Energy Research Knowledge Centre Solar Photovoltaics · Energy Research Knowledge Centre Solar...

52

Energy Research Knowledge Centre Solar Photovoltaics An overview of European research and policy

Transcript of Energy Research Knowledge Centre Solar Photovoltaics · Energy Research Knowledge Centre Solar...

Energy Research Knowledge Centre

Solar PhotovoltaicsAn overview of European research and policy

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e

Contents At a glance 3

1. The current issues in brief 6 - PV installations and generation 6 - PV company revenues and PV investment trends 7 - Status of renewable deployment in Europe to mitigate greenhouse gas emissions and energy insecurity 10

2. Policy framework 11 - European policy framework 11 - European highlights by theme 14 - Overview of selected national policy frameworks 17

3. PV research roadmaps 22 - Theme 1: Improved performance, with reduced cost,

for PV systems 22 - Theme 2: Quality assurance, long term reliability and

sustainability 26 - Theme 3: Electricity system integration 27

4. Research programmes 28 - European research programmes 28 - Selected national research programmes 30 - Non-European research programmes 32

5. Research benefits and implications 35 - Technological development 35 - Societal aspects 39

6. Policy implications at EU level 40 - Regulatory support 40 - Financial support 41 - Stakeholder involvement 42 - Research, development and demonstration support 42

7. Recommendations on future research directions 43

References 44

List of Acronyms 49

This publication was produced by the Energy Research Knowledge Centre (ERKC), funded by the European Commission, to support its Strategic Energy Technologies Information System (SETIS). It represents the consortium’s views on the subject matter. These views have not been adopted or approved by the European Commission and should not be taken as a statement of the views of the European Commission.

The manuscript was produced by Carol Olson and Koen Schoots from the Energy Research Centre of the Netherlands (ECN) and Gabor Heves from the Regional Environmental Centre for Central and Eastern Europe, Hungary.

We thank the following peer reviewers who helped shape this brochure: Wim Sinke (Sci-ence & Technology Working Group member of the European Photovoltaic Technology Plat-form) and Pietro Caloprisco (Policy Working Group Coordinator of the European Photo-voltaic Industry Association).

While the information contained in this bro-chure is correct to the best of our knowledge, neither the consortium nor the European Com-mission can be held responsible for any inac-curacy, or accept responsibility for any use made thereof.

Additional information on energy research programmes and related projects, as well as on other technical and policy publications is available on the Energy Research Knowledge Centre (ERKC) portal at:

setis.ec.europa.eu/energy-research

Manuscript completed in September 2014© European UnionReproduction is authorised provided the source is acknowledged.Cover: © GOPAcomPhoto credits: Istockphoto, ECN, Shutterstock

Printed in Belgium

S o l a r P h o t o v o l t a i c s1

At a glance

Key messages• CoordinatedpublicandprivateresearchsupportforbasicPVresearchremainscrucial.

• EnablinggridintegrationoflargevolumesofPVpowerremainsoneofthekeyprioritiesofsolarPVresearch.

• PublicandprivateresearchsupportcouldboosttheintroductionofnewPVconceptsandmanufacturingprocesses.

Europe has been the leader in photovoltaic (PV) research and markets over the past decade, with the growth of the photovoltaic industry surpassing expectations. In Europe this industry includes all activities up to PV module production (i.e. the upstream indus-try) as well as the downstream industry involving PV installation and deployment. As of mid-2014 however, the global photo-voltaic industry is in transition, with Europe no longer holding the reins. European par-ties nonetheless remain active in the entire value chain and hold strong positions in many areas. For example, while production is shifting to Asia, Europe still holds a strong position in equipment manufacturing. Three snapshots are needed to put the current tra-jectory of the photovoltaic (PV) industry into perspective.

First, the amount of installed capacity and the contribution to electricity production of PV are growing. The global annual amount of new installed PV systems has grown from 31 GW in 2012 to 38 GW in 2013.

Second, despite the increasing number of GigaWatt, global investment in solar in 2013 fell 20 % compared to 2012. The main rea-son for this was the uncertainty felt by inves-tors caused by changes to policies support-ing renewable deployment. While a newly maturing industry would otherwise expect to undergo healthy consolidation, growth has coincided with a faltering global economy. Additional policy and trade uncertainties have been heavy blows to the PV industry. The global market has also experienced a shake-up through mergers of major com-panies or by minor companies going out of business. The third snapshot is the contribution of installed PV toward achieving policy goals to mitigate climate change and securing Europe’s energy supply. Today, the EU imports more than 80 % of the oil and more than 60 % of the gas it consumes. If current trends continue, import levels could reach more than 70 % of overall EU energy needs by 2030. By the end of 2013, PV contributed significantly

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e2

to the electricity generation system in a num-ber of European countries, and provided 2.2 % of electricity consumption in Europe.

Innovation is considered a key strategy to sur-viving the tough market challenges by raising efficiency, cutting costs and differentiating products. However, corporate funding for PV research is under pressure. The research and development (R&D)-to-sales intensity for EU-based PV companies in 2010 was about 2 %, a level that indicates under-investment in research. The Solar Energy Industrial Ini-tiative Implementation Plan (SEII IP) states that a first focus for PV technology develop-ment should be to ensure increased quality and performance at acceptable manufactur-ing costs for a range of PV technologies and applications. A second focus for research is associated with the issue of large penetra-tions of PV electricity into the grid. Third, also associated with PV deployment on a large scale, a research focus into issues of quality assurance, long-term reliability and sustain-ability (SEII IP) is needed.

There are several policies in place at Euro-pean and Member State level to support research and development in quality and long-term reliability, and integration of PV in the electricity system. The manufacturing

of PV in Europe is supported through policies supporting market uptake. To this end, many EU Member States implemented a subsidy scheme for photovoltaic deployment, such as feed-in tariffs, direct subsidies, green electric-ity schemes or tax credits. This policy brochure puts focus on these market uptake policies as they play a vital role for investments in man-ufacturing and R&D as well. In 2012, most of these PV support schemes were drastically reduced. Some changes to the policies even included retroactive penalties.

Research programmesIn the 2007-2013 EU programming period EUR 258 million was allocated to PV within the Seventh Framework Programme (FP7). Most research on photovoltaics was financed under the FP7 sub-programmes energy and nanosciences, nanotechnologies, materials & new production technologies (NMP). The Solar Europe Industry Initiative (SEII) represents the perspective of industry in European energy research policy. To reach the SEII objectives, the SEII Implementation Plan (SEII IP) esti-mates total funding of around EUR 9 billion is needed from EU, industry and Member States through their national research programmes in the overall period (2010-2020). The over-all targets of the European Energy Research Alliance – Joint Programme on Photovoltaic

Innovative solar energy panel on

roof in Hamburg, Germany.

© iStockphoto

S o l a r P h o t o v o l t a i c s3

Solar Energy (EERA – PV) coincide with those of the SEII and cover five sub-programmes in PV cell material research, module technology and education activities.

The link between national and European research programmes (most importantly the SET-Plan and the Solar Europe Industry Initia-tive) is represented by SOLAR-ERA.NET, which started its activities in early 2013 with Euro-pean Commission funding. SOLAR-ERA.NET is a network that brings together more than 20 research, technology and development (RTD) and innovation programmes in the field of solar electricity technologies in the European Research Area (ERA). The network of national and regional funding organisations has been established in order to increase transnational cooperation between RTD and innovation programmes and to contribute to achieving the objectives of the SEII through dedicated transnational activities.

At Member State level, Germany has by far the most extensive photovoltaic research pro-grammes, both on a federal and on a state level. A number of budget lines are allocated for PV research, adding up to a total for 2014 of EUR 114 million dedicated to PV only and EUR 431 million to PV and other energy tech-nologies. There are also extensive PV research programmes in France, Italy and Spain. Aus-tria, the Netherlands and Switzerland have prioritised PV in their national energy R&D programmes. Belgium, Estonia, Greece, Ire-land, Norway, Slovenia and the UK, national programmes put limited emphasis on PV.

Developments outside the EUUntil now China was primarily known for low-cost PV manufacturing and not particu-larly for innovation. However, the situation has rapidly changed, with corporate R&D at EUR 271 million and state R&D spend-ing at EUR 698 million in 2012. China is

currently the biggest investor in solar R&D. The USA launched its SunShot Initiative in 2011, which aims to achieve large-scale PV penetration by 2020. The total budget of the SunShot Initiative was EUR 343 million in 2012. Japan has established an impor-tant PV research programme, receiving an annual budget of EUR 73 million. Korea has a comparably high national PV R&D budget of EUR 67 million. A country with huge solar potential and some degree of a national PV research and development programme is Australia (EUR 22 million in 2011).

Research prioritiesThe most prominent roadmaps for the PV industry are the SEII PV Implementation Plan, the PV Strategic Research Agenda (SRA, 2011) of the European Photovoltaic Technol-ogy Platform and the International Technol-ogy Roadmap for Photovoltaic.

According to the SEII Implementation Plan, the challenge now for Europe is to face global competition by building on its strong starting position in terms of technology and markets and by focusing on aspects where Europe can make a clear difference. Increased invest-ment in innovation in all parts of the PV value chain are crucial for Europe to maintain and possibly increase its global role in manufac-turing and deployment of PV, both in terms of incorporating PV into Europe’s electricity mix as well as supplying competitive prod-ucts and solutions to markets worldwide. To these ends, the European PV industry has identified the following areas that need to be addressed:

• wafer silicon technologies• thin-film and emerging technologies• concentrator PV technologies• building-integrated photovoltaics• balance of system• cross-cutting and system perspective.

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e4

Other focal areas are research in electricity system integration, quality assurance, long-term reliability and sustainability.

Research benefits and implicationsPV research is increasingly widening its focus from a relatively narrow perspective on the cell device structure and materials in the early 2000s, to a wider view on cell, module, and balance of system components, system inte-gration, quality, reliability and sustainability. The PV value chain is much broader than only cell devices, modules, materials and equip-ment, as it also includes systems – where developments in the aforementioned areas are integrated – and the installation of PV systems. Although the production of cells and modules is now shifting to Asia, European R&D also contributes to other areas that are fully present in Europe. Also, European companies have a strong position in the construction of production facilities in Asia. As PV technology and industry matures, and as the societal and material pressures to transition to a renew-able energy system mount, European R&D is providing technical solutions to solve energy transition challenges in all parts of the PV value chain. This stimulates the creation of intellectual property and new businesses.

The number of jobs in the solar PV sector increased dramatically between 2001 and 2011; however recent industry consolidation has caused a deviation from this trend. The number of jobs in the European PV indus-try decreased from over 330 000 jobs in 2012 to 253 000 jobs in 2013. Education and training remains an important factor in maintaining Europe’s role as a knowledge-based and competitive global player.

Policy implications at EU levelRegulatory and administrative barriers should be resolved to enable further pen-etration of photovoltaics. Most importantly, there are still large administrative and reg-ulatory obstacles in connecting large vol-umes of PV power to the electric grid. This impacts the design and functioning of the electricity markets as well. Depending on national regulations, fulfilling construction standards may also represent a significant additional administrative barrier. By col-lecting and analysing the most significant barriers against investing into photovoltaic energy production, non-technical research can provide a lot of impetus to increasing the impact of European and national renew-able energy policies. R&D is necessary to bring PV electricity costs to such a level that it eventually becomes competitive at wholesale electric-ity market price levels without the support of subsidies. Therefore, while direct mar-ket subsidies will be mostly eliminated by the end of the current decade, PV systems research and power grid network develop-ment need steady and predictable financ-ing. Due to strong industry consolidation, industry R&D budgets have been con-strained. Public financial support for applied research is necessary to ensure that the momentum is not slowed at a time when energy transition must be addressed.

© Shutterstock

S o l a r P h o t o v o l t a i c s5

The European photovoltaic R&D commu-nity is well organised, with representatives contributing substantially to European photovoltaic R&D goal setting and policy-making. As PV research is a very applica-tion-oriented area, industry priorities are already reflected in European funding calls. Involvement of stakeholders such as tran-sition system operators (TSOs), delivery system operators (DSOs) and utilities may advance PV deployment and developments in grid integration. A stronger involvement of EU Member States in the European industry initiatives (EII’s) may bring signifi-cant added value, both from a financial as well as from a research coordination point of view. At present, Member State involve-ment is very difficult to assess, mainly due to the lack of a centralised monitoring sys-tem of national R&D activities. The ERKC could fill this gap.

Now that the basic technologies are in place, R&D policy focus will gradually shift towards issues related to market uptake. In this regard R&D support focusing on technologies for integration of PV in the energy system such as smart grids, storage technologies and consumer pricing has high policy rel-evance. The analysis in this Policy Brochure leads to the following recommendations for future research directions:

• grid integration of large volumes of PV power and cost reduction to remain key priorities of solar PV research;

• public support for basic PV research remains crucial as well as non-technical PV research to overcome grid integration and electricity market barriers;

• government support to boost the introduc-tion of new PV concepts such as organic PV and building-integrated PV in the market.

© iStockphoto

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e6

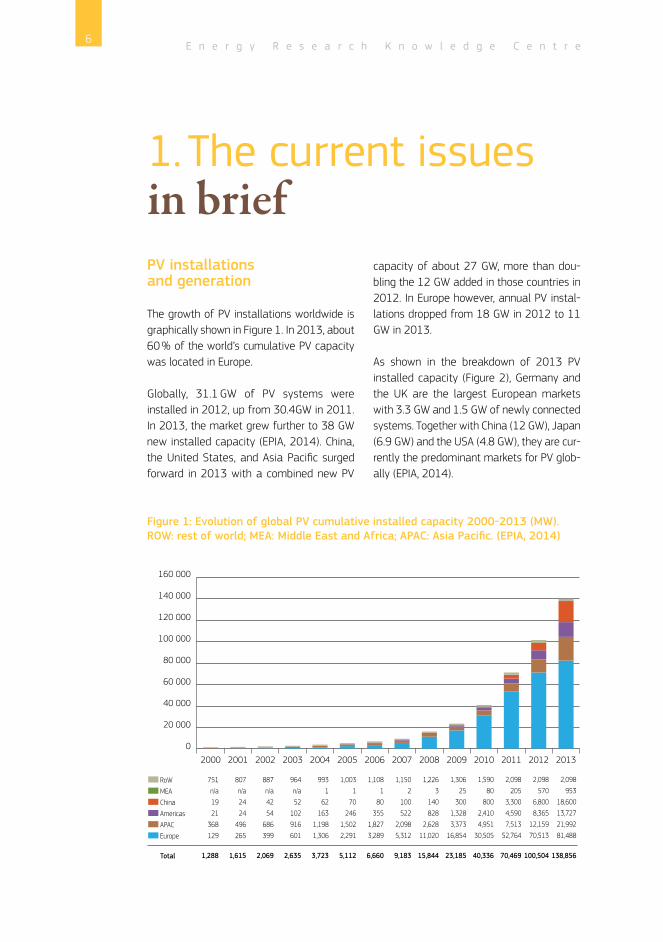

1. The current issues in briefPV installations and generation

The growth of PV installations worldwide is graphically shown in Figure 1. In 2013, about 60 % of the world’s cumulative PV capacity was located in Europe. Globally, 31.1 GW of PV systems were installed in 2012, up from 30.4GW in 2011. In 2013, the market grew further to 38 GW new installed capacity (EPIA, 2014). China, the United States, and Asia Pacific surged forward in 2013 with a combined new PV

capacity of about 27 GW, more than dou-bling the 12 GW added in those countries in 2012. In Europe however, annual PV instal-lations dropped from 18 GW in 2012 to 11 GW in 2013.

As shown in the breakdown of 2013 PV installed capacity (Figure 2), Germany and the UK are the largest European markets with 3.3 GW and 1.5 GW of newly connected systems. Together with China (12 GW), Japan (6.9 GW) and the USA (4.8 GW), they are cur-rently the predominant markets for PV glob-ally (EPIA, 2014).

Figure 1: Evolution of global PV cumulative installed capacity 2000-2013 (MW). ROW: rest of world; MEA: Middle East and Africa; APAC: Asia Pacific. (EPIA, 2014)

RoW

MEA

China

Americas

APAC

Europe

751

n/a

19

21

368

129

807

n/a

24

24

496

265

887

n/a

42

54

686

399

964

n/a

52

102

916

601

993

1

62

163

1,198

1,306

1,003

1

70

246

1,502

2,291

1,108

1

80

355

1,827

3,289

1,150

2

100

522

2,098

5,312

1,226

3

140

828

2,628

11,020

1,306

25

300

1,328

3,373

16,854

1,590

80

800

2,410

4,951

30,505

2,098

205

3,300

4,590

7,513

52,764

2,098

570

6,800

8,365

12,159

70,513

2,098

953

18,600

13,727

21,992

81,488

Total 1,288 1,615 2,069 2,635 3,723 5,112 6,660 9,183 15,844 23,185 40,336 70,469 100,504 138,856

160 000

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

S o l a r P h o t o v o l t a i c s7

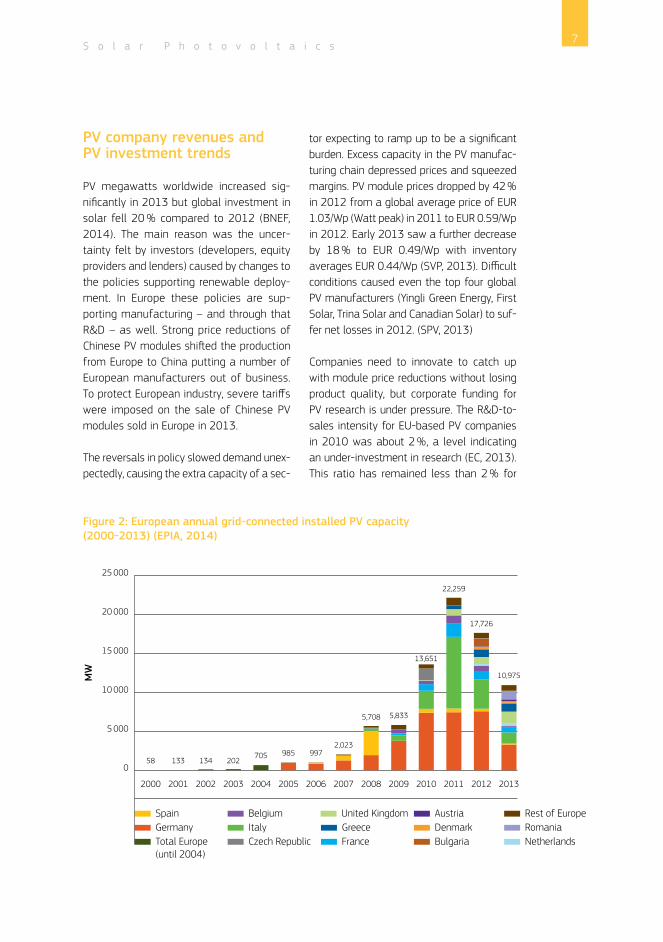

PV company revenues and PV investment trends

PV megawatts worldwide increased sig-nificantly in 2013 but global investment in solar fell 20 % compared to 2012 (BNEF, 2014). The main reason was the uncer-tainty felt by investors (developers, equity providers and lenders) caused by changes to the policies supporting renewable deploy-ment. In Europe these policies are sup-porting manufacturing – and through that R&D – as well. Strong price reductions of Chinese PV modules shifted the production from Europe to China putting a number of European manufacturers out of business. To protect European industry, severe tariffs were imposed on the sale of Chinese PV modules sold in Europe in 2013. The reversals in policy slowed demand unex-pectedly, causing the extra capacity of a sec-

tor expecting to ramp up to be a significant burden. Excess capacity in the PV manufac-turing chain depressed prices and squeezed margins. PV module prices dropped by 42 % in 2012 from a global average price of EUR 1.03/Wp (Watt peak) in 2011 to EUR 0.59/Wp in 2012. Early 2013 saw a further decrease by 18 % to EUR 0.49/Wp with inventory averages EUR 0.44/Wp (SVP, 2013). Difficult conditions caused even the top four global PV manufacturers (Yingli Green Energy, First Solar, Trina Solar and Canadian Solar) to suf-fer net losses in 2012. (SPV, 2013) Companies need to innovate to catch up with module price reductions without losing product quality, but corporate funding for PV research is under pressure. The R&D-to-sales intensity for EU-based PV companies in 2010 was about 2 %, a level indicating an under-investment in research (EC, 2013). This ratio has remained less than 2 % for

Figure 2: European annual grid-connected installed PV capacity (2000-2013) (EPIA, 2014)

Spain Belgium United Kingdom AustriaGermany Italy Greece DenmarkTotal Europe (until 2004)

Czech Republic France Bulgaria

Rest of EuropeRomaniaNetherlands

25 000

MW

20 000

15 000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

10 000

5 000

0705

13413358 202985 997

2,023

5,708 5,833

13,651

22,259

17,726

10,975

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e8

many of the top PV module manufacturers from 2007 through 2011 (Osborne, February 2013). In addition, after a slight decrease of 1 % between 2011 and 2012, the combined corporate and government R&D investment in solar PV contracted by 23 % in 2013 as compared to 2012 (BNEF, 2014). Due to a second year of financial losses for the indus-try worldwide, the top 12 PV module manu-facturers (of which two are European) were forced to reduce their R&D spending by 9 % in 2012 and another 9 % in 2013 (Osborne, June 2013; September 2014).

Innovation is considered to be a key strat-egy to survive the tough market challenges

in order to raise efficiency, cut costs and differentiate products. The first theme for photovoltaic research, as laid out in the SEII PV Implementation Plan (see Chapter 3), is PV technology developments to ensure increased quality and performance at com-petitive manufacturing costs, for a range of PV technologies and applications (SEII). This would allow a high penetration of unsubsi-dised PV electricity throughout the world.

In 2012, PV provided more newly installed electricity generation capacity in Europe than any other electricity generating technology (EPIA). It now contributes significantly to the electricity generation system in a number of European countries, and provides 2.2 % of European electricity demand (Eurostat, 2014).

With PV installations providing 5.6 % of elec-tricity demand in Germany in 2012 on aver-age, but occasionally peaking up to 45 %, its presence is being felt in energy markets (Figure 3). Consequently, challenges associ-

Innovation is a key strategy to surviving market challenges.

Figure 3: Annual average and maximum instantaneous PV contribution to electricity consumption in 2012 (%). (EPIA, 2013)

PV average contribution to electricity consumption in 2012 (le� axis)PV maximum instantaneous contribution to electricity consumption in 2012 (right axis)

50

40

45

30

35

20

15

5

25

10

0

BelgiumBulgaria

Czech RepublicFrance

GermanyGreece Italy

Spain

10

8

9

6

7

4

3

1

5

2

0

S o l a r P h o t o v o l t a i c s9

ated with grid and market integration of high penetrations of PV are coming to the fore. A second theme is research into large penetra-tions of PV electricity into the grid. A third theme, also associated with PV deployment on a large scale, is research into issues of quality assurance, long-term reliability and sustainability (SEII).

In 2013, total investments for renewable energy in Europe totalled EUR 38 billion, a 44 % drop over 2012 (BNEF, 2014). Growth in global R&D, across all industries, is expected to be driven by Asia, as the US and Europe’s allocations for R&D will not keep up with their projected inflation rates. According to Battelle, Europe’s gross expenditure on R&D (GERD) was EUR 261 million in 2012 as compared to EUR 263.2 million in 2013, a growth of 0.8 % which is significantly lower than the most recent inflation rate of 1.7 % for the EU. In contrast, China’s R&D growth of 11.6 % outpaces its expected inflation rate of 3.6 %. (Grueber, 2012; EC, 2013).

In China, the world’s biggest investor in solar R&D by far, corporate spending fell by more than EUR 38 million to EUR 271 million, while state spending increased almost EUR 53 mil-lion to EUR 698 million. (BNEF, 2013)

In March 2013, module prices rose for the first time since 2009. In 2013, the PV indus-try started to turn around from its downward trend as demand increased in the US and Asia. In 2014 the market continued to grow to 45.4 GW. For 2015, the global market is expected to grow at a slower pace (Osborne, 2014) to 53 GW with major markets located in Asia and the US (Osborne, October 2014; Parnell, 2013).

Europe has been in the driver’s seat for research and deployment of photovoltaic energy over the past decade, but now the situ-ation has begun to change. Deployment of PV is shifting to other areas in the global mar-ket. The issue at hand is how will this affect Europe’s role as leader in the PV industry?

© iStockphoto

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e10

Status of renewable deployment in Europe to mitigate greenhouse gas emissions and energy insecurity

In a 2012 EC staff working paper, the fragility of the European energy supply is described. Today, the EU imports more than 80 % of the oil and more than 60 % of the gas it consumes. If current trends continue, import levels could reach more than 70 % of the EU overall energy needs by 2030. Renewables increase Europe’s independence from fossil fuel imports, which at present come from relatively few countries, and are expected to become more expensive (EC SWD 149/2012).

Emissions of CO2 decreased by only 2.5 % in Europe in 2013, as compared with 2012, despite the installations of renewable energy sources (Eurostat, 2014). Worldwide invest-ment in fossil fuel electricity generation

capacity (EUR 203 billion) overshadows the (EUR 171 billion) global investment in all renewable energy capacity (BNEF, 2014).

Analysis by the IEA concludes that the green-house gas emissions of the global energy supply has remained unchanged for the past 20 years, reflecting the continued domination of fossil fuels in the energy mix and the slow uptake of other, low carbon technologies. The world is not on track to realise the interim 2020 targets in the IEA Energy Technol-ogy Perspectives 2012 2°C Scenario (IEA, TCE 2013). The European Commission also warns that, despite a strong initial start in EU renewables growth under the RES, the eco-nomic crisis is now affecting the renewable energy sector, particularly its cost of capital, as it has all other sectors of the economy. This, combined with ongoing administrative barriers, delayed investment in infrastructure and disruptive changes to support schemes, means further efforts are needed to achieve the 2020 targets (EC COM 175/2013).This Policy Brochure:

• broadly summarises the current status of the photovoltaic industry, research policy and research agenda (status as of Oct 2014);

• highlights the policy implications of the results of energy research programmes and projects;

• is primarily intended for policy and deci-sion-makers;

• focuses solely on photovoltaic (PV) solar technologies, i.e. flat-panel and concentra-tor PV, small rooftop-integrated and large power stations. It excludes those that gen-erate electricity indirectly, i.e. concentrat-ing solar (thermal) power; and

• looks at three main themes: competitive PV technology development; PV quality, reliability and sustainability; and PV grid integration.

© iStockphoto

S o l a r P h o t o v o l t a i c s11

2. Policy frameworkEuropean policy framework

The Directive on Electricity Production from Renewable Energy Sources (RES Directive) is a part of the EU climate and energy package and entered into force in 2009. It sets man-datory targets for the share of renewable energies in electricity production in each indi-vidual EU Member State, in order to achieve 20 % renewable energy contribution to the total energy consumption in the EU by 2020.

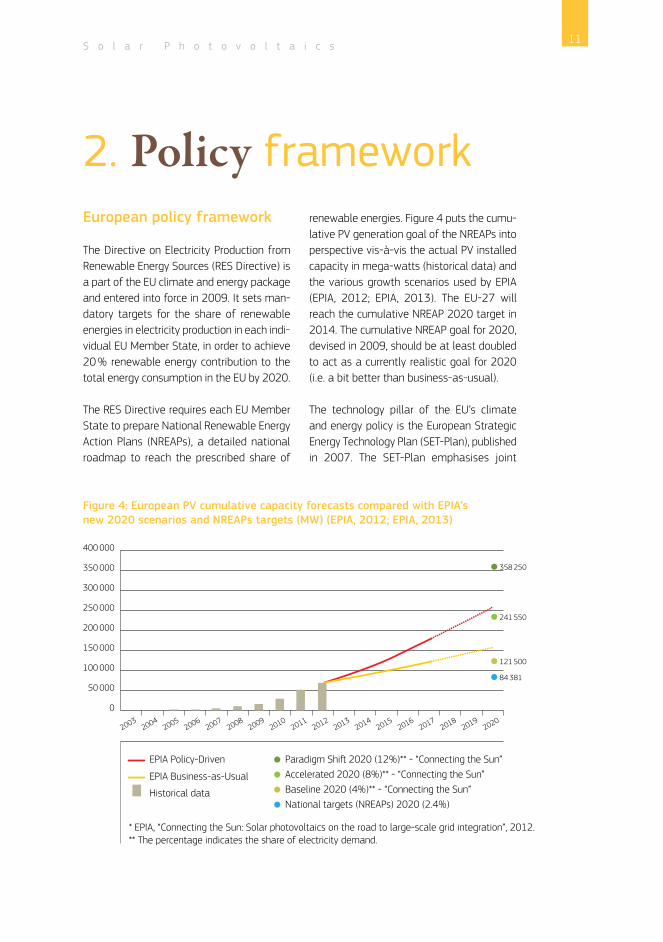

The RES Directive requires each EU Member State to prepare National Renewable Energy Action Plans (NREAPs), a detailed national roadmap to reach the prescribed share of

renewable energies. Figure 4 puts the cumu-lative PV generation goal of the NREAPs into perspective vis-à-vis the actual PV installed capacity in mega-watts (historical data) and the various growth scenarios used by EPIA (EPIA, 2012; EPIA, 2013). The EU-27 will reach the cumulative NREAP 2020 target in 2014. The cumulative NREAP goal for 2020, devised in 2009, should be at least doubled to act as a currently realistic goal for 2020 (i.e. a bit better than business-as-usual).

The technology pillar of the EU’s climate and energy policy is the European Strategic Energy Technology Plan (SET-Plan), published in 2007. The SET-Plan emphasises joint

Figure 4: European PV cumulative capacity forecasts compared with EPIA’s new 2020 scenarios and NREAPs targets (MW) (EPIA, 2012; EPIA, 2013)

EPIA Policy-Driven Paradigm Shi 2020 (12%)** - “Connecting the Sun”

EPIA Business-as-Usual

400 000

350 000

300 000

250 000

200 000

150 000

100 000

20032004

20052006

20072008

20092010

20112012

20132014

20152016

20172018

20192020

50 000

0

Accelerated 2020 (8%)** - “Connecting the Sun”Baseline 2020 (4%)** - “Connecting the Sun”National targets (NREAPs) 2020 (2.4%)

* EPIA, “Connecting the Sun: Solar photovoltaics on the road to large-scale grid integration”, 2012.** The percentage indicates the share of electricity demand.

Historical data

358 250

241 550

121 500

84 381

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e12

strategic planning in the area of technol-ogy development and commercialisation of renewable and low carbon technologies. It sets up a framework for cooperation between Member States as well as between industry, research centres and universities, with an aim to address Europe’s global competitiveness in the renewable energy sector. The SET-Plan outlines a public-private partnership (PPP) in which basic research is primarily covered by public (EU and national) funds, while applied research is backed mainly by the private sec-tor. The SET-Plan roadmap envisions up to 15 % of the European electricity to be gener-ated by PV, significantly more ambitious than the NREAP’s cumulative goal.

Implementation of the SET-Plan is also sup-ported by a series of industry-led European Technology Platforms. In terms of helping to shape research priorities the EU Photovoltaic Technology Platform and the European Pho-tovoltaic Industry Association (EPIA) are the two main stakeholder platforms that bring in and consolidate the main messages of the European photovoltaic community. The main research priorities for photovoltaic research and development are outlined in the strate-gic research agenda for photovoltaic solar

energy technology, the 2nd edition of which appeared in 2011. It aims to guide the prior-ity setting of European and national photo-voltaic research programmes.

One of the major components of the SET-Plan is the creation of European Industrial Ini-tiatives (EII). A broad partnership of European industry and the research community, the SEII aims to align the agendas and resources of the EU, Member States, industry and aca-demia in the field of industrial research and innovation with the aim of accelerating the development and deployment of solar tech-nologies (SEII PV IP, 2013). The SEII target for the PV contribution to European electricity in 2020 is 12 %, also an order of magnitude above the NREAP goal.

To reach NREAP goals and support the introduction of renewable energy sources, many EU Member States have implemented some kind of a subsidy scheme for photo-voltaic deployment, such as feed-in tariffs, direct subsidies, green electricity schemes or tax credits. In reaction to a reduction in PV costs and the close achievement of national renewable action plan targets, most of these PV support schemes were drasti-

© iStockphoto

S o l a r P h o t o v o l t a i c s13

cally reduced in 2012. Some changes to the policies even included retroactive penalties (EPIA, 2013).

In May 2013 the Energy Technology and Innovation Communication was published, announcing that the SET-Plan remains the core of the European Commission’s energy research strategy. It expressed the need to reinforce the SET-Plan to better align energy research and innovation capacity in Europe with the upcoming challenges of a develop-ing energy transition up to 2020 and beyond (EC ETI, 2013). To that end, an integrated roadmap was announced that consolidates the SET-Plan technology roadmaps and puts energy technology research in the perspec-tive of the development of the entire energy system. The integrated roadmap will retain the technology specificities and cover the entire development chain from research to demonstration to market development and roll-out. Development of the integrated road-map kicked off in September 2013.

The European Commission presented a framework on the 2030 targets to achieve EU’s climate and energy goals. The frame-work proposes a 40 % reduction of green-house gases compared to 1990 levels, increasing energy efficiency by 30 % and increasing the share of renewable energy to at least 27 % (EC COM (2014) 15). The urgency to reflect on the targets for 2030 are not only due to long investment cycles for energy generation facilities and supply but also because the pressure that the eco-nomic crisis is applying on Member States was not foreseen when the framework was developed in 2008/09. In March 2014 the European Council agreed to decide on a framework no later than October 2014.

Conscious that Europe’s R&D spending was lagging behind that of the US and Japan,

the European Commission communicated in 2010 that an Innovation Union had been agreed by Member States. For the first time, the EU proposed a comprehensive and concerted research strategy to take advan-tage of resources across Europe in order to achieve the goals set out in the Europe 2020 strategy. One of the seven flagship initiatives is devoted to a resource efficient Europe which includes the Energy Roadmap 2050. This sets out conditions that must be met to ensure competitiveness and energy security while meeting Europe’s goal of a decarbonised energy supply (EU Innovation Union). Horizon 2020, which runs from 2014 to 2020, is the financial instrument to imple-ment the innovation union. Its funding frame-work emphasises international research col-laborations.

The alignment of PV R&D infrastructure and programmes aims to accelerate innovation in this field. The EERA joint programme on photovoltaic solar energy aims to provide Europe-wide programming and aligning of R&D activities in Member States and focuses primarily on cost reduction of PV systems through enhancement of performance, development of low-cost, high throughput manufacturing processes and improvement of reliability and lifetime of PV systems and components. SOLAR-ERA.NET is a Euro-pean network of programme coordinators and managers from eight Member States. Its objective is to enhance the cooperation between regional and national R&D pro-grammes in the field of PV and concentrated solar power (CSP) and by that improve the effectiveness of programme management and R&D activities.

Relevant policy developments and objectives are outlined below according to the three thematic groupings identified by SEII in their PV Implementation Plan 2013-2015.

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e14

European highlights by theme

Theme 1: Improved performance, with reduced cost, for PV systems

Wafer silicon, thin-film and emerging and CPV technologiesSolar energy (including both PV and CSP) was one of the six priority areas identified by the SET-Plan in 2007. The European Photovol-taic Technology Platform set out a strategic research agenda in 2007 as a guide for FP7 in the area of photovoltaics. The agenda focused on the goals of improved efficiency with reduced cost for PV cells and modules and balance of systems. Concerning PV, it specifically addressed wafer silicon, thin-film and emerging as well as concentrator PV (CPV) technologies. Since 2007, this drive to improve the performance at reduced cost has been seen as the key to increasing the competitive-ness and deployment of PV to meet Europe’s decarbonisation and innovation goals.

Building-integrated photovoltaics (BIPV)The European Energy Performance of Build-ings Directive was passed in 2010 and will

require practically all new buildings to reach almost zero emissions by 2020. While this is to be achieved largely through energy savings, many new buildings will also generate their own heat and/or power. Rooftop and building-integrated photovoltaics (BIPV) will play an important role in this – especially when the on-going cost reduction is considered.

France has had the most ambitious poli-cies for BIPV, including Feed-in tariffs (FIT) and investment subsidies which date back to 2006, 59 % of all French PV systems are building-integrated. Investment subsidy and FIT policies in Italy have allowed 30 % of Italian PV systems to be building-integrated. Although PV only contributes less than 1 % to the Swiss electricity mix, 30 % of all installed PV systems in Switzerland are BIPV (Heinstein, 2013). Building regulations and standards must consider BIPV as full-fledged building components (e.g. facade elements, glass-shadings or roof-tiles), and hence dif-ferentiate them from traditional roof-top systems. From a regulatory point of view BIPV products must conform to both PV and building standards.

Finally, there is a role for ‘smart buildings’ that coordinate photovoltaic power systems with various other systems to optimise energy use. The EC’s Smart Cities Stakeholder Plat-form is one example of a European initiative that looks at this integration issue. Its Work-ing Group on Energy Efficiency and Buildings collects technological innovations in this field and helps to accelerate their uptake. Cross-cutting and system perspectiveStandardisation of PV system components enables more economic maintenance and enhances recycling. For modules and some components there are IEC (International Elec-trotechnical Commission) standards present.

© iStockphoto

S o l a r P h o t o v o l t a i c s15

However, these standards do not cover all PV components allowing manufacturers to use their own standards and measures for their PV products. Also for new concepts such as BIPV and inverter grid interfaces, standards are not yet present. The establishment of EU-wide standards has large implications, e.g. for earlier investments in production equip-ment and material supply contracts. The need and requirements for standardisation are currently still under debate by the solar PV industry. However, the 2013-2015 Imple-mentation Plan of the SEII expresses a need for such standardisation.

Theme 2: Quality assurance, long term reliability and sustainability

Although the lifetime of photovoltaic panels is usually guaranteed for 20 years (mean-ing the modules still produce 80 % of their

original power after 20 years of operation), large-scale uptake and the passage of time mean that Europe needs to prepare to properly handle dismantled photovol-taic systems (including inverters and other accessories). As the first step, in 2007 the photovoltaic industry established a volun-tary recycling scheme for photovoltaic mod-ules, called PV CYCLE. This is a non-profit association in charge of collection and recycling and it has the support of 90 % of producers in the market.

The European Waste Electrical and Electronic Equipment (WEEE) Directive was amended in January 2012 so that since the first quarter of 2014 recycling of photovoltaic panels is mandatory (EC WEEE, 2012). The Directive requires all PV manufacturers and importers to assure the take-back and recycling of PV modules and other PV system components, most importantly inverters and other electri-cal equipment.

© iStockphoto

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e16

Theme 3: Electricity system integration

Enabling large scale deploymentThe issue of grid integration is tackled in a number of European policy documents, of which only a selection can be mentioned here.

The 2008 EC Green Paper - Towards a secure, sustainable and competitive European energy network1 calls for significant invest-ments into trans-European energy networks (TEN-E) in order to increase the security of supply and interconnection of EU Member State energy networks. Once the basic infra-structure is in place, costs of grid connection for PV power can be reduced by developing standard systems on a continental scale. To foster the development of consistent rules for grid integration across Europe the Agency for the Cooperation of Energy Regu-lators2 (ACER) and the European Network of Transmission System Operators for Electric-ity3 (ENTSO-E) were created in 2009. These institutions developed a number of network

codes; for the PV sector, the most relevant are the network code requirements for grid connection applicable to all generators4.

Within the framework of the EC’s SET-Plan the European Electricity Grid Initiative (EEGI) is a European Industrial Initiative5 that deals with the issue of grid integration. This includes a nine-year European R&D programme to accelerate innovation in European electric-ity networks. The EEGI Implementation Plan explicitly lists the priorities for photovoltaic grid integration and the linkage with the Solar Europe Industry Initiative (SEII).

One of the goals of the Energy Roadmap 2050 is to address the necessity to develop flexible electricity infrastructure to integrate a higher penetration of renewables than envisioned in Europe 2020.

Solar resources and monitoringThe mapping and monitoring of renewable energy resources, as well as ways to accu-rately forecast these resources in the short term is appearing as part of the package on adapting the operation of the electricity sys-tem to function with a higher penetration of renewables.

The EU’s Joint Research Centre (JRC) offers the Photovoltaic Geographical Information System (PV-GIS), which is an online solar resource tool that maps potential PV system energy output. The JRC’s Renewable Energy Monitoring in Europe and Africa (REMEA) Action seeks to map raw renewable energy sources in Europe, Africa and Asia, and set up international collaborations for future data collection of this kind.

1 http://europa.eu/legislation_summaries/energy/internal_energy_market/en0004_en.htm2 http://www.acer.europa.eu/Pages/ACER.aspx3 https://www.entsoe.eu/4 https://www.entsoe.eu/resources/network-codes/requirements-for-generators/5 http://www.smartgrids.eu/node/20

© iStockphoto

S o l a r P h o t o v o l t a i c s17

Overview of selected national policy frameworks

GermanyGermany’s transition to an energy supply dominated by renewable energy technolo-gies, or “Energiewende”, is based on the gov-ernments ‘Energy Concept’, enacted on 28 September 2010, with the revisions for the early phase-out of nuclear energy following the accidents at Fukushima, Japan, beginning on 11 March 2011 (BMWi). Energy research for the Energiewende is carried out under the German government’s Sixth Energy Research Programme entitled “Research for an envi-ron-mentally sound, reliable and affordable energy supply.” The Federal Ministry for Eco-nomic Affairs and Energy (BMWi) is responsi-ble for application-oriented research, and the Federal Ministry of Education and Research (BMBF) coordinates the funding of basic research. 67 million and 63.6 million euros were allocated for photovoltaics research in 2012 and 2013, respectively.

Under the 6th Energy Research Programme, the Federal Government allocated approxi-mately EUR 3.5 billion for funding the research and development of energy tech-nologies between 2011 and 2014, a con-siderable portion of which comes from the Energy and Climate Fund.

The development of organic solar cells, also a theme 1 component, is a funding area of the BMBF. The BMBF is overseeing a 6th ERP activity on research for sustainable develop-ment, in which EUR 2 billion is slated to be invested by 2015. The energy topic, which encompasses both fundamental and applied research, is geared to support the German energy transition, and contains a funding priority called solar energy use. Funding pri-orities have also been identified for energy storage technologies and grid structures.

Solar energy use sets out three main activi-ties: organic electronics (which includes photovoltaics), the Photovoltaics Innovation Alliance, which is a joint activity with BMU, and the Leading Edge Cluster Competition – Solar Valley Central Germany, which encour-ages cooperation in research with industry and encompasses 98 coordinated projects that address basic issues across the whole value-added chain of crystalline and thin-film silicon solar modules (BMBF).

Energy storage, electricity grids (theme 3) and solar buildings – energy efficient cities (theme 1) are inter-ministerial topics over-seen by BMBF for basic research, and BMU and BMWi for applied research.

The federal government is continuing its policy of increasing efficiency and integrating renewable energy in buildings with the 2009 Energy Saving Ordinance (Energie-einspar-verordnung, EnEV) including the proposed revision in 2012, the Renewable Energies Heat Act (Erneuerbare-Energien-Wärme-Gesetz, EEWärmeG) and the implementa-tion of the European Energy Performance in Buildings Directive (EPBD). The aim is to have almost climate-neutral building stock in Ger-many by 2050. Climate-neutral means that the buildings require very little energy, and that any energy they require can be covered primarily by renewable energy. Funding for research into the integration of PV in build-ings is provided by the BMWi (theme 1).

ItalyThe National Research System was reformed in 1998 (Legislative Decree No 204/1998) to offer a programmatic, coherent and integrated orientation for research. The key mechanism is the National Research Programme (PNR), which is formulated by the Ministry of Education, Universities and Research (MIUR) after extensive consulta-

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e18

tion and approval by the Inter-ministerial Committee for Economic Planning (CIPE), a collective government body that coordinates decisions on economic policy.

The most recent PNR covers the period 2014-2020 and allocates a total yearly investment of 900 million euros to implement a broad research programme (ERAWATCH). Regions playing a strategic role are in charge of promoting applied research, innovation and technology transfer programmes and pro-jects. As well as having the power to allocate their own funds to research, they participate in the management of European structural funds via the regional innovation strategies and actively contribute to the more general objective of smart growth. The main pub-lic R&D institutions which carry out energy research in Italy are the National Agency for Energy, New Technologies and the Environ-ment (ENEA), the National Research Council (CNR) and Research on Energy Systems (RSE SpA). ENEA conducts PV research at centres in Portici, Casaccia and Manfredonia (ENEA). The Netherlands

In 2011, the Dutch government reformed the national research policy framework by intro-ducing the ‘Top Sector Policy’, which relies on

participation from the private sector. Energy is one of the nine top sectors defined. In each sector, top consortia for knowledge and inno-vation (TKIs), which include industry, research organisations and the government, cooper-ate to develop and implement a long-term strategy, the so-called Innovation Contract. TKI-Solar is one constituent of the Energy Top Sector.

The Innovation Contract for solar is the roadmap for fundamental and applied sci-ence and technology development. For the period 2012-2020, the contract identifies two programme lines: 1) PV technologies and 2) Building Integrated PV. A total of 19 projects started in 2012, committing EUR 41 million in project costs and a contribution of EUR 23.4 million in public funding (IEA-PVPS, NSR, the Netherlands, 2012).

SpainSpain’s National Strategy for Science and Technology (EESTI) is implemented through a series of national plans for research, development and technological innovation. The most recent National Plan (2013–2016) addresses the implementation of a sustain-able, efficient and clean national energy sys-tem, with renewable energies highlighted as one strategic area to contribute to this goal (ERKC, 2013).

The main player in Spain’s R&D and inno-vation policies is the new State Secretariat for Research, Development and Innovation (SEIDI), belonging to the Ministry of Economy and Competitiveness (MINECO) and the Min-istry of Industry, Energy and Tourism (MITYC).

The Centre for Energy, Environment and Tech-nological Research (CIEMAT), the National Renewable Energy Centre (CENER) and the Energy City Foundation (CIUDEN) are public R&D institutions which also receive private-

Solar panel field in

Tuscany, Italy.© iStockphoto

S o l a r P h o t o v o l t a i c s19

sector funding. Spain has a quasi-federal de-centralised political system, which is also reflected in its R&D and innovation-related policies. (Fernandez-Zubieta, 2012)

Spanish R&D expenditure has been decreas-ing sharply from 2011 to the present, to the extent that the 2013 budget is much lower than the one from 2002. Severe cuts have raised concerns from research organisations about the financial stability of the Spanish R&D and innovation system and fears that underinvestment in research could hamper Spain’s attempts to address the challenges of the current economic crisis. The new EESTI (2013-2020) has set a new lower target of 2 % gross expenditures in R&D (GERD) per GDP for 2020, a target that is below the European target of 3 % GERD per GDP for 2020 (Fernandez-Zubieta, 2012).

SwitzerlandAfter the Swiss resolution to phase out nuclear power (adopted in 2011) a new national energy strategy based on energy efficiency and renewable energy was formu-lated by the Federal Council, with innovative R&D as a main pillar of this strategy. The Energy Research Commission (CORE) devel-ops a federal energy research master plan every four years, comments on public energy research activities and provides appropriate information concerning developments in the area of energy research. Within the federal administration, energy research support is organised by the State Secretariat for Edu-cation, Research and Innovation (SERI), the Swiss Federal Office of Energy (SFOE) and the Commission for Technology and Innovation (CTI). The main public funding source is the ETH Board, the strategic management and supervisory body for Switzerland’s technical research institutions (ETH domain). Energy research in Switzerland is carried out mainly by the members of the ETH domain (ETHZ,

EPFL, PSI, Empa and Eawag). Beyond that, energy research is carried out by the regional state, or cantonal, universities and the uni-versities of applied science.

In 2013, a new Photovoltaic Systems Centre became operational in Neuchâtel as a new division of the Swiss Centre for Electronics and Microtechnology (CSEM). A joint effort by CSEM and the Federal Polytechnic School of Lausanne (EPFL), the initiative began in 2010. Dedicated to applied research and technol-ogy transfer in the domain of solar energy, it has received CHF 19 million of funding from the Swiss government for the period 2013-2016. The objectives of the new photovoltaic systems centre (PV-centre) will be to speed up the industrialisation process, develop new generations of photovoltaic cells and mod-ules and support the transition to a national energy system in which solar power will play an essential role. ChinaThe State Council, represented by the National Steering Group for Science, Tech-nology and Education, oversees the Chinese research system and directs the implement-ing and coordinating agencies, such as the Ministry of Science and Technology and the

Solar power generation plant in Extremedura, Spain.© iStockphoto

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e20

Chinese Academy of Sciences, and finally the R&D performers: universities, research insti-tutes and enterprises (ERKC).

Although its research infrastructure is still highly centralised, the trend since the 1980s towards a more market-oriented economy is visible in the funding and performance of research. The business sector funds 74 % of all R&D and performs 76 % of all R&D. Gov-ernment funding covers 22 % of R&D in China; half of which is provided by the central govern-ment. Public research institutes perform 15 % of all R&D, followed by universities at 8 %. Since 2005 China has become the second largest spender on R&D globally (Li, 2012).

The Chinese government’s 12th Science and Technology (S&T) Five Year Plan (2011-2015) indicates a continuation of the 20 % annual increase in government RD&D fund-ing, as in the last ten years, to reach a tar-get over 2.2 % of GDP by 2015, and 2.5 % of GDP by 2020. There are targets for the business sector as well: large- and medium-sized enterprises are expected to increase their R&D intensity to beyond 1.75 % by 2015. Moving towards a business enter-prise-centred national innovation system is prescribed as a long-term strategic goal in the Medium- and Long-term National Plan for Science and Technology Development (2006-2020). Implementation of this plan has led to a policy mix designed to promote business investment in R&D through national R&D programmes, tax credits, R&D subsidies and financial market regulations (Li, 2012).

JapanJapan’s level of R&D investment has been significant over recent decades. As a propor-tion of GDP, gross expenditure on R&D (GERD) was 3.57 % in 2010 (Woolgar, 2012). A high priority is placed on energy R&D, as Japan is highly reliant on fossil fuel imports. After the

Fukushima nuclear plant accident in March 2011, the Japanese government revised the 2010 Strategic (or Basic) Energy Plan, which highlighted, among other things, the need to create distributed energy systems.

The Research and Development Subcommit-tee of the Industrial Structure Council devel-ops Japan’s energy technology and advises the Ministry of Economy, Trade and Industry (METI) and the Ministry of Education, Cul-ture, Sports, Science and Technology (MEXT). METI allocates funding for renewable energy, energy efficiency, the rational use of fossil fuel and power generation (including nuclear power), and technologies relating to climate change. MEXT funds basic research carried out in universities and institutes. Other insti-tutes that play important roles in renewable energy research in Japan are the National Institute of Advanced Industrial Science and Technology (AIST), and the New Energy and Industrial Technology Development Organi-sation (NEDO).

In addition to the technological development of a range of PV technologies (including crys-talline silicon, thin-film silicon, thin-film CIGS, and organic thin-film solar cells), the devel-opment of grid control technologies such as forecasting, power conditioning and control technology and electrical storage technol-ogy are being pursued (theme 1 and theme 3). In 2012, NEDO started the review of the roadmap for PV technology development, ‘PV2030+’. In addition, AIST embarked on the establishment of a new research cen-tre in Koriyama City, Fukushima Prefecture to mainly support renewable energy-related industries following the Great East Japan Earthquake. With regards to PV technology, the development of production technology with a pilot line for high efficiency crystalline silicon solar cells/modules and research for demonstration of systems are planned.

S o l a r P h o t o v o l t a i c s21

KoreaAround 75 % of the country’s PV R&D budget is governed by MOTIE (Ministry of Trade, Industry and Energy), which focuses on indus-try-oriented research and developments. Approximately 18 % is governed by MSIP (Ministry of Science, ICT and Future Planning) for mostly fundamental research (Park, 2013).

The PV R&D budget governed by MOTIE is spent mainly by R&D projects planned through the Korea Institute of Energy Tech-nology Evaluation and Planning’s (KETEP) convergent core technology development programme, the Korea Institute for Advance-ment of Technology’s (KIAT) expanded econ-omy region leading industry development programme and the Korea Evaluation Insti-tute of Industrial Technology’s (KEIT) SME development and support programme. KETEP has played the leading role in national PV R&D programmes since 2008 (Park, 2013).

Efforts include the development of crystalline Si, thin-film and concentrated PV technolo-gies as well as building-integrated PV. Korea has followed a similar direction as Europe in terms of the energy performance of buildings. The Korea Energy Management Corporation (KEMCO) has stated that all new buildings, from 2025, should carry zero-energy building status. ‘Not only is a significant improvement in the energy efficiency of buildings neces-sary in order to meet these requirements in the short term, but in particular, a massive expansion of BIPV capacities must also take place to facilitate the proper integration of photovoltaics in buildings regarding technical and formal criteria’ (Schuetze, 2013).

KETEP also launched the green, energy-inde-pendent islands project in 2012, aimed at diffusing renewable energy while maximis-ing local adaptability. The convergence of PV with other renewable energy sources and diesel fuel aims to provide an energy-mixed electric power supply to grid-connected and stand-alone islands in the south-western islands region (Park, 2013).

The Institutes for Region Programme Evalu-ation were established in 2013, which will conduct the evaluation and planning of regional programmes including R&D pro-grammes funded by MOTIE through KIAT. Three Institutes – Chungcheong, Daegyeong and Honam – will plan and manage the regional PV R&D programmes covering the entire value chain of the PV industry with special emphasis on regional needs. Chun-gcheong Institute focuses on parts in particu-lar, Daegyeong Institute on equipment and Honam Institute on materials for the entire PV value chain (Park, 2013).

© iStockphoto

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e22

3. PV research roadmaps

The most prominent roadmaps for the PV industry are: the SEII PV Implementation Plan, the PV Strategic Research Agenda (SRA, 2011) of the European Photovoltaic Technology Platform, the SETIS Technology Roadmaps (SETIS), the Energy Technologies and Innovation Communication and Inte-grated Roadmap (EC COM 253/2013), and the International Technology Roadmap for Photovoltaic (ITRPV, 2013).

SEII’s most recent PV Implementation Plan (PV IP) outlines specific priorities that relate to photovoltaic R&D for 2013-2015, and is structured around three pillars: PV system performance enhancement with associated cost reduction; quality and lifetime enhance-ment; and implementation of large-scale integration and grid connection.

Fully cognisant of rapid price erosion and the industry shakeout, the 2013 SEII PV IP argues that current uncertainty about the future of the sector will pass because underlying technological development is sound. The challenge now for Europe is to meet fierce global competition by building on its strong starting position in terms of technology and markets and by focusing on aspects where Europe can make a clear difference. Innovations in all parts of the PV value chain are crucial for Europe to play an important role in the large-scale global manufacturing and deployment of PV, both

in terms of incorporating PV into Europe’s electricity mix as well as supplying com-petitive products and solutions to markets worldwide. Investment in research, devel-opment and demonstration now will aid Europe to position itself to benefit from the growth that will definitely continue once the crisis comes to an end (SEII PV IP, 2013 p.3). The first two themes address quality in two different ways. Quality is seen as a major driver for a competitive European industry (SEII PV IP, 2013 p.5). The third theme con-cerns large-scale PV grid integration.

Theme 1: Improved performance, with reduced cost, for PV systems

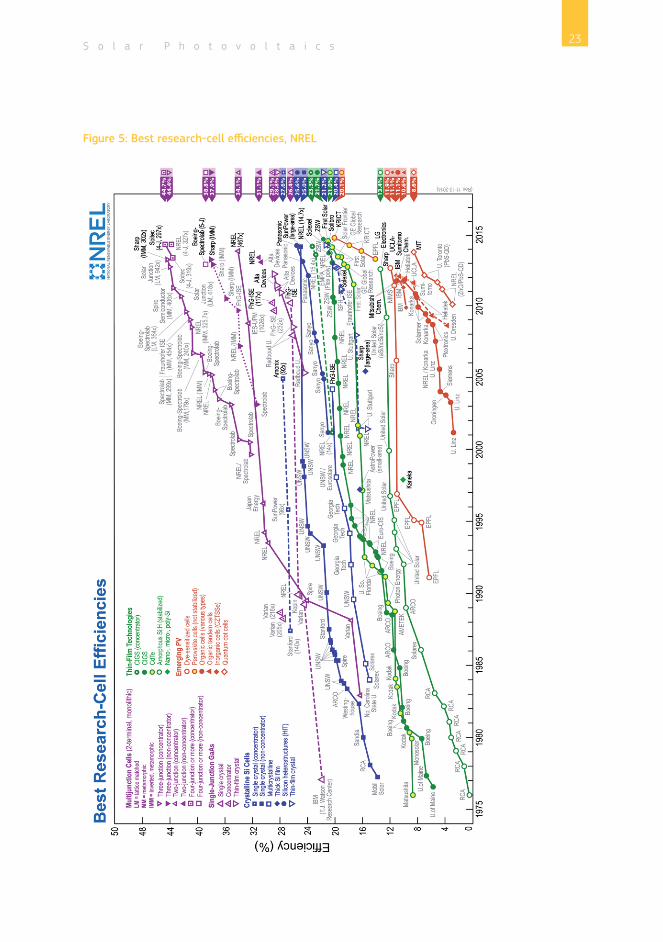

Performance and lifetime enhancement coupled with the reduction of manufacturing costs are the focus of the first theme. Current standard commercial crystalline silicon mod-ules have an efficiency of 15.5-17 %. Top-end commercially available monocrystalline modules by Panasonic and SunPower have significantly higher efficiencies of respec-tively 19 % and 22 %. Best lab cell efficien-cies as of August 2013 are shown in Figure 5.In order to address the fierce global com-petition and maintain a standing in the marketplace, the European PV industry has identified the following areas that need to be addressed to increa

S o l a r P h o t o v o l t a i c s23

Figure 5: Best research-cell efficiencies, NREL

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e24

Wafer silicon technologiesWith over 80 % of the market share, the wafer silicon technologies have a decidedly leading position among PV technologies. As shown in Figure 5, crystalline Si cells have achieved efficiencies of over 24 %. Top end commercially available monocrystalline Si modules are typically between 19-22 %.The twin goals of performance enhancement and energy cost reduction are envisioned to be achievable by continuing to develop high efficiency cells and modules in a way that sustainably reduces the manufacturing costs per watt. The optimisation of the production yield is a focal point, with an emphasis on introducing greater automation, standardisa-tion and in-process quality monitoring. A pri-ority is given to developing new low-energy silicon feedstock technologies and silicon growth techniques that are compatible with the re-use of expensive crucibles. Improving the amount of silicon lost in the wafering step, and developing device architectures that can deliver higher efficiencies with thin-ner wafers are also highlighted (SEII).

Thin-film and emerging/novel technologiesThin-film technologies encompass a wide range of material systems. Inorganic thin-film technologies (a-Si, CdTe and CIGS) are the most successful to date and provide advantages in flexibility, low weight, aes-thetics and low material consumption, to name only a few. However, higher efficiency for the photoactive layer(s) is a key issue for these materials to gain a higher market share. Module level efficiencies of 12-16 % are explicitly targeted.

Emerging technologies such as organic PV should be further supported and more atten-tion given to cell design and light manage-ment concepts that promise to overcome the Shockley-Queisser efficiency limit, such as quantum and nanoparticle technologies and direct bandgap materials with optical confinement.

The development of the materials (encapsu-lation, glass plus antireflective layers, trans-

Silicon wafers in laboratory.

© iStockphoto

S o l a r P h o t o v o l t a i c s25

parent conductive oxides, etc.) and manufac-turing processes for thin-film modules are highlighted as key areas. Costly production equipment used for low production volumes is not sustainable, and so an emphasis is set on developing low cost, large area deposi-tion equipment, with increased deployment of laser technology. Another critical issue for thin-film technology is the ageing behaviour and consequent estimate of lifetime (SEII).

Concentrator PV (CPV) technologiesConcentrator PV (CPV) technology includes both low concentration (normally below a concentration factor of 100x) and high con-centration (between 300x and 1000x). CPV technologies are considered to offer strong potential to increasing efficiency, with cost reduction implications. In the recent past, cell efficiencies have increased beyond expecta-tions, and R&D efforts to increase cell effi-ciencies are now targeted towards achieving 50 % by producing new cell architectures with new equipment. The current roadmap calls for more attention to development and optimisation of the concentrator system as a whole. High priority is given to develop-ing high throughput, high precision low-cost assembly technology for CPV modules. At a somewhat lower priority level, the goal of developing industrial low-cost automated manufacturing processes for high efficiency CPV cells and optics are also articulated (SEII).

Building-integrated photovoltaics (BIPV)The development of building-integrated PV is considered to be a promising application for almost all PV technologies. Facades of commercial and public buildings are consid-ered to be a promising and largely untapped market segment. The challenge is for BIPV to demonstrate the flexibility of the appli-cation (variation of dimensions, aesthetics, and compatibility with new and old build-

ings) and compliance with building sector standards and codes. The goals include the development of low-cost multifunctional BIPV products, with new installation meth-ods and concepts, and the optimisation of the performance of aesthetically designed cells for long-term higher energy output and with inherent security mechanisms to ensure their safety and reliability. Industrial auto-mated low-cost manufacturing processes are sought with the flexibility to produce a variety of BIPV products.

Balance of systemWith the decline of the module price, the cost of the balance of system components (i.e. the inverter, cabling, switches, support racks, batteries) takes on more importance in the overall system price. In addition, it is gener-ally desirable that electronic components have lifetime expectancies greater than 20 years. Lower cost manufacturing processes resulting in an increasingly reliable compo-nent with longer-term performance is a key goal. While inverter conversion efficiencies are already in the range of 90-95 % (which is close to the theoretical limit), further

© iStockphoto

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e26

research and development is still needed to increase the life expectancy of inverters to greater than 20 years. Furthermore, inverter research is aimed at supplying the function-alities in terms of control and communica-tion features that ease the large-scale grid integration of PV.

A systemic holistic approach is explicitly called for in the optimisation of all the sys-tem components together for different PV system sizes and applications to minimise cost. Improved lifetimes and low-cost power electronics are also sought, together with low-cost, high-accuracy tracking systems/platforms for different applications.

Cross-cutting and system perspectiveCross-cutting topics pertain to all technolo-gies. The topics on balance of system and in theme 2 on quality, reliability and sustain-ability are also cross-cutting issues but have been made separate categories because of their ‘gravity and importance’. The remaining cross-cutting issues, dealt with in this section, pertain to creased overall system performance and/or reduced losses, reduced system costs, and enhanced PV system bankability.

Theme 2: Quality assurance, long term reliability and sustainability

Quality, reliability and sustainability are issues that increase in importance as PV technologies claim an increasing share of electricity generation.

Quality assurance aims to ensure that all safety requirements and relevant perfor-mance standards are met by the evolving PV technologies. It includes such activities as sys-tematic monitoring, inspection and measure-ments embedded in each production process and associated equipment from raw materials to the end installation (field-tests), including transportation and final recycling. Long term reliability of PV systems refers to maintaining the high quality and performance of the PV system until the pre-defined end of life without retrofitting. The sustainability aspect includes the evaluation of the PV system to determine the environmental impact of the technology, in terms of energy use, life-cycle emissions, material depletion or scarcity issues and the development of recycling processes.

S o l a r P h o t o v o l t a i c s27

Theme 3: Electricity system integration

Enabling large scale deploymentBalancing services and/or back-up capac-ity is required for all electricity generators when the operation of the generator does not match the demand. The reasons can be various: maintenance, changes in demand that are too fast for the generator to respond to, outages etc. The current electricity sys-tem (i.e. infrastructure and market) evolved to accommodate the rhythm of the major-ity of generators (i.e. coal, gas and nuclear). Solar energy, like wind energy, is more vari-able, which has both predictable (day-night, seasonal) component and an unpredictable (clouds) component.

The ability of the current electricity system to be able to integrate renewables has typi-cally been underestimated. A few years ago, the idea that the Portuguese grid operator would report 70 % of electricity generated by renewables over a whole quarter, would have been considered fantasy. There are a range of technical and operational solutions for balancing renewables that are being iden-tified by some utilities with high penetrations of renewables. The SEII Plan sets research aims to enable high penetrations of PV whilst minimising the cost impact by:

• identifying, analysing and valorising fully the potential of PV technology;

• integrating storage solutions in PV sys-tems;

• creating a continuum among all the stake-holders (e.g. transmission system opera-tors, distribution system operators, PV developers, utilities etc.);

• increasing the overall flexibility of the power system;

• overcoming bottlenecks in the distribution grid; and

• ensuring a fair financing of all parties involved.

System integration is one of the two top pri-orities of the Solar Europe Industry Initiative, with the other being cost reduction. Examples of key research areas include the develop-ment of smart grids, improved power stor-age technologies, more durable inverters and developing consumer-oriented measures, such as flexible/demand-based electricity pricing. Solar resources and monitoringThe ability to plan and predict solar resources takes on greater importance as more PV electricity is integrated into the European electricity supply. The aim of this cluster of activities is to gather and disseminate accurate and reliable information on the solar resource to facilitate all aspects of PV integration. Historical data is publicly acces-sible to stakeholder groups in the EU Member States. Forecasting of the solar resource still needs further research.

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e28

4. Research programmesEuropean research programmes

Currently, the most significant European research programmes with PV relevance are:

• Seventh Framework Programme and Hori-zon 2020

• Intelligent Energy Europe Programme (IEE)• Solar Europe Industry Initiative• The Photovoltaic European Research Area

Network (SOLAR-ERA.NET)• European Energy Research Alliance – Pho-

tovoltaics (EERA – PV)• Knowledge and Innovation Communities

(KIC) of the European Institute of Innova-tion and Technology (EIT): KIC InnoEnergy and KIC Climate

• International Energy Agency Photovoltaic Power Systems Programme

• Energy Materials Industrial Research Ini-tiative

• Photonics 21 Initiative• NER-300.

In the 2007-2013 EU programming period the largest photovoltaic research budget of EUR 258 million was allocated within FP7 (Technopolis, 2014). Most research on photo-voltaics was financed under the FP7 sub-pro-grammes Energy and Nanosciences, nano-technologies, materials and new production technologies. Here the main research themes included cost optimisation (manufacturing process optimisation), PV cell material devel-opment, concentrator PV, multifunctional PV modules and building integration.

FP7 has been succeeded by Horizon 2020, which has EUR 5.9 billion allocated to non-nuclear energy research for the period 2014-2020. The energy challenge is comprised of seven research areas: 1) reducing energy consumption and carbon footprint; 2) low-cost, low-carbon electricity supply; 3) alter-native fuels and mobile energy sources; 4) a single, smart European electricity grid; 5) New knowledge and technologies; 6) robust decision making and public engagement; and 7) market uptake of energy and ICT innova-tion. The calls specific to PV are in the low-cost, low-carbon electricity supply area. The topics are defined by challenges, and in the 2014-2015 work programme, all renewable electricity technologies are included in the same call. There is an explicit focus on indus-try-, innovation-based and close-to-market projects. The new work programme is bian-nual (it was annual in FP7), running for the period 2014-2015.

While FP7 projects focus more on the core technical aspects, IEE-funded projects also look at socio-economic issues, such as human capacity building, legal aspects or financial support schemes. Some examples of IEE funded projects include PVs in Bloom (supporting public and private investment), PV legal (tackling administrative barriers), PV grid (promoting large-scale grid access) and PV parity (support schemes). A number of PV projects were funded within IEE’s priority area of Building skills and capacities, which focus on increasing human capacities. From 2014 onwards, the types of activities covered by

S o l a r P h o t o v o l t a i c s29

the IEE programme are now funded under the Horizon 2020 programme (IEE, 2014).

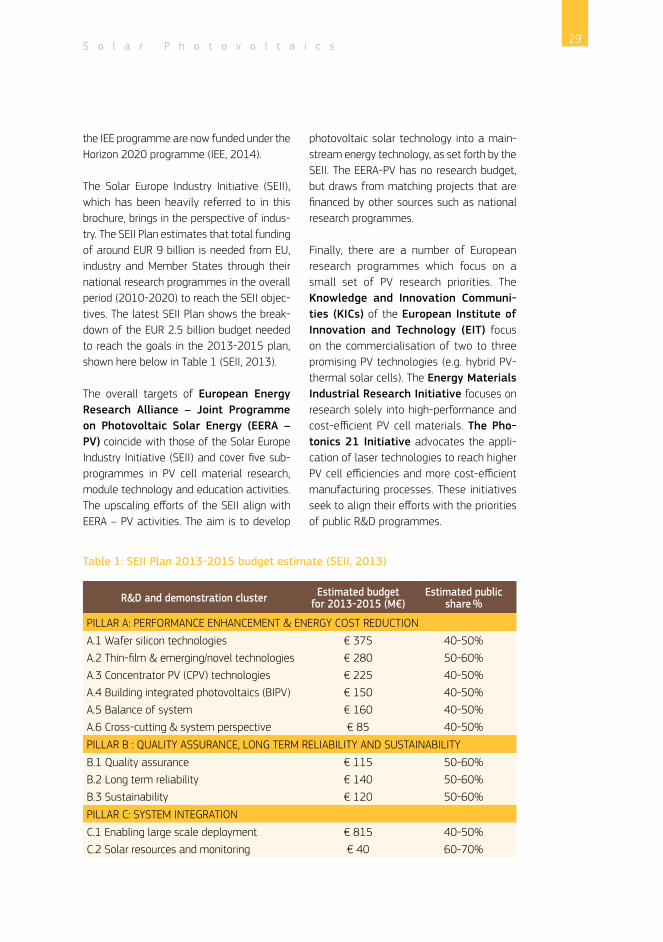

The Solar Europe Industry Initiative (SEII), which has been heavily referred to in this brochure, brings in the perspective of indus-try. The SEII Plan estimates that total funding of around EUR 9 billion is needed from EU, industry and Member States through their national research programmes in the overall period (2010-2020) to reach the SEII objec-tives. The latest SEII Plan shows the break-down of the EUR 2.5 billion budget needed to reach the goals in the 2013-2015 plan, shown here below in Table 1 (SEII, 2013).

The overall targets of European Energy Research Alliance – Joint Programme on Photovoltaic Solar Energy (EERA – PV) coincide with those of the Solar Europe Industry Initiative (SEII) and cover five sub-programmes in PV cell material research, module technology and education activities. The upscaling efforts of the SEII align with EERA – PV activities. The aim is to develop

photovoltaic solar technology into a main-stream energy technology, as set forth by the SEII. The EERA-PV has no research budget, but draws from matching projects that are financed by other sources such as national research programmes.

Finally, there are a number of European research programmes which focus on a small set of PV research priorities. The Knowledge and Innovation Communi-ties (KICs) of the European Institute of Innovation and Technology (EIT) focus on the commercialisation of two to three promising PV technologies (e.g. hybrid PV-thermal solar cells). The Energy Materials Industrial Research Initiative focuses on research solely into high-performance and cost-efficient PV cell materials. The Pho-tonics 21 Initiative advocates the appli-cation of laser technologies to reach higher PV cell efficiencies and more cost-efficient manufacturing processes. These initiatives seek to align their efforts with the priorities of public R&D programmes.

Table 1: SEII Plan 2013-2015 budget estimate (SEII, 2013)

R&D and demonstration cluster Estimated budget for 2013-2015 (M€)

Estimated public share %

PILLAR A: PERFORMANCE ENHANCEMENT & ENERGY COST REDUCTION

A.1 Wafer silicon technologies € 375 40-50%A.2 Thin-film & emerging/novel technologies € 280 50-60%A.3 Concentrator PV (CPV) technologies € 225 40-50%A.4 Building integrated photovoltaics (BIPV) € 150 40-50%A.5 Balance of system € 160 40-50%A.6 Cross-cutting & system perspective € 85 40-50%

PILLAR B : QUALITY ASSURANCE, LONG TERM RELIABILITY AND SUSTAINABILITY

B.1 Quality assurance € 115 50-60%B.2 Long term reliability € 140 50-60%B.3 Sustainability € 120 50-60%

PILLAR C: SYSTEM INTEGRATION

C.1 Enabling large scale deployment € 815 40-50%C.2 Solar resources and monitoring € 40 60-70%

E n e r g y R e s e a r c h K n o w l e d g e C e n t r e30

Selected national research programmes

The link between national and European research programmes (most importantly the SET-Plan and the Solar Europe Industry Initiative) is represented by SOLAR-ERA.NET, which started its activities in early 2013 with European Commission (ERA NET) funding. At present 17 countries and regions participate in SOLAR-ERA.NET with current calls addressing PV and CSP with a funding of EUR 12 million. SOLAR-ERA.NET is a network bringing together more than 20 RTD and innovation programmes in the field of solar electricity technologies in the European Research Area. The network of national and regional funding organisations has been established in order to increase transnational cooperation between RTD and innovation programmes and to contrib-ute to achieving the objectives of the Solar Europe Industry Initiative (SEII) through dedicated transnational activities (www.solar-era.net).