Emailing Fundamental Analysis

43

description

Emailing Fundamental Analysis

Transcript of Emailing Fundamental Analysis

3

5

7

9

11

13

15

40

50

60

70

80

90

100

110

120

2011 2012 2013 2014 2015

Sto

ck

Pri

ce

CEB

Price EPS

HIGH OIL PRICES

OVERCAPACITY

DECLINING OIL PRICES

INDUSTRY

RATIONALIZATION

PRICE WARS

Earnings

0.4

0.45

0.5

0.55

0.6

0.65

0.7

0.75

0.8

0.85

0.9

5

8

11

14

17

20

23

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15

Sto

ck

Pri

ce

DNL

Price EPS

MORE SPECIALIZATION

SIGNIFICANT MARGIN IMPROVEMENT

ASSET CONSOLIDATION

Earnings

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

10

15

20

25

30

35

40

45

2011 2012 2013 2014 2015

Sto

ck

Pri

ce

ALI

Price EPS

AGGRESSIVE LAUNCHES

MARGIN IMPROVEMENT

BRAND BUILDING

STRATEGIC LAND ACQUISITION

Earnings

3.4

3.9

4.4

4.9

5.4

5.9

6.4

6.9

7.4

20

50

80

110

140

170

200

230

2011 2012 2013 2014 2015

Sto

ck

Pri

ce

URC

Price EPS

INT’L BUSINESS

CONSOLIDATION

COFFEE MIXES

RTD TEA

LOW COMMODITY PRICES

Earnings

0.4

0.45

0.5

0.55

0.6

5

6

7

8

9

10

11

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

Sto

ck

Pri

ce

RWM

Price EPS

SOLAIRE OPENS CITY OF DREAMS OPENS

CHINA CRACKDOWN

Earnings

150

200

250

300

350

400

450

1500

2500

3500

4500

5500

6500

7500

8500

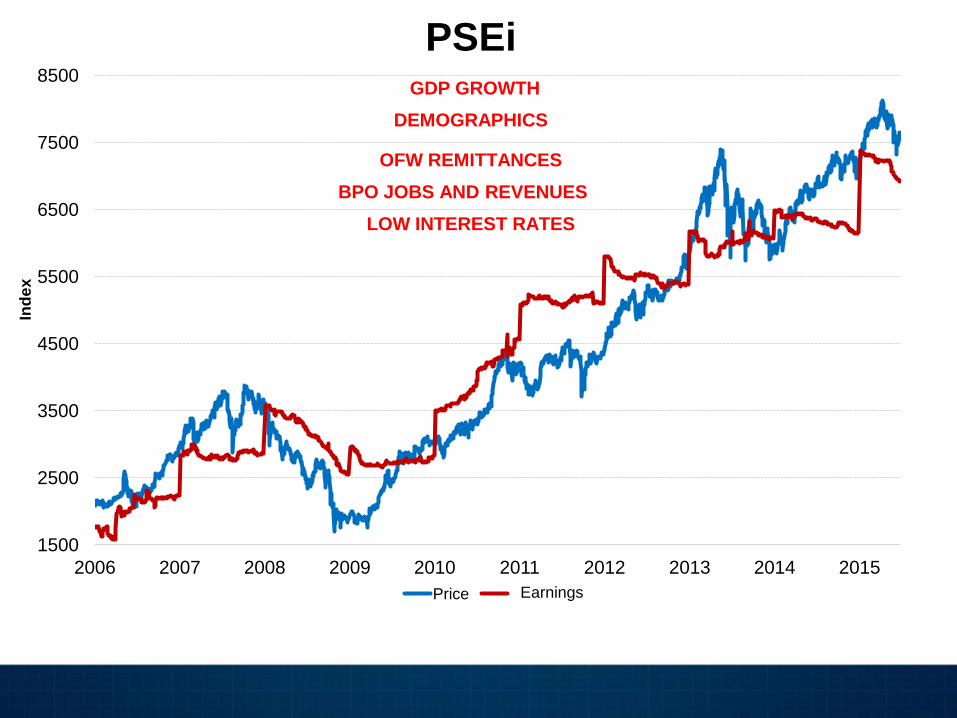

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ind

ex

PSEi

Price EPS

GDP GROWTH

OFW REMITTANCES

BPO JOBS AND REVENUES

DEMOGRAPHICS

LOW INTEREST RATES

Earnings

How do we develop expectations?

Top down approach

Macro-Economics Analysis

Industry Analysis

Company

Analysis

Top down approach

How do we develop expectations?

GDP growth, BPO and OFW

remittances, demographics, low

interest rates

Property Sector

Consumer Sector

Banking Sector

ALI, SMPH

JFC, DNL

Valuations

• Market price – Current price

• Fair Value (FV) estimate – Target price

Why is FV estimate important?

A benchmark based on earnings and

fundamentals

Absolute Valuation

• Discounted Cash Flow Method

ADVANTAGES DISADVANTAGES

• Most commonly used

• Specific assumptions

can be made

• Time consuming

• Information heavy

Company

Value of a company = How much cash it can make

Year 1 Cash Earnings

Year 2 Cash Earnings

Year 3 Cash Earnings

… and so on

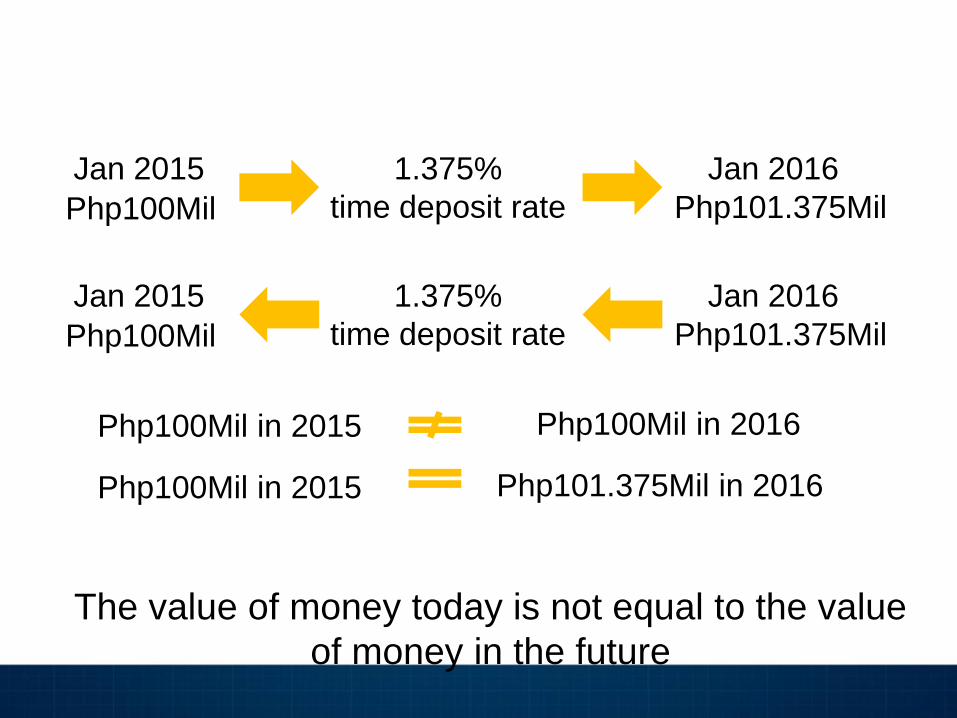

Php100Mil

1.375%

time deposit rate

Jan 2015 Jan 2016

Php101.375Mil

The value of money today is not equal to the value

of money in the future

Php100Mil

1.375%

time deposit rate

Jan 2015 Jan 2016

Php101.375Mil

Php100Mil in 2015 Php100Mil in 2016

Php100Mil in 2015 Php101.375Mil in 2016

Company

Value of a company = How much cash it can make

Year 1 Cash Earnings

Year 2 Cash Earnings

Year 3 Cash Earnings

… and so on

VALUE NOW

Company

Year 1 Cash Earnings

Year 2 Cash Earnings

Year 3 Cash Earnings

… and so on

VALUE NOW

FV estimate = Value of company per share

Absolute Valuation

• Discounted Cash Flow Method

ADVANTAGES DISADVANTAGES

• Most commonly used

• Specific assumptions

can be made

• Time consuming

• Information heavy

When do you BUY?

When do you SELL?

Relative Valuation • P/E and EPS growth

• P/BV and ROE

LOOP – Law Of One Price

DISADVANTAGES

• Easy to apply • Comparables and

multiples can be very

subjective

ADVANTAGES

Identical assets should trade at the same price

P/E and EPS growth

General Rule: Relatively cheaper if P/E is lower

STOCK A STOCK B

Current Price: Php10 Current Price: Php100

2015 EPS: Php1 2015 EPS: Php50

10X P/E 2X P/E

EPS = Earnings

Number of shares P/E =

Current price

Earnings per share

P/E and EPS growth

Higher EPS growth justifies higher P/E

STOCK A STOCK B

10X P/E 2X P/E

2016: 100% growth EPS 2016: 0% growth EPS

Limitation of relative valuation: Looking at a point in time

Which stock looks cheap?

Which stock looks expensive?

Company EPS Growth P/E

A

B

C

D

10%

20%

15%

8%

10.0

8.0

12.0

15.0

P/E and EPS growth

Company B looks cheap

Company D looks expensive

2015E P/E EPS growth

Consumer 28.2 13%

CIC 24.9 24%

CNPF 22.5 8%

DNL 27.9 -11%

EMP 18.3 22%

JFC 34.6 16%

PGOLD 21.5 9%

PIP 19 10%

RFM 15.9 8%

RRHI 24.2 21%

URC 33 13%

P/E and EPS growth

P/E and EPS growth 2015E P/E EPS growth

Conglomerates 18.4 18%

AC 24.5 10%

AEV 15.7 9%

AGI 13.6 29%

COSCO 13.2 11%

DMC 12.1 37%

FPH 8.2 1%

GTCAP 18.8 39%

JGS 21.1 30%

LTG 23 47%

MPI 12.5 20%

SM 23 8%

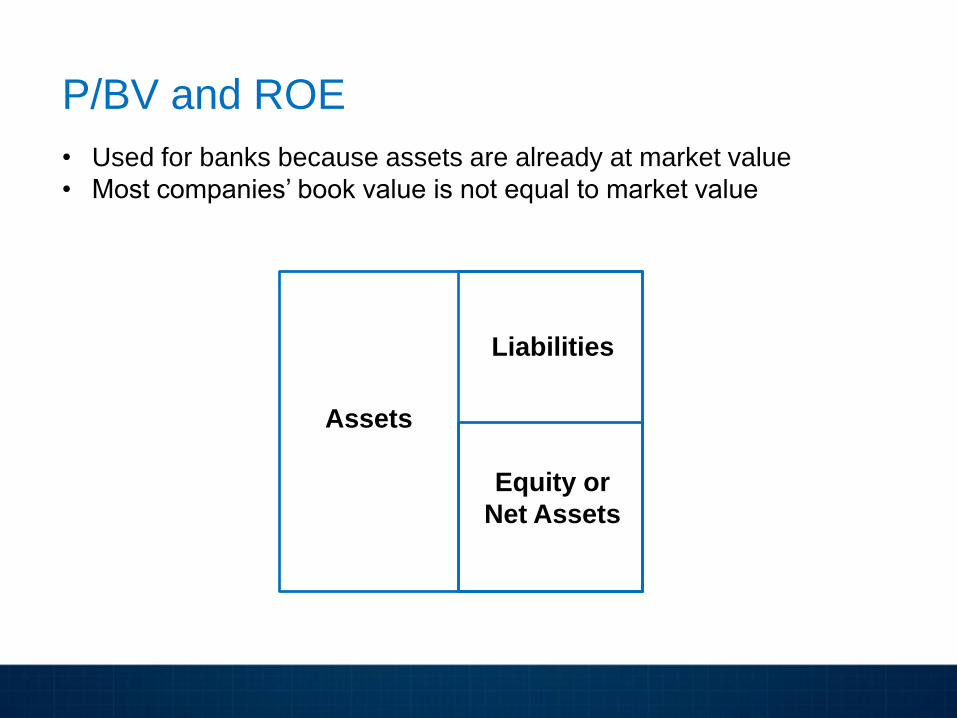

P/BV and ROE

• Used for banks because assets are already at market value

• Most companies’ book value is not equal to market value

Assets

Liabilities

Equity or

Net Assets

P/BV and ROE

General Rule: Relatively cheaper if P/BV is lower

Higher ROE justifies higher P/BV

P/BV = Current price

Book value per share

Book value per share = Equity

Number of shares

ROE = Net income

Equity

Which stock looks cheap?

Which stock looks expensive?

Company ROE P/BV

A

B

C

D

15%

12%

8%

15%

0.9

1.4

1.9

1.7

P/BV and ROE

Company A looks cheap

Company C looks expensive

P/BV and ROE

2015E P/BV ROE

Banks and Financials 1.8 13%

BDO 2.1 14%

BPI 2.6 15%

CHIB 1.3 10%

EW 1.0 11%

MBT 1.5 12%

PNB 1.0 7%

RCB 1.0 10%

SECB 1.8 16%

UBP 1.3 16%

Dividend Yield

• Salary as an investor

• Suited for more conservative investors

• Most high dividend yielding stocks are utility companies with

slower earnings growth

Ticker Company Dividend Yield

MER Manila Electric Company 5.2%

AEV Aboitiz Equity Ventures 2.7%

GLO Globe Telecom, Inc. 2.9%

TEL Philippine Long Distance Company 5.6%

Dividend Yield = Dividends per share

Current price

Where to get Information?

COL Reports

Investment Guide

COLing the Shots

- Monthly strategy reports

- Focused on relevant issues

for the month

Market Strategy

- Semi-annual strategy reports

- Focused on longer term

relevant issues (past six

months, next six to twelve

months)

COL Reports

Company Report

- Company specific

- Earnings reports

- Meetings with management

Daily/Weekly

- Summary of both recent

economic and company

specific news

COL Reports

How to find

the reports

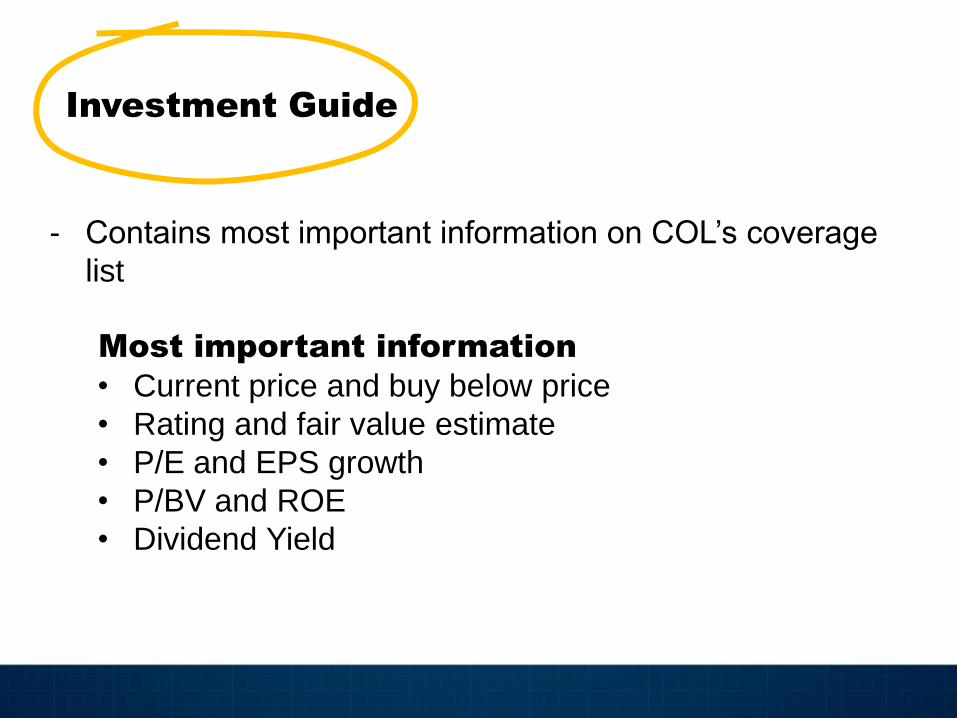

Investment Guide

- Contains most important information on COL’s coverage

list

Most important information

• Current price and buy below price

• Rating and fair value estimate

• P/E and EPS growth

• P/BV and ROE

• Dividend Yield

How to find Investment Guide

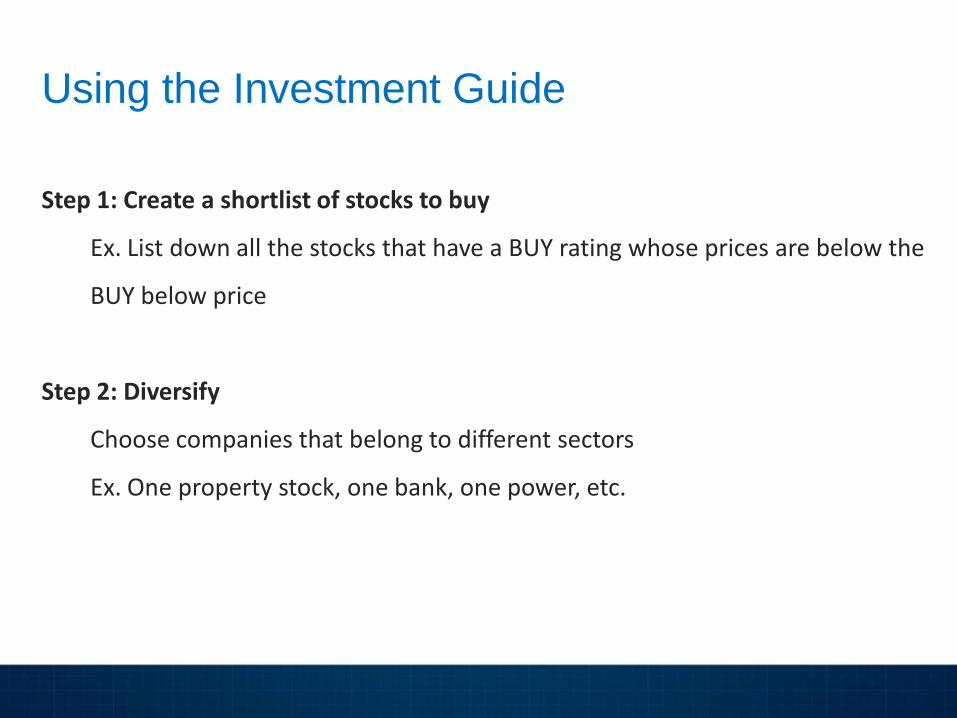

Step 1: Create a shortlist of stocks to buy

Ex. List down all the stocks that have a BUY rating whose prices are below the

BUY below price

Step 2: Diversify

Choose companies that belong to different sectors

Ex. One property stock, one bank, one power, etc.

Using the Investment Guide

Step 3: Determine your preferences Growth, value or income - Growth: high EPS growth - Value: high capital appreciation potential, low P/E, low P/BV - Income: high dividend yield Liquidity - Active traders with large portfolio: go for larger market cap stocks - Long term investor: can invest in smaller market cap stocks

Names - Major shareholders (Ayala, Aboitiz, Sy, Gokongwei, MVP, etc) - Brands (Jollibee, SM, Meralco, etc.)

Using the Investment Guide

COLing the Shots Model Portfolio

Sector Current Price Buy Below Price FV estimate

AC Conglomerates 791 701.6 877

MBT Banks 92.4 87.2 109

SMPH Property 20 18.88 23.6

FGEN Power 25.55 28.8 36

CEB Airline 85.55 124.8 156

FLI Property 1.87 1.94 2.42

Sources of Information

PSE Website

Focus on company

disclosure, especially 17A

(annual report) and 17Q

(quarterly report)

Company Website

Learn more about what

the company does

Sometimes, the company

would have press

releases, presentations

available

Newspaper Reports

“Be fearful when others are greedy and

greedy only when others are fearful”

- Warren Buffet

Invest for the Long Term

67

35

24

41

25 22 27

18 15 17 12 12 13

9 8 11 7 8

-39

-22 -16

-32

-16 -15 -11 -10 -8

-4 -5 -5 1 -3 -3 3 -2 -2

-60

-40

-20

0

20

40

60

80

1 2 5 10 20 30

Co

mp

ou

nd

An

nu

al

Re

turn

s (

%)

Years of Holding Period

Maximum and Minimum Real Holding Period Returns, 1802-1997

Maximum and Minimum Real Holding Period Returns, 1802-1997

Stocks

T-Bills

Bonds

Stocks

BondsT-Bills

26.7

17.7 14.9 16.912.4 11.6 12.6

8.8 8.3 10.67.4 7.6

-60

-40

-20

0

20

40

60

80

1 2 5 10 20 30

Years of Holding Period

Co

mp

ou

nd

An

nu

al R

etu

rns

(%

).

Stocks outperform all asset classes in the long run