Emerging Issues in the Functioning of the US Treasury … Issues... · Emerging Issues in The...

53

Emerging Issues in The Functioning of the US Treasury Market APRIL 2016 Promontory Financial Group, LLC 801 17th Street, NW, Suite 1100 | Washington, DC 20006 +1 202 384 1200 | promontory.com

Transcript of Emerging Issues in the Functioning of the US Treasury … Issues... · Emerging Issues in The...

Emerging Issues in The Functioning of the US Treasury Market

APRIL 2016

Promontory Financial Group, LLC 801 17th Street, NW, Suite 1100 | Washington, DC 20006 +1 202 384 1200 | promontory.com

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

Contents

I. Introduction ........................................................................................................ 2

II. Roles of the U.S. Treasury Market .................................................................... 4

A. Financing the U.S. Government ....................................................................................... 5

B. Execution of U.S. Monetary Policy ................................................................................... 8

C. High-Credit-Quality Investment ...................................................................................... 10

D. Store of Value and Liquidity ............................................................................................ 11

E. Interest-Rate Risk Management ..................................................................................... 14

F. Pricing Benchmarks and Macroeconomic Indicators ...................................................... 15

III. Market Characteristics Required to Support Participant Needs ..................... 17

A. Liquidity .......................................................................................................................... 18

B. Transparency .................................................................................................................. 29

C. Operational Reliability and Resilience ............................................................................ 32

D. Supportive Regulatory Framework ................................................................................. 38

Conclusion .......................................................................................................... 43

Bibliography ........................................................................................................ 44

This report was sponsored by the Securities Industry and Financial Markets Association (“SIFMA”). SIFMA and other institutions have contributed some of the information and materials included in it or used in its preparation. These institutions may be affected by changes to the structure or processes of the U.S. Treasury market, and may respond to the U.S. Department of the Treasury’s request for information (“RFI”) on it.

This report reflects Promontory’s views on matters that may be relevant to the RFI. Promontory believes the data and information furnished by others and incorporated into, or used as the basis of, this report are reliable, but it has not independently verified their accuracy. This report may also contain predictions or conclusions that are subject to inherent uncertainties; Promontory accepts no responsibility for actual results or future events.

This report is not to be reproduced, quoted, or distributed without Promontory’s prior written consent. This report may not incorporate all matters that a third party might consider pertinent or necessary to its evaluation. Promontory accepts no duty, responsibility, or liability to any person, and shall not be liable for any loss, damage, or expense, from using or relying upon this report.

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 2

I. Introduction The market for U.S. Treasury securities is unique among sovereign debt markets, and security markets more broadly, in its scale, liquidity, and interconnectedness with the global financial system. Treasury securities play central roles in the execution of U.S. monetary and fiscal policy and serve the investment and risk management needs of a heterogeneous complex of private-sector stakeholders, both domestic and international. Sustaining the high levels of market quality,1 efficiency, and operational functioning that are characteristic of the Treasury market is of paramount concern to both public authorities and private-sector participants.

Recent events of extreme market volatility — most notably the October 2014 “flash rally,” which was unrelated to any obvious fundamental macroeconomic factors — have prompted concerns that the functioning of the Treasury market has been impaired. A Joint Staff Report undertaken by a number of U.S. public agencies acknowledged the challenges in determining the root causes of the volatility events and thereby in designing compensatory measures and controls to protect the stability and quality of the Treasury market.2 Following the Joint Staff Report, the Department of the Treasury issued a request for information3 (“RFI”) on the U.S. Treasury market. In the RFI, the Department of the Treasury solicited views on such issues as market structure, market quality, transparency, and market data reporting. Based on the results of this RFI, the Department of the Treasury, and potentially other U.S. regulatory authorities, will consider introducing measures to improve market quality and the regulators’ visibility into market functioning.

In this paper, we seek to provide context for these developments and to explore a number of the major topics related to market quality. We cover two broad thematic areas:

• The extensive and wide-ranging roles of the U.S. Treasury market, emphasizing the importance of the market in serving the diverse needs of public and private stakeholders, including interconnectivity with the broader financial system. A key inference is that proposed changes to market structure or processes, along with exogenous developments impacting market participants, need to be examined not just for their efficacy in addressing the issues specifically targeted, but also for their secondary effects on overall Treasury market functioning and quality.

1 Key characteristics that define market quality include liquidity and transparency. Please see section III for further discussion. 2 “The U.S. Treasury Market on October 15, 2014,” U.S. Department of the Treasury, Board of Governors of the Federal Reserve System, Federal Reserve Bank of New York, Securities and Exchange Commission, and Commodity Futures Trading Commission (July 13, 2015). 3 “Notice Seeking Public Comment on the Evolution of the Treasury Market Structure,” U.S. Department of the Treasury, Federal Register (January 22, 2016).

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 3

• The market characteristics needed to support participants’ needs. We identify four characteristics of market quality with particular and current relevance to developments in the Treasury market — namely liquidity, transparency, operational reliability and resilience, and a supportive regulatory framework. We describe a number of aspects of the Treasury market as currently structured (including emerging challenges) that are relevant to proposals that have been made to enhance these characteristics.

Despite the recent volatility events, the U.S. Treasury market retains its reputation as the deepest and highest-quality securities market in the world. The long-standing cooperation among public- and private-sector stakeholders is important to responding appropriately to emerging challenges in order to ensure that the market continues to serve the many and diverse needs of its participants efficiently and sustainably.

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 4

II. Roles of the US Treasury Market The market for U.S. Treasury securities is the largest and most heavily traded of the world’s securities markets. In its scale and interconnectedness with the global financial system and real economy, the market is unique. Treasury securities play multiple cornerstone roles and serve the needs of a heterogeneous group of public- and private-sector stakeholders. As a result of this foundational position in the global economy, both the financial services industry and the regulatory authorities overseeing the Treasury market have a strong and common interest in sustaining the liquidity, price transparency and quality of execution that have historically been the hallmarks of the Treasury market. Moreover, it is important that the market sustain these vital characteristics under the broadest range of macro-economic and general financial market conditions.

A number of developments in recent years have brought both benefits and challenges to market functioning. First, the unprecedented level of issuance of Treasury securities after the financial crisis has increased the need for risk-absorbing capacity in the market in order to address the resulting larger portfolio-rebalancing needs. This has occurred at a time when the risk capacities and appetites of the traditional liquidity providers have been under pressure. As a second example, the growth of electronic trading has reduced execution costs dramatically over the past two decades. At the same time, however, electronic trading has introduced new risks as a result of increased execution speed, leading to the possibility that a counterparty, price, or operational disruption can propagate more rapidly through the market system. Finally, recent microstructural developments in the market — including the evolution of algorithmic trading, the entrance of new types of market participants, and the evolution of dealer-to-dealer and dealer-to-client platforms — arguably have not been accompanied to a corresponding degree by measures to provide transparency to the appropriate regulatory authorities on market functioning. This situation poses challenges to the authorities in designing and taking appropriate anticipatory measures to preserve market quality.

In this section, we explore a number of the key roles and uses of Treasury securities. We focus particularly on the following areas:

• Financing the U.S. government

• Execution of U.S. monetary policy

• High-credit-quality investment

• Store of value and liquidity

• Interest-rate risk management

• Pricing benchmarks and macroeconomic indicators

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 5

We describe how the market is fundamentally interconnected with the execution of public-sector fiscal and monetary policies and with the functioning of other markets. Throughout, we emphasize the fundamental interplay between the different quality characteristics of the market — liquidity, transparency, and operational reliability and resilience. In reviewing the many market roles and varied needs of participants, we note that public- and private-sector initiatives to preserve or maintain market quality need to account for the complex interlinkages that exist between the Treasury market and the broader financial system and economy. Proposed changes to market structure or processes, as well as exogenous developments impacting market participants, need to be examined not just for their efficacy in addressing the individual challenges described above, but also for their secondary effects on overall Treasury market functioning and quality.

A. Financing the US Government Treasury securities serve as the primary vehicle for financing the operations of the U.S. government and comprise the major portion of the total federal debt.4

Fiscal measures taken in the wake of the 2008 global financial crisis led to high issuance levels and to a historically high outstanding stock of Treasury securities, standing at approximately $13.2 trillion at the end of 2015.5

GROWTH IN MARKETABLE DEBT Total outstanding as of December 2015: $13.2 Trillion

Source: U.S. Treasury

4 Treasury Bulletin, U.S. Department of the Treasury (March 2016). 5 Ibid.

2

4

6

8

10

12

14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Trill

ions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 6

Net issuance levels have now moderated, as stimulus measures have been scaled down. Nevertheless, total gross issuance, covering ongoing deficit requirements and rollover of maturing debt, remains elevated by historical standards.

ISSUANCE OF US TREASURY SECURITIES

Source: U.S. Treasury

In managing the issuance of Treasury securities, the Department of the Treasury’s stated policy goal is to finance government borrowing needs at the lowest cost over time.6 Success in executing this policy clearly requires that Treasury securities remain an attractive asset class for the widest possible range of investors and that the functioning of the Treasury’s primary and secondary markets remains efficient and resilient under the broadest domestic and international macroeconomic circumstances. To these ends, the Department of the Treasury and the Federal Reserve (the latter as the government’s fiscal agent) have long supported the development of Treasury securities products and primary and secondary market infrastructures. Such measures as the introduction of “regular and predictable” auctions in the 1970s; the development of the primary-dealer system; and the introduction of new products such as STRIPS in the 1980s, Treasury inflation-protected securities (“TIPS”) in the 1990s, the Treasury Automated Auction Processing System (“TAAPS®”), and, most recently, floating-rate securities — have all underpinned the fundamental role of the Treasury market in the domestic and global financial systems and the status of Treasury securities as the low-risk asset class of choice among virtually all investor types.7

6 “Debt Management Overview and Quarterly Refunding Process,” U.S. Department of the Treasury (September 17, 2015). 7 Kenneth D. Garbade, “The Emergence of ‘Regular and Predictable’ as a Treasury Debt Management Strategy,” Federal Reserve Bank of New York Economic Policy Review (March 2007).

-200

0

200

400

600

800

1,000

1,200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ions

Gross Issues Net Cash Raised

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 7

COMPOSITION OF US TREASURY SECURITIES Total outstanding as of December 2015: $13.2 Trillion

Source: U.S. Treasury

Crucial to the risk-free status and attractiveness of Treasury securities is the maintenance of a resilient, deep, and liquid secondary market. Liquidity and resiliency in the secondary market are major focuses of this paper. We describe the recent evolution of these aspects of the secondary market in the next section. However, in connection with the Department of the Treasury’s goal of funding the government at the lowest cost over time, it is worth noting here that there is evidence that investors are prepared to pay a premium for liquidity and operational reliability, so that the execution and settlement of transactions in Treasury securities can be assured in the size and with the immediacy required.8 Changes to regulation, market infrastructure, or market practices in response to external influences, such as macroprudential requirements or technology developments, therefore need to be crafted to ensure that Treasury securities’ fundamental attractiveness to investors is maintained or enhanced.

8 Francis A. Longstaff, “The Flight-to-Liquidity Premium in U.S. Treasury Bond Prices,” Journal of Business (2004); and Stefan Nagel, “The Liquidity Premium of Near-Money Assets,” Bank for International Settlements (September 2014).

11%

64%

13%

9%

3%

Bills

Notes

Bonds

TIPS

FRNs

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 8

B. Execution of US Monetary Policy9 The primary mandate of the Federal Reserve is to foster maximum employment and stable prices.10 The Federal Reserve uses a range of monetary policy tools in pursuit of this mandate, and adapts the design of such tools over time to prevailing economic and market conditions. These tools include short-term and long-term measures, the most notable being open market operations (“OMOs”), bank reserve requirements, and the discount-window facility.11 For the purposes of this paper, we focus specifically on OMOs, since these are largely conducted through the Treasury market or with Treasury securities as collateral.

OMOs can be conducted on either a permanent or temporary basis. Permanent OMOs consist of the outright purchase or sale of securities, while temporary OMOs consist of the purchase of securities under agreements to resell or vice versa (repos and reverse repos). These operations allow the Federal Reserve to add or drain funds from the banking system, so as to influence short-term interest rates and, in particular, to adjust the federal funds rate to the targets set by the Federal Open Market Committee. Outright purchases or sales of medium- and long-term debt can also be used to influence longer-term interest rates.

Temporary OMOs were used on an almost daily basis in the years before the financial crisis as the primary tactical monetary-policy tool to keep the federal funds rate close to target.12 In the aftermath of the crisis, the Federal Reserve has used permanent OMOs as part of a number of large-scale asset purchase programs to ease monetary conditions and thereby provide substantial stimulus to the real economy. These securities purchases have led to a substantial increase in the Federal Reserve’s System Open Market Account (“SOMA”).

9 “Quarterly Report on Federal Reserve Balance Sheet Developments,” Board of Governors of the Federal Reserve System (March 2016). 10 “Monetary Policy and the Economy,” Board of Governors of the Federal Reserve System (2013); and “Open Market Operations,” Federal Reserve Bank of New York (August 2007). 11 “Quarterly Report on Federal Reserve Balance Sheet Developments,” Board of Governors of the Federal Reserve System (November 2012). 12 “Credit and Liquidity Programs and the Balance Sheet,” Board of Governors of the Federal Reserve System (December 2015).

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 9

FEDERAL RESERVE HOLDINGS OF US TREASURY SECURITIES Total holdings as of December 2015: $2.5 Trillion

Source: Federal Reserve System

Temporary OMOs have been used much less frequently during the post-crisis period.13 However, a resumption of temporary OMOs is possible as monetary conditions normalize over the coming years, and the Federal Reserve has continued to ensure in particular that the reverse-repo OMO mechanism remains available as a means of an anticipated gradual rate tightening. Indeed, the first official rate rise in almost a decade, in December 2015, was effected through a combination of overnight and term-reverse repos.14

Although the Federal Reserve has the authority to transact in a range of assets — including federal agency debt — for the conduct of monetary policy, Treasury securities remain the most widely used asset in both permanent and temporary OMOs. The Federal Reserve therefore places great reliance on the existence of a deep and liquid Treasury market to ensure that operations can be conducted on a timely basis, in scale, and with predictable transmission mechanisms to the broader financial system and ultimately to the real economy. The unique characteristics of the Treasury market provide the Federal Reserve with flexibility in implementing monetary policy along a number of dimensions. First, given the depth and liquidity of the market, the Federal Reserve can conduct OMOs in readily available instruments of various durations. Second, the breadth of the market along the entire yield curve also allows the Federal Reserve flexibility in targeting its operations at different points in the yield curve. Lastly, the benchmark pricing role of the U.S. Treasury market, and its corresponding integration with other interest rates, allows Federal Reserve OMOs to influence interest rates throughout the economy to a greater degree than they would be able to with less integrated securities or with less integrated markets.

13 Simon Potter, “Implementation of Open Market Operations in a Time of Transition” (September 25, 2014). 14 “Quarterly Report on Federal Reserve Balance Sheet Developments,” Board of Governors of the Federal Reserve System (March 2016).

0

500

1,000

1,500

2,000

2,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 10

The primary dealers have historically been the Federal Reserve’s main counterparties for the execution of OMOs. In the past five years, the Federal Reserve has expanded the eligible counterparties for certain limited types of OMOs to include a number of government-sponsored enterprises (“GSEs”), banks, and domestic money-market funds. However, the primary dealers remain central to the general operation of monetary policy.15 For that reason, the Federal Reserve has a significant interest in maintaining an active and resilient core primary-dealer community.

C. High-Credit-Quality Investment Treasury securities comprise the largest global asset pool that can be considered to carry virtually no credit risk. Treasury securities are backed by the full faith and credit of the U.S. government — an attribute whose credibility is based on the general taxing powers of the federal government, the relative political stability of the U.S., the size of the U.S. economy, and the historical record of no defaults on the federal debt.

SIZE OF US SOVEREIGN DEBT MARKETS AS COMPARED TO OTHER SOVEREIGN DEBT MARKETS U.S. debt figure includes non-marketable debt; all figures in U.S. dollars

Source: Bank for International Settlements

As a consequence, Treasury securities are typically the asset of choice for investors with limited risk appetite. Indeed, during times of economic crisis or elevated financial risk, Treasury securities are regarded as the ultimate safe-haven investment, and there have

15 Ibid.

8,618

2,685

8,419

15,834

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000

Eurozone

United Kingdom

Japan

United States

Billions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 11

historically been many instances of a flight to quality, when investors have moved out of riskier investments into Treasury securities during market crises.16

While the low credit risk of Treasury securities is the ultimate source of their safe-haven status, investors’ ability to transact efficiently and in large size, even under crisis conditions, is critical to this status. Treasury securities must therefore enjoy a strong secondary market, with dealers having ample market and liquidity risk capacity to meet investor needs. Market infrastructures also need to be robust to ensure efficient operation even under extreme conditions. They must, moreover, have mechanisms ensuring that purchases and sales of Treasury securities minimize transaction and counterparty credit risks.

D. Store of Value and Liquidity Closely related to the low credit-risk profile of Treasury securities is their use as a highly liquid store of value. Most market participants consider Treasury securities to be near cash equivalents, with an ability to be converted into cash virtually immediately when needed. The uses of Treasury securities as a close substitute for cash are manifest across a wide range of holders and on a global scale. Non-U.S. official currency-reserve managers are estimated to be one of the largest groups of holders, with $4 trillion of official foreign holdings as of December 2015.17 The depth of the Treasury market is therefore closely tied to the U.S. dollar’s status as the most widely accepted reserve currency.

OFFICIAL FOREIGN HOLDINGS OF US TREASURY SECURITIES Total holdings as of December 2015: $3.9 Trillion Includes notes and bonds over 1 year in original term to maturity

Source: U.S. Treasury

16 Ricardo J. Caballero and Pablo Kurlat, “Flight to Quality and Bailouts: Policy Remarks and a Literature Review,” MIT Department of Economics Working Paper (October 2008). 17 “Portfolio Holdings of U.S. and Foreign Securities,” U.S. Department of the Treasury.

0 500

1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 12

The $2.2 trillion U.S.-dollar repo market, 60% of which is based on the use of Treasury securities as collateral, is essentially predicated on the notion that Treasury securities are effectively cash equivalents.18

PRIMARY-DEALER REPO AND REVERSE REPO Outstanding by security as of December 2015

Source: Federal Reserve Bank of New York

TOTAL PRIMARY-DEALER REPO OUTSTANDING All securities outstanding as of December 2015: $2.2 Trillion

Source: Federal Reserve Bank of New York

18 Viktoria Baklanova, Adam Copeland, and Rebecca McCaughrin, “Reference Guide to U.S. Repo and Securities Lending Markets,” Federal Reserve Bank of New York (December 2015).

0 200 400 600 800

1,000 1,200 1,400

ABS Corporate Equities Federal Agency & GSE

Agency MBS Other US Treasuries TIPS

Bill

ions

Repos Reverse Repos

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 13

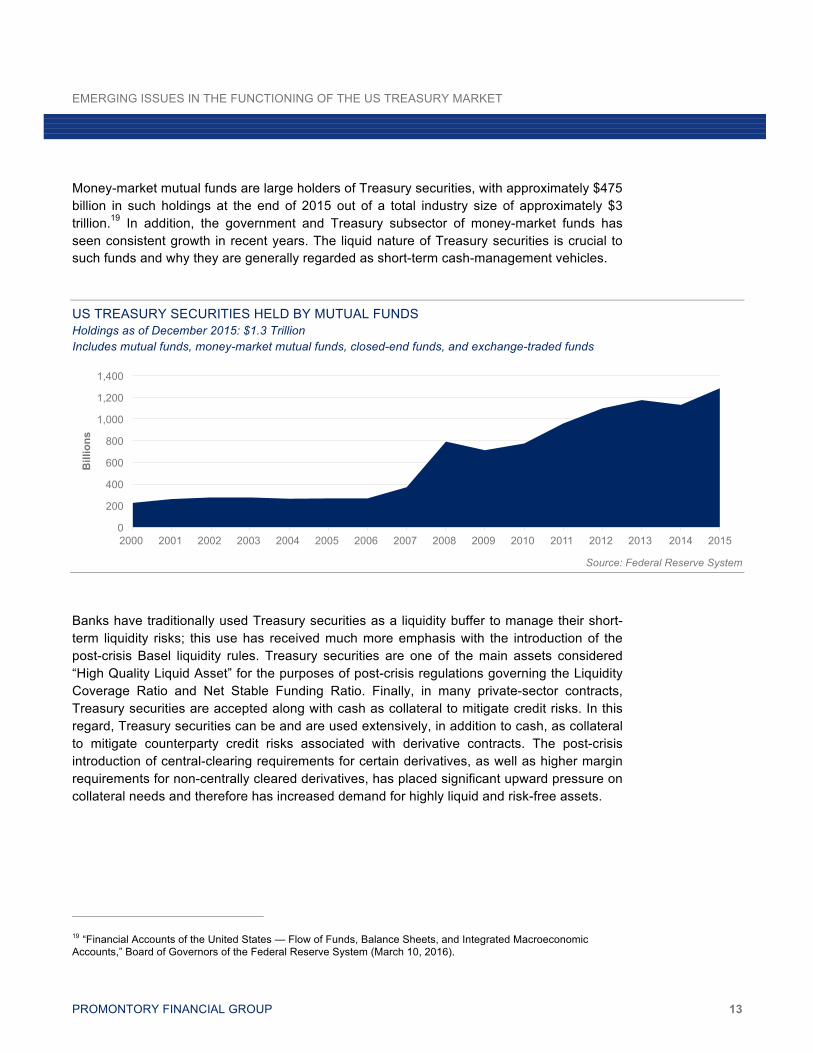

Money-market mutual funds are large holders of Treasury securities, with approximately $475 billion in such holdings at the end of 2015 out of a total industry size of approximately $3 trillion.19 In addition, the government and Treasury subsector of money-market funds has seen consistent growth in recent years. The liquid nature of Treasury securities is crucial to such funds and why they are generally regarded as short-term cash-management vehicles.

US TREASURY SECURITIES HELD BY MUTUAL FUNDS Holdings as of December 2015: $1.3 Trillion Includes mutual funds, money-market mutual funds, closed-end funds, and exchange-traded funds

Source: Federal Reserve System

Banks have traditionally used Treasury securities as a liquidity buffer to manage their short-term liquidity risks; this use has received much more emphasis with the introduction of the post-crisis Basel liquidity rules. Treasury securities are one of the main assets considered “High Quality Liquid Asset” for the purposes of post-crisis regulations governing the Liquidity Coverage Ratio and Net Stable Funding Ratio. Finally, in many private-sector contracts, Treasury securities are accepted along with cash as collateral to mitigate credit risks. In this regard, Treasury securities can be and are used extensively, in addition to cash, as collateral to mitigate counterparty credit risks associated with derivative contracts. The post-crisis introduction of central-clearing requirements for certain derivatives, as well as higher margin requirements for non-centrally cleared derivatives, has placed significant upward pressure on collateral needs and therefore has increased demand for highly liquid and risk-free assets.

19 “Financial Accounts of the United States — Flow of Funds, Balance Sheets, and Integrated Macroeconomic Accounts,” Board of Governors of the Federal Reserve System (March 10, 2016).

0

200

400

600

800

1,000

1,200

1,400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 14

BANK HOLDINGS OF US TREASURY SECURITIES Holdings as of December 2015: $507 Billion Includes U.S.-chartered depository institutions, foreign banking offices in the U.S., and banks in U.S.-affiliated areas

Source: Federal Reserve System

The existence of a deep, robust, and resilient secondary Treasury market, where pricing reflects fundamental value, is critical to the use of Treasury securities as a store of value. Ample trading liquidity is required under even normal conditions to be able to respond to investors’ needs to store and redeem the “cash value.” Under crisis conditions, when the maintenance of value is most critical, the market needs to have sufficient capital to continue to function efficiently and offer protections against operational and counterparty failures.

E. Interest-Rate Risk Management A wide range of market participants — including bank portfolio and asset managers, fixed-income and swaps dealers, bond underwriters, and mortgage bankers and servicers — rely on Treasury securities to actively assume interest-rate risk or to manage the rate risk inherent in their business activities. Each of these participants will have a unique risk profile — by term and duration, scale, and variability. Collectively, they rely on the availability of Treasury securities across an extensive term structure for their investment and hedging needs.

The deep liquidity in the Treasury market allows bond portfolio managers to actively adjust their interest-rate risk rapidly to match their investment objectives, in response to macroeconomic events and other external developments. Fixed-income dealers and underwriters use Treasury securities to hedge their overall interest-rate risk exposures arising from inventory holdings or new issue commitments in corporate and asset-backed securities. Similarly, interest-rate derivative dealers also manage their rate risk, at least in part, through the Treasury market. Dealers’ hedging needs — for example when pricing a new bond issue — can be both large and very immediate in nature, and so dealers depend on a sizeable and rapid risk-absorbing capacity in the Treasury market for execution. Mortgage servicers have also historically been sizable participants in the market, using medium- and long-term

0

100

200

300

400

500

600

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 15

Treasury securities to hedge the linear component of interest-rate risk arising from their mortgage-prepayment exposures.

Since the underlying businesses of many of the above institutions relate to other markets and instruments, they often view the Treasury market as part of the supporting infrastructure of their business and so are concerned about the cost efficiency and resilience of execution in Treasury securities. Trading liquidity and interest-rate risk absorption capacity are therefore key considerations in using Treasury securities, particularly with the increasing prevalence of liquid rate management alternatives such as interest-rate swaps.

F. Pricing Benchmarks and Macroeconomic Indicators Since Treasury securities are assumed to be virtually free of default risk, tradable in a deep and highly liquid market, and regularly issued along a broad maturity spectrum ranging from 13 weeks to 30 years, their yields serve as benchmark risk-free rates, directly or indirectly, for pricing and valuation of virtually all U.S.-dollar-denominated fixed-income securities and derivatives, including corporate bonds, and mortgage- and asset-backed securities. Treasury rates are used widely as reference rates in a wide range of commercial and consumer financial products and contracts, and serve as an input, directly or indirectly, for the valuation bases for retirement and insurance plans. Treasury rates thus influence pricing and valuation throughout the financial system.

The level and shape of the Treasury yield curve are used by the public and private sector as key indicators of macroeconomic and financial market conditions and expectations. The relative value of TIPS to fixed-coupon Treasury securities is also used as an indicator of future inflationary expectations. Thus, Treasury rates are a significant input into the development of macroeconomic and monetary policy, as well as in private-sector investment and business decisions.

For Treasury securities to function in this benchmark role, it is critical that pricing in the Treasury market reflect the perceived underlying value at each maturity across the yield curve. In particular, pricing should not be subject to idiosyncratic volatility over short or long time scales. To achieve this pricing quality, the Treasury market should include a wide range of participants, so that price formation indeed reflects a representative sampling of economic interests. Moreover, there should be ample market depth, so that pricing is not unduly influenced by temporary imbalances of supply and demand. Relatedly, to the extent that benchmark pricing is in turn driving interest-rate hedging decisions, the benchmark securities need to be tradable in corresponding size to the hedging requirements, without materially altering the benchmark price. Indeed, recent regulatory guidance for the establishment of

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 16

financial benchmarks emphasizes the need for depth and quality in the underlying market in which the benchmarking instruments are transacted.20

Conclusion The quality of the Treasury market is a fundamental underpinning of the global financial and economic system. Measures to ensure the continued quality of the market need to be calibrated and adapted to this unique and cornerstone nature — to ensure that they resolve the immediate challenges they seek to address, but also take account of their potentially broad impact on overall market quality and functioning.

20 “Principles for Financial Benchmarks,” International Organization of Securities Commissions (July 2013).

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 17

III. Market Characteristics Required to Support Participant Needs In the previous section, we described both the variety and foundational nature of the roles played by the U.S. Treasury market. In doing so, we emphasized the importance of market quality in supporting the multifaceted needs of the wide variety of market participants. In this section, we explore the essential characteristics of market quality, with particular reference to the current challenges in the U.S. Treasury market. We also present facts relevant to evaluating proposals that have been made by public- and private-sector institutions for addressing the emerging issues.

We identify four characteristics of market quality with particular and current relevance to developments in the Treasury market, namely:

• Liquidity — the ability of the market to support the strategic and tactical transaction needs of the various participant categories, without shifting price levels materially from fundamental values, and under a wide variety of market and exogenous conditions.

• Transparency — the provision of appropriate visibility to participants and regulators regarding price formation, activity, and market quality.

• Operational Reliability and Resilience — the continued development of robust market infrastructure and processes to ensure the efficiency of market operation, certainty in transaction completion, and management of operational and counterparty risks.

• Supportive Regulatory Framework — the evolution of regulatory oversight and requirements, including both direct regulation and the impacts of broader prudential regulatory requirements, to support market quality, promote sound market practices and appropriate risk management by participants, and prevent fraudulent or manipulative behaviors.

We address these four characteristics in depth in the remainder of this section. However, it should be noted that efforts to sustain these characteristics will in turn promote additional positive features of the Treasury market:

• Pricing Reflective of Fundamental Value — Treasury securities’ use as a store of value and the benchmark nature of Treasury rates mean that Treasury pricing must reflect fundamental value, with minimal idiosyncratic influences. These features depend on the liquidity, depth, and operational reliability of the Treasury market.

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 18

• Product Diversity and Innovation — Participants use Treasury securities to manage a wide range of financial risks and require diverse maturities and structural profiles. In addition, participants benefit from access to a variety of financing and execution services. Liquidity, operational reliability and resilience, and a sound regulatory environment are crucial in supporting both product and service innovation.

• Market Access — Market quality, and the fulfillment of the Treasury market’s fundamental role of financing the U.S. government, benefits from offering broad market access to a variety of participants. Such access encourages additional pools of risk capacity to balance supply and demand over time, the anchoring of pricing in fundamental value, and the development of innovative services and market infrastructure.

A. Liquidity Liquidity is a fundamental component of a financial marketplace’s quality. Despite its importance, liquidity is difficult to define precisely. Liquidity is multifaceted and has a number of potential modes of measurement. As a working definition for current purposes, we will consider liquidity to be a market’s capacity to execute transactions in sizes and timeframes that reflect general participant needs, without materially shifting prices away from fundamental values. A closely related concept is that of resiliency, which in broad terms is taken as the maintenance of liquidity over a wide range of market and exogenous scenarios. A market lacking resilient liquidity may exhibit frequent periods of volatility without any obvious external drivers — where prices depart from fundamental values, and the ability to execute transactions in otherwise normal size is severely curtailed.

Liquidity is closely related to the other desirable characteristics of market quality described in this paper.21 In liquid markets, prices remain aligned with fundamental values, with variations being very temporary and reflecting regular transactional activity rather than idiosyncratic factors. A wide diversity of market participants, with varying investment horizons and objectives, will contribute to maintaining high levels of liquidity and resilience across the full market. The presence of participants with elevated risk capacities is also crucial to ensuring the resiliency of liquidity, particularly under stressed market conditions. Price transparency, as well as efficiency and robustness in market infrastructures and processes, in turn supports market participation and hence liquidity.

These considerations apply with special importance to the U.S. Treasury market. High and resilient levels of liquidity are essential in supporting the needs of the major participant types

21 “Fixed income market liquidity,” Committee on the Global Financial System, Bank for International Settlements (January 2016).

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 19

described in the previous section.22 A deep secondary market, where investors can transact efficiently at low cost and at prices reflecting fundamental value, is crucial to the attractiveness of Treasury securities as an asset class.23 In turn this attractiveness assists the U.S. Treasury in fulfilling its mission of funding the U.S. government through the primary market and at the lowest cost over time. Deep liquidity in the secondary market is also essential in allowing the Federal Reserve to conduct monetary-policy operations. Liquidity also supports the stability of markets that use U.S. Treasury securities as benchmarks, such as the markets for corporate bonds and mortgage-backed securities. A significant and sustained disruption in Treasury market liquidity would have profound consequences for financial and (by extension) macroeconomic stability.24 The occurrence of volatility events in the Treasury market, such as that on October 2014, is therefore of significant concern, since these types of events may be the symptom of deeper fragilities in the functioning of the market. Further underscoring this concern is the fact that the October 2014 event was not associated with any obvious external drivers.

While liquidity is a multifaceted concept, for the purposes of this discussion, we will focus on two specific dimensions.

• The first and obvious dimension is the demand/supply axis. Market participants may be natural liquidity suppliers, act as liquidity takers, or play a mixture of both roles depending on particular circumstances. Moreover, the scale of demand or supply can vary across this dimension.

• The second dimension is closely related to the notion of resiliency. There is no standard market terminology to describe this concept; but for the purposes of this paper, we will adopt the labels “strategic” liquidity and “tactical” liquidity for the two ends of this dimension.

We characterize strategic liquidity by a high risk capacity across a wide range of market scenarios, including those induced by crisis-like externalities, and for sustained time periods. Additionally, there will be a general expectation, if not a formal commitment, that suppliers of strategic liquidity will continue to make two-way markets even under volatile market scenarios.

Tactical liquidity, conversely, reflects a generally low risk capacity and activity over very short timescales. Suppliers of tactical liquidity may not carry any expectation of ongoing market support.

22 Jerome Powell, remarks at “The Evolving Structure of U.S. Treasury Markets” conference at the Federal Reserve Bank of New York (October 20, 2015); and Simon Potter, “Challenges Posed by the Evolution of the Treasury Market” (April 13, 2015). 23 Ibid. 24 Ibid.

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 20

TREASURY SECONDARY-MARKET LIQUIDITY PROFILE

Source: Promontory Financial Group

Each type of Treasury market participant typically occupies a quadrant in this two-dimensional liquidity space. The changing dynamics of the market — both structural, such as the rapid advances of electronic trading or capacity constraints arising from regulation, and circumstantial, such as the current environment of low interest rates and monetary stimulus through quantitative easing (“QE”) — are reflected in shifts in occupancy of each of these liquidity sectors. In particular, significant shifts in occupancy across the supply and demand dimension at each level of resilience may give rise to fundamental imbalances. Such imbalances may be reflected in an increased frequency of liquidity events and deterioration in market quality. We will discuss the correspondent current dynamics in the U.S. Treasury market more fully below.

The quadrant relating to the supply of strategic liquidity is of particular importance to the Treasury market’s functioning. This quadrant has typically been the domain of the primary dealers. In recent years, there have been new entrants to the marketplace, including proprietary trading firms, which — while sometimes operating as net liquidity suppliers — tend to provide only tactical liquidity. Buy-side institutions may have greater risk capacity than the proprietary trading firms, but lack a mandate to act as liquidity suppliers. The official sector has the capacity for liquidity intervention and has historically done so in particularly

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 21

acute cases.25 But such intervention has to be undertaken carefully, given potential conflicts with other public-policy mandates, and is generally not desirable as a normal feature of the market. In consequence, factors that erode the role or participation of the primary dealers as suppliers of strategic liquidity, without any offsetting measures to stimulate new entrants to this quadrant, risk creating the types of undesirable imbalances that might have been manifest in volatility events such as those in October 2014 — and which in turn damage confidence in the Treasury market.

ASSESSING LIQUIDITY CONDITIONS IN THE TREASURY MARKET

The multifaceted nature of liquidity, as discussed above, makes it difficult to find any single measure to capture and describe the various aspects of the concept. We review below a number of different liquidity measures that are commonly cited by market stakeholders.26 In the aggregate, these forms of measurement give an indicative picture of liquidity, if still a limited one because of the unavailability of data or lack of conceptual or measurement precision. Furthermore, while there are multiple technical measures of tactical liquidity, it is more difficult to assess (the arguably more important) strategic liquidity. While there are some indirect measures of strategic liquidity, partial reliance has to be placed on reviewing the tactical liquidity measures on a trend basis in order to assess strategic liquidity conditions. A further difficulty arises in the Treasury market due to its segmented nature between on-the-run and off-the-run issues and the fact that off-the-run issues largely trade in the dealer-to-customer sector. In the absence of formalized trade-reporting mechanisms, there is limited aggregate visibility available into this sector.

The main market-based metrics, which tend to focus on tactical liquidity, are:

Bid-ask spread, which is the difference between bid and ask (or offer) prices, typically for a reference bond that can be tracked over time. This measure is essentially a measure of trading cost. While variations in the spread can also give some indication of risk capacity, the metric does not directly reference the quantity of bonds that can be traded at the bid or ask prices. Bid-ask spreads can be readily assessed in central limit-order books (“CLOBs”) — such as those operated by the Treasury interdealer brokers (“IDBs”)27 for cash, or by the Chicago Mercantile Exchange (“CME”) for Treasury futures — or on a survey basis for the dealer-to-customer segment of the market.

25 For example, in October 2008, the Treasury reopened four security issues following a number of settlement failures in Treasury securities related to the Lehman insolvency. See Kenneth Garbade, Frank M. Keane, Lorie Logan, Amanda Stokes, and Jennifer Wolgemuth, “The Introduction of the TMPG Fails Charge for U.S. Treasury Securities,” Federal Reserve Bank of New York Economic Policy Review (October 2010). 26 “Market-making and proprietary trading: industry trends, drivers, and policy implications,” Committee on the Global Financial System, Bank for International Settlements (November 2014); and “Shifting tides — market liquidity and market-making in fixed income instruments,” BIS Quarterly Review (March 2015). 27 IDBs facilitate trading among dealers in the secondary market. IDBs act as agents in the dealer community, and their role is to match buyers and sellers of Treasury securities in a private, closed market.

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 22

Market depth attempts to assess the volume that can be transacted at or close to the current market-price levels. At its simplest, market depth may reference the committed volume quoted at the best bid or ask price level. A slightly more sophisticated variant considers the aggregate committed volume across a predefined range of bid or ask price levels starting from the best bid or ask. An alternative market depth measure is the realized trade size at a given price level (i.e., before there is a price change). In practical terms, market depth measures can only be readily assessed for CLOBs. Market depth measures may underestimate liquidity somewhat, since dealers are generally reluctant to display full size on CLOBs.

Price impact seeks to assess the change in price when an “aggressor” — a liquidity taker — hits a bid or lifts an offer. In practice, the data is rarely available to calculate these metrics directly. Proxies, such as intraday price variations for days when there is little market-moving external news, are sometimes used.

Based on these market-based metrics, there is some evidence of a decline in Treasury cash liquidity in the recent post-crisis years, but assessments of the severity of the decline vary. Bid-ask spreads widened sharply in the crisis years, but subsequently returned to longer-run averages.

BID-ASK SPREAD IN SECONDARY MARKET FOR US TREASURY SECURITIES 1-week moving average of 10-year U.S. Treasury; in 32nds

Source: BrokerTec

Market depth has declined in the past three years to below a decade long average, but this measure has exhibited some major variations over the averaging period, so the decline may ultimately prove to be a transient phenomenon. If intraday price variation can be taken as a proxy price-impact measure, then there appears to have been a recent widening of this measure, indicative of a decline in liquidity. However, periodic speculation about when

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80 0.90 1.00

2008 2009 2010 2011 2012 2013 2014 2015 2016

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 23

interest rates may rise from their historic lows over this period may also have led to bouts of market volatility even in the absence of specific market-moving news, so it is difficult to derive a precise signal from this source.

MARKET DEPTH IN SECONDARY MARKET FOR US TREASURY SECURITIES 1-month moving average of 10-year market depth

Source: BrokerTec

INTRADAY RANGE IN SECONDARY MARKET FOR US TREASURY SECURITIES

Source: BrokerTec

We obtain somewhat more convincing, if also more indirect or anecdotal, evidence for a decline in liquidity conditions in the Treasury market, from considering measures that relate to strategic liquidity and market aggregates.

0

50

100

150

200

250

300

350

400

2011 2012 2013 2014 2015 2016

Mill

ions

1m moving average of 10y UST market depth period average

0

1

2

3

4

5

6

7

8

9

2013 2014 2015 2016

Bas

is P

oint

s

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 24

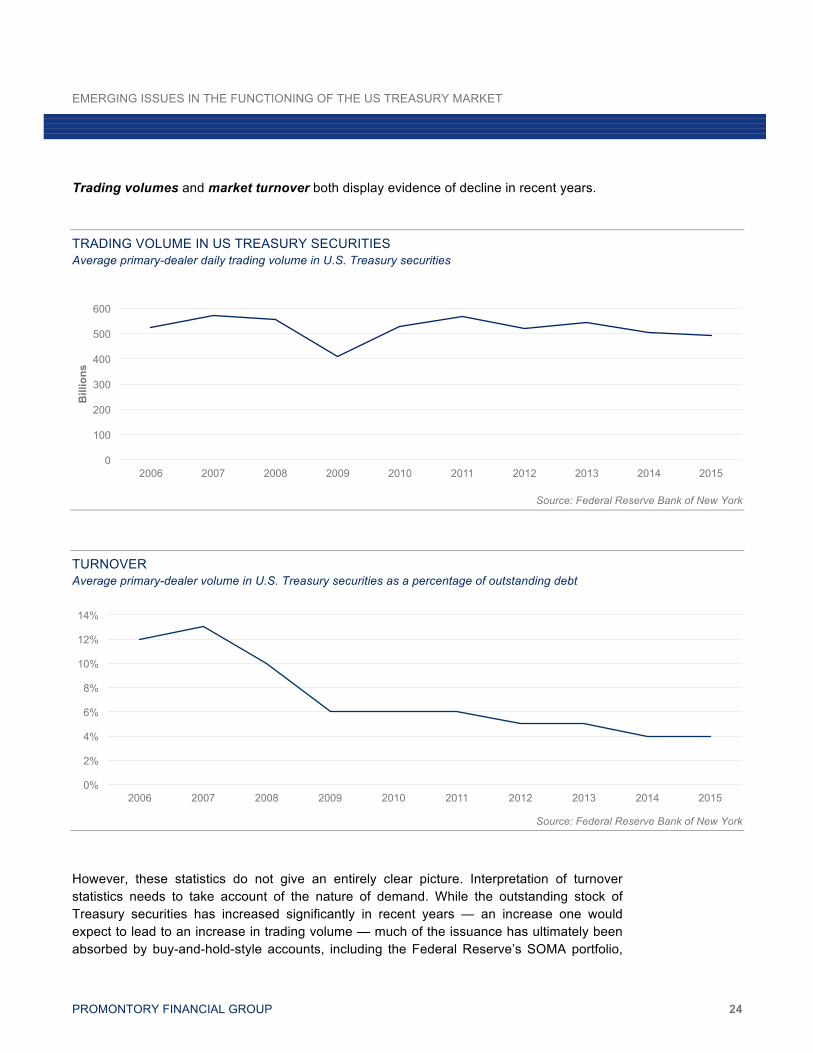

Trading volumes and market turnover both display evidence of decline in recent years.

TRADING VOLUME IN US TREASURY SECURITIES Average primary-dealer daily trading volume in U.S. Treasury securities

Source: Federal Reserve Bank of New York

TURNOVER Average primary-dealer volume in U.S. Treasury securities as a percentage of outstanding debt

Source: Federal Reserve Bank of New York

However, these statistics do not give an entirely clear picture. Interpretation of turnover statistics needs to take account of the nature of demand. While the outstanding stock of Treasury securities has increased significantly in recent years — an increase one would expect to lead to an increase in trading volume — much of the issuance has ultimately been absorbed by buy-and-hold-style accounts, including the Federal Reserve’s SOMA portfolio,

0

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ions

0%

2%

4%

6%

8%

10%

12%

14%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 25

overseas reserve managers’ holdings, and banks’ investment portfolios — the last of which have substantially expanded their holdings in high-quality liquid assets following the introduction of Basel III liquidity requirements. The growth in these type of portfolios affects both liquidity supply (the proportion of “free float” relative to total issuance is reduced) and liquidity demand (since these portfolios are not traded). Additionally, volume statistics can be influenced by such factors as internalization of customer flow or disintermediation of some of the sampled market participants. Volume can also be affected by market outlook for future rate moves; the volume declines in recent years may partly reflect the continuation of a low-rate environment for a considerable period. Overall, it is the balance of these structural and circumstantial factors that therefore needs to be assessed in considering secondary-market liquidity conditions.

Perhaps the most definitive evidence for deterioration of liquidity — particularly of strategic liquidity — comes from analysis of primary-dealer activities. Although the number of primary dealers has returned roughly to pre-crisis levels, there are numerous indicators of reduced activity in both the primary and secondary markets. We discuss some of the potential reasons for this below. There are two particularly striking metrics in this regard. The first is the reduction in demand by primary dealers at Treasury auctions, a declining trend that has held for over five years.

NUMBER OF PRIMARY DEALERS Dealer number as of April 2016

Source: Federal Reserve Bank of New York

22 22 22 20

17 18 18

21 21 21 22 22 23

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 26

CHANGING COMPOSITION IN TREASURY AUCTION TAKEDOWN 6-month moving average

Source: U.S. Treasury

The second has been the marked decline in dealer inventory in fixed-income securities to levels not seen since early in the century. While some circumstantial factors related to the low level of interest rates may play a role in this decline, the overall trend is more likely to be structural in origin.

SECURITIES POSITIONS OF US BROKER-DEALERS Includes Treasury securities, agency bonds, municipal securities, and corporate bonds

Source: Federal Reserve System

0%

10%

20%

30%

40%

50%

60%

2009 2010 2011 2012 2013 2014 2015 Primary Dealer Funds Foreign/Intl

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 27

PRIMARY-DEALER REPO OUTSTANDING — US TREASURY SECURITIES AND TIPS

Source: Federal Reserve Bank of New York

LIQUIDITY SUPPLY AND DEMAND DRIVERS28

We close this section by considering qualitatively the evolution of several drivers of liquidity supply and demand in the Treasury market. These drivers derive from a combination of structural and circumstantial factors. An understanding of these factors — particularly of structural factors that relate to the supply of strategic liquidity — is essential in developing regulatory or industry initiatives to bolster market quality. Among the principal drivers, we identify the following:

Monetary Policy

Accommodative monetary policies, in conjunction with forward guidance suggesting persistently low interest rates, has likely had a strong effect on sustained demand for fixed-income assets, including Treasury securities, by institutional investors. Moreover, this demand has progressively extended across the maturity spectrum. Additionally, the large-scale purchases of government bonds by the Federal Reserve under the QE programs might have impacted the Treasury securities available for trading, even though there have been restrictions on the amount of particular issues purchased and the Federal Reserve has expanded its securities-lending program in recent years.

28 See previous chart on Growth and Marketable Debt in Section II.

1,673

1,568

1,481

1,350

1,400

1,450

1,500

1,550

1,600

1,650

1,700

2013 2014 2015

Bill

ions

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 28

Primary-Market

Issuance of Treasury securities since the crisis has expanded the stock of outstanding Treasury securities to unprecedented levels. While much of the new issuance has been absorbed by buy-and-hold private- and public-sector portfolios, including overseas accounts, elevated levels of issuance normally lead to elevated liquidity demand in the immediate post-issuance period.

Prudential Regulation

Perhaps the most cited effect on the supply of strategic liquidity has been the impact of post-crisis prudential banking regulation on capital and liquidity.29 As the vast majority of primary dealers are bank-owned, their activities have been affected by elevated regulatory requirements for capital and liquidity buffers for the parent balance sheets. While the enhanced prudential requirements have contributed to a more resilient financial system overall, some of these requirements may have had unforeseen or disproportionate consequences on certain activities such as those of the primary dealers.

Higher capital requirements have directly influenced capacity for risk taking, and particularly affected lower-margin businesses such as government-bond market making. Leverage restrictions, including the supplementary leverage ratio, have made it more onerous to retain low-risk but low-margin assets on the balance sheet. This may have affected inventory levels, on the one hand, but also the provision of financing facilities to trading accounts, leading to an overall reduced supply of liquidity services in Treasury securities. Finally, in respect of liquidity supply, Volcker rule restrictions on proprietary trading by banks have also been suggested as factors in reduced primary-dealer inventory and risk-taking services.30 Treasury securities are exempt from the Volcker rule requirements. However, as banks have reduced proprietary activities in other asset classes, there may have been knock-on effects both in proprietary activities in Treasury securities and in demand for Treasury securities as short-term hedges for other fixed-income proprietary trading.

A combination of liquidity regulation and mandatory margin requirements for uncleared derivatives has sharply increased the demand for high-quality liquid assets. Since these assets tend to be held rather than traded, liquidity supply is also likely to have been impacted.

29 “Fixed income market liquidity,” Committee on the Global Financial System, Bank for International Settlements (January 2016); and “Market-making and proprietary trading: industry trends, drivers, and policy implications,” Committee on the Global Financial System, Bank for International Settlements (November 2014). 30 “Market-making and proprietary trading: industry trends, drivers, and policy implications,” CGFS.

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 29

Evolution of Algorithmic Trading31

The evolution of electronic trading in the interdealer market, together with the opening of IDB platforms to participants other than the primary dealers, has seen the emergence of many new and substantial proprietary players in the cash Treasury market.32 These new entrants, many of which were originally active in the Treasury futures market, largely engage in trading benchmark, on-the-run issues, as opposed to off-the-run issues. Proprietary trading firms (“PTFs”) operate across a spectrum of liquidity demand and supply roles.33 Some are essentially net consumers of liquidity, while others act as short-term intermediaries with some capacity (unlike the IDB business model) to provide liquidity to client-facing dealers. However, as the PTFs tend to have little sustained risk-taking capacity — and typically do not carry overnight positions — they are generally not suppliers of strategic liquidity. Indeed, there are also concerns that the activities of the PTFs under normal market conditions may cause an illusion of market liquidity — that is, liquidity that could rapidly evaporate in a crisis.34 Finally, there remains a fear that without established standards35 of operational risk controls for PTFs or controls over PTFs generally, a PTF’s poorly designed algorithm could provoke a disruptive market event.36

B. Transparency It is generally accepted by market participants and regulators that a principle of transparency is fundamental to the fair and efficient functioning of any marketplace.37 Transparency regarding pricing, market activity, and market quality is considered to promote healthy competition in the marketplace, support fair and equitable access to potential participants, and ground transaction pricing in fundamental value, thereby offering investor protection.

In this regard, the U.S. Treasury market traditionally has offered very high levels of pre-trade price transparency. Benchmark bond prices are widely available in real time through multiple information services. Even for less liquid off-the-run or TIPS issues, the general homogeneity of the asset class means that price levels can be readily inferred for these less liquid securities by reference to the benchmark rates. However, comprehensive transaction-level

31 “Best Practices for Treasury, Agency Debt, and Agency Mortgage-Backed Securities Markets,” Treasury Market Practices Group, Federal Reserve Bank of New York (June 2015); “Automated Trading in Treasury Markets,” Treasury Market Practices Group, Federal Reserve Bank of New York (June 10, 2015); and Morten Linnemann Bech, Anamaria Illes, Ulf Lewrick, and Andreas Schrimpf, “Hanging up the phone — electronic trading in fixed income markets and its implications.” BIS Quarterly Review (March 2016). 32 “Automated Trading in Treasury Markets.” Treasury Market Practices Group, Federal Reserve Bank of New York (June 10, 2015). 33 “Electronic trading in fixed income markets,” Bank for International Settlements (January 21, 2016). 34 Ibid. 34 Ibid. 35 “Best Practices for Treasury, Agency Debt, and Agency Mortgage-Backed Securities Markets,” Treasury Market Practices Group, Federal Reserve Bank of New York (revised June 2015). 36 Ibid. 37“Objectives and Principles of Securities Regulation,” International Organization of Securities Commissions (June 2010).

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 30

information has not been available for the cash U.S. Treasury market, and this is of course a specific concern raised in the RFI and by market regulators more broadly.38 In particular, there is limited visibility into the dealer-to-customer segment of the market and for non-centrally cleared activities.

In addressing forms of transparency such as transaction reporting, it becomes necessary for transparency to be considered in conjunction with other measures to promote market quality, rather than as an isolated principle. The level and type of transparency considered optimum have to take account of the nature of the asset class being traded and that market’s particular microstructure.39 For example, where the functioning of a market relies in part on the presence of dealers acting as liquidity providers, pre-trade and immediate post-trade transparency initiatives need to be carefully designed and tailored to the specific market structure. Post-trade transparency protections may be necessary to give liquidity providers time to reduce their exposures after executing a large client order, before revealing the activity to the general marketplace. Otherwise, liquidity providers might have a disincentive to offering their services, to the detriment of the overall functioning of the market. Indeed, there is an extensive literature on the need for achieving a balanced application of a general transparency principle, which largely cautions against a blanket transposition of transparency provisions from one market or asset class to another, without regard to the underlying market structure.40

In considering how a general principle of transparency can be optimally applied, it is useful to first distinguish between a number of commonly considered types of market information that might be collected and/or disseminated under transparency provisions. For convenience, we classify such information as either aggregate information or specific information.

AGGREGATE INFORMATION

• Information that supports an analysis and monitoring of market quality: comprising data on market size, turnover, liquidity conditions, and execution quality. Typically these metrics would be available on a periodic basis and in aggregated form. This information could be used by market participants in considering information that supports their market strategies and business activities, and by regulators in assessing market quality and microstructure.

38 “Notice Seeking Public Comment on the Evolution of the Treasury Market Structure,” U.S. Department of the Treasury, Federal Register (January 22, 2016). 39 Jose Ramon Martinez-Resano, “Size and Heterogeneity Matter. A Microstructure-Based Analysis of Regulation of Secondary Markets for Government Bonds” (2005). 40 Antonio Weiss, remarks at the “2015 Roundtable on Treasury Markets and Debt Management” at the Federal Reserve Bank of New York (November 20, 2015).

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 31

• Information supporting an analysis and monitoring of market or operational risk concentrations: This information would be used primarily by regulators and operators of market infrastructure to assess and address systemic risks in the market.

SPECIFIC INFORMATION

• Pre-trade information on price and market depth: This data is primarily of interest to market participants to inform their trading and investment decisions.

• Transaction and, where relevant, order-book data: This data would be used by regulators and/or platform operators, in real or nearly real time, for surveillance of market participants to ensure adherence to regulatory and platform rules. This data could also be used by regulators for analysis of market events like the October 2014 volatility event. Some market participants may use the information to inform their trading strategies.

In the major U.S. markets, transparency in providing most of the types of aggregate information above is normally thought to support market integrity and quality. Cost considerations certainly play a role in the extent of the data that market participants are readily willing to provide. Anonymity and confidentiality provisions to protect commercially sensitive information also have to be considered. Market-microstructure factors play less of a role in considering the desirability of providing supporting data, although they may of course influence the costs of data collection and aggregation.

There is generally less consensus among market participants about pre-trade and immediate post-trade transparency, which falls in the category of specific information. There are particular concerns when this information is to be disseminated widely to other participants, rather than to public authorities only. In the context of the cash U.S. Treasury markets, and government-bond markets more broadly, arguments have been advanced that any requirements for immediate or near-immediate marketwide disclosures should be considered only with caution. These arguments take into account the information asymmetries that such disclosures seek to resolve, as well as the dealer-based microstructure of government-bond markets relative to markets in other asset classes.41 Transaction reporting in equity markets, for example, is held to be necessary as a fundamental part of price formation, with a view to investor protection. By contrast, investors generally have equal access to the macroeconomic information that drives government-debt valuations. Moreover, as noted above, transparency provisions need to take account of the nature of the asset class and the consequences for the market microstructure — dealers as warehousers of risk inventory, in addition to central limit-order books — that appears to have evolved in most major government-debt markets. It can be argued that such providers of risk warehousing need to be incentivized to play this

41 Jose Ramon Martinez-Resano, “Size and Heterogeneity Matter. A Microstructure-Based Analysis of Regulation of Secondary Markets for Government Bonds” (2005).

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 32

role by having some protection of their ability to take on and offset large risk positions over a suitable period.42 Holding to an absolute standard of immediate transparency for pre-trade market depth and post-trade reporting could therefore hinder market functioning.

Finally, a distinction should be made between providing additional pre- and post-trade information for general publication and reporting that information to regulators. The provision of data to the public needs to take account of the nature of the microstructure in the Treasury market and make a balanced assessment of the benefits of increased information relative to the potential consequences for the supply of liquidity. By contrast, the provision of data to regulators generally raises no such concerns. The lack of consolidated pre-trade and transaction reporting in Treasury securities leaves regulators with less than optimal visibility into the functioning of the Treasury market. This was evident in the difficulty regulators experienced in analyzing the October 2014 volatility event. While regulators currently receive certain aggregate reporting on a periodic basis from primary dealers,43 intermediaries, and the Fixed Income Clearing Corporation (“FICC”), this type of information may need to be enhanced and supplemented with more specific information to allow regulators to carry out their role in ensuring market quality and efficiency.

C. Operational Reliability and Resilience Operational reliability and resilience are essential to support the quality and smooth functioning of a financial market. Market reliability is reflected in how well the market infrastructure can consistently deliver anticipated performance; minimize failure; and anticipate, prepare for, and respond to incremental change and sudden disruptions. Such reliability and resilience support investor confidence, reduce costs of participation, promote efficient price discovery, support liquidity, and reduce idiosyncratic volatility. A robust operational infrastructure is especially important in the specific context of the U.S. Treasury market, given:

• The fundamental role that Treasury securities play in fiscal and monetary operations, where any disruptions could have macroeconomic effects.

• The extensive use of Treasury securities in hedging and collateral activities in other markets, so that operational failures in the Treasury market could rapidly propagate through the financial system.

• The use of Treasury securities as a store of value and liquidity; operational failures in accessing this liquidity when needed could affect a wide spectrum of contractual and risk management arrangements.

42 For example, TRACE reporting for corporate bonds and Commodity Futures Trading Commission and CME Group rules for block trading in the futures markets allow for lagged publication of activity. 43 For example, see the FR 2004 Weekly Report of Dealer Positions, Transactions, and Financing.

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 33

Operationally, the Treasury market consists of a heterogeneous set of firm-specific internal systems, procedures, and practices, coupled to an increasingly standardized set of marketwide infrastructures (trading, clearing, and settlement systems) as shown in Figure A.

These systems and practices have developed over the last several decades as the market has evolved and responded to demands for higher standards of operational capacity, reliability, and resiliency. Contributing to and supporting this evolution are a number of associated industry protocols, best practices, and supporting policies. For example, the Treasury Market Practices Group44 (“TMPG”) has developed a set of best practices in the Treasury market, for promoting liquidity and transparency, maintaining a robust control environment, managing risks arising from large positions, and promoting efficient market clearing.45 In the area of operational reliability, the TMPG has issued recommendations on practices and charges for settlement fails, timely trade confirmations for tri-party repos, contingent operational plans for Treasury debt payments, and the implementation of new technologies or algorithmic strategies. Regulatory initiatives with particular relevance for the resilience of the Treasury market include the “Interagency Paper on Sound Practices to Strengthen the Resilience of the U.S. Financial System”; the “Principles for financial market infrastructures”; and Title VIII of the Dodd-Frank Act.46 We discuss below four specific aspects of the Treasury market’s operational reliability and resiliency: auction processes, secondary-market trading, secondary-market clearing, and settlement.

44 The TMPG is a group of market professionals committed to supporting the integrity and efficiency of the Treasury and government-debt markets. 45 “Best Practices for Treasury, Agency Debt, and Agency Mortgage-Backed Securities Markets,” Treasury Market Practices Group, Federal Reserve Bank of New York (February 2016). 46 “Interagency Paper on Sound Practices to Strengthen the Resilience of the U.S. Financial System,” Board of Governors of the Federal Reserve System, Securities and Exchange Commission, and Office of the Comptroller of the Currency (April 7, 2003); and “Principles for financial market infrastructures,” Committee for Payment and Market Infrastructures and International Organization of Securities Commissions (April 2012).

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 34

FIGURE A. – OPERATIONAL RELATIONSHIPS IN US TREASURY MARKET

Source: Promontory Financial Group

AUCTION PROCESS

The last decade witnessed striking advances in bid submission, bid processing, and announcement of auction results.47 Prior to 1993, bids were submitted on paper forms and processed manually. This procedure had several drawbacks for market participants and the Treasury. First, auction results frequently were announced in the afternoon, leaving market participants uncertain about the status of their bids. Such uncertainty may have led them to enter bids at higher yields than they would have if auction results had been announced more promptly. Second, manual processing was inefficient both for the Treasury and for market participants.48 Third, in the wake of the Salomon Brothers auction-procedures violations in 1991, the Treasury needed to improve the controls over bidding to ensure market integrity. Finally, throughout the 1980s and 1990s, the number of primary dealers steadily decreased from around 47 to 22, increasing concerns about auction access, collusion, and efficient sale and distribution of the Treasury’s debt.

47 Kenneth Garbade and Jeffrey Ingber, “The Treasury Auction Process: Objectives, Structure, and Recent Adaptations,” Federal Reserve Bank of New York Current Issues in Economics and Finance (February 2005). 48 For example, as stated in Garbade and Ingber (2005), “dealers had a lot to lose if they tendered bids early at prices that failed to reflect a late-developing rally or market pullback, so on auction days they stationed employees in the lobby of the Federal Reserve Bank of New York and relayed bidding instructions over the telephone immediately before the close of bidding.”

EMERGING ISSUES IN THE FUNCTIONING OF THE US TREASURY MARKET

PROMONTORY FINANCIAL GROUP 35

To address these concerns, the Treasury in 1993 introduced an early version of auction automation — the TAAPS® — and in 2008 improved the functionality of the system, in an upgrade dubbed New TAAPS® or NTAAPS®. Today, NTAAPS® is a streamlined and efficient process that electronically receives and processes tenders sent into U.S. Treasury auctions.

Electronic processing dramatically reduced the time between the close of bidding and the announcement of results from several hours to two minutes, thus materially reducing bidder risk exposure. It also made it operationally feasible for a wider spectrum of institutions to purchase marketable securities directly, in a process called “direct bidding,” thus reducing or eliminating intermediary costs and maximizing the breadth of the auction market.

SECONDARY-MARKET TRADING