Energy Indicators: Assesing the Energy Transition in the LAC

35

Energy Indicators: Assesing the Energy Transition in the LAC Ruben Contreras Lisperguer Economic Affairs Officer Energy and Water Unit Natural Resources Division UN ECLAC Regional Observatory on Sustainable Energies

Transcript of Energy Indicators: Assesing the Energy Transition in the LAC

Energy Indicators: Assesing the Energy Transition in the LAC

Ruben Contreras Lisperguer

Economic Affairs Officer

Energy and Water Unit

Natural Resources Division

UN ECLAC

Regional Observatory on Sustainable Energies

Has there been an energy transition in the Latin American

region?

¿How does ECLAC define Energy Transition in Latin America and the Caribbean??

Energy transition will be understood as the process of change in policies,institutions, regulations and investments that promote the generation and moresustainable uses of energy aiming at the decarbonization of the economy,prioritizing:

• More generation of electricity from renewable sources, with an emphasis onvariable renewables.

• More energy efficiency of energy systems, including transport.• More sustainable management of fossil fuels and biofuels• More energy complementarity leading to less regional energy vulnerability

Objective: Decarbonization

Strategy: Energy Transition

Instrument: Environmental Big Push

• Are the existing indicators comprehensive, robust and comparable?

• How the existing indicators can be improved?

• Role of regional cooperation and knowledge sharing

Devil is in Detail: Need for Disaggregation

• Energy access: share of population with access

➔ Improvement: Access Quality?, Impact on poorest sector?, Share of rural and urban population

• Renewable energy share in final energy

➔ Improvement: RE in heat, electricity, mobility, End-of-Life

• Energy intensity: primary energy per GDP

➔Improvement: Sectoral tracking (households, industry, transport)

➔Challenge: Considering the heterogeneity between countries (climate, economic structure, etc.)

Energy Matrix

LAC vs the World - Total Primary Energy Supply 2000 - 2017 (Percentages)

50.5

36.543.1

32.0

4.6

23.15.5 26.9

19.4

20.6

25.2

22.0

1.1

0.5

0.8

0.614.8

10.217.4

9.8

0.0 0.0 0.0 0.00.0 0.1 0.2 1.28.5

2.3

7.52.5

1.06.7

0.35.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

ALC Mundo ALC Mundo

2000 2017Petróleo Carbón Gas Natural Geotermia Bioenergía Calor Solar y Eólico Hidroenergía Nuclear

39%

33%

17%

5%5% 1%

Consumo energía final regional - 2017

TRANSPORTE INDUSTRIAL RESIDENCIAL COMERCIAL, SERVICIOS, PÚBLICO AGRO, PESCA Y MINERÍA CONSTRUCCIÓN Y OTROS

Energy Consumption by Sector 2017. The transport sector is one of the largest consumer of energy resources, with 99% coming from fossil fuels.

50

7009

6

15

328

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1

Consumo energía final del sector INDUSTRY por fuentes al 2017

ELECTRICIDAD GAS LICUADO GASOLINA/ALCOHOL

KEROSENE/JET FUEL DIÉSEL OIL FUEL OIL

COQUE CARBÓN VEGETAL GASES

OTRAS SECUNDARIAS

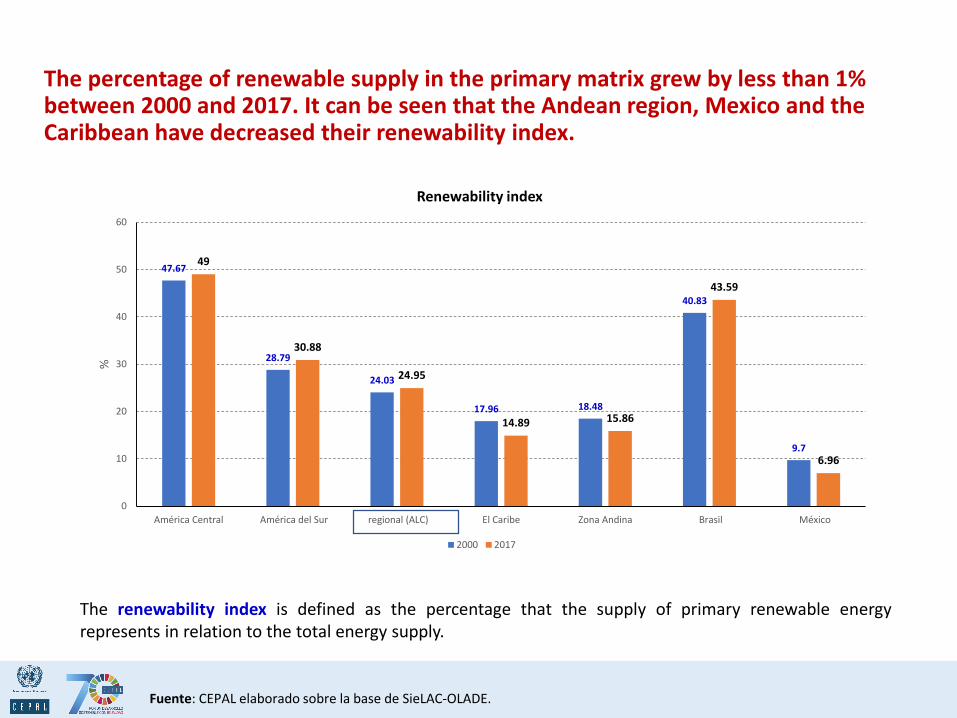

Fuente: CEPAL elaborado sobre la base de SieLAC-OLADE.

01

52

41

60000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Consumo energía final del sector TRANSPORT por fuentes al 2017

OTRAS SECUNDARIASGASESCARBÓN VEGETALCOQUE

KEROSENE/COMBUSTIBLE JETDIÉSELGASOLINA/ALCOHOL

The percentage of renewable supply in the primary matrix grew by less than 1% between 2000 and 2017. It can be seen that the Andean region, Mexico and the Caribbean have decreased their renewability index.

Fuente: CEPAL elaborado sobre la base de SieLAC-OLADE.

The renewability index is defined as the percentage that the supply of primary renewable energyrepresents in relation to the total energy supply.

47.67

28.79

24.03

17.96 18.48

40.83

9.7

49

30.88

24.95

14.89 15.86

43.59

6.96

0

10

20

30

40

50

60

América Central América del Sur regional (ALC) El Caribe Zona Andina Brasil México

%

Renewability index

2000 2017

Hidro16%

Térmica66%

Nuclear11%

Geotermia2%

Eólica4%

Solar1%

Mundo

Electricity generation matrix: in Latin America and the Caribbean, 53% is renewable, of which 83% is hydroenergy.

Matriz de generación eléctrica en

América Latina y el Caribe y el Mundo

2017

(En porcentaje respecto al total)

Hidroenergía44%

Gas natural27%

Petróleo y derivados

11%

Carbón mineral y

coque7%

Biomasa5%

Geotermia1%

Eólica3%

Solar0%

Nuclear2%

ALC

Fuente: Organización Latinoamericana de Energía (OLADE)

23% renovable

Térmica en ALC es deun 45%: Incluye GasNatural (27%) +Petróleo y Derivados(11%) y CarbónMineral (7%)

Fuente: CEPAL elaborado sobre la base de SieLAC-OLADE y base de datos de la IEA.

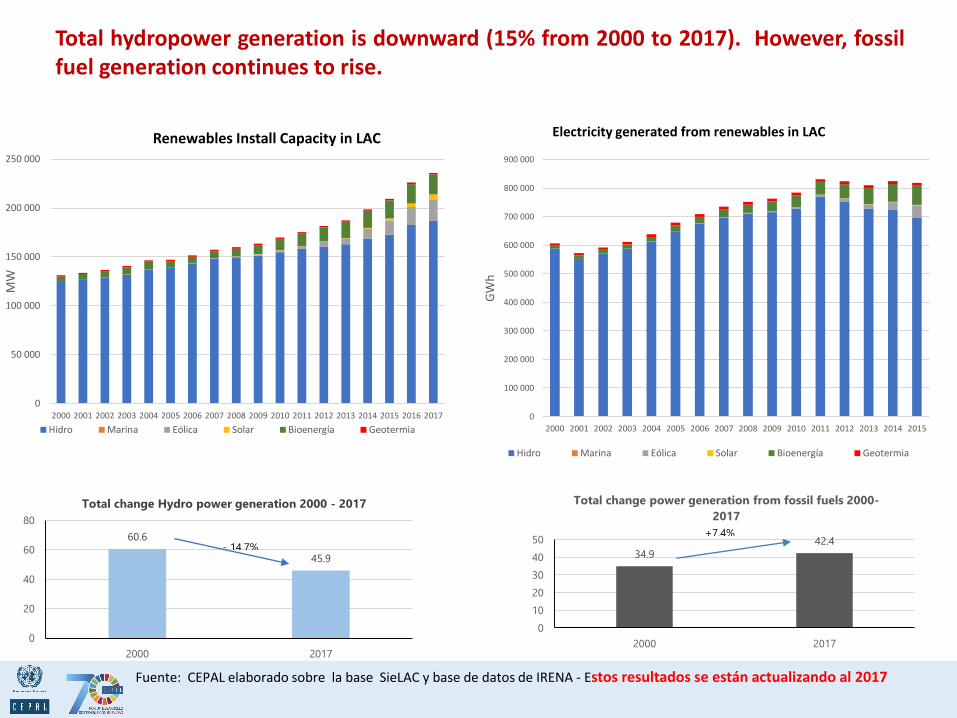

60.6

45.9

0

20

40

60

80

2000 2017

Total change Hydro power generation 2000 - 2017

- 14.7%34.9

42.4

0

10

20

30

40

50

2000 2017

Total change power generation from fossil fuels 2000-

2017

+7.4%

Total hydropower generation is downward (15% from 2000 to 2017). However, fossilfuel generation continues to rise.

Fuente: CEPAL elaborado sobre la base SieLAC y base de datos de IRENA - Estos resultados se están actualizando al 2017

0

50 000

100 000

150 000

200 000

250 000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MW

Renewables Install Capacity in LAC

Hidro Marina Eólica Solar Bioenergía Geotermia

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

800 000

900 000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

GW

h

Electricity generated from renewables in LAC

Hidro Marina Eólica Solar Bioenergía Geotermia

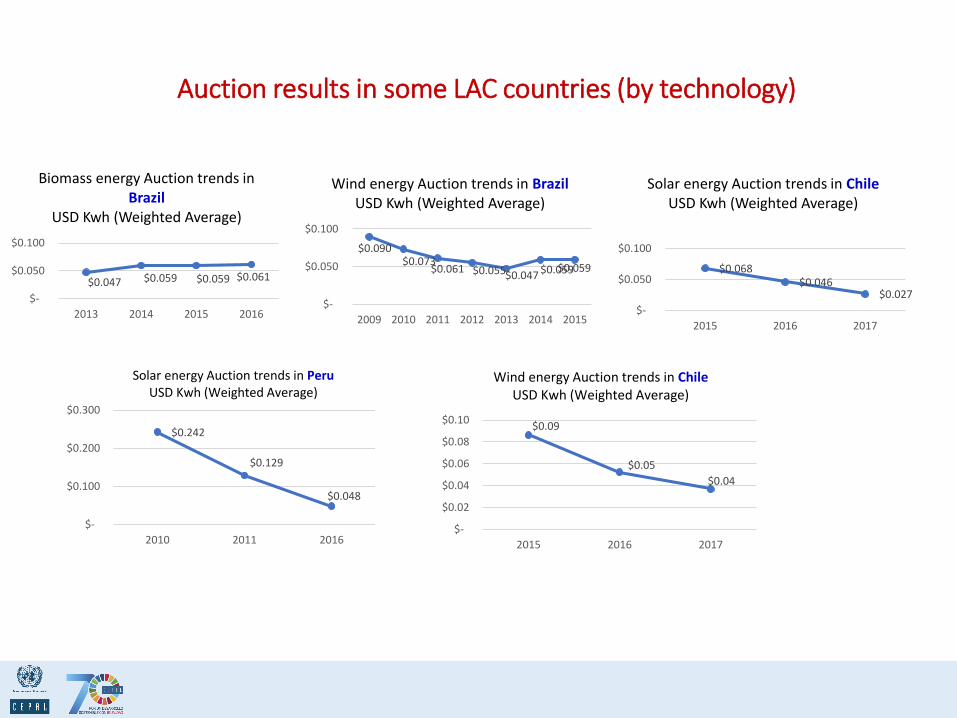

Auction results in some LAC countries (by technology)

$0.047 $0.059 $0.059 $0.061

$-

$0.050

$0.100

2013 2014 2015 2016

Biomass energy Auction trends in Brazil

USD Kwh (Weighted Average)

$0.090 $0.073

$0.061 $0.055 $0.047 $0.059 $0.059

$-

$0.050

$0.100

2009 2010 2011 2012 2013 2014 2015

Wind energy Auction trends in BrazilUSD Kwh (Weighted Average)

$0.068 $0.046

$0.027

$-

$0.050

$0.100

2015 2016 2017

Solar energy Auction trends in ChileUSD Kwh (Weighted Average)

$0.242

$0.129

$0.048

$-

$0.100

$0.200

$0.300

2010 2011 2016

Solar energy Auction trends in PeruUSD Kwh (Weighted Average)

$0.09

$0.05

$0.04

$-

$0.02

$0.04

$0.06

$0.08

$0.10

2015 2016 2017

Wind energy Auction trends in ChileUSD Kwh (Weighted Average)

Installed renewable energy capacity in the electricity sector has advanced significantly

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Bioenergía Geotermia Hidroeléctricas Solar Eólica

3,664.6360.8

115,694.2

5.1 90.5

19,480.3

665.0

175,395.2

5,251.6

17,440.2

2000 2017

Fuente: Elaboración CEPAL sobre base de datos de Financial Times fDi Markets.

Announcement of Foreign Direct Investment in the energy sector: shows an increase

in non-hydro renewables, confirming the beginning of a transition.

$144,379 $113,413

$-

$50,000

$100,000

$150,000

$200,000

Accumulated investment 2005 and 2018 (MUSD)

Fosil Renovable

$99,628

$13,786

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Renovable No-Hidro Renovable Hidro

Accumulated investment for non-hydro renewables and hydro 2005 and 2018 (MUSD)

$16,385.02

$4,536.93 $3,783.10

$6,554.71 $7,548.69

$- $-

$5,000

$10,000

$15,000

$20,000

Fosil Renovable no hidro Hidro

Comparison of Investment between 2005 and 2018 (MUSD) by technology

2005 2018

The foreign direct investment announced in the energy sector represents in renewables an annual investment of approximately 0.16% of the region's GDP (from 2005 to 2018) considering the annual regional GDP at constant dollar prices, while fossil fuels represent 0.21%.

Flexibility, Rotating mass to support system stability: Attention should be paid to the issue of margin reserve and ancillary/secondary services - storage will be key in the near future

65.0%

66.0%

67.0%

68.0%

69.0%

70.0%

71.0%

72.0%

73.0%

74.0%

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

REs Penetration vs Reserve Margin

Hydro Solar Wind Biomass Reserve [%]

[MW]

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

REs Penetration vs Reserve Margin

Hydro Solar Wind Biomass Reserve [%]

[MW]

Escenario base ECOSUD - Sudamérica Escenario Renovables + Integración ECOSUD - Sudamérica

El escenario ER+INT (~800 mil millones US$) representa a la región una inversión anual aproximada del 1% del PIB de la región (del año 2019 al 2032) considerando el PIB total anual a precios en dólares constantes.

Una transición energética sostenible conlleva requisitos para nuevos patrones de uso de minerales

18,000 87,000

509,000

1,005,004

105,000

127,000

163,000

189,180

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2010 2017 2025 2030

Baterias Otros usos

Notas: Las baterías incluye para vehículos (híbridos, híbridos enchufables y eléctricos con batería), camiones y autobuses (livianos, medianos y pesados), vehículos

de dos y tres ruedas, redes de almacenamiento y productos electrónicos de consumo. Los valores en % refieren a la tasa crecimiento anual promedio para esos años

15

85

41

5976

24

84

16

Demanda mundial de litio

En

mil

es d

e to

nel

adas

eq

uiv

alen

tes

de

carb

on

ato

de

liti

o

Porcentaje (%)

+8.2%

+15.4%

+12.2%

Fuente: Comisión Económica para América Latina y el Caribe (CEPAL), sobre la base estadística de McKinsey & Company (2018),

“Energy Technology Perspectives 2015: Mobilising Innovation to Accelerate Climate”. Metals and mining, McKinsey & Company.

Beyond Access

The number of people without access to electricity services fell from 43.6 million in 2000 to 14 million in 2016.

Acceso a los servicios eléctricos en América Latina y el Caribe

(En cientos de millones de personas)

Fuente: Comisión Económica para América Latina y el Caribe (CEPAL), en base a los datos del Global Tracking Framework Initiative

446454

462471

479487

495503

511518

526533

540547

555562

569576

583590

598605

612619

626632

639

382394

402413

424432

444453

463473

482491

500509

517526

536545

556564

573582

591600

607615

625

350

400

450

500

550

600

650

Población total Población con acceso

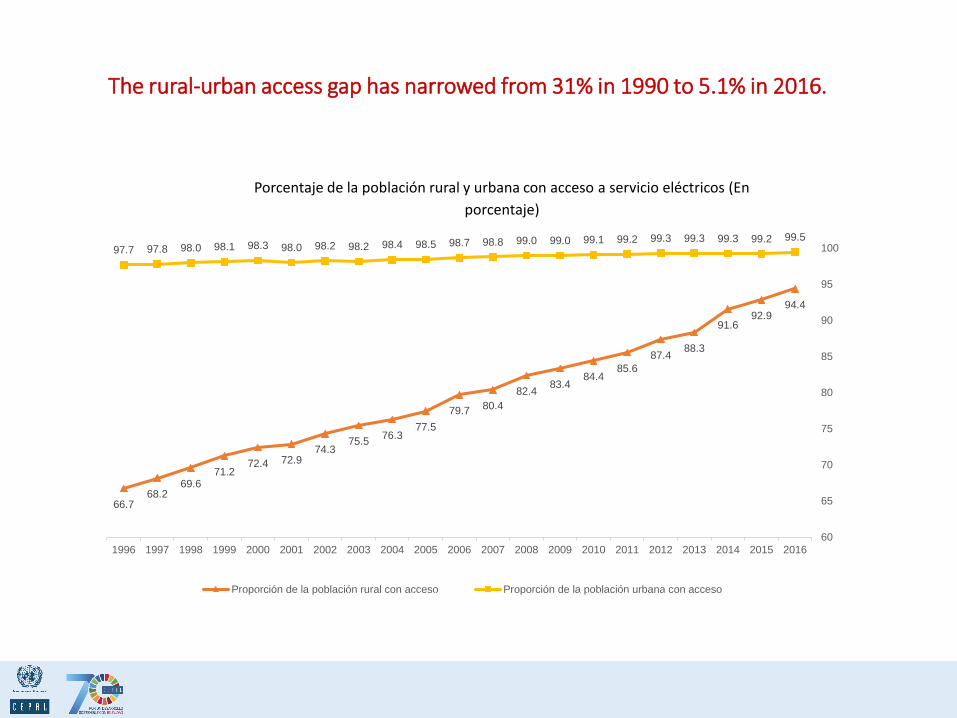

The rural-urban access gap has narrowed from 31% in 1990 to 5.1% in 2016.

Porcentaje de la población rural y urbana con acceso a servicio eléctricos (En

porcentaje)

66.768.2

69.671.2

72.4 72.974.3

75.576.3

77.5

79.7 80.4

82.483.4

84.485.6

87.488.3

91.692.9

94.4

97.7 97.8 98.0 98.1 98.3 98.0 98.2 98.2 98.4 98.5 98.7 98.8 99.0 99.0 99.1 99.2 99.3 99.3 99.3 99.2 99.5

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

60

65

70

75

80

85

90

95

100

Proporción de la población rural con acceso Proporción de la población urbana con accesoFuente: Comisión Económica para América Latina y el Caribe (CEPAL), en base a los datos del Global Tracking Framework Initiative

Actualizado a octubre de 2019

ECLAC Household Survey Data Bank processing

Some Electricity indicators

ROSE

Fuente: CEPAL, Banco de Datos de Encuestas de Hogares (BADEOHG). Se incluyeron 16 países.ECLAC Household Survey Data Bank

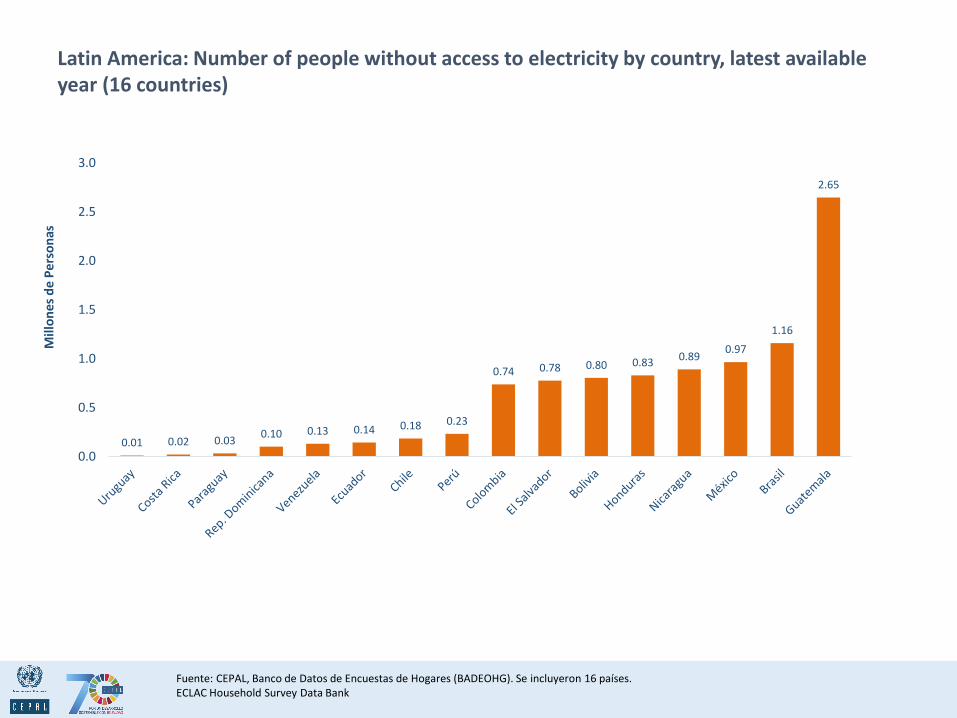

Latin America: Number of people without access to electricity by country, latest available year (16 countries)

0.01 0.02 0.030.10 0.13 0.14 0.18 0.23

0.74 0.78 0.80 0.830.89

0.97

1.16

2.65

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Mill

on

esd

e P

ers

on

as

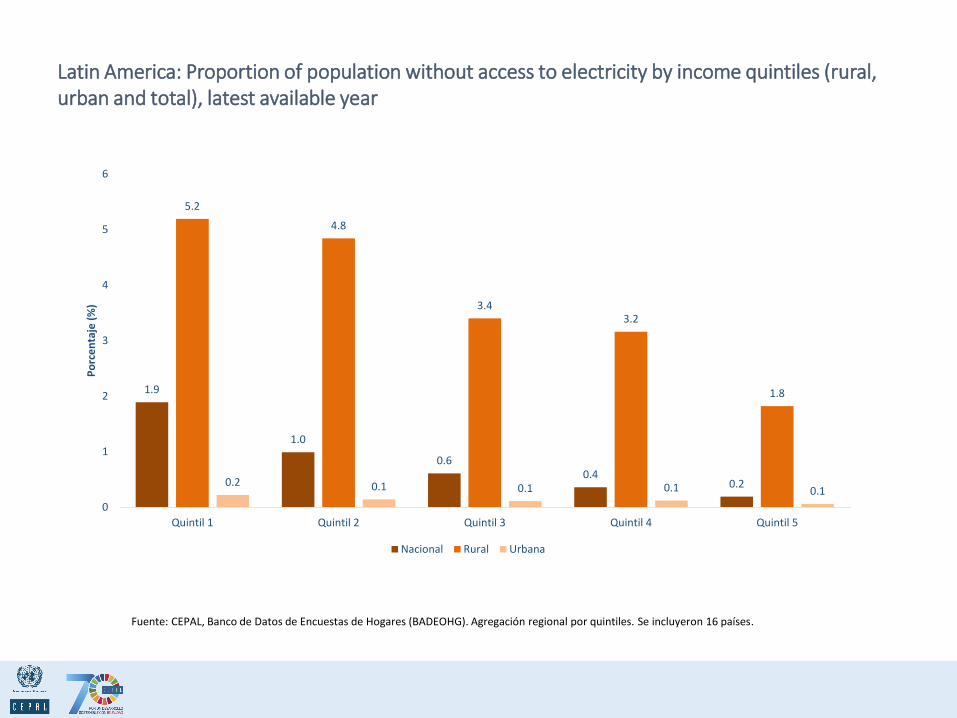

Latin America: Proportion of population without access to electricity by income quintiles (rural, urban and total), latest available year

Fuente: CEPAL, Banco de Datos de Encuestas de Hogares (BADEOHG). Agregación regional por quintiles. Se incluyeron 16 países.

1.9

1.0

0.60.4

0.2

5.2

4.8

3.43.2

1.8

0.2 0.1 0.1 0.1 0.1

0

1

2

3

4

5

6

Quintil 1 Quintil 2 Quintil 3 Quintil 4 Quintil 5

Po

rce

nta

je (

%)

Nacional Rural Urbana

Fuente: CEPAL, Banco de Datos de Encuestas de Hogares (BADEOHG).Promedio regional ponderado por población. Se incluyeron 9 países.ECLAC Household Survey Data Bank

Latin America: Proportion of indigenous and Afro-descendant population and rest of population without access to electricity, latest available year

0.6 0.9 1.1 1.2 1.6 2.23.6

12.6

22.0

26.7

0.3 0.2 0.3 0.6 1.0 1.30.4

4.6

13.8

10.1

0

5

10

15

20

25

30

Uruguay Brasil Perú México Chile AL Ecuador Bolivia Nicaragua Guatemala

Po

rce

nta

je(%

)

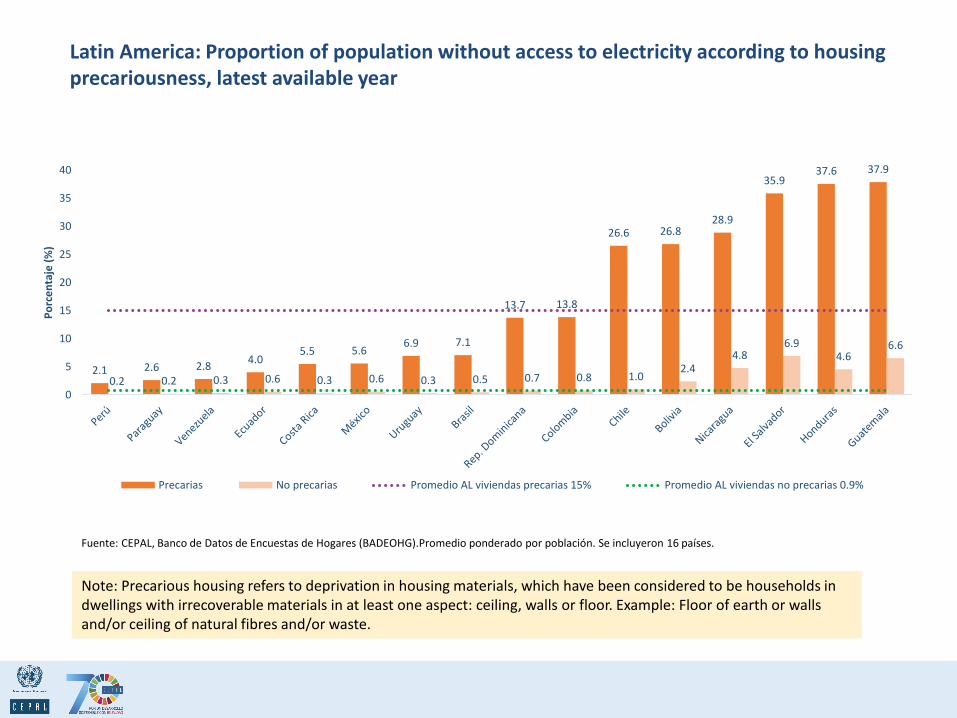

Latin America: Proportion of population without access to electricity according to housing precariousness, latest available year

Note: Precarious housing refers to deprivation in housing materials, which have been considered to be households in dwellings with irrecoverable materials in at least one aspect: ceiling, walls or floor. Example: Floor of earth or walls and/or ceiling of natural fibres and/or waste.

Fuente: CEPAL, Banco de Datos de Encuestas de Hogares (BADEOHG).Promedio ponderado por población. Se incluyeron 16 países.

2.1 2.6 2.84.0

5.5 5.66.9 7.1

13.7 13.8

26.6 26.828.9

35.937.6 37.9

0.2 0.2 0.3 0.6 0.3 0.6 0.3 0.5 0.7 0.8 1.02.4

4.86.9

4.66.6

0

5

10

15

20

25

30

35

40

Po

rce

nta

je (

%)

Precarias No precarias Promedio AL viviendas precarias 15% Promedio AL viviendas no precarias 0.9%

Energy Efficiency

Intensidad energética en base a la energía primaria en América Latina y el Caribe versusotras regiones (En MegaJoule/PIB)

Históricamente, la región ha tenido la menor intensidad energéticaa nivel mundial, pero también ha sido la que menos ha mejorado.

4.4 4.3 4.3 4.2 4.2 4.2 4.2 4.2 4.2 4.3 4.2 4.2 4.3 4.3 4.2 4.2 4.2 4.0 4.0 4.0 4.0 3.9 4.0 3.9 3.93.8

0

1

2

3

4

5

6

7

8

9

10

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Asia oriental y el Pacífico Europa y Asia central América Latina y el Caribe

América del Norte Miembros OCDE

Fuente: Comisión Económica para América Latina y el Caribe (CEPAL), en base a los datos del Global Tracking Framework Initiative

0%

20%

40%

60%

80%

100%

2006 2009 2012

Increasing number of countries with quantitative targets

Targets are expressed in different ways and relate to different part of the consumption: on total (primary )consumption (around 20%) , on final energy consumption (around 20%) , or end-use sectors (case of 60% of countries)

0%

20%

40%

60%

80%

100%

Primary Final consumptionEnd-use sectors Energy Suppliers

• Countries with quantitative targets

Source WEC surveys ( 85 countries, of which 10 in Latin America)

Primary and final intensity trends: case of Brazil

Source BIEE/EPE

Different trends as to the variation of primary and final intensity in Brazil depending on energy transformations and mainly the power sectorSince 1998, and especially since 2005, energy transformations contribute to increase the primary intensity due to the development of thermal power generation and biofuels production

-2%-2%-1%-1%0%1%1%2%2%3%3%

1990-1993 1993-1998 1998-2005 2005-2010

%/a

ño

Intensidad primária Intensidad final Transformación

El ROSE utilizará el conocimiento y la metodología empleada en el desarrollo del programa BIEE

Data-Mapper: sitio Web de la Base de datos para elaboración de Indicadores en EE

Sitio Web: https://www.cepal.org/es/proyectos/programa-biee-

base-de-indicadores-de-eficiencia-energetica

Base de datos ‘Data-Mapper’: http://www.biee-cepal.enerdata.eu/

ECLAC Project: The Regional Observatory on Sustainable Energies (ROSE)

BIEEEnergy

Efficiency

ECOSUDComplementarity

and Energy integration

Regional Technical Forum of

Energy Planners

Regional Political Dialogue on EE

Regional Observatory on Sustainable Energies (ROSE)

Energy Data in the form of Energy Indicators

General objective: To strengthen the national capacities of all Member States in Latin America and the Caribbean to design, implement and monitor sustainable energy strategies, plans and policies based on objective evidence.

Specific objectives:1 Strengthen the technical capacities of beneficiary countries to producerelevant and consistent data (e.g. social changes in access) to develop energy indicators.

2 Improve the capacity of beneficiary countries to design and implement evidence-based policies and action plans on sustainable energy.

One of ROSE's actions is to create spaces for political-technical dialogue in the region topromote efforts to achieve Agenda 2030 and SDG7.

3.6 Objectives of the "Regional Observatory on Sustainable Energy".

Reunión preparatoria del Foro - Río de Janeiro, EPE – marzo 6, 2018

REGIONAL TECHNICAL FORUM OF ENERGY PLANNERS

1er Foro Técnico de Planificadores Energéticos – Bogotá, Ministerio de Energía y Minas de Colombia, 5-junio-2018

2do Foro Técnico de Planificadores Energéticos – Santiago en CEPAL, 30

octubre 2018

ENERGY PRODUCTION - GENERATION [GWh]

BASE

RE

RE + INT

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

Biomass

Wind

Solar

Ocean

Nuclear

Mini-Hydro

Hydro

Geothermal

Gas

FuelOil

Diesel

Coal

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

Biomass

Wind

Solar

Ocean

Nuclear

Mini-Hydro

Hydro

Geothermal

Gas

FuelOil

Diesel

Coal

CONTINENTAL LATIN AMERICA

Renewable Energy Share in % All Hydro (<30% included)

Description:

Horizon:Units:Scenarios:

Notes:

Latin America Electricity Production Mix Forecast15 years [2018-2032]Annual GWh (lossless)-BASE-RE: Renewable Energy -RE+INT: Interconnected and RE ECOSUD update. Central America + Mexico from GoF

2018

2032

74%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

Biomass

Wind

Solar

Ocean

Nuclear

Mini-Hydro

Hydro

Geothermal

Gas

FuelOil

Diesel

Coal

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

Biomass

Wind

Solar

Ocean

Nuclear

Mini-Hydro

Hydro

Geothermal

Gas

FuelOil

Diesel

Coal

TOTAL COSTS: Production + Investment

CONTINENTAL LATIN AMERICA

Description:

Horizon:Units:

Notes:

LATIN AMERICA production and investment costs15 years [2018-2032]Annualized Capital and Operational Costs in Million USDReal annualized costs. Regional discount rate of 8% used for NPV calculations. WACC, economic life project specific. 2016 USD used for all input costs projections

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

MX

CA

BR

SA

SA represents South America

excluding Brazil

BASE

Total Costs

B$852

Generation Costs

FO&M CostTransmission

Build Cost

Annualized total costs in MUSD [M$]

Annualized

Build Cost

BASE

RE-optimistic

Generation Costs

FO&M CostTransmission

Build Cost

Annualized

Build Cost

Generation Costs

FO&M CostTransmission

Build Cost

Annualized

Build Cost

B$466.1 B$203.4

B$0.91B$181.6

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2018

20

19

20

20

20

21

2022

2023

2024

2025

2026

20

27

20

28

20

29

2030

2031

2032

MX

CA

BR

SA0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

MX

CA

BR

SA

RE

Total Costs

B$817

B$316.7 B$303.4

B$ 2.3B$194.6

RE

B$310.7 B$301.5

B$195.4 B$4.61

Re + INT

Total Costs

B$812

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

MX

CA

BR

SA

RE + INT

ECLAC Partners for Sustainable Energy

THANKS