice has ruled that this type of supportdoes not constitute state aid under the EU Treaty (ENDS, 2001). Nevertheless, an implicitsubsidy element is involved. In 1997, electricity production from renewables in the fivecountries mentioned (excluding large scale hydro, which usually does not qualify for such‘feed in’ arrangements) amounted to 33 TWh (calculated on the basis of EC (2000v) andEurostat, (2000a)). Assuming an average price premium of EUR 0.03 per kWh, the implicitannual subsidy can be estimated to be in the order of magnitude of EUR 1 billion.

13

2. ENERGY SUBSIDIES IN THE EUROPEAN UNION

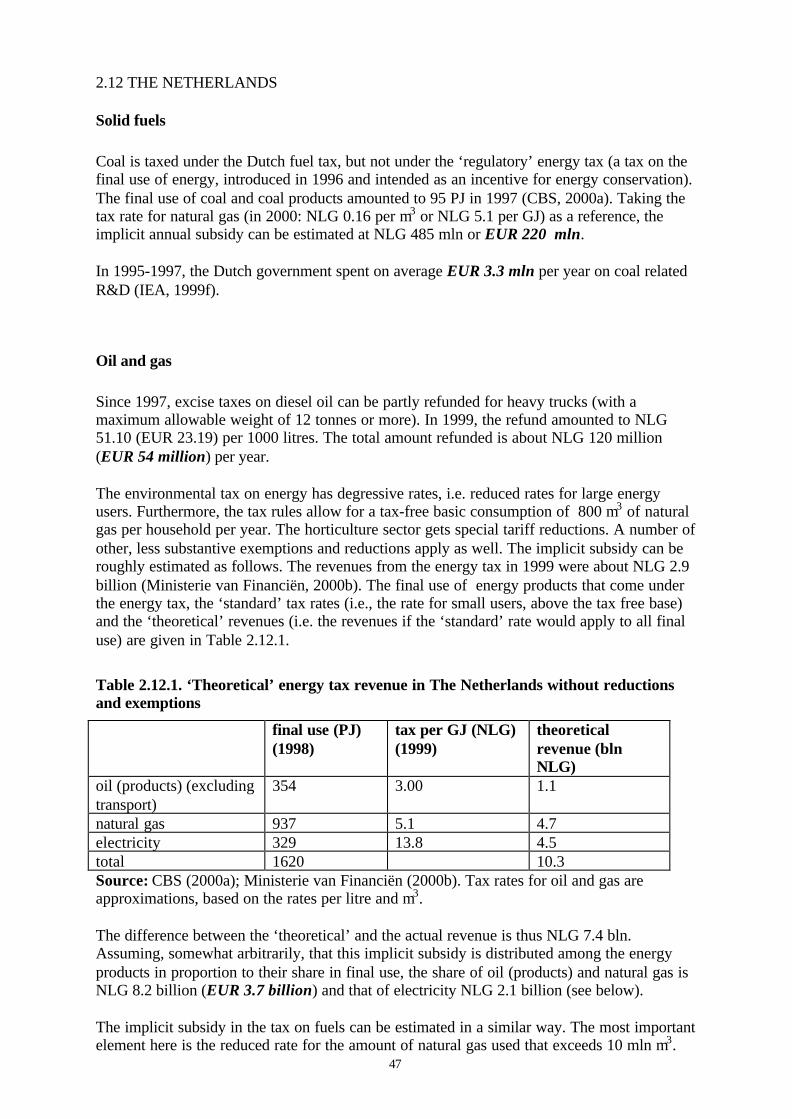

This Chapter provides information on the energy subsidies provided by the EU and its fifteenmember states. They are classified by category of energy: solid fuels (coal, lignite and peat);oil and gas; nuclear energy; renewables; and electricity. The most recent availableinformation has been used, generally relating to the late 1990s or the year 2000.

To the extent possible, attempts have been made to quantify the amounts of subsidiesinvolved5. As a reasonably precise quantification of subsidies is not always possible, theamounts mentioned should be treated with caution and mainly be regarded as indicators ofthe orders of magnitude. The (rounded) total amounts of quantifiable subsidies by type ofenergy are mentioned in the tables at the end of each section. Subsidies to electricity havebeen ‘translated’ into subsidies for primary energy sources by distributing them according tothe share of each energy type in total gross electricity generation in 1998.

5 Quantifiable subsidy amounts have been expressed in Euros per year (printed bold and in italics).Exchange rates used are those of December 31st, 1999. Incidentally, the value of the Euro and the US Dollarwere almost exactly the same by that date. In case of subsidy amounts showing large differences betweendifferent years, averages of several years have been calculated to the extent possible.

14

2.1 THE EUROPEAN UNION

General

Many EU energy subsidy schemes and funding programmes cover energy in general and cantherefore not always be attributed (completely) to a particular type of energy. The main‘general’ support schemes that are relevant for energy include:- The Thematic Programme ‘Energy’ within the 5th framework programme for research,

technological development and demonstration (1999-2002). The budget is EUR 1,042mln, of which 1,026 mln for ‘key actions’. Part of this amount could be attributed tospecific types of energy (see Table 2.1.1)6;

- Parts of the Structural Funds (which include the Regional Development Fund (ERDF),the Social Fund and the Guidance section of the European Agricultural Guidance andGuarantee Fund). Under Objective I, an amount of EUR 2,496 mln was budgeted forenergy projects in the period 1994-1999. Energy projects have been financed undernational programmes as well as under various Community Initiatives, such as Interreg II,FEDER, Urban, EMS, Leader and Regis II;

- Parts of Phare (mainly within the sectors ‘environment and nuclear safety’ and‘infrastructure’, for which in the period 1990-1998 EUR 447 mln and EUR 958 mln hasbeen disbursed, respectively - EC, 2000s);

- ALURE: a programme for economic co-operation in the energy sector between the EUand Latin America (budget: EUR 25 mln for the period 1998-2002);

- Synergy: a programme for co-operation with non-member countries in the area of energy.It has a budget of EUR 15 mln for the period 1998-2002;

- ETAP: a programme for analysis and forecast at the EU level, and other related work inthe energy sector (budget: EUR 5 mln for the period 1998-2002)

Table 2.1.1. Subdivision of RTD subsidies for energy in the 5th Framework ProgrammeKey action: Cleaner energysystems, including renewables

Key action: Economic and efficientenergy for a competitive Europe

Total (mln €)

percentage amount (mln € ) percentage amount (mln € )coal 1.6 7.7 0.3 2.0 9.7oil and gas 2.6 12.7 25.7 140.7 153.4renewables 50.3 240.7 27.6 151.2 391.9electricity 22.9 109.7 5.9 32.0 141.7other/notattributable

22.6 108.3 40.4 221.1 329.4

TOTAL 100 479 100 547 1,026

Solid fuels

The CARNOT programme was devised in order to promote European technology relating tothe clean and efficient use of solid fuels. It covers the years 1998-2002 and has a budget ofEUR 3 mln (somewhat less than EUR 1 mln per year).

Within the framework of the ECSC, a coal research programme has been running for morethan 40 years. The current annual budget is about EUR 25 mln.

6 This has been done by attaching to each RTD project that has been funded up to now a weightconsisting of the product of its duration and number of participating institutions.

15

The share of coal in the 5th RTD programme’s budget was estimated at EUR 9.7 mln (cf.Table 2.1.1) or EUR 2 mln per year.

Under a 1994-1999 Structural Funds programme, financial support for the use of peat inIreland has been provided (EC, 2001). The amount involved was about IEP 20 mln (IEA,1999c) or EUR 4 mln per year.

Under the Phare programme, support for coal related projects amounted to a total of EUR26.75 mln (EUR 3.3 mln per year) over the period 1990-1997 (calculated after ERM, 1999).

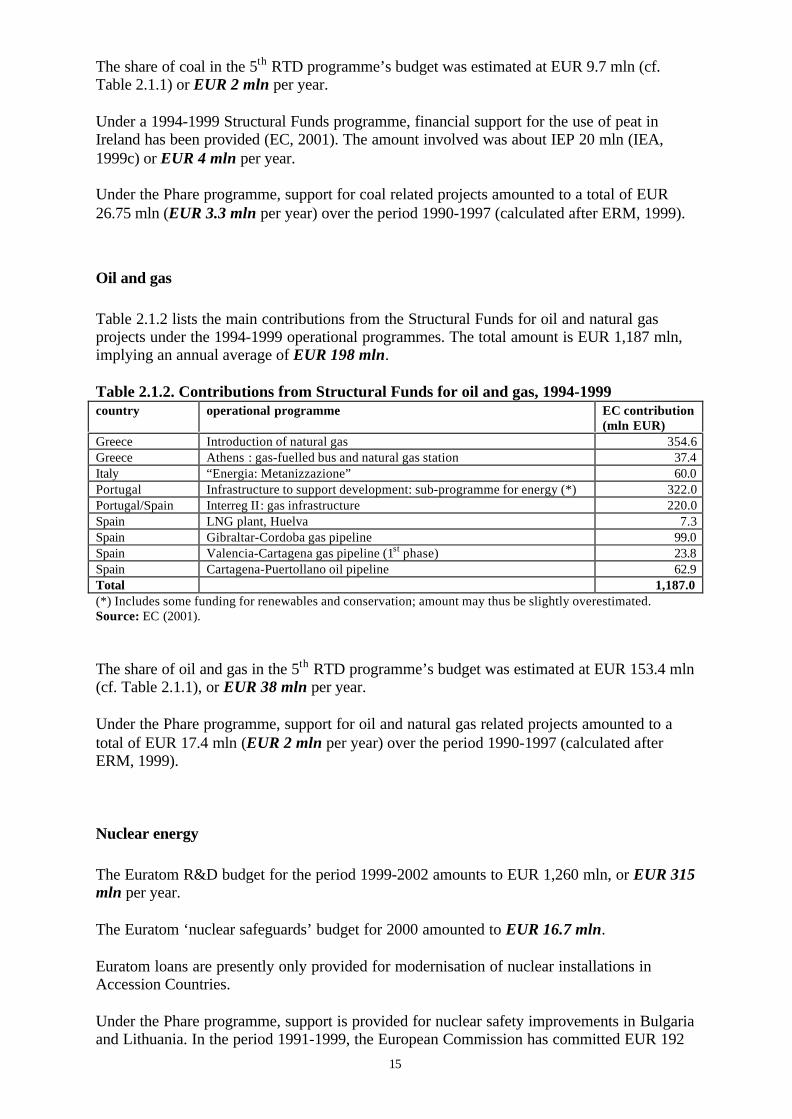

Oil and gas

Table 2.1.2 lists the main contributions from the Structural Funds for oil and natural gasprojects under the 1994-1999 operational programmes. The total amount is EUR 1,187 mln,implying an annual average of EUR 198 mln.

Table 2.1.2. Contributions from Structural Funds for oil and gas, 1994-1999country operational programme EC contribution

(mln EUR)Greece Introduction of natural gas 354.6Greece Athens : gas-fuelled bus and natural gas station 37.4Italy “Energia: Metanizzazione” 60.0Portugal Infrastructure to support development: sub-programme for energy (*) 322.0Portugal/Spain Interreg II: gas infrastructure 220.0Spain LNG plant, Huelva 7.3Spain Gibraltar-Cordoba gas pipeline 99.0Spain Valencia-Cartagena gas pipeline (1st phase) 23.8Spain Cartagena-Puertollano oil pipeline 62.9Total 1,187.0(*) Includes some funding for renewables and conservation; amount may thus be slightly overestimated.Source: EC (2001).

The share of oil and gas in the 5th RTD programme’s budget was estimated at EUR 153.4 mln(cf. Table 2.1.1), or EUR 38 mln per year.

Under the Phare programme, support for oil and natural gas related projects amounted to atotal of EUR 17.4 mln (EUR 2 mln per year) over the period 1990-1997 (calculated afterERM, 1999).

Nuclear energy

The Euratom R&D budget for the period 1999-2002 amounts to EUR 1,260 mln, or EUR 315mln per year.

The Euratom ‘nuclear safeguards’ budget for 2000 amounted to EUR 16.7 mln.

Euratom loans are presently only provided for modernisation of nuclear installations inAccession Countries.

Under the Phare programme, support is provided for nuclear safety improvements in Bulgariaand Lithuania. In the period 1991-1999, the European Commission has committed EUR 192

16

mln (on average EUR 21 mln per year) for nuclear safety under the Phare programme (EC,2000u).

Renewables

Financial support for renewable energy is mainly coming from the Structural Funds. Theamount spent on renewable energy in the period 1994-1999 is estimated at EUR 300 mln(EUR 50 mln per year). Projects have been supported in Greece, Spain, France, Ireland, Italy,Portugal, Austria and the United Kingdom, featuring notably wind, solar and biomass (EC,1999c).

The share of renewables in the 5th RTD programme’s budget was estimated at EUR 391.9mln (cf. Table 2.1.1) or EUR 98 mln per year.

A source of funding dedicated specifically to renewable energy is the Altener programme.The budget for Altener II (1998-2002) is EUR 77 mln or EUR 15 mln per year.

Under the Phare programme, support for renewables related projects amounted to a total ofEUR 14.3 mln (EUR 1.8 mln per year) over the period 1990-1997 (calculated after ERM,1999).

Electricity

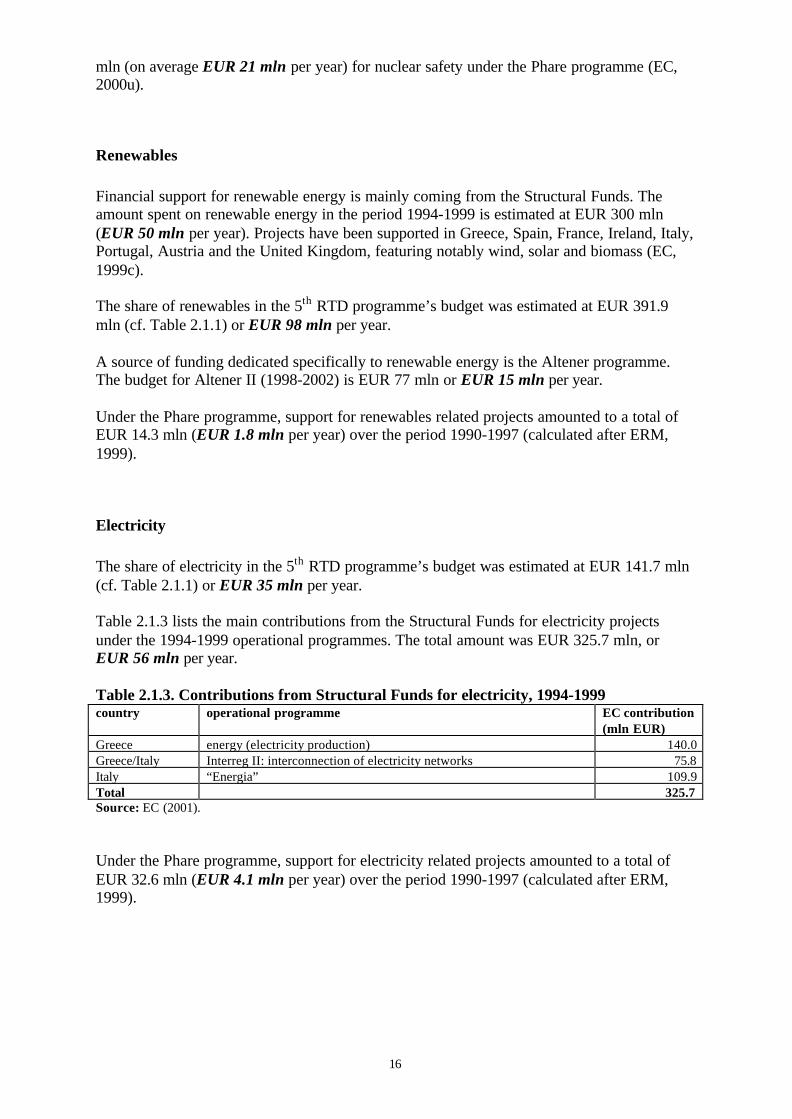

The share of electricity in the 5th RTD programme’s budget was estimated at EUR 141.7 mln(cf. Table 2.1.1) or EUR 35 mln per year.

Table 2.1.3 lists the main contributions from the Structural Funds for electricity projectsunder the 1994-1999 operational programmes. The total amount was EUR 325.7 mln, orEUR 56 mln per year.

Table 2.1.3. Contributions from Structural Funds for electricity, 1994-1999country operational programme EC contribution

(mln EUR)Greece energy (electricity production) 140.0Greece/Italy Interreg II: interconnection of electricity networks 75.8Italy “Energia” 109.9Total 325.7Source: EC (2001).

Under the Phare programme, support for electricity related projects amounted to a total ofEUR 32.6 mln (EUR 4.1 mln per year) over the period 1990-1997 (calculated after ERM,1999).

17

Table 2.1.4. European Union: Summary TableFinal energy consumption (1998): 945.5 MtoeGross electricity generation (1998): 2,490 TWh

coal oil & gas nuclear renewables electricityshare in gross electricity generation (1998) 27% 23% 34% 15%quantifiable subsidies (mln EUR per year) 35 240 350 165 95quantifiable subsidies, incl. attributedelectricity subsidies (mln EUR per year) 60 260 380 180Source: Energy statistics: Eurostat (2000a); other figures: this section.

18

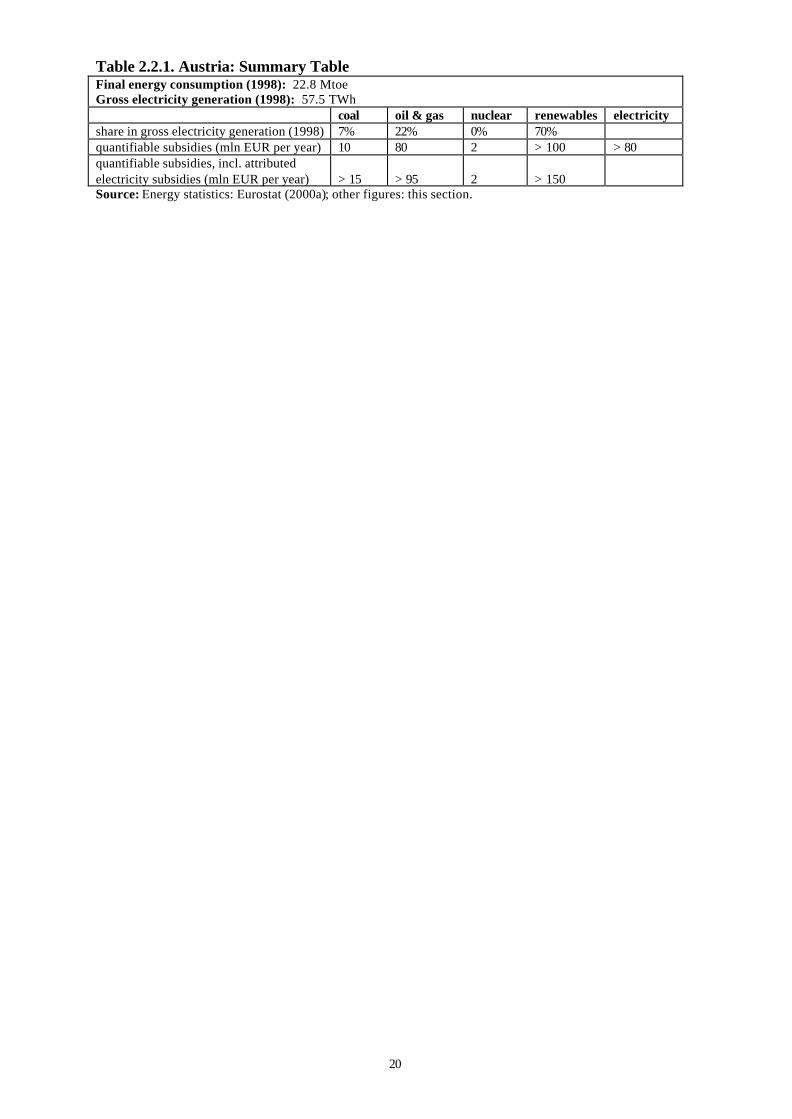

2.2 AUSTRIA

Solid fuels

The importance of coal in Austria’s energy market has greatly diminished over the past twodecades. Out of about 20 coal mines operating in the 1960s, only one still operates. Thegovernment’s financial support to the coal industry in 1996 was estimated to have beenaround ATS 75 million (EUR 5.5 mln). This support was mainly used for social programmesin connection with mine closures (which is not an energy subsidy in terms of this report), andfor exploration (IEA, 1998b).

Coal and coal products are not subject to the energy tax. If coal were taxed at the same rateper GJ as natural gas (ATS 0.6 per m3 or ATS 1.8 per GJ), the 66.6 PJ final use of coal andcoal products in 1998 (Statistik Österreich, 2000) would have been subject to a total taxamount of ATS 119.9 mln or EUR 8.7 mln.

In the years 1995-1998, the Austrian government spent less than EUR 1 mln per year on coalrelated R&D (IEA, 1999f).

Oil and gas

Natural gas and electricity are subject to an energy tax of ATS 0.60 per m3 and ATS 0.2 perkWh, respectively. Until June 2000, the rate for electricity was ATS 0.1 per kWh. For energyintensive enterprises there is a ceiling on the total tax burden of the energy tax. Total final gasconsumption amounted to 161.7 PJ or 4.49 bln m3 in 1998 and total final electricityconsumption to 179.8 PJ or 49.9 TWh (Statistik Österreich, 2000). If all final consumptionwere taxed, the revenues would have been ATS 2.7 billion and ATS 5.0 billion, respectively,or ATS 7.7 billion in sum. Total revenues from the energy tax were ATS 5.5 billion in 1997(EC, 2000b). Assuming (somewhat arbitrarily) an equal distribution of this implicit subsidybetween gas and electricity, both received ATS 1.1 billion or EUR 80 mln.

In 1998, the Austrian government spent less than EUR 1 mln per year on oil and gas relatedR&D (IEA, 1999f).

Land-locked Austria is not a member of an International Oil Pollution Compensation Fund.

Nuclear energy

Austria has no nuclear power plants.

In 1995-1998, the Austrian government spent on average EUR 2.0 mln per year on nuclearrelated R&D (IEA, 1999f). This budget was mainly for nuclear fusion.

19

Renewables

IEA (1998a) reports the following subsidies for renewable energy in Austria:- federal subsidies for biomass-based district heating: ATS 192 million (EUR 14 million)

in 1996;- capital subsidies of 8 to 25% for investments in small hydropower plants (no amounts

specified);- subsidies administered by the Ministry of Agriculture and Forests for biomass and small

hydropower projects: ATS 190 million (EUR 14 million) in 1996;- provincial support for solar, biomass and heatpumps: ATS 500 million (EUR 36 million)

in 1996;- guaranteed minimum prices for electricity from renewables that is traded between

provinces, ranging from ATS 0.421 to ATS 0.9 (EUR 0.03 to EUR 0.07) per kWh (noamounts specified).

In 1997, an investment fund was created providing subsidies of ATS 80 million (EUR 5.8million) per year for investments in power plants based on renewable sources (Novem,2001).

There are also a number of renewable energy subsidy schemes running at the level of theLänder.

For electricity from renewables, there is no exemption from the energy tax. However, thefinal use of renewable energy is not taxed. If renewables were taxed at the same rate per GJas natural gas (ATS 0.6 per m3 or ATS 1.8 per GJ), the 104.7 PJ final use of renewableenergy in 1998 (Statistik Österreich, 2000) would have been subject to a total tax amount ofATS 188.5 mln or EUR 13.7 mln.

Furthermore, firewood, straw and wood by-products are subject to a reduced VAT rate of10% (the standard rate is 20%) (EC, 2000b). Total final use of firewood amounted to 80.9 PJin 1998 (Statistik Österreich, 2000). Tentatively assuming a price of EUR 5 per GJ, andassuming that 50% of the firewood use can profit from the VAT reduction (the other halfremaining outside formal markets or being used by firms), the implicit subsidy can beroughly estimated at EUR 20 mln.

In 1995-1998, the Austrian government spent on average EUR 8.9 mln per year onrenewables related R&D (IEA, 1999f).

Electricity

Energy intensive industries do not have to pay the full amount of energy tax on electricity.The implicit annual subsidy was estimated above at EUR 80 mln.

There are some cross-subsidies for electricity at the provincial and municipal level. Forexample, special low prices are often charged to the public transport sector (IEA, 1998b).

In 1995-1998, the Austrian government spent on average EUR 3.4 mln per year on electricityrelated R&D (IEA, 1999f).

20

Table 2.2.1. Austria: Summary TableFinal energy consumption (1998): 22.8 MtoeGross electricity generation (1998): 57.5 TWh

coal oil & gas nuclear renewables electricityshare in gross electricity generation (1998) 7% 22% 0% 70%quantifiable subsidies (mln EUR per year) 10 80 2 > 100 > 80quantifiable subsidies, incl. attributedelectricity subsidies (mln EUR per year) > 15 > 95 2 > 150Source: Energy statistics: Eurostat (2000a); other figures: this section.

21

2.3 BELGIUM

Solid fuels

Solid fuels (coal, coke and lignite) are subject to a reduced VAT rate of 12%, whereas otherfuels are subject to the general rate of 21%. Assuming a price of EUR 300 per tonne, andassuming that half of the 307 kilotonnes of coal consumption in the services & householdssector in 1998 (Eurostat, 2000a) could benefit from the VAT reduction, the implicit subsidycan be estimated at some EUR 4 mln per year. In its recent plan on sustainable development(Federal Government of Belgium, 2000) the federal government has mentioned the abolitionof this tax reduction as a possible policy measure.

Coal is also exempted from the energy tax. While this does not constitute a subsidy forindustrial users (other industrial fuels remain untaxed as well), it creates a tax advantage forthe household use of coal. If we take the energy tax rate for natural gas (BEF 0.433 per m3) asa reference, the corresponding tax rate for coal should be about BEF 0.400 per kg (based onenergy content only). Again assuming that households account for some 150 ktonnes of coaluse, the implicit subsidy is BEF 60 mln or EUR 1.5 mln.

In 1995-1997, the Belgian government spent on average EUR 1.8 mln per year on coalrelated R&D (IEA, 1999f).

Oil and gas

In 1995-1997, the Belgian government spent on average less than EUR 1 mln per year on oiland gas related R&D (IEA, 1999f).

Belgium is a member of the 1992 International Oil Pollution Compensation Fund. Thisimplies a maximum compensation for oil spills of EUR 175 mln.

Nuclear energy

More than 50% of the Belgian electricity supply is provided by nuclear power plants. Nuclearpower is to be phased out by 2030. Funds for decommissioning the nuclear power plants arecollected through a levy on all electricity. The amount of implicit subsidy involved isunknown.

A fund has been set up by the government and the utilities to deal with radioactive wastefrom the defunct EUROCHEMIC installation (a reprocessing plant), the Waste Departmentof CEN/SCK (a nuclear research institution) and the dismantling of a reactor in Mol, becauseno financial provisions for managing these materials had been made (EC, 1999d). Thegovernment’s contribution to this fund is unknown.

In 1995-1998, the Belgian government spent on average EUR 38.9 mln per year on nuclearrelated R&D (IEA, 1999f).

22

Renewables

Since 1995, electricity generated from renewables is supported with a subsidy of BEF 1(EUR 0.025) per kWh. The measure was estimated to cost BEF 30 million (EUR 0.7 million)per year (IEA, 1998a). In July 1998 the amount of support was increased to BEF 2 (EUR0.05) per kWh for hydro and wind power installations with a maximum capacity of 10 MW(Federaal Planbureau, 1999). Therefore, the order of magnitude of the subsidy is now likelyto be some EUR 1 mln.

In all three administrative regions (Flanders, Wallonia and Brussels Capital) investments inrenewable energy are eligible to a subsidy of 15%. In the case of photovoltaic energy inFlanders there is an investment subsidy of 50%. Furthermore, 14% of investments inrenewable energy can be deducted from company profits (IEA, 1998a). Subsidies forrenewable energy are also available in the Walloon region, but information on budgets isgenerally lacking (Novem, 2001).

In 1995-1997, the Belgian government spent on average EUR 3.5 mln per year onrenewables related R&D (IEA, 1999f).

Electricity

Over the past decade, the ‘social electricity tariff’, intended to protect low-incomehouseholds, has involved an average amount of cross-subsidy of BEF 500 mln or EUR 12mln per year (IEA, 1997b). As this is a transfer between electricity users and does notdiscriminate between fuels, it is excluded from our quantification.

In 1995-1997, the Belgian government spent on average EUR 4.2 mln per year on electricityrelated R&D (IEA, 1999f).

Table 2.3.1. Belgium: Summary TableFinal energy consumption (1998): 37.4 MtoeGross electricity generation (1998): 83.2 TWh

coal oil & gas nuclear renewables electricityshare in gross electricity generation (1998) 17% 24% 55% 2%quantifiable subsidies (mln EUR per year) 7 < 1 > 40 5 4quantifiable subsidies, incl. attributedelectricity subsidies (mln EUR per year) 8 1 > 40 5Source: Energy statistics: Eurostat (2000a); other figures: this section.

23

2.4 DENMARK

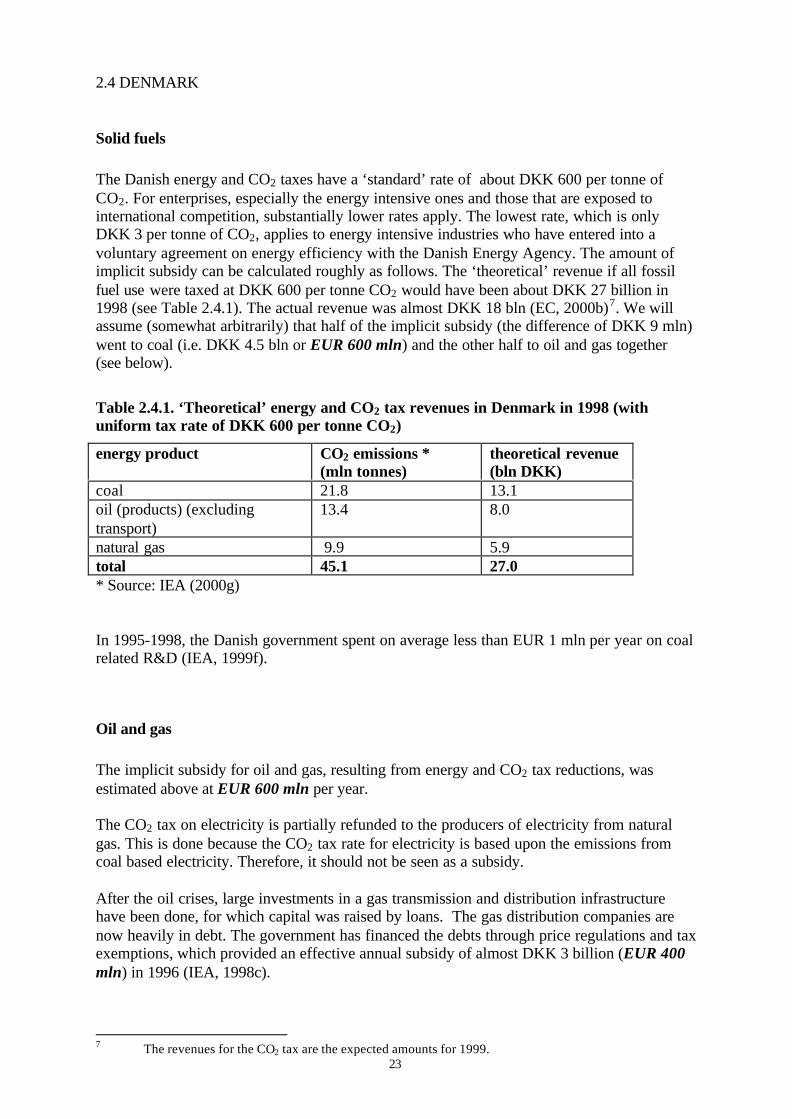

Solid fuels

The Danish energy and CO2 taxes have a ‘standard’ rate of about DKK 600 per tonne ofCO2. For enterprises, especially the energy intensive ones and those that are exposed tointernational competition, substantially lower rates apply. The lowest rate, which is onlyDKK 3 per tonne of CO2, applies to energy intensive industries who have entered into avoluntary agreement on energy efficiency with the Danish Energy Agency. The amount ofimplicit subsidy can be calculated roughly as follows. The ‘theoretical’ revenue if all fossilfuel use were taxed at DKK 600 per tonne CO2 would have been about DKK 27 billion in1998 (see Table 2.4.1). The actual revenue was almost DKK 18 bln (EC, 2000b)7. We willassume (somewhat arbitrarily) that half of the implicit subsidy (the difference of DKK 9 mln)went to coal (i.e. DKK 4.5 bln or EUR 600 mln) and the other half to oil and gas together(see below).

Table 2.4.1. ‘Theoretical’ energy and CO2 tax revenues in Denmark in 1998 (withuniform tax rate of DKK 600 per tonne CO2)

energy product CO2 emissions *(mln tonnes)

theoretical revenue(bln DKK)

coal 21.8 13.1oil (products) (excludingtransport)

13.4 8.0

natural gas 9.9 5.9total 45.1 27.0* Source: IEA (2000g)

In 1995-1998, the Danish government spent on average less than EUR 1 mln per year on coalrelated R&D (IEA, 1999f).

Oil and gas

The implicit subsidy for oil and gas, resulting from energy and CO2 tax reductions, wasestimated above at EUR 600 mln per year.

The CO2 tax on electricity is partially refunded to the producers of electricity from naturalgas. This is done because the CO2 tax rate for electricity is based upon the emissions fromcoal based electricity. Therefore, it should not be seen as a subsidy.

After the oil crises, large investments in a gas transmission and distribution infrastructurehave been done, for which capital was raised by loans. The gas distribution companies arenow heavily in debt. The government has financed the debts through price regulations and taxexemptions, which provided an effective annual subsidy of almost DKK 3 billion (EUR 400mln) in 1996 (IEA, 1998c).

7 The revenues for the CO2 tax are the expected amounts for 1999.

24

Royalty payments on oil and gas production have been abolished in the most recent licensingrounds (IEA, 1998c).

In 1995-1998, the Danish government spent on average EUR 2.8 mln per year on oil and gasrelated R&D (IEA, 1999f).

Denmark is a member of the 1992 International Oil Pollution Compensation Fund. Thisimplies a maximum compensation for oil spills of EUR 175 mln.

Nuclear energy

Denmark has no nuclear power plants.

In 1995-1998, the Danish government spent on average EUR 1.7 mln per year on nuclearrelated R&D (IEA, 1999f).

Renewables

Electricity from renewables is exempted from the energy and CO2 taxes on electricity. In thecase of the CO2 tax this exemption is achieved by granting a refund of DKK 0.1 per kWh tothe producers of electricity from renewables. This is equal to the CO2 tax rate for electricity,which is based upon coal based electricity. Therefore, it should not be seen as a subsidy. Theexemption from the energy tax, however, can be seen as a subsidy. The amount involved canbe estimated as follows. In 1998, the total revenues of the energy tax on electricity amountedto DKK 7.0 billion (EC, 2000b). Final consumption of electricity was 32.0 TWh (Eurostat,2000a), implying an effective tax rate of DKK 0.22 per kWh. Given a gross electricityproduction from renewables of 4.3 TWh (Eurostat, 2000a), the total amount of subsidyinvolved can be estimated at DKK 937 mln or EUR 126 mln.

By 2002, the direct financial support of electricity from renewables will be replaced by asystem of ‘green certificates’. This system has recently been approved by the EuropeanCommission.

In the period 1995-1999 the Danish Energy Agency paid an amount of DKK 329.7 mln (onaverage EUR 8.9 mln per year) in subsidies for investments in renewable energy installations(Energistyrelsen, 2000b).

A subsidy scheme for investments in solar cells was started in 1998. An amount of DKK 1billion was reserved for a period of five years (EUR 27 mln per year) (ENDS, 1998a).

Shareholders in private wind turbine cooperatives can opt for a model of income taxation inwhich the first DKK 3000 (EUR 400) of income from the sale of wind power is tax free(Energistyrelsen, 1999). As the extent to which this scheme is used is unknown, the amountof subsidy involved cannot be calculated.

In 1995-1998, the Danish government spent on average EUR 17.2 mln per year onrenewables related R&D (IEA, 1999f).

25

Electricity

In 1995-1998, the Danish government spent on average EUR 4 mln per year on renewablesrelated R&D (IEA, 1999f).

Table 2.4.2. Denmark: Summary TableFinal energy consumption (1998): 15.1 MtoeGross electricity generation (1998): 41.1 TWh

coal oil & gas nuclear renewables electricityshare in gross electricity generation (1998) 58% 32% 0% 10%quantifiable subsidies (mln EUR per year) 600 1,000 2 > 180 4quantifiable subsidies, incl. attributedelectricity subsidies (mln EUR per year) 600 1,000 2 > 180Source: Energy statistics: Eurostat (2000a); other figures: this section.

26

2.5 FINLAND

Solid fuels

Since 1996, investment aid for electricity and heat generation from peat has ceased, but it stillexists for cogeneration and district heating plants using mixtures of peat and wood as a fuel(IEA, 1999b) (see below under renewables). Furthermore, small scale peat power is includedin the refund scheme for the tax on electricity (see below under renewables). The implicitsubsidies cannot be calculated due to lack of data.

In 1995-1997, the Finnish government spent on average EUR 3.6 mln per year on coalrelated R&D (IEA, 1999f).

Oil and gas

In the past, the use of natural gas has been stimulated by subsidies and a reduced VAT rate.Following Finland’s accession to the EU, these arrangements have been terminated.Presently, natural gas benefits from a reduced CO2 tax rate: FIM 51 instead of FIM 102 pertonne of CO2. This tax reduction is not relevant for gas used for electricity generation,because since 1997 fuel inputs for electricity are exempt from the CO2 tax (instead, theelectricity itself is taxed). Gas use for other purposes than electricity production in Finlandamounted to 1.2 Mtoe in 1997 (calculated after EC, 1999a), or 900 mln m3. Given anemission of 1.96 kg CO2 per m3, the total CO2 emissions from this gas use are some 1.76 mlntonnes, which means that the tax reduction implies a subsidy of FIM 90 mln (EUR 15 mln)per year for natural gas.

In 1995-1997, the Finnish government spent on average less than EUR 1 mln per year on oiland gas related R&D (IEA, 1999f).

Finland is a member of the 1992 International Oil Pollution Compensation Fund. This impliesa maximum compensation for oil spills of EUR 175 mln.

Nuclear energy

Radioactive waste producers have full responsibility for managing their radioactive waste andfor covering all related expenses. In order to cover expected expenses for radioactive wastemanagement and decommissioning of the nuclear plants, the operators of the plants payannual fees to a government-controlled fund, which are tax-exempted (EC, 1999d).

In 1995-1997, the Finnish government spent on average EUR 8.4 mln per year on nuclearrelated R&D (IEA, 1999f).

27

Renewables

Since 1997, when the Finnish CO2 tax was transformed into a general tax on electricity, a taxrefund equal to the electricity tax is available for electricity from renewables (IEA, 1998a).The revenues from the electricity tax were estimated at FIM 2 billion in 1999 (EC, 2000b).As renewables account for about 30% of Finnish electricity production, the subsidy impliedcan be estimated at FIM 857 million or EUR 144 million per year.

Investment subsidies for new and renewable energy technologies are available to a maximumof 30% of the investment cost. In 1998, the amount of available subsidies was FIM 130million (EUR 22 million) (IEA, 1999b). It should be noted that these subsidies are partlyaccruing to non-renewable energy (e.g. subsidies to combined heat and power / districtheating plants using a mixture of wood and peat as a fuel).

Subsidies are also granted for the management of young forests and the harvesting of woodfor energy. These subsidies amount to between FIM 12 and 15 per MWh (IEA, 1999b).Given a biomass input for power generation of 1.32 Mtoe (15.35 TWh) in 1997 (EC, 1999a),and assuming that all of this biomass input benefited from the support scheme, the totalamount of subsidy can be estimated at FIM 184 mln (EUR 31 mln) per year.

In 1995-1998, the Finnish government spent on average EUR 4.5 mln per year on renewablesrelated R&D (IEA, 1999f).

Electricity

The tax on electricity is levied at a reduced rate for industry and greenhouse horticulture:FIM 0.025 instead of FIM 0.041 per kWh. Industrial electricity use amounted to 39.6 TWh in1997 (calculated after EC, 1999a), so the tax reduction implies a subsidy of FIM 633 mln(EUR 106 mln) to industry. The subsidy to greenhouse horticulture cannot be calculated dueto lack of data.

In 1995-1997, the Finnish government spent on average EUR 15.7 mln per year on electricityrelated R&D (IEA, 1999f).

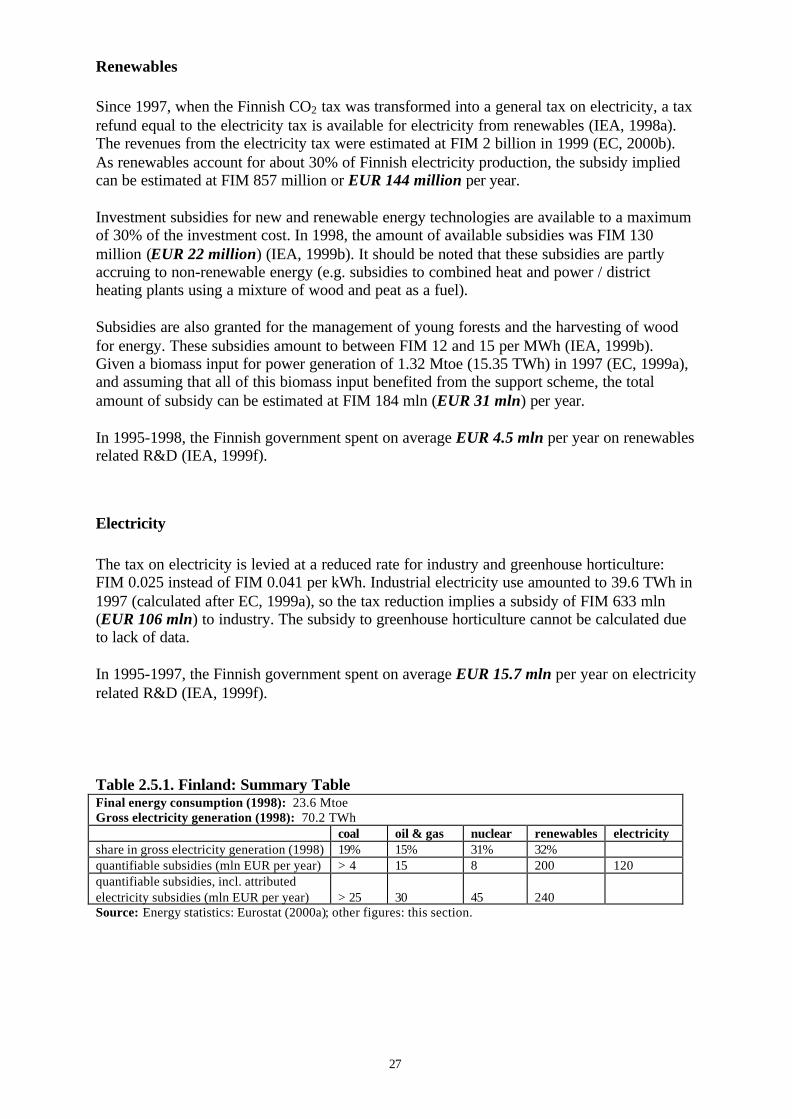

Table 2.5.1. Finland: Summary TableFinal energy consumption (1998): 23.6 MtoeGross electricity generation (1998): 70.2 TWh

coal oil & gas nuclear renewables electricityshare in gross electricity generation (1998) 19% 15% 31% 32%quantifiable subsidies (mln EUR per year) > 4 15 8 200 120quantifiable subsidies, incl. attributedelectricity subsidies (mln EUR per year) > 25 30 45 240Source: Energy statistics: Eurostat (2000a); other figures: this section.

28

2.6 FRANCE

Solid fuels

According to the European Commission (2000a), state aid to coal mining in France amountedto an average EUR 72 million per year in the period 1995-1996. IEA (2000d) estimated thePSE (Producer Subsidy Equivalent) at FRF 2,578 mln or EUR 393 million in 1998. Thisamount includes aid to current production only. Total subsidies for the French coal miningindustry (including social programmes related to mine closure) are much higher: Bonduelle etal. (1998) mention an annual amount of FRF 4.5 billion (EUR 686 million) and according toIEA (2000d) the total support (PSE + assistance not benefiting current production) amountedto FRF 6.6 billion (EUR 1 billion) in 1998.

Indirect types of support to coal include (Bonduelle et al., 1998):- compulsory purchases of coal-generated electricity (implicit subsidy estimated at FRF

600 mln or EUR 91 mln per year);- the rehabilitation of old mine areas;- uninternalised external costs (uncompensated environmental damage) from coal-fired

power plants.

In 1995-1998, the French government spent on average EUR 5.4 mln per year on coal relatedR&D (IEA, 1999f).

The use of coal is not taxed in France (apart from VAT). However, as there is not (yet) ageneral energy tax scheme, this cannot be regarded as a subsidy.

Indigenous coal production in France is to be progressively reduced and will ceasecompletely by 2005 (IEA, 2000d).

Oil and gas

The Institut Français du Pétrole (IFP) receives a certain percentage of the revenues of the taxon oil products and invests it in R&D. In 1996, the R&D funds financed in this wayamounted to FRF 871 mln for oil and FRF 235 mln for gas (Bonduelle et al., 1998); togetherFRF 1,106 mln (EUR 169 mln). As this is financed solely by a tax on oil products, it is not tobe considered a subsidy. The oil support fund FSH receives an annual budget in the order ofFRF 240 mln (EUR 37 mln) per year from the government (IEA, 2000d). The R&D budget ofGaz de France (GDF) amounted to FRF 634 mln (EUR 97 mln) in 1999 (IEA, 2000d). As inthe case of EDF (see below), this should not be regarded as a subsidy. According to IEA(1999f), the average government budget for oil and gas related R&D amounted to EUR 32.5mln per year on average in the period 1995-1998.

In response to protests against high prices of oil products, the French government decided inSeptember 2000 to reduce diesel excise tax rates in case of sharp price increases of crude oil.While this measure is not a subsidy, it has the effect of stabilising the price of diesel, thusmaking its use more attractive. Taxes on diesel have been traditionally low in France,compared to taxes on other motor fuels.

29

France has informed the European Commission that it intends to apply a reduced dieselexcise tax rate for short distance public passenger transport, starting in 2001.

Since the early 1990s, the government has maintained a support policy for small retailers ofautomotive fuels. The aim of this policy is to maintain petrol supply in remote areas. Thepolicy is financed by a tax that yielded a total revenue of FRF 53 mln in 1997. The tax wasraised in December 1999 to yield a total revenue of FRF 73 mln. The government intends tomaintain this higher level of support in 2001 (IEA, 2000d). As the tax is (presumably) leviedon oil products, the support can be considered to be a cross-subsidy.

Indirect subsidies to the oil industry include (Bonduelle et al., 1998):- uninternalised external costs of the use of oil products, in particular by motor vehicles;- military expenditures to protect the interests in oil producing areas, such as the Persian

Gulf.

France is a member of the 1992 International Oil Pollution Compensation Fund. This impliesa maximum compensation for oil spills of EUR 175 mln. The ‘Erika’ oil spill (December1999) has caused considerable damage on the French coast. Although Fina Elf, which hadhired the Erika, promised to pay at least USD 85 million compensation, it is likely that asubstantial amount of implicit subsidy by way of uncompensated damage will be involved.By December 2000, some 2,950 claims had been received by the 1992 IOPC Fund for clean-up operations, property damage and loss of earnings in the fishery and tourism sectors. Some1,770 claims had been assessed. Of these, 1,460 claims totalling FRF 113 million had beenapproved for FRF 84 million. Payments had been made totalling FRF 42 million, i.e. 50% ofthe amounts approved (IOPC Funds, 2001).

Nuclear energy

The main part of public spending on nuclear R&D in France takes place through theCommissariat à l’énergie atomique (CEA). Nuclear R&D expenses by CEA amounted toFRF 4,638 mln in 1996. Another large publicly financed nuclear research institute is thedepartment IN2P3 of the Centre national de recherche scientifique (CNRS), whose nuclearbudget amounted to FRF 1,234 mln in 1995 (Bonduelle et al., 1998). In our view, the R&Dbudget of electricity company EDF (FRF 594 mln in 1995, according to Bonduelle et al.,1998; FRF 3.1 billion in 1999, according to IEA, 2000d) should not be considered as asubsidy, but as ‘normal’ R&D expenses of an enterprise (although it is state-owned). Thesame is true for the FRF 1,251 mln spent on nuclear R&D by Cogéma (IEA, 2000d). Thetotal annual amount of nuclear R&D subsidy could thus be estimated at about FRF 7 bln orslightly above EUR 1 bln. According to IEA (1999f), the average annual government budgetfor nuclear R&D in the period 1995-1998 was EUR 515.8 mln, which can be used as aconservative estimate.

The annual budget of the Direction de la Sûreté des Installations Nucléaires (DSIN), which ischarged with safeguarding the security of nuclear installations, can be regarded as a subsidyto nuclear energy. This budget amounts to FRF 650 mln (EUR 99 mln) (Bonduelle et al.,1998). Government proposals seeking greater independence for the safety authorities haverecently been rejected by the National Assembly (IEA, 2000d).

According to EDF, the owner of all nuclear power plants in France, the cost ofdecommissioning the existing plants will amount to FRF 102 billion. This amount is basedupon an average decommissioning cost that is fixed by the Ministry of Industry, amounting toFRF 1,698 per kW installed by the end of 1998. The cumulated provisions amounted to FRF

30

44.5 billion in 1998. Given an average age of 13 years and a lifetime of 30 years, EDFconcludes that these provisions are sufficient to cover all decommissioning costs (EDF,1999). However, doubts have been expressed whether the budget for decommissioning (15%of the investment costs) will be sufficient (Bonduelle et al., 1998). Moreover, if the economiclife of the reactors is reduced (e.g. due to increasing maintenance costs) the necessaryprovisions for decommissioning will not be realised.

Other forms of indirect support to the nuclear industry include (Bonduelle et al., 1998):- nuclear overcapacity, leading to exports of electricity at prices below the level of full cost

coverage;- investments in new nuclear plants at times of overcapacity, the main purpose of the

investment being support to nuclear plant builder Framatome;- the mandatory reprocessing of spent nuclear fuel (intended to support reprocessing firm

Cogema);- limited liability for damage due to a nuclear accident (to FRF 600 mln or EUR 91 mln);- impacts of the nuclear cycle on health (estimated using the ‘ExternE’ methodology at

FRF 120 mln to 5940 mln, or EUR 18 mln to 905 mln per year).

Renewables

In 1996, the government initiated ‘EOLE’, a plan to promote grid-connected wind electricity.It is run in a similar fashion to the UK's NFFO, whereby the government (in co-operationwith EDF and ADEME) launches a competitive bid process for a certain amount of capacity.Successful bids are chosen on cost grounds: the average in 1997 was FRF 0.337 per kWh.EOLE aims to drive costs down to (a competitive) FRF 0.25 per kWh by 2005. A market forpower from the successful bids is guaranteed, and will be bought for the rate determined atthe time of bidding for 15 years (IEA, 1998a). So far, the amount of capacity that wasaccepted following the bidding rounds has exceeded expectations: a total of 124 MW wasaccepted (IEA, 2000d). Assuming a load factor of 0.2, the energy generated by the 124 MWwind turbine capacity could be 217 GWh per year. With a premium of FRF 0.087 per kWh,the implied subsidy amounts to FRF 18.9 mln or EUR 2.9 mln per year.

In 1998, a biogas programme was started, designed to equip waste dumps with combustionfacilities for the use of methane from waste fermentation. Like the ‘EOLE’ programme, it isbased on calls for tender. The first tendering round for 10 MW of electricity generatingcapacity was successfully concluded in May 1999 (IEA, 2000d). Given this relatively smallcapacity, the amount of subsidy involved probably does not (yet) exceed EUR 1 mln.

The ‘HELIOS 2006’ programme, established in May 1999 and carried out by ADEME,provides investment subsidies for households equipping themselves with solar water heaters(IEA, 2000d). Total funding is FRF 30 mln or (assuming the programme’s duration is 7years) less than EUR 1 mln per year.

Promotion of wood energy for heating is being strengthened via a ‘Wood Energy Plan’. Thetotal budget for the plan, which ran between 1995 and 1998, was FRF 215 mln, of which FRF74.5 mln came from the national government, and the remainder from regional, local or EUfunds (IEA, 1998a). On 1 January 1999, FRF 120 mln of subsidies had been spent (of whichFRF 47 mln were from ADEME). This programme was extended to comprise the ‘WoodWastes Plan’, announced in February 1998. Under this plan, viability studies relating to theuse of wood wastes as well as investment costs of installations using wood wastes aresubsidised. At present, ADEME spends FRF 65 mln (EUR 10 mln) per annum on theseprogrammes (IEA, 2000d).

31

Firewood is subject to a reduced VAT rate of 5.5%, whereas other energy products arecharged with 19.6% VAT (EC, 2000c). The use of wood for heating houses in France wasestimated at 7.1 Mtoe in 1996 (IEA, 1998a). It is not known to what extent this wood waspurchased in transactions involving VAT (a significant part of the firewood used in Franceremains outside formal markets). Tentatively, one could assume that 50% of the firewoodwas formally traded, at an average price of FRF 500 per toe (including 5.5% VAT), implyinga subsidy of FRF 237 mln or EUR 36 mln per year.

The Amortisation of Electrification Costs Fund (FACE) includes a source of finance forinvestments in renewables and demand-side management in rural areas. The annual budgetfor this part of FACE is FRF 100 mln (EUR 15 mln). The majority of funds are spent onphotovoltaic systems in rural areas, and aim to reduce either grid extensions or gridstrengthening, via reducing peak demand or increasing stand-alone generation capacity (IEA,1998a).

EDF is obliged to purchase renewables-based electricity from independent power producerson the basis of ‘avoided cost’. In March 2001, the European Court of Justice has ruled thatthis type of support does not constitute state aid under the EU Treaty (ENDS, 2001).

Biofuels benefit from excise tax exemption of up to FRF 2.3 per litre for RME and FRF 3.29per litre for ethanol (FRF 1.46 for ethanol-derived ETBE). The Government estimates thatthis subsidy will cost FRF 1.5 billion (EUR 230 mln) per year in lost tax receipts. Thisprogramme is followed for agricultural reasons, as it is not cost-effective in terms of CO2reduction alone (IEA, 1998a). In a recent judgement (case T-184/97), the European Court ofJustice ruled that the French tax exemptions for biofuels are incompatible with EC legislationon mineral oil excise taxation (ECJ, 2000).

Tax credits are available for investments in renewable energy technologies in overseasdepartments for small hydro, wind, biomass photovoltaic and solar thermal power schemes,whereby renewable energy investments by a company can be deducted against taxable profits(IEA, 1998a). Bonduelle et al. (1998) mention a general tax deduction for investments inrenewable energy equipment amounting to 25% of the total investment. The amount ofsubsidy (tax foregone) is unknown.

According to IEA (1998a), national government expenditure on renewables R&D accountedfor 1% of total energy R&D budget in 1996 (EUR 5.8 mln). This was the lowest reportedproportion of any OECD country's energy R&D budget that is spent on renewable energy.The majority is spent on biomass, photovoltaics and geothermal. On average, the governmentbudget for renewables related R&D amounted to EUR 4.5 mln per year in the period 1995-1998 (IEA, 1999f). ADEME is the main organisation involved, its R&D budget amounting tosome FRF 20 mln (EUR 3 mln) per year (Bonduelle et al., 1998). In 1999, ADEME’sspending on renewable R&D had increased to FRF 82 mln (EUR 12.5 mln) (IEA, 2000d).

Electricity

Reinforcement and extension of the electricity grid in rural areas is financed withcontributions from the FACE (see above). In recent years, these amounted to FRF 2.2 bln(EUR 335 mln) per year (Bonduelle et al., 1998). As FACE is financed by a levy onelectricity use, its expenses can only be regarded as cross-subsidies.

32

EDF runs a programme ‘Vivrélec’, aiming at promoting the use of electricity for domesticspace heating. It is estimated that in 1997 an amount of FRF 234 to 546 mln (EUR 36 to 83mln) was spent under this programme. However, as this money comes from EDF’s ownfunds, it should not be regarded as a subsidy in our definition.

Similarly, the money transfers resulting from the principle of ‘péréquation tarifaire’ shouldnot be regarded as subsidies. This principle implies that all consumers in France (includingthe overseas territories), regardless where they live, should face the same tariff structure andrates. It is obvious, however, that large amounts of ‘cross subsidy’ are involved. IEA (2000d)estimates that it constitutes a transfer of wealth from metropolitan France to other areas(including the overseas departments) in the order of FRF 2 billion (EUR 300 million) peryear.

Apart from nuclear R&D, no specific government subsidies for electricity related R&D isreported.

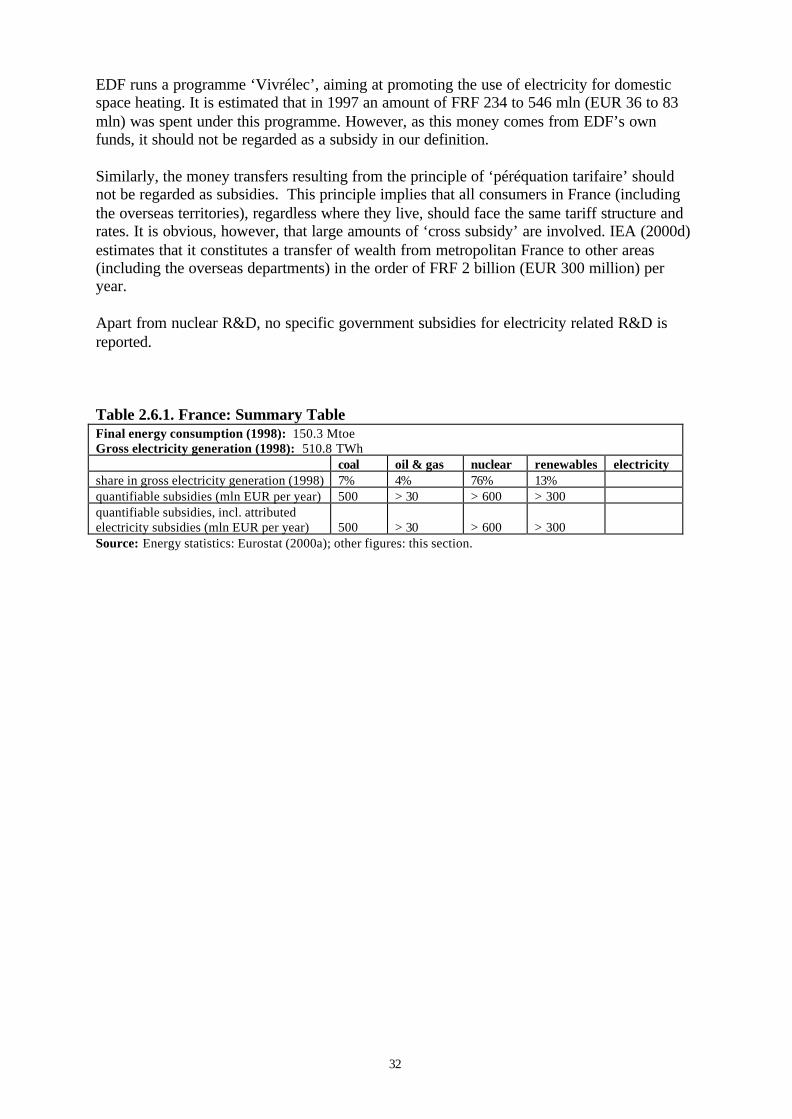

Table 2.6.1. France: Summary TableFinal energy consumption (1998): 150.3 MtoeGross electricity generation (1998): 510.8 TWh

coal oil & gas nuclear renewables electricityshare in gross electricity generation (1998) 7% 4% 76% 13%quantifiable subsidies (mln EUR per year) 500 > 30 > 600 > 300quantifiable subsidies, incl. attributedelectricity subsidies (mln EUR per year) 500 > 30 > 600 > 300Source: Energy statistics: Eurostat (2000a); other figures: this section.

33

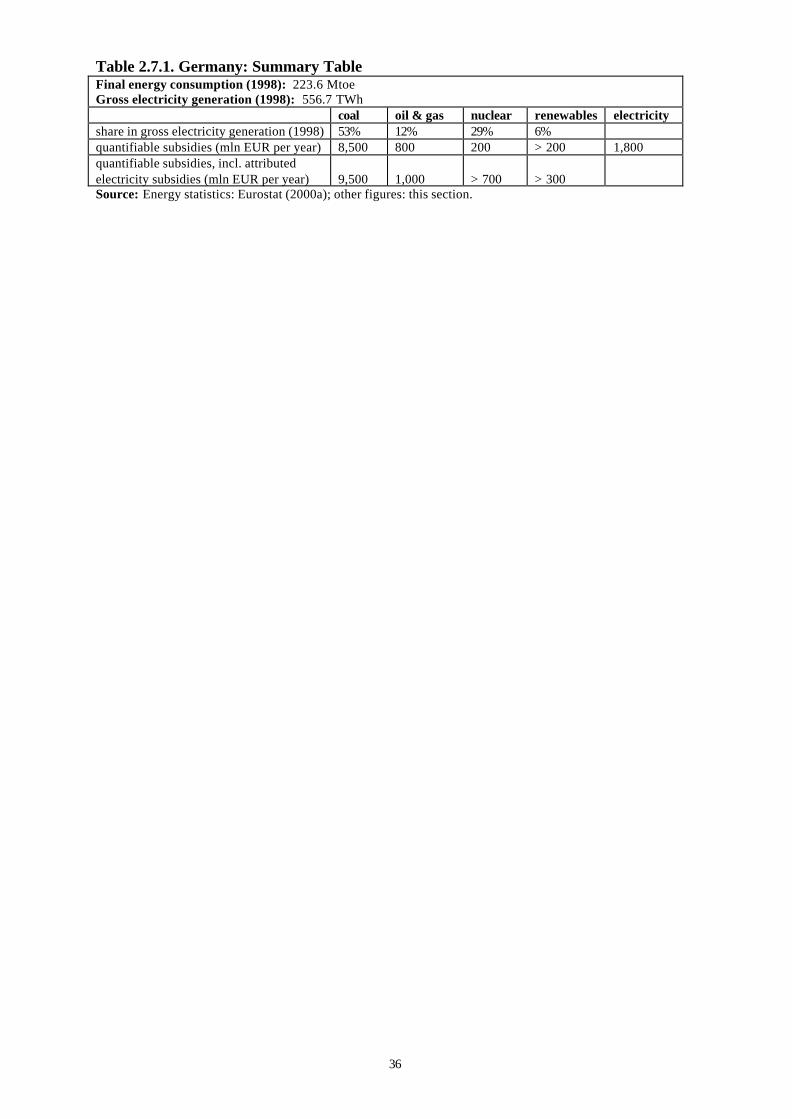

2.7 GERMANY

Solid fuels

According to the European Commission (2000a), state aid to coal production in Germanyamounted to an average EUR 4.8 billion per year in the period 1995-1998. This amountincludes aid to current production only. Since 1996, these subsidies are financed directlyfrom the federal budget. Before that time, they were financed by the ‘Kohlepfennig’, asurcharge on the electricity bills. The German Ministry of Finance foresees a decrease ofGerman coal subsidies from DEM 9.25 billion (EUR 4.8 billion) in 1998 to DEM 5.3 billion(EUR 2.7 billion) in 2005 (Bundesfinanzministerium, 2000a).

In the new Bundesländer, subsidies have been provided in the past by some Ländergovernments for lignite fired power plants. Until 2005, access to the grid in this part ofGermany can be denied if it endangers lignite based power generation (IEA, 1998d).

In contrast with other fossil fuels and electricity, coal remains untaxed under the ‘ecologicaltax reform’ which was introduced in 1999. If we take natural gas as a reference, which istaxed (in 2000) at 6.8 DEM per MWh, then, given a coal consumption of 86.7 Mtoe (= 1028TWh) in 1997 (EC, 1999a), tax revenues would have been almost DEM 7 billion (EUR 3.6billion).

In 1995-1998, the German government spent on average EUR 5.1 mln per year on coalrelated R&D (IEA, 1999f). These spendings have been decreasing substantially over the past15 years (in 1987, they amounted to more than EUR 150 mln).

Oil and gas

Gas and oil used in combined heat and power (CHP) installations with an operating time of70% or more, and power plants achieving an electrical efficiency of at least 57.5% areexempted from the mineral oil tax. Furthermore, the increases in the mineral oil tax that areintroduced under the ecological tax reform are reduced by 80 to 100% for industry andagriculture. The loss of tax income for the federal government in the year 2000 was estimatedat DEM 1 billion (EUR 511 million) (Subventionsbericht, 1999).

Individual enterprises can get a tax refund if the additional tax burden brought about by theecological tax reform (i.e. the introduction of the electricity tax and the increase in the taxrates for oil products and gas) exceeds the reduction in social security and pensioncontributions (which was included in the tax reform as a compensatory measure) by a factorof 1.2 or more. The amount of implicit subsidy involved is unknown, but it is probablyalready included in the above mentioned amount.

Natural gas or liquid petrol gas used as a propellant in public transport vehicles is taxed at areduced rate. The subsidy involved amounted to DEM 4 million in 1998 and was expected toincrease to DEM 30 million (EUR 15 mln) in 1999 (Subventionsbericht, 1999).

As in other countries, the own use of oil products by manufacturers of these products isexempted from the mineral oil tax. The implicit subsidy is estimated at DEM 310 mln (EUR159 mln) in 1999 (Subventionsbericht, 1999).

34

Since 1974, the federal government has built a crude oil reserve in salt caverns nearWilhelmshaven. This reserve (amounting to 7.3 Megatonnes) is financed and controlled bythe federal government (IEA, 1998d). The amount of public money involved is unknown.Tentatively, it could be estimated by assuming that the value of the reserve is at least EUR 1billion and that the annual costs in terms of storage and interest amount to 10% of this value,i.e. EUR 100 mln. In 1997, it was decided to sell the total amount of the reserve (IEA,1998d).

In 1995-1998, the German government spent less than EUR 1 mln per year on oil and gasrelated R&D (IEA, 1999f).

Germany is a member of the 1992 International Oil Pollution Compensation Fund. Thisimplies a maximum compensation for oil spills of EUR 175 mln.

Nuclear energy

Reserves set aside by the Association of German Utilities (VDEW) for future reactor closuresand nuclear waste disposal costs amounted to DEM 54 billion at the end of 1996. Thesereserves are tax exempt (IEA, 1998d). The amount of implicit subsidy is unknown. Thefederal government is considering setting up a tax on a portion of the reserves to financefuture end-storage facility operating costs (IEA, 1998d).

The federal government’s budget for R&D in the area of nuclear energy (fission and fusion)in the period 1996-2000 amounted to an average of DEM 390 mln (EUR 200 mln) per year(IEA, 1998d).

Renewables

Since 1991, electricity from renewables can be fed into the grid at a guaranteed price underthe ‘Stromeinspeisungsgesetz’. These prices are set at a percentage of final user prices,depending on the type of renewable: wind and solar electricity are paid 90% of the averageconsumer end price, small hydro facilities and biomass/waste are paid 80%, and large hydroschemes are paid 65% (IEA, 1998a). The cost of this scheme was estimated at DEM 780 mln(EUR 400 mln) in 1996 (EC, 2000b). The system is currently under revision. Future supportwill depend on the type of renewable and location. The total costs of the new system areestimated to be in the range of DEM 1.5 billion (EUR 770 million) in the first year,increasing to DEM 4 billion (EUR 2.05 billion) in 2005 (ENDS, 1999c). In March 2001, theEuropean Court of Justice has ruled that this type of support does not constitute state aidunder the EU Treaty (ENDS, 2001).