Elizabeth K. Steiner, et al. v. Morgan Stanley Dean Witter...

32

• ; --• IN THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OP NEW YORk., • f;;IP Ce'j Elizabeth K. Steiner, Custodian for Katherine Esther Liggett tlIMANY and Elizabeth K. Steiner. Custodian for Max Alexand TM t yigritt 61 53 UAJNY, on behalf of themselves 4nther, : similarly situated, Plaintiffs, Civ, Action No. -against- Morgan Stanley Dean Witter 8z. Co., Morgan Stanley Technology Fund (flkia Morgan Stanley CLASS ACTION COMPLAINT Dean Witter Technology Fund), Morgan Stanley : FOR VIOLATIONS OF TIIE • . . - . Dean Witter Distributors Inc., Morgan Stanley : FEDERAL SECURITIES LAWS Dean Witter Advisors lnc•, and Morgan Stanley • Dean Witter Investment Management Inc., : JURY TRIAL DEMANDED Defendants. Plaintiffs. by their undersigned attorneys, individually and on behalf of the Class described below, bring this complaint (the "Complaint - ) against the defendants named herein upon actual knowledge, except for those allegations identified as upon information and belief which are based upon, inter alid, the investigation of plaintiffs counsel, which included, among, other things, a review of public statements made by defendants and their employees. Securities and Exchange C.oninnission ("SEC") filings, and press releases and media reports, and allege as follows: • NATURE OF THE ACTION 1. This is a federal securities class action brought by the plaintiffs against • defendants Morgan Stanley Dean Witter Sc Co. ("MSDW" or the "Company"), Morgan Stanley • ;HY

Transcript of Elizabeth K. Steiner, et al. v. Morgan Stanley Dean Witter...

• ;--•

IN THE UNITED STATES DISTRICT COURTFOR THE SOUTHERN DISTRICT OP NEW YORk.,

•

f;;IPCe'jElizabeth K. Steiner, Custodian for Katherine

Esther Liggett tlIMANY and Elizabeth K.Steiner. Custodian for Max Alexand

TMt yigritt 61 53

UAJNY, on behalf of themselves 4nther, :similarly situated,

Plaintiffs, Civ, Action No.

-against-

Morgan Stanley Dean Witter 8z. Co., MorganStanley Technology Fund (flkia Morgan Stanley CLASS ACTION COMPLAINTDean Witter Technology Fund), Morgan Stanley : FOR VIOLATIONS OF TIIE

•. .

- . Dean Witter Distributors Inc., Morgan Stanley : FEDERAL SECURITIES LAWSDean Witter Advisors lnc•, and Morgan Stanley

• Dean Witter Investment Management Inc., : JURY TRIAL DEMANDED

Defendants.

Plaintiffs. by their undersigned attorneys, individually and on behalf of the Class

described below, bring this complaint (the "Complaint -) against the defendants named herein

upon actual knowledge, except for those allegations identified as upon information and belief

which are based upon, inter alid, the investigation of plaintiffs counsel, which included, among,

other things, a review of public statements made by defendants and their employees. Securities

and Exchange C.oninnission ("SEC") filings, and press releases and media reports, and allege as

follows: •

NATURE OF THE ACTION

1. This is a federal securities class action brought by the plaintiffs against

•defendants Morgan Stanley Dean Witter Sc Co. ("MSDW" or the "Company"), Morgan Stanley

•

;HY

,• - •

.•

• n: •

••••,:--a• Technoiogy Fund ("Technology Fund" or the "Fund"), Morgan Stanley Dean -Witter

• . . Distributors Inc. ("Distributors"), Morgan Stanley Dean Witter Advisors Inc_ ("Advisors"), and

• Morgan Stanley Dean Witter Investment Management inc. ("Investment Management") (all

collectively, "defendants"). on behalf of a class (the "Class - ) consisting of those (whether or

riot they were clients of MSDW) who purchased shares of any and/or every class of the Fund's. .

shares from the public offering of the Fund on or about September 25, 2000 through July 31,

2002, inclusive (the "Class Pet iod").J...

2. Plaintiffs seek to recover damages caused to the Class by defendants' violations:4 , •

of Section 10(b) of the Securities Exchange Act of 1934 (the "Exchange Act"), Rule 10h-5

promulgated thereunder, Section 20(a) of the Exchange Act, and Sections 11, 12 and 15 of the

Securities Act of 1933.

3. Defendant Morgan Stanley Dean Witter is one oldie largest securities broker-

dealers and one of the leading financial management and advisory companies in thc world. As

an investment bank, MSDW claims to be one of the top global underwriters and market makers

of debt and equity securities and a leading strategic advisor to corporations, institutions, and

individuals worldwide. All of the other defendants are, directly or indirectly, wholly-owned

subsidiaries of MSDW.

4. The defendants were: (1) the underwriters for the common stock of certain of

the companies in the Funds portfolio (and, hence thc agents or former agents of those

companies); (2) the investment bankers and corporate finance specialists for certain of the

companies whose securities arc in the Fund's portfOlio; (3) seeking to obtain additional

-2-:

investment banking business from these present and former clients and from other companies

• whose shares also were/are in the Fund's portfolio; (4) the issuers of the shares in the Fund; (5)

• preparing and publicly disseminating research reports and recommendations on many of thc

companies who shares were in the Fund's portfolio; and (6) the broker for certain members of

the Class.

5. I fence, MSDW and the other defendants had a duty to plaintiffs and the Class to

provide information which was truthful and was not false or inisteading; and to disclose

information which was material to plaintiffs and the Class in their decisions to purchase or sell

shares of the Fund.

. . 6. This action arises as a result of the issuance by the defendants of shares in the

• Fund, and concerns material misstatements and omissions by defendants in the Prospectus and

Statement of Additional Information which include but are not limited to the following: (I)

• defendants failed to disclose and omitted material information that MSDW had had investment. .

banking relationships with, including having brought public. certain of the companies whose

securities were part of the Fund's portfolio. Defendants disclosed neither this general fact nor

the identities of the particular companies with which it had investment banking relationships.

(2) defendants failed to disclose and omitted material information concerning that IVISDW was

continuing to seek investment banking relationships with many of the companies whose

securities were part of the Fund's portfolio; (3) delendanis failed to disclose arid omitted

material information concerning that a material part of the total compensation paid to MSDW

research analysts was based upon obtaining investment banking business ibr MSDW and not

-3-

. ,,•,k

•

•upon the accuracy of their research about a given company. I•Ience, MSDW and its affiliated

companies including the Fund recommended investments in and/or invested in companies in

order to enhance MSDW's opportunity to obtain investment banking business from those

companies (without regard to whether they were good investments for the investors including

plaintiffs and the Class); and (4) although the August 17. 2000 Prospectus states that "the Fund

may engage in active and frequent trading of its portfolio securities. The Fund's portfolio

turnover rate may exceed 250'N,"; defendants failed to disclose and omitted material

information that the Fund would keep portfolio positions if it thought retaining ownership of

that company's securities would enhance MSDW's chance of obtaining investment banking

business from that company, even if that security was no longer a good investment and the

security otherwise would have been sold by defendants.

7. Suthinvestment banking engagements Nverc worth millions of dollars in fees to

MSDW_

• JURISDICTION AND VENUE

8. This Court has jurisdiction over the suhject manta- of this action pursuant to

Section 27 of the Securities Exchange Act of 1934 (the "Exchange Act"), 15 U.S.C. §§ 78aa,

Section 22 of the Securities Act of 1933, and 28 U.S.C. § 1331.

9. Plaintiffs bring this action pursuant to the Exchange Act. as amended, 15 U.S.C.

• §§78j(b), 78t(a), Rule 10b-5 protmilgated thereunder, 17 LER. g 240.101)-5 and 15 U.S.C.

§§ 77(k), 77(1) and 77(o).

10. Venuc is proper in this District because Defendants conduct business in this

. .

-4-,

..

. .—

District and many of the wrongful acts alleged herein took place or originated in this District.

11. In addition, many of the defendants are headquartered in this District in New

York County, New York (or were headqualteted theic at the time of the public offering).

12. In connection with the acts alleged in this Complaint, Defendants, directly or

indirectly, used the tneans and instrumentalities of interstate commerce, including,. but not

limited to, the interstate telephone communications and the facilities of the national

securities markets.

PARTIES

13. Plaintiffs Elizabeth K. Steiner, Custodian for Katherine Esther Liggett

UTMAJNY and Elizabeth K. Steiner, Custodian for Max Alexander Liggett LITMA/NY

purchased shares of the Fund during the Class Period. and were damaged thereby, as set forth

in the certification attached hereto.

14. Defendant Morgan Stanley Dean Witter is, in its own words in the Statement of

Additional Information incorporated into the relevant prospectus herein, ''a preeminent global

financial services firm that maintains leading market positions in each of its three primary

businesses: securities, asset management and credit services." MSDW claims to be one of the.;

world's leading financial management and advisory companies. As an investment bank,

MSDW claims to be one of the top global underwriters and market makers of debt and equity

securities and a leading strategic advisor to corporations, institutions, and individuals

worldwide. MSDW I s worldwide headquarters is in this District in New York County, New

York.

-5-

w • •. .

"Or•

15. Defendant Technology Fund is a non-diversified mutual fund with its principal

place of business in New York County. New York, The Fund's stated objective, for its

shareholders, is to provide Iong-term capital appreciation. The Technology Fuud invests

primarily in common stocks of companies involved in technology and technology-related

industries.. .

16. Defendant Morgan Stanley Dean Witter Advisors Inc., the investment manager,

provides administrative services to and manages the Fund's business affairs. Advisors, upon

information and belief, is headquartered in New York County, New York.

17. Advisors has in turn contracted with defendant Morgan Stanley Dean Witter•

. Investment Management Inc._ the. Sub-Advisor, to invest the Fund's assets including the placing

of orders for the purchase and sales of securities. Investment Managenient is headquartered in

: •

New York County, New York,

18. Defendant Morgan Stanley Dean Witter Distributors Inc. was the Technology

•:Fund's principal underwriter. Distributors, upon information and belief, is headquartered in

New York County, New York...•

19. Defendants Technology Fund, Advisors, Investment Management and

Distributors each are a wholly-w,vned subsidiary (either directly Or indirectly) of MSDW.

• 20. Pursuant to agreements which Distributors has entered into, the Fund's shares

are sold through the Dean Witter arm of MSDW and through other selected broker-dealers.

-6-. •

•.4•• _• •

e

CLASS ACTION ALLEGATIONS

21. Plaintiffs bring this action as a class action pursuant to Rule 23(a) and (b)(3) of

the Federal Rules of Civil Procedure on behalf of a class consisting of all persons and entities

who purchased shares of the Fund during the Class Period, except for those persons employed

by or affiliated with defendants.

22. Members of the Class are so numerous that joinder of all members is

impracticable. While the exact number oF Class members is unknown to plaintiffs at this time••••,.[•••, •

and can only he ascertained through appropriate discovery, plaintiffs believe that there are

thousands of members of the Class located throughout thc United States.

23. In the Fund's first semi-annual report in 2001. filed with the SEC on April 20,

2001, which covered its first four months of operation through February 28, 2001, the Fund had

over 150 million shares outstanding, with at least 8 million shares outstanding in each of the

four classes.

• i.24. In the Fund's most recent semi-annual report filed April 23, 2002, for the six

month time period ending Fcbniary 28, 2002, the Fund had over 150 million shares

outstanding, with at least 6 million shares in each of its four classes.

25. The Fund has been sold to class members using a written prospectus and

statement of additional infomtation, and the Fund also has issued semi-annual reports and other

SEC filings, all of which make the action suitable and appropriate lor class treatment.

26. Throughout the Class Period, record owners and other members of the Class

may be identified from records maintained by the Fund andlor its transfer agent and may be

-7-

•:• .

notified of the pendency of this action by mail and publication, using forms of notice similar to

those customarily used in securities class actions.

27. Plaintiffs' claims are typical of the claims of the other members of the Class.

. .Plaintiffs and the other members of the Class, by virtue of their purchases of shares of the Fund

during the Class Period, have sustained damages as a result of Defendants unlawful activities

• as alleged herein. Plaintiffs have retained counsel competent and experienced in class and

securities litigation and intend to prosecute this action vigorously. The interests of the Gass

. • will be fairly and adequately protected by plaintiffs. Plaintiffs have no interests which are

contrary to ur in conflict with those of the Class which plaintiffs seeks to represent.

28. A class action is superior to all other available methods for the Fair and efficient.• •

• adjudication of this controversy. Plaintiffs know of no difficulty to be encountered in the

• management of this action that would preclude its maintenance as a class action.

29. Common questions of law and fact exist as to all members of the Class and

predominate over any questions solely affecting individual members of the Class. Among the

questions of law and fact common to the Class are:

a. Whether the federal securities laws were violated by Defendants' acts as

alleged herein;

b. Whether Defendants participated directly . or indirectly in the course of

. conduct complained of herein; and

Whether members of the Class have sustained damages as a result of

De ftaidasits' conduct, and the proper ineasuir of such damages.

. .

•

BACKGROUND OF THE ACTION •

30. Historically, brokerage firms like IVISDW that performed both investment•

banking and research analysis functions maintained a "Chinese wail" between the two functions•

to ensure that the analysts research and recommendations remained objective and were nut•

influenced by the firm's interest in attracting and retaining investment banking business.•t•••

31. In recent years, however, the "Chinese wall" has apparently crumbled, with

research analysts directly performing investment banking functions and receiving

compensation based on their contributions to generating iirvestinent banking business,

including underwriting initial public offerings ("IPO's") and secondary offerings of equity

securities, underwriting debt offerings, and performing services in merger and acquisition

• transactions, without disclosing such material conflicts of interest to the investing public.

32. The conflicts of interest exhibited by Wall Street analysts also began to draw the

attention of various state and federal government authorities. For example, on April 23, 2000,•. .

the Sunday Times of London reported:•

. in the fiercely competitive•battle for big underwriting deals. rinvcstincntj banks are. resorting to practices that are alarming regulators. They are hyping stocks. encouraging

companies to use creative accounting and, if they arc venture capital investors, dumpingstocks as soon as the companies float.

Individual investors often pay for these practices. They act (often with disastrous results)on the "hot tips" of analysts appearing on 24-hour financial television channels. ..1 . hey arepersuaded In believe commercials that tell them they can become overnight millionairesby trading stocks. And they are completely misled by the creative accounting condoned(but not revealed) in some analysts' reports.

One 30-year Wall Street veteran says: It is the most corrupt thing I have ever seen. After„„ •the market crashes later this year or next, you are going to see congressional hearings intoall the terrible things that have been going, on."

• -9-

•.. .

4t ;Aq; ', .

'r

Arthur Levitt, the Securities and Exchange Commission (SEC) Chairman, has repeatedlycomplained about the glowing reports that analysts issue on companies with which their

" firms hope to do business.

; The "Chinese walls" that once separated researchers and hankers have all but disappearedin today's banking world and researchers have often become blatant pitchmen for bankdeals. Levitt says they 'act more like promoters and marketers than unbiased anddispassionate analysts . . a 'sell' recommendation from an analyst is as common as aBarbra Streisand concert."

Among those who have been pitching hardest for deals is Mary Meeker, Morgan StanleyDean Witter's celebrated Internet analyst. She played a pivotal role in winning a deal forMorgan Stanley to be the lead manager of Lastminute.com's float last month. lierexuberant report on the company was supposed to encourage investors. But the sharesare now trading at less than half their flotation price.

(inc orher former bosses at Morgan Stanley says: She has become a combination ofanalyst and banker. It is a model that doesn't really work."

• 33. On June 14, 2001, the United States 'louse of Representatives Subcommittee on

Capital Markets, Insurance, and Government Sponsored Enterprises (the "Subcommittee")

•began holding hearings entitled "Analyzing the Analysts: Are Investors Getting Unbiased

Research From Wail Street?" In his opening remarks. Representative Paul E. Kanjorski, the

ranking Democratic member of the Subs.:ornmittce. stated:

Unlike some other sources of investment advice, the vast majority of the general publichas usually considered the research prepared by Wall Street experts as reliable and

• valuable. With the burst of the high-tech bubble, however came rising skepticism amonginvestors concerning the objectivity of some analysts' overly optimistic recommendations.Many in the media have also asserted that a variety of conflicts of interest may havegradually depreciated analyst independence during the Internet craze and affected thequality of their opinions_ 'We have debated the issues surrounding analyst independence

• for many years. After the deregulation of trading commissions in 1975. Wall Street firmsbegan using investment banking as a means to compensate their research departments,and lvithin the last few years the tying of analyst compensation to investment bankingactivities has become increasingly popular. As competition among prokerage firms for1PO's, mergers, and acquisitions grew, so did the potential or large:conipensation

-10-•

•

..•••• „

::,:: • •i. ••. •• packages for sell-side analysts. These pay practices, however, may have also affected

analyst independence. While some brokerage houses suggest that they have executed animpenetrable Chinese wall that divides analyst research lioni other firm functions likeinvestment banking and trading, the truth, as we have learned from many recent newsstories, is that they must initiate a proactive effort to rebuild their imaginary- walls.

.• The release of some startling statistics has also called into question thc actualindependence of analysts. A report by First Call, for example, found that less than one

• •

•percent of 28,000 recommendations issued by brokerage analysts during late 1999 anti

• most of 2000 called For investors to selI stocks in their portfolios. Within the very sametime frame, the NASDAQ composite average fell dramatically. In hindsight, theserecommendations appear dubious. Furtherniure. First C:all has determined that the ratioof buy to sell recommendations by brokerage analysts rose from 6:1 in the early 1990's to100:1 in 2000. .Many parties have consequently suggested that analysts may have becomemerely cheerleaders for the investment banking divisitm in their brokerage houses_ 1agree. To me, it appears we may have obsequious 'analysts instead of objective analysts.

.„ .34. The erosion of analysts objectivity discussed hy Rep. Kanjorski also was the

subject of a December 31, 2000 article in the Nen , Fork Times, which reported:

Of all the rude awakenings that the bear market in stocks has brought to investors,perhaps the most jarring has been the realization of how woefully wrong Wall Street'sresearch analysts have been this year on the stocks they follow. While the market sank toits worst performance in more than a decade, many of those analysts kept right on smilingand saying "buy."

:••••llow can so many who are paid so much to scrutinize companies have blown it sospectacularly for their investor customers?

• The answer lies in a subtle but significant change in the way Wall Street analysts do their•• • work — and how they are rewarded for it. That shift, which has brought riches and

. stardom to many securities analysts, has cost investois billions of dollars in losses.

• • • The fact is, although brokerage firm stock gurus are still called analysts. their day-to-day• .• pursuits involve much less analysis and much more salesmanship than ever before.

"The competition for investing banking business is so keen that analysts' sellrecommendations on stocks ot banking clients or potential banking clients are very rare,"said Arthur Levitt. the chairman of the Securities and Exchange Commission. "Whetherthis is an actual or perceived conflict, clearly, in the minds of many institutional buyers,

. •brokerage firm analysis has diminished credihility."

-11-•

,•

_r- g•

• 35. On January 30, 2001, 60 Minutes H aired a story focusing on Wall Street

analysts' conflicts of interest and singled out MSDW analyst Mary Meeker and Merrill Lynch

& Co. analyst Henry Blodget as two examples:

SCOTT PELLEY (co-anchor): -Fhe big brokerage houses on Wall Street these days makemost of their money in what's called investment banking - simply put, that's raisingmoney for companies that need cash. For example., if Amazon.coni needs money, it goesto its brokerage house, Merrill Lynch. Merrill Lynch offers Amazon stock for sale, andthe higher the price of the stock, the more money Merrill Lynch makes. Now imagine

• what any analyst is going to say about a stock that his own firm is offering for sale.

TOM BROWN (former analyst): They literally are cheerleaders because even if you're -this company that you're working on is not a client of the firm, every company's apotential client, so the investment banking group wants you to be wildly bullish abouteverybody.

PELLEY: Meaning that if there's had news about a stork. you're not likely. ' to hear it front• the analyst. This 1999 study from Dartmouth College and Cornell University says

analysts show `significant evidence of bias' when they recommend stocks that are handledby their Inn. The study points to this internal memo from brokerage house MorganStanley. ft tells analysts, quote, "... we do not make negative or controversial commentsabout our clients. ..." Morgan has since disavowed that rnemo, but just look at a recentexample of one of thc firm's clients, Priecline.eorn. Morgan madc millions in fees raisingmoney for Priceline. Morgan's analyst, iMary Meeker, seen here on CNBC. recommendedbuying Priceline's stock at $134 a share. When it fell to $78. she repeated her huyrecommendation and she kept recommending Pricclinc as it fell to less than $3....

••

PELLEY: Investors may have lost a fortune, but last year Bludgct and Meeker werereportedly paid about $15 million each. Both analysts declined requests for interviews.

• Merrill Lynch, Blodget's firm, did send us an e-mail saying its "analysts makeindependent recommendations based upon their best judgments." Mary Meeker atMorgan Stanley sent us a statement, saying in part, "We maintain a strict separation of theinvestment banking and research functions within the firm. Our research is objective, andhas a long-term focus."

. 36. On April 20, 2001, The New York Time.s. reported:

The nation's top securities regulator put Wall Street firms on notice yesterday, saying that• the activities of their research anahsts and the potential fbr conflict in the stock

-12-

..

*

recommendations they make to investors will conie under increased scrutiny.

Laura S. Unger, the acting chairvvoinan of the Securities and Exchange Commission, usedthe issue of analyst independence as the focus °Fa speech yesterday before theNorthwestern University School of Law. She warned brokerage firms to "reinvigoratepublic confidence" by resolving the "blatant conflicts" their analysts face.

"This is an area that people have been grumbling about for sonic time," Ms. Unger said inan interview after the speech. "Given the CIE tent maiket conditions. preserving theintegrity of information is more important than ever."

Specific conflicts raised in Ms. Unger's speech included the widespread practice ofpaying analysts based upon the investment banking fees generated when their firms raisemoney for the companies the analysts follow. Such an arrangement encourages an analystto be overly positive to keep investment banking tees coming in.

Another concern of Ms. Unger's are analysts who own shares in the companies theyfollow or who receive discowited shares in a company before the shares are offered to thepublic. She also criticized brokerage firms that acquire a stake in a start-up company inexchange for helping it raise money from the public. After the stock has come public,Ms. [Inger said, some firms have issued favorable research reports, what she called "abooster shot", which propelled the stock price higher and allowed the firm to sell its stake•into an inflated market.

= . While she called on Wall Street firms to resolve the conflicts themselves, Ms. Unger saidthat the SEC inspections of firins in coming months would focus on areas of potentialconflict. One focus will be the so-called Chinese wall that is said to separate investmentbanking departments from their counterparts in research but the many critics suspect hasbeen demolished.

Brokerage firm practices relating to analysts will also come under the microscope inWashington next month at hearings planned by Representative Richard H. Baker, aRepublican of Louisiana. Mr. Baker, chairman of the I louse subcommittee on capitalmarkets, is concerned that individual investors may not know how biased the advicecoming from analysts can be.

,Among the conflicts Mr. Baker plans to address at the hearings are analysts personalownership of stocks and the temptation to use upbeat research reports to help generateinvestment banking fees for their firms and for themselves.

37. On May 7, 2001, The hwestmerli Decriers 'Digest reported:

-13-

, The SEC thinks that the Chinese wall, which is supposed to keep investment bankers andtheir clients from influencing analysts, needs in he t rerigl [wiled, and !here's currently talkof beefing up thc disclosure requirements on Wall Street analyst reports. But these areconsidered minor improvements, as few think that substantive, long-term change canoccur without significantly altering the way analysts are paid at major underwriters, "Thecompensation of the analyst conies out of the pocket of the investment bank. That is thebiggest problem of all," says George Salem, a retired bank-stock analyst who took a lot ofheat at several firms for his critical view of the industry. Salem's controversial calls dateto the early 1980's, an indication of just how long the problem has been going on.

After May Day 1975, when commissions were deregulated, firms began focusing oninvestment banking revenue to pay the analysts' keep. The Chinese wall has been erodingever since, pretty much crumblin g over the last decade, as many firms even quitseparating the two groups. Analysts have worked on M&.A deals and have become key tolanding plum underwriting assignments. Bonuses have become directly tied to the deals

• analysts work on. And analysts pay and prominence, boosted by their media appearanceson such media outlets as CNBC, have never been greater than in the last couple of yearsof the bull market.

"I don't see much hope for changing the problem until you change the compensation,"says Chuck [WI, director of research at First Call/Thoruson Financial. "When you've got

• big bucks on the line, whether you consciously go along with it or whether you try to beobjective, 1 think subconsciously at least something creeps in there."

• Many in the industry think that the compensation structure is just plain wrong. "Researchanalysts should not be compensated out of an investment banking budget," says Salem."When they are working in a research department. they are supposed to be working for

• the 'investor': Salem, and others, say that changing the situation would require

• 'enforcement action from the SEC.... For now, the industry is grappling with solutions

• to handling the conflict of interest that analysts face. "These conflicts of interest exist andthere is no question that the managing of these conflicts needs to be improved," saysPatricia Walters, senior vp, professional standards and advocacy at the Association for

• investment Management and Research, an industry group of analysts, who is working ona set of objectivity standards it plans to release shortly. 'F he industry group's membershipis primarily composed of buy-side analysts, not those working fbr Wall Street'sinvestment banks.

Again, it comes down to money. If the compensation scheme and job description relatespurely to the investment process, and there is no incentive for the analyst to participate inany fashion on the corporate banking side, in terms of either new business opportunitiesor developing information to he used hy COT-pm-air billikeiti, ihtfil you mally 118Vt! Crecled

true firewall," says Samuel Jones, senior vp and chief investment officer at Trillium Asset

-14-

. •. .

.1

• ‘.Management Corp. in Boston. who is a member of the AIMR task force.

38. The New York State Attorney General began an investigatis..)ri into conflicts of

interest between Merrill Lynch's research analysts and its investment bankers.

39. On April g , 2002, following a ten-month investigation. New York State

Attorney General Eliot Spitzer filed a General Business Law Article 23 -A action against

Merrill Lynch detailing in an extensive affidavit the material misrepresentations and omissions

of Merrill Lynch and its analysts, beginning in late 1999, in connection with Merrill Lynch's

investment banking relationship with certain Internet companies, and Merrill's false and

misleading analyses of those Internet companies. The result of that investigation and litigation••,:

was an ugreement on May 21, 2002 between Merrill Lynch and Spitzer under which Merrill

Lynch agreed to pay tines of $100 million.

40. In an article entitled "Requiem for an I Ionorable Profession," concerning the

conflicts of interest between research and investment banking and the New York Attorney

General's investigation into Merrill Lynch's practices, the New York Times wrote:

Similar reorganizations [of research and investment banking departments to avoidconflicts of interest, as then was being discussed as part of - the proposed Merrill Lynchsettlemen[]. may well he needed at other firms. INIneh also transfortned their researchdepartments into sales forces. All of the analysts who spoke of their experiences at thelargest firrns on the Street, including Merrill, Salomon Smith Barney. J.P. MorganSecurities and Morgan Stanley Dean Witter, said that most of their time was spent not inanalyzing companies financial statements and operations, making the right calls rurinvestors, but in selling their firms' services.

"You were not so much an analyst as a marketing machine." said une formeranalyst who spoke on condition oranonymity. "Market to the sales force, to the bankers,to the is.suers, to the big investors so you could get that following that perpetuates yourbanking capabilities."

-15-

. .

How helpful analysts were to the investment bankers was central to theircompensation and to their job security, the former analysts said....

41. Indeed, in the summer of 1998, when Merrill Lynch was eager to win more

investtnent banking business from Enron. Merrill replaced a research analyst who had angered

Enron executives by rating the company's stock 'neutral" with an analyst who soon upgraded

the rating, according to Congiessional investigators as reported in the July 30, 2002 New York

Times.

42, The New York State Attorney General is now beginning to investigate other

Wall Street firms, particularly Morgan Stanley and Salomon Smith Barney. Regulators fronn

several other states, including California and New Jersey, have agreed to help Attorney Genera!r,

Spitzer. New York Times, June 18, 2002.

43. On July 11, 2002, Morgan Stanley filed its Repoit 10-Q lot the quarter ended

May 31, 2002. IVISDW announced that in addition to the ongoing investigations by the SEC,

NASD, New York Stock Exchange and the New York State Attorney General into research

analyst - investment banking conflicts, the United States Attorney's Office fur the Southeni

District of New York had served MSDW with a request for documents. The July 12, 2002

New York Times stated that securities firms including MSDW may now face criminal charges.

44. Morgan Stanley boasts that it has one of the world's Finest teams of stuck

analysts. New York Tirnes, July 7, 2002.

45. Members of - the Class were not made aware ol - the conflicts ol interest that lay at

the heart of MSDW's ieseaich and analysis department. As a result. Class members who

purchased Tech Fund shares were severely damaged by defendants' unlawful conduct as

-16- 4

.;

"-, described herein.

46. MSDW earned millions of dollars in fees in connection with these transactions,

and many of MSDW's research analysts were compensated as if they were investment bankers

rather than research analysts.

,Morgan Stanley's IPO for the Technology Fund

47. Morgan Stanley decided to use its paramount reputation on Wall Street,

including the reputation of its securities research, to start a technology fund,

48. MSDW filed a Registration Statement with the SEC on June 16, 2000.

49. the Registration Statement was amended by an SEC filing on August 7, 2000,

which contained a draft in ospeetus and statement uf additional information.

50. The final Prospectus and Statement of Additional Information which was

distributed to prospective purchasers is dated August 17. 2000 and was filed with the SEC on

or about September 19, 2000,

51. The Fund's initial offering was from approximately September 25, 2000 through

October 24, 2000. The initial offering price was $10.00 per share.

52. A subsequent lirospeetus (dated October 31, 2001) was filed with the SEC on

November 16, 2001, and became effective on or about October 31. 2001.

53. In the Fund's first semi-annual report in 2001 filed with the SEC on April 20,

2001, which covered its first four months of operation through February 28. 2001, the Fund liad

over 150 million shares outstanding, with at least 8 million shares outstanding in each of the

four classes.

-17-

; •

54. In the Fund's most recent semi-annuat repnrt filed April 23, 2002, for the six

month time period ending February 28, 2002, the Fund had over 150 million shares

„outstanding, with at least 6 million shares in each of its four classes.

55. The total cost of its common stock portfolio, as stated in its first semi-annual

report, was approximately $1.289 billion.-

56. The total value of the Fund's common stock portfolio as of end of the time

period covered by the serni-annual report dated April 23. 2002, was $480.1 million as of

February 28, 2002.

57. As of July 30, 2002, the per share price had declined hum $10.00 per share to

approximately $2.73 per share. The hind's low price was approximately $1.97 per share,

reached toward the end of July, 2002.

58• To date, the Fund has lost appioximately $800 million. which is at least

approximately 73% of its original value.

TIIE FALSE AND MISLEADING STATEMENTS AND MATERIALOMISSIONS CONTAINED IN "1 - 11E ItEGISTRATION STATEMENT,

PROSPECTUS AND STATEMENT OF ADDITIONAL INFORMATION

59. The defendants were: (1) the underwriters tor the common stock ofcertain of

the companies in the Fund's portfolio (and, hence the agents or former agents of those

companies); (2) the investment bankers and corporate finance specialists for certain of the

companies whose seciiriiies iire iii tlie Fund's portfolio; (3) seeking to obtain additional

investment banking business from these present and former clients and from other companies

whose shares also were/arc if] iIic FIJI !TS pOr110110. (4) the issuers of all shares in the Fund; (5)

-18-

_

preparing and publicly disseminating research reports and recommendations on many of the

• companies who shares wete in the Fund's poi tfolio; and (6) the broker for certain members of•

- • the Class.•

60. Hence, MSDW and the ether defendants had a duty to plaintiffs arid the Class to

provide information which was truthful and was not false or misleading; and to disclose

information which was material to plaintiffs and the Class in their decisions to purchase or sell

shares of the Fund.

61. The Registration Statement, Prospectuses, and Statement at Additional:

Information entitled to disclose. numerous FTEliCii rril ci iii WCIC FtitillifV.11 u IIC isc1ii! iii

order to render the statements made therein not materially misleading at the time it was

declared effective and thereafter. including but not limited to that:

(1) defendants failed to disclose and omitted material information that MSDW

had had investment banking relationships with, including having brought public, certain of thc

companies whose securities were part of the Fund's portfolio. Defendants disclosed neither this

general fact nor the identities of the particular companies with which it had investment banking

relationships.

(2) defendants failed to disclose and omitted material information concerning that

, MSDW was continuing to seek investment banking relationships with many of the companies

whose securities were part of the Fund's portfolio:

(3) defendants failed to disclose and omitted material information concerning that

a material part of the total compensation paid to MSDW research analysts was based upon

,-19-

...

"!

obtaining investment banking business for IvISDW and not upon the accuracy of their research

- about a given company. I Ience, MSDW and its affiliated companies including the Fund

recommended investtnents in and/or invested in companies in order to enhance MSDW's

opportunity to obtain investment banking business lion' those companies (without regard to

whether they were good investments for the investors including plaintiffs and the (lass); and

(4) although the Prospectus states that the Fund may engan in active and

frequent trading of its portfolio sectuities. The Fund's portfolio turnover rate may exceed

250%"; defendants failed to disclose and omitted material information that the Fund would

keep portfolio positions if it thought retaining ownership of that company's securities would

enhance MSDW"s chance of obtaining, investment banking business from that company, even if

that security was no longer a good investment and the security otherwise would have heen sold

by defendants.

62. MSDW had been thc underwriter for the initial public offerings for thc

following securities which defendants purchased for the Technology Fund: limeade

Communications Systems, Inc., Cisco Systems, Inc., Apple Computer. Inc., Ariba, Inc., AT&T

Wireless Group, inc.. Cachellow Ine,, CuraCien Corporation, FLAG Telecom Ifoldings Ltd.,

Palm, Inc., Redback Networks Inc., VeriSign, Inc., Veritas Software Corp., and Rroadcom

Corp. The Fund also owned Time Warner Telecom Inc.. for which MSDW had acted as

underwriter in a secondary public offering. MSDW also did , investmcnt banking work in the,

transactions involving Norte' and Alcatel, two other securities contained in the hind portfolio,

• with respect to Is,1&A transactions. Upon information and belief, defendants participated in

-20-

. ,..• _

other offerings and corporate Finance work for other corporations vvhosc securities were

• purchased for the Fund's portfolio.

SCIENTER ALLEGATIONS

63. Defendants knew that a material part of the total compensation of MSDW's

• research analysts was based upon their origination/involvement in investing banking

transactions rather than upon their research.

64. Whether or not they had a 1,viit1en document concerning their total compensation

arrangement, virtually all senior research analysts and some mid-level research analysts on

Wall Street (including those at 11.4SUW) have an express understanding that a material part of

their total compensation is based upon their origination/involvement in investing banking

transactions rather than upon their research.

• • •

• 65. If in \Nriting, such a doeun tent would provide that a material part or the research• •

analyst's total compensation would be based upon their origination/involvement in investing

.•banking transactions rather than upon their research.

•

. 66. Such a document often states that the research analyst would receive a certain

percentage of the investment banking fee derived from the public offering or other transaction• •

which they originated.

. .67. For example, MSDW analyst Mary Meeker acted more like an investment

hanker, participating in deal-making and business generatin activities, in the hopes of securing

• lucrative investment banking fees for lvISDW and substantial compensation for herself, which

reportedly reached $15 million in 1999 (according lo the April 22, 2001 The Times ni l.on(fon).

-21-

68. Defendants knew that potential purchasers would consider it material that

defendants had in the past and were presently seeking investment banking relationships with

many of the companies whose securities were in the Technology Fund's portfolio.

• 69. Many research reports slate that the broker-dealer has or is seeking investment

banking relationships with the corporation %Odell is the subject of the reports. But, the

defendants did not disclose these material relationships and facts detailed above, including but

not limited to that they failed to disclose in the relevant public filings.

70. Regulatory rules require that ftinis maintain a "Chinese wall': however, that

• wall apparently has crumbled, with research analysts directly performing investment banking

. functions and receiving compensation based on their contributions to generating investment

banking business. including underwriting initial public offerings ("1P(Ys") and secondary

offerings of equity securities, underwriting debt ollerings, and performing services in merger

and acquisition transactions, without disclosing such material conflicts of interest to the

investing public.

71. Defendants did not disclose that there was no Chinese Wall between research

and investment tiatikingicuiporate finance.

72• One factor in a corporation retaining an underwriter for its public offering is

whether the broker- dealer will support the price of the stock through its market-making

activities.

73• Buying millions of dollars worth of stock for a related mutual fund has the same

positive impact on supporting the stock price (by removing stock from the tuarket, to control

-2.2-..

•

• . 1. .

• • • • • • •A

• . •

the shares, so that large sales do not inordinately depress the stock price) as does traditional

market-making activity itself.

74. The Defendants' unlawful conduct allowed MSDW to gain millions of dollars in

commissions through sales of the Technology Fund and million of &Hats in fees during the

Class Period.

75. Members of the Class lost enormous sums of money investing in the Fund as a

result of Defendants' unlawful conduct.

COUNT• •

Against Each Defendant for Violation of5 10(3) of the Exchane Act and Rule 10b-5

•76. Plaintiffs repeat and reallege all preceding and subsequent paragraphs as if set

•

. .•

forth fully herein.

• 77. During the Class l'criod, Defendants carried out a p/an, scheme and course of

• conduct, as alleged herein, which was intended to. and did, throughout the Class Period: (i)

deceive the investing public, including plaintiffs and other Class members; (ii) cause plaintiffs

and other members of the Class to purchase Fund shares which they would not have otherwise

purchased. In furtherance of this unlawful scheme, plan and course of conduct, defendants

took the actions set forth herein.

78. Defendants: (i) employed devices. schemes. and artifices to defraud; (ii) made

untrue statements of material fact and/or omitted to state malcrial facts necessary to make thc•

statements not misleading; and (iii) engaged in nets. practices and a course of conduct which

operated as a fraud and deceit upon the purchasers of Fund shares in an effort to fraudulently

-23-

...

: •

.1"-C •.• '

.ls •

• •

. s

• induce purchases of the Fund shares in violation of Section 10(b) of the Exchange Act and

• Rule 10h-5.

• 79. As a result of the dissemination of the materially false and misleading

• .information and failure to disclose material facts as alleged herein. plaintiffs and members of

the Class purchased shares in the Technology Fund which they would not have purchased but

. .for defendants' unlawful conduct.

i. 80. Relying directly or indirectly on the fake and misleading statements made by•• •

• the defendants, and/or on the absence of material information that was known to defendants but•..

not disclosed in public statements by defendants during the Class Period, plaintiffs and the

other members of the Class acquired shares of Fund shares during the Class Period and were

• • damaged thereby.

81. At the time of the misrepresentations and omissions as alleged herein, plaintiffs

• and the other members of the Class were ignorant of their falsity and believed them to be nue.

}lad plaintiffs and the other members of the Class known the material information omitted

pursuant to defendants' fraudulent scheme, plaintiffs and the other members of the Class would

,;;:...• not have purchased or otherwise acquired Fund shares during thc Class Period. or. if they had

acquired such shares during the Class Period, they would not have done so at the prices which

they paid.

82. By virtue of the foregoing, defendants violated Section 10(1)) of the Exchange

Act and Rule 10b-5 promulgated thereunder and are liable to plaintiffs and the other members

of the Class. •

-24-..

•

: p

83. As a direct and proxirnate result of defendants unlawfill conduct as alleged-

herein, plaintiffs and the other members of the Class suffered damages in connection with their

• purchases of Fund shares during the Class Period.

COUNT II

r., Against Defendant IVISDNV forControlling Person Liability Pursuant 10 20(a) of the Exchange Act

84. Plaintiffs repeat and reallege all preceding and subsequent paragraphs as if set

forth fully herein.

85. With respect to the unlawhil conduct alleged herein, IVISDW is a controlling

person pursuant to Section 20(a) of- the Exchange Act, 15 U.S.U. § 78t(a), because it controlled

the dissemination of the Registration Statement and Prospectus and had and exercised the

power and influence to 4:4111NC the other defendants to engage in the conduct complained of

• herein, and had the power to cause the other defendants to refrain fr(ini the conduct complained

of herein.

86. By virtue ()ilia! foregoing, 11-1SDW is liable to plaintiffs and the other members

of the Class.

87. As a direct and proximate result oflVISDW's unlawful conduct as alleged

herein, plaintiffs and the other members of the Class suffered danines in connection with their

purchases of Fund shares during the Class Period.

-25-

. !

•

„•.

COUNT HI

Against the Fund and Distributors For Violation of§ 11 of the Securities Act and Against MOW

Under § 15 of the Securities Act for Violation of § 11 •

88. Plaintiffs incorporate each of the foregoing paragraphs as if fully set forth•

hcrcin.

'Hi • • 89. The Technology Fund is the issuer of thethares sold pursuant to the

. Registration Statement and Prospectus.

90. Distributors was the principal underwriter of the Fund's share. offering.

91. Technology Fund and Distributors participated in the preparation of, issued,

caused to be issued and participated in the issuance of the materially false and misleading

• -Registration Statement and Prospectus, which was inaccurate and misrepresented or failed to

disclose, inter alia, certain material facts, as set forth herein. None of these defendants made a

reasonable investigation or possessed reasonable grounds for the belief that the statements

contained in the Registration Statement and Prospectus vvcrc true, without omissions of any

material facts and were not misleading.

92. Distributors assisted in the preparation of the Registration Statement and

Prospectus, and was required to investi gate with due diligence the representations contained

therein to confirm that they did not contain materially- misleading statements or °inn to state

• material facts. Distributors did not perform this investigation Irvith due diligence and, indeed,

had a substantial direct interest in the success of the Offering, as detailed above and, thus, is

liable under Section 1 i of the Securities Act_

. .. .

-26-'

•. ...; .

• -r; n •

r .

,- '

-!, •

1. Ito

93. The Fund and Distributors IN ele responsible for the preparation of the

Registration Statement and Prospectus and failed to make a reasonable investigation or possess

reasonable grounds for believing that the representations contained in the Registration.*;

Statement and Prospectus were true and that they disclosed all material facts.

94. 114SW also is secondarily liable as a control person of the Fund under Section

15 of the Securities Act.

95. As a direct and proximate result of the false and misleading statements in the

Registration Statement and Prospectus, tens of millions of Fund shares yere sold in the

• Offering.

96. To date. the Fund has lost approximately 1 g00 million, which is at least

approximately 73% of its original value.

97. Plaintiffs and other members of the Class purchased their Fund shares in or

traceable to the Offering without knowledge of the untruths or omissions alleged herein.

98. 1 he action was brought within one year alter the discovery of the untrue

statements and omissions and within three years after the Fund was offered to the public.

• COUNT IV

' Against Each Defendant for Violation of § 12(a)(2) of the Securities Act andAgainst INISDIV Under § 15 of the Securities Act for Violation of § 12(a)(2)

99. Plaintiffs incorporate each of the foregoing allegations as it - fully set forth

herein.

100. Each defendant was a seller, offeror, and/or solicitor of sales of Technology

Fund shares for their financial benefit pursuant to the Registration Statement/Prospectus in

-27-

E

' a

connection with the Offering.:

101. None of thc defendants named in this Count made a reasonable investigation or

possessed reasonable grounds for the belief that the statements contained in the Registration

Statement were true, without omissions of any material facts and were not misleading.

102. The Registration Statement/ Prospectus contained misstatements of material

facts, omitted to state other facts necessary to make the statements made not misleading, and

concealed and failed to disclose material facts. Defendants actions of solicitation included but

were not limited to the preparation of thc false and misleading Registration Statement and

Prospectus disseminated to public investors.

103. Each defendant was responsible for the preparation of the Registration

Statement and Prospectus and failed to make a reasonable investigation or possess reasonable

grounds for believing that the representations comained in the Registration Statement and

Prospectus were true and that they disclosed all material facts. Each defendant is primarily

liable under Section 12 of the Securities Act.

; : 104. TvISDW also is secondarily liable as a control person of the kind tinder Section

,15 of the Securities Act.

105. Plaintiffs and other members of the Class purchased the Fund shares issued

pursuant to the false and misleading Registration Statement and Prospectus. Plaintiffs did not

know, or in the exercise of due diligence could not have known. of the untruths and omissions

contained in the Registration Statement and Prospectus.

106. By reason of the conduct alleged herein. the defendants violated. and/or

-28-

:

.•

5;4-•' 4

controlled a person who violated, Section 12( a)( 2) of the Securities Act,

107. Plaintiffs, individually and representatively, hereby elect to rescind and tender to

Distributors those securities that plaintiffs and the other members of the Class continue to own,

in return for the consideration paid for those securities together with interest thereon. Plaintiffs

and members of the Class who have sold their Technology Fund common stock are entitled to

recissory damages.

108_ The action was brought within one year after the discovery of the untrue

statements and omissions and within three years after the cot-ninon stock was offered to thc

PRAYER FOR R_ELI EF

WHEREFORE, plaintiffs, on behalf of themselves and on behalf of the Class, pray for

• judgment as follows:

A. Declaring this action to be a proper class action pursuant to Rule 23(a) and (b)(3) of.• .

the Federal Rules of Civil Procedure and certifying plaintiffs as class representatives

of the Class and their counsel as class counsel:

B. Against Defendants, jointly and severally, for damages suffered as a result of• •

Defendants' violations of the securities laws;

C. Awarding plaintiffs and the other members of the Class pre-judgment and post-

judgment interest, as well as their reasonable attorneys' fees and expert witness fees

arid other costs and expenses;

-29-

D. Awarding recission or recissionary damages to members of the Class who no longer

hold Technology Fund shares; and

E. Granting such other and further relief as the Court deems just and proper.

JURY DEMAND

Plaintiffs demand a trial by jury.

DM IA): July 31. 2002

WOLF HALDENSTEIN ADLERFREEMAN & HERZ, LIP

Daniel W. Krasner ( 1(6381)270 Madison AvenueNew York, NY 10016(elephone (212) 545-4600Fax (212) 545-4653

Attorneys For Plaintiffs279683

-riN` •

-

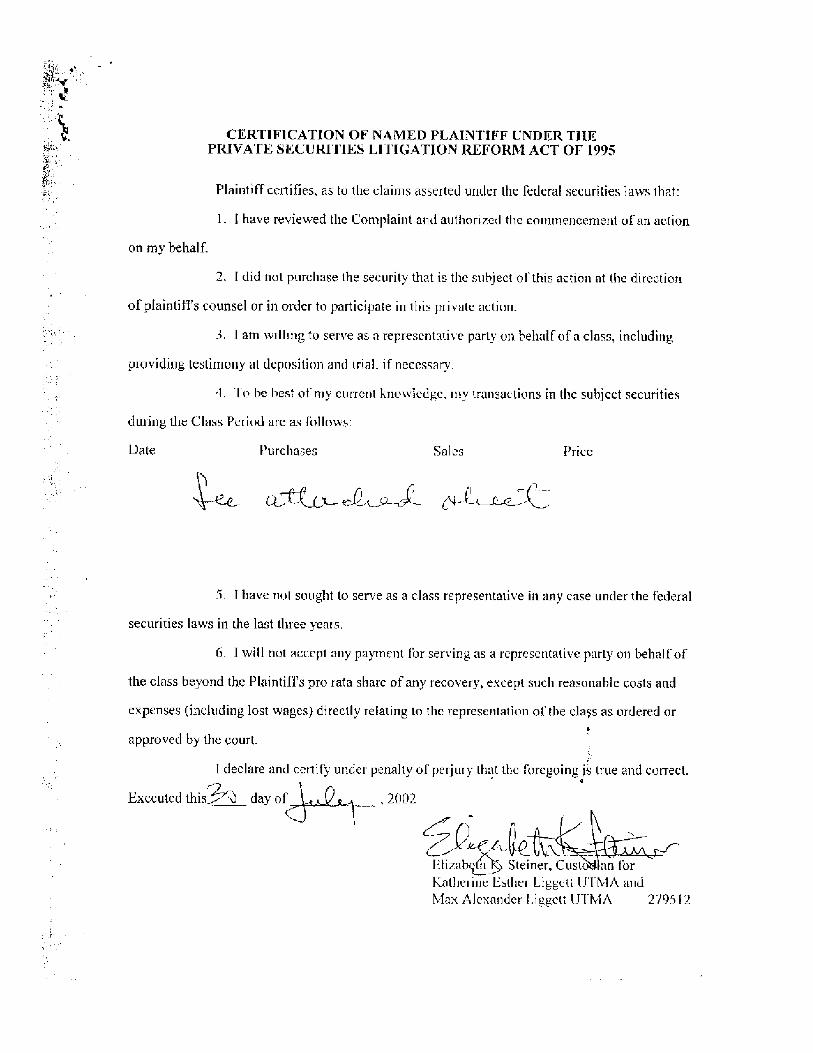

tfq CERTIFICATION OF NAMED PLAINTIFF UNDER TIIEst.L. PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

Plaintiff certifies, as to the claims asserted under the federal securities laws that:

1. I have reviewed the Complaint and authorized the commencement of an action

on my behalf.

2. I did not purchase the security that is the subject of this action at the direction

of plaintiffs counsel or in order to participate in this private action.

3. I am willing to serve as a representative party on behalf of a class, including

providing testimony at deposition and trial. if necessa7

lo be best of my current knowledge, my transactions in the subject securities

during the Class Period are as follows:

• Date Purchases Sales Price

• 1 I have not sought to serve as a class representative in any case under the federal

securities laws in the last three years.

6• I will not accept any payment for serving as a representative party on behalf of

the class be yond the Plaintiffs pro rata share of any recovery, except such reasonable costs and

expenses (including lost wages) directly relating to the representation of the class as ordered or

approved by the court.

I declare and certify under penalty of perjury that the foregoing is true and correct.•.

Executed this-_--"217.) day of , 2002

-(2-CA-(4) tin4, " -F.lizabgitt Steiner, Custo, an forKatherine Esther Liggett UTM A andMax Alexander Liggett UTMA 279512

'`voPlaintiffs Certification Attachment

Elizabeth K. Steiner, Custodian for Katherine Esther I.ipget 1.1 . 1 MA/NY

Date Purchases Sales Price•

10/11/00 1,000 shares Class C $10.0011/29/00 645.161 shares Class C $ 7.753112101 1,084.599 shares Class C $ 4.614/29/02 865.052 shares Class C $ 2.89

Elizabeth K. Steiner, Custodian for Max Alexander Ligget IJIMA/NY

Date Purchases Sales Price

10/11/00 1,000 shares Class C $10.0011/29/00 645.161 shares Class C S 7.753112/01 1,084.599 shares Class C $ 4.614/29/02 865.052 shares Class C 5 2.89

,