Energy - | Ministry of Finance · vi. Create a cutting ... energy mark rmed by the s. There a and...

14

Chapter 14 Energy Energy is the lifeline of an economy and is a vital input to sustain industrial, commercial and domestic activities. Energy disruptions and energy shortages not only result in loss of economic growth and employment but adversely affect social cohesion in the society. Energy crisis in Pakistan had been brewing since 2007 and deepened in 2012 which hugely negatively affected the economic growth and employment. Absence of effective planning, an economically and financially viable strategy and incapacitated regulator resulted in supply-demand gap. The situation has been further compounded due to high transmission and distribution losses, development of black-market for power and declining revenue collection. This led to persistent accumulation of circular debt. Consequently, the federal budget had to absorb huge quantum of subsidies to bridge the financial gaps in power sector threatening the fiscal stability on the one hand, and increasing the public debt. Nevertheless, realizing the gravity of situation and importance of energy for economic activities with particular emphasis on reviving the almost stalled industrial sector, job creation and income generation, the present government has put this issue on top of its economic reform agenda by pursuing a comprehensive plan to address these problems. In this context, government retired the circular debt (Rs 480 billion) immediately after taking oath which added 1752 MW of electricity into the system. In order to resolve the issue on permanent basis, government developed National Power Policy (2013) which was announced to provide an affordable energy in the country through efficient generation, transmission and distribution system. It is expected that the policy will set Pakistan on a trajectory of rapid economic growth and social development. More specifically, in order to reduce the cost of power generation to an affordable amount, a 84 MW New Bong Hydropower Project being the first hydro IPP in Pakistan/AJ & K has been commissioned while 10.5 MW Gas Based Davis Energen Project at Jhang started producing electricity and is contributing to FESCO's Network. Likewise 2 x 660 MW Imported Coal based Power Project at Port Qasim, Karachi has been inaugurated. In short, the government has realized the challenges faced by Pakistan energy system. Thus efforts are underway to reform existing energy system to actualize the energy sector’s aspirations. It is projected that by the end of the decade Pakistan will be transformed from an energy deficient to a regional exporter of power while the efficiency improvements in transmission and distribution will decrease the high cost of power to the end consumer which will bring prosperity and social development in the country. Box-1: Salient Features of National Power Policy 2013 The Ministry of Water and Power has developed Power Policy to support the current and future energy needs of the country and to set Pakistan on a trajectory of rapid economic growth and social development. It will also address the key challenges of the power sector in order to provide much needed relief to the citizens of Pakistan. To achieve the long-term vision of the power sector and overcome its challenges, following nine goals have been set: i. Build a power generation capacity that can meet Pakistan’s energy needs in a sustainable manner. ii. Create a culture of energy conservation and responsibility iii. Ensure the generation of inexpensive and affordable electricity for domestic, commercial, and industrial use by using indigenous resources such as coal (Thar coal) and hydel. iv. Minimize pilferage and adulteration in fuel supply v. Promote world class efficiency in power generation vi. Create a cutting edge transmission network vii. Minimize inefficiencies in the distribution system viii. Minimize financial losses across the system ix. Align the ministries involved in the energy sector and improve the governance of all related federal and provincial departments as well as regulators

-

Upload

phungthien -

Category

Documents

-

view

213 -

download

0

Transcript of Energy - | Ministry of Finance · vi. Create a cutting ... energy mark rmed by the s. There a and...

Chapter 14

Energy

Energy is the lifeline of an economy and is a vital input to sustain industrial, commercial and domestic activities. Energy disruptions and energy shortages not only result in loss of economic growth and employment but adversely affect social cohesion in the society. Energy crisis in Pakistan had been brewing since 2007 and deepened in 2012 which hugely negatively affected the economic growth and employment. Absence of effective planning, an economically and financially viable strategy and incapacitated regulator resulted in supply-demand gap. The situation has been further compounded due to high transmission and distribution losses, development of black-market for power and declining revenue collection. This led to persistent accumulation of circular debt. Consequently, the federal budget had to absorb huge quantum of subsidies to bridge the financial gaps in power sector threatening the fiscal stability on the one hand, and increasing the public debt.

Nevertheless, realizing the gravity of situation and importance of energy for economic activities with particular emphasis on reviving the almost stalled industrial sector, job creation and income generation, the present government has put this issue on top of its economic reform agenda by pursuing a comprehensive plan to address these problems. In this context, government retired the circular debt (Rs 480 billion) immediately after taking oath which

added 1752 MW of electricity into the system. In order to resolve the issue on permanent basis, government developed National Power Policy (2013) which was announced to provide an affordable energy in the country through efficient generation, transmission and distribution system. It is expected that the policy will set Pakistan on a trajectory of rapid economic growth and social development. More specifically, in order to reduce the cost of power generation to an affordable amount, a 84 MW New Bong Hydropower Project being the first hydro IPP in Pakistan/AJ & K has been commissioned while 10.5 MW Gas Based Davis Energen Project at Jhang started producing electricity and is contributing to FESCO's Network. Likewise 2 x 660 MW Imported Coal based Power Project at Port Qasim, Karachi has been inaugurated.

In short, the government has realized the challenges faced by Pakistan energy system. Thus efforts are underway to reform existing energy system to actualize the energy sector’s aspirations. It is projected that by the end of the decade Pakistan will be transformed from an energy deficient to a regional exporter of power while the efficiency improvements in transmission and distribution will decrease the high cost of power to the end consumer which will bring prosperity and social development in the country.

Box-1: Salient Features of National Power Policy 2013

The Ministry of Water and Power has developed Power Policy to support the current and future energy needs of the country and to set Pakistan on a trajectory of rapid economic growth and social development. It will also address the key challenges of the power sector in order to provide much needed relief to the citizens of Pakistan. To achieve the long-term vision of the power sector and overcome its challenges, following nine goals have been set:

i. Build a power generation capacity that can meet Pakistan’s energy needs in a sustainable manner. ii. Create a culture of energy conservation and responsibility

iii. Ensure the generation of inexpensive and affordable electricity for domestic, commercial, and industrial use by using indigenous resources such as coal (Thar coal) and hydel.

iv. Minimize pilferage and adulteration in fuel supply v. Promote world class efficiency in power generation

vi. Create a cutting edge transmission network vii. Minimize inefficiencies in the distribution system

viii. Minimize financial losses across the system ix. Align the ministries involved in the energy sector and improve the governance of all related federal and provincial

departments as well as regulators

218 P

The main tar

i. To fullyii. To diii. To div. To i

14.1 Pakist

Figure belooverall ene(Ministry oPetroleum component from policyimpacts the and laws foorganizationElectricity (NEPRA) a(OGRA).

Fig-14.1: P

The first stagovernmentcompanies primary enefrom import

The seconelectricity getc. Energyprivate comfrom publ

Pakistan Eco

rgets of this Poy eliminate loadecrease cost decrease transimprove colle

tan’s Energy

ow give us ergy sector of Water and

and Naturain the whole

y to generatienergy mark

rmed by the ns. There a

and Powand Oil and

Pakistan’s En

age is primart being primhas solid hoergy from dting these fro

nd stage isgeneration, ry in Pakistanmpanies but lic limited

onomic Surve

olicy for year ad shedding; of generation

smission losseection of bills t

y System

a visual prein Pakistan

d Power andal Resourcese system witon and distrket through rpublic secto

are two regwer Regulad Gas Regu

nergy System

ry energy sume supplier told. The govomestic resoom rest of th

s conversioefining and

n is generatemost of th

companie

ey 2013-14

2017 are:

from 12c/unies from 25 perto 95 percent.

esentation of. Public s

d the Ministrs) is the lath its intervenibution chainrules, regula

or institutionsgulators Natation Authulatory Auth

m

upplies wherto the genervernment su

ources as wehe world.

on process processing o

ed by publiche energy cos. During

it to 10c/unit; rcent to 16 per

f the ector ry of

argest ntion n. It

ations s and ional

hority hority

e the ation

upply ell as

like of oil c and omes

the

convvarioliqueusedenerpublGovsectoprivHubmajoand procyeardistrmanIn etowachanto bthe gearlythe 1994introthis Thissectoand nowpowprovinveavailackprovguarforecoorcriticom

Pressectoand (GEresoby IPow(WinGen

rcent

version procous plants efaction etcd by energyrgy system lic sector. Ho

vernment of or alone theate sector in

b Power Proor power pro

the world cess was verrs to fully ribution of naged by tweearly 90s thards market nge in the poring in moregovernment y 90s. The fiunbundling 4 and compoduced the Ppolicy was t

s policy resuor, promotioprivatization

w private sectwer productvinces have best in the eneilability of nk of technivincial govrantees to thign direct invrdination placal for th

mplicated sect

sently, the geor is done tMangla dam

ENCOs) genources. The pIPPs (Indepe

wer Plants) / nd Power

neration), H

cess, primary(heat, pow

.), oil refiney industry it

of Pakistanowever, it waPakistan to

erefore it wan. As a resuoject (HUBCoject which as well. H

ry slow andestablish inelectricity

elve Area Elehere was a s

economy wower sector oe private invintroduced n

first visible sof WAPDA

pleted in 19Power Policy to restructureulted in de-ron of IPPs, ren of selectedtor has also btion. Undebeen given coergy sector. Hnatural resoical knowlevernment the private vestment andan are reasohe provincetor.

eneration of through hydms etc. whilnerate electrprivate sectoendent PoweCPPs (CaptiGeneration)

Hub Powe

y energy is er, gas, peeries and soself. Prior tn mainly cas becominghandle and

as decided tult in 1985, aCO) was inwas unique

However, its d it took then 1997. Til

was coordectricity Boashift in glob

which led to of Pakistan. Tvestment. Folnumber of postep in this dA, the proces998. The of 1994. Th

e the entire pregulation oestructuring d corporate become a maer 18th Aonsiderable aHowever, duurces in theedge, inabilto provide sector for bd the absence

ons which ares to hand

electricity bdel sources lle generationricity throur electricity er Plants), Sive Power P, HPG (Hy

er Compan

supplied totrochemical,

ome of it isto 1985, theconsisted ofg difficult for

finance theto bring thea 1292 MW

nitiated as a in Pakistan

installatione project 12l 1994, thedinated andards (AEBs).bal thinkinga structural

The idea wasllowing this,olicies in the

direction wasss started ingovernment

he impetus ofpower sector.f the powerof WAPDAentities. Till

ajor player inAmendment,autonomy to

ue to unequale provinces,lity of the

sovereignbringing thee of nationalre becomingdle such a

by the publiclike Terbelan companiesugh thermalis generated

SPPs (Smalllants), WPGydel Power

ny Limited

o , s e f r e e

W a n n 2 e d . g l s , e s n t f . r

A l n , o l , e n e l g a

c a s l d l

G r d

(HUBCO) (KESC) wcompany. generated bElectric Poinstitution wof all geneinfluence w

In the third to energy sNational (NTDC) aninto power include LESFESCO, MHowever a transmissionpercent. Thpossible mminimum lepercent till 2

The interactservices occshould be nenergy prodgovernmentpart of the ftariff as mapay the priFrom FY03has been givwhich is mu

In 1995 themillion TOEthat time welectricity 1the energy million TOEgrowth rate

0

20

40

60

80

100

120

% Sha

re

Figu

Sou

and Karachwhile KESC

Some portby NPPs (Nuwer Companwhich manaeration comp

within the sys

stage, the geservices whiTransmissio

nd KESC. Tdistribution

SCO, QESCOMEPCO, HES

major portin and distrihe present

measures toevel and the 2017.

tion of supplcur through noted that thducts does nt heavily inffinal price byajority of coice if determ3 to FY13 a tven as subsiduch higher th

e total energEs. The main

were Oil 41.15.5 percent

supply of thEs with an ane of 4 per

1995

re 14.3: PrimaC

urce: Energy Year

hi Electric SC is verticion of eleclear Power ny (PEPCO

ages the genpanies and tem

enerated enerch are main

on DistribuThe NTDC i

companies O, PESCO, ISCO, KESCion of energibution whic

governmeno reduce ttarget is to re

liers and conenergy mar

he determinanot happen frfluence the my paying sub

onsumers wimined by fretotal amount dy to power han the cost

y supply of n sources of 6 percent, gand coal 5.8he economynnual averagrcent. There

2003

ary Energy SuCoal E

rs Book, various i

Supply Comcally integr

ectricity is Plants). Pak) is an umb

neration activthus has st

rgy is transmnly done thrution Coms further div(DISCOs) wIESCO, GEP

CO and SEPgy is lost duch is almos

nt is takingthese losseseduce these t

nsumer of enrket. Howevation of pricereely becausmarket and bbsidy on the ll not be ab

ee market foof Rs 1.7 trisector an amof Diamer B

Pakistan waf energy suppgas 36.8 per percent. In

y increased tge (1995 to 2e was not

2005

upply By sourcElectricity

issues, HDIP

mpany rated also

kistan brella vities trong

mitted ough

mpany vided which PCO, PCO. uring st 25 g all s to to 16

nergy er, it es of e the bears final

ble to orces. illion

mount Basha

Damshow

Howcausprestarifener

14.2

In 2thouprimtonn2 peproc

FiguPaki

as 28 ply at rcent, 2013 to 64 2013)

only

increchanseenwhil2013whicrelat

2233445

Rs B

illio

n

2010

Y

ceOil

m. The trend wn in Figure

wever, withdse huge sosent governmff and movinrgy supplies

2: Energy Su

2013, indigenusand tonnesmary energy nes of oil equercent of enecess.

ure14.3 showistan by sour

ease in enenge in the pn. The sharele the share 3 on accountch led the sutive cheaper

050

100150200250300350400450500

FY03

FY04

Figure 14.2

2011

Years

Gas

Source: Budget Wing

of subsidies14.2 below:

drawing theocio-economment is trying toward cespecially fo

upply

nous energy s of oil equivsupplies remuivalent (TOergy was los

ws the trendrces.

ergy supply patterns of ene of oil decof gas incret of rise in o

upplier to shir source. Ho

FY05

FY06

FY07

FY08

2: Subsidies t

2012

Energy S

g, Ministry of Finance

Energy

s given in th

e subsidy atmic cost thing to rationcheaper eneror electricity

availability valent (TOE)mained 64, 5OE) showingst during the

ds of energy

but also anergy sourccreased to 3eased to 48.2oil prices inteift toward gawever this s

FY08

FY09

FY10

FY11

to Power Sect

2013

Supply

y 219hese years is

t once mayherefore thenalizing thergy mix forgeneration.

was 65,639) while total88 thousand

g that almoste conversion

y supply of

a very cleares had been32.5 percent2 percent inernationally,as which is ashift exerted

FY12

FY 1

3

Years

tor

0

10

20

30

40

50

60

70

Million TO

E

9s

y e e r

9 l d t n

f

r n t n , a d

220 P

pressure onterms of eefficient sou

14.2.1 Oil

Overtime tsources of eis highest wrisks and beconomy. energy for increasing cThe price oincreased toan increase its price in prices domeMay 2014 fgenerating increased mproduced oproduced tprice of eleKWh. In oIPP involveThat is thecircular debmore than hoil reservesreserves wemillion barroil and 37recoverableon account crude oil reMarch FY correspondi11 percent growth of barrels in million barr

(MMCFD)

Pakistan Eco

n domestic reefficiency, ource of prima

there was energy supplywhich has exbrought negOil is mosPakistan, th

continuouslyof oil was $ o $ 110perbof almost hu1995. This

estically, escfrom Rs 9 pone unit

manifold i.en furnace oi

through diesectricity in Pother words, es a subsidy e root cause bt. Furthermhalf of the os. On June 3ere 1,102.6 rels(68 perce1.0 million

e reserves. Fuof import

emained 44.914 compare

ing period lawhile loca

12 percent July-March rels in corre

(-0.

3,400

3,500

3,600

3,700

3,800

3,900

4,000

Ju

Figure 14.

Source: Min

onomic Surve

esources of oil is still cary energy su

changing py, still relianxposed the gative repertly an imphe price of y especially i

10 per barrearrels in Maundred timealso led to a

calating to Rper liter in 1at IPP the

e., Rs.18/- pil and Rs.24sel, while tPakistan is a

every unit of Rs 9 to of the grow

more, Pakistaoriginal dom0, 2013, origmillion bar

ent) cumulatibarrel (32

urther a hugof crude oil9 million baed to 40.9 mast year posl crude extras it stood FY 14 co

sponding pe

9%) (0.4%)

ul Aug

.4: Gas Produ

nistry of Petroleu

ey 2013-14

gas, howeveconsidered aupplies.

attern in mnce on oil andcountry to m

rcussions onorted sourcwhich has

in last few yel in 1995 way 2014 shos as comparean increase i

Rs 107 per lit995. The co

ermal plant per KWh w

4/- per unit wthe average about Rs. 9/generated bRs 15 per Kwing probleman has exhau

mestic recoverginal recoverrrels with 7ive productiopercent) bal

ge amount is l. The impoarrel during million barreting a growtraction post

at 23.0 miompared to eriod last yea

(5.0%)

(-0.7%

Sep Oct

ction during J

um and Natural R

er, in as an

major d gas many n the ce of been

years. which wing ed to in oil ter in ost of

has when when

sale - per

by an KWh. m of usted rable rable

731.5 on of lance paid

ort of July-

els in th of ted a illion 20.5

ar. In

monimpobilligrow

RealhighPakiThuprovblocforeabouof tblocPunjAfteexplmomfinanrentawellbeensupphas sour

14.2

The natu2013cum(44 Wheof ntrillicubicomcurrbelo

%) (0.1%)

(

t Nov

July‐April

Resources

netary valueort of petroon in corres

wth 6.2 perce

lizing the rih use of petistan is tryis on Janu

visionally awcks to eight ign companiut 103,348 Sthe area alrecks, 21 blockjab, 8 in Kher execution loration activmentum andncial benefials. During tls have beenn made. Althply yet duesubstituted

rce of energy

2.2 Gas

original dural gas were3. 30.9 trilli

mulative prodpercent) w

en comparednatural gas oion cubic feeic feet of n

mparison of gent year and

ow:

(-0.8%)

(-4.1%

Dec Jan

s, US $ 4.3leum crude sponding perent.

isk and chaltroleum cruing to explouary 21, 2warded 50 companies iies. The totaSq. Kms whieady under ks are locatehyber Pakhtu

of agreemenvities in the d provincests in terms the current fin spudded ahough oil is to continuouoil in many

y supplies.

domestic ree 55.6 trillionion cubic feduction and was balanced with domeson June 30, et which rep

natural gas ras productiod last year i

%) (-4.2%)

Feb

2012‐13

3 billion wacompared t

riod last yea

llenges invoude, the Govore domestic2014 the

petroleum including boal area of theich is aroundexploration.

ed in Baluchunkhwa and nts for thesecountry wills will get of social w

iscal year, 73and 18 discoefficient primus rise in itsy ways bein

ecoverable n cubic feet et (56 perce24.7 trillion

e recoverablstic recovera

2012, thesepresent that reserve are

on during Julyis shown in

(-2.3%)

(0.5%

Mar April

3 2013‐14

as spent onto US $ 4.0ar posting a

olved due tovernment ofc resources.governmentexploration

oth local andese blocks isd 38 percent. Out of 50histan, 15 in

6 in Sindh.e blocks, thel pick a new

immediatewelfares and3 numbers ofoveries havemary energys prices, gasg a cheaper

reserves ofon June 30,

ent) was then cubic feetle reserves.

able reservese were 56.00.38 trilliondepleted. Ay – April forFigure 14.4

%)

4

n 0 a

o f . t n d s t 0 n . e

w e d f e y s r

f , e t . s 0 n A r 4

Energy 221

The worrisome factor is that our gas reserves are depleting and if gas consumption grows annually even at moderate rates, the present recoverable reserve will largely be exhausted by 2025. As this limit approaches the marginal cost of gas supplies will rise.

To avoid such a situation we have two choices: efficient use of gas and an increase in the gas exploration rate along with diversification of energy mix. Realizing this fact, the government is attracting foreign investment to explore new fields. Although exploring of natural gas is sub-component of mining and quarrying, yet on a positive note it should be noted that both private and public gross fixed capital formation in mining and quarrying at basic prices of 2005-06 had shown positive growth of 25 percent in FY 14 that earlier had declined to 14 percent in FY 13.

Increasing demand of natural gas with its limited supply has made room for Liquefied Petroleum Gas (LPG) which is also a primary source of energy. Currently about 1000 tons/day LPG is being produced domestically contributing less than 1 percent to the total energy supply mix. Because of its characteristics LPG is fast becoming a fuel of choice in the areas, where natural gas distribution network is not available. Pakistan Petroleum Limited (PPL) is the pioneer of the natural gas industry in the country which operates six producing fields in Sui, Kandhkot, Adhi, Mazarani, Chachar and Hala while Oil and Gas Regulatory Authority (OGRA) is empowered to regulate the LPG sector under OGRA Ordinance 2002 and LPG (Production & Distribution) Rules 2001 w.e.f 15th March, 2003. OGRA has simplified the procedure for grant of LPG license and the same is granted on fast track basis once the requirements are met / compiled. During July-Dec, 2013 two licenses for construction of LPG storage and filling plants were issued. In addition, OGRA has also issued 15 licenses for construction of LPG auto refueling station. OGRA is playing a vital role to increase private investment on midstream and downstream petroleum industry, During July- December, 2013 an investment of Rs. 0.264 billion has been made in LPG infrastructure whereas total investment in the sector till end of this fiscal year is estimated about Rs. 17.464 billion.

Natural gas and LPG are considered as cheaper than oil but both are expensive than coal and fortunately Pakistan has huge coal resources estimated to exceed 185 billion tons which generally ranks from lignite to sub-bituminous. However, less focus has been given to this cheaper primary energy supply.

14.2.3 Coal

The share of coal in energy supply is almost stagnant to 6 percent since 1995. The federal and provisional governments have started giving importance to coal exploration and development activities. The federal government has been striving hard for optimum development and utilization of indigenous coal resources and pursuing the policy of promoting coal based power generation. A summary of the efforts made in this regard is presented below:-

i. The federal government sponsored discovery and evaluation of Thar coal deposits, development of infrastructure in this coal-field and studies to determine its mine ability and for gasification incurring more than Rs 2.000 billion.

ii. Lakhra Coal Development Corporation has been set up as a joint venture of Pakistan Mineral Development Corporation, WAPDA and Government of Sindh to fulfill coal requirement of 150 MW Khanote Power Plant.

iii. The Finance Division has sponsored under PSDP a pilot project for Underground Coal Gasification at Thar Coal Block- V.

iv. Federal Government is pursuing the policy of promoting coal based power generation and conversion of oil and gas-based power plants to indigenous/imported coal that would later on, be replaced by Thar coal depending upon its availability.

Government of Sindh has leased out a coal block for an integrated mining project and power generation to increase the share of coal. The details are as under:-

a) Government of Sindh has entered into a joint venture with M/s Engro Powergen (Pvt) Limited for Coal Mining in Block-II and established a Company under Companies Act, 1984 viz. “Sindh Engro Coal Mining Company” for development of Coal Mine and installation 600-1000 MW Power Plant.

b) M/s Cougar Energy UK limited has been allocated Block-III in Thar coalfield for extraction Underground Coal Gasification and establishing 400 MW Power Plant.

c) M/s Bin Daen Group, UEA has been allocated Block-IV in Thar coalfield for developing Coal Mine and installing 1000 MW Power Plant.

222 P

d) One

CommMW Projeconnenotifichairmthe pr

e) M/s allocadevelPlant

f) M/s Expoconduintegrplant

g) GoveJ.V wallocadevelfired

It is expecfederal and

Private Pow‘One Windothe field oGovernmeninception addition of of twenty processing Gas and Hy(IPP) projec8,835 MWprojects, fifcapacity of the remainicapacity of

MW

F

Pakistan Eco

Block has mission of Pbased on Un

ect in Blockection, the ied Govermanship of Droject.

Oracle Coated Block loping Coal t of 300 MW

China Natioort Corporaucted feasibrated coal mat Sonda-Jer

ernment of with M/s Al-ated area loping Coal Power Plant

cted that wid provincial

wer and Infraow’ facilitatof power gent of Pakist

has succearound 8,65

nine (29) nineteen (1

ydel) based Icts with a cu. Out of thefteen (15) p6,948 MW ang four (4) p

f 1,887 MW

(6.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jul

Fig‐14.5: Com

Source: Ministry

onomic Surve

been allocaPakistan fornderground Ck-V Thar cGovernmen

rning BodDr. Samar M

alfield Plc, –VI in ThMine and

W extendable u

onal Machination of bility studymining and rrick in distr

Sindh enteriAbbas Grou

in Badin Mine and

t of 300-600

ith ongoing governmen

astructure Btor to the prieneration ontan (GOP). ssfully ma7 MW throu

IPPs. PPI9) multiple Independentumulative caese nineteen

projects haviare based onprojects havconsist of tw

%) (4.0%)

Aug

mparative Data

y of Water and Po

ey 2013-14

ated to Planr Plot ProjecCoal Gasificcoalfield. In nt of Sindh dy under Mubarakman

UK has har coalfieldinstalling Pup to 1000 M

nery Import China (C

y for 400 coal-fired p

rict, Thatta.

ing into anoup Company

coalfield installing CMW.

efforts of nts, the shar

Board (PPIB)ivate investon behalf ofPPIB, since

anaged capugh establishmIB is currfuel (Oil, C

t Power Prodapacity of arn in processing a cumuln hydro, wheving a cumulwo (2) gas b

(13.0%)(12.0

Sep Oct

a of Electricity

ower

nning ct 50 ation

this has the

d for

been d for ower

MW.

and CMC)

MW ower

other with

for Coal-

both re of

coalleadelect

14.2

Elecobtacoalwas as ipercPEPhydr750 for 3.3WAKESone almoineffplanelectyear

) is a ors in f the e its acity ment ently Coal, ducer ound

s IPP lative ereas, lative based

projbase

Govgeneenergovefor reguIt iswill variowhicnextbelo

%)

(-1.0%)

Nov

y Generation

l in primary d to cheapertricity genera

2.4 Electrici

ctricity is a ained by convl, nuclear pow

decline in st declined f

cent in 201PCO system iro 6,773 MWMW. Thus

29.7 percentpercent. O

APDA and exSC, 750 by

critical issost fifty pe

fficient recovnts and inapptricity generr and last yea

ects, one (1)ed project.

vernment of eration mix rgy resourceernment is cthese projec

ularly in ordes expected th

be added ious resourcech will redut four years.ow:

(8.0%)(4.0%

Dec Jan

July‐April

2012

energy suppr energy mation will red

ity

secondary everting primwer and otheshare of elecfrom 15.5 13. The insis 22,812 MWW, thermal 1 the hydropt, thermal 6f this 11,4

x-WAPDA GPAEC, and ue is that rcent of ins

very system, propriate fueration duringar is shown in

) oil based p

f Pakistan athrough dev

es particularlommitted tocts and moner to complehat 16, 564 in the nationes by comp

uce / elimina. The detail

%)(9.0%)

(

Feb M

2‐13 201

ply will incremix which w

duce the cost

energy sourmary sources

er natural soctricity in enpercent in

stalled capaW as of June15,289 MW power capaci7.0 percent 93 MW is

GENCOs, 2,2rest by IPPelectricity gstalled capalack of wear

el mix. A cog July – Aprin Figure 14.5

project and o

aims to achvelopment ofly hydel an

o arrange timnitor their d

ete them as pMW power

nal grid systpleting the nate load shed

of the proj

(7%)

(11%)

Mar Apr

13‐14

ease and willwhen use int.

ce which islike gas, oil,urces. There

nergy supply1995to 12.9

acity in thee 2013; withand nuclear

ity accountsand nuclearowned by

216 MW bys. However,generated isacity due tor and tear of

omparison ofil for current5below:

one (1) coal

hieve powerf indigenousd coal. The

mely financesdevelopmentper schedule.r generationtem through

new projectsdding duringect is given

l n

s , e y 9 e h r s r y y , s o f f t

l

r s e s t .

n h s g n

Table 14.1: NYear

2014

2015

2016

2017

2018

Upto 2018 TSource: Paki After geneCompanies supplying ebills. So an

Another wrecommendefficient DIin order to distribution structure noincentive ainefficient Dgovernment

F

G

M

Q

H

T

P

S

Fig

S

New Projects

Guddu-NandipuGuddu-Quaid-eQuaid-eGuddu Quaid-eNeelumGolen GPatrind TerbelaCoal PlaCoal PlaThar CoCoal PlaGaddan

Total Generatstan Electric P

eration of e(DISCOS)

electricity tonother critica

worrisome ds a tariff ISCOs and preduce their losses. Hotified by thas a result tDISCOs havt. Thus ele

0%

IESCO

FESCO

GEPCO

LESCO

MEPCO

QESCO

HESCO

TESCO

PESCO

SEPCO

gure 14.6: Co

ource: National E

s Nam

1 ur Power Proj2

e-Azam Solar e-Azam Solar Steam (3) e-Azam Solar

m Jhelum HydeGol HPP

a 4th Extensionant at Sahiwalant at Jamshooal Plant ant Larkana

ni Power Park tion AdditionPower Compa

electricity, are mainly

o consumersal point afte

factor is structure wunishment tor respective

However, thhe governmethe combineve to be bornectricity gen

5%

mparison of T

Electric Power Re

e of Project

ject

Park (Phase-IPark (Phase-I

Park (Phase-Iel

n l ro

n any Ltd

the Distribuy responsibles and colle

er inefficienc

that NEwith incentiv

o inefficient transmissione unified t

ent disallowsed losses ofne by the feneration bec

10% 15

T & D losses a

egulatory Author

I) II)

III)

ution e for cting cy in

the gperfdistr

EPRA ve to

ones n and tariff s this f the deral come

overto trcost furntherminterbeinmajocircu

5% 20%

among DISCO

rity

Capacity(243 MW)(425 MW)(243 MW)(100 MW)(300 MW)(261 MW)(600 MW)(969 MW)(106 MW)(147 MW)(1410 MW(1200 MW(1320 MW(1320 MW(1320 MW(6600 MW16564 MW

generation stform well ribution (T &

r expensive oransmission

of generatnace oil submal power rvenes throu

ng necessity ority of peoular debt and

25%

s

AGGG

G

WW

W) WW) W) GW) GW) GW) PuW

tage is that tin terms

& D) losses.

one due to coand distrib

tion coupledbstantially h

generation. gh subsidiesof life will

ople. Howevd when the p

30%

2012 2

Energy

Agency GENCOs GENCOs GENCOs

PPDB PPDB

GENCOs PPDB

WAPDA WAPDA

PPDB WAPDA

PPDB GENCOs GENCOs GENCOs ublic + Pvt

the main DISof transm

ostly input anution losses

d with rise has raised t

The govers realizing thbecome una

ver, this alspresent gove

35% 40

2013 2014

y 223

Fuel Gas Oil Gas

Solar Solar Gas

Solar Hydel Hydel Hydel Hydel COAL COAL COAL COAL COAL

SCOs do notmission and

nd other dues. This highin price of

the cost ofrnment thusat the power

affordable too results in

ernment paid

0%

t d

e h f f s r o n d

224 Pakistan Economic Survey 2013-14

the unsustainable level of circular debt there was 1752 MW increase in capacity utilization.

To diversify the primary energy supply in the generation, Pakistan Atomic Energy Commission (PAEC) produce electricity through nuclear plants. By this time three nuclear power plants are operational. The first nuclear power plant i.e. Karachi Nuclear Power Plant (KANUPP) completed its 30 years design life in 2002.

14.2.5 Nuclear Energy

Pakistan Atomic Energy Commission (PAEC) is responsible for planning, construction and operation of nuclear power plants in the country. PAEC is currently operating three nuclear power plants Karachi Nuclear Power Plant (KANUPP), Chashma Nuclear Power Plant Unit-1 (C-1) and Unit-2 (C-2). The construction of two more units C-3 and C-4 of 340 MW each is in progress. The second and third nuclear power plants i.e., (C-1 and C-2) are performing very well. Performance of all three

operating nuclear power plants is given in the following Table 14.3:

Table 14.2: Electricity generation S.No Source Capacity addition

(MW) IPPS – Fuel Operated Plants 1 KAPCO 282 2 HUBCO (RFO) 363 3 HUBCO Narowal

(RFO) 204

IPPS – Gas Operated Plants 4 Liberty (Gas) 193 5 Saif Power (Gas &

HSD) 56

6 Halmore (Gas & HSD)

48

GENCOs 7 Jamshoro (RFO) 388 8 Guddu (Gas) 136 9 Muzaffargarh (RFO) 82 Total 1,752 Source: Ministry of Water and Power

Table 14.3: Performance of the Operating Nuclear Power Plants in Pakistan Plants Gross Capacity (MW) Grid Connection Data Electricity sent to Grid (million KWh)

July 1, 2014 to March 31, 2014

Lifetime upto March 31, 2014

KANUPP 100 18-Oct-71 291 13,004 C-1 325 13-Jun-00 1,840 26,781 C-2 330 14-Mar-11 1,866 6,096 Source: Pakistan Atomic Energy Commission The construction of fourth and fifth nuclear plants, Chashma Nuclear Power Plant unit 3 & 4 (C-3 and C-4) at Chashma site, is ahead of the schedule. The Domes on containment buildings of C-3 and C-4 were placed on the 6th March, 2013 and 2nd January, 2014, respectively. Status of under construction nuclear power plant is given in the following Table 14.4:

Table 14.4: Status of under construction nuclear power plant Plants Gross

Capacity (MW)

First Concrete Pour Date

Target Commercial Operation

Date C-1 340 4-Mar-11 30-Apr-16 C-2 340 18-Dec-11 31-Dec-16

Source: Pakistan Atomic Energy Commission PAEC is implementing nuclear power program 2030 set by Energy Security Plan of the Government of Pakistan. The ground breaking ceremony of Karachi Coastal Power Project (K-2 and K-3) was held on 26th November, 2013. To meet the targets, sites are being identified for more under power plants.

Technical and engineering infrastructure is in place to provide technical support to existing under construction and future nuclear power plants

One reason of energy crises is expensive input and if timely efforts are not made for cheaper energy mix, the problem can be more severe in future. The government is committed to achieve less oil dependent power generation mix through development of indigenous energy resources particularly hydel and coal. Recently, the Executive Committee of the National Economic Council (ECNEC) approved four development projects in power sector having a combined generation capacity of 3,511 MW. The approved projects include K-I and K-II Nuclear Projects situated in Karachi (Province of Sindh; generation capacity 2,200 MW), Nandipur (Province Punjab; generation capacity 425 MW; cost Rs 57,380 million) and Neelum-Jhelum hydroelectric project (AJK; generation capacity 969 MW). Government of Pakistan is committed to arrange timely finances for these projects and monitor their development regularly in order to complete them as per schedule. Also one other

Energy 225 diversification in using energy mix in the generation of electricity is by producing electricity by Co-Generation for which government is seriously thinking. Co-Generation is a high efficiency energy system that produces both electricity (and mechanical power) and valuable heat from a single fuel source. Pakistan being the fifth largest sugarcane producer in the world has the potential to generate electricity of almost 2,000 MW through Co-Generation. Bagasse (process waste of sugar industry) is a fibrous residue of cane stalk obtained after crushing. When burned in quantity, bagasse produces sufficient heat energy to supply all the needs of a typical sugar mill, with energy to spare. To this end, a secondary use of bagasse is in Co-Generation. Development of Co-Generation plants based on high pressure boilers is gaining momentum worldwide. Thus Co-Generation by sugar mills by utilizing bagasse and coal provides one of the most economically viable options for thermal power generation, earlier it remained unexploited in Pakistan.

14.3.Energy Consumption

Energy consumption is the amount of energy left for final use after subtracting energy lost in transformation and distribution from primary energy supplies. It is considered as the oxygen of an economy and the lifeline of the economic growth particularly in the industrialization stage of an emerging economy. The importance of energy

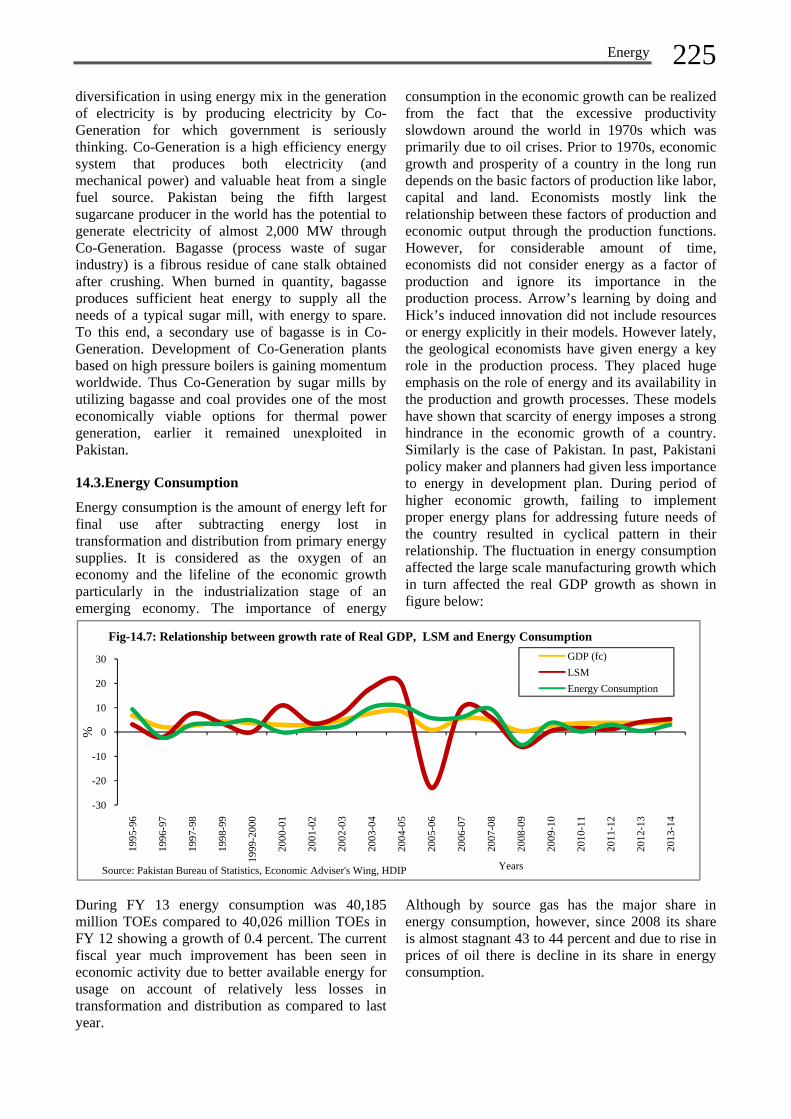

consumption in the economic growth can be realized from the fact that the excessive productivity slowdown around the world in 1970s which was primarily due to oil crises. Prior to 1970s, economic growth and prosperity of a country in the long run depends on the basic factors of production like labor, capital and land. Economists mostly link the relationship between these factors of production and economic output through the production functions. However, for considerable amount of time, economists did not consider energy as a factor of production and ignore its importance in the production process. Arrow’s learning by doing and Hick’s induced innovation did not include resources or energy explicitly in their models. However lately, the geological economists have given energy a key role in the production process. They placed huge emphasis on the role of energy and its availability in the production and growth processes. These models have shown that scarcity of energy imposes a strong hindrance in the economic growth of a country. Similarly is the case of Pakistan. In past, Pakistani policy maker and planners had given less importance to energy in development plan. During period of higher economic growth, failing to implement proper energy plans for addressing future needs of the country resulted in cyclical pattern in their relationship. The fluctuation in energy consumption affected the large scale manufacturing growth which in turn affected the real GDP growth as shown in figure below:

During FY 13 energy consumption was 40,185 million TOEs compared to 40,026 million TOEs in FY 12 showing a growth of 0.4 percent. The current fiscal year much improvement has been seen in economic activity due to better available energy for usage on account of relatively less losses in transformation and distribution as compared to last year.

Although by source gas has the major share in energy consumption, however, since 2008 its share is almost stagnant 43 to 44 percent and due to rise in prices of oil there is decline in its share in energy consumption.

-30

-20

-10

0

10

20

30

1995

-96

1996

-97

1997

-98

1998

-99

1999

-200

0

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

%

Years

Fig-14.7: Relationship between growth rate of Real GDP, LSM and Energy Consumption GDP (fc)LSMEnergy Consumption

Source: Pakistan Bureau of Statistics, Economic Adviser's Wing, HDIP

226 P

14.3.1 Oil (

Transport asector in tHowever, dincrease in share increaof oil in treason is th

Source: Hydr

During Julyconsumptiowhile share0.8 and 0.compared th

During FY was US $ 1it was 19.million metmillion metMarch FY

Percen

tage

Share

Power41.1

Other Go1.6

Sh

Pakistan Eco

(Petroleum P

and power she usage o

during last twthe usage o

ases to 40.0 transport sechat majority

rocarbon Devel

y – March Fon is increase of transpor6 percentaghe same duri

13 the imp14.9 billion. I.2 million mtric tons of tric tons of p14, the impo

0%5%

10%15%20%25%30%35%40%45%

Percen

tage

Sha

re

Figure 14.8

Source: Hydroca

Households0.5

vt.

hare of sectorOil/Pe

July-M

onomic Surve

Product)

sectors remaf oil / petr

wo decade thof oil in powpercent in 2

ctor is almoof commercFigure 14.9:

lopment Institut

FY 14, shareed by 1.7 prt and indus

ge point, resing July – M

port bill of If to look intmetric tons petroleum p

petroleum cruort bill of pe

2008

8: Energy Cons

arbon Developmen

rs in Consumetroleum (%)

March FY 13

ey 2013-14

ained the higroleum prodhere is signifwer sector a2013 while uost stagnant,cial transport

Share of sect

te of Pakistan

e of power ipercentage ptry decreasespectively, warch FY 13.

petroleum gto quantity t

including products andude. During etroleum post

2009

sumption by S

nt Institute of Pak

Industy7.4

Agriculture0.1

T

mption of )

ghest ducts. ficant s the

usage , the t still

use whilshiftoil ideclJulypetrocorr

tors in consu

in oil points ed by when

group terms 12.3

d 6.9 July-ted a

negaof pduribillia neimpoas itcomperioquancrudmain

2010

Years

Source

kistan

ransport49.3

Powe42.8

oil and thele usage of ot toward CNin agriculturline in activy-March FY oleum prodesponding p

mption of Oi

ative growthpetroleum prng July-Maron during co

egative growtort of petrolt was US $ 4

mpared to USod last yeantities of botde (5.0 percen reason attri

2011

Oil CoalLPG

Hous0

er

Other Govt.1.6

Share of sO

J

ere is negligoil in househoNG from oil. re and indu

vity due to p14, the comp

duct is littleeriod last ye

il / Petroleum

h of 1.3 perceroducts stoorch FY 14 orrespondingth of 5.6 perleum crude i4.3 billion duS $ 4.1 billioar. There wth petroleumnt and 4.3 peibuted to the

2012

G

seholds0.4

sectors in ConOil/Petroleum

July-March FY 1

gible shift toold decline thThe declinestry could bpower shortposition of ue variant frar as shown

m

ent. The valuod at US $compared to

g period last rcent. Howevincreased byuring July-Mon during co

was positivem products an

ercent respece increase in

2013

Gas Electricity

Industy6.2

A

nsumption ofm (%)

4

oward CNGhat show the

e in usage ofbe linked totage. Duringusage of oil /rom that inbelow:

ue of import 6.6 billiono US $ 7.0year postingver, value of

y 6.2 percentMarch FY 14orrespondinge growth innd petroleumctively). Thequantity and

Agriculture0.2

Transport48.7

f

G e f o g / n

t n 0 g f t 4 g n

m e d

decrease in prices of pwas global change in which refleproduct.

14.3.2 Natu

Pakistan ishouseholds,major end uof consumpThere was fertilizer inperformancreason of abto frail funcconfronting

Source: Hydro 14.3.3 Elect

The consumand is the hprime reasoalso brougpeople. Theconomic g

Industry22.6

Transport(CNG)

8.2

Sha

value of pepetroleum pr

increase in pits consump

ect that petr

ural Gas

the larger , power, feruser of gas. Inption of gas

sharp declndustry whie of fertilizebnormal reductioning of SNg the worst

ocarbon Develo

tricity

mption of elehighest amonon is technoght significahere is cycgrowth and

Power27.5

t

are of sectors

Ju

-5

0

5

10

15

1995

-96

Gro

wth

Rat

e (%

)

Fig-14.11

Source: HD

etroleum proroducts globprice of petr

ption patternroleum crud

consumer ortilizer and n last two deamong its u

line in gas ich had neger sector. In uction in gasNGPL-basedgas crisis

Figure 1

opment Institute

ectricity has ng all sourceological advant change clical relati

electricity

s in Consump(%)

uly-March FY 13

1996

-97

1997

-98

1998

-99

1: Relationshand elect

DIP, PBS and EA

duct is declibally. Even troleum cruden had been e is an inel

of the gas. industry are

ecades the pausers is chan

consumptiogatively affeFY 13, the ms supply wasd fertilizer plwhich caus

14.10: Share o

e of Pakistan

increased rapes of energy.vancement w

in lifestyleionship betwconsumptio

Households23.2

Comm3.3

Cem0.

Fertilizer15.2

ption of Gas

1999

-00

2000

-01

2001

-02

ip between grtricty consum

A Wing

ining there e, no seen

lastic

The e the attern nged. on in ected main s due lants, ed a

sharfertiPakaAgrishorferti19 pperiocomhousprioinduoil wuse to lprescauscons

of sectors in c

pidly One

which e of ween n. It

implby hwhicthe advagrowcons

ercial3

ment.1

Industry21.7

2002

-03

2003

-04

2004

-05

Year

rowth of GDPmption

rp decline ilizer plants arab, Dawooitech, remairtages. Durinilizer industrpercent whicod last fiscal

mmitment of sehold, powerity basis. H

ustry is declinwith gas. Tiof gas (CNGload managscribed hourssed decline sumption as

consumption

lies that the higher growch is obvioustandard of

ance technowth of GDP sumption of

Power26.1

y

Transport(CNG)

7.0

Share of se20

05-0

6

2006

-07

2007

-08

2008

09

rs

P (fc)

in the ovon the SNG

od Hercules,ined the mang July-Marry in gas coch was 15 pl year. This mthe governm

er industry aHowever, thening as powell FY 13, th

G) as input ingement in gs / days for s

in the shashown below

of Gas

period of hiwth rate of us in the sensf living or ological gowill negativelectricity as

ectors in Con(%)

July-March FY

2008

-09

2009

-10

2010

-11

2011

-12

Electricity Con

GDP (fc)

Energy

erall produGPL networ, Engro's neain sufferersrch FY 14, tonsumption percent in comajor upturnment to proand fertilizere usage of ger industry cahere was incn transport, hgas sector supplying CN

are of transpw:

igher growthelectricity cse that growproduction

oods. Likewvely affect ths shown belo

H

nsumption of

Y 14

2012

-13

2013

-14

nsumption

y 227uction. Fourrk, includingw plant and of the gasthe share ofincreased to

orrespondingn was due toovide gas tor industry ongas in poweran substitute

crease in thehowever duethere were

NG that hadport in gas

h is followedconsumption

wth improvesby utilizing

wise, lowerhe growth ofow:

ouseholds23.2

Commercial3.1

Cement0.0

Fertilizer19.0

f Gas

7r g d s f o g o o n r e e e e d s

d n s g r f

228 P

The lower goccurred dugrowth in cwill lower t

Prior to unsectors exconsumptiohousehold. percent in 1industrial uof load shhome applimade the shincreased to1993. In consumptio10 percenttransformatindustrial agriculture almost 26 significant 14.3.4 Coal

Pakistan’s cbituminous.2000. Abouthe country and 56.1 pdecrease opercent, reshas been shence utilimomentumPakistan ha185 billionidentified atThe powersignificance

Pakistan Eco

growth in elue to loss of gconsumptionthe growth o

nbundling oxhibit a chon pattern,

The share o1993 to 29 punits are usinedding. Incriance due tohare of resideo 47 percentcase of ag

on decreased t in 2013, ion away and servicin real GDPpercent in change in

l

coal generall. Coal conut 39.1 perce

has been utpercent by

of 3.46 percpectively. A

switched oveization of . s huge coal rn tons; int Thar coal fr project at e due to

0

1993

1998

2003

2008

2013

Years

Fig‐14.12

Source: Hydr

onomic Surve

ectricity congrowth mom

n of electriciof GDP in ne

of WAPDAhange in

especially f industry de

percent in 20ng own captrease in usa

o technologicential electrict in 2013 frogriculture se

from 15 pethis show

from agricues sector.

P declined to1990s.Howethe consum

ly ranks fromnsumption isent of total ctilized by bri

cement faccent and in

Almost wholeer from furningenious c

resources estncluding 17fields (Sindh

Port Qasimimportance

% 1

2: Share in ele

rocarbon Develop

ey 2013-14

nsumption camentum and lity in one peext period. P

A to presenttheir electr

industry ecreased from

013 because tive unit becage of electcal improvemcity consumpom 36 perceector, electrercent in 199w the struculture secto

The share 21 percent

ever, there imption patter

m lignite to s varying scoal consumeick kilns inductories, showncrease of e cement indunace oil to coal is gai

timated to ex75 billion Province) a

m had a spof Karach

10%

ectricity consu

pment Institute of

an be ower eriod olicy

makconshighdow

t, all ricity

and m 36 large cause trical ment ption

ent in ricity 93 to ctural or to e of from is no rn of

comcomalmoyear

sub-since ed in ustry wing 1.83 ustry coal

ining

xceed tons, lone.

pecial hi in

Pakithe prodplana caGad6,6014.4

The posssustagovebeendeve(ARDev

20%

umption

f PakistanPe

rcen

tage

Sha

re (%

)

kers need psumption ofher growth i

wn the pace o

mmerce. Howmposition of

ost similar tr as shown be

istan's econoeconomic d

duction of elnts is cheaperapacity of 66dani in Baluc00 MW in the4 Alternative

Governmensible measurainable devernment in itn giving delopment of

RE) resourcesvelopment Bo

30%

Agric

Com

0%5%

10%15%20%25%30%35%40%45%50%

Household

Figure

plans to af electricity in GDP whif growth in c

wever, duringshare of ele

to that in coelow:

omy and it cdevelopment lectricity fror, ten coal-fi60 MW eachchistan, whice national gre Sources of

nt of Pakistres to ensurvelopment ts bid to divedue attentiof Alternatives in the counoard (AEDB

40%

Percentage S

cultural I

mercial H

d Commercial

Secto

e 14.13: Sharconsump

July-Ma

address the that will o

ich otherwiscoming years

g July-Marchectricity conorresponding

an play a crof Pakistan

om the coal red power ph, are beingch would ad

rid. f Energy

tan (GoP) ire energy sin the co

ersify its eneron towards e / Renewantry. Alterna

B) has been m

50%

Share (%)

ndustrial

Household

Industrial Agric

rs

re in electrictytion

arch FY 13 July-M

growth inccur due tose will slows.

h FY 14, thensumption isg period last

rucial role inn. Since thefired powerrojects, with

g initiated atdd a total of

s taking allsecurity andountry. Thergy mix, has

fast trackable Energyative Energymandated to

cultural

y

March FY 14

n o w

e s t

n e r h t f

l d e s k y y o

Energy 229 act as a central agency for development and promotion of Alternative & Renewable Energy (ARE) technologies in the country and to facilitate the private sector investment in this sector.

Steps Taken By AEDB to Attract Investment in the Sector

AEDB has undertaken a number of supportive measures in order to promote ARE technologies and to attract private sector investments, which include;

Identification of new corridors for wind and solar energy projects development. Resource assessment of these corridors is underway.

National Grid Code for wind power projects has been amended. Grid Integration Plan 2010 -2015 for wind power projects has been developed by AEDB to support NTDC.

Local manufacturing of micro wind turbine has been started. Manufacturing for large wind turbines is also being encouraged. M/s DESCON has setup a wind turbine tower manufacturing facility and has provided towers for the first wind project in Pakistan. M/s Three Gorges Corporation / CWE (China) has also established a tower manufacturing facility which will be upgraded to wind turbine assembling facility in future.

Issues related to financing of projects have been resolved and now leading financing agencies like International Finance Corporation (IFC), Asian Development Bank (ADB), Overseas Private Investment Corporation (OPIC), Economic Cooperation Organization (ECO), Trade Bank etc. are offering financing to wind power projects in Pakistan.

14.4.1 Wind

Thirty five wind power IPPs holding LOIs issued by AEDB are at various stages of project development.

Operational (Achieved Commercial Operations Date)

FFC Energy Limited: 49.5 MW wind project, Jhampir, Distt. Thatta, Sindh

Zorlu Enerji (Pvt.) Ltd. 56.4 MW wind project, Jhampir, Distt. Thatta, Sindh.

Under Construction 50 MW Three Gorges First Wind Farm

Pakistan (Pvt.) Ltd., Jhampir Sindh 50 MW Foundation Wind Power I Ltd.

Khuttikun, Gharo, Sindh 50 MW Foundation Wind Power II (Pvt.)

Ltd., Khuttikun, Gharo, Sindh

Twelve projects with a cumulative capacity of 630 MW are expected to achieve Financial Close by 2014.

NERPA announced a new upfront tariff of US cents 13.5244 per kWh on 24th April 2013 for 500 MW wind power projects. The wind power companies interested in opting Upfront Tariff will have to achieve Financial Close of their project by September 30, 2014.

14.4.2 Solar

In Solar Energy, 24 LOIs for cumulative capacity of approximately 792.99 MW On-Grid Solar PV power plants have been issued. Four (4) companies have submitted the feasibility studies of their projects and one feasibility study is approved by AEDB. Other sponsors are at the stage of preparation of feasibility studies

Solar Village Electrification Program was initiated under PM’s directive. 3000 Solar Home Systems have been installed in 49 villages of district Tharparkar, Sindh. Another 51 villages in Sindh and 300 villages in Baluchistan have been approved for electrification using solar energy and will be implemented shortly.

AEDB in light of SRO 575(1)12006 issued duty exemption certificates for a large number of solar panels / solar modules to private sector companies for installation / generation of almost 64.57MW of energy in the country. These solar panels / solar modules are deployed all over the country.

AEDB issued tax exemption certificate for import of almost 16715 units of Solar Water Heaters in the country. These heaters are deployed all over the country especially in Baluchistan, Gilgit-Baltistan, Khyber Pakhtunkhwa and Northern Punjab.

AEDB also issued tax exemption certificate for import of about 1429 units of Solar Water Pumping System in the country. These water pumping systems are installed for community drinking and agriculture purpose all over Pakistan.

14.4.3 Biomass / Waste-to-energy

Framework for power Co-Generation has been approved by ECC for bagasse/biomass based sugar industry projects. 1500-2000 MW of power is expected to be generated in next 2-3 years. LOIs has been issued to following investors / sugar mills under this framework;

M/s JDW Sugar Mills Unit-II (26 MW), Rahim Yar Khan, Punjab.

230 Pakistan Economic Survey 2013-14

M/s JDW Sugar Mills Unit-III, (26 MW),

Ghotki, Sindh. M/s Hamza Sugar Mills Ltd., (15 MW) M/s RYK Sugar Mills Ltd., (19 MW) Rahim

Yar Khan, Punjab. M/s Chiniot Power Plant, (15 MW), Chiniot,

Punjab.

14.4.4 Small / Mini / Micro Hydro

Eight hydro projects have been initiated under the Renewable Energy Development Sector Investment Program (REDSIP) with the support of Asian Development Bank (ADB). These projects are being implemented in Khyber Pakhtunkhwa and Punjab with an estimated cost of US $ 290 Million.

Another 02 small hydro power projects have been initiated under REDSIP. PC-I for these projects have been approved. Loan approval from ADB is awaited.

The Government of Punjab issued LOIs to private investors for establishment of 10 small hydro projects with a cumulative capacity of 142 MW at different location in Punjab.

AEDB is building capacities for private sector investment in Khyber Pakhtunkhwa (22 projects of cumulative 92 MW capacity through Pakhtunkhwa Hydel Development Organization (PHYDO) and Punjab (30 projects of cumulative 240 MW capacity through Energy Department / Punjab Power Development Board (PPDB).

AEDB initiated a program with the assistance of GIZ support to assist the provinces solicit private investments in small hydro sector; under this program Pre-Feasibility Studies for 25 hydro sites in AJK, Sindh, Punjab and Khyber Pakhtunkhwa with the cumulative capacity of 284.14 MW have been completed.

Public sector Hydro power projects initiated in:

Khyber Pakhtunkhwa (worth U$ 150.99 Million, of 17.0MW, 36.6MW and 2.6 MW)

Punjab (worth U$ 138.74 Million, of 5.38MW, 4.04MW, 2.82MW, 4.16MW and 7.64MW)

Gilgit-Baltistan(worth U$ 71.12 Million, of 26MW and 4MW).

14.4.5 Clean Development Mechanism (CDM)

CDM is one of the instruments that developers of the Alternative and Renewable Energy (ARE) Projects pursue and earn financial returns by getting their projects registered with CDM Executive Board and selling the accrued Certified Emission Reduction (CER) certificates in the international carbon market.

Way Forward

Realizing the criticality of energy for economic growth, it is the main focus of Pakistan Vision 2025. The vision aims at ensuring uninterrupted access to affordable and clean energy for all sections of the population and aimed at resolving structural changes within the energy sector are fundamental to future economic prospects. The main elements of this vision include: 1. Optimize energy supply mix–economic,

scalable, indigenous by 2025 2. Reduce “cost per unit” 3. Reduce supply gap by 2018 and exceed demand

gap by 2025 4. Create and encourage culture of conservation

and efficiency in the usage of energy

Nonetheless, these projects have long digestion period and would come in to system in few years. It is also highlighted that through efficient reallocation of natural gas based on economic sense is essential to get best value for money.