Eight steps in the accounting cycle

9

EIGHT STEPS IN THE ACCOUNTING CYCLE. hor Unkn, (2015) For Dummies, Website resource p://www.dummies.com/how-to/content/the-eight-steps-of-the-accounting-cycle.html a business accountant or owner you will want to know your profits, assets and debts in quarterly or yearly accounting format, whether it be in a manual or computerize account Remember to have proper accounting system to follow the basic account principles. beginning of the accounting periods, no mater where to end or start, balanced should b Or carry over to the following month. Walther, L Ph.D. (2013) Principles of Accounting www.principlesofaccounting.com

-

Upload

lacey-frantz -

Category

Documents

-

view

30 -

download

1

Transcript of Eight steps in the accounting cycle

EIGHT STEPS IN THE ACCOUNTING CYCLE.

Author Unkn, (2015) For Dummies, Website resourcehttp://www.dummies.com/how-to/content/the-eight-steps-of-the-accounting-cycle.html

As a business accountant or owner you will want to know your profits, assets and debts in amonthly, quarterly or yearly accounting format, whether it be in a manual or computerize account system.

Remember to have proper accounting system to follow the basic account principles. Also, the beginning of the accounting periods, no mater where to end or start, balanced should be at zero

Or carry over to the following month.

Walther, L Ph.D. (2013) Principles of Accountingwww.principlesofaccounting.com

1.) TRANSACTIONSTransaction begin the entire process of accounting. They can include the sales or returning of a sold product, the purchase of supplies

used by the business or the asset exchange. Many transaction can affect transactions, including payroll and deposits of money.

Photo reference from: Business Transactions - Wiggmax.com

Each given transaction is listed in the appropriate accounting journal in chronological order of each transactions. For example, payment for a transaction on credit would be listed under the Accounts Payable Account.

2.) JOURNAL ENTRIES

The General Ledger - Account Posting and Journal Entry Exampleswww.loscostos.info

3.) TRIAL BALANCE

At the end of each monthly, quarterly of yearly accounting you will calculate a trial balance. Trail balances are useful in many ways,

but mostly to find errors in the accounting process. They also prepare you for the next In the accounting process.

www.msofficeguru.org

Samples of Trial Balances For a company Called England tour company as illustrate by author Walther, L Ph.D. (2013)

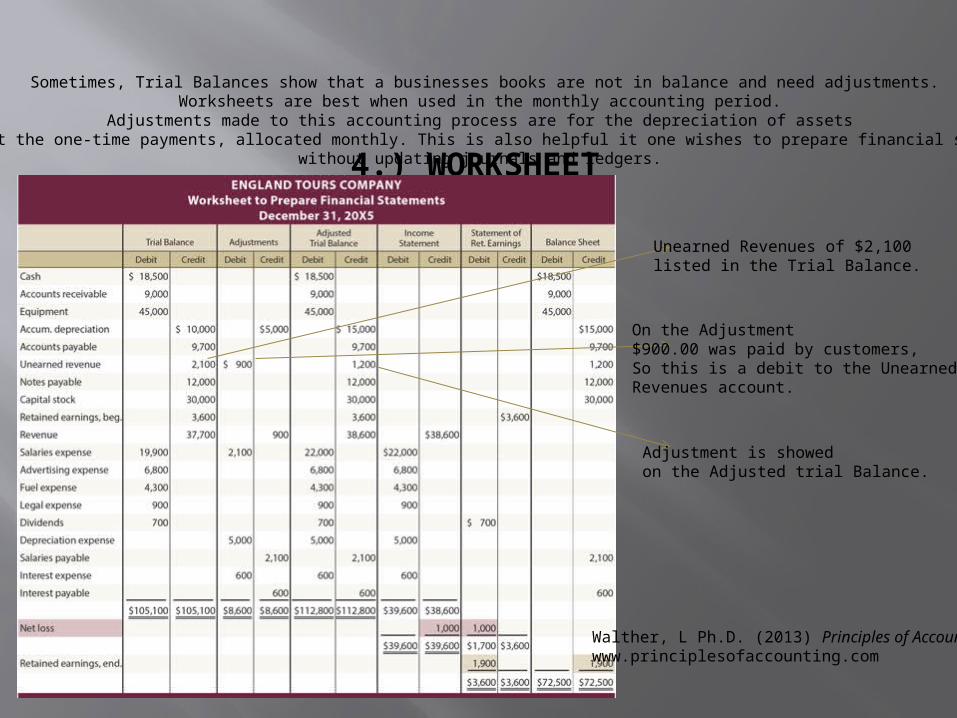

4.) WORKSHEET

Sometimes, Trial Balances show that a businesses books are not in balance and need adjustments.Worksheets are best when used in the monthly accounting period.

Adjustments made to this accounting process are for the depreciation of assets And adjust the one-time payments, allocated monthly. This is also helpful it one wishes to prepare financial statements

without updating journals and ledgers.

Unearned Revenues of $2,100 listed in the Trial Balance.

On the Adjustment$900.00 was paid by customers, So this is a debit to the Unearned Revenues account.

Adjustment is showed on the Adjusted trial Balance.

Walther, L Ph.D. (2013) Principles of Accountingwww.principlesofaccounting.com

6.) ADJUSTING JOURNAL ENTRIESThe next step would be to post any corrections needed to any accounts the adjustment affects. This is not necessary until the Trial

Balance is completed and the adjustments have been Identified.

Walther, L Ph.D. (2013) Principles of Accountingwww.principlesofaccounting.com

Here you can see the adjusted Unearned Revenues mentions in The previous slide.

7.) FINANCIAL STATEMENTS

Financial statements are your Income Statement and balance Sheet after your haveAlready corrected the adjustments

8.) CLOSING THE BOOKS

The final step is closing the expense and revenues accounts so the next beginning Accounting period start with a zero balance.

The objectives are to update the retained earnings and to reset the temporary accounts

http://www.principlesofaccounting.com/chapter4/chapter4.html

References: Walther, L Ph.D. (2013) Principles of Accounting, website references

www.principlesofaccounting.com Author Unknown, (2015) Accounting For Dummies, Website resource:

http://www.dummies.com/how-to/content/the-eight-steps-of-the-accounting-cycle.html

Salinas, A. (2012) The General Ledger, Website photo reference, http://www.loscostos.info/financial-accounting/general-ledger.html