ELSA 9M17 Eng Ver 2 - Elnusa · The return of those blocks to Pertamina are expected to...

16

www.elnusa.co.id Analyst Meeting PT Elnusa Tbk November 2017

Transcript of ELSA 9M17 Eng Ver 2 - Elnusa · The return of those blocks to Pertamina are expected to...

www.elnusa.co.id

Analyst MeetingPT Elnusa Tbk

November 2017

2

9M‐17 Financial Highlight

(Rp Bn)

INCOME STATEMENT 9M16 9M17 % Change

Revenue 2.524 100% 3.321 100% 31,6%

Cost of Revenue 2.094 83% 2.987 90% 42,6%

Gross Profit 430 17% 335 10% (22,1%)

Operating Profit 281 11% 154 5% (45,3%)

EBITDA 505 20% 433 13% (14,4%)

Net Profit 178 7% 86 3% (51,9%)

BALANCE SHEET FY16 9M17 % Change

Cash & Equivalents 744 18% 734 16% (1,4%)

Account Receivables 714 17% 985 22% 38,0%Total Assets 4.191 100% 4.469 100% 6,6%Account Payables & Accruals 638 15% 888 20% 39,1%Short Term Bank Loan 516 12% 597 13% 15,8%Long Term Bank Loan 34 1% 12 0% (64,4%)Total Liabilities 1.313 13% 1.572 35% 19,7%Total Equity 2.878 69% 2.897 65% 0,7%

3

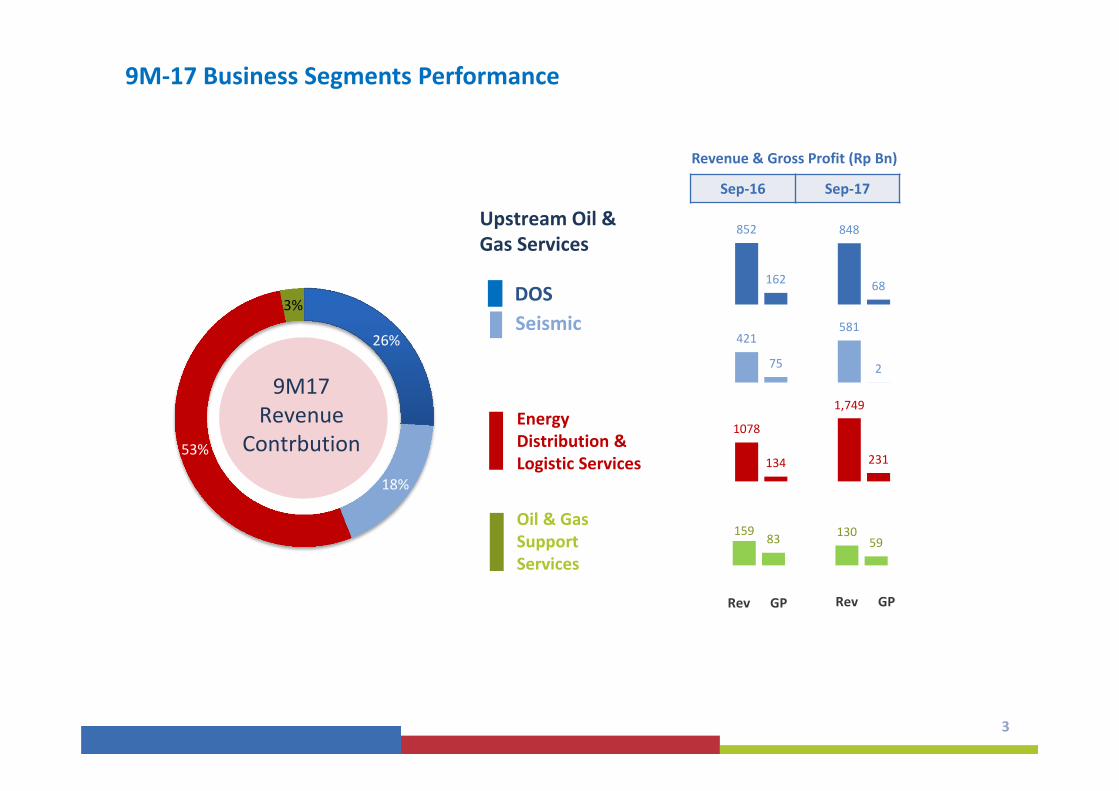

9M‐17 Business Segments Performance

26%

18%

53%

3%

DOS GSC EPN Others

9M17Revenue

Contrbution

DOSSeismic

Upstream Oil & Gas Services

Oil & Gas Support Services

Energy Distribution & Logistic Services

852 848

162 68

421581

75 2

1078

1,749

134 231

159 13083 59

Revenue & Gross Profit (Rp Bn)

Sep‐16 Sep‐17

Rev GP Rev GP

4

2017 Operating Game Project (Non Asset Based)strategy

Seismic & DOS major significant projectshad just started in the second half 2017.

Lower contribution in upstream segmentEspecially From 3 of Elnusa’s major contributorOil & gas blocks

Decreasing numbers of projects and activities in upstream industry as the impact of low oil price.

Factors that Affect Elnusa’s 2017 Performance :

5

Global Oil Price Has Been Going Down Since 2015

Pergerakan dan Proyeksi Harga Minyak Mentah Dunia (West Texas Intermediate /WTI)

Source : US Energy Information Association

6

Indonesia Upstream Investment (USD Mn)

Low Oil Price Also Affecting Domestic Upstream Slow Activities

4,08

3

3,29

5

10,247

1,773

6,905 6,566

2015A 2016A 2017P

Seismic ‐ 2D (km)

Seismic ‐ 3D (sqkm)

35 43 25

541

227 223

2015A 2016A 2017P

Exploration Drilling (# of well)

Development Drilling (# of well)

1,320 1,012 907

31,578

38,827

57,512

2015A 2016A 2017P

Workover (# of activities)Well Services (# of activities)

Source : SKK Migas & PTM

7

ELNUSA has been working for more than 25 years in East Kalimantan (especially in Total Mahakam) Those area generated around 45%‐65% (USD 40‐65 mn) of revenue contribution in Drilling & Oilfield

Services business each year. For the last 3 years, revenue contribution from East Kalimantan area has been declining (nearly

about 60% or amounting to USD38 mn) because the Blocks Operator/Owner lower their activitiestowards Blocks transition to Pertamina.

The return of those blocks to Pertamina are expected to stimulate the blocks activities and also ELNUSA operational side.

1. Mahakam (Total EP – exp. 2018 )2. Sanga Sanga (VICO – exp. 2018)3. Attaka (Chevron – exp.2017/2018)

Transition Period

05

10152025

303540

2014 2015 2016 2017 F 2018 <

DOS Revenue Contribution (USD Mn)

Total Mahakam

Chevron

Vico Sanga‐Sanga

‐48%

‐93%‐52%

8

4

6

3

4

3

‐ 1 2

2018 2019 2020 2021 2022 2023 2024 2025 2026

Expired Blocks Expired Block Migas di Indonesia

Lower Contribution due to Impact of Indonesia Expired Blocks

8

8

Significant Ongoing Project 2017 : Land & Marine Seismic

3D Land Seismic Klamosossa, West Papua

3D Marine Seismic Andaman, Aceh

Indonesian Flag Seismic Marine Vessel.Efficient survey seismic utilization with 3D seismic capacity complemented with 10 seismic streamers

Client : Talisman Andaman. Total seismic area : 2500 km2. Periode : Aug – Nov 2017

Client: Pertamina EP. Total seismic area: 500 Km2. Shoot points : 40.900. Period : 2017‐2018.

9

Significant Ongoing Project 2017 : Drilling & Oilfield Services

Operation &Maintenance Projects

Drilling, East Kalimantan

Client : Pertamina EP Drilling of 3 Brajanata exploration wells East

Kalimantan Using Electric Modular Rig 1600HP Period : Jun – Des 2017

Papua Client : BP Tangguh. Jobs : Mechanical & Electrical OM. Period : 5 tahun (2017 ‐ 2022).

Sumatera Selatan Client : Conoco Phillips

Jobs : Construction Maintenance (2017). Clients : Pertamina Aset 2

Jobs : TAPSPD 3 tahun (2016 – 2019).

10

Business Portfolio Expansion to Maintain Revenue Stability

Upstream Oil & Gas ServicesEnergy Distribution & Logistic ServicesOil & Gas Support Services

55%38%

8%

1H2016

39%

56%

5%

1H2017

58%33%

9%

48%43%

9%

2015 2016

Pendapatan Konsolidasi

4%21%

27%

48%

14%

27%

18%

41%

13%

34%

17%

36%

22%

25%

16%

37%1H2016

1H2017

2015 2016

Non Asset Based Services (OM)Asset : Hydraulic Workover ServicesAsset : Electric Wireline Logging ServicesAsset : Other Asset Based Services

Pendapatan DOS

Distribution & Logistic Services Operating Game Project (Non Asset Based)

11

Recovery Action 2017

1,672

3,736

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Rp bn

Actual Projection

Drilling Pertamina Aset 5 & CoPi Kuala Kurun.

Subsea Pertamina Aset 4

Workover Pertamina aset

2,3, 4 & 5.

Marine Seismic PHE & Conrad.

Addition ofTransportastion &

Depo / DPPU

Addition of 6 Pertamina KSO management.

3D Seismik Klamasossa & 3D Marine Seismic

Talisman Andaman3.321

To win remaining Marine Seismic Project. Maintain the productivity of Land &

Marine Seismic projects. Optimizing the performance of

Operation & Maintenance projects . Improving the productivity of contracts

and asset utilization in Drilling & Oilfield Services.

Increasing numbers of transportation& Depo management.

1. Menjaga Kinerja Existing Business

12

Current Order Book (1H17)

Business Total Contract 2017 Value Carried Forward Value

Seismic Services 1,430 930 500

Drilling & Oilfield Services 3,073 1,080 1,993

Total 4,503 2,010 2,493

Significant Contract of Seismic Services• Land Seismic in West Papua & Sumatera (Pertamina)•Marine Seismic in Laut Jawa, Aceh & Maluku (PHE, Repsol & ESDM)

Significant Contract of Drilling & Oilfield Services• Drilling exploration of Pertamina in East Kalimantan• Workover in Pertamina aset 3 & 4.

Business Total Contract 2017 Value Carried Forward Value

Transportation & Logistic 2,039 1,848 191

Transportation & Logistic Services Contract• Transportation contract extension and also 2017 new project amounting to Rp995 bn• Depot Management business add new contracts from KSO and private companies.

Rp bn

Rp bn

13

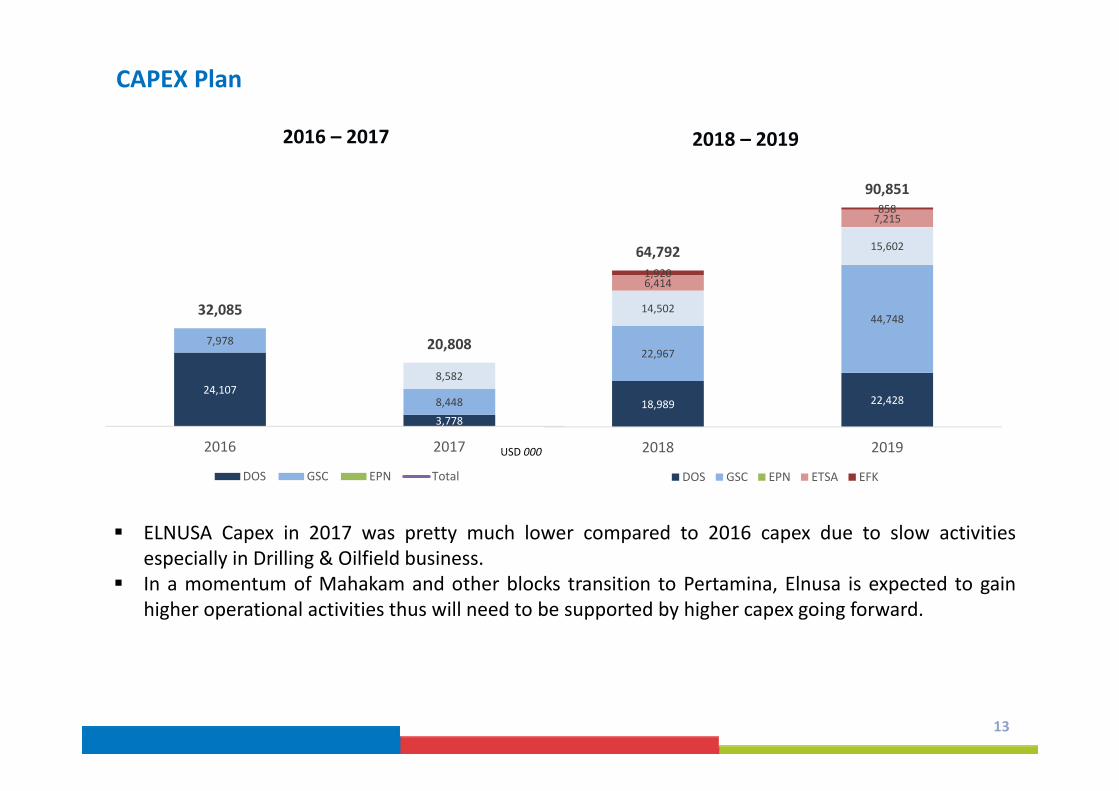

CAPEX Plan

USD 000

2016 – 2017 2018 – 2019

18,989 22,428

22,967

44,74814,502

15,602

6,414

7,215

1,920

858

64,792

90,851

2018 2019

DOS GSC EPN ETSA EFK

ELNUSA Capex in 2017 was pretty much lower compared to 2016 capex due to slow activitiesespecially in Drilling & Oilfield business.

In a momentum of Mahakam and other blocks transition to Pertamina, Elnusa is expected to gainhigher operational activities thus will need to be supported by higher capex going forward.

24,107

3,778

7,978

8,448

8,582

32,085

20,808

2016 2017

DOS GSC EPN Total

14

2. New Busines Expansion to Increase Revenue

Jasa Klien

Electric Submersible Pump PertaminaAsset 3 dan Asset 4

Flare Gas Pertamina Asset 5 Sanga‐ Sanga

Review Cost Structure• In line with the market demand, costefficiency have to be conductedcontinuously by reducing activities thatis not providing added value.

• Efficiency obtained among others fromthe reduction of subcontractor costs,direct material, direct labor, rent dantravel expense.

3. Cost Efficiency to Maintain Profitability

Perbaikan Proses Bisnis

Asset Integrity

Pembuatan Standar Project Management

Penguatan implementasi Budaya Perusahaan

15

Corporate Strategy : Direction Stability :

Strenghten Position Growth :

Increase Business Sustainability

Corporate Strategy : Portfolio Optimization,

integration & differentiation.

Focus on energy in core business and selective in adjacent energy.

Corporate Strategy : Parenting Financial Control to

Strategic Control. Optimize Parent

Value Added.

Penajaman Visi Perusahaan : From “Trusted Energy Services” to “Reputable Energy Services Company by Providing Total Solution”

©Juli 2017

PT Elnusa Tbk.Graha ElnusaJl. T.B. Simatupang Kav. 1BJakarta 12560, IndonesiaTel: +62 21‐788308050 Fax: +62 21‐78830907www.elnusa.co.id

The following presentation has been prepared by PT Elnusa Tbk. (the “Company”) and contains certain projections, plans, business strategies, policies of the Company and industry data in which the Company operates in, which could be treated as forward‐looking statements within the meaning of applicable law. Such forward‐looking statements, by their nature, involve risks and uncertainties that could prove to be incorrect and cause actual results to differ materially from those expressed or implied in these statements. The Company does not guarantee that any action, which may have been taken in reliance on this document will bring specific results as expected. The Company disclaims any obligation to revise forward‐looking statements to reflect future events or circumstances.