Emerging Dominance of Aquaculture

69

Emerging Dominance of Aquaculture: Emerging Dominance of Aquaculture: The Future of the Seafood Market The Future of the Seafood Market and Fisheries Management and Fisheries Management James L. Anderson James L. Anderson Department of Environmental and Natural Resource Department of Environmental and Natural Resource Economics Economics University of Rhode Island University of Rhode Island Kingston, RI 02879 Kingston, RI 02879 USA USA IIFET 2008 IIFET 2008 Nha Nha Trang Trang , Vietnam , Vietnam July 21 July 21 - - 25, 2008 25, 2008

Transcript of Emerging Dominance of Aquaculture

Emerging Dominance of Aquaculture:Emerging Dominance of Aquaculture:The Future of the Seafood MarketThe Future of the Seafood Market

and Fisheries Managementand Fisheries Management

James L. AndersonJames L. AndersonDepartment of Environmental and Natural Resource Department of Environmental and Natural Resource

EconomicsEconomicsUniversity of Rhode Island University of Rhode Island

Kingston, RI 02879Kingston, RI 02879USAUSA

IIFET 2008IIFET 2008

NhaNha TrangTrang, Vietnam, VietnamJuly 21July 21--25, 200825, 2008

Key ThemesKey Themes

Aquaculture will dominate the seafood Aquaculture will dominate the seafood market market –– esp. international tradeesp. international tradeWinners will control costs and manage for Winners will control costs and manage for marketsmarketsFisheries managed more like Fisheries managed more like ‘‘aquacultureaquaculture’’------ winwinAquaculture sectors managed more like Aquaculture sectors managed more like fisheries (US marine aquaculture) fisheries (US marine aquaculture) ------ loselose

Seafood SectorSeafood SectorExtremely Complex and Diverse Extremely Complex and Diverse –– 100s of species, many technologies, many areas100s of species, many technologies, many areas

Highly InternationalHighly InternationalBureaucratic Regulatory Environment Bureaucratic Regulatory Environment FragmentedFragmentedWastefulWastefulMarketing is Not Advanced Marketing is Not Advanced Highly Misunderstood by Consumers Highly Misunderstood by Consumers including Chefs including Chefs Volatile Volatile –– in Prices and Quantitiesin Prices and Quantities

Simple RealitiesSimple RealitiesDemand for Fish

Fishermen Catch Fish

Poorly Defined Rights and Responsibilities (Traditional Fisheries Management)

Overfishing, Rent Dissipation

Reduced Supply and Unmet Demand

Enter Aquaculture

Inefficient Fisheries Management and/or Unmet Demands are the Stimuli for Aquaculture and Innovation

Simple RealitiesSimple RealitiesPeople whose lives depend on the harvest of seafood People whose lives depend on the harvest of seafood

want:want:

–– Better control of cost Better control of cost –– Minimize environmental/exogenous shocksMinimize environmental/exogenous shocks–– Better control fish stock and growth rates Better control fish stock and growth rates –– Manage to meet the market demandManage to meet the market demand–– Sustainable profitsSustainable profits

CONTROLCONTROLof production and marketing throughof production and marketing through

Ownership, Information and TechnologyOwnership, Information and Technology

If the Future will be Dominated If the Future will be Dominated by Aquacultureby Aquaculture

What does it mean for the future of the What does it mean for the future of the seafood sector?seafood sector?

What does it mean for the future of What does it mean for the future of fisheries/aquaculture management?fisheries/aquaculture management?

U.S. Per Capita Consumption of Red Meat, U.S. Per Capita Consumption of Red Meat, Poultry, and Fish and Shellfish, 1909Poultry, and Fish and Shellfish, 1909--20062006

Source: USDA/Economic Research Service. *2004-2006 Red Meat and Poultry data are forecasts.

0

20

40

60

80

100

120

140

1909 1915 1921 1927 1933 1939 1945 1951 1957 1963 1969 1975 1981 1987 1993 1999 2005*

Poun

ds p

er C

apita

Red Meat Poultry Fish & Shellfish

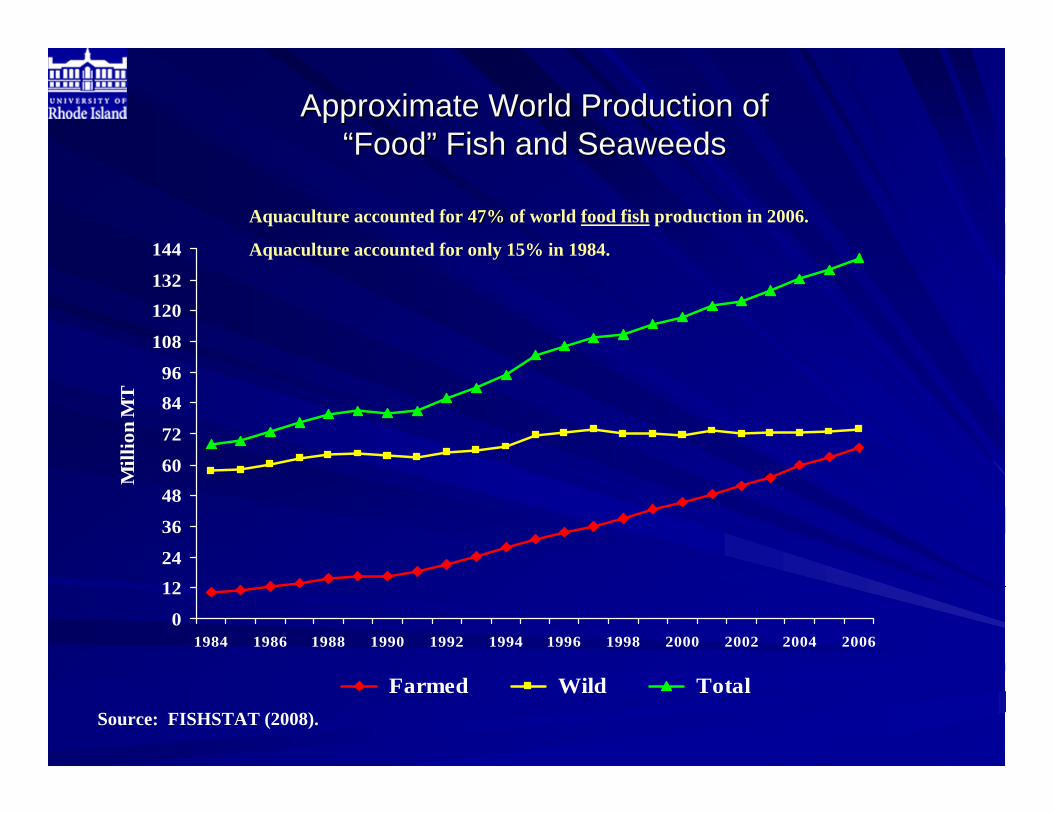

Approximate World Production of Approximate World Production of ““FoodFood”” Fish and SeaweedsFish and Seaweeds

0

1224

36

4860

72

8496

108

120132

144

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Mill

ion

MT

Farmed Wild Total

Aquaculture accounted for 47%47% of world food fish production in 2006.

Aquaculture accounted for only 15% in 1984.

Source: FISHSTAT (2008).

To develop expectations about the future of To develop expectations about the future of the seafood sector, we must consider the seafood sector, we must consider

aquaculture and fisheries interact?aquaculture and fisheries interact?

In the ecosystem? In the ecosystem? In the market ?In the market ?

Aquaculture and Fisheries: Aquaculture and Fisheries: EcosystemEcosystem

Use of wild fish for inputsUse of wild fish for inputs

Disease transmission and related interactions Disease transmission and related interactions

Intentional releases or unintentional escapesIntentional releases or unintentional escapes

Use or enhancement of habitatUse or enhancement of habitat

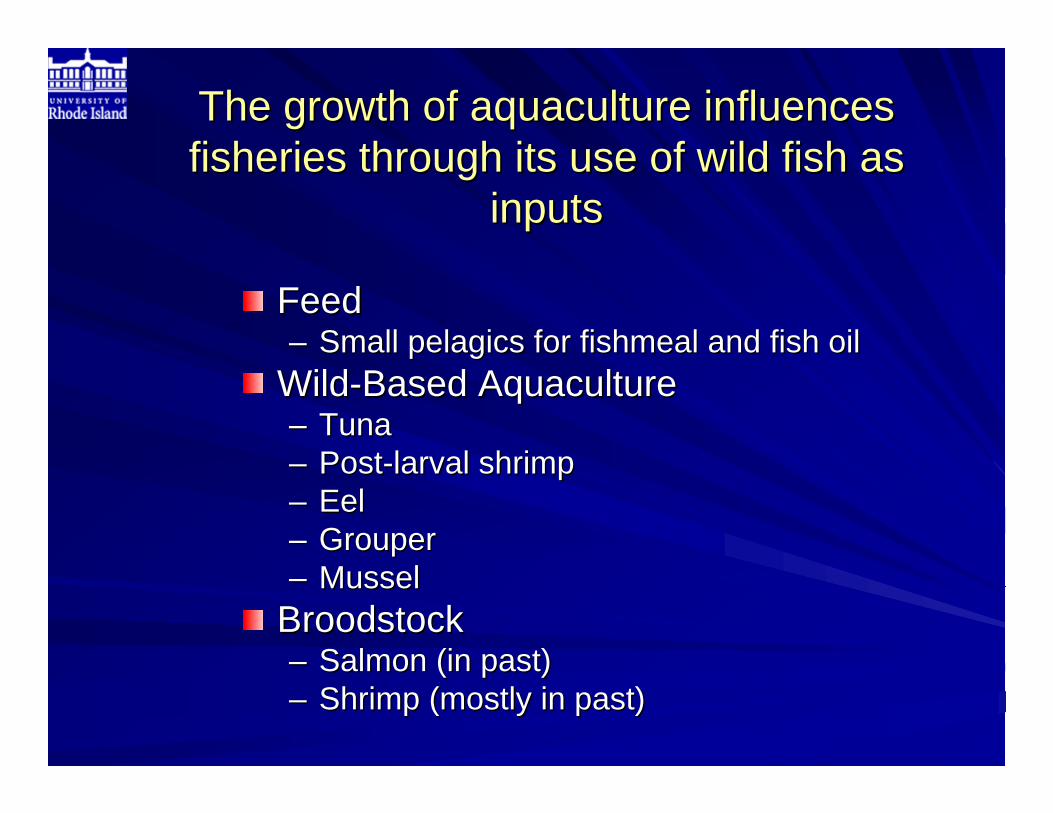

The growth of aquaculture influences The growth of aquaculture influences fisheries through its use of wild fish as fisheries through its use of wild fish as

inputsinputs

FeedFeed–– Small pelagics for fishmeal and fish oilSmall pelagics for fishmeal and fish oil

WildWild--Based AquacultureBased Aquaculture–– Tuna Tuna –– PostPost--larval shrimplarval shrimp–– EelEel–– GrouperGrouper–– MusselMussel

BroodstockBroodstock–– Salmon (in past)Salmon (in past)–– Shrimp (mostly in past)Shrimp (mostly in past)

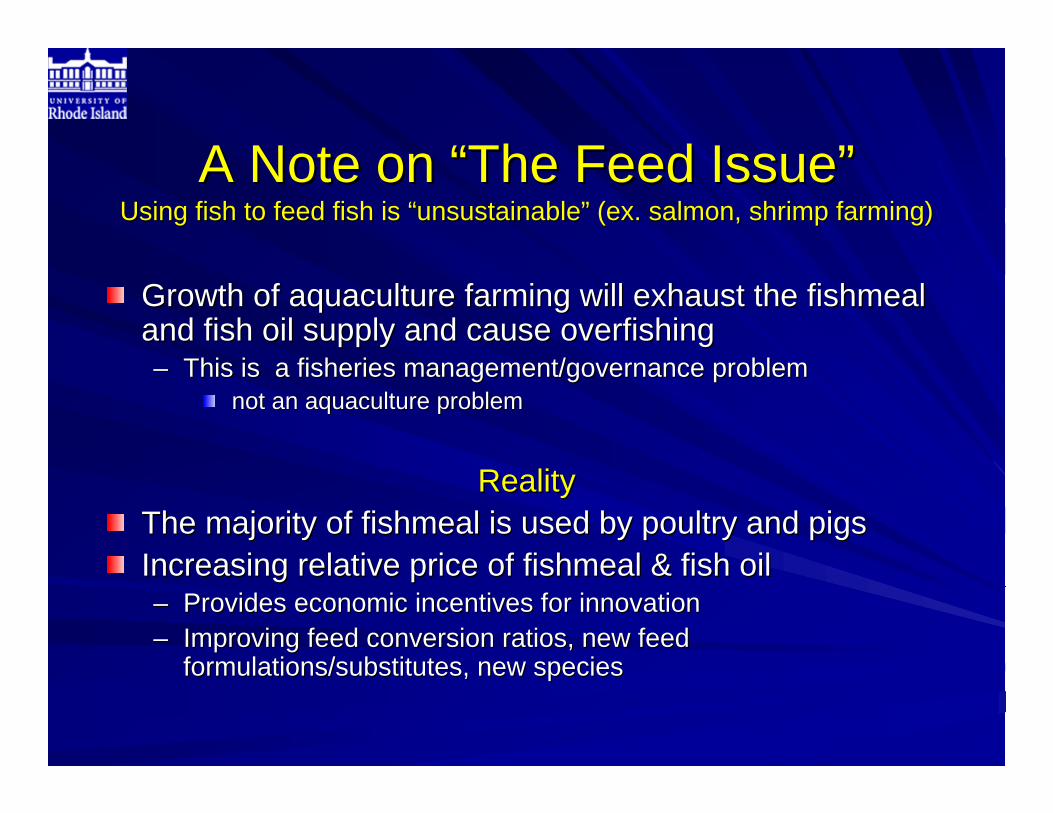

A Note on A Note on ““The Feed IssueThe Feed Issue””Using fish to feed fish is Using fish to feed fish is ““unsustainableunsustainable”” (ex. salmon, shrimp farming)(ex. salmon, shrimp farming)

Growth of aquaculture farming will exhaust the fishmeal Growth of aquaculture farming will exhaust the fishmeal and fish oil supply and cause overfishing and fish oil supply and cause overfishing –– This is a fisheries management/governance problem This is a fisheries management/governance problem

not an aquaculture problemnot an aquaculture problem

RealityRealityThe majority of fishmeal is used by poultry and pigsThe majority of fishmeal is used by poultry and pigsIncreasing relative price of fishmeal & fish oil Increasing relative price of fishmeal & fish oil –– Provides economic incentives for innovationProvides economic incentives for innovation–– Improving feed conversion ratios, new feed Improving feed conversion ratios, new feed

formulations/substitutes, new speciesformulations/substitutes, new species

Aquaculture and DiseaseAquaculture and DiseaseAquaculture and Disease

Example:

Parasite, B. ostreae, was introduced (probably) into France in oysters imported from California which originated from the NMFS Aquaculture Lab in CT

Example:Example:

Parasite, Parasite, B. ostreae,B. ostreae, was introduced was introduced (probably) into France in oysters (probably) into France in oysters imported from California which imported from California which originated from the NMFS Aquaculture originated from the NMFS Aquaculture Lab in CT Lab in CT

NRC. 2004. Nonnative Oysters in the Chesapeake Bay. Nat. Academy Press. Washington DC. p 40.

NRC. 2004. Nonnative Oysters in the Chesapeake Bay. Nat. Academy Press. Washington DC. p 16.

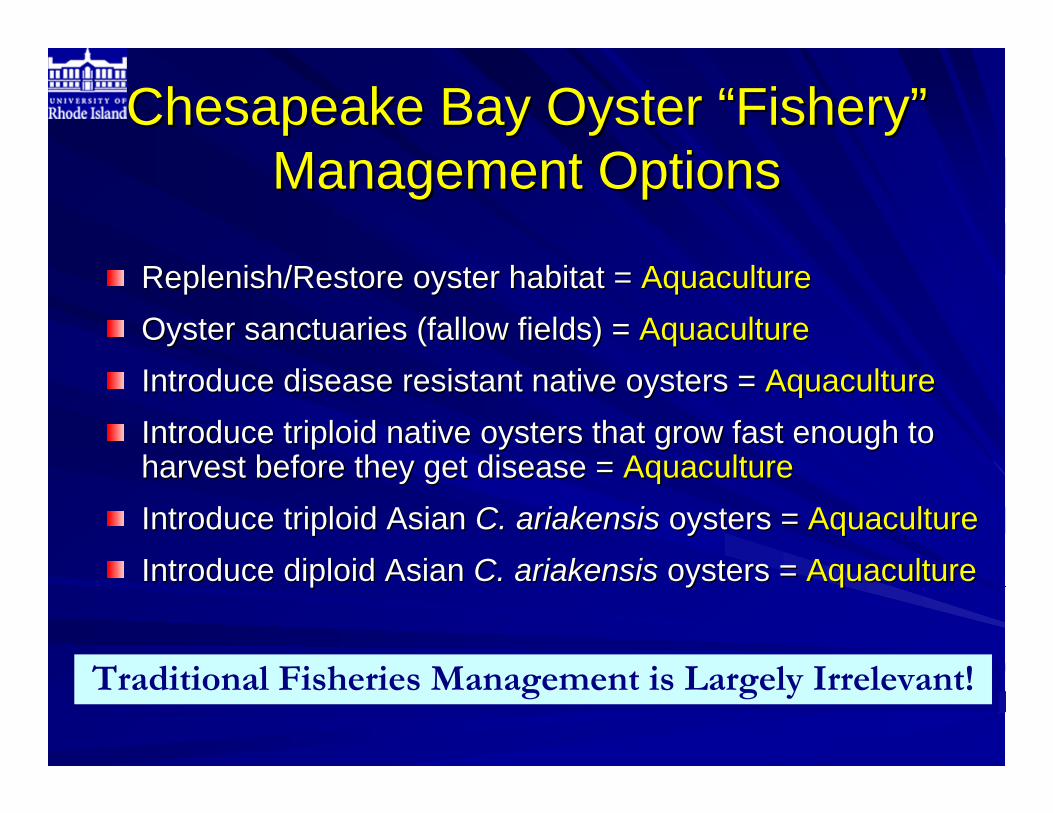

Chesapeake Bay Oyster Chesapeake Bay Oyster ““FisheryFishery””Management OptionsManagement Options

Replenish/Restore oyster habitat = Replenish/Restore oyster habitat = AquacultureAquacultureOyster sanctuaries (fallow fields) = Oyster sanctuaries (fallow fields) = AquacultureAquacultureIntroduce disease resistant native oysters = Introduce disease resistant native oysters = AquacultureAquacultureIntroduce triploid native oysters that grow fast enough to Introduce triploid native oysters that grow fast enough to harvest before they get disease = harvest before they get disease = AquacultureAquacultureIntroduce triploid Asian Introduce triploid Asian C. C. ariakensisariakensis oysters = oysters = AquacultureAquacultureIntroduce diploid Asian Introduce diploid Asian C. C. ariakensisariakensis oysters = oysters = AquacultureAquaculture

Traditional Fisheries Management is Largely Irrelevant!Traditional Fisheries Management is Largely Irrelevant!

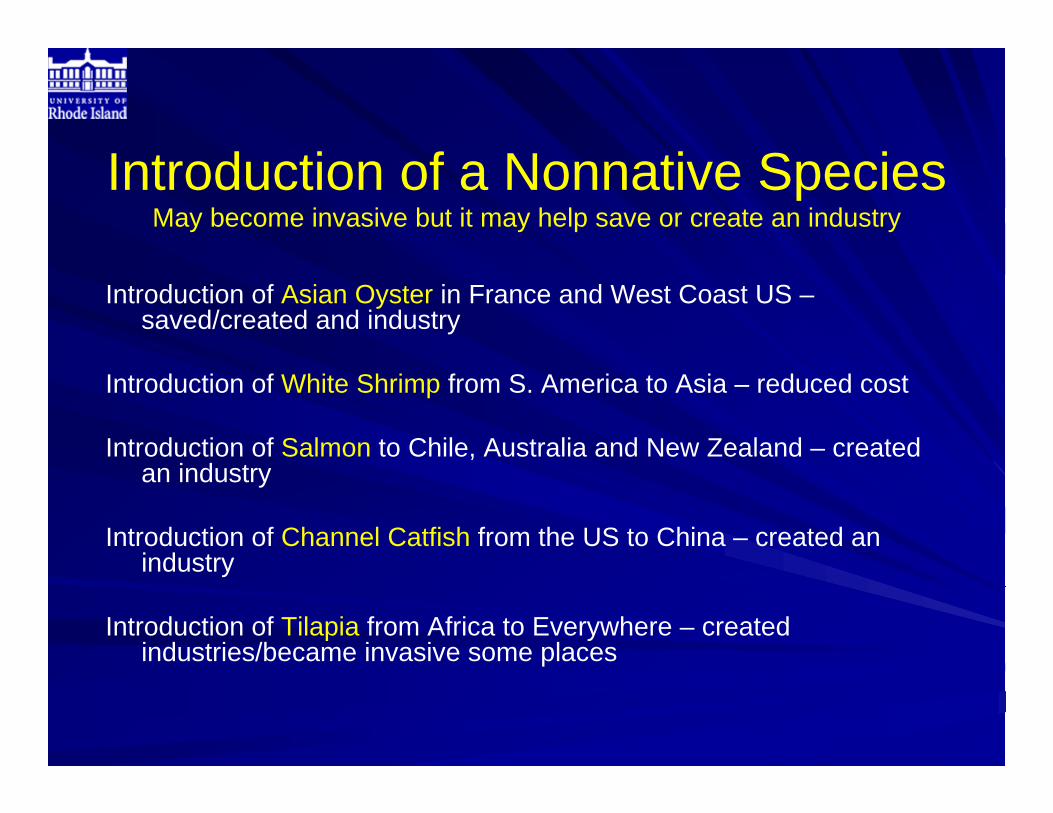

Introduction of a Nonnative SpeciesMay become invasive but it may help save or create an industry

Introduction of Asian Oyster in France and West Coast US –saved/created and industry

Introduction of White Shrimp from S. America to Asia – reduced cost

Introduction of Salmon to Chile, Australia and New Zealand – created an industry

Introduction of Channel Catfish from the US to China – created an industry

Introduction of Tilapia from Africa to Everywhere – created industries/became invasive some places

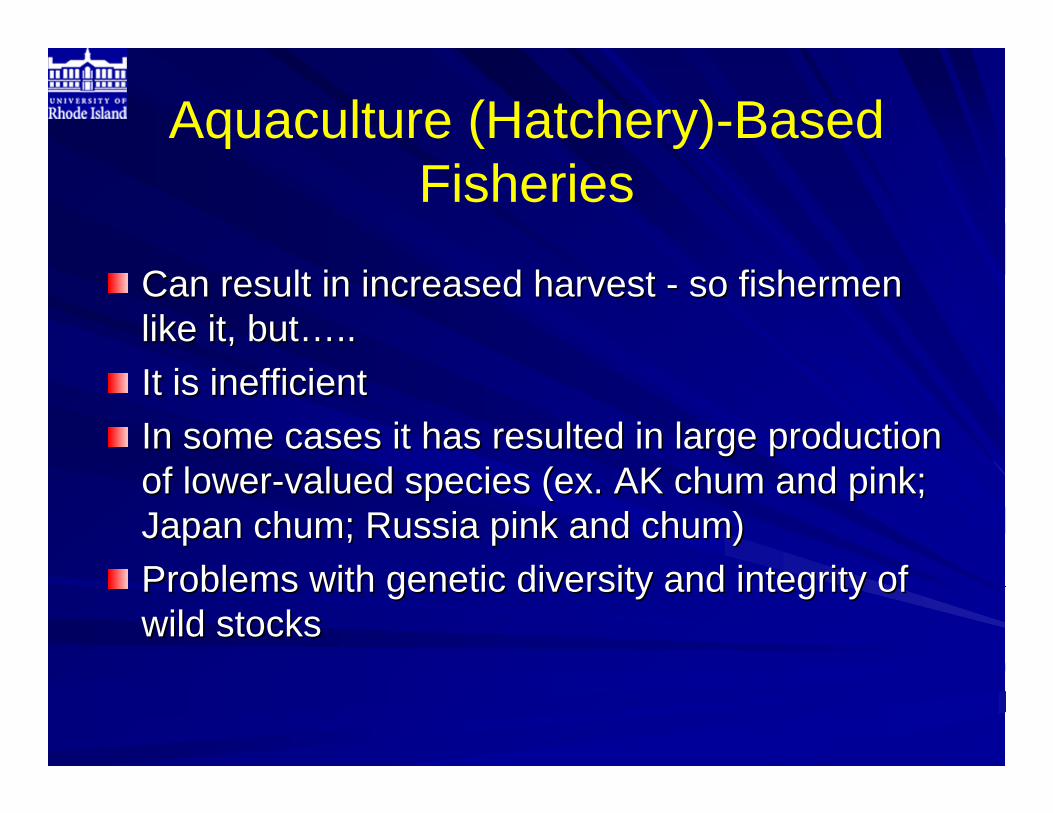

Aquaculture (Hatchery)-Based Fisheries

Can result in increased harvest Can result in increased harvest -- so fishermen so fishermen like it, butlike it, but……....It is inefficientIt is inefficientIn some cases it has resulted in large production In some cases it has resulted in large production of lowerof lower--valued species (ex. AK chum and pink; valued species (ex. AK chum and pink; Japan chum; Russia pink and chum)Japan chum; Russia pink and chum)Problems with genetic diversity and integrity of Problems with genetic diversity and integrity of wild stockswild stocks

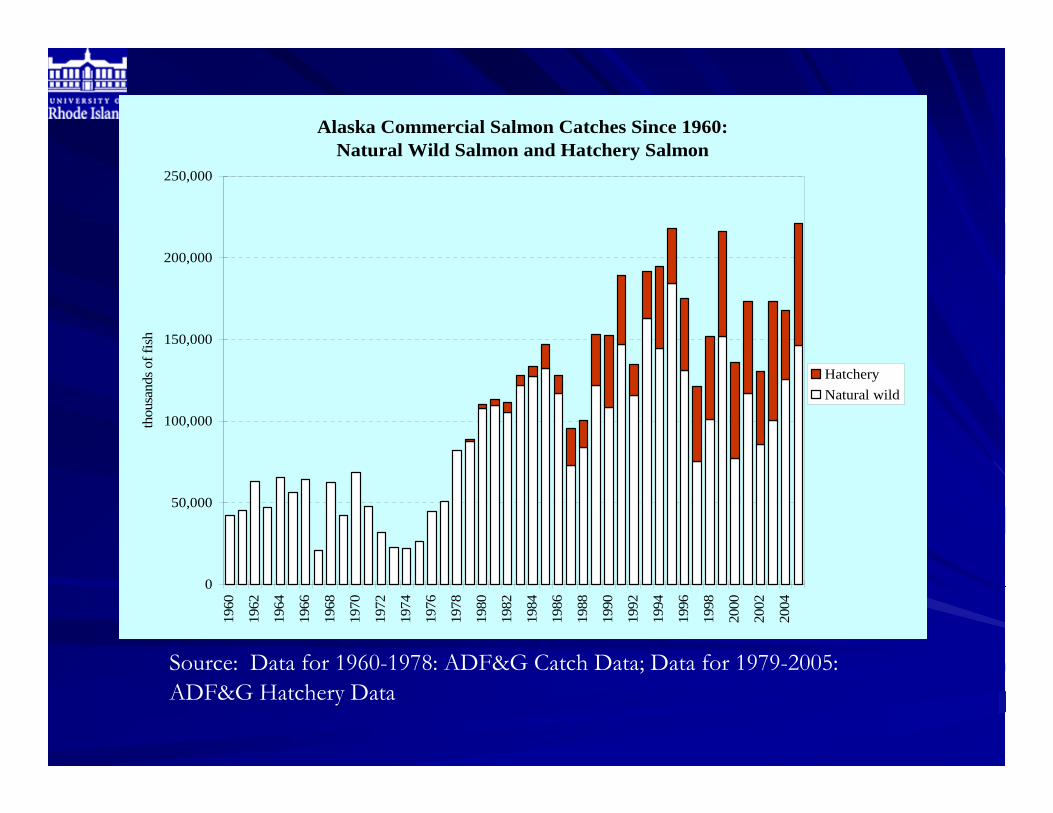

Alaska Commercial Salmon Catches Since 1960: Natural Wild Salmon and Hatchery Salmon

0

50,000

100,000

150,000

200,000

250,000

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

thou

sand

s of f

ish

HatcheryNatural wild

Source: Data for 1960-1978: ADF&G Catch Data; Data for 1979-2005: ADF&G Hatchery Data

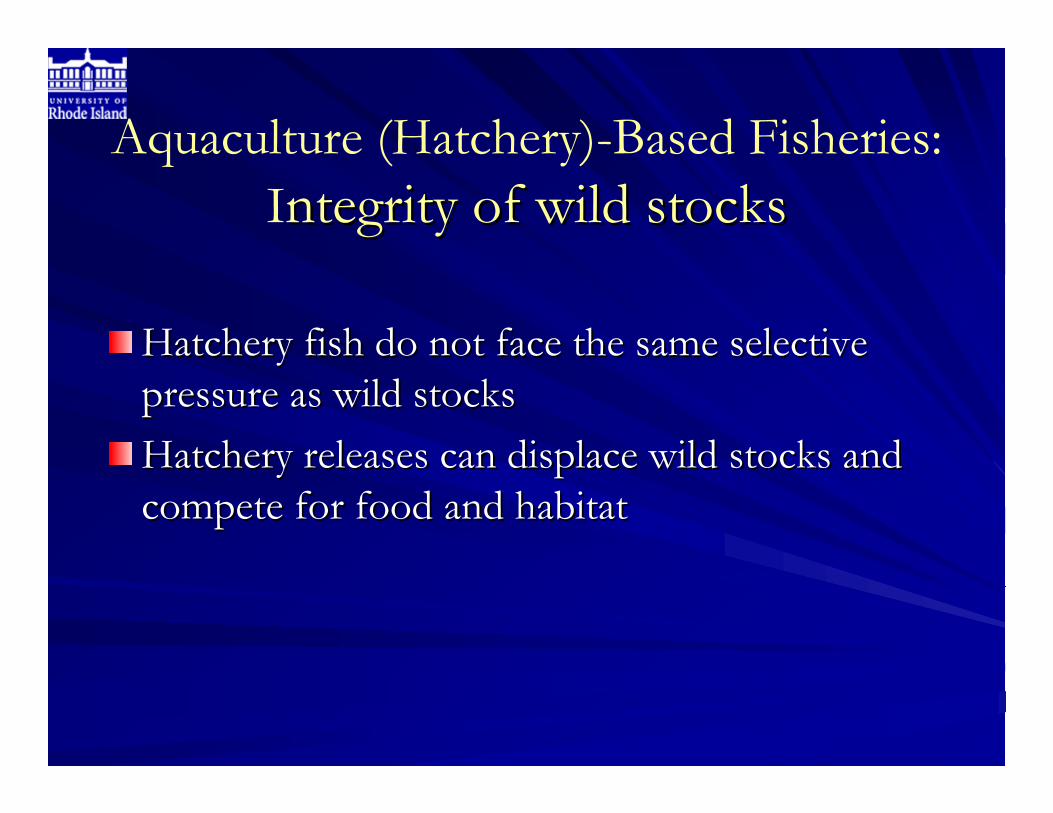

Aquaculture (Hatchery)-Based Fisheries: Integrity of wild stocksntegrity of wild stocks

Hatchery fish do not face the same selective Hatchery fish do not face the same selective pressure as wild stockspressure as wild stocksHatchery releases can displace wild stocks and Hatchery releases can displace wild stocks and compete for food and habitatcompete for food and habitat

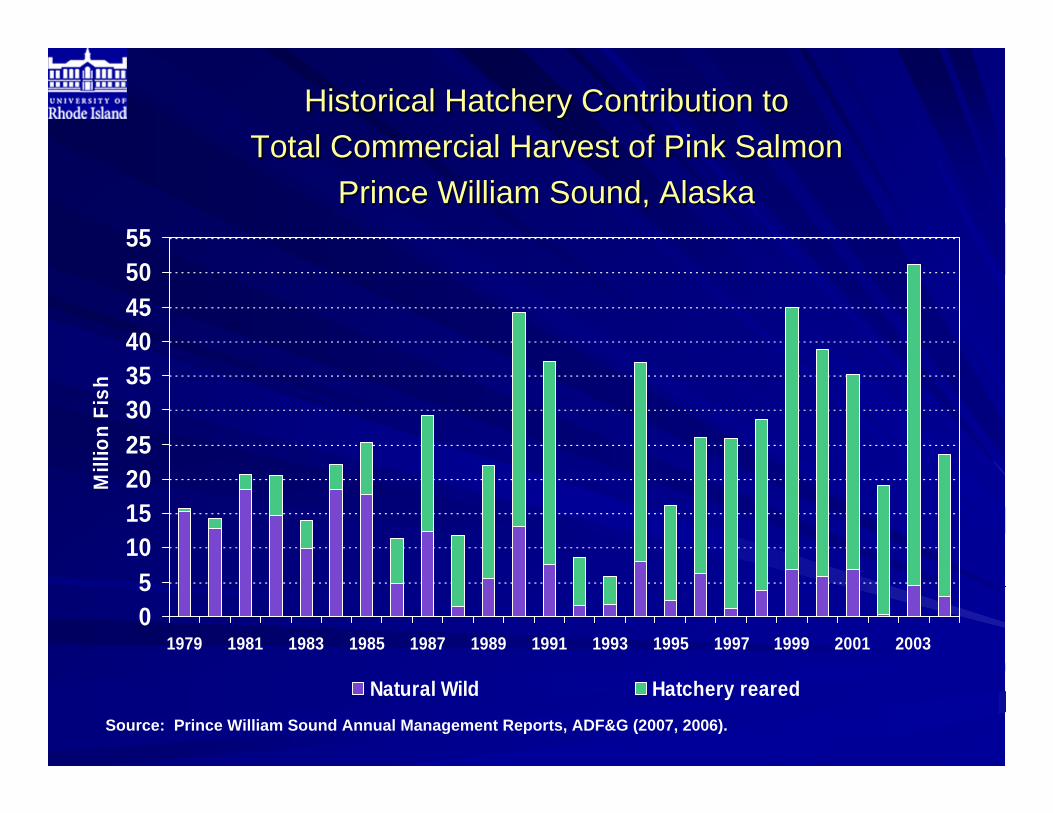

Historical Hatchery Contribution to Historical Hatchery Contribution to Total Commercial Harvest of Pink Salmon Total Commercial Harvest of Pink Salmon

Prince William Sound, AlaskaPrince William Sound, Alaska

Source: Prince William Sound Annual Management Reports, ADF&G (2007, 2006).

05

10152025303540455055

1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

Mill

ion

Fish

Natural Wild Hatchery reared

Aquaculture and HabitatAquaculture and Habitat

Negative for wild fish stocksNegative for wild fish stocksShrimp farms in the estuary Shrimp farms in the estuary -- mangrovemangroveExcessive finfish cage culture and pollutionExcessive finfish cage culture and pollution

Positive for wild fish stocksPositive for wild fish stocksOyster reef buildingOyster reef buildingRotational Management of Scallops (like Rotational Management of Scallops (like forestry) forestry) –– creates marine protected areas creates marine protected areas (fallow fields) (fallow fields)

Aquaculture and fisheries interact in the Aquaculture and fisheries interact in the ecosystem.ecosystem.

Aquaculture Aquaculture isis a fisheries management option. a fisheries management option.

Very little economic research has been done to Very little economic research has been done to evaluate the interactions.evaluate the interactions.

Aquaculture and Fisheries: Aquaculture and Fisheries: International Trade and the MarketInternational Trade and the Market

Aquaculture has had a Tremendous Aquaculture has had a Tremendous Influence on Fisheries through Influence on Fisheries through

International Trade and the MarketInternational Trade and the Market

Increased supply has influenced prices Increased supply has influenced prices –– Influenced effort in some fisheries (ex. salmon) Influenced effort in some fisheries (ex. salmon)

Changed consumer behavior and developed new markets Changed consumer behavior and developed new markets (ex. catfish) (ex. catfish) Accelerated globalization (ex. shrimp, tilapia, salmon)Accelerated globalization (ex. shrimp, tilapia, salmon)–– Reaction more trade barriersReaction more trade barriers

Increased concentration and vertical integration (ex. salmon)Increased concentration and vertical integration (ex. salmon)New product forms and improved quality and consistency (ex. New product forms and improved quality and consistency (ex. tilapia, salmon)tilapia, salmon)Forward thinking and market driven (ex. salmon, oysters)Forward thinking and market driven (ex. salmon, oysters)Improved stability and reduce uncertainty (ex. salmon)Improved stability and reduce uncertainty (ex. salmon)

Growing Market Share and Growing Market Share and Product InnovationProduct Innovation

Consistently AvailableConsistently AvailableConsistent QualityConsistent QualityStable or Declining CostStable or Declining CostMeet Consumer DemandsMeet Consumer Demands

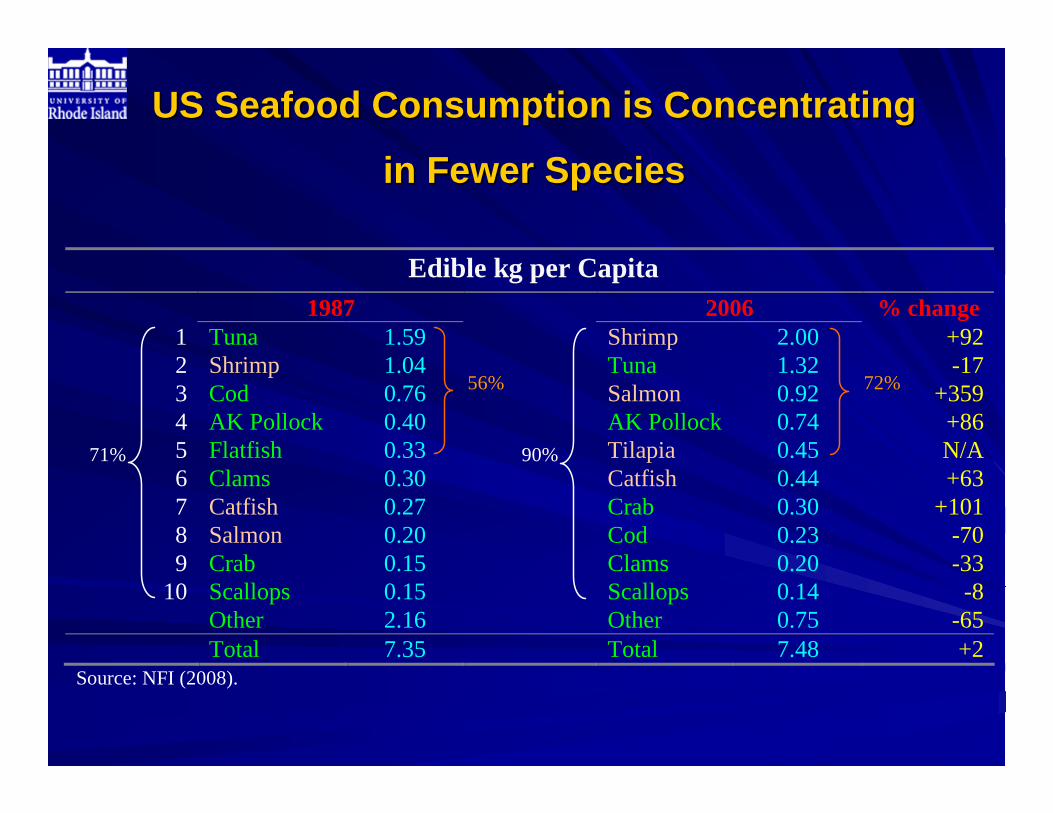

Edible kg per Capita

1987 2006 % change 1 Tuna 1.59 Shrimp 2.00 +92 2 Shrimp 1.04 Tuna 1.32 -17 3 Cod 0.76 Salmon 0.92 +359 4 AK Pollock 0.40 AK Pollock 0.74 +86 5 Flatfish 0.33 Tilapia 0.45 N/A 6 Clams 0.30 Catfish 0.44 +63 7 Catfish 0.27 Crab 0.30 +101 8 Salmon 0.20 Cod 0.23 -70 9 Crab 0.15 Clams 0.20 -33

10 Scallops 0.15 Scallops 0.14 -8 Other 2.16 Other 0.75 -65 Total 7.35 Total 7.48 +2

Source: NFI (2008).

71% 90%

56% 72%

US Seafood Consumption is ConcentratingUS Seafood Consumption is Concentrating

in Fewer Speciesin Fewer Species

U.S. Retail Sales, 1994 vs. 2007U.S. Retail Sales, 1994 vs. 2007Source: Source: Seafood BusinessSeafood Business

1994 2007

1 Shrimp Shrimp

2 Salmon Salmon

3 Pollock, Cod, Haddock Crab

4 Catfish Tilapia

5 Flounder Catfish

Best Sellers (Seafood Case)

Sources: Perkins, C. (1994) and Robinson, F. (2004)

Large Retailer and Chain Large Retailer and Chain Restaurant Demands have:Restaurant Demands have:

Encouraged vertical and horizontal integrationEncouraged vertical and horizontal integrationStimulated globalizationStimulated globalizationEncouraging various certification programs Encouraging various certification programs ––Sustainability and SafetySustainability and Safety–– Farmed SalmonFarmed Salmon–– Wild SalmonWild Salmon–– ShrimpShrimp–– Alaska PollockAlaska Pollock

Note on Selling Sustainability and Health Note on Selling Sustainability and Health to US Consumersto US Consumers

Sustainability and SafetySustainability and Safety are essentially required esp. now that are essentially required esp. now that companies like WalMart and Darden Restaurants are involvedcompanies like WalMart and Darden Restaurants are involvedHealthfulnessHealthfulness is important but secondary to the US consumer is important but secondary to the US consumer –– We We are Fat!are Fat!Priorities for the Bulk of Real Consumers Priorities for the Bulk of Real Consumers (not Green Peace members, (not Green Peace members, Gourmets, pregnant mothers or movie stars)Gourmets, pregnant mothers or movie stars)–– ConvenienceConvenience–– TasteTaste–– PricePrice

–– Perceived ValuePerceived Value

Photo: Jingjie Chu

Photo: Jingjie Chu

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

2000

US$

/lb

Wild Cod, fillet,frozen

Farmed Salmon,2-3 lb fillet ,fresh

Farmed Catfish,fillet, frozen

RealReal Price Trends of SeafoodPrice Trends of Seafood

Sources: USDA, 1990-2008; Urner-Barry Publications, 1990- 2008; USDC/NMFS, 1990-2008.

-20

-15

-10

-5

0

5

10

15

20Ja

n-85

Jan-

86

Jan-

87

Jan-

88

Jan-

89

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

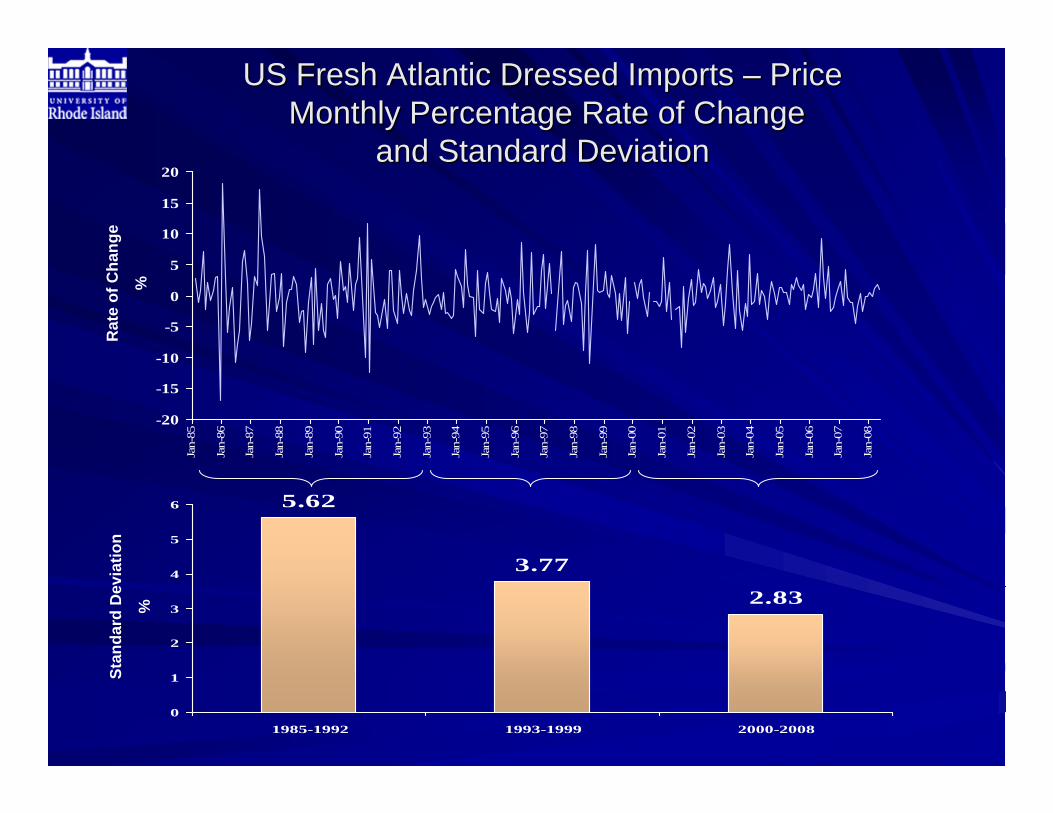

US Fresh Atlantic Dressed Imports US Fresh Atlantic Dressed Imports –– PricePriceMonthly Percentage Rate of Change Monthly Percentage Rate of Change

and Standard Deviationand Standard Deviation

5.62

3.77

2.83

0

1

2

3

4

5

6

1985-1992 1993-1999 2000-2008

Rat

e of

Cha

nge

%St

anda

rd D

evia

tion

%

Cost Share: Aquaculture vs. Fishery Item Aquaculture Fishery Labor 4-10% 25-45% Maintenance 2-4% 9-23% Fuel 1-4% 4-11% Fingerlings 2-15% — Feed 40-60% —

Cost Factors Influencing Cost Factors Influencing CompetitivenessCompetitiveness

AquacultureAquacultureBiotechnologyBiotechnologyDisease ManagementDisease ManagementFeed Cost/ QualityFeed Cost/ QualityConsolidation/ Consolidation/ RestructuringRestructuringFarm ManagementFarm ManagementRegulationsRegulations

FisheryFisheryFisheries GovernanceFisheries GovernanceFish StockFish StockEnvironmentEnvironmentCrewCrew--share share ArrangementsArrangementsMaintenance/RepairMaintenance/Repair

“Technical Progress has been Futile”

Rolf Willmann, FAO, Loss in Resource Rents Session, IIFET 2008

Production Cost: Salmon Aquaculture vs. Production Cost: Salmon Aquaculture vs. Capture FisheriesCapture Fisheries

0

10

20

30

40

50

60

70

80

90

100

1985 1988 1991 1994 1997 2000 2003 2006

2006

NO

K/kg

Export Price Production CostSources: Norwegian Directorate of Fisheries (2005); Guttormsen (2007).

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

1985 1988 1991 1994 1997 2000 2003 200620

06 U

S$/k

g

Ex-vessel Price Production Cost

Salmon Aquaculture in NorwayBristol Bay Drift Gillnet Sockeye Salmon Fishery

Sources: ADF&G (2007); Valderrama (2008).

Norway: Salmon FarmingNorway: Salmon Farming

Photos: J.L. Anderson

Alaska’s Bristol Bay drift gillnet salmon fishery -2005.

(Photograph by Bart Eaton, Source: Gunnar Knapp)

Wild Salmon Wild Salmon FisheryFishery

MSC Certified MSC Certified Sustainable Alaska Sustainable Alaska Sockeye FisherySockeye Fishery

Norway: Salmon ProcessingNorway: Salmon Processing

Photos: J.L. Anderson

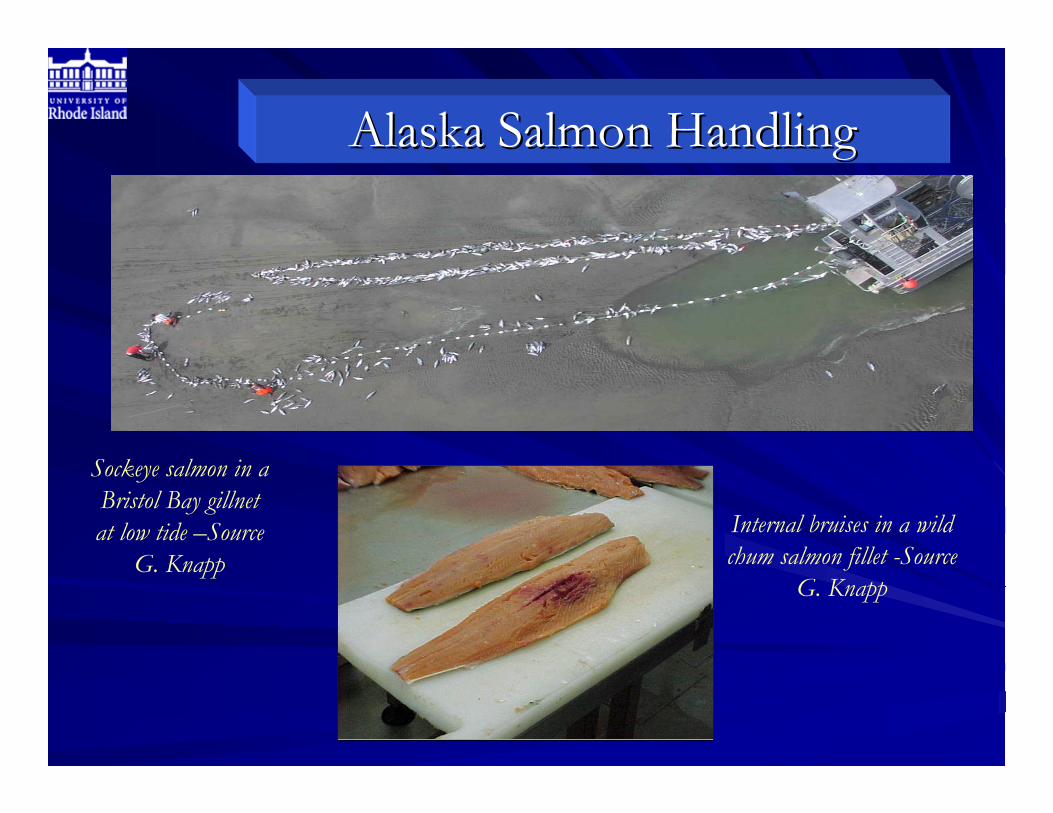

Internal bruises in a wild chum salmon fillet -Source

G. Knapp

Alaska Salmon Handling Alaska Salmon Handling

Sockeye salmon in a Bristol Bay gillnet at low tide –Source

G. Knapp

Permit Market Value and Permit Market Value and Percent of Permits Fished in the Bristol Bay Sockeye Fishery Percent of Permits Fished in the Bristol Bay Sockeye Fishery

Source: CFEC (2007).

0%

20%

40%

60%

80%

100%

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Perc

ent

Perm

its

Fish

ed

0

60

120

180

240

300

Tho

usan

d D

olla

rs

Permit Market Value Percent Permits Fished

Drift Gillnet Fishery

Competition with farmed salmon has Competition with farmed salmon has increased efficiency through reduction of increased efficiency through reduction of efforteffort–– Bristol Bay Salmon, AlaskaBristol Bay Salmon, Alaska

Competition with farmed salmon has Competition with farmed salmon has increased efficiency through attempts to increased efficiency through attempts to restructure the fleet restructure the fleet –– Chignik Salmon Coop., AlaskaChignik Salmon Coop., Alaska

The Aquaculture Sector Creates The Aquaculture Sector Creates New MarketsNew Markets

Salmon Farmers created new markets in Salmon Farmers created new markets in southern USsouthern USFarmed Salmon created new markets premium Farmed Salmon created new markets premium wild salmonwild salmonNew Products New Products –– PinPin--BoneBone--Out Salmon FilletOut Salmon FilletNew markets are all being developed by New markets are all being developed by aquaculturistsaquaculturists: ex. sturgeon, barramundi, tilapia, : ex. sturgeon, barramundi, tilapia, basabasa, oysters, cobia, mussels and many other , oysters, cobia, mussels and many other species species

0

50

100

150

200

250

300

350

400

450

500

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Diesel Fuel: Diesel Fuel: Producer Price Index Producer Price Index 1990 = 1001990 = 100

Source: U.S. Bureau of Labor Statistics (2008).

Implications of Rising Fuel CostImplications of Rising Fuel Cost

Stronger competitive position of Stronger competitive position of farmedfarmed fish fish and shellfish and shellfish

over:over:WildWild--caughtcaught seafood seafood

0

300

600

900

1,200

1,500

1991 1993 1995 1997 1999 2001 2003 2005 2007

US$

/MT

Fishmeal

Soybean meal

Fishmeal and Soymeal PricesFishmeal and Soymeal Prices

Fishmeal: 64/65%, any origin, wholesale, CIF Hamburg.Soybean meal: 44%, any origin, CIF Rotterdam/Hamburg.

Source: Oil World / GLOBEFISH (2007).

Implications of Rising Feed CostImplications of Rising Feed Cost

Stronger competitive position of farmed Stronger competitive position of farmed shellfish (clams, oyster, mussels, scallops) shellfish (clams, oyster, mussels, scallops)

compared to: compared to: Farmed Finfish and Shrimp Farmed Finfish and Shrimp

Beef, Pork and ChickenBeef, Pork and Chicken

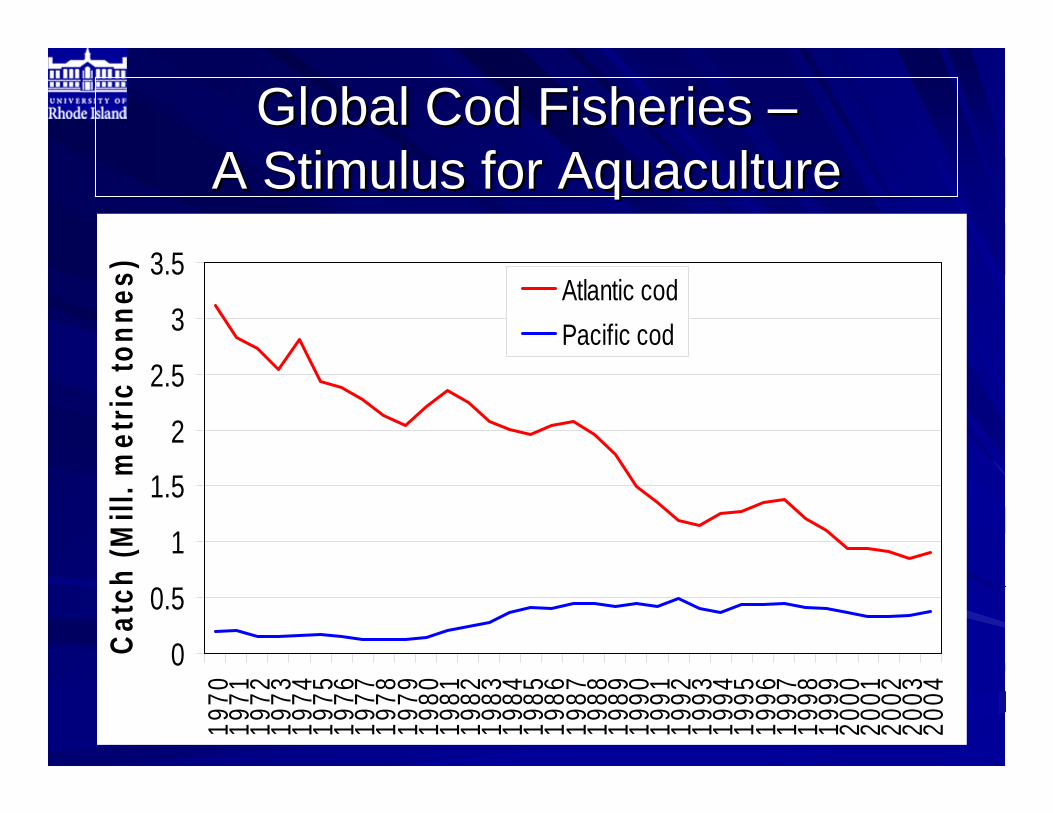

Global Cod Fisheries Global Cod Fisheries ––A Stimulus for AquacultureA Stimulus for Aquaculture

0

0.5

1

1.5

2

2.5

3

3.519

7019

7119

7219

7319

7419

7519

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

04

Cat

ch (M

ill. m

etric

tonn

es)

Atlantic codPacific cod

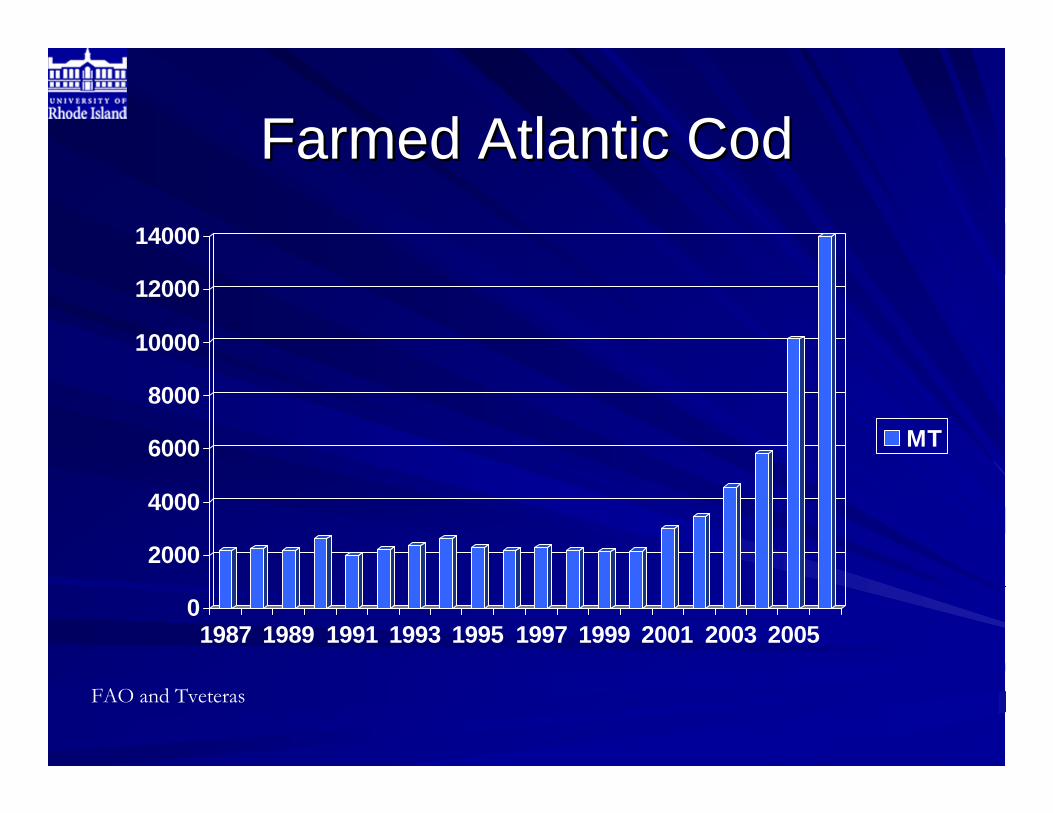

Farmed Atlantic CodFarmed Atlantic Cod

0

2000

4000

6000

8000

10000

12000

14000

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

MT

FAO and Tveteras

World Tilapia Production World Tilapia Production

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Mill

ion

MT

Other

Tanzania

Mexico

Taiwan

Brazil

Thailand

Uganda

Philippines

Indonesia

Egypt

China

Global production of tilapia grew at an average annual rate of 7% (farmed 12%) between 1981 and 2005.

Source: FISHSTAT (2007).

Photo: J.L. Anderson

0

20

40

60

80

100

120

140

160

180

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

MT

(000

's)

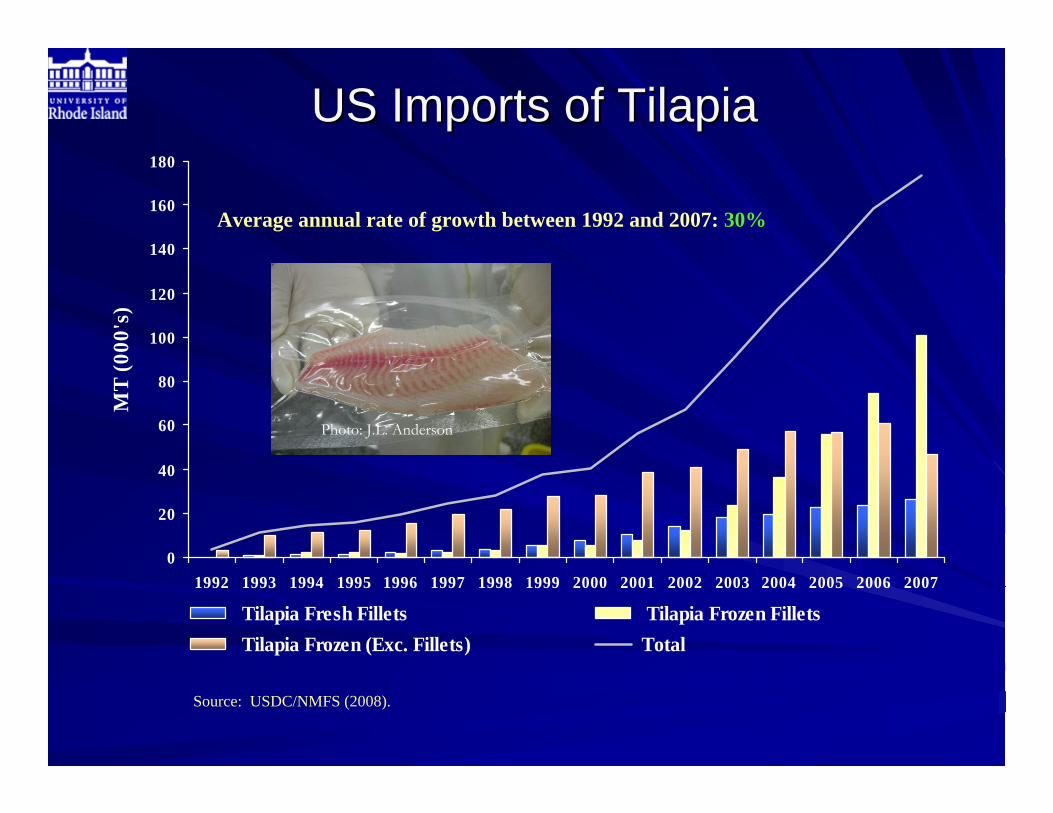

Tilapia Fresh Fillets Tilapia Frozen Fillets Tilapia Frozen (Exc. Fillets) Total

US Imports of TilapiaUS Imports of Tilapia

Source: USDC/NMFS (2008).

Average annual rate of growth between 1992 and 2007: 30%

Photo: J.L. Anderson

Tilapia MarketTilapia MarketVery rapid growthVery rapid growthCompetition for flatfish, Competition for flatfish, snapper and other snapper and other whitefishwhitefishFillets Fillets –– Market innovationMarket innovationMany environmental Many environmental NGOs are positive about NGOs are positive about tilapiatilapiaIncrease globalizationIncrease globalizationWalWal--MartMart

Photo: J.L. Anderson

U.S. Imports of Salmon vs. TilapiaU.S. Imports of Salmon vs. TilapiaActual (1989Actual (1989--2006) and Forecast (20072006) and Forecast (2007--

2015)2015)

0

50

100

150

200

250

300

350

400

450

500

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

MT

(000

's)

Salmon & Trout Tilapia

360

Source: USDC (2006); Seafood Market Analyst, SeafoodReport.com: U.S. Imports Edition, 2006.Upper and lower bounds represent 95% confidence intervals.

437

Expect Continued Rapid GrowthExpect Continued Rapid GrowthRough Est. 2006Rough Est. 2006

Tilapia Tilapia –– 2.8 million MT2.8 million MTPangasius Pangasius –– over 500,000 MTover 500,000 MTChannel Catfish Channel Catfish –– over 400,000 MTover 400,000 MTFlatfish Flatfish –– 140,000 MT 140,000 MT Barramundi Barramundi –– 35,000 MT35,000 MTCod Cod –– 15,000 MT15,000 MTCobia Cobia -- ??

Blue Revolution?Blue Revolution?

With all this technological change, one might With all this technological change, one might expect countries that think they are expect countries that think they are

adaptive and entrepreneurial adaptive and entrepreneurial -- like the US like the US –– to be leadersto be leaders

Maybe NotMaybe NotTimes are ChangingTimes are Changing

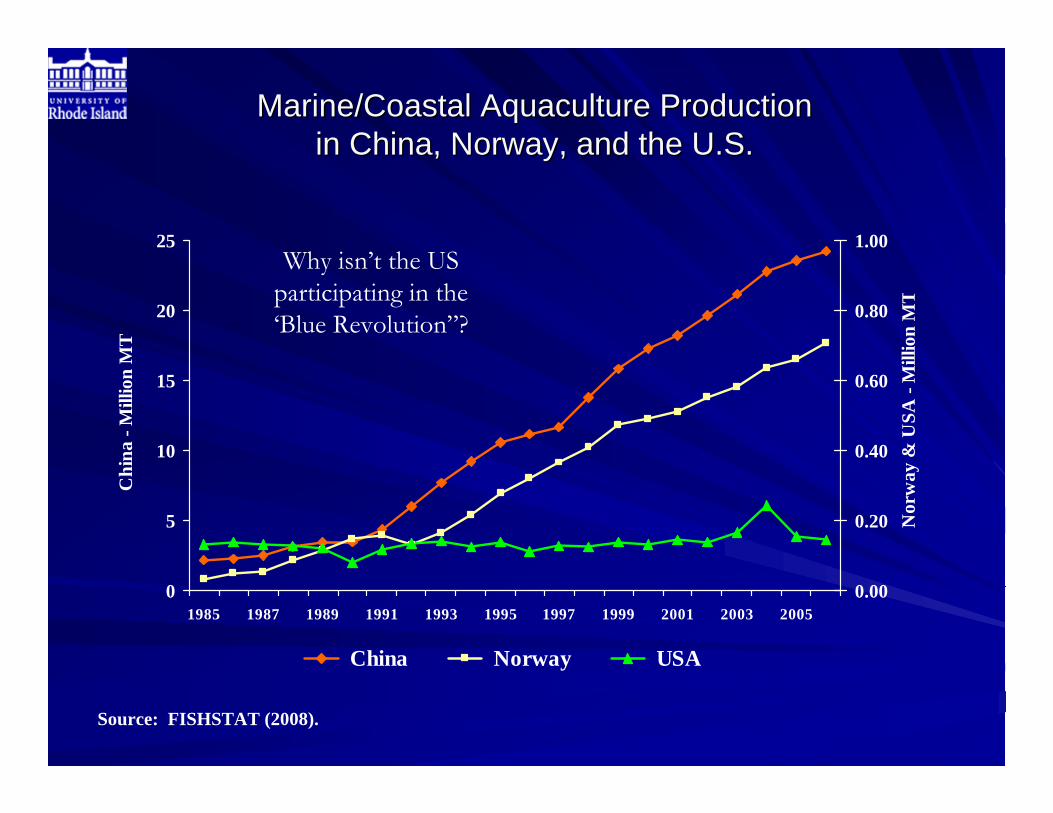

Marine/Coastal Aquaculture Production Marine/Coastal Aquaculture Production in China, Norway, and the U.S.in China, Norway, and the U.S.

0

5

10

15

20

25

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Chi

na -

Mill

ion

MT

0.00

0.20

0.40

0.60

0.80

1.00

Nor

way

& U

SA -

Mill

ion

MT

China Norway USA

Source: FISHSTAT (2008).

Why isn’t the US participating in the ‘Blue Revolution”?

Fisheries Management Fisheries Management --““The integrated process of information gathering, analysis, The integrated process of information gathering, analysis,

planning, decisionplanning, decision--making, allocation of resources and making, allocation of resources and formulation and enforcement of fishery regulations by which the formulation and enforcement of fishery regulations by which the fisheryfishery

management authoritymanagement authority controlscontrols the the present and future behavior of present and future behavior of interested parties in the fisheriesinterested parties in the fisheries,,

in order to ensure the continued productivity of the living in order to ensure the continued productivity of the living resources.resources.”” (FAO 1999). (FAO 1999).

The difference between traditional fisheries The difference between traditional fisheries management and management and ““aquacultureaquaculture”” management management

boils down to:boils down to:Who is in CONTROLWho is in CONTROL

What is being CONTROLLEDWhat is being CONTROLLED

Traditional fisheries management – Governing institutions CONTROL individual or group

behavior – but not the aquatic organism

Aquaculture– The individual or group, CONTROLS the production, harvest and

marketing of the aquatic organism - the individual or group receives rights for CONTROL from by the governing institution

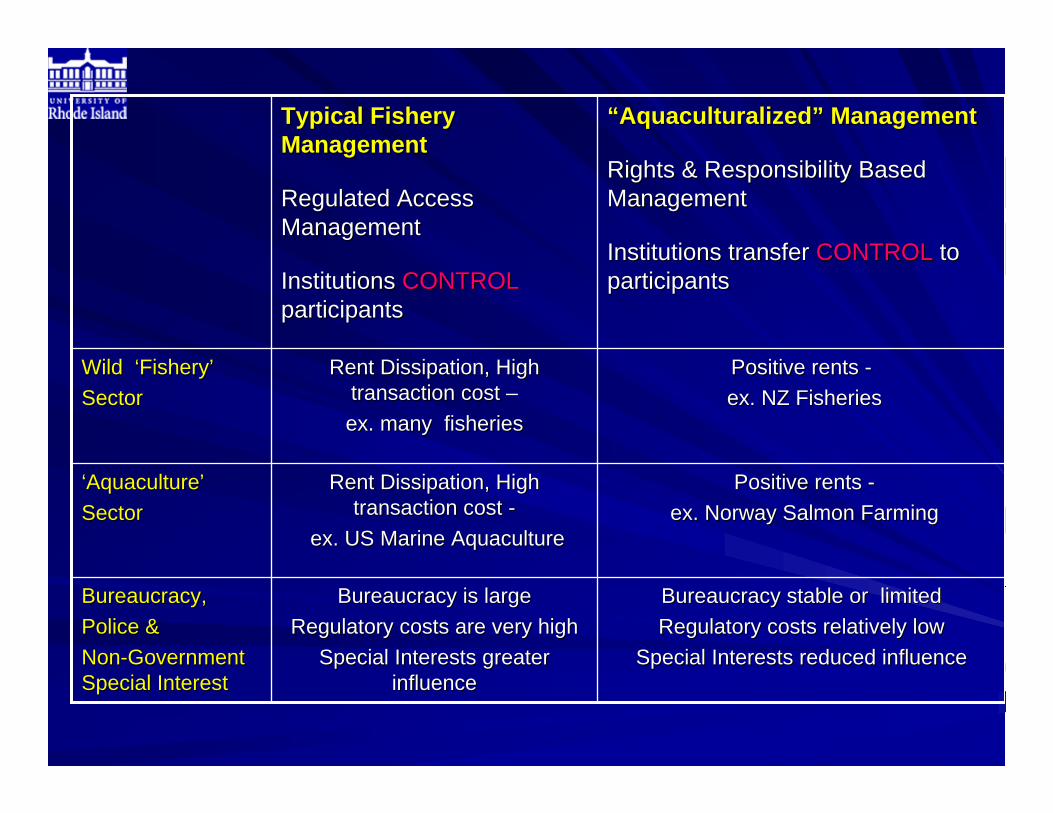

Positive rents Positive rents --ex. Norway Salmon Farmingex. Norway Salmon Farming

Rent Dissipation, High Rent Dissipation, High transaction cost transaction cost --

ex. US Marine Aquacultureex. US Marine Aquaculture

‘‘AquacultureAquaculture’’SectorSector

Bureaucracy stable or limitedBureaucracy stable or limitedRegulatory costs relatively lowRegulatory costs relatively low

Special Interests reduced influenceSpecial Interests reduced influence

Bureaucracy is largeBureaucracy is largeRegulatory costs are very highRegulatory costs are very high

Special Interests greater Special Interests greater influenceinfluence

Bureaucracy,Bureaucracy,Police &Police &NonNon--Government Government Special InterestSpecial Interest

Positive rents Positive rents --ex. NZ Fisheriesex. NZ Fisheries

Rent Dissipation, High Rent Dissipation, High transaction cost transaction cost ––ex. many fisheriesex. many fisheries

Wild Wild ‘‘FisheryFishery’’SectorSector

““AquaculturalizedAquaculturalized”” ManagementManagement

Rights & Responsibility Based Rights & Responsibility Based ManagementManagement

Institutions transfer Institutions transfer CONTROLCONTROL to to participantsparticipants

Typical Fishery Typical Fishery ManagementManagement

Regulated Access Regulated Access Management Management

Institutions Institutions CONTROL CONTROL participantsparticipants

““AquaculturizationAquaculturization”” of Fisheries of Fisheries -- Taking ControlTaking ControlAssign Ownership RightsAssign Ownership Rights

Individual or community fisheries quota Individual or community fisheries quota Cooperative area management fisheriesCooperative area management fisheries

Plant the Field / Breed the Animals: Plant the Field / Breed the Animals: Salmon hatcheries (nearly 40% of AK harvest originates in hatcheSalmon hatcheries (nearly 40% of AK harvest originates in hatcheries)ries)Oyster/scallop enhancementOyster/scallop enhancement

Crop and Forest Rotation Crop and Forest Rotation Rotational Scallop FisheriesRotational Scallop Fisheries

Fallow Fields/Range Management Fallow Fields/Range Management Marine Reserves/SanctuariesMarine Reserves/Sanctuaries

Land/Habitat RestorationLand/Habitat RestorationRebuild Oyster Beds Rebuild Oyster Beds Remove damsRemove damsArtificial ReefsArtificial Reefs

Feed/Fertilize Feed/Fertilize Maine Lobsters get ~ 80% of the feed from baitMaine Lobsters get ~ 80% of the feed from baitCaptureCapture--Based Aquaculture Based Aquaculture -- BluefinBluefin Tuna farmingTuna farming

Control Predators/Provide Protection Control Predators/Provide Protection Lobster pots Lobster pots Harvest starfish in oyster bedsHarvest starfish in oyster beds

Eliminate Costless Access (Cattle Rustlers) Eliminate Costless Access (Cattle Rustlers) Eliminate unregulated open accessEliminate unregulated open access

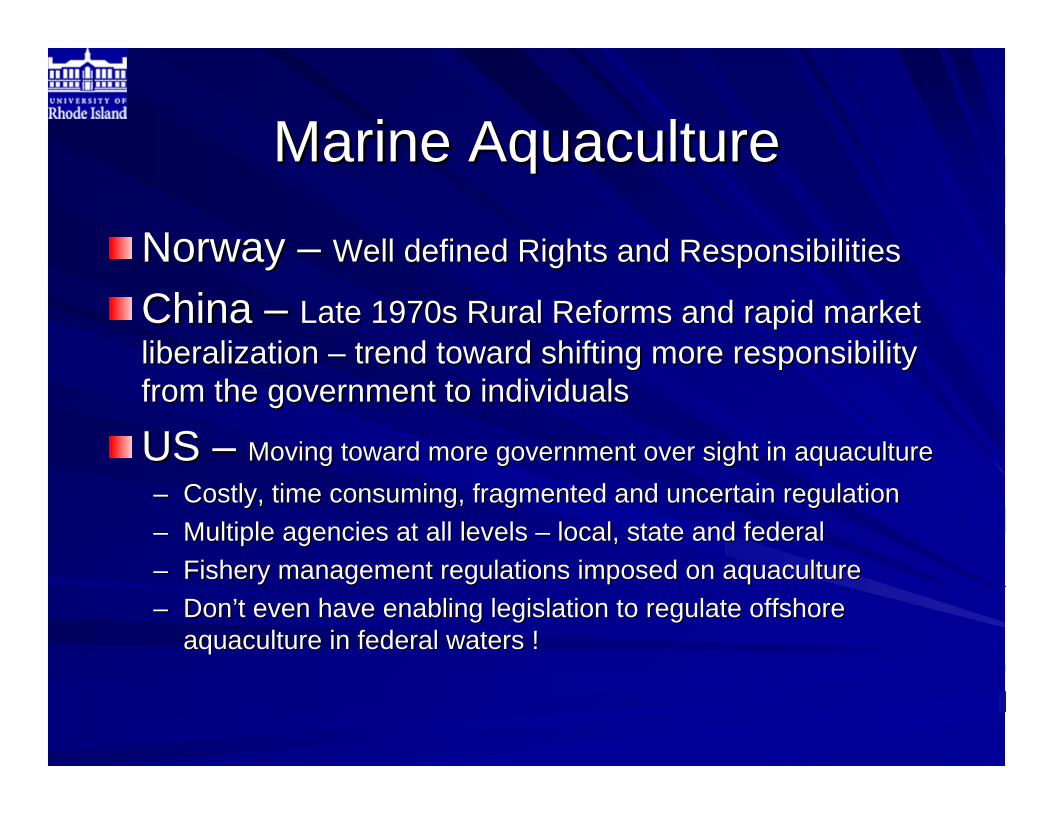

Marine AquacultureMarine Aquaculture

Norway Norway –– Well defined Rights and ResponsibilitiesWell defined Rights and Responsibilities

China China –– Late 1970s Rural Reforms and rapid market ate 1970s Rural Reforms and rapid market liberalization liberalization –– trend toward shifting more responsibility trend toward shifting more responsibility from the government to individualsfrom the government to individuals

US US –– Moving toward more government over sight in aquacultureMoving toward more government over sight in aquaculture–– Costly, time consuming, fragmented and uncertain regulationCostly, time consuming, fragmented and uncertain regulation–– Multiple agencies at all levels Multiple agencies at all levels –– local, state and federal local, state and federal –– Fishery management regulations imposed on aquacultureFishery management regulations imposed on aquaculture–– DonDon’’t even have enabling legislation to regulate offshore t even have enabling legislation to regulate offshore

aquaculture in federal waters !aquaculture in federal waters !

Note on ChinaNote on China

Photo: Jingjie ChuPhoto: J.L. Anderson

Photo: Jingjie Chu

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Export ValueImport Value

China: International Seafood Trade China: International Seafood Trade ($1000)($1000)

China: #1 Seafood Exporter #6 Seafood ImporterSource: FishStat, FAO 2008

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006Export QuantityImport Quantity

China: International Seafood Trade China: International Seafood Trade (MT)(MT)

China: #1 Seafood Exporter #1 Seafood ImporterSource: FishStat, FAO 2008

US Imports from China: 2007US Imports from China: 2007(Source: NMFS 2008)(Source: NMFS 2008)

Breaded Shrimp Breaded Shrimp -- #1 #1 (Thailand #2) (Thailand #2)

Squid Squid -- #1 #1 (Thailand #2)(Thailand #2)

Scallops Scallops -- #1 #1 (Canada #2)(Canada #2)

Tilapia Tilapia -- #1 #1 (Ecuador #2) (Ecuador #2)

Alaska Pollock Alaska Pollock -- #1 #1 (South Korea #2)(South Korea #2)

Flatfish Fillets Flatfish Fillets -- #1 #1 (Canada #2)(Canada #2)

Cod Fillets Cod Fillets -- #1 #1 (Iceland #2)(Iceland #2)

2006: Total 2006: Total -- #1 in Quantity#1 in Quantity.. #3 in Value (Canada #1).. #3 in Value (Canada #1)

US Exports to China:2007US Exports to China:2007(Source: NMFS 2008)(Source: NMFS 2008)

Salmon Salmon -- #1#1 (Canada #2)(Canada #2)

Flatfish Flatfish -- #1#1 (Canada #2)(Canada #2)

Groundfish Groundfish -- #1#1 (Germany #2)(Germany #2)

Frozen Frozen -- #1#1 (Japan #2)(Japan #2)

Total Total -- #1 Quantity#1 Quantity: #3 Value : #3 Value (Japan #2 Quantity: # 1 Value)(Japan #2 Quantity: # 1 Value)

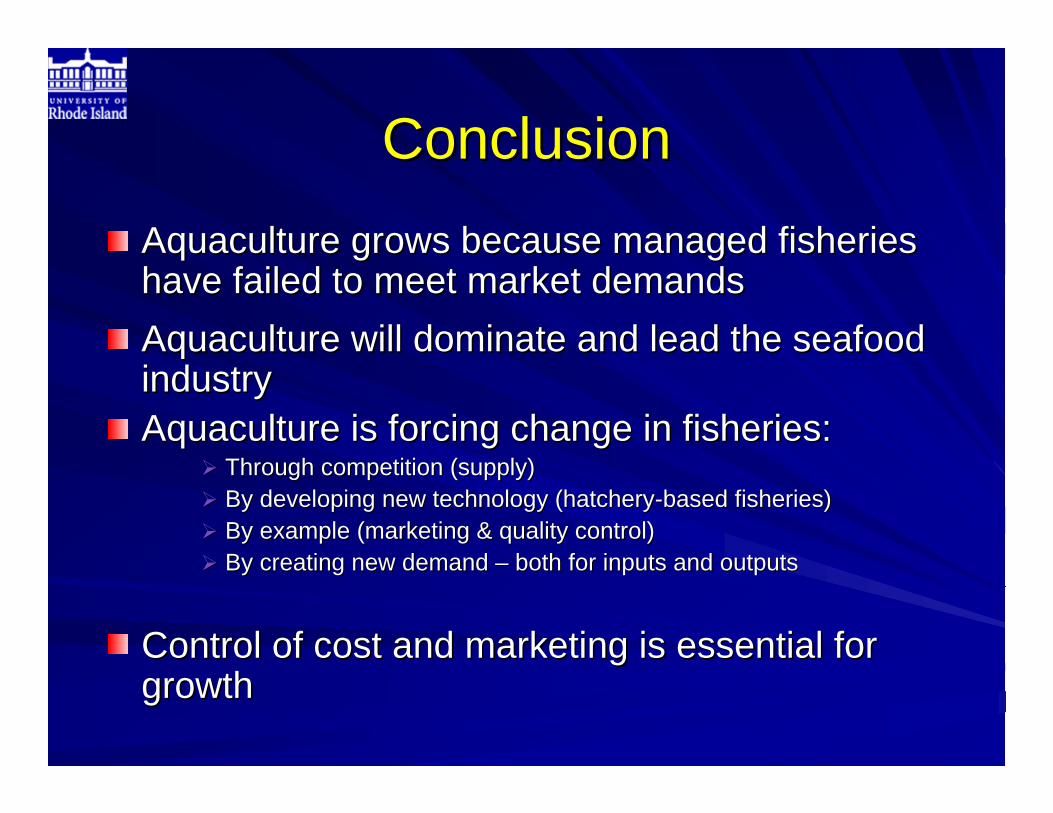

ConclusionConclusionAquaculture grows because managed fisheries Aquaculture grows because managed fisheries have failed to meet market demandshave failed to meet market demandsAquaculture will dominate and lead the seafood Aquaculture will dominate and lead the seafood industry industry Aquaculture is forcing change in fisheries: Aquaculture is forcing change in fisheries:

Through competition (supply)Through competition (supply)By developing new technology (hatcheryBy developing new technology (hatchery--based fisheries)based fisheries)By example (marketing & quality control)By example (marketing & quality control)By creating new demand By creating new demand –– both for inputs and outputsboth for inputs and outputs

Control of cost and marketing is essential for Control of cost and marketing is essential for growthgrowth

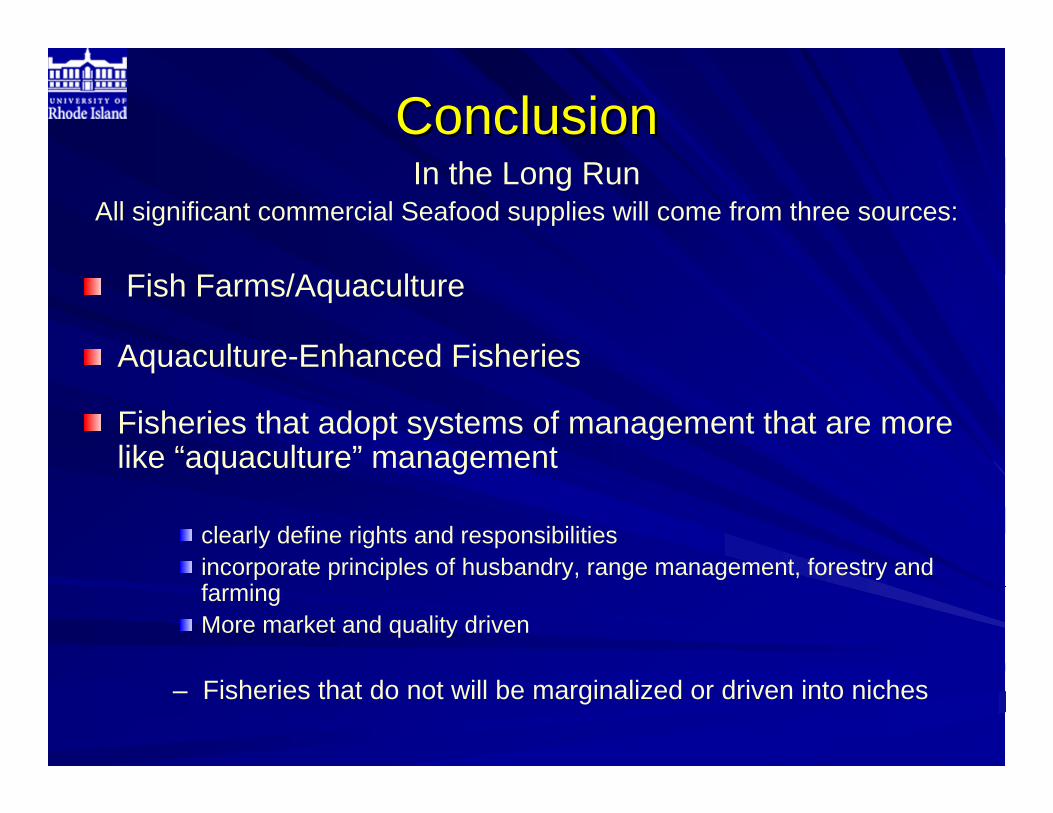

ConclusionConclusionIn the Long Run

All significant commercial Seafood supplies will come from three sources:

Fish Farms/Aquaculture

Aquaculture-Enhanced Fisheries

Fisheries that adopt systems of management that are more like “aquaculture” management

clearly define rights and responsibilitiesincorporate principles of husbandry, range management, forestry and farming More market and quality driven

– Fisheries that do not will be marginalized or driven into niches

Thank YouThank You