Electronic Placing in the London Market Market Reform Briefing

26

Electronic Placing in the London Market Market Reform Briefing Rob Gillies Head of Market Processes Lloyd’s Market Association

-

Upload

arden-willis -

Category

Documents

-

view

30 -

download

0

description

Electronic Placing in the London Market Market Reform Briefing. Rob Gillies Head of Market Processes Lloyd’s Market Association. Why electronic placement The electronic placement process Progress, experiences and lessons so far The future. Why electronic processes - PowerPoint PPT Presentation

Transcript of Electronic Placing in the London Market Market Reform Briefing

Electronic Placing in the London Market

Market Reform Briefing

Rob GilliesHead of Market Processes

Lloyd’s Market Association

• Why electronic placement

• The electronic placement process

• Progress, experiences and lessons so far

• The future

• Why electronic processes

• The electronic placement process

• Progress, experiences and lessons so far

• The future

1700 2000

2010?

Improved efficiencyReduced costs

Exploit strategic business opportunities

Why change?

Global and market change

Customer service demands

Need for increased return

on capital

Agents for Change

• The global marketplace

• Convergence of insurance and capital markets

• Growth of self-insurance

• High transaction costs

• Market process inefficiencies

• Restrictive practices

(Dennis Mahoney – Acord Forum London, 2007)

Global and market change

“We remain convinced that electronic processing is the future for this market…”

Ian Summers, Director of Change Strategy at Aon

“Exchanging structured data to support the placing process is the way the market has to go in the next few years if we are to remain competitive”

Trina-Lane Pearce, UK Operations Manager at Catlin

“In this market, companies that embrace new technology not only improve their business today, but they also safeguard their business for tomorrow”

Lisa Gibbard, Head of IT at Aspen

Realisation of Benefits

• Easy access to information from multiple systems

• Less administration for underwriter – reduced re-keying of data

• Ability to direct work to available resources (workflow)

• Reporting (business activity monitoring) to assist with process transparency and management controls

• External and internal auditing and compliance

• Automatic recording of quotes

• Improved data integrity

• Increased operational efficiency through the electronic exchange of information and workflow(Lisa Gibbard, Aspen Re – Market Reform Forum, March 2008)

• Why electronic processes

• The electronic placement process

• Progress, experiences and lessons so far

• The future

Mar

ket R

efor

m 2

008

Market Reform Offi ce

Steps towards the vision

Increase proportion of risks for which structured data is exchanged

Adopt MRCE & increase use of e-endorsements

Further reduce legacy risks

Adopt Electronic Policies

With

All risk submissions sent electronically; wholly electronic trading for some simple risks with no manual intervention; face-to-face when required for large and complex risks

Vision 2007—2009 To be the market of choice

2008 actions for market firms

All claims processed and agreed electronically; face-to-face negotiation only when required for complex claims

All accounting and settlement of risks performed electronically

P L A C I N G

C L A I M S

A & S

Develop and extend ECF

Adopt ECF for legacy claims

Implement service targets for ECF claims

Develop & extend IMR use for all payments

Extend use of De-linking

Increase use of ACORD messaging for A&S submissions

Electronic Placing Steering Group - Vision

The use of electronic processes, compliant with ACORD international

data standards, for the submission of risk details, the agreement of

terms, and contract formation for all risk placements and contract

amendments in the London market, enabling the selective use of

negotiation outside the electronic process where required by trading

partners.

The use of electronic processes, compliant with ACORD international

data standards, for the submission of risk details, the agreement of

terms, and contract formation for all risk placements and contract

amendments in the London market, enabling the selective use of

negotiation outside the electronic process where required by trading

partners.

What is electronic placing?

Face to Face

Complex

Face to Face, Telephone, Electronic

Moderate

Electronic

Simple

Negotiation

Data Exchange

Strategic Opportunities

• Less reliance on geographical boundaries

• Time freed up to concentrate on business acquisition

• Serve an enlarged customer base or branch network by increasing capacity to process business online

• Increase portfolio of simple, low volatility business

• Greater opportunities for market segmentation

• Global management of orders enables clear view and assignment of responsibility.

Increased Regulatory Compliance

• Increased use of industry model contracts eases compliance burden

• Earlier checks made to meet regulatory and risk management requirement

• Full audit trail for placing process

• Enhanced security of information

Increased Market Transparency

• Consistency in provision of data

• Data seamlessly translated from one market to another

Reduced Costs• Photocopying,

scanning and indexing of paper documents no longer necessary

• Reduced risk data capture time through straight-through-processing

• Simple endorsements processed fully electronically

• Lowering operational costs through efficiency gains

Increased Operational Efficiency

• Improvement in peer review process

• Earlier availability of data and documents for review

• Reduced risk of errors associated with manual processes

• Faster release of capital through earlier signed lines

• Quotes bound on line, speeding up placement process

• Improved exposure management

• Standard data re-used for A&S process

Electronic exchange of data and documents

Selective use of face-to-face negotiation

enables

Benefit delivery Benefit delivery

Improved customer service + Increased return on capital

Benefit delivery

Improved management information

Earlier sight of data and documents

Improved access to marketsMore productive use of time

Electronic exchange of data and documents

Selective use of face-to-face negotiationenables

Brokers (examples) Insurers (examples)Benefit delivery

Improving the broker-insurer relationship

Resource: Electronic Placing Benefits Model

Increased quality negotiating time

Opportunity to grow businessIncreased attention to the

customer

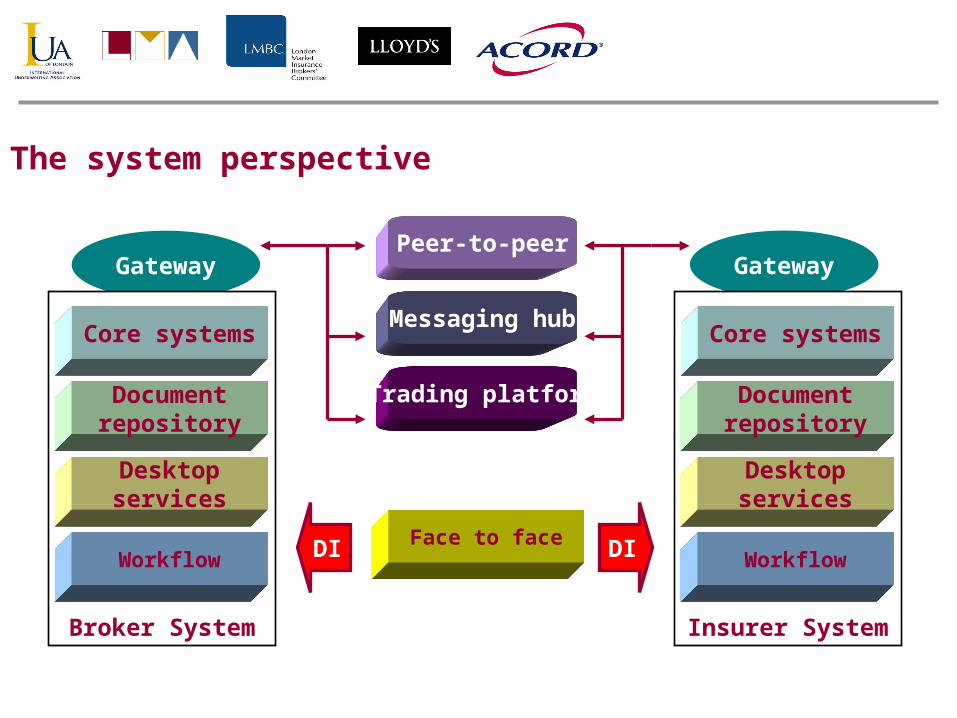

The system perspective

Face to faceDI DI

GatewayGatewayPeer-to-peer

Messaging hub

Trading platform

Insurer System

Core systems

Document repository

Desktop services

Workflow

Broker System

Core systems

Document repository

Desktop services

Workflow

The practitioner’s perspective

• Why electronic processes

• The electronic placement process

• Progress, experiences and lessons so far

• The future

Who’s doing what?

Trading Platforms• Aon use of RI3K

ACORD Messaging• Increasing numbers transacting live business• Increasing numbers positioning ready to participate• Benfield 1 April lead on two-way messaging

General• Much increased general level of interest over 2007• Other activity such as broker and underwriter portals and

eReinsure• Lloyd’s Information Exchange

Resource: Landscape Analysis

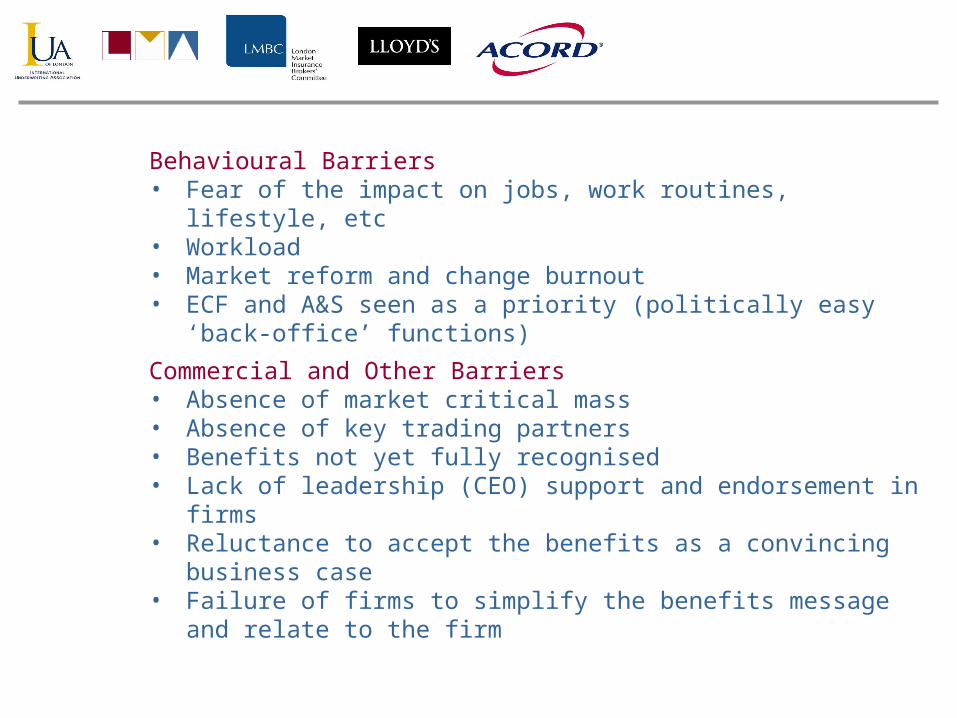

Experiences and lessons so far

Technological Barriers• Upgrading internal core systems• Conflict with other projects• Conflict with other reform activity• Integration with front and back office systems• Development of functionality by suppliers

Process Barriers• Failure to deliver minimum levels of value required by

organisations to participate• Version control between paper and electronic slips and other

documents• Duplicate processes – EP and non-EP• Slip signature and evidence of cover• Predominance of Outlook as user interface and ‘workflow’

tool• Differences between London and international processes

Behavioural Barriers• Fear of the impact on jobs, work routines, lifestyle, etc• Workload• Market reform and change burnout• ECF and A&S seen as a priority (politically easy ‘back-

office’ functions)

Commercial and Other Barriers• Absence of market critical mass• Absence of key trading partners• Benefits not yet fully recognised• Lack of leadership (CEO) support and endorsement in firms• Reluctance to accept the benefits as a convincing business

case• Failure of firms to simplify the benefits message and relate

to the firm

Commercial and Other Barriers• Absence of market critical mass (1)• Absence of key trading partners (2)• Benefits not yet fully recognised (3)• Lack of leadership (CEO) support and endorsement in firms

(5)• Reluctance to accept the benefits as a convincing business

case• Failure of firms to simplify the benefits message and relate

to the firm

Behavioural Barriers• Fear of the impact on jobs, work routines, lifestyle, etc (4)• Workload• Market reform and change burnout• ECF and A&S seen as a priority (politically easy ‘back-

office’ functions)

Top Five Barriers to Adoption

• Why electronic processes

• The electronic placement process

• Progress, experiences and lessons so far

• The future

Current and Planned Activity

Roadmap• One way placing• Two way placing• Multi-section risks• Additional messaging capability• Additional structured data• Alignment with eMRCE• Broker engagement• Market wide Class of Business pilot

Implementation Group• Evidence of cover• Adherence to validation rules

Resource: Roadmap

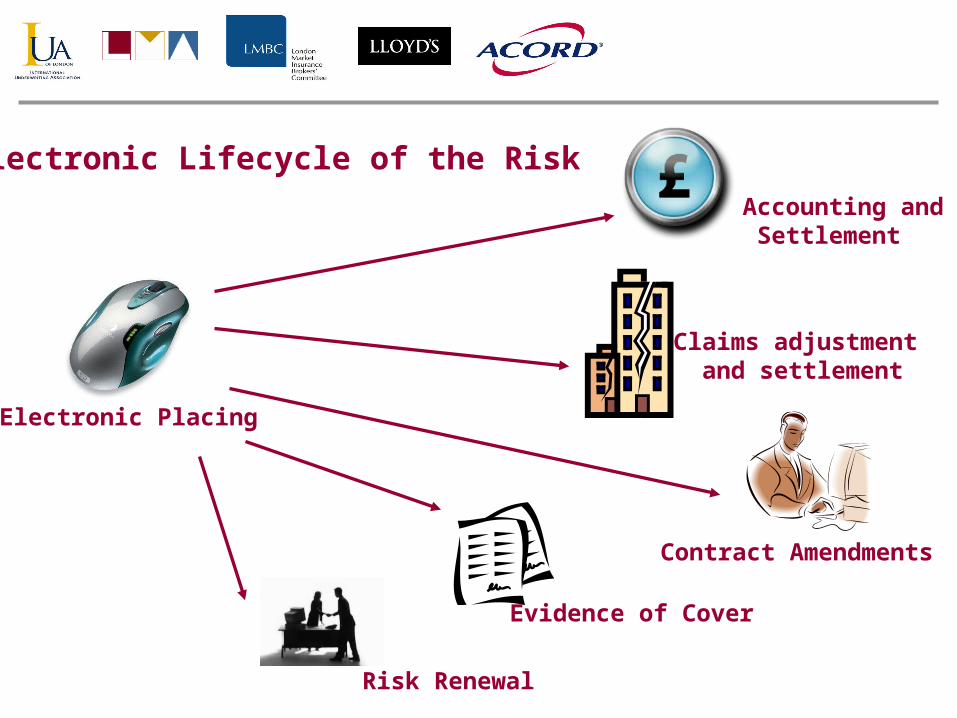

Electronic Placing

Accounting and Settlement

Electronic Lifecycle of the Risk

Claims adjustment and settlement

Evidence of Cover

Risk Renewal

Contract Amendments

Rob GilliesHead of Market ProcessesLloyd’s Market Association020 7327 [email protected]

Resources: www.lmalloyds.com