Employee Benefits in Captives. Speakers: George O’Donnell, Senior Vice President, Benefit Funding...

56

Employee Benefits in Captives

-

Upload

juliet-henderson -

Category

Documents

-

view

224 -

download

0

Transcript of Employee Benefits in Captives. Speakers: George O’Donnell, Senior Vice President, Benefit Funding...

Employee Benefits in Captives

Speakers:• George O’Donnell, Senior Vice President, Benefit Funding

Strategies, Aon Consulting• Brian Quinn, Director & Chief Underwriting Officer, Granite

Management Limited• Molly Seaburg, Risk Manager – Microsoft Business Risk

Management, Microsoft Corporation• Christina Reisinger, Director Risk Management, Cephalon, Inc.

Moderator:• Philip Barnes, Managing Director, Aon Insurance Managers

(Bermuda) Ltd.

Where We Are Today:

Overview of US and Global Captive Benefits Activity

Types of EB Risks:

• Death/Term Life

• Disability / Income Replacement

• Personal Accident / Accidental Death & Dismemberment

• Medical / Active Health

• Post-Retirement Health

• Risk riders of pension policies in some Continental European countries, e.g. Germany, Belgium, Switzerland, Denmark

Employee Benefit Risks – What are They?

U.S. Activity (Dept. of Labor Approval)

– ADM (2)– AGL Resources– Alcoa– Alcon– Astra Zeneca (2)– Banner Health– Cephalon– Coca-Cola– ConAgra Foods– Deutsche Post/DHL

– Heinz (2)– International Paper– Memorial Sloan Kettering– Microsoft– NiSource (2)– SCA– Sun Microsystems– UTC– Wells Fargo– YKK

Growth in U.S. / Dept. of Labor Approvals

x

x

x x

x x

x x x

x x x

x x x

x x x

x x x

x x x

x x x

x x x

x x x x

x x x x

x x x x x

x x x x x

x x x x x

x x x x x x

x x x x x x

x x x x x x x

x x x x x x x

x x x x x x x x

x x x x x x x x

x x x x x x x x 2000 01 02 03 04 05 06 07 08 09 10

Between 2005 and 2010, over 300% increase in cumulative number of DOL-approved transactions

x

Global Benefits Activity

• Currently at least 30 companies have reinsured global employee benefit programs through captives

• Virtually all such arrangements are in non-US captive domiciles

• Multi-national pooling is the precursor to “captivation”

Why?

The Reasons Behind the Transactions

The risk profile of employee benefits is characterised by high and stable frequency with low average severity

…146146

10 44 78 112 146

84.84% 13.61% 1.55% 50 66

10 44 78 112 146

Mean=39.99965

Distribution for Aggregate Losses

0.000

0.010

0.020

0.030

0.040

0.050

0.060

Mean=39.99965

10 44 78 112 146

… and a CAT-tail …

Rational for EB in Captive

Implying that for most corporations employee benefit risk can be fully retained . . .

. . . Except for the CAT-tail

The Numbers Can Sometimes be Compelling . . . An Example

Most Recent Experience

April 2010

Total (All Lines)

Annual Premium

Projected Claims

Projected L/R

% Insurer Fees

Total

% CaptiveRetention

$ Retention toCaptive

6,371227

3,705,560

58.2%

19.3%

77.5%

22.5%

1,434,327

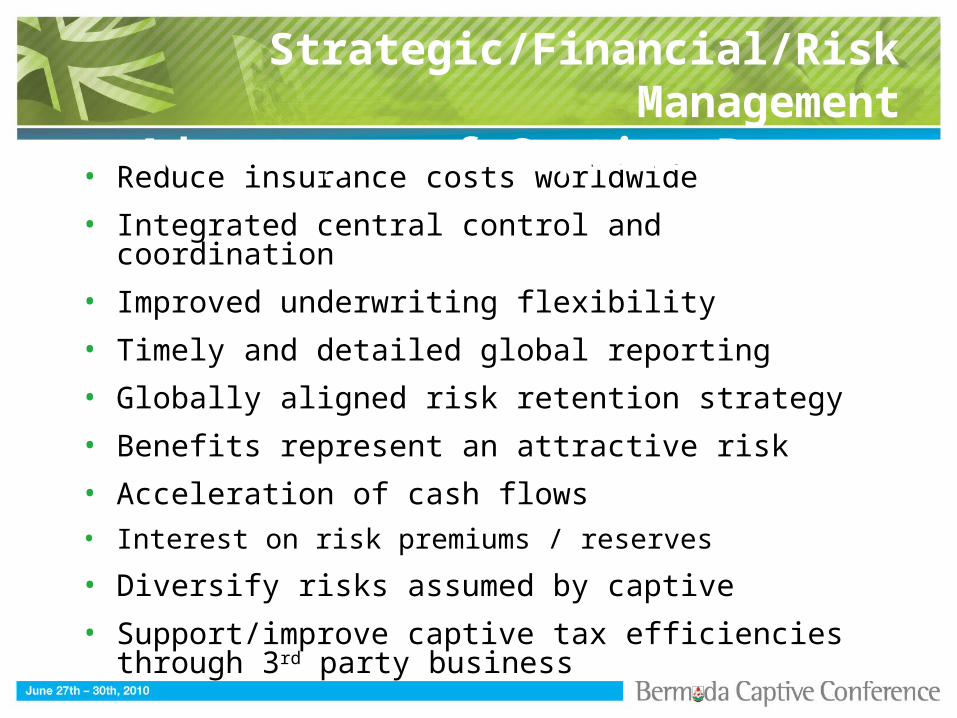

• Reduce insurance costs worldwide

• Integrated central control and coordination

• Improved underwriting flexibility

• Timely and detailed global reporting

• Globally aligned risk retention strategy

• Benefits represent an attractive risk

• Acceleration of cash flows

• Interest on risk premiums / reserves

• Diversify risks assumed by captive

• Support/improve captive tax efficiencies through 3rd party business

Strategic/Financial/Risk ManagementAdvantages of Captive Program

Structure

How Captive Benefits Arrangements Work

Employer

Captive

Benefit Claims

Direct Premium

Reinsurance Premium

Reinsurance Claims

Employees

Dividends

Fronting Carrier

U.S. Captive Transactions

U.S. Dept. of Labor Requirements

CAPTIVE REQUIREMENTS

• US nexus

• Financially sound

• Authorized to reinsure benefits

PROTECTION OF PARTICIPANTS

• Indemnity reinsurance (front is primarily liable)

• Fronting carrier has Best’s “Excellent” rating

• Immediate and objectively determinable benefit enhancement

• Notification to participants

REASONABLENESS OF THE TRANSACTION

• Reasonable premiums

• Similar to formulae used by other carriers

• No commissions paid by plan

INDEPENDENT CERTIFICATION

• Independent fiduciary must review and approve the transaction

Examples of Benefit Plan Enhancements

Benefit Enhancements - - A Sampling of the Possibilities

• Beneficiary Assistance / Counseling

• Travel Assistance Program

• Will preparation and legal services - - access to on-line will and forms, plus discounted legal fees

• Employer-paid plan providing benefit up to three times the basic life insurance benefit, subject to a schedule of amounts

• Portability provision for life coverages - - continue at group rates upon employment termination

• Improve Accelerated Death Benefit, e.g., from 50% ($100,000 max) to 75% ($250,000 max), 6 mos. to 12 mos.

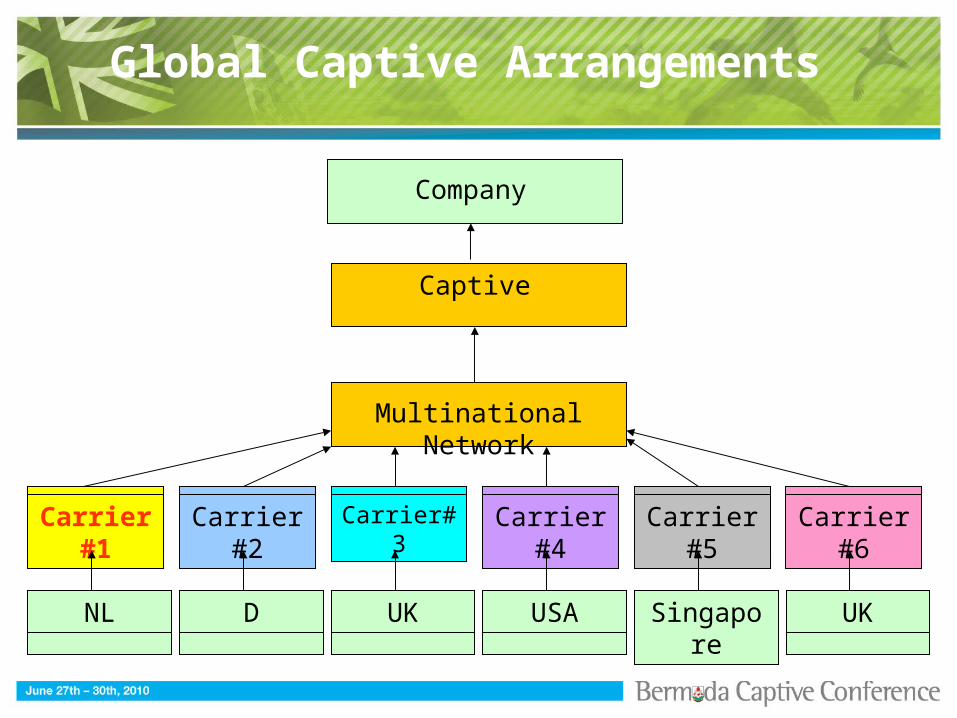

Multinational Network

Captive

UK

Carrier#3

USA

Carrier#4

Singapore

Carrier#5

UK

Carrier#6

D

Carrier#2

NL

Carrier#1

Company

Global Captive Arrangements

International Employee BenefitsThe GM Story

Brian Quinn - GRANITE Management Limited

General Motors - 2010 HighlightsGeneral Motors - 2010 Highlights

Successfully transitioned to four brands in North America, with combined sales of Chevrolet, Buick, GMC, and Cadillac surpassing sales with eight brands a year ago

Announced investments of more than $2.3 billion in the U.S. and Canada, adding more than 9,100 jobs

Paid back the loan portion of support from the U.S. and Canadian governments

Achieved first quarterly profit as a new company and positive operating cash flow, both important milestones

Making progress in restructuring operations in Europe Opel/Vauxhall’s Plan for the Future has reached a significant

milestone with a European-wide tentative labor agreement GMIO, continuing its strong growth, recently recorded its 1

millionth sale this year in China, more than two months earlier than its 1 millionth sale last year

The new GM has a cleaner, healthier balance sheet Solidly positioned in China, Brazil, and other growing markets

General International Limited (GIL)General International Limited (GIL)

General Motors’ Bermuda domiciled reinsurance captive

GIL Mission Statement

“The primary focus of GIL is to provide insurance and reinsurance services and savings/financial efficiencies to General Motors’ affiliates, employees and suppliers worldwide when corporate programs or local retentions are not viable options.”

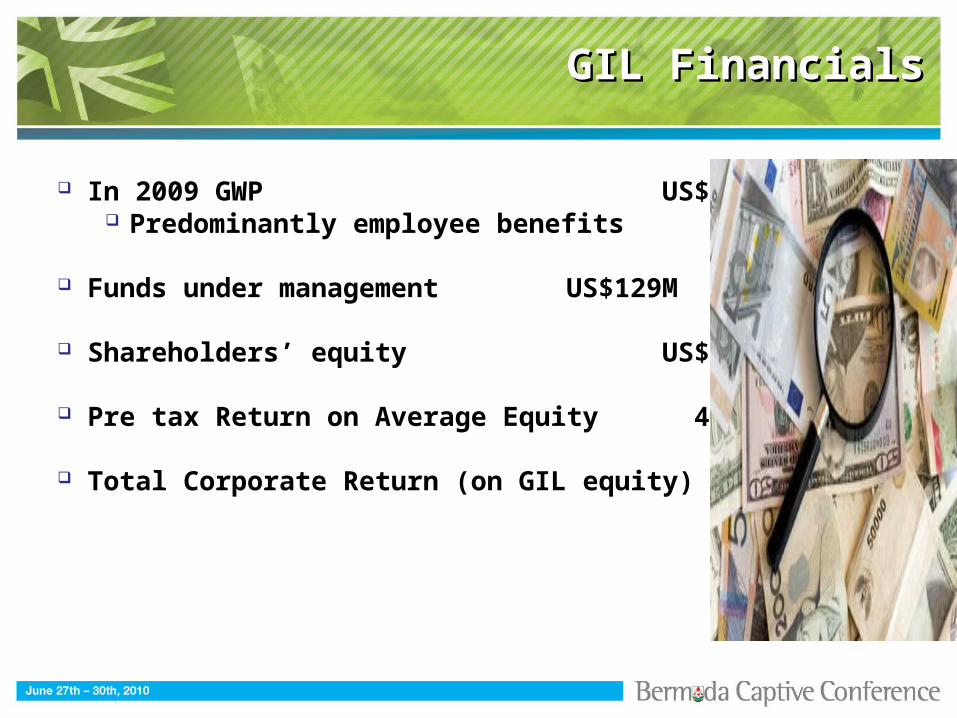

GIL FinancialsGIL Financials

In 2009 GWP US$ 90M Predominantly employee benefits

Funds under management US$129M

Shareholders’ equity US$ 70M

Pre tax Return on Average Equity 41.6%

Total Corporate Return (on GIL equity) 119.8%

The GM International Employee The GM International Employee Benefit (IEB) ProjectBenefit (IEB) Project

Captive reinsurance first considered in the late ’90s

3 passively managed multinational pooling arrangements

Scant knowledge of its global risk benefit exposures

Self-insured programs in the U.S.

Commenced the IEB project in 2000 Managed jointly by the captive and GM HR

GM Corporate Goals for IEB ProjectGM Corporate Goals for IEB Project

Ensure that GM units are paying appropriate premiums for level of claims incurred

Monitor all costs charged to GM units Reinsure 100% of Employee Benefit programs

Improve financial efficiency Maximize investment returns Improve understanding of global programs

and exposures Stable source of “unrelated” premium

income per IRS

Insured Employee Benefit Funding Insured Employee Benefit Funding MechanismsMechanisms

Least Financially Efficient

Most Financially Efficient

Fully Stop Multinational Captive Self

Insured Loss Pooling Reinsurance Insurance

Managing The RiskManaging The Risk

Why take the “Risk” into the company Risk taken when benefit promise was made Need to “manage the risk”

Insurance companies will manage it for a price Captive reinsurance can manage and cap the cost No insurance company will subsidize a benefit

promise over time

Captive Reinsurance vs. the MarketCaptive Reinsurance vs. the Market

The GM program has always beaten the market Target premiums to equal claims plus admin cost

Why can units sometimes get cheaper quotes? Buy-in the risk but in time;

Price will increase to cover costs plus profit

Can’t units change every year to get cheapest quote Disruption to employees Budgeting uncertainty and volatility Market fatigue Loss of control Relationships

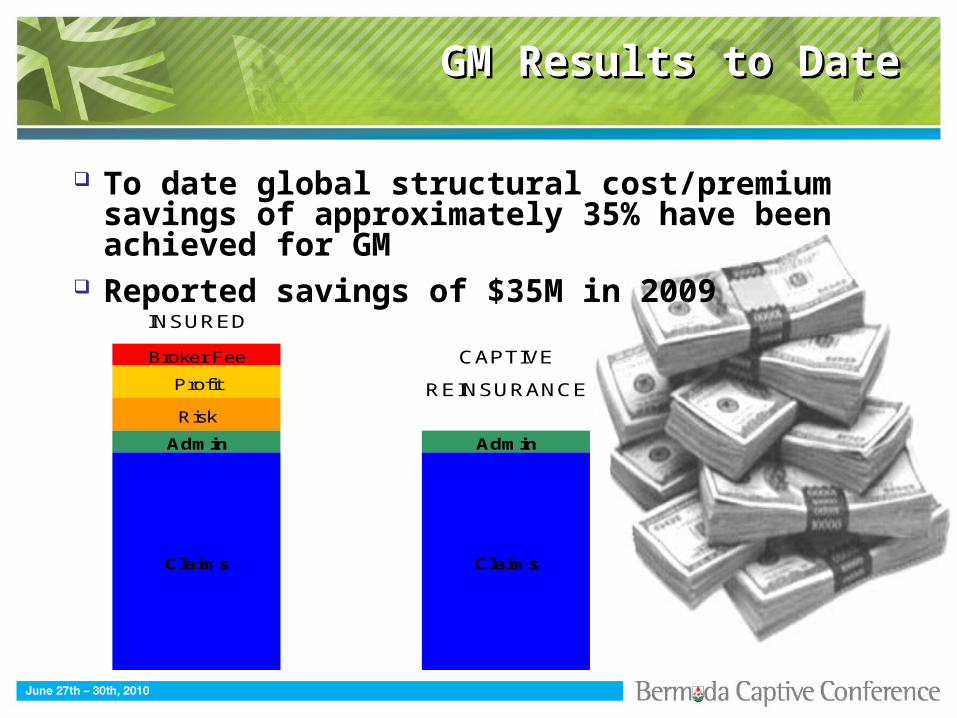

GM Results to DateGM Results to Date

To date global structural cost/premium savings of approximately 35% have been achieved for GM

Reported savings of $35M in 2009

INSURED

Broker Fee CAPTIVE

Profit REINSURANCE

Risk

Admin Admin

Claims Claims

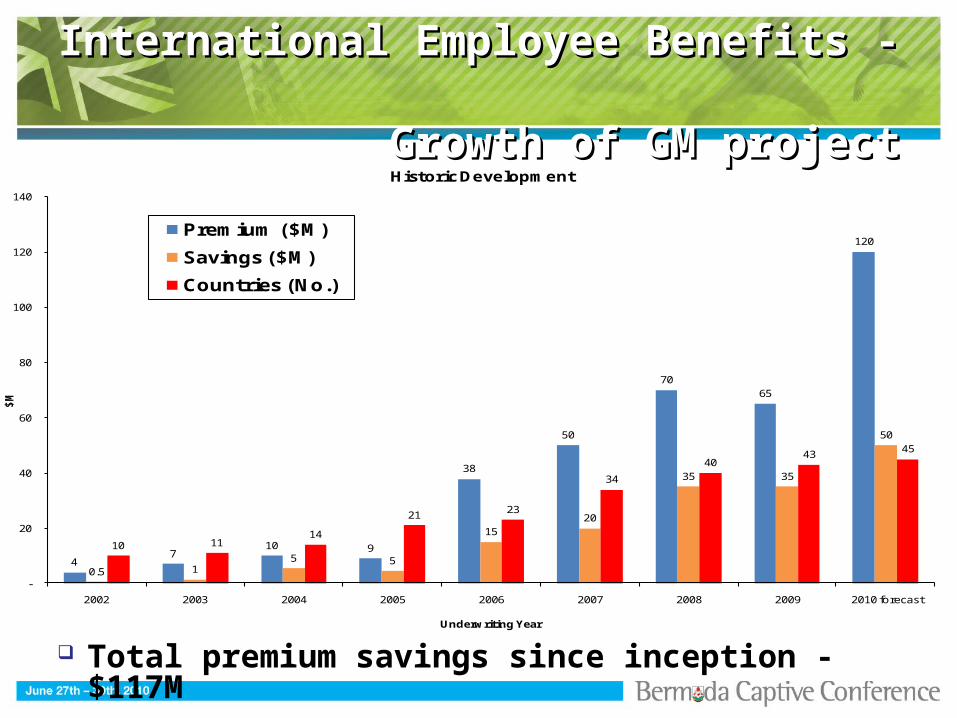

International Employee Benefits - International Employee Benefits - Growth of GM projectGrowth of GM project

47

10 9

38

50

7065

120

0.5 15 5

1520

35 35

50

10 1114

21 23

34

4043 45

-

20

40

60

80

100

120

140

2002 2003 2004 2005 2006 2007 2008 2009 2010 forecast

$M

Underwriting Year

Historic Development

Premium ($M)

Savings ($M)

Countries (No.)

Total premium savings since inception - $117M

Lessons learned by GMLessons learned by GM

Move quickly as there is no need to delay

Each country is different but the goal is the same

The amount of premium you think you have is probably understated

Need to gain confidence of local leadership

Question all frictional costs

Be creative and demand creativity from your global partners/fronting insurers

IEB Captive Reinsurance - AdvantagesIEB Captive Reinsurance - Advantages

Significantly reduced employee benefit cost

Enhanced knowledge and control of local programs

Superior corporate governance Central knowledge and control FAS reporting

Excellent stable source of captive business IRS requirements Captive metrics and IRR

Enhances relationship between HR and Finance divisions

What Next?What Next?

Captive reinsurance arrangements are merely the beginning

Shift focus from negotiating to claims management Analyze claims and identify abuses Implement controls to reduce/eliminate abuses

Unit HR and Finance departments responsible for risk/claim management Educate employees Analyze the big cost drivers (i.e. special clinics)

Microsoft CorporationMolly A. Seaburg

Risk Manager, SMSG

Agenda

• An overview of our company

• MSFT from the Risk Manager’s perspective

• What led us to decide to reinsure employee benefits to one of our captives

• The key stakeholders in the process, and how we addressed their respective concerns

• Our experience so far

• Our future plans for “captivating” benefit programs

Company Overview

• Microsoft Corporation is the worldwide leader in software services, and solutions that help people and businesses realize their full potential.– Founded in 1975 in Albuquerque, NM– Moved to Washington in 1979– Incorporated June 25, 1981– Currently employ >88,000 employees

worldwide• >53,000 in the US

– Currently have subsidiaries in 112 countries– Annual revenue for FY09 was $58.4 billion

Microsoft – Redmond Campus

Company Overview

• Microsoft Corporation – Where are we going?– Software – YES– Online Services

• Includes MS Exchange, Sharepoint, Amalga, Xbox Live, & Bing

– Windows Azure• Operating system for cloud computing

– Storage, computing and networking infrastructure services

– Accessibility that is easy and secure and accessible on any device from any location

– Kinect formally Project Natal for Xbox 360• Body recognition, sensors, verbal recognition

Microsoft from a Risk Manager Perspective

• MSFT From the Risk Manager’s Perspective– A great deal to contemplate with all different

risks– For Risk Management, this implies a

philosophy of the basics:• Risk ID, Assessment, Response,

Financing, & Monitoring

• Treasurer Challenge– What can Risk Management do to prolong the

life cycle of the MS dollar?– What can Risk Management do to increase

shareholder value?

Captive Centric Framework

• Microsoft’s captives were established and operated consistent with this philosophy– 3.5 captives

• Bermuda – est. 1998– Branch in VT – est. 2008

• Vermont – est. 2000• Arizona – est. 2008

• Why so many?

Benefits & Captives

• Benefits and Captives – How we got there– Foot in the door

• And so it began…– Internal Meetings with HR, Tax and LCA

(2008)– Commissioned feasibility analyses on big

picture– Re-evaluated – established timeline

• Finally decided in July 2009 to proceed with reinsuring Long-Term Disability (LTD) in the Bermuda branch

Stakeholders

• Key Internal Stakeholders / Issues & Answers– Human Resources

• Why does Risk want to do this? • How will this affect our relationship with our

current carrier? • How will this affect plan design? • How will this be communicated to

employees?• Will this mean more work for us?

Stakeholders

• Key Internal Stakeholders . . . (Cont’d)– Finance

• Capital requirements for reinsurance collateral?

• Letter of Credit, Reg 114 Trust, or Funds Withheld?

• Accounting?

Stakeholders

• Key Internal Stakeholders . . . (Cont’d)– Legal

• ERISA attorney briefings • Contract attorneys provided input on

reinsurance contract– Risk Management

• Coordination of events• Tracking of timeline and deliverables• Creating smooth transitions – being the

backstop

Stakeholders

• Key Stakeholders / Fronting Carrier– Commitment / cooperation of fronting carrier

greatly expedites the process– Prudential has extensive experience as a

fronting carrier, and was always committed to achieving success

– Carrier provides initial drafts of reinsurance agreements, which were reviewed / modified in response to comments by MSFT and its advisors

Stakeholders

• Key Stakeholders / Independent Fiduciary– Milliman has rendered fiduciary opinions in

several previous transactions– MSFT’s transaction was very similar to

preceding EXPO transactions, and did not pose any unusual issues

– A favorable fiduciary opinion was issued quickly

Experience So Far

• Our Experience so Far . . .– So far, so good

• Preliminary meetings with fronting carrier, treasury controller, captive managers, risk management

• Reporting – clean and timely– We’ll keep you posted

Our Future Plans

• Our Future Plans . . .– Review of additional lines of domestic benefits– Currently reviewing the reinsurance of our

international benefits into the captive• Multiple countries• Multiple lines• Timing – phases/waves

Cephalon, IncChristina Reisinger

Director Risk Management

Cephalon Story

• Cephalon is a global biopharmaceutical company dedicated to discovering, developing and bringing to market medications to improve the quality of life of individuals around the world. Since its inception in 1987, Cephalon has brought first-in-class and best-in-class medicines to patients in several therapeutic areas.

• Cephalon has the distinction of being one of the world's fastest-growing biopharmaceutical companies, now among the Fortune 1000 and a member of the S&P 500 Index, employing approximately 4,000 people worldwide. The company sells numerous branded and generic products around the world. In total, Cephalon sells more than 150 products in nearly 100 countries

A Decade of Solid Growth

*2010 estimates depict the midpoint of guidance ranges provided in press release issued 5/4/10.

Cephalon’s Captive Program

In addition to ERISA benefits Cephalon places the following programs in their Captive:

• Buy-Down Program Workers’ Compensation and Auto

• Worldwide Product Liability

• Quota Share Excess Liability

• Worldwide Clinical Trials

What About Federal Government Requirements?

• Pre-approval of DOL if benefit regulated by ERISA

• Fronting carrier must reinsure to captive

• Fronting carrier rated at least “A minus” by Best (DOL initially required “A”; the DOL has relaxed it position)

• Captive must have a US presence (either domicile or branch)

• HR involvement:– “Benefit enhancement” – Independent fiduciary review/approval– Employee Communication

“Benefit Enhancements”

• Fronting Carrier is generally able to work with you to “tweak” existing contracts

• Example– Accelerated life insurance death benefits (6 mos. – 12

mos.)– Tuition reimbursements in event of disability– Day care for dependent child in event of employee

disability– Other miscellaneous (travel aid, etc.)

Dealing With the “Tricky Stuff”…

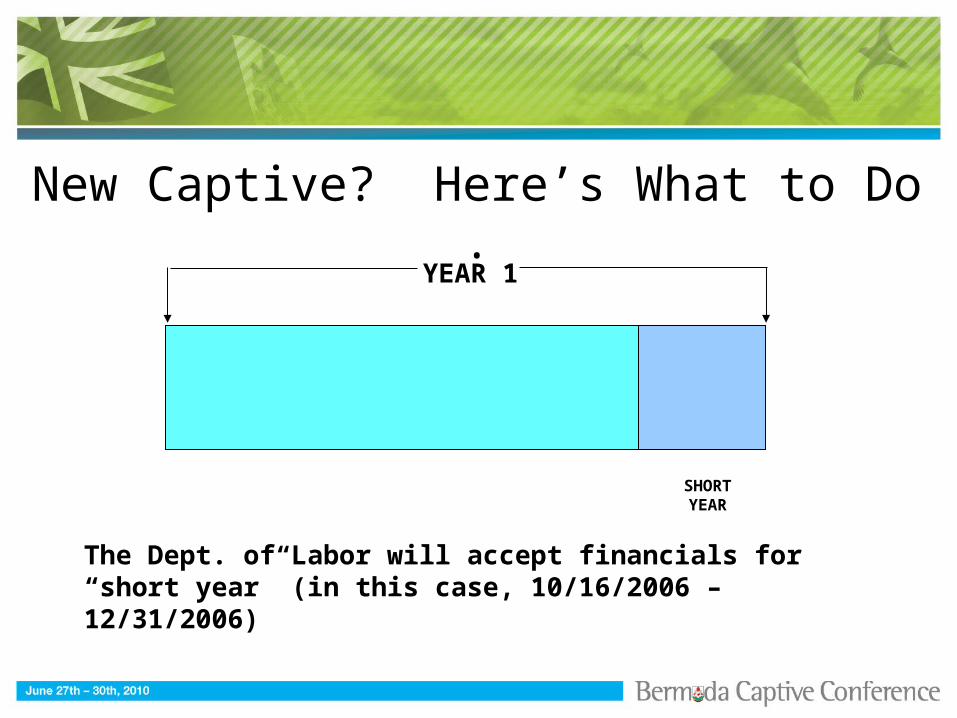

• Suppose you have a new captive (less than a year old)?– DOL requires financial statements for most recent

taxable year– How can this requirement be satisfied by a new captive?

• Suppose you have an offshore captive – what’s involved in establishing a US branch?

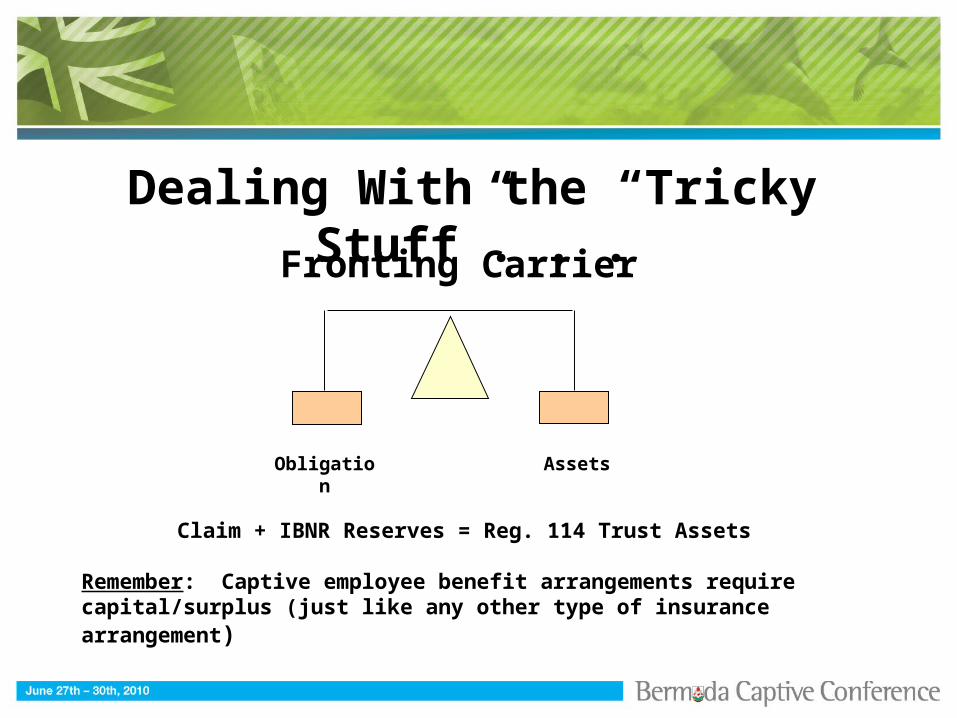

• The fronting carrier will require security (collateral) for the reinsurance obligation from the captive to the fronting carrier– What are the requirements, and how do I meet them?

• What to do about the DOL-mandated “benefit enhancements”?

New Captive? Here’s What to Do .

SHORT YEAR

The Dept. of Labor will accept financials for “short year” (in this case, 10/16/2006 – 12/31/2006)

YEAR 1

What if You Have an Offshore Captive?

VERMONT BERMUDA

• Patriot Act and related legislation– Additional due diligence, particularly if funding for branch

originates offshore– Form W-8 BEN– US financial institutions involved in this transaction are required to

“know their customers”

BRANCH CAPTIVE

Dealing With the “Tricky Stuff”. . .

Fronting Carrier

Obligation Assets

Claim + IBNR Reserves = Reg. 114 Trust Assets

Remember: Captive employee benefit arrangements require capital/surplus (just like any other type of insurance arrangement)

Any Questions?