Eliminating Standard Costing: A Step-by-Step Methodology · 2017-09-29 · 8/29/2017 1 Eliminating...

13

8/29/2017 1 Eliminating Standard Costing: A Step-by-Step Methodology Nick Katko COO & CFO Tenmast Software Company Lexington, KY 1. GAAP Principles 2. Lean Inventory Valuation & GAAP Compliance 3. Lean Inventory Valuation Examples 4. Wrap Up & Questions Workshop Agenda

Transcript of Eliminating Standard Costing: A Step-by-Step Methodology · 2017-09-29 · 8/29/2017 1 Eliminating...

8/29/2017

1

Eliminating Standard Costing: A Step-by-Step Methodology

Nick Katko

COO & CFO

Tenmast Software Company

Lexington, KY

1. GAAP Principles

2. Lean Inventory Valuation & GAAP Compliance

3. Lean Inventory Valuation Examples

4. Wrap Up & Questions

Workshop Agenda

8/29/2017

2

GAAP Principles Inventory Valuation and Cost of Goods Sold

“Actual expenses incurred to get goods in condition for sale”

Inventory at Cost

Acquisition Costs

Production Costs

“ involves many

considerations”

8/29/2017

3

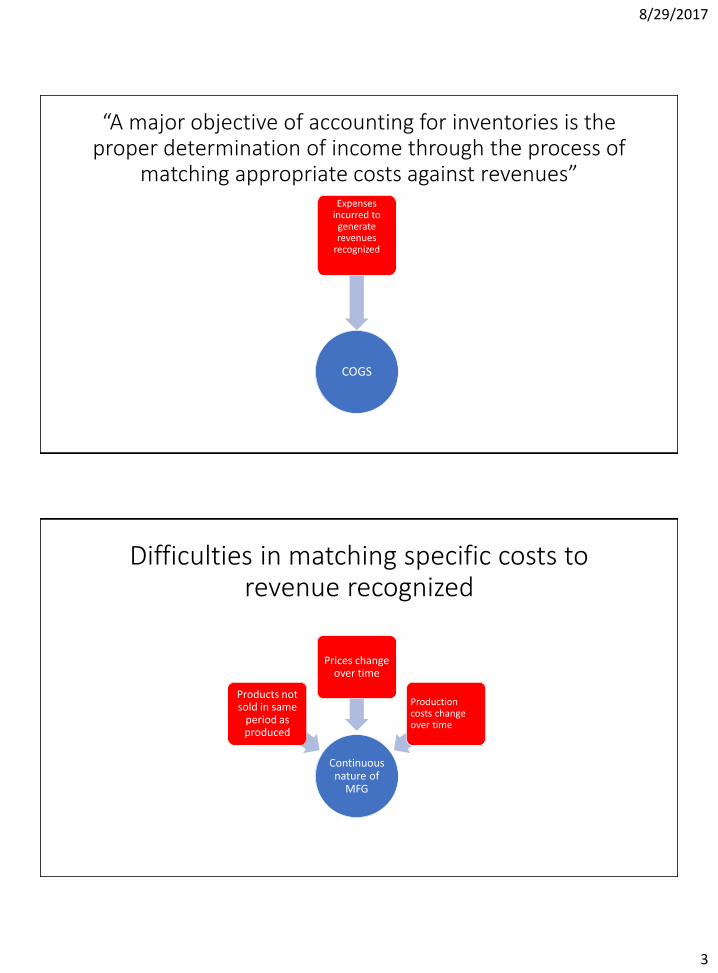

“A major objective of accounting for inventories is the proper determination of income through the process of

matching appropriate costs against revenues”

COGS

Expenses incurred to generate revenues

recognized

Difficulties in matching specific costs to revenue recognized

Continuous nature of

MFG

Products not sold in same

period as produced

Prices change over time

Production costs change over time

8/29/2017

4

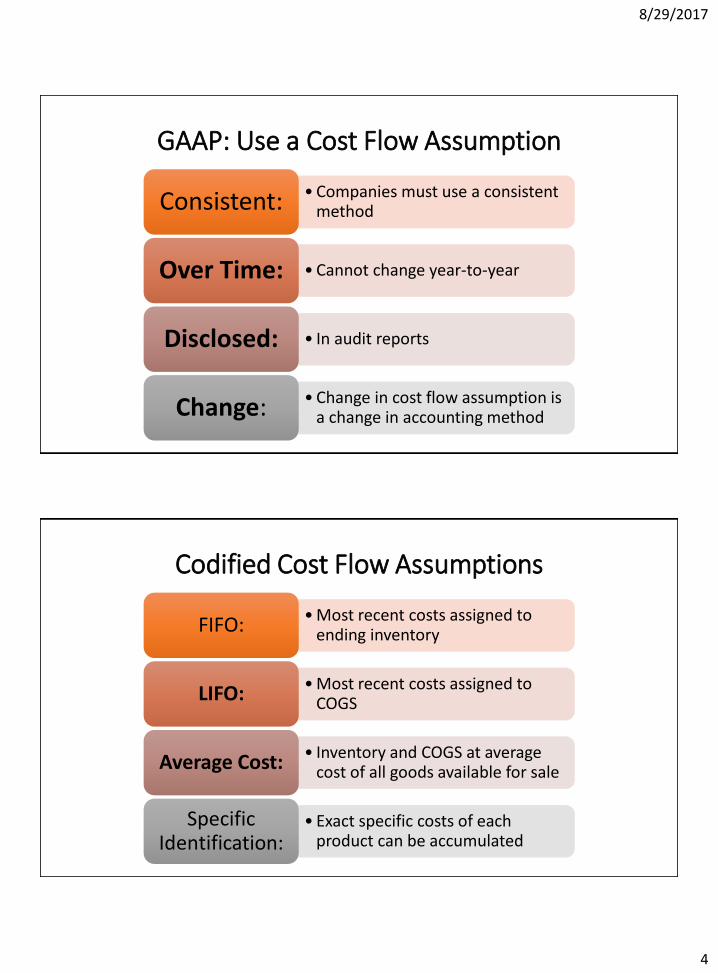

GAAP: Use a Cost Flow Assumption

• Companies must use a consistent method Consistent:

• Cannot change year-to-year Over Time:

• In audit reports Disclosed:

• Change in cost flow assumption is a change in accounting method Change:

Codified Cost Flow Assumptions

• Most recent costs assigned to ending inventory FIFO:

• Most recent costs assigned to COGS LIFO:

• Inventory and COGS at average cost of all goods available for sale Average Cost:

• Exact specific costs of each product can be accumulated

Specific Identification:

8/29/2017

5

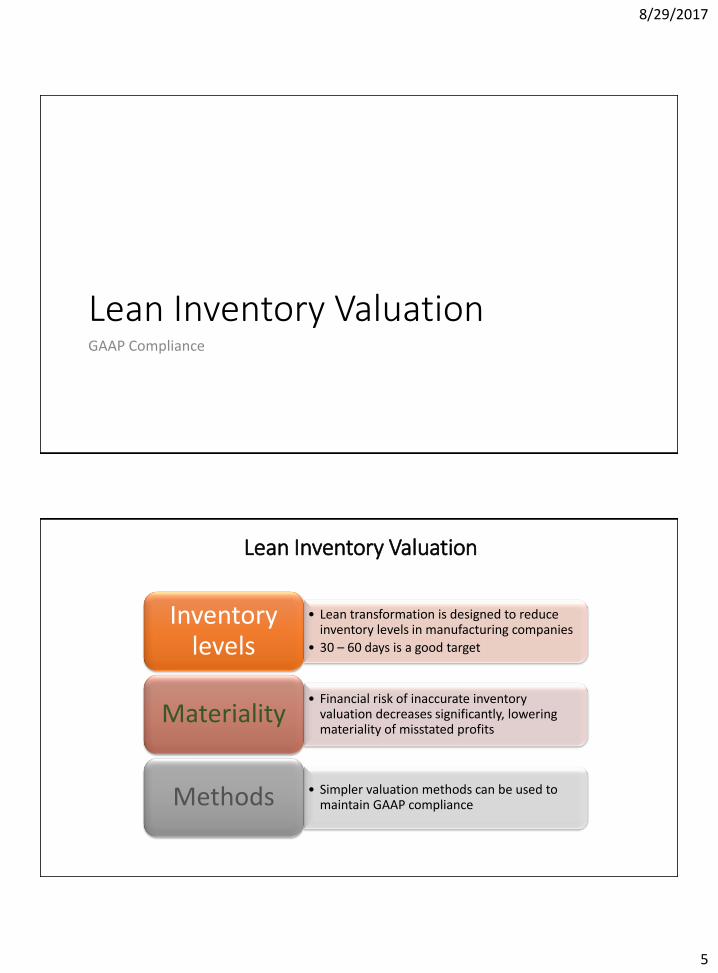

Lean Inventory Valuation GAAP Compliance

Lean Inventory Valuation

• Lean transformation is designed to reduce inventory levels in manufacturing companies

• 30 – 60 days is a good target

Inventory levels

• Financial risk of inaccurate inventory valuation decreases significantly, lowering materiality of misstated profits

Materiality

• Simpler valuation methods can be used to maintain GAAP compliance Methods

8/29/2017

6

Lean Inventory Valuation & GAAP

• Inventory and COGS at average cost of all goods available for sale

• But not individual product costs

Average Cost:

• 30-60 Days Low

Inventories:

Lean Inventory Valuation - Material

Quantity Monthly physical

Track in ERP

Cost VSP&L: average cost per unit or

per day

Individual part: average cost or last price paid

Few Parts Many Parts

8/29/2017

7

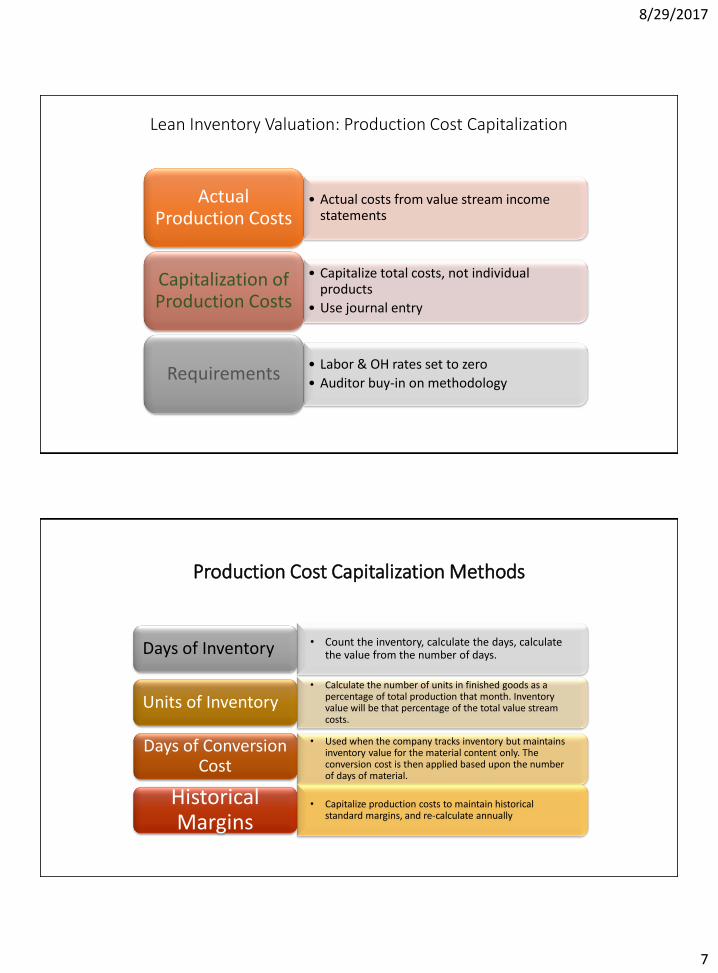

Lean Inventory Valuation: Production Cost Capitalization

• Actual costs from value stream income statements

Actual Production Costs

• Capitalize total costs, not individual products

• Use journal entry

Capitalization of Production Costs

• Labor & OH rates set to zero

• Auditor buy-in on methodology Requirements

Production Cost Capitalization Methods

• Count the inventory, calculate the days, calculate the value from the number of days. Days of Inventory

• Calculate the number of units in finished goods as a percentage of total production that month. Inventory value will be that percentage of the total value stream costs.

Units of Inventory

• Used when the company tracks inventory but maintains inventory value for the material content only. The conversion cost is then applied based upon the number of days of material.

Days of Conversion Cost

• Capitalize production costs to maintain historical standard margins, and re-calculate annually

Historical Margins

8/29/2017

8

Lean Inventory Valuation Examples

TOTAL

$2,048,686

$849,526

$312,984

$342,421

$116,550

$53,731

$41,200

$9,664

$1,726,076

$322,610

16%

$1,186,035

$963,148

($222,887)

$99,723

5%

Calculate the Inventory Value Using the “Days of Inventory Method”

REVENUE

Materials

Direct Labor

Support Labor

Machines

Outside process

Facilities

Other Costs

TOTAL COST

VALUE STREAM PROFIT

Return on Sales

Opening Inventory

Closing Inventory

Inventory Adjustment

NET PROFIT

1. Calculate the material cost per day. 2. Calculate the conversion cost per day 3. Calculate Raw Material value (#days * material cost per day) 4. Calculate the Finished Goods value (#days *( material + conversion

cost per day)) 5. Calculate WIP value (#days * material cost per day + #days/2 *

conversion cost per day) 6. Calculate total inventory value by adding the three together

TOTAL

$2,048,686

$849,526

$312,984

$342,421

$116,550

$53,731

$41,200

$9,664

$1,726,076

$322,610

16%

$1,186,035

Closing Inventory

Inventory Adjustment

Days in the month Total Material CostMaterial Cost per

Day

Total Conversion

Cost

Conversion cost

per day

20 $849,526 $42,476 $876,550 $43,828

Days Material Value Conversion Value Total Value

Raw Material 10 $424,763 $0 $424,763

Work in Process 3 $127,429 $65,741 $193,170

Finished Goods 4 $169,905 $175,310 $345,215

TOTAL INV VALUE 17 $722,097 $241,051 $963,148

Days in the month Total Material CostMaterial Cost per

Day

Total Conversion

Cost

Conversion cost

per day

20 $849,526 $876,550

Days Material Value Conversion Value Total Value

Raw Material 10

Work in Process 3

Finished Goods 4

TOTAL INV VALUE 17

8/29/2017

9

Total Units

Manufactured Total Material Cost

Average Material

Cost per Unit

Total Conversion

Cost

Average

Conversion cost

per Unit

22,861 $849,526 $37.16 $876,550 $38.34

Quantity Material Value Conversion Value Total Value

Raw Material 11,430 $424,744 $0 $424,744

Work in Process 3,430 $127,460 $65,758 $193,218

Finished Goods 4,573 $169,898 $175,341 $345,276

TOTAL INV 19,433 $963,238 $722,140 $241,098

TOTAL

$2,048,686

$849,526

$312,984

$342,421

$116,550

$53,731

$41,200

$9,664

$1,726,076

$322,610

16%

$1,186,035

$963,163

($222,872)

$99,737

5%

Calculate the Inventory Value Using the “Number of Units Inventory Method”

REVENUE

Materials

Direct Labor

Support Labor

Machines

Outside process

Facilities

Other Costs

TOTAL COST

VALUE STREAM PROFIT

Return on Sales

Opening Inventory

Closing Inventory

Inventory Adjustment

NET PROFIT

1. Calculate average material cost and average conversion cost 2. Calculate Raw Material value (#units * material cost per unit) 3. Calculate the Finished Goods value ((#units * material +

conversion cost per unit)) 4. Calculate WIP value (#units * material cost per unit + #units/2 *

conversion cost per unit) 5. Calculate total inventory value by adding the three together

TOTAL

$2,048,686

$849,526

$312,984

$342,421

$116,550

$53,731

$41,200

$9,664

$1,726,076

$322,610

16%

$1,186,035

Closing Inventory

Inventory Adjustment

Total Units

ManufacturedTotal Material Cost

Average Material

Cost per Unit

Total Conversion

Cost

Average

Conversion cost

per Unit

22,861 $849,526 $876,550

Quantity Material Value Conversion Value Total Value

Raw Material 11,430

Work in Process 3,430

Finished Goods 4,573

TOTAL INV 19,433

Calculate the Inventory Value Using the “Days of Conversion Cost Method”

Inventory Value

Materials Only

Number of Days in

the Month

Number of Days of

Inventory

$474,036 20 11.16

Inventory Value

Materials Only

Number of Days in

the Month

Number of Days of

Inventory

$474,036 20

This method is used when the company tracks inventory but maintains inventory value for the ,material content only. The conversion cost is then applied based upon the number of days of material.

1. Calculate the number of days of inventory. (Days in the month *

Inventory value / Monthly Material Cost) 2. Calculate the Conversion Cost Applied. (Number of days of

inventory * total conversion cost / Number of Days in the Month) 3. Calculate total inventory cost. (Add materials value plus

conversion cost applied)

Opening Inventory

Closing Inventory

Inventory Adjustment

NET PROFIT

TOTAL

$2,048,686

$849,526

$312,984

$342,421

$116,550

$53,731

$41,200

$9,664

$1,726,076

$322,610

16%

$1,186,035

$963,152

($222,883)

$99,726

5%

TOTAL

$2,048,686

$849,526

$312,984

$342,421

$116,550

$53,731

$41,200

$9,664

$1,726,076

$322,610

16%

$1,186,035

Closing Inventory

Inventory Adjustment

REVENUE

Materials Direct Labor Support Labor Machines Outside process Facilities Other Costs

TOTAL COST

VALUE STREAM PROFIT Return on Sales

Total Conversion

Cost

Conversion Cost

Applied

Total Inventory

Cost

$876,550 $489,115 $963,151

Total Conversion

Cost

Conversion Cost

Applied

Total Inventory

Cost

$876,550

8/29/2017

10

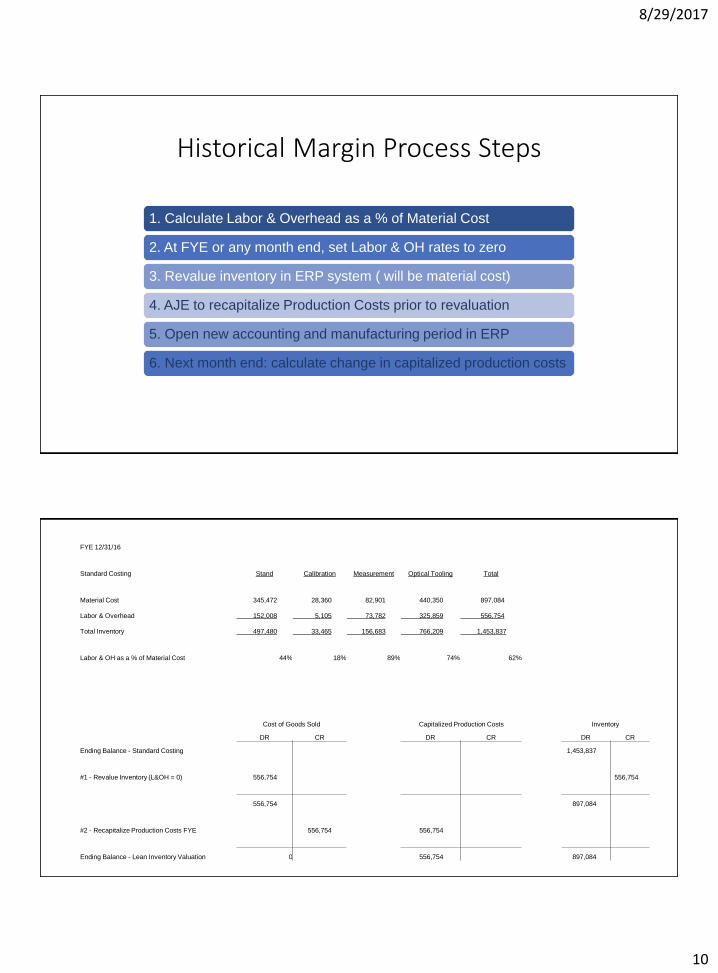

1. Calculate Labor & Overhead as a % of Material Cost

2. At FYE or any month end, set Labor & OH rates to zero

3. Revalue inventory in ERP system ( will be material cost)

4. AJE to recapitalize Production Costs prior to revaluation

5. Open new accounting and manufacturing period in ERP

6. Next month end: calculate change in capitalized production costs

Historical Margin Process Steps

FYE 12/31/16

Standard Costing Stand Calibration Measurement Optical Tooling Total

Material Cost 345,472 28,360 82,901 440,350 897,084

Labor & Overhead 152,008 5,105 73,782 325,859 556,754

Total Inventory 497,480 33,465 156,683 766,209 1,453,837

Labor & OH as a % of Material Cost 44% 18% 89% 74% 62%

Cost of Goods Sold Capitalized Production Costs Inventory

DR CR DR CR DR CR

Ending Balance - Standard Costing 1,453,837

#1 - Revalue Inventory (L&OH = 0) 556,754 556,754

556,754 897,084

#2 - Recapitalize Production Costs FYE 556,754 556,754

Ending Balance - Lean Inventory Valuation 0 556,754 897,084

8/29/2017

11

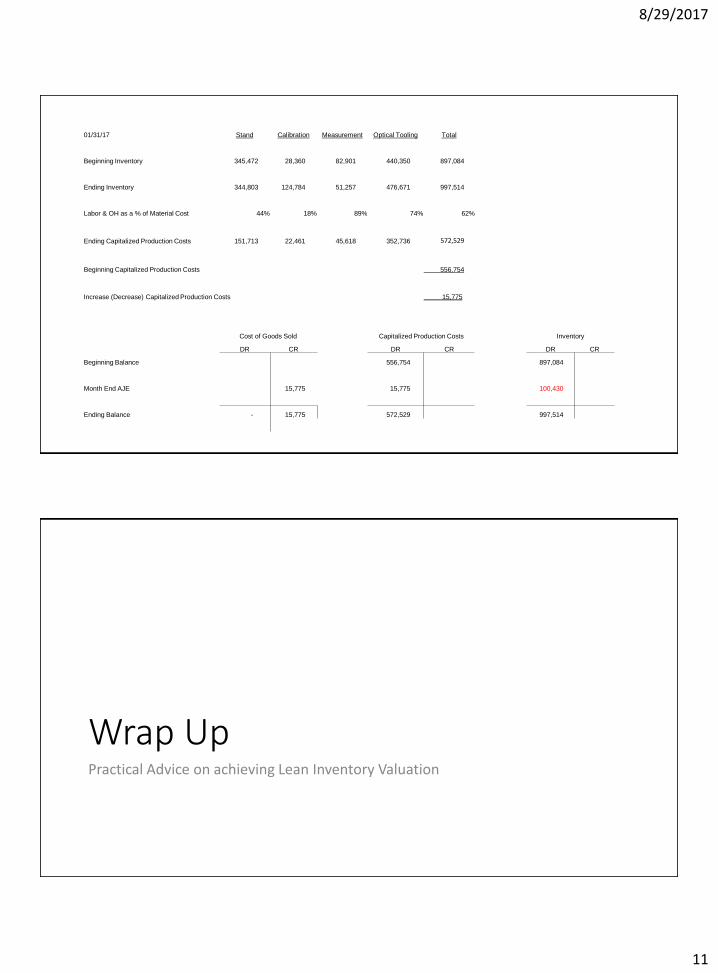

01/31/17 Stand Calibration Measurement Optical Tooling Total

Beginning Inventory 345,472 28,360 82,901 440,350 897,084

Ending Inventory 344,803 124,784 51,257 476,671 997,514

Labor & OH as a % of Material Cost 44% 18% 89% 74% 62%

Ending Capitalized Production Costs 151,713 22,461 45,618 352,736 572,529

Beginning Capitalized Production Costs 556,754

Increase (Decrease) Capitalized Production Costs 15,775

Cost of Goods Sold Capitalized Production Costs Inventory

DR CR DR CR DR CR

Beginning Balance 556,754 897,084

Month End AJE 15,775 15,775 100,430

Ending Balance - 15,775 572,529 997,514

Wrap Up Practical Advice on achieving Lean Inventory Valuation

8/29/2017

12

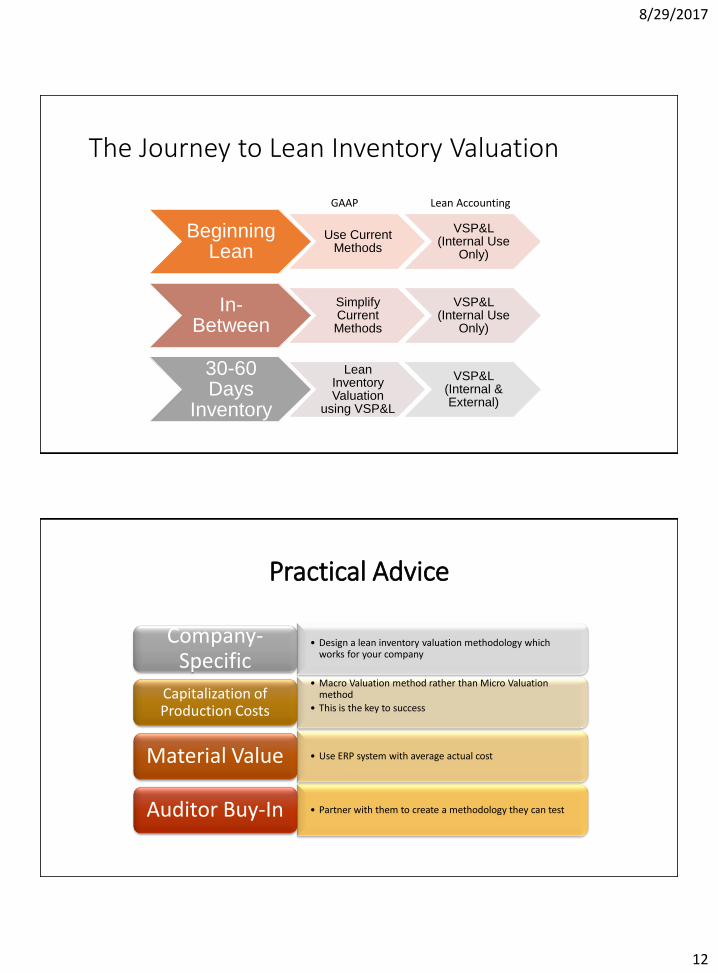

The Journey to Lean Inventory Valuation

Beginning Lean

Use Current Methods

VSP&L (Internal Use

Only)

In-Between

Simplify Current Methods

VSP&L (Internal Use

Only)

30-60 Days

Inventory

Lean Inventory Valuation

using VSP&L

VSP&L (Internal & External)

Lean Accounting GAAP

Practical Advice

• Design a lean inventory valuation methodology which works for your company

Company-Specific

• Macro Valuation method rather than Micro Valuation method

• This is the key to success

Capitalization of Production Costs

• Use ERP system with average actual cost Material Value

• Partner with them to create a methodology they can test Auditor Buy-In

8/29/2017

13

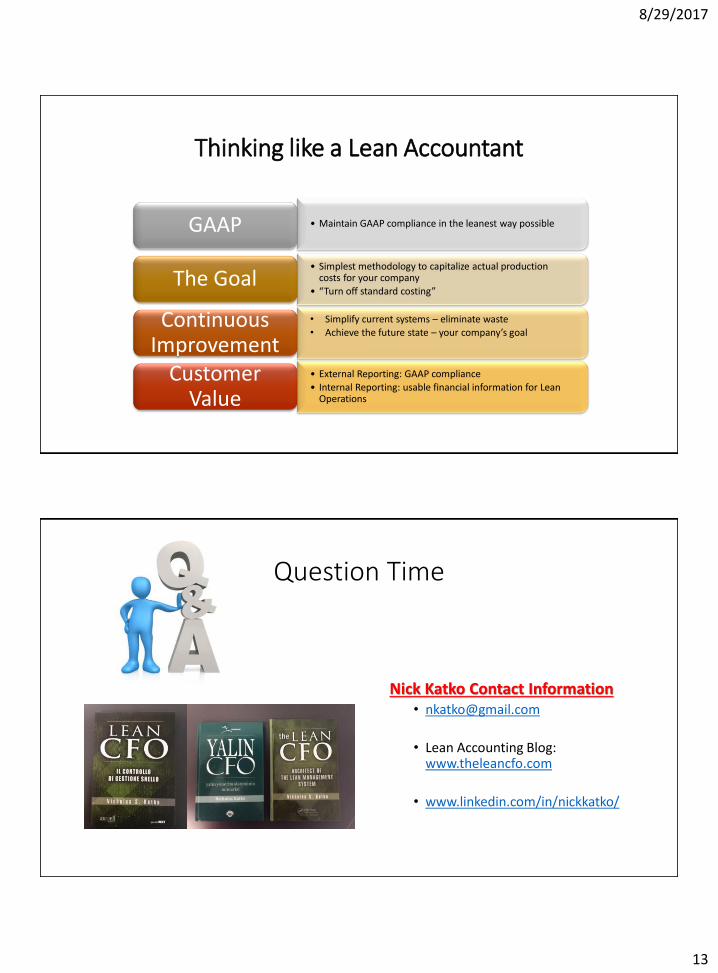

Thinking like a Lean Accountant

• Maintain GAAP compliance in the leanest way possible GAAP

• Simplest methodology to capitalize actual production costs for your company

• “Turn off standard costing”

The Goal

• Simplify current systems – eliminate waste

• Achieve the future state – your company’s goal

Continuous Improvement

• External Reporting: GAAP compliance

• Internal Reporting: usable financial information for Lean Operations

Customer Value

Question Time

Nick Katko Contact Information • [email protected]

• Lean Accounting Blog: www.theleancfo.com

• www.linkedin.com/in/nickkatko/