eHealth Strategy Business Plan - University of Michiganioe481/ioe481_past_reports/w0009.pdf ·...

81

- - University of Michigan Health System eHealth Strategy Business Plan April 21, 2000 Univ eL’s it V of Michigan Iusiness SchooL Multidisciplinary Action Project Team Julie Brennan Sachin Kheterpal, M.D. Chekesha Kidd Jin-Kyoung Kim Tim Mohnke Ron Perry Faculty Advisor: Jane Dutton Company Liaisons: Deborah Biggs J.D., Paul Taheri M.D., M.B.A.

Transcript of eHealth Strategy Business Plan - University of Michiganioe481/ioe481_past_reports/w0009.pdf ·...

_

-

-

University of MichiganHealth System

eHealth Strategy Business Plan

April 21, 2000

Univ eL’s it V

of MichiganIusinessSchooL

Multidisciplinary Action Project TeamJulie BrennanSachin Kheterpal, M.D.Chekesha KiddJin-Kyoung KimTim MohnkeRon Perry

Faculty Advisor: Jane DuttonCompany Liaisons: Deborah Biggs J.D., Paul Taheri M.D., M.B.A.

University ofMichi2an Health System E-Health Stratev Business Plan

L UMHS BACKGROUND 1

A. CURRENT CHALLENGES 1

B. USE OF TECHNOLOGY AT UMHS 1

IL MARKET ANALYSIS .._.—.— .... .... -..

A. INDUSTRY ANALYSIS 2

B. TARGETMARKEI 3

C. COMPETmON 4

D. REGULATORY ISSUES 6

E. FUTURE TARGET MARKETS 6

III. PROPOSED PRODUCT AND SERVICE................................._.........__.. ........... .......7

A. PRODUCT OVERVIEW 7

B. PRODUCT ARCHITECTURE 7

C. CONSUMER USE 10

D. PRODUCT BENEFITS 11

E SECURITY AND CONFIDENTIALITY 12

F. COPYRIGHTS, PATENTS, AND TRADE SECRETS 13

0. PRODUCT LIABILITY 13

H. PRODUCT EXTENSIONS 13

H. EXIT STRATEGY 13

1V. COMPANY .. .................................13

A. NATUREOFTRE BUSINESS 13

B. DISTiNCTIVE COMPETENCIES AND UNIQUE RESOURCES 14

V. MARKETING AND SALES STRATEGY...... .. ........................... ..

A. POTENTIAL CUSTOMERS AND NEEDS IDENTIFICATION 15

B. MARKET SEGMENTS AN]) CUSTOMER PRI0RTnzATION 15

C. PRICING 15

D. DISTRIBUTION AND PROMOTION 17

VL ORGANIZATION, MANAGEMENT, O’.VNERSRIP, AND OPERATIONS. _..................................17

A. STRUCTURE 17

B. STAFFING — PRODUCT DEVELOPMENT 18

C. STAFFING - OPERATIONS 19

D. INCENTIVE STRUCTURE 19

E. PARThERSIIWS AND ALLIANCES 21

VIL FUTURE PRODUCTS.._................ ....._-.---.......

A. PHYSICIAN INFORMATION WEB PAGE (P1W) 24

B. DECISION SUPPORT SYSTEM 24

C. CONTINUING MEDICAL EDUCATION 24

D. JUST -IN-TIME EDUCATION 24

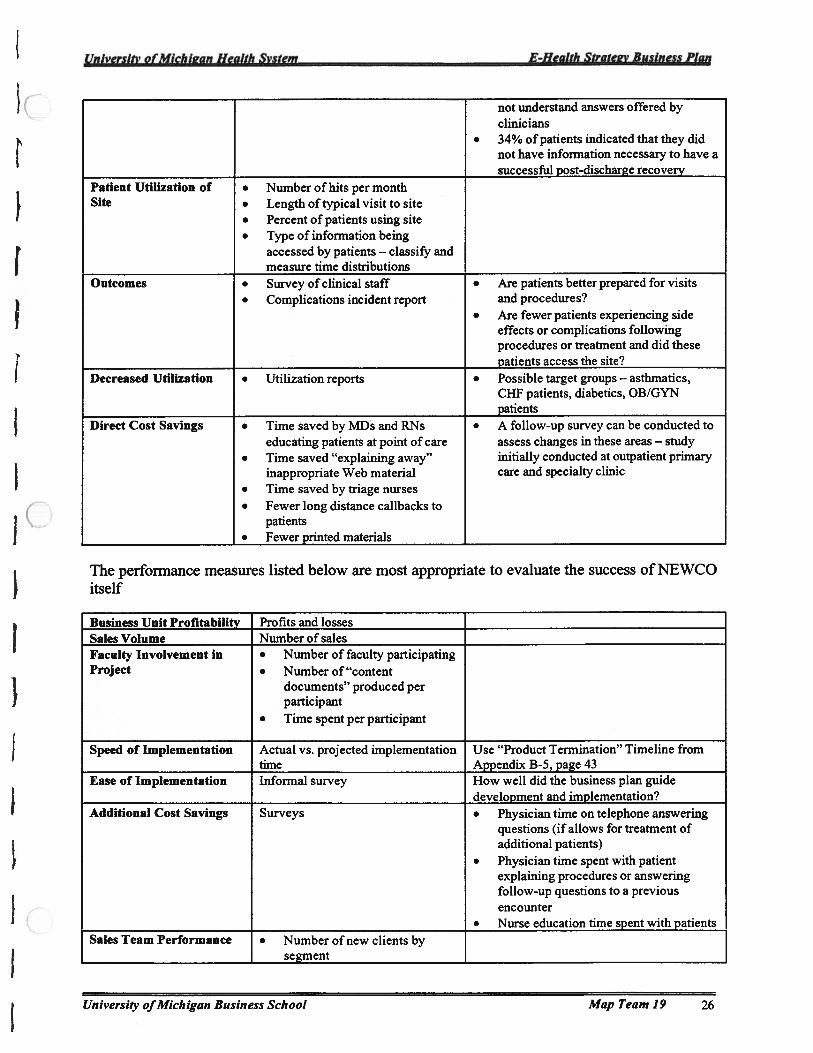

VIII. PERFORMANCE METRICS .. .................. ....... ......._ .. ......

IX. FUNDING REQUIREMENTS........................... ............- .. ._.....

A. CURRENT FUNDING REQUIREMENTS 27

B. FUNDING REQUIREMENTS THROUGH 2005 28

C. LONG RANGE FINANcLL SFRATEGY 28

X. FINANCIAL PROJECTIONS .. ...... .. ......... ..

A. ASSUMPTIONS 29

B. 5-YEAR PROJECTIONS 30

University’ ofMichigan Business School Map Team 19

University ofMichi2an Health System E-Health Stratev Business Plan

LIST OF APPENDICES

APPENDIX A: MARKET ANALYSIS 31

APPENDIX A-i: Technical Demands of Health-Related Applications of the Internet 32APPENDIX A-2: Competitive Analysis - Players 32APPENDIX A-3: Competitive Analysis — Tier 4 Competitors 33APPENDIX A-4: Competitive Analysis — Tier 3 Competitors 35APPENDIX A-5: Future Target Markets 37

APPENDIX B: PROPOSED PRODUCT AND SERVICE 38

APPENDIX B-i: Overview of CPW 39APPENDIX B-2: Detailed Product Map 40APPENDIX B-3: Technical Architecture 41APPENDIX B-4: Education Delivery Process 42APPENDIX B-5: Product Termination Timeline 43

APPENDIX C: SLAES AND’MARKETJNG 44

APPENDIX C-i: Target Customers of CPW 45APPENDIX C-2: Potential Customer Analysis 46APPENDIX C-3: Market Segmentation 47APPENDIX C-4: Segment Prioritization Template 48APPENDIX C-5: Customer Prioritization Template 49APPENDIX C-6: EVA Analysis 50

APPENDIX D: ORGAMZATION AND PARTNERSHIP 51

APPENDIX D-i: Organization Chart of NEWCO 52APPENDIX D-2: Staffing and Salaries - Product Development Phase 53APPENDIX D-3: Staffing and Salaries - Operations Phase 54APPENDIX D-4: Competitive Analysis 56APPENDIX D-5: Potential Partners Company Description 57APPENDIX D-6: Required Capabilities of Potential Partners 59

APPENDIX E: FUTURE PRODUCTS 60

APPENDIX E- 1: Product Synergies 61

APPENDIX F: FINANCIAL PROJECTIONS 63

APPENDIX F-i: Development Phase Financial Projection Assumptions 64APPENDIX F-2: Product Development Cost Summary 65APPENDIX F-3: Detailed Product Development Costs 66APPENDIX F-4: Detailed General & Administrative Costs - Operations 67APPENDIX F-5: Proforma Income Statement and Statement of Cash Flows 68APPENDIX F-6: Sensitivity Analysis 69

APPENDIX G: LIST OF INTERVIEWS 70

BIBLIOGRAPHY 73

University ofMichigan Business School Map Team 19

Universifl’ ofMichigan Health System E-Health Siraiev Business Plan

Executive Summary

University of Michigan Health System BackgroundWith an annual expense budget of $1 billion dollars and 15,663 employees and faculty, theUniversity of Michigan (UMHS) rivals many prominent US firms in temis of size while facingunique regulatory and legislative challenges as a public institution. Due to increasing fmancialpressures placed upon health systems, and academic medical centers in particular, UMHS isfaced with the task of fmding innovative profitable endeavors that leverage its significantintellectual capital, technical knowledge, clinical experience, and prestige.

Market AnalysisAs superior clinical outcomes become more commonplace among providers, consumers of the$1.2 trillion health care industry are increasingly demanding a superior service experience todifferentiate health systems and providers. At the same time, health systems must increase thepatient base in order to maintain revenues in the face of decreasing reimbursement rates andutilization. Patient education and information have been identified as two of the most importantmodifiers of overall patient satisfaction. Surveys indicate that patients want more educationalinformation from their physician. Furthermore, data indicate that 52 million individuals will visitWeb health care sites in the year 2000. The case to satisfy the health care consumer’s unmet needfor reputable, individualized, timely, and usable health care education materials is extremelycompelling.

,-, Proposed Product‘..J NEWCO will develop a software engine that links existing patient information databases with

appropriate educational content to create a customized patient web page (CPW) accessed bypatients using a unique patient ID and password. The web page will contain information aboutthe patient’s current conditions, treatments, medications, and procedures in addition to basichealth maintenance activity educational materials. Once developed and proven using the UMHSpatient set, the web engine will be sold to other health systems, payors, and self-insuredcorporations.

Marketing StrategyNEWCO has identified that current industry trends are forcing health care institutions to seekcredible clinical content providers and tools to increase patient base. Utilizing UMHS’significant national brand awareness, its patient base as a showcase for the product, and strategicrelationships, NEWCO will successfully segment and target entities responsible for ensuringpatient satisfaction, outcomes, and cost reduction: 3600 hospitals, 4000 payors, and Fortune 100self-insured companies.

Competitive AnalysisThough over 15,000 health care web sites currently offer static web content that must be filteredand interpreted by the patient, only a handful of competitors such as Cemer Corporation andLDX / ChannelHealth hope to deliver customized patient web content. None of these potentialcompetitors has ownership of the crucial patient data necessary to develop, deploy, or refme theproduct. Furthermore, they do not possess the credible and evidence-based clinical contentoffered by UMHS.

University ofMichigan Business School Map Team 19 ui

University ofMichi2an Health System E-Health Strate’v Business Plan

Company Description, Organizational Structure, and ManagementNEWCO will be a Michigan for-profit taxable subsidiary of the Michigan Health Corporation(MHC). MHC was established by the Regents of the University as a vehicle to participate in,coordinate, and develop health care related activities to maintain and enhance the educational,research and service missions of the University. Technical staff will be full-time employees andstockholders of NEWCO. UMHS clinical staff will be motivated to develop clinical contentthrough market-competitive cash reimbursement and stock ownership.

Revenues and ProfitabilityNEWCO requests an initial investment of $1.6 million from UMHS over an eight-month productdevelopment period to realize revenues of $11 million in 2003, resulting in an NPV of $4.9million and payback period of three years on a cumulative cash flow basis. These projections arebased upon conservative estimates of staffing requirements, development costs, and marketshare. Equity relationships with strategic technical, content, and distribution partners will beinvestigated to decrease the UIvIHS capital investment.

Value to U1fflSThe CPW product line will be used as a launching pad to future strategic health care productofferings such as a Customized Physician Information Web Page, Decision Support System, andInteractive Continuing Medical Education and Just-In-Time Education.

The formation of NEWCO and successful launch of the CPW will add needed non-clinicalrevenue to the UMHS bottom line while furthering its educational mission. In addition, it willencourage UMHS faculty to leverage their intellectual capital through internal UMHS ventures.

University ofMichigan Business School Map Team 19 iv

University ofMichiean Health System E-Health Stratevv Business Plan

L IJMHS Background

The University of Michigan Health System (UMHS) is comprised of the Medical School and itsFaculty Group Practice, 7 hospitals, 30 health centers, 120 outpatient clinics, M-CARE HMOand Michigan Health Corporation. In order to retain its non-profit fmancial status, decisions andbusiness endeavors must directly affect the three pronged mission of excellence in patient care,education, and research.

Recognized by US News and World Report as a top 10 medical center and medical school,UMHS has earned an excellent reputation. In FY 1999, UMHS received 36,713 admissions and1,231,216 outpatient visits. UMHS has been fortunate to maintain a profitable operation in pastyears. As health care industry pressures increase, however, the health system must continue togenerate revenue while decreasing costs and providing high quality patient care. UMHS mustsimultaneously build upon its existing educational and research activities.

A. Current Challenges

The majority of academic medical center revenue is generated through clinical care. With themovement to managed care and discounted fee-for-service, hospital margins have been declining(Spanier, 2000). UMHS, like other academic medical centers, has traditionally relied on cross-subsidization of funding from clinical services to support research and educational missions.This is becoming more difficult as reimbursement declines and pressures to reduce costs

“—- continue. To thrive in the future, UMHS must leverage its strengths and develop innovativemethods of generating revenue. eBusiness has the potential to serve as a significant source ofrevenue for early-to-market organizations. UMHS should take advantage of this opportunity.

Currently, massive amounts of clinical, research, and educational information reside withinUMHS’s databases, Internet sites, individual departments, and faculty minds. However, UMHSis not fully leveraging its intellectual capital. Members of the faculty are selling their clinicalknowledge to Internet content providers such as Oncology.com. To curb this “brain drain,” thehealth system has the opportunity to develop an innovative business and incentive structure toencourage faculty to participate in activities that will benefit patients, the health system, thefaculty members themselves.

B. Use of Technology at UMHS

One of UMHS’s greatest strengths is its advanced research and application of technology.Throughout the University campus, UMHS participates in development and use of cutting-edgetechnology. Some of the existing projects include:

Visible Human Project Medical Readiness TrainereMail for clinical care enhancement (CHOICES) Web-based health risk appraisal and educationClinical telemedicine and tele-education Remote patient wound managementSurgical Simulation Center

University ofMichigan Business School Map Team 19 1

University ofMichk’an Health System E-iIealth Strateav Business Plan

UMHS is also a leader in the development of the Intemet2 project based in Ann Arbor. Intemet2is an initiative led by over 170 universities working with industry and government to developand deploy advanced network applications and technology. These activities uniquely positionUMHS to serve as a leader in developing an eHealth strategy to better serve patients, families,and communities.

IL Market Analysis

A. Industry Analysis

The health care services industiy is comprised of a complex network of private for-profitcorporations, non-profit organizations, federal agencies, and state bodies. Academic medicalcenters are affected by all of the changes in the health care industry in general. Some of thesechallenges include, but are not limited to:

• Rapid increase in the age of the population• Continued transition to ambulatory care from inpatient care• Declining funding and reimbursement• Increasing consumer power and knowledge• Large uninsured population - approximately 40 million Americans remain uninsured• Patient rights initiatives - improving patient rights to choice, information, and privacy• Internet and technology changes affecting the delivery of care• Increasing utilization of homeopathic therapies by patients and allopathic clinicians

A major trend affecting all types of medical care is the increasingly important role of technology.The Internet is being used by patients to gather information about their own, their families’, andfriends’ diseases or health status. Health care providers use the Internet to collect clinical data,track patient records, and communicate within their own institutions.

The chart below illustrates the evolution of health care and the impact of technology.

Today Time

a,

Cu>a,

Cu0,

RemoteCare

RemoteTreatment

(::(fradjtjon\mea

- Telecare- DistantMonitoring

- Medscape-WebMD

- Magazine- Brochure

- Telemedicine- Remote prescription

- Customized patient info- Personalized healtheducation

Source: Goldman Sachs, MAP Team analysis

University ofMichigan Business School Map Team 19 2

University ofMichiL’an Health System E-Health Stratev Business Plan

Currently, consumers and providers have the opportunity to retrieve static and limited interactive

information from Web sites. Due to current reimbursement guidelines and changes to operations

that are necessary to accommodate new technology, remote care is not immediately feasible for

most institutions. However, as technology and infrastructures advance, remote care will becomemore ubiquitous. In the future, the Internet and private networks will be utilized for extensiveresearch, training and education opportunities. Today, educational opportunities are the most

promising because they require limited technology infrastructure and are not capital intensive fororganizations with mature IT infrastructure.

The table in Appendix A-l page 32 provides a relative scale of the importance of varioustechnological capabilities in the delivery of education, research and clinical care.

Within the health care field, the Internet provides a variety of media for providers and other

organizations to communicate with consumers. According to a study published by the ComputerScience and Telecommunications Board and the National Research Council (2000),

“Ongoing trends in health care are likely to reinforce the trend toward consumer-oriented health information. . . Patients have been encouraged to take a more active

role in their own health care, and care providers have recognized the value ofengaging patients to participate more meaningfully in their own care. Attempts bycare providers and managed care plans to streamline services and cut costs have

shortened hospital stays, increasing the need for patients and their families tounderstand how to provide care for themselves. Greater emphasis is being placedon preventive care, which requires consumers to understand health risks and theeffects of different behaviors on health. These trends heighten the need forconsumers to have access to reliable health information and open channels ofcommunication to care providers and other health professionals.”

As technology and health care continue to merge, full-service health sites will emerge in the

consumer market. According to research by Forrester (2000), “health systems will need topublish their own materials and participate in direct-to-consumer marketing as educated,

empowered consumers shop for health services with increasing discernment.”

B. Target Market

The patient education market offers the greatest opportunity for web-based products and is our

initial target market. Currently, patient education over the Internet consists of Web sitesproviding healthcare information for health information seekers. The sites typically include basichealth information, community interaction (via chat rooms/news groups), and access to moreadvanced information through search and message boards. Information posted on the Internet isnot monitored for quality or accuracy, yet consumers continue to demand more.

Medical information is the second most sought after topic on Internet, and 40% of all US Internet

users are somewhat active health info seekers (Goldman, 1999). In 1998, 34 million peopleaccessed health information on the Web. In 1999, 45 million people sought health information onthe Web, and in 2000, 52 million people will seek health information on the Web. 53% of online

Universitr ofMichigan Business School Map Team 19 3

/

University ofMichi’an Health System E-Health Strate’ Business Plan

health information seekers are female, and 60% of online health information seekers are over theage of 40 (Goldman, 1999). The market segment continues to grow.

Over the past decade, the patient has become more of a partner in physician-patient encounter.Education is a key component of this encounter, but the majority of patients do not feel that theirphysician provides adequate information during encounters. Consequently, many individualsturn to the Internet for additional information. The younger the patient, the more likely they areto use the Internet for health information. However, the fastest growing online population isindividuals over the age of fifty. 84% of patients surveyed during a MEDSTAT study indicatedthat they want better access to health care information (Picker, 1999). 77% of patientsinterviewed in a recent survey stated they would like to receive on-line information from theirphysician (Healtheon, 2000).

Many providers rely on patient satisfaction measures to determine how well they are meetingconsumer needs. The Picker Survey allows providers to evaluate how well they are addressingthe educational needs of patients. The primary factors that correlate best with overall patientsatisfaction are emotional support and informationleducation. A customized web site that allowsproviders to better educate their patients will increase overall satisfaction leading to higher levelsof patient retention and referrals.

Although patients are actively seeking information on the web, physicians do not believe thatmedical information on Internet has helped to better educate patients (Picker, 1999). According

C to interviews conducted by the UMHS MAP Team, most physicians do not refer patients toparticular health/medical sites, mainly because they are not able to identify credible and safesites. Consumers, including patients and clinicians, feel the sites lack credibility of content(Physician, 2000). “A recent study found that 6% of the 400 sites containing information on aform of cancer called Ewing’s sarcoma contained erroneous information, and many more were

There is an unmet need in the patient education market for a credible, accurate and easy-to-navigate patient information site. “Consumers need effective searching and filtering tools thatcan identify and rank information according to their needs and capabilities and present theinformation in a form that they can understand. . . Consumers also need a way to judge the quality,authoritativeness, and provenance of the information.”(Goldman, 1999) Better educated patientswill be able to work with their physicians to produce better health outcomes. Physicianscurrently spend valuable time “uneducating’ patients concerning information they received onthe Internet. A site that proactively directs high-quality information to patients and links patientsto other credible sites will reduce these problems and fulfill an unmet patient need.

C. Competition

Market estimates indicate that there are 15,000 consumer health information web sites, but thereis a clear lack of differentiation among most sites. Some sites are sponsored by credible medicalorganizations such as the American Cancer Society or the American Medical Association; otherscontain postings by any individual. Unfortunately, many people are unable to discern betweenaccurate and inaccurate information, and this is a major concern of health care professionals.

University ofMichigan Business School Map Team 19 4

University ofMichii’an Health System E-Health Stratei’v Business Plan

Out of the 15,000 health information web sites, there is a handful of established players, such asMedscape and WebMD, who have distinguished themselves through content, credibility orinfrastructure. New players such as Medem, created by a consortium of seven medicalassociations, are emerging and hope to provide credible information for patients and providers.Other companies are focusing solely on providing content; ADAM, a major commercial medicalcontent provider with 10,000 pages on 1,500 topics, is an example. Similarly, PubmedJMedlineis a search engine providing 9.2 million medical citations.

Recently developed sites allow users to type in personal information in order to receive updatesand information specific to their disease state. WebMD is an example of such a site. These sitesare not connected to personal medical records that allow the site to proactively “push”appropriate information to consumers.

A few companies offer products that allow patients to receive individualized health information.Individual patients can then access a personal web page and obtain relevant health information.Medivation is marketing its product to small physician practices and individual offices. IDX /ChannelHealth and Cemer have also establishid individual web sites; these are being marketedto physician groups, hospitals, and health systems.

Academic medical centers have access to patient records and credible medical education contentthat would enable them to create individualized web products. IT-savvy centers such as JohnsHopkins and Mayo Clinic have developed consumer Web sites and possess internal publishingcapabilities. Intellihealth is a site that was initially developed and co-branded by Hopkins andAetna. This partnership has since ended (Advisory, 2000), but Hopkins retains the experience tolaunch new products. Mayohealth is a similar site sponsored by the Mayo Clinic. Duke also hasthe potential to develop advanced applications from its current web site.

Although academic medical centers are uniquely positioned to create individualized medicalcontent web sites, the MAP Team was unable to identify any AMCs developing or offering aproduct with individualized health content linked to medical records. The market for this productis attractive, and it is likely that other AMCs may attempt to develop a product in the near future.

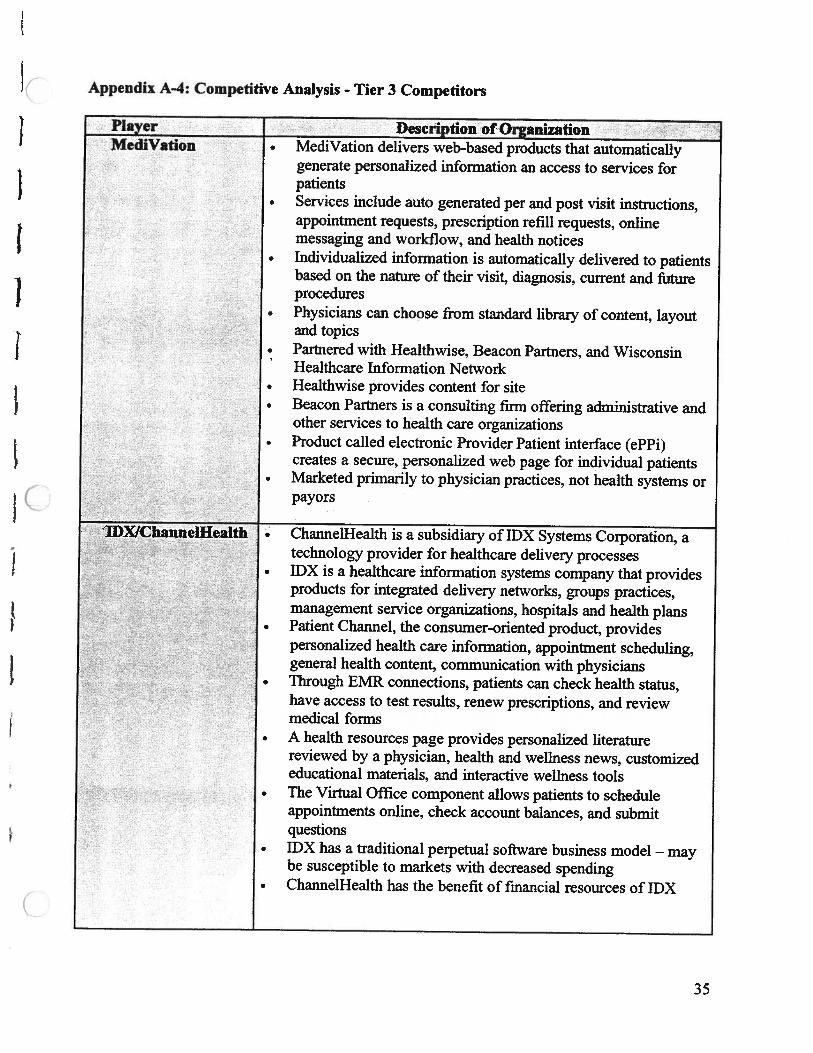

Please review Appendices A2, A3, and A4 on pages 32-35 for a schematic representation of thiscompetitor analysis.

Although the market for individualized patient education is large, barriers to entry haveprevented many companies from launching products to meet truly consumer needs. The greatestbarriers to entry include:

• Access to patient data: The producer of an individualized patient web site must haveaccess to patient data in order to link appropriate content to an individual’s site. Onlymedical providers and payors have direct access to this data.

• Credibility of clinical content: Successful players must provide general and high-level

care information. Those that hold the content internally have a significant advantage overthose that have to purchase it from others.

Universig’ ofMichigan Business School Map Team 19 5

University ofMichwan Health System E-Health Sfratev Business Plan

• Breadth and depth of clinical content: Content must be specific enough to address theindividual needs and concerns of a wide variety of patients.

• Technology resources: Organizations must have the technical capability to develop andcustomize patient-specific sites.

• Costs of development and maintenance: Costs to develop software and technologyinfrastructure are high and often prohibitive for many organizations

D. Regulatory Issues

Legislation and government play a major role in the health care industry. Recent legislation hasfocused on decreasing costs within the health care industry, increasing consumer rights andaccess to care, and ensuring security of information. The most relevant pieces of legislation arebriefly discussed below.

a) Balanced Budget Act (BBA)The 1997 Balanced Budget Act reduced the Medicare budget significantly over five years,which continues to greatly affect provider reimbursement.

b) Health Insurance Portability and Accountability Act (HIPAA)’The proposed enactment of HIPAA will force sweeping changes to strengthen healthinformation access, security, and privacy.

c) Patients’ Bill ofRightsThe Patients’ Bill of Rights is intended to provide increased access to health care services andenforce legal liability for payor clinical recommendations.

d) Other LegislationThe Medical Information Protection Act of 1999, Health Care Personal InformationNondisclosure Act of 1999, and the Medical Information Privacy and Security Act 2 are threelaws that require specified health entities in possession of protected health information toallow the subjects of the information to inspect, copy and amend it.

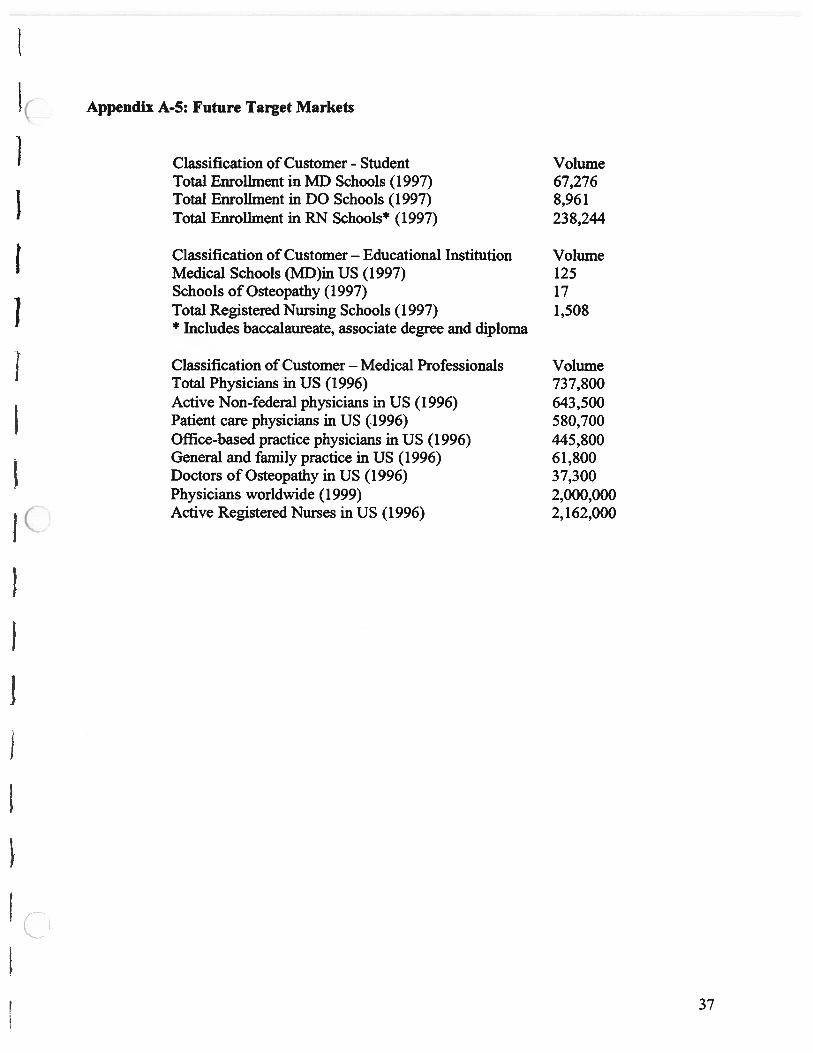

E. Future Target Markets

Patients will be our initial target in the education market. The product will be marketed tohospitals, physicians, health systems, payors and self-insured corporations; the information willbe transmitted to patients through these parties. Future target markets for educational materialswill include practicing physicians, medical schools, students, other medical institutions, andother health professionals. Information concerning the sizes of these various markets can befound in Appendix A-5, page 37.

‘For further details on HIPAA, visit the Department of Health and Human Services at www. hhs.gov.2 Information concerning the three bills related to health privacy was derived from bill summaries contained on theLibrary of Congress’s THOMAS system, available online at http://thomas.loc.gov/home/thomas.html

University ofMichigan Business School Map Team 19 6

Universiti’ ofMjchi’gn Health System E-Health Stratev Business Plan

IlL Proposed Product and Service

A. Product Overview

NEWCO will develop a software engine that links existing patient information databases withappropriate educational content to create a Customized Patient Web Page (CPW) accessed bypatients using a unique patient ID and password. The web page will contain information aboutthe patient’s current conditions, treatments, medications, and procedures. In addition, the sitewill present basic health maintenance educational materials and provider communication. Aschematic of the CPW is available in Appendix B-i, page 39.

A basic review of the healthcare information technology industry reveals that 95% of health careinstitutions do not have the comprehensive electronic medical record (EMR) necessary toidentify a given patient’s cliiical conditions (Goldman, i999). No database describes a patient’ssocial history, past medical history, active diseases processes, current medications, or desiredhealth maintenance activities.

A clinician carrying the title of “patient educator” must select the appropriate educationalmaterials that apply to a given patient’s demographics, ethnicity, clinical condition, and healthstatus. Because the current process does not leverage existing patient data or contribute to areusable knowledge base, the task is repeated each time a new patient is encountered. As a result,health care entities must engage in an extremely expensive, labor-intensive process of repeatedlycollating a patient’s personalized educational materials (traditional or electronic) de novo.

There are unmet needs for high quality, personalized health care information. Encouraged by“my” web site fever (myYahoo.com, mySAP.com, etc.), consumers are now demanding accessto the right information at the right time on the Internet, not all information all of the time aspreviously thought. This holds particularly true for the healthcare information market.

B. ProductArchitecture

The proposed product is a set of software engines that perform several crucial functions:i. Interface to the reimbursement and EMR databases2. Translation and mapping of client-specific patient condition databases to a single,

common, reusable patient condition database3. Storage of patient education content in a single, reusable content database4. Linkage of the patient condition database to the content database5. Delivery of desired content as an HTML-based, secure and confidential web site

As the diagram below illustrates, the software engines will create three electronic databases toperform these five functions. The three electronic databases, described in greater detail below,are:

1. Patient-specific clinical conditions2. Patient education material3. Linkages between patient conditions and appropriate education materials

University ofMichigan Business School Map Team 19 7

Ilnivpr.clft, nfMlphirjran I1aIIh cv.ctni F-ffpalIh .cfratoi, Rnclnpvc Plan

Patient Clinical Condition and Reimbursement Database

Though the patient specific, discrete clinical data created by an EMR is not available at mosthealth systems, all entities involved in the health care delivery process must codif’ a patient’sclinical diagnoses and treatment in order to be reimbursed. Communication between clinicalproviders (health systems, hospitals, clinics, etc) and payors (government, private insurance, etc)occurs through three ubiquitous lexicons used throughout the United States:

1. Current procedural terminology (CPT) of 4,000 codes2. International classification of diagnoses (lCD) of 15,000 codes3. Diagnosis related groups (DRG)

All health care institutions must create electronic databases of patient CPT, lCD, and DRG codesin order to participate in the electronic data interchange (EDI) mandated by payors. The creationof these databases is a complex and confusing process. After disbursing clinical services, aclinician creates documentation necessary to accurately communicate the patient’s history,status, and care plan from one provider to another — the paper medical record. An abstractor orhealth record analyst (HRA) reviews this clinical documentation at a later date and identifieswhich CPT, lCD, and DRG codes apply to the clinical encounter and patient. Because theprimary purpose of this data is communication with payors, the codes selected by the HRAs areoptimized for maximum reimbursement. Several codes often describe a given condition, but aspecific code may be chosen based upon experience regarding its likelihood of acceptance andreimbursement by the patient’s specific payor. In isolation, a given lexicon’s single code may notaccurately represent a patient’s true clinical condition. When utilized in aggregate and withrelatively simple filters to exclude contradictory conclusions, the codes are capable of accuratelydescribing a patient’s clinical conditions. For example, these electronic databases are a crucial

Engine

For a more detailed product diagram, please review Appendix B-2, page 40:

University ofMichigan Business School Map Teaml9 8

University ofMichiL’an Health System E-Health Strate’v Business Plan

source of clinical information employed for clinical outcome research, individual clinician and

institutional benchmarking, and cost-per-case analysis.

As industry trends force health care institutions to migrate to EMR, increasing amounts of

patient information databases will be available. Once available, these EMR databases will be

employed in lieu of billing data to improve the specificity and accuracy of the educational

content delivered to the patient.

Patient Educational Material / Content Database

The second set of databases necessary to provide customized content is the patient education

information. This clinical content currently exists in many forms: pamphlets, clinical care

protocols, practice guidelines, web site content, and other published materials. It is available

from a variety of sources in the public and private domain ranging from government

organizations to for-profit medical content entities previously mentioned. To date, this content

has been stored and distributed at a macroscopic condition level (asthma) or health maintenance

activity (breast cancer detection) level. However, this information can easily be digested into

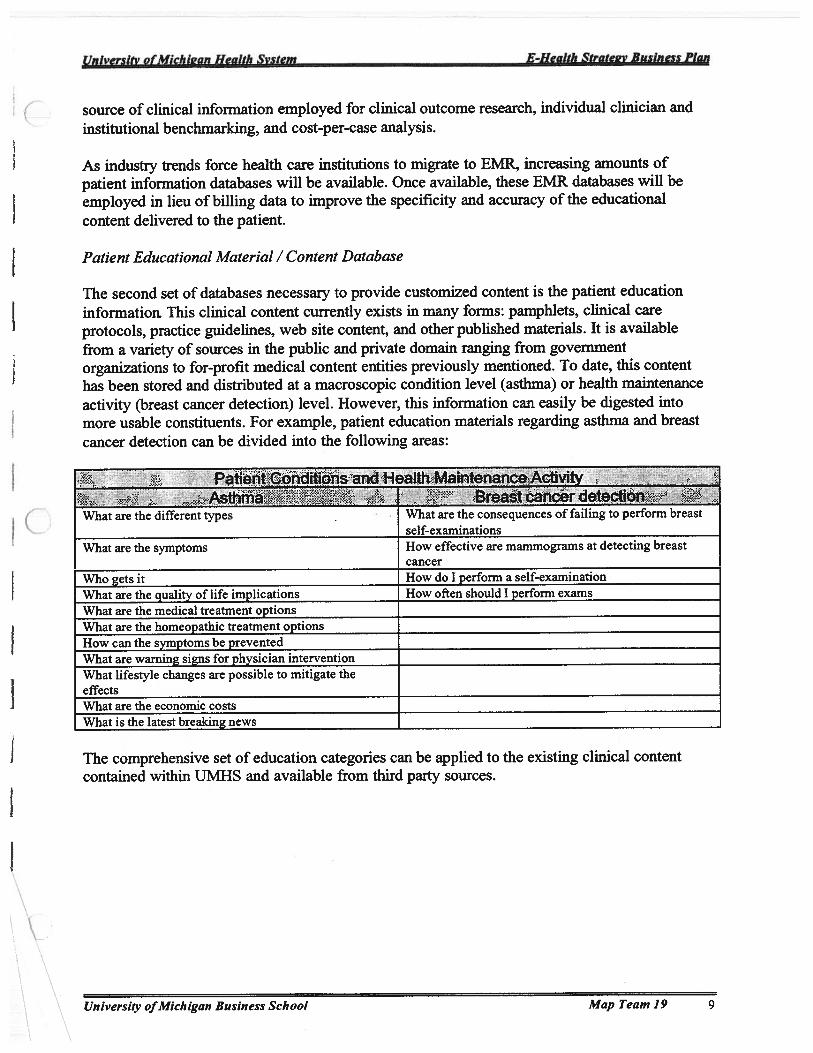

more usable constituents. For example, patient education materials regarding asthma and breast

cancer detection can be divided into the following areas:

Patient Conditions and Health Maintenance ActivityAsthma Breast cancer detection

Vhat are the different types Vhat are the consequences of failing to perform breastself-examinations

What are the symptoms How effective are mammograms at detecting breastcancer

Who gets it How do I perform a self-examinationWhat are the quality of life implications How often should I perform examsWhat are the medical treatment optionsWhat are the homeopathic treatment optionsHow can the symptoms be preventedWhat are warning signs for physician interventionWhat lifestyle changes are possible to mitigate theeffectsWhat are the economic costsWhat is the latest breaking news

The comprehensive set of education categories can be applied to the existing clinical content

contained within UMHS and available from third party sources.

Unn ersiti’ ofMichigan Business School Map Team 19 9

11nivprcifr nfPfirhiornn 1-b’alIh v.cIm F-IIpalfh Stratepv Ruxincx Plan

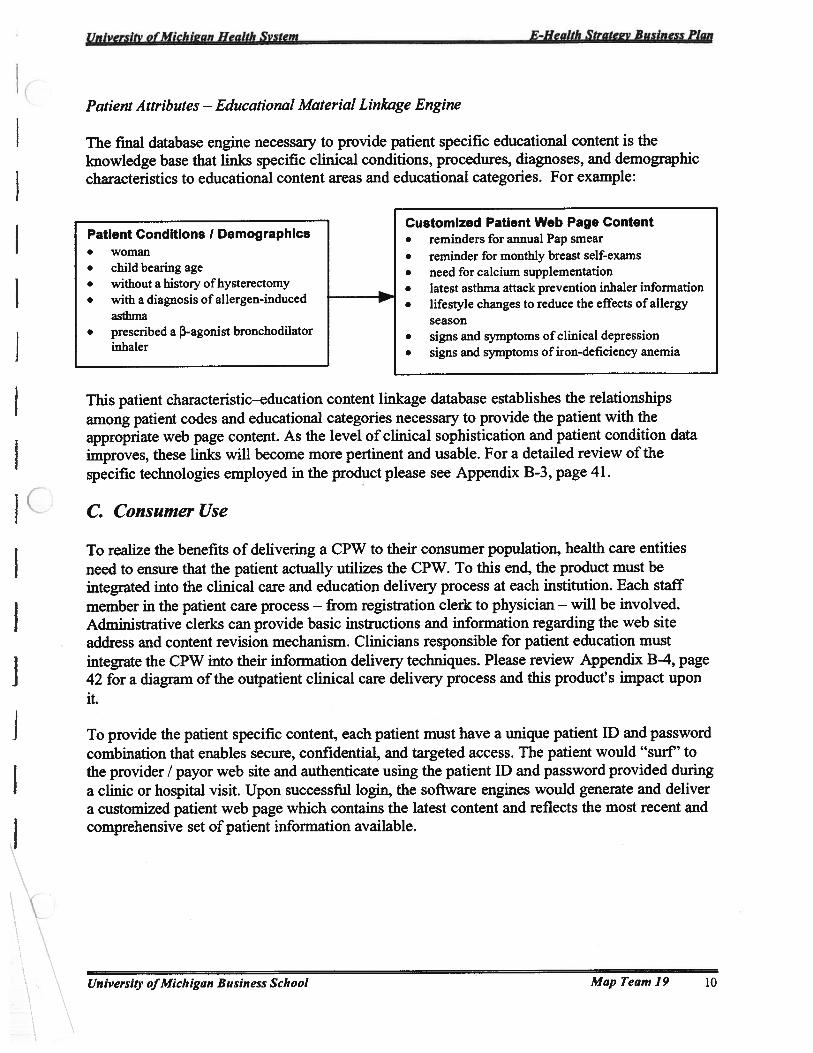

Patient Attributes — Educational Material Linkage Engine

The fmal database engine necessary to provide patient specific educational content is theknowledge base that links specific clinical conditions, procedures, diagnoses, and demographiccharacteristics to educational content areas and educational categories. For example:

This patient characteristic—education content linkage database establishes the relationshipsamong patient codes and educational categories necessary to provide the patient with theappropriate web page content. As the level of clinical sophistication and patient condition dataimproves, these links will become more pertinent and usable. For a detailed review of thespecific technologies employed in the product please see Appendix B-3, page 41.

C. Consumer Use

To realize the benefits of delivering a CPW to their consumer population, health care entitiesneed to ensure that the patient actually utilizes the CPW. To this end, the product must beintegrated into the clinical care and education delivery process at each institution. Each staffmember in the patient care process — from registration clerk to physician — will be involved.Administrative clerks can provide basic instructions and information regarding the web siteaddress and content revision mechanism. Clinicians responsible for patient education mustintegrate the CPW into their information delivery techniques. Please review Appendix B-4, page42 for a diagram of the outpatient clinical care delivery process and this product’s impact uponit.

To provide the patient specific content, each patient must have a unique patient ID and passwordcombination that enables secure, confidential, and targeted access. The patient would “surf’ tothe provider / payor web site and authenticate using the patient ID and password provided duringa clinic or hospital visit. Upon successful login, the software engines would generate and delivera customized patient web page which contains the latest content and reflects the most recent andcomprehensive set of patient information available.

University ofMichigan Business School Map Team 19 10

Patient Conditions I Demographics• woman• child bearing age• without a history of hysterectomy• with a diagnosis of allergen-induced

asthma• prescribed a 13-agonist bronchodilator

inhaler

Customized Patient Web Page Content• reminders for annual Pap smear• reminder for monthly breast self-exams• need for calcium supplementation• latest asthma attack prevention inhaler information• lifestyle changes to reduce the effects of allergy

season• signs and symptoms of clinical depression• signs and symptoms of iron-deficiency anemia

University ofMichigan Health System E-Health Stratev Business Plan

D. Product Benefits

The CPW, a consumer-focused product, actually provides benefits to all participants in thehealthcare delivery process. Thus, it is useful to review the salient benefits to each party:

Patient BenefitsTrustworthy information — The CPW enables patients to access medical informationwhich has been approved by UMHS and their personal physicians. It has been shown that77% of consumers preferred to receive information from their personal physician(FindJSVP Survey). Both the “Block M” and physician stamp of approval lend far greatercredibility than information obtained through third party web sites.

• Usable information — This categorization and digestion of educational content is crucialto providing an integrated educational experience that views the patient as a whole personrather than a list of diseases, conditions or demographic attributes. A patient withdiabetes and asthma needs to review the necessary lifestyle changes to mitigate the effectof their conditions as a whole, not as specific reactions to specific diagnoses.

• Empowerment in clinical care delivery — By actively and continuously participating inthe consumption of personalized medical information, the patient becomes more of anactive partner in the healthcare delivery process.

• Educational reinforcement — It is estimated that patients recall 43% of the informationgiven to them by physicians during clinical visits (Routine, 1999). The Internet providesan unprecedented opportunity to enable patients to access dynamic, individualizedmedical content at any time, thereby increasing their overall retention of information.

• Improved clinical outcomes — There is strong evidence suggesting that better patienteducation will improve clinical outcomes. A study of medication side effect reportingrevealed that informing patients of a medication’s side effect profile would decrease thelikelihood of complaints from 10% to 8% (Journal of Family Practice). In the healthmaintenance activity realm, timely and appropriate mammography screening can reducemortality by 16% in women aged 40-49 (Patient, 1999).

Clinician Benefits• Leverage Internet for patient education — Recent surveys indicate that physicians want

to use the internet to educate patients but do not feel they have appropriate sites available(Healtheon, 1999).

• Increased control over Internet information — A significant proportion of a clinician’seducational effort is expended to integrate and clarify the Internet content acquired by thepatient through third-party sources (Woolliscroft, 1999). 89% of physicians are affectedby Internet educational materials, but only 33% have any control over a web site(Healtheon, 1999).

• Ideal method for reinforcing education— In a survey of primary care patients, 54% ofrespondents would utilize educational tools that reiterated and reinforced informationoriginally offered by their physician (Nathan, 1994).

• More “efficient” use of valuable clinician time — Rather than repeating basic materialseasily delivered through a web page, clinicians will be able to focus their time on trulyintegrative and interactive information during the care episode.

University ofMichigan Business School Map Team 19 11

University ofMichi2an Health System E-Health Sfrate-v Business Plan

• Increased patient satisfaction — National Picker survey data establish that improvingpatient education efforts will directly improve overall patient satisfaction (Picker, 1999).

• Increased patient compliance — Recent studies have affirmed that computer aidededucation resulted in statistically significant increases in medication administrationcompliance and overall outcomes. (Edworthy, 1999)

Medical Institution and Payor Benefits• Increased patient satisfaction— More than 50% of patients that reviewed and discussed

Internet health information with their clinician reported they were more satisfied withtheir treatment as a result (Leaffer, 2000).

• Improved clinical outcomes — As mentioned in the Patient Benefits section, breastcancer detection research indicates that education improves compliance with healthmaintenance activities and treatment plans, which directly improved outcomes.

• Higher patient retention rates — By increasing patient satisfaction and clinicaloutcomes, health care entities will be able to prevent the common “health plan shuffle”.The higher retention rates obviate the expense of acquiring new patients to fill capacity oflost customers. Preliminary UMHS data indicate that for inpatient admissions, the costdifferential between retaining a patient and acquiring a new patient is several hundreds ofdollars (Bruck, 2000).

• Decreased resource utilization — A study by the LifeMasters corporation indicated thateducation alone can directly decrease health system resource utilization.

• More efficient use of clinician time — As mentioned earlier, the CPW will allowphysicians to focus on more complex educational encounters.

• Industry prestige and brand equity

E. Security and Confidentiality

The typical Internet user identifies security and confidentiality as one of the most significantconcerns regarding Internet transactions. The sensitive nature of personal health care raisessecurity concerns to an appropriately high level. Because the web site is provided by the patient’shealth system, concerns regarding communication of sensitive data to third parties is allayed;rather than using “healthinfo.com”, the patient would be using a trusted physician or healthsystem site, “myinfo.umich.edu” for example. The threat of emerging privacy standards such asHIPAA reinforce the critical value of this architecture.

The existing security mechanisms employed for the burgeoning eCommerce industry such assecure sockets layer (SSL) and 128-bit encryption will ensure that data security is notcompromised during electronic transmission from the health system site to the patient’s desktop.At institutions possessing an Internet firewall to ensure authenticated access to internal ITresources, the software engines will communicate securely across the firewall while ensuringeasy access to the consumer. The product will employ emerging security standards andtechnologies as they are developed by health care IT consortiums such as the 11.19 group.

Universii’ ofMichigan Business School Map Team 19 12

University ofMichkan Health System E-HealIh Strate2v Business Plan

F. Copyrights, Patents, and Trade Secrets

Traditionally, the software industry has not employed copyrights and patents as a means ofgaining a sustainable competitive advantage. Courts have previously deemed that user interfacescreens, business logic, and software functionality are not patentable intellectual property eventhough the source code base underlying them may be. However, recent developments in theindustry such as Amazon.com’s successful patent acquisition for the “One Click” shopping carthave raised new opportunities. During the development phase, legal counsel will be retained toinvestigate the patentable intellectual property and processes created by the company.

G. Product Liability

Clearly, the distribution of medical information can involve significant liability exposure. Theseparation of clinical care and instructions from educational material and information isparticularly dubious when the source of the information is the patient’s clinical provider. Thereexists significant legal precedent for this differentiation if the provider employs a proactivedisclaimer describing the educational intention of the content. In addition, an informed consentagreement can protect the health care institution from liability if it specifically addresses the useof the web site as an educational tool rather than clinical care delivery tool.

H. Product Extensions

The first generation CPW will be a launching pad to more a sophisticated and comprehensivepatient web site product line. Transactional functions such as appointment scheduling, medicalbill payment and review, direct physician communication, medication prescription fulfillment arelogical next steps in the maturation of the CPW and have been identified as “version 2.0”features.

New products targeted at a broader market and customer needs will be discussed in the FutureProducts section of this document.

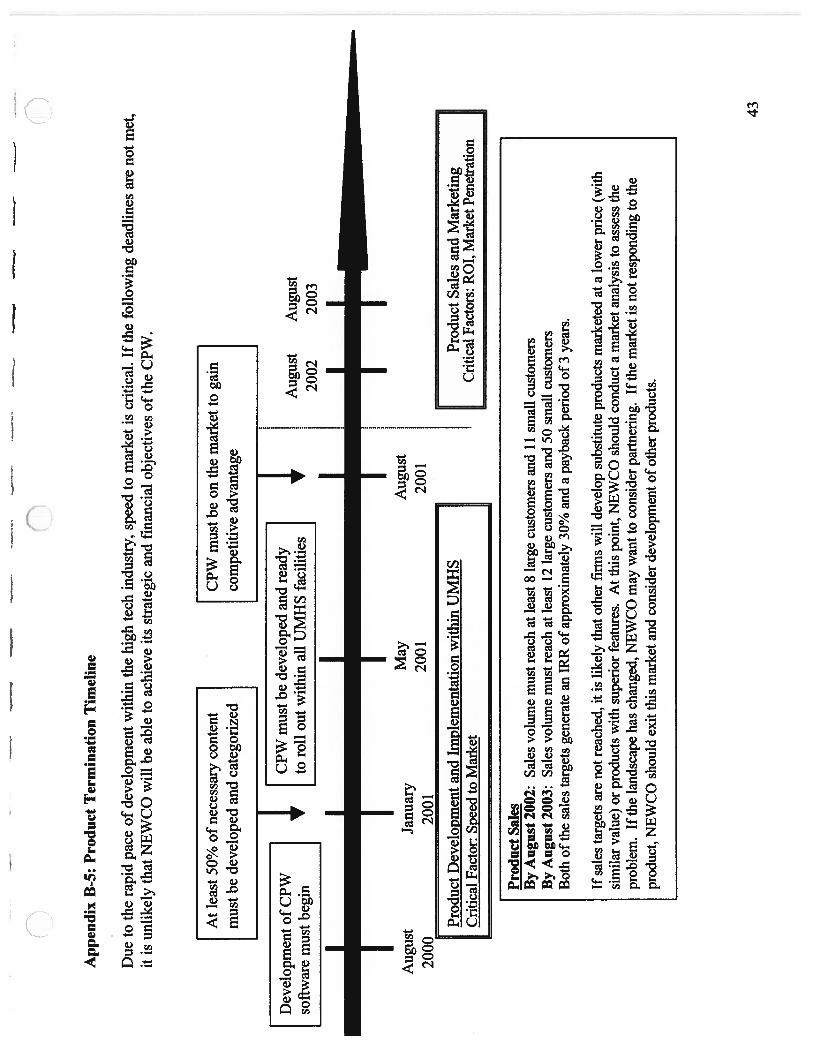

IL Exit Strategy

Due to the rapid pace of development within the high tech industry, speed to market is critical.The profitability of the product is also important to ensure resources for future products. Atimeline of critical deadlines for product development and sales is included in Appendix B-5,page 43.

W. Company Description

A. Nature of the Business

The organization that will develop and launch this product will be a Michigan, for-profit taxablesubsidiary (NEWCO) under Michigan Health Corporation (MHC). NEWCO will be the vehiclethrough which UMHS can develop its eHealth strategy and future sources of revenue related to

University ofMichigan Business School Map Team 19 13

University ofMichiL’an Health System E-HeaJth Strate-v Business Plan

technology and health care delivery. Initially, the business will be responsible for thedevelopment and maintenance of the CPW, including all stages of testing and implementation. Inaddition, the business will market and distribute the product to organizations outside of UMHS.As the product is implemented within UMHS and other organizations, the company will provideuser support and customization as necessaiy. As future product lines develop, the company willbe responsible for all aspects of research, development and distribution. NEWCO will executeeHealth strategic product development in conjunction with Ulvl}{S leadership.

In order to succeed in this market, organizations must demonstrate the following characteristics:• Credible and tnsstworthy content• Direct access to patient clinical information• Brand recognition• User friendly web site design• Technology research and capabilities• Design support• User support• Speed of new products to market• Integration of systems• Support of institutional leadership, including individuals at all levels of the organization• Security of information

B. Distinctive Competencies and Unique Resources

Although NEWCO is independent of UMHS, it will be able to leverage many of the system’sstrengths while mitigating its weaknesses in the development and marketing of the CPW. Someof UMHS’ s competencies and unique resources include:

• Credibility• Direct access to patient data• Enormous base of intellectual capital and well-recognized centers of excellence• Existing Web-enabled clinical content• Leadership support for IT development• Crucial payor perspective of the M-CARE HMO• Access to resources and expertise of other University of Michigan professional schools• Existing technology infrastructure• Software development experience• Centralized clinical data repository• Extensive alumni network

Though the company leverages the strengths of the health system, it will be able to react to themarket more quickly and efficiently than a large academic medical center.

University ofMichigan Business School Map Team 19 14

(Jnlversitv ofMichian Health System E-Health Stratev Business Plan

V. Marketing and Sales Strate!v

A. Potential Customers and Needs Identification

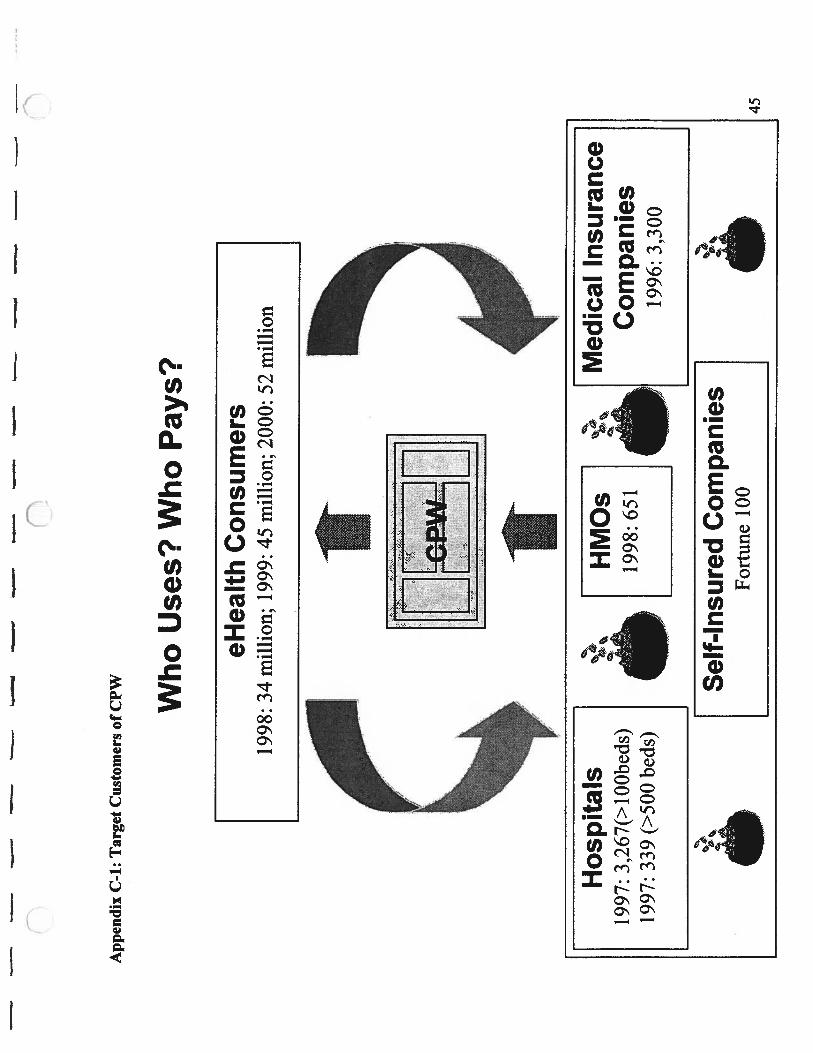

Hospitals, physicians, medical insurance companies (payors) and self-insured companies arepotential purchasers of the CPW (Appendix C-i, page 45). Physicians are important consumersof the product, but we intend to reach them through organizations that are better able to affordour product. In the US, there are more than 6,000 hospitals (Hospitals, 1999) striving to maintainmarket share, increase patient satisfaction, improve clinical outcomes, and increase clinicalefficiency. A hospital market analysis is provided in Appendix C-2, page 46. In addition tohospitals, medical insurance companies and self-insured companies may be interested in thisproduct. There are 651 HMOs and 3,300 medical insurance companies in the United States as of1998 and 1996, respectively (Congressional, 1999; Insurance Handbook). HMOs and insurersare interested in decreasing patient utilization while maintaining the quality of care. Self-insuredcompanies which include many Fortune 100 companies have a similar interest in reducing healthcare risks and costs, improving the health condition of employees and their families, anddecreasing patient utilization.

B. Market Segments and Customer Prioritization

Potential customers can be segmented by category and size. Appendix C-3, page 47, illustrates,.—- market segmentation by size and category. Each segment should be prioritized for efficient and

I effective marketing and sales activities. Possible segment prioritization criteria include:• Size of the market• Potential market penetration level• Prestige of customers• Possibility of referral to other potential customers• Fit with organizational goals

A template for segment prioritization is provided in Appendix C-4, page 48.

Customers within each segment should be prioritized for efficient and effective marketing andsales. Possible customer prioritization criteria include:

• Financial capability• Possibility of continuous partnership• Prestige of customers• Possibility of referral to other potential customers• Fit with organizational goals

A template for customer prioritization is provided in Appendix C-5, page 49.

C. Pricing

A price for the product can be determined by assessing the customer value of the product.Customers of the product receive several benefits. The primary benefits include efficiencies

University ofMichigan Business School Map Team 19 15

nfMb.1.;,,,,.. U,IiI, E-Health Stratev Business Plan

gained from decreased clinicians’ and nurses’ patient education time spent at the point of care,decreased costs of patient cailbacks, reduced volume of triage calls, and potential reductions inthe patient education budget. These benefits can be quantified by estimating time saved at thepoint-of-care, analyzing the costs of triage before and after our product is implemented, andanalyzing patient education budget reports. An additional benefit, which is not quantifiable atthis point, is decreased variable cost per case. Further study on this benefit is important foraccurate product pricing. The most important benefit, however, is the intangible value ofbuilding brand equity through enhanced customer satisfaction. Institutions that introduce thisproduct may be more competitive than others because they are able to change the tide ofmisinformation by controlling information received by patients.

The MAP team identified potential price structures by estimating Economic Value Added (EVA)of primary benefits to the customer. EVA can be measured using three steps.

1. Estimate Total EVA to Customer (See Steps 1,2, 3 in chart below)2. Detennine customization cost per customer, which is equivalent to the variable cost per

license.3. Subtract the license fee (fixed cost), to arrive at customer value

EVA Pricing Method

800

600

$000s400-

—License200

0-— I

Total EVA to Total cost

Assumptions : 50% of first year’s primary benefits charged as the price(1) EVA of reduced physicians’ and nurses’ time spent educating patients(2) EVA of reduced number of triage calls(3) EVA of reduced expenses associated with patient education materials

The MAP team calculated a range of $230,000-$730,000 of customer EVA. Therefore, a price

C range of $120,000- $360,000 is possible based upon the category and size of the customer.Appendix C-6 on page 50 provides detailed calculations of EVA by customer segment.

Customervalue

550(1

Pricing range

‘JrI 60

Customizationcustomer costs

60

University ofMichigan Business School Map TeamI9 16

(Jniversifv ofMichifais Health System E-Health Sfratep-v Business Plan

Therefore, an appropriate pricing model for hospital customers would be:

Maximum Pricing = EVA(education efficiency gain) + EVA(patient callback efficiencygain) + EVA(decreased variable cost per case) + EVA(decrease in cost of patient educationmaterials)

An appropriate pricing model for payors and self-insured companies customers would be:

Maximum Pricing = EVA(decrease of patient utilization) + EVA(decrease in cost of patienteducation materials)

D. Distribution andPromotion

It is critical to understand the decision making process of medical software purchase in hospitalsand other companies in order to market the product. The purchasing process is usually initiatedby a ClO of the organization and finalized by an agreement within the management leadership.Consequently, ClO contact is very important. Another possible point of contact is the healthcarecost manager within a hospital or health system. To gain access to these key decision-makers, thecompany needs a direct sales force. This sales force will be responsible for contacting customers,

C generating Request for Proposals (RFPs), responding to questions from potential customers, anddemonstrating the product at the point-of-sales. The sales force should have or develop specificproduct knowledge, medical knowledge, IT skills and interpersonal skills. The number of salespeople required should be determined by sales projection of the product.

Another distribution option is to establish a partnership with another company. Partnerships aredescribed in a later section of this plan.

Effective promotion of our product requires deep consideration of costs associated withpromotion, ability to reach our target audience, and the degree of push and pull marketingnecessary. There are three main promotion tools in medical software sales practice.

• Medical information technology conferences• Advertising in health care magazines, newspapers, and websites and sponsorships at

medical conferences• Personal referrals citing the benefits of the products (word of mouth)

VL Oranization. Manaementg Ownership and Operations

A. Structure

The company, NEWCO, that will develop and launch the CPW will be established as a for-profitsubsidiary under MHC. The University of Michigan is a public institution, and as a result it issubject to certain restrictions. The MHC was established by the Regents of the University as a

University ofMichigan Business School Map Team 19 17

University ofMichwan Health System E-Health Strate’v Business Plan

vehicle to participate in, coordinate and develop health care related activities to maintain andenhance the educational, research and service missions of the University. Specifically, MHCexists to enable the University to pursue health care initiatives that it would not otherwise be ableto pursue.

The CPW will initially be launched by the eHealth subsidiary, with NEWCO controlling 100%interest in the company. However, as we begin marketing the product to outside organizations,the venture may be spun off into an independent business under the umbrella of the largereHealth subsidiary. This spin-off structure will facilitate partnerships and possible funding.Parties outside of UMHS will have the ability to assume partial ownership in the company. Inaddition, the company will offer two levels of stock options, one with voting rights and onewithout voting rights. MHC may maintain a controlling interest in any of the companieslaunched under it, but this will be decided by leadership based upon individual situations. Thediagram in Appendix D- 1, page 52 illustrates the structure of this entity.

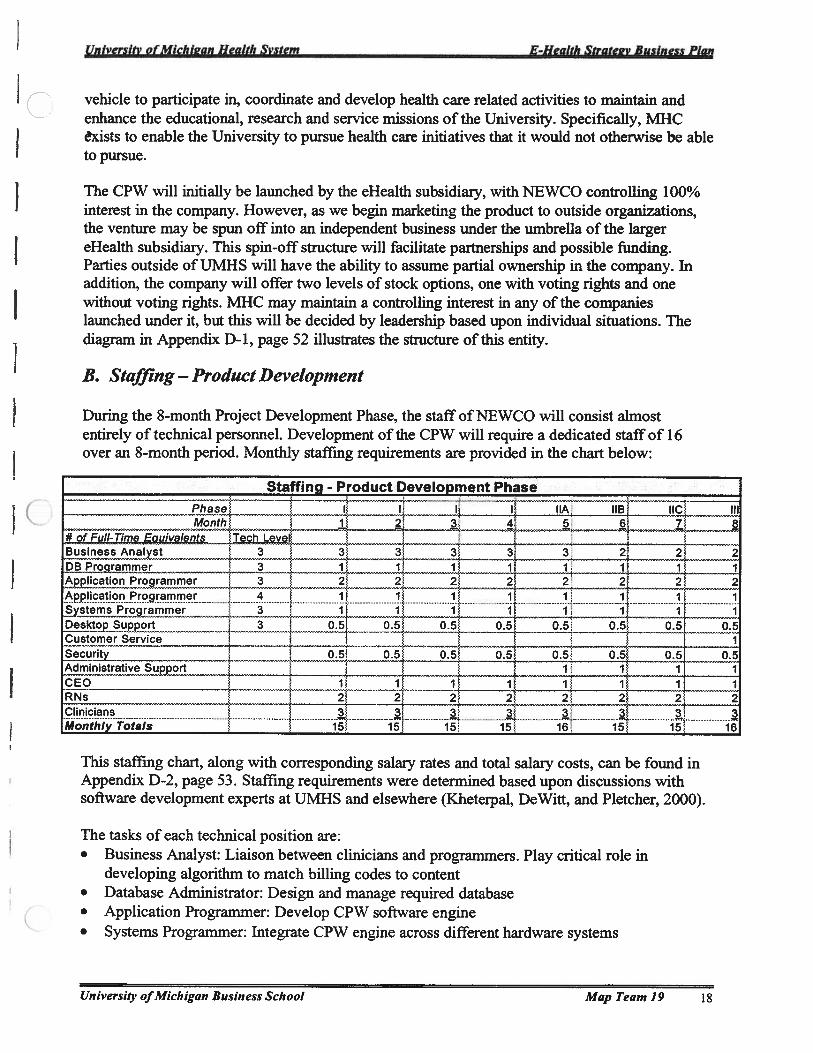

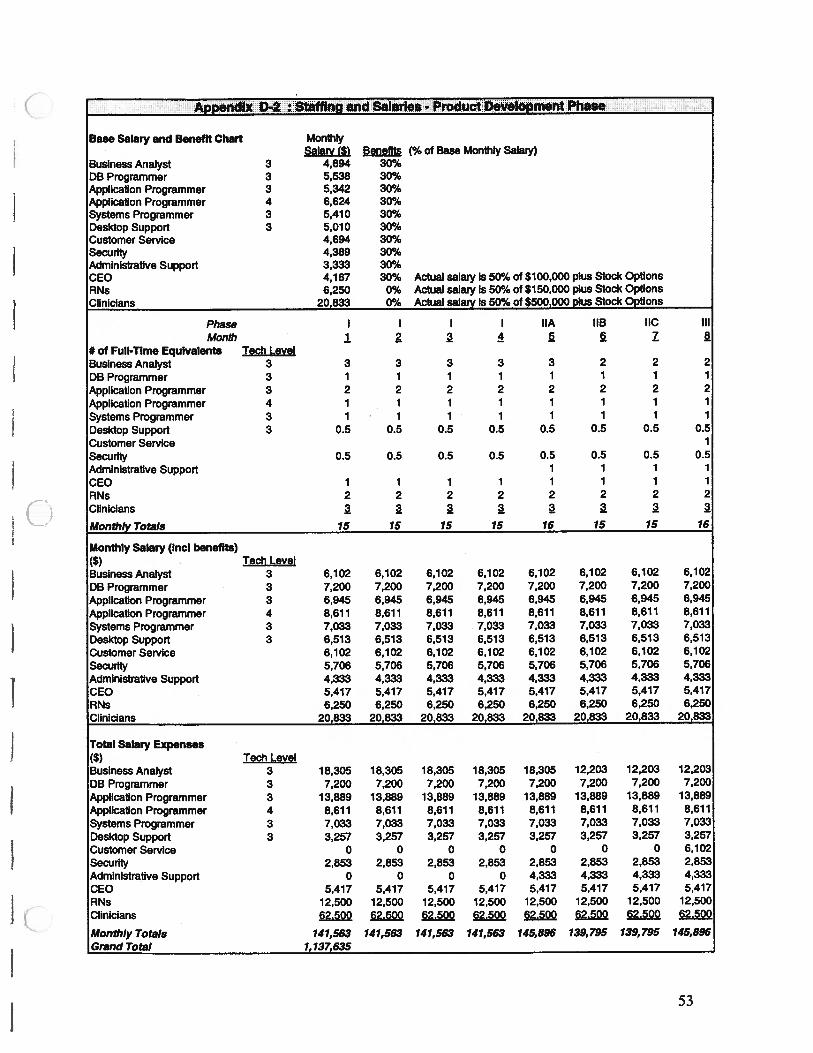

B. Staffing — Product Development

During the 8-month Project Development Phase, the staff of NEWCO will consist almostentirely of technical personnel. Development of the CPW will require a dedicated staff of 16over an 8-month period. Monthly staffmg requirements are provided in the chart below:

Staffing_-_Product_Development Phase

Phase I I I I hA IIB IICMonth 1 2 3 4 5 6 7 8

#9f Full-Time Equivalents Tech Level — — — — — —

Business Analyst 3 3 3 3 3 3 2 2 2DB Programmer 3 1 1 1 1 1 1 1 1Application Programmer 3 2 2 2 2 2 2 2 2Application Programmer 4 1 1 1 1 1 1 1 1Systems Programmer 3 1 1 1 1 1 1 1 1Desktop Support 3 05 05 05 05 05 05 05 05Customer Service ISecurity 05 05 05 05 05 05 05 05Administrative Support 1 1 1 1CEO 1 1 1 1 1 1 1 1RNs 2 2 2 2 2 2 2 2Clinicians 3. 3 3. 3 3. 3 3. 3Monthly Totals 15 15 15 15 16 15 15 16

This staffmg chart, along with corresponding salary rates and total salary costs, can be found inAppendix D-2, page 53. Staffing requirements were determined based upon discussions withsoftware development experts at UMHS and elsewhere (Kheterpal, DeWitt, and Pletcher, 2000).

The tasks of each technical position are:• Business Analyst: Liaison between clinicians and programmers. Play critical role in

developing algorithm to match billing codes to content• Database Administrator: Design and manage required database• Application Programmer: Develop CPW software engine• Systems Programmer: Integrate CPW engine across different hardware systems

University ofMichigan Business School Map Team 19 18

University ofMichk’an Health System E-Health Strate2’v Business Plan

C • Desktop Support: Provide and maintain productivity software for each employee

• Security Expert: Design and implement firewalls and other data security functions to ensure

integrity of data transmitted from host server to patient web site

• Clinician: Work with Business Analyst in providing expertise to match billing codes to

content• RN: Work with Business Analyst in providing expertise to match billing codes to content

• Customer Service: Provide support to test pilot customers and relay feedback to technical

team

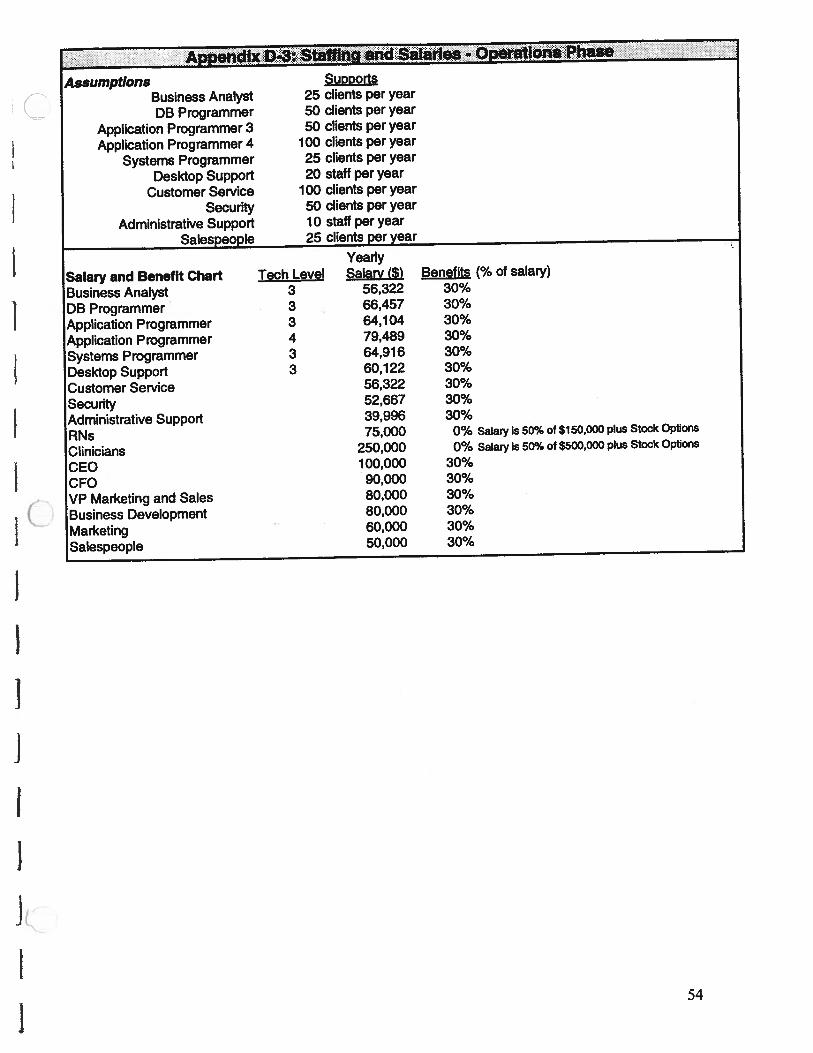

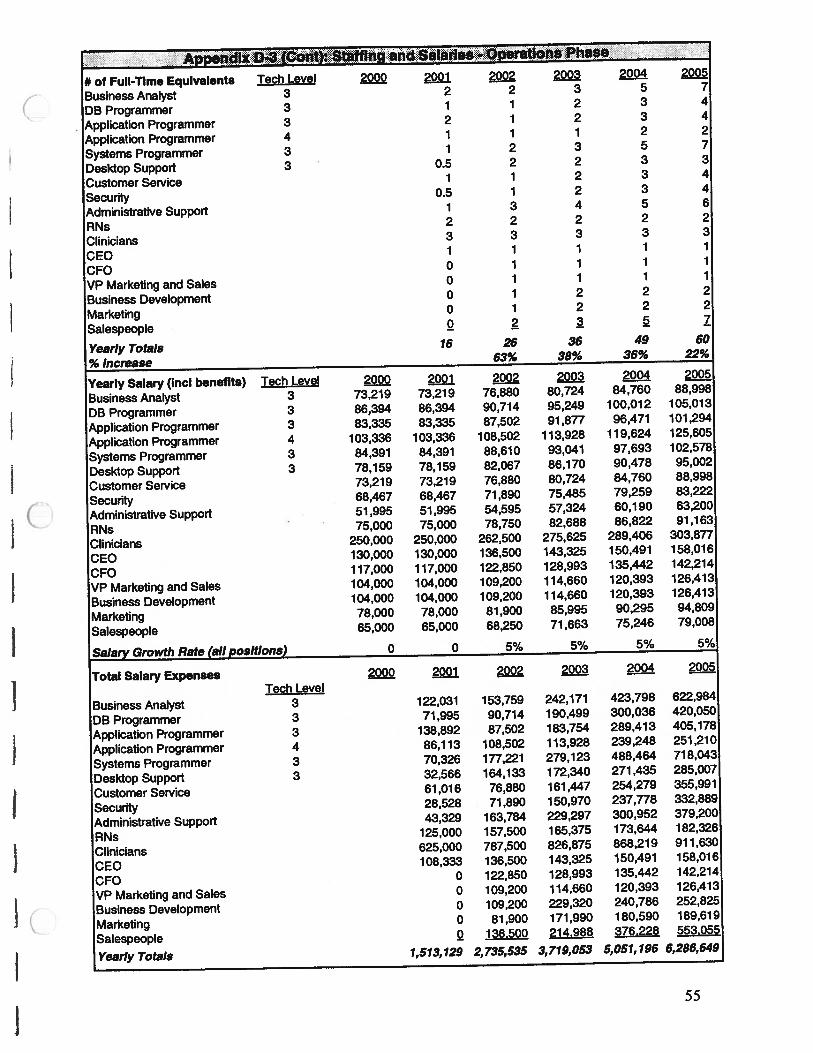

C. Staffing — Operations

Staffmg requirements following product development were detennined based upon sales

projections. The number of new clients per year was used to assess the number of FTEs needed

at each functional level during the years 200 1-2005. Software industry standards of the number

of new clients that can be supported by each position were the basis of these calculations, and are

available in Appendix D-3, page 54. The following table lists the yearly staffmg requirements.

Staffing - Operations Phase

2000 2001 2O02 2003 2004 2005

# of Full-TimEowvaIents Tech Levei

Business Analyst 3 2 2 7

Dammer 3 J_AjjonProjarnmer 3 2 3 4

Pppcionfoqrarnn_ 4 ____1 1 2 2

....3 i23J 5 7

Desktopy__ 3 2 3 3

çustomerse_._,

12; 3 4

&.uñtyAdmhiistratjypj__RNs 2. 2 2 2 2

Chnicians 3 3 3. 3 3

CEOCFO 0, 1 1 I I

VP Marketing and S&es :ziztz iTh minessD 1 2 2

Marketing 1 2

Salespeople 2 7

Yearly Totals 16 26 36 49 60

%lncrease 63% 38% 36% 22%

Annual staffmg requirements, corresponding salary rates, and total salary costs are provided inAppendix D-3 on page 54.

D. Incentive Structure

One goal of NEWCO is to encourage UMHS faculty continue to use their knowledge to benefitpatients, the system, and themselves. As a result, the incentive structure is an important aspect of

this plan. Although participants will be offered cash compensation for their content

University ofMichigan Business School Map Team 19 19

University ofMichiL’an Health System E-Health Stratee-v Business Plan

C contributions, a stock option program will also be developed. There are several reasons for

offering such a plan.• “The principle underlying these systems is the use of rewards to create among

employees and management alike a shared sense of identity, commitment, and goalsfor the organization.” (Wilson, 1995)

• Physicians and other contributors will have reason to continue to participate in thelong-term development of content and applications

• Compensation for work will be competitive with consulting offers from organizations

such as Medscape and WebMD

Recognizing the support of physicians, nurses, clinical and non-clinical staff within the healthsystem will be critical to the success of the product, all UMHS employees will be offered

restricted stock options, regardless of their role in the development or use of the product. Theseoptions will not have voting rights. The purpose of this offering is to initiate support for theproduct as it is developed. Option packages will vary depending on the employee’s position

within UMHS.

During the product development phase, physician participation will be crucial to the product’ssuccess. We will offer the option of cash compensation, at approximately $250 per hour3,or

nonqualified stock options for consulting services (Miller Canfield Presentation; Brock, 2000).

f The nonqualified stock options will be available to individuals after they have completed aspecified service to the company. Ideally, NEWCO will recruit one physician from each

C department to assist with the development of appropriate content links. This can be facilitatedusing one of two methods. The first option is to recruit a representative from each department towork on the project for a certain percentage of their time designed to UMHS. This time will not

be considered consulting time. The second option is to employ the department representatives as

J consultants and require them to designate their four days of consulting work per month to the

development of the product. Nurse educators acting as consultants in the development phase willreceive similar stock options.

After the product has been developed, NEWCO will need ongoing support for contentdevelopment. An advisory board will be established to review future content and evaluate new

product lines. The advisory board will consist of five physicians from the original contentdevelopment team (department representatives), consumer representatives, and other individualsfrom inside or outside of the health system as deemed appropriate by company leadership. Theadvisory board will be rewarded with voting stock options consisting of approximately 10%-20% of the total stock. Physicians who continue to generate content for the site will becompensated with cash ($250 per hour) or restricted, non-voting stock options, based upon theirpreference.

Finally, individuals involved with the development of the product will be acknowledged inproduct descriptions included with the software package. However, individual names will not beattached to content segments. Clinicians are frequently involved in ventures that serve to provide

This is competitive with Oncology.com feesBased on Miller Canfield presentation regarding industry standards

University ofMichigan Business School Map Team 19 20

University ofMichi2an Health System E-Health Strate-v Business Plan

higher quality patient care, even if no personal financial reward is obtained. NEWCO will

provide an option for individuals to gain this job satisfaction while working within the UIvIHS.

It is important to avoid incentive structures that override the faculty’s primary obligation to theUniversity for research, education and care delivery. The current structure allows faculty toparticipate in ventures similar to NEWCO that are outside of the University. The proposed

incentive structure will incent faculty to help support UMHS’s missions.

Future questions that NEWCO will need to address include:• What will individuals pay for their shares? ($.0l or a price close to the IPO)

• How long until the shares are vested?• What happens if the company is sold?

E. Partnershzvs andAiiances

Partnerships and alliances are important to build relationships with potential customers andimprove effectiveness of business processes. While NEWCO possesses the necessary resources

to achieve specific business goals, it may not be equipped to handle the project the most efficientway possible. For the CPW product, three functional areas categorize potential partners: (1)marketing and distribution, (2) content production, and (3) development and implementation.

The advantage of marketing and distribution partnerships is to improve the effectiveness of sales

a (1 and build relationships with potential partners. This should be done while building the brand

j recognition and the reliability of the product. This is important in the CPW because of themarketing strategy of selling to health systems and third party payors (such as self-insured

companies) on a national basis. Potential partners include companies with an established

foothold in the healthcare technology market, such as pharmaceutical companies, EMR software

companies, medical content providers, and medical device companies. Marketing and

distribution partners would provide specific capabilities such as funding for promotion and

distribution, skilled salesforce, and most importantly, a connection to their established customerbase.

Content development partnerships could provide a useful way to tap into the existing base ofWeb-enabled medical content. While the majority of this content is general in nature, it couldprovide a basis for the CPW database. Additionally, the increase in knowledge through theinclusion of another content source could create synergies to provide NEWCO with more usefulinformation. Potential partners for content development are WebMD, Medscape, and DrKoop.These companies were selected based on their established presence in eHealth and history ofdistinguishing themselves through content, credibility, and infrastructure. However, a keyresource of UMHS is its faculty. The enormous amount of clinical knowledge available withinUMHS and that which afready exists within the UMHS data warehouse does not create animmediate need to pursue content partnerships (Hampton, 2000). Furthermore these companiesare unfavorable because they do not desire exclusive AMC alliances (Medscape, 2000).

The inclusion of a development partnership is aimed at reducing risk and improving the speed ofdevelopment. Technology based products and services must address the issues of time-to-market

University ofMichigan Business School Map Team 19 21

University ofMichiean Health System E-HealIh Strate-v Business Plan

as well as unique design capabilities. The CPW is a product that will be intricate in both itsdesign and capabilities. In order to fully enable UIvIHS to compete in this new market, it may benecessary to form a partnership an&or alliance with a technology or Internet software company.This option is being considered for numerous reasons, mainly issues concerning productdevelopment and implementation efficiency and the need for technological expertise. UMHSprovides value through its core competencies and key resources, namely its ability to providecredible healthcare content and access to its faculty. However, the potential value added from apartner could be two fold: technology and development expertise as well as security expertise tomaintain patient confidentiality and regulatory compliance. This type of partnership is necessaryin the early stages of implementation in order to achieve UMHS’s ultimate goals.

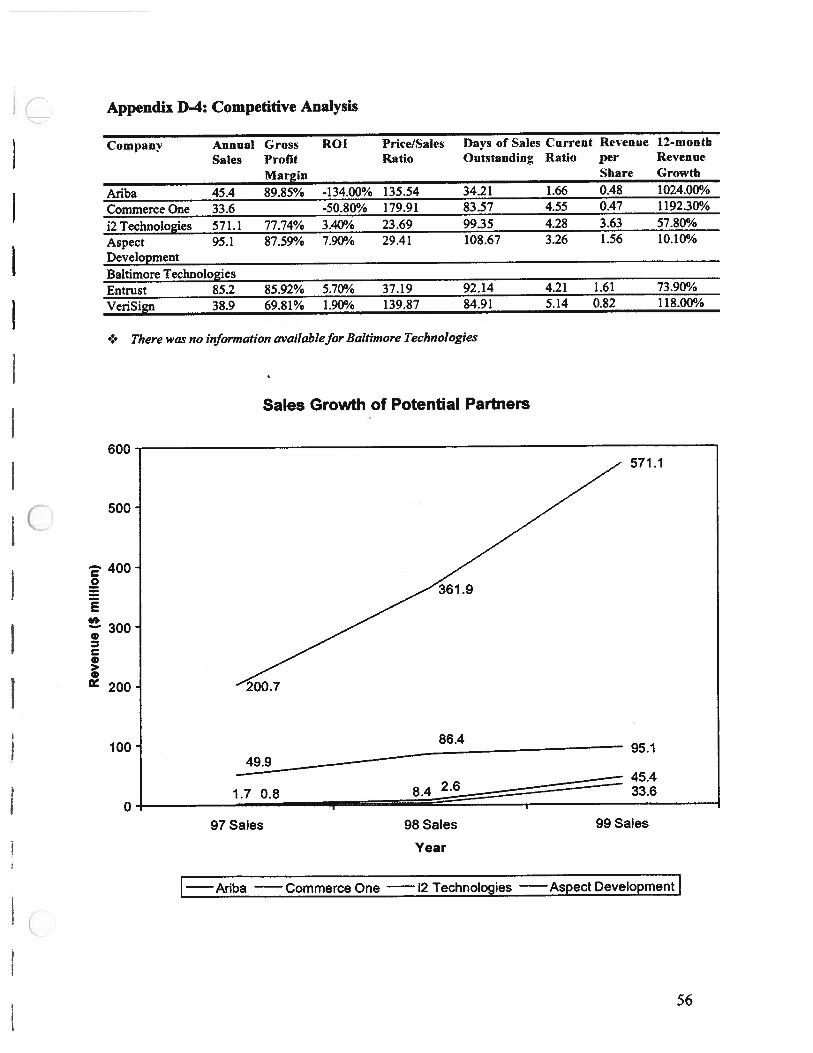

In order to explore the partnership/alliance option we have researched seven companies.Companies were selected on the basis of reputation, performance, and potential growth. In thecategory of potential product development partnerships i2 Technologies, Aspect Development,Ariba, and Commerce One have been analyzed. In the security partners realm, Entrust, yen Sign,and Baltimore Technologies (which recently acquired GTE Cybertrust) have been considered(Baltimore, 2000). Brief overviews of each company, comparative performance analysis, andpartnership recommendations can be found in Appendix D-5, page 57.

Product Development Partners

In order to consummate a beneficial development partnership, NEWCO will select a company

( that possesses specific capabilities. These include sufficient funding resources and developmentexpertise that will produce synergies through increased knowledge and development timeefficiency. i2 Technologies’ size and experience (established in 1988, i2 Technologies currentlyhas approximately 2800 employees) makes it the most attractive development partner forNEWCO (Hoovers, 2000).

The acquisition of Aspect Development and the alliance established with Ariba have solidified i2Technologies’ leadership position in the software industry (Aspect, 2000; MSDW, 2000). This,along with its illustrated growth (it is expected that they will sustain annual revenue growth of50% through 2005), has positioned it as the leading potential partner for UMHS in the productdevelopment of the CPW (Hoovers, 2000).

Security Partners

Entrust and VeriSign are the leading competitors in the security side of our partnership analysis.They employ two different business models: VeriSign utilizes a service model and entered themarket with a focus on the consumer. Entrust maintains a licensing model focusing on theenterprise but is expanding its offerings to include outsourced services. VeriSign is offered at ahigh premium over Entrust, and it is believed that this premium is unwarranted (Goldman Sachs,1999). This phenomenon may lead VeriSign to future instability. Additionally, Entrust’srevenues are growing faster than VeriSign’s and the revenue stream is more diverse (GoldmanSachs, 1999). These factors, when combined with their established healthcare presence, has ledus to recommend Entrust as the leading candidate for a security partnership (Entrust, 2000).

University ofMichigan Business School Map Team 19 22

University ofMichk’an Health System E-Health Stratev Business Plan

It is unclear as to whether or not a second alliance with a security partner for the development of

a co-branded product is necessary. Many of the software development firms have securityprecautions as an aspect of development. This avenue should be explored.

Potential Development Partner Analysis

Company Product/Service FE 1999 Revenue 12-month OverallAttributes ($ millions) Growth Assessment

i2 Technologies • General collaborative 571.1 57.8% +-t

solutions for B2BeCommerce

Aspect • Software 95.1 10.1% +++

Development development• Provision of

efficiencies ofprocurement, design,operationsmanagement, and thesupply chain

Ariba • Global eMarkets 45.4 1024.0% ++

Commerce One • Global eMarkets 33.6 1192.3% ++

Entrust • PM Technology 85.2 73.9% ++++

solutions• Digital certificates

VeriSign • Digital certificates 38.9 118.0% ±+++

Baltimore • Computer and 30.0 -H-

Technologies network securityservices

Companies in bold are highly recommendedforpartnershipPlus signs (+) on a scale of 1 to 5) denote the increasing level ofquality respective ofreputation, performance, and

potential growth‘‘ Information not availableOverall Assessment is based on information provided in Appendix D-5, page 57.

VIE Future Products

NEWCO will utilize the core competencies, customer information, and distribution channelsgained from the development and implementation of the CPW to launch future products. Theproducts to be developed, in chronological order, are:

• Physician Information Web Page• Decision Support System• Continuing Medical Education (developed in conjunction with JIT)

• Just-in-Time (JIT) Education (developed in conjunction with CME)

University ofMichigan Business School Map Team 19 23

University ofMichigan Health System E-Health Stralei’v Business Plan

The following are summary descriptions of NEWCO’s future products. Each summary describesthe product and the related synergies for previously developed products. For an overview ofproduct synergies based on core competencies, customer information, and distribution channels,see Appendix E- 1, page 61.

A. Physician Information Web Page (P1W)

The Physician Information Web Page (P1W) will be the second product launched by NEWCO.The P1W is similar in nature to the CPW in that it proactively “pushes” necessary information tothe customer, the physician. This product will be capable of delivering new drug information,latest breaking medical news, institutional concerns, and CME information. If the purchaserchooses to integrate the P1W with the CPW, the information will be able to help physicians innew ways such as informing them of cost differentials among pharmaceuticals or highlightingpatient concerns based on patient Web behavior.

B. Decision Support System

The Decision Support System will support clinicians’ diagnoses and treatment decisions byproactively providing information based on patient symptoms and diagnoses. Building upon thesoftware development skills and the learning experience of both the CPW and the P1W, NEWCOcan create a database driven Decision Support System that will be used as a tool by physicians

(. and their support staff. This product will compete directly with MDConsult but will have theadvantage of being able to “leap frog” the competitors’ technology and content. The DecisionSupport System will aggressively gain market share by utilizing distribution channels set up withprevious products. The product will incorporate UMHS patient care guidelines in its software aswell as drug and reference databases. It will be sold to hospitals and health systems for use byRNs, PAs, and other health professionals in triage decisions. Physicians will be targeted at thepoint of care once the system is validated.

C. Continuing Medical Education

CME programs have been ineffectively impacting physician behavior and are currently offeredfree of charge in many formats. There is an opportunity to generate revenue by developingCMEs that actually change physician behavior. The current lack of physician response to CMEsis due to the manner in which the CME has traditionally been delivered. Various studies haveshown that interactive CME courses, especially courses held over multiple periods, have hadpositive outcomes on physician performance (Davis, 1999). Utilizing concurrent developmentsof the MRT, the Visible Human, and MT Education, NEWCO can impact the way CMEs aretaught and fill the market need for superior CME.

D. Just-in-Time Education

Just-in-Time Education is the next natural progression from Decision Support Systems. Thedifference between the two products is that while Decision Support Systems can assist at thepoint of care for 80% - 90% of a physician’s cases, it is limited mostly to primary care and

University ofMichigan Business School Map Team 19 24

Iiniuorvitv nf PJipI, ionn I-IpnIWI, cvcii’n F..Th’i,Iiii .iraIpoi, R,,cinjicc Plnn

known clinical situation. Just-in-Time Education is the link between cutting edge research and

physicians at the point of care, involving everything from what to do in the case of rare druginteraction side-effects to reinforcing new diagnostic techniques learned in a CME course.

These four products will take advantage of concurrent developments already underway in the

realms of distance education and telemedicine, culminating in the advancement of telecare (see

Figure 7-1). Whereas “telemedicine” can be defmed as cost-effective examples of tele-radiology,

tele-consulting, and tele-disease management, “telecare” is seen as the advancement of these

areas which are currently limited by infrastructure feasibility and cost / reimbursement issues.

However, telecare is not only limited by infrastructure and reimbursement. Patient acceptance

and provider familiarity with technology are two obstacles that could slow the acceptance of

telecare. As the infrastructure for telecare becomes more ubiquitous, organizations that already

have a presence in health technology will be the first to gain acceptance with patients and

providers. It is due to these behavioral factors that NEWCO’ s future products will facilitate the

acceptance of UMHS as a premiere telecare provider.

f)istanccEducation

I.— 1)ecisiin

cp’v = —0

.1

___

Figure 7-1: The advancement of products to telecare

VIEL Performance Metrics

To evaluate the success of our product and company, it is necessary to defme and implement