EIGHTH ANNUAL SOUTHERN CALIFORNIA ECONOMIC RECOVERY …economy.scag.ca.gov/Economy site document...

43

Orange County Business Council November 2017 EIGHTH ANNUAL SOUTHERN CALIFORNIA ECONOMIC RECOVERY & JOB CREATION SUMMIT 2017 ORANGE COUNTY ECONOMIC UPDATE Prepared for the Southern California Association of Governments

Transcript of EIGHTH ANNUAL SOUTHERN CALIFORNIA ECONOMIC RECOVERY …economy.scag.ca.gov/Economy site document...

Orange County Business Council November 2017

EIGHTH ANNUAL SOUTHERN CALIFORNIA ECONOMIC RECOVERY & JOB CREATION

SUMMIT

2017 ORANGE COUNTY ECONOMIC UPDATE

Prepared for the

Southern California Association of Governments

Table of Contents Page | i

Table of Contents

Section 1 ‐ Introduction .................................................................................................................. 3

Section 2 – Current Economic Conditions ...................................................................................... 5

Section 3 ‐ Key Existing and Emerging Industries ......................................................................... 12

Section 4 – Industry Innovation in Orange County ....................................................................... 17

Section 5 ‐ Occupational Employment and Salary Growth ........................................................... 23

Section 6 ‐ Income and Poverty Statistics ..................................................................................... 27

Section 7 ‐ Educational Attainment Demographics ...................................................................... 30

Section 8 ‐ Housing Market and Construction Activity ................................................................. 33

Section 9 ‐ Final Thoughts ......................................................................................................... 4039

List of Figures Page | ii

List of Figures

Exhibit 2.1 Unemployment Rates (Jan. 2008 – Aug. 2017) ................................................................................................................ 57

Exhibit 2.2 Orange County Labor Force Characteristics (2008‐2017) ................................................................................................. 68

Exhibit 2.3 Orange County Labor Force Participation Rate (2001 – 2017 YTD) ................................................................................... 68

Exhibit 2.4 SCAG Region GDP Growth (2012 ‐ 2016) ......................................................................................................................... 79

Exhibit 2.5 2016 SCAG Regional GDP ($ in Billions) ......................................................................................................................... 810

Exhibit 2.6 Orange County Projected Population Change by Age Group (2010‐2060) ...................................................................... 911

Exhibit 2.7 Orange County Projected Population Change (2010‐2060) ............................................................................................ 911

Exhibit 2.8 Orange County Population Growth (2000‐2016) ......................................................................................................... 1012

Exhibit 3.1 Orange County Industry Employment Breakdown (August 2017) ................................................................................ 1214

Exhibit 3.2 Orange County Annual Industry Trends (2010‐2017 YTD) ............................................................................................ 1315

Exhibit 3.3 Orange County Annual Industry Cluster Employment Trends (2009‐2016) .................................................................. 1416

Exhibit 3.4 Orange County Annual Industry Cluster Salary Trends (2009‐2016) ............................................................................. 1517

Exhibit 3.5 Projected Changes in Orange County Employment by Industry (2014 – 2024) ............................................................. 1618

Exhibit 4.1 Top 10 Orange County Industry Clusters by Location Quotient ................................................................................... 1820

Exhibit 4.2 Venture Capital Investments in Orange County, 2006 – Q2 2017 ................................................................................. 1921

Exhibit 4.3 Venture Capital Investments in Orange County by Sector, 2011‐2016 ......................................................................... 1921

Exhibit 4.4 Proportion of Venture Capital Investments in Orange County by Sector, 2016 ............................................................ 2022

Exhibit 4.5 Top 10 California Counties by Patent Count, 2012‐2016 ..................................................... Error! Bookmark not defined.23

Exhibit 4.6 Patent Grants Awarded per 10,000 Residents in the United States, California and Orange County, 2008‐2015 ............ 2123

Exhibit 5.1 Orange County Occupational Employment Distribution .............................................................................................. 2325

Exhibit 5.2 Orange County Occupational and Salary Year‐over‐Year Absolute Growth .................................................................. 2426

Exhibit 5.3 Projected Orange County Employment Growth by Occupational Group and Current Average Salaries (2014‐2024) ..... 2527

Exhibit 5.4 Average Salaries of Fastest‐Growing Occupations in Orange County (2014‐2024)........................................................ 2628

Exhibit 6.1 Orange County Income and Poverty Rates (2000‐2016) .............................................................................................. 2729

Exhibit 6.2 Orange County Household Income Profile .................................................................................................................. 2830

Exhibit 6.3 Percent of Orange County Households Earning Above or Below $50,000 .................................................................... 2830

Exhibit 6.4 Poverty Rates by Region (2014) .................................................................................................................................. 2931

Exhibit 7.1 Orange County Educational Attainment, Population over 25 (2016) ........................................................................... 3032

Exhibit 7.2 Orange County Tech‐Related Degrees Granted (2000 – 2016) ..................................................................................... 3033

Exhibit 7.3 Median Wages by Educational Attainment, Orange County Workers over 25 (2015) ................................................... 3234

Exhibit 7.4 Orange County Unemployment & Poverty Rates by Educational Attainment (2016) ................................................... 3234

Exhibit 8.1 Orange County Median Home Prices (2008‐2017): New vs. Existing Homes ................................................................ 3335

Exhibit 8.2 Southern California Regional Home Prices (All Structures), 2007‐YTD 2017 ................................................................. 3436

Exhibit 8.3 Orange County Home Sales, 2007‐July 2017 ............................................................................................................... 3436

Exhibit 8.4 Orange County Building Permits (2009‐2017) ............................................................................................................. 3537

Exhibit 8.5 Orange County Average Apartment Rental Rates, 2012 – 2017 YTD ............................................................................ 3738

Exhibit 8.6 California Association of Realtors Affordability Index ................................................................................................. 3738

Exhibit 8.7 Orange County Renter and Owner Housing Costs as a Percent of Income (2016) ......................................................... 3839

Exhibit 8.8 Orange County Foreclosures, 2007‐Q2 2017 ............................................................................................................... 3940

Section 1 – Introduction Page | 3

Section1‐Introduction

Commissioned by the Southern California Association of Governments (SCAG), the 2017 Orange

County Economic Update was created to provide an overview of current economic,

demographic, and housing conditions in Orange County, as well as short‐ and long‐term

projections of these conditions. This will help local elected officials, business leaders, and

policymakers better understand current and future economic trends and their potential to

enhance or disrupt local and regional economic strategies. The eighth annual Southern

California Economic Summit, the occasion of this report’s release, will be held on November 9,

2017, co‐hosted by SCAG and the Southern California Leadership Council.

Metrics highlighted in this report include measures and projections of demographics,

employment, industry clusters, educational attainment levels, income and poverty, and the

housing market, broken down into the following sections:

Current Economic Conditions

Key Existing and Emerging Industries

Innovation in Orange County

Occupational Employment and Salary Growth

Income and Poverty Statistics

Educational Attainment Demographics

Housing Market and Construction Activity

This report highlights economic trends at the local, regional, state and national level to provide

elected officials and regional stakeholders with a better understanding of the current economic

landscape, allowing them to better align current and proposed strategies and policies to

maximize their effectiveness leverage these trends while minimizing their potential negative

impacts. While Orange County’s demographics and housing industry have been undergoing

decade‐long shifts, such as an aging population and high housing prices, new trends are

beginning to emerge due to technological advancements and changing generational

preferences. These new shifts include the continued disruption to retail brought on by e‐

commerce, the growing use of artificial intelligence (AI) and computer learning, and a shifting

labor market underscored by changes for in‐demand skills.

While some degree of uncertainty will likely continue looming over parts of the regional

economy, local and regional leaders should continue to look forward and plan for the future.

Crafting strategies to capitalize, leverage, and maximize the upside of economic development

opportunities, while anticipating potential economic disruptions and minimizing the downside

of their negative impacts, will be key to responding and adapting to a changing economic

landscape. Orange County, with its diversified labor market, strong industry clusters, strong

List of Figures Page | 4

business climate, and innovative spirit must continue to act as the engine for regional economic

activity.

Section 2 – Current Economic Conditions Page | 5

Section2–CurrentEconomicConditions

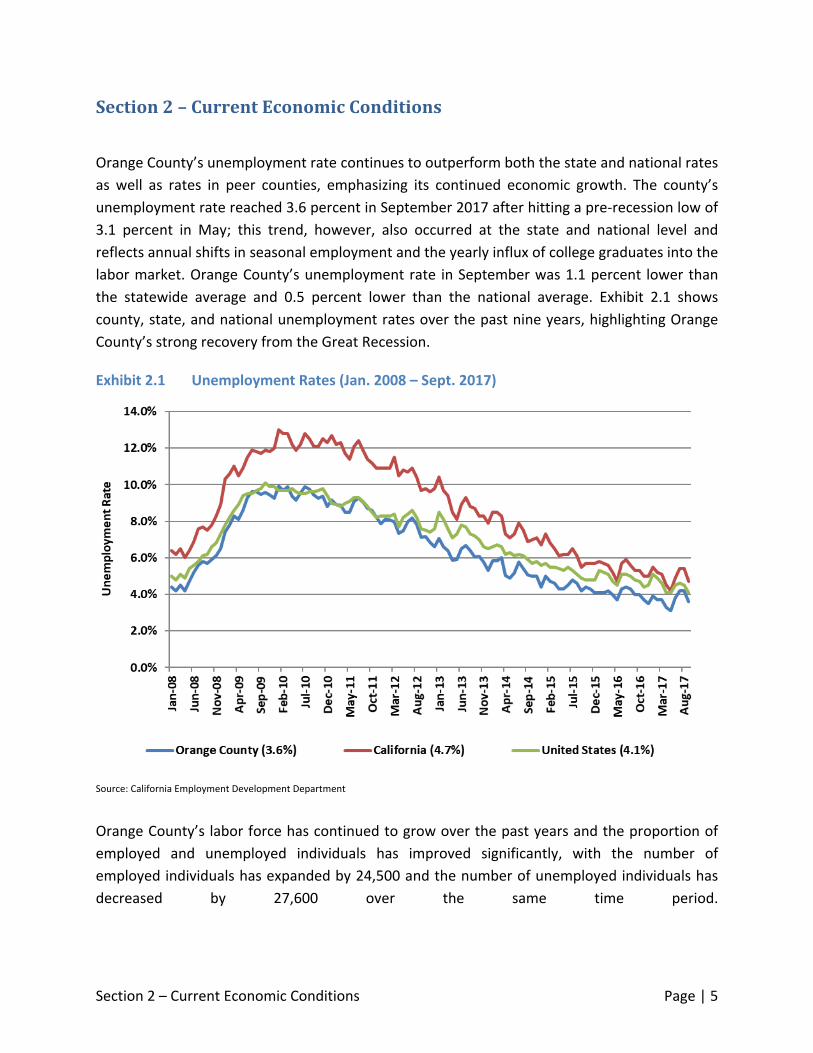

Orange County’s unemployment rate continues to outperform both the state and national rates

as well as rates in peer counties, emphasizing its continued economic growth. The county’s

unemployment rate reached 3.6 percent in September 2017 after hitting a pre‐recession low of

3.1 percent in May; this trend, however, also occurred at the state and national level and

reflects annual shifts in seasonal employment and the yearly influx of college graduates into the

labor market. Orange County’s unemployment rate in September was 1.1 percent lower than

the statewide average and 0.5 percent lower than the national average. Exhibit 2.1 shows

county, state, and national unemployment rates over the past nine years, highlighting Orange

County’s strong recovery from the Great Recession.

Exhibit 2.1 Unemployment Rates (Jan. 2008 – Sept. 2017)

Source: California Employment Development Department

Orange County’s labor force has continued to grow over the past years and the proportion of

employed and unemployed individuals has improved significantly, with the number of

employed individuals has expanded by 24,500 and the number of unemployed individuals has

decreased by 27,600 over the same time period.

Section 2 – Current Economic Conditions Page | 6

Exhibit 2.2 Orange County Labor Force Characteristics (2008‐2017)

Source: California Employment Development Department

Orange County’s labor force participation reflects overall demographic trends. As of September,

the county had a labor force participation rate of 50.5 percent, well below pre‐recession highs

and unchanged compared to last year; Orange County has a growing population of retirees and

a shrinking working‐age population driven in part by high housing costs. These trends are

expected to continue and, alongside automation, will further transform the county’s labor

market.

Exhibit 2.3 Orange County Labor Force Participation Rate (2001 – 2017 YTD)

Source: California Employment Development Department

Section 2 – Current Economic Conditions Page | 7

Exhibit 2.4 SCAG Region GDP Growth (2012 ‐ 2016)

Source: OCBC Analysis of U.S. Department of Commerce, Bureau of Economic Analysis Data

Exhibit 2.4 above shows the sustained growth of the Southern California regional economy.

Total GPD for the SCAG region (including Los Angeles, Orange, San Bernardino, Riverside,

Imperial, and Ventura counties) grew from $951.5 billion in 2012 to $1,204.9 billion in 2016; the

SCAG region’s economy is larger than those of Australia, Mexico, and Indonesia. Orange County

accounted for 23.7 percent of the region’s GDP, $286.5 billion, in 2016, trailing only Los Angeles

County. Exhibit 2.5 breaks down the SCAG GDP by county.

Section 2 – Current Economic Conditions Page | 8

Exhibit 2.5 2016 SCAG Regional GDP ($ in Billions)

Source: OCBC Analysis of U.S. Department of Commerce, Bureau of Economic Analysis Data,

Orange County, as previously mentioned, is currently undergoing several major, long‐term

demographic shifts with significant economic consequences. The California Department of

Finance predicts that the county’s School Age, College Age, and Working Age populations will

shrink by 21 percent, 16 percent, and 0.4 percent, respectively, between 2010 and 2060.

Older age groups, on the other hand, will experience dramatic growth: 103 percent for Young

Retirees, 223 percent for Mature Retirees, and 487 percent for Seniors, as shown in Exhibit. 2.6.

County stakeholders and policymakers must address the impacts of these changes, which will

affect everything from industry employment, as an older population increases demand for

healthcare services, to senior services, to the housing market, as retirees may seek to find

smaller, more affordable living accommodations.

Section 2 – Current Economic Conditions Page | 9

Exhibit 2.6 Orange County Projected Population Change by Age Group (2010‐2060)

Source: California Department of Finance, Demographic Research Unit

Orange County’s demographic makeup is also shifting, as shown in Exhibit 2.7; the California

Department of Finance estimates Orange County will continue to become more diverse over

the coming decades. The county’s diverse population has already provided major economic

benefits by attracting well‐educated and talented workers from around the world. As the

county becomes more diverse, policymakers should ensure world‐class education, training, and

economic opportunity for all ethnic groups. Improving English language programs, for example,

will help guarantee a steady supply of young workers to fill job openings created by the

retirement of older workers.

Exhibit 2.7 Orange County Projected Population Change (2010‐2060)

Section 2 – Current Economic Conditions Page | 10

Source: California Department of Finance, Demographic Research Unit

Before 2000, Orange County’s population growth came from migration into the region rather

than natural increase (births minus deaths), a trend that has since reversed. Since 2000, natural

increase has increased the county’s population by 415,721, an average 24,454 per year, while

net migration (both national and international) has reduced the population by 35,041, an

average of 2,061 per year since 2000. While international migration into Orange County

remains a steady source of population growth, negative domestic migration continues to limit

growth. The county’s net migration first turned negative in 2002 and persisted until 2010,

reflecting the effects of rising home prices and the Great Recession. As the recession took hold,

individuals and families saw their savings depleted, forcing many residents to leave Orange

County for more affordable areas. Since 2010, however, net migration has turned positive,

averaging 8,392 per year due to sustained international migration.

Exhibit 2.8 Orange County Population Growth (2000‐2016)

Section 2 – Current Economic Conditions Page | 11

Source: California Department of Finance, Demographic Research Unit

As the end of 2017 nears, Orange County continues to show economic resilience in the face of

demographic and technological disruption. Alongside demographic shifts, advancing technology

and generational preferences are transforming many of Orange County’s established industries.

In retail, for example, e‐commerce continues to take more and more market share from

traditional “brick‐and‐mortar” malls, a trend that will accelerate growth in logistics and

industrial (warehouse) retail estate. In manufacturing, the emergence of “Industry 4.0” has led

to the Digital Factory, which combines digital and physical systems through automation,

machine learning, and the Internet of Things (IoT) to significantly increase efficiency. These

emerging technologies have the potential to transform a wide variety of industries in addition

to retail and manufacturing.

Technological advances, which provide significant benefits for traditional and emerging

industry clusters, require a strong support system to flourish. Along with the looming skills gap,

they encourage the creation of new educational programs that develop the “hard” technical

skills needed for these new jobs. This focus, however, has led many programs to neglect the

“soft” skills, such as leadership and teamwork, which are equally important in the job market

and play a major role in productivity and career advancement.

Section 3 – Key Existing and Emerging Industries Page | 12

Section3‐KeyExistingandEmergingIndustries

Recent data from the California Employment Development Department (EDD) shows that

Professional & Business Services, Leisure & Hospitality, and Educational & Health Services

continue to be Orange County’s largest industries in terms of employment. Construction saw

the largest percentage growth of employment (7.9 percent) over the past year, followed by

Other Services (3.4 percent) and Leisure and Hospitality (2.1 percent).

Exhibit 3.1 Orange County Industry Employment Breakdown (September 2017)

Source: California Employment Development Department

Section 3 – Key Existing and Emerging Industries Page | 13

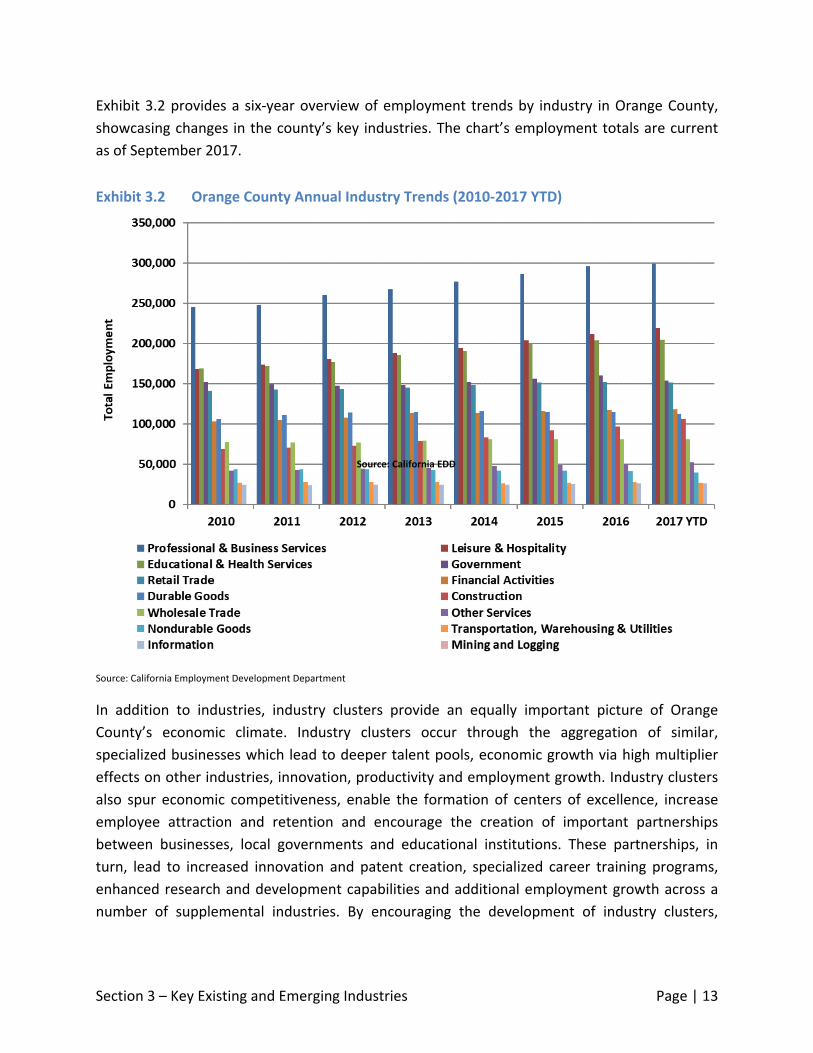

Exhibit 3.2 provides a six‐year overview of employment trends by industry in Orange County,

showcasing changes in the county’s key industries. The chart’s employment totals are current

as of September 2017.

Exhibit 3.2 Orange County Annual Industry Trends (2010‐2017 YTD)

Source: California Employment Development Department

In addition to industries, industry clusters provide an equally important picture of Orange

County’s economic climate. Industry clusters occur through the aggregation of similar,

specialized businesses which lead to deeper talent pools, economic growth via high multiplier

effects on other industries, innovation, productivity and employment growth. Industry clusters

also spur economic competitiveness, enable the formation of centers of excellence, increase

employee attraction and retention and encourage the creation of important partnerships

between businesses, local governments and educational institutions. These partnerships, in

turn, lead to increased innovation and patent creation, specialized career training programs,

enhanced research and development capabilities and additional employment growth across a

number of supplemental industries. By encouraging the development of industry clusters,

Source: California EDD

Section 3 – Key Existing and Emerging Industries Page | 14

Orange County can strengthen the regional economy and provide a variety of employment

opportunities both within the clusters themselves and across all industries in the region.

Driven by a growing economy, Orange County’s Tourism cluster added 6,788 jobs between

2015 and 2016, the most of any industry cluster. Construction, benefitting from increasing

housing demand, saw the second largest increase in jobs (5,758), followed by Hotels and

Restaurants (5,608) which also benefited from the county’s status as a world‐class tourist

destination. The Information Technology (IT) and Biotechnology clusters also saw employment

growth; this growth is especially welcome considering the innovative nature of these clusters as

well as their above average wages.

Exhibit 3.3 Orange County Annual Industry Cluster Employment Trends (2009‐2016)

Source: California Employment Development Department, Quarterly Census of Employment and Wages

Wage growth provides another reason for optimism. Orange County’s average 2016 cluster

employment salary was $68,467, a 0.5 percent increase from 2015. All of Orange County’s

major industry clusters experienced salary increases in 2016 except for Biotechnology, which

Section 3 – Key Existing and Emerging Industries Page | 15

experienced a decline due to a significant drop in one sub‐sector, Research and Development in

Physical, Engineering and Life Sciences; this sector experienced a dramatic salary increase in

2015, suggesting that this year’s decrease reflects normalization of data rather than a severe

decline. The highest increase in average percent salary over the past year occurred in Business

and Professional Services, which increased by 8.3 percent or by $7,144 since 2015. The second

highest percent increase in cluster salaries was in the Information Technology industry cluster,

which increased by 6.2 percent, followed by Construction which increased by 3.7 percent and

Tourism which saw salaries increase by 3.5 percent; this is an especially welcome increase for a

regionally important industry typically characterized by traditionally low‐skill, low‐wage

positions.

Exhibit 3.4 Orange County Annual Industry Cluster Salary Trends (2009‐2016)

Source: California Employment Development Department, Quarterly Census of Employment and Wages

Section 3 – Key Existing and Emerging Industries Page | 16

The California Employment Development Department’s (EDD) 2014‐2024 employment

projections predict that the Professional and Businesses Services sector will add almost 50,000

jobs between 2014 and 2024; Educational Services and Healthcare and Leisure and Hospitality

are expected to add 38,999 and 36,200 jobs, respectively, over the same period. The growth in

Healthcare employment reflects Orange County’s aging population, which will require more

and more health services over time.

Exhibit 3.5 Projected Changes in Orange County Employment by Industry (2014 – 2024)

Source: California Employment Development Department

Section 5 – Occupational Employment and Salary Growth Page | 17

Section4–IndustryInnovationinOrangeCounty

Technology, as mentioned before, has evolved at an incredible pace over the recent past,

disrupting industry after industry and forcing stakeholders to rethink their short‐ and long‐term

plans. Orange County, along with the rest of the United States, is the middle of a shift from a

production‐based economy to a knowledge‐based, increasingly interconnected digital economy

fueled by automation, robotics, machine learning, big data and various communication

technologies. These trends are especially apparent in Orange County, which is home to industry

clusters that continue to spur innovation. This section highlights key regional industry clusters,

their recent evolution, and their valuable contributions to the regional economy.

Industry clusters, as mentioned before, are regional concentrations of related organizations

which supplement and complement one another’s operations allowing for increased levels of

innovation, competitiveness, economic growth and job creation. Detroit’s automotive industry,

Hollywood’s film industry and the Napa and Sonoma Valley wine industry are examples of

world‐class industry clusters. These clusters typically provide increased level of economic

activity through high multiplier effects and above‐average wages paid to workers, while their

proximity to customers and complimentary industries leads to collaboration and innovation as a

well as economic growth.

Industry clusters rely on support from suppliers, administrative service providers, venture

capital sources, research organizations, and educational institutions. Together these services

create an innovative ecosystem which drives innovation, provides high‐wage occupations and

greatly enhances regional productivity.

The U.S. Cluster Mapping Project, an interactive website created by Harvard Business School

and the U.S. Economic Development Administration, provides a detailed view of Orange

County’s strongest industries. The concentration of these industries is measured by the

“location quotient:” the ratio of an industry’s share of total state employment in a location

relative to its share of total national employment. The location quotient, in other words,

measures the specialization or concentration of a cluster in a particular location relative to the

national average.

Medical Devices, the most concentrated industry in the county, boasts a location quotient of

5.83, indicating industry employment in Orange County is almost 6 times more concentrated

than at the national level. Orange County’s Medical Devices industry employed 18,625 workers

as of 2015, the highest in the nation and 7.41 percent of national Medical Device employment.

Apparel, the second most concentrated industry in Orange County, employed 3,745 workers, or

2.9 percent of the national share, with an LQ of 2.35. Biopharmaceuticals, IT & Analytical

Instruments, and Hospitality and Tourism also have significant concentrations in Orange

Section 5 – Occupational Employment and Salary Growth Page | 18

County. Exhibit 4.1 shows the industry clusters with the highest Location Quotients in Orange

County, illustrating their local and national importance.

Exhibit 4.1 Top 10 Orange County Industry Clusters by Location Quotient

O.C. Industry Clusters by Location Quotient

Industry Cluster Location Quotient

Employment (2015)

Share of National Employment

National Ranking

Medical Devices 5.83 18,625 7.41% 1 Apparel 2.35 3,745 2.99% 3 Biopharmaceuticals 2.15 6,623 2.73% 6 IT & Analytical Instruments 1.92 26,041 2.44% 5 Hospitality and Tourism 1.89 76,013 2.40% 5 Aerospace Vehicles and Defense 1.88 12,610 2.39% 11 Lighting and Electrical Equipment 1.72 6,377 2.19% 4 Metalworking Technology 1.72 10,737 2.19% 6 Recreational and Electric Goods 1.63 3,159 2.08% 3 Financial Services 1.56 38,169 1.99% 7 Source: U.S. Cluster Mapping, Harvard Business School, U.S. Economic Development Administration

Orange County’s highly concentrated industry clusters drive overall economic activity and

increase the area’s specialization and ability to innovate, as illustrated by the startups that the

county draws like a magnet. Exhibit 4.2 shows annual venture capital investments in Orange

County from 2006 to year‐to‐date 2017. After more than $900 million in venture capital funding

in 2011, investments in Orange County continually decreased, eventually hitting approximately

$500 million in 2014 before jumping back up to $1,151 million in 2015 and $1,140 million in

2016. Orange County venture capital investments in have been focused on high‐tech start‐ups

largely located in the Irvine area, which benefits from a number of incubators and other

business support organizations such as UCI Applied Innovation at the Cove.

Section 5 – Occupational Employment and Salary Growth Page | 19

Exhibit 4.2 Venture Capital Investments in Orange County, 2006 – Q2 2017

Source: National Venture Capital Association, Orange County Register

Taking a closer look at where venture capital investments have been concentrated, Exhibit 4.3

below highlights the total investments by sector in Orange County between 2011 and 2016. The

top three sectors included Software with $1.18 billion, Medical Devices and Equipment with

$1.03 billion and Industrial/Energy with $723 million.

Exhibit 4.3 Venture Capital Investments in Orange County by Sector, 2011‐2016

Source: National Venture Capital Association, Orange County Register

Section 5 – Occupational Employment and Salary Growth Page | 20

In 2016, venture capital investments in Orange County were primarily focused in Software (36

percent), Media and Entertainment (13 percent) and Mobile and Telecommunications (13

percent). Sizeable investments were also seen in Healthcare and Medical Devices and

Equipment which combined represented 19 percent of total investments for the year. These

investments help to highlight the innovation and emerging sectors which are driving economic

activity in the region.

Exhibit 4.4 Proportion of Venture Capital Investments in Orange County by Sector, 2016

Source: National Venture Capital Association, Orange County Register

Exhibit 4.5 shows the number of patents awarded per 10,000 residents in the United States,

California and Orange County, highlighting the state and county’s concentration of innovation.

While Orange County and California rates tracked each other fairly well from 2008 to 2011 and

were consistently more than double that of the nation, in 2012, a small divergence between the

county and state started in 2012 and continually grew, with the most recent reading in 2015

registering 10.3 patents per 10,000 residents at the state level and 9.0 per 10,000 residents in

Section 5 – Occupational Employment and Salary Growth Page | 21

Orange County. This divergence is likely explained by the high level of patent growth in less‐

populated counties such as Santa Clara County and San Mateo County.

Exhibit 4.5 Patent Grants Awarded per 10,000 Residents in the United States, California

and Orange County, 2008‐2015

Source: United States Patent and Trademark Office, U.S. Census Bureau – American Community Survey

As mentioned in the industry clusters section, innovation – as measured by patents and venture

capital investment – is primarily driven by collaboration among stakeholders. Regional

partnerships between economic and workforce development organizations, educational

institutions and businesses create the necessary environment for innovative startups. The

Applied Innovation Program at the University of California, Irvine recently launched “The Cove,”

a 46,000 square foot office space and technological facility. The Cove provides a collaborative

space which leverages the strengths of a world‐class educational institution, resources of

seasoned business leaders and the entrepreneurial spirit of Orange County residents to create

an environment which continually pushes innovation in the region.

UCI’s Applied Innovation Program also provides several other services for entrepreneurs,

including the Wayfinder Incubator, a highly selective support program that provides access to

strategic resources and networks, the Experts‐in‐Residence network, a group of local business

leaders volunteering their time to support entrepreneurship at UCI, and the BioENGINE

program, which fosters collaborative development of digital health solutions. The I‐Corps,

funded by the National Science Foundation (NSF), helps broaden the impact of research

projects, while Tech Surge – a special track of the New Venture Competition – helps UCI

innovators succeed in the commercial market. Finally, the ANTrepereneur Center was founded

in 2014 with the mission of bringing innovative, entrepreneurial thinking to the UCI campus.

Section 5 – Occupational Employment and Salary Growth Page | 22

Together, these institutions and programs are building a strong foundation for Orange County’s

next generation of entrepreneurs.

Section 5 – Occupational Employment and Salary Growth Page | 23

Section5‐OccupationalEmploymentandSalaryGrowth

As seen in Exhibit 5.1, Office & Administrative Support is the largest single occupational

category in Orange County, accounting for 16.8 percent of employment; Sales & Related

occupations at 10.7 percent and Food Preparation & Service‐Related occupations at 9.6 percent

also make up a large proportion of country employment.

Exhibit 5.1 Orange County Occupational Employment Distribution

Source: California Employment Development Department, Occupational Employment Survey

According to the California Employment Development Department’s Occupational Employment

Survey, Orange County has added 39,350 new jobs over the past year, an increase of 2.6

percent over the previous year; average salaries have increased by $1,522 or 2.8 percent. In

Section 5 – Occupational Employment and Salary Growth Page | 24

terms of absolute growth, Business and Financial Operations occupations added 6,6306 jobs, an

increase of 6.5 percent, followed by Construction and Extraction occupations with 6,350, an

increase of 9.7 percent and Food Preparation and Serving‐Related occupations with 5,090 jobs,

a 3.5 percent increase. Only five occupational groups saw decreases in overall employment

with the largest losses in Production occupations (3,890 jobs), Life, Physical and Social Science

occupations (1,050 jobs), and Protective Service occupations (860 jobs).

Most Orange County occupational groups saw salary increases over the past year, a welcome

development considering the county’s high cost of living. The average wage for all county

occupations increased by 2.7 percent, with the largest increases occurring in Management

($3,321), Farming, Fishing and Forestry ($3,266) and Construction and Extraction ($3,045). A

few occupational groups, however, lost salary: Healthcare Practitioners and Technical ($4,840),

Life, Physical and Social Science ($3,790), and Business and Financial Operations ($297).

Exhibit 5.2 Orange County Occupational and Salary Year‐over‐Year Absolute Growth

Source: California Employment Development Department, Occupational Employment Survey

Section 5 – Occupational Employment and Salary Growth Page | 25

Looking forward, to the EDD2014 ‐ 2024 occupational projects predict that overall occupational

employment will grow by 227,900 jobs in Orange County, reaching total employment of

1,829,000 by 2024. The Food Preparation and Serving Related occupational group is expected

to add 27,450 jobs over this period, followed by Construction and Extraction (expected to add

22,160 jobs) and Office and Administrative support (21,840 jobs). These occupational groups,

however, provide relatively low wages. The fastest growing occupational groups which pay

above average wages include Business and Financial Operations (18,430 jobs at an average

annual salary of $82,513), Management (16,000 at $130,559) and Healthcare Practitioners and

Technical (12,910 at $93,972).

Exhibit 5.3 Projected Orange County Employment Growth by Occupational Group and

Current Average Salaries (2014‐2024)

Source: California Employment Development Department, Employment Projections

Section 5 – Occupational Employment and Salary Growth Page | 26

EDD estimates that Web Developers (+48.9%), Floor Layers, Except Carpet, Wood and Hard

Tiles (+45.2%), and Operations Research Analysts (+42.2%) will be the fastest growing

occupations on a percentage basis between 2014 and 2024. The first two occupations are part

of Orange County’s most rapidly expanding industries, Information Technology and

Construction.

Exhibit 5.4 Average Salaries of Fastest‐Growing Occupations in Orange County (2014‐2024)

Source: California Employment Development Department

Section 6 – Income and Poverty Statistics Page | 27

Section6‐IncomeandPovertyStatistics

According to the most recent measures from the U.S. Census Bureau’s American Community

Survey, Orange County’s median household income reached $81,837 in 2016, an increase of

$3,409 or 4.3 percent over the past year. Orange County’s median income was 20.8 percent

higher than the state average of $67,739 and 42 percent higher than the national average of

$57,617. Per capita incomes in Orange County increased by 7.3 percent, more than $2,500,

between 2015 and 2016.

The county poverty rate decreased from 12.7 percent in 2015 to 11 percent in 2016, another

sign of economic growth. This growth is especially important because of Orange County’s rising

cost of living, which has priced many residents – especially young workers and families – out of

the area.

While definitions of poverty differ, the 2017 Orange County Comprehensive Economic

Development Strategy (CEDS) defines struggling or “red‐zone” census tracts as those with a

combination of below‐average income and above‐average unemployment when compared to

national rates. The number of Orange County “red‐zones” fell from 71 in 2016 to 52 in 2017, a

dramatic improvement.

Exhibit 6.1 Orange County Income and Poverty Rates (2000‐2016)

Source: U.S. Census Bureau, 2016 American Community Survey, 1‐Year Estimates

Exhibit 6.2 shows household income distribution across various income groups in 2000, 2015,

and 2016. According to the U.S. Census Bureau, households making between $50,000 and

$74,999 were the largest income group in 2000, accounting for 20.7 percent of the county. This

income group has since declined and now represents only 16.3 percent of Orange County

households; the $100,000 to $149,999 income group now represents the largest portion (18.3

Section 6 – Income and Poverty Statistics Page | 28

percent) of county households. Overall, lower income groups have shrunk since 2000 while

higher income groups have steadily increased. This illustrates the region’s economic growth and

is especially important when Orange County’s high (and rising) cost of living is taken into

account.

Exhibit 6.2 Orange County Household Income Profile

Source: U.S. Census Bureau, 2016 American Community Survey, 1‐Year Estimates

Exhibit 6.3 Percent of Orange County Households Earning Above or Below $50,000

Source: U.S. Census Bureau, 2016 American Community Survey, 1‐Year Estimates

Section 6 – Income and Poverty Statistics Page | 29

Poverty rates also vary depending on the source’s methodology. The two primary Orange

County poverty measures are the U.S. Census Bureau rate using federal‐level standards and the

California Poverty Measure (CPM) developed by the Public Policy Institute of California and

Stanford University. The CPM takes California‐specific economic and demographic trends into

account, providing a potentially more accurate poverty measurement. While Orange County, as

shown in Exhibit 6.4, has the region’s lowest poverty rate according to the U.S. Census, its CPM

was the second highest in Southern California.

Exhibit 6.4 Poverty Rates by Region (2014)

Poverty Rates by Region, 2014

County

Percentage in Poverty, Official Poverty Rate

Measure

Percentage in Poverty, CPM

Measure Differential

Percentage of Children Ages 17 and Below in Poverty, Official Rate

Orange 12.3% 21.5% 9.2% 18.2%

Los Angeles 18.3% 25.6% 7.3% 27.5%

Riverside 16.8% 19.7% 2.9% 24.6%

San Bernardino 19.9% 19.4% 0.5% 28.9%

California 16.1% 21.0% 4.9% 23.7%

United States 14.0% 19.5% Source: U.S Census Bureau, Public Policy Institute of California, Stanford University,

Section 7 – Educational Attainment Demographics Page | 30

Section7‐EducationalAttainmentDemographics

Orange County’s highly educated population is one of its primary competitive advantages; this

deep talent pool supports innovation, industry cluster formation and expansion, and overall

economic growth. Exhibit 7.1 shows the educational attainment of the county’s population over

age 25. In 2016, 47.7 percent of this group had an associate’s degree or higher, an increase of

1.3 percent from 2015. This provides one indicator of county residents’ increasing educational

attainment.

Exhibit 7.1 Orange County Educational Attainment, Population over 25 (2016)

Source: U.S. Census Bureau, 2016 American Community Survey, 1‐Year Estimates

Exhibit 7.2 offers another indicator of this positive trend, the increasing number of tech‐related

degrees awarded at local universities and colleges, such as the University of California, Irvine,

California State University, Fullerton, and Chapman University. The number of undergraduate

tech‐related degrees continues to grow substantially, more than doubling from 2000 to 2015

and increasing further to 3,202 in 2016. Tech‐related graduate degrees have seen even more

dramatic growth over the same time period, increasing from 434 in 2000 to 1,220 in 2015 and

further to 1,564 in 2016. UC Irvine and California State University, Fullerton were major

contributors to this recent, dramatic growth in undergraduate and graduate tech‐related

degrees.

Exhibit 7.2 Orange County Tech‐Related Degrees Granted (2000 – 2016)

Section 7 – Educational Attainment Demographics Page | 31

Source: OCBC Analysis of University of California, Irvine; Chapman University; California State University, Fullerton Data

While Orange County educational attainment has consistently increased over the past decade,

occupational and industry trends are changing the labor market value of these degrees.

Constantly evolving technology, for example, increases demand for specialized education and

training programs focused on “hard” skills. This trend, combined with rising college tuition

costs, has created a demand for certifications or other specialized training programs that

develop the skills necessary for high‐wage technical occupations.

These programs provide access to important employment opportunities at a lower cost than

traditional education, thus expanding access to these lucrative jobs for lower‐income residents.

Specialized “hard” skills programs, however, may neglect the equally important “soft” or

interpersonal skills that are also essential for career advancement. The rapidly evolving 21st

century labor market will require a mix of both “hard” and “soft” skills, making it imperative

that local educators, policymakers, and stakeholders create or improve programs that provide a

well‐rounded education. These improvements would also help close the persistent skills gap

that threatens to limit future economic growth.

Section 7 – Educational Attainment Demographics Page | 32

Exhibit 7.3 Median Wages by Educational Attainment, Orange County Workers over 25

(2015)

Source: U.S. Census Bureau, 2016 American Community Survey, 1‐Year Estimates

Despite labor market changes and the rising cost of education, academic degrees continue to

provide significant economic benefits, as seen in Exhibits 7.3 and 7.4; higher educational

attainment clearly correlates with both higher median wages and lower rates of poverty and

unemployment.

Exhibit 7.4 Orange County Unemployment & Poverty Rates by Educational Attainment (2016)

Source: U.S. Census Bureau, 2016 American Community Survey, 1‐Year Estimates

Section 8 – Housing Market and Construction Activity Page | 33

Section8‐HousingMarketandConstructionActivity

Orange County’s housing market – driven by job creation, rising incomes, and a low interest

rate environment – continues to outperform peer regions and state and national averages. This

trend, which reflects a growing economy, may also have significant negative consequences as

the county’s expensive housing market also continues to price many residents out of the area.

Exhibit 8.1 shows Orange County home prices from January 2008 to August 2017, broken down

into prices paid for new and existing single‐family housing units. The price of new homes sales

have risen to an average price of $789,000 as of August 2017, while existing home prices have

increased by 5.5 percent year over year, reaching a new high of $685,000.

Exhibit 8.1 Orange County Median Home Prices (2008‐2017): New vs. Existing Homes

Source: California Association of Realtors, CoreLogic/DataQuick

Chapman University predicts that a combination of factors – population growth, wage growth,

a limited housing supply and low interest rates – will increase county home prices by 6.2

percent in 2017, significantly more than the 4.3 percent increase in 2016.

The substantial price increases in Orange County, as well as other peer counties, can be seen in

Exhibit 8.2 below. According to CoreLogic and DQNews, Orange County structures sold for a

median price of $675,000 in July 2017, much higher than the average of $550,000 paid for

structures in Los Angeles and Ventura counties. Home prices in coastal counties, as seen in the

graph, have rapidly increased and surpassed pre‐recession highs while prices in inland counties

have seen more moderate growth and have yet to surpass pre‐recession highs.

Section 8 – Housing Market and Construction Activity Page | 34

Exhibit 8.2 Southern California Regional Home Prices (All Structures), 2007‐YTD 2017

Source: CoreLogic, DQNews, September 2017

Exhibit 8.3 shows Orange County home sales between 2007 and July 2017. According to

CoreLogic, county home sales totaled 37,848 in 2016, 34.5 percent more than in 2007.

CoreLogic estimates that Orange County is on track to reach new highs with 22,112 homes sold

thus far in 2017. However, several factors, including high home prices, a lack of supply, and

seasonal trends in home buying may limit sales for the rest of this year.

Exhibit 8.3 Orange County Home Sales, 2007‐July 2017

Section 8 – Housing Market and Construction Activity Page | 35

Source: CoreLogic, DQNews

According to the U.S. Census Bureau’s Building Permit Survey, Orange County building permits

have increased from an average of 182 per month in 2009 to 487 per month in 2012 and

further to almost 1,000 per month in 2016. August 2017 had a total of 599 building permits

with a year‐to‐date total of 6,165, which suggests that the lower monthly total does not reflect

the beginning of a decline. Irvine had 150 building permits in August, the most of any city, with

major levels of construction also occurring in Costa Mesa (70 permits), Anaheim (61), and Lake

Forest (53).

Exhibit 8.4 Orange County Building Permits (2009‐2017)

Section 8 – Housing Market and Construction Activity Page | 36

Source: U.S. Census Bureau, Building Permit Survey

Orange County apartment rental rates have mirrored the rise in home prices, increasing from

$1,967 in 2016 to $2,114 in August 2017, a 7.5 percent increase.

Section 8 – Housing Market and Construction Activity Page | 37

Exhibit 8.5 Orange County Average Apartment Rental Rates, 2012 – 2017 YTD

Source: Apartmentlist.com; Rentbits.com

Affordability, as mentioned before, remains a serious concern for Orange County. The rapid

increases in home prices and lack of available supply have driven apartment rental rates in the

region, further exacerbating this problem. According to the California Association of Realtor’s

Traditional Housing Index and First‐Time Buyer Affordability Index, which measure the

percentage of households which can afford to purchase a median price home in a specific

region, Orange County is the least affordable county in Southern California. Only 21 percent of

Orange County households could afford to purchase a median‐priced home as of Q2 2017, a

slight year‐over‐year decrease. Orange County also ranks well below its neighbors on the First‐

Time Home Buyer Affordability Index, with only 40 percent of households able to afford lower‐

price starter homes.

Exhibit 8.6 California Association of Realtors Affordability Index

California Association of Realtors Affordability Index

Traditional Affordability Index First‐Time Home Buyer Affordability Index

County Q2 2017 Q1 2017 Q2 2016 Q2 2017 Q1 2017 Q2 2016

Orange County 21 21 22 40 42 43

Los Angeles 28 29 30 46 48 49

Riverside County 39 39 41 58 60 61

San Bernardino 51 52 56 68 70 73

San Diego 26 28 28 45 48 48

Ventura 27 28 33 49 51 54

Section 8 – Housing Market and Construction Activity Page | 38

Source: California Association of Realtors

Exhibit 8.7 shows the percentage of income spent by Orange County residents on housing,

illustrating the heavy burden faced by many county renters and homeowners. The primary rule

of thumb when measuring affordability is the 30 percent rule – a person or household should

spend 30 percent of their income or less on housing; currently, according to the U.S. Census’s

2016 American Community Survey, 33 percent of homeowners and 54.1 percent of renters

spend more than 30 percent of their income on housing costs. This, in turn, leads to a

corresponding decrease in discretionary spending ‐‐ and the ability to save for the future ‐‐ and

thus serves to inhibit widespread future economic prosperity in Orange County over time.

Exhibit 8.7 Orange County Renter and Owner Housing Costs as a Percent of Income (2016)

Source: U.S. Census Bureau, 2016 American Community Survey, 1‐Year Estimates

While affordability rates are concerning, county foreclosures have steadily decreased since

peaking at 11,615 in 2008. Only 408 foreclosures took place in Q2 2017, illustrating that,

despite affordability concerns, county homeowners are not facing increased closures.

Section 8 – Housing Market and Construction Activity Page | 39

Exhibit 8.8 Orange County Foreclosures, 2007‐Q2 2017

Source: CoreLogic, DQNews

Section 9 – Final Thoughts Page | 40

Section9‐FinalThoughts

As local, regional and national demographics and industry sectors continue to evolve, Orange

County remains a standout performer in both Southern California and the nation as a whole.

Looking forward, local stakeholders and policymakers must identify opportunities and build on

positive developments of demographic, economic and technological change while mitigating

the potential negative or disruptive effects of these trends. A continually aging population, for

example, will put pressure on the labor market by increasing the ratio of dependents to

providers and driving demand for Healthcare jobs. Technological improvements will continue to

disrupt seemingly resilient industries, such as the Transportation sector with self‐driving

vehicles, the Retail sector with e‐commerce, and restaurants with computerized ordering

kiosks. These changes, while providing higher levels of productivity and efficiency for

organizations, may limit new job growth, especially for low‐skill, entry‐level positions.

Educational attainment – especially the development of both “hard” and “soft” skills – remains

the best defense against automation in the new digital economy.

Orange County’s elected officials, policymakers, and stakeholders will need to act quickly to

ensure future prosperity and further economy growth. Once again, Orange County’s primary

competitive advantage – its well‐educated, talent pool – will pay significant dividends because

these individuals will have a higher level of resilience to automation. While Orange County’s

educational system is already one of the best in the state, local leaders will need to continually

update it in order to prepare students for a rapidly evolving workplace.

Alongside this report, Orange County Business Council and other community and regional

partners also provide a variety of other economic and demographic reports including:

Orange County Workforce Indicators Report: A product of the research partnership

between the Orange County Business Council, County of Orange, and Orange County

Development Board, the Workforce Indicators Report examines the growth of industry

and employment, salary and wage trends, demographic changes and the educational

attainment of Orange County students. Click here for a link to the report.

Orange County Community Indicators Report: The product of a partnership between

Children & Families Commission of OC, Orange County United Way, CalOptima, the

Orange County Community Foundation, PIMCO Foundation, Orange County Department

of Education, Hope through Housing Foundation, Orange County Funders Roundtable,

JPMorgan Chase, the County of Orange, Orange County Business Council, La Jolla

Institutethe 2017 Orange County Community Indicators Report focuses on three pivotal

issues currently facing Orange County: housing, children’s health and wellbeing, and the

opportunity gap between high‐ and low‐income families and their children. The report

Section 9 – Final Thoughts Page | 41

also updates previous reports’ information about population, demographic, and

workforce trends. Click here for a link to the report.

Orange County Workforce Housing Scorecard: The 2015 Workforce Housing Scorecard

analyzes current and projected housing trends and their impacts on the county’s

economy, demographics, and business competitiveness. The OC Workforce Housing

Scorecard report will be updated in 2018. Click here for a link to the report.

Orange County 2013‐2018 Comprehensive Economic Development Strategy (CEDS):

Created through a partnership between the Orange County Development Board and

Orange County Business Council, this report represents an annually updated five‐year

plan for preserving Orange County’s competitive advantages, addressing the county’s

weaknesses, and making the most of future opportunities. As part of the five‐year plan,

this reports identifies census tracts and cities in the region currently underperforming

economically in comparison to national averages allowing policymakers and

stakeholders to create better, more effective strategies and programs aimed at

improving these economically disadvantaged regions. Click here for a link to the report.