Electronic Banking 01

21

Electronic B anking Md Sajib Hossain, Lecturer , Department of Finance,DU

-

Upload

azizul-islam-rahat -

Category

Documents

-

view

223 -

download

0

Transcript of Electronic Banking 01

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 1/21

Electronic Banking

Md Sajib Hossain, Lecturer, Department of Finance,DU

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 2/21

Electronic Banking

• Electronic Banking is transforming the financial services

industry through various impossible innovations. Electronic

banking allow banks to expand their markets for traditional

deposit taking and credit extension activities, and to offer new

products and services or strengthen their competitive positionin offering existing payment services.

• It is about performing banking through electronic means.

Doing all the activities of a bank with itself and providing

banking services through electronic or digital method likeinternet, mobile phone, ATM , telecommunication network ,

SMS banking etc.

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 3/21

Basic Features of E-Banking

• All branches connected with central server for 24 hours a day and 365

days in a year.

• Customers can perform banking transactions from any branch located at

any place.

•

Customers gets banking services through electronic delivery channels onthe basis of 24 X 365 hours.

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 4/21

Scope of Existing Electronic Banking in

Bangladesh• Internet Banking

• Automated Teller Machine

• Mobile Banking

• Electronic Fund Transfer like BEFTN

• SWIFT

• Tele banking

• SMS banking

• Banking Kiosks

•

Point of Sale ( POS) Terminal• Others

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 5/21

Benefits of Electronic Banking

• 24 hours access

• Fast transactions

• Paperless transactions

• Convenience

• Worldwide access

• Allow transaction from any delivery channel

• Allow plastic money /E-cash /Digital cash

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 6/21

Infrastructure requirement for E-

banking• Computer network and data communication

• Integrated Core banking software/ solution

• Hardware platform

• Proper manpower with ICT knowledge and skills

Additional Infrastructure requirements

ACHS

National Payment Gateway

ICT act or Cyber law

E- business

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 7/21

Internet banking

• In Internet banking , a channel of e-banking, customer is given

a specific user ID and a confidential/secret or secured

password so that they can access to their own account.

• Bank offers e-banking in two main ways: First an existing bank

with physical offices can establish a Web site and offers its

customers internet banking in addition to its tradition banking

• Second bank can be established as virtual or “internet bank”

only

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 8/21

Internet banking

• Internet banking offerings provided by banks can broadly be

grouped in three groups with distinct risks profile:

Information

Communicative

Transactional

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 9/21

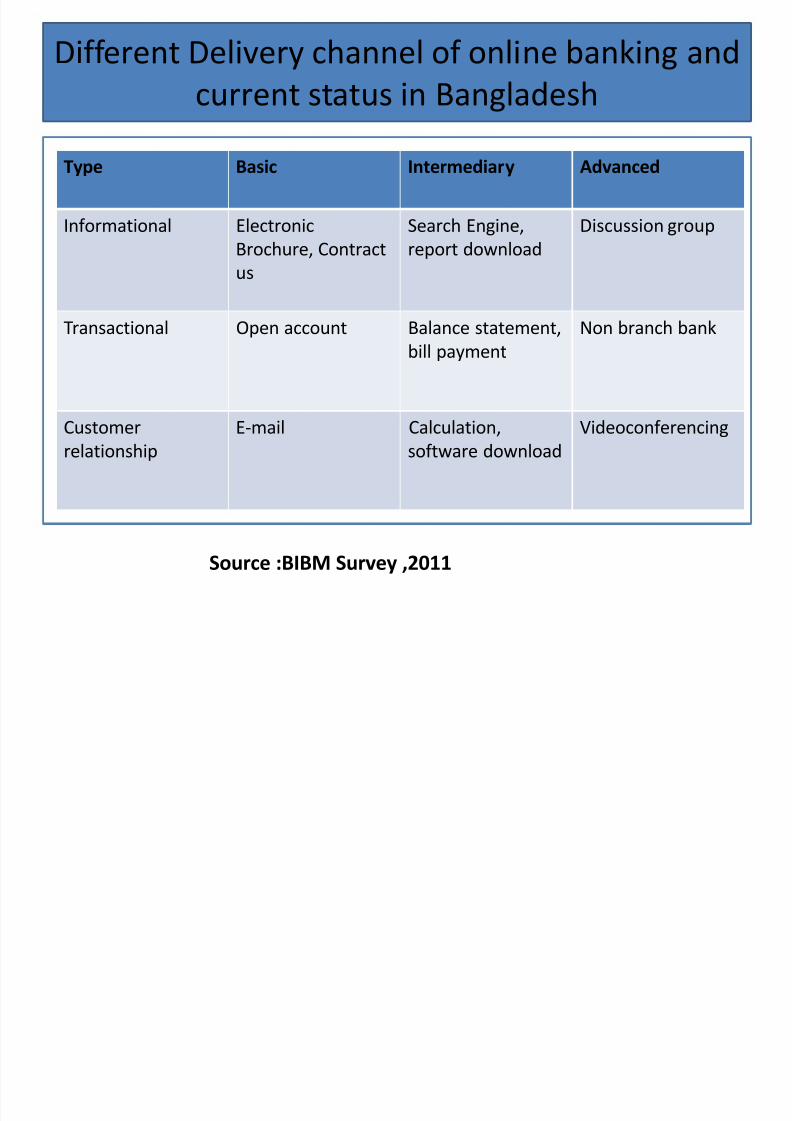

Different Delivery channel of online banking and

current status in Bangladesh

Source :BIBM Survey ,2011

Type Basic Intermediary Advanced

Informational Electronic

Brochure, Contract

us

Search Engine,

report download

Discussion group

Transactional Open account Balance statement,

bill payment

Non branch bank

Customer

relationship

E-mail Calculation,

software download

Videoconferencing

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 10/21

Security with Internet banking

• Providing internet banking requires high level of

security. For example DBBL data center is equipped

with world’s no networking equipment from CISCO

such as switch , router and PIX firewall.• Any customers requiring internet banking services

must pass throw two firewalls such as Check Point

Firewalls and CISCO firewalls.

• Log in ID is mapped with User ID along with setting

the transaction limit

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 11/21

Internet banking services in

bangladesh• Accounts summary

• Accounts Details

• Account activity

• Transfer of funds

• Third party Transfer

• Pay Bills

• Standing instructions

• Open/Modify term deposits

•

Loan repayments• Statement request

• Open FDR

• Cheque book request

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 12/21

Internet banking services in

bangladesh• Stop payment cheque

• Interest rate and Foreign exchange rate inquiry

• Re-fill prepaid card

• Change password

• L/C and BG

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 13/21

Automated Teller Machines:

An automatic teller machine or automated

teller machine (ATM) is an electronic device

which allows a bank's customers to makecash withdrawals and check their account

balances at any time without the need for a

human teller. Many ATMs also allow people to

deposit cash or cheques, transfer money

between their bank accounts or even buy

postage stamps.

ATM

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 14/21

ATM

• When an individual withdraw cash from your ATM, this information goes

to the host processor through a dedicated telephone line, which then

routes the transaction request to the cardholder's bank or the institution

that issued the card. The host processor causes an electronic funds

transfer to take place from the customer's bank account to the host

processor's account.

• Once the funds are transferred to the host processor's bank account, the

processor sends an approval code to the ATM authorizing the ATM

machine to dispense the cash requested. The processor then ACHs the

cardholder's funds into the merchant's bank account, usually within 12 to

24 hours.

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 15/21

How Do ATMs Work?

An ATM is simply a data terminal with two input and four output

devices.

the ATM has to connect to, and communicate through, a hostprocessor.

ATMs connect to the host processor through a normal phone line.

The host processor may be owned by a bank or financial institution,

or it may be owned by an independent service provider.

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 16/21

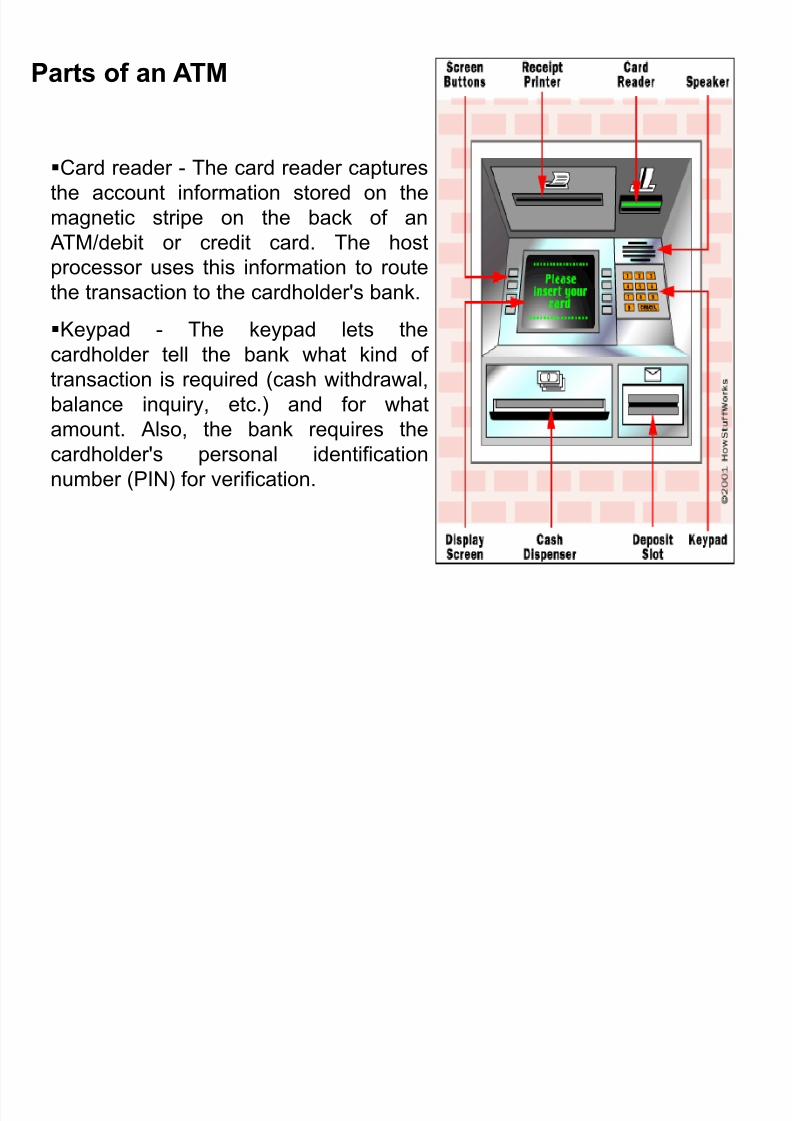

Parts of an ATM

Card reader - The card reader captures

the account information stored on the

magnetic stripe on the back of an

ATM/debit or credit card. The host

processor uses this information to routethe transaction to the cardholder's bank.

Keypad - The keypad lets the

cardholder tell the bank what kind of

transaction is required (cash withdrawal,

balance inquiry, etc.) and for what

amount. Also, the bank requires the

cardholder's personal identification

number (PIN) for verification.

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 17/21

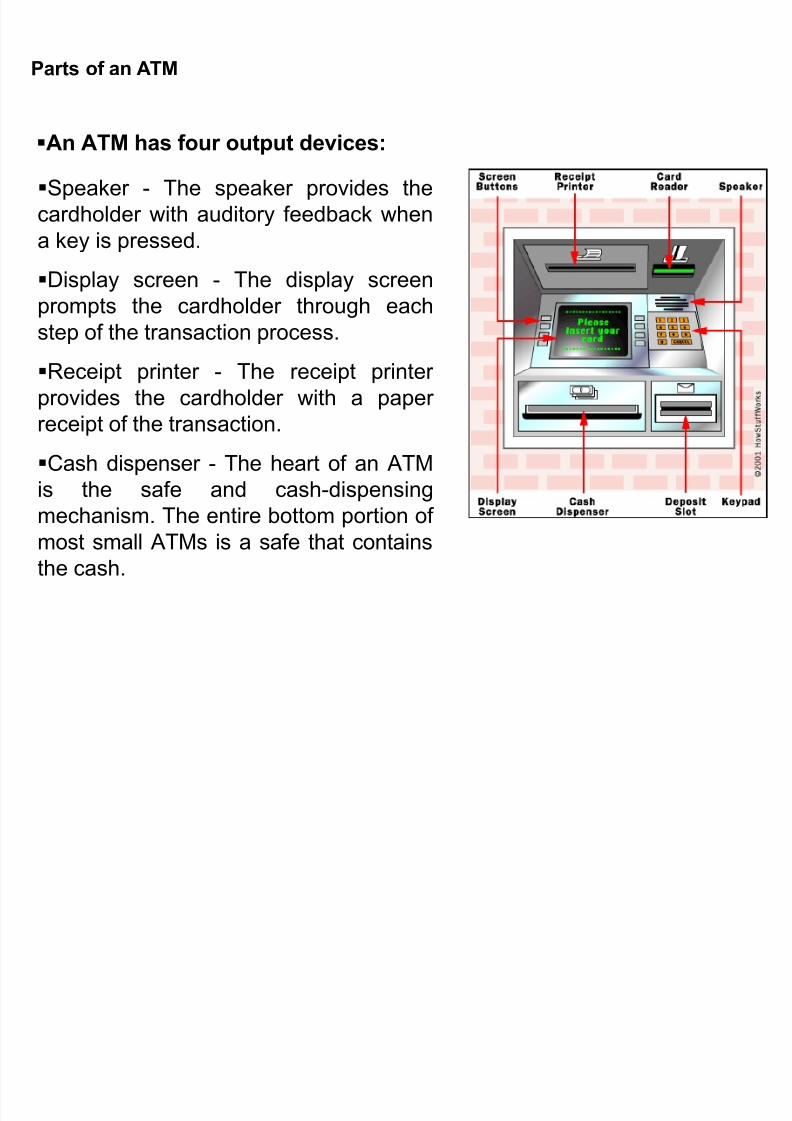

Parts of an ATM

An ATM has four output devices:

Speaker - The speaker provides the

cardholder with auditory feedback when

a key is pressed.

Display screen - The display screenprompts the cardholder through each

step of the transaction process.

Receipt printer - The receipt printer

provides the cardholder with a paper

receipt of the transaction.

Cash dispenser - The heart of an ATM

is the safe and cash-dispensing

mechanism. The entire bottom portion of

most small ATMs is a safe that contains

the cash.

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 18/21

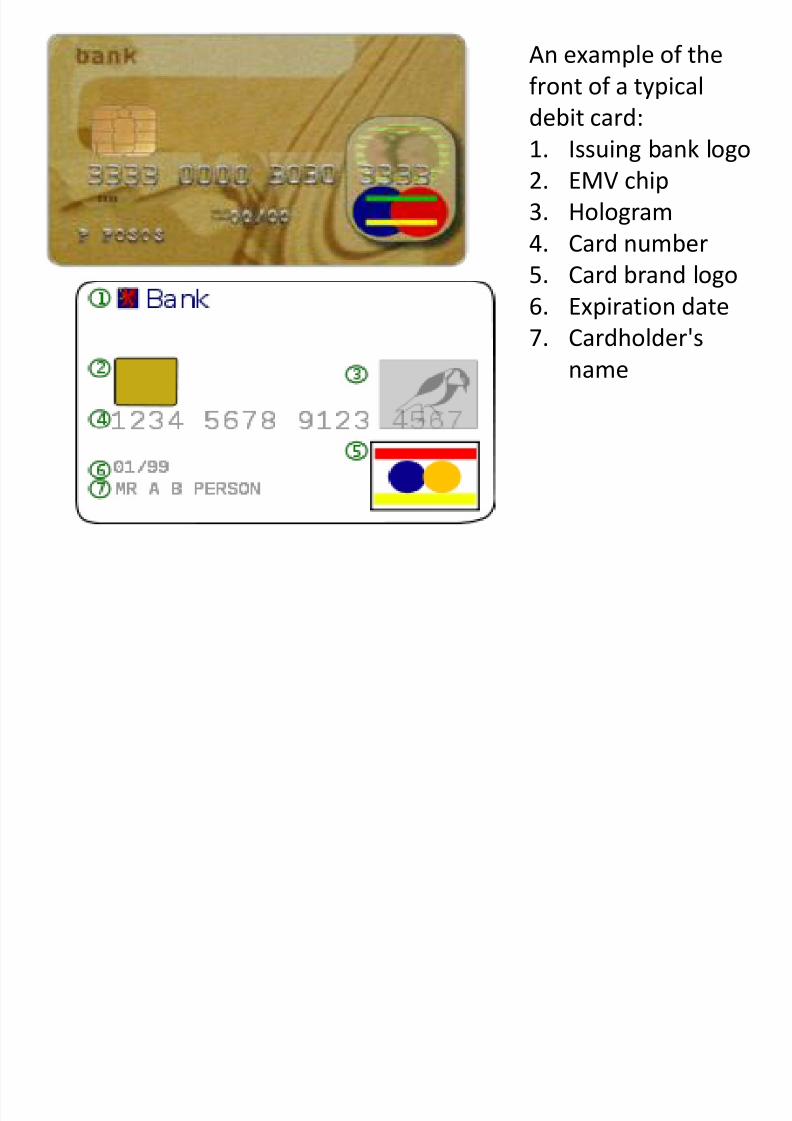

An example of the

front of a typical

debit card:

1. Issuing bank logo2. EMV chip

3. Hologram

4. Card number

5. Card brand logo6. Expiration date

7. Cardholder's

name

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 19/21

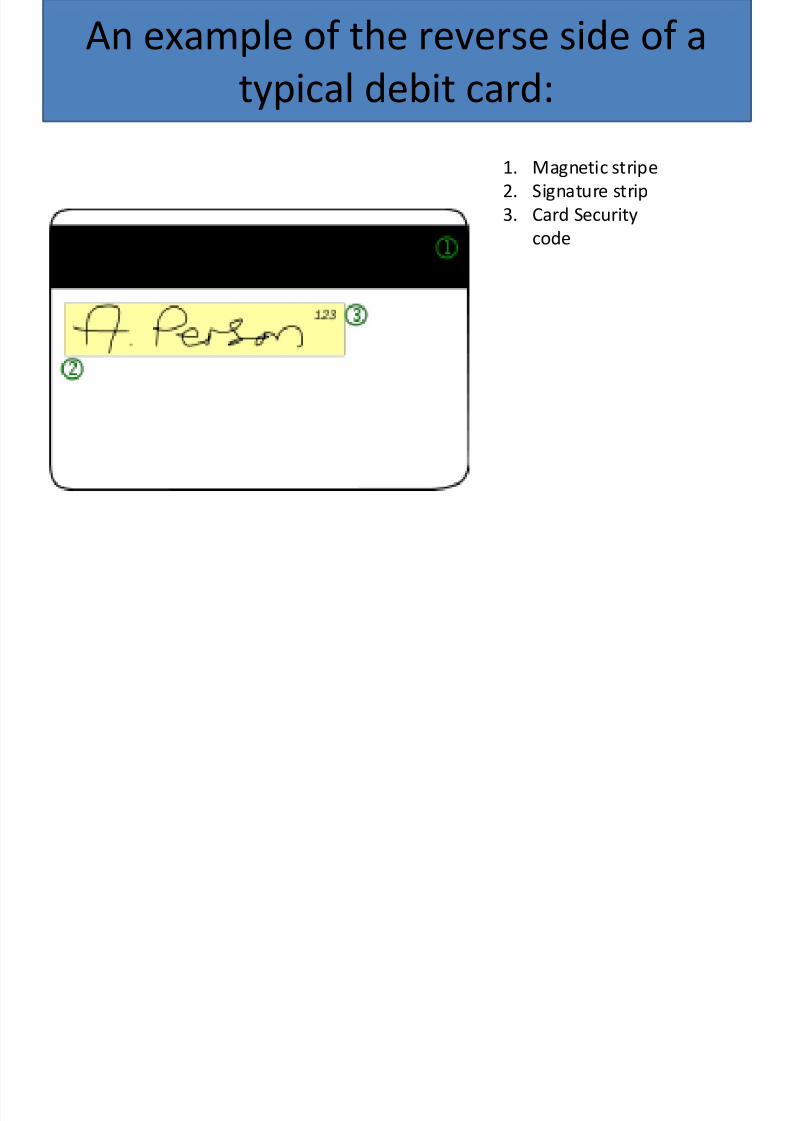

An example of the reverse side of a

typical debit card:

1. Magnetic stripe

2. Signature strip

3. Card Security

code

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 20/21

Point of Sale ( POS)

• Usually the banks distribute the POS terminals to big hotels ,

departmental shops where the customers frequently visits.

• This is small electronic device connected with

the banks' database through switching software.

• Both merchants and the customers should

have a account in the bank.

The bank may charge a fee to both customers

and the merchants forthis type of service.

7/28/2019 Electronic Banking 01

http://slidepdf.com/reader/full/electronic-banking-01 21/21

Benefits of POS• To a merchant POS can provide

1. manage inventory

2. Manage markdowns or promotions

3. Track promotions

4. Reduce paper work

5. Faster transaction6. Accuracy

7. Analysis

• Disadvantages of POS1. Connection reliability

2. Web-based POS fee

3. POS software up gradation

4. Hardware could cause problems